Embed Size (px)

Citation preview

FINANCIAL SERVICES

Technical Practices

Survey 2014

Risk and Capital Management

kpmg.co.uk

B TPS 2014

Contents

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

1 Foreword 1

2 Executive summary 2

3 Introduction 3

3.1: Objectives 3

3.2: Survey methodology 3

3.3: Topics of interest 4

3.4: Interpretation of the results 4

4 Profi le of Respondents 5

4.1: Profi le 5

4.2: Size of actuarial function 9

4.3: Which Peak is biting? 12

4.4: Which Pillar is biting? 12

5 Assets 13

5.1: Investment Strategy: Current vs. future Solvency II 14

5.2: Asset transition plan for Solvency II 15

5.3: Strategy for issuer options in light of the Matching Adjustment under Solvency II 16

5.4: Pillar 3 readiness for assets 17

5.5: Challenges faced when investing in alternative assets 18

5.6: Total assets and alternative assets 19

5.7: Rationale for investing in alternative assets 23

6 Solvency I 24

6.1: Base mortality assumptions 24

6.2: Mortality improvement model 26

6.3: Choice of CMI model 27

6.4: Long term improvement factor (CMI model) or underpin (cohort model) 28

6.5: Liquidity premium 29

7 With-Profi ts 30

7.1: The with-profi ts landscape 31

7.2: With-profi ts capital strength 33

7.3: Solvency II and with-profi ts 35

7.4: With-profi ts risk management 37

8 Risk Capital 41

8.1: All Risks 41

8.2: Market Risk Modelling 48

8.3: Interest Rate Risk 51

8.4: Credit Spread Risk 57

8.5: Equity risk 62

8.6: Equity, Property and Interest Rate Volatility 63

8.7: Market Risk Diversifi cation 68

8.8: Credit Default Risk 69

8.9: Insurance Risk 72

8.10: Mortality and longevity risk 73

8.11: Morbidity Risk 87

8.12: Persistency Risk 91

8.13: Mass Lapse Risk 99

8.14: Expense Risk 104

8.15: Liquidity risk 107

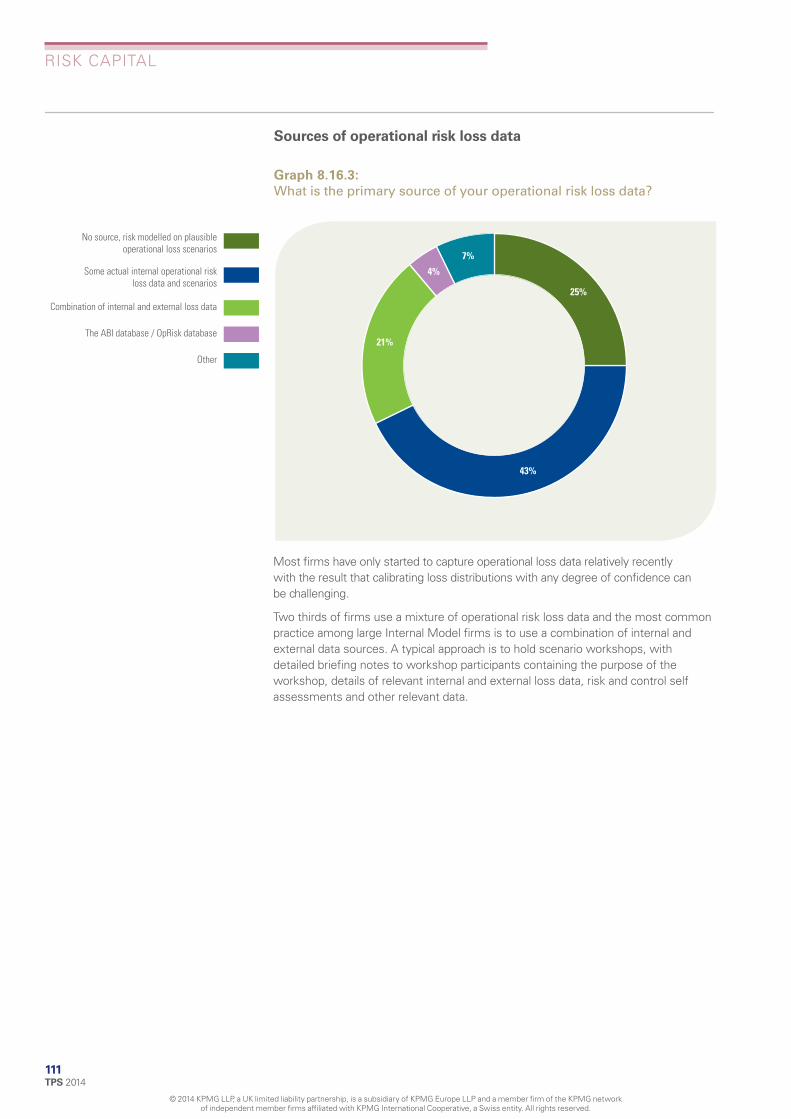

8.16: Operational Risk 109

8.17: Aggregation 113

8.18: Capital Fungibility 124

9 Modelling 125

9.1: Modelling platforms 125

9.2: Economic Scenario Generators 126

9.3: Projecting the balance sheet 127

9.4: Projecting new business 129

10 Solvency II 131

10.1: Transition from ICA to Solvency II 131

10.2: Solvency II Approach 139

10.3: Profi t and Loss Attribution 156

11 Financial Reporting 158

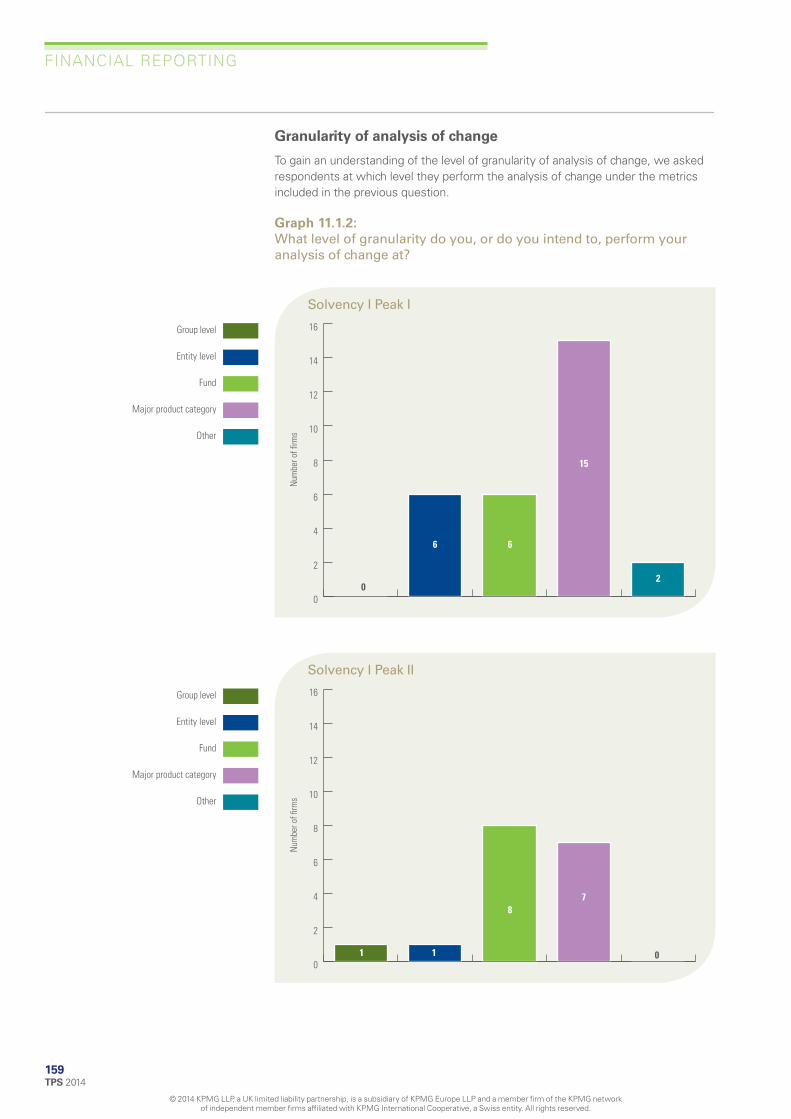

11.1: Analysis of change 158

11.2: The most important metric to the Board 163

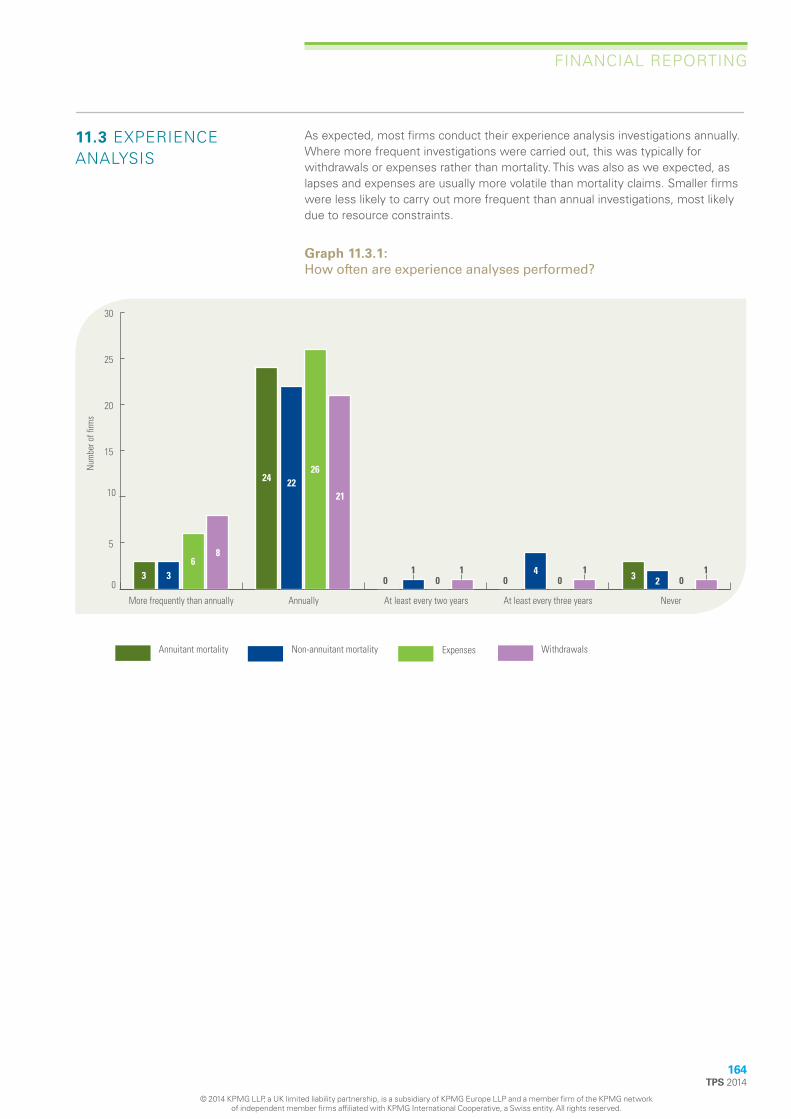

11.3: Experience Analysis 164

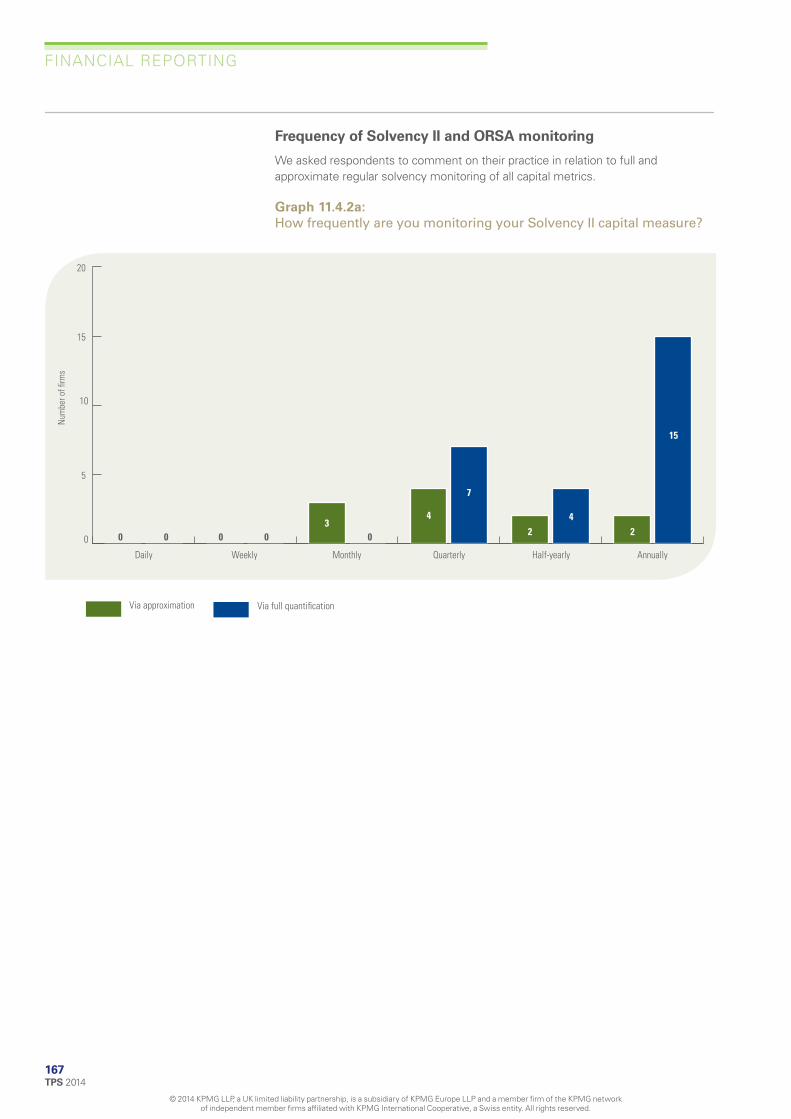

11.4: Solvency monitoring 165

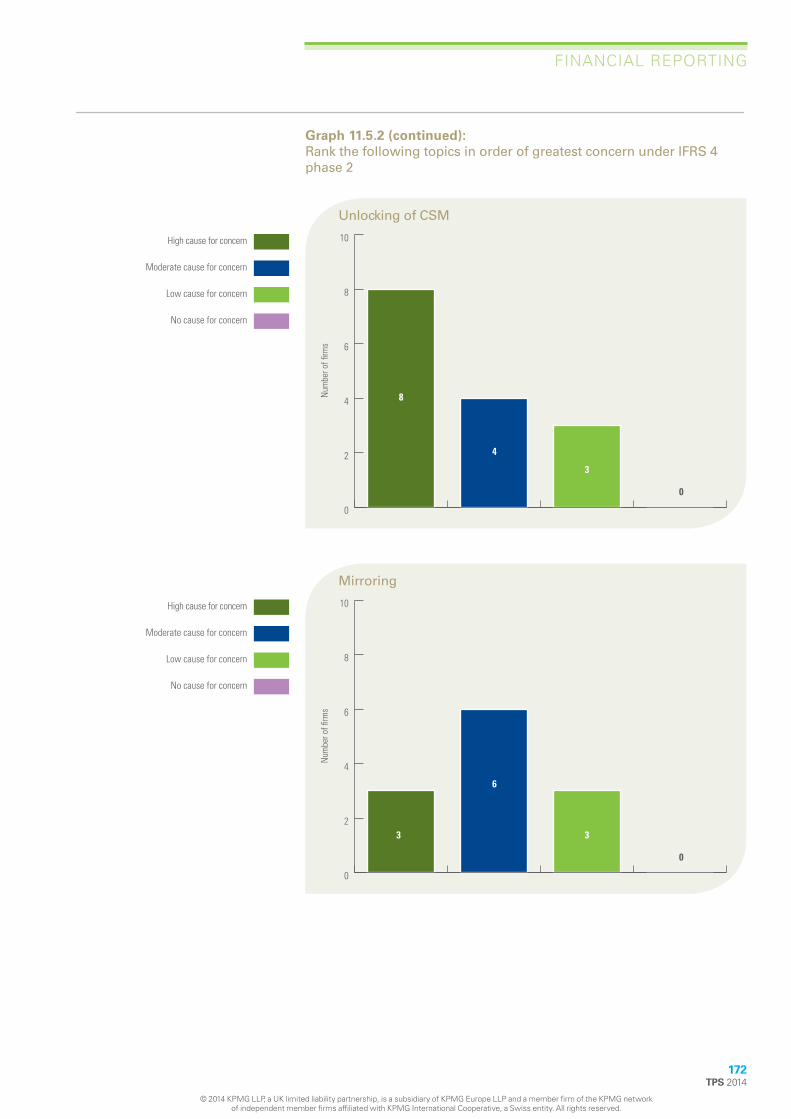

11.5: IFRS 4, phase II 170

11.6: Current Embedded Value Reporting 175

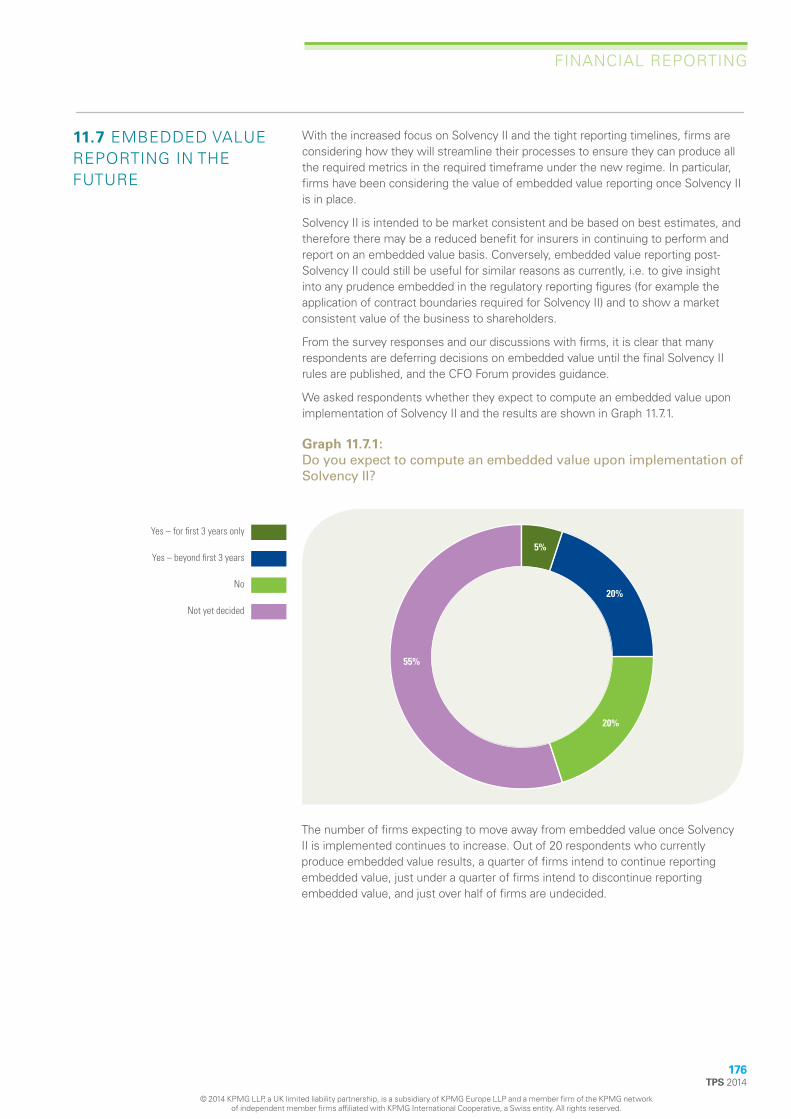

11.7: Embedded Value Reporting in the Future 176

11.8: Key differences between Embedded Value Reporting and Solvency II in the Future 177

12 Tax 179

12.1: Deferred Tax on the Stressed Balance Sheet 180

12.2: Future position and tax modelling 184

12.3: Tax Methodology 186

13 Acknowledgements 187

14 List of participants 189

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

1 Foreword

As always, it gives me great pleasure to present our report on this year’s Technical Practices Survey.

John A Jenkins

Partner, KPMG LLP

Now in its ninth year, our Technical Practices Survey continues to be highly regarded by individuals, respondents and indeed other consultancies as a guide to the range of practices adopted in various areas of UK life actuarial work.

The main focus of our Technical Practices Survey remains on ICA, to identify how practices have changed since last year. However, with the greater clarity around the Solvency II implementation date, we have expanded this section to explore a number of current issues relating to Solvency II. Our approach aims to build on the experience of past surveys and deliver more insights into the UK life industry’s approach to both the ICA and Solvency II.

Working in a top advisory fi rm, some of the most common questions we have been asked by our clients over the last 12 months relate to ICA and the transition towards Solvency II. Therefore, specifi c questions on these areas were included, focusing on what other respondents are doing, how they approach certain problems and what best practice (and the range of practices) on certain items appears to be.

The survey requires a large investment of resources on our part – an investment that we think is well worth the time and effort because of the usefulness of the results. We are grateful to all the respondents who found the time in their busy schedules to take part and would like to extend our thanks to all of you once again. In Section 14 of this report, we have listed the 32 respondents who have contributed to this survey. As I am sure you will agree, the range of fi rms involved by size and type makes the results set out an excellent indication of the UK life industry’s approach to ICA and Solvency II. I hope that if you have not been able to take part in the survey this year that you would be able to do so in 2015.

I would like to extend a very special thank you to all my colleagues for their hard work in carrying out the survey and compiling this report (details of whom can be found in Section 13), whilst at the same time carrying out their client service responsibilities. I would also like to extend particular thanks to Kim Owen, Simon Hogley, and Jane Parker for their hard work in managing the survey.

I believe that you will fi nd this report useful and interesting and look forward to receiving any comments or suggestions you may have on how we can make the questions, analysis or report even more useful or relevant to you.

Regards

John A Jenkins

Partner, KPMG LLP

1 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

2 Executive Summary

The purpose of our Technical Practices Survey is to enable UK life insurance fi rms to identify where the key technical issues lie within the industry, and the range of methodologies and approaches that have been used.

In addition to the insight gained from the responses to each of the distinct survey questions, we have observed some overall themes from our analysis of this year’s responses.

With regard to the calculation of risk capital under the ICA, we have observed that fi rms’ approaches are broadly consistent with last year. Other than the specifi c points noted below, the calibration of stresses and modelling techniques in use has been largely stable.

The standard industry approach for applying longevity stresses under the ICA has been to use a run-off approach. As we move towards Solvency II, the industry has been considering whether this approach is still appropriate. The Solvency II Risk Margin should cover the risk from time 1 onwards and so potentially the run-off approach results in double counting the capital requirement. We have observed that a number of respondents are now using an approach based on a 1-year stress, and increased use of this approach is consistent with our expectation as the implementation of Solvency II approaches. We can understand both approaches and we believe that there are challenges to overcome with both of them.

We observed movement in fi rms’ aggregation methodology, with an increased use of simulation and copula approaches. This movement is also to be expected as fi rms align to Solvency II, however it is interesting to see this borne out by results.

We have increased the granularity with which we asked questions relating to interest rate and credit spread risk, and also relating to correlations. In particular, our questions relating to interest and credit risk have been split by duration in addition to by credit rating. This year is the fi rst time that we have asked respondents to populate a template correlation matrix. We believe that these examples of additional granularity represent an improvement to the survey and will be more useful for fi rms’ benchmarking requirements.

With regard to Solvency II, we observe that larger Internal Model or Partial Internal Model fi rms are focussing on Pillar 3 and IMAP, while the focus of Standard Formula fi rms remains on Pillar 1 valuation and the ORSA. There is still uncertainty over the fi nal form of the regulations, in particular for the Matching Adjustment and Volatility Adjustment, and we have observed that many fi rms are not intending to apply for the Matching Adjustment or use the Volatility Adjustment. In terms of the overall Solvency II impact, half of respondents indicated that they are worse off under Solvency II (including 11 fi rms who stated they will be materially worse off).

We have observed some movement in fi rms’ use or intended use of embedded value. Compared to last year, there are now more fi rms adopting full Market Consistent Embedded Values or Market Consistent European Embedded Values. Of the fi rms who currently produce embedded value results, a quarter of fi rms intend to continue reporting embedded value, just under a quarter of fi rms intend to discontinue reporting embedded value, and just over half of fi rms are undecided.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

2

3 Introduction

3.1 OBJECTIVES

3.2 SURVEY METHODOLOGY

3 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

The KPMG Life Actuarial team has been carrying out the Technical Practices Survey since 2006. This year our aim has been to provide detailed analysis on how the UK life insurance industry has approached the year end 2013 ICA process and calculation, and also to provide insight into the main technical challenges fi rms are facing with regard to Solvency II implementation.

The data for this project was collected through a survey that was sent out to respondents for completion in May and June. In order to make the data as representative as possible, almost every UK life offi ce with an internal actuarial function was invited to participate. We attempted to keep the survey to a reasonable length and were hopeful it was not too onerous to complete.

For data protection and commercial confi dentiality reasons, individual responses have been, and will continue to be, treated with strictest confi dence. For the purposes of this report, the results have all been presented in an aggregate format or have been made anonymous.

The survey primarily contained multiple choice or numeric response questions. Multiple choice questions typically are quicker to answer than open response questions and so we have used the multiple choice format wherever possible (with a suitable other or not applicable option) so that the survey could be completed in a time-effi cient manner. Each year we review the feedback we receive in order to improve the options for these questions.

Note that where results are presented as percentage of fi rms, there are instances where the sum of the separate components may not total exactly 100% due to rounding.

Introduction

We wanted to highlight any common issues that respondents may be

having, as well as provide a reflection of the variety of approaches adopted

within the industry.

3.3 TOPICS OF INTEREST The survey questions were designed to address the issues that clients have raised over the past 12 months. This year’s survey has kept the main area of focus on the ICA to enable comparisons with last year. However, to refl ect the greater clarity around the Solvency II implementation date, we also expanded this section to cover some of the main technical challenges fi rms are facing with regard to Solvency II implementation.

As with prior years, the survey also covered other areas where fi rms have experienced some diffi culty with actuarial techniques. We asked questions relating to alternative assets, with-profi ts, Solvency I, other reporting metrics, and deferred tax assets. We wanted to highlight any common issues that respondents may be having, as well as providing a refl ection of the variety of approaches adopted within the industry.

3.4 INTERPRETATION OF THE RESULTS

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

4

Our survey was targeted at over 60 UK life offi ces with internal actuarial functions, and we are delighted to have had 32 responses this year.

The true test of the survey is that it continues to retain a signifi cant level of interest. It is pleasing to see that this year we have a high response rate despite the burden presented by reporting requirements and their developments. We believe that this refl ects that fi rms participating in the survey continue to fi nd the results to be very useful and relevant.

While the number of responses should be considered as very healthy for this type of survey, the response rate alone does not convey all the information about the representative nature of the survey. For example, some individual responses were completed on behalf of all the separate insurance businesses within an individual group. The responses have been from fi rms of varying sizes which operated in a wide range of markets. Additionally, respondents varied in structure and have included some that were part of larger (often multi-national) groups; others are large in their own right and listed on various European exchanges.

When presenting our analysis we have also provided the context for our fi ndings by including a profi le of the respondents. A graphical representation of the respondents can be found in Section 4, and a full list of participant is in Section 14 of this report. Most of the major UK life offi ces have taken part in the survey.

4 Profi le of Respondents

In order to set the context for the findings of the survey, this section outlines the profile of survey participants.The profi le captures respondents’ attributes such as size of in-force liabilities in terms of Peak 1 insurance liabilities plus WPICC, ownership status, composition of in-force business by product class and reporting basis.

We have also included in this section an analysis of the number of actuarial staff working in fi rst and second line functions.

4.1 PROFILE

5 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Our survey received participation from a wide spectrum of respondents in the UK life insurance market, ranging from small to large businesses in terms of their in-force liabilities. We have categorised respondents by size, with reference to the size of their Peak 1 insurance liabilities plus WPICC.

Throughout this year’s survey, we use the following defi nition when referring to the size of the respondent:

Small: Peak 1 liabilities plus WPICC totalling less than £500m

Medium: Peak 1 liabilities plus WPICC totalling more than £500m, but less than £5bn

Large: Peak 1 liabilities plus WPICC totalling more than £5bn

Profile of Respondents

Graph 4.1.1:

Respondents by size of Peak I liabilities plus WPICC as at 31 December 2013

16%

53%

31%

Small

Medium

Large

Graph 4.1.1 shows that out of 32 respondents, 16% are small, 31% are medium and 53% are large. The profi le of respondents is very similar to that in the 2013 survey, hence making it possible to compare trends in responses over recent years.

Graph 4.1.2:

Respondents by ownership status

22%

34%

38%

3% 3%

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

6

Listed Company

Has listed parents

Unlisted company

Part of unlisted group

Mutual

The respondents represent a diverse group by ownership status, as indicated in Graph 4.1.2. Most respondents are listed, either directly (22%) or through a parent company (38%). Mutuals comprise 34% of respondents while just 6% of respondents were unlisted.

Profile of Respondents

Graph 4.1.3:

Composition of in force business of respondents in terms of Peak 1 liabilities plus WPICC

13%

18%

38%

1%

11%

11%

10%

7 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Conventional with-profits business

Unitised with-profits business

Non-linked non-profit business

Unit-linked business

Annuities

Reinsurance accepted

Other

Graph 4.1.3 shows the average composition of the in-force business by product class in terms of Peak 1 insurance liabilities plus WPICC. Unit-linked business remains the largest product class, as it was in 2013, accounting for over a third of the total. The next largest class is annuities, which accounts for 18% of the total. This is again very similar to previous years; however, we might expect to see a gradual decline in this proportion in the future following the changes to retirement income announced in the budget this year. In total, with-profi ts business comprises around 24% of all business. Other liabilities are largely made up of index-linked products.

8TPS 2014

Profile of Respondents

Graph 4.1.4:

Composition of in force business of respondents in terms of Peak 1 liabilities plus WPICC (split by size of fi rm)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

10%

18%

38%

11%

11%

13%

Overall Small Medium Large

Conventional with-profits business

Unitised with-profits business

Non-linked non-profit business

Unit-linked business

Annuities

Reinsurance accepted

Other

1%

40%

22%

27%

11%

1%16%

50%

4%

16%

11%

10%

19%

35%

14%

7%

15%

1%

Further analysis of the results in Graph 4.1.3 shows that the composition of liabilities in medium and large fi rms is broadly consistent with the overall picture in Graph 4.1.4 above. However, the composition of Peak 1 liabilities for small fi rms is signifi cantly different, with none of the small fi rms responding having any unit-linked or unitised with-profi ts business, instead having more non-linked non-profi t business and reinsurance accepted.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Profile of Respondents

4.2 SIZE OF ACTUARIAL FUNCTION

We asked respondents to provide their number of FTE actuarial staff, by area, ignoring line 1 and line 2 differences and internal structure.

Graph 4.2.1:

Number of FTE actuarial staff by size of fi rm

0

10

20

30

40

50

60

70

80

90

22

82

10

Small Medium Large

Mea

n nu

mbe

r of F

TEs

The relationship between the size of the 32 respondents and the number of actuarial staff employed by them is shown in Graph 4.2.1. As expected, this shows that, on average, large fi rms have considerably larger actuarial teams than small and medium sized fi rms.

In the analysis above we have excluded two respondents from the small fi rms category. These were both reinsurers with signifi cantly larger actuarial teams than other fi rms in the same category. Reinsurers typically have larger actuarial teams than other fi rms, refl ecting the importance of pricing and portfolio analysis for these fi rms. Including these responses, the average actuarial team size for a small fi rm would have been 22 staff, the same as for medium-sized fi rms.

9 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

10TPS 2014

Profile of Respondents

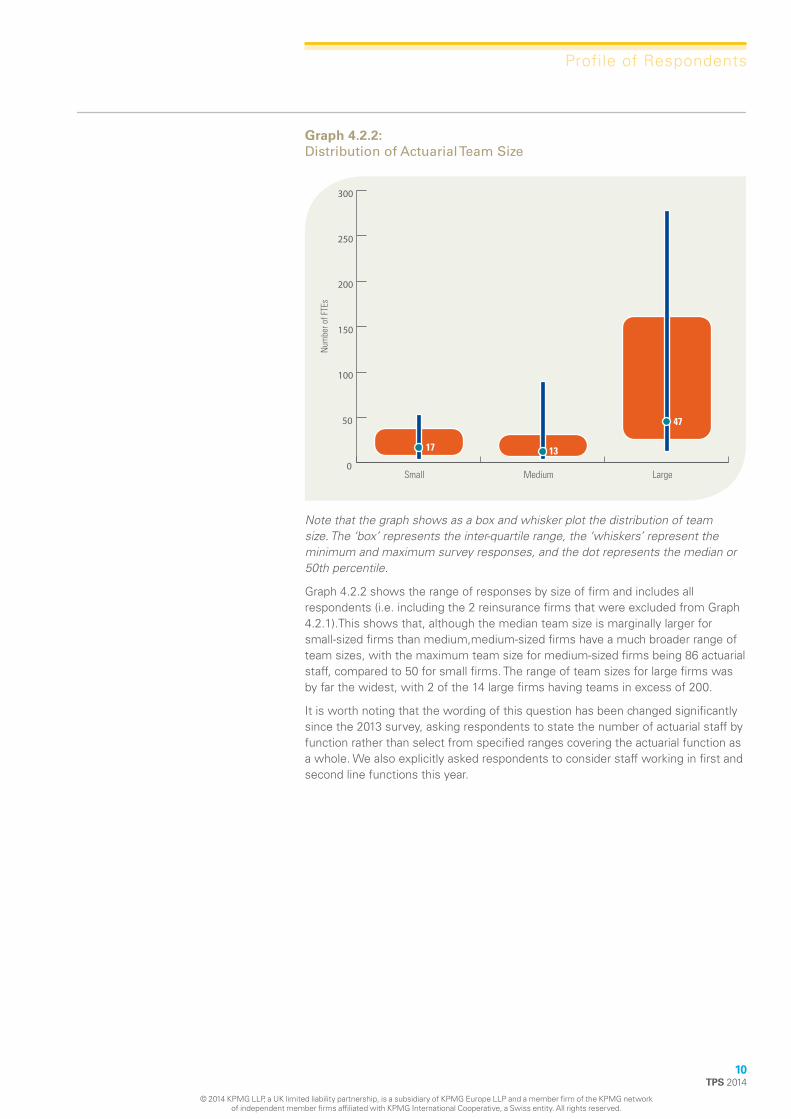

Graph 4.2.2:

Distribution of Actuarial Team Size

0

50

100

150

200

250

300

17

Small Medium Large

Num

ber o

f FTE

s

13

47

Note that the graph shows as a box and whisker plot the distribution of team size. The ‘box’ represents the inter-quartile range, the ‘whiskers’ represent the minimum and maximum survey responses, and the dot represents the median or 50th percentile.

Graph 4.2.2 shows the range of responses by size of fi rm and includes all respondents (i.e. including the 2 reinsurance fi rms that were excluded from Graph 4.2.1).This shows that, although the median team size is marginally larger for small-sized fi rms than medium,medium-sized fi rms have a much broader range of team sizes, with the maximum team size for medium-sized fi rms being 86 actuarial staff, compared to 50 for small fi rms. The range of team sizes for large fi rms was by far the widest, with 2 of the 14 large fi rms having teams in excess of 200.

It is worth noting that the wording of this question has been changed signifi cantly since the 2013 survey, asking respondents to state the number of actuarial staff by function rather than select from specifi ed ranges covering the actuarial function as a whole. We also explicitly asked respondents to consider staff working in fi rst and second line functions this year.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Profile of Respondents

Graph 4.2.3:

Team size by business area

0%

20%

40%

60%

80%

100%

22%

13%

6%

45%

48%

20%

Overall Small Medium Large

Aver

age

split

35%

38%

12%

7%

27%

21%

47%

15%

16%

28%

11 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Pricing

Valuation and financial reporting (including pillar 2)

Financial and risk management

Other including business support

When considering the split of resources by function, valuation and fi nancial reporting was the largest area overall, accounting for 45% of actuarial employees on average. However, for small respondents, most staff were employed in pricing activity. This may refl ect the nature of the business of these fi rms – as highlighted in Graph 4.1.4, small fi rms have a greater proportion of reinsurance and annuity liabilities than medium and large respondents.

Also of interest is that large fi rms have a greater proportion of staff working in fi nancial reporting and risk management than smaller fi rms. This may be a refl ection of the resources deployed by some large fi rms on the development and validation of Internal Models for Solvency II.

Profile of Respondents

4.3 WHICH PEAK IS BITING?

Graph 4.3.1:

Which UK PRA Pillar 1 Peak was biting at the 2013 year end valuation?

12%

41%

47%

UK PRA Peak 1

UK PRA Peak 2

N/A (Regulatory reporter)

Graph 4.3.1 splits respondents by reporting basis and depicts which peak bites for respondents who report on a realistic basis. Of the 32 respondents, 19 reported on a realistic basis and 13 on a regulatory only basis at year end 2013. Out of the realistic basis life firms, Peak 1 bites for 4 firms (21%) with Peak 2 biting for the remaining 15 firms (79%). The 2013 survey showed that Peak 1 was biting for around 40% of the realistic basis respondents, compared with 21% this year. This is in part due to different respondents between the two surveys, although two respondents have indicated that they switched from Peak 1 biting at the end of 2012, to Peak 2 at the end of 2013.

4.4 WHICH PILLAR IS BITING?

Graph 4.4.1:

Which Pillar will bite as at year end 2013?

41%

59%

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

12

Pillar 1

Pillar 2

As shown in Graph 4.4.1, respondents were split 41% to 59% on whether Pillar 1 or Pillar 2 ICA capital requirements were more onerous as at year end 2013, respectively. This shows little change from the 2013 survey when 60% of firms had Pillar 2 biting .

5 Assets

In this section we consider assets, in particular exploring alternative assets held by insurers as well as investigating asset strategies and planning for a Solvency II environment. Firms who participated in this section hold a combined total of £347bn assets of which £12bn are alternative assets.

We are revisiting alternative assets which were a theme of the 2013 survey. Insurers have shown a growing interest in these asset types in order to obtain higher yields and diversification in a low interest environment. We explore firms’ appetite for various alternative assets and how this compares to the results of the 2013 survey.

Preparation for Solvency II will include considering asset data fl ows for Pillar 3 reporting requirements and reconsidering asset investment strategies to optimise capital positions, in particular, considering admissibility of assets and eligibility of assets in order to apply for the Matching Adjustment.

13 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

14TPS 2014

Assets

5.1 INVESTMENT STRATEGY: CURRENT VS FUTURE SOLVENCY II

Graph 5.1.1:

When setting the investment strategy for your business in the current / future Solvency II environment, rate the following metrics in terms of their importance?

Not Considered

Considered to a small extent to inform or verify investment strategy in parts of the business

Widely used measure for setting investment strategy across most business units

Essential measure for setting investment strategy across all business units

Profit return metric:Current 34% 29% 24% 13%

Solvency II 37% 24% 25% 14%

Capital Measures:Current

Solvency II

16% 22% 27%

15% 14% 26%

34%

45%

Risk adjusted performance metrics:Current

Solvency II

48% 17%

41% 21%

10%

14%

24%

24%

ALM / liquidity coverage:Current

Solvency II

16% 31% 32%

23% 25% 30%

21%

22%

Stress tests:Current

Solvency II

24% 41%

31% 31%

28%

31%

7%

7%

Projected metrics:Current

Solvency II

0%

47% 33%

39% 40%

10% 20% 30% 40% 50% 60% 70% 80%

16% 3%

16% 6%

90% 100%Percentage of firms

Graph 5.1.1 shows an aggregated view of responses to this question, by grouping the different metrics into higher level headings. In general we can see that metrics used for setting investment strategies have the same level of importance in the current environment when compared to a Solvency II environment. This suggests that fi rms aren’t planning signifi cant changes to the use of their metrics when setting investment strategies in a Solvency II environment.

Capital measures are an important investment measure for the majority of fi rms (on the graph this category has combined responses for regulatory solvency measures, economic capital and risk appetite). In particular, risk appetite had most fi rms ranking it as important, with 17 out of 29 respondents ranking it as essential and 6 out of 29 ranking it as a widely used in the current environment. A slightly greater level of importance is expected in the Solvency II environment, which may be driven by the encouragement of fi rms to manage their business using a risk based view.

Projected metrics appear not to be an important investment measure for the majority of fi rms (on the graph this category has combined responses for projected future capital, profi t, risk appetite and liquidity metrics). In particular 14 out of 29 respondents say they do not consider projected liquidity requirements and a further 12 say they only consider it to a small extent in the current environment. Only 3 ranked it as a widely used or essential measure. It is no surprise that when asked, these three fi rms are annuity providers and have a higher proportion relative to their peers invested in alternative assets, which tend to be illiquid by nature. Firms may want to understand their liquidity exposure better so they can explore options in purchasing higher yielding assets via the liquidity premium and avoiding forced asset sales at inopportune times.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Assets

5.2 ASSET TRANSITION PLAN FOR SOLVENCY II

Graph 5.2.1:

What is your current position in terms of developing an asset transition plan for Solvency II?

20%

7%

40%

7%

27%

15 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Not applicable - we do not intend to change our asset strategy, so no transition

plan is required

We are awaiting further guidance and/or the outcome of our internal analysis of the

Solvency II regulations (e.g. transitional rules) before we decide a formal transition plan

We are currently developing our Solvency II asset transition plan

We have already developed a draft transition plan

Other

Firms may want to reconsider their asset strategy in order to comply with Solvency II admissibility requirements and also for the eligibility of assets in order to apply for the Matching Adjustment.

The highest proportion, 40% of respondents said that they are awaiting further guidance and/or the outcome of their internal analysis of Solvency II regulations before deciding a formal transition plan.

Out of the 20% of fi rms who do not intend to change their strategy, none of them hold alternative assets. This may suggest they are holding simpler assets types and hence no asset transition plans are required.

Only 7% of fi rms have already developed a draft transition plan. The fi rms who selected “other” said that they were already managing their assets based on a Solvency II world but that they will review and reassess when further clarifi cation on Solvency II guidance is issued.

Assets

5.3 STRATEGY FOR ISSUER OPTIONS IN LIGHT OF THE MATCHING ADJUSTMENT UNDER SOLVENCY II

Graph 5.3.1:

Please select your firm’ s current thinking on the approach it will take to allow the Matching Adjustment to be recognised

4

2

3

5 1

3

TPS 2014 16

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Not applicable - we do not currently and do not intend to hold assets with issuer options

Not applicable - we intend to sell our assets with issuer options before Solvency II fully

implements

No action - we expect that the ongoing lobby / discussions with the regulatory bodies will mean that we will be able to recognise the

illiquidity premium without restructuring when Solvency II fully implements

No action - we will accept the lower free capital business implications of not being able

to recognise the illiquidity premium

We intend to create a SPV structure to allow us to recognise the matching adjustment

Other

Under current Solvency II rules, assets with issuer options are not eligible for a Matching Adjustment. As the Matching Adjustment is only applicable to annuity business, we have restricted the results in this graph to the 18 firms who responded and who are also annuity providers.

Seven firms responded not applicable as they do not hold or intend to hold assets with issuer options before Solvency II implements. Five firms said they would take no action and will accept the lower free capital business implications of not being able to recognise the Matching Adjustment. Surprisingly four out of these five are large annuity providers with over £500m annuity business each. The cause for this is not clear, but it could possibly be that assets with issuer options are not significant for these fi rms.

Only a small proportion of firms are planning to take action, with 2 respondents saying they intend to create a Special Purpose Vehicle structure to allow them to recognise the Matching Adjustment. If choosing this option, firms will need to weigh up whether the extra capital required in order to get a rating for a Special Purpose Vehicle is at least offset by the capital benefit gained from recognition of the Matching Adjustment. Although only two respondents have said that they plan to take action, we have seen a large increase in companies considering this option in the recent months.

Those who selected “other” said that they were awaiting further guidance from the PRA or they will use a combination of the options in Graph 5.3.1 above; i.e. for some assets they will take no action, for others they will use a Special Purpose Vehicle. It is interesting to see that where action is being taken, a Special Purpose Vehicle strategy has been the only one used.

Firms will have to be careful if they plan investment restructuring such as setting up a Special Purpose Vehicle structure, in order to obtain a portfolio of eligible assets for the Matching Adjustment. This is because they will also need to demonstrate their compliance with the Directive’s requirements for risk management and with the Prudent Person Principle. The latter requires fi rms to be able to identify, measure, and manage risks within their asset portfolios, to invest in the best interest of all policyholders and benefi ciaries, and to only use derivative instruments where they genuinely contribute to a reduction in risk or facilitate efficient portfolio management.

Assets

5.4 PILLAR 3 FOR READINESS FOR ASSETS

Graph 5.4.1:

What is the current status of your Solvency II Pillar 3 Reporting for Assets?

17 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Overall 1 12 10 4 1 1

Developed methodology for separating investment returns between risks

1 5 7 6 5 5

Developed process for collection of data 2 16 4 5 2

Developed plans / framework to ensure control, quality and ownership of data

3 9 7 7 2 1

Developed delivery plans to set out process to ensure able to meet tighter reporting deadlines

2 9 9 7 2

Engaged with external data providers to remedy the gaps 2 11 9 5 2

Developed tactical and strategic solutions for the sourcing / remediation of data

1 16 5 3 2 2

Data gap analysis on the asset forms 5 17 4 1 2

0 5 10 15 20 25 30

Number of firms

Completed, no further work required Planned for 2015

Currently underway Other

Planned for later this year Not applicable – not relevant for our business

The recent confi rmation that Solvency II will be introduced on 1 January 2016 and the publication by EIOPA in September 2013 of its proposals for the preparation of Solvency II, has put renewed pressure on fi rms to further develop their Pillar 3 plans in the preparatory period and, ultimately, when Solvency II goes live. The fi rst key reporting milestone for fi rms will be the preparatory QRTs and narrative reporting, with Solo reports due end June 2015 and Group reports due in the second week of July 2015.

The overall readiness bar in graph 5.4.1 is calculated as the average of the readiness of fi rms to the seven listed asset development areas in this graph. Overall, very few fi rms have completed the Pillar 3 asset development areas mentioned in the question.

Only one fi rm, which is a large fi rm, has responded to having already completed all areas, whilst no small fi rms have completed any of the areas mentioned in the question. Only one fi rm has stated they will start all tasks in 2015.

The task which is furthest behind in completion is developing methodology for separating investment returns between risks. Only 6 out of the 24 fi rms for whom this task is applicable have completed or started the task. Seven plan to start later in the year and a further 6 to start in 2015.

18TPS 2014

Assets

5.5 CHALLENGES FACED WHEN INVESTING IN ALTERNATIVE ASSETS

Graph 5.5.1:

When assessing the viability of investing in Alternative Asset Classes and/or performing due diligence on the investments, please select the level of diffi culty/challenge the following areas currently pose to your business

Some significant issues exist

Some limited issues but not to the extent they would stop us investing

We have not yet developed our thinking on this issue

Not applicable - we outsource this element

Not an issue, we have a fully developed process

Not applicable - we do not invest in assets where this is an issue

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Developing asset selection criteria

Availability of asset / market data

Understanding / developing asset modelling and methodologies

Regulatory constraints / concerns

Developing risk monitoring and governance processes

Developing ALM strategy to balance profit vs capital volatility

Hedging unwanted risk elements

Political and Reputational risk considerations

47% 33% 8% 8%

12%7%6%18%12%

47% 22% 10% 6% 10%

50%9% 18% 24%

47% 38% 4% 11%

53%29%6% 6% 6%

32% 29% 6% 26%

47% 24% 18%6%6%

46%

2% 2%

4%

3%

1%

3%

Political and reputational risk considerations

Graph 5.5.1 shows an aggregated view of responses to this question, by grouping the different challenges into higher level headings. Out of the 28 respondents to this question, 11 fi rms indicated that all of the above areas were not applicable as they do not invest in assets where it is an issue. As such this left 17 fi rms for which the rest of the analysis is based on.

For a given area, roughly half of the fi rms experience some level of issue, whether limited or signifi cant. The aggregated categories causing the greatest issues are ‘availability of assets / market data’ and ‘regulatory constraints / concerns’. In particular, ‘regulatory constraints / concerns’ causes an issue for the largest number of fi rms, with 10 fi rms indicating they are experiencing limited issues and 2 fi rms indicating signifi cant issues.

As noted above, the analysis in Graph 5.5.1 is shown at a grouped level. At an ungrouped level (not shown on the graph) the response for which fi rms indicated they had the greatest number of signifi cant issues is ‘obtaining relevant market data to assess credit risk calibration’, with 3 out of 17 fi rms selecting this option. We have seen fi rms having a number of different issues with credit risk calibration data, including the use of US data to model UK exposures, length of the dataset to use (i.e. credibility vs. appropriateness), the extent to which data should be split by duration, and the extent to which data should be split by sector.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

19 TPS 2014

Assets

5.6 TOTAL ASSETS AND ALTERNATIVE ASSETS

Total conventional and alternative assets held

Graph 5.6.1:

Please provide the amount of total assets (conventional and alternative) held in relation to each of the funds

0

20

40

60

80

100

120

140

160

180

Annuity business With-profits Protection business Shareholder funds

£Bn

Total assets

Total alternative assets

£103.6Bn

£166Bn

£38.1Bn £32

Bn£8.9Bn £2.8

Bn£0.1Bn

£0.3Bn

When compared to the 2013 survey results, we observe that annuity business and with-profi ts business remain the funds with the most amounts of alternative assets held. However, out of the £2.8bn of alternative assets held within with-profi ts funds, 41% of this is held by one fi rm. As per the 2013 survey results, a very small proportion of alternative assets are held within protection business and shareholder funds. This is not surprising since protection business is non illiquid and guaranteed in nature.

Alternative assets within the annuity fund and with-profi ts fund represent 8.6% and 1.7% of total assets within each of these funds respectively in 2014. This compares to 6.7% and 2.1% in 2013. This suggests that the proportion of alternative assets held has remained fairly stable over the year. However, it should be noted that the sample of respondents for 2014 does not entirely match that of 2013.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

20TPS 2014

Assets

Relative amount of alternative assets held

Graph 5.6.2:

Distribution of alternative asset types held within annuity funds

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

0%

5%

10%

15%

20%

25%

30%

Asset category

Rela

tive

% o

f alte

rnat

ive

asse

ts h

eld

(%)

PE/venture capital

Infrastructure bonds

Infrastructure loans

Social housing bonds

Social housing loans

Covered bonds

Hedge funds

Residential mortgages

Commercial mortgages

Other structured/securitised assets6.9%

9.6%

4.5%

15.4%

11.7%

23.6% 26.7%

0.5%0.0%1.1%

0.0%Other alternative assets

Most alternative assets invested by insurers are held within the annuity funds. We have therefore provided analysis of the amount of different alternative assets held within annuity funds only.

As per 2013, the most widely held alternative assets within the annuity fund are other structured / securitised assets and other alternative assets, which include equity release and sale and lease back type assets. None of the respondents hold investments in PE / venture capital and hedge funds. In fact, respondents who participated in both the 2013 and 2014 survey have since switched out of PE / Venture capital assets since 2013. Investments in commercial and residential mortgages appear to be more popular. When comparing the fi rms who responded to both the 2013 and 2014 survey, investment in these asset types have increased from £347m and £585m to £1,042m and £1,368m respectively. This could be due to fi rms looking to benefi t from a higher yield through holding more illiquid asset types.

Assets

TPS 2014

Investment of new money in alternative assets

Table 5.6.3:

Number of firms who plan to invest a proportion of new money in alternative assets within each fund over the next 12 months

Nil 0% < x ≤

5% 5% < x ≤

10% 10% < x ≤

25% 25% < x ≤

50% 50% < x ≤

100%

Annuity Business

9 3 4 1 1 1

With- profits 17 2 0 0 0 0

Protection business

19 0 0 0 0 0

Shareholder funds

16 1 0 2 0 0

There were a total of 19 respondents to this question. All of these respondents indicated that they did not plan to newly invest in alternative assets within the protection fund and sixteen said the same for the shareholder fund. This is consistent with the low investments in alternative assets within protection and shareholder funds that we are currently seeing.

Surprisingly, a high proportion, seventeen out of nineteen said they do not plan to newly invest in alternative assets within the with-profits fund. Out of the six respondents who said they currently hold alternative assets in the with-profi ts fund, two did not respond to this question, two said they did not plan to newly invest in alternative assets and two said they would. These results suggest there may be less investment in alternative assets within the with-profits funds over the next 12 months.

Around half (10 out of 19) of the respondents plan to newly invest in alternative assets within the annuity funds. Seven out of these ten firms said they will invest up to 10% of their new assets within the annuity fund on alternative assets. Only one fi rm said they will invest more than 50%. Of these ten firms, two do not currently hold alternative assets and have said that they wish to invest 10% and 15% of new money into alternative assets. Interestingly, there are a further three firms who currently hold alternative assets and do not plan to invest new money in these asset types.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

21

Assets

Graph 5.6.4:

Likelihood of firms investing in different alternative asset types backing annuity business over the next 12 months

0 1 2 3 4 5 6 7

1

0

0

Number of firms

12

13

1

1

2

2

3 1

2 2

1114

1

1

1

2 1 1

Certain Slightly likely

Very likely Moderately likely

PE / Venture Capital

Infrastructure Bonds

Infrastructure Loans

Social Housing Bonds

Social Housing Loans

Covered Bonds

Hedge Funds

Residential Mortgages

Commercial Mortgages

Other Structured / Securitised Assets

Equity release

Commercial Loans

Table 5.6.3 shows that the vast majority of assets to be invested in alternative assets are within annuity funds hence our analysis focuses on the ten respondents who said they plan to newly invest in alternative assets within the annuity fund over the next 12 months.

None of the respondents plan on investing in PE/Venture Capital and hedge funds. The most likely alternative assets for insurers to invest in are infrastructure loans and commercial and residential mortgages. Newly invested money in commercial and residential mortgages would be consistent with the investments we are seeing in the current environment. In fact, 7 out of the 10 fi rms are at least considering investing in commercial mortgages, with 4 of them saying they are certain to invest in this asset type. However, currently a small proportion of total alternative assets (0.5%) are currently held in infrastructure loans. Out of the three fi rms who said they are certain to invest in infrastructure loans, only one of them currently holds this asset type. This may be demonstrating an increased appetite for the purchase of highly illiquid assets in trade off for a higher yield.

One fi rm indicated they were certain to invest in equity release and another one fi rm was certain to invest in commercial loans. These fi rms already have current holdings in these asset types and the choices to invest in them may be due to these fi rms’ overall strategy as opposed to the attractiveness of these asset types.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

22

Assets

5.7 RATIONALE FOR INVESTING IN ALTERNATIVE ASSETS

Graph 5.7.1:

Where appropriate, please indicate the rationale(s) for investment in

your alternative assets

0

5

10

15

20

13

Num

ber o

f firm

s

15 16

13

8

6

Yield pick-up

Risk/return trade-off

Portfolio diversification

ALM - duration matching

ALM - cash flow matching

Expected capital benefit

We asked insurers to indicate the rationale for their investment in alternative assets and there were 19 respondents to this question.

The most popular rationales for investment in alternative assets are portfolio diversifi cation and risk/return trade off, with 16 and 15 respondents respectively selecting these options. Firms with long term illiquid liabilities such as annuities may already have a high exposure to corporate bonds and will not consider liquidity risk as a material one. Hence, there is no surprise these are the most popular rationales since insurers are able to further diversify their portfolio by investing in new alternative assets that also offer higher yields via the liquidity premium.

The least widely used rationale for investing is expected capital benefi t, with only 6 out of 19 respondents selecting this option, suggesting that the cash fl ow properties of alternative assets are more valuable to insurers than capital considerations.

Five fi rms selected all six options as a rationale for investing in alternative assets.

23 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

6 Solvency I

While the main focus of our Technical Practices Survey is the ICA and Solvency II, we recognise that clients continue to find comparisons of key basis items for Peak 1 and Peak 2 to be very useful.

As such we have continued our questions around the Pillar 1 mortality assumptions and introduced a new question on the assumed level of liquidity premium under Peak 1.

6.1 ANNUITY BASE MORTALITY ASSUMPTIONS

We asked respondents which base annuitant mortality table they use for their most material annuity business. Of 28 respondents who answered the question on the Peak 1 basis, 23 (82%) said they use the ‘00’ tables, with the other 5 respondents saying they use other tables. All respondents who answered ‘00’ tables for their base annuity table use gender-specifi c mortality tables.

Of the 17 respondents who answered the question on the Peak 2 basis, 15 (88%) said they use the ‘00’ tables, with the other 2 respondents saying they use other tables. All respondents who answered ‘00’ tables for their base annuity table use gender-specifi c mortality tables.

We also asked fi rms what table multipliers they apply to their base mortality tables. We received 23 responses to this question, of which all 23 covered Peak 1 and 12 covered Peak 2 bases with the results shown overleaf.

For both the Peak 1 bases and the Peak 2 basis, the majority of respondents use table multipliers lower than 100% (both for males and females).

On the Peak 1 basis, the average table multiplier is 91.5% for males and 80.5% for females. On the Peak 2 basis, the average table multiplier is 93.7% for males and 90.9% for females.

We also compared table multipliers between Peak 1 and Peak 2. Of the 12 respondents on the Peak 2 basis, 8 respondents use higher table multipliers, 2 use the same table multiplier and the remaining 2 use lower table multipliers than their Peak 1 basis.

We note that of those respondents who use higher table multipliers for the Peak 2 basis, 5 use lower mortality improvement factors, 2 use the same mortality improvement factors and one respondent said they use higher mortality improvement factors for the PRA Peak 2 basis.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

24

Solvency I

Graph 6.1.1:

Mortality table multiplier - Peak 1 Valuation

0

1

2

3

4

5

6

< 80%

Num

ber o

f firm

s

0 0 1

00 0

[80%

, 85%

)

[85%

, 90%

)

[90%

, 95%

)

[95%

, 100

%)

[100%

, 105

%)

[105%

, 110

%)

[110%

, 115

%)

[115%

, 120

%)

≥ 120

%

111

33 3

2

3

4

5

4

555

Male

Female

Graph 6.1.2:

Mortality table multiplier - Peak 2 Valuation

0

1

2

3

4

5

6

< 80%

Num

ber o

f firm

s

11 0 0 0 00

[80%

, 85%

)

[85%

, 90%

)

[90%

, 95%

)

[95%

, 100

%)

[100%

, 105

%)

[105%

, 110

%)

[110%

, 115

%)

[115%

, 120

%)

≥ 120

%

2

4

11111 1

2 2222

25 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Solvency I

6.2 MORTALITY IMPROVEMENT MODEL

We asked respondents about the mortality improvement model used to calculate their liabilities under Peak 1 and Peak 2.

Graph 6.2.1:

Peak 1 - Mortality Improvement Models

4%12%

28%

Long cohort

CMI 2009

CMI 2011

CMI 2012

CMI 2013

Other

24%

28%

4%

Long cohort

CMI 2009

CMI 2011

CMI 2012

CMI 2013

Other

Graph 6.2.2:

Peak 2 - Mortality Improvement Models

6%7%

20%

27%

40%

Long cohort

CMI 2009

CMI 2011

CMI 2012

CMI 2013

Other

For both Peak 1 and Peak 2 the majority of respondents use the CMI model. In the 2013 survey the majority of respondents used the 2011 model; however we can see that over the past year many respondents have moved to either the 2012 or 2013 models.

Three respondents answered “other”, two of which said they use their own model and the other saying they use average of medium and long cohort models.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

26

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Solvency I

6.3 CHOICE OF CMI MODEL

This question considers only those fi rms who use the CMI models as shown in section 6.2.

14 out of 19 respondents use the Core CMI mortality improvement model to value their Peak 1 liabilities, and 5 use the Advanced model.

10 out of 14 respondents use the Core CMI mortality improvement model to value their Peak 2 liabilities, and 4 use the Advanced model.

Graph 6.3.1:

Peak 1 - Core / advanced version of the CMI mortality improvement model

26%

74%

Core

Advanced

Graph 6.3.2:

Peak 2 - Core / advanced version of the CMI mortality improvement model

29%

71%

These results are in line with our expectation as the Core model is easier to use than the Advanced model given the complexity of calibrating the various parameters in the Advanced model. As expected, out of the fi ve respondents who used the Advanced model, 4 are large insurers and the remaining one is a medium-size reinsurer. The results are similar to those from the 2013 survey. 27

Solvency I

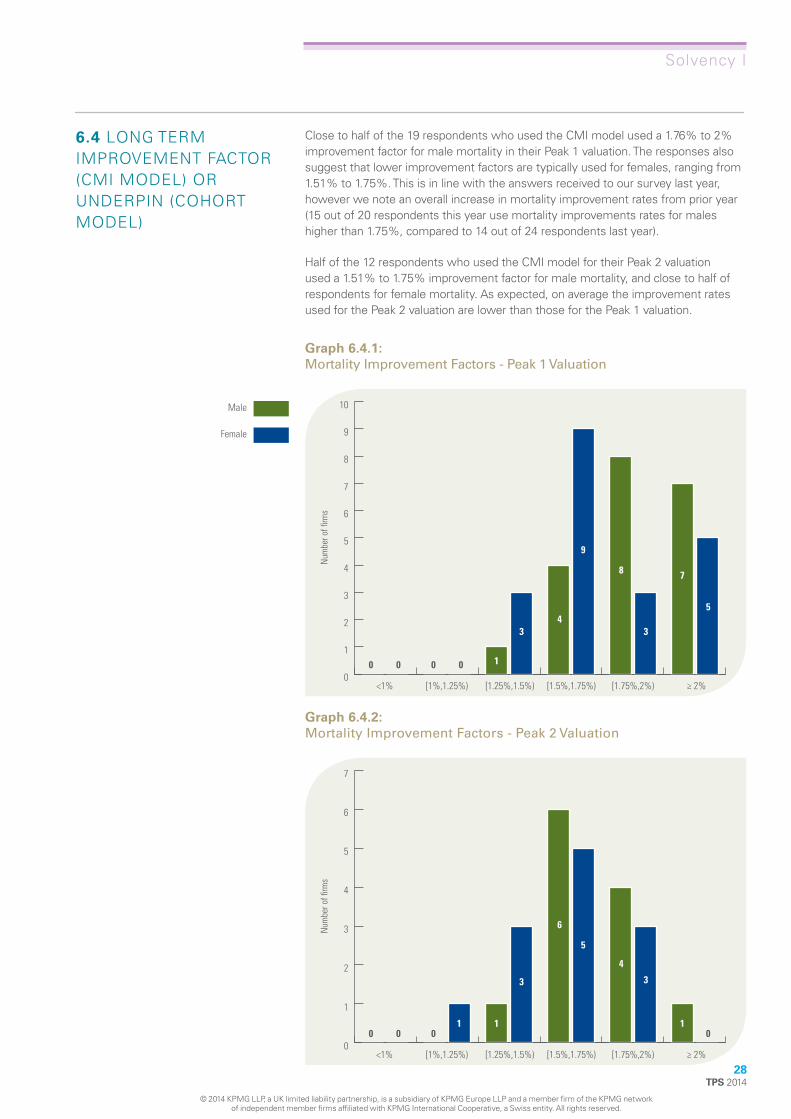

6.4 LONG TERM IMPROVEMENT FACTOR (CMI MODEL) OR UNDERPIN (COHORT MODEL)

Close to half of the 19 respondents who used the CMI model used a 1.76% to 2% improvement factor for male mortality in their Peak 1 valuation. The responses also suggest that lower improvement factors are typically used for females, ranging from 1.51% to 1.75%. This is in line with the answers received to our survey last year, however we note an overall increase in mortality improvement rates from prior year (15 out of 20 respondents this year use mortality improvements rates for males higher than 1.75%, compared to 14 out of 24 respondents last year).

Half of the 12 respondents who used the CMI model for their Peak 2 valuation used a 1.51% to 1.75% improvement factor for male mortality, and close to half of respondents for female mortality. As expected, on average the improvement rates used for the Peak 2 valuation are lower than those for the Peak 1 valuation.

Graph 6.4.1:

Mortality Improvement Factors - Peak 1 Valuation

0

1

2

3

4

5

6

7

8

9

10

1

<1% [1%,1.25%) [1.25%,1.5%)

Num

ber o

f firm

s

0

[1.5%,1.75%) [1.75%,2%) ≥ 2%

0 0 0

3 4

9

8

3

7

5

Male

Female

Graph 6.4.2:

Mortality Improvement Factors - Peak 2 Valuation

28 TPS 2014

0

1

2

3

4

5

6

7

1

<1% [1%,1.25%) [1.25%,1.5%)

Num

ber o

f firm

s

0

[1.5%,1.75%) [1.75%,2%) ≥ 2%

0 0 0

3

6

5

4

3

1 1

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

29 TPS 2014

Solvency I

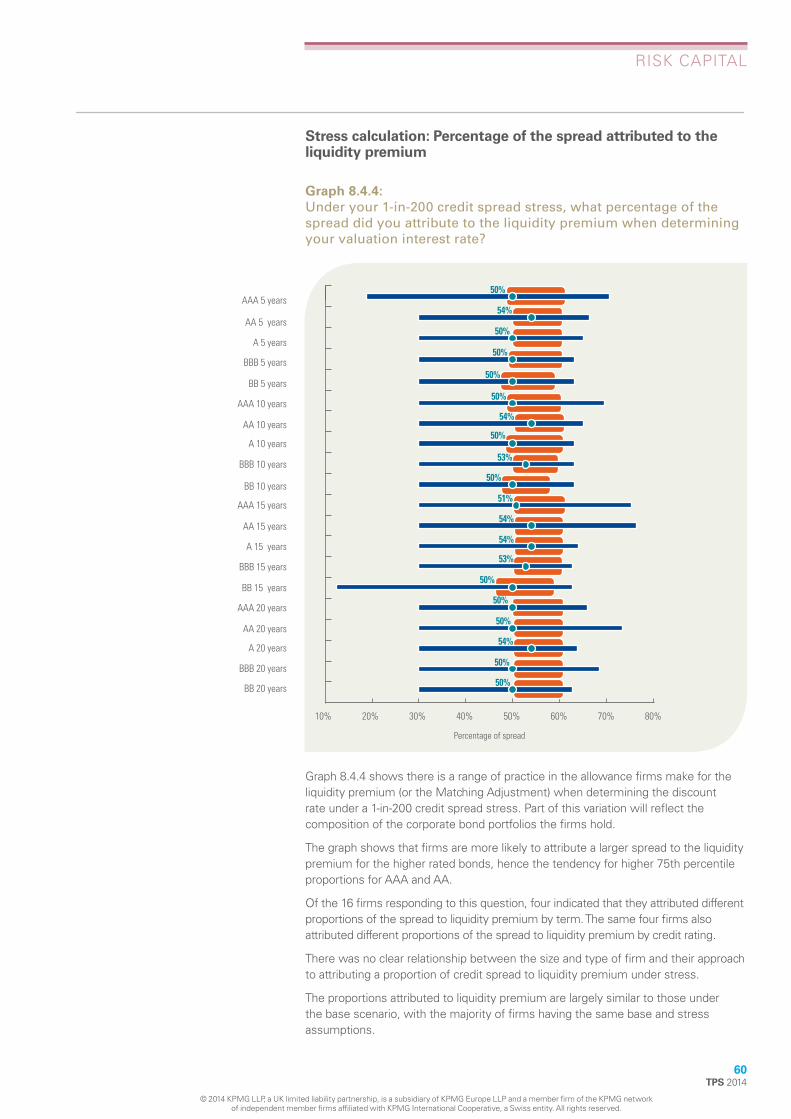

6.5 LIQUIDITY PREMIUM We asked fi rms what proportion of their credit spread was attributed to the liquidity premium in their valuation interest rates for Peak 1 reporting, by credit rating. We received 22 responses to this question. Of these, 8 applied a fl at percentage across all ratings, and 14 applied a percentage that differed by rating. Graph 6.5.1 illustrates the range of responses received.

Graph 6.5.1:

For PRA Peak 1 reporting, what percentage of the spread did you attribute to liquidity when determining your valuation interest rate for the following bond ratings?

0%

20%

40%

60%

80%

100%

60%

AAA AA A

Perc

enta

ge o

f spr

ead

58%53%

BBB BB Flat%

51% 50% 51%

Note that the graph shows as a box and whisker plot the distribution of percentage of spread. The ‘box’ represents the inter-quartile range, the ‘whiskers’ represent the minimum and maximum survey responses, and the dot represents the median or 50th percentile.

The median percentage of yield spread attributable to the liquidity premium generally decreased by credit rating. For stronger credit ratings (AAA and AA) the lower inter-quartile was lower than that for weaker credit ratings (A and BBB), except BB.

For fi rms where the responses differed by rating, a broad range of responses was observed. For example, for AAA rated bonds the minimum and maximum percentage were respectively 21% and 95%.

For fi rms with a fl at percentage across all ratings, responses were between 21% and 60%.

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member fi rm of the KPMG network of independent member fi rms affi liated with KPMG International Cooperative, a Swiss entity. All rights reserved.

7 With-profi ts

Since publication of the last Technical Practices Survey we have seen fi rms continuing to re-evaluate their strategies with respect to with-profi ts.

The impacts of FSA PS12/04, the Retail Distribution Review and the reduction in customer demand for with-profits products over recent years have caused a number of firms to stop writing new business.

The vast majority of with-profi ts funds are now closed and a signifi cant volume of business is now reaching maturity, driven by the peak in mortgage endowment sales in the late 1980’s. This run-off may be accelerated further for funds with signifi cant amounts of pension savings business if customers choose to take advantage of the increased benefi t fl exibility announced in this year’s Budget.

These factors mean that the past twelve months have seen a number of fi rms take further actions to help ensure an effi cient run-off of their with-profi ts business. For example, a number of fi rms have undertaken transactions to transfer annuity business out of their with-profi ts funds, either to the fi rm’s non-profi t fund or to another provider. Without such measures the ratio of with-profi ts business to non-profi t business within the fund would change rapidly over future years, potentially giving rise to risk exposures that are inconsistent with the expectations of with-profi ts policyholders and constraining the fund’s ability to distribute the estate as it would like.

It is likely that fi rms will continue to explore such options and that, as the withprofi ts run-off accelerates across the industry, further consolidation will take place between providers.

The past year has also seen fi rms increasingly turn their attention to the treatment of their with-profi ts business under Solvency II. This poses a number of challenges, in terms of the reporting requirements of the QRTs, the impact of ring-fenced funds and the extent to which management actions are allowed for within the balance sheet.

This year’s Technical Practices Survey provides excellent coverage of the UK with-profi ts market. 21 of this year’s respondents have with-profi ts funds and these include all but three of the UK’s realistic reporting fi rms. Given the nature of with-profi ts business and the defi nitions used in this survey, the respondents with with-profi ts funds are primarily large fi rms (14 respondents) with 6 medium fi rms and only 1 small fi rm.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

30

WITH-PROFITS

7.1 THE WITH-PROFITS LANDSCAPE

Number of with-profi ts funds

Graph 7.1.1:

How many with-profits funds are there in your fi rm?

0

2

4

6

8

10

8

1

Num

ber o

f firm

s

Number of funds

6

4

2

1

2 3-5 6-10 >10

Graph 7.1.1 shows the number of with-profi ts funds of each of the respondents. In total, 21 of the 32 participants in this year’s survey have at least 1 with-profi ts fund. Throughout the remainder of this section the analysis considers only these 21 fi rms.

13 of the 21 respondents with with-profits business have more than one with-profi ts fund, and on average each firm has 2.9 with-profits funds. This demonstrates the extent to which the with-profits market has already consolidated, with many of the fi rms with multiple funds having acquired at least one of these through acquisition activity.

A small number of fi rms have been the most active in this area pursuing consolidation strategies, with one respondent having 13 separate with-profi ts funds. Excluding this respondent, the average funds per fi rm would have reduced to 2.4.

31 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

WITH-PROFITS

Number of open and closed with-profi ts funds

Graph 7.1.2:

How many of your with-profits funds are closed to new business and in run-off, or open to new business?

20%

80%

Closed to new business and in run-off

Open to new business

Graph 7.1.2 shows the number of open and closed funds covered by this year’s survey. Only 20% of the funds currently remain open to new business. While this appears to be a signifi cant fall since last year, this is primarily due to a difference in the information requested between the two surveys. The 2013 survey did not ask fi rms to specify how many of their funds were open or closed, asking only whether the main with-profi ts fund remained open.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

32

WITH-PROFITS

7.2 WITH-PROFITS CAPITAL STRENGTH

Pillar 2 basis

Graph 7.2.1:

How many of your with-profits funds are self-suppor ting on a Pillar 2 basis?

7%

10%

83%

Do not cover their realistic liabilities

Fully cover their own realistic liabilities, but not their ICA & ICG

Fully cover their own realistic liabilities, ICA & ICG

Graph 7.2.1 shows that 83% of the with-profi ts funds covered by the survey are fully self-supporting in that the assets of the fund are suffi cient to cover their own realistic liabilities plus the fund’s ICA and any ICG that applies.

17% of the funds covered (10 funds) are not self-supporting. 6 of these cover their realistic liabilities but not the capital requirements while 4 require external support to cover their realistic liabilities. 9 of the 10 funds that are not fully self-supporting are proprietary funds, and therefore are reliant on capital support from other shareholder owned funds. Only one mutual with-profi ts fund was unable to meet its capital requirements and was receiving capital support from another fund.

Due to the timing of the survey it is likely that some respondents will have answered this question based upon year-end 2012 results while others will have answered with respect to year-end 2013 results.

33 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

WITH-PROFITS

Solvency II framework

Graph 7.2.2:

How many of your with-profits funds do you expect to be self-supporting under the Solvency II framework?

6%

7%

8%

79%

Funds do not cover their BEL

Funds fully cover their own BEL, but not their Risk Margin or SCR

Funds fully cover their own BEL and Risk Margin, but not their SCR

Funds fully cover their own BEL, Risk Margin and SCR

Under Solvency II Pillar 1, 48 of the 61 with-profi ts funds are fully self-supporting and cover their own BEL, Risk Margin and SCR. Of the 13 funds that do not, the split is broadly even – 5 do not have suffi cient assets to cover their best estimate liabilities, 4 cover their BEL but not the Risk Margin and the remaining 4 cover their Risk Margin but not the SCR. This is broadly the same as the pattern observed in the 2013 survey.

A comparison with Graph 7.2.1 shows that slightly more funds are expected not to be fully self-supporting under Solvency II compared to the current ICAS regime. This is perhaps to be expected given some of the Solvency II requirements. However, it is worth noting that not all of the funds requiring additional capital under the ICAS regime also require capital support to meet their Solvency II capital requirements – there are two funds that currently support their Pillar 2 realistic liabilities but not their ICA or ICG which are fully self-supporting under Solvency II.

All 13 of the funds requiring additional capital under Solvency II are owned by proprietary fi rms and 12 of these belong to large fi rms, the remaining fund belonging to a small fi rm.

It is unclear the extent to which respondents have made allowance within their current Solvency II estimates for the revised long-term guarantees (LTG) package. Furthermore, it is possible that the recently published PRA consultation paper CP 16/14 may also change the position shown in graph 7.2.2.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

34

WITH-PROFITS

7.3 SOLVENCY II AND WITH-PROFITS

Presentation of with-profits funds under the prospective approach required under Solvency II

Graph 7.3.1:

Are you currently able to present your with-profits funds under the prospective approach required under Solvency II?

50%

6%

44%

Yes

No - some further development is required

No - significant further development is required

Graph 7.3.1 shows the proportion of respondents that are able to present their with-profi ts funds under the prospective approach required under Solvency II for QRT reporting. This is a complex area with fi rms being required to value fi rst the future guaranteed benefi ts and then any discretionary benefi ts in excess of this on a prospective basis. The nature of this differs fundamentally from the current Realistic Balance Sheet approach where the liabilities are based on the retrospective asset share plus a value for the cost of guarantees. In addition, fi rms will need to explicitly value and report items such as future premiums and expenses and show liabilities gross and net of reinsurance. Current models may not readily provide these outputs and, in the case of reinsurance, may implicitly allow for this by considering only the net liability.

Half of the respondents indicated that they are currently able to meet the prospective reporting requirements, with 44% recognising that some further system and process development is required to satisfy the QRT requirements. 6% of respondents require signifi cant further development in this area.

35 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

WITH-PROFITS

Consideration of with-profits run-off plan as part of the ORSA

Graph 7.3.2:

Will you be considering your with-profits run-off plan as part of your ORSA going forward?

37%

63%

Yes

No - we will consider it outside of the ORSA process

16 of the respondents indicated that they have one or more run-off plans in place that will need to be considered and reviewed on an ongoing basis. The analysis shows that there is not a consistent approach across the market with approximately one third of respondents intending to consider this as part of their ORSA process and the remainder intending to address this separately. This is a noticeably different picture to that provided by the 2013 survey when 56% of respondents stated that they would consider their run-off plans as part of their ORSA, suggesting that this is an area where fi rms are continuing to develop their thinking.

TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

36

WITH-PROFITS

7.4 WITH-PROFITS RISK MANAGEMENT

Structural derisking options

Graph 7.4.1:

Which of the following structural derisking options are you considering in respect of your with-profi ts funds?

37 TPS 2014

© 2014 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member fi rms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Outsource all/part of the cost base 42% 5%

Remove conventional non profit business 6% 41%

Reinsurance 28% 6%

Buy out any pension scheme deficit 9% 18%

Fund restructuring to allow NP sales without WP sales 22%

Remove unit linked non profit business 21%

Remove subsidiaries from the with-profits fund 11%

Other 17% 33%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

% of firms with with-profits funds

Already undertaken Under active consideration

Graph 7.4.1 shows the structural derisking options that fi rms with with-profi ts funds have either already taken or are considering. This graph excludes any respondents who stated that a particular action was not applicable to their with-profi ts funds.

The most widely used structural action is outsourcing all or part of the with-profi ts cost base, either to a third party or an internal service company. 42% of respondents have already taken this action with another 5% giving active consideration to this. This is another example of the effects of with-profi ts run-off, with those responsible for managing with-profi ts funds using such arrangements to protect with-profi ts policyholders from the effects of spreading overhead costs across a rapidly reducing in-force book.

The second most common action overall is removing non-profi t business from the fund. 47% of respondents have either taken this action (6%) or are actively considering this (41%). Although the question did not specifi cally ask about the type of non-profi t business, much of this is likely to be annuities which, given their rate of run-off, otherwise would remain in-force within the fund after the withprofi ts liabilities have all expired. Fewer fi rms (21%) were considering removing unit-linked business from the with-profi ts fund. This perhaps refl ects the uncertainty around the value that will be generated by such business, particularly in light of the recent budget changes which mean future persistency experience on unit-linked pensions business is much more of an unknown quantity, and the likely faster run-off compared to annuities.

A number of fi rms either already have or are actively exploring buying-out the withprofi ts fund’s share of any pension scheme defi cit. Such actions are likely to increase as the with-profi ts run-off accelerates and those responsible for managing the fund seek to limit the fund’s exposure to what can often be a material risk.

WITH-PROFITS

Finally, 22% of respondents indicated that they are considering changing their fund structure to allow the continued sale of non-profit business, should new sales of with-profits cease. This question was only relevant to mutuals. The actions potentially include making use of the rule waiver outlined in PS 14/5: Response to CP12/38 – Mutuality and with-profits funds: a way forward, which would allow mutuals to recognise some of the inherited estate as members’ capital and to use this to fund other commercial activities. This is an interesting development since, as yet, no firm has used this new option.

A number of fi rms indicated that they have taken, or are considering, other options. These included reviewing existing estate distribution mechanisms and converting with-profi ts business to a non-profi t basis.

Number of management actions

Graph 7.4.2:

Average number of management actions assumed for with-profi ts business

0

1

2

3

4

5

6

7