Embed Size (px)

Citation preview

Financial Financial StatementsStatements

Andrew GrahamAndrew Graham

Queens UniversityQueens University

School of Policy StudiesSchool of Policy StudiesTwo LecturesTwo Lectures

Canadian Public Sector Financial Management

2

The Road to Financial Statement Enlightenment

Comp. Inc.

S/H Equity Stmt

Cash Flows

Income Statement

Balance SheetShould I stop and ask

for directions?

Canadian Public Sector Financial Management

3

A number must be kept in contextin context with the financial statementfinancial statement where it is presented…

Warning! All numbers are not the same!

Canadian Public Sector Financial Management

4

Beware of Financial VertigoBeware of Financial Vertigo

• Easy to get confused with terminology• Much of what passes for complexity in

financial statements is a terminology issue

• Sometimes this is counterintuitive – debits and credits as an example

• Terminology used often has the same meaning, e.g. revenue and income do not mean the same thing

Canadian Public Sector Financial Management

5

Purpose of Financial Purpose of Financial StatementsStatements

• To establish the basic rules and assumptions that are used to provide financial information

• They will tell the accountant and end user what financial items are to be measured and when and how to measure them.

Canadian Public Sector Financial Management

6

Source: Public Service Accounting Board, CICA

Canadian Public Sector Financial Management

7

Section 1Section 1The Accounting CycleThe Accounting Cycle

Canadian Public Sector Financial Management

8

Canadian Public Sector Financial Management

9

The Accounting CycleThe Accounting Cycle

The accounting process is a series of activities that begins with a transaction and ends with the closing of the books. Because this process is repeated each reporting period, it is referred to as the accounting cycle and includes these major steps:

• Identify the transaction or other recognizable event.• Prepare the transaction's source document such as

a purchase order or invoice.• Analyze and classify the transaction. • Record the transaction by making entries in the

appropriate journal. Such entries are made in chronological order.

Canadian Public Sector Financial Management

10

The Accounting CycleThe Accounting Cycle

• Post general journal entries to the ledger accounts.

The above steps are performed throughout the accounting period as transactions occur or in periodic batch processes. The following steps are performed at the end of the accounting period:

• Prepare the trial balance to make sure that debits equal credits.

• Correct any discrepancies in the trial balance. If the columns are not in balance, look for math errors, posting errors, and recording errors. Posting errors include:

posting of the wrong amount, omitting a posting, posting in the wrong column, or posting more than once.

Canadian Public Sector Financial Management

11

The Accounting CycleThe Accounting Cycle

• Prepare adjusting entries to record accrued, deferred, and estimated amounts.

• Post adjusting entries to the ledger accounts.• Prepare the adjusted trial balance. This step is

similar to the preparation of the unadjusted trial balance, but this time the adjusting entries are included. Correct any errors that may be found.

• Prepare the financial statements. Income statement: prepared from the revenue, expenses, gains,

and losses. Balance sheet: prepared from the assets, liabilities, and equity

accounts. Cash flow statement: derived from the other financial statements

using either the direct or indirect method.

Canadian Public Sector Financial Management

12

The Accounting CycleThe Accounting Cycle

• Prepare closing journal entries that close temporary accounts such as revenues, expenses, gains, and losses.

• Post closing entries to the ledger accounts.

Canadian Public Sector Financial Management

13

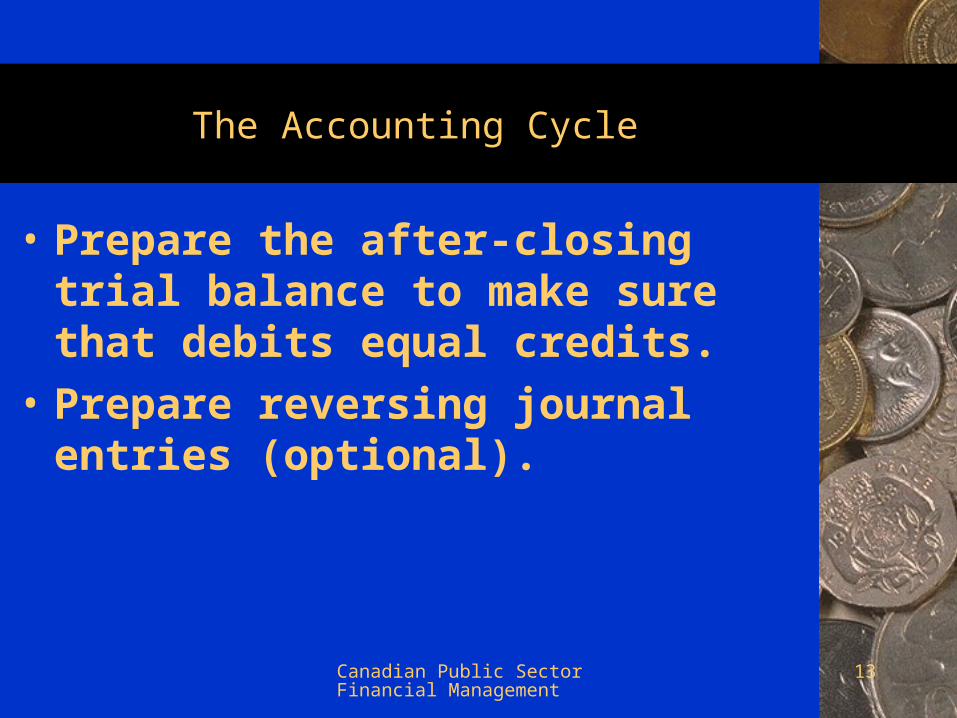

The Accounting CycleThe Accounting Cycle

• Prepare the after-closing trial balance to make sure that debits equal credits.

• Prepare reversing journal entries (optional).

Canadian Public Sector Financial Management

14

Section 2Section 2The Fundamental Accounting The Fundamental Accounting

EquationEquation

Canadian Public Sector Financial Management

15

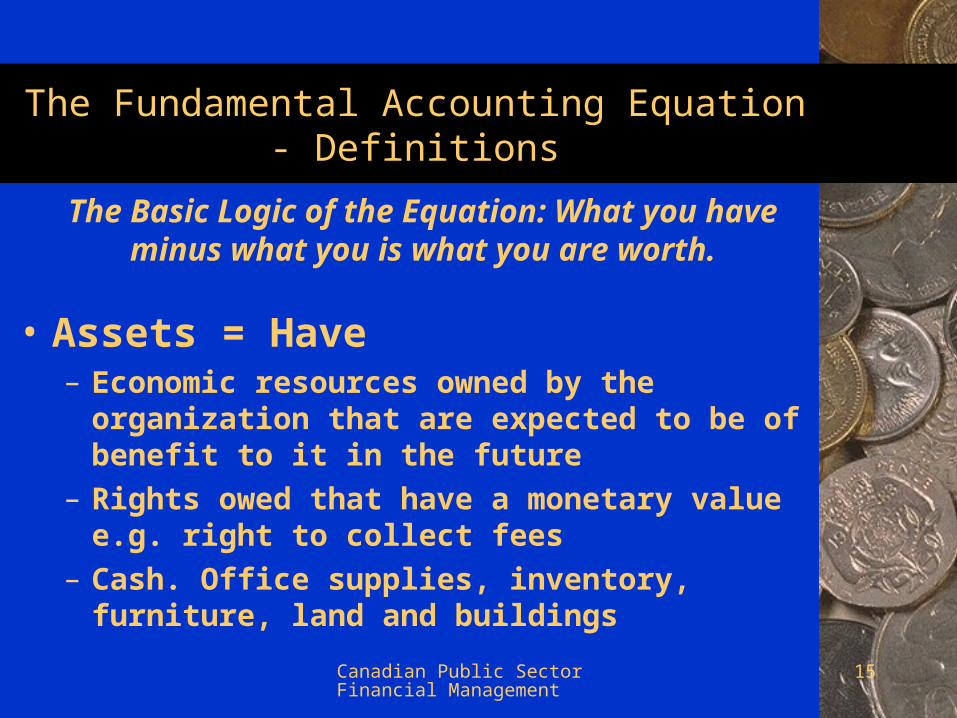

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

• Assets = Have– Economic resources owned by the

organization that are expected to be of benefit to it in the future

– Rights owed that have a monetary value e.g. right to collect fees

– Cash. Office supplies, inventory, furniture, land and buildings

The Basic Logic of the Equation: What you have minus what you is what you

are worth.

Canadian Public Sector Financial Management

16

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

Grouping of assets for presentation on Financial Reports:

Very liquid – cash and securities Assets for immediate use - inventory Productive Assets – plant and machinery Accounts receivable Fixed Assets – capital holdings Restricted Assets – non-mission

holdings or assets held subject to highly restrictive conditions.

Canadian Public Sector Financial Management

17

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

• Liabilities = Owe– Outsider claims which are economic

obligations payable to outsiders– Outside parties are called creditors

Canadian Public Sector Financial Management

18

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

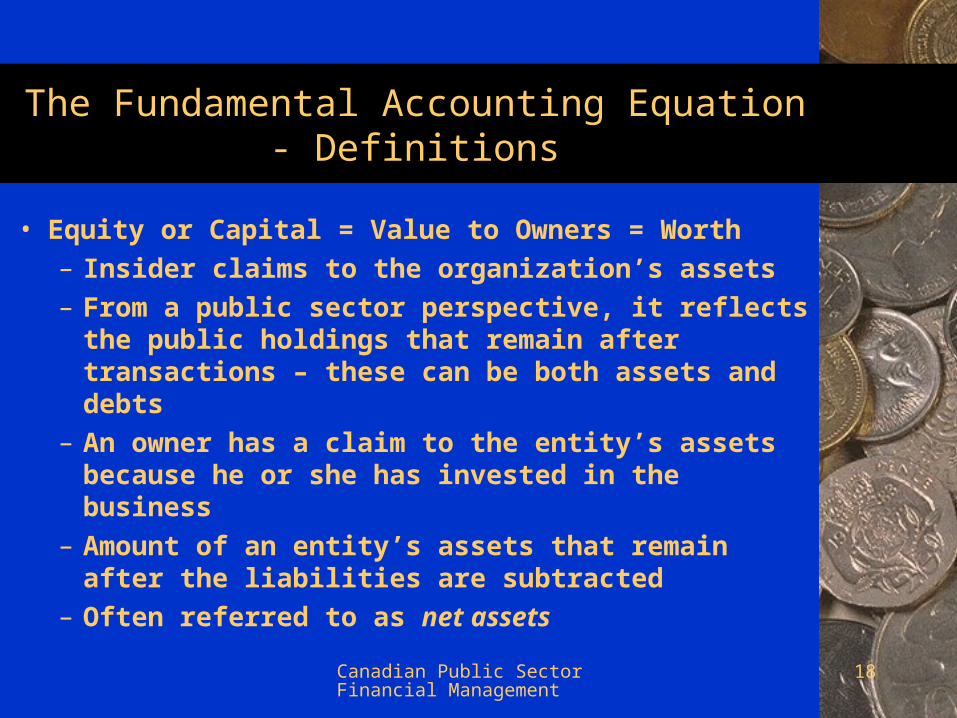

• Equity or Capital = Value to Owners = Worth– Insider claims to the organization’s assets– From a public sector perspective, it reflects

the public holdings that remain after transactions – these can be both assets and debts

– An owner has a claim to the entity’s assets because he or she has invested in the business

– Amount of an entity’s assets that remain after the liabilities are subtracted

– Often referred to as net assets

Canadian Public Sector Financial Management

19

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

• All receivables are assets• All payables are liabilities

Canadian Public Sector Financial Management

20

The Fundamental Accounting Equation - The Fundamental Accounting Equation - DefinitionsDefinitions

• Capital stock – amount invested in the corporation by its owners

• Retained Earnings – amount earned by income-producing activities and kept for use in the organization

• Net Income, Earnings, Profit or Loss – result of taking total revenues and total expenses into account over a specified period

Canadian Public Sector Financial Management

21

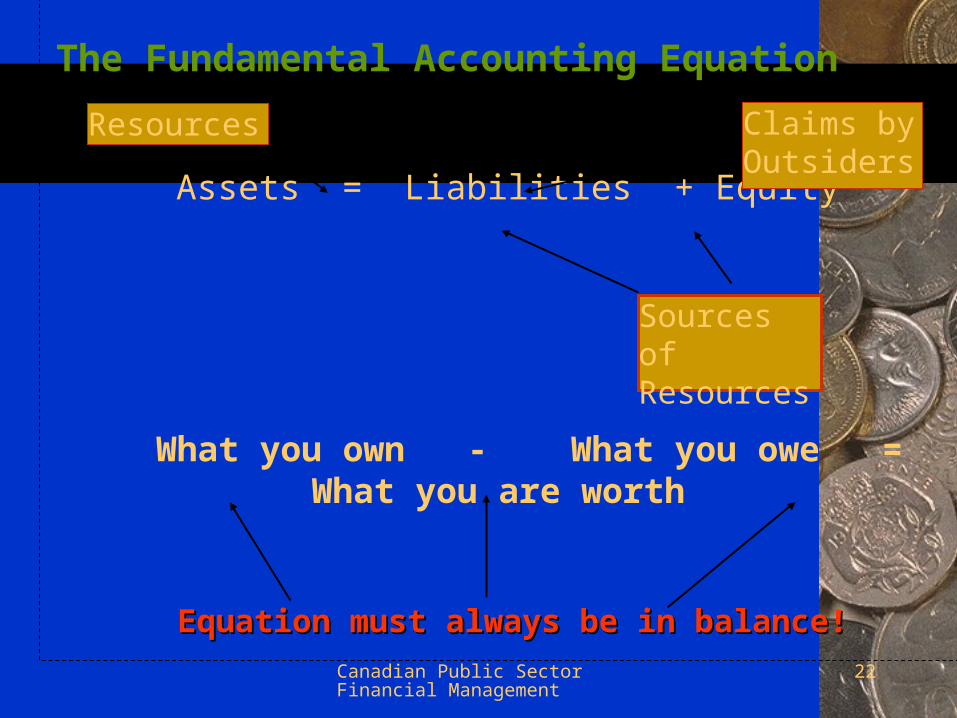

The Fundamental Accounting EquationThe Fundamental Accounting Equation

Assets = Liabilities + EquityAssets = Liabilities + Equity or Assets

- Liabilities = Equity

What you own minus what you owe is what you are worth.

Canadian Public Sector Financial Management

22

Assets = Liabilities + Equity

What you own - What you owe = What you are worth

The Fundamental Accounting Equation

Resources

Sources of Resources

Claims by Outsiders

Equation must always be in balance!Equation must always be in balance!

Canadian Public Sector Financial Management

23

Components of Retained Earnings: Flow Chart to Better Components of Retained Earnings: Flow Chart to Better Understand Financial StatementsUnderstand Financial Statements

Revenues of the Period

Beginning Balance of Retained Earnings

Expenses for the Period

Net Income (or Net Loss) for the Period

Dividends for the Period

Ending Balance of Retained Earnings

minus

plus or minus

minus equals

equals

Canadian Public Sector Financial Management

24

Section 3Section 3Recording Financial Recording Financial

InformationInformation

Canadian Public Sector Financial Management

25

Recording Financial InformationRecording Financial Information

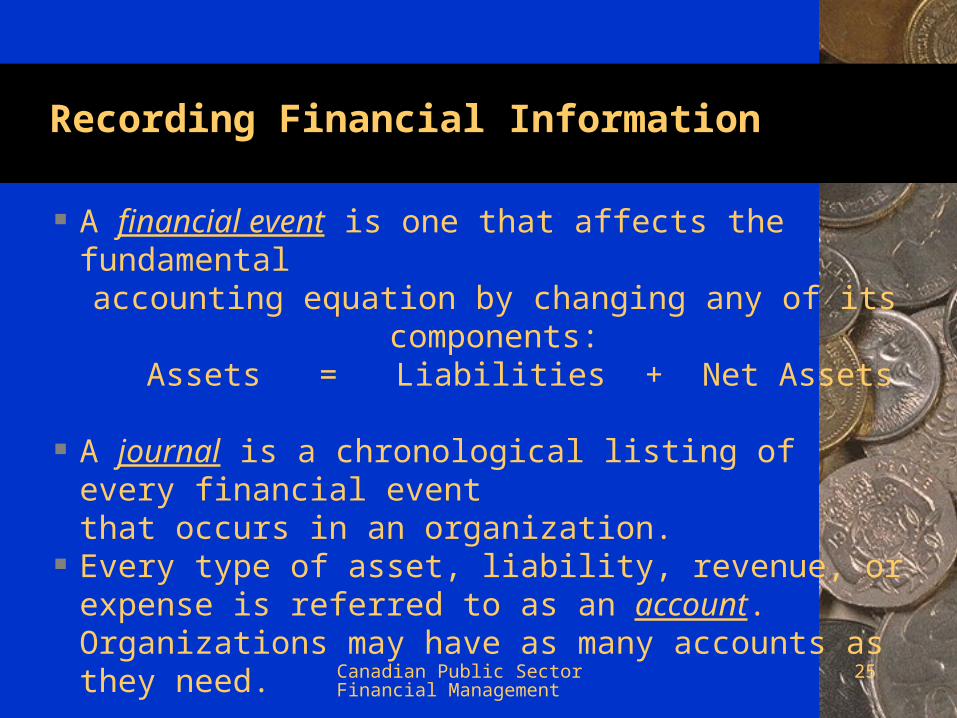

A financial event is one that affects the fundamental accounting equation by changing any of its components:

Assets = Liabilities + Net Assets

A journal is a chronological listing of every financial event that occurs in an organization.

Every type of asset, liability, revenue, or expense is referred to as an account. Organizations may have as many accounts as they need.

Canadian Public Sector Financial Management

26

Recording Financial Information Recording Financial Information – Debits and Credits– Debits and Credits

• Financial events are recorded as a series of debits and credits

• Increases in assets are recorded by debits and decreases are recorded by credits.

• Increases in liabilities and in owner's equity are recorded by credits and decreases are recorded by debits.

Canadian Public Sector Financial Management

27

Recording Financial Information Recording Financial Information – Debits and Credits– Debits and Credits

• Notice that the debit and credit rules are related to an account's location in the balance sheet. If the account appears on the left-hand side of the balance sheet (asset accounts), increases in the account balance are recorded by left-side entries (debits).

• If the account appears on the right-hand side of the balance sheet (liability and owner's equity accounts), increases are recorded by right-side entries (credits).

Canadian Public Sector Financial Management

28

Debits, Credits and the T-Account

Increases are recorded on one

side of the T-account, and decreases are

recorded on the other side.

Left or

Debit Side

Right or

Credit Side

Title of Account

Canadian Public Sector Financial Management

29

DebitDebit CreditCredit

A debit in an A debit in an increase in increase in an asset an asset item; a item; a decrease in a decrease in a claim or claim or expense itemexpense item

A credit is an A credit is an increase in a increase in a claim item; a claim item; a decrease in decrease in an asset or an asset or revenue revenue item.item.

Canadian Public Sector Financial Management

30

AA = LL + NANAASSETSASSETS

Debit for

Increase

Credit for

Decrease

NET ASSETSNET ASSETS

Debit for

Decrease

Credit for

Increase

LIABILITIESLIABILITIES

Debit for

Decrease

Credit for

Increase

Debits and credits affect accounts as follows:

Debit and Credit RulesDebit and Credit Rules

Canadian Public Sector Financial Management

31

A Sample Transaction Suppose HOS buys inventory for $2,000. We could just

add it to assets. But, that puts the Fundamental Equation out of balance.

Assets = Liabilities + Net Assets$2,000 = no change + no change

In a sense, we have not "paid" for the supplies. Suppose the seller sent HOS a bill. We would record the full transaction as:

Assets = Liabilities + Net Assets

Supplies Accounts Payable + $2,000 = + $2,000 + no change

To record a financial event, at least two elements of the fundamental equation must change!

Canadian Public Sector Financial Management

32

A One-Sided Change Example

Not every financial event (transaction) results in changes to both sides of the fundamental equation. Suppose HOS paid for the inventory in cash. Then the transaction would have been recorded as follows:

Assets = Liabilities + Net Assets Inventory Cash

+ $2,000 - $2,000 = no change + no change

The fundamental equation is still in balance. But, all of the changes occurred on the left side of the equation.

Canadian Public Sector Financial Management

33

Recording TransactionsRecording Transactions

The first step in recording a transaction is determining what has happened and what accounts will be impacted.

Suppose near the end of the year, HOS buys a one-year insurance policy for $100 and pays for the policy in cash. Two things have happened:

- Cash has gone down by $100.- HOS owns a new $100 asset called "prepaid

insurance."

Here's the way the transaction would be recorded: Assets = Liabilities + Net Assets

P/I Cash + $100 - $100 = no change + no change

Canadian Public Sector Financial Management

34

Another ExampleAnother Example

HOS mails a cheque to its bedpan supplier for $2,000 to pay part of the $7,000 it owed them at the start of the year. Two things have happened:

- Cash has gone down by $2,000.- HOS's accounts payable have decreased by $2,000.

Here's the way the transaction would be recorded:

Assets = Liabilities + Net Assets

Cash = Accounts Payable - $2,000 = - $2,000 + no change

Canadian Public Sector Financial Management

35

A Non Transaction

HOS signs a binding contract to buy an X-Ray machine that will cost $50,000.

This event will not give rise to a journal entry because it does not meet the rules for recognition.

- The value of the transaction is known.

- The timing of the transaction is known.

- But, HOS does not yet own the equipment. There has been no exchange. So HOS does not owe the money. No liability unless we owe the creditor.

Canadian Public Sector Financial Management

36

Section 4Section 4

The Long March Through The Long March Through Financial Statements Financial Statements beginning with the beginning with the

Statement of Financial Statement of Financial Position or Balance SheetPosition or Balance Sheet

Canadian Public Sector Financial Management

37

There are only

types of accounts in the accounting world

AssetsAssets

LiabilitiesLiabilities

EquityEquity

RevenueRevenue

ExpenseExpense

Cumulative Transactions

Current Period Transactions

Canadian Public Sector Financial Management

38

Balance SheetBalance Sheet

Income StatementIncome Statement

Statement of Cash FlowsStatement of Cash Flows

Statement of Shareholders’ EquityStatement of Shareholders’ Equity

Statement of Comprehensive IncomeStatement of Comprehensive Income

There are only

Formal Financial Statements

Canadian Public Sector Financial Management

39

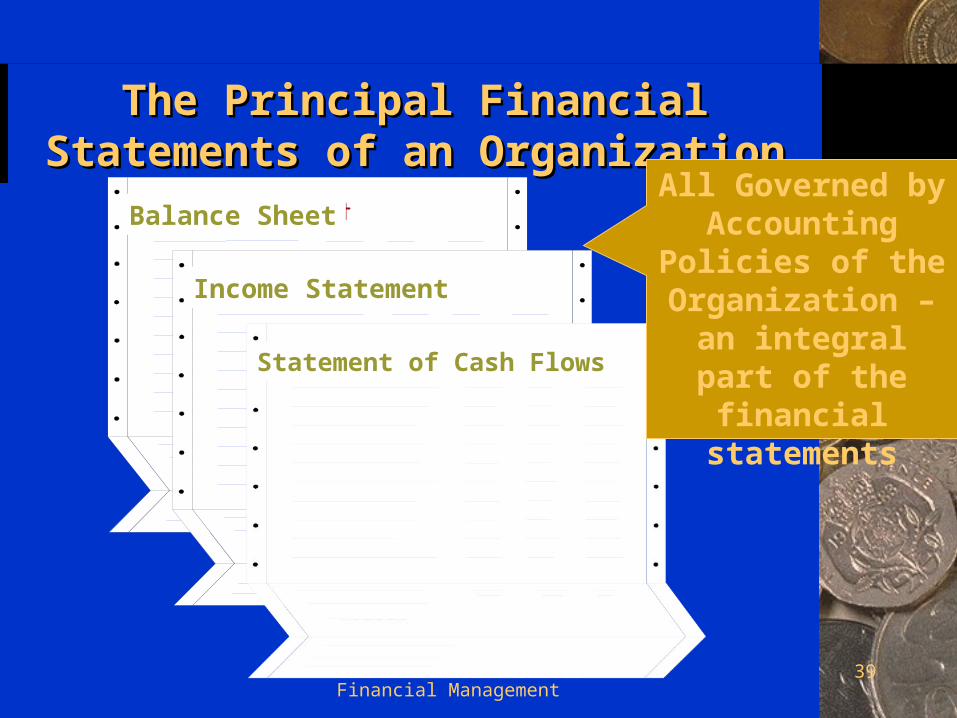

The Principal Financial The Principal Financial Statements of an OrganizationStatements of an Organization

Income Statement

Balance Sheet

Statement of Cash Flows

All Governed by Accounting

Policies of the Organization –

an integral part of the financial

statements

Canadian Public Sector Financial Management

40

Describes where the

organization stands at a

specific date.

Income Statement

Balance Sheet

Statement of Cash Flows

Canadian Public Sector Financial Management

41

Depicts the revenue and

expenses for a designated

period of time.

Income Statement

Balance Sheet

Statement of Cash Flows

Canadian Public Sector Financial Management

42

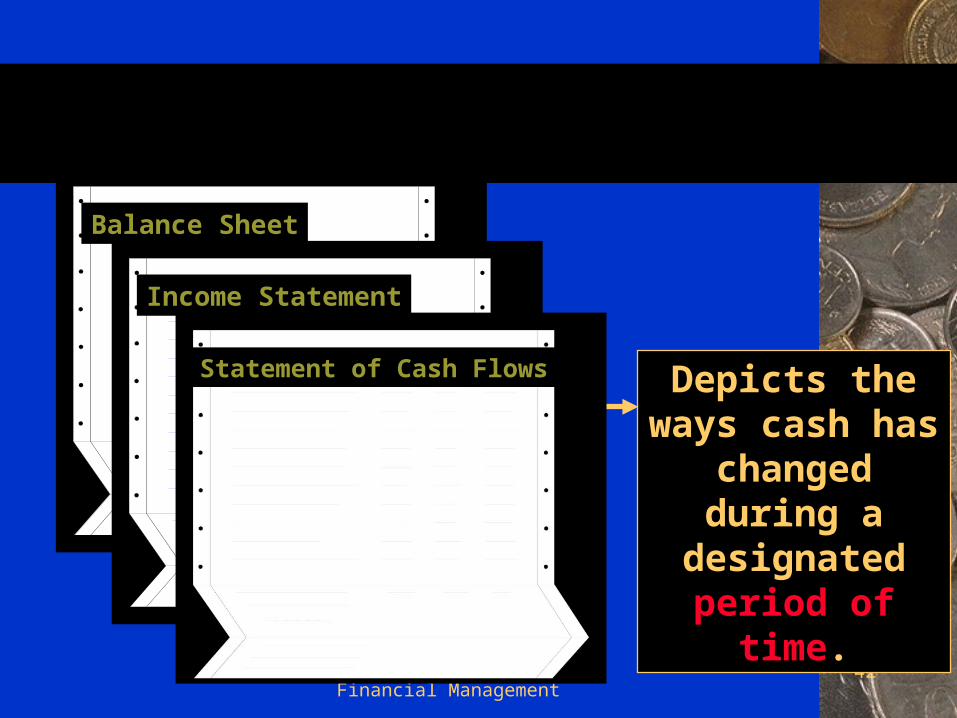

Depicts the ways cash has changed during

a designated period of time.

Income Statement

Balance Sheet

Statement of Cash Flows

Canadian Public Sector Financial Management

43

The Balance Sheet

Assets = Liabilities + Equity

The Income Statement

Revenues - Expenses = Net Income

Statement of Cash Flows

Reconciliation of the Change in Cash and Cash Equivalents

Statement of Shareholders’ Equity

Reconciliation of the Changes in the Owners’ Equity Accounts

Statement of Comprehensive Income

Reconciliation of Fair Value Changes and Adjustments

Operating Liabs

Short-term & Long-term

Debt

Paid-in Capital + Retained Earnings +

Accum. Other Comprehensive Income

Canadian Public Sector Financial Management

44

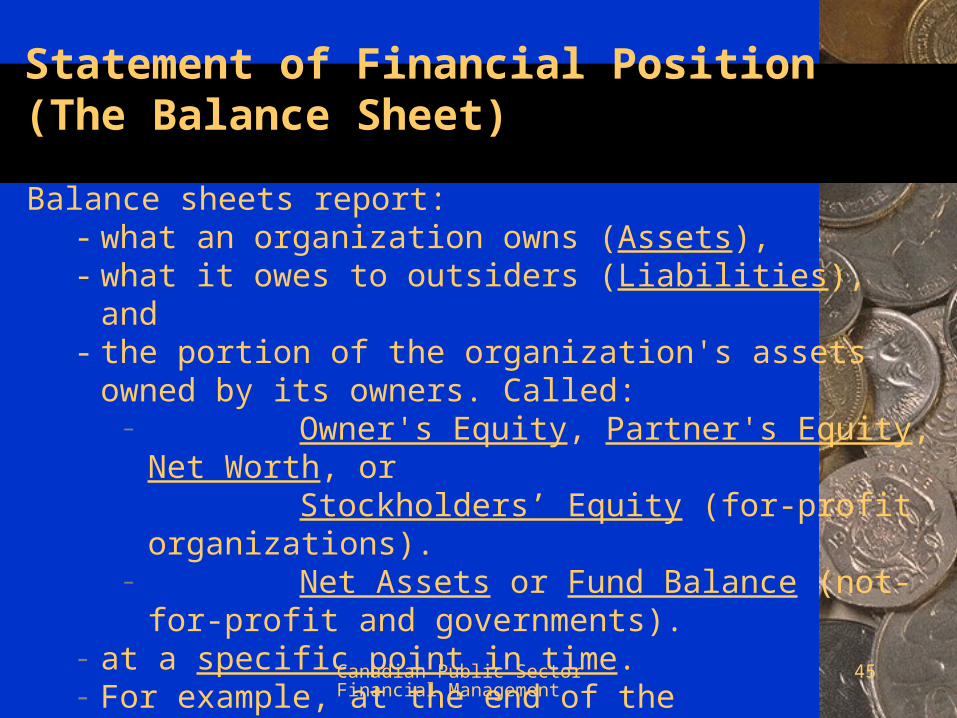

Statement of Financial Position or The Balance Sheet

The Balance Sheet reports:

Has Today = Owes today + Worth today

A Snapshot in timeA Snapshot in time

Canadian Public Sector Financial Management

45

Statement of Financial Position (The Balance Sheet)

Balance sheets report:- what an organization owns (Assets), - what it owes to outsiders (Liabilities), and - the portion of the organization's assets owned by

its owners. Called:– Owner's Equity, Partner's Equity, Net

Worth, or Stockholders’ Equity (for-profit

organizations).– Net Assets or Fund Balance (not-for-

profit and governments).- at a specific point in time. - For example, at the end of the organization's Fiscal

Year.

Canadian Public Sector Financial Management

46

Meals for the Homeless Balance Sheet

ASSETS LIABILITIES & NET ASSETS

Current Assets Liabilities

Cash $ 1,000 Current Liabilities

Marketable Securities 3,000 Wages Payable (Accrued Expenses)

$ 2,000

Accounts Receivable 55,000 Accounts Payable 2,000

Inventory 2,000 Notes Payable 6,000

Prepaid Expenses 1,000 Current Portion - Mortgage Payable

4,000

Total Current Assets $62,000 Total Current Liabilities

$ 14,000

Long-Term Assets Long-Term Liabilities

Fixed Assets Mortgage Payable $ 12,000

Property $ 40,000 Total Long-Term Liabilities

$ 12,000

Equipment, Net 35,000

Investments 8,000 TOTAL LIABILITIES $ 26,000

Total Long-Term Assets $ 83,000 NET ASSETS 119,000

TOTAL ASSETS $145,000 TOTAL LIABILITIES & NET ASSETS

$145,000

Canadian Public Sector Financial Management

47

Current and Long-Term AssetsCurrent and Long-Term Assets Assets on the balance sheet are divided into

current or short-term (those that are cash or cash-equivalents or are expected to become cash or will be used up within twelve months) and long-term (those that will not).

Short-Term or Current Assets are listed in order of declining liquidity and normally include:

- cash and cash equivalents,- marketable securities,- accounts receivable,- inventory, and- prepaid expenses (long-term prepaid

expenses are called Deferred Charges)

Canadian Public Sector Financial Management

48

Cash and Cash EquivalentsCash and Cash Equivalents

• The ultimate liquid assets• Includes all forms of

immediately available funds, including bank deposits

• Always denominated in Canadian funds even if foreign currencies being held

Canadian Public Sector Financial Management

49

Marketable SecuritiesMarketable Securities

Marketable securities include equity and debt instruments that can be bought and sold in public and private markets.

The values of marketable securities are reported by governments and not-for-profit organizations at fair market value.

If there is any dispute about fair market value, then cost is used to provide a value.

Canadian Public Sector Financial Management

50

Accounts ReceivableAccounts Receivable• When an organization produces a product,

service or obligation for another entity and it is transferred to the entity, the organization acquires the right to collect the money from that entity – this establishes a receivable account

• An accounts receivable entry is made when this occurs but before the entity pays for it

• Knowing what the outstanding accounts receivable are for the organization is an important indicator of its anticipated income, the degree to which is it efficiently collecting for its services and the degree to which it is carrying debt that it should collect

Canadian Public Sector Financial Management

51

InventoryInventory

• Inventory is both the finished products held by the organization for sale to an outside buyer and the products used to make the finished product

• Three kinds of inventory: – Raw material inventory– Work-in-progress inventory– Finished goods inventory

This becomes an accounts

receivable when it is sold and cash

when the customer pays for it.

Canadian Public Sector Financial Management

52

Pre-paid expensesPre-paid expenses

• Financial obligations that the organization has already paid for but not yet received

• Examples are: insurance, rent, deposits made with suppliers, salary advances

• They are current assets not because they can be turned into cash, but because the organization will have to use cash to pay for them in the near future and they are generally available for consumption within the twelve month period

Canadian Public Sector Financial Management

53

Current Asset Cycle – a way to Current Asset Cycle – a way to think of the relationship of think of the relationship of

these categoriesthese categories

CashCash

InventoryInventoryAccounts Accounts ReceivableReceivable

This is why they are called

“Working Assets”

Canadian Public Sector Financial Management

54

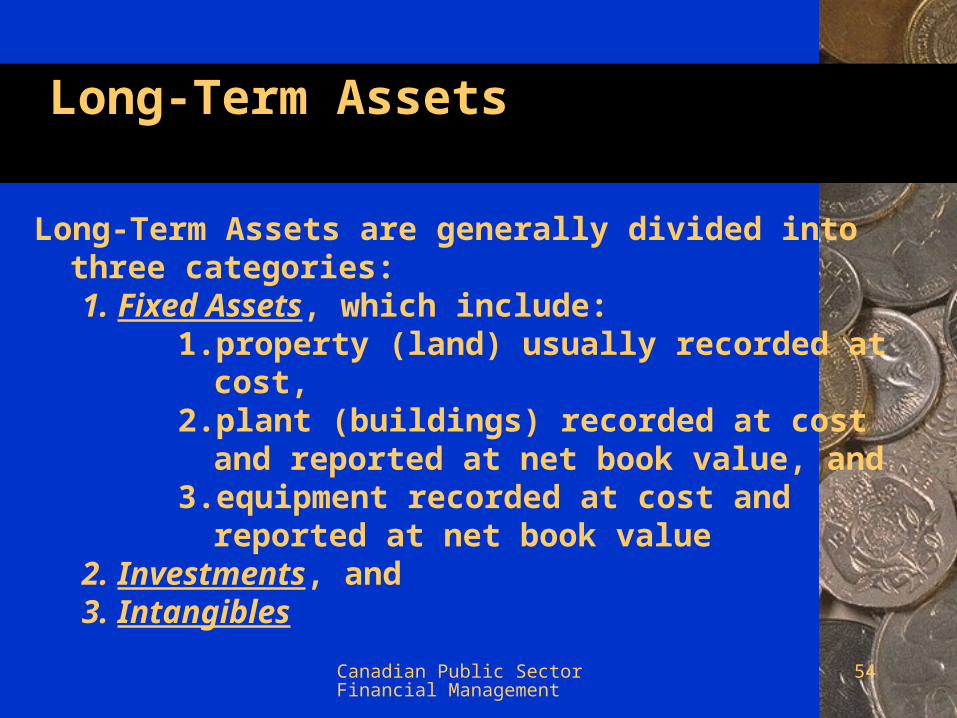

Long-Term AssetsLong-Term Assets

Long-Term Assets are generally divided into three categories:1.Fixed Assets, which include:

1.property (land) usually recorded at cost,

2.plant (buildings) recorded at cost and reported at net book value, and

3.equipment recorded at cost and reported at net book value

2.Investments, and3.Intangibles

Canadian Public Sector Financial Management

55

Fixed AssetsFixed Assets

• Productive assets not intended for sale.• They will be used over and over again to

produce value to the end product of the organizations

• Commonly include land, buildings, machinery, equipment, furniture, vehicles, etc.

• Normally reported on Balance Sheet in Net Fixed Asset format: blued at original cost minus an allowance for depreciation

Canadian Public Sector Financial Management

56

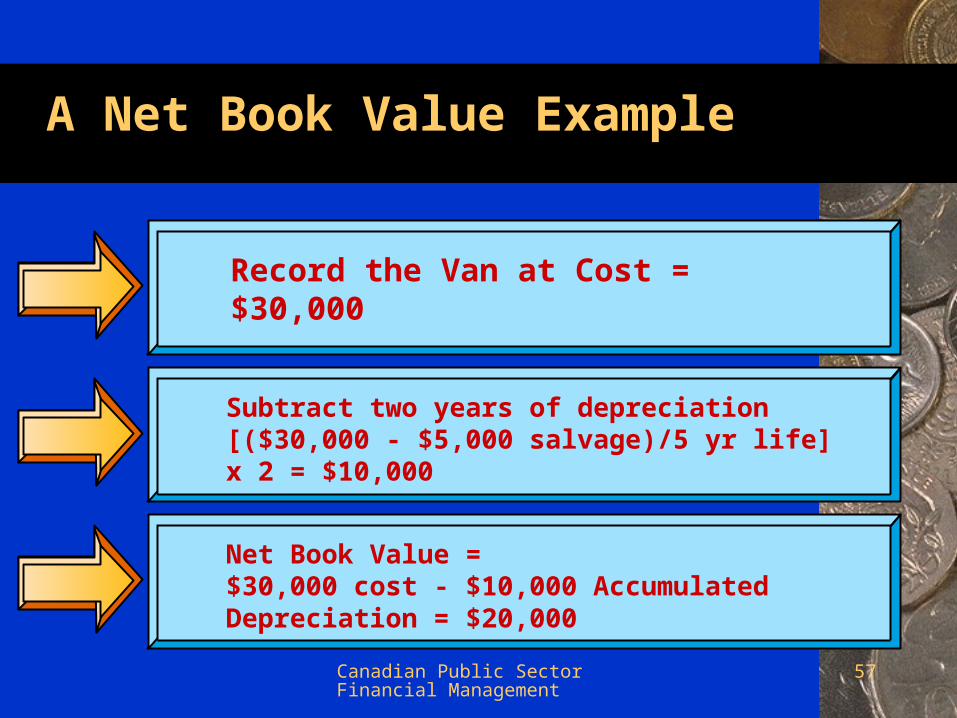

Net Fixed Asset DeterminationNet Fixed Asset Determination

Recorded at cost when acquired. Reported net of accumulated depreciation on the

balance sheet.

Suppose an organization buys a van for $30,000 and expects to use it for five years and sell it for $5,000. Assuming that the van will be used up evenly over the five years, how would its value appear on the balance sheet at the end of two years?

Canadian Public Sector Financial Management

57

A Net Book Value Example

Subtract two years of depreciation[($30,000 - $5,000 salvage)/5 yr life] x 2 = $10,000

Record the Van at Cost = $30,000

Net Book Value =$30,000 cost - $10,000 Accumulated Depreciation = $20,000

Canadian Public Sector Financial Management

58

Fixed Assets on the Balance SheetFixed Assets on the Balance SheetAll three values - cost, accumulated

depreciation, and net book value are shown. Museum A Museum B

Are these two museums really similar or different?

Net Fixed Assets orNet Book Value $1,000,000 $

1,000,000

PP&E at cost $40,000,000

$ 2,000,000

Accumulated Depreciation (39,000,000)

(1,000,000)

Net Book Value $ 1,000,000

$ 1,000,000

Canadian Public Sector Financial Management

59

Recognizing Asset TransactionsRecognizing Asset Transactions

Financial events are recorded at the time of Recognition

Asset transactions are recognized when:- they are owned by the organization,- they have a monetary value,- that monetary value can be

objectively determined.

Canadian Public Sector Financial Management

60

Recognizing Asset TransactionsRecognizing Asset Transactions

• Which of the following should be recognized as assets?– the amount due on a bill sent

to a client?– an overhead projector?– a fundraising mailing list

developed in an organization?

Canadian Public Sector Financial Management

61

Can Intangible Assets Appear on Can Intangible Assets Appear on a Balance Sheet?a Balance Sheet?

• What are intangible assets? An asset that has no substance or physical properties. Intangible assets include goodwill, patent rights, permits, copyrights and licenses.

• How are they assets? An intangible is any event that creates or modifies perceptions of the future behavior, value or relevance, of the organization but that are seen as usable assets that can be converted into (ultimately) cash.

Canadian Public Sector Financial Management

62

Can Intangible Assets Appear on Can Intangible Assets Appear on a Balance Sheet?a Balance Sheet?

• Intangibles, intangible assets, knowledge assets and intellectual capital are more or less synonyms. All are widely used – intangibles specifically in the accounting literature, knowledge assets by economists and intellectual capital predominantly in the management literature.

• Intangibles create future value. All intangibles are future-oriented. (Because of this they are ignored by traditional accounting systems – conservatism concept, materiality concept).

• Rule of quantification – slippery slope of quantification

• Good will and knowledge assets………

Canadian Public Sector Financial Management

63

Meals for the HomelessBalance Sheet

$145,000TOTAL LIABILITIES & NET ASSETS$145,000TOTAL ASSETS

119,000NET ASSETS$ 83,000 Total Long-Term Assets

$ 26,000TOTAL LIABILITIES 8,000Investments

35,000 Equipment, Net

$ 12,000 Total Long-Term Liabilities$ 40,000 Property

$ 12,000 Mortgage PayableFixed Assets

Long-Term LiabilitiesLong-Term Assets

$ 14,000 Total Current Liabilities$62,000 Total Current Assets

4,000 Current Portion – Mortgage 1,000 Prepaid Expenses

6,000 Notes Payable2,000 Inventory

2,000 Accounts Payable55,000 Accounts Receivable, Net

$ 2,000 Wages Payable (Accrued Expenses)3,000 Marketable Securities

Current Liabilities$ 1,000 Cash

LiabilitiesCurrent Assets

LIABILITIES & NET ASSETS ASSETS

Canadian Public Sector Financial Management

64

Liabilities

Liabilities are economic obligations of the organization such as money that it owes to lenders, suppliers, employees, etc.

Like assets, liabilities are categorized as short term and long term depending on when they are due for payment.

Can be categorized and groups for presentation on the balance sheets by:

To whom the debt is owned and Whether the debt is payable within the year

Canadian Public Sector Financial Management

65

Short-term or current Short-term or current liabilitiesliabilities

• Generally consist of:– specific "payables" which are typically

due within a specified period, usually the current fiscal year, e.g. wages or salary payable

– Generally have the following groupings: •Accounts payable to suppliers•Accrued expenses owed to employees and

other for services•Current debt owed to lenders•Taxes owed

Canadian Public Sector Financial Management

66

Accrued Expenses – Wage Accrued Expenses – Wage PayablePayable

• Monetary obligations similar to accounts payable

• Some flexibility on how these categories are used

• Generally accrued expenses involve financial obligation within the organization

• Therefore, this often records salary earned but not yet paid, interest due but not yet paid on bank debt, pension buy-outs, outstanding training costs

Canadian Public Sector Financial Management

67

Accounts PayableAccounts Payable

• Bills, generally to other organization for material sand equipment bought on credit, that must soon be paid

• When it receives materials, the organization can either pay for them immediately with case or wait and let what is owed become an account payable– notes payable – i.e., short-term loans,

and that portion of long-term debt which is due during the coming year.

Canadian Public Sector Financial Management

68

Notes Payable/Current Portion Notes Payable/Current Portion of Debtof Debt

• Short-term obligations that are payable in a year or less

• Brings in long-term obligations, but only the amount to be spent within the year to discharge it

Canadian Public Sector Financial Management

69

Long-Term LiabilitiesLong-Term Liabilities

Long-Term Liabilities included in Liabilities section is the current portion of the long-term liability that would have to be paid in the next 12 months:

- Long-Term Debt,– Capital Leases– Long-Term Unsecured Loans– Mortgages– Bonds Payable

- Pension Liabilities, and- Contingent Liabilities.

Canadian Public Sector Financial Management

70

Amortizing Long-Term DebtAmortizing Long-Term Debt Suppose that Meals buys a delivery van for $32,000.

It finances $25,000 of the purchase price with a five-year loan at 8% interest per annum.

The loan calls for annual payments (in arrears) of $6,261.41.

How much of each year's payment would be interest?

What would be the amounts shown on the Balance Sheet at the end of year 3?

Canadian Public Sector Financial Management

71

Amortizing Long-Term DebtAmortizing Long-Term DebtBeginning Total Interest Ending

Balance ($)

Payment ($)

Portion ($)

Principal ($)

Balance ($)

Year 1 25,000 6,261 2,000 4,261 20,739

Year 2 20,739 6,261 1,659 4,602 16,136

Year 3 16,136 6,261 1,291 4,971 11,166

Year 4 11,166 6,261 893 5,368 5,798

Year 5 5,798 6,261 464 5,798 0

End of Year 3 Bal. Sheet: Short-term Liability $5,368; Long-term Liability $5,798.

How was the $6,261.41 calculated?

Canadian Public Sector Financial Management

72

Liability Recognition

Liabilities are recognized when: they are legally owed, have to be paid, and the amount to be paid can be objectively

measured. Which of the following should be recognized as

a liability? a bill received from a vendor? wages that are due to a worker? a $5 million lawsuit filed against an

organization?

Canadian Public Sector Financial Management

73

Net Asset CategoriesNet Asset Categories The amount of total assets minus total liabilities equals

equity. Because equity is equal to the net difference between assets and liabilities, it is also called net assets.

Both ‘net worth’ and ‘book value’ hold the same meaning as ‘net assets’ and ‘shareholder value’

The net worth of an organization represents the sum of the organization's earnings from inception plus any paid-in capital (in for-profits) less any payments that have been made to the organization's owners. Also call Capital Stock

Retained earnings: money that is held after all liabilities have been discharged and not used for assets – can also be negative value, i.e. debt

Canadian Public Sector Financial Management

74

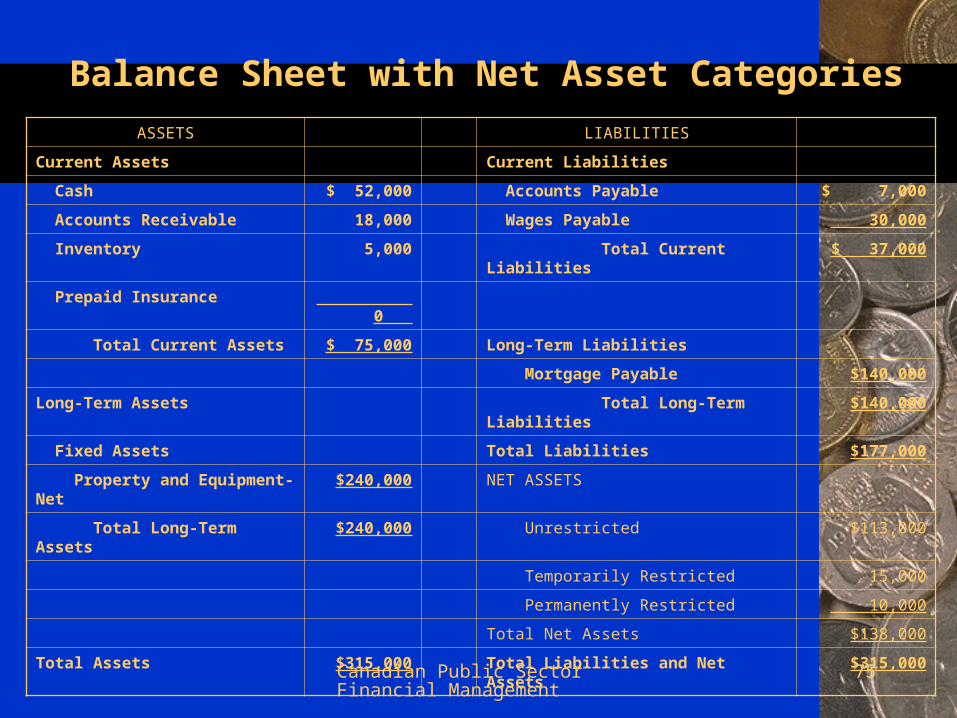

Net Asset CategoriesNet Asset Categories

• In not-for-profit organizations, net worth is called "Net Assets" and is broken down into three categories.– Unrestricted Net Assets, which have

not been restricted by donors (also cumulative profits appear here).

– Temporarily Restricted Net Assets, the use of which has been restricted by donors.

– Permanently Restricted Net Assets, which are restricted in perpetuity.

Canadian Public Sector Financial Management

75

Balance Sheet with Net Asset CategoriesASSETS LIABILITIES

Current Assets Current Liabilities

Cash $ 52,000 Accounts Payable $ 7,000

Accounts Receivable 18,000 Wages Payable 30,000

Inventory 5,000 Total Current Liabilities $ 37,000

Prepaid Insurance 0

Total Current Assets $ 75,000 Long-Term Liabilities

Mortgage Payable $140,000

Long-Term Assets Total Long-Term Liabilities

$140,000

Fixed Assets Total Liabilities $177,000

Property and Equipment-Net

$240,000 NET ASSETS

Total Long-Term Assets $240,000 Unrestricted $113,000

Temporarily Restricted 15,000

Permanently Restricted 10,000

Total Net Assets $138,000

Total Assets $315,000 Total Liabilities and Net Assets $315,000

Canadian Public Sector Financial Management

76

Section 5Section 5

Generating a Balance Generating a Balance SheetSheet

Canadian Public Sector Financial Management

77

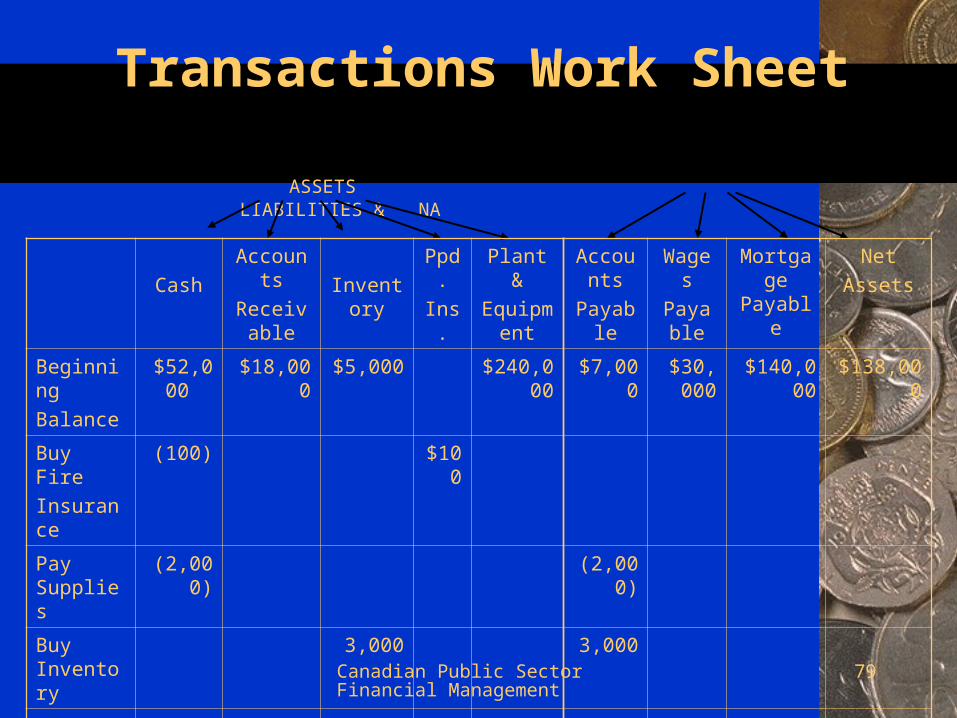

Generating a Balance SheetGenerating a Balance Sheet

Generating a balance sheet involves:

Beginning with the starting balance sheet,Recording all of the transactions for the period, Adding the impact of the transactions to the

starting balance sheet,Formatting the resulting balance sheet

accounts into the balance sheet reporting format.

Canadian Public Sector Financial Management

78

The Starting Balance Sheet

ASSETS LIABILITIES AND NET ASSETS

Current Assets Current Liabilities

Cash $ 52,000

Accounts Payable $ 7,000

Accounts Receivable 18,000 Wages Payable 30,000

Inventory 5,000 Total Current Liabilities $ 37,000

Prepaid Insurance 0

Total Current Assets $ 75,000

Long-Term Liabilities

Mortgage Payable $140,000

Long-Term Assets Total Long-Term Liabilities

$140,000

Fixed Assets Total Liabilities $177,000

Property and Equipment, Net

$240,000

Total Long-Term Assets

$240,000

Total Net Assets 138,000

Total Assets $315,000

Total Liabilities and Net Assets

$315,000

Canadian Public Sector Financial Management

79

Transactions Work Sheet

ASSETS LIABILITIES & NA

CashAccoun

tsReceivable

Inventory

Ppd.

Ins.

Plant &

Equipment

Accounts

Payable

Wages

Payable

Mortgage

Payable

NetAssets

BeginningBalance

$52,000

$18,000

$5,000 $240,000

$7,000

$30,000

$140,000

$138,000

Buy FireInsurance

(100) $100

Pay Supplies

(2,000)

(2,000)

Buy Inventory

3,000 3,000

Receive Payment (12,00

0)(12,000

)

Ending Balance

$61,900

$ 6,000

$8,000 $100

$240,000

$8,000

$30,000

$140,000

$138,000

Canadian Public Sector Financial Management

80

The Ending Balance SheetASSETS LIABILITIES

Current Assets Current Liabilities

Cash $ 61,900

Accounts Payable $ 8,000

Accounts Receivable 6,000 Wages Payable 30,000

Inventory 8,000 Total Current Liabilities

$ 38,000

Prepaid Insurance 100

Total Current Assets

$ 76,000

Long-Term Liabilities

Mortgage Payable $140,000

Long-Term Assets Total Long-Term Liabilities

$140,000

Fixed Assets Total Liabilities $178,000

Property and Equipment, Net

$240,000

Total Long-Term Assets

$240,000

Total Net Assets 138,000

Total Assets $316,000

Total Liabilities and Net Assets

$316,000

Canadian Public Sector Financial Management

81

Section 6Section 6The Income Statement or The Income Statement or Statement of Operations Statement of Operations ((Also called Activity Statement, Also called Activity Statement,

Statement of Revenues and Expenses, or Statement of Revenues and Expenses, or Profit and Loss (P&L) Statement)Profit and Loss (P&L) Statement)

Canadian Public Sector Financial Management

82

What is an Income Statement?What is an Income Statement?

• Reports on cash movements in the organization

• Statement of cash movement for a specific period of time, usually a quarter, month or year – a specified period of time.

• Unlike a Balance Sheet which is a snapshot of a specific day

Canadian Public Sector Financial Management

83

What is an Income Statement?What is an Income Statement?

• Linkage is that the net income for this year as shown on an Income Statement is added to Retained Earnings on the Balance Sheet to show increase/decrease in Net Assets as a result of this year’s income

• Therefore, the Income Statement shows for a period all the transactions taken by the organization to either increase assets or decrease liabilities on the Balance Sheet

• Key tool in financial control and budgetary management: used to inform of current financial situation, identify surplus/deficits, measure performance

Canadian Public Sector Financial Management

84

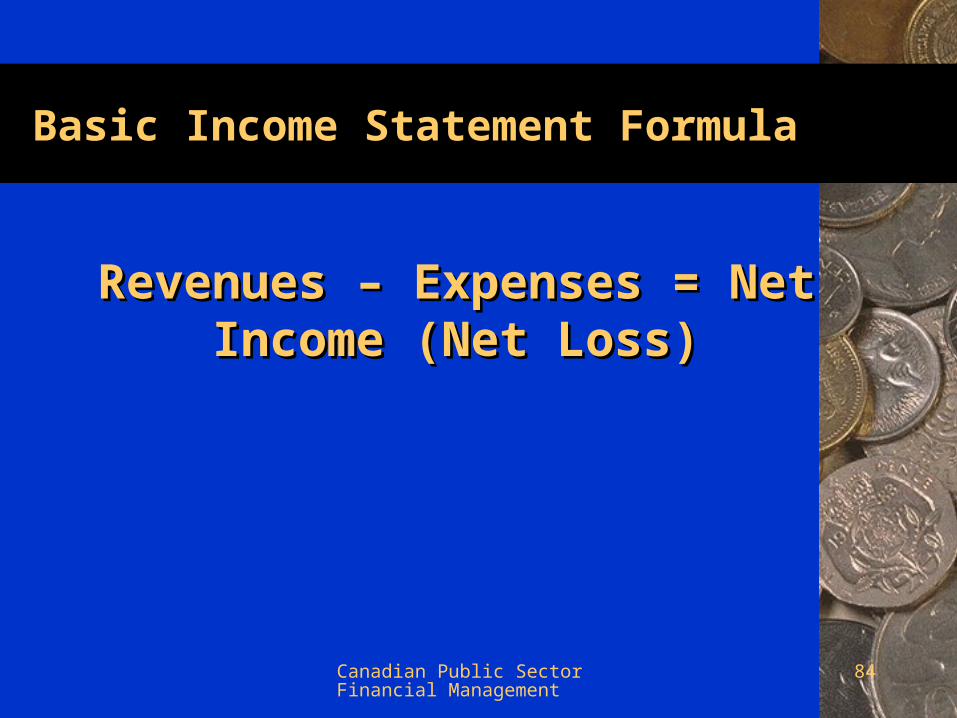

Basic Income Statement Basic Income Statement FormulaFormula

Revenues – Expenses = Net Income Revenues – Expenses = Net Income (Net Loss)(Net Loss)

Canadian Public Sector Financial Management

85

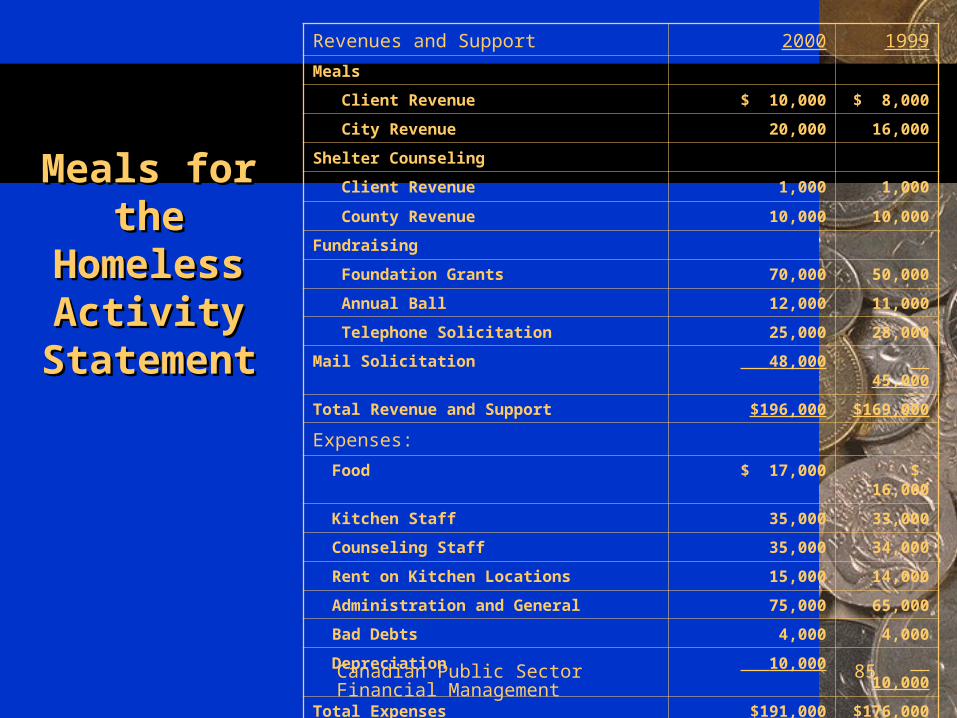

Meals for Meals for the the

HomelessHomelessActivity Activity

StatementStatement

Revenues and Support 2000 1999

Meals

Client Revenue $ 10,000 $ 8,000

City Revenue 20,000 16,000

Shelter Counseling

Client Revenue 1,000 1,000

County Revenue 10,000 10,000

Fundraising

Foundation Grants 70,000 50,000

Annual Ball 12,000 11,000

Telephone Solicitation 25,000 28,000

Mail Solicitation 48,000 45,000

Total Revenue and Support $196,000 $169,000

Expenses:

Food $ 17,000 $ 16,000

Kitchen Staff 35,000 33,000

Counseling Staff 35,000 34,000

Rent on Kitchen Locations 15,000 14,000

Administration and General 75,000 65,000

Bad Debts 4,000 4,000

Depreciation 10,000 10,000

Total Expenses $191,000 $176,000

Change in Net Assets $ 5,000 $ (7,000)

Canadian Public Sector Financial Management

86

The Income Statement: Revenues The Income Statement: Revenues and Supportand Support

– represent inflows that the organization has received or is entitled to receive.

– result in an inflow of Assets to the organization and an increase in Net Assets.

Canadian Public Sector Financial Management

87

The Income Statement: The Income Statement: Revenues and SupportRevenues and Support

• Revenues are generally the result of an exchange for goods and services that the organization has provided or budgetary decisions that a government makes

• Support is the result of gifts, grants, and other contributions to the organization.

• Category of other income from fees or non-tax income streams

Canadian Public Sector Financial Management

88

Expenses and Net Income

Expenses represent the recognition of the use of an asset to generate revenue and support or otherwise carry on the operations of the entity which result in an outflow of assets and a decrease in Net Assets.

Net Income is the difference between revenues and support and expenses.

Canadian Public Sector Financial Management

89

Expenses and Net IncomeExpenses and Net Income

• Profits are an excess of revenues over expenses. Also called a surplus or increase in net assets.

• Losses are an excess of expenses over revenues. Also called a deficit or decrease in net assets.

Canadian Public Sector Financial Management

90

Cost vs. ExpenseCost vs. Expense

• Cost describes how money is spent to build inventories or add to plant or capacity

• Expense is any other operating expenditure.

• Note: An expenditure can be either a cost or an expense. Expenditure simply means the use of cash to pay for an item purchased.

Canadian Public Sector Financial Management

91

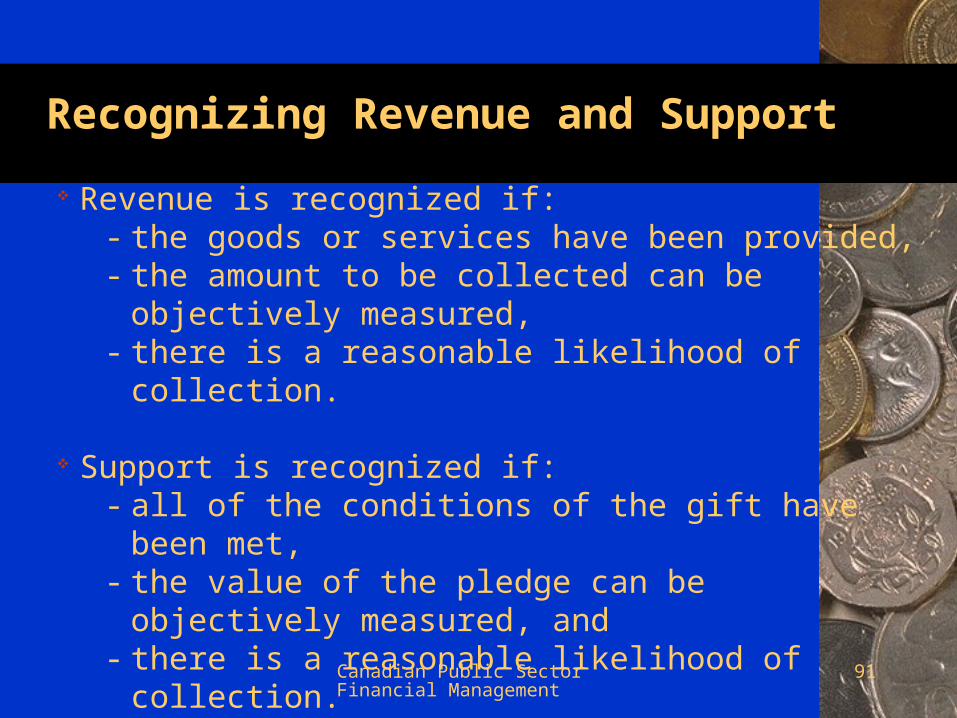

Recognizing Revenue and SupportRecognizing Revenue and Support

Revenue is recognized if:- the goods or services have been provided,- the amount to be collected can be objectively

measured, - there is a reasonable likelihood of collection.

Support is recognized if:- all of the conditions of the gift have been met,- the value of the pledge can be objectively

measured, and- there is a reasonable likelihood of collection.

Canadian Public Sector Financial Management

92

Recognizing ExpensesRecognizing Expenses

Expense Recognition depends on the type of expense:

- Product costs are those directly connected to providing goods and services. They are recognized based on the matching principle, which holds that expenses should be recorded in the same period as the revenue they were used to generate.

- Period Costs, like rent, are those related to the passage of time. They are recognized in the time period they are incurred.

Canadian Public Sector Financial Management

93

Expired and Unexpired Costs

Suppose Meals bought 100 canned hams at a cost of $1,000 in March. At acquisition, Meals would recognize the hams as an asset (Inventory). They are also an unexpired cost.

If they paid for the hams in cash, Cash would go down by $1,000. Otherwise Accounts Payable increases $1,000.

In May, Meals used 50 of the hams to produce meals. - At use, the hams become an expense

(expired cost) of $500 (50 hams * $10 per ham = $500), and the value of the asset (Inventory) is reduced by $500.

This is a Product Cost. The inventory becomes an expense as used to provide service.

Canadian Public Sector Financial Management

94

Inventory ExpenseInventory Expense

Inventory expenses represent the cost of using supplies to operate an organization. Inventory expense and the ending inventory value are calculated using the following relationship:

Beginning Inventory + Purchases - Consumption = Ending

5 + 10 - 13 = 2

Canadian Public Sector Financial Management

95

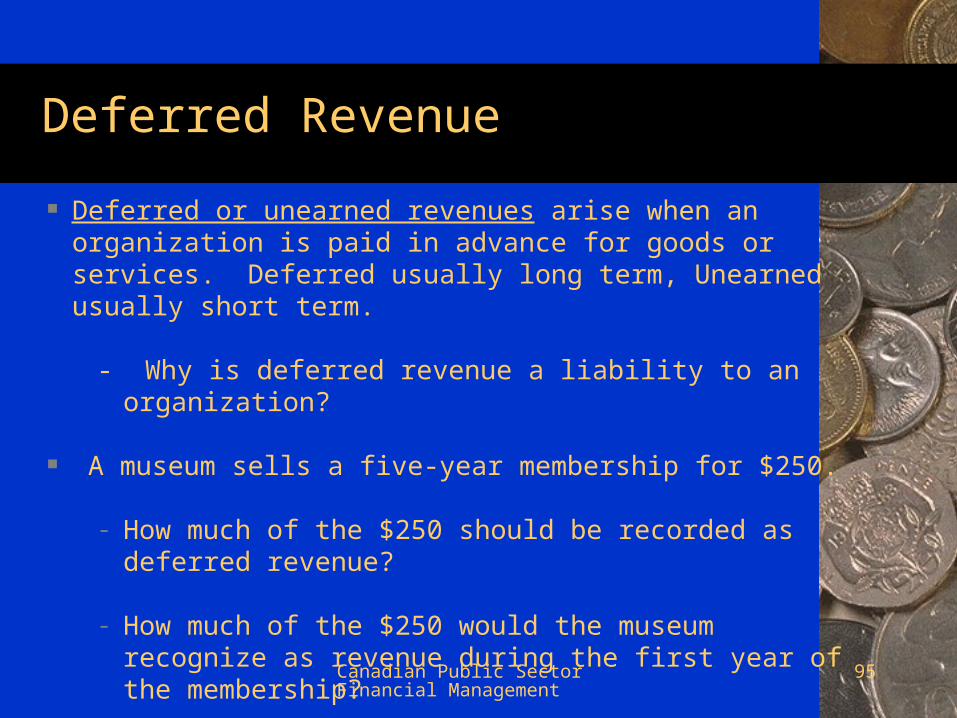

Deferred Revenue

Deferred or unearned revenues arise when an organization is paid in advance for goods or services. Deferred usually long term, Unearned usually short term.

- Why is deferred revenue a liability to an organization?

A museum sells a five-year membership for $250.

- How much of the $250 should be recorded as deferred revenue?

- How much of the $250 would the museum recognize as revenue during the first year of the membership?

Canadian Public Sector Financial Management

96

Where the Income Statement and Balance Sheet Meet

Event Statement Impact

Note

RevenueRecognized

You provide aservice and earn revenue

AR or Cash up B/SRevenue up I/S

AR is a “holding area”for unpaid bills that you have sent out

No impacton revenue

Someone paysa bill you sent

AR down B/SCash up B/S

No impacton expenses

When you buysomething

AP up or

Cash down B/SInventory up B/S

AP is where you keeptrack of what you owe to others

ExpenseRecognized

When you use something

Asset down orLiability up B/SExpense up I/S

Canadian Public Sector Financial Management

97

Reflecting the Change in Net Assets on the Balance Sheet

Net income is reported as a change in net assets on the balance sheet.

Activity Statement

Balance Sheet

Total Revenue and Support

$81,000

Total Expenses - 80,050

Increase in Net Assets $ 950

Unrestricted

Temp. Rest. Perm. Rest.

Beginning Balances

$113,000 $15,000 $10,000

Increase in Net Assets

950

Ending Balances $113,950 $15,000 $10,000

Canadian Public Sector Financial Management

98

Section 7Section 7Cash Flow StatementsCash Flow Statements

Canadian Public Sector Financial Management

99

The Cash Flow StatementThe Cash Flow Statement

• The Cash Flow Statement shows:Cash on hand at the start of the

periodCash received in the periodCash spent in the periodCash on hand at the end of the

period

Canadian Public Sector Financial Management

100

•Change in Cash & Cash Equivalents

•Net Income Line

•Cash Generated by Operating Activities

•Cash Generated by Investing Activities

•Cash Generated by Financing Activities

There are only

Sections on the Cash Flow Statement

Canadian Public Sector Financial Management

101

The Cash Flow StatementThe Cash Flow Statement

– Why does an organization need both an operating statement and a cash flow statement?

• Cash flow statements provide vital budget to plan information in purely cash terms

• Cash flow information gives you information on your budgetary flexibilities and also on the actual cash performance versus the predicted one for cash/budget management purposes

– Why is it important to know the sources and uses of cash flow?

• This will depend on the nature of the organization – less so with single source (budget funds) of cash

Canadian Public Sector Financial Management

102

The Cash Flow StatementThe Cash Flow Statement

– Isn't knowing if cash increased or decreased enough? •No, source and availability are

important

Canadian Public Sector Financial Management

103

The Cash Flow Statement

Start with Change in Net Assets [i.e., net income] as a first approximation of cash flow, and then make adjustments. Why isn't this good enough? Why are the other adjustments needed?

Assets = Liabilities + Net Assets Assets = Liabilities + Net Assets

Cash + Other Assets = Liabilities + Net Assets Cash = Liabilities + Net Assets Other Assets

The Cash Flow Statement is equal to the change in the other balance sheet accounts.

Canadian Public Sector Financial Management

104

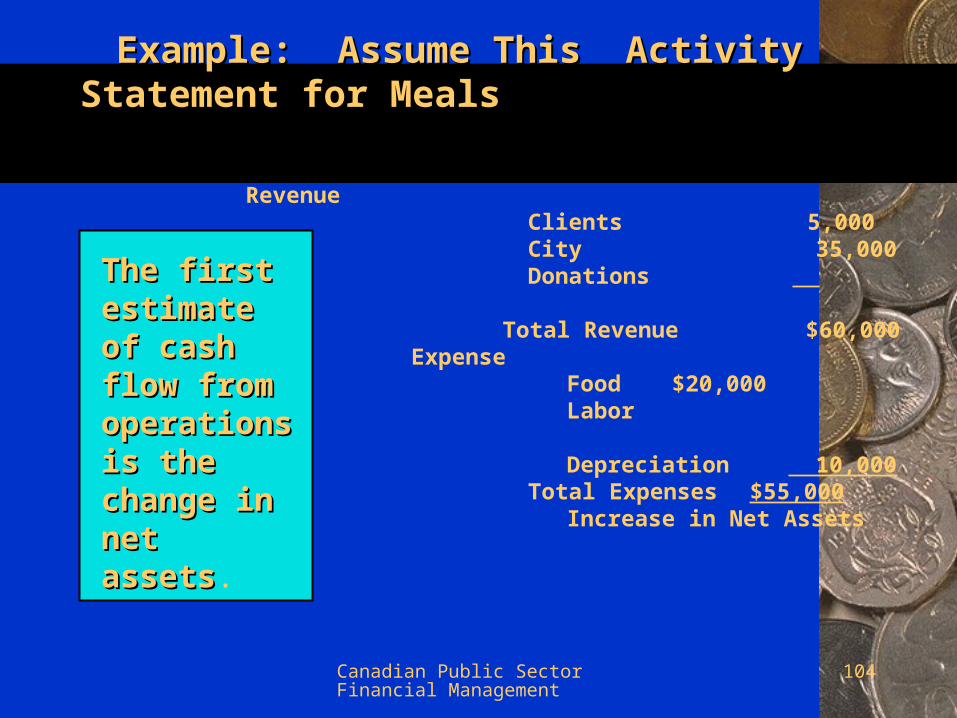

Example: Assume This Activity Example: Assume This Activity Statement for MealsStatement for Meals

Revenue Clients 5,000 City 35,000 Donations 20,000 Total Revenue $60,000 Expense Food $20,000 Labor 25,000 Depreciation 10,000 Total Expenses $55,000 Increase in Net Assets

$ 5,000

The first The first estimate estimate of cash of cash flow from flow from operations operations is the is the change inchange innet assetsnet assets.

Canadian Public Sector Financial Management

105

The Increase in Net Assets is an approximation of cash flow. Adjustments are needed to arrive at true cash flow.

The first adjustment is for "Expenses not requiring cash" such as depreciation or amortization. Why doesn't depreciation require cash?

The remainder of the adjustments to operating cash flow are for changes in balance sheet accounts related to operations.

Adjusting the Increase in Net Assets to Cash Flow

Canadian Public Sector Financial Management

106

Adjusting the Increase in Net Assets Adjusting the Increase in Net Assets to Cash Flowto Cash Flow

Why subtract an increase in Accounts Receivable? The increase in net assets includes all revenue.

What if A/R increases? Was all revenue collected in cash? If not, then how would you have to adjust the Change in Net Assets to make it a closer measure of cash flow?

Canadian Public Sector Financial Management

107

The Statement of Cash Flows

Cash Flows from Operating Activities

2000

1999

Increase in Net Assets $ 5,000

$ (7,000)

Add Expenses Not Requiring Cash:

Depreciation 10,000

10,000

Other Adjustments:

Add Decrease in Inventory 2,000

2,000

Add Increase in Notes Payable 1,000

3,000

Subtract Increase in Receivables

(17,000) (12,000)

Subtract Decrease in Wages Payable

(1,000) 0

Subtract Decrease in Accounts Payable

(1,000) (2,000)

Subtract Increase in Prepaid Expenses

(1,000) 0

Net Cash Used for Operating Activities

$ (2,000) $ (6,000)

Canadian Public Sector Financial Management

108

2000 1999

Cash Flows from Investing Activities

Sale Stock Investments $ 4,000

$ 5,000

Purchase of Delivery Van (32,000)

Net Cash from Investing Activities

$ 4,000

$ (27,000)

Cash Flows from Financing Activities

Increase in Mortgages $ 25,000

Repayments of Mortgages $ (5,000) (4,000)

Net Cash from Financing Activities

$ (5,000) $ 21,000

Net Increase/(Decrease) in Cash $ (3,000) $ (12,000)

Cash, Beginning of Year 5,000

17,000

Cash, End of Year $ 2,000

$ 5,000

The Statement of Cash Flows, continued

Canadian Public Sector Financial Management

109

The Cash Flow StatementThe Cash Flow Statement

Cash flows relating to investment and financing activities are listed separately.

The method shown was the indirect method. The direct method is easier, just requiring a listing of all cash inflows and outflows (could be taken from transactions worksheet cash column). But indirect method provides more information.

Canadian Public Sector Financial Management

110

How to Cook the BooksHow to Cook the Books

• There is fraud and there is distortion possible in all this. So too is creative accounting.

• So much relies upon issues such as recognition rules, when expenses and expenditures are actually recognized

Canadian Public Sector Financial Management

111

How to Cook the BooksHow to Cook the Books

• Some common means to cook the books:

• Padding revenue expectations• Accelerating and decelerating expenditures

flows• Improperly lowering costs• Assuming ‘efficiencies’ planned will be

achieved• Not accruing liabilities• Flipping lower valued assets for higher ones• Shifting expenses between periods and

years• Accelerating depreciation rates

Canadian Public Sector Financial Management

112

Are we having fun

yet?