Embed Size (px)

Citation preview

Financial Risk Management for Insurers

1. Futures Contracts

2. Interest Rate Futures

Overview

• What is a futures contract?

• How does a futures contract differ from a forward contract?

• What is the basis and what determines the relationship of the spot and futures price?

• What types of interest rate futures exist?

• How do we price interest rate futures?

• How do we determine the best hedge?

Futures Contract Basics

• Similar to a forward, a future obligates one party to buy and another to sell a specified asset in the future at a price agreed on today

• Futures can be cash settled or require physical delivery of underlying asset

• Most contracts are closed out before maturity

What is the use of a futures contract?

• Help reduce uncertainty in future spot price• Agricultural futures were one early contract

– Farmer can lock in future price of corn before harvest (protect against drop in price)

– User of corn can protect against rise in price

• Futures are now available on many assets– Agricultural (corn, soybeans, wheat, etc.)– Financial (interest rates, FX, and equities)– Commodities (oil, gasoline, and metals)

Differences between Forwards and Futures

• Features reducing credit risk– Daily settlement or mark-

to-market

– Margin account

– Clearinghouse

• Features promoting liquidity– Contract standardization

– Traded on organized exchanges

Daily Settlement

• Recall that forward contracts have no settlement until maturity

• Futures contracts settle every day– Like a series of one day forward contracts

• At end of trading day, any contract value must be paid– Contract is “marked-to-market”

• Risk is reduced to daily price movement

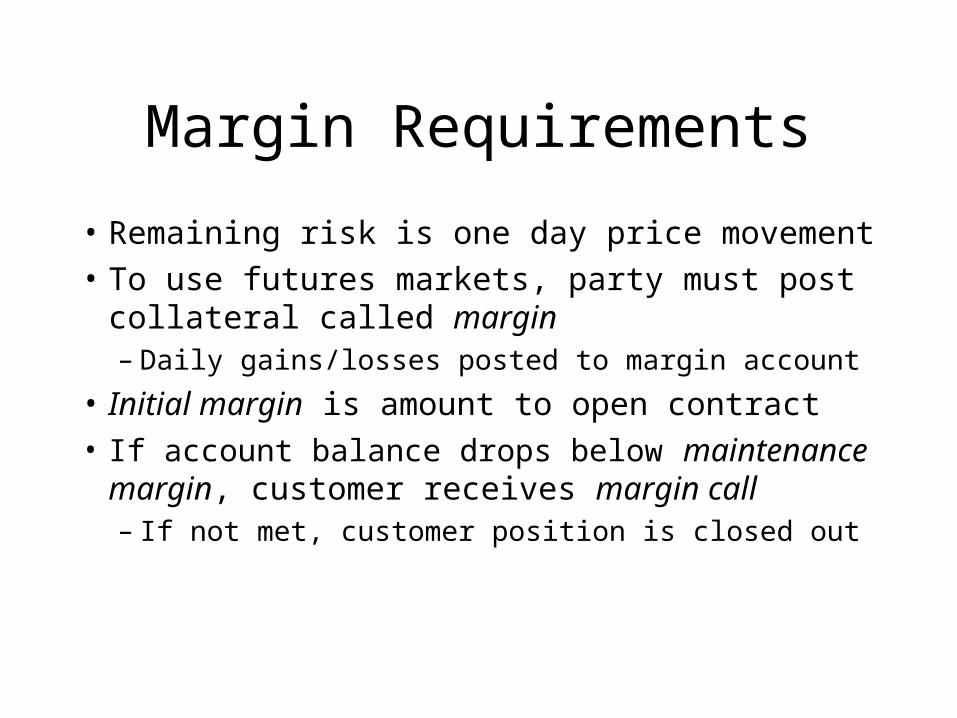

Margin Requirements

• Remaining risk is one day price movement

• To use futures markets, party must post collateral called margin– Daily gains/losses posted to margin account

• Initial margin is amount to open contract• If account balance drops below maintenance

margin, customer receives margin call– If not met, customer position is closed out

Margin Account Example

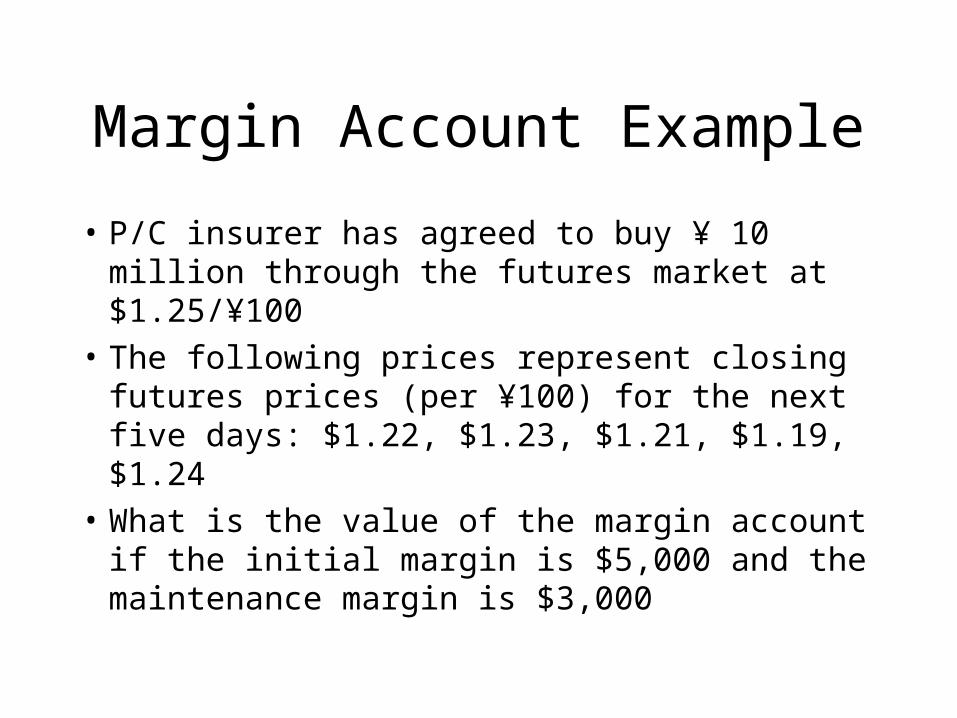

• P/C insurer has agreed to buy ¥ 10 million through the futures market at $1.25/¥100

• The following prices represent closing futures prices (per ¥100) for the next five days: $1.22, $1.23, $1.21, $1.19, $1.24

• What is the value of the margin account if the initial margin is $5,000 and the maintenance margin is $3,000

Margin Account Example Solution

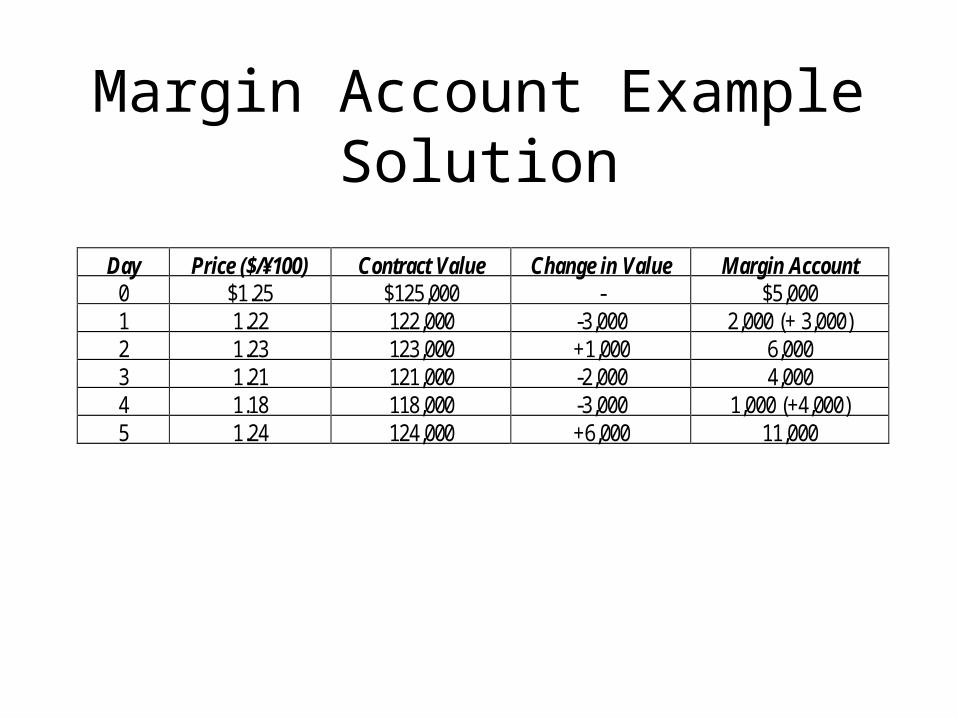

Day Price ($/¥100) Contract Value Change in Value Margin Account0 $1.25 $125,000 - $5,0001 1.22 122,000 -3,000 2,000 (+ 3,000)2 1.23 123,000 +1,000 6,0003 1.21 121,000 -2,000 4,0004 1.18 118,000 -3,000 1,000 (+4,000)5 1.24 124,000 +6,000 11,000

Clearinghouse

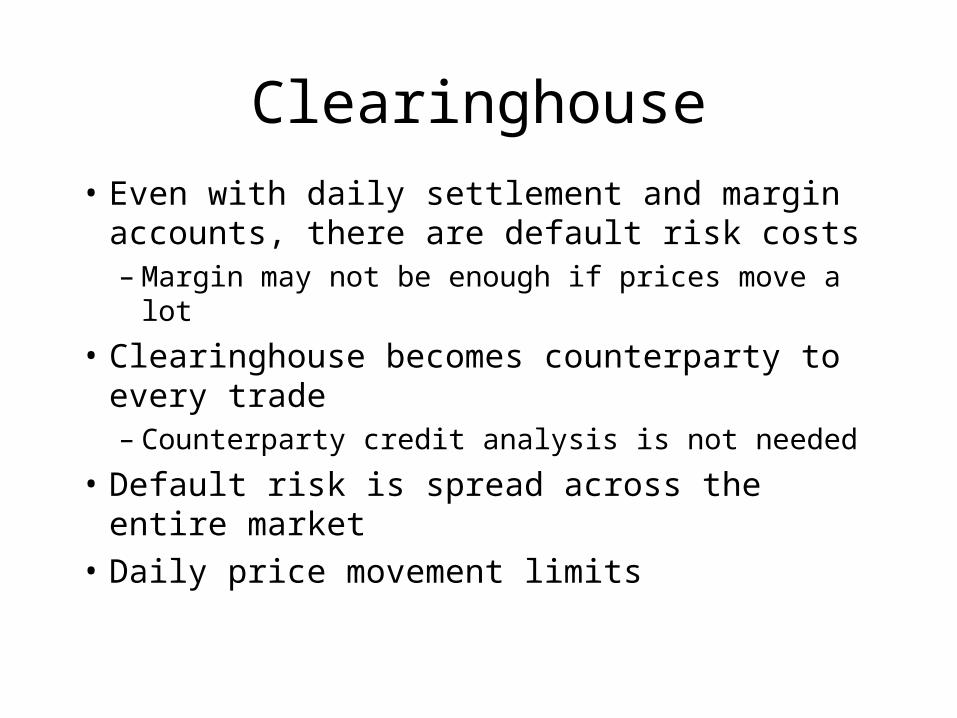

• Even with daily settlement and margin accounts, there are default risk costs– Margin may not be enough if prices move a lot

• Clearinghouse becomes counterparty to every trade– Counterparty credit analysis is not needed

• Default risk is spread across the entire market

• Daily price movement limits

Liquidity Enhancements of Futures Contracts

• Forward contracts are negotiated by contracting parties

• Futures are standardized contracts– Asset type, quantity, maturity

• Futures are traded on organized exchanges

Interest Rate Futures Contracts

• Most popular contracts divided by the type of interest rate exposure

• Short term interest futures– Treasury Bill (T-bill)– Eurodollar CD (or just Eurodollar futures)

• Intermediate or long term interest futures– Treasury bond or note (T-bond or T-note)– Municipal index

T-bill Futures

• At maturity, short position must deliver $1 million of T-bills with 13 weeks to maturity– Either a new issue or an existing issue

• Essentially, a T-bill future can be used to hedge the future interest rate

• 90 or 91 day forward rate beginning at the maturity date of the futures contract

• Smallest change (one tick) in value is $25

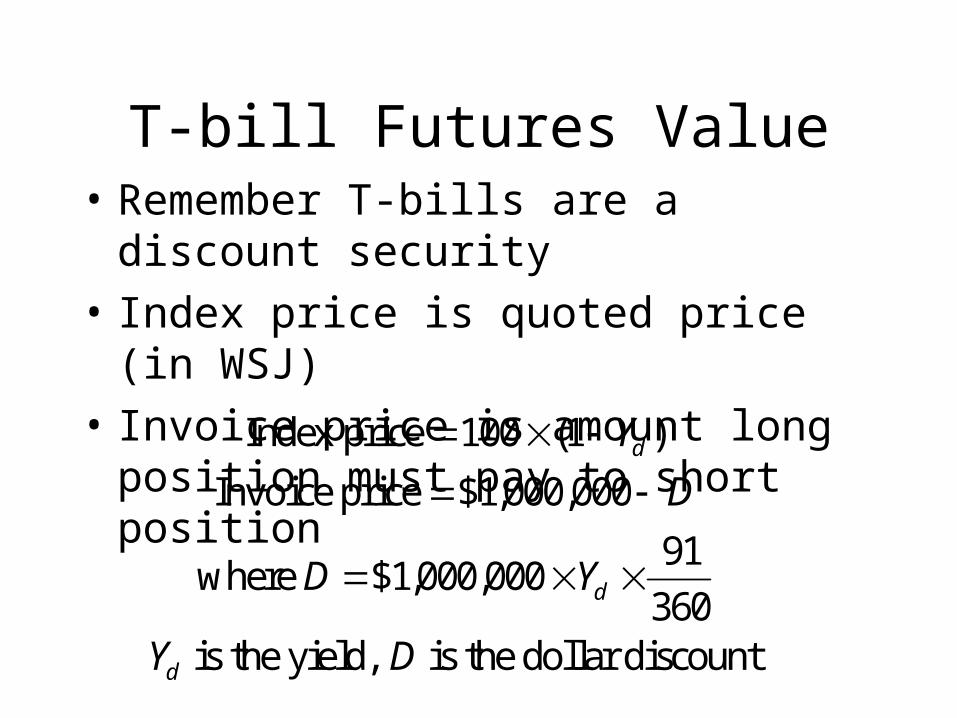

T-bill Futures Value• Remember T-bills are a discount security

• Index price is quoted price (in WSJ)

• Invoice price is amount long position must pay to short position

Index price

Invoice price

where

is the yield, is the dollar discount

100 1

000 000

000 00091

360

( )

$1, ,

$1, ,

Y

D

D Y

Y D

d

d

d

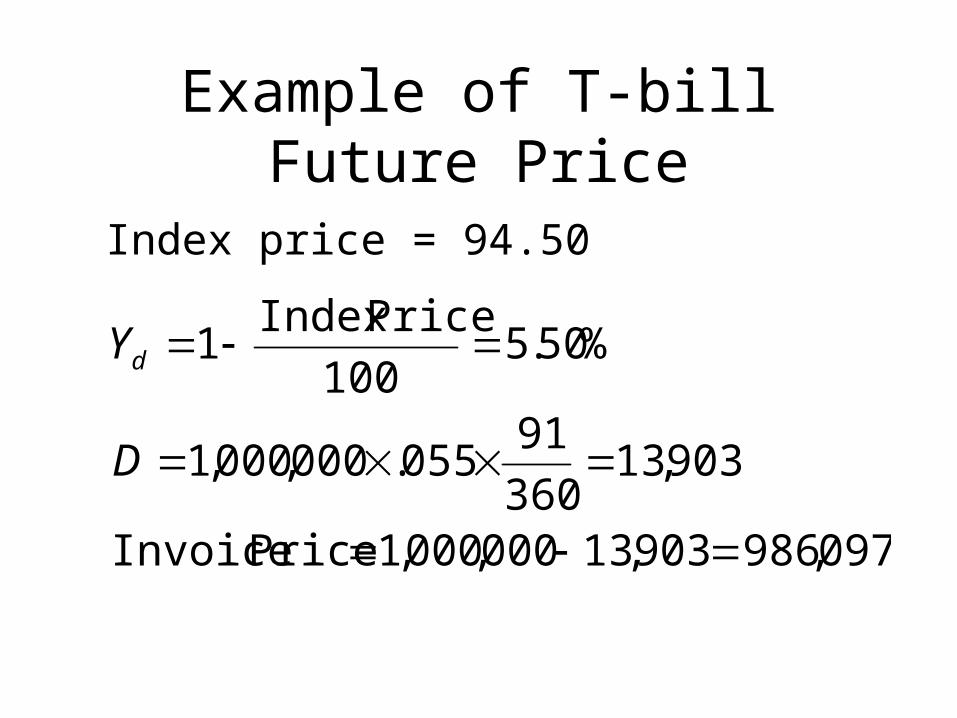

Example of T-bill Future Price

Index price = 94.50

097,986903,13000,000,1 Price Invoice

903,13360

91055.000,000,1

%50.5100

PriceIndex 1

D

Yd

Eurodollar Futures

• Underlying rate is 90-day future LIBOR– London InterBank Offered Rate– Has some credit risk

• Cash settled (no delivery of some financial instrument)

• Most heavily traded futures contract in the world

• Used to hedge future interest rates

T-bond Futures

• Underlying instrument is hypothetical bond with $100,000 face value and 8% coupon

• Seller has option to deliver a number of bonds at maturity

• Settlement value is adjusted based on actual bond delivered

• Seller will evaluate which bond is cheapest to deliver

Before Pricing Futures Contracts: A side comment

• Pricing of derivatives usually uses arbitrage arguments

• Arbitrage is present if:– A zero net investment can generate a non-zero

cash flow (cash flow must have no uncertainty)– The return of a cash investment exceeds the

risk-free rate, assuming there is no uncertainty in the return

Futures Prices

• At maturity, the spot price and futures price must be equal– If not, an arbitrage opportunity exists (Why?)

• Before maturity, the spot price and futures price need not be equal due to cost of carry

• Cost of carry reflects the benefit or cost of holding the asset vs. the benefit or cost of using the futures market

Cost of Carry

• Holding the asset– We must pay storage and insurance costs

• Using futures– We earn interest on our money until maturity

• For commodities: Ft(1+rf)<P0+c, where c is the storage and insurance costs

• If inequality goes is reversed, sell the future and buy the asset in the spot market

Valuation of Interest Rate Futures

• There should be no benefit from using cash market or futures market– Compare outlays at maturity

• Tradeoff: Buy now (P) or later (F)– Lose interest on spot price P for t years– Earn coupon before futures maturity

F r t P P c t P

F P t r c

or

[ ( )]1

Forwards Prices vs. Futures Prices• Margin payments are difference in value

– We have ignored these cash flows

• If interest rates increase, bond values decrease and short futures position has gain– Margin received earns higher interest rate

– If rates decline, margin payments can be financed at lower interest

• Short futures position is better than forward position in both cases– Opposite is true for long position

Futures Price Behavior

• Expectations model says that the futures price is the expected future spot price– Expected profit on futures is zero

• Futures price will only increase with the risk-free rate

• For financial futures, expectations model is equilibrium price

Normal Backwardation

• Net long spot positions– e.g., farmers want to hedge

future price risk

• They are willing to sell futures at prices below the expected future spot price to entice investors

• Long futures position receives a positive return

Normal Backwardation

Time

Fut

ures

Pri

ce

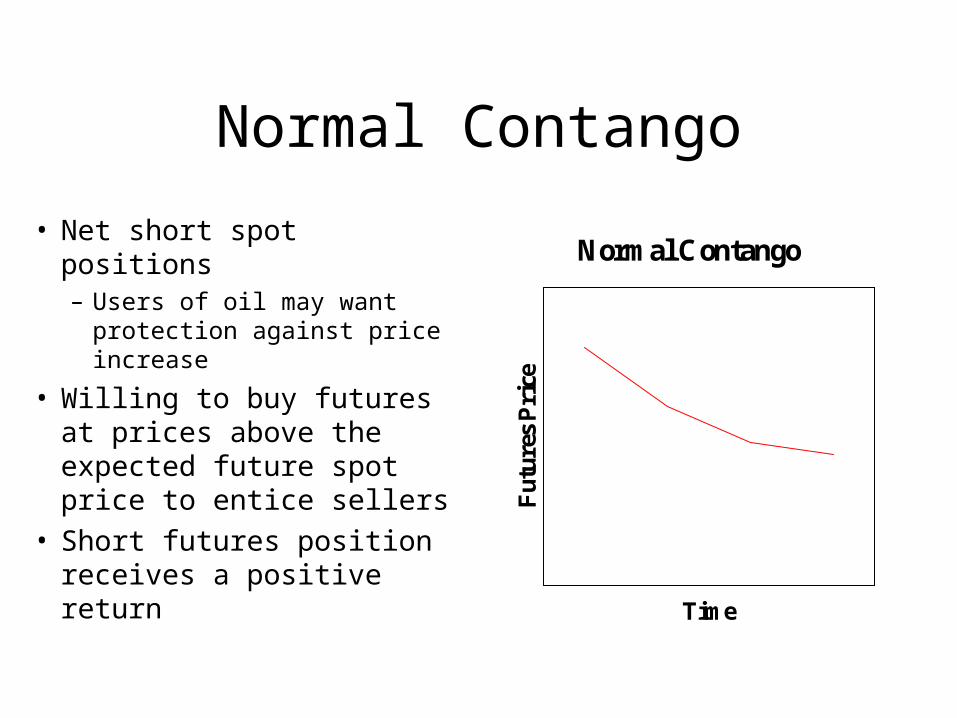

Normal Contango

• Net short spot positions– Users of oil may want

protection against price increase

• Willing to buy futures at prices above the expected future spot price to entice sellers

• Short futures position receives a positive return

Normal Contango

Time

Fut

ures

Pri

ce

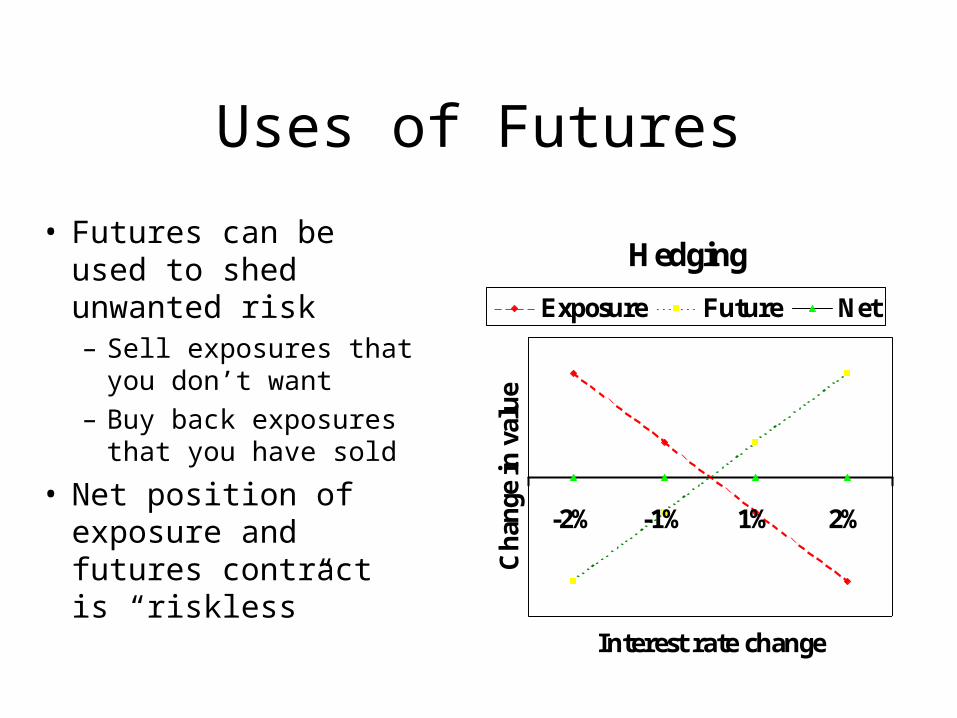

Uses of Futures

• Futures can be used to shed unwanted risk– Sell exposures that you

don’t want

– Buy back exposures that you have sold

• Net position of exposure and futures contract is “riskless”

Hedging

-2% -1% 1% 2%

Interest rate change

Ch

ange

in

val

ue

Exposure Future Net

Determining the Required Hedge• Hedging is only “riskless” if underlying

futures asset corresponds to exposure

• Typically, futures contracts do not exist for every type of exposure

• Decisions must be made– Which futures contract is best?– Which maturity is appropriate?– How many contracts to buy/sell?

Basis• Basis is difference between spot price and futures price: F

- P– Risk exposure becomes change in basis– If held to maturity, basis risk is zero

• Factors affecting the basis– Futures price and spot prices converge– Cost of carry may change (e.g., interest rates) – If cross-hedging, spot price and futures price may not move

together perfectly– Some other random and unpredictable factor

Maturity Mismatches

• Multiple exposures in the future

• Strip hedge uses x contracts with maturity t1, y contracts with maturity t2, etc.

• Rolling hedge aggregates all future exposure and uses only short-term contracts– Longer term contracts have less liquidity– At first exposure date, unwind position and use short term

contracts again until next exposure– Assumes all contracts move together regardless of maturity

Selecting the Best Futures Contract

• Frequently, there is no futures contract that matches the hedger’s exposure exactly

• We want to determine the best cross-hedge

• Use the most closely correlated future– Regress exposure against available futures contracts

• Determine the appropriate number of contracts– Futures contract value may be more volatile than

hedge required

Example• A life insurer needs to lock in the one month

interest rate, 6 months from now• There is no futures contract which is based on the

one-month rate– T-bills, Eurodollar futures are 3-month rates

• The insurer regresses its exposure and finds that 50% of its exposure is explained by the 6-month Eurodollar futures contract

• Insurer needs only a 16% hedge (Why?)

Next time...

• Swap contracts

• What are interest rate swaps?

• What other kinds of swaps exist?

• Why would someone use a swap?

![SolMcL 6e ch10 [唯讀] week...Futures Contract Futures contracts are traded on an organized futures exchange. Futures contracts are standardized in terms of size and maturity. There](https://img.pdfslide.us/doc/110x75/5e755f8a76c40b3c45782924/solmcl-6e-ch10-e-week-futures-contract-futures-contracts-are-traded-on.jpg)