Embed Size (px)

Citation preview

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 1 Knowledge-Based Audits of Governmental Entities

FINANCIAL STATEMENT PRESENTATION AND DISCLOSURES CHECKLIST

Beginning of Form PURPOSE This form has been designed to help the auditor determine whether the financial statements include the presentations and disclosures required by generally accepted accounting principles in regards to government-wide and fund financial statements as well as management’s discussion and analysis (MD&A) and other required supplementary

information. INSTRUCTIONS This checklist is intended to be used as a guide for determining whether the financial statements of general-purpose state and local government entities include the primary presentation and disclosure requirements of accounting principles generally accepted in the United States of America (U.S. GAAP). This checklist is not designed for special-purpose governments such as risk entity pools or pension or other postemployment benefit plan financial statements. The form is current through GASB Statement No. 82, Pension Issues - An amendment of GASB Statements No. 67, No. 68, and No. 73 as well as the GASB Implementation Guide Update 2016-1 . Most of the questions addressed in this checklist refer to specific authoritative literature and may use the following acronyms:

GASB—Governmental Accounting Standards Board Statement GASB Cod. Sec.—Governmental Accounting Standards Board Codification of Governmental Accounting

and Financial Reporting Standards GASBI—Governmental Accounting Standards Board Interpretation GTB—Governmental Accounting Standards Board Technical Bulletin GCON—Governmental Accounting Standards Board Concepts Statement NCGA—National Council on Governmental Accounting NCGAI—National Council on Governmental Accounting Interpretation AAG-SLG— AICPA Audit and Accounting Guide, "State and Local Governments" AAG-SLA— AICPA Audit Guide “Government Auditing Standards and Circular A-133 Audits” SAS—AICPA Statement on Auditing Standards AU-C (or AU)—Statement on Auditing Standards, Professional Standards, published by the AICPA CON—Financial Accounting Standards Board Concepts Statement

Some of the questions included in the checklist do not refer to any specific authoritative literature. Nevertheless, the disclosure items they address are considered informative disclosures for users of the financial statements and usually are disclosed. These disclosures are generally accepted by accountants and auditors and, accordingly, are referenced as “Generally Accepted Practice” in this checklist. The auditor should review the topics within the table of contents for possible disclosures. For each topic that is applicable, the auditor should then select “Item Present;” otherwise, he or she should select “Item Not Present.” For each topic marked “Item Present,” the auditor should complete the individual checklist items by selecting “Yes,” “No,” or “N/A” (not applicable). Any item marked “No” should be explained in the checklist or in a separate memorandum. For topics marked “Item Not Present,” individual checklist items will not be shown.

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 2 Knowledge-Based Audits of Governmental Entities

FINANCIAL STATEMENT PRESENTATION AND DISCLOSURES CHECKLIST

Purpose and Instructions

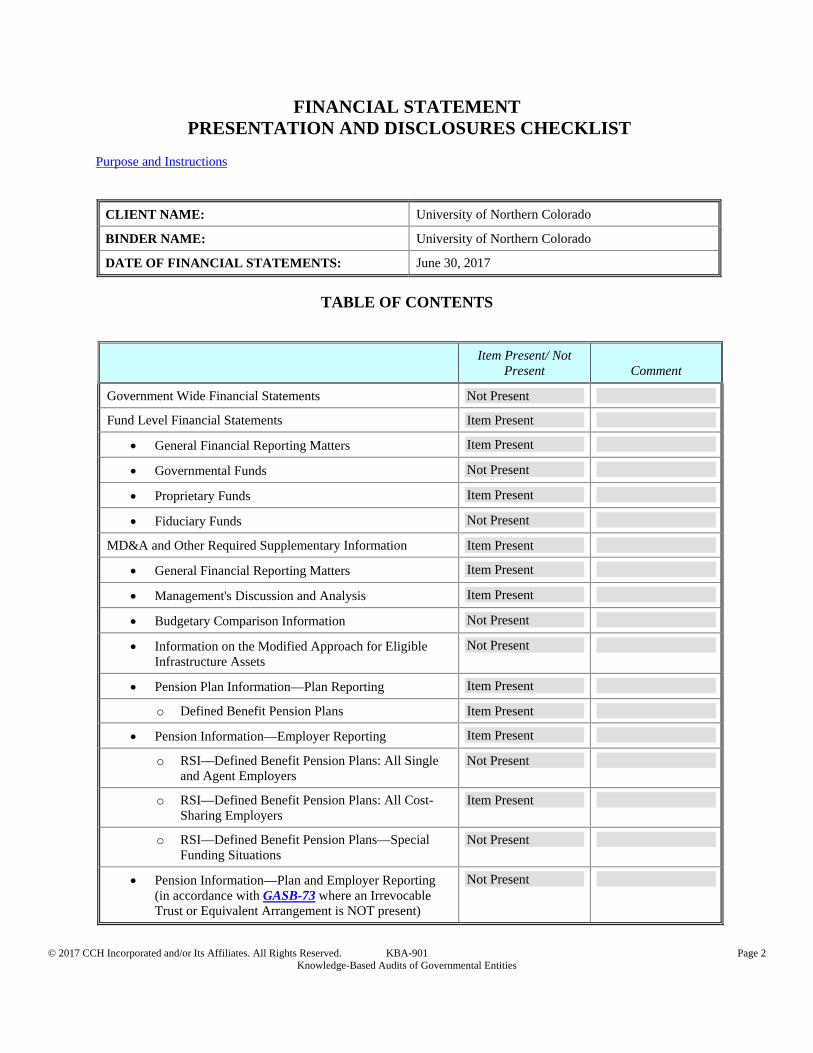

CLIENT NAME: University of Northern Colorado

BINDER NAME: University of Northern Colorado

DATE OF FINANCIAL STATEMENTS: June 30, 2017

TABLE OF CONTENTS

Item Present/ Not

Present Comment

Government Wide Financial Statements Not Present

Fund Level Financial Statements Item Present

General Financial Reporting Matters Item Present

Governmental Funds Not Present

Proprietary Funds Item Present

Fiduciary Funds Not Present

MD&A and Other Required Supplementary Information Item Present

General Financial Reporting Matters Item Present

Management's Discussion and Analysis Item Present

Budgetary Comparison Information Not Present

Information on the Modified Approach for Eligible Infrastructure Assets

Not Present

Pension Plan Information—Plan Reporting Item Present

o Defined Benefit Pension Plans Item Present

Pension Information—Employer Reporting Item Present

o RSI—Defined Benefit Pension Plans: All Single and Agent Employers

Not Present

o RSI—Defined Benefit Pension Plans: All Cost-Sharing Employers

Item Present

o RSI—Defined Benefit Pension Plans—Special Funding Situations

Not Present

Pension Information—Plan and Employer Reporting (in accordance with GASB-73 where an Irrevocable Trust or Equivalent Arrangement is NOT present)

Not Present

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 3 Knowledge-Based Audits of Governmental Entities

Item Present/ Not

Present Comment

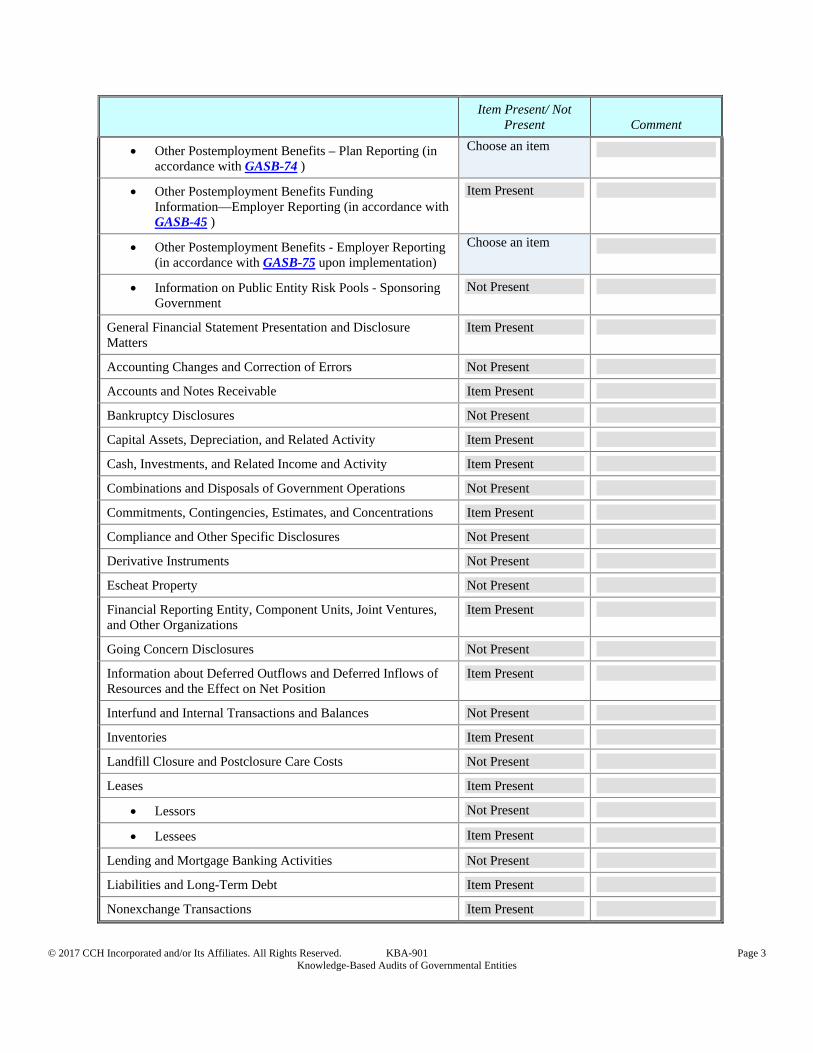

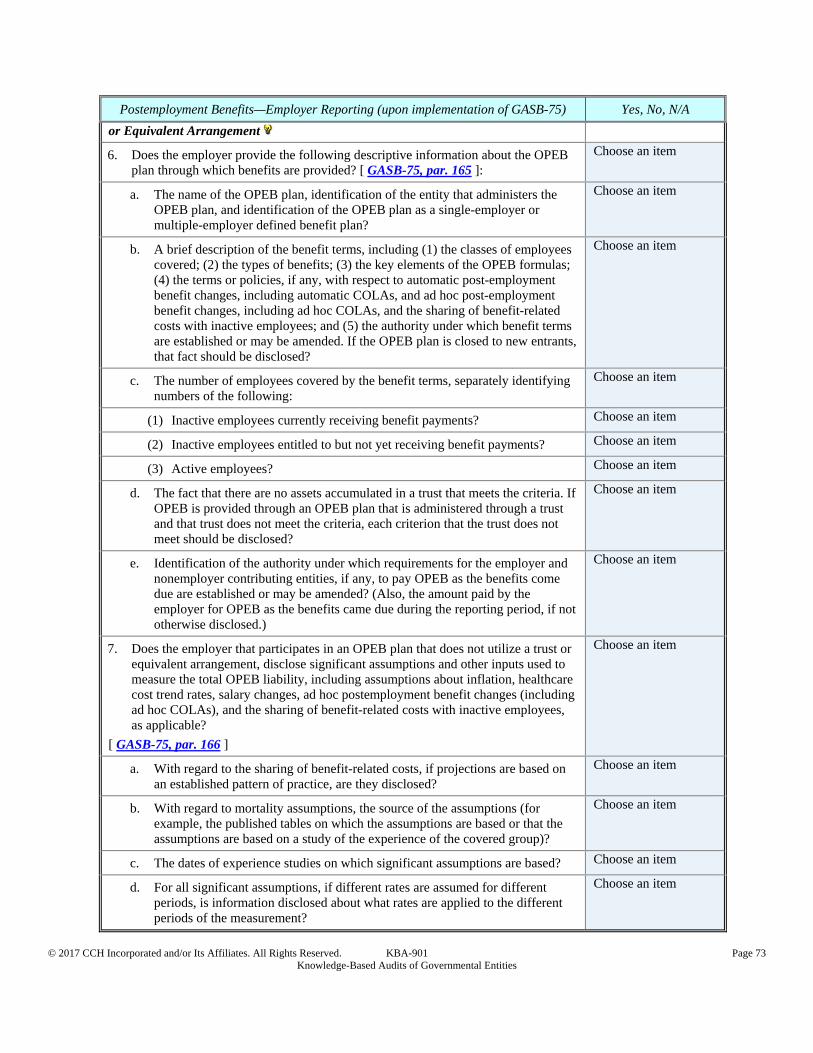

Other Postemployment Benefits – Plan Reporting (in accordance with GASB-74 )

Choose an item

Other Postemployment Benefits Funding Information—Employer Reporting (in accordance with GASB-45 )

Item Present

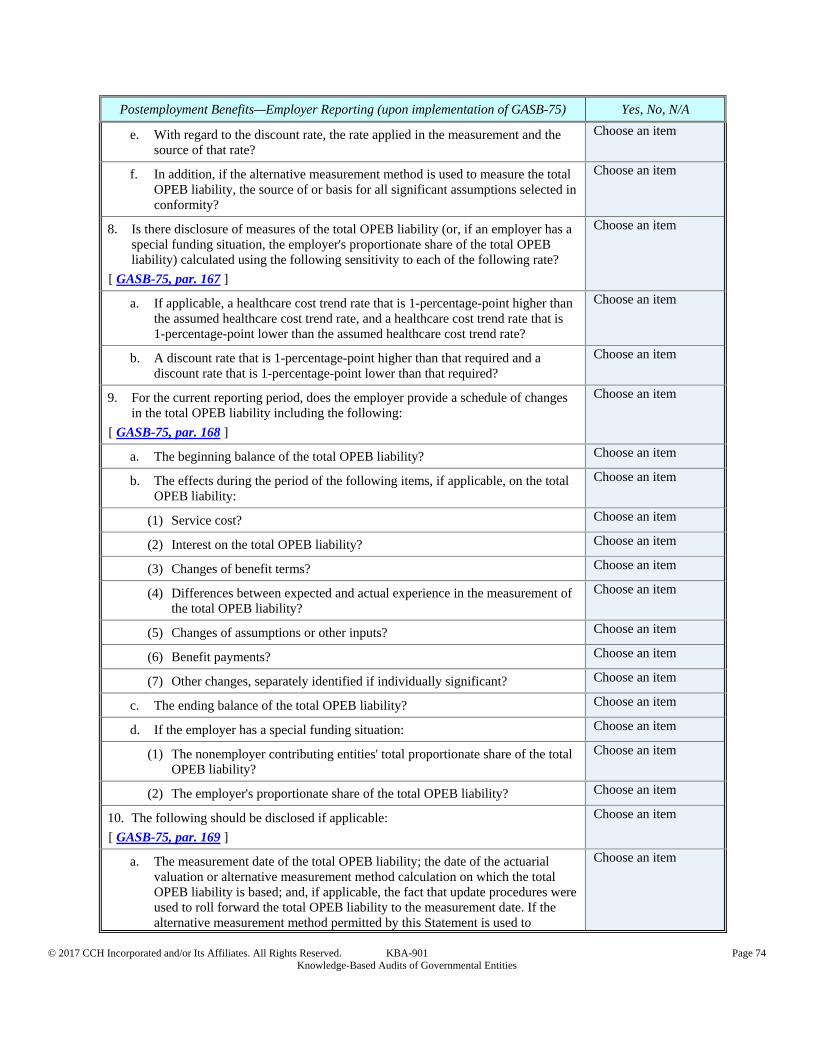

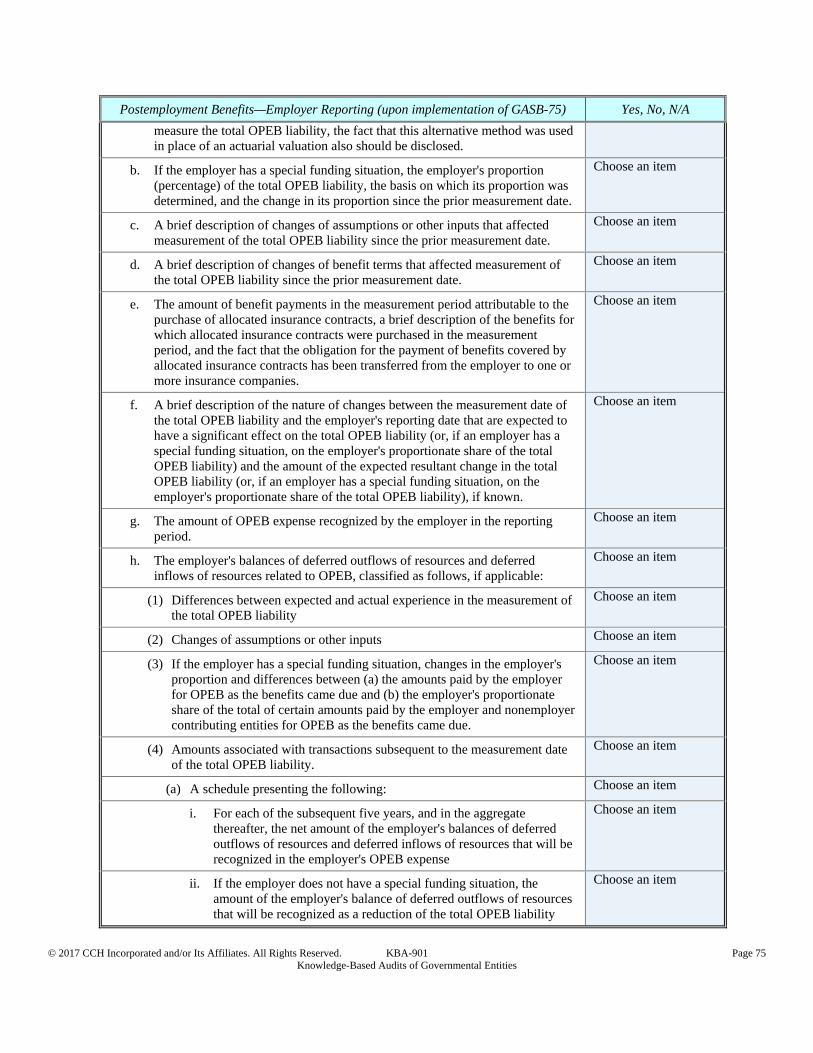

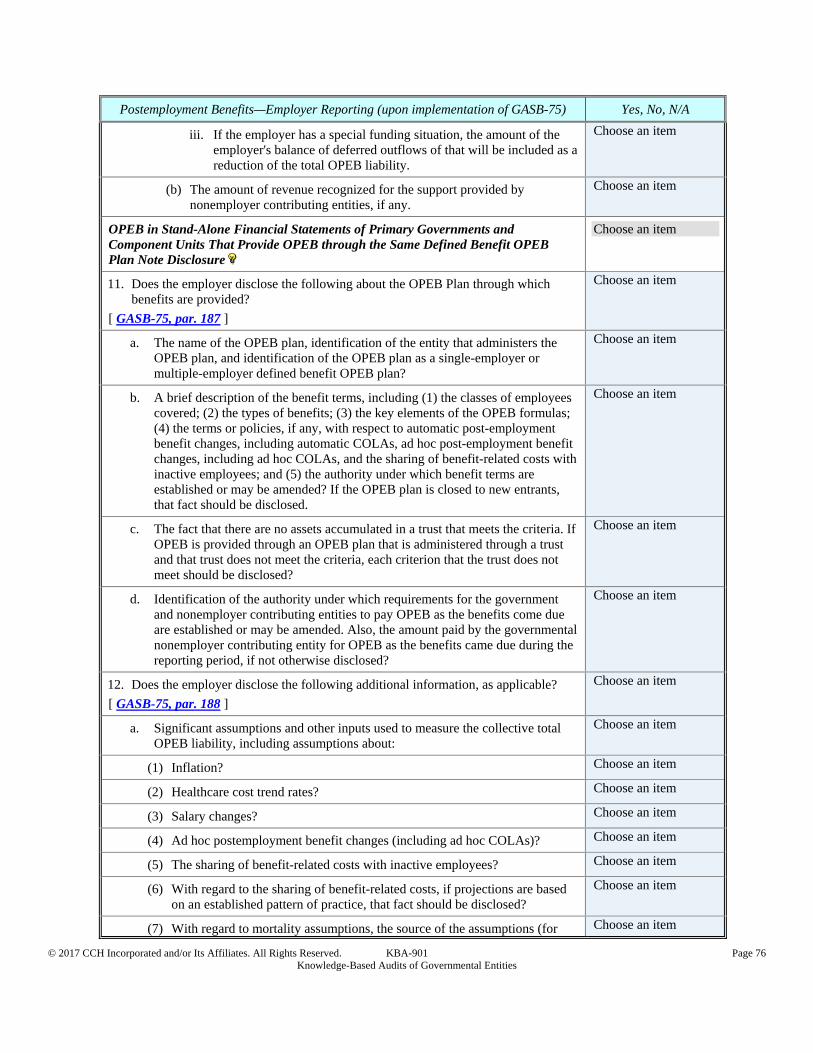

Other Postemployment Benefits - Employer Reporting (in accordance with GASB-75 upon implementation)

Choose an item

Information on Public Entity Risk Pools - Sponsoring Government

Not Present

General Financial Statement Presentation and Disclosure Matters

Item Present

Accounting Changes and Correction of Errors Not Present

Accounts and Notes Receivable Item Present

Bankruptcy Disclosures Not Present

Capital Assets, Depreciation, and Related Activity Item Present

Cash, Investments, and Related Income and Activity Item Present

Combinations and Disposals of Government Operations Not Present

Commitments, Contingencies, Estimates, and Concentrations Item Present

Compliance and Other Specific Disclosures Not Present

Derivative Instruments Not Present

Escheat Property Not Present

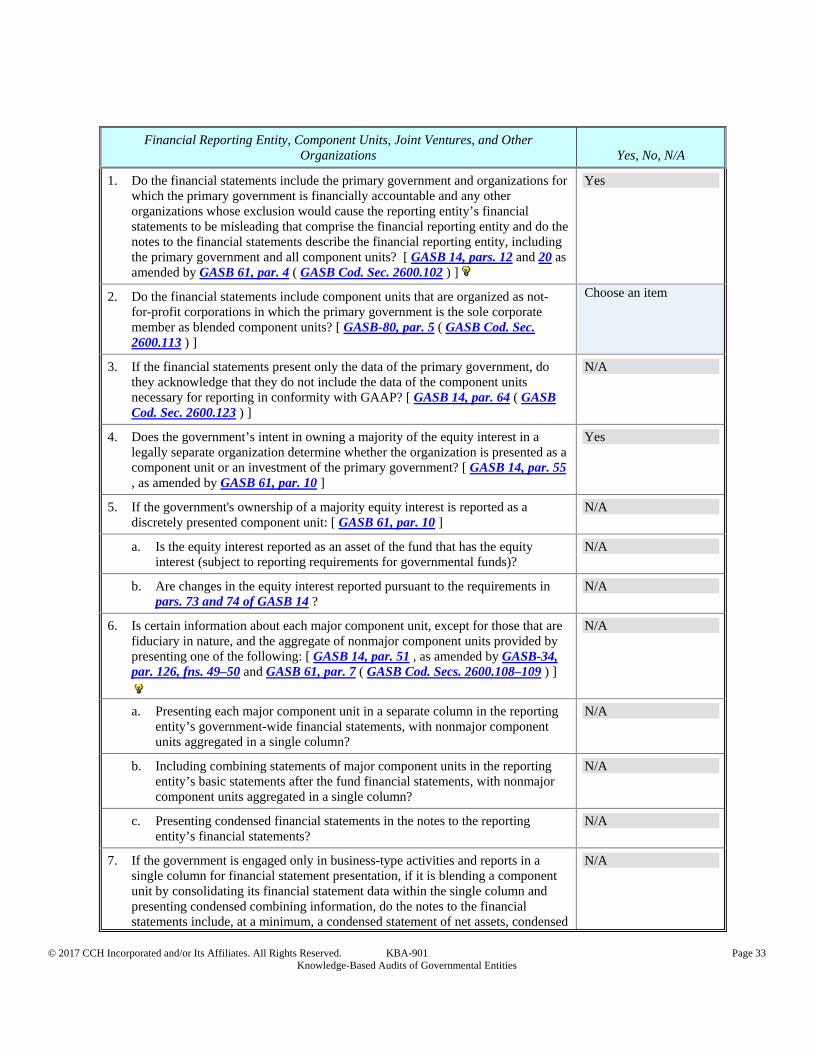

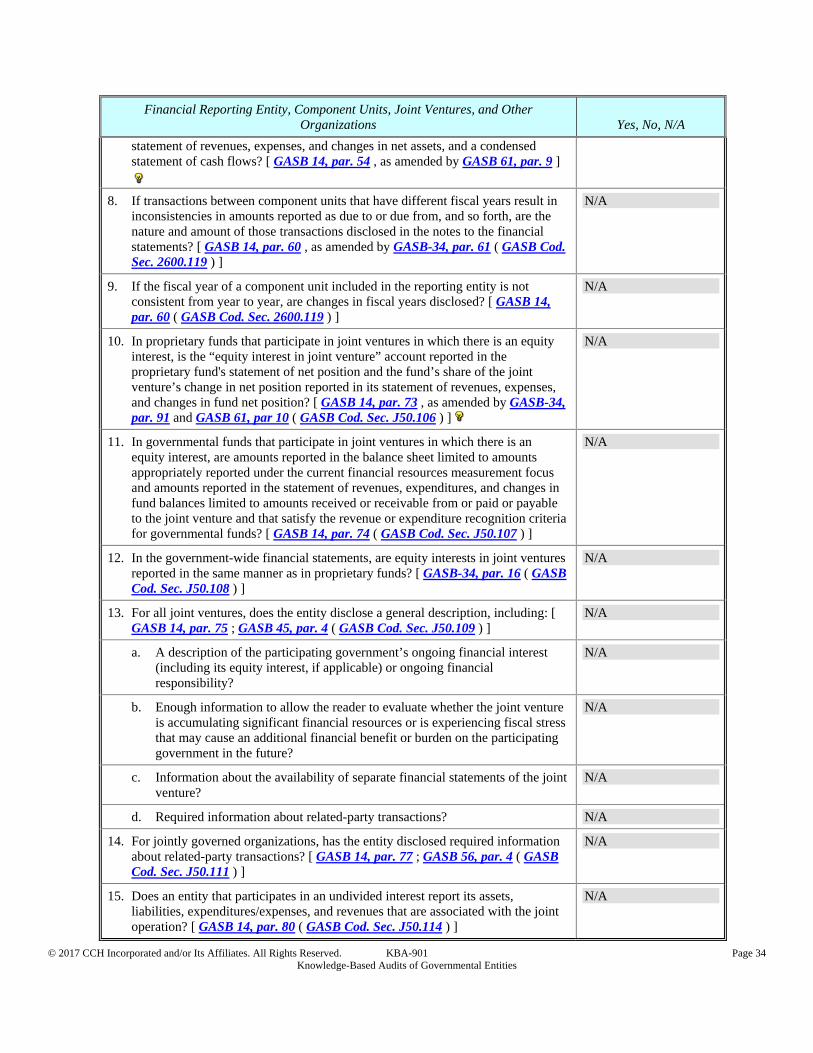

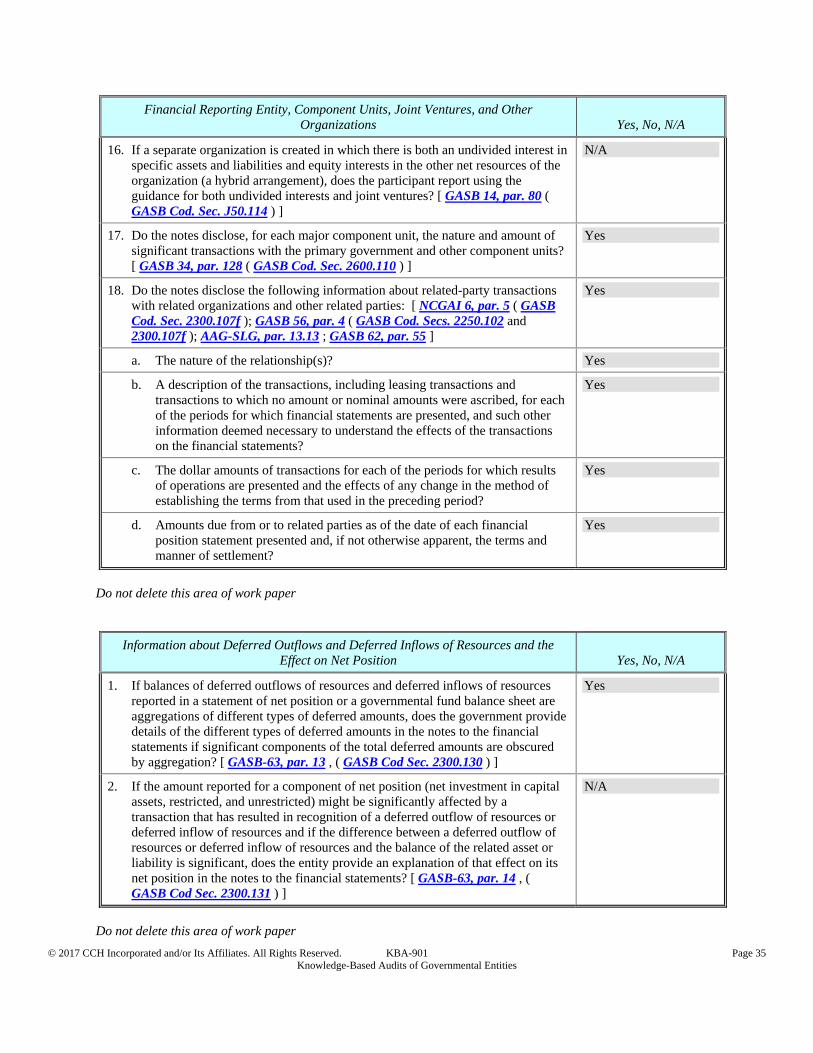

Financial Reporting Entity, Component Units, Joint Ventures, and Other Organizations

Item Present

Going Concern Disclosures Not Present

Information about Deferred Outflows and Deferred Inflows of Resources and the Effect on Net Position

Item Present

Interfund and Internal Transactions and Balances Not Present

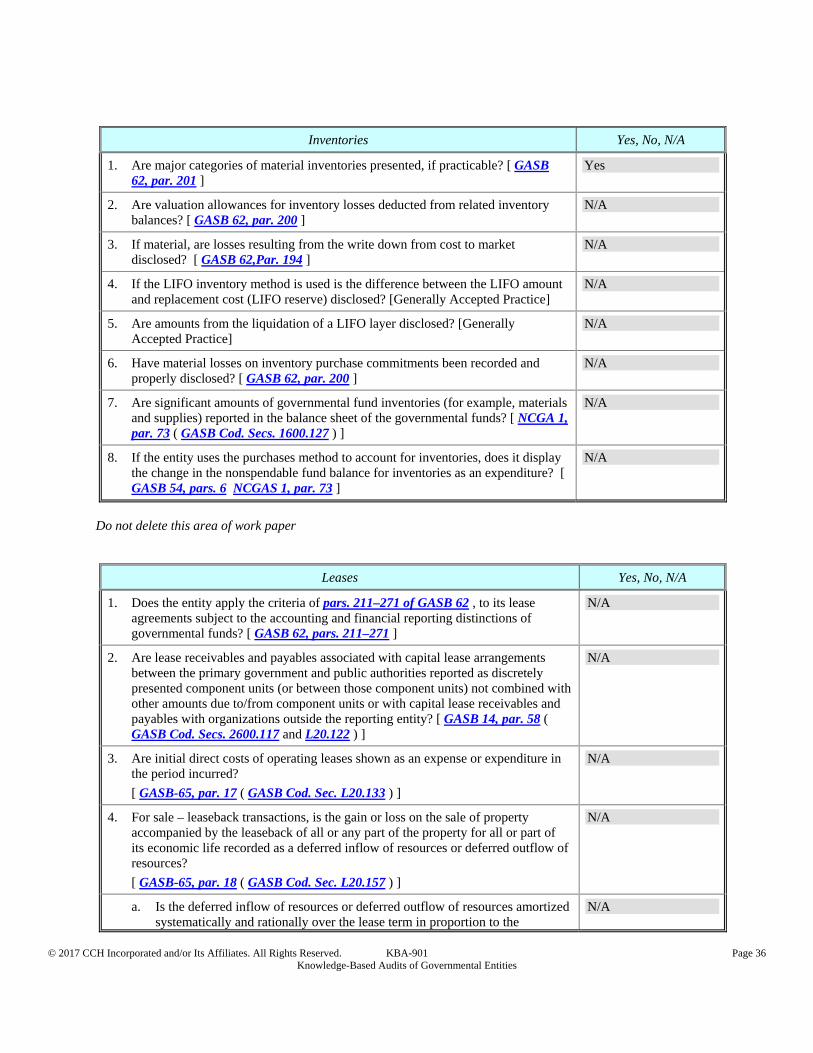

Inventories Item Present

Landfill Closure and Postclosure Care Costs Not Present

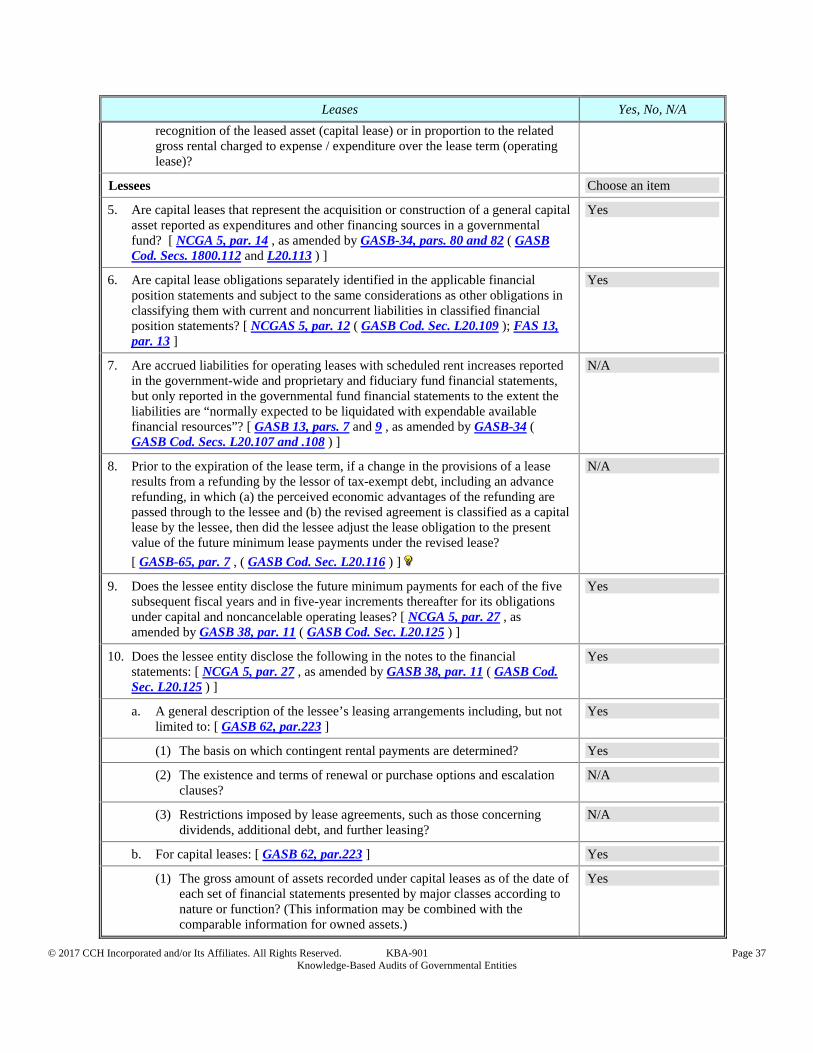

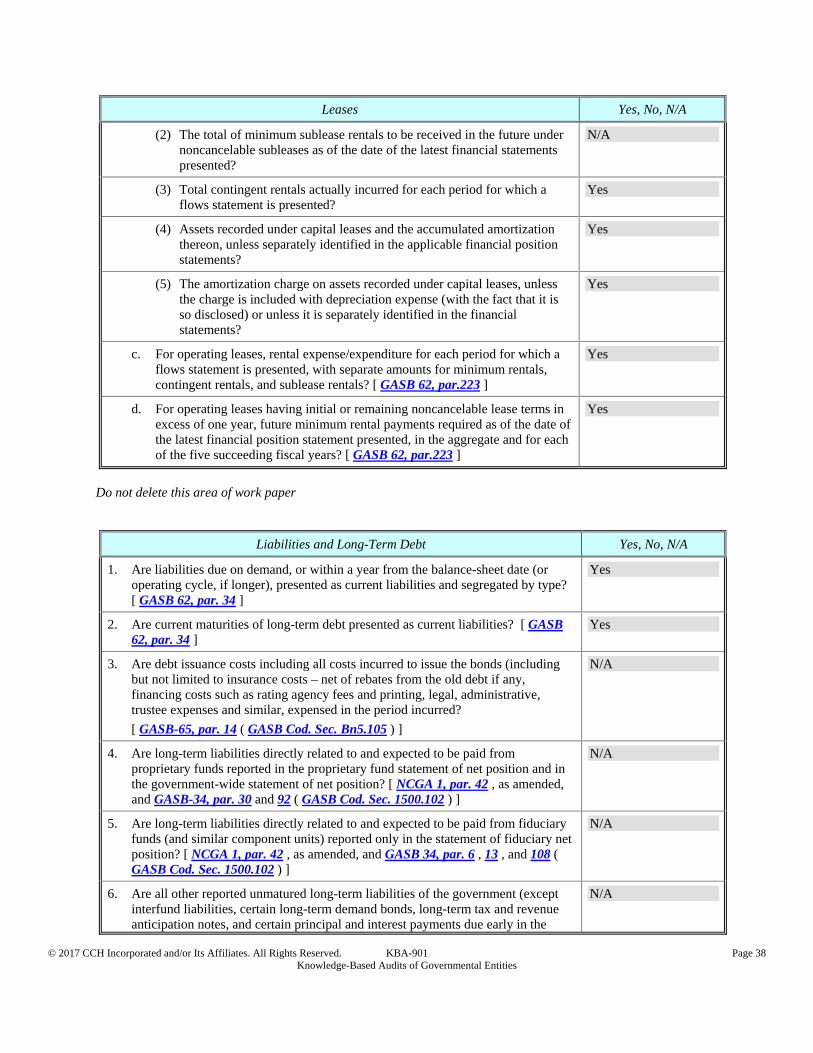

Leases Item Present

Lessors Not Present

Lessees Item Present

Lending and Mortgage Banking Activities Not Present

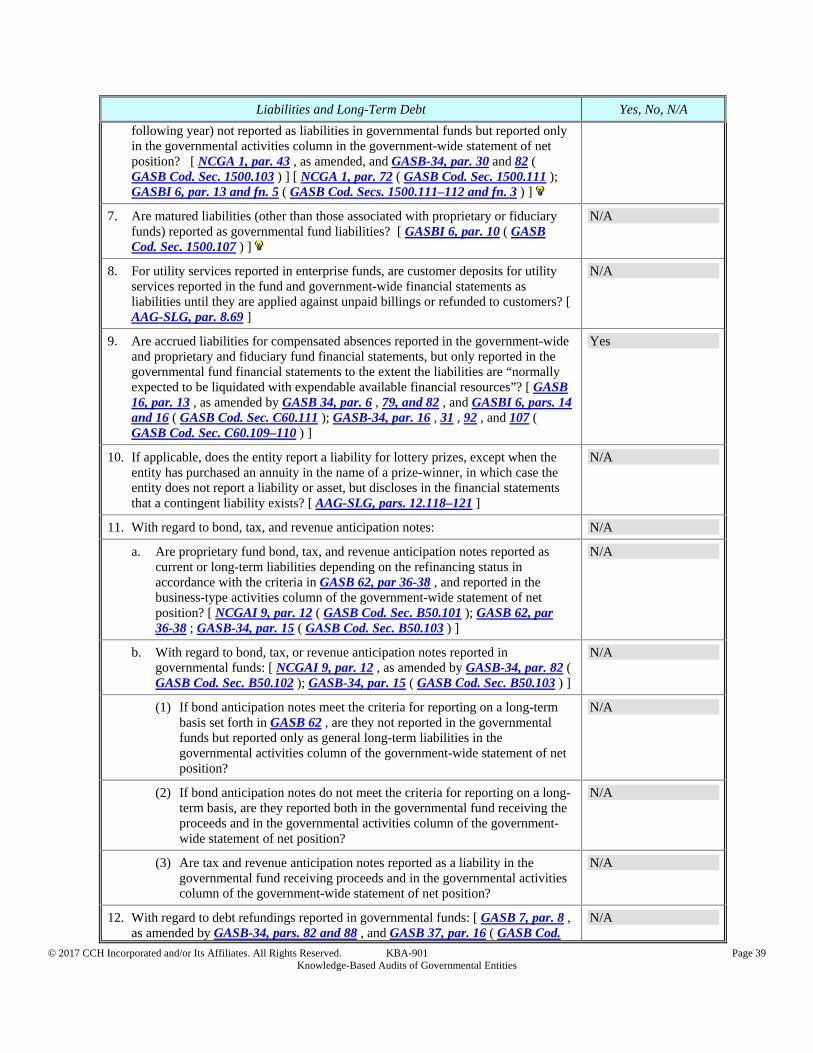

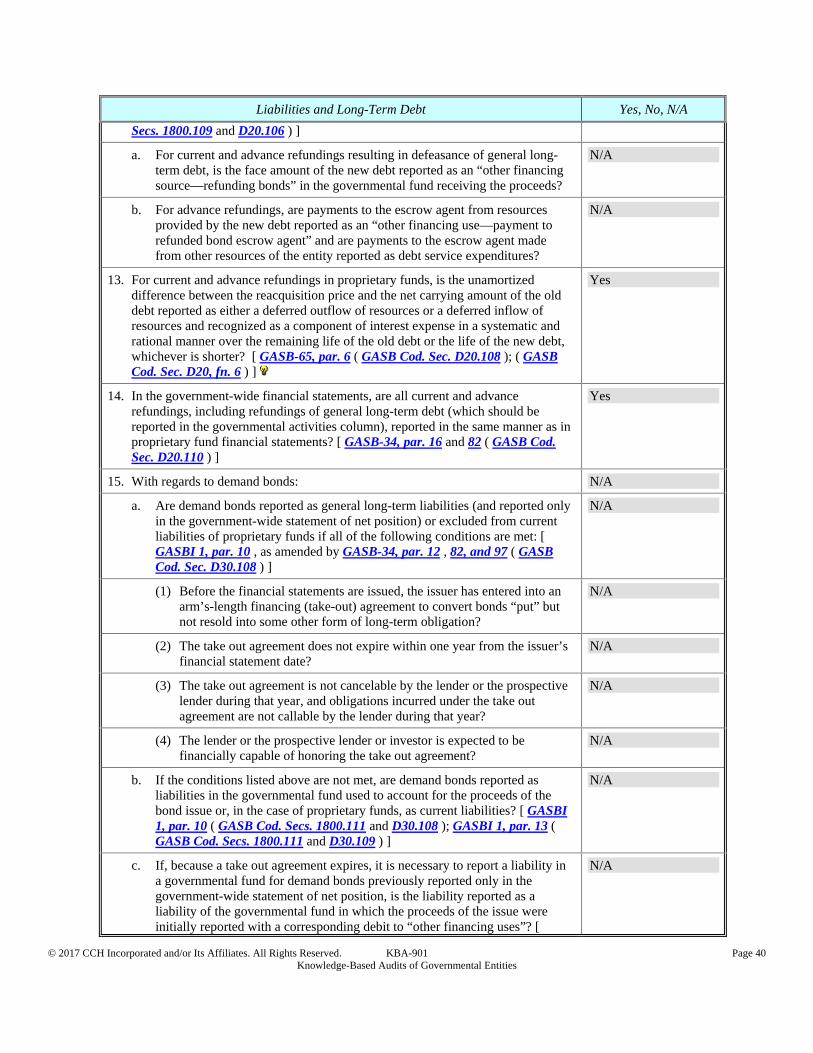

Liabilities and Long-Term Debt Item Present

Nonexchange Transactions Item Present

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 4 Knowledge-Based Audits of Governmental Entities

Item Present/ Not

Present Comment

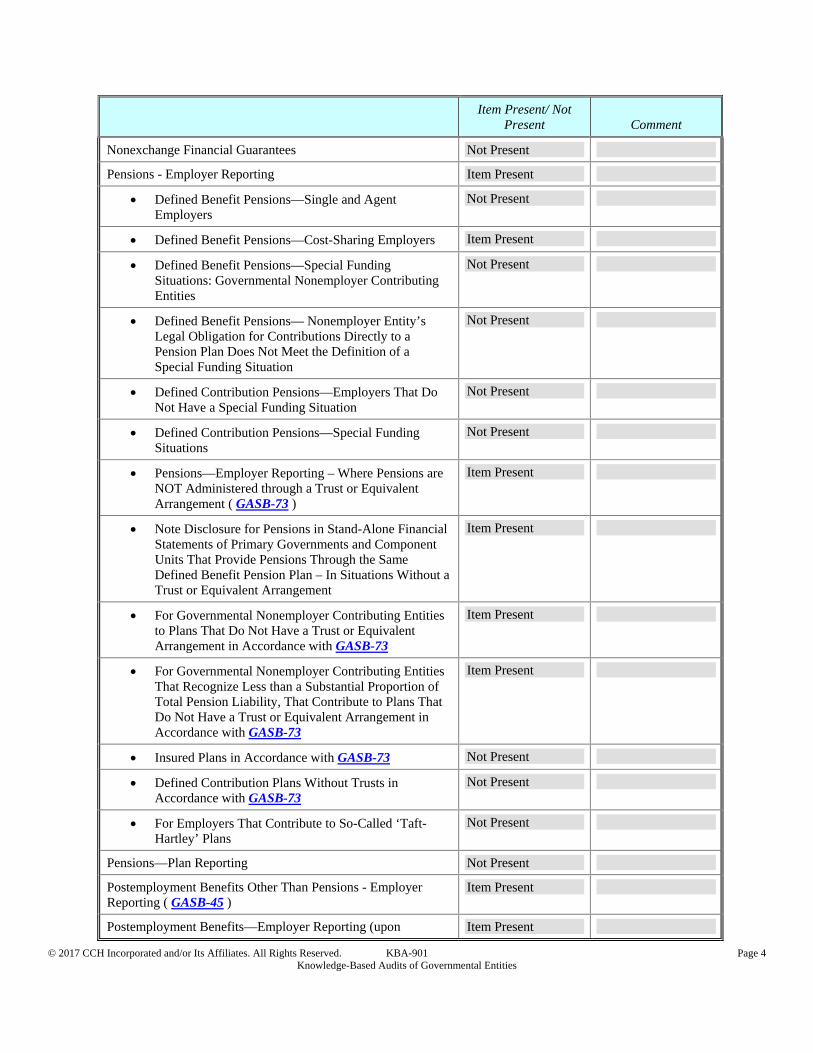

Nonexchange Financial Guarantees Not Present

Pensions - Employer Reporting Item Present

Defined Benefit Pensions—Single and Agent Employers

Not Present

Defined Benefit Pensions—Cost-Sharing Employers Item Present

Defined Benefit Pensions—Special Funding Situations: Governmental Nonemployer Contributing Entities

Not Present

Defined Benefit Pensions— Nonemployer Entity’s Legal Obligation for Contributions Directly to a Pension Plan Does Not Meet the Definition of a Special Funding Situation

Not Present

Defined Contribution Pensions—Employers That Do Not Have a Special Funding Situation

Not Present

Defined Contribution Pensions—Special Funding Situations

Not Present

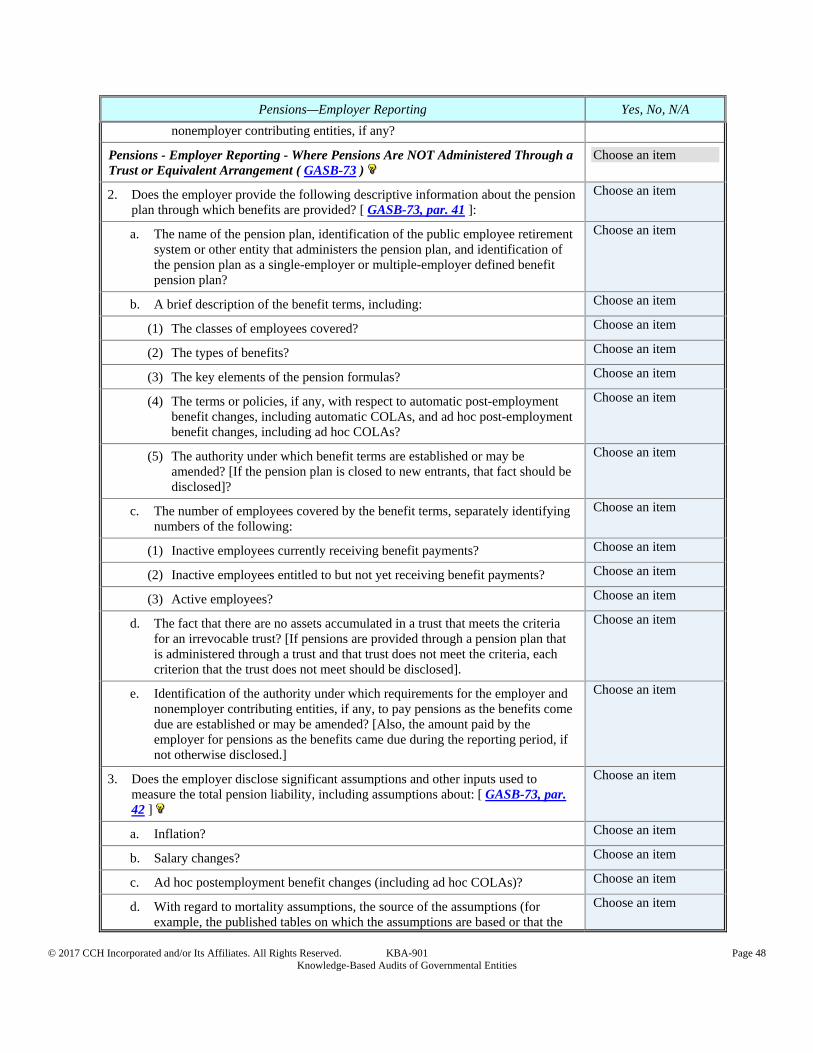

Pensions—Employer Reporting – Where Pensions are NOT Administered through a Trust or Equivalent Arrangement ( GASB-73 )

Item Present

Note Disclosure for Pensions in Stand-Alone Financial Statements of Primary Governments and Component Units That Provide Pensions Through the Same Defined Benefit Pension Plan – In Situations Without a Trust or Equivalent Arrangement

Item Present

For Governmental Nonemployer Contributing Entities to Plans That Do Not Have a Trust or Equivalent Arrangement in Accordance with GASB-73

Item Present

For Governmental Nonemployer Contributing Entities That Recognize Less than a Substantial Proportion of Total Pension Liability, That Contribute to Plans That Do Not Have a Trust or Equivalent Arrangement in Accordance with GASB-73

Item Present

Insured Plans in Accordance with GASB-73 Not Present

Defined Contribution Plans Without Trusts in Accordance with GASB-73

Not Present

For Employers That Contribute to So-Called ‘Taft-Hartley’ Plans

Not Present

Pensions—Plan Reporting Not Present

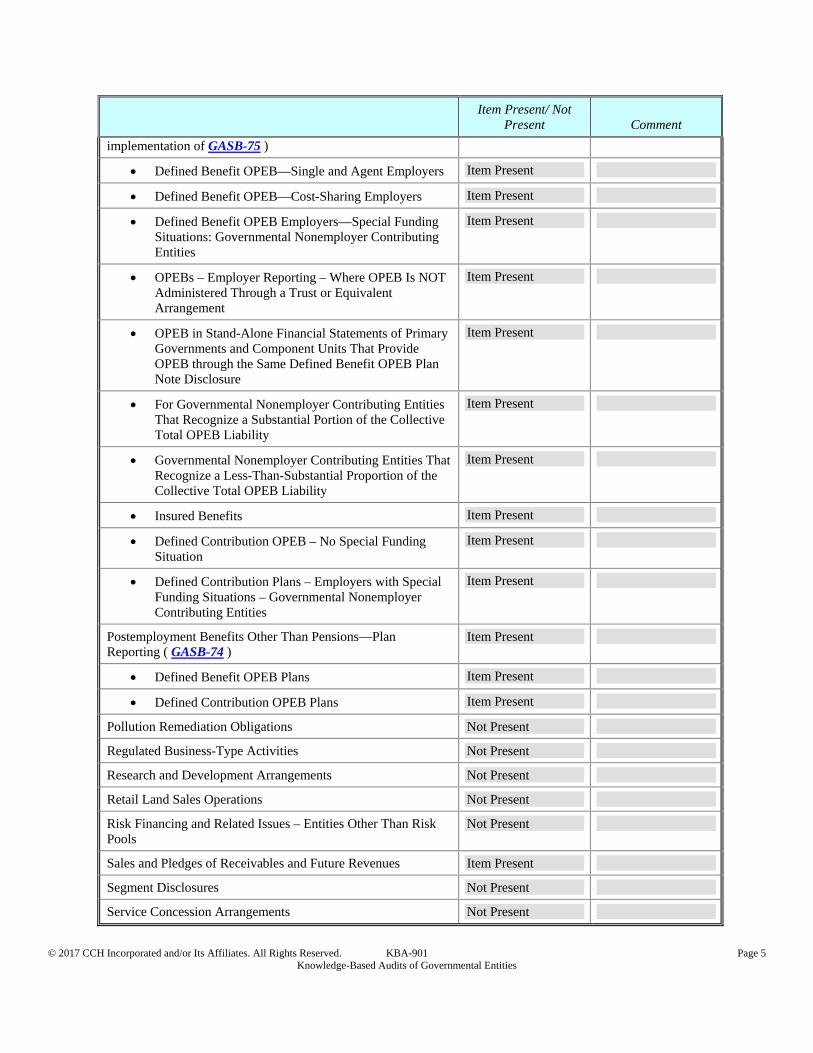

Postemployment Benefits Other Than Pensions - Employer Reporting ( GASB-45 )

Item Present

Postemployment Benefits—Employer Reporting (upon Item Present

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 5 Knowledge-Based Audits of Governmental Entities

Item Present/ Not

Present Comment

implementation of GASB-75 )

Defined Benefit OPEB—Single and Agent Employers Item Present

Defined Benefit OPEB—Cost-Sharing Employers Item Present

Defined Benefit OPEB Employers—Special Funding Situations: Governmental Nonemployer Contributing Entities

Item Present

OPEBs – Employer Reporting – Where OPEB Is NOT Administered Through a Trust or Equivalent Arrangement

Item Present

OPEB in Stand-Alone Financial Statements of Primary Governments and Component Units That Provide OPEB through the Same Defined Benefit OPEB Plan Note Disclosure

Item Present

For Governmental Nonemployer Contributing Entities That Recognize a Substantial Portion of the Collective Total OPEB Liability

Item Present

Governmental Nonemployer Contributing Entities That Recognize a Less-Than-Substantial Proportion of the Collective Total OPEB Liability

Item Present

Insured Benefits Item Present

Defined Contribution OPEB – No Special Funding Situation

Item Present

Defined Contribution Plans – Employers with Special Funding Situations – Governmental Nonemployer Contributing Entities

Item Present

Postemployment Benefits Other Than Pensions—Plan Reporting ( GASB-74 )

Item Present

Defined Benefit OPEB Plans Item Present

Defined Contribution OPEB Plans Item Present

Pollution Remediation Obligations Not Present

Regulated Business-Type Activities Not Present

Research and Development Arrangements Not Present

Retail Land Sales Operations Not Present

Risk Financing and Related Issues – Entities Other Than Risk Pools

Not Present

Sales and Pledges of Receivables and Future Revenues Item Present

Segment Disclosures Not Present

Service Concession Arrangements Not Present

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 6 Knowledge-Based Audits of Governmental Entities

Item Present/ Not

Present Comment

Special Assessments Not Present

Subsequent Event Disclosures Item Present

Tax Abatement Disclosures Not Present

Termination Benefits Not Present

Do not delete this area of work paper Do not delete this area of work paper Do not delete this area of work paper

General Financial Reporting Matters Yes, No, N/A

1. To the extent applicable, does the entity report governmental, proprietary, and fiduciary funds that meet the generally accepted criteria for those funds? [ GASB 34, par. 63 ( GASB Cod. Sec. 1300.102 ) ]

Yes

2. Following the government-wide financial statements, are financial statements presented for the three fund categories—governmental, proprietary, and fiduciary, to the extent those fund categories are applicable? [ GASB-34, par. 6b(2) and 74 ( GASB Cod. Secs. 2200.102b(2) and .151 ) ]

N/A

3. Are the governmental fund financial statements presented using the current financial resources measurement focus and the modified accrual basis of accounting? [ GASB-34, par. 79 ( GASB Cod. Sec. 1300.102a ) ]

N/A

4. Are the proprietary fund financial statements presented using the economic resources measurement focus and the accrual basis of accounting? [ GASB-34, par. 92 ( GASB Cod. Sec. 1300.102b and P80.102 ) ]

Yes

5. Are the fiduciary fund financial statements reported using the economic resources measurement focus and the accrual basis of accounting? [ GASB-34, par. 107 ( GASB Cod. Sec. 1300.102c ) ]

N/A

Do not delete this area of work paper

Proprietary Funds Yes, No, N/A

1. Are proprietary fund financial statements limited to presenting enterprise funds and internal service funds, to the extent applicable? [ GASB-34, pars. 67–68 ( GASB Cod. Secs. 1300.109–110 ) ]

Yes

2. Are enterprise funds used to report:

a. Only activities for which a fee is charged to external users for goods or services?

b. Activities that are financed with debt that is secured solely by a pledge of the

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 7 Knowledge-Based Audits of Governmental Entities

Proprietary Funds Yes, No, N/A

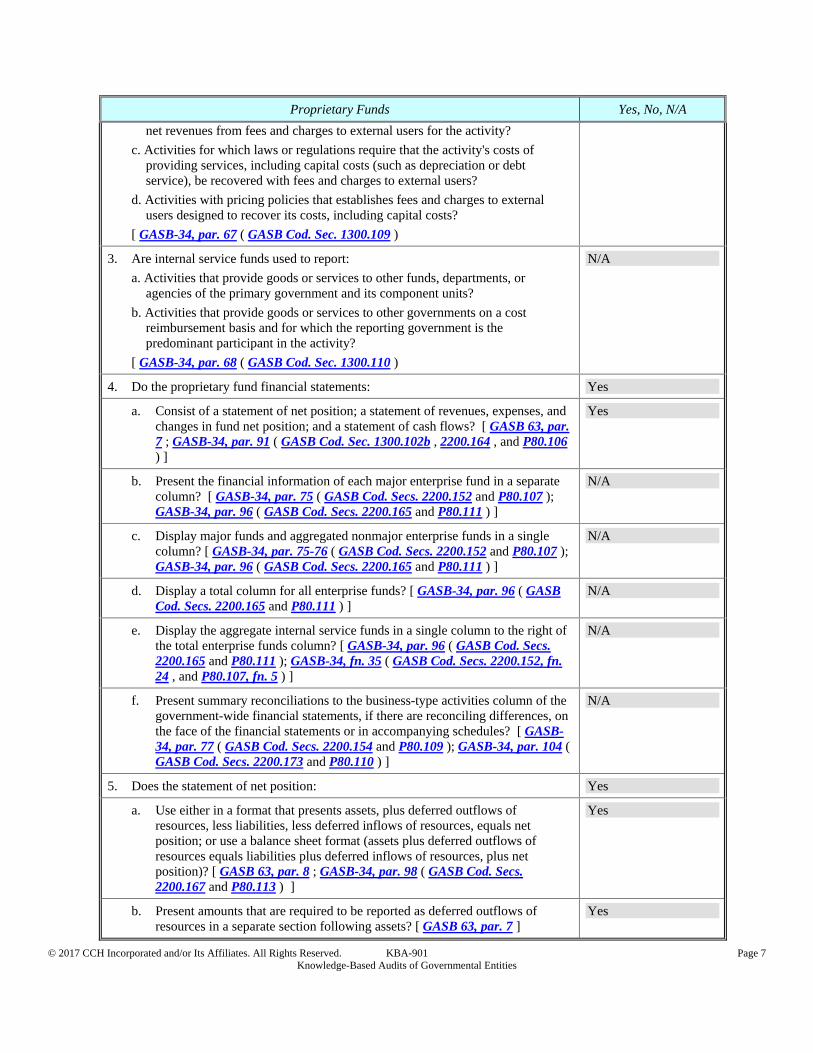

net revenues from fees and charges to external users for the activity?

c. Activities for which laws or regulations require that the activity's costs of providing services, including capital costs (such as depreciation or debt service), be recovered with fees and charges to external users?

d. Activities with pricing policies that establishes fees and charges to external users designed to recover its costs, including capital costs?

[ GASB-34, par. 67 ( GASB Cod. Sec. 1300.109 )

3. Are internal service funds used to report:

a. Activities that provide goods or services to other funds, departments, or agencies of the primary government and its component units?

b. Activities that provide goods or services to other governments on a cost reimbursement basis and for which the reporting government is the predominant participant in the activity?

[ GASB-34, par. 68 ( GASB Cod. Sec. 1300.110 )

N/A

4. Do the proprietary fund financial statements: Yes

a. Consist of a statement of net position; a statement of revenues, expenses, and changes in fund net position; and a statement of cash flows? [ GASB 63, par. 7 ; GASB-34, par. 91 ( GASB Cod. Sec. 1300.102b , 2200.164 , and P80.106 ) ]

Yes

b. Present the financial information of each major enterprise fund in a separate column? [ GASB-34, par. 75 ( GASB Cod. Secs. 2200.152 and P80.107 ); GASB-34, par. 96 ( GASB Cod. Secs. 2200.165 and P80.111 ) ]

N/A

c. Display major funds and aggregated nonmajor enterprise funds in a single column? [ GASB-34, par. 75-76 ( GASB Cod. Secs. 2200.152 and P80.107 ); GASB-34, par. 96 ( GASB Cod. Secs. 2200.165 and P80.111 ) ]

N/A

d. Display a total column for all enterprise funds? [ GASB-34, par. 96 ( GASB Cod. Secs. 2200.165 and P80.111 ) ]

N/A

e. Display the aggregate internal service funds in a single column to the right of the total enterprise funds column? [ GASB-34, par. 96 ( GASB Cod. Secs. 2200.165 and P80.111 ); GASB-34, fn. 35 ( GASB Cod. Secs. 2200.152, fn. 24 , and P80.107, fn. 5 ) ]

N/A

f. Present summary reconciliations to the business-type activities column of the government-wide financial statements, if there are reconciling differences, on the face of the financial statements or in accompanying schedules? [ GASB-34, par. 77 ( GASB Cod. Secs. 2200.154 and P80.109 ); GASB-34, par. 104 ( GASB Cod. Secs. 2200.173 and P80.110 ) ]

N/A

5. Does the statement of net position: Yes

a. Use either in a format that presents assets, plus deferred outflows of resources, less liabilities, less deferred inflows of resources, equals net position; or use a balance sheet format (assets plus deferred outflows of resources equals liabilities plus deferred inflows of resources, plus net position)? [ GASB 63, par. 8 ; GASB-34, par. 98 ( GASB Cod. Secs. 2200.167 and P80.113 ) ]

Yes

b. Present amounts that are required to be reported as deferred outflows of resources in a separate section following assets? [ GASB 63, par. 7 ]

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 8 Knowledge-Based Audits of Governmental Entities

Proprietary Funds Yes, No, N/A

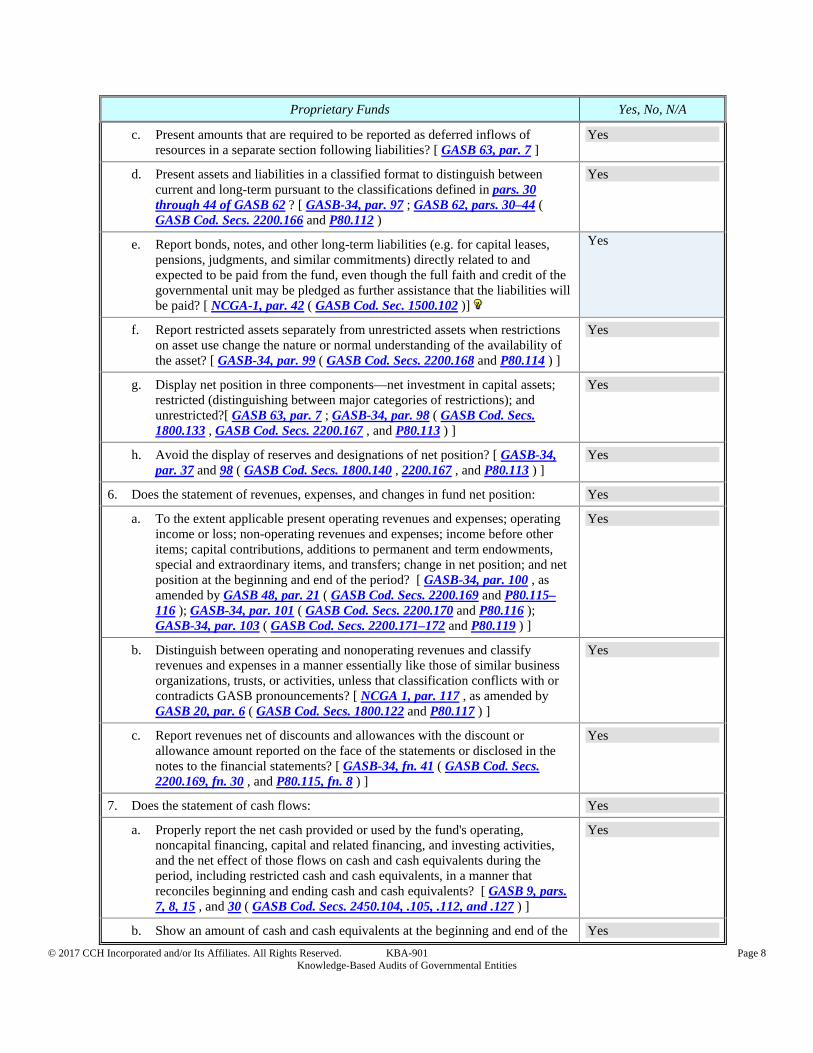

c. Present amounts that are required to be reported as deferred inflows of resources in a separate section following liabilities? [ GASB 63, par. 7 ]

Yes

d. Present assets and liabilities in a classified format to distinguish between current and long-term pursuant to the classifications defined in pars. 30 through 44 of GASB 62 ? [ GASB-34, par. 97 ; GASB 62, pars. 30–44 ( GASB Cod. Secs. 2200.166 and P80.112 )

Yes

e. Report bonds, notes, and other long-term liabilities (e.g. for capital leases, pensions, judgments, and similar commitments) directly related to and expected to be paid from the fund, even though the full faith and credit of the governmental unit may be pledged as further assistance that the liabilities will be paid? [ NCGA-1, par. 42 ( GASB Cod. Sec. 1500.102 )]

Yes

f. Report restricted assets separately from unrestricted assets when restrictions on asset use change the nature or normal understanding of the availability of the asset? [ GASB-34, par. 99 ( GASB Cod. Secs. 2200.168 and P80.114 ) ]

Yes

g. Display net position in three components—net investment in capital assets; restricted (distinguishing between major categories of restrictions); and unrestricted?[ GASB 63, par. 7 ; GASB-34, par. 98 ( GASB Cod. Secs. 1800.133 , GASB Cod. Secs. 2200.167 , and P80.113 ) ]

Yes

h. Avoid the display of reserves and designations of net position? [ GASB-34, par. 37 and 98 ( GASB Cod. Secs. 1800.140 , 2200.167 , and P80.113 ) ]

Yes

6. Does the statement of revenues, expenses, and changes in fund net position: Yes

a. To the extent applicable present operating revenues and expenses; operating income or loss; non-operating revenues and expenses; income before other items; capital contributions, additions to permanent and term endowments, special and extraordinary items, and transfers; change in net position; and net position at the beginning and end of the period? [ GASB-34, par. 100 , as amended by GASB 48, par. 21 ( GASB Cod. Secs. 2200.169 and P80.115–116 ); GASB-34, par. 101 ( GASB Cod. Secs. 2200.170 and P80.116 ); GASB-34, par. 103 ( GASB Cod. Secs. 2200.171–172 and P80.119 ) ]

Yes

b. Distinguish between operating and nonoperating revenues and classify revenues and expenses in a manner essentially like those of similar business organizations, trusts, or activities, unless that classification conflicts with or contradicts GASB pronouncements? [ NCGA 1, par. 117 , as amended by GASB 20, par. 6 ( GASB Cod. Secs. 1800.122 and P80.117 ) ]

Yes

c. Report revenues net of discounts and allowances with the discount or allowance amount reported on the face of the statements or disclosed in the notes to the financial statements? [ GASB-34, fn. 41 ( GASB Cod. Secs. 2200.169, fn. 30 , and P80.115, fn. 8 ) ]

Yes

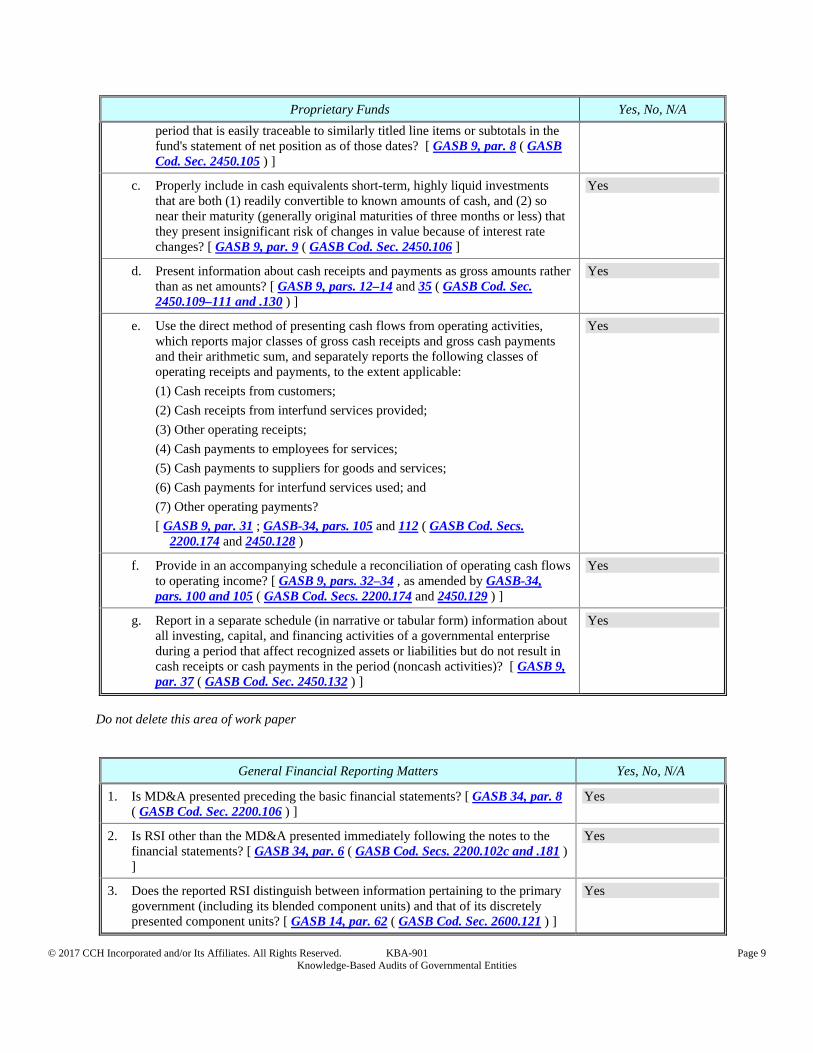

7. Does the statement of cash flows: Yes

a. Properly report the net cash provided or used by the fund's operating, noncapital financing, capital and related financing, and investing activities, and the net effect of those flows on cash and cash equivalents during the period, including restricted cash and cash equivalents, in a manner that reconciles beginning and ending cash and cash equivalents? [ GASB 9, pars. 7, 8, 15 , and 30 ( GASB Cod. Secs. 2450.104, .105, .112, and .127 ) ]

Yes

b. Show an amount of cash and cash equivalents at the beginning and end of the Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 9 Knowledge-Based Audits of Governmental Entities

Proprietary Funds Yes, No, N/A

period that is easily traceable to similarly titled line items or subtotals in the fund's statement of net position as of those dates? [ GASB 9, par. 8 ( GASB Cod. Sec. 2450.105 ) ]

c. Properly include in cash equivalents short-term, highly liquid investments that are both (1) readily convertible to known amounts of cash, and (2) so near their maturity (generally original maturities of three months or less) that they present insignificant risk of changes in value because of interest rate changes? [ GASB 9, par. 9 ( GASB Cod. Sec. 2450.106 ]

Yes

d. Present information about cash receipts and payments as gross amounts rather than as net amounts? [ GASB 9, pars. 12–14 and 35 ( GASB Cod. Sec. 2450.109–111 and .130 ) ]

Yes

e. Use the direct method of presenting cash flows from operating activities, which reports major classes of gross cash receipts and gross cash payments and their arithmetic sum, and separately reports the following classes of operating receipts and payments, to the extent applicable:

(1) Cash receipts from customers;

(2) Cash receipts from interfund services provided;

(3) Other operating receipts;

(4) Cash payments to employees for services;

(5) Cash payments to suppliers for goods and services;

(6) Cash payments for interfund services used; and

(7) Other operating payments?

[ GASB 9, par. 31 ; GASB-34, pars. 105 and 112 ( GASB Cod. Secs. 2200.174 and 2450.128 )

Yes

f. Provide in an accompanying schedule a reconciliation of operating cash flows to operating income? [ GASB 9, pars. 32–34 , as amended by GASB-34, pars. 100 and 105 ( GASB Cod. Secs. 2200.174 and 2450.129 ) ]

Yes

g. Report in a separate schedule (in narrative or tabular form) information about all investing, capital, and financing activities of a governmental enterprise during a period that affect recognized assets or liabilities but do not result in cash receipts or cash payments in the period (noncash activities)? [ GASB 9, par. 37 ( GASB Cod. Sec. 2450.132 ) ]

Yes

Do not delete this area of work paper

General Financial Reporting Matters Yes, No, N/A

1. Is MD&A presented preceding the basic financial statements? [ GASB 34, par. 8 ( GASB Cod. Sec. 2200.106 ) ]

Yes

2. Is RSI other than the MD&A presented immediately following the notes to the financial statements? [ GASB 34, par. 6 ( GASB Cod. Secs. 2200.102c and .181 ) ]

Yes

3. Does the reported RSI distinguish between information pertaining to the primary government (including its blended component units) and that of its discretely presented component units? [ GASB 14, par. 62 ( GASB Cod. Sec. 2600.121 ) ]

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 10 Knowledge-Based Audits of Governmental Entities

Management’s Discussion and Analysis Yes, No, N/A

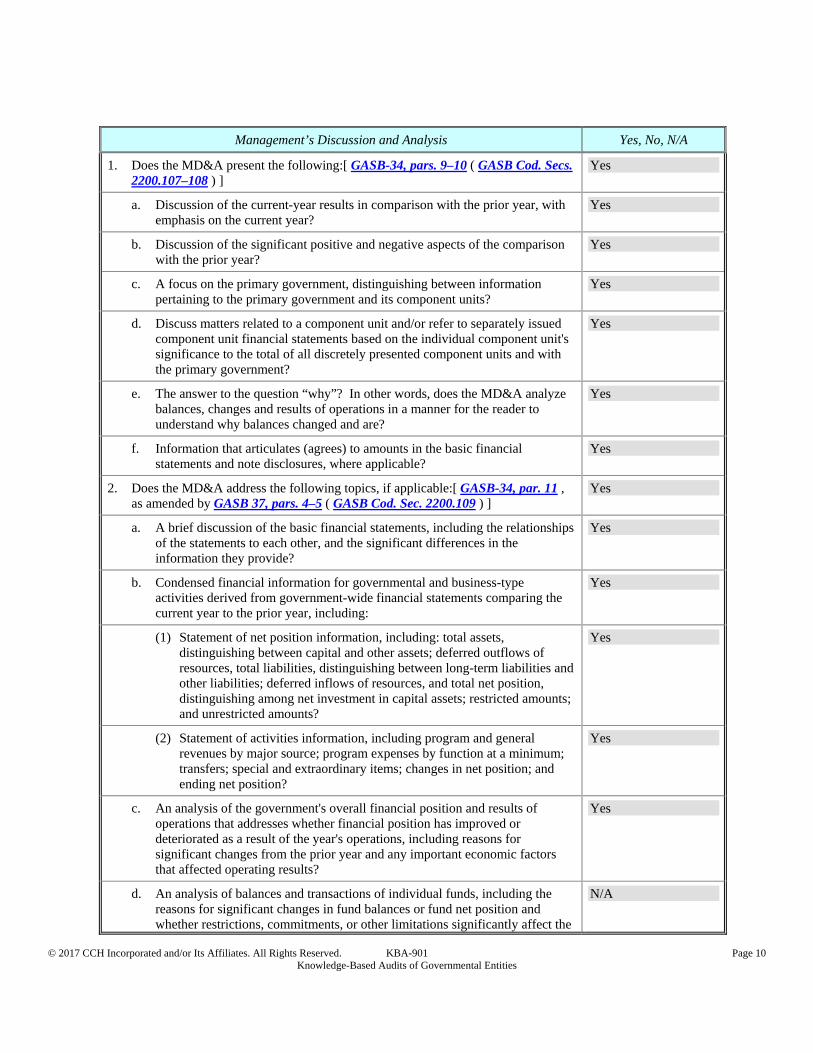

1. Does the MD&A present the following:[ GASB-34, pars. 9–10 ( GASB Cod. Secs. 2200.107–108 ) ]

Yes

a. Discussion of the current-year results in comparison with the prior year, with emphasis on the current year?

Yes

b. Discussion of the significant positive and negative aspects of the comparison with the prior year?

Yes

c. A focus on the primary government, distinguishing between information pertaining to the primary government and its component units?

Yes

d. Discuss matters related to a component unit and/or refer to separately issued component unit financial statements based on the individual component unit's significance to the total of all discretely presented component units and with the primary government?

Yes

e. The answer to the question “why”? In other words, does the MD&A analyze balances, changes and results of operations in a manner for the reader to understand why balances changed and are?

Yes

f. Information that articulates (agrees) to amounts in the basic financial statements and note disclosures, where applicable?

Yes

2. Does the MD&A address the following topics, if applicable:[ GASB-34, par. 11 , as amended by GASB 37, pars. 4–5 ( GASB Cod. Sec. 2200.109 ) ]

Yes

a. A brief discussion of the basic financial statements, including the relationships of the statements to each other, and the significant differences in the information they provide?

Yes

b. Condensed financial information for governmental and business-type activities derived from government-wide financial statements comparing the current year to the prior year, including:

Yes

(1) Statement of net position information, including: total assets, distinguishing between capital and other assets; deferred outflows of resources, total liabilities, distinguishing between long-term liabilities and other liabilities; deferred inflows of resources, and total net position, distinguishing among net investment in capital assets; restricted amounts; and unrestricted amounts?

Yes

(2) Statement of activities information, including program and general revenues by major source; program expenses by function at a minimum; transfers; special and extraordinary items; changes in net position; and ending net position?

Yes

c. An analysis of the government's overall financial position and results of operations that addresses whether financial position has improved or deteriorated as a result of the year's operations, including reasons for significant changes from the prior year and any important economic factors that affected operating results?

Yes

d. An analysis of balances and transactions of individual funds, including the reasons for significant changes in fund balances or fund net position and whether restrictions, commitments, or other limitations significantly affect the

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 11 Knowledge-Based Audits of Governmental Entities

Management’s Discussion and Analysis Yes, No, N/A

availability of fund resources for future use?

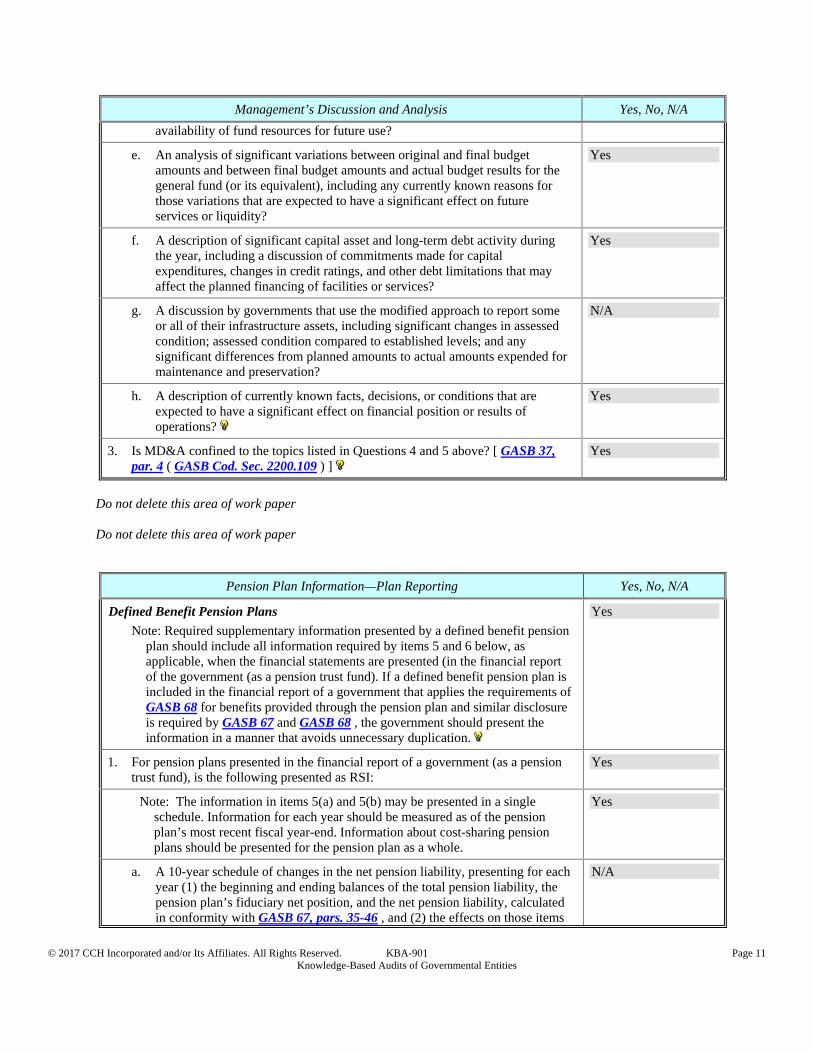

e. An analysis of significant variations between original and final budget amounts and between final budget amounts and actual budget results for the general fund (or its equivalent), including any currently known reasons for those variations that are expected to have a significant effect on future services or liquidity?

Yes

f. A description of significant capital asset and long-term debt activity during the year, including a discussion of commitments made for capital expenditures, changes in credit ratings, and other debt limitations that may affect the planned financing of facilities or services?

Yes

g. A discussion by governments that use the modified approach to report some or all of their infrastructure assets, including significant changes in assessed condition; assessed condition compared to established levels; and any significant differences from planned amounts to actual amounts expended for maintenance and preservation?

N/A

h. A description of currently known facts, decisions, or conditions that are expected to have a significant effect on financial position or results of operations?

Yes

3. Is MD&A confined to the topics listed in Questions 4 and 5 above? [ GASB 37, par. 4 ( GASB Cod. Sec. 2200.109 ) ]

Yes

Do not delete this area of work paper Do not delete this area of work paper

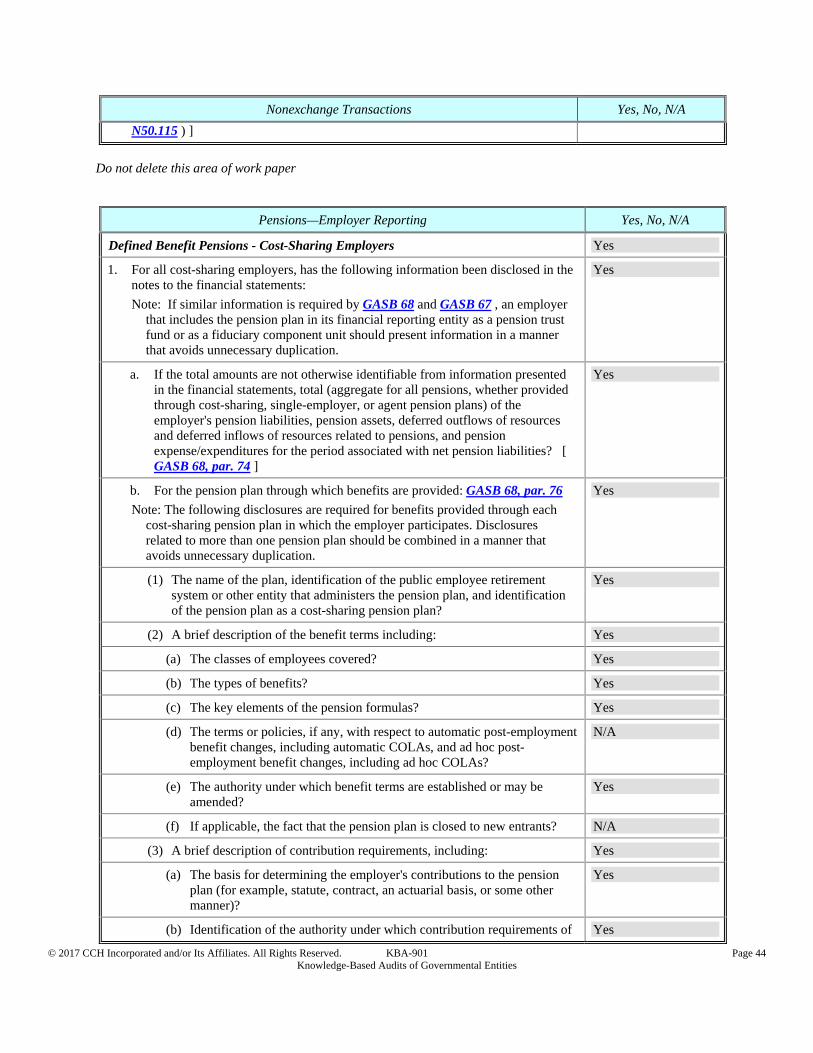

Pension Plan Information—Plan Reporting Yes, No, N/A

Defined Benefit Pension Plans

Note: Required supplementary information presented by a defined benefit pension plan should include all information required by items 5 and 6 below, as applicable, when the financial statements are presented (in the financial report of the government (as a pension trust fund). If a defined benefit pension plan is included in the financial report of a government that applies the requirements of GASB 68 for benefits provided through the pension plan and similar disclosure is required by GASB 67 and GASB 68 , the government should present the information in a manner that avoids unnecessary duplication.

Yes

1. For pension plans presented in the financial report of a government (as a pension trust fund), is the following presented as RSI:

Yes

Note: The information in items 5(a) and 5(b) may be presented in a single schedule. Information for each year should be measured as of the pension plan’s most recent fiscal year-end. Information about cost-sharing pension plans should be presented for the pension plan as a whole.

Yes

a. A 10-year schedule of changes in the net pension liability, presenting for each year (1) the beginning and ending balances of the total pension liability, the pension plan’s fiduciary net position, and the net pension liability, calculated in conformity with GASB 67, pars. 35-46 , and (2) the effects on those items

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 12 Knowledge-Based Audits of Governmental Entities

Pension Plan Information—Plan Reporting Yes, No, N/A

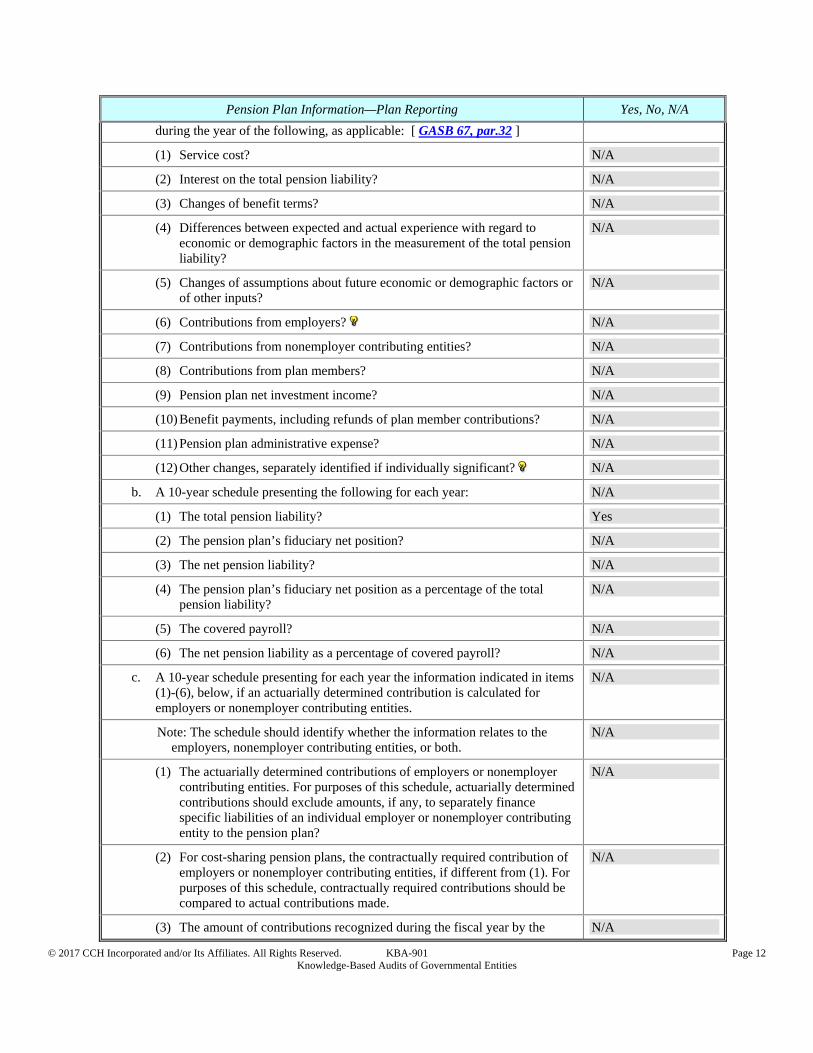

during the year of the following, as applicable: [ GASB 67, par.32 ]

(1) Service cost? N/A

(2) Interest on the total pension liability? N/A

(3) Changes of benefit terms? N/A

(4) Differences between expected and actual experience with regard to economic or demographic factors in the measurement of the total pension liability?

N/A

(5) Changes of assumptions about future economic or demographic factors or of other inputs?

N/A

(6) Contributions from employers? N/A

(7) Contributions from nonemployer contributing entities? N/A

(8) Contributions from plan members? N/A

(9) Pension plan net investment income? N/A

(10) Benefit payments, including refunds of plan member contributions? N/A

(11) Pension plan administrative expense? N/A

(12) Other changes, separately identified if individually significant? N/A

b. A 10-year schedule presenting the following for each year: N/A

(1) The total pension liability? Yes

(2) The pension plan’s fiduciary net position? N/A

(3) The net pension liability? N/A

(4) The pension plan’s fiduciary net position as a percentage of the total pension liability?

N/A

(5) The covered payroll? N/A

(6) The net pension liability as a percentage of covered payroll? N/A

c. A 10-year schedule presenting for each year the information indicated in items (1)-(6), below, if an actuarially determined contribution is calculated for employers or nonemployer contributing entities.

N/A

Note: The schedule should identify whether the information relates to the employers, nonemployer contributing entities, or both.

N/A

(1) The actuarially determined contributions of employers or nonemployer contributing entities. For purposes of this schedule, actuarially determined contributions should exclude amounts, if any, to separately finance specific liabilities of an individual employer or nonemployer contributing entity to the pension plan?

N/A

(2) For cost-sharing pension plans, the contractually required contribution of employers or nonemployer contributing entities, if different from (1). For purposes of this schedule, contractually required contributions should be compared to actual contributions made.

N/A

(3) The amount of contributions recognized during the fiscal year by the N/A

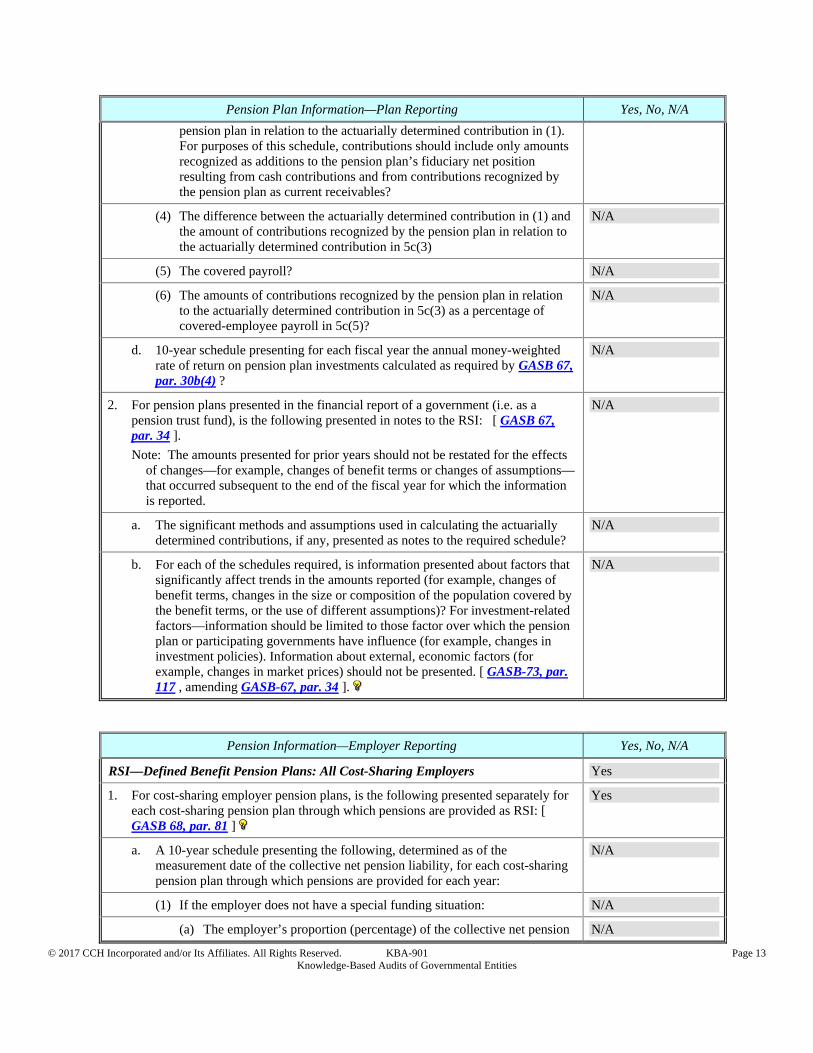

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 13 Knowledge-Based Audits of Governmental Entities

Pension Plan Information—Plan Reporting Yes, No, N/A

pension plan in relation to the actuarially determined contribution in (1). For purposes of this schedule, contributions should include only amounts recognized as additions to the pension plan’s fiduciary net position resulting from cash contributions and from contributions recognized by the pension plan as current receivables?

(4) The difference between the actuarially determined contribution in (1) and the amount of contributions recognized by the pension plan in relation to the actuarially determined contribution in 5c(3)

N/A

(5) The covered payroll? N/A

(6) The amounts of contributions recognized by the pension plan in relation to the actuarially determined contribution in 5c(3) as a percentage of covered-employee payroll in 5c(5)?

N/A

d. 10-year schedule presenting for each fiscal year the annual money-weighted rate of return on pension plan investments calculated as required by GASB 67, par. 30b(4) ?

N/A

2. For pension plans presented in the financial report of a government (i.e. as a pension trust fund), is the following presented in notes to the RSI: [ GASB 67, par. 34 ].

Note: The amounts presented for prior years should not be restated for the effects of changes—for example, changes of benefit terms or changes of assumptions—that occurred subsequent to the end of the fiscal year for which the information is reported.

N/A

a. The significant methods and assumptions used in calculating the actuarially determined contributions, if any, presented as notes to the required schedule?

N/A

b. For each of the schedules required, is information presented about factors that significantly affect trends in the amounts reported (for example, changes of benefit terms, changes in the size or composition of the population covered by the benefit terms, or the use of different assumptions)? For investment-related factors—information should be limited to those factor over which the pension plan or participating governments have influence (for example, changes in investment policies). Information about external, economic factors (for example, changes in market prices) should not be presented. [ GASB-73, par. 117 , amending GASB-67, par. 34 ].

N/A

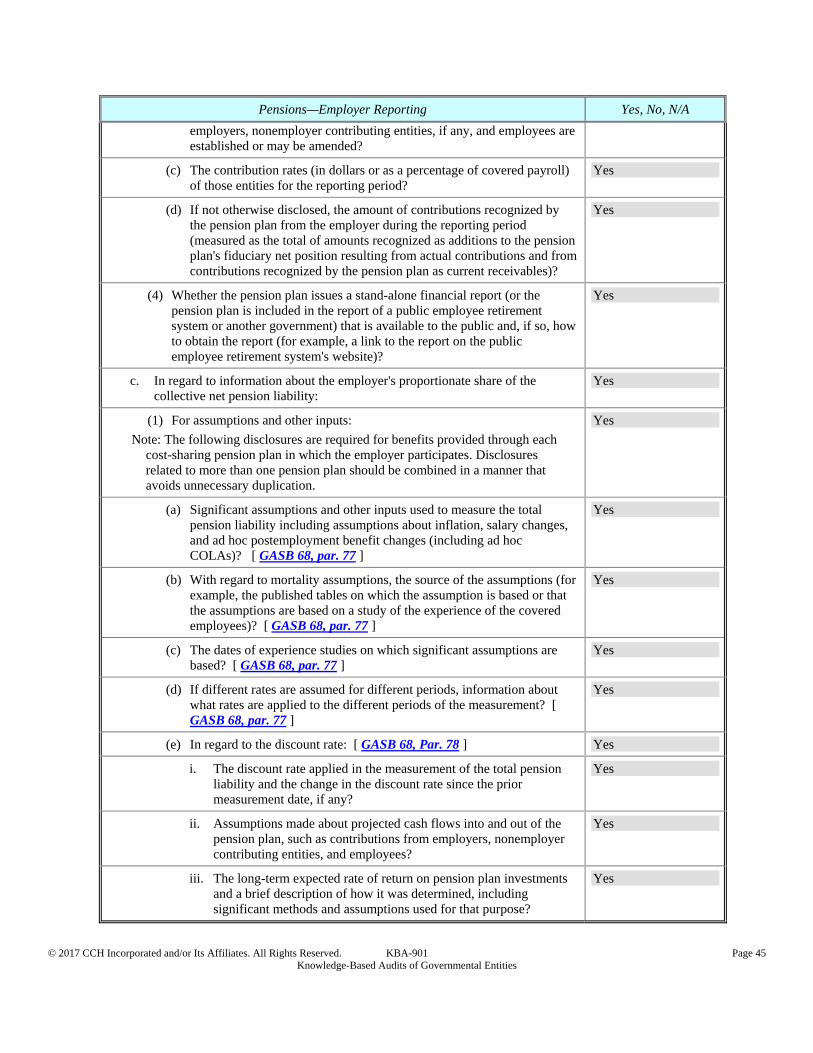

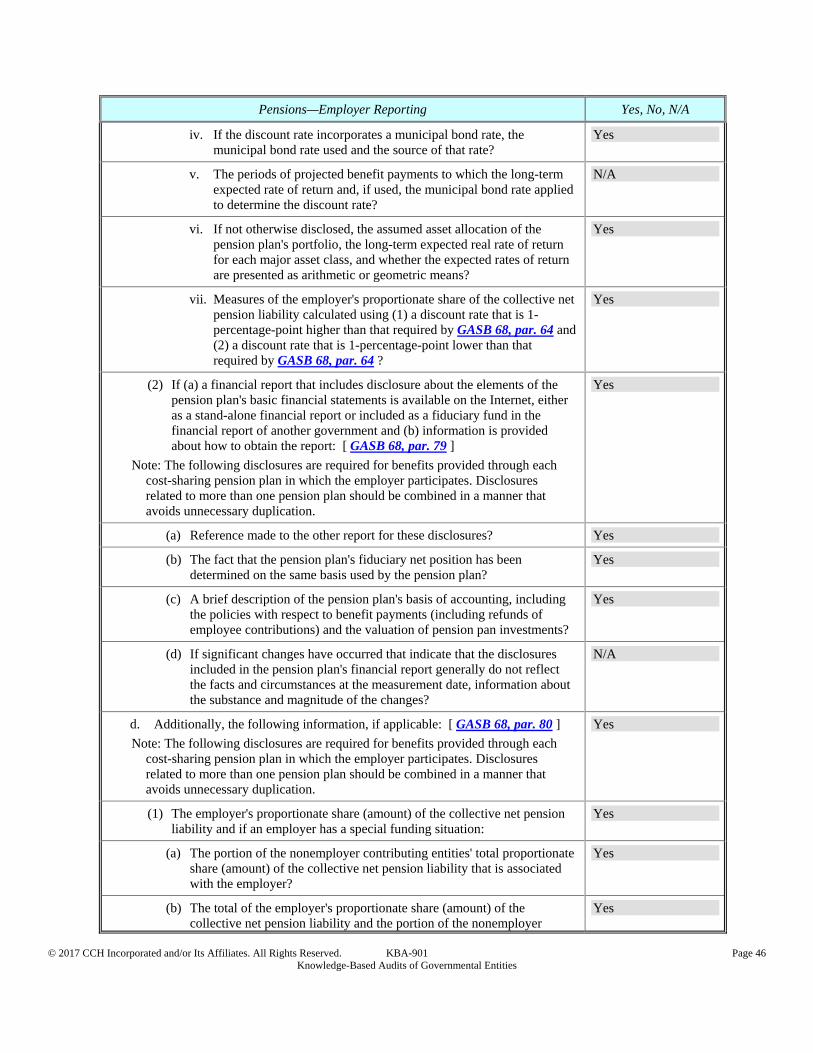

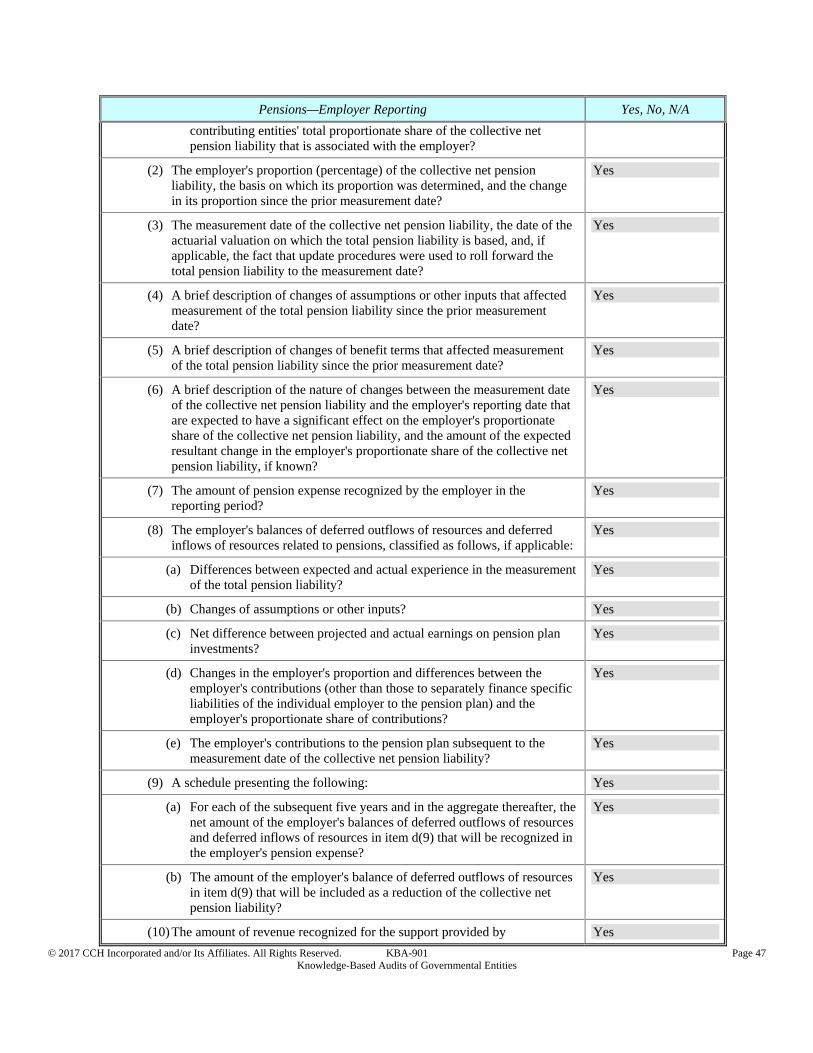

Pension Information—Employer Reporting Yes, No, N/A

RSI—Defined Benefit Pension Plans: All Cost-Sharing Employers Yes

1. For cost-sharing employer pension plans, is the following presented separately for each cost-sharing pension plan through which pensions are provided as RSI: [ GASB 68, par. 81 ]

Yes

a. A 10-year schedule presenting the following, determined as of the measurement date of the collective net pension liability, for each cost-sharing pension plan through which pensions are provided for each year:

N/A

(1) If the employer does not have a special funding situation: N/A

(a) The employer’s proportion (percentage) of the collective net pension N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 14 Knowledge-Based Audits of Governmental Entities

Pension Information—Employer Reporting Yes, No, N/A

liability?

(b) The employer’s proportionate share (amount) of the collective net pension liability?

N/A

(c) The employer’s covered payroll? N/A

(d) The employer’s proportionate share (amount) of the collective net pension liability as a percentage of the employer’s covered payroll?

N/A

(e) The pension plan’s fiduciary net position as a percentage of the total pension liability?

N/A

(2) If the employer has a special funding situation: N/A

(a) The employer’s proportion (percentage) of the collective net pension liability?

N/A

(b) The employer’s proportionate share (amount) of the collective net pension liability?

N/A

(c) The portion of the nonemployer contributing entities’ total proportionate share (amount) of the collective net pension liability that is associated with the employer?

N/A

(d) The total? N/A

(e) The employer’s covered payroll? N/A

(f) The employer’s proportionate share (amount) of the collective net pension liability as a percentage of the employer’s covered payroll?

N/A

(g) The pension plan’s fiduciary net position as a percentage of the total pension liability?

N/A

b. If the contribution requirements of the employer are statutorily or contractually established, a 10-year schedule presenting the following, determined as of the employer’s most recent fiscal year-end, for each cost-sharing pension plan through which pensions are provided for each year:

N/A

(1) The statutorily or contractually required employer contribution? N/A

(2) The amount of contributions recognized by the pension plan in relation to the statutorily or contractually required employer contribution?

N/A

(3) The difference between the statutorily or contractually required employer contribution and the amount of contributions recognized by the pension plan in relation to the statutorily or contractually required employer contribution?

N/A

(4) The employer’s covered payroll? N/A

(5) The amount of contributions recognized by the pension plan in relation to the statutorily or contractually required employer contribution as a percentage of the employer’s covered payroll?

N/A

2. Is information presented about factors that significantly affect trends in the amounts reported above presented as notes to the RSI? [ GASB 68, par. 82 ] [See amendment above made by GASB-73 ].

Yes

Do not delete this area of work paper

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 15 Knowledge-Based Audits of Governmental Entities

Do not delete this area of work paper

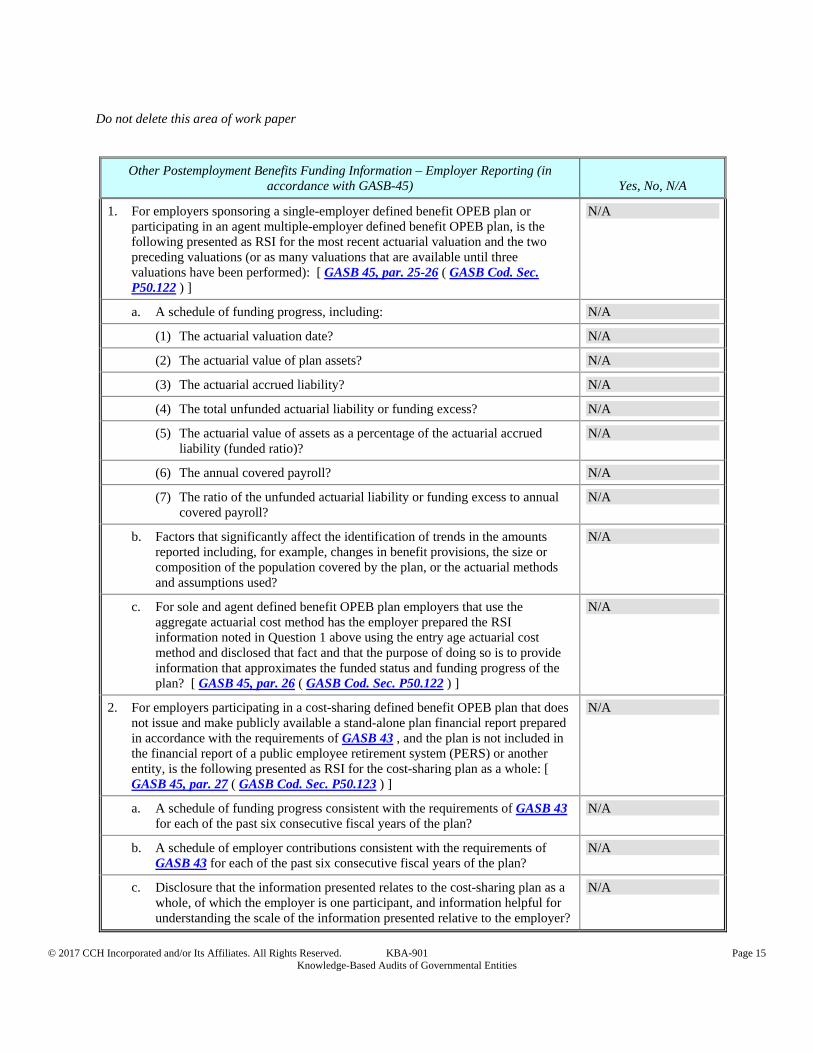

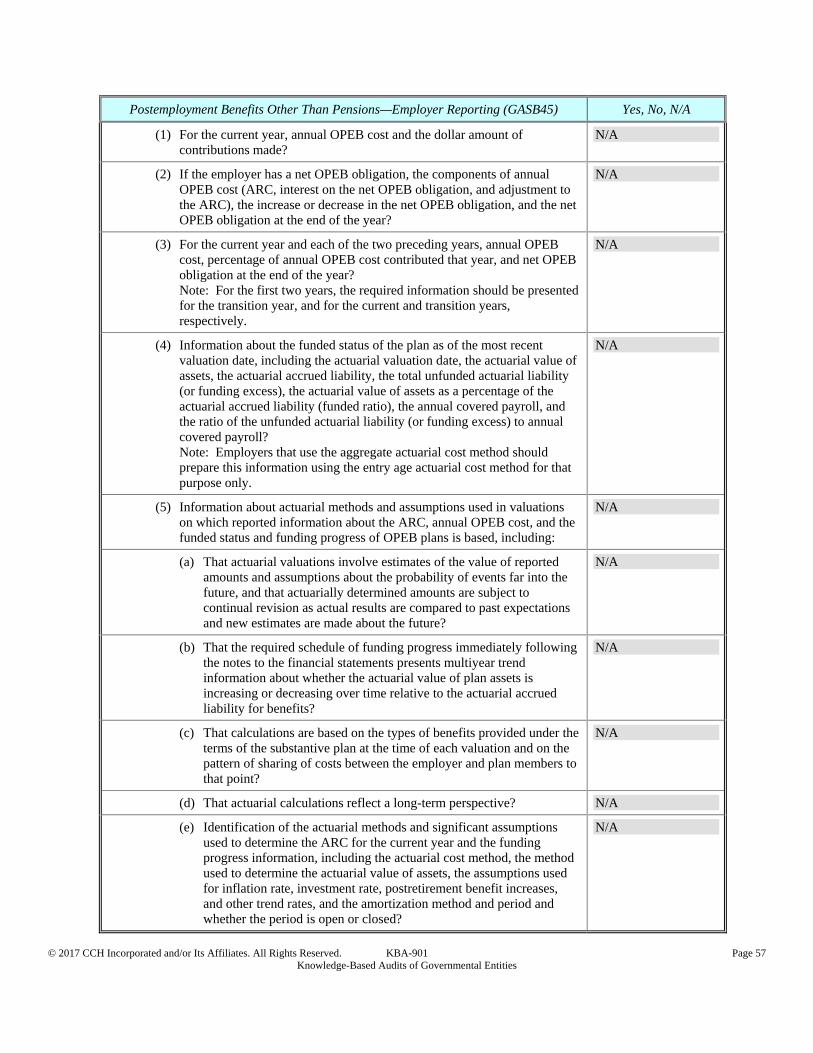

Other Postemployment Benefits Funding Information – Employer Reporting (in accordance with GASB-45) Yes, No, N/A

1. For employers sponsoring a single-employer defined benefit OPEB plan or participating in an agent multiple-employer defined benefit OPEB plan, is the following presented as RSI for the most recent actuarial valuation and the two preceding valuations (or as many valuations that are available until three valuations have been performed): [ GASB 45, par. 25-26 ( GASB Cod. Sec. P50.122 ) ]

N/A

a. A schedule of funding progress, including: N/A

(1) The actuarial valuation date? N/A

(2) The actuarial value of plan assets? N/A

(3) The actuarial accrued liability? N/A

(4) The total unfunded actuarial liability or funding excess? N/A

(5) The actuarial value of assets as a percentage of the actuarial accrued liability (funded ratio)?

N/A

(6) The annual covered payroll? N/A

(7) The ratio of the unfunded actuarial liability or funding excess to annual covered payroll?

N/A

b. Factors that significantly affect the identification of trends in the amounts reported including, for example, changes in benefit provisions, the size or composition of the population covered by the plan, or the actuarial methods and assumptions used?

N/A

c. For sole and agent defined benefit OPEB plan employers that use the aggregate actuarial cost method has the employer prepared the RSI information noted in Question 1 above using the entry age actuarial cost method and disclosed that fact and that the purpose of doing so is to provide information that approximates the funded status and funding progress of the plan? [ GASB 45, par. 26 ( GASB Cod. Sec. P50.122 ) ]

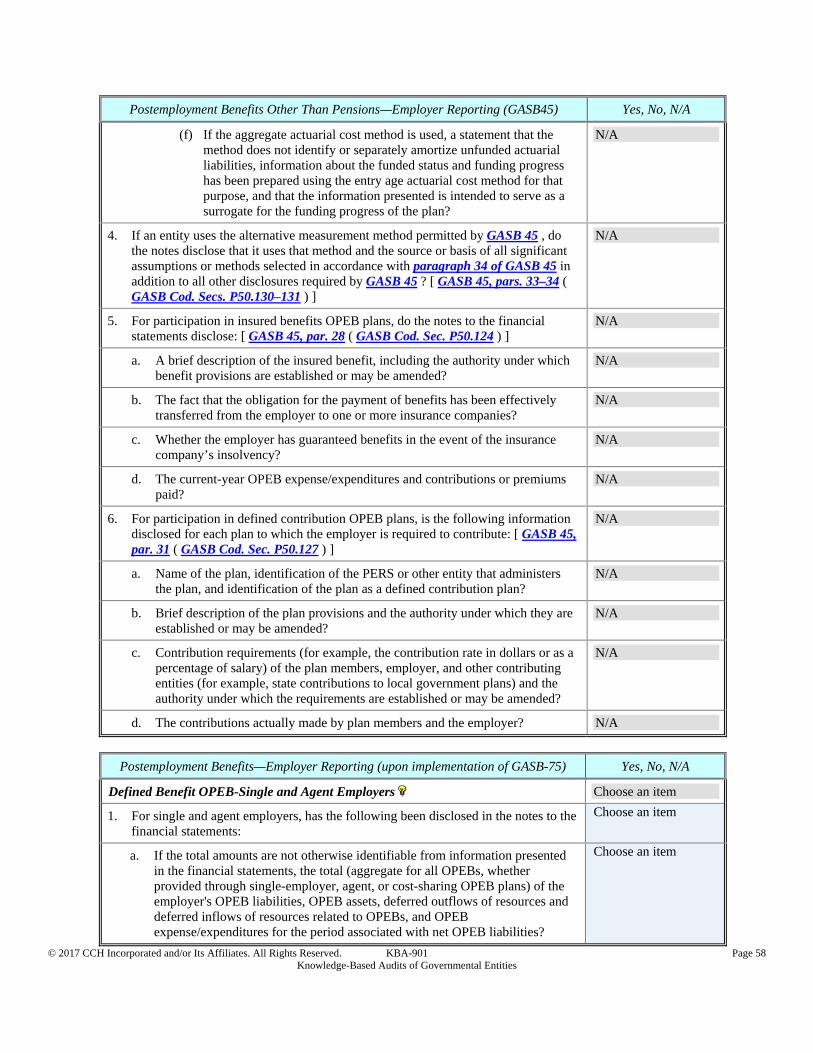

N/A

2. For employers participating in a cost-sharing defined benefit OPEB plan that does not issue and make publicly available a stand-alone plan financial report prepared in accordance with the requirements of GASB 43 , and the plan is not included in the financial report of a public employee retirement system (PERS) or another entity, is the following presented as RSI for the cost-sharing plan as a whole: [ GASB 45, par. 27 ( GASB Cod. Sec. P50.123 ) ]

N/A

a. A schedule of funding progress consistent with the requirements of GASB 43 for each of the past six consecutive fiscal years of the plan?

N/A

b. A schedule of employer contributions consistent with the requirements of GASB 43 for each of the past six consecutive fiscal years of the plan?

N/A

c. Disclosure that the information presented relates to the cost-sharing plan as a whole, of which the employer is one participant, and information helpful for understanding the scale of the information presented relative to the employer?

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 16 Knowledge-Based Audits of Governmental Entities

Other Postemployment Benefits Funding Information – Employer Reporting (in accordance with GASB-45) Yes, No, N/A

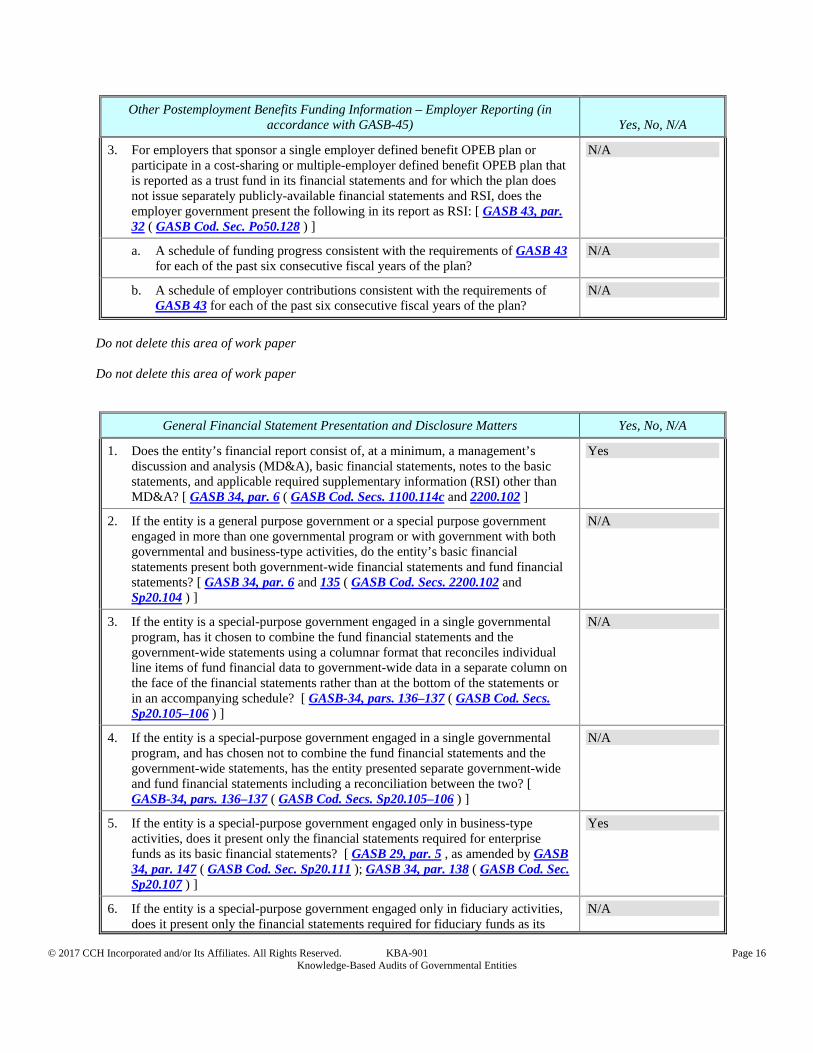

3. For employers that sponsor a single employer defined benefit OPEB plan or participate in a cost-sharing or multiple-employer defined benefit OPEB plan that is reported as a trust fund in its financial statements and for which the plan does not issue separately publicly-available financial statements and RSI, does the employer government present the following in its report as RSI: [ GASB 43, par. 32 ( GASB Cod. Sec. Po50.128 ) ]

N/A

a. A schedule of funding progress consistent with the requirements of GASB 43 for each of the past six consecutive fiscal years of the plan?

N/A

b. A schedule of employer contributions consistent with the requirements of GASB 43 for each of the past six consecutive fiscal years of the plan?

N/A

Do not delete this area of work paper Do not delete this area of work paper

General Financial Statement Presentation and Disclosure Matters Yes, No, N/A

1. Does the entity’s financial report consist of, at a minimum, a management’s discussion and analysis (MD&A), basic financial statements, notes to the basic statements, and applicable required supplementary information (RSI) other than MD&A? [ GASB 34, par. 6 ( GASB Cod. Secs. 1100.114c and 2200.102 ]

Yes

2. If the entity is a general purpose government or a special purpose government engaged in more than one governmental program or with government with both governmental and business-type activities, do the entity’s basic financial statements present both government-wide financial statements and fund financial statements? [ GASB 34, par. 6 and 135 ( GASB Cod. Secs. 2200.102 and Sp20.104 ) ]

N/A

3. If the entity is a special-purpose government engaged in a single governmental program, has it chosen to combine the fund financial statements and the government-wide statements using a columnar format that reconciles individual line items of fund financial data to government-wide data in a separate column on the face of the financial statements rather than at the bottom of the statements or in an accompanying schedule? [ GASB-34, pars. 136–137 ( GASB Cod. Secs. Sp20.105–106 ) ]

N/A

4. If the entity is a special-purpose government engaged in a single governmental program, and has chosen not to combine the fund financial statements and the government-wide statements, has the entity presented separate government-wide and fund financial statements including a reconciliation between the two? [ GASB-34, pars. 136–137 ( GASB Cod. Secs. Sp20.105–106 ) ]

N/A

5. If the entity is a special-purpose government engaged only in business-type activities, does it present only the financial statements required for enterprise funds as its basic financial statements? [ GASB 29, par. 5 , as amended by GASB 34, par. 147 ( GASB Cod. Sec. Sp20.111 ); GASB 34, par. 138 ( GASB Cod. Sec. Sp20.107 ) ]

Yes

6. If the entity is a special-purpose government engaged only in fiduciary activities, does it present only the financial statements required for fiduciary funds as its

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 17 Knowledge-Based Audits of Governmental Entities

General Financial Statement Presentation and Disclosure Matters Yes, No, N/A

basic financial statements? [ GASB 34, par. 139 ( GASB Cod. Sec. Sp20.108 ) ]

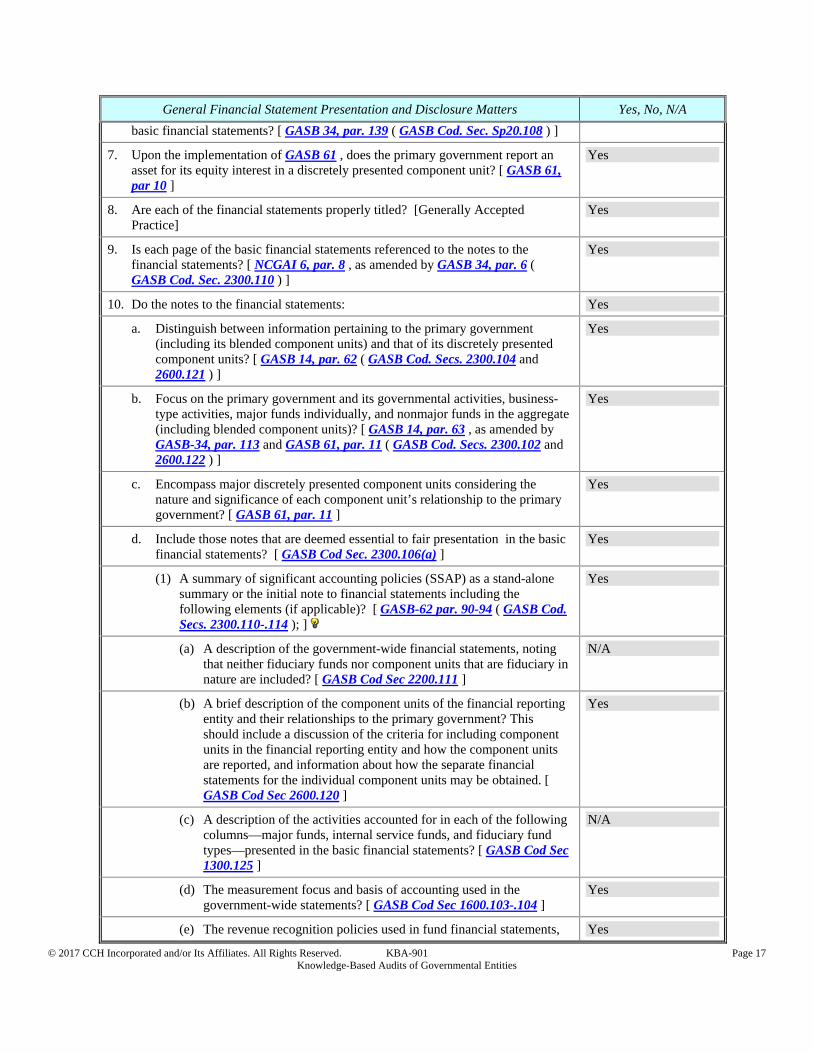

7. Upon the implementation of GASB 61 , does the primary government report an asset for its equity interest in a discretely presented component unit? [ GASB 61, par 10 ]

Yes

8. Are each of the financial statements properly titled? [Generally Accepted Practice]

Yes

9. Is each page of the basic financial statements referenced to the notes to the financial statements? [ NCGAI 6, par. 8 , as amended by GASB 34, par. 6 ( GASB Cod. Sec. 2300.110 ) ]

Yes

10. Do the notes to the financial statements: Yes

a. Distinguish between information pertaining to the primary government (including its blended component units) and that of its discretely presented component units? [ GASB 14, par. 62 ( GASB Cod. Secs. 2300.104 and 2600.121 ) ]

Yes

b. Focus on the primary government and its governmental activities, business-type activities, major funds individually, and nonmajor funds in the aggregate (including blended component units)? [ GASB 14, par. 63 , as amended by GASB-34, par. 113 and GASB 61, par. 11 ( GASB Cod. Secs. 2300.102 and 2600.122 ) ]

Yes

c. Encompass major discretely presented component units considering the nature and significance of each component unit’s relationship to the primary government? [ GASB 61, par. 11 ]

Yes

d. Include those notes that are deemed essential to fair presentation in the basic financial statements? [ GASB Cod Sec. 2300.106(a) ]

Yes

(1) A summary of significant accounting policies (SSAP) as a stand-alone summary or the initial note to financial statements including the following elements (if applicable)? [ GASB-62 par. 90-94 ( GASB Cod. Secs. 2300.110-.114 ); ]

Yes

(a) A description of the government-wide financial statements, noting that neither fiduciary funds nor component units that are fiduciary in nature are included? [ GASB Cod Sec 2200.111 ]

N/A

(b) A brief description of the component units of the financial reporting entity and their relationships to the primary government? This should include a discussion of the criteria for including component units in the financial reporting entity and how the component units are reported, and information about how the separate financial statements for the individual component units may be obtained. [ GASB Cod Sec 2600.120 ]

Yes

(c) A description of the activities accounted for in each of the following columns—major funds, internal service funds, and fiduciary fund types—presented in the basic financial statements? [ GASB Cod Sec 1300.125 ]

N/A

(d) The measurement focus and basis of accounting used in the government-wide statements? [ GASB Cod Sec 1600.103-.104 ]

Yes

(e) The revenue recognition policies used in fund financial statements, Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 18 Knowledge-Based Audits of Governmental Entities

General Financial Statement Presentation and Disclosure Matters Yes, No, N/A

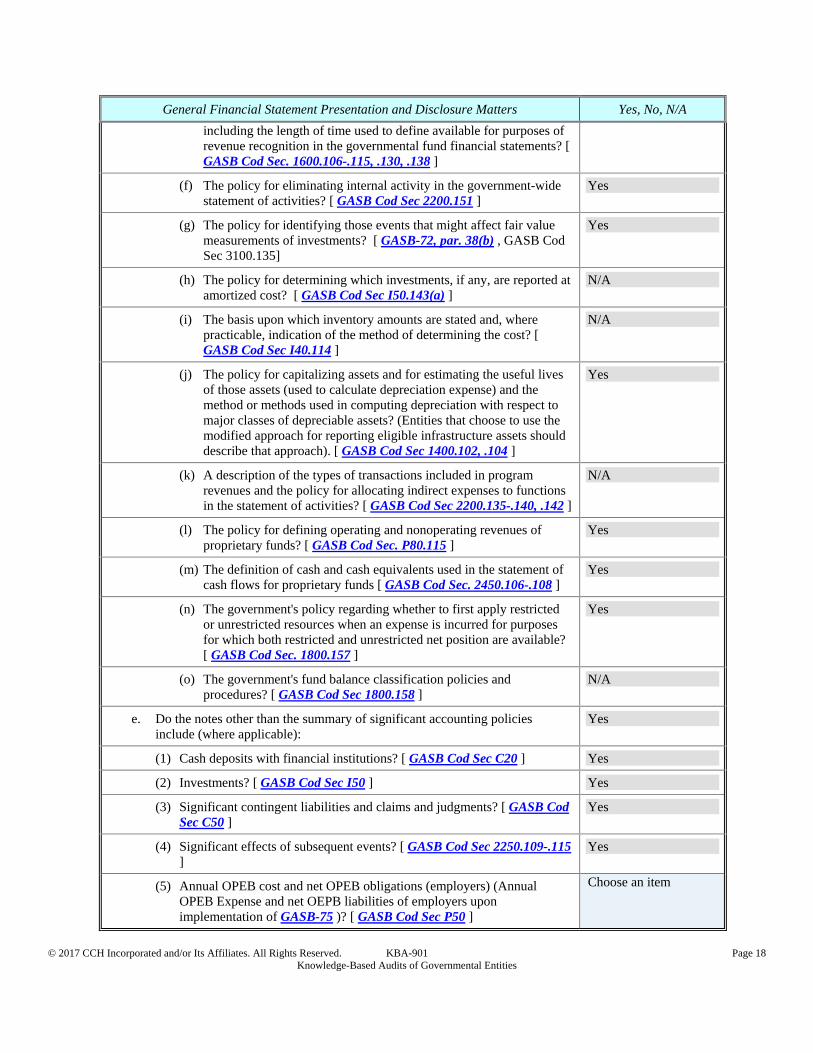

including the length of time used to define available for purposes of revenue recognition in the governmental fund financial statements? [ GASB Cod Sec. 1600.106-.115, .130, .138 ]

(f) The policy for eliminating internal activity in the government-wide statement of activities? [ GASB Cod Sec 2200.151 ]

Yes

(g) The policy for identifying those events that might affect fair value measurements of investments? [ GASB-72, par. 38(b) , GASB Cod Sec 3100.135]

Yes

(h) The policy for determining which investments, if any, are reported at amortized cost? [ GASB Cod Sec I50.143(a) ]

N/A

(i) The basis upon which inventory amounts are stated and, where practicable, indication of the method of determining the cost? [ GASB Cod Sec I40.114 ]

N/A

(j) The policy for capitalizing assets and for estimating the useful lives of those assets (used to calculate depreciation expense) and the method or methods used in computing depreciation with respect to major classes of depreciable assets? (Entities that choose to use the modified approach for reporting eligible infrastructure assets should describe that approach). [ GASB Cod Sec 1400.102, .104 ]

Yes

(k) A description of the types of transactions included in program revenues and the policy for allocating indirect expenses to functions in the statement of activities? [ GASB Cod Sec 2200.135-.140, .142 ]

N/A

(l) The policy for defining operating and nonoperating revenues of proprietary funds? [ GASB Cod Sec. P80.115 ]

Yes

(m) The definition of cash and cash equivalents used in the statement of cash flows for proprietary funds [ GASB Cod Sec. 2450.106-.108 ]

Yes

(n) The government's policy regarding whether to first apply restricted or unrestricted resources when an expense is incurred for purposes for which both restricted and unrestricted net position are available? [ GASB Cod Sec. 1800.157 ]

Yes

(o) The government's fund balance classification policies and procedures? [ GASB Cod Sec 1800.158 ]

N/A

e. Do the notes other than the summary of significant accounting policies include (where applicable):

Yes

(1) Cash deposits with financial institutions? [ GASB Cod Sec C20 ] Yes

(2) Investments? [ GASB Cod Sec I50 ] Yes

(3) Significant contingent liabilities and claims and judgments? [ GASB Cod Sec C50 ]

Yes

(4) Significant effects of subsequent events? [ GASB Cod Sec 2250.109-.115 ]

Yes

(5) Annual OPEB cost and net OPEB obligations (employers) (Annual OPEB Expense and net OEPB liabilities of employers upon implementation of GASB-75 )? [ GASB Cod Sec P50 ]

Choose an item

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 19 Knowledge-Based Audits of Governmental Entities

General Financial Statement Presentation and Disclosure Matters Yes, No, N/A

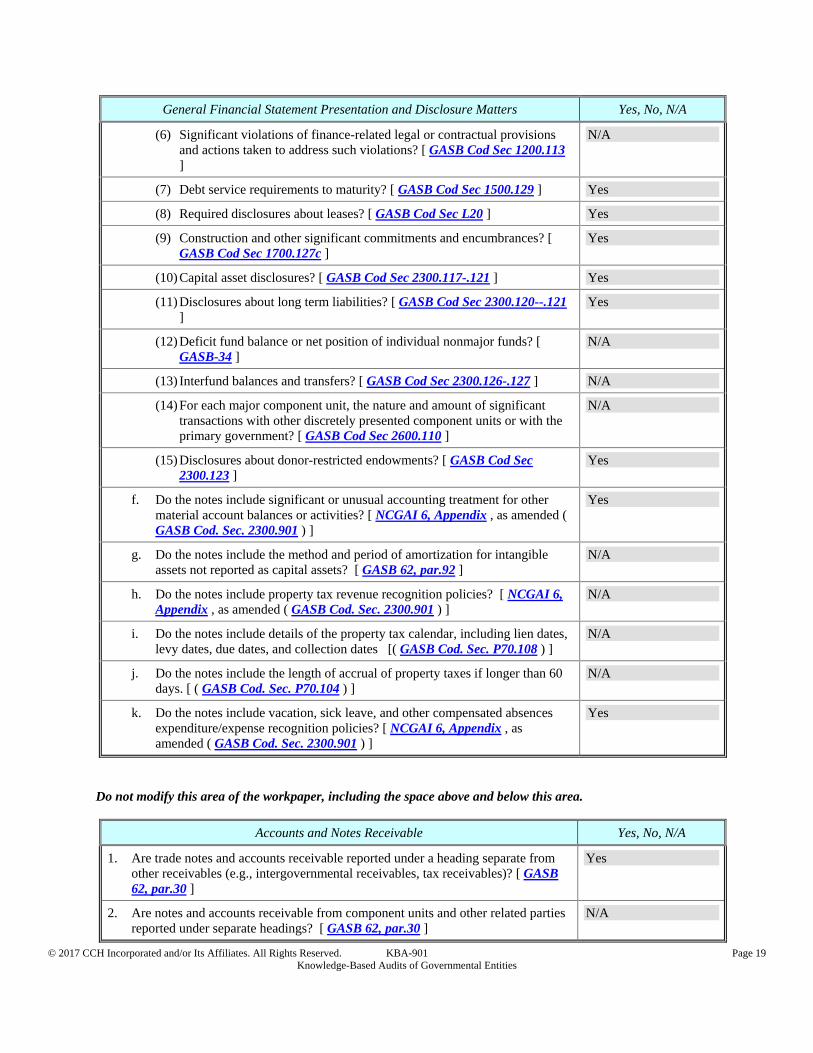

(6) Significant violations of finance-related legal or contractual provisions and actions taken to address such violations? [ GASB Cod Sec 1200.113 ]

N/A

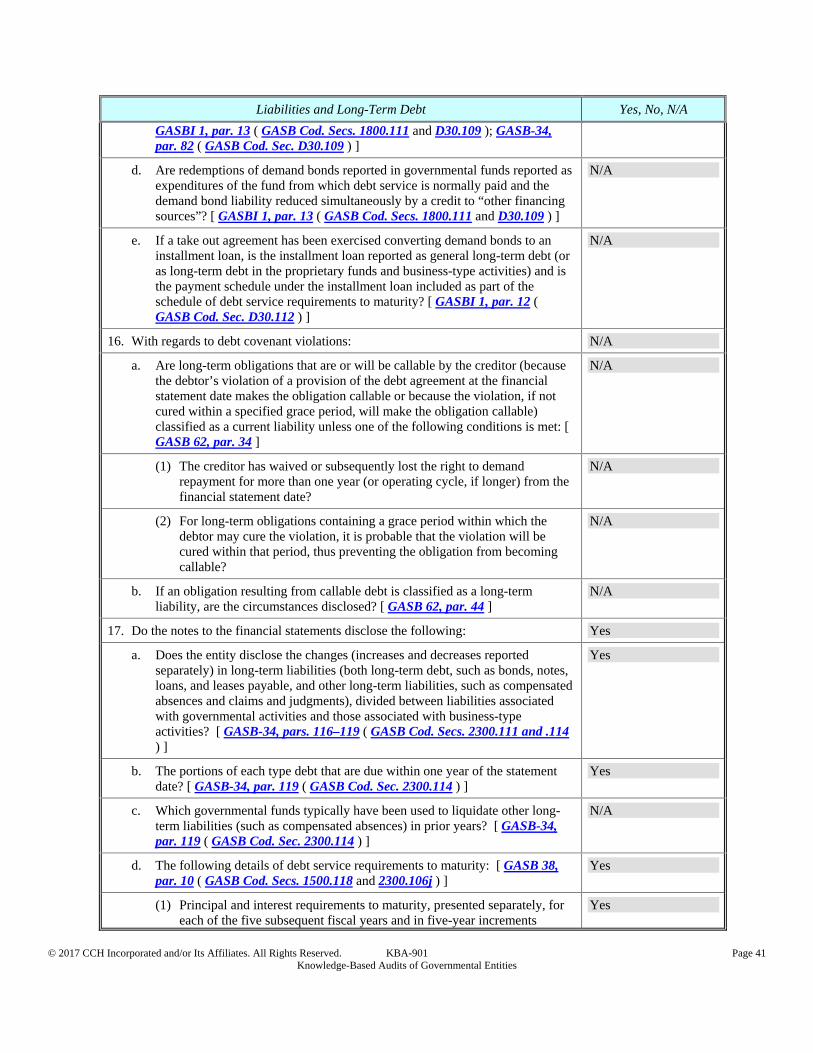

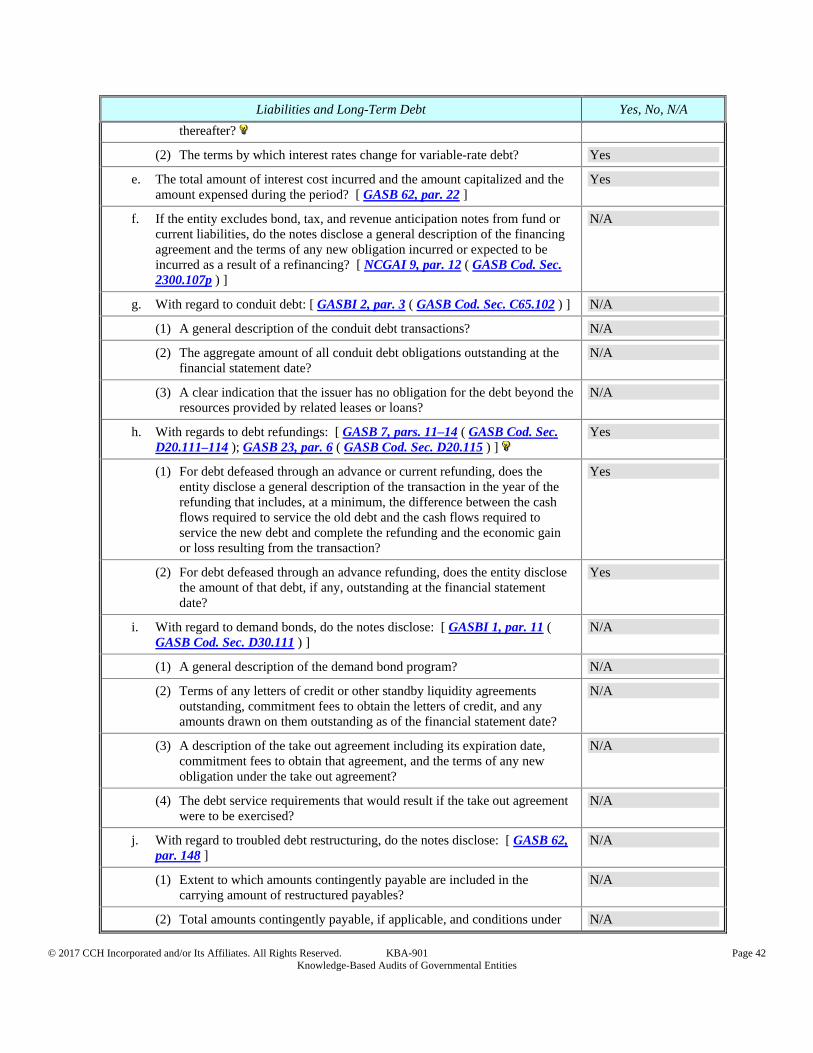

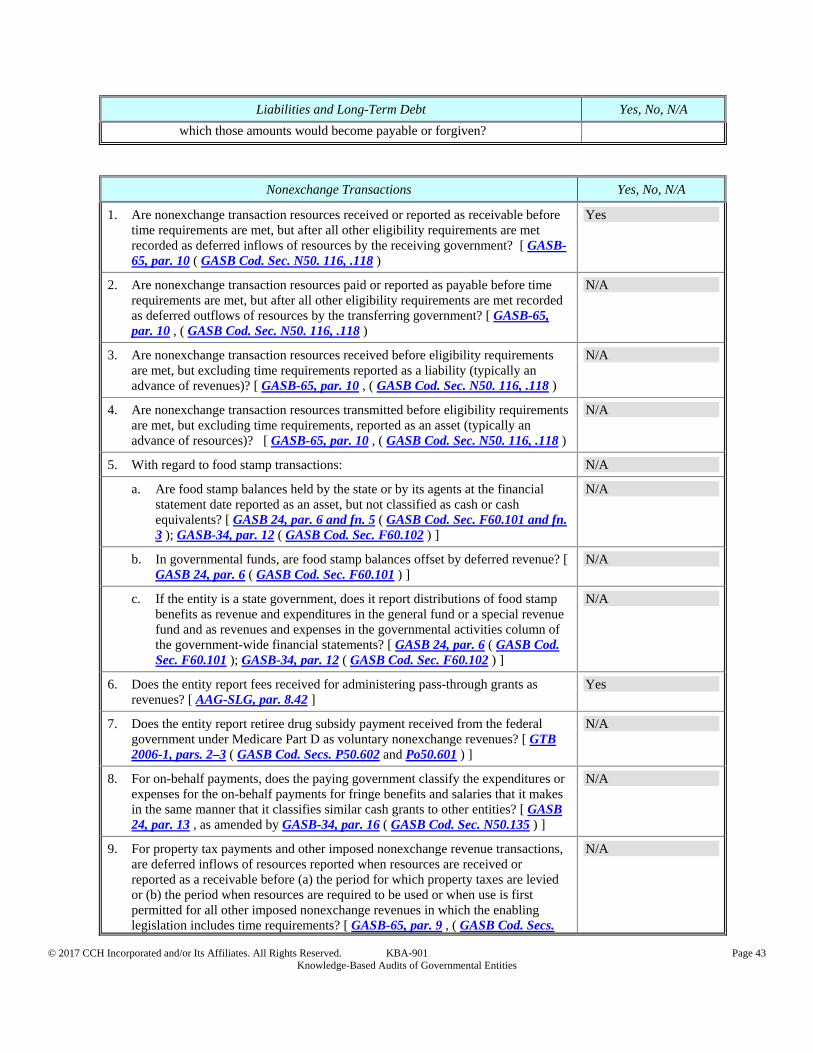

(7) Debt service requirements to maturity? [ GASB Cod Sec 1500.129 ] Yes

(8) Required disclosures about leases? [ GASB Cod Sec L20 ] Yes

(9) Construction and other significant commitments and encumbrances? [ GASB Cod Sec 1700.127c ]

Yes

(10) Capital asset disclosures? [ GASB Cod Sec 2300.117-.121 ] Yes

(11) Disclosures about long term liabilities? [ GASB Cod Sec 2300.120--.121 ]

Yes

(12) Deficit fund balance or net position of individual nonmajor funds? [ GASB-34 ]

N/A

(13) Interfund balances and transfers? [ GASB Cod Sec 2300.126-.127 ] N/A

(14) For each major component unit, the nature and amount of significant transactions with other discretely presented component units or with the primary government? [ GASB Cod Sec 2600.110 ]

N/A

(15) Disclosures about donor-restricted endowments? [ GASB Cod Sec 2300.123 ]

Yes

f. Do the notes include significant or unusual accounting treatment for other material account balances or activities? [ NCGAI 6, Appendix , as amended ( GASB Cod. Sec. 2300.901 ) ]

Yes

g. Do the notes include the method and period of amortization for intangible assets not reported as capital assets? [ GASB 62, par.92 ]

N/A

h. Do the notes include property tax revenue recognition policies? [ NCGAI 6, Appendix , as amended ( GASB Cod. Sec. 2300.901 ) ]

N/A

i. Do the notes include details of the property tax calendar, including lien dates, levy dates, due dates, and collection dates [( GASB Cod. Sec. P70.108 ) ]

N/A

j. Do the notes include the length of accrual of property taxes if longer than 60 days. [ ( GASB Cod. Sec. P70.104 ) ]

N/A

k. Do the notes include vacation, sick leave, and other compensated absences expenditure/expense recognition policies? [ NCGAI 6, Appendix , as amended ( GASB Cod. Sec. 2300.901 ) ]

Yes

Do not modify this area of the workpaper, including the space above and below this area.

Accounts and Notes Receivable Yes, No, N/A

1. Are trade notes and accounts receivable reported under a heading separate from other receivables (e.g., intergovernmental receivables, tax receivables)? [ GASB 62, par.30 ]

Yes

2. Are notes and accounts receivable from component units and other related parties reported under separate headings? [ GASB 62, par.30 ]

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 20 Knowledge-Based Audits of Governmental Entities

Accounts and Notes Receivable Yes, No, N/A

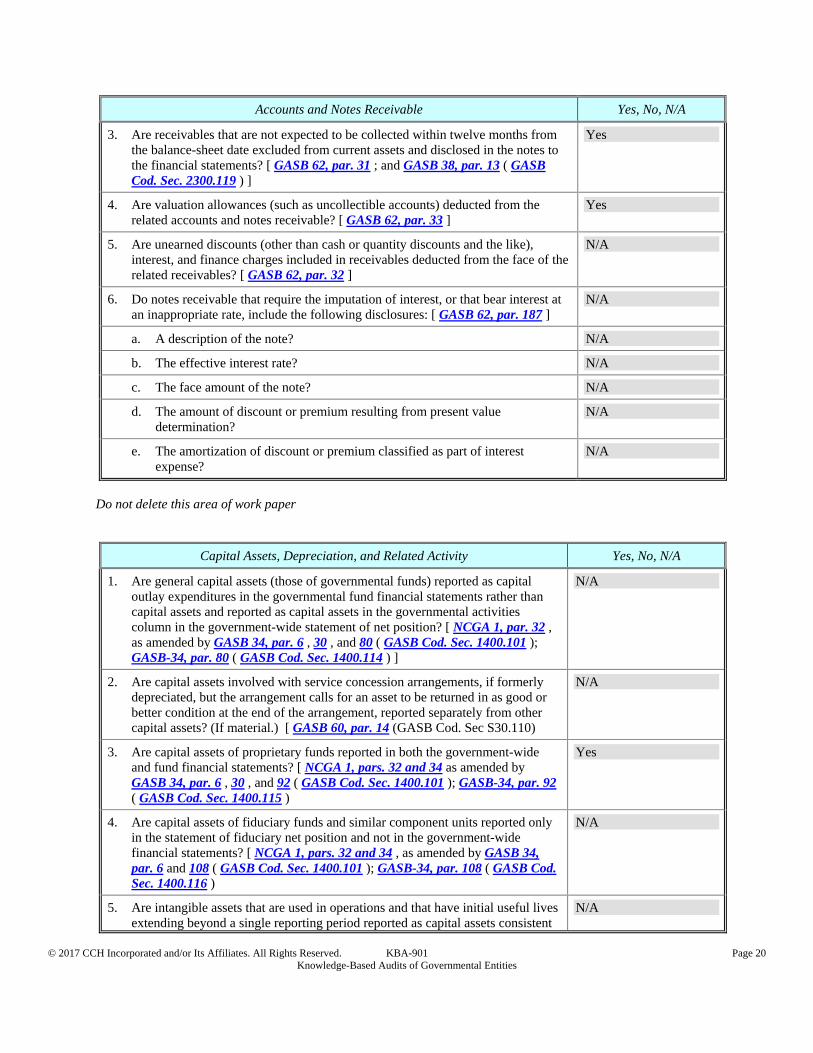

3. Are receivables that are not expected to be collected within twelve months from the balance-sheet date excluded from current assets and disclosed in the notes to the financial statements? [ GASB 62, par. 31 ; and GASB 38, par. 13 ( GASB Cod. Sec. 2300.119 ) ]

Yes

4. Are valuation allowances (such as uncollectible accounts) deducted from the related accounts and notes receivable? [ GASB 62, par. 33 ]

Yes

5. Are unearned discounts (other than cash or quantity discounts and the like), interest, and finance charges included in receivables deducted from the face of the related receivables? [ GASB 62, par. 32 ]

N/A

6. Do notes receivable that require the imputation of interest, or that bear interest at an inappropriate rate, include the following disclosures: [ GASB 62, par. 187 ]

N/A

a. A description of the note? N/A

b. The effective interest rate? N/A

c. The face amount of the note? N/A

d. The amount of discount or premium resulting from present value determination?

N/A

e. The amortization of discount or premium classified as part of interest expense?

N/A

Do not delete this area of work paper

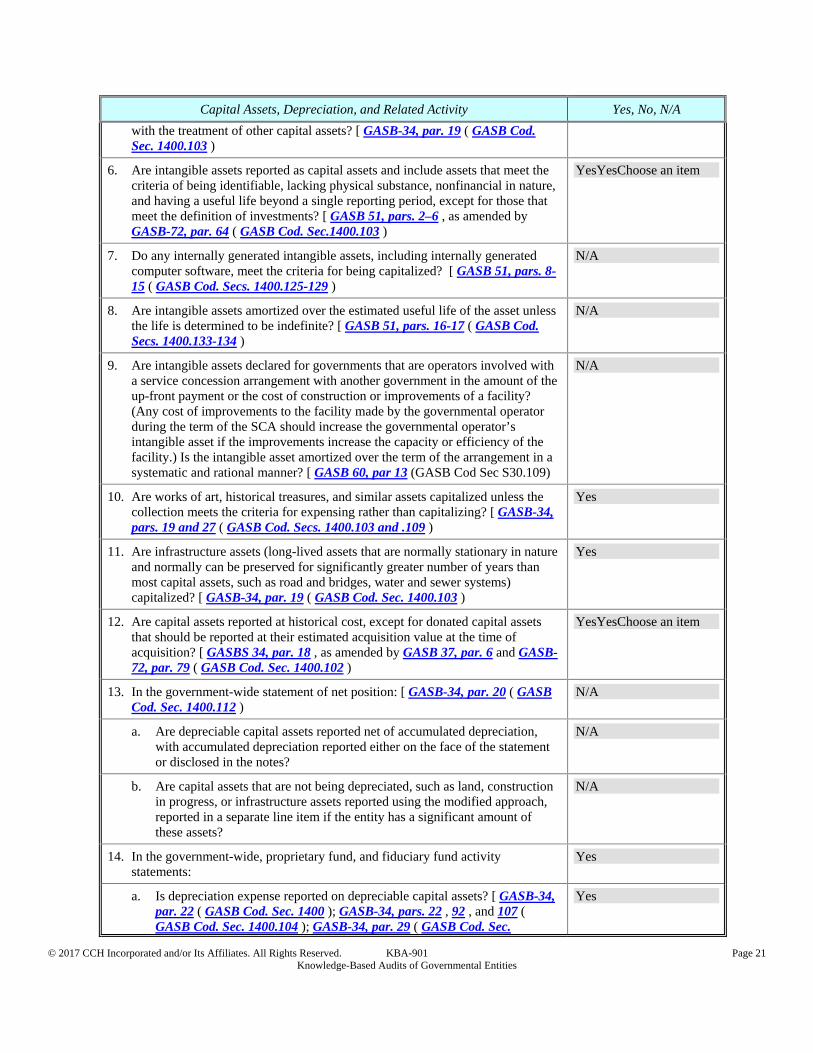

Capital Assets, Depreciation, and Related Activity Yes, No, N/A

1. Are general capital assets (those of governmental funds) reported as capital outlay expenditures in the governmental fund financial statements rather than capital assets and reported as capital assets in the governmental activities column in the government-wide statement of net position? [ NCGA 1, par. 32 , as amended by GASB 34, par. 6 , 30 , and 80 ( GASB Cod. Sec. 1400.101 ); GASB-34, par. 80 ( GASB Cod. Sec. 1400.114 ) ]

N/A

2. Are capital assets involved with service concession arrangements, if formerly depreciated, but the arrangement calls for an asset to be returned in as good or better condition at the end of the arrangement, reported separately from other capital assets? (If material.) [ GASB 60, par. 14 (GASB Cod. Sec S30.110)

N/A

3. Are capital assets of proprietary funds reported in both the government-wide and fund financial statements? [ NCGA 1, pars. 32 and 34 as amended by GASB 34, par. 6 , 30 , and 92 ( GASB Cod. Sec. 1400.101 ); GASB-34, par. 92 ( GASB Cod. Sec. 1400.115 )

Yes

4. Are capital assets of fiduciary funds and similar component units reported only in the statement of fiduciary net position and not in the government-wide financial statements? [ NCGA 1, pars. 32 and 34 , as amended by GASB 34, par. 6 and 108 ( GASB Cod. Sec. 1400.101 ); GASB-34, par. 108 ( GASB Cod. Sec. 1400.116 )

N/A

5. Are intangible assets that are used in operations and that have initial useful lives extending beyond a single reporting period reported as capital assets consistent

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 21 Knowledge-Based Audits of Governmental Entities

Capital Assets, Depreciation, and Related Activity Yes, No, N/A

with the treatment of other capital assets? [ GASB-34, par. 19 ( GASB Cod. Sec. 1400.103 )

6. Are intangible assets reported as capital assets and include assets that meet the criteria of being identifiable, lacking physical substance, nonfinancial in nature, and having a useful life beyond a single reporting period, except for those that meet the definition of investments? [ GASB 51, pars. 2–6 , as amended by GASB-72, par. 64 ( GASB Cod. Sec.1400.103 )

YesYesChoose an item

7. Do any internally generated intangible assets, including internally generated computer software, meet the criteria for being capitalized? [ GASB 51, pars. 8-15 ( GASB Cod. Secs. 1400.125-129 )

N/A

8. Are intangible assets amortized over the estimated useful life of the asset unless the life is determined to be indefinite? [ GASB 51, pars. 16-17 ( GASB Cod. Secs. 1400.133-134 )

N/A

9. Are intangible assets declared for governments that are operators involved with a service concession arrangement with another government in the amount of the up-front payment or the cost of construction or improvements of a facility? (Any cost of improvements to the facility made by the governmental operator during the term of the SCA should increase the governmental operator’s intangible asset if the improvements increase the capacity or efficiency of the facility.) Is the intangible asset amortized over the term of the arrangement in a systematic and rational manner? [ GASB 60, par 13 (GASB Cod Sec S30.109)

N/A

10. Are works of art, historical treasures, and similar assets capitalized unless the collection meets the criteria for expensing rather than capitalizing? [ GASB-34, pars. 19 and 27 ( GASB Cod. Secs. 1400.103 and .109 )

Yes

11. Are infrastructure assets (long-lived assets that are normally stationary in nature and normally can be preserved for significantly greater number of years than most capital assets, such as road and bridges, water and sewer systems) capitalized? [ GASB-34, par. 19 ( GASB Cod. Sec. 1400.103 )

Yes

12. Are capital assets reported at historical cost, except for donated capital assets that should be reported at their estimated acquisition value at the time of acquisition? [ GASBS 34, par. 18 , as amended by GASB 37, par. 6 and GASB-72, par. 79 ( GASB Cod. Sec. 1400.102 )

YesYesChoose an item

13. In the government-wide statement of net position: [ GASB-34, par. 20 ( GASB Cod. Sec. 1400.112 )

N/A

a. Are depreciable capital assets reported net of accumulated depreciation, with accumulated depreciation reported either on the face of the statement or disclosed in the notes?

N/A

b. Are capital assets that are not being depreciated, such as land, construction in progress, or infrastructure assets reported using the modified approach, reported in a separate line item if the entity has a significant amount of these assets?

N/A

14. In the government-wide, proprietary fund, and fiduciary fund activity statements:

Yes

a. Is depreciation expense reported on depreciable capital assets? [ GASB-34, par. 22 ( GASB Cod. Sec. 1400 ); GASB-34, pars. 22 , 92 , and 107 ( GASB Cod. Sec. 1400.104 ); GASB-34, par. 29 ( GASB Cod. Sec.

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 22 Knowledge-Based Audits of Governmental Entities

Capital Assets, Depreciation, and Related Activity Yes, No, N/A

1400.111 )

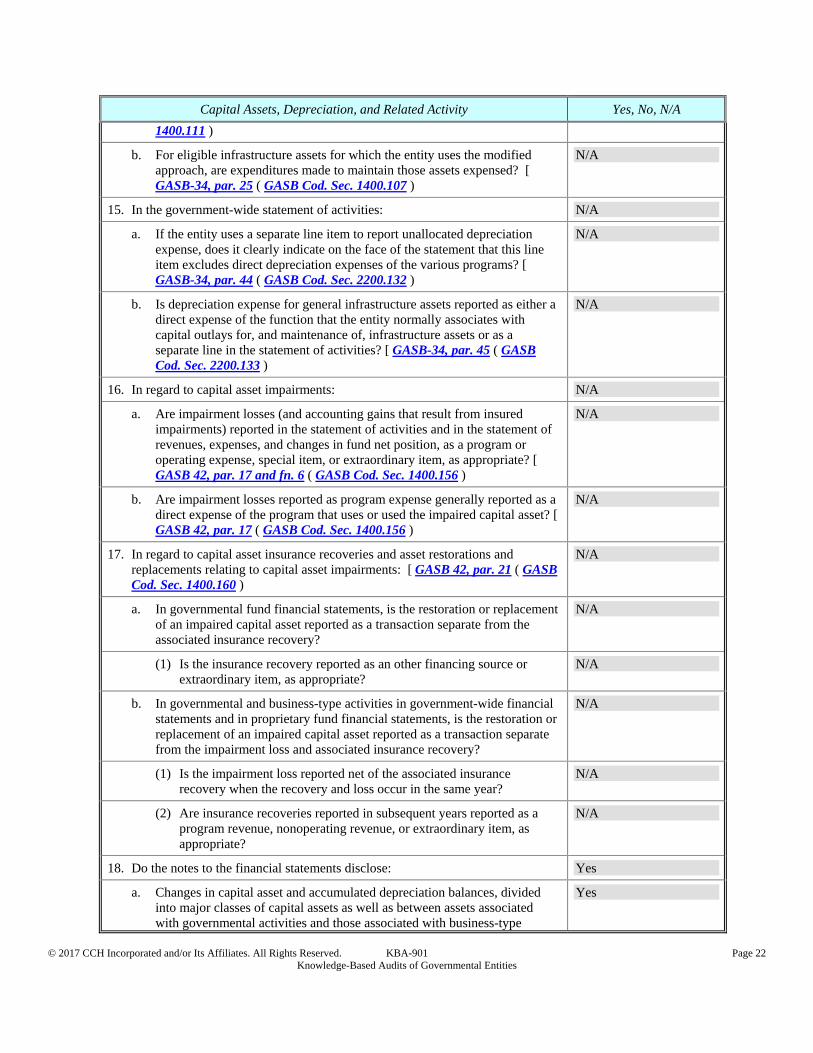

b. For eligible infrastructure assets for which the entity uses the modified approach, are expenditures made to maintain those assets expensed? [ GASB-34, par. 25 ( GASB Cod. Sec. 1400.107 )

N/A

15. In the government-wide statement of activities: N/A

a. If the entity uses a separate line item to report unallocated depreciation expense, does it clearly indicate on the face of the statement that this line item excludes direct depreciation expenses of the various programs? [ GASB-34, par. 44 ( GASB Cod. Sec. 2200.132 )

N/A

b. Is depreciation expense for general infrastructure assets reported as either a direct expense of the function that the entity normally associates with capital outlays for, and maintenance of, infrastructure assets or as a separate line in the statement of activities? [ GASB-34, par. 45 ( GASB Cod. Sec. 2200.133 )

N/A

16. In regard to capital asset impairments: N/A

a. Are impairment losses (and accounting gains that result from insured impairments) reported in the statement of activities and in the statement of revenues, expenses, and changes in fund net position, as a program or operating expense, special item, or extraordinary item, as appropriate? [ GASB 42, par. 17 and fn. 6 ( GASB Cod. Sec. 1400.156 )

N/A

b. Are impairment losses reported as program expense generally reported as a direct expense of the program that uses or used the impaired capital asset? [ GASB 42, par. 17 ( GASB Cod. Sec. 1400.156 )

N/A

17. In regard to capital asset insurance recoveries and asset restorations and replacements relating to capital asset impairments: [ GASB 42, par. 21 ( GASB Cod. Sec. 1400.160 )

N/A

a. In governmental fund financial statements, is the restoration or replacement of an impaired capital asset reported as a transaction separate from the associated insurance recovery?

N/A

(1) Is the insurance recovery reported as an other financing source or extraordinary item, as appropriate?

N/A

b. In governmental and business-type activities in government-wide financial statements and in proprietary fund financial statements, is the restoration or replacement of an impaired capital asset reported as a transaction separate from the impairment loss and associated insurance recovery?

N/A

(1) Is the impairment loss reported net of the associated insurance recovery when the recovery and loss occur in the same year?

N/A

(2) Are insurance recoveries reported in subsequent years reported as a program revenue, nonoperating revenue, or extraordinary item, as appropriate?

N/A

18. Do the notes to the financial statements disclose: Yes

a. Changes in capital asset and accumulated depreciation balances, divided into major classes of capital assets as well as between assets associated with governmental activities and those associated with business-type

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 23 Knowledge-Based Audits of Governmental Entities

Capital Assets, Depreciation, and Related Activity Yes, No, N/A

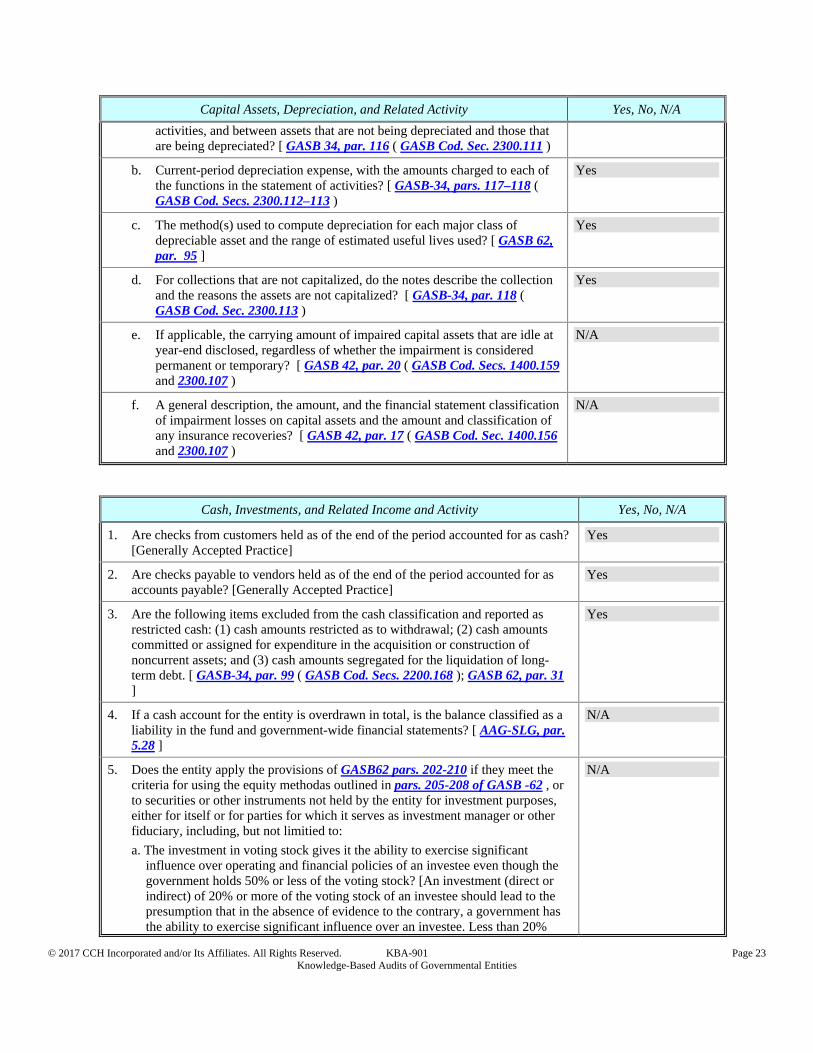

activities, and between assets that are not being depreciated and those that are being depreciated? [ GASB 34, par. 116 ( GASB Cod. Sec. 2300.111 )

b. Current-period depreciation expense, with the amounts charged to each of the functions in the statement of activities? [ GASB-34, pars. 117–118 ( GASB Cod. Secs. 2300.112–113 )

Yes

c. The method(s) used to compute depreciation for each major class of depreciable asset and the range of estimated useful lives used? [ GASB 62, par. 95 ]

Yes

d. For collections that are not capitalized, do the notes describe the collection and the reasons the assets are not capitalized? [ GASB-34, par. 118 ( GASB Cod. Sec. 2300.113 )

Yes

e. If applicable, the carrying amount of impaired capital assets that are idle at year-end disclosed, regardless of whether the impairment is considered permanent or temporary? [ GASB 42, par. 20 ( GASB Cod. Secs. 1400.159 and 2300.107 )

N/A

f. A general description, the amount, and the financial statement classification of impairment losses on capital assets and the amount and classification of any insurance recoveries? [ GASB 42, par. 17 ( GASB Cod. Sec. 1400.156 and 2300.107 )

N/A

Cash, Investments, and Related Income and Activity Yes, No, N/A

1. Are checks from customers held as of the end of the period accounted for as cash? [Generally Accepted Practice]

Yes

2. Are checks payable to vendors held as of the end of the period accounted for as accounts payable? [Generally Accepted Practice]

Yes

3. Are the following items excluded from the cash classification and reported as restricted cash: (1) cash amounts restricted as to withdrawal; (2) cash amounts committed or assigned for expenditure in the acquisition or construction of noncurrent assets; and (3) cash amounts segregated for the liquidation of long-term debt. [ GASB-34, par. 99 ( GASB Cod. Secs. 2200.168 ); GASB 62, par. 31 ]

Yes

4. If a cash account for the entity is overdrawn in total, is the balance classified as a liability in the fund and government-wide financial statements? [ AAG-SLG, par. 5.28 ]

N/A

5. Does the entity apply the provisions of GASB62 pars. 202-210 if they meet the criteria for using the equity methodas outlined in pars. 205-208 of GASB -62 , or to securities or other instruments not held by the entity for investment purposes, either for itself or for parties for which it serves as investment manager or other fiduciary, including, but not limitied to:

a. The investment in voting stock gives it the ability to exercise significant influence over operating and financial policies of an investee even though the government holds 50% or less of the voting stock? [An investment (direct or indirect) of 20% or more of the voting stock of an investee should lead to the presumption that in the absence of evidence to the contrary, a government has the ability to exercise significant influence over an investee. Less than 20%

N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 24 Knowledge-Based Audits of Governmental Entities

Cash, Investments, and Related Income and Activity Yes, No, N/A

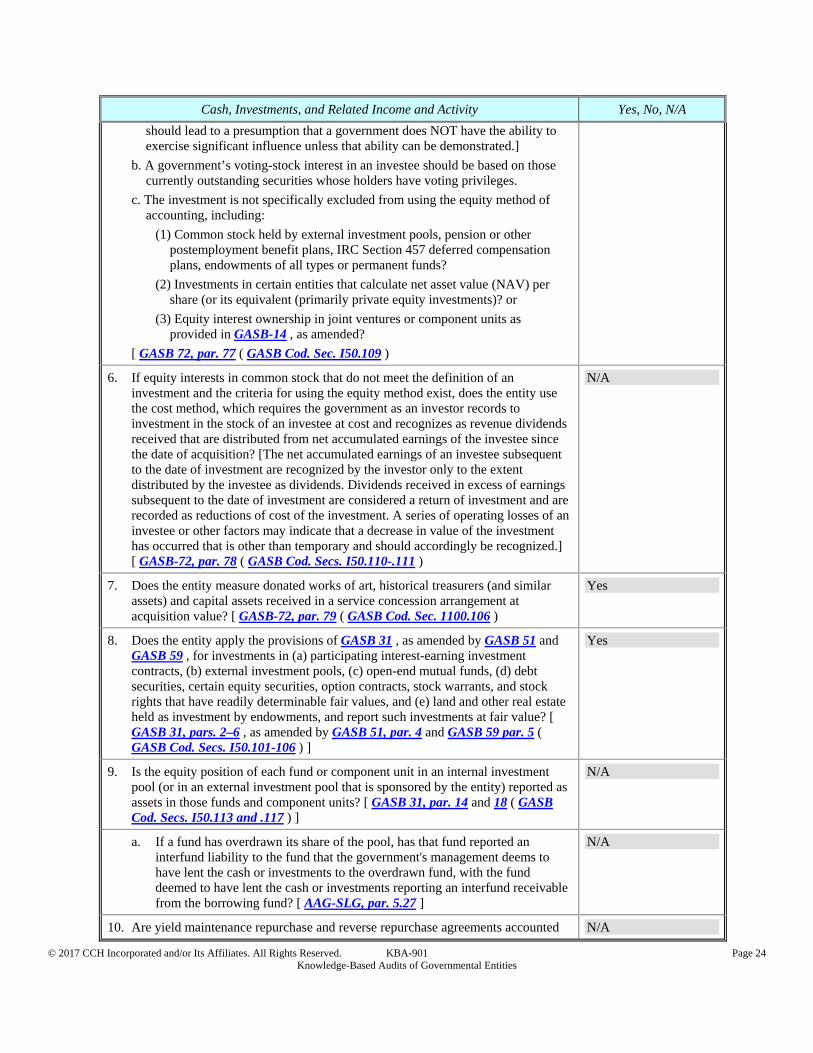

should lead to a presumption that a government does NOT have the ability to exercise significant influence unless that ability can be demonstrated.]

b. A government’s voting-stock interest in an investee should be based on those currently outstanding securities whose holders have voting privileges.

c. The investment is not specifically excluded from using the equity method of accounting, including:

(1) Common stock held by external investment pools, pension or other postemployment benefit plans, IRC Section 457 deferred compensation plans, endowments of all types or permanent funds?

(2) Investments in certain entities that calculate net asset value (NAV) per share (or its equivalent (primarily private equity investments)? or

(3) Equity interest ownership in joint ventures or component units as provided in GASB-14 , as amended?

[ GASB 72, par. 77 ( GASB Cod. Sec. I50.109 )

6. If equity interests in common stock that do not meet the definition of an investment and the criteria for using the equity method exist, does the entity use the cost method, which requires the government as an investor records to investment in the stock of an investee at cost and recognizes as revenue dividends received that are distributed from net accumulated earnings of the investee since the date of acquisition? [The net accumulated earnings of an investee subsequent to the date of investment are recognized by the investor only to the extent distributed by the investee as dividends. Dividends received in excess of earnings subsequent to the date of investment are considered a return of investment and are recorded as reductions of cost of the investment. A series of operating losses of an investee or other factors may indicate that a decrease in value of the investment has occurred that is other than temporary and should accordingly be recognized.] [ GASB-72, par. 78 ( GASB Cod. Secs. I50.110-.111 )

N/A

7. Does the entity measure donated works of art, historical treasurers (and similar assets) and capital assets received in a service concession arrangement at acquisition value? [ GASB-72, par. 79 ( GASB Cod. Sec. 1100.106 )

Yes

8. Does the entity apply the provisions of GASB 31 , as amended by GASB 51 and GASB 59 , for investments in (a) participating interest-earning investment contracts, (b) external investment pools, (c) open-end mutual funds, (d) debt securities, certain equity securities, option contracts, stock warrants, and stock rights that have readily determinable fair values, and (e) land and other real estate held as investment by endowments, and report such investments at fair value? [ GASB 31, pars. 2–6 , as amended by GASB 51, par. 4 and GASB 59 par. 5 ( GASB Cod. Secs. I50.101-106 ) ]

Yes

9. Is the equity position of each fund or component unit in an internal investment pool (or in an external investment pool that is sponsored by the entity) reported as assets in those funds and component units? [ GASB 31, par. 14 and 18 ( GASB Cod. Secs. I50.113 and .117 ) ]

N/A

a. If a fund has overdrawn its share of the pool, has that fund reported an interfund liability to the fund that the government's management deems to have lent the cash or investments to the overdrawn fund, with the fund deemed to have lent the cash or investments reporting an interfund receivable from the borrowing fund? [ AAG-SLG, par. 5.27 ]

N/A

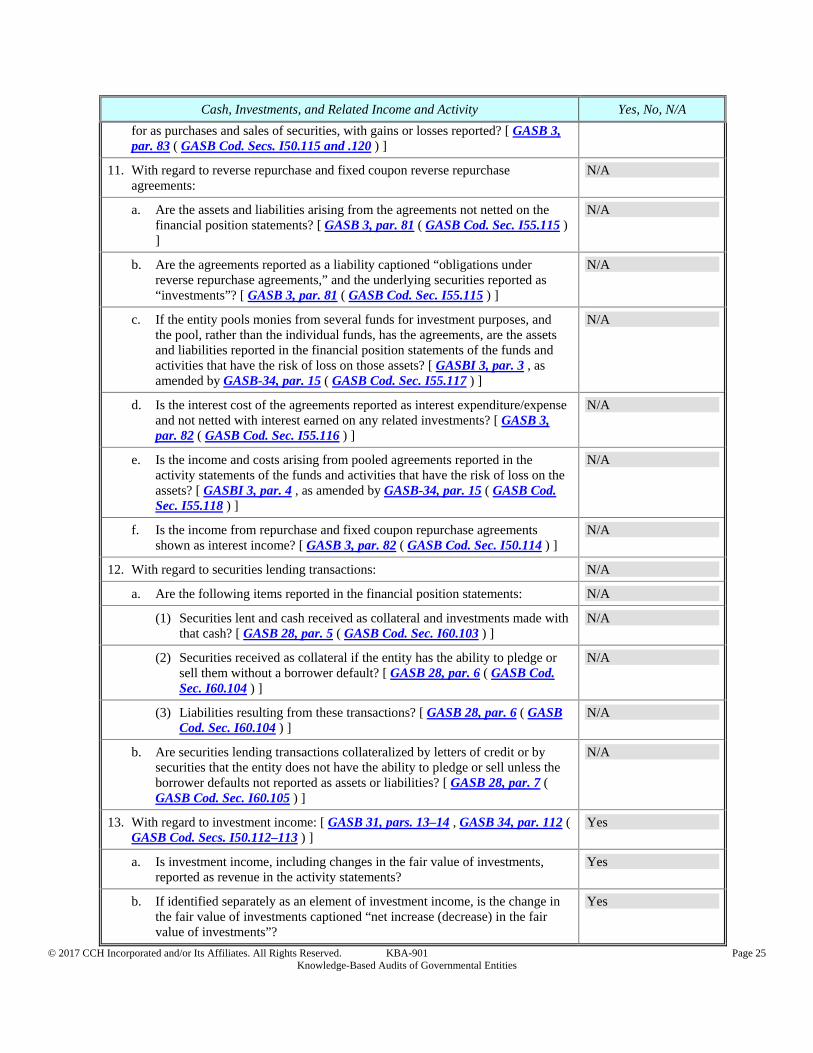

10. Are yield maintenance repurchase and reverse repurchase agreements accounted N/A

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 25 Knowledge-Based Audits of Governmental Entities

Cash, Investments, and Related Income and Activity Yes, No, N/A

for as purchases and sales of securities, with gains or losses reported? [ GASB 3, par. 83 ( GASB Cod. Secs. I50.115 and .120 ) ]

11. With regard to reverse repurchase and fixed coupon reverse repurchase agreements:

N/A

a. Are the assets and liabilities arising from the agreements not netted on the financial position statements? [ GASB 3, par. 81 ( GASB Cod. Sec. I55.115 ) ]

N/A

b. Are the agreements reported as a liability captioned “obligations under reverse repurchase agreements,” and the underlying securities reported as “investments”? [ GASB 3, par. 81 ( GASB Cod. Sec. I55.115 ) ]

N/A

c. If the entity pools monies from several funds for investment purposes, and the pool, rather than the individual funds, has the agreements, are the assets and liabilities reported in the financial position statements of the funds and activities that have the risk of loss on those assets? [ GASBI 3, par. 3 , as amended by GASB-34, par. 15 ( GASB Cod. Sec. I55.117 ) ]

N/A

d. Is the interest cost of the agreements reported as interest expenditure/expense and not netted with interest earned on any related investments? [ GASB 3, par. 82 ( GASB Cod. Sec. I55.116 ) ]

N/A

e. Is the income and costs arising from pooled agreements reported in the activity statements of the funds and activities that have the risk of loss on the assets? [ GASBI 3, par. 4 , as amended by GASB-34, par. 15 ( GASB Cod. Sec. I55.118 ) ]

N/A

f. Is the income from repurchase and fixed coupon repurchase agreements shown as interest income? [ GASB 3, par. 82 ( GASB Cod. Sec. I50.114 ) ]

N/A

12. With regard to securities lending transactions: N/A

a. Are the following items reported in the financial position statements: N/A

(1) Securities lent and cash received as collateral and investments made with that cash? [ GASB 28, par. 5 ( GASB Cod. Sec. I60.103 ) ]

N/A

(2) Securities received as collateral if the entity has the ability to pledge or sell them without a borrower default? [ GASB 28, par. 6 ( GASB Cod. Sec. I60.104 ) ]

N/A

(3) Liabilities resulting from these transactions? [ GASB 28, par. 6 ( GASB Cod. Sec. I60.104 ) ]

N/A

b. Are securities lending transactions collateralized by letters of credit or by securities that the entity does not have the ability to pledge or sell unless the borrower defaults not reported as assets or liabilities? [ GASB 28, par. 7 ( GASB Cod. Sec. I60.105 ) ]

N/A

13. With regard to investment income: [ GASB 31, pars. 13–14 , GASB 34, par. 112 ( GASB Cod. Secs. I50.112–113 ) ]

Yes

a. Is investment income, including changes in the fair value of investments, reported as revenue in the activity statements?

Yes

b. If identified separately as an element of investment income, is the change in the fair value of investments captioned “net increase (decrease) in the fair value of investments”?

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 26 Knowledge-Based Audits of Governmental Entities

Cash, Investments, and Related Income and Activity Yes, No, N/A

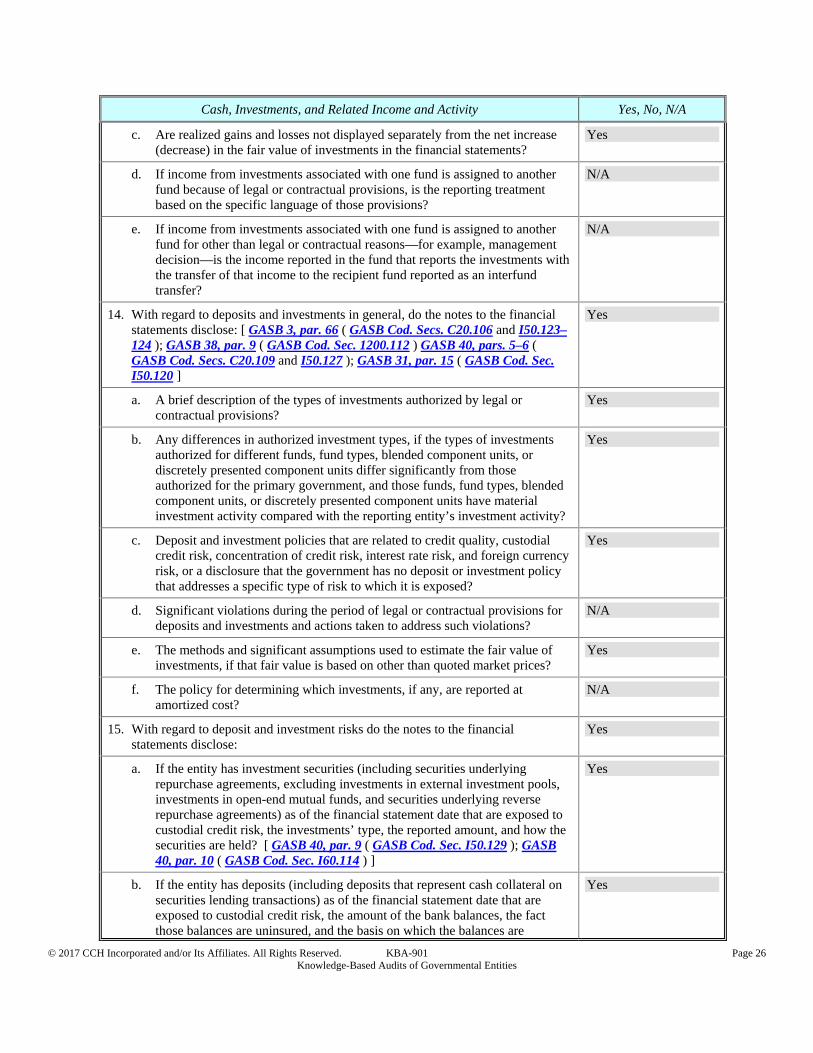

c. Are realized gains and losses not displayed separately from the net increase (decrease) in the fair value of investments in the financial statements?

Yes

d. If income from investments associated with one fund is assigned to another fund because of legal or contractual provisions, is the reporting treatment based on the specific language of those provisions?

N/A

e. If income from investments associated with one fund is assigned to another fund for other than legal or contractual reasons—for example, management decision—is the income reported in the fund that reports the investments with the transfer of that income to the recipient fund reported as an interfund transfer?

N/A

14. With regard to deposits and investments in general, do the notes to the financial statements disclose: [ GASB 3, par. 66 ( GASB Cod. Secs. C20.106 and I50.123–124 ); GASB 38, par. 9 ( GASB Cod. Sec. 1200.112 ) GASB 40, pars. 5–6 ( GASB Cod. Secs. C20.109 and I50.127 ); GASB 31, par. 15 ( GASB Cod. Sec. I50.120 ]

Yes

a. A brief description of the types of investments authorized by legal or contractual provisions?

Yes

b. Any differences in authorized investment types, if the types of investments authorized for different funds, fund types, blended component units, or discretely presented component units differ significantly from those authorized for the primary government, and those funds, fund types, blended component units, or discretely presented component units have material investment activity compared with the reporting entity’s investment activity?

Yes

c. Deposit and investment policies that are related to credit quality, custodial credit risk, concentration of credit risk, interest rate risk, and foreign currency risk, or a disclosure that the government has no deposit or investment policy that addresses a specific type of risk to which it is exposed?

Yes

d. Significant violations during the period of legal or contractual provisions for deposits and investments and actions taken to address such violations?

N/A

e. The methods and significant assumptions used to estimate the fair value of investments, if that fair value is based on other than quoted market prices?

Yes

f. The policy for determining which investments, if any, are reported at amortized cost?

N/A

15. With regard to deposit and investment risks do the notes to the financial statements disclose:

Yes

a. If the entity has investment securities (including securities underlying repurchase agreements, excluding investments in external investment pools, investments in open-end mutual funds, and securities underlying reverse repurchase agreements) as of the financial statement date that are exposed to custodial credit risk, the investments’ type, the reported amount, and how the securities are held? [ GASB 40, par. 9 ( GASB Cod. Sec. I50.129 ); GASB 40, par. 10 ( GASB Cod. Sec. I60.114 ) ]

Yes

b. If the entity has deposits (including deposits that represent cash collateral on securities lending transactions) as of the financial statement date that are exposed to custodial credit risk, the amount of the bank balances, the fact those balances are uninsured, and the basis on which the balances are

Yes

© 2017 CCH Incorporated and/or Its Affiliates. All Rights Reserved. KBA-901 Page 27 Knowledge-Based Audits of Governmental Entities

Cash, Investments, and Related Income and Activity Yes, No, N/A

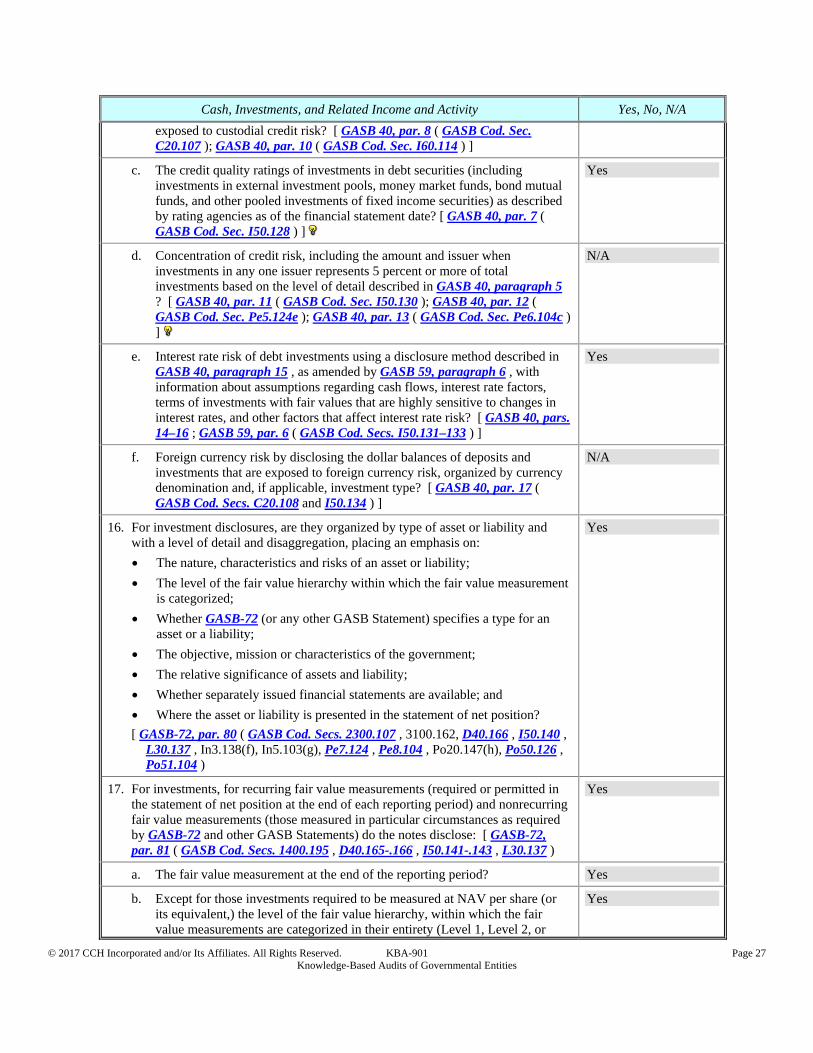

exposed to custodial credit risk? [ GASB 40, par. 8 ( GASB Cod. Sec. C20.107 ); GASB 40, par. 10 ( GASB Cod. Sec. I60.114 ) ]

c. The credit quality ratings of investments in debt securities (including investments in external investment pools, money market funds, bond mutual funds, and other pooled investments of fixed income securities) as described by rating agencies as of the financial statement date? [ GASB 40, par. 7 ( GASB Cod. Sec. I50.128 ) ]

Yes

d. Concentration of credit risk, including the amount and issuer when investments in any one issuer represents 5 percent or more of total investments based on the level of detail described in GASB 40, paragraph 5 ? [ GASB 40, par. 11 ( GASB Cod. Sec. I50.130 ); GASB 40, par. 12 ( GASB Cod. Sec. Pe5.124e ); GASB 40, par. 13 ( GASB Cod. Sec. Pe6.104c ) ]

N/A

e. Interest rate risk of debt investments using a disclosure method described in GASB 40, paragraph 15 , as amended by GASB 59, paragraph 6 , with information about assumptions regarding cash flows, interest rate factors, terms of investments with fair values that are highly sensitive to changes in interest rates, and other factors that affect interest rate risk? [ GASB 40, pars. 14–16 ; GASB 59, par. 6 ( GASB Cod. Secs. I50.131–133 ) ]

Yes

f. Foreign currency risk by disclosing the dollar balances of deposits and investments that are exposed to foreign currency risk, organized by currency denomination and, if applicable, investment type? [ GASB 40, par. 17 ( GASB Cod. Secs. C20.108 and I50.134 ) ]

N/A

16. For investment disclosures, are they organized by type of asset or liability and with a level of detail and disaggregation, placing an emphasis on:

The nature, characteristics and risks of an asset or liability;

The level of the fair value hierarchy within which the fair value measurement is categorized;

Whether GASB-72 (or any other GASB Statement) specifies a type for an asset or a liability;

The objective, mission or characteristics of the government;

The relative significance of assets and liability;

Whether separately issued financial statements are available; and

Where the asset or liability is presented in the statement of net position?

[ GASB-72, par. 80 ( GASB Cod. Secs. 2300.107 , 3100.162, D40.166 , I50.140 , L30.137 , In3.138(f), In5.103(g), Pe7.124 , Pe8.104 , Po20.147(h), Po50.126 , Po51.104 )

Yes

17. For investments, for recurring fair value measurements (required or permitted in the statement of net position at the end of each reporting period) and nonrecurring fair value measurements (those measured in particular circumstances as required by GASB-72 and other GASB Statements) do the notes disclose: [ GASB-72, par. 81 ( GASB Cod. Secs. 1400.195 , D40.165-.166 , I50.141-.143 , L30.137 )

Yes

a. The fair value measurement at the end of the reporting period? Yes

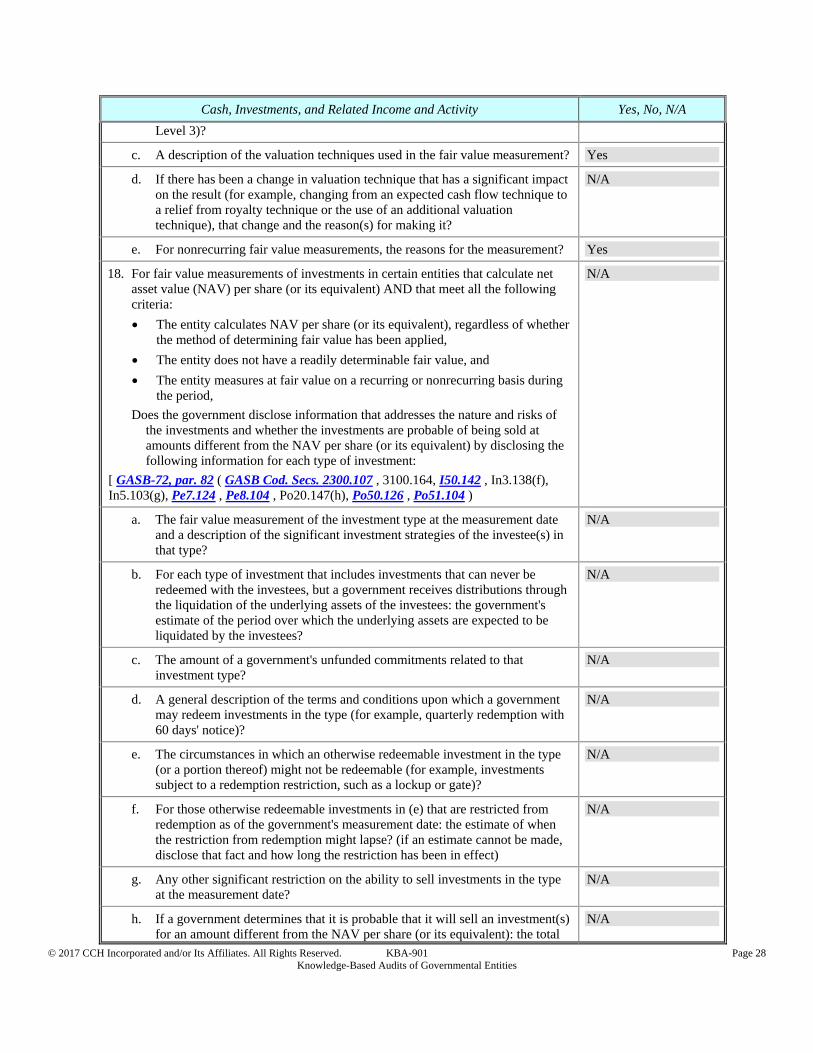

b. Except for those investments required to be measured at NAV per share (or its equivalent,) the level of the fair value hierarchy, within which the fair value measurements are categorized in their entirety (Level 1, Level 2, or

Yes