Embed Size (px)

Citation preview

Financial SectorFinance 724/824, Spring 2011

Lauren Kirk, Krystal Patel, Bryan McElwain, Matt McHenry, Chris Koenig

Table of ContentsFinancial Sector

Overview of Sector

Business Analysis

Financial Analysis

Valuation Analysis

Recommendation

Economic Analysis

Section 1

Section 2

Section 3

Section 4

Section 5

Section 6

2

Overview of Financial SectorA category of stocks containing firms that provide

financial services to commercial and retail customers.

This sector includes banks, investment funds, insurance

companies and real estate.

3

• Financial Sector is 3rd largest

at 17% of overall market

Overview of Financial Sector

23%

18%

17%

12%

11%

9%

6%

3% 2% Basic Materials

Consumer Goods

Financial

Technology

Industrial Goods

Healthcare

Services

Utilities

Conglomerates

4

• Financial Sector is 2nd

largest at 15.47% of S&P

• Market Cap: $1922.61B

Overview of Financial Sector

5

10.60%

10.42%

13.09%

15.47%

11.27%

11.23%

18.07%

3.66%

2.98%3.21%

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Telecom Services

Utitlies

52%

15%

5%

5%

5%

3%

3%2%

2%

2%

Money Center Banks

Regional - Midwest Banks

Asset Management

Foreign Regional Banks

Property & Casualty

Insurance

Life Insurance

REIT - Diversified

Investment Brokerage -

National

Insurance Brokers

Real Estate Development

Top 10 Industries make up 94% of Financial Sector

Money Center Banks make up 52% of entire Financial Sector

Financial SectorTop Industries

6

Company Ticker Market Cap ($B) EPS P/E NP margin

Operating

Margin ROE

JP Morgan JPM 181.63 4.5 10.12 16.91% 42.10% 9.69%

Wells Fargo WFC 153.53 2.42 11.99 14.86% 22.30% 10.53%

Citigroup Inc C 132.78 0.31 14.64 12.65% 15.22% 6.67%

Bank of America BAC 125 -0.44 - -2.03% -1.20% -1.77%

Goldman Sachs GS 78.93 9.11 16.65 18.17% 28.05% 11.50%

American Express Co AXP 58.93 3.59 13.65 13.42% 19.72% 26.15%

American Intl Group Inc AIG 56.13 14.11 2.21 15.62% 23.20% 30.11%

US Bancorp USB 49.52 1.94 13.28 18.20% 23.41% 12.80%

Metlife Inc MET 49.19 3.17 14.69 5.27% 7.51% 6.51%

Morgan Stanley MS 40.48 1.76 14.87 14.36% 16.31% 7.97%

BlackRock Inc BLK 37.59 11.27 17.4 23.80% 34.81% 8.06%

The Bank of

New York Mellon BK 35.74 2.13 13.5 19.08% 26.62% 8.43%

Simon Property Group SPG 33.62 2.08 54.99 19.04% 35.01% 13.27%

PNC Finl Services Group PNC 32.64 5.97 10.4 19.16% 25.73% 8.77%

Prudential Financial Inc PRU 30.89 5.75 11.02 8.10% 11.51% 9.39%

Lincoln National Corp LNC 9.86 2.56 12.18 9.14% 14.65% 6.60%

CIT Group Inc. CIT 8.5 2.18 19.45 8.19% 12.07% 5.97%

Top Players in Financial Sector

7

•As of 3/31, we have $213,107 in gains

•2 of the four financial stocks are in the top 10 holdings of the portfolio

Quick Facts

S&P Weight: 15.47%

SIM Weight: 14.19%

SIM relative to S&P: -1.29%

SIM Class Financial Sector

8

Quantity Security Ticker GIC Sector Unit Cost Total CostMarket Price Market Value Gain

30,000 Wells Fargo & Company WFC Financials 30.23 $906,804.72 31.71 $951,300.00 $44,495.28

21,000 JPMorgan Chase & Co JPM Financials 41.18 $864,859.08 46.10 $968,100.00 $103,240.92

17,400 CIT Group Inc. CIT Financials 43.29 $753,162.48 42.55 $740,370.00 -$12,792.48

15,700 Lincoln National Corporation LNC Financials 25.06 $393,463.98 30.04 $471,628.00 $78,164.02

$2,918,290.26 $3,131,398.00 $213,107.74

Top 10 Holdings

Ticker Security Mkt. Value % Mkt. Value

CVX Chevron Corp. $1,074,900 4.87%

AAPL Apple Inc. $1,045,523 4.74%

WMT Wal-Mart Stores Inc. $972,034 4.41%

JPM JPMorgan Chase & Co $968,100 4.39%

GD General Dynamics Corp. $957,000 4.34%

WFC Wells Fargo & Company $951,300 4.31%

NIHD NII Holdings Inc. $941,742 4.27%

RIG Transocean LTD $904,220 4.10%

FLS Flowserve Corp. $901,600 4.09%

HPQ Hewlett Packard Co. $889,049 4.03%

Grand Total $9,605,467 43.53%

*MetLife currently not in SIM Portfolio

Sector PerformanceSector Last 12 months Last 3 months Last 1 month

Energy (XOM.S) 28.68 11.29 2.40

Material (DD.S) 33.66 10.30 6.26

Industrials (GE.S) 28.17 7.59 5.20

Consumer Discretionary (TGT.S) 32.88 9.18 8.26

Consumer Staples (PG.S) 24.73 11.86 8.26

Healthcare (MRK.S) 22.20 13.14 9.48

Financials (JPM.S) 10.26 5.07 2.96

Information Technology (MSFT.S) 25.22 5.69 4.39

Telecom (VZ.S) 29.93 7.73 4.64

Utilities (EXC.S) 15.65 7.10 6.67

9

Morningstar.com

External Factors

Political

Dodd-Frank Legislation

Reform Consumer Protection Act

Unemployment rate

2-year treasury note rate

Velocity of money supply

Federal funds rate

Personal savings rate

10

Economic

• Maturity Phase

• Barriers to entry high

• High Capital Requirements

• Regulations

• Competition and Consolidation

• Bank of America/Merrill Lynch

• JP Morgan buys failed WaMu

• Buyer Power

• Commodity for general customers

• Supplier Power

• Federal Reserve

• Substitution

• Savings, Credit Cards, Investing, Insurance

• Commodity for general customers

Porter’s 5 Forces

11

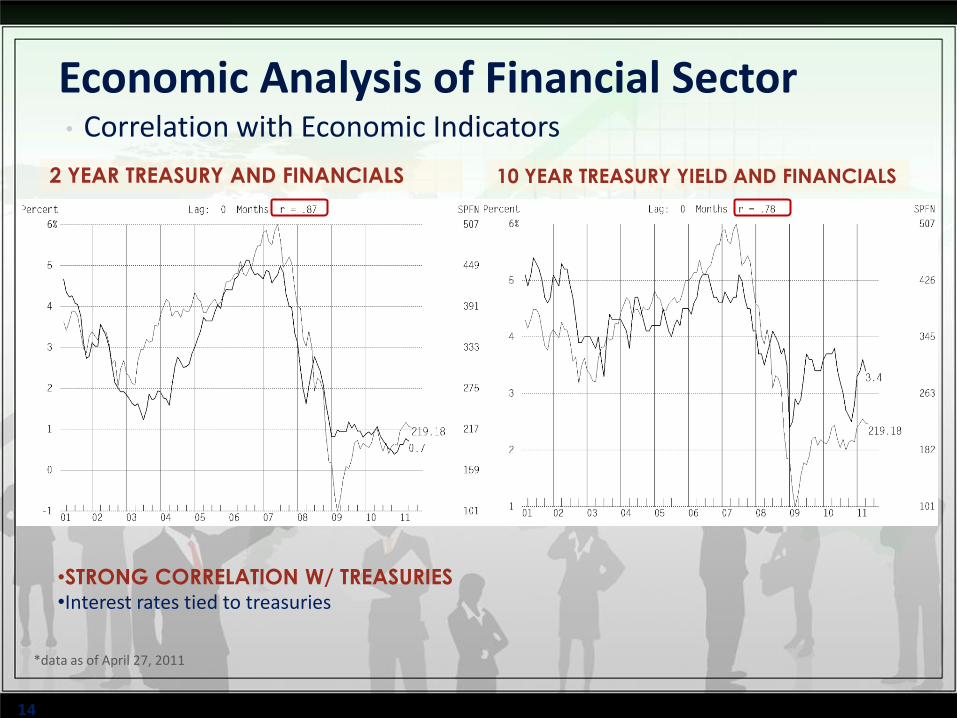

Economic Analysis

12

FEDERAL FUNDS RATE AND FINANCIALS EMPLOYMENT AND FINANCIALS

Economic Analysis of Financial Sector• Correlation with Economic Indicators

•STRONG CORRELATION W/ FED FUNDS RATE•Cut from 1.0% to .25% in 2008

• Influences short-term interest rates, deposits, bank loans, credit card interest rates, and adjustable-rate mortgages

•STRONG CORRELATION WITH EMPLOYMENT

•Hit high of 10.2% in Oct ‘09

13

2 YEAR TREASURY AND FINANCIALS 10 YEAR TREASURY YIELD AND FINANCIALS

Economic Analysis of Financial Sector• Correlation with Economic Indicators

*data as of April 27, 2011

14

•STRONG CORRELATION W/ TREASURIES•Interest rates tied to treasuries

HOUSING STARTS AND FINANCIALS CONSUMER CONFIDENCE AND FINANCIALS

Economic Analysis of Financial Sector• Correlation with Economic Indicators

Number of new houses on which construction has been started

•2005: 2,068,300 homes•2010: 586,900 homes

15

Increasing•Now at 65.4•Depends on labor market, global economy, etc.

Financial Analysis

16

•21% drop in 2008

•Downward slope since that point

• Earnings per Share

growth rates:

•5 yr at -52%

•3 yr at 50%

•Current Yr at 14%

•Long term at 7%

Financial Sector Revenues

17

Sector Net Profit Margin Relative to S&P

Net Profit

High 2.3

Low -0.2

Median 2.1

Current 1.3

18

Financial Sector - Industry Revenues

Revenues Historical Growth Rates Expected Growth Rate

Industry10 yr 5 yr 3 yr

Last 12

Months

Current Q

(March)

Current Yr

('11)

Next Yr

('12)

Money Center Banks 1% -5% -5% -22% -24% -10% 5%

Regional Banks 2% -5% -12% -17% -9% -10% 3%

Asset Management 8% -3% -13% 19% 20% 20% 9%

Property & Casualty

Insurance3% 1% 0% -11% 3% 7% 2%

Life Insurance 5% 3% -3% 14% 3% 4% 5%

REIT - Diversified - - -10% 0% -4% -2% -2%

Investment Brokerage -

National1% -19% -2% -2% -12% 4% 8%

Insurance Brokers 4% -7% -5% -7% -15% -9% 1%

Real Estate Development - - -23% 7% 38% 33% 10%

19

Financial Sector - Industry EPS

ESP Historical Growth Rates Expected Growth Rate

Industry10 yr 5 yr 3 yr

Last 12

Months

Current Q

(March)

Current Yr

('11)

Next Year

('12)

Future

Growth Rate

Money Center Banks -14% - 156% 235% -1% 21% 30% 5%

Regional Banks -18% - - 170% - 104% 42% 6%

Asset Management 5% -4% -12% 15% 15% 14% 17% 11%

Property & Casualty

Insurance8% -8% -2% -37% -14% 0% 11% 9%

Life Insurance 8% -2% -3% 21% 9% 10% 12% 12%

REIT - Diversified - - -15% 8% 6% 1% 2% 5%

Investment Brokerage

- National-9% - 387% 14% -73% 6% 31% 12%

Insurance Brokers -10% - 227% -32% 16% -14% 14% 11%

Real Estate

Development- - -15% -1% -1% 14% 16% 7%

20

Valuation Analysis

21

Financial Sector ValuationTrailing P/E

22

*10 year time period

Financial Sector ValuationForward P/E

23

*10 year time period

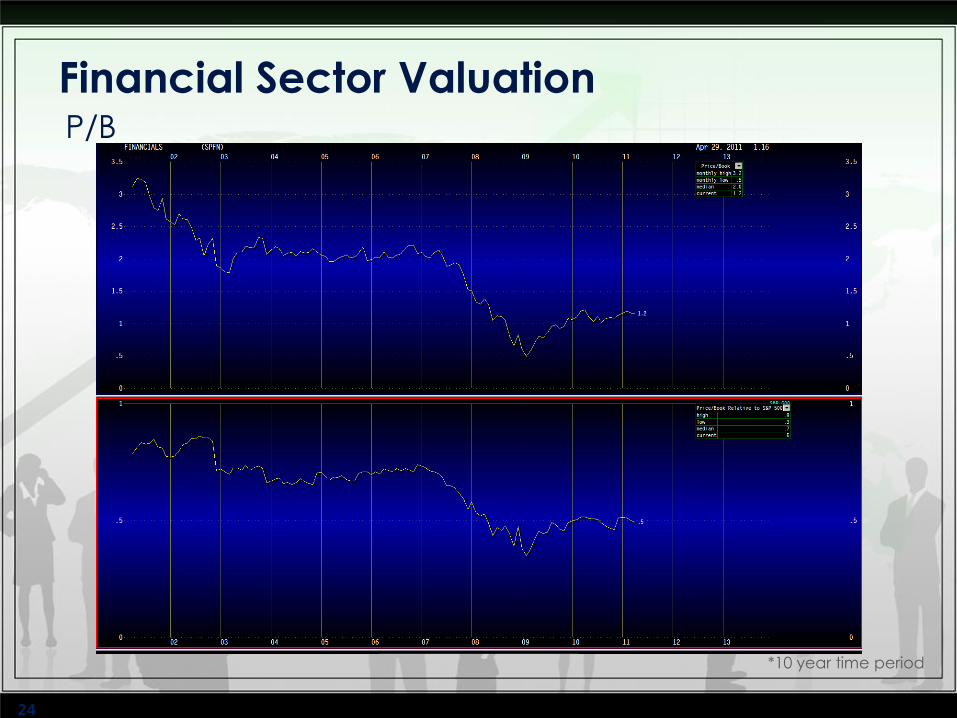

Financial Sector ValuationP/B

24

*10 year time period

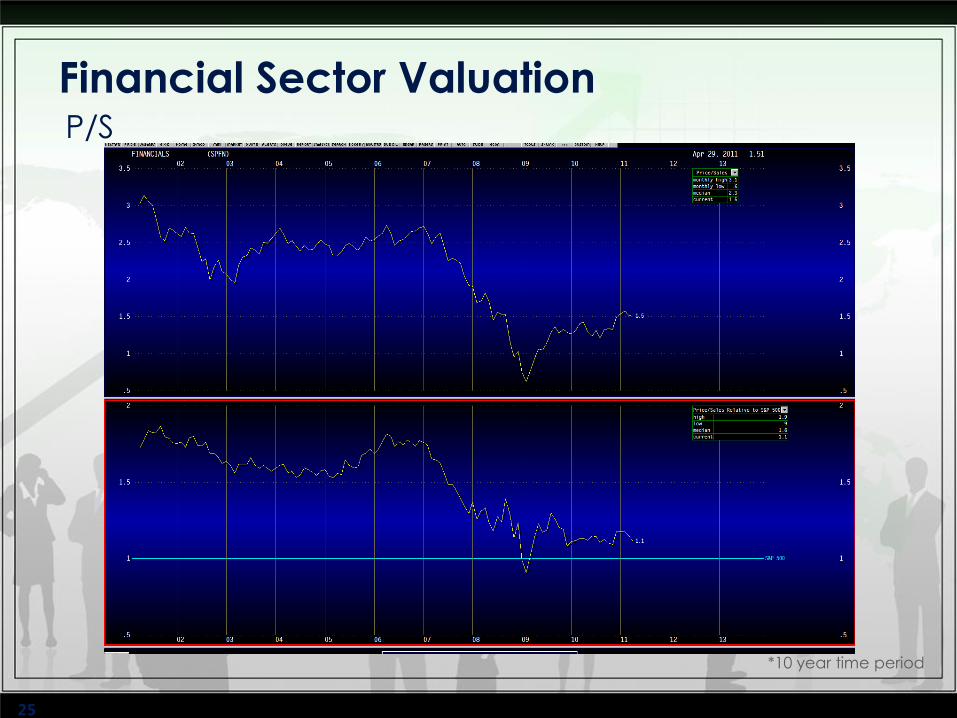

Financial Sector ValuationP/S

25

*10 year time period

•Overall in sector and industries, current valuations are below the median

Financial Sector Valuation

Absolute Basis High Low Median Current

P/Trailing E 135.2 10.5 14.0 13.8

P/Forward E 20.1 10.6 12.7 12.2

P/B 3.2 .5 2.0 1.1

P/S 3.1 .6 2.4 1.5

P/CF 140.7 7.2 9.9 10.8

Relative to SP500 High Low Median Current

P/Trailing E 7.8 .65 .77 .89

P/Forward E 1.4 .60 .77 .87

P/B .9 .3 .7 .5

P/S 1.9 .9 1.6 1.1

P/CF 13.4 .7 .9 1.1

26

*10 year time period

Industry ValuationRelative to S&P 500

Absolute

Basis

High Low Median Current

P/Trailing E 17.2 4.0 13.1 9.8

P/Forward E 15.0 4.4 12.4 8.9

P/B 2.2 .5 1.5 1.0

P/S 1.5 .3 1.1 .9

P/CF 13.8 4.6 10.7 9.3

Relative to

SP500

High Low Median Current

P/Trailing E .87 .38 .69 .64

P/Forward E .90 .35 .70 .64

P/B .7 .3 .5 .4

P/S 1.0 .4 .7 .7

P/CF 1.1 .6 1.0 .9

Insurance/Life Insurance

Mortgage Investment

Absolute

Basis

High Low Median Current

P/Trailing E 54.3 10.4 22.7 18.7

P/Forward E 39.7 11.9 18.1 16.3

P/B 5.7 .7 2.3 1.5

P/S 9.2 1.9 6.4 3.8

P/CF 27.9 6.7 14.6 14.6

Relative to

SP500

High Low Median Current

P/Trailing E 2.9 .90 1.3 1.2

P/Forward E 2.9 .90 1.2 1.2

P/B 2.0 .5 .9 .7

P/S 6.9 2.4 4.2 2.9

P/CF 2.6 .7 1.5 1.5

27

*10 year time period

Industry ValuationRelative to S&P 500

Money Center Banks

28

*10 year time period

Absolute Basis High Low Median Current

P/Trailing E 54.8 9.5 13.7 13.3

P/Forward E 25.2 10.0 12.4 11.0

P/B 2.8 0.7 2.1 1.4

P/S 3.9 0.8 3.3 2.0

P/CF 32.8 5.6 10.3 11.4

Relative to SP500 High Low Median Current

P/Trailing E 4.6 0.61 0.74 0.88

P/Forward E 1.6 0.52 0.75 0.80

P/B 0.9 0.5 0.7 0.6

P/S 2.7 1.2 2.2 1.5

P/CF 2.9 0.7 1.0 1.2

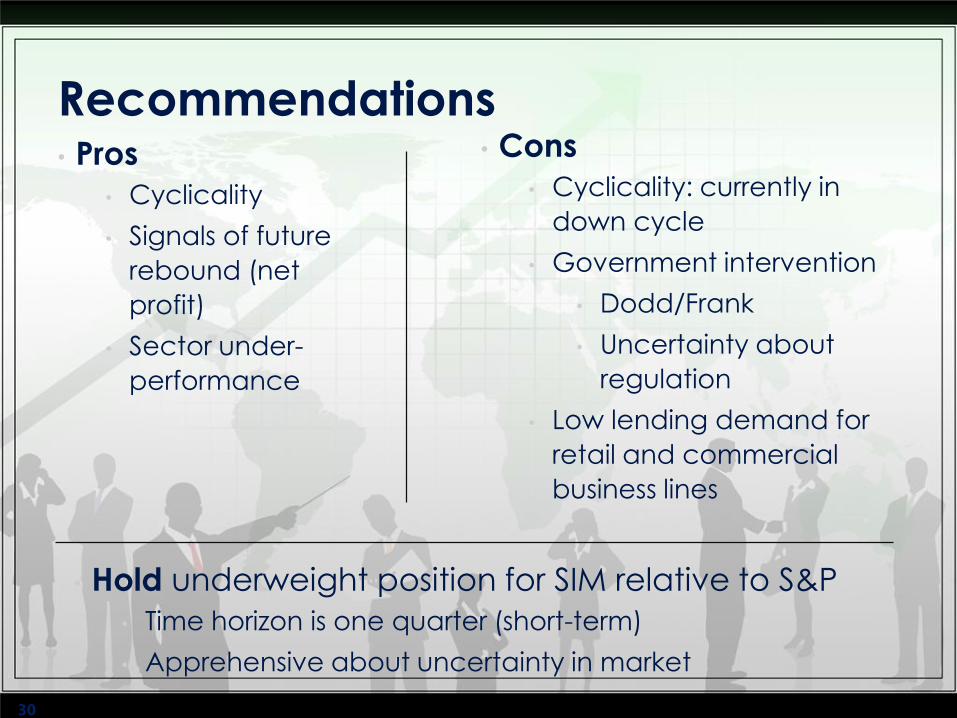

Recommendations

29

• Pros

• Cyclicality

• Signals of future

rebound (net

profit)

• Sector under-

performance

Recommendations

30

• Cons

• Cyclicality: currently in

down cycle

• Government intervention

• Dodd/Frank

• Uncertainty about

regulation

• Low lending demand for

retail and commercial

business lines

• Hold underweight position for SIM relative to S&P

• Time horizon is one quarter (short-term)

• Apprehensive about uncertainty in market

QUESTIONS?31

![Liziê D. T. Prola, Lilian Buriol, Clarissa P. Frizzo ... · 8a, 10a, 11a, and 1.0 mmol for 9a), 2-aminoacetophenone (1.0 mmol), [HMIM][TsO] (1.0 mmol) and TsOH (1.0 mmol). After](https://img.pdfslide.us/doc/110x75/5f6d314f14e48a24b56ae7a6/lizi-d-t-prola-lilian-buriol-clarissa-p-frizzo-8a-10a-11a-and-10.jpg)