Embed Size (px)

Citation preview

Canadian Public Policy

Financial Services Reform in Canada: The Evolution of Policy DissensionAuthor(s): William D. ColemanSource: Canadian Public Policy / Analyse de Politiques, Vol. 18, No. 2 (Jun., 1992), pp. 139-152Published by: University of Toronto Press on behalf of Canadian Public PolicyStable URL: http://www.jstor.org/stable/3551420 .

Accessed: 15/06/2014 01:51

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

University of Toronto Press and Canadian Public Policy are collaborating with JSTOR to digitize, preserveand extend access to Canadian Public Policy / Analyse de Politiques.

http://www.jstor.org

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

Financial Services Reform in

Canada: The Evolution of Policy Dissension* WILLIAM D. COLEMAN Department of Political Science McMaster University

Cet article examine l'6volution de la rdglementation des services financiers au Canada en mettant l'accent sur les ddveloppements r6cents des anndes 80. En d6pit de pressions du march6 et de pressions internationales pour une meilleure harmonisation de la rdglementation i l'intdrieur d'un meme pays, la reglementation des services financiers au Canada semble moins bien harmonisee qu'a tout autre moment durant la periode aprbs-guerre. Le texte soutient que la reforme rdcente de la r6glementation a 6t6 congue dans un climat de conflit f6d6ral-provincial. Les groupes d'int6rbt representant les diff6rentes parties du marchd n'en sont pas arrives a un consensus sur les changements requis. De plus, les diff6rents types de firmes financibres dtaient liees a diff6rents niveaux de gouvernement. Consdquemment, la rdglementation et le contr6le des services financiers sont devenus plus fragmentds au Canada. L'article conclut avec certaines suggestions pour d'6ventuels changements bas es sur le modble de la Communaut" Economique Europdenne.

This article examines the evolution of financial services regulation in Canada, focussing on developments in the 1980s. Despite market and international pressures toward increased regulatory harmonization within nation-states, financial services regulation in Canada emerged less harmonized than any time in the postwar period. It argues that regulatory reform was drawn into the vortex of federal-provincial conflict. Interest associations representing the various market groups lacked a consensus on the changes needed. In addition, different levels of government were attached to particular types of financial firms. Consequently, regulation and supervision of financial services became more fragmented in Canada. The article concludes with some suggestions for changes based on the European Economic Community model.

The regulation of financial services in

Canada has increasingly suggested the age-old image of two ships passing in the night. Internationalization and what the French call ddcloisonnement (desegmenta- tion) are the dominant market trends. Market segments historically dominated by one group of firms have been opened to new competitors. In Canada, business lending is no longer the preserve of the chartered banks, mortgage loans the fiefdom of trust and loan and life insurance companies, and

market-making in securities the monopoly of an independent set of investment houses. Innovations in financial products have hastened desegmentation by enabling large borrowers to substitute securities for some types of loans (Bryant, 1987). Concurrently, these changing national markets have opened up to international competition (Pauly, 1988; Economic Council of Canada, 1989).

The globalization of financial services and its impact on domestic market struc-

Canadian Public Policy - Analyse de Politiques, XVIII:2:139-152 1992 Printed in Canada/Imprim6 au Canada

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

tures have increased the significance of su- pranational policy-making, particularly the deliberations of the International Organi- zation of Securities Commissions (IOSCO) and of the Committee on Banking Supervi- sion and Regulation, a sub-committee of the Group of ten central bank governors, that meets regularly at the Bank for Inter- national Settlements in Basel. The impor- tance of these supranational organizations has placed additional pressure on partici- pating governments to develop national positions on regulatory policy. Yet, when one looks at the evolution of financial serv- ices regulation in Canada, increasing frag- mentation in policy objectives and ap- proaches has accompanied these market pressures and international changes.

This article focusses on two subsets of fi- nancial services, banking and investment services, for which we adopt functional defi- nitions. Following the Economic Council of Canada (1987:81), banking is defined as the provision of a means of payment. A means of payment refers to any financial instru- ment that is widely accepted in payment for goods and services and for the discharge of debt. By this definition, any institution that accepts deposits redeemable on demand or transferable by cheque would be considered to be involved in banking. Accordingly, trust companies, credit unions, and caisses populaires as well as chartered banks en- gage in 'banking'. Investment services in- volves market intermediaries who accept monies 'for the purchase of the debt or eq- uity of another corporate entity' (Ontario, 1985:9). Such services include the issuing and trading of securities including stocks, bonds, short-term money market instru- ments, and a host of new financial innova- tions.

This article examines why regulatory harmonization has declined in Canada. It notes that oversight of financial services has tended to develop along the jurisdic- tional fault lines of the federal system, lead- ing to increasing institutional overlap and variance in regulatory regimes. In the 1960s, the federal government passed on an

opportunity to check this path of develop- ment. In the ensuing years, the provincial governments became increasingly impor- tant policy actors and came to view finan- cial services policy from their own particu- lar points of view. The organization of interests in the financial services sector tended to follow these jurisdictional boun- daries. As vested interests came under threat, they moved to support the level of government most likely to protect their most crucial interests. Consequently, in the 1980s, when regulatory reform became vital, it was drawn into the vortex of fed- eral-provincial conflict. Lacking consensus among the interest associations repre- senting the various market groups, and with all stakeholders attached to particular sets of institutions, regulation and supervi- sion of financial services became more frag- mented in Canada.

This argument is developed in four steps. The first section presents a frame- work for analysing regulatory regimes in territorially-segmented states. The second section reviews the evolution of financial services regulation until 1980. The next part examines the four key governments in financial services regulation, emphasizing the structure of the industries they super- vise. It also reviews briefly the organization of interests in the financial sector. Then it surveys the evolution of financial services regulation in the 1980s, showing the grow- ing divergence among the four govern- ments. The final section juxtaposes state structure and the organization of interests in an attempt to account for the increasing divergence in policy objectives and ap- proach among the four governments. The article concludes with some suggestions for possible reform.

I A Framework for Analysis

In order to examine the evolution of finan- cial services regulation, it is necessary first of all to have a way of classifying regulatory regimes that cover segmented territorial markets. Abstracting from experience both

140 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

in Canada and in Europe, the following five regime types might be distinguished. 1. A Wholly Consistent Regime. The boun- daries of the internal market for financial services correspond fully with the boundar- ies of the jurisdiction of the regulatory authority. A single regulator supervises the gamut of institutions involved in financial services. 2. A Partially Consistent Regime. The de- fined internal market is territorially divided among a number of regulatory authorities who agree among themselves to recognize each others' competence and to establish a restricted set of common stand- ards. Accordingly, once they have been chartered by one of the regulatory authori- ties, firms can operate freely throughout the broader internal market. They are free to engage in any activity permitted either by their respective chartering authority or by authorities in other 'host' jurisdictions.1 3. A 'National Treatment' Regime. Borrow-. ing from the terminology of international trade, this regime again involves a number of regulatory authorities supervising a por- tion of a more broadly defined internal market. It is more restrictive than a par- tially consistent regime because each regu- latory authority requires a firm to apply for a separate licence to operate in its jurisdic- tion. In addition, licensed firms are per- mitted to engage only in those activities permitted by the 'host' authority and are subject to the supervision of that authority for such activities performed within its jur- isdiction. Institutions chartered by the 'host' authority and those chartered by other outside authorities are regulated in the same way and have the same business powers within a given jurisdiction. No dis- tinctions are made between 'domestic' and 'foreign' firms. 4. An Extraterritorial Regime. Similar to the national treatment regime, this ar- rangement includes a number of regulatory authorities sharing supervision of a broader internal market. It departs from national treatment in that one or more of these authorities requires as a condition of

operating within their jurisdiction that fi- nancial institutions follow their rules in all other jurisdictions. Thus, if such an author- ity said that commercial loans could com- prise a maximum of 15 per cent of total assets, then financial institutions wishing to operate within its territory would need to ensure that they complied with this max- imum, not only in that territory but also in all other jurisdictions. Taken to its extreme where all regulatory authorities behaved in this manner, the internal market would be crisscrossed with a melange of rules under- mining greatly the economic advantages of a single internal market. 5. A Protectionist Regime. A number of reg- ulatory authorities operate within a broader territory. Each authority erects barriers to prevent the entry of firms from other jurisdictions. 'Foreign' firms that do establish offices in a given territory face sharp restrictions that prevent them from offering any serious competition to domes- tic institutions.

II Evolution of the Regulatory System Until 1980

Until the end of the 1940s, the chartered banks occupied a dominant position in banking activities, suffering only minor competition from other financial interme- diaries. Given that these banks were regu- lated by a single office, the former Inspector General of Banks, the system approxi- mated the wholly consistent model. But developments in the subsequent four de- cades edged Canada progressively away from this model toward a national treat- ment regime with extraterritorial ele- ments. A national treatment regime also took hold in investment services.

Over the course of the 20th century, the Canadian approach to financial regulation came to be loosely organized around what has been called the 'four pillars'. Each pil- lar comprised a core function, a particular type of financial institution, and a separate regulator. Loosely defined, these pillars had formed around the functions of com-

Financial Services Reform 141

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

mercial banking, trusts and estates man- agement, underwriting of insurance, and investment banking. Traditionally, com- mercial banking was carried out by the domestically-owned chartered banks and was regulated by the Inspector General of Banks, a federal government agency at- tached to the Department of Finance. This arrangement was based on The Constitu- tion Act, 1867, which by section 91(15) allo- cates to the federal parliament legislative power in relation to 'banking, incorpora- tion of banks, and the issue of paper money'. Gradually over the 20th century, the chartered banks secured the addition of other activities to their core function, in- cluding consumer finance, residential mortgage lending, and longer-term de- posits.

Trust companies, which emerged in the 1870s, took responsibility for a second core function, trusts and estate management. Although trust companies could be chartered by the federal or provincial governments, jurisdiction over their core function fell clearly to the provinces based on section 92(13), the property and civil rights clause, of The Constitution Act, 1867. Hence, federally chartered trust companies remained subject to provincial government licensing and supervision when it came to trust and estates management. Similar to the chartered banks, trust companies added other activities to their core function, the most important being mortgage lend- ing, long-term investment certificates and term deposits. For provincially-chartered institutions, these were often defined in ways designed to ward off federal regula- tion.

Other types of financial institutions clustered around these two pillars. Build- ing societies, which emerged in the mid- 19th century, tended to evolve into loan cor- porations specializing in mortgage finance. In the 20th century, many of these corpora- tions became the property either of trust companies or of chartered banks. Financial co-operatives also began to be formed around the beginning of the 20th century.

Despite repeated efforts by Alphonse Des- jardins in Quebec to convince the federal government to set up a regulatory frame- work for financial co-operatives, it refused, arguing that these were local concerns more properly the responsibility of provin- cial governments (Rudin, 1990:124ff; Neufeld, 1972:384). In subsequent years, provincial governments gradually put into place a legislative framework for credit un- ions/caisses populaires and adapted this framework as the co-operatives expanded and set up provincial clearing corporations (centrals). The federal government added to this system in 1953 when it passed legislation empowering the Canadian Cooperative Credit Society (CCCS) to serve as a national central for several of the (Eng- lish Canadian) provincial centrals.

In short, the cluster of activities around the core functions of trust and estates man- agement and commercial banking respec- tively expanded throughout the 20th cen- tury to the point where the similarities between the respective institutions - chartered banks, financial co-operatives, and trust and loan companies - increas- ingly overshadowed any differences. Since the acceptance of deposits and the offering of loans are activities normally associated with banking, provincial governments in their supervision of some trust companies and of financial co-operatives quietly be- came participants in banking regulation. The original conception of a wholly con- sistent banking regime under the supervi- sion of a federal government regulator was slowly being undermined.

In anticipation of the revision of The Bank Act due in 1964, the federal govern- ment created a royal commission to review the whole banking and financial system. In its comprehensive study, the Porter Com- mission (Canada, 1964:362) noted that banks, some trust companies, and local fi- nancial co-operatives were all carrying on essentially similar business. Regretting that the patchwork system of regulation and supervision tended to inhibit competi- tion among these various institutions, it

142 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

recommended a new approach to regula- tion (Canada, 1964:363). The Commission suggested first that the federal government provide a functional definition of banking: the issuance of demand liabilities, transfer- able and short-term deposits, and other short-term banking claims. Based on this definition, it argued that the chartered banks, savings banks, some trust and loan companies, some sales finance companies and the central societies of credit unions and caisses populaires (but not the local co- operatives themselves) were all doing bank- ing and should be subject to federal super- vision and regulation. The proposed re- furbishment of the wholly consistent regu- latory system for banking was to be based on the federal government's jurisdiction in section 91(15). Constitutional experts agree that if the federal government were to pro- vide such a functional definition of bank- ing, it could extend its regulatory powers much as the Commission suggested (Hogg, 1985:528-32).

The federal government did not want another jurisdictional skirmish with the provinces in the already turbulent mid- 1960s. Nor did the chartered banks favour giving the 'near banks' full banking status. Accordingly, the federal government avoided political problems and did not re- spond to the Commission's recommenda- tions in the 1967 Bank Act. Subsequent fed- eral governments have not shown much interest in asserting their authority over banking.

Over the course of the 20th century, the core of investment services, the underwrit- ing of corporate equities and bonds, had come to be the business of specialized in- vestment dealers (Drummond, 1987). Com- mercial banks withdrew from this field early in the century and were formally barred from it in the 1980 Bank Act. Over the period from the mid-1920s to 1945, in- vestment services came to be supervised by provincial securities commissions in con- junction with industry-controlled self-reg- ulatory organizations (Dey and Makuch, 1979; Coleman, 1989). Ontario assumed a

leading role in developing regulatory policy and other provinces tended to follow (Wil- liamson, 1960), yielding again a regime that approximated the wholly consistent model. Nonetheless, the willingness of provinces to follow Ontario's lead tended to diminish over time.

Accordingly, Canada entered the present period of increasing internationalization and competition with threatened wholly consistent regulatory systems anchored on relatively fixed boundaries between bank- ing and investment services. These boun- daries were reinforced by the division of powers between the federal and provincial governments.

III Financial Services Regulation in the 1980s

The Actors In seeking to study the evolution of finan- cial services supervision and regulatory policy during the 1980s, it is useful to con- centrate our attention on the federal government and the three more important provincial governments - Ontario, Quebec, and British Columbia. Each of these authorities revamped its regulatory ap- paratus during the decade. These reforms tended to unify previously disparate agen- cies and branches and to increase the re- sources and visibility of supervisors.

Influenced by the Parizeau Report pub- lished 14 years earlier (Quebec, 1969), the Quebec government moved to strengthen its supervisory capacity in 1983 by concen- trating responsibility for trust and loan companies, financial co-operatives and in- surance companies in a new office, the In- specteur g6neral des institutions finan- cieres. Ontario followed in 1987 with the creation of a Ministry of Financial Institu- tions which was responsible for the same range of services as Quebec's Inspecteur g~ndral. British Columbia's new legislation in 1989 concentrated supervisory responsi- bilities in the hands of a new Superinten- dent of Financial Institutions. Finally, the federal government through the Financial

Financial Services Reform 143

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

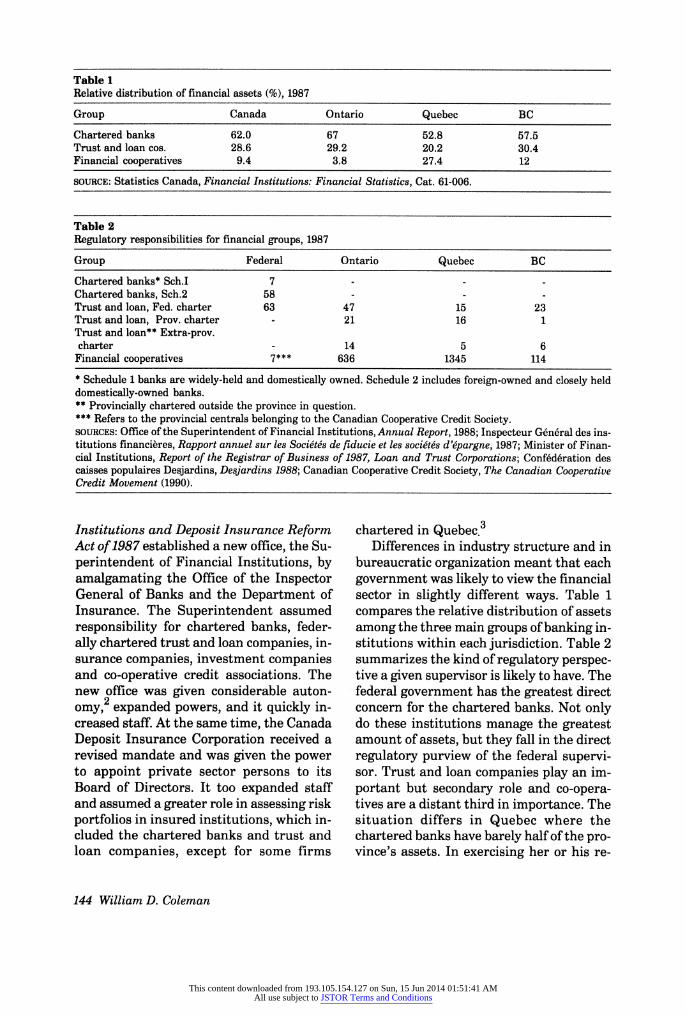

Table 1 Relative distribution of financial assets (%), 1987

Group Canada Ontario Quebec BC

Chartered banks 62.0 67 52.8 57.5 Trust and loan cos. 28.6 29.2 20.2 30.4 Financial cooperatives 9.4 3.8 27.4 12

SOURCE: Statistics Canada, Financial Institutions: Financial Statistics, Cat. 61-006.

Table 2 Regulatory responsibilities for financial groups, 1987

Group Federal Ontario Quebec BC

Chartered banks* Sch.I 7 Chartered banks, Sch.2 58 Trust and loan, Fed. charter 63 47 15 23 Trust and loan, Prov. charter - 21 16 1 Trust and loan** Extra-prov. charter - 14 5 6

Financial cooperatives 7*** 636 1345 114

* Schedule 1 banks are widely-held and domestically owned. Schedule 2 includes foreign-owned and closely held domestically-owned banks. ** Provincially chartered outside the province in question. *** Refers to the provincial centrals belonging to the Canadian Cooperative Credit Society. SOURCES: Office of the Superintendent of Financial Institutions, Annual Report, 1988; Inspecteur General des ins- titutions financibres, Rapport annuel sur les Socidt6s de fiducie et les socidtis d'dpargne, 1987; Minister of Finan- cial Institutions, Report of the Registrar of Business of 1987, Loan and Trust Corporations; Conf6d6ration des caisses populaires Desjardins, Desjardins 1988; Canadian Cooperative Credit Society, The Canadian Cooperative Credit Movement (1990).

Institutions and Deposit Insurance Reform Act of 1987 established a new office, the Su- perintendent of Financial Institutions, by amalgamating the Office of the Inspector General of Banks and the Department of Insurance. The Superintendent assumed responsibility for chartered banks, feder- ally chartered trust and loan companies, in- surance companies, investment companies and co-operative credit associations. The new office was given considerable auton- omy,2 expanded powers, and it quickly in- creased staff. At the same time, the Canada Deposit Insurance Corporation received a revised mandate and was given the power to appoint private sector persons to its Board of Directors. It too expanded staff and assumed a greater role in assessing risk portfolios in insured institutions, which in- cluded the chartered banks and trust and loan companies, except for some firms

chartered in Quebec.3 Differences in industry structure and in

bureaucratic organization meant that each government was likely to view the financial sector in slightly different ways. Table 1 compares the relative distribution of assets among the three main groups of banking in- stitutions within each jurisdiction. Table 2 summarizes the kind of regulatory perspec- tive a given supervisor is likely to have. The federal government has the greatest direct concern for the chartered banks. Not only do these institutions manage the greatest amount of assets, but they fall in the direct regulatory purview of the federal supervi- sor. Trust and loan companies play an im- portant but secondary role and co-opera- tives are a distant third in importance. The situation differs in Quebec where the chartered banks have barely half of the pro- vince's assets. In exercising her or his re-

144 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

sponsibilities which do not include over- sight of the chartered banks, the provincial supervisor will see co-operatives as of par- ticular importance, followed by trust and loan companies. The Ontario scenario reverses that of Quebec, with trust and loan companies commanding considerably more attention than credit unions. The British Columbia supervisor will have a view more similar to that of Quebec. Virtually no trust companies are chartered directly in BC, meaning that trust and loan supervisory re- sponsibilities are less onerous; credit un- ions will command greater attention.

Responsibility for the formulation of reg- ulatory policy also varies in the four juris- dictions. For the federal, Quebec and British Columbia governments, this re- sponsibility is assumed by the respective fi- nance ministries which, given their man- dates, are driven to consider financial sector reform in the context of broad mac- roeconomic objectives. Regulators are af- forded the opportunity to comment on policy proposals, but the final word rests with the finance minister. In Ontario, policy responsibility rests with a financial institutions ministry separate from the treasury department. Given its consumer protection mandate, this ministry is more likely to formulate policy concentrating on depositor safety rather than on macroe- conomic concerns. We see below that this regulatory mandate reinforces a tendency for Ontario to be the most conservative policy-maker among the four jurisdictions.

Finally, the institutional divisions in the marketplace are mirrored in the organiza- tion of interests (Coleman, 1988:chap.9). The chartered banks are represented by the Canadian Bankers' Association (CBA), a centralized group with representative of- fices in each of the principal provincial capi- tals. Trust and loan companies have the Trust Companies Association of Canada (TCAC) as their representative. The TCAC, with a staff about one-sixth that of the CBA, does not have permanent representation in the provincial capitals; it contents itself with a series of provincial divisions that are

operated with central office support. During the late 1980s, the association was weakened by the fact that not all trust com- panies, including the largest, were mem- bers. Representation of financial co-opera- tives tends to be quite fractured as befits their provincial orientation. The Canadian Cooperative Credit Society acts on behalf of English Canadian credit unions on the fed- eral plane while the provincial centrals per- form this function at the provincial level. The caisses populaires in Quebec do not belong to CCCS; they are represented politically at both federal and provincial levels by La Conf6deration des caisses populaires et d'6conomie Desjardins du Quebec. No peak association or committee exists for drawing together these various associations and financial co-operative cen- tral organizations.

Policy Developments By the early 1980s, a number of develop- ments pushed regulatory reform onto the policy agenda. Following the 1980 Bank Act, the federal government had committed itself to modernizing the legislation for other financial institutions. The ownership of trust companies had completed an evolu- tion toward closely-held ownership, usually with links to non-financial firms, that raised questions about basic ownership rules and regulatory procedures. Increas- ing overlapping in the provision of financial services by chartered banks, trust and loan companies, and financial co-operatives gave rise to the issue of a 'level (regulatory) playing field'. A little later in the decade, a series of failures of financial institutions added to the urgency for reform.

The federal government developed a first set of proposals in a Green Paper (Dept. of Finance, 1985), which was revised substantially in a White Paper published in 1986 (Dept. of Finance, 1986). Noteworthy in the latter document was a clear prefer- ence for widely-held ownership and for re- stricting ownership links between financial and non-financial firms. These federal pro- posals represented a challenge to Quebec

Financial Services Reform 145

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

which had accepted closely-held ownership and commercial links in its 1984 reform of insurance legislation.

In subsequent iterations in the policy process, it was evident that the key Canadian authorities were faced with weighing three somewhat contradictory ob- jectives: ensuring an efficient and competi- tive financial system; protecting deposi- tors; and encouraging the development of financial institutions under their own par- ticular jurisdiction. The fact that the key jurisdictions did not weigh these objectives in the same way hastened the decline of wholly consistent regulatory regimes in Canada.

In Ontario, new legislation was con- ceived against a backdrop of a series of widely publicized failures of trust and loan companies. When coupled with the fact that policy was developed by the regulatory authority and not by the treasury ministry, it was not surprising that depositor safety was the highest priority. In the words of a government official, 'Ontario probably has the strongest consumer protection mindset of all the jurisdictions ... Ontario says first our job is to protect the public and to ensure that their deposits or insurance or whatever is protected. Everybody else says that too, but it's a question of emphasis. We say that's goal number one. Most of the other governments say that's goal number two.'4 The new trust and loan legislation that came into effect in 1988 was very con- servative. It retained the traditional ap- proach of setting limits on particular kinds of lending and sought to restrict tightly transactions between shareholders and the company, and between companies related together in a conglomerate. It provided no specific encouragement to Ontario- chartered companies, nor did it greatly favour networking among financial institu- tions.

In fact, with consumer protection as its dominant thrust, it directly undermined the possibility even of a national treatment regulatory regime when it introduced the so-called 'equals approach' to regulation.

Presaged by a White paper in 1983 and en- dorsed by a special task force in 1985 (On- tario, 1985), this legislation states that a trust company that wishes to operate in On- tario must follow Ontario regulations and procedures in all its operations, including those in other provinces. This condition ap- plies even if the company is incorporated under federal law or the law of another pro- vince. In practice, then, the legislation is extra-territorial: any trust company that wishes to operate in Ontario, regardless of where it received its charter, must operate according to Ontario rules throughout Canada.

The Quebec government followed a very different strategy. In defining its objectives in a White Paper (Quebec, 1987:51-56), the Finance ministry listed first the need to en- sure the efficient functioning of the finan- cial system followed by consumer protec- tion. It then added two objectives not found in other jurisdictions: protecting Quebec's jurisdiction over financial services and pro- moting the growth of the financial sector it- self. In this respect, financial services was a sector chosen for particular government encouragement. The White Paper states (1987:61) that the government wants to en- courage financial institutions chartered by other governments to apply for a Quebec charter or to move part of their operations or portfolio to Quebec.

These objectives were at the centre of new legislation on insurance companies (1984), trust and loan companies and finan- cial co-operatives (1988), and on financial intermediaries (1989). These laws were dis- tinguished by a fairly conservative ap- proach to asset and liability management and by an innovative reworking of struc- tural relationships in order to encourage fi- nancial supermarkets, networking, and generally the decompartmentalization of the financial sector (Quebec, 1988). Quebec authorities also explicitly endorsed owner- ship linkages between commercial and fi- nancial firms (Quebec, 1990). They argued that commercial firms could be an impor- tant source of additional capital for finan-

146 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

cial institutions; revised regulatory poli- cies, in turn, would discourage self-dealing and would protect the depositor base of the financial intermediaries. Taken together, these reforms were designed to promote such Quebec-based institutions as the co- operative Mouvement Desjardins, in- digenous financial conglomerates (the Laurentian Group, Power Financial), and more broadly based conglomerates (Bell Canada Enterprises, Imasco).

British Columbia followed yet a third course, a course that gives greatest empha- sis to ensuring an effective and efficient fi- nancial sector. In the words of a BC govern- ment official, 'the purpose of regulating the financial sector is one of economic effi- ciency ... The Government's role then is to make that industry as efficient as it can be by ensuring that confidence in the financial system is there'. But the same official stressed that the instillation of confidence must not come from extensive state inter- vention: 'the economic efficiency costs of over-regulation are such that we want to very carefully balance where we draw the line between instilling confidence by regu- lating and intervening in a market'. This reluctance led the same official finally to distinguish British Columbia's approach from that of Quebec: 'Quebec's objective is to encourage economic development through the financial sector and that is to use a Quebec incorporated approach ... In the B.C. view, the financial sector is an im- portant part of the economy and it should work to provide that function but the government should not be forcing that. That is most properly a market-directed ac- tivity for allocating those resources.'5 The resulting BC legislation, the Financial In- stitutions Act 1989, reflected these priori- ties by moving away from the more tradi- tional regulatory legislation found in Ontario and Quebec toward the 'prudent investor' approach.6 They also opened the door to ownership linkages between differ- ent types of financial institutions and to some networking and financial super- markets, as found in Quebec (BC, 1988).

The final federal reforms were tabled in 1990 following these provincial changes (Dept. of Finance, 1990). They left room for two different ownership regimes, one based on the widely-held chartered banks and fi- nancial co-operatives and the other on closely-held trust companies, foreign banks and nascent domestic chartered banks. Trust companies would need to widen the proportion of shares sold publicly, a move designed to anchor a new internal control system over self-dealing. The federal government also favoured a prudent inves- tor approach similar to that found in BC. In shifting away from the principles enun- ciated in its 1986 White Paper, the federal policy lowered significantly the number of areas of conflict with Quebec. In essence, Ontario was left as the odd province out.

The regulatory picture became even more complex with the deregulation of in- vestment services. Beginning in the 1960s, a flurry of financial innovations gradually served to blur the boundaries between banking and investment services. Con- sequently, the Canadian chartered banks began to seek re-entry into corporate un- derwriting in order to maintain market share and to compete better with universal banks common in Europe.7 When the Com- mission des valeurs mobilibres du Quebec accepted a bank-owned securities dealer late in 1986, the Ontario and federal governments agreed to let the barrier fall. Banks, trust companies, and financial co- operatives were permitted to be active in corporate underwriting, but were required to operate through separately capitalized securities affiliates. These would house ac- tivities related to the primary distribution of equity securities, primary distribution of corporate debt securities, and secondary market trading in equity securities. When the chartered banks either purchased in- vestment houses or set up their own (Bore- ham, 1990), they entered into the regula- tory purview of provincial securities commissions. This change in status was not an easy one and led to a series of juris- dictional skirmishes between the provinces

Financial Services Reform 147

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

and the Office of the Superintendent of Fi- nancial Institutions (OSFI), the federal regulator. Peace obtained when a series of bilateral memoranda of understanding were signed between OSFI and respective provincial governments.

By 1990, therefore, investment services were regulated under a national treatment regime, with the provinces still the domi- nant players. Banking was governed by a similar regime, but with an extraterritorial component arising out of Ontario's 'equals approach'. Coordinating structures varied for the two systems. In investment services, despite increasing legislative differences, provincial securities commissions had a long tradition of co-operation in the de- velopment of 'national' regulations to be adopted in each jurisdiction. They had their own organization, the Canadian Securities Administrators, with an extensive com- mittee structure and a habit of regular meetings. In the banking area, arrange- ments were less formalized. The Western provinces met in the spring of 1988 and for- mally agreed to improve the exchange of in- formation and to consult on further policy changes. Quebec welcomed this initiative, convened a meeting of all relevant provin- cial officials in October 1988, and succeeded in having the agreement expanded to in- clude all provinces. Yet this agreement did not put into place any permanent co-ordi- nating body, a step recommended by the then President of the Canadian Bankers Association (MacIntosh, 1988) and by the Senate Banking Committee (Canada, 1990). More important, like the Canadian Securities Administrators, it did not in- clude the most important regulatory authority, the federal government. The 'equals approach' adopted by Ontario further complicated efforts at policy co- ordination. By its very character, it repre- sented a vote of non-confidence in other su- pervisors, generating some tension and ill-will in the process.

In the absence of permanent federal-pro- vincial co-ordinating bodies, the reform process was remarkably haphazard. After

consultations with the provinces by the fed- eral government following its 1985 Green Paper, no other systematic consultation took place. The respective provinces tended to develop their reforms in relative isola- tion from one another and from the federal government. The federal proposals that emerged in 1990 tried to respond to these provincial changes, but the differences among the provinces made this a difficult task. By the end of 1991, when the federal proposals became law, Canada had moved further away from wholly consistent regu- latory regimes for financial services than at any other time in the postwar period.

IV Federalism and Policy Conflict

The trend in Canada toward divergent reg- ulatory perspectives and increased difficul- ties in harmonizing regulatory and super- vision policy contrasts sharply with de- velopments in other nation states. With its new banking act of 1984, France brought under a single supervisory system commer- cial banks, state-supported savings banks, agricultural co-operatives, co-operatives oriented toward small business, regional co-operatives, finance houses, leasing firms and factoring concerns (Voisin, 1987). Suc- cessive reforms in Britain in 1979, 1986 and 1987 have created a common regulatory base for the highly diverse British banking sector, have broken down the long-standing barriers between commercial banks and building societies, and produced a regula- tory system for investment banking that is closely co-ordinated with the Bank of Eng- land (Moran, 1986; 1990).

It might be countered that Britain and France are unitary states. Yet in Germany, a federal state, three revisions of the bank- ing law since 1976 ensure a single super- visory system for private commercial banks, community-owned savings banks, publicly controlled Landesbanken, mort- gage savings banks, and financial co-opera- tives (Hiitz, 1990). These changes have not been impeded by the fact that the largest deposit gathering group in the German

148 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

banking system, the Sparkassen and Land- esbanken, are publicly-owned and closely linked to the state (Lainder) governments. More striking, the European Economic Community, with only the skeleton of a confederal constitution and widely differ- ing banking systems, has put into place a legal framework that will create a partially- consistent regulatory regime in the Com- munity as a whole. Only the United States among countries relevant for comparison had more difficulties than Canada in developing a relatively consistent regula- tory regime.

There is no reason to assume that the Canadian financial sector was more heter- ogeneous than those found in these other jurisdictions. Hence it would seem that one might look to political variables in a search for explanations of the Canadian develop- ments. In itself, the division of powers in Canadian federalism presented opportuni- ties for erecting a wholly consistent regula- tory system. Section 91(15) provided ample room for the federal government to assume fuller responsibility for banking regulation. Earlier studies also showed that the federal government had constitutional authority for taking a prominent role in the regula- tion of investment services (Anisman and Hogg, 1979).8 In short, it is difficult to argue that federalism in its own right was an ob- stacle to more harmonized regulatory ar- rangements.

An explanation of Canadian develop- ments must thus take a more complex route: in the absence of a consensus on basic policy principles among key societal actors, disputes were transposed from the bureaucratic to the political realm for reso- lution, a forum that gave free rein to fed- eral-provincial and Quebec nationalist con- flicts. The resulting admixture of a national treatment and an extraterritorial regime was based heavily on mutual distrust among regulatory authorities.

First, it is important to note that the Canadian interest intermediation system had no real capacity for reaching a consen- sus on matters in dispute. As we indicated

in the first section of this article, each fi- nancial services subsector is organized by a distinct association. This segmented pat- tern of organization reinforced rather than cross-cut the most important policy dis- putes in the field. Thus, the chartered banks and English-Canadian financial co- operatives supported the widely-held ownership principle and the Trust Compa- nies Association, home to the trust compa- nies owned by large conglomerates, defended the closely-held model and the possibility of ownership links between fi- nancial and non-financial firms. The In- vestment Dealers Association of Canada fought long and hard to maintain a division between investment services and commer- cial banking, with the other associations as its principal foes. The final difficult issue involved the question of retailing insurance in bank and trust company branches and pitted the Canadian Life and Health In- surance Association plus various brokers and underwriters associations against the chartered banks' and trust companies' as- sociations.

Given then that the Canadian financial sector had no peak associations in the fi- nancial services sector available for resolv- ing internal conflicts, and that different governments had competing objectives as we have seen, these disputes entered a more public and political domain for reso- lution. Only at this point did federal struc- tures in Canada work against a harmonious conclusion. The dispute over ownership structures became a particularly treacher- ous minefield. The widely-held ownership principle was supported by the Canadian Bankers' Association, the best-funded lobby in the field, and by the Bank of Canada which saw it as the key to a stable financial system.9 The principle also had some support from the federal supervisor's office. In contrast, the closely-held prin- ciple enjoyed the backing of the largest trust companies and of their owners, in- cluding such influential business persons as Paul Desmarais and Peter and Edgar Bronfman. These persons were able to pres-

Financial Services Reform 149

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

sure the Prime Minister's Office directly. In addition, the principle received support from Quebec, which saw conglomerates as important contributors to the growth of its financial structure, and from BC, which wanted more competition for the chartered banks, and hence a more efficient financial sector.

These battle lines tended to mirror those drawn over the question whether commer- cial firms should be able to own financial institutions. Here again Quebec played a pivotal role. With its objective of building up an indigenous Quebec-based financial sector, it saw these linkages as crucial sources of capital for financial sector growth. No other government in Canada treated financial services in this way as a special 'chosen' sector. Consistent with the objective of building an autonomous fran- cophone business community that had been central to government policy since 1960, the Quebec government believed that a self- sufficient financial sector was vital to its own political autonomy. Its consistent sup- port for the expansion of the co-operative- based Mouvement Desjardins conglom- erate and its staunch opposition to any federal involvement in the regulation of provincial financial institutions were re- lated components of this policy objective. Partisan consensus between the Liberal party and the Parti quebbcois on these basic goals and the policy lead given by Jacques Parizeau10 enabled Quebec to move quickly and efficiently on an innovative set of policy reforms. Other jurisdictions, particularly the federal government, were left on the defensive.

Finally, the issue of regulating securities activities of banks and federally-chartered trust companies was drawn into the fed- eral-provincial maw. Given the emphasis in international circles on consolidated super- vision of financial conglomerates and the high level of international trading in securi- ties, it might have been predicted that the banking supervisor would come to oversee the securities activities of the chartered banks and federal trust companies. Or,

deregulation might have provided the im- petus for creating a national securities reg- ulator similar to those already found in the United States, Britain, France and Japan. From the outset, the provinces, particularly Quebec and British Columbia, would cede no ground in the securities area. The result- ing political compromise sees somewhat clumsy information-sharing arrangements between the federal supervisor and the pro- vincial securities commissions, with the lat- ter remaining the lead regulators of securi- ties. And Canada continues to be rep- resented in such important international fora as the International Organization of Securities Commissions by Ontario and Quebec. No other country has its repre- sentation divided among sub-national agencies.11

V Conclusion

The process of regulatory reforms of finan- cial services in Canada during the 1980s did not produce an optimal regulatory system. There is a single market for financial serv- ices and international pressures are suffi- ciently strong to require that market to be more efficient than it has been in the past. Accordingly, national treatment regimes (with extraterritorial elements for bank- ing) are anachronistic and an obstacle to efficient operations. In addition, regulatory complexity may render more difficult the protection of consumers of financial serv- ices.

At this stage, it would be politically naive to expect the federal government to exert its authority and to establish wholly con- sistent regulatory regimes for banking and investment services. A close alternative would be a partially consistent regime analogous to the system that has developed in the European Economic Community. The changes required are not unrealistic, even in the Canadian context. 1. Establishment of a permanent federal-

provincial co-ordinating body composed of regulators which would meet regu- larly and would assume responsibility

150 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

for ensuring a single market for financial services.12

2. Agreement by the regulators with parlia- mentary approval on a restricted set of common standards related to capital adequacy, solvability, self-dealing and related matters.

3. Mutual recognition of regulatory com- petence. Hence a financial services firm chartered under one jurisdiction would have a 'licence' to operate freely in all jurisdictions. The 'home' authority as- sumes regulatory responsibility.

Such a system would be a significant change from the present regime because it would assume relevant jurisdictions trust rather than distrust one another. It would still permit regulators to innovate in developing policy, albeit within defined limits, thereby keeping the system rela- tively dynamic. The permanent dialogue among officials on regulatory principles and procedures would probably foster a sys- tem more responsive to problems and hence better protective of consumers' interests. Finally, regulatory arrangements would facilitate, rather than impede, the single market in financial services in Canada.

Notes

* Research supported by Social Sciences and Humanities Research Council, Research Grant 410-88-0629.

1 Beginning at the end of 1992, this model will govern banking in the European Economic Com- munity. See Commission des Communaut6s Europ6ennes (1990) for an overview.

2 The Superintendent was appointed by the Gover- nor-in-Council for a seven-year term and the of- fice was designated as a 'separate employer' allowing it to assume responsibility for its own personnel policy.

3 Quebec is the only province to have set up and put into effect a separate deposit insurance facility, the R6gie d'Assurance-D6p6ts du Quebec. This agency insures the deposits of financial co-opera- tives, of provincially-chartered trust companies held in Quebec, and of some federal and extra-pro- vincial trust companies held in Quebec.

4 Confidential interview, April 1989. 5 Confidential interview, June 1989. 6 Prudent standards are defined in the act as 'those

that in the overall context of an investment and loan portfolio, a prudent person would apply to in- vestments and loans made on behalf of another person to whom there is owed a fiduciary duty to make investments without undue risk of loss and with a reasonable expectation of fair return' (BC, 1989:s.133).

7 Universal bank is a term used in various ways. Here we use it in the general sense to refer to banks that offer the gamut of financial services from traditional banking to investment banking, portfolio management, and investment counsel- ling.

8 Some of the political obstacles to occupying this room are reviewed by Courchene (1986:chap.8).

9 The Bank's position was made known in the tes- timony by then Governor Gerald Bouey (1985) to the House of Commons Finance Committee which was conducting hearings on the government's Green Paper on reform.

10 Parizeau had headed a Quebec government study commission in the late 1960s (Quebec, 1969) whose report presaged somewhat the approach to reform he later followed as Finance Minister. This line was continued by Pierre Fortin who had re- sponsibility for financial reforms under the Bourassa government between 1985 and 1989. Fortin now has a senior executive position with the Mouvement Desjardins.

11 For a while, Germany, also a federal state where the Liinder have important control over securities regulation, was represented by a trade associa- tion, the Arbeitsgemeinschaft der deutschen Wertpapierb6rsen. Recently, the Lander and fed- eral government have agreed to have the federal Finance ministry serve as the German repre- sentative.

12 For a discussion of the role of such a committee in the EEC and its increasing importance in EEC banking matters, see France, Commission ban- caire (1990).

References

Anisman, Philip and Peter Hogg (1979) 'Consti- tutional Aspects of Federal Securities Legislation.' In Canada, Consumer and Cor- porate Affairs Canada. Proposals for a Se- curities Markets Law for Canada, Vol. 3, Background Papers (Ottawa: Supply and Services Canada).

Boreham, Gordon (1990) 'Three Years After Canada's "Little Bang",' Canadian Banker, 97(5):6-15.

Bouey, Gerald K. (1985) 'Statement on the Green Paper,' Bank of Canada Review (August):3-8.

British Columbia. Ministry of Finance and Cor-

Financial Services Reform 151

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions

porate Relations (1988) Financial Institu- tions Act: Major Policy Proposals (Victoria).

- (1989) Financial Institutions Act. Bryant, Ralph C. (1987) International Financial

Intermediation (Washington: Brookings). Canada. Royal Commission on Banking and Fi-

nance (1964) Report (Ottawa: Queen's Printer).

Canada. Senate, Standing Committee on Bank- ing, Trade and Commerce (1990) Canada 1992: Toward a National Market in Finan- cial Services (Ottawa).

Coleman, William D. (1988) Business and Politics: A Study of Collective Action (Mon- treal: McGill-Queen's University Press).

- (1989) 'Self-Regulation in the Canadian Se- curities Industry: A Case Study of the Invest- ment Dealers Association of Canada,' Canadian Public Administration, 32 (Winter):503-23.

Commission des Communautes Europ6ennes (1990) Un Marche Commun des Services (Luxembourg: Official Publications of the European Communities).

Courchene, Thomas (1986) Economic Manage- ment and the Division of Powers. Studies of the Royal Commission on the Economic Union and Development Prospects for Canada, Vol. 67 (Toronto: University of Toronto Press).

Department of Finance (1985) The Regulation of Canadian Financial Institutions: Pro- posals for Discussion (Ottawa: Department of Finance).

- (1986) New Directions for the Financial Sector (Ottawa: Department of Finance).

- (1990) Reform of Federal Financial Institu- tions Legislation: Overview of Legislative Proposals (Ottawa: Department of Finance).

Dey, Peter and Stanley Makuch (1979) 'Govern- ment Supervision of Self-Regulatory Organi- zations in the Canadian Securities Industry.' In Canada, Consumer and Corporate Affairs Canada. Proposals for a Securities Markets Law for Canada, Vol. 3, Background Papers (Ottawa: Supply and Services Canada).

Drummond, Ian W. (1987) Progress Without Planning: The Economic History of Ontario from Confederation to the Second World War (Toronto: University of Toronto Press).

Economic Council of Canada (1987) A Frame- work for Financial Regulation (Ottawa: Supply and Services Canada).

(1989) Globalization and Canada's Finan- cial Markets: A Research Report (Ottawa: Supply and Services Canada).

France, Commission Bancaire (1990) 'L'6labor- ation du droit bancaire europ6en,' Bulletin de la Commission bancaire, No. 3:79-94.

Hogg, Peter (1985) Constitutional Law of Canada, 2nd ed. (Toronto: Carswell).

Hfitz, Gerhard (1990) Die Bankenaufsicht in den BRD und in den USA: Ein Rechtsver- gleich (Berlin: Dunckler and Humblot).

MacIntosh, Robert (1988) 'Quebec's Financial System After Meech Lake: Remarks to the Canadian Club of Montreal' (Toronto: Canadian Bankers' Association).

Moran, Michael (1986) The Politics of Banking, 2nd ed. (London: Macmillan).

(1990) 'Regulating Britain, Regulating America: Corporatism and the Securities In- dustry.' In Colin Crouch and Ronald Dore (eds.), Corporatism and Accountability: Or- ganized Interests in British Public Life (Ox- ford: The Clarendon Press).

Neufeld, E.P. (1972) The Financial System of Canada: Its Growth and Development (New York: St. Martin's Press).

Ontario, Task Force on Financial Institutions (1985) Final Report. Toronto.

Pauly, Louis W. (1988) Opening Financial Markets: Banking Politics in the Pacific Rim (Ithaca: Cornell University Press).

Quebec. Study Committee on Financial Institu- tions (1969) Report (Quebec: Editeur officiel).

(1987) Reform of Financial Institutions in Quebec (Quebec: Editeur officiel).

(1988) Decompartmentalization of Interme- diaries: Discussion Paper (Quebec: Editeur officiel).

(1.990) Quinquennial Report on the Appli- cation of the Act Respecting Insurance: Changes (Quebec: Office du Ministere des Fi- nances).

Rudin, Ronald (1990) In Whose Interest? Que- bec's Caisse Populaires 1900-1945 (Montreal: McGill-Queen's University Press).

Voisin, Colette (1987) 'Le systeme bancaire frangais: vingt ans de mutations,' Regards sur l'actualiti, 128:3-41.

Williamson, J. Peter (1960) Securities Regula- tion in Canada (Toronto: University of Toronto Press).

152 William D. Coleman

This content downloaded from 193.105.154.127 on Sun, 15 Jun 2014 01:51:41 AMAll use subject to JSTOR Terms and Conditions