Embed Size (px)

Citation preview

Financial Sector Development

Sustainable Growth, Regional Balance, Social Development for Poverty Reduction

Bangkok, October 26, 2006Renuka VongviriyathamGE Money Retail Bank

More balance financial sectorNo. of financial institutions supervised by BOT declinedFinancial strength of Thai banks improvedLoan growth in line w/ econ growth

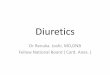

Thai Financial Sector: More Resilient to Shock

Financial Strength of Thai Commercial Banks

0%

10%

20%

30%

40%

50%

60%

70%

80%

1998

1999

2000

2001

2002

2003

2004

2005

1H06

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%% of (risk) assets

% Reserve to NPLs (LS)

% NPLs to Loans (LS)

ROA (RS)

Tier 1 (LS)

Pre-crisis

Jun-97Dec-02 Dec-04 Oct-05 Jan-06

Domestic Private Banks 14 6 [1] 6 8 [6] 10 [9]

Domestic Private Banks (with the majority foreign ownership and control)

0 4 [2] 3 [5] 4 [7] 4 [10]

Foreign (single branch) Banks 14 18 18 18 17State-owned Banks 1 3 [3] 3 3 3 [11]

Total Commercial Banks 28 31 30 33 34Finance Companies 91 19 18 13 9 [12]

Credit Foncier Companies 12 6 5 5 4 [13]

Specialized Financial Institutions 7 9 [4] 8 [5] 10 [8] 10Total Financial Institutions 138 65 61 61 57Stand-alone IBFs of Foreign Banks 17 7 4 2 0Total 155 72 65 63 57

Source: BOT & WB’s estimate

Source: BOT & SEC & WB’s estimate Source: BOT & WB’s estimate

Financial Sector Breakdown

0%20%40%60%80%

100%

19

96

19

98

19

99

20

02

20

03

20

04

20

05

1H 2

00

6

Total Bond MarketStock marketLoans from financial inst .

Major Reform ActionsSeveral Master Plans being implemented

Financial Sector Master Plan (2004-2009); Capital Market Master Plan II (2006-2010); and Insurance Master Plan (2006)Master Plan for Grass Root Financial Services (draft)

BOT’s supervisory policies, procedures, practices being strengthened & more transparentSome improvement in contract enforcement regime

Formal out-of-court mediation framework establishedSpecial Bankruptcy Court establishedLegal execution process streamlined to expedite auctions of foreclosed assets

Credit Bureau in operations and governing law amendedCapital market development

New Public Debt Law enacted (2005); Bond market information centralized; a central depository agency created Derivatives Law enacted; TFEX launched its equity future in 2006

Deregulation of consumer finance market

Reform GapsLegal reform for contract enforcement and secured transactionBanking law & Central Bank lawLimited deposit insurance – to enhance market disciplineAmendments to Public Limited Companies law; Securities and Exchange law; Insurance Industry lawSupervision of financial conglomerate and insurance industryPolicy direction for state-owned financial institutions and its implementation (incl. risk management & CG & supervision)Restriction on issuance of gov’t securitiesRestriction on utilization of Credit Bureau information

Looking in Detail: Resiliency to Shock not Tested

Performance variedLarge private banks capable of weathering economic shocksSmall players need to strengthen their franchises to compete

NPLs and ReserveJune 06

-

2

4

6

8

10

12

14

16

18

20

Ba

nk

A

Ba

nk

B

Ba

nk

C

Ba

nk

D

Ba

nk

E

Ba

nk

F

Ba

nk

G

Ba

nk

H

Ba

nk

I

Ba

nk

J

Ba

nk

K -

20

40

60

80

100

120NPLsReserve coverage

% of Loans % of NPLs

Source: FitchRatings; Phatra Securities

Source: FitchRatings; Phatra Securities Source: FitchRatings; Phatra

SecuritiesInterest Spread of Thai Commercial

Banks

CapitalJune 06

0%

5%

10%

15%

20%

25%

Ba

nk

A

Ba

nk

B

Ba

nk

C

Ba

nk

D

Ba

nk

E

Ba

nk

F

Ba

nk

G

Ba

nk

H

Ba

nk

I

Ba

nk

J

Ba

nk

K

% of Loans

Areas for Improvement

Reasons for Reduction in Headline NPLs

0

200

400

600

800

1000

1200

Debt rest .(net of

reentry NPLs )

Reclassifiedas PLs

Transfer toAMC

Write-off Others incl.principle

repay .

Bill

ion

Bah

t 18%17%

25%

13%

27%

Resource allocation

Efficiency; credit risk

Source: BOT & WB’s estimate

Source: BOT & WB’s estimate

Source: BOT & WB’s estimate

Source: BOT & WB’s estimate

Asset quality

Number of Population per Branch ofBanks and SFIs (BAAC, GSB, and GHB)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000P

erso

ns

per

bra

nch

Bangkok

Central

North South

East

Northeast

Thailand's Average

Access to finance

MLR minus 3m Deposit Rates and NetLoan Spread of Thai Commercial Banks

-1

-1

2

3

4

5

6

7

8

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Percent

MLR - 3m Deposit Rates

Net Loan Spread

Share of Financial Inst's Loans

0%20%40%60%80%

100%1

99

6

19

98

19

99

20

02

20

03

20

04

20

05

1H 0

6

finco and credit foncier companiesforeign banksprivate commercial banksstate commercial banksSFIs

Looking into the FutureSaving for retirement & growth

Are we saving enough?How to increase return on saving?Not only boost saving but not waste itInstruments

More efficient financial intermediaries

Balance bet. efficiency and stabilityInfrastructure & legal frameworkMarket mechanism & supervisionEffective exit mechanism

Financial service liberalizationUnavoidable When and how?Prepare for increase in volatility

Access to financeSMEs Low income HH

Demographic Trend

0%

20%

40%

60%

80%

100%

1996 2000 2005 2010 2015 2020

60+

50-59

30-39

20-29

0-19

Source: NSO & WB’s estimate

Domestic Saving to GDP Ratios

0

5

10

15

20

25

30

35

40

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

as %

of

GD

P

Gross domestic saving to GDP ratioHousehold saving to GDP ratioCorporate saving to GDP ratio

Source: NI 1980-2001 and NI 2004

Appendix

WB’s CDP-FC Program

Launched in April 03Subsequent to crisis responded assistance and CDPC – both emphasized short-term structural reform to cope with the impact of the financial crisisGeared toward medium-term issues of enhancing competitiveness of the financial and corporate sectorsConcluded in June 06

The Country Development Partnership (CDP) is a knowledge-based partnership that provides support

in terms of policy advice, third party technical assistance, and capacity building in response to the

needs of the authorities.

CDP-FC: CDP Financial and Corporate Sector Competitiveness

CDPC: CDP Competitiveness

Strengthening financial sector strategy and structureEnhancing supervision and regulationImproving the speed and quality of corporate debt restructuringEnhancing intermediation on a risk-adjusted basisImproving corporate governanceDeveloping capital markets

CDP-FC’s Six Components

CDP-FC’s End OutcomesPromote sustainable growthDecrease vulnerability, frequency, and costs of downturnsImprove resource allocation to most productive uses Ensure access to assets and income opportunities for all segments of society

CDP-FC’s Intermediate Outcomes

1. Strengthen the Financial Sector Strategy and Structure

2. Enhance Supervision and Regulation

3. Improve the Speed and Quality of Corporate Debt Restructuring

4. Enhance Intermediation on a Risk Adjusted Basis

5. Enhance Corporate Governance

6. Develop Capital Markets

Strengthen the financial sector strategy and structureImprove the depth and efficiency of the financial sector Enhance market discipline of deposit taking financial institutionsIncrease access to financial services to SMEs and low-income household

Enhance supervision and capacity of supervisors for financial institutions Improve framework to supervise financial conglomerate and better cooperation across regulatory agenciesEnhance disclosure by financial institutions

Improve speed and quality of corporate restructuring via TAMC Improve the legal regime for credit enforcementImprove out-of-court debt restructuring regime

Enhance level playing field between state and private financial institutions as well as between small and large institutionsStrengthen information infrastructure

Enhance corporate governance, disclosure, and accountability of Thai firmsImprove accounting and auditing standards and professionalsStrengthen the oversight and the accountability of the board of directors of public companiesStrengthen shareholders’ right

Enhance the depth and efficiency of domestic capital market as alternative sourceImprove market liquidity and transparencyPrimary market mechanism strengthenedThe quality of supplies improvedEfficiency of the trading and the clearing & settlement platforms for securities trading strengthened Improve risk management mechanism for market players