Embed Size (px)

Citation preview

Financial Risk Management of Insurance Enterprises

Swaps

Overview

• What is a swap contract?

• Which swap contracts are most popular?

• How is an interest rate swap structured?

• How does a swap contract differ from forwards and futures?

• What are some applications of swaps?

Why Did Swap Contracts Evolve?

• Breakdown of the Bretton Woods system of fixed exchanged rates occurred in the early 1970s

• Companies were exposed to exchange rate volatility if they had foreign subsidiaries

• Profits produced by subsidiary, when translated to dollars, produced losses– e.g., the dollar price of foreign currencies was uncertain

• Wanted a hedge to protect against FX volatility

Before Swaps

• Companies used parallel back-to-back loans

• Interest paid on borrowing is in foreign currency, interest received is in dollars– Principal amount of loans selected so that interest

payments equal income of subsidiary

• Problems with back-to-back loans– Default of counterparty did not release obligation– Inflated balance sheet amount of debt

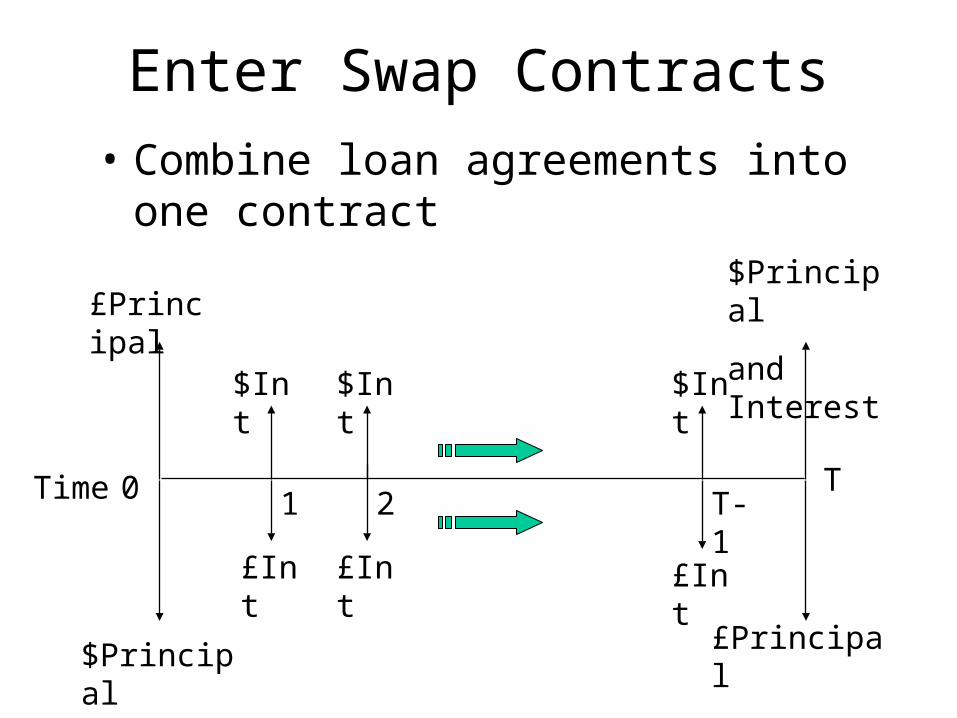

Enter Swap Contracts

• Combine loan agreements into one contract

$Principal

$Principal

and Interest£Principal

£Principal

and Interest

0 1 2 T-1TTime

$Int $Int $Int

£Int £Int £Int

Currency Swap

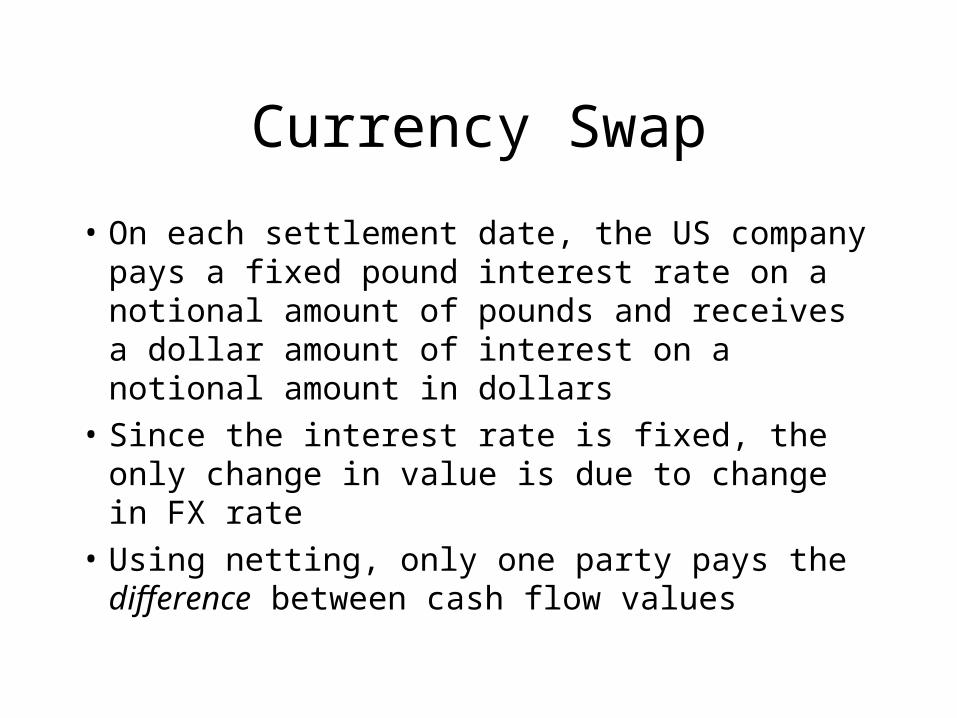

• On each settlement date, the US company pays a fixed pound interest rate on a notional amount of pounds and receives a dollar amount of interest on a notional amount in dollars

• Since the interest rate is fixed, the only change in value is due to change in FX rate

• Using netting, only one party pays the difference between cash flow values

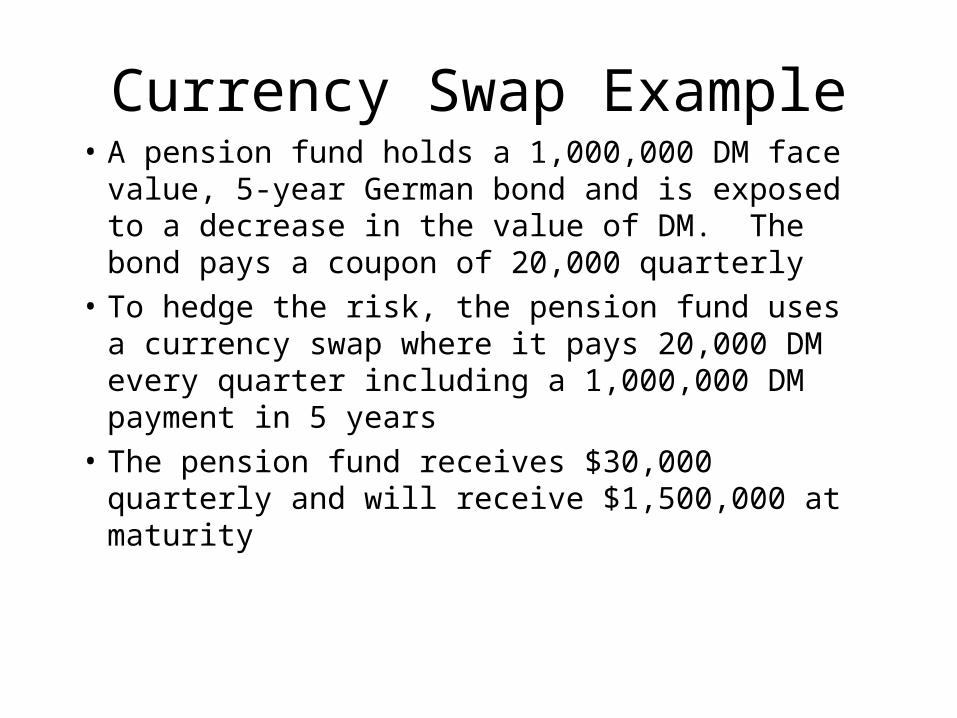

Currency Swap Example• A pension fund holds a 1,000,000 DM face value,

5-year German bond and is exposed to a decrease in the value of DM. The bond pays a coupon of 20,000 quarterly

• To hedge the risk, the pension fund uses a currency swap where it pays 20,000 DM every quarter including a 1,000,000 DM payment in 5 years

• The pension fund receives $30,000 quarterly and will receive $1,500,000 at maturity

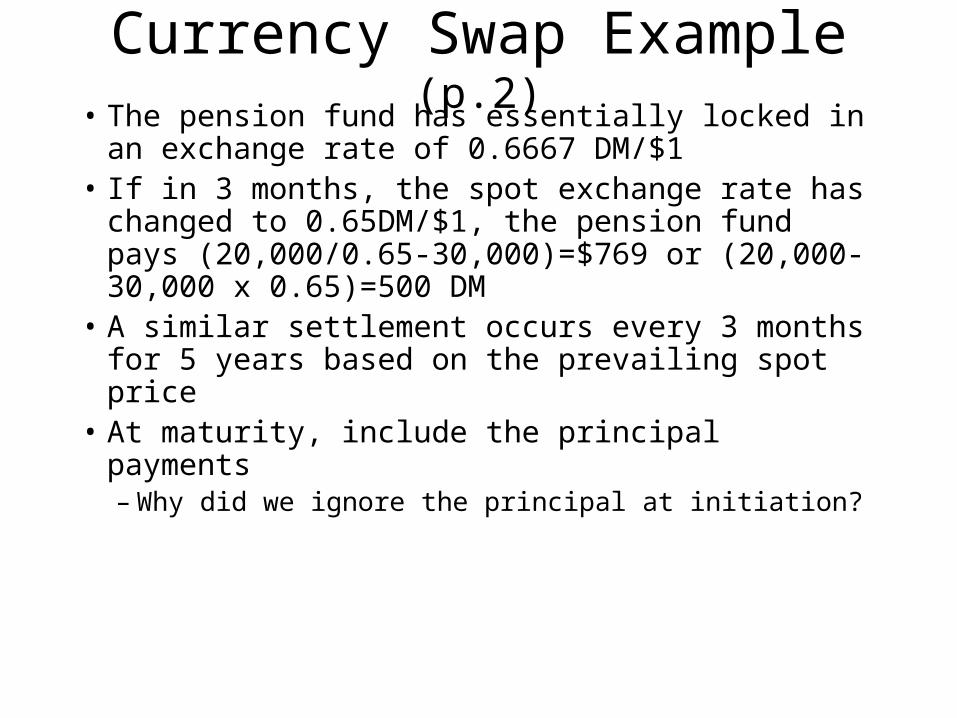

Currency Swap Example (p.2)• The pension fund has essentially locked in an

exchange rate of 0.6667 DM/$1• If in 3 months, the spot exchange rate has changed

to 0.65DM/$1, the pension fund pays (20,000/0.65-30,000)=$769 or (20,000-30,000 x 0.65)=500 DM

• A similar settlement occurs every 3 months for 5 years based on the prevailing spot price

• At maturity, include the principal payments– Why did we ignore the principal at initiation?

Swap Contract Provisions

• An agreement between two parties to exchange (or swap) periodic cash flows

• At each payment date, only the net value of cash flows is exchanged

• The cash flows are based on a notional principal or notional amount

• The notional amount is only used to determine the cash flows

Other Swaps

• Although concerns of foreign currency volatility were the primary force behind the evolution in swaps, other swaps are commonly used

• Currency-coupon or cross-currency interest rate swap– Still two different currencies– One interest rate is a fixed rate, one rate is floating

Other Swaps (p.2)

• Interest rate swap– Special case of currency-coupon swap: there is only

one currency– Two interest rates: one fixed and one floating– Interest rate swaps are now the most actively traded

type of swap contract– We will see its usefulness to insurers

• Basis-rate swap or basis swap– Interest rate swap with two floating rates

Other Swaps (p.3)

• Commodity swap (e.g., oil swap)– Notional principal is in units of a commodity

– Over the entire life of the swap, one party pays a fixed price per commodity unit, the other party pays a floating price

• Equity swap– One party pays the return on an equity index (such as

the S&P 500) while receiving a floating interest rate

– Really a type of basis swap

Commodity Swap Example• P/L insurer expects to pay claims over the next 4 years

on existing policies. A portion of the claims are based on lumber costs. Insurer estimates that it will require 80,000 board-feet of lumber every 6 months.

• Insurer is exposed to increasing lumber prices

• Forward contracts are liquid for short-term only. Insurer can lock in a fixed price by entering into a swap with a notional amount of 80,000 board-feet of lumber at a price of $350 per 1,000 board-feet

Commodity Swap Example (p.2)• In 6 months, if the spot price of lumber increases to $400

per 1,000 board-feet, the insurer receives (400-350) x 80 =$4,000– The gain on the swap will offset the higher cash prices that the

insurer pays on lumber

• Now, one year into the swap, scientists invent a seed for a quick-growing tree which increases the supply of lumber, and the price of lumber drops to $250 per 1,000 board-feet, the insurer must pay $8,000

• Net effect is fixed price for 80,000 board-feet

A Closer Look at Interest Rate Swaps

• One party pays a fixed interest rate while receiving a floating rate payment

• Typical contract:– Floating rate is LIBOR (note, this has credit

risk)– Settlement is quarterly

• However, interest rate swaps are privately negotiated so anything goes

A Closer Look at Interest Rate Swaps (p. 2)

• Assume a quarterly settlement• At the first settlement date (in three months),

the floating rate is (current) spot 3-month LIBOR

• For future periods, the floating side is determined by the future level of LIBOR

• At settlement, the payment is based on the difference of LIBOR and the fixed rate times the notional principal

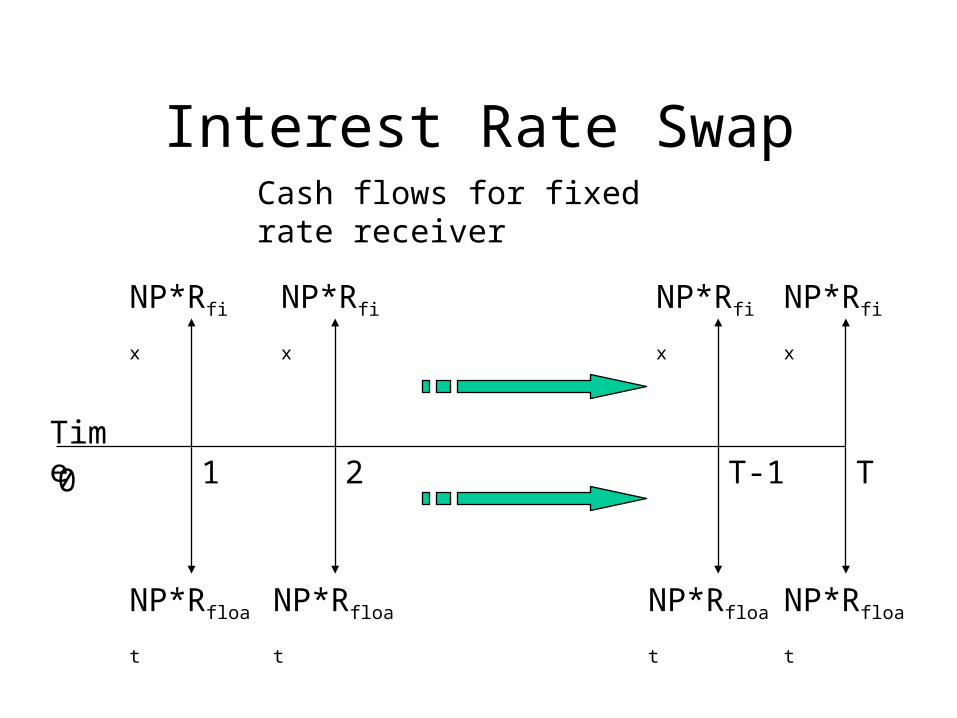

Interest Rate Swap

NP*Rfix NP*Rfix NP*Rfix NP*Rfix

NP*Rfloat NP*Rfloat NP*Rfloat NP*Rfloat

Cash flows for fixed rate receiver

Time

0 1 2 T-1 T

Why Use Interest Rate Swaps?• Essentially translates a fixed cash flow into a

floating cash flow (or vice versa)

• Companies with interest rate exposure can adjust their interest rate risk

• Insurers with long term assets and shorter term liabilities can enter a swap in which they pay a fixed rate and receive a floating rate– This swap provides cash inflows if interest rates rise

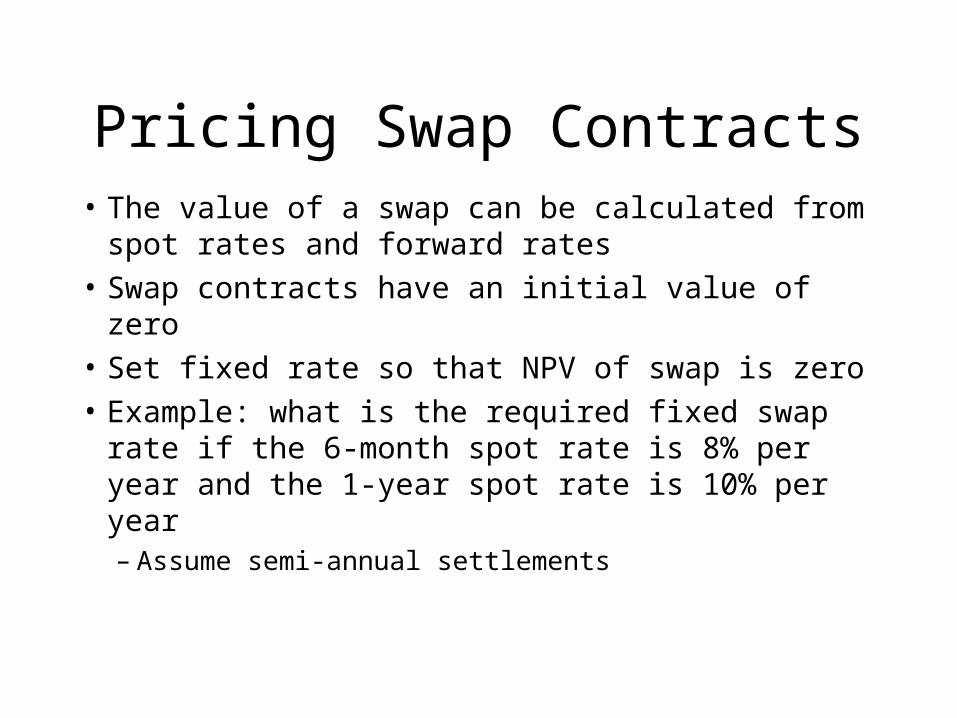

Pricing Swap Contracts• The value of a swap can be calculated from

spot rates and forward rates

• Swap contracts have an initial value of zero

• Set fixed rate so that NPV of swap is zero

• Example: what is the required fixed swap rate if the 6-month spot rate is 8% per year and the 1-year spot rate is 10% per year– Assume semi-annual settlements

Pricing an Interest Rate Swap

%70.9

0101

75.5

)081(

00.4

:zero is NPV that soset is rate fixed The

%5.1121)08.1(

10.1

10.1)1()08.1(

2

1

2

11

2

1

1

2

12

1

2

1

R

.

R%-

.

R%-

R

or

R

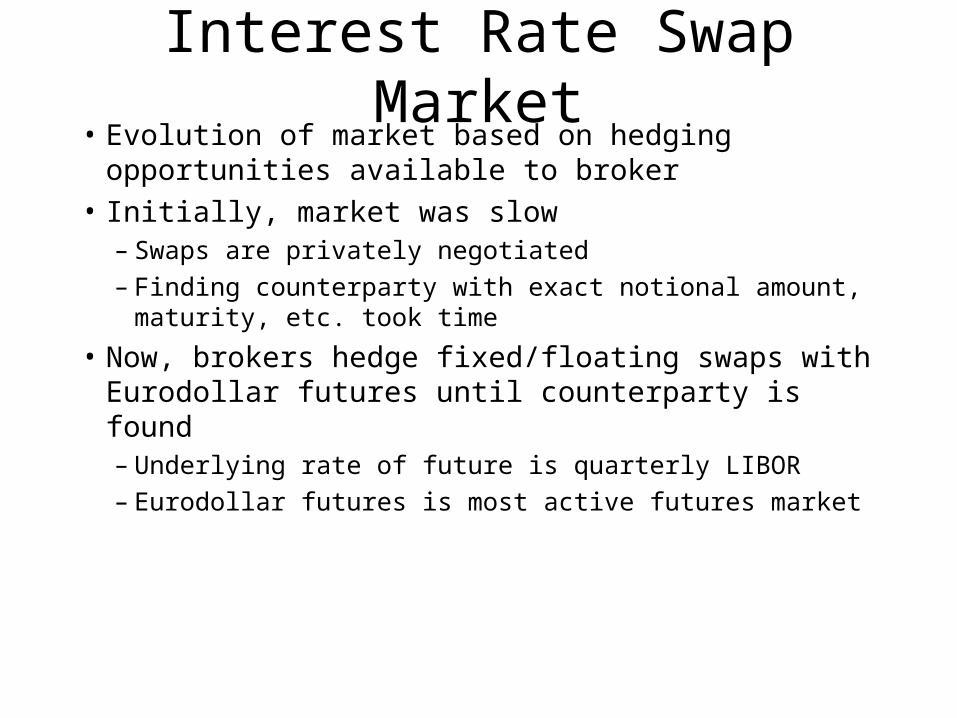

Interest Rate Swap Market• Evolution of market based on hedging opportunities

available to broker• Initially, market was slow

– Swaps are privately negotiated– Finding counterparty with exact notional amount, maturity,

etc. took time

• Now, brokers hedge fixed/floating swaps with Eurodollar futures until counterparty is found– Underlying rate of future is quarterly LIBOR– Eurodollar futures is most active futures market

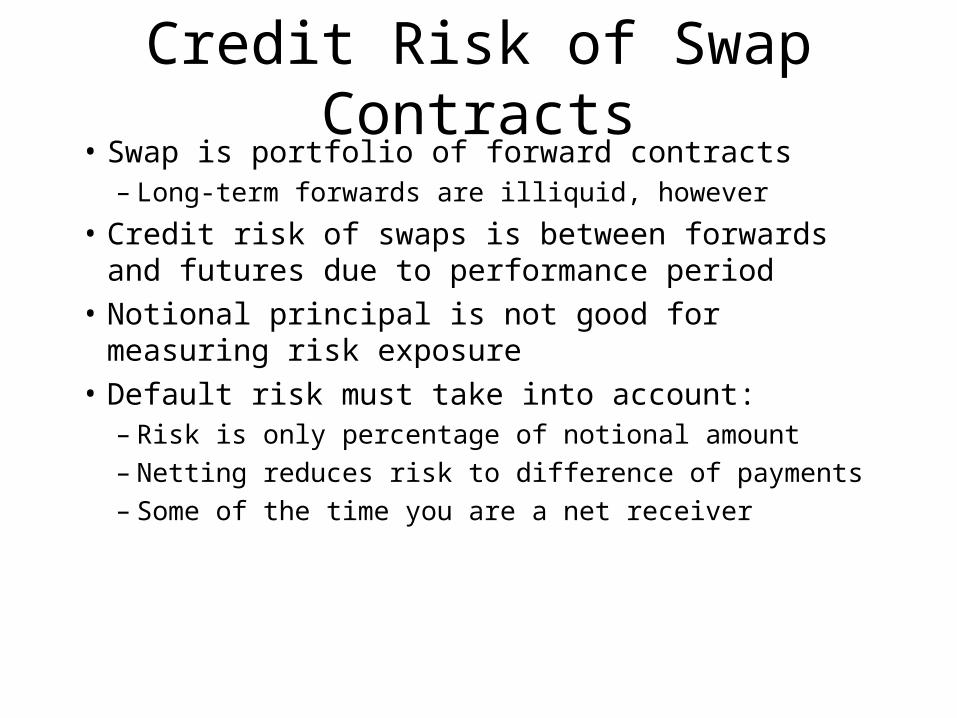

Credit Risk of Swap Contracts• Swap is portfolio of forward contracts

– Long-term forwards are illiquid, however

• Credit risk of swaps is between forwards and futures due to performance period

• Notional principal is not good for measuring risk exposure

• Default risk must take into account:– Risk is only percentage of notional amount– Netting reduces risk to difference of payments– Some of the time you are a net receiver

Next Lecture

• Options - puts and calls

• What is the difference between options and other derivative contracts?

• Applications of option contracts