Embed Size (px)

Citation preview

Osborne Books Tutor Zone

FinancialStatements ofLimitedCompanies Chapter activities

© Osborne Books Limited, 2016

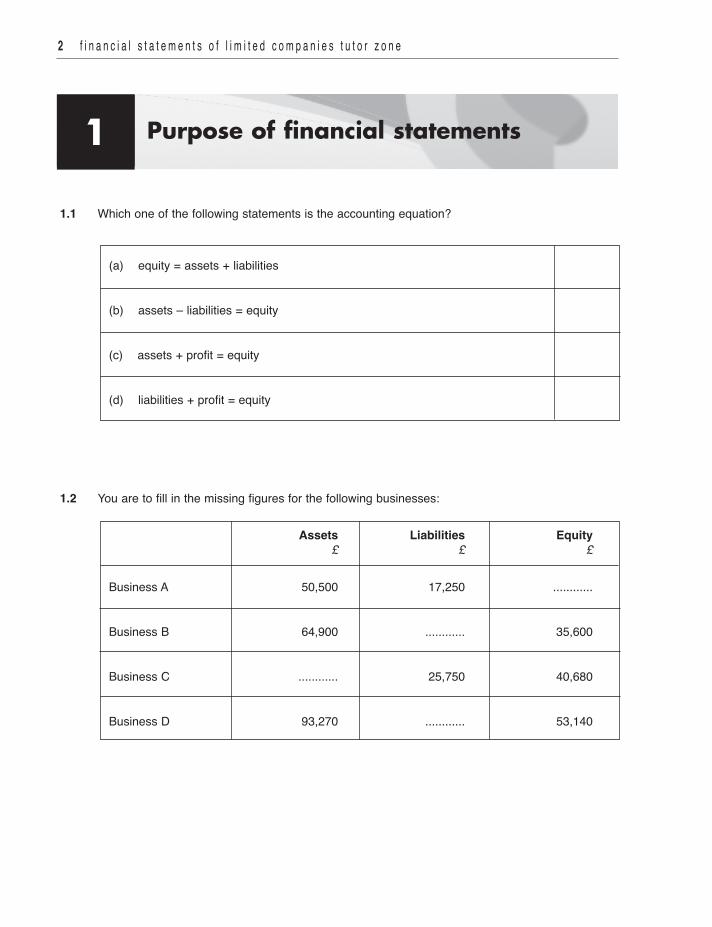

1.1 Which one of the following statements is the accounting equation?

(a) equity = assets + liabilities

(b) assets – liabilities = equity

(c) assets + profit = equity

(d) liabilities + profit = equity

1.2 You are to fill in the missing figures for the following businesses:

Assets Liabilities Equity £ £ £

Business A 50,500 17,250 ............

Business B 64,900 ............ 35,600

Business C ............ 25,750 40,680

Business D 93,270 ............ 53,140

Purpose of financial statements1

2 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

c h a p t e r a c t i v i t i e s 3

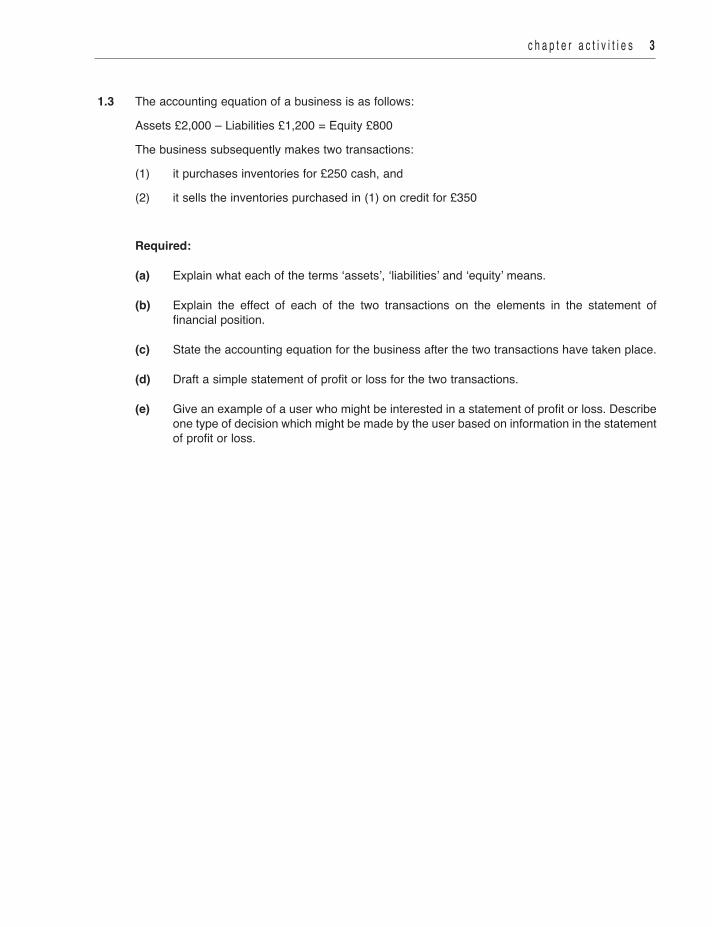

1.3 The accounting equation of a business is as follows:

Assets £2,000 – Liabilities £1,200 = Equity £800

The business subsequently makes two transactions:

(1) it purchases inventories for £250 cash, and

(2) it sells the inventories purchased in (1) on credit for £350

Required:

(a) Explain what each of the terms ‘assets’, ‘liabilities’ and ‘equity’ means.

(b) Explain the effect of each of the two transactions on the elements in the statement offinancial position.

(c) State the accounting equation for the business after the two transactions have taken place.

(d) Draft a simple statement of profit or loss for the two transactions.

(e) Give an example of a user who might be interested in a statement of profit or loss. Describeone type of decision which might be made by the user based on information in the statementof profit or loss.

4 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

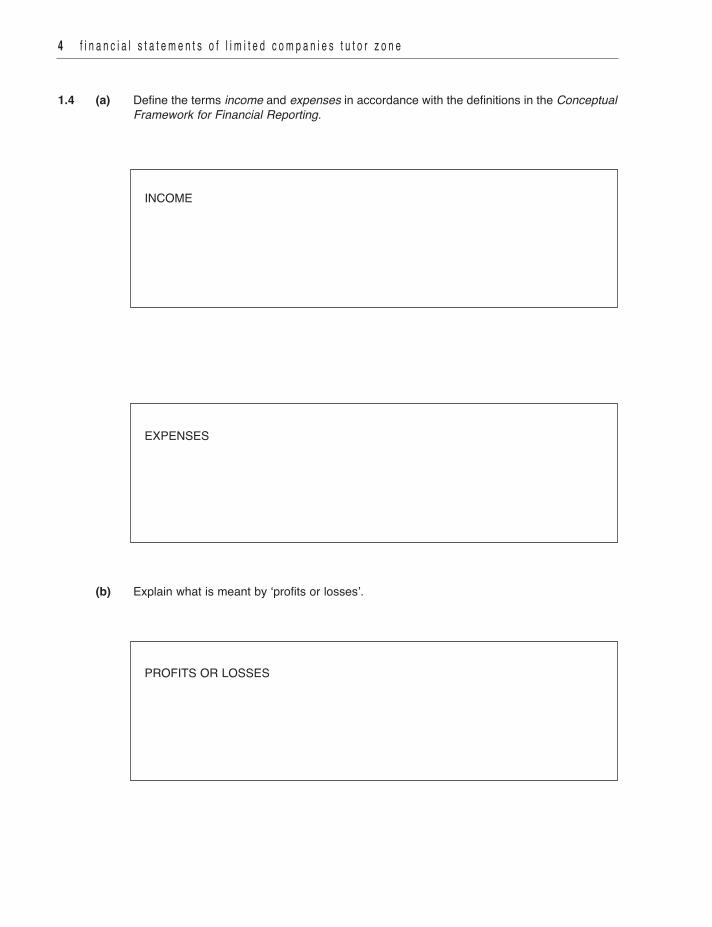

1.4 (a) Define the terms income and expenses in accordance with the definitions in the Conceptual Framework for Financial Reporting.

INCOME

EXPENSES

(b) Explain what is meant by ‘profits or losses’.

PROFITS OR LOSSES

c h a p t e r a c t i v i t i e s 5

1.5 The Conceptual Framework for Financial Reporting identifies two fundamental qualitativecharacteristics and four enhancing qualitative characteristics that identify the types of informationlikely to be most useful to users of financial statements for making decisions.

(a) State the two fundamental qualitative characteristics identified by the ConceptualFramework for Financial Reporting.

1

2

(b) Explain what is meant by each of these fundamental qualitative characteristics.

(c) State the four enhancing qualitative characteristics identified by the Conceptual Frameworkfor Financial Reporting.

1

2

3

4

6 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

1.6 Write in the accounting concept which relates to each of the statements below.

Statement Accounting concept

(a) The financial statements do not include the personal assets and liabilities of those who play a part in owning or running the entity

(b) The statement of profit or loss shows the amount of expense that should have been incurred

(c) The financial statements are prepared on the basis that there is no intention to reduce significantly the size of the entity

(d) Low-cost non-current assets are charged as expenses in the statement of profit or loss

1.7 Mark has just been appointed as a trainee accountant in an accounting practice. Mark has beenstudying accounting for two years, but this is his first employment in this sector. He is provided witha tax guide and asked to complete some tax computations of which he has no practical experience.Explain which fundamental principle in accordance with the AAT Code of Professional Ethics maybe threatened by this situation and suggest actions that may be taken to minimise any threats.

1.8 You are working in an accounting practice and in the process of preparing a new client’s financialstatements. The client wishes to expand in the near future and will need to apply for a loan. Theclient requests that you present a favourable liquidity position in the financial statements in order toobtain the financing required and states there will be a cash bonus for you on completion. Which threat to fundamental principles of professional ethics arises from this situation?

c h a p t e r a c t i v i t i e s 7

2.1 Show whether the following statements about a public limited company are true or false.

Statement True False

(a) The issued share capital is over £50,000

(b) There must be a minimum of one member (shareholder)

(c) There must be at least two directors

(d) The company must raise capital from the public on the Stock Exchange or similar markets

(e) The Articles of Association provide the constitution of the company

Introduction to limited companyfinancial statements2

• Blank photocopiable pro-formas in the format used in AAT Assessments – of the statement ofprofit or loss and other comprehensive income and the statement of financial position, areincluded in the Appendix of Financial Statements of Limited Companies Tutorial – it is advisableto enlarge them to full A4 size. Blank workings sheets are also included in the Appendix.

• Pro-formas and workings sheets are also available to download fromwww.osbornebooks.co.uk.

8 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

2.2 Which one of the following investments in a company receives a return on the investment that mayvary with the profits of the company?

(a) Ordinary shares

(b) Preference shares

(c) Debentures

(d) Long-term loans

2.3 A new company issues 500,000 ordinary shares of 25p each at a premium of 20 per cent. Whatamount will be shown as the total of the equity section of the company’s statement of financialposition?

(a) £600,000

(b) £125,000

(c) £25,000

(d) £150,000

c h a p t e r a c t i v i t i e s 9

2.4 What type of reserves are (1) retained earnings, and (2) revaluation reserve?

(a) Both revenue reserves

(b) Both capital reserves

(c) (1) Revenue reserve (2) Capital reserve

(d) (1) Capital reserve (2) Revenue reserve

2.5 Distinguish between:

(a) Intangible non-current assets.

(b) Tangible non-current assets.

Give an example of each.

2.6 What does total equity comprise on a company statement of financial position?

(a) Ordinary share capital, plus share premium

(b) Ordinary share capital, plus capital and revenue reserves

(c) Ordinary share capital, plus capital and revenue reserves, plus non-currentliabilities

(d) Ordinary share capital, plus capital and revenue reserves, plus non-currentliabilities, plus current liabilities

1 0 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

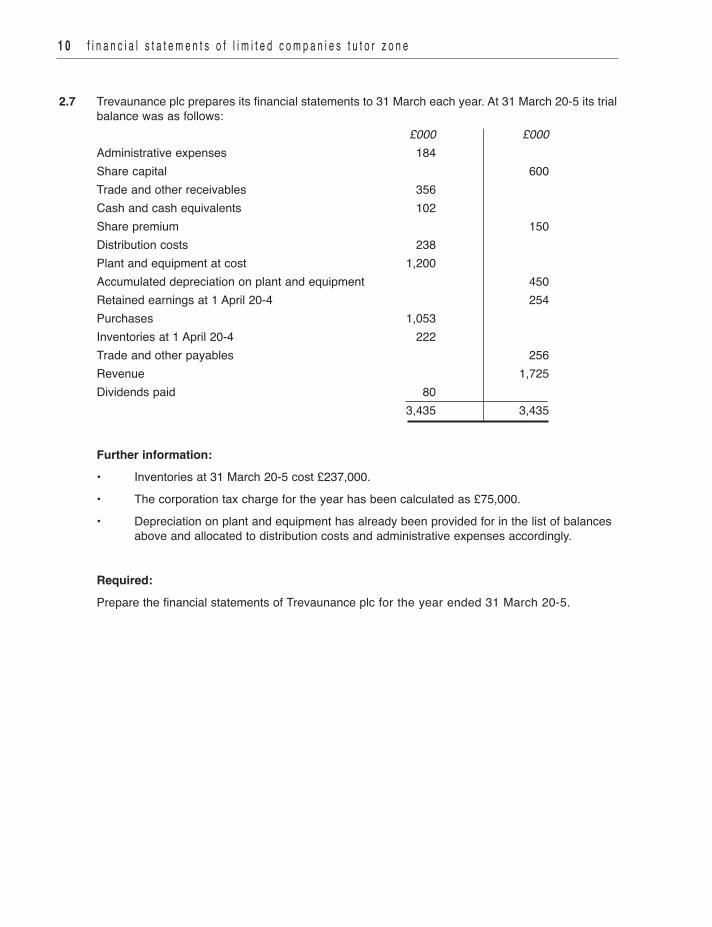

2.7 Trevaunance plc prepares its financial statements to 31 March each year. At 31 March 20-5 its trialbalance was as follows:

£000 £000 Administrative expenses 184 Share capital 600 Trade and other receivables 356 Cash and cash equivalents 102 Share premium 150 Distribution costs 238 Plant and equipment at cost 1,200 Accumulated depreciation on plant and equipment 450 Retained earnings at 1 April 20-4 254 Purchases 1,053 Inventories at 1 April 20-4 222 Trade and other payables 256 Revenue 1,725 Dividends paid 80 3,435 3,435

Further information: • Inventories at 31 March 20-5 cost £237,000. • The corporation tax charge for the year has been calculated as £75,000. • Depreciation on plant and equipment has already been provided for in the list of balances

above and allocated to distribution costs and administrative expenses accordingly.

Required:Prepare the financial statements of Trevaunance plc for the year ended 31 March 20-5.

c h a p t e r a c t i v i t i e s 1 1

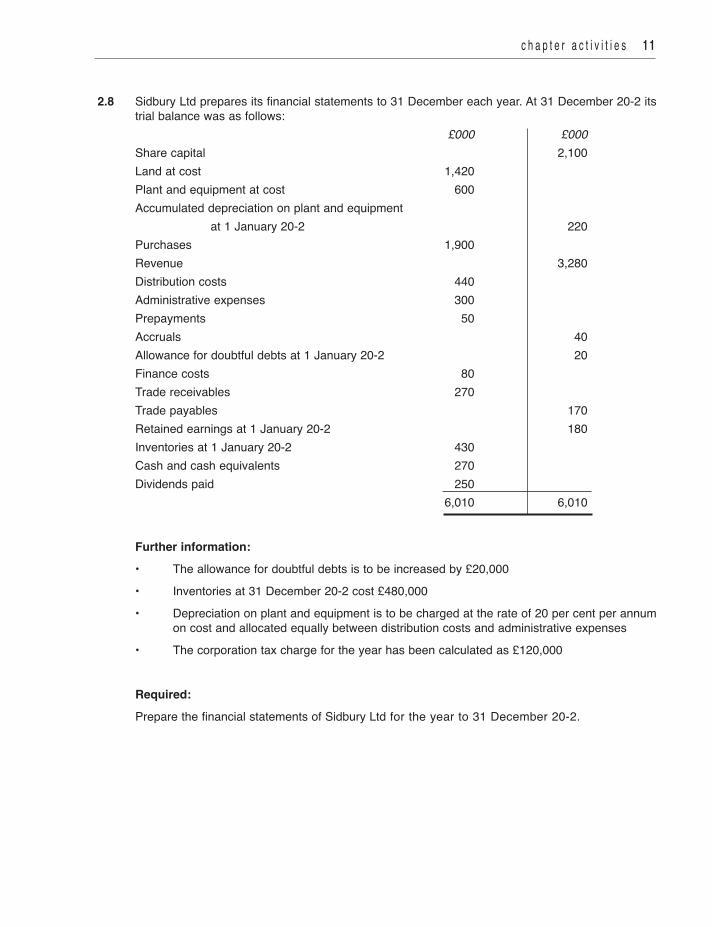

2.8 Sidbury Ltd prepares its financial statements to 31 December each year. At 31 December 20-2 itstrial balance was as follows:

£000 £000 Share capital 2,100 Land at cost 1,420 Plant and equipment at cost 600 Accumulated depreciation on plant and equipment at 1 January 20-2 220 Purchases 1,900 Revenue 3,280 Distribution costs 440 Administrative expenses 300 Prepayments 50 Accruals 40 Allowance for doubtful debts at 1 January 20-2 20 Finance costs 80 Trade receivables 270 Trade payables 170 Retained earnings at 1 January 20-2 180 Inventories at 1 January 20-2 430 Cash and cash equivalents 270 Dividends paid 250 6,010 6,010

Further information: • The allowance for doubtful debts is to be increased by £20,000 • Inventories at 31 December 20-2 cost £480,000 • Depreciation on plant and equipment is to be charged at the rate of 20 per cent per annum

on cost and allocated equally between distribution costs and administrative expenses • The corporation tax charge for the year has been calculated as £120,000

Required:Prepare the financial statements of Sidbury Ltd for the year to 31 December 20-2.

1 2 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

3.1 According to IAS 1 Presentation of Financial Statements, what is the objective of financialstatements? Complete the following sentence:

The objective of financial statements is to

3.2 The directors of Presingold plc, a recently-formed trading company, seek your guidance on thefollowing issues:(a) What items do we have to show on the face of the statement of profit or loss and other comprehensive income?(b) How should we analyse our expenses for the statement of profit or loss and other comprehensive income?

Published financial statements oflimited companies3

• Blank photocopiable pro-formas in the format used in AAT Assessments – of the statement ofprofit or loss and other comprehensive income and the statement of financial position, areincluded in the Appendix of Financial Statements of Limited Companies Tutorial – it isadvisable to enlarge them to full A4 size. Blank workings sheets are also included in theAppendix.

• Pro-formas and workings sheets are also available to download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 1 3

3.3 During its financial year ended 31 March 20-1, Sepulveda Ltd pays an interim ordinary dividend of£22,000. In April 20-1 the company proposes a final dividend for the financial year ended 31 March20-1 of £35,000.What amount will be shown for dividends in the statement of changes in equity for the year ended31 March 20-1?

(a) £22,000

(b) £35,000

(c) £57,000

(d) £13,000

3.4 According to IAS 1, Presentation of Financial Statements,

(a) How are current assets defined?

(b) How are current liabilities defined?

(a) Current assets are:

(b) Current liabilities are:

1 4 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

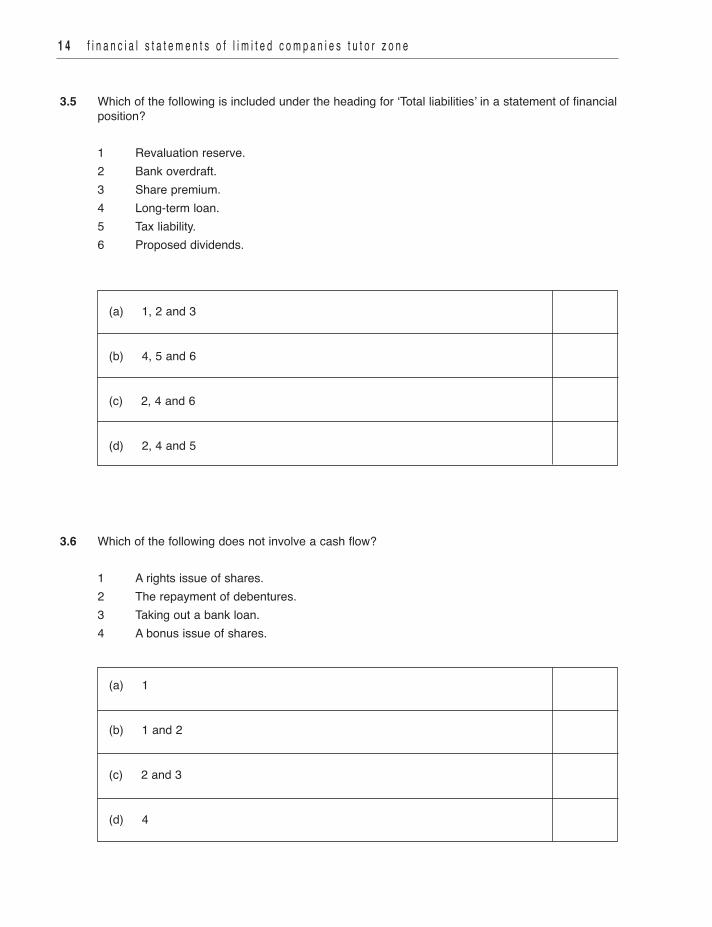

3.5 Which of the following is included under the heading for ‘Total liabilities’ in a statement of financialposition?

1 Revaluation reserve.2 Bank overdraft.3 Share premium.4 Long-term loan.5 Tax liability.6 Proposed dividends.

(a) 1, 2 and 3

(b) 4, 5 and 6

(c) 2, 4 and 6

(d) 2, 4 and 5

3.6 Which of the following does not involve a cash flow?

1 A rights issue of shares.2 The repayment of debentures.3 Taking out a bank loan.4 A bonus issue of shares.

(a) 1

(b) 1 and 2

(c) 2 and 3

(d) 4

c h a p t e r a c t i v i t i e s 1 5

3.7 You have been assigned to assist in the preparation of the financial statements of McTaggart Ltdfor the year ended 30 April 20-4.You have been provided with an extract from the extended trial balance of McTaggart Ltd on30 April 20-4 (set out on the next page).You have been given the following further information:• Depreciation has been calculated on the non-current assets of the business and has

already been entered on a monthly basis into the distribution costs and administrativeexpenses ledger balances as shown on the extended trial balance.

• The corporation tax charge for the year has been calculated as £1,113,000.• Interest on the non-current loan has not been paid for the last month of the year; the interest

charge for April 20-4 amounts to £26,000.• All of the operations are continuing operations.

Required:

(a) Draft the statement of profit or loss for McTaggart Ltd for the year ended 30 April 20-4.

(b) Draft the statement of financial position for McTaggart Ltd as at 30 April 20-4.

1 6 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

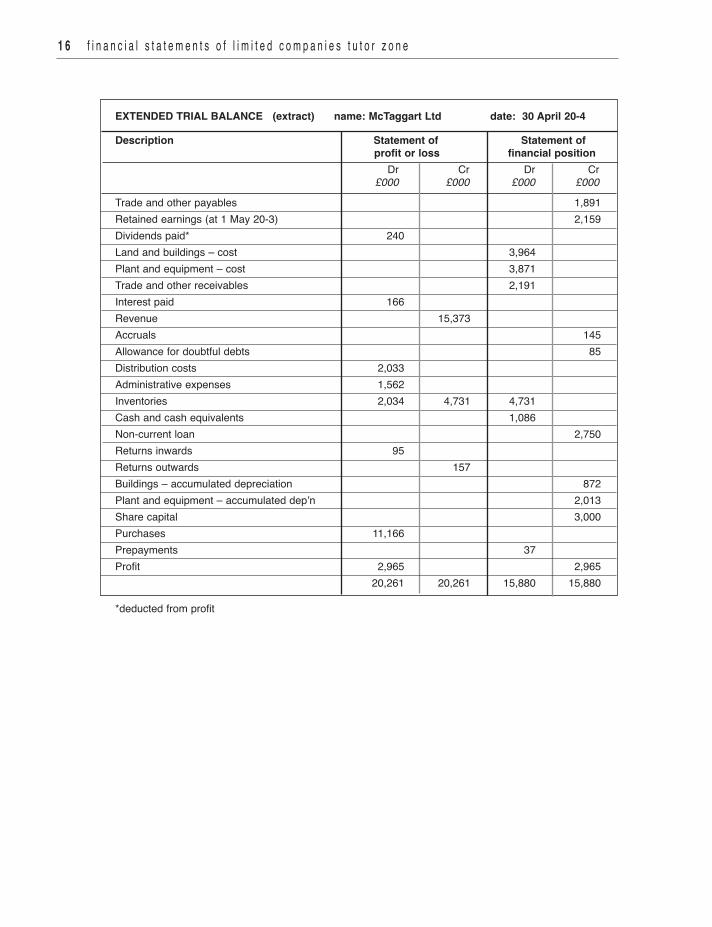

EXTENDED TRIAL BALANCE (extract) name: McTaggart Ltd date: 30 April 20-4

Description Statement of Statement ofprofit or loss financial position

Trade and other payables 1,891Retained earnings (at 1 May 20-3) 2,159Dividends paid* 240Land and buildings – cost 3,964Plant and equipment – cost 3,871Trade and other receivables 2,191Interest paid 166Revenue 15,373Accruals 145Allowance for doubtful debts 85Distribution costs 2,033Administrative expenses 1,562Inventories 2,034 4,731 4,731Cash and cash equivalents 1,086Non-current loan 2,750Returns inwards 95Returns outwards 157Buildings – accumulated depreciation 872Plant and equipment – accumulated dep’n 2,013Share capital 3,000Purchases 11,166Prepayments 37Profit 2,965 2,965 20,261 20,261 15,880 15,880

*deducted from profit

Dr Cr Dr Cr £000 £000 £000 £000

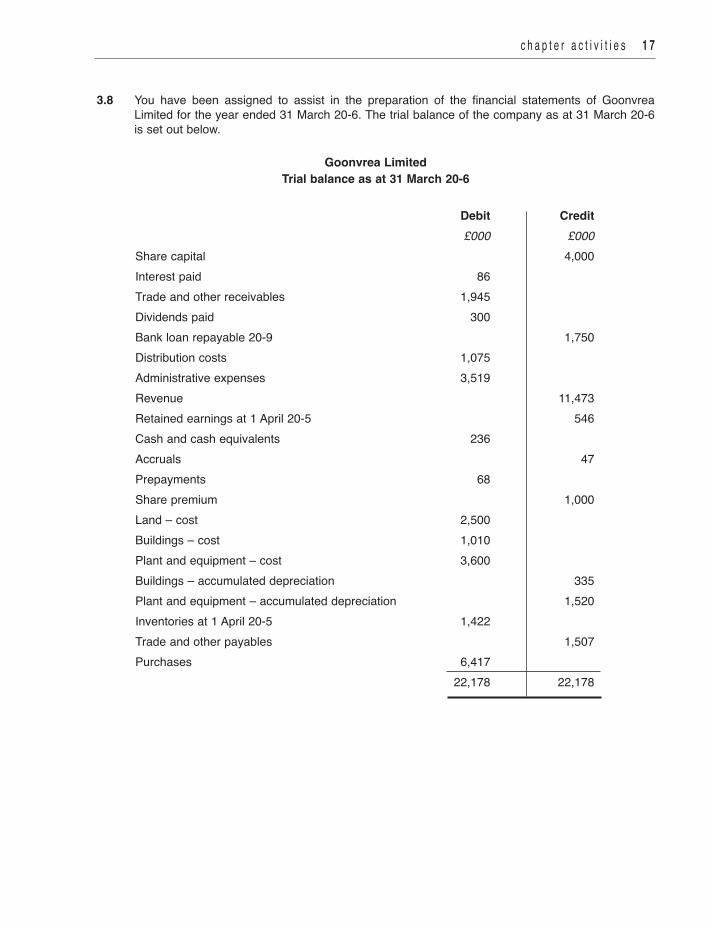

3.8 You have been assigned to assist in the preparation of the financial statements of GoonvreaLimited for the year ended 31 March 20-6. The trial balance of the company as at 31 March 20-6is set out below.

Goonvrea LimitedTrial balance as at 31 March 20-6

Debit Credit £000 £000Share capital 4,000Interest paid 86Trade and other receivables 1,945Dividends paid 300Bank loan repayable 20-9 1,750Distribution costs 1,075Administrative expenses 3,519Revenue 11,473Retained earnings at 1 April 20-5 546Cash and cash equivalents 236Accruals 47Prepayments 68Share premium 1,000Land – cost 2,500Buildings – cost 1,010Plant and equipment – cost 3,600Buildings – accumulated depreciation 335Plant and equipment – accumulated depreciation 1,520Inventories at 1 April 20-5 1,422Trade and other payables 1,507Purchases 6,417 22,178 22,178

c h a p t e r a c t i v i t i e s 1 7

Further information: • The inventories at the close of business on 31 March 20-6 cost £1,539,000. • The corporation tax charge for the year has been calculated as £80,000. • The land has been revalued by professional valuers at £2,750,000. The revaluation

is to be included in the financial statements for the year ended 31 March 20-6. • All of the operations are continuing operations.

Required:

(a) Draft the statement of profit or loss and other comprehensive income for Goonvrea Limited for the year ended 31 March 20-6.

(b) Draft the statement of financial position for Goonvrea Limited as at 31 March 20-6.

1 8 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

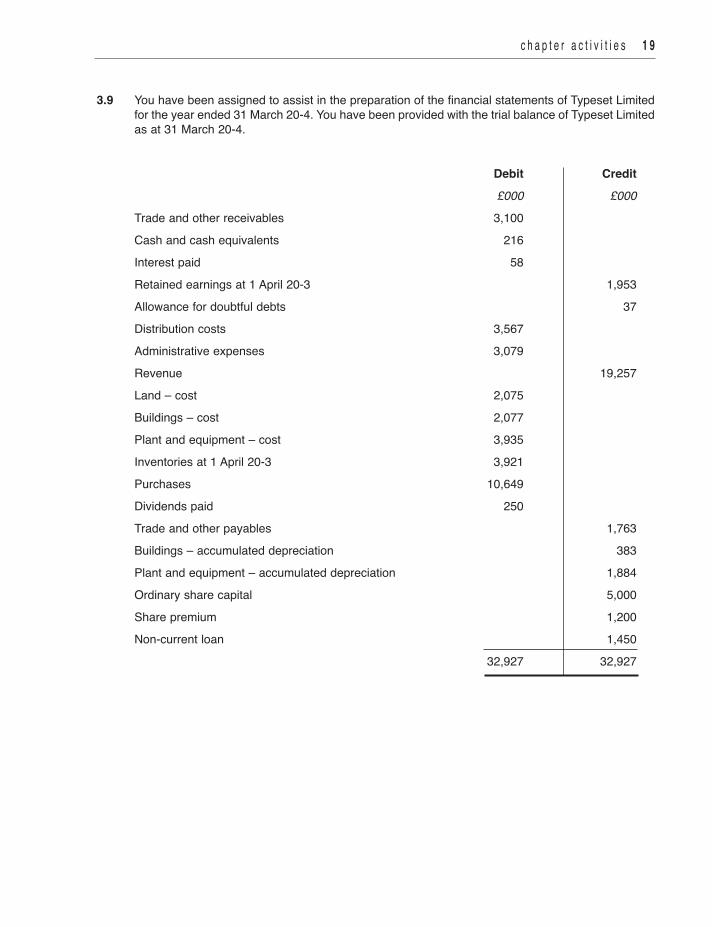

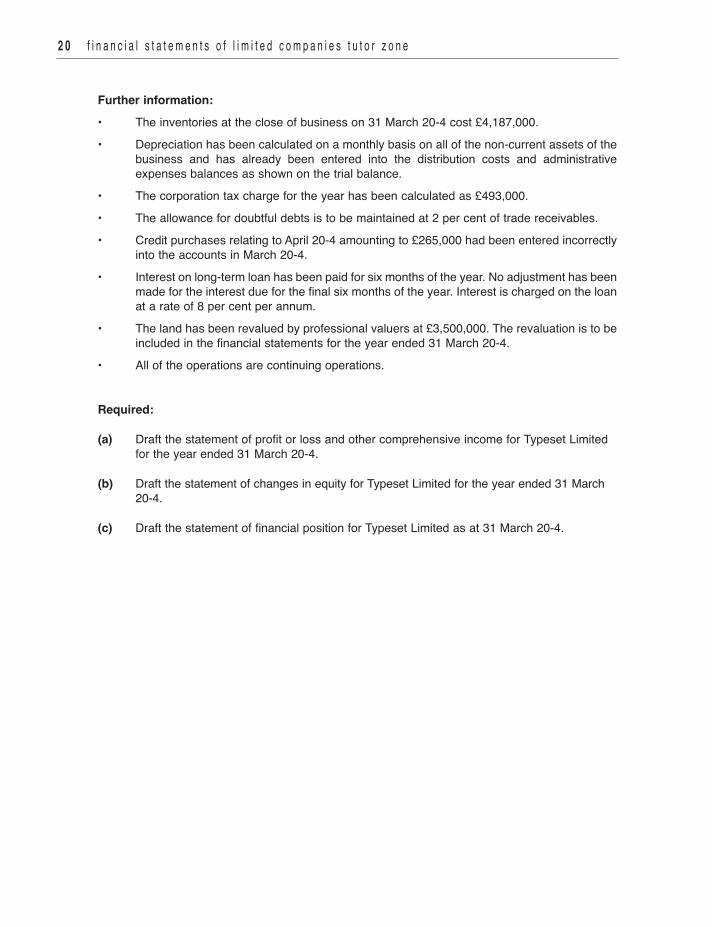

3.9 You have been assigned to assist in the preparation of the financial statements of Typeset Limitedfor the year ended 31 March 20-4. You have been provided with the trial balance of Typeset Limitedas at 31 March 20-4.

Debit Credit £000 £000 Trade and other receivables 3,100 Cash and cash equivalents 216 Interest paid 58 Retained earnings at 1 April 20-3 1,953 Allowance for doubtful debts 37 Distribution costs 3,567 Administrative expenses 3,079 Revenue 19,257 Land – cost 2,075 Buildings – cost 2,077 Plant and equipment – cost 3,935 Inventories at 1 April 20-3 3,921 Purchases 10,649 Dividends paid 250 Trade and other payables 1,763 Buildings – accumulated depreciation 383 Plant and equipment – accumulated depreciation 1,884 Ordinary share capital 5,000 Share premium 1,200 Non-current loan 1,450 32,927 32,927

c h a p t e r a c t i v i t i e s 1 9

Further information: • The inventories at the close of business on 31 March 20-4 cost £4,187,000. • Depreciation has been calculated on a monthly basis on all of the non-current assets of the

business and has already been entered into the distribution costs and administrative expenses balances as shown on the trial balance.

• The corporation tax charge for the year has been calculated as £493,000. • The allowance for doubtful debts is to be maintained at 2 per cent of trade receivables. • Credit purchases relating to April 20-4 amounting to £265,000 had been entered incorrectly

into the accounts in March 20-4. • Interest on long-term loan has been paid for six months of the year. No adjustment has been

made for the interest due for the final six months of the year. Interest is charged on the loan at a rate of 8 per cent per annum.

• The land has been revalued by professional valuers at £3,500,000. The revaluation is to be included in the financial statements for the year ended 31 March 20-4.

• All of the operations are continuing operations.

Required:

(a) Draft the statement of profit or loss and other comprehensive income for Typeset Limited for the year ended 31 March 20-4.

(b) Draft the statement of changes in equity for Typeset Limited for the year ended 31 March 20-4.

(c) Draft the statement of financial position for Typeset Limited as at 31 March 20-4.

2 0 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

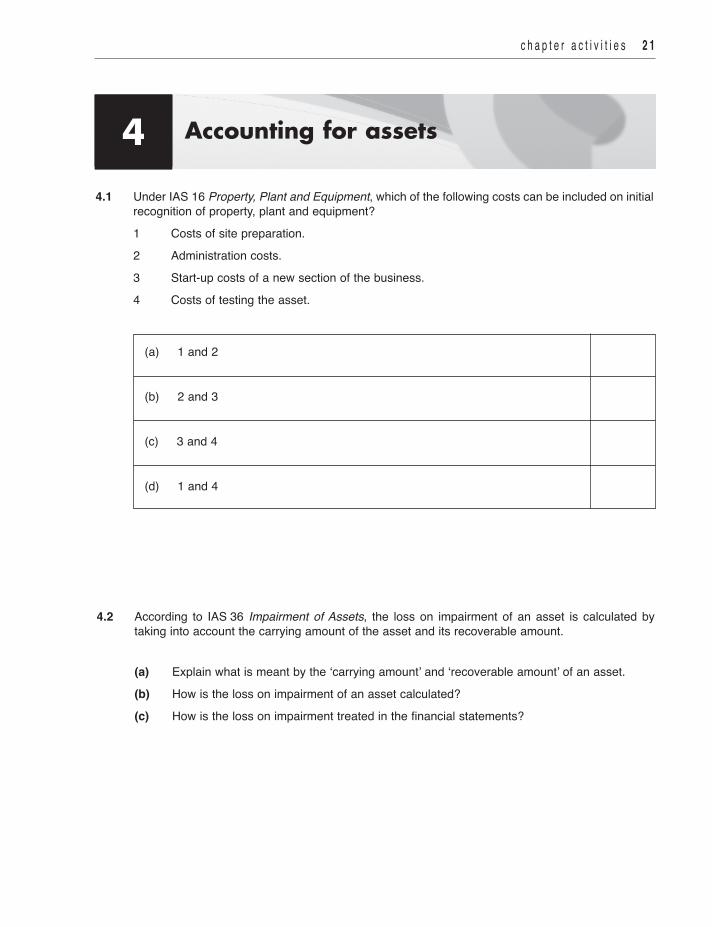

4.1 Under IAS 16 Property, Plant and Equipment, which of the following costs can be included on initialrecognition of property, plant and equipment?

1 Costs of site preparation. 2 Administration costs. 3 Start-up costs of a new section of the business. 4 Costs of testing the asset.

(a) 1 and 2

(b) 2 and 3

(c) 3 and 4

(d) 1 and 4

c h a p t e r a c t i v i t i e s 2 1

4.2 According to IAS 36 Impairment of Assets, the loss on impairment of an asset is calculated bytaking into account the carrying amount of the asset and its recoverable amount.

(a) Explain what is meant by the ‘carrying amount’ and ‘recoverable amount’ of an asset. (b) How is the loss on impairment of an asset calculated? (c) How is the loss on impairment treated in the financial statements?

Accounting for assets4

2 2 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

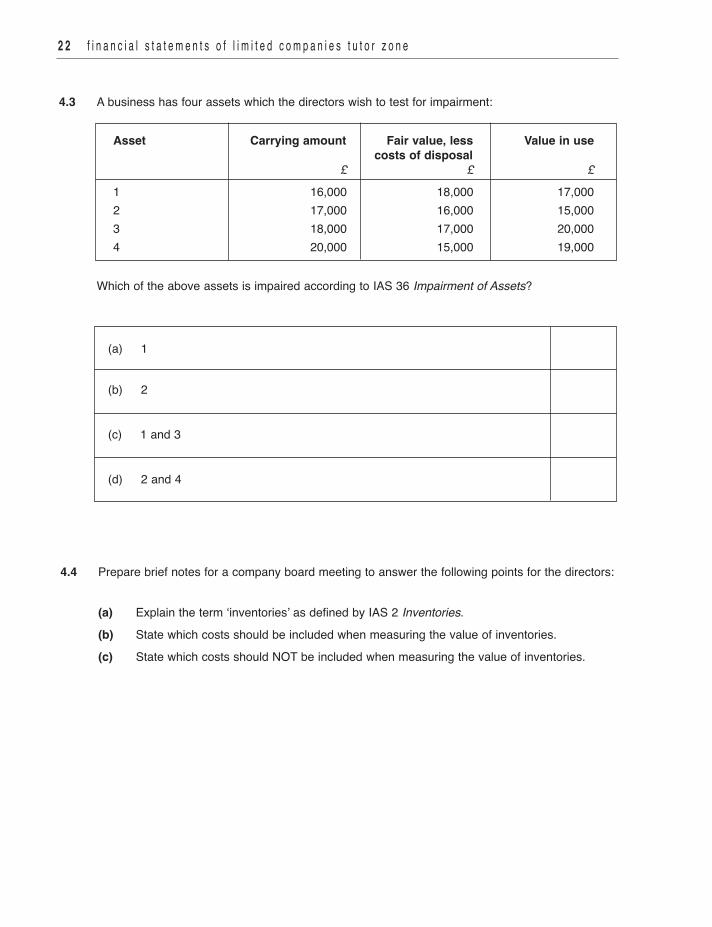

4.3 A business has four assets which the directors wish to test for impairment:

Which of the above assets is impaired according to IAS 36 Impairment of Assets?

(a) 1

(b) 2

(c) 1 and 3

(d) 2 and 4

Asset Carrying amount Fair value, less Value in use costs of disposal £ £ £

1 16,000 18,000 17,0002 17,000 16,000 15,0003 18,000 17,000 20,0004 20,000 15,000 19,000

4.4 Prepare brief notes for a company board meeting to answer the following points for the directors:

(a) Explain the term ‘inventories’ as defined by IAS 2 Inventories. (b) State which costs should be included when measuring the value of inventories. (c) State which costs should NOT be included when measuring the value of inventories.

c h a p t e r a c t i v i t i e s 2 3

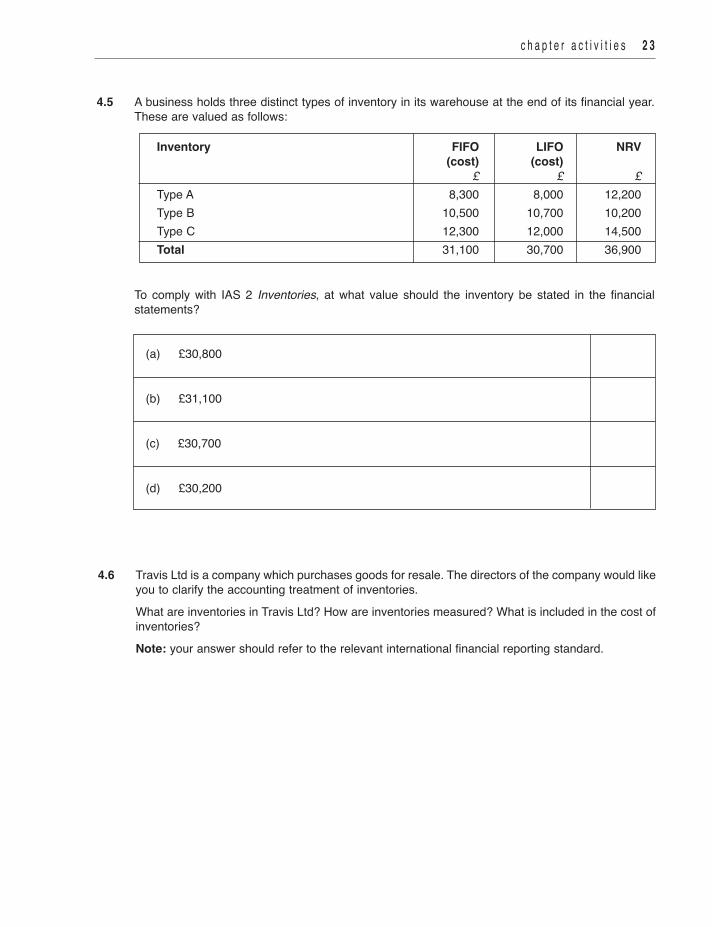

4.5 A business holds three distinct types of inventory in its warehouse at the end of its financial year.These are valued as follows:

To comply with IAS 2 Inventories, at what value should the inventory be stated in the financialstatements?

(a) £30,800

(b) £31,100

(c) £30,700

(d) £30,200

Inventory FIFO LIFO NRV (cost) (cost) £ £ £Type A 8,300 8,000 12,200 Type B 10,500 10,700 10,200Type C 12,300 12,000 14,500Total 31,100 30,700 36,900

4.6 Travis Ltd is a company which purchases goods for resale. The directors of the company would likeyou to clarify the accounting treatment of inventories.What are inventories in Travis Ltd? How are inventories measured? What is included in the cost ofinventories?

Note: your answer should refer to the relevant international financial reporting standard.

2 4 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

4.7 You have been approached by Samuel Taylor, who runs a trading company, Tayloriana Limited forhelp with the year end financial statements. He employs a bookkeeper who has produced anextended trial balance for the company as at 31 March 20-5. Samuel is negotiating to merge hiscompany with Coleridge Limited, which operates in the same area of activity as his own. Thedirectors of Coleridge Limited would like to see the latest profit figures of Samuel's business. Youhave been asked to assist in the preparation of a statement of comprehensive income for the yearended 31 March 20-5.Samuel Taylor has given you the following information from Tayloriana Limited:1 Inventories have been counted on 31 March 20-5. The cost of the inventories calculated on

a first in, first out basis is £49,300. The selling price of the inventories is estimated at£65,450.

2 After the year-end, one of the trade receivables, whose year-end balance was £2,500 wentinto liquidation. The liquidator has stated that there are no assets available to pay claimants.No provision for this bad (irrecoverable) debt has been made in the financial statements andthe balance is still included in year-end trade receivables figure.

TaskExplain to Samuel Taylor the appropriate accounting treatment of the above items by reference toapplicable accounting standards.

4.8 Prepare briefing notes for a company board meeting dealing with the following matters:(a) How a revaluation surplus could arise.(b) The recommendation of one of the directors is to lease assets as he says that this means

that the assets can be kept off the statement of financial position. Comment on thisrecommendation.

4.9 Elizabeth Ogier is the Managing Director and major shareholder of Ogier Perfumes Limited, awholesale perfume business. She has asked you to assist in the preparation of the year-endfinancial statements of the company.• The inventories at the close of business on 30 September 20-9 were valued at cost at

£49,477. However, included in this balance were some items which had cost £8,200 but itis estimated that they could now be sold for only £4,800.

• The purchases figure includes items to the value of £2,000 which Elizabeth took for personaluse and for gifts to friends.

TaskDraft a letter to Ms Ogier justifying any adjustments you have made to:• the inventories valuation on 30 September 20-9• the balances in the trial balance as a result of her taking items from the company for

personal use or for gifts to friendsYour explanation should make reference, where relevant, to accounting concepts and applicableinternational financial reporting standards.

c h a p t e r a c t i v i t i e s 2 5

4.10 IAS 1 Presentation of Financial Statements, requires the disclosure of accounting policies in thenotes to the financial statements.Explain why the disclosure of accounting policies is useful to users of financial statements. Illustrateyour answer with reference to:(a) Depreciation.(b) Research and development.(c) Inventories.

2 6 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

5.1 With reference to IAS 37 Provisions, Contingent Liabilities and Contingent Assets, you are to:

(a) Define a provision and explain the accounting treatment, if any, in the year-end financialstatements.

(b) Define a contingent liability and explain the accounting treatment, if any, in the year-endfinancial statements.

5.2 A business prepares its financial statements to 31 December each year. The following events tookplace after 31 December but before the date on which the financial statements were authorised forissue:

1 A major customer who owes money to the company at the end of the financial year isdeclared bankrupt.

2 A major purchase of non-current assets has been made.Which of the above is likely to be classified as an adjusting event under IAS 10 Events after theReporting Period?

(a) 1 only

(b) 2 only

(c) 1 and 2

(d) Neither 1 nor 2

Accounting for liabilities and thestatement of profit or loss5

c h a p t e r a c t i v i t i e s 2 7

5.3 Travis Ltd is a company which purchases goods for resale. The directors of the company would likeyou to clarify when they should recognise revenue arising from the sale of goods.

What is revenue in Travis Ltd? How should it be measured? When should revenue be recognised?

Note: your answer should refer to the relevant international financial reporting standard.

5.4 Following your preparation of the statement of profit or loss and other comprehensive income andstatement of financial position of Deskover Limited, you have had a meeting with the directors atwhich certain other matters were raised. One of the customers of Deskover Limited has been having cashflow problems. The accountbalance at the end of the year was £186,000. Against this there was a specific provision of £93,000.One month after the year-end, the directors received a letter from the liquidators of the customerstating that the business had gone into liquidation. The liquidators have stated that there will be noassets available to meet any of the amounts due to the unsecured claimants.

TaskState whether any adjustments need to be made to the financial statements of Deskover Limitedas a result of the liquidation of the customer. Set out any adjustment required in the form of a journalentry and justify the accounting treatment by reference to applicable international financial reportingstandards.

5.5 You have been asked to help prepare the financial statements of Brecked plc for the year ended31 March 20-1.Legal proceedings have been started against Brecked plc because of faulty products supplied to acustomer. The company’s lawyers advise that it is probable that the entity will be found liable fordamages of £250,000.Task 1Make any necessary journal entry in respect of the above information. The date and narrative arenot required.Task 2Explain your treatment of the probable damages arising from the legal proceedings. Refer, whererelevant, to international financial reporting standards.

2 8 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

6.1 Olson Ltd has a profit before tax of £40,000 for the year, and finance costs are £5,000. Thestatement of profit or loss and the statement of financial position show the following:

£Depreciation charge 15,000Decrease in inventories 4,000Increase in trade and other receivables 6,000Decrease in trade and other payables 3,000

What is the cash generated by operations for the year?

(a) £64,000 inflow

(b) £65,000 inflow

(c) £61,000 inflow

(d) £55,000 inflow

Statement of cash flows6

• A blank photocopiable pro-forma in the format used in AAT Assessments – of the statement ofcash flows, is included in the Appendix of Financial Statements of Limited Companies Tutorial –it is advisable to enlarge it to full A4 size. Blank workings sheets are also included in the Appendix.

• Pro-formas and workings sheets are also available to download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 2 9

6.2 Herrera Ltd has a loss before tax of £22,000 for the year and the statement of profit or loss and thestatement of financial position show the following:

£Depreciation charge 6,000Finance costs 2,000Increase in inventories 5,000Decrease in trade and other receivables 3,000Increase in trade and other payables 4,000

What is the cash generated by operations for the year?

(a) £2,000 outflow

(b) £16,000 outflow

(c) £12,000 outflow

(d) £14,000 outflow

3 0 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

6.3 You have been asked to help prepare the statement of cash flows and statement of changes inequity for Westlake Ltd for the year ended 31 March 20-1.

The most recent statement of profit or loss and statement of financial position (with comparativesfor the previous year) of Westlake Ltd are set out below.

Westlake Ltd – Statement of profit or loss for the year ended 31 March 20-1

£000Continuing operationsRevenue 22,000Cost of sales –13,400Gross profit 8,600Dividends received 50Loss on disposal of property, plant and equipment –20Distribution costs –3,380Administrative expenses –4,050Profit from operations 1,200Finance costs –83Profit before tax 1,117Tax –204Profit for the year from continuing operations 913

c h a p t e r a c t i v i t i e s 3 1

Westlake Ltd – Statement of financial position as at 31 March 20-1 20-1 20-0 £000 £000 Assets Non-current assets Property, plant and equipment 10,155 8,670

Current assets Inventories 2,745 2,320 Trade and other receivables 2,120 1,950 Cash and cash equivalents 0 47 4,865 4,317 Total assets 15,020 12,987

EQUITY AND LIABILITIES Equity Share capital 6,000 5,000 Share premium 1,250 1,000 Retained earnings 5,533 4,895 Total equity 12,783 10,895

Non-current liabilities Bank loans 850 600 850 600

Current liabilities Trade and other payables 1,076 1,154 Tax liability 204 338 Bank overdraft 107 0 1,387 1,492 Total liabilities 2,237 2,092 Total equity and liabilities 15,020 12,987

Further information:• The total depreciation charge for the year was £1,755,000.• Property, plant and equipment costing £356,000 with accumulated depreciation of £247,000

was sold in the year.• All sales and purchases were on credit. Other expenses were paid for in cash.• A dividend of £275,000 was paid during the year.

(a) Prepare a reconciliation of profit before tax to net cash from operating activities for Westlake Ltd for the year ended 31 March 20-1.

(b) Prepare the statement of cash flows for Westlake Ltd for the year ended 31 March20-1.

(c) Draft the statement of changes in equity for Westlake Ltd for the year ended 31 March20-1.

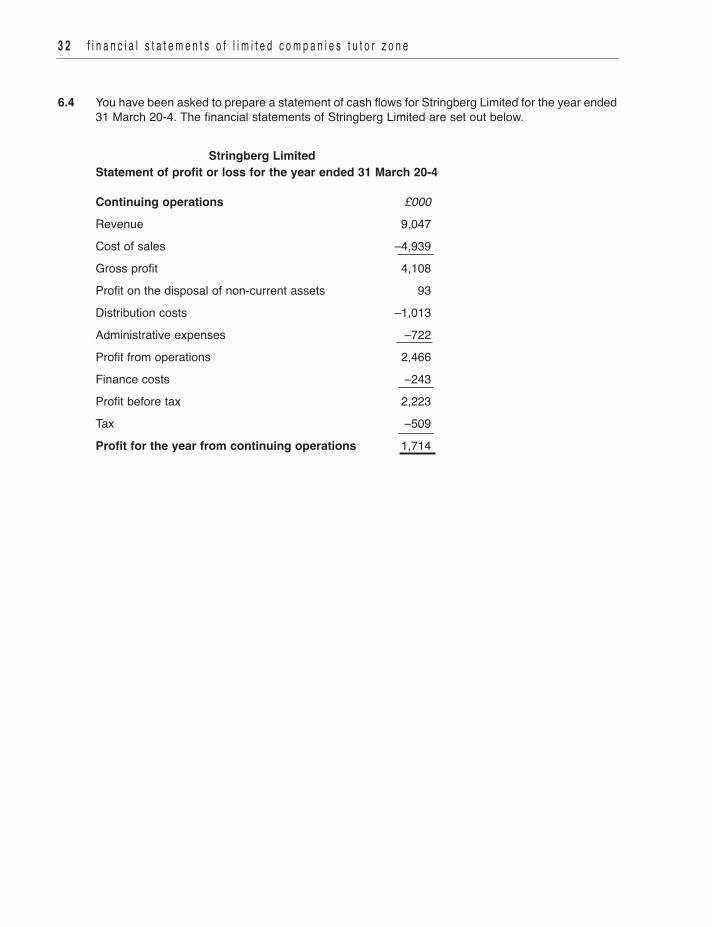

6.4 You have been asked to prepare a statement of cash flows for Stringberg Limited for the year ended31 March 20-4. The financial statements of Stringberg Limited are set out below.

Stringberg LimitedStatement of profit or loss for the year ended 31 March 20-4

Continuing operations £000Revenue 9,047Cost of sales –4,939Gross profit 4,108Profit on the disposal of non-current assets 93Distribution costs –1,013Administrative expenses –722Profit from operations 2,466Finance costs –243Profit before tax 2,223Tax –509Profit for the year from continuing operations 1,714

3 2 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

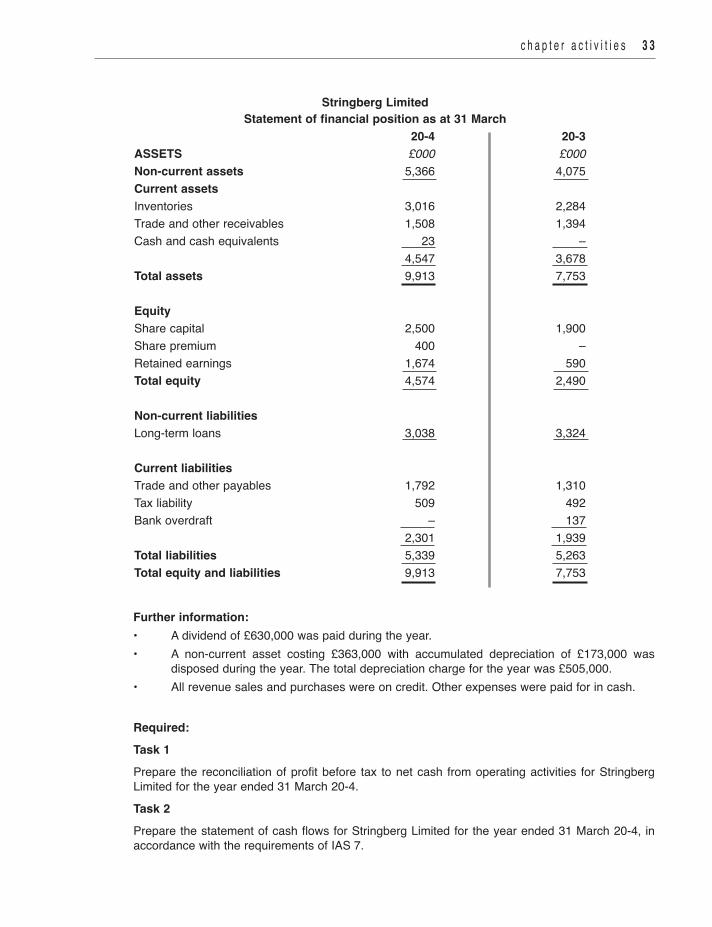

c h a p t e r a c t i v i t i e s 3 3

Stringberg LimitedStatement of financial position as at 31 March

20-4 20-3ASSETS £000 £000Non-current assets 5,366 4,075Current assetsInventories 3,016 2,284Trade and other receivables 1,508 1,394Cash and cash equivalents 23 – 4,547 3,678Total assets 9,913 7,753

EquityShare capital 2,500 1,900Share premium 400 –Retained earnings 1,674 590Total equity 4,574 2,490

Non-current liabilitiesLong-term loans 3,038 3,324

Current liabilitiesTrade and other payables 1,792 1,310Tax liability 509 492Bank overdraft – 137 2,301 1,939Total liabilities 5,339 5,263Total equity and liabilities 9,913 7,753

Further information: • A dividend of £630,000 was paid during the year. • A non-current asset costing £363,000 with accumulated depreciation of £173,000 was

disposed during the year. The total depreciation charge for the year was £505,000. • All revenue sales and purchases were on credit. Other expenses were paid for in cash.

Required:Task 1Prepare the reconciliation of profit before tax to net cash from operating activities for StringbergLimited for the year ended 31 March 20-4.Task 2Prepare the statement of cash flows for Stringberg Limited for the year ended 31 March 20-4, inaccordance with the requirements of IAS 7.

3 4 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

7.1 A limited company has the following statement of profit or loss:

(a) State the formula that is used to calculate each of the following ratios: (1) Gross profit percentage (2) Administrative expenses/revenue percentage (3) Operating profit percentage (4) Interest cover

(b) Calculate the above ratios (to the nearest one decimal place).

£000Continuing operationsRevenue 350Cost of sales –190Gross profit 160Distribution costs –40Administrative expenses –65Profit from operations 55Finance costs –12Profit before tax 43Tax –6Profit for the year from continuing operations 37

Interpretation of financial statements7

c h a p t e r a c t i v i t i e s 3 5

7.2 The following information is taken from the statement of financial position of a limited company.

(a) State the formula that is used to calculate each of the following ratios: (1) Current ratio (2) Acid test (quick) ratio (3) Inventory turnover (4) Inventory holding period (5) Trade receivables collection period (6) Trade payables payment period (7) Gearing

(b) Calculate the above ratios (to the nearest one decimal place).

£000Inventories 175Trade receivables 210Bank overdraft 35Trade payables 190Non-current liabilities 355Share capital 600Retained earnings 145

Further information:Revenue for year 3,110Cost of sales for year 2,045

3 6 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

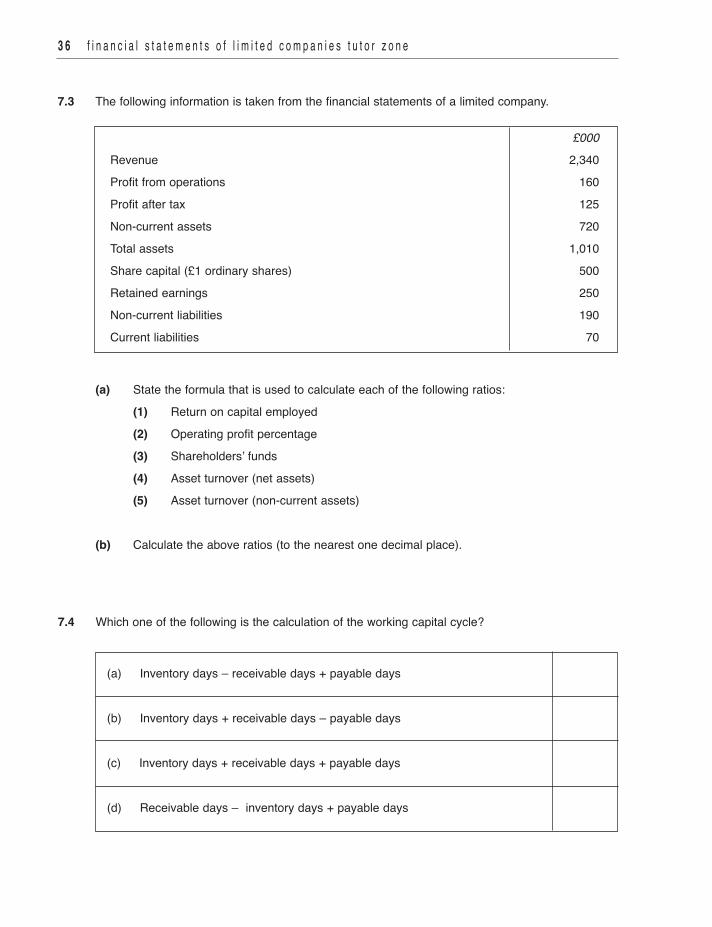

7.3 The following information is taken from the financial statements of a limited company.

(a) State the formula that is used to calculate each of the following ratios: (1) Return on capital employed (2) Operating profit percentage (3) Shareholders’ funds (4) Asset turnover (net assets) (5) Asset turnover (non-current assets)

(b) Calculate the above ratios (to the nearest one decimal place).

£000Revenue 2,340Profit from operations 160Profit after tax 125Non-current assets 720Total assets 1,010Share capital (£1 ordinary shares) 500Retained earnings 250Non-current liabilities 190Current liabilities 70

7.4 Which one of the following is the calculation of the working capital cycle?

(a) Inventory days – receivable days + payable days

(b) Inventory days + receivable days – payable days

(c) Inventory days + receivable days + payable days

(d) Receivable days – inventory days + payable days

c h a p t e r a c t i v i t i e s 3 7

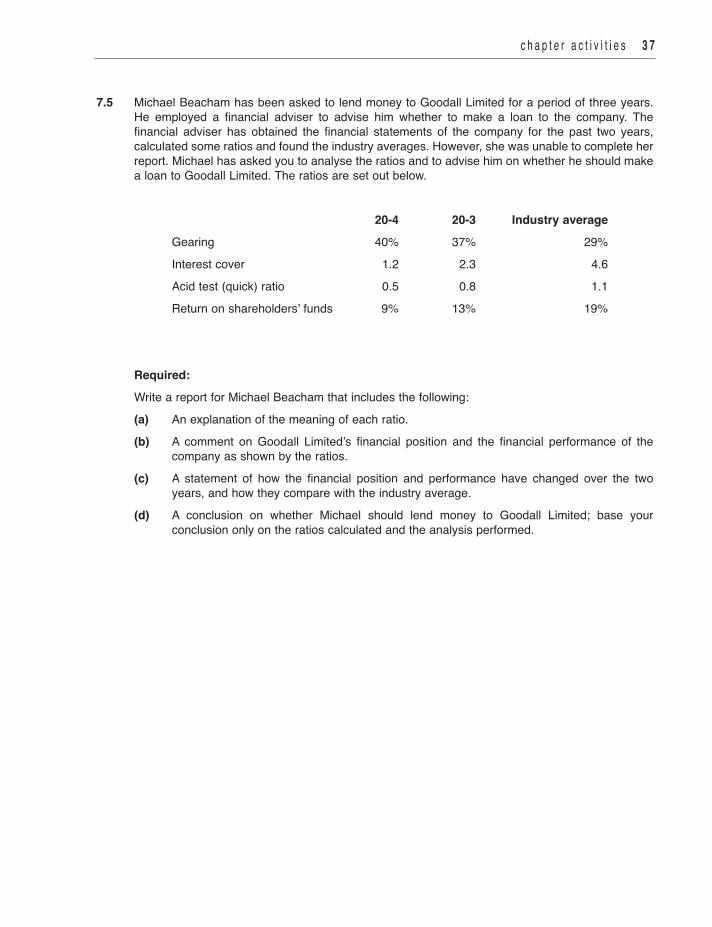

7.5 Michael Beacham has been asked to lend money to Goodall Limited for a period of three years.He employed a financial adviser to advise him whether to make a loan to the company. Thefinancial adviser has obtained the financial statements of the company for the past two years,calculated some ratios and found the industry averages. However, she was unable to complete herreport. Michael has asked you to analyse the ratios and to advise him on whether he should makea loan to Goodall Limited. The ratios are set out below.

20-4 20-3 Industry average Gearing 40% 37% 29% Interest cover 1.2 2.3 4.6 Acid test (quick) ratio 0.5 0.8 1.1 Return on shareholders’ funds 9% 13% 19%

Required: Write a report for Michael Beacham that includes the following: (a) An explanation of the meaning of each ratio. (b) A comment on Goodall Limited’s financial position and the financial performance of the

company as shown by the ratios. (c) A statement of how the financial position and performance have changed over the two

years, and how they compare with the industry average. (d) A conclusion on whether Michael should lend money to Goodall Limited; base your

conclusion only on the ratios calculated and the analysis performed.

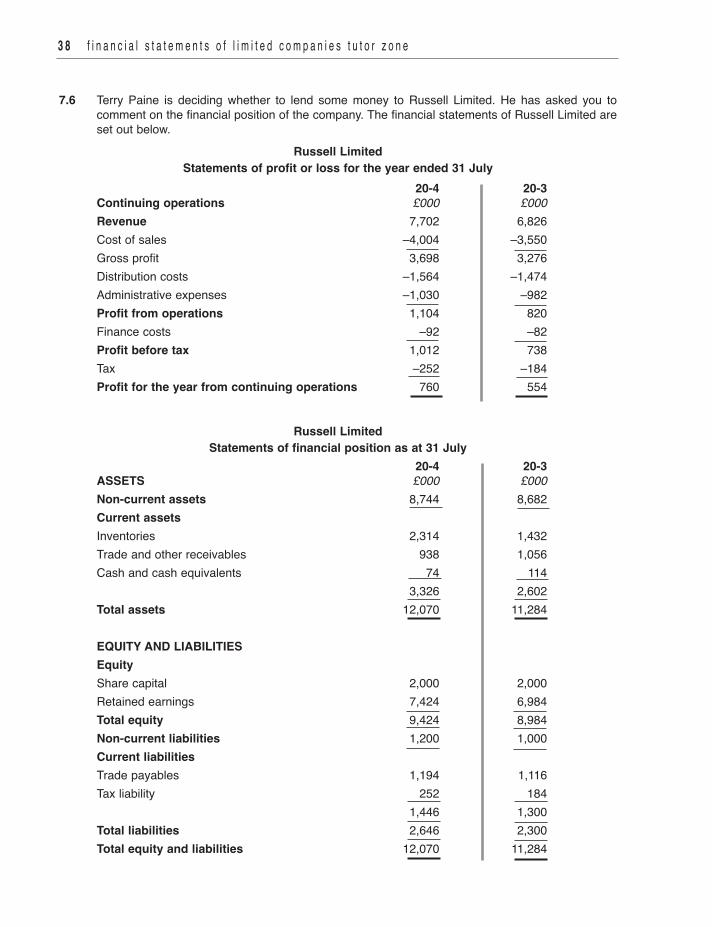

7.6 Terry Paine is deciding whether to lend some money to Russell Limited. He has asked you tocomment on the financial position of the company. The financial statements of Russell Limited areset out below.

Russell LimitedStatements of profit or loss for the year ended 31 July

20-4 20-3Continuing operations £000 £000Revenue 7,702 6,826Cost of sales –4,004 –3,550Gross profit 3,698 3,276Distribution costs –1,564 –1,474Administrative expenses –1,030 –982Profit from operations 1,104 820Finance costs –92 –82Profit before tax 1,012 738Tax –252 –184Profit for the year from continuing operations 760 554

Russell LimitedStatements of financial position as at 31 July

20-4 20-3ASSETS £000 £000Non-current assets 8,744 8,682Current assetsInventories 2,314 1,432Trade and other receivables 938 1,056Cash and cash equivalents 74 114 3,326 2,602Total assets 12,070 11,284

EQUITY AND LIABILITIES EquityShare capital 2,000 2,000Retained earnings 7,424 6,984Total equity 9,424 8,984Non-current liabilities 1,200 1,000Current liabilitiesTrade payables 1,194 1,116Tax liability 252 184 1,446 1,300Total liabilities 2,646 2,300Total equity and liabilities 12,070 11,284

3 8 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

Required:Prepare a report for Terry Paine that includes the following:

(a) A calculation of the following ratios of Russell Limited for each of the two years: • Current ratio • Acid test (quick) ratio • Gearing • Interest cover (b) An explanation of the meaning of each ratio. (c) A comment on the financial position of Russell Limited as shown by the ratios. (d) A comment on the way the financial position has changed over the two years covered by the

financial statements. (e) A conclusion on whether Terry Paine should lend money to Russell Limited. Base your

conclusion only on the ratios calculated and analysis performed.

c h a p t e r a c t i v i t i e s 3 9

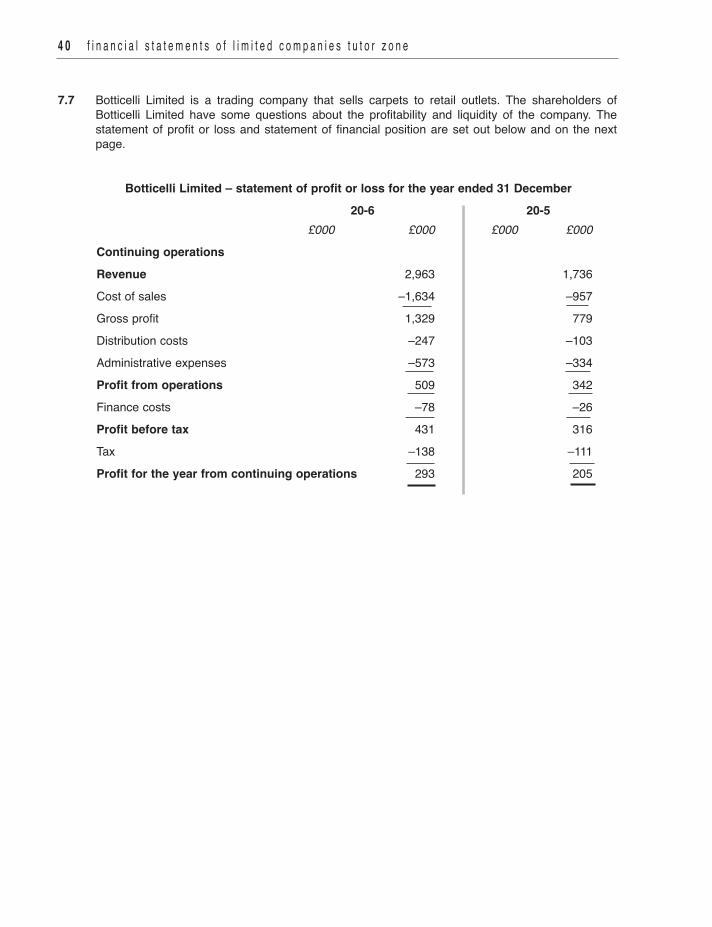

7.7 Botticelli Limited is a trading company that sells carpets to retail outlets. The shareholders ofBotticelli Limited have some questions about the profitability and liquidity of the company. Thestatement of profit or loss and statement of financial position are set out below and on the nextpage.

Botticelli Limited – statement of profit or loss for the year ended 31 December 20-6 20-5 £000 £000 £000 £000Continuing operationsRevenue 2,963 1,736Cost of sales –1,634 –957Gross profit 1,329 779Distribution costs –247 –103Administrative expenses –573 –334Profit from operations 509 342Finance costs –78 –26Profit before tax 431 316Tax –138 –111Profit for the year from continuing operations 293 205

4 0 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

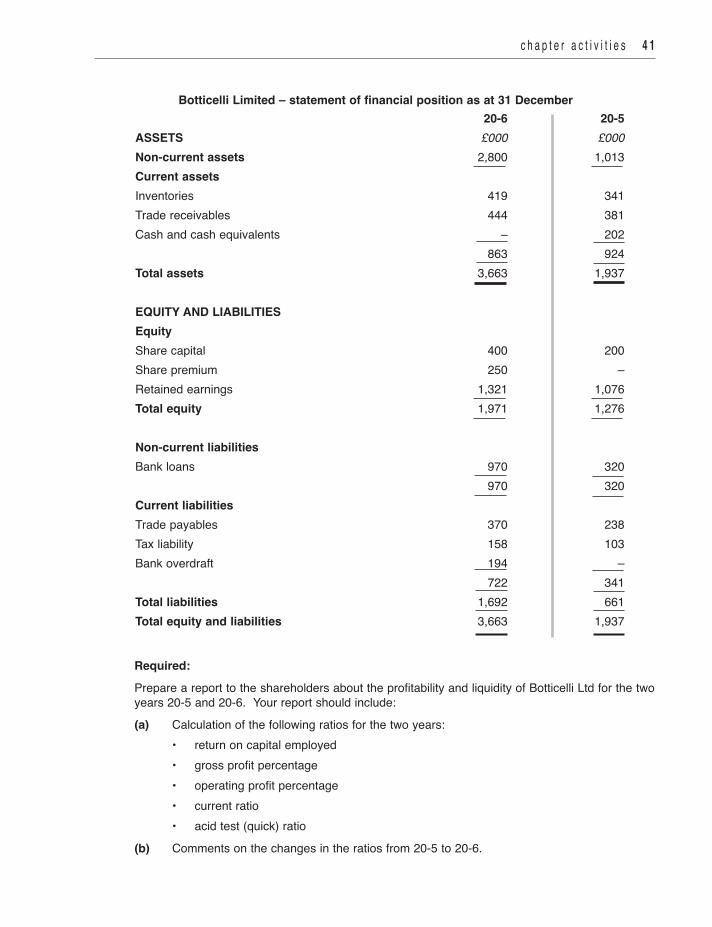

Botticelli Limited – statement of financial position as at 31 December 20-6 20-5ASSETS £000 £000Non-current assets 2,800 1,013Current assetsInventories 419 341Trade receivables 444 381Cash and cash equivalents – 202 863 924Total assets 3,663 1,937

EQUITY AND LIABILITIESEquityShare capital 400 200Share premium 250 –Retained earnings 1,321 1,076Total equity 1,971 1,276

Non-current liabilitiesBank loans 970 320 970 320Current liabilitiesTrade payables 370 238Tax liability 158 103Bank overdraft 194 – 722 341Total liabilities 1,692 661Total equity and liabilities 3,663 1,937

Required:Prepare a report to the shareholders about the profitability and liquidity of Botticelli Ltd for the twoyears 20-5 and 20-6. Your report should include:(a) Calculation of the following ratios for the two years: • return on capital employed • gross profit percentage • operating profit percentage • current ratio • acid test (quick) ratio(b) Comments on the changes in the ratios from 20-5 to 20-6.

c h a p t e r a c t i v i t i e s 4 1

4 2 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

8.1 Hyde plc invested £400,000 in 240,000 ordinary shares of £1 each in Park Limited. At the date ofacquisition the equity of Park Limited comprised £400,000 in share capital and £160,000 in retainedearnings.

What is the value of goodwill at the date of acquisition?

(a) £64,000

(b) £240,000

(c) £160,000

(d) £400,000

8.2 At 31 March 20-1 the equity of Gate Limited comprises £200,000 in share capital and £120,000 inretained earnings. The parent company, Alder plc, currently owns 150,000 of £1 ordinary shares inGate Limited.

What is the value of the non-controlling interest at 31 March 20-1?

(a) £30,000

(b) £50,000

(c) £240,000

(d) £80,000

Consolidated financial statements8• Blank photocopiable pro-formas in the format used in AAT Assessments – of the consolidated

statement of profit or loss, and the consolidated statement of financial position, are includedin the Appendix of Financial Statements of Limited Companies Tutorial – it is advisable toenlarge them to full A4 size. Blank workings sheets are also included in the Appendix.

• Pro-formas and workings sheets are also available to download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 4 3

8.3 Clerk plc owns 80% of the ordinary shares in Well Limited. Revenue for the year ended 31 March20-1 is: Clerk £400,000, Well £150,000. The revenue of Clerk plc includes goods sold to WellLimited for £15,000. All of these goods still remain in the inventory of Well Limited at the end of theyear.

What is the value for revenue that will be shown in the consolidated statement of profit or loss forClerk plc and its subsidiary undertaking for the year ended 31 March 20-1?

(a) £550,000

(b) £535,000

(c) £565,000

(d) £515,000

4 4 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

8.4 The Finance Director of Wood plc has asked you to prepare the draft consolidated statement ofprofit or loss for the group. The company has one subsidiary undertaking, Plank Limited. Thestatements of profit or loss for the two companies, prepared for internal purposes, for the yearended 31 March 20-1 are set out below.

Statements of profit or loss for the year ended 31 March 20-1

Wood plc Plank LimitedContinuing operations £000 £000Revenue 31,600 10,800Cost of sales –17,000 –5,600Gross profit 14,600 5,200Distribution costs –3,600 –1,300Administrative expenses –3,000 –1,160Dividends received from Plank Limited 600Profit from operations 8,600 2,740Finance costs –1,600 –240Profit before tax 7,000 2,500Tax –2,240 –740Profit for the year from continuing operations 4,760 1,760

Further information:• Wood plc acquired 75% of the issued share capital and voting rights of Plank Limited on 1 April 20-0.• During the year Plank Limited sold goods which had cost £600,000 to Wood plc for £1,000,000. All of the goods had been sold by Wood plc by the end of the year.• Dividends paid during the year were: Wood plc, £1,500,000 Plank Limited, £800,000• There were no impairment losses on goodwill during the year.

Required:Draft a consolidated statement of profit or loss for Wood plc and its subsidiary undertaking for theyear ended 31 March 20-1.

c h a p t e r a c t i v i t i e s 4 5

8.5 You have been asked to assist in the preparation of the consolidated financial statements of theJake Group. Set out below are the statements of financial position of Jake Limited and Dinos Limited as at 30 September 20-1:

Statements of financial position as at 30 September 20-1 Jake Ltd Dinos LtdASSETS £000 £000Non-current assets 18,104 6,802Investment in Dinos Limited 5,000 Current assets 4,852 2,395Total assets 27,956 9,197

EQUITY AND LIABILITIESEquityShare capital 5,000 1,000Share premium 3,000 400Retained earnings 13,080 6,250Total equity 21,080 7,650Non-current liabilitiesLong-term loan 4,500 1,000Current liabilities 2,376 547Total liabilities 6,876 1,547Total equity and liabilities 27,956 9,197

Further information: • The share capital of both Jake Limited and Dinos Limited consists of ordinary shares of £1

each. There have been no changes to the balances of share capital and share premiumduring the year. No dividends were paid by Dinos Limited during the year.

• Jake Limited acquired 600,000 of the issued share capital and voting rights of Dinos Limitedon 30 September 20-0.

• At 30 September 20-0 the retained earnings of Dinos Limited were £5,450,000. • The fair value of the non-current assets of Dinos Limited at 30 September 20-0 was

£3,652,000 as compared with their carrying amount of £3,052,000. The revaluation has notbeen reflected in the books of Dinos Limited (ignore any depreciation implications).

• For the year to 30 September 20-1, Jake Limited has written off ten per cent of the goodwillon the acquisition of Dinos Limited as an impairment loss.

• Jake Limited has decided non-controlling interest will be valued at their proportionate shareof net assets.

Required: You are to prepare the consolidated statement of financial position of Jake Limited and its

subsidiary undertaking as at 30 September 20-1.

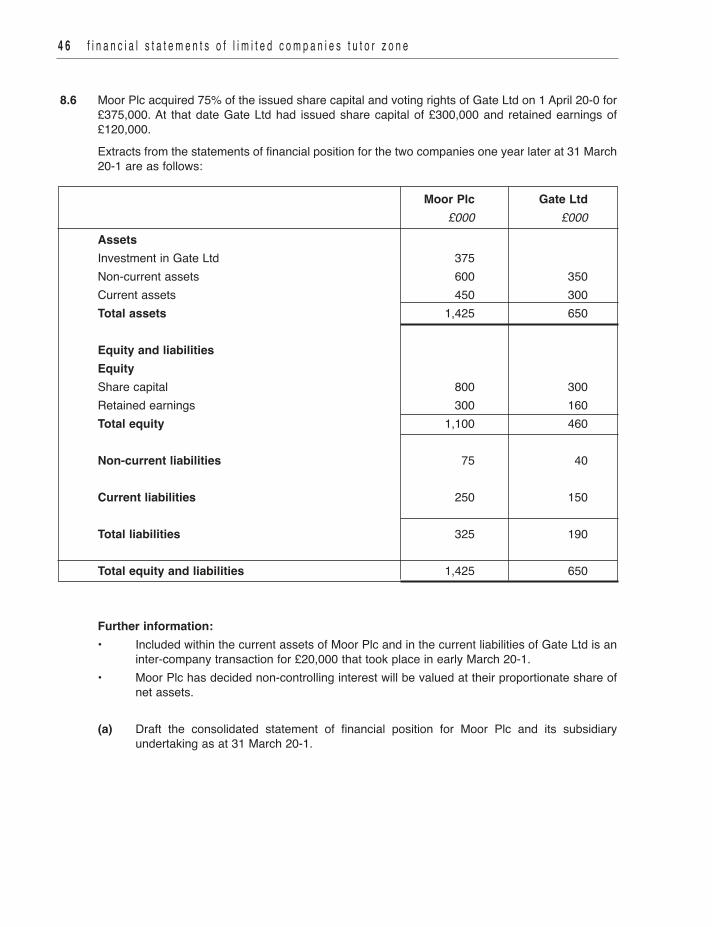

8.6 Moor Plc acquired 75% of the issued share capital and voting rights of Gate Ltd on 1 April 20-0 for£375,000. At that date Gate Ltd had issued share capital of £300,000 and retained earnings of£120,000.Extracts from the statements of financial position for the two companies one year later at 31 March20-1 are as follows:

Moor Plc Gate Ltd £000 £000AssetsInvestment in Gate Ltd 375Non-current assets 600 350Current assets 450 300Total assets 1,425 650

Equity and liabilitiesEquityShare capital 800 300Retained earnings 300 160Total equity 1,100 460

Non-current liabilities 75 40

Current liabilities 250 150

Total liabilities 325 190

Total equity and liabilities 1,425 650

Further information:• Included within the current assets of Moor Plc and in the current liabilities of Gate Ltd is an inter-company transaction for £20,000 that took place in early March 20-1. • Moor Plc has decided non-controlling interest will be valued at their proportionate share of net assets.

(a) Draft the consolidated statement of financial position for Moor Plc and its subsidiary undertaking as at 31 March 20-1.

4 6 f i n a n c i a l s t a t e m e n t s o f l i m i t e d c o m p a n i e s t u t o r z o n e

West Plc acquired 60% of the issued share capital and voting rights of Minster Ltd on 1 April 20-0.Extracts from their statements of profit or loss for the year ended 31 March 20-1 are shown below:

West Plc Minster Ltd £000 £000Continuing operationsRevenue 5,200 2,400Cost of sales –2,400 –1,500Gross profit 2,800 900Other income – dividend from Minster Ltd 100 –Distribution costs and administrative expenses –1,700 –350Profit before tax 1,200 550

Additional data:During the year Minster Ltd sold goods which had cost £60,000 to West Plc for £80,000. One-quarter of these goods still remain in inventory at the end of the year.

(b) Draft the consolidated statement of profit or loss for West Plc and its subsidiary undertaking up to and including the profit before tax line for the year ended 31 March 20-1.

c h a p t e r a c t i v i t i e s 4 7