Embed Size (px)

Citation preview

i

FINANCIAL STATEMENTS ANALYSIS AND FINANCIAL

PERFORMANCE FOR BANKS LISTED ON RWANDA STOCK OF

EXCHANGE: A COMPARATIVE STUDY FOR BANK OF KIGALI

PRE-POST LISTING

HIGANIRO MAJOGI INNOCENT

MBA/78611/14

A Research Project Submitted in Partial Fulfilment for the Award of

the Degree of Master of Business Administration (Accounting &Finance

option) of Mount Kenya University

MAY 2017

ii

DECLARATION

This research proposal is my original work and has not been presented to any other

Institution. No part of this research proposal should be reproduced without the authors‟

consent or that of Mount Kenya University.

Students Name: Higaniro Majogi Innocent

Reg: MBA/78611/14

Sign ____________________ Date _____________

This research has been submitted with my approval as The Mount. Kenya University

Supervisor.

Name: Dr. Rusibana Claude, PhD

Sign ____________________ Date _____________

iii

DEDICATION

To my beloved spouse Consolatrice Murekatete, my daughters and sons Sylvie Teta,

Trebor Shema, Theillah Shima, Doxa Touvia, and my loved late son Tracy Shami.

I deeply express my grateful thanks to my parents, Majogi Ignace and Mukasarasi

Madalina and Mukamurigo Budensiana my mother in law.

iv

ACKNOWLEDGEMENT

My gratitude to Almighty God, for the gift of life, love and blessings, perseverance to

perform this work far way.

I hereby acknowledge the Government of Rwanda, Mount Kenya University which have

ensured our Education improvement. I am grateful to the lecturers who provided their

knowledge to me during my study.

I am very thankful to Dr. Rusibana Claude, my supervisor during this work; his

availability, simplicity, and especially his scientific rigor have been of great importance

for this work to be completed.

My special thanks to my beloved spouse and children, relatives and friends for both

spiritual and material support, encouragement during my stay at Mount Kenya University.

v

ABSTRACT

Banks and other financial institutions are a unique set of business firms whose assets and

liabilities, regulatory restrictions, economic functions and operation make them an

important subject of research. Bank Performance monitoring, analysis and control deserve

special attention in respect to their operation and performance results from the viewpoint

of different stakeholders, such as investors/owners, regulators, customers, and

management.In today‟s financial world, financial performance is a mundane amongst the

perspective of various stakeholders, be it in the management, lenders, owners and

investors‟ perspective. And this is out of analysis of financial statements. Financial

performance is crucial for taking financial decisions related to planning and control.

Hence, it forms the basis as one of the paramount importance for taking financial

decisions effectively. The aim of this study is to analyse and compare the pre and post

listing impact on financial performance of Bank of Kigali; the study has covered 2008 to

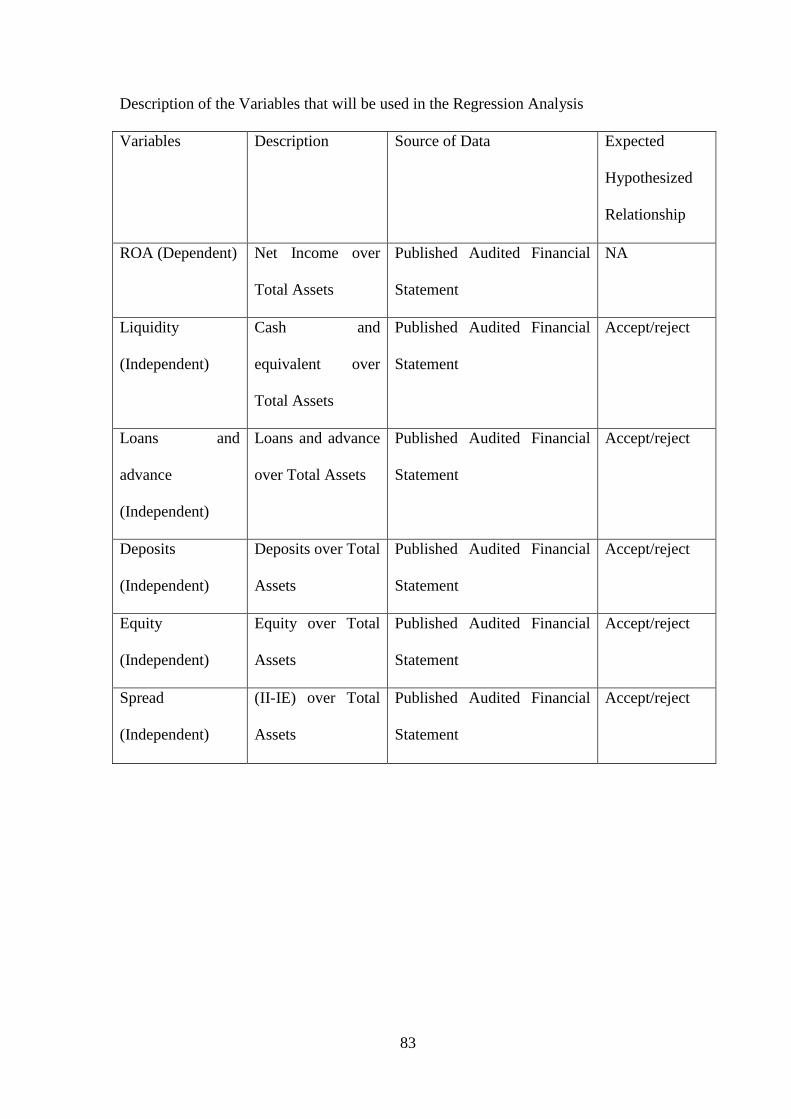

2014 and was focused on profitability ratio using ROA as dependent variable and five

independent variables such Liquidity (LQR), Credit facilities (NCA), Deposit to Assets

Ratio (DTA), Capital Adequacy Ratio (CAR), Spread Ratio (SP), (AU and NPM) using

modified DuPont analysis. Listing a company on a stock exchange opens a lot of

opportunities for the business especially for financing for businesses in emerging markets.

But does listing on a stock exchange in Rwanda impact financial performance? This study

would benefit to Commercial Banks managers as it will provide them a better

understanding for the impact to list on Stock exchange; thus be able to focus on

improving these factors to ensure that their financial performance keeps

improving.Multicollinearity test was used to test the correlation between independent

variables and selected the relevant variables. For the purpose of comparison Cross-section

design was used to identify relations between dependents and potential explanatory

variables was presented. Econometric model are given to select the relevant variables for

the model. Finally the econometric specification was tested using Hausman tests. E-view

was used to run the model. The result prove that there was a positive significance between

dependent variables and dependent variable pre-post listing except liquidity ration with

negative significance and spread ratio which has proved no significance on ROA and

result for this study show that β1=0.337 and P= 0.000<5% in pre-listing,β1=-1.061 with

P=0.021<5%, β2=-0.001 with P= 0.779 >5% pre-listing and β2= 0.104 with P=0.004<5%

and prove the impact for loans and advance in post and not in pre.β3=-0.063 with P=

0.168 >5% β3= 4.486 with P=0.000<5% and this demonstrate that the deposit impacted

positively on profitability in post-period better as it had no significance in pre-listing

period. β4= 0.017 with P= 0.050 <5% pre and β4=0.427 with P=0.016<5% post-listing

prove effects of total equity for Bank of Kigali profitability strong significance post

listing better than in pre.β5=0.051 with P=0.011 pre and β5= 0.423 with P=0.351>5%prove

that there was a significance effect pre but not in post-listing period. The financial

performance of BK improved significantly from the listing period on Rwanda stock

exchange and the researcher recommend to BK to improve their Cash and cash equivalent

policy to avoid its negative effect on ROA and try to minimize the cost of borrowing and

recommend for further research using other indicators.

vi

TABLE OF CONTENTS

DECLARATION................................................................................................................ ii

DEDICATION...................................................................................................................iii

ACKNOWLEDGEMENT ................................................................................................ iv

ABSTRACT ........................................................................................................................ v

TABLE OF CONTENTS ................................................................................................. vi

LIST OF TABLES ............................................................................................................ ix

FIGURE .............................................................................................................................. x

LIST OF ACRONYMS AND ABBREVIATIONS ........................................................ xi

DEFINITION OF KEY TERMS .................................................................................... xii

CHAPTER ONE: INTRODUCTION .............................................................................. 1

1.0 Introduction .................................................................................................................... 1

1.1 Background of the Study ............................................................................................... 1

1.2 Statement of the Problem ............................................................................................... 4

1.3 Objectives of the study................................................................................................... 6

1.3.1 General Objective ....................................................................................................... 6

1.3.2 Specific objectives of the study .................................................................................. 6

1.4 Hypothesis...................................................................................................................... 6

1.5 Significance of the study ................................................................................................ 7

1.5.1 Bank Management ...................................................................................................... 7

1.5.2 Researchers and Academicians ................................................................................... 8

1.6 Limitation of the study ................................................................................................... 8

1.7 Scope of the study .......................................................................................................... 8

vii

1.7.1 Geographical Scope .................................................................................................... 8

1.7.2 Content Scope ............................................................................................................. 8

1.7.3 Time Scope ................................................................................................................. 9

1.8 Organization of the study ............................................................................................... 9

CHAPTER TWO: REVIEW OF THE RELATED LITERATURE .......................... 10

2.0 Introduction .................................................................................................................. 10

2.1 Theoretical Literature ................................................................................................... 10

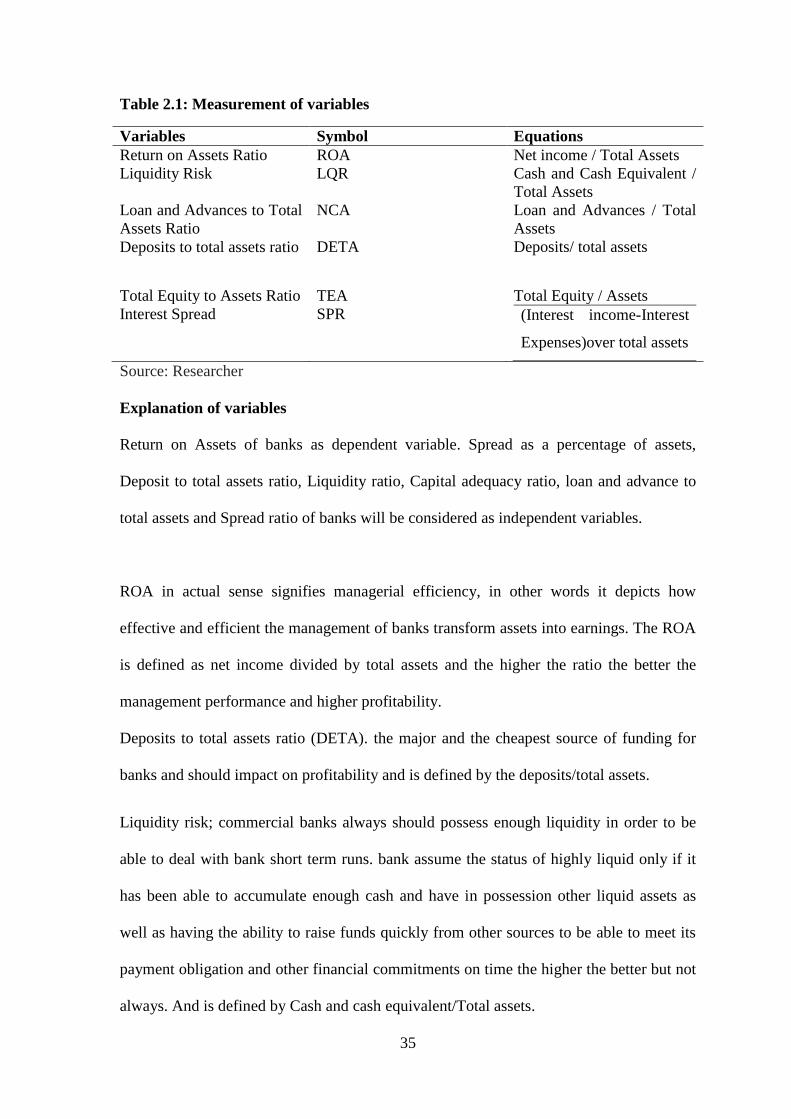

2.1.1 Profit Measures and Determinants of Commercial Banks Profitability ................... 11

2.1.2 Return on Assets (ROA). .......................................................................................... 12

2.1.3 Deposits to total assets ratio (DETA) ....................................................................... 12

2.1.4 Liquidity ratio ........................................................................................................... 13

2.1.5 Capital and reserve to total assets ratio (CRTA) ...................................................... 13

2.1.6 Loans and advances to total assets ratio (LOTA) ..................................................... 13

2.1.7 Interest rate (Spread) ................................................................................................. 14

2.1.8 Limitations of Using Financial Ratios ...................................................................... 14

2.2 Empirical Literature ..................................................................................................... 16

2.3 Critical Review and Research Gap identification ........................................................ 28

2.4 Theoretical framework ................................................................................................. 29

2.5 Conceptual framework ................................................................................................. 33

CHAPTER THREE: RESEARCH METHODOLOGY .............................................. 37

3.0 Introduction .................................................................................................................. 37

3.1 Research Design........................................................................................................... 37

3.2 Target Population ......................................................................................................... 37

viii

3.3 Sample Design ............................................................................................................. 38

3.3.1 Sample Size ............................................................................................................... 38

3.4 Data Collection Methods ............................................................................................. 38

3.4.1 Data Collection Instruments ..................................................................................... 39

3.4.2 Administration of Data Collection Instruments ........................................................ 39

3.4.3 Reliability and validity .............................................................................................. 40

3.5 Data analysis Procedure ............................................................................................... 41

3.6 Econometric Model ...................................................................................................... 41

3.7 Ethical consideration .................................................................................................... 42

CHAPTER FOUR: RESEARCH FINDINGS AND DISCUSSION ........................... 43

4.0 Introduction .................................................................................................................. 43

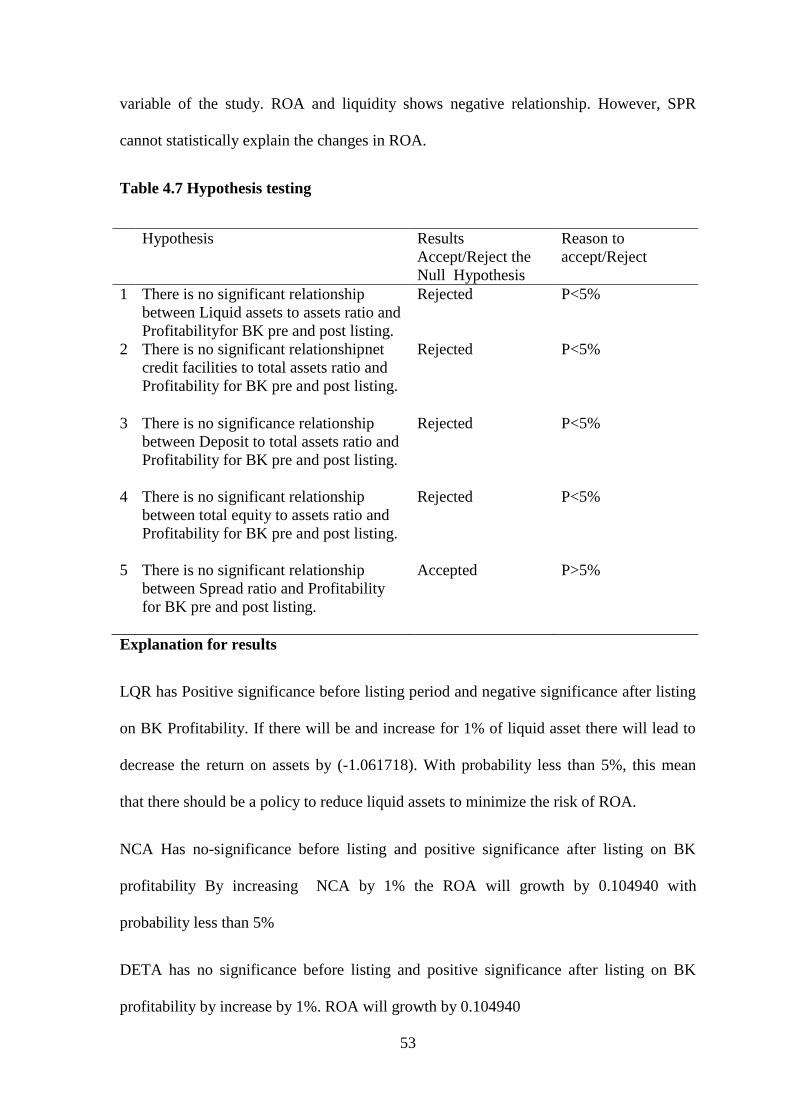

4.2 Presentation of Findings Pre-post listing period .......................................................... 52

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS . 55

5.0 Introduction .................................................................................................................. 55

5.1 Summary of Findings ................................................................................................... 55

5.2 Conclusion ................................................................................................................... 57

5.3 Recommendation ......................................................................................................... 57

5.4 Suggestions for further study ....................................................................................... 58

REFFERENCES .............................................................................................................. 59

APPENDICES .................................................................................................................. 74

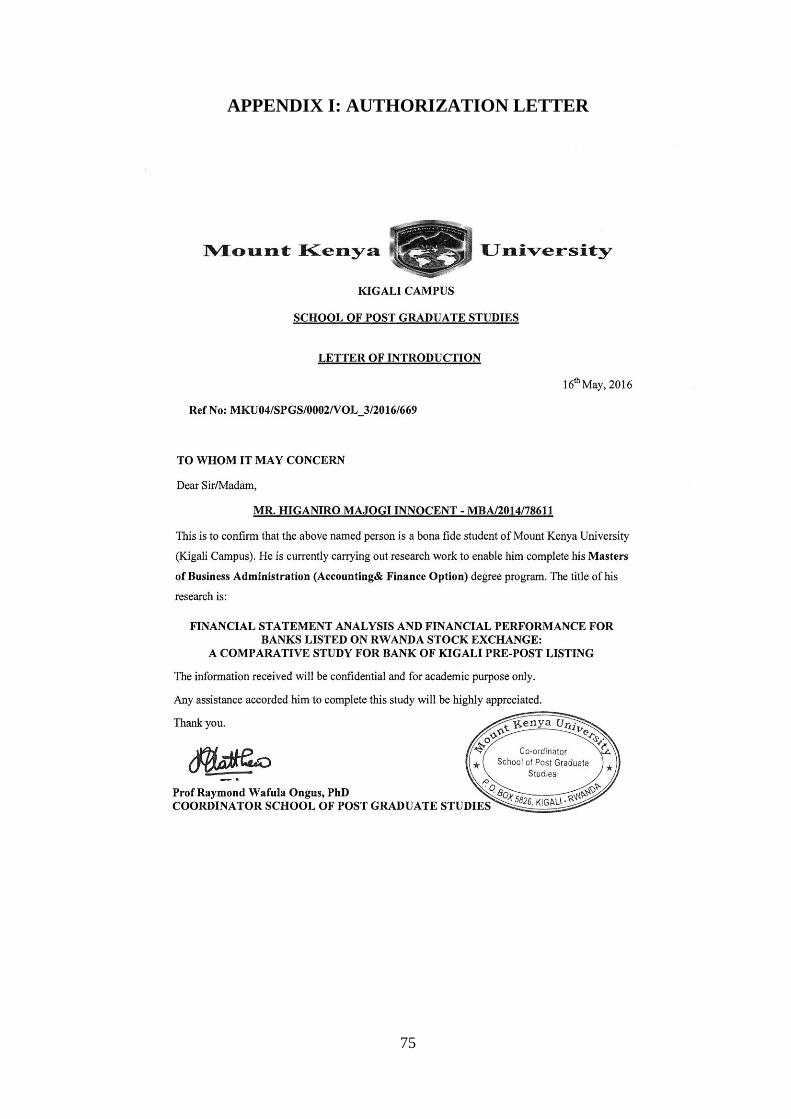

APPENDIX I: AUTHORIZATION LETTER .............................................................. 75

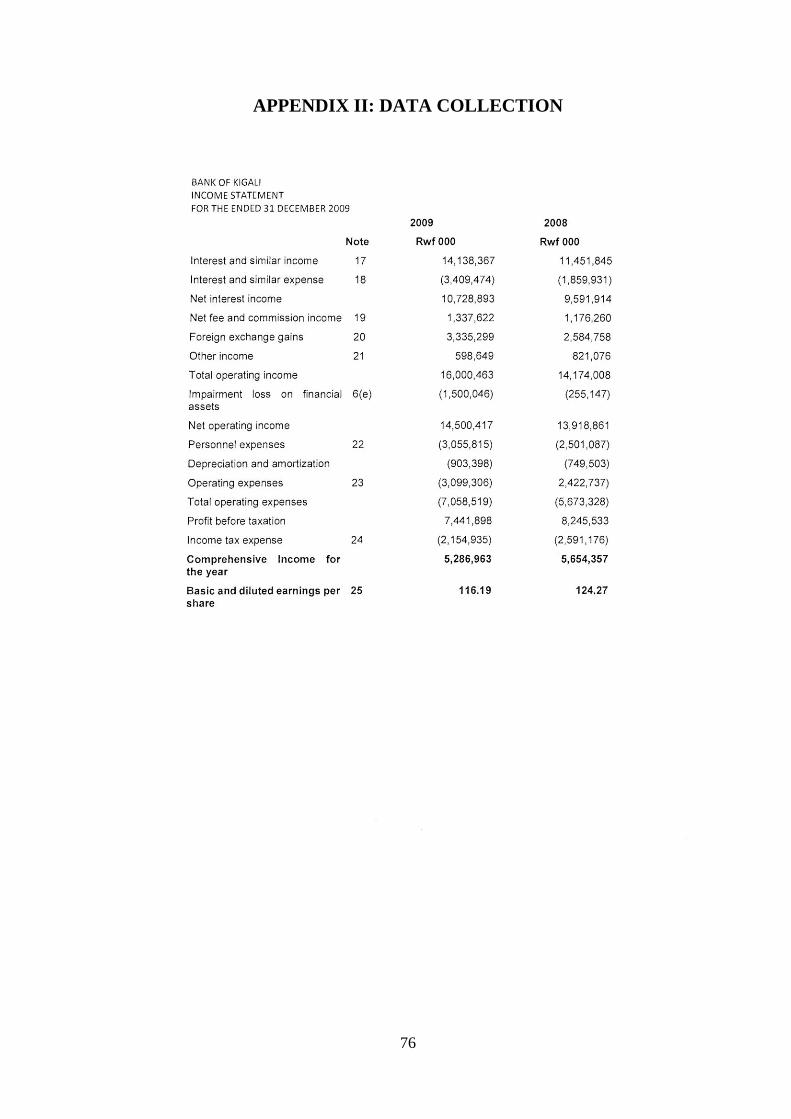

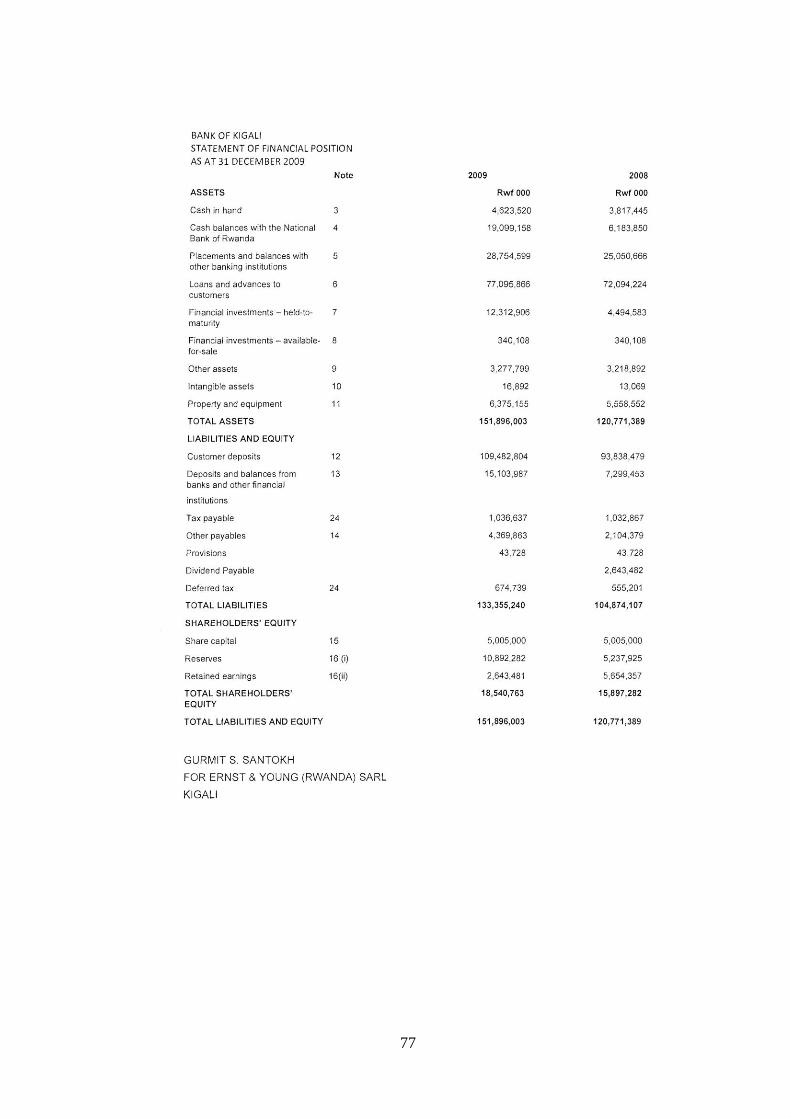

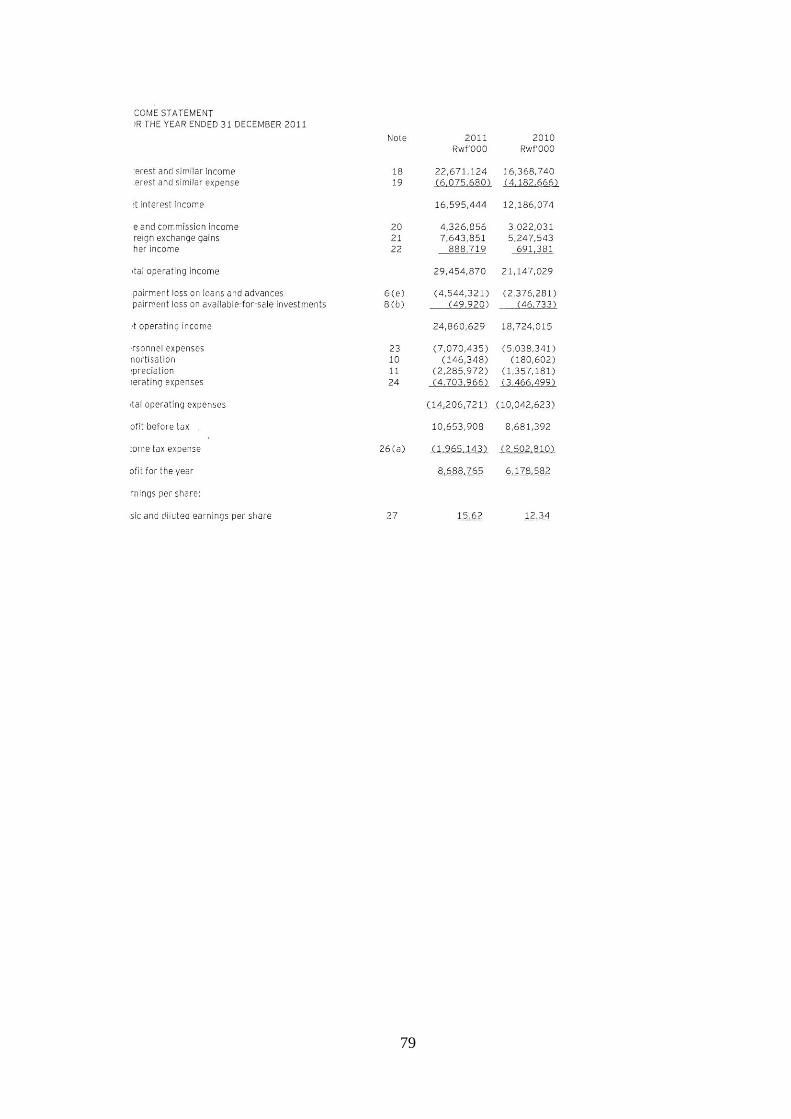

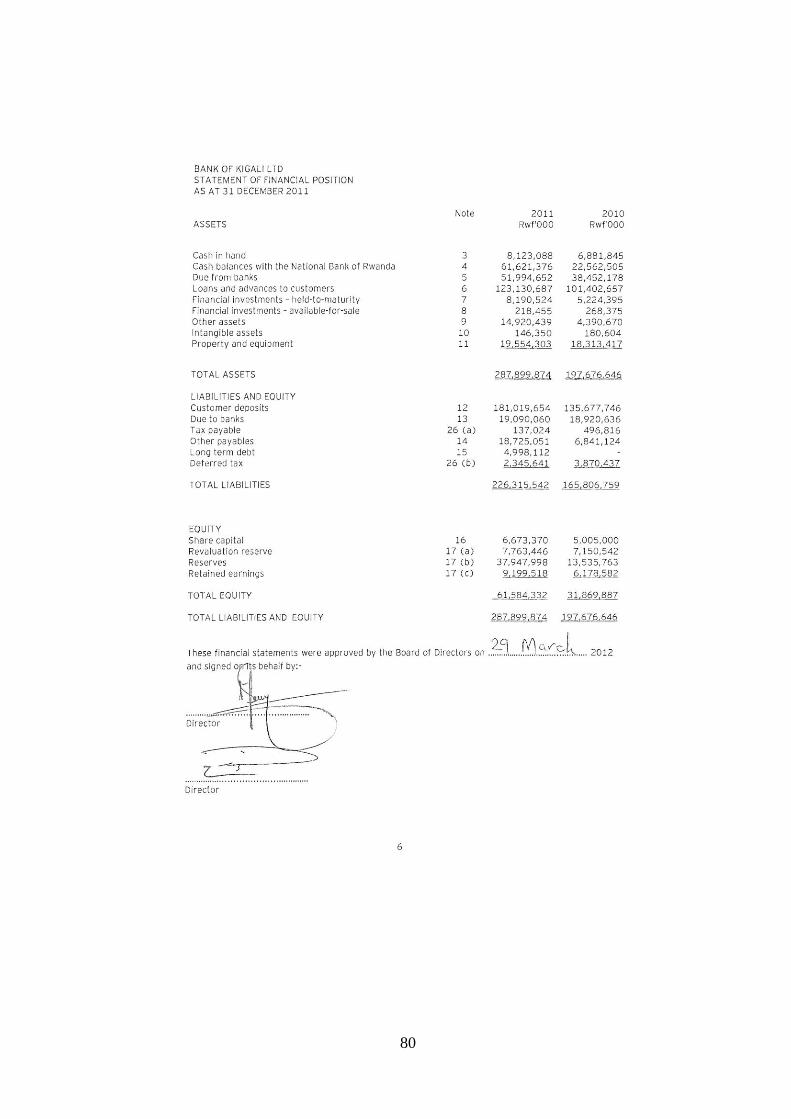

APPENDIX II: DATA COLLECTION ......................................................................... 76

ix

LIST OF TABLES

Table 2.1: Measurement of variables .................................................................................35

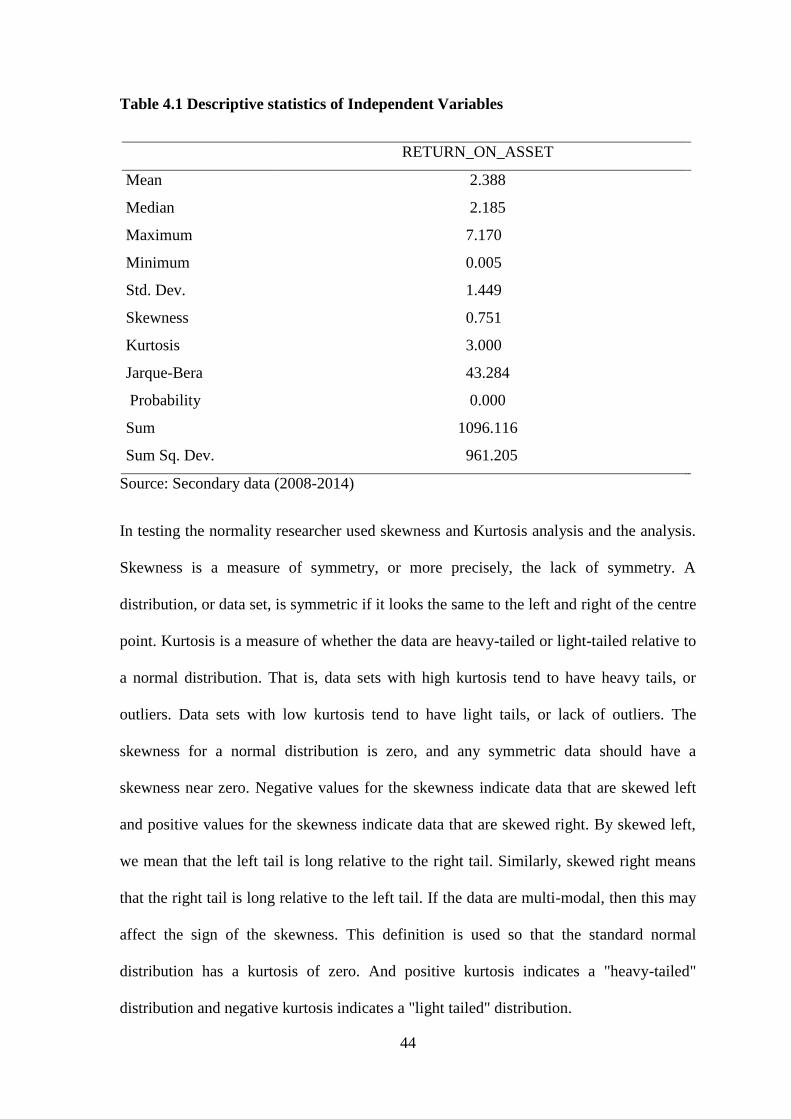

Table 4.1 Descriptive statistics of Independent Variables .................................................44

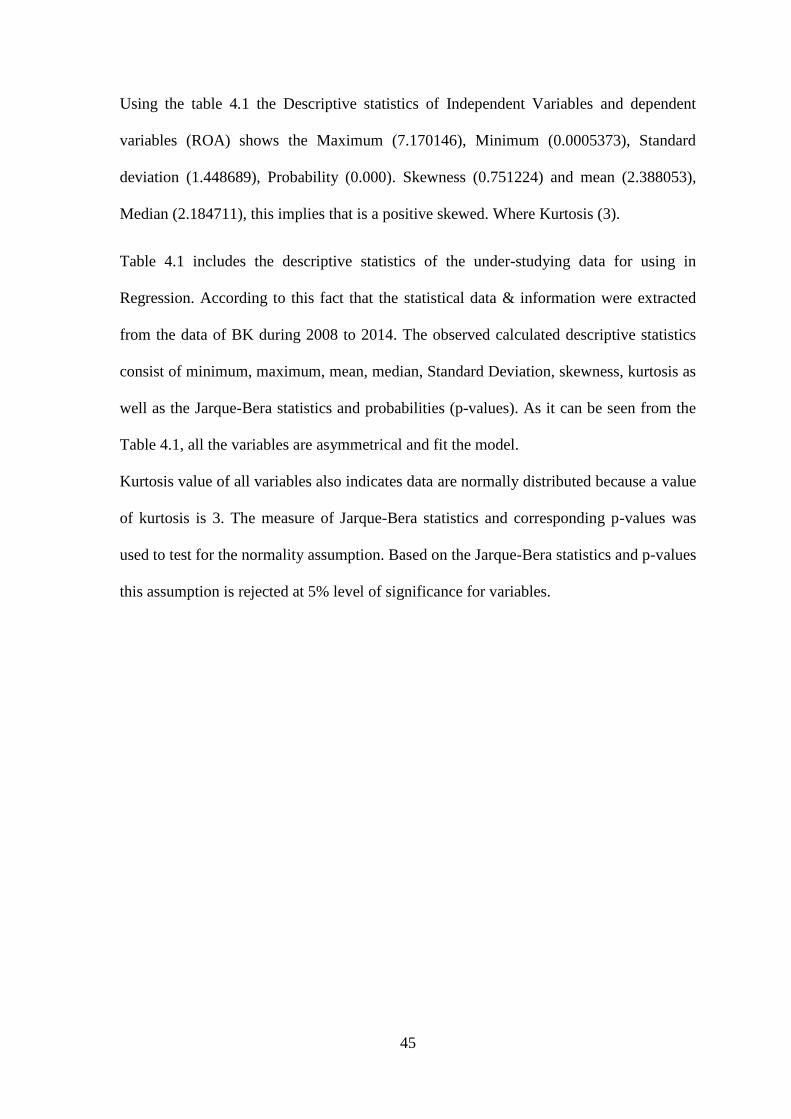

Table 4.2 Financial statements ratios, determinants of firm performance .........................46

Table 4.3 Correlation analysis of Variables .......................................................................47

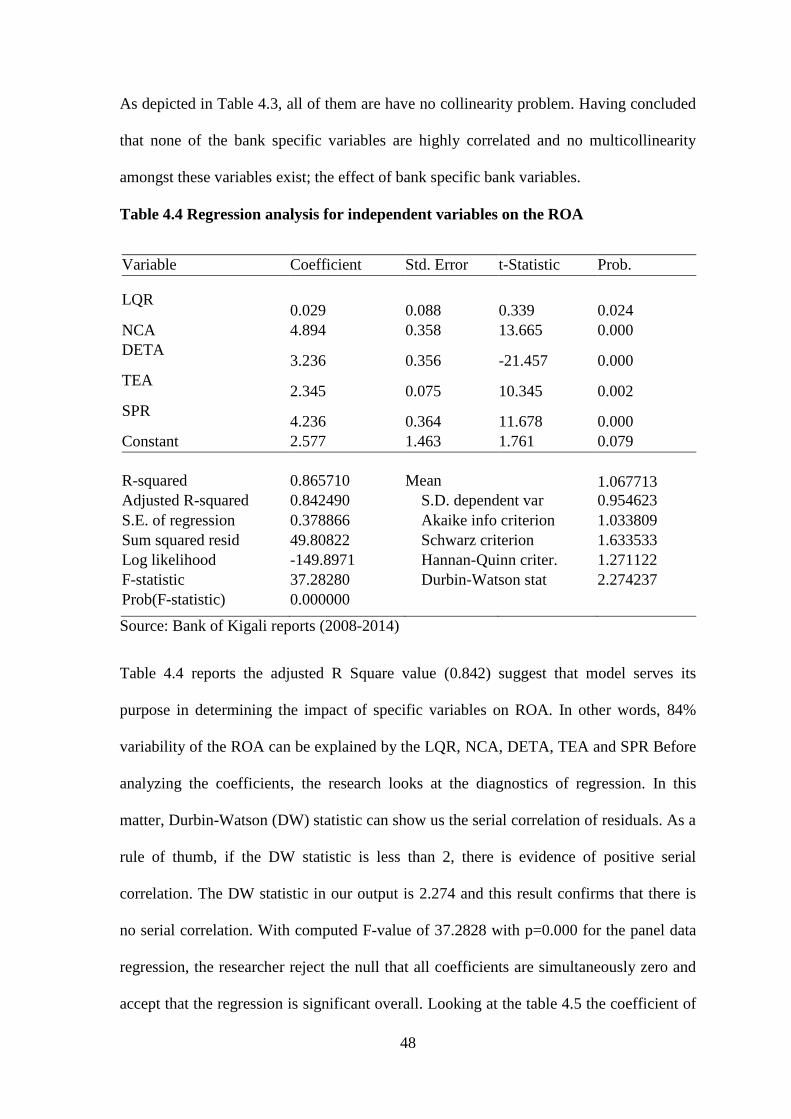

Table 4.4 Regression analysis for independent variables on the ROA ..............................48

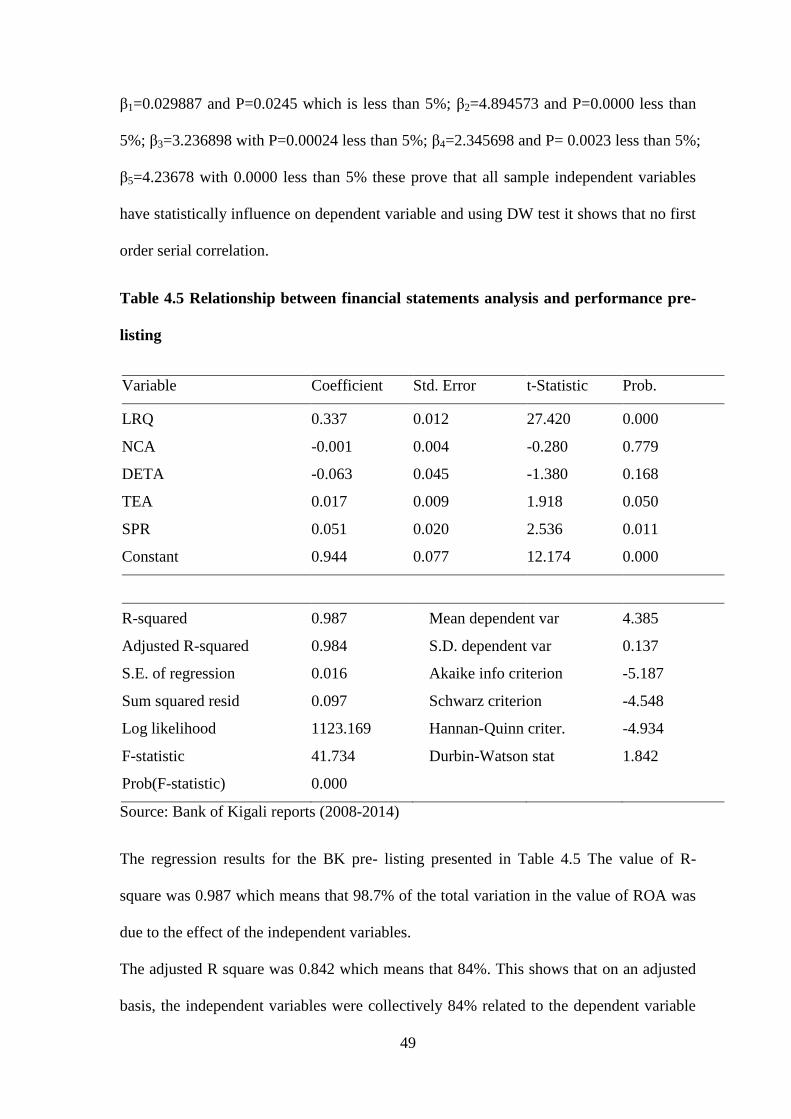

Table 4.5 Relationship between financial statements analysis and performance pre-listing

............................................................................................................................................49

Table 4.6 Relationship between financial statements analysis and performance post-listing

............................................................................................................................................51

Table 4.7 Hypothesis testing ..............................................................................................53

x

FIGURE

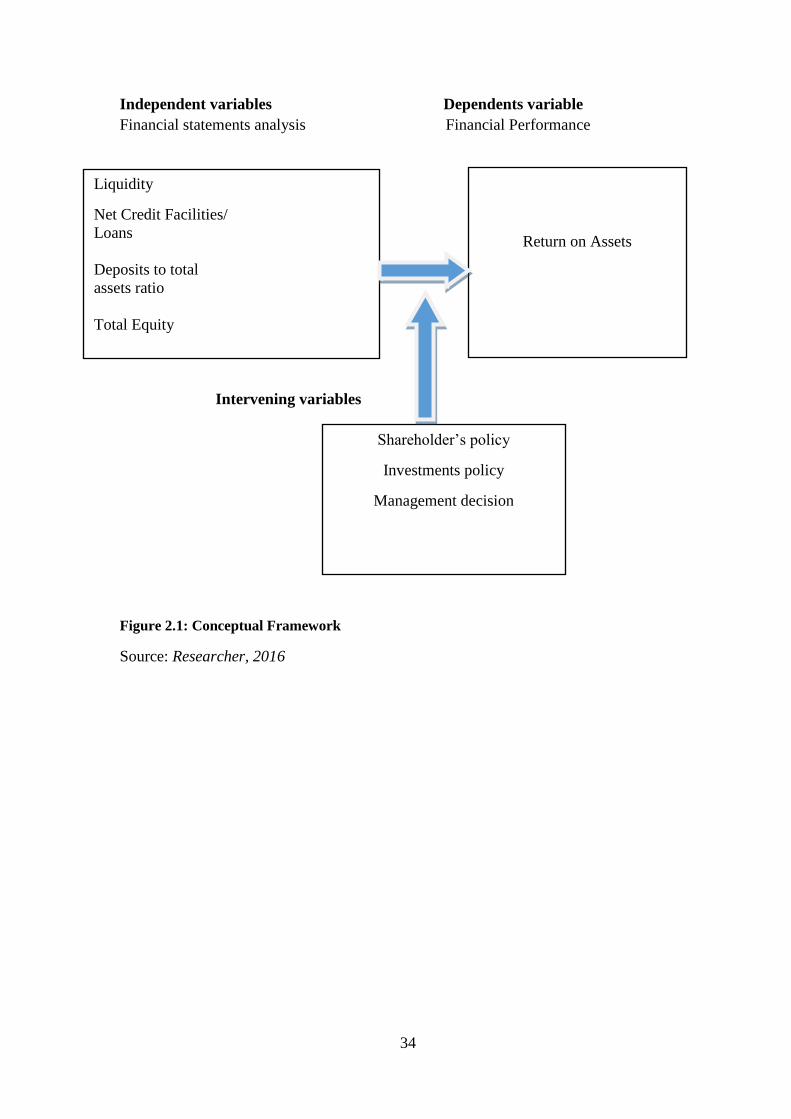

Figure 2.1: Conceptual Framework ................................................................................... 34

xi

LIST OF ACRONYMS AND ABBREVIATIONS

AU : Asset Utilization

BK : Bank of Kigali

CDR : Cash Deposit Ratio

CRTA : Capital and reserve to total assets ratio

DETA : Deposit to Total Asset Ratio

DTAR : Debt to Total Assets Ratio

DW : Durbin-Watson

EM : Equity Multiplier

IER : Income to expense Ratio

LAR : Loan and Advance to Asset Ratio

LQR : Liquidity Risk

NCA : Non Current Assets

NII : Non-Interest Income

NIM : Net Interest Margin

PER : Profit Expense Ratio

PM : Profit Margin

ROA : Return on Assets

ROD : Return on Deposit

ROE : Return on Equity

SPR : Spread Ratio

TEA : Total Equity to Assets

xii

DEFINITION OF KEY TERMS

Commercial banks are companies that take in money from individuals or companies and

use those funds to purchase financial assets such as deposits, loans, and securities as

opposed to tangible property. Commercial Banks are Depository firms and loans that pay

interest on deposits and then lend money in the form of interest-earning loans.

Financial statements analysis is the selection, evaluation, and interpretation of financial

data, along with other pertinent information, to assist in investment and financial

decision-making. The term “Financial Analysis,” also known as analysis and

interpretation of financial statements refer to the process of determining financial strength

and weaknesses of the firm by establishing strategic relationship between the items of the

balance sheet, income statement and other operative data.

Financial statements; financial statements refer to such statements, which contains

financial information about an enterprise. It is the final product of accounting work done

during the accounting period – quarterly/ half-yearly/annually. Financial statements are

prepared in monetary terms. Some refer to them as „Annual Accounts‟, when they are

prepared on a yearly basis. However, interim financial statements are prepared for a

shorter period, usually a quarter, and hence called „Quarterly Financial Statements‟.

Stock exchange; the word “Stock Exchange” is made from two words 'Stock' and

Exchange. Stock means part or fraction of the capital of a company, and Exchange means

a transferring the ownership; representing a market for purchasing and selling. Thus, we

can describe the stock exchange as a market or a place where different types of securities

are bought and sold. A stock exchange is a secondary market of securities because the

trading happens only for the securities that have already been issues to the public.

i

The financial statements are prepared by the board of directors for reporting to

shareholders in discharge of their stewardship function and hence corporate law enjoins

upon them the responsibility of laying down them before annual general meeting of the

shareholders so as to give a „true and fair view‟ of the affairs of the company.

The profit and loss account shall be annexed to the balance sheet and auditor‟s report

(including the auditor‟s separate, special, or supplementary report, if any) shall be

attached thereto. Financial statements consists the basic statement of accounts used to

convey the quantitative information of financial nature about a business to shareholders,

creditors and others interested in the reporting company‟s financial condition, result of

operation uses and sources of funds

.

1

CHAPTER ONE: INTRODUCTION

1.0 Introduction

This chapter begins by presenting a brief background of the study which is followed by

the statement of the problem, following the statements of the problem the general and

specific objectives of the study are presented. After that, the next section presents the

research hypothesis. Finally, significance of the study, scope and limitation of the study

including organization of the study are presented.

1.1 Background of the Study

Banking sector plays an important role in sustaining financial markets and has a

significant impact on the success of the economy. Sound financial health of a bank is the

guarantee not only to its depositors but is equally significant for the shareholders,

employees and whole economy as well. As a sequel to this maxim, efforts have been

made from time to time, to measure the financial position of each bank and manage it

efficiently and effectively Din Sangm, (2010). The Banking sector all over the world acts

as the life blood of modern trade and economic development and through being a major

source of finance to the economy Ongore and Kusa, (2013).

Assessing the health of an economy can be accomplished by studying the financial

performance of financial institutions, Haque and Sharma, (2011). The banking and

financial industry has become a reality in today's economy, as it is witnessing a growing

both in terms of the number of such institutions, or in terms of the amount of money

managed by or diversity activities. In spite of this progress and successes achieved by the

banking and financial institutions, it still have challenges which will require further

intensive efforts on the part of these institutions. Such to enhance the quality of its

2

products, services, diversity and to keep pace with the rapid developments taking place in

the world in this field.

Commercial banks have been attacked by the globalization, competition (from

nonbanking financial institutions) and volatile market dynamic pressures, Casu et al,

(2006). So banks attempt to find new method to improve their services. To understand the

superior performance and struggle for it, managers and policy makers stated the major

question is "What drives performance?" To address this question, researchers have

focused their efforts on the operational details Soteriou and Zenios, (1999).

In Developing countries like Rwanda, banks play a major role in financial development.

This is especially true since stock and corporate bond markets are usually underdeveloped.

Moreover, the development of the banking system and improving of its financial

performance is related to higher economic growth of a country. In Rwanda commercial

banks contribute to economic growth through their financial intermediation role. Better

performance of commercial banks is pro foundation for product innovation,

diversification and efficiency of the commercial banks Hempell, (2002).

The stability of commercial banks as whole in the economy depends on better financial

performance. Better financial performance level has tendency to absorb risks and shocks

that commercial banks can face.

Rwanda Commercial banks are faced with increasing competition and rising costs as a

result of regulatory requirements, financial and technological innovation, and entry of

large foreign banks in the retail banking environment. These changes had a dramatic

effect on the performance of the commercial banks in Rwanda.

3

Although an important and relevant information about bank's financial performance can

be provided by accounting and financial ratios, assessing the relationship among many

factors that are related to bank performance such as assets, revenue, profit, market value,

number of employees, investments, and customer satisfaction can assist in improving

bank productivity Seiford and Zhu, (1999).

The performance evaluation of a commercial banks is usually related to how well the

bank can use its assets, shareholders‟ equities and liabilities, revenues and expenses.

The evaluation of a firm‟s performance usually employs the financial ratio method,

because it provides a simple description about the firm‟s financial performance in

comparison with previous periods and helps to improve its performance of management

(Lin et al., 2005).

The financial environment of any economy consists of typically five components namely:

money, financial instruments, financial institutions, rules and regulations and financial

markets. Among the various financial institutions, banks are a fundamental component

and the most active players in the financial system Dhanabhakyam&Kavitha, (2012).

Initially studies on banks performance analysis used different financial ratios, such as

return on assets, return on investment, return on equity, equity to assets, internal growth

of equity, etc.

Though these ratios are still used in the financial industry, it has been recognized that

these ratios can be called partial productivity indicators, and holistic total factor

productivity can be measured by considering various financial indicators simultaneously

Tapas, (1998).

4

By the scope of its functions, banks are the key to economic growth of any economy

(Rashid, 2010). Further, banks are a fundamental component of the financial system, and

are also active players in financial markets Guisse, (2012).

The essential role of a bank is to connect those who have capital (such as investors or

depositors), with those who seek capital (such as individuals wanting a loan, or

businesses wanting to grow). Banks have control over a large part of the supply of money

in circulation.

Through their influence over the volume of bank money, they can influence in nature and

character of production in any country Brigham & Houston, (2011).

In consistent with Kumbirai, & Webb (2010), a single bank is highly connected with

other banks for payment system and other functions of bank such that the failure of a

single bank not only affects its shareholders and depositors rather it affects rest other

banks and even all rest other business. The failure of a single bank creates an economic

turmoil situation and is regarded as a disaster for the economy.

1.2 Statement of the Problem

Commercial Banks play vital role in the economic development of the countries, they

allocate resource and channel funds from savers to investors continuously Okoth et al.

(2013). They do so, if they get necessary earnings to cover their operational cost they

incur. Moreover for sustainable intermediation function, banks need to be gainful.

Beyond the intermediation function, the financial performance of banks has critical

implications for economic growth of countries. Good financial performance rewards the

shareholders for their investment. This in turn, gives confidence for additional investment

and brings about economic growth. On the other hand, poor management may lead to

banking failure which have negative consequence on the economic growth

Okothetal.(2013).

5

Banking efficiency is important at both macro and micro levels and in order to allocate

resources effectively, banks should be sound and efficient Hussein (2000).

Allocative efficiency is the extent to which resources are being allocated to the use with

the highest expected value. A firm is technically efficient if it produces a given set of

outputs using the smallest possible amount of inputs Falkena et al, (2004). Financial

performance or profitability can be defined as factors that are influenced by a bank‟s

management decisions. The management of enterprise is depending on accounting

information for taking various strategic decisions and financial statements provide such

information. This information is made useful by analysing and interpretation of financial

statements with help of financial analysis techniques among which the common technique

to use is financial ratios also known as accounting ratios. Accounting ratios are important

tools in the management for decision making. R.K. Sharma, Shashi K. Gupta, (2001),

financial statements are prepared primarily for decision making, but the information

provided in financial statements is not an end in itself and no meaningful conclusion can

be drawn from these statements alone. Ratio analysis helps in making decisions from the

information provided in these financial statements. Thus, the proper use of accounting

ratios assists management in communicating information which is pertinent and

purposeful for decision makers to ensure the effectiveness of management in the

enterprise.The objective of financial statements is to provide information about the

financial position, performance and changes in financial position of an enterprise that is

useful to a wide range of users in making economic decisions.

Difference between financial performances for the two different period and advice for

management decision.

6

1.3 Objectives of the study

1.3.1 General Objective

The main objective of this research was to analyze, evaluate and compare financial

statements for Bank of Kigali to determine the impact on its financial performance Pre-

Post listing on Rwanda stock Exchange.

1.3.2 Specific objectives of the study

The objectives of this study are summarized as follows:

i. To evaluate and compare the impact of Liquid assets to assets ratio for Bank of

Kigali Profitability pre and post listing to Rwanda Stock Exchange .

ii. To investigate and compare the effect of Loans and Advance to total assets ratio

for Bank of Kigali profitability pre and post listing to Rwanda Stock Exchange.

iii. To compare the impact of deposit to total assets ratio for Bank of Kigali

profitability pre and post listing to Rwanda Stock Exchange.

iv. To compare the effects of total equity to assets ratio for Bank of Kigali

profitability pre and post listing to Rwanda Stock Exchange.

v. To compare the effect of Spread ratio for Bank of Kigali profitability pre and post

listing to Rwanda Stock Exchange.

1.4 Hypothesis

The study will be based on the following hypothesis which will be developed and tested

Ho1: There is no significant relationship between Liquid assets to assets ratio and

Profitability for BK pre and post listing, to Rwanda Stock Exchange.

Ho2: There is no significant relationship for net credit facilities to total assets ratio and

Profitability for BK pre and post listing, to Rwanda Stock Exchange.

7

Ho3: There is no significance relationship between total Deposit to total assets ratio and

Profitability for BK pre and post listing, to Rwanda Stock Exchange.

Ho4: There is no significant relationship betweentotal equity to assets ratio and

Profitability for BK pre and post listing, to Rwanda Stock Exchange.

Ho5: There is no significant relationship between Spread ratio and Profitability for BK

pre and post listing, to Rwanda Stock Exchange.

1.5 Significance of the study

Rwanda has a vision 2020 agenda and one of its aims is to be a middle income economy

by the year 2020.

This can be achieved if the level of economic investment increases in the country.

It would also be crucial that equity market is developed to provide access to finance for

investors and the study will show the effect for listing on Rwanda stock Exchange (RSE),

compare the period before and after listing.

The study was motivated by the fact that, the measurement of financial performance of

the banking sector was important for several reasons.

1.5.1 Bank Management

This study will be beneficial to Commercial Banks managers as it will help them better

understand the determinant factors of their financial performance and the impact to list on

Stock exchange; thus be able to focus on improving these factors to ensure that their

financial performance keeps improving.

Financial performance is a vital factor for financial institutions wishing to carry out their

business successfully, given the increasing competition in the financial markets

Financial performance measures are critical aspects of banking sector that enable us to

distinguish banks that has the capability to survive and prosper from those that may have

8

problems with competitiveness. Additionally, financial ratios enable us to identify unique

bank strengths and weaknesses, which in itself inform bank profitability, liquidity and

credit quality.

1.5.2 Researchers and Academicians

Researchers and academicians in the field of finance, economics and banking will find

this study a useful guide for carrying out further studies in the area.

1.6 Limitation of the study

The following are the limitation of the present study:-

This study was limited to the comparative study of financial performance of two period.

This study was based on secondary data and was to analyze and evaluate data from the

latest six years period i.e. since 2008-2010 and 2012-2014 (i.e. 6 years historical data)

and the transitional year was not concerned in the study, only selected financial ratios and

statistical tools and techniques were used.

1.7 Scope of the study

1.7.1 Geographical Scope

The study was carried out in Rwanda and covered Bank of Kigali operations.

1.7.2 Content Scope

In pursuance of objective of the study attention was made and focused on the effect of

Financial Statements analysis for Bank of Kigali (BK) in order to conduct an empirical

investigation as to whether there is a relationship for Financial Performance between the

two periods under study. In view of the impossibility of covering every type of financial

statement, this study was therefore restricted to the analysis of the income statement and

the Balance Sheet for BK, by means of financial ratios and trend analysis for profitability

(ROA).

9

1.7.3 Time Scope

The study will cover the period from 2008 to 2014, three years pre and three years post

listing on Rwanda Stock Exchange (RSE). And the transition (2011) year was not

concerned by the study.

1.8 Organization of the study

This study was organized into the following three chapters: Chapter one of this study;

Introduction to the study, background of the study, statement of the problems,

significance of the study, objectives of the study, Hypothesis, Scope and limitations of the

study and Organization of the study. Chapter Two; Review of Related Literature, This

includes reviews of related literature, empirical literature, Critical Review and Research

Gap identification, theoretical framework and Conceptual framework. Chapter Three;

Research Methodology: Introduction, Research Design, Sample Design, Target

Population, Sample Design, Sample Size, Sampling Technique, Data Collection Methods,

Data Collection Instruments, Administration of Data Collection Instruments, Reliability

and validity , Data analysis Procedure, Ethical Consideration. Chapter Four: Research

Findings and Discussion: Introduction, Findings Discussion and Interpretation. Chapter

Five; Summary, Conclusions and Recommendations; Introduction, Summary and

Recommendations.

10

CHAPTER TWO: REVIEW OF THE RELATED LITERATURE

2.0 Introduction

This chapter is composed of five major parts: the related literature, empirical studies,

Critical Review, Research Gap identification, conceptual framework and the theoretical

framework.

2.1 Theoretical Literature

With regards to the discussions and analysis of the various theories and issues involve in

this part of the study. The study has chosen to expound on the various theories in books,

articles and working papers to be able layout or explore the factors characterizing the

profitability of Commercial Banks from Financial statements analysis to draw the

financial performance and profitability, this part of the thesis was focused on theories

which include profit measurement theories and various profit determinants and financial

performance theories of commercial banks. According to Pandey (1997) has defined as

the finance statement provides a summarized view of the financial operation of the firm.

Therefore, something can be learnt about a firm and careful examination of the financial

statements as invaluable documents or performance reports. Thus, the analysis of

financial statement is an important aid to financial analysis or ratio analysis is main tool

of financial statement analysis.

Beginning with Beaver's (1966) expressed that standard financial ratios can predict the

financial performance of firms, many subsequent studies have attempted to demonstrate

the predictive value of various techniques for estimating actual business performance.

According to Meigs and Meigs (2003), the purpose of financial statement analysis is to

provide information about a business unit for decision making purpose and such

11

information need not to be limited to accounting data. While ratios and other relationships

based on past performance may be helpful in predicting the future earnings performance

and financial health of a company, we must be aware of the inherent limitations of such

data.

According to Baisi (2005) and Foster (1986) ratio analysis is importance to provides the

framework for the decision making; used by analyst to judge the performance of the

company; used in credit analysis to make judgment with regard to provide loans or not, it

is frequently used by the banks.

2.1.1 Profit Measures and Determinants of Commercial Banks Profitability

With regards to the main focus of this study, the elaboration of the various profit

measures and determinants theories which has been considered in other related studies is

very significant to the realization of the factors to be investigated in this study. According

to Devinaga Rasiah (2010) documented that most researchers who focused their studies in

this area are for instance, divide the determinants of commercial banks performance and

profitability into two categories thus, the Internal and the External factors. According to

Husni (2011) the internal determinants of banks profitability are normally consisting of

factors that are within the control of commercial banks. They are the factors which affect

the revenue and the cost of the banks. Some studies classified them into two categories

namely the financial statement variables and non-financial variables. The financial

statement variables include factors that are directly related to the bank‟s balance sheet and

income statement. Whiles, the non-financial statement variables include factors like the

number of branches of a particular bank, location and size of the bank; Haron, Sudin

(2004).According to Anthony Karkrah and Ameyaw (2010) many researchers have

presented ROA as an appropriate measure of bank profitability.

12

2.1.2 Return on Assets (ROA).

This study was considered Return on Assets as profitability measures. According to

Rasiah (2010) presented that banks generate income mostly on their assets and the assets

could be termed as income and non-income generating. With regards to commercial

banks income Rasiah (2010) classified it into two, namely interest and non-interest

income. The interest income consist of rates charge on loans, overdraft and trade finance

which the banks offers to customers. Whereas, the non-interest income is consisting of

fees, commissions, brokerage charges and returns on investments in subsidiaries and

securities. According to Vong et al (2009), the major source of banks revenue is interest

income. It contributes the major income of commercial banks earnings. The other source

of banks revenue includes dividends and gains from dealing in the securities market.

There could be also some minor sources of income for instance earnings from trust

activities and service charges on deposit accounts; Vong et al (2009).

The return on total assets of the bank: Base on the argument made by Rivard and Thomas

(1997) that bank profitability is best measured by ROA because ROA cannot be distorted

by high equity multiplier. This study will choose to use (ROA) thus returns on total assets

to measure performance of the banks. ROA in actual sense signifies managerial efficiency,

in other words it depicts how effective and efficient the management of banks has been as

they seek to transform assets into earnings. The ROA is defined as net income divided by

total assets.

2.1.3 Deposits to total assets ratio (DETA)

The effect of fund source (DETA) on profitability is captured by the deposits/total assets

ratio. It is believed to be the major and the cheapest source of funding for banks,

empirical evidence provided by Husni Ali Khrawish (2011) prove that customer deposits

13

impact banking performance positively as long as there is a sufficient demand for loans in

the market.

2.1.4 Liquidity ratio

According to Devinaga Rasiah (2010) commercial banks are required by regulators to

hold a certain level of liquidity assets. And the reason behind this regulation is to make

sure that the commercial banks always possess enough liquidity in order to be able to deal

with bank runs. He further argue that a bank assume the status of highly liquid only if it

has been able to accumulate enough cash and have in possession other liquid assets as

well as having the ability to raise funds quickly from other sources to be able to meet its

payment obligation and other financial commitments on time.

2.1.5 Capital and reserve to total assets ratio (CRTA)

This is defined as total equity over total assets; this is expected to uncover the capital

adequacy of the banks and capture the general average safety and soundness of the banks.

According to Molyneux (1993) banks with high level of equity can reduce their cost of

capital and that could impact positively on profitability.

2.1.6 Loans and advances to total assets ratio (LOTA)

This reveals the asset composition which is estimated by total loans and advances divided

by total asset. Loans provide major means of earnings for commercial banks and it is

often believed that the more banks offer loans the more it does generate revenue and more

profit; Abreu and Mendes (2000). Base on this loans are expected to have a positive

relationship with bank performance.

14

2.1.7 Interest rate (Spread)

Devinaga Rasiah (2010) advocates that interest rate have been captured in most studies as

profitability determinant of commercial banks because net interest income which results

from the deference between interest income and interest expenses has enormous impact

on banks profitability. He stated that most research papers on banks‟ profit determinants

present the interest rate as external variable because changes in interest rates is mostly

cause by government economic policies and supply and demand market conditions.

Moreover, He mentioned that the impact of interest rate changes on the commercial banks

profitability depend on the extent and speed at which the change have on short and long

term period of banks portfolio. And also the speed and flexibility with which the bank can

amend its revenue sources and cost of funds to match up to the change. In addition, it is

also about the proportionality of the bank‟s assets and liabilities that are long period

rather than short period. further stated that the interest rate fluctuations does affect the

long term maturity assets of the commercial banks as well hence profitability with a view

that whenever the general market interest rates falls the market value of longer assets with

fixed contractual terms will increase.

2.1.8 Limitations of Using Financial Ratios

Financial ratios have certain limitations in their use and are not meant to be applied as

definitive answers. They are usually used to provide additional details in the

determination of the results of financial and managerial decisions. They can provide clues

to the company‟s performance or financial situation.

However, on their own, they cannot explain whether performance is good or bad. As for

the external financial analysis, ratios also play a role of basic indicators, showing just an

overview of studying business entity. Ratios have to be interpreted carefully. Some of the

limitations about using ratios in financial analysis are Girmachew(2010).

15

Ratios with large deviations from the norm only indicate symptoms of a problem. It is

essential always to carry out additional analysis based on internal data to isolate the

causes of the problem. Ratio analysis just directs attention to potential weak spots. It does

not provide conclusive evidence and only shows the existence of a problem; there is

considerable subjectivity involved, as there is no “correct” number for the various ratios.

Further, it is hard to reach a definite conclusion when some of the ratios are favorable and

some are unfavorable;

Ratios may not be strictly comparable for different firms due to a variety of factors such

as different accounting practices or different fiscal year periods. Furthermore, if a firm is

engaged in diverse product lines, it may be difficult to identify the industry category to

which the firm belongs. Also, just because a specific ratio is better than the average does

not necessarily mean that the company is doing well; it is quite possible rest of the

industry is doing very poorly;

Ratios are based on financial statements that reflect the past and not the future. Unless the

ratios are stable, it may be difficult to make reasonable projections about future trends.

Furthermore, financial statements such as the balance sheet indicate the picture at “one

point” in time, and thus may not be representative of longer periods;

Financial statements provide an assessment of the costs and not value. For example, fixed

assets are usually shown on the balance sheet as the cost of the assets less their

accumulated depreciation, which may not reflect the actual current market value of those

assets;

16

Financial statements do not include all items. For example, it is hard to put a value on

human capital (such as management expertise). And recent accounting scandals have

brought light to the extent of financing that may occur off the balance sheet;

Results can be distorted by inflation, which can cause the book values of inventory and

depreciable assets to differ greatly from their true (replacement) values. Additionally,

inventory costs and depreciation write-offs can differ from their true values, thereby

distorting profits. Without adjustment, inflation tends to cause older firms (older assets) to

appear more efficient and profitable than newer firms (newer assets); « Difficulty to

decide the proper basis of comparison. The problem of standards of comparison is usually

an important case. It is also impossible to compile an industry wide averages or ratios that

serve as a useful standard to measure all firms; « The standard of comparison do not

consider the different technological, social, market, etc. , conditions of a company;

2.2 Empirical Literature

Summary of previous Empirical studies on financial performance analysis in the context

of different countries. This section gives a brief review of the previous studies made on

the determinants of bank financial performance from both developed and developing

countries.

The study in US by Bordeleau E., et al. (2010) presented The effect of liquid asset

holdings on U.S. and Canadian banks and the Results proposed that profitability is

improved for banks that hold some liquid assets, however, there is a place at which

holding further liquid assets minimize a banks‟ profitability, all else equal.

The Study in Australia by Olagunju, David and Samuel (2012) found out that there is a

positive significant relationship between liquidity and profitability. They concluded that

17

there is a bi-directional relationship between liquidity and profitability where the

profitability in commercial banks is significantly influenced by liquidity and vice-versa

The study in Swiss by Liu et al. (2010) stated that there is empirical evidence that

liquidity, measured by total loans to total assets, positively affects bank profitability.

Abreu and Mendes (2002) stated that liquidity is negatively affects bank profitability

measured by ROA, ROE and NIM Another determinant of profitability is the level of

operational efficiency.

The study in China by Heffernan and Fu (2010) seek to see the performance banks

between 1999 and 2006 and examine the determinants that affect the performance. The

findings show that NIM and Economic Value Added do better than Return on Average

Assets and Return on Average Equity. They also find that the type of bank is an

influential factor of bank profitability while bank size is not an influential factor. They do

not find any effect from the bank listing and the percentage of foreign ownership to

profitability.

The Study in India by Narang et al (2011), Chaudhry (2012), and Uppal et al (2012).

Have examined Indian banking system in terms of their performance and profitability.

And found that some banks achieved excellent performance with regard to index of

interest earned to total assets ratio.

The study in India by Chaudhary (2012) made an analysis of the performance of selected

public and private banks on the basis of parameters recommended in the CAMEL Model.

Researchers have taken various parameters to evaluate banks' performance such as

The Study in Australia by Olagunju, David and Samuel (2012) found out that there is a

positive significant relationship between liquidity and profitability. They concluded that

18

there is a bi-directional relationship between liquidity and profitability where the

profitability in commercial banks is significantly influenced by liquidity and vice-versa

The study in Swiss by Liu et al. (2010) stated that there is empirical evidence that

liquidity, measured by total loans to total assets, positively affects bank profitability.

Abreu and Mendes (2002) stated that liquidity is negatively affects bank profitability

measured by ROA, ROE and NIM Another determinant of profitability is the level of

operational efficiency.

The study in China by Heffernan and Fu (2010) seek to see the performance banks

between 1999 and 2006 and examine the determinants that affect the performance. The

findings show that NIM and Economic Value Added do better than Return on Average

Assets and Return on Average Equity. They also find that the type of bank is an

influential factor of bank profitability while bank size is not an influential factor. They do

not find any effect from the bank listing and the percentage of foreign ownership to

profitability.

The Study in India by Narang et al (2011), Chaudhry (2012), and Uppal et al (2012).

Have examined Indian banking system in terms of their performance and profitability.

And found that some banks achieved excellent performance with regard to index of

interest earned to total assets ratio.

The study in India by Chaudhary (2012) made an analysis of the performance of selected

public and private banks on the basis of parameters recommended in the CAMEL Model.

Researchers have taken various parameters to evaluate banks' performance such as

business per employee, profit per employee, total deposits, total advances, total

19

investment, total assets, total income, total expenditure and net profits. They suggested

that suitable and stringent efficient management information system should be developed.

The study in India by Uppal (2010) and Ramaratnam et al (2011) examined certain key

parameters to evaluate the performance of the Indian banks during the global financial

turmoil. Chaudhary et al (2011) made a comparative study of public and private sector

banks to evaluate their performance. They suggested that suitable and stringent efficient

management information system should be developed.

The studies in Pakistan by Khizer et al (2011), about banks‟ profitability, stated a

significant relation between asset management ratios, capital and economic growth and

with ROA, the operating efficiency, asset management and economic growth are

significant with the ROE. On the other hand, domestic banks are determined to have a

lesser capital adequacy ratio than foreign banks.

The study in Pakistan by SairaJavaid et.al (2011). examined the profitability of top 10 the

commercial banks for the period of 2004-2008.Pooled ordinary least square has been used

to check the impact of internal factors includes assets, loan, equity and deposits on the

profitability of banks on dependant variable called return on asset (ROA).The study found

that internal factors stated above effect the bank‟s profitability. Bank size or total assets

does not lead any profitability of commercial.

The study in Pakistan by Gul et al. (2011).Examined the relationship between bank

specific and macro-economic characteristics of bank profitability by using data of top

fifteen commercial banks over the period 2005-2009. They used the pooled Ordinary

Least Square (POLS) method to investigate the impact of assets, loans, equity, deposits,

economic growth, inflation and market capitalization on major profitability indicators i.e.,

20

return on asset (ROA), return on equity (ROE), return on capital employed (ROCE) and

net interest margin (NIM) separately. Stated that the empirical results have found strong

evidence that both internal and external factors have a strong influence on the profitability.

The study in Pakistan by Ali et al. (2011) conducted a comprehensive study about banks‟

profitability where they found significant relation between asset management ratio,

capital and economic growth and with ROA.

The study in Indonesia by Syafri (2012). Checked the profitability of the commercial

banks listed in the stock exchange for the period of 2002 to 2011 using pooling data from

commercial banks. He applied the pooling data regression model in which return on

assets is dependent variable and internal and external determinants have been used as

independent variables. He has said in his research that loan to total assets, total equity to

total assets have positive effect on profitability while on the other hand bank size and cost

to income ratio have negative effect and economic growth and non-interest income to

total assets have no effect.

The study in Iran by Yadollahzadehetal. (2013).Examine the effective factors on the

performance of commercial banks in for nine commercial banks during 2006- 2010 using

panel data regression method. They considered Return on asset and return on equity as

dependent variables which are separately examined by explanatory variables including

bank's size, gearing ratio, nonperforming loans, asset management, operating efficiency

and capital adequacy ratio. Their research results show that the variables of bank's size,

management efficiency and capital adequacy ratio have a positive effect on the

performance of commercial banks while the variables of operating efficiency, gearing

ratio and non-performing loans have a negative effect on the performance.

21

The study Iran by Shahchera M. (2012)presented the influence of liquid asset holdings on

Iranian banks profitability by using the Generalized Method of Moment (GMM), this

study analysed the profitability of listed banks using unbalanced panel data for the period

2002-2009, and used the liquidity asset and liquidity asset- square for estimating liquid

asset and profitability relationship. The estimated relationship between liquid assets and

bank profitability is as predictable. Coefficients for the liquid assets ratio, its square,

business cycle, regulation and its product of interaction business cycle and regulation are

all statistically significant. The study found evidence of a non‐linear relationship between

profitability and liquid asset holdings. A substantial result of this study is that the

business cycles significantly influence bank profits. The coefficient of regulation is

negative and significant.

The study in Saudi Arabia by Almumani (2014). The purpose of his study was to analyse

and compare the performance of Saudi banks that listed in stocks market for the period

2007-2011. The study was an evaluator in nature, drawing sources of information from

secondary data. The financial performance of banks is studied on the basis of financial

ratios and variables. Financial performance was measured by two approaches; trend

analysis and inter-firm analysis. It was found that increasing of assets, operating expenses,

and cost to income causes a decrease in Saudi bank‟s profitability, while increasing of

operating income causes an increase in the profitability of Saudi Banks. Analysis show

that all the variables of study have a positive mean value and all banks are generating

income. Saudi joint venture banks proved to be more proficient in generating profits,

absorbing loan losses and dominating in ROE, while, Saudi established banks have more

capacity of absorbing asset losses and dominating in ROA.

22

The study in Jordan by Abdelkarim Almumani (2013).Analysed the internal factors that

impact on the profitability of the commercial banks listed in Amman Stock Exchange for

the duration of 2005-2011.The study constitutes that the cost-income ratio has a

significant collide with the profitability of commercial banks.

The study in Jordan by Almazari (2011). attempted basically to measure the financial

performance of seven Jordanian commercial banks for the period 2005-2009, by using

simple regression in order to estimate the impact of independent variable represented by;

the bank size, asset management, and operational efficiency on dependent variable

financial performance represented by; return on assets and interest income size. It was

found that a bank with higher total deposits, credits, assets, and shareholders‟ equity does

not always mean that has better profitability performance. Also found that there exists a

positive correlation between financial performance and asset size, asset utilization and

operational efficiency, which was also confirmed with regression analysis that financial

performance is greatly influenced by these independent factors.

The study in Malaysia by Masood and Ashraf (2012). Conducted a study on determinants

of Islamic banks on panel countries data. The results of study signified that larger assets

size banks lead to higher profitability and management efficiency can work for better

return on assets (ROA). The efficiency of management for effective running of operating

expenses effect bank profitability significantly and positively.

The study in Palestinian by Alkhatib (2012). empirically examined the financial

performance of five commercial banks listed on Palestine securities exchange(PEX).to

assess the financial performance of Palestinian commercial banks, Alkhatib(2012)

developed 3 models; each consists of one dependent variable and 4 identical independent

23

variables. He used ROA as an internal financial performance indicator the Tobin‟s Q

model (price/book) as a market financial performance indicator and finally the economic

value added as an economic financial performance indicator. Bank size, credit risk,

operational efficiency and asset management were used as independent variables. The

study employed the correlation and multiple regression analysis of annual time series data

from 2005-2010.the result of the research reveal that, bank size and asset management

were positively related with ROA but credit risk and operational efficiency were

negatively correlated with ROA under the first model. Under the second model both bank

size and asset management were positively correlated whereas credit risk and operational

efficiency is negatively correlated with the market performance of banks measured by

Tobin‟s Q. under the third model that is the model which use economic performance of

banks measured by EVA, except operational efficiency, bank size, credit risk and asset

management ratio were positively correlated with EVA.

The study in Malaysia by Asma et al., (2011). Reviewed the profitability determinants of

Islamic banks in Malaysia. The bank-specific determinants such as bank size, liquidity,

capital adequacy, expense management and credit risk effect were went through and

found that the only bank size statistically affects the Islamic banks profitability in

Malaysia.

The study in Malaysian by Lamarana (2012).Examined the performance of the local

banks and foreign banks and compares their profitability in the financial sector. This

comparative study aims to investigate the factors influencing bank profitability in for the

period 2005-2011 covering 16 major commercial banks (8 locally owned and 8 foreign

owned).he use ROA and ROE as a dependent variable. On the other hand, capital

24

adequacy, asset quality, management efficiency, liquidity and bank size are the

independent variables. The researcher use regression analysis to the panel data. The

comparison between the two categories of ownership indicates that foreign banks are

more profitable than domestic banks.

The Study in South Africa by Kumbirai, and Webb (2010) investigated the performance

of South Africa‟s commercial banking sector for the period 2005- 2009. Financial ratios

are employed to measure the profitability, liquidity and credit quality performance of five

large South African based commercial banks. The study found that overall bank

performance increased considerably in the first two years of the analysis. A significant

change in trend is noticed at the onset of the global financial crisis in 2007, reaching its

peak during 2008-2009. This resulted in falling profitability, low liquidity and

deteriorating credit quality in the South African Banking sector.

The study in Nigeria by Uremadu S. (2012), presented the effect of bank capital structure

and liquidity on profitability using Nigerian data during the period from1980 to 2006

studied is the data were analysed using descriptive statistics and the auto-regressive

distributed lag (ADL) model. The study practised data on an OLS methodology that

incorporated unit root tests for stationary and co- integration. The study found a positive

impact of cash reserve ratio, liquidity ratio and a negative effect of bank credits to the

domestic economy, savings deposit rate, gross national savings (proxy for deposits with

the central bank), balances with the central bank, inflation rate and foreign private

investments, on banking system profits. They equally noticed that liquidity ratio drive

banks‟ profits in Nigeria, closely followed by balances with the central bank and then,

gross national savings and foreign private investments, followed case in that order.

25

The study in Nigeria by Adebayo O. et al. (2011) stated that the point to which effective

liquidity management impacts profitability in commercial banks and how commercial

banks can stimulate their liquidity and profitability situation by using quantitative

methods of research. Many findings were reaching through the analysis of both the

structured and unstructured questionnaire on the management of banks and the financial

reports of the tested banks. The data obtained from the Primary and Secondary sources

were analysed through collection, sorting and grouping of the data in tables of

percentages and frequency distribution. The hypothesis was statistically tested through

Pearson correlation data analysis. Findings indicated that there is significant relationship

between liquidity and profitability. That means profitability in commercial banks is

significantly influenced by liquidity and vice versa. The study concluded that for the

prosperity of operations and survival, commercial banks should not expose efficient and

effective liquidity management and that both illiquidity and excess liquidity are "financial

diseases" that can simply wear out the profit rule of a bank as they affect banks in order to

arrive high profitability level.

The study in Nigeria by Saleem Q., et al. (2011). Presented the relationship between

liquidity and profitability and results revealed that there is a significant impact of only

liquid ratio on ROA.

The study in Ghana by Lartey V., et al. (2013) stated the relationship between the

liquidity and the profitability of banks listed on Ghana Stock Exchange is presented.

Seven out of the nine listed banks were involved in the study. The study was descriptive

in nature. It used the longitudinal time dimension, specifically, the panel method.

26

Document analysis was the main research procedure used to collect secondary data for

the study. The financial reports of the seven listed banks were studied and relevant

liquidity and profitability ratios were computed. The trend in liquidity and profitability

were determined by the use of time series analysis. The main liquidity ratio was regressed

on the profitability ratio. It was revealed that for the period 2005-2010, both the liquidity

and the profitability were dropping. It was also revealed that there was a very weak

positive relationship between the liquidity and the profitability of the listed banks in

Ghana.

The study in Ghana by Karkrah and Ameyaw (2010) on profitability determinants of

commercial banks revealed that the equity ratio which is the measure of the capital

strength of the banks posted a positive relation with the banks ROA. They documented

that their finding is in line with the findings of Suffian et al (2008) which reveals positive

relation between Philippines banks level of capitalization and profitability. The result was

also consistent with the finding of Berger (1995), Demirguc-Kunt and Huizinga (1999),

Pasiouras and Kosmidou (2007). Capital ratio was presented in Devinaga Rasiah (2010)

study as (CTRA) Capital and reserve as a percentage of total assets.

The study in Ghana by Devinaga Rasiah (2010) asserted that the lower returns on liquid

assets and excessive fund which has not been invested may also negatively affect the

profitability of banks. And because of this, liquidity management serves as an important

determinant of commercial bank profitability. It may not be prudent for commercial

banks to hold huge amount of an idle funds because it deprive the banks of income and

profitability. This is because the more the banks turn funds into loans or invest them the

27

more its accumulate income and profit. This has been confirmed by the study of

Eichengreen& Gibson (2001) which documented that the fewer the amount of funds tied

up in liquid investment and the liquid assets the higher the profitability.

The study in Ghana by Karkrah and Ameyaw (2010) supported by the empirical findings

which revealed that non-interest income is an important driver of commercial banks

profitability and there is a positive relationship existing between non-interest income and

profitability in the Ghanaian banking sector. However P. I. Vong et al (2009) cited in

their study that the findings of Gischer and Juttner (2001) prove that non-interest income

generating services impact negatively on commercial banks‟ profitability. According to

them, Gischer and Juttner (2001) claim that the negative relationship exhibited by their

observation is attributed to the fact that the non-income generating services are more

prone to intense competition than the traditional income activities of the banks.

The study in Ghana by Karkrah and Ameyaw (2010) on profitability determinants of

commercial banks revealed that the equity ratio which is the measure of the capital

strength of the banks posted a positive relationship with the banks ROA which was in line

with the study of Suffian et al (2008) which as well revealed positive relation existing

between Philippines banks level of capitalization and profitability.

Study in Ghana by Karkrah and Ameyaw (2010) revealed that non-interest income is an

important driver of commercial banks profitability and there is a positive relationship

existing between non-interest income and profitability in the Ghanaian banking sector.

The study in Kenya by Okothetal. (2013) studies the Determinants of Financial

Performance of Commercial Banks. The authors used linear multiple regression model

28

and Generalized Least Square on panel data to estimate the parameters. Stated that bank

specific factors significantly affect the performance of commercial banks in Kenya,

except for liquidity variable.

The study in Tanzania by Srinivas, Madishetti et.al (2013). analysed the profitability

determinants of commercial banks for the period of 2006-2012.Internal determinants use

the variables like liquidity risk, credit risk, operating efficiency, business assets and

capital adequacy. All of these variables are independent. The study found that internal

variables determine the bank‟s profitability commercial banks.

The study of Frederic (2014) examined the factors responsible for determining the

performance of domestic commercial banks in Uganda. The study used linear multiple

regression analysis over the period 2000-2011 to analyse the data of all licensed domestic

and foreign commercial banks. The study found that, management efficiency; asset

quality; interest income; capital adequacy and inflation influence on the bank‟s

performance in Uganda.

2.3 Critical Review and Research Gap identification

The analysis of financial performance, particular in commercial banks is well researched

and they received increased attention. From the above review of empirical works, it is

clear that different authors have approached financial performance of banks in different

ways in varying levels of analysis. These different approaches helped in the emergence of

more and more literature on the subject over time. It gives an idea on extensive and

diverse works on financial performance of banks. It has been noticed that the studies

financial performance of banks in various aspects provide divergent results relating to the

study period overlap or coincide. The main reason for divergence in the results is use of

different method for the measurement of financial performance of banks and its

29

determinants. All the studies aimed to analyze the financial performance of listed

Financial Institutions in Rwanda with number of elements from Financial Statements and

Management Efficiency.

To the best of my knowledge the relationship between financial statements and financial

performance analysis pre-post listing banks in Rwanda has not yet been studied.

Therefore, this research will bridge the existing literature by showing the relationship

between financial statement and financial performance and compare the period before and

after listing on Rwanda Stock Exchange (RSE) and provide the information, knowledge

and identify the gap that the researcher left out in the area of research which will help to

determine the impact of listing to the financial performance for Rwanda Commercial

banks. In this study, the major area is to disclose the financial performance related to BK

before and after listing on Rwanda Stock Exchange (RSE). Therefore, this topic may be

new as well as the researches efforts may be appreciable.

2.4 Theoretical framework

The theoretical framework gives the meaning of a word in terms of the theories on

financial statement such as proprietary, theory, entity theory, DuPont mean- variance of

portfolio investment theory and the modern portfolio theory. It assumes both knowledge

and acceptance of the theories that this research work depends upon.

Proprietary theory

In the proprietary view, the assets are considered the proprietors‟ assets, and the liabilities

are the proprietors‟ liabilities. According to Newlove and Garner (1951) under proprietary

theory “liabilities are negative assets-negative properties, which must be sharply defined

and separated in the accounting process. Revenues are increases in proprietorship and

expenses are decreases. Net profits, the excess of revenues over expenses, accrues

30

directly to the owners; it represents an increase in the wealth of the proprietors.

(Hendriksen and Van Breda, 1992) Staubus (1959) narrowed the concept of owners to

common stockholders and considered preference shareholders as liability holders and

stressed the importance to investors of the estimation of future cash receipts.

The proprietary approach represents an agency view of the company where the main

responsibility of management is to manage the firm in the best interests of the owners. As

the assets and liabilities are considered the owners‟ assets and liabilities, the

maximization of profits equals maximization of the increase in the shareholders‟ net

assets. For this reason, the asset/liability approach to income determination, where

income is the by-product of the valuation of assets and liabilities, is the most direct way

of quantifying the increase in net assets. Under both the proprietary theory and the

asset/liability approach to income determination, it is imperative that shareholders‟

interests are sharply distinguished from the interests of the providers of debt capital in

order to be able to measure the increase in net assets by Hendriksen (1965).

Entity theory and enterprise or social theory

Under the entity view, transactions are analysed as to their effect on the accounting entity.

Financial statements are prepared from the viewpoint of the entity. The income statement

is meant to calculate income for distribution and analyse the company‟s performance over

a period, whereas the balance sheet serves to indicate the security or riskiness of the

company‟s financial position.

Entity theory views the entity as “having a separate existence – an arm‟s length

relationship with its owners. The relation to the owners is regarded as not particularly

different from that to the long-term creditors. Lorig, (1964). Suojanen (1954)‟s enterprise

31

or social theory sees the large listed corporation as an institution with social

responsibilities. Companies‟ actions affect many different stakeholders such as

stockholders, creditors, customers, employees, the government as a taxing and regulatory

authority and the public at large. Hendriksen and Van Breda, (1992); Kam, (1990);

Suojanen, (1954) .traces this institutionalization of the large enterprise to the separation of

management and ownership leading to increasingly large proportions of income being

retained within the company to reduce the corporation‟s dependence on external

financing. Large corporations may decide to pay only „conventionally adequate dividends‟

because this ties in with their survival and growth objectives. Suojanen, (1958).

Financial reports according to the enterprise theory are to be prepared from the

perspective of the enterprise as a social institution. Income generated by the enterprise is

analysed to measure the contribution of the enterprise to society using the concepts

developed in national income analysis. Therefore, ultimately, the balance sheet is

secondary to output, income and value added considerations. The balance sheet equation

expressing the enterprise theory according to Meyer (1973).

Suojanen,(1958).Proposes that large companies prepare a value added statement in

addition to the balance sheet and income statement. “If the enterprise is considered to be

an institution, its operations should be assessed in terms of its contribution to the flow of

output of the community. Suojanen, (1954) “Although stockholders have legal rights as

owners, from the point of view of the enterprise their rights are subsidiary to the

organization and its survival.” Kam, (1990).

Financial ratios analysis using the modified DuPont model

Measuring and analysing the ratios that provide a clear picture of a banks‟ financial

position is becoming more and more important, most notably when efforts to preserve

financial stability are at the fore. Furthermore, a preliminary analysis of the financial

32

indicators gives a picture of the banking sector and can highlight weaknesses which could

reveal themselves in the future.

Cole (1972) was the first that adapted and applied the DuPont model for banks. The

banking system operates like any other industry in a regulated, supervised and