Embed Size (px)

Citation preview

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd [2016] AICmr 88 (9 December 2016) Decision and reasons for decision of Australian Privacy Commissioner, Timothy Pilgrim

Complainants: Financial Rights Legal Centre Inc

Consumer Action Law Centre

Financial Counselling Australia

Australian Privacy Foundation

Respondent: Veda Advantage Information Services and Solutions Ltd

Decision date: 9 December 2016

Application number: CP14/03515, CP14/04469, CP14/04470

Catchwords: Privacy — Privacy Act 1988 — Part IIIA — Privacy (Credit Reporting)

Code 2014 (Version 1.2) — APP 7

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 2

Contents

Determination ................................................................................................................ 4

Background .................................................................................................................... 4

The Veda Group .............................................................................................................. 5

The Law .......................................................................................................................... 5

Terminology ................................................................................................................... 8

The complaints ............................................................................................................... 9

Representative complaints ............................................................................................10

First representative complaint .......................................................................................11

Second representative complaint ...................................................................................11

Third representative complaint ......................................................................................13

Investigation process .....................................................................................................14

The first complaint .........................................................................................................14

Veda’s websites .............................................................................................................14

The prominence issue ....................................................................................................17

Findings in relation to prominence issue ........................................................................18

The online access issue ..................................................................................................23

Findings in relation to online access issue ......................................................................25

The phone access issue ..................................................................................................39

Findings in relation to the phone access issue ................................................................41

The onerous identification issue ....................................................................................43

Findings in relation to the onerous identification claim ..................................................45

The second complaint ....................................................................................................46

The timing issue .............................................................................................................46

Findings in relation to timing issue .................................................................................47

The direct marketing issue .............................................................................................47

Findings in relation to the tick box 1 ...............................................................................51

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 3

Findings in relation to tick box 2.....................................................................................55

The third complaint .......................................................................................................56

The 12-month issue .......................................................................................................56

Findings in relation to 12-month issue ............................................................................58

Expedited delivery .........................................................................................................60

The excessive charge issue .............................................................................................61

Findings in relation to excessive charges issue ................................................................62

The VedaScore issue ......................................................................................................64

Findings in relation to the VedaScore claim ....................................................................67

Declarations ..................................................................................................................70

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 4

Determination 1. Veda Advantage Information Services and Solutions Ltd (Veda) interfered with the privacy of the class of

individuals identified as ‘members of the public seeking to access a free copy of their credit report from

Veda Advantage’ in breach of the Privacy Act 1988 (Cth) (Privacy Act) by:

I. failing to prominently state that individuals have a right to obtain their credit reporting information

free of charge in certain circumstances, in contravention of paragraph 19.3(a) of the Privacy (Credit

Reporting) Code 2014 (version 1.2) (CR code)

II. failing to take reasonable steps to ensure that free access to credit reports was as available and as

easy to identify and access as paid access to credit reports, in contravention of paragraph 19.3(b) of

the CR code

III. using and disclosing personal information it held about individuals seeking free access to credit

reports for the purpose of direct marketing in breach of Australian Privacy Principle (APP) 7

IV. charging for the ‘expedited delivery’ of a credit report in breach of s 20R(5), in circumstances where

the individual (or access seeker) had not sought access to credit reporting information within the

preceding 12-month period.

Background

2. This determination relates to three representative complaints (the complaints) made under Part V of the

Privacy Act. The complaints are made jointly by consumer advocacy groups, Financial Rights Legal Centre

Incorporated, the Consumer Action Law Centre, Financial Counselling Australia and the Australian Privacy

Foundation (complainants) on behalf of a class of individuals identified as ‘members of the public seeking

to access a free copy of their credit report from Veda Advantage’ (class members, hereafter also referred

to as access seekers). The respondent to the complaint is Veda Advantage Information Services and

Solutions Limited (Veda).

3. It is complained that a number of Veda’s acts and practices relating to the provision of credit reporting

information (CRI), are in breach of the Privacy Act and the CR code.

4. Specifically, the complaints relate to alleged breaches of:

(a) section 20R of the Privacy Act (access to credit reporting information)

(b) APP 7 (direct marketing) under the Privacy Act; and

(c) paragraphs 19.3 and 19.4 of the CR code (access).

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 5

The Veda Group

5. The Veda Group Limited is an information services and aggregation business. It comprises a number of

separate companies, including the respondent in this matter, Veda Advantage Information Services and

Solutions Limited, which operates a credit reporting business. The respondent is a ‘credit reporting body’

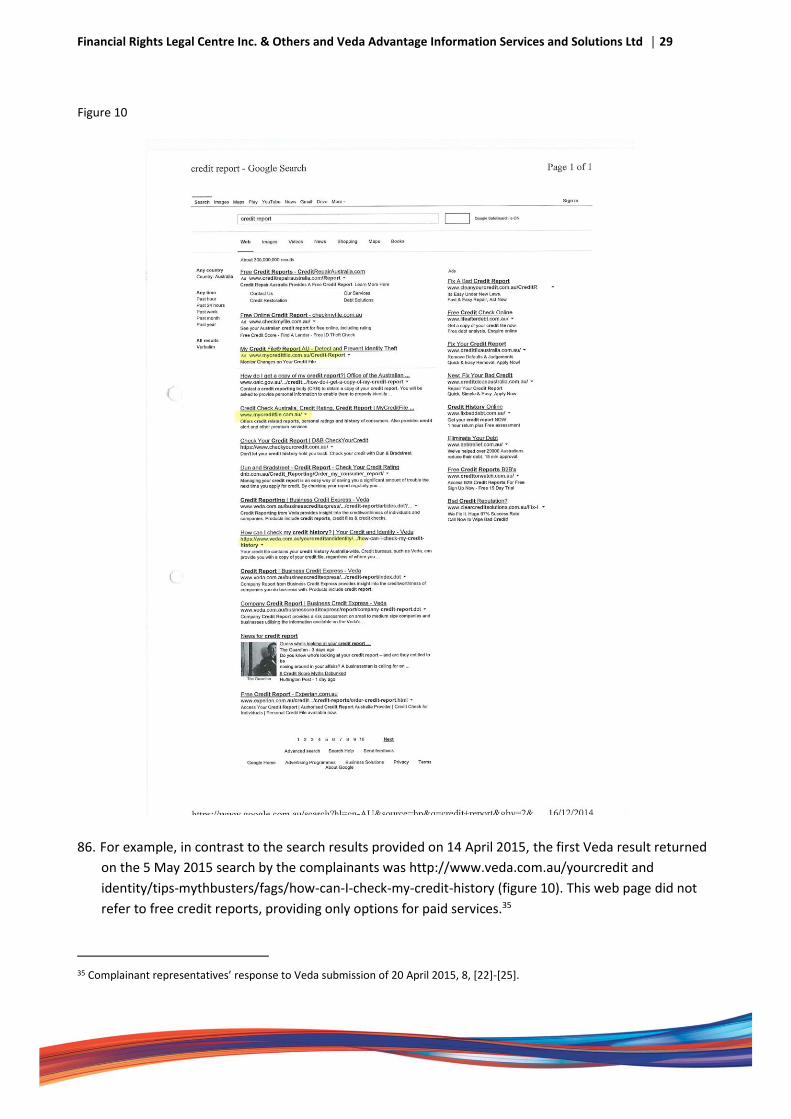

under the Privacy Act1, and is the major credit reporting body in Australia. According to its website, Veda

is a ‘data analytics company and the leading provider of credit information and analysis in Australia and

New Zealand’.2

6. Veda collects, holds, uses and discloses information about individuals and corporations for the purpose of

providing information about the creditworthiness of an individual or corporation. It holds data on more

than 16.4 million individuals and 3.6 million companies and businesses.3 In February 2016, the Veda

Group Limited was acquired by Equifax Incorporated, a leading consumer credit reporting agency in the

United States and ‘a global leader in consumer, commercial and workforce information solutions’.4

The Law

7. The credit reporting provisions in Part IIIA of the Privacy Act govern the handling of information held by

credit reporting bodies (CRBs) and credit providers (CPs) relating to credit reporting.

8. Section 20R of the Privacy Act deals with access to credit reporting information. It relevantly states:

Access

(1) If a credit reporting body holds credit reporting information about an individual, the body must, on request by an access seeker in relation to the information, give the access seeker access to the information.

and

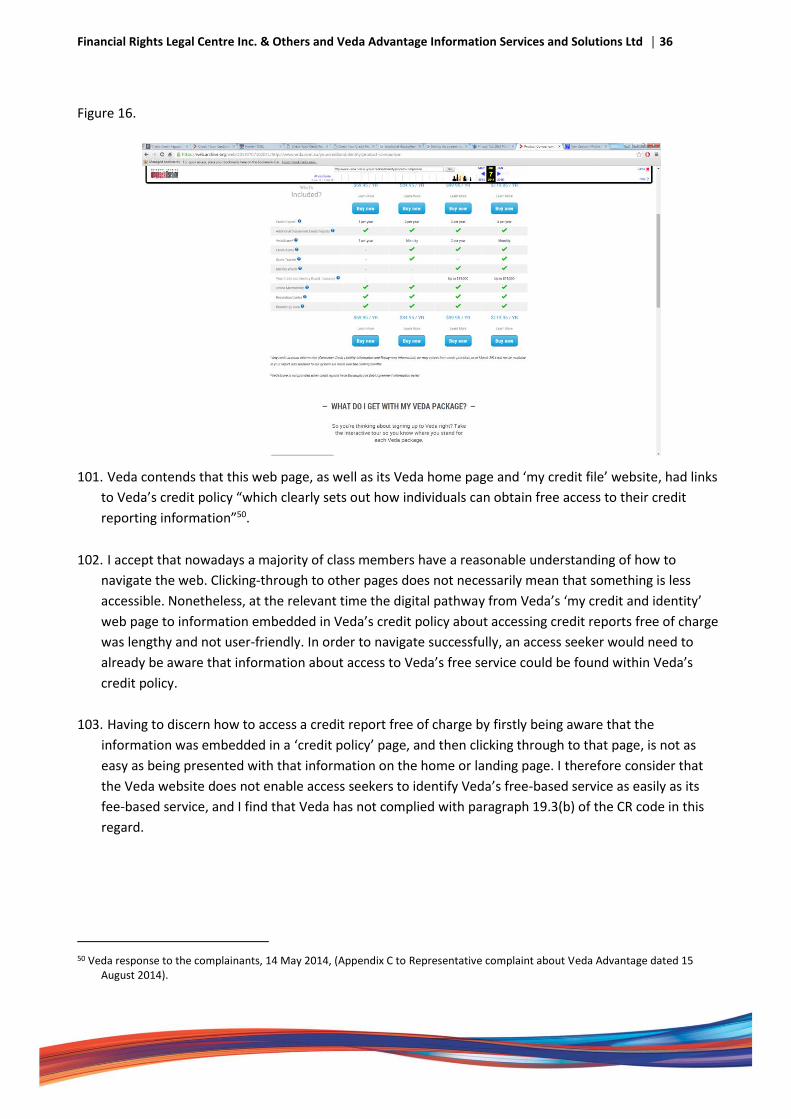

Dealing with requests for access

(3) The credit reporting body must respond to the request within a reasonable period, but not longer than 10 days, after the request is made.

(4) If the credit reporting body gives access to the credit reporting information, the access must be given in the manner set out in the registered CR code.

1 Under s 6(1) of the Privacy Act 1988 (Cth), credit reporting body is defined to mean: (a) an organisation, or (b) an agency

prescribed by the regulations; that carries on a credit reporting business.

2 https://www.veda.com.au/about-us. Accessed 10 August 2016.

3 https://www.veda.com.au/business. Accessed 10 August 2016.

4 https://www.veda.com.au/insights/equifax-completes-acquisition-australias-leading-credit-information-company-veda-group. Accessed 10 August 2016.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 6

Access charges

(5) If a request under subsection (1) in relation to the individual has not been made to the credit reporting body in the previous 12 months, the body must not charge the access seeker for the making of the request or for giving access to the information.

(6) If subsection (5) does not apply, any charge by the credit reporting body for giving access to the information must not be excessive and must not apply to the making of the request.

9. APP 7 deals with direct marketing. It states:

7.1 If an organisation holds personal information about an individual, the organisation must not use or disclose the information for the purpose of direct marketing.

The relevant exceptions to this is set out in APP 7.3:

7.3 Despite subclause 7.1, an organisation may use or disclose personal information (other than sensitive information) about an individual for the purpose of direct marketing if:

(a) the organisation collected the information from:

(i) the individual and the individual would not reasonably expect the organisation to use or disclose the information for that purpose; or

(ii) someone other than the individual; and

(b) either:

(i) the individual has consented to the use or disclosure of the information for that purpose; or

(ii) it is impracticable to obtain that consent; and

(c) the organisation provides a simple means by which the individual may easily request not to receive direct marketing communications from the organisation; and

(d) in each direct marketing communication with the individual:

(i) the organisation includes a prominent statement that the individual may make such a request; or

(ii) the organisation otherwise draws the individual’s attention to the fact that the individual may make such a request; and

(e) the individual has not made such a request to the organisation.

10. The CR code is a written code of practice about credit reporting under s 26N(1) of the Privacy Act. Under

s 26L of the Privacy Act, if an entity is bound by the registered CR code it must not do an act or engage in

a practice that breaches the code.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 7

11. The CR code adds to aspects of the credit reporting obligations imposed by Part IIIA, relevantly here,

obligations relating to access:

19. Access

19.3 If a CRB has a service whereby an individual (whether personally or through another access seeker) may

for a fee obtain their credit reporting information (fee-based service):

a. the information made available by the CRB about the fee-based service must prominently state that individuals have a right under Part IIIA to obtain their credit reporting information free of charge in the following circumstances:

i. if the access request relates to a CP's decision to refuse the individual's consumer credit application;

ii. if the access request relates to a decision by a CRB or CP to correct credit reporting information or credit eligibility information about the individual; and

iii. once every 12 months (this is in addition to any access given in accordance with

paragraphs 19.3(i) or (ii))

b. the CRB must take reasonable steps to ensure that its service, whereby individuals may obtain their credit reporting information free of charge, is as available and easy to identify and access as its fee-based service.

Source Notes: Sec 20R, 21T

19.4 Where credit reporting information is provided to an access seeker free of charge by a CRB as required

by Part IIIA, the Regulations or this CR code:

a. the CRB must provide the access seeker with access to:

i. all credit information in relation to the individual currently held in the databases that the CRB utilises for the purposes of making disclosures permitted under Part IIIA; and

ii. all current CRB derived information about the individual that is available;

b. the CRB must present the information clearly and accessibly and provide reasonable explanation and summaries of the information to assist the access seeker to understand the impact of the information on the individual's credit worthiness; and

c. if the CRB does not provide the information to the access seeker in the manner requested by the access seeker, the CRB must take reasonable steps to provide access in a way that meets the needs of the CRB and the individual.

Source Notes: Sec 20R, Explanatory Memorandum p.178

12. Section 13 of the Privacy Act provides that an act or practice of an entity is an interference with the

privacy of an individual if:

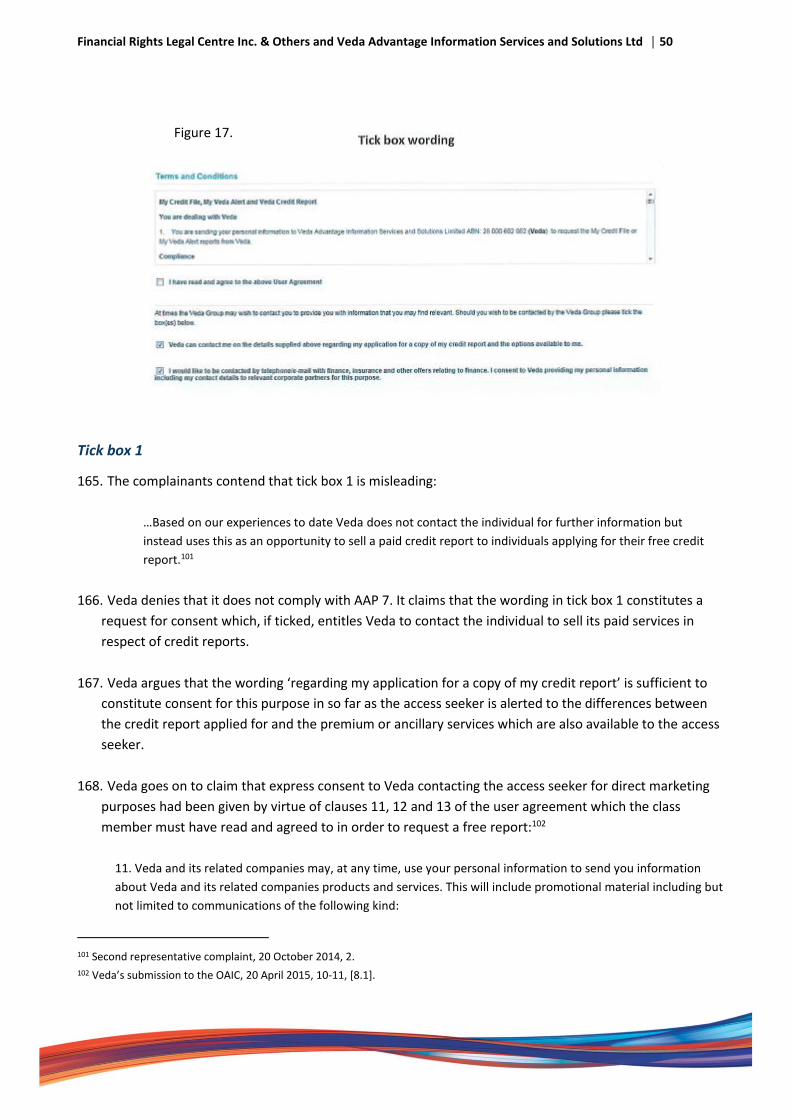

(a) the act or practice breaches a provision of Part IIIA in relation to personal information about the individual; or

(b) the act or practice breaches the registered CR code in relation to the personal information about the individual and the code that binds the entity.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 8

Terminology

13. The term ‘credit report’ which I refer to on various occasions in this determination and which appears

numerous times in correspondence from the complainants and Veda, is not a term used in the Privacy

Act or the CR code.

14. The appropriate term for an individual’s credit report is ‘credit reporting information’, which is defined

in s 6 of the Act to be: ‘... credit information, or CRB derived information, about the individual’.5

15. Credit information is defined in the Privacy Act at s 6N. There is no need to replicate the full definition

here, suffice to say that it is personal information about an individual (other than sensitive information)

that is, relevantly:

……..

(b) consumer credit liability information about the individual; or

(c) repayment history information about the individual; or

…….

(e) the type of consumer credit or commercial credit, and the amount of credit sought in an application;

i. that has been made by the individual to a credit provider; and

ii. in connection with which the provider has made an information request in relation to the individual; or

(f) default information about the individual; or

(g) payment information about the individual; or

……

16. Under subsection 6(1) of the Privacy Act, CRB derived information means any personal information

(other than sensitive information):

a. that is derived by a credit reporting body from credit information about the individual that is held by the

body; and

b. that has any bearing on the individual’s credit worthiness; and

c. that is used, has been used or could be used in establishing the individual’s eligibility for consumer

credit.

17. Personal information is defined in section 6(1) of the Privacy Act to mean information or an opinion

about an identified individual, or an individual who is reasonably identifiable:

a. whether the information or opinion is true or not; and

b. whether the information or opinion is recorded in a material form or not.

5 Privacy Act 1988 (Cth), s 6(1).

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 9

18. Over the years the provision of credit information to individuals by CRBs has generally been coined as

access to your ‘credit file’ or ‘credit report’. For convenience and comprehensiveness, I have used the

term ’credit report’ interchangeably with ‘credit reporting information’. Accordingly, where I have used

the term ‘credit report’ in the context of access to credit reporting information, I am referring to a

report provided to an individual by a CRB that includes all credit information about the individual and all

CRB derived information about the individual held by the CRB at the time of the request.

The complaints

19. The first complaint lodged on 15 August 2014 alleges that in contravention of section 19.3 of the CR

code:

(a) Veda has failed to prominently state that individuals have a right to obtain their credit reporting

information free of charge in certain circumstances (the prominence issue); and

(b) Veda has not taken reasonable steps to ensure that free access to credit reports online is as

available and as easy to identify and access as paid access to credit reports (the online access

issue); and

(c) individuals are not able to obtain a free credit report from Veda over the phone, but credit

reports issued via a fee-based service are available over the phone (the phone access issue); and

(d) Veda’s identification requirements to obtain a free credit report are more onerous than those for

credit reports issued via a fee-based service (the onerous identification issue).

20. The second complaint was lodged 20 October 2014 subsequent to Veda making free credit reports

available online on the Veda website by completing a form. The complainants allege that:

free credit reports are not being provided by Veda within the 10 day requirement under s 20R(3)

of the Act (the timing issue); and

tick boxes on Veda’s online application form for a free credit report lead to the marketing of

Veda’s fee-based services, in breach of APP 7 (the direct marketing issue). 6

21. The third complaint lodged on 20 October 2014 alleges that:

6 In their complaint dated 20 October 2014, the complainants identified as an issue the inconsistencies between free credit report

information on Veda’s ‘my credit file’ website, and the actual process of applying online for free credit report. In its submission dated 20 April 2005, Veda declared that the information on the ‘my credit file’ website had been corrected. The complainants confirmed this in their response to Veda’s submission. I understand that the claim regarding the discrepancy is no longer in issue, having been adequately dealt with.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 10

Veda is charging for access even when an individual has not requested a credit report within the

previous 12 months in contravention of s 20R(5) of the Privacy Act (the 12-month issue)

Veda is charging for the ‘expedited delivery’ of a credit report, in breach of s 20R(5), in

circumstances where the access seeker had not sought access to credit reporting information

within the preceding 12-month period (expedited delivery issue); and

the cost of a Veda credit report issued through its fee-based service is excessive, in contravention

of s 20R(6) of the Privacy Act (the charge issue) ; and

Veda does not include the individual’s VedaScore information in a free credit report, in

contravention of s 19.3(b) and 19.4(a) of the CR code (the VedaScore issue).

Representative complaints

22. The complaints have been made under s 36 of the Privacy Act, which provides for the making of

representative complaints. Additionally a representative complaint must meet the requirements of s 38

of the Privacy Act.7

23. Section 38(1) states that a representative complaint may be lodged under s 36 of the Privacy Act only if:

(a) the class members have complaints against the same person; and

(b) all the complaints are in respect of, or arise out of, the same, similar or related circumstances; and

(c) all the complaints give rise to a substantial common issue of law or fact.

24. Section 38(2) sets out further conditions for a representative complaint to be made. Specifically, it states that the representative complaint must:

(a) describe or otherwise identify the class members; and

(b) specify the nature of the complaints made on behalf of the class members

(c) specify the nature of the relief sought; and

(d) specify the questions of law or fact that are common to the complaints of the class members.

7 Section 36(2A) of the Privacy Act states that in the case of a representative complaint, s 36 has effect subject to s 38.

8 Veda’s submission to the OAIC, 20 April 2015.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 11

25. Veda has raised objections to the complaints being treated as representative complaints because, Veda

argues, the complaints have been made by the aforementioned consumer advocacy groups on behalf of

individuals who have complained to them about acts or practices that may be an interference with their

privacy.8

26. A person on behalf of an individual or individuals, as well as individuals themselves, can make a

complaint under s 36 of the Privacy Act. I am satisfied that the complaints received were validly made

under s 36. In respect of whether or not the complaints meet the requirements under s 38 of the Privacy

Act for representative complaints, I will consider each complaint in turn.

First representative complaint

27. I am satisfied that in respect to the first complaint, the requirements for making a representative

complaint under s 38 have been met. Though this complaint deals with a wide range of issues, I am

satisfied that the claims made are connected by circumstances sufficiently related to warrant their

grouping as a representative complaint. All class members are affected in common by Veda’s practices

surrounding its services to provide access to credit reporting information free-of-charge. The

complainants allege inequities between accessing credit reporting information free-of-charge and

accessing this information through Veda’s fee-based service. This raises questions as to whether these

practices are in contravention of s 19.3 of the CR code.

28. The complainants on behalf of all class members seek a declaration that Veda must take action to ensure

that its provision of free-of-charge access to credit reporting information is as available, and as easy to

identify and access as its fee-based services.

Second representative complaint

29. The second complaint made on 20 October 2014 similarly includes a varying range of issues, this time

relating to the use of Veda’s online application form to lodge a request for a free credit report.

30. One of the issues raised with this second complaint is the claim that class members were not receiving

free-of-charge access to their credit reporting information within the 10-day period mandated by s 20(3)

of the Privacy Act (the timing issue).

31. Veda objects to the timing issue being included within the scope of the second complaint because the

complainants have based its inclusion on a single instance of a credit report not being received within 10

days.8 Veda submits that the timing issue should be treated as a separate complaint by the concerned

individual under s 36(1) of the Privacy Act.9

8 Veda’s submission to the OAIC, 20 April 2015, 8-9, [6.1]-[6.2].

9 Veda’s submission to the OAIC, 20 April 2015,9, [6.6].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 12

32. The complainants have confirmed the inclusion of this issue within the second complaint was based on a

single instance of a credit report being provided outside the 10-day requirement. The complainants

argue that it is reasonable to assume there may have been other instances where the statutory

timeframe has not been met.10

33. Under s 38, I must be satisfied that all the complaints are in respect of, or arise out of, the same, similar

or related circumstances, and all the complaints give rise to a substantial common issue of law or fact.

34. Veda points out there is nothing in the complaint that establishes:

that there are any class members with complaints against Veda in respect of, or arising out of, the

same or similar or related circumstances as the timing issue; or

that there are any complaints by class members that give rise to a substantial common issue of

law or fact as the timing issue.11

35. I disagree. Firstly, I note that the Privacy Act has a remedial purpose, and the purpose of representative

procedures is to reduce the need for multiple complaints. I further note that all the complaints by class

members under this representative complaint arise out of attempts to lodge an online application form

on Veda’s website to access credit reporting information free-of-charge. Class members are therefore

affected by a common circumstance. Veda is alleged in this complaint of having an online process in

place that disadvantages class members who are applying online for a free credit report over those

customers who apply online for their credit reporting information through one of Veda’s paid services.

There is a substantial common issue of fact: do impediments in fact exist for class members applying

online for a free credit report that don’t exist for those customers who pay a fee to access the online

service?

36. The fact that both the class member who is complaining of receiving their free credit report out-of-time

after lodging an application for one online, and the class member who is complaining of having to tick

boxes during the online application process that allegedly results in direct marketing activity, are having

difficulties with Veda’s free credit report online access service is, in my view, enough to constitute a

common issue of fact. The differences in the circumstances do not in my opinion prevent them from

being included in a representative complaint.

37. I am therefore satisfied that in respect of the second complaint, the requirements for the making of a

representative complaint under s 38 have been met.

10 Complainants’ submission in reply to the OAIC, 15 June 2015, 13, [46].

11 Veda’s submission to the OAIC, 20 April 2015, 9, [6.4].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 13

38. In relation to representative complaint two, the complainants on behalf of all class members seek a

declaration that Veda must take action to ensure that:

I. Veda has systems in place that prevent delays in providing requested free credit reports

II. Veda collects and maintains records for the monitoring of its compliance with s 20R of the

Privacy Act; and

III. a request for a free credit report is not used as a direct marketing opportunity in

contravention of APP 7.

Third representative complaint

39. In the third representative complaint, class members are allegedly affected by the practices of Veda in

relation to credit report charges:

paying for access to credit reporting information that should otherwise be free-of-charge

paying an excessive charge for credit reporting information

receiving less credit reporting information in Veda’s free credit report compared to the

information provided with a paid report.

40. The remedy sought by the complainants is a declaration by the Commissioner that:

I. Veda’s charge in relation to credit reporting information is excessive

II. that Veda provide its actual costs relating to the issuing of credit reporting information, and the

$79.95 amount charged by Veda be reduced to that amount; and

III. VedaScore information be provided in the free credit report.

41. In this third representative complaint, the circumstances of class members are tied by a common

integer; that is, the entitlement to credit reporting information free of charge and what comprises that

entitlement. I am satisfied that the issues outlined in this third complaint are sufficiently related to

warrant dealing with this as a representative complaint for the determination of the common issue so

defined. In respect of this third complaint, the requirements for the making of a representative

complaint have been met.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 14

Investigation process

42. The investigation of these representative complaints involved the following steps:

11 November 2014 — correspondence to Veda regarding the opening of an investigation

under s 40(1) of the Act

11 March 2015 — correspondence to Veda initiating the s 52 determination process

20 April 2015 — Veda’s initial submissions received

21 April 2015 — Veda’s initial submissions provided to the complainants

15 June 2015 — the complainant’s submissions received

30 March 2016 — OAIC representatives make an onsite visit to Veda’s premises to observe

firsthand how certain processes occur.

The first complaint

Veda’s websites

43. Veda maintains two websites, available at the domain names <www.veda.com.au> (the Veda website)

and <www.mycreditfile.com.au> (my credit file website).

44. Customers looking to obtain copies of their Veda credit reports can do so through the Veda website by

clicking on the ‘Get Your Credit Report’ button. This button re-directs users to the my credit file website.

45. At the relevant time12 the my credit file website detailed a caption beneath its ‘My Veda Alert’ heading,

which read as follows (figure 1):

‘My Veda Alert - Get your credit report to help ensure your credit history is accurate and up to date. Your credit file

will be despatched in one working day. You also receive email alerts whenever specific changes occur on your credit

file for 12 months. Buy Now $79.95’13

12 For the purposes of this determination, I shall accept as the time of the alleged breach, the date of the initial complaint on 15

August 2014 or thereabouts.

13 Initial representative complaint about Veda Advantage to the OAIC, 15 August 2014, 3.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 15

Figure 1 — Veda’s my credit file homepage

46. The complainants allege that a class member must scroll down the web page through a list of fee-for-

service options before being alerted by a button with the words ‘Free file, Find out more’ that they may

be able to access a free copy of their credit report (figure 2).

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 16

Figure 2 — first appearance of the option to get a free credit report

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 17

The prominence issue

47. Under paragraph 19.3(a) of the CR code, information made available by the CRB about the fee-based

service must prominently state that access seekers have a right to obtain, on request, their credit

reporting information free of charge in certain circumstances including once every 12 months.

48. The complainants argue that information made available on Veda’s websites about its paid services do

not prominently outline access seekers’ right of free access to credit reporting information in certain

circumstances. The complainants contend that on the my credit file website, although the ‘paid report’

option is very prominent, the ‘free report’ button is below the fold-line (see figure 2), and the statement

about the rights of access seekers to free reports is not prominent.

49. Veda on the other hand argues that it meets the requirements of paragraph 19.3(a) of the CR code:

‘both free and paid services are prominently identified, and available and accessible from the home page of the

website. The ‘free report’ button is prominent and physically close to the information regarding the paid service.’14

50. Veda contends that the correct interpretation of paragraph 19.3(a) in the context of a website-based

service, having regard to the purpose of the provision ’to give visibility to the rights to credit reporting

information free of charge’, is that the phrase ‘the information made available by the CRB about the fee-

based service’ means information made available on the website as a whole:

‘The paragraph does not require the placement of the specified statement regarding free reports, or a “free

report” button at every single instance where information regarding a fee-based service appears on a website.

This would be an absurd and unreasonable interpretation, which goes beyond the object or purpose of the

paragraph. Once a user is alerted to the possibility of a free report, the user does not then need to be reminded at

every step that a free report is available….

‘By analogy, in the circumstances of a hard copy brochure regarding a fee-based service, paragraph 19.3(a) could

not reasonably be interpreted to require multiple prominent statements regarding free reports, appearing in each

paragraph of the brochure where information regarding a fee-based service appeared.’

51. In this respect Veda notes that the first two relevant links to credit reports on the Veda website

homepage, entitled ’get your credit report’, link to the my credit file website, which contains a

prominent ’free report’ button, and contains the information regarding free reports required by

paragraph 19.3(a) of the CR code. The your credit and identity

(www.veda.com.au/yourcreditandidentity) web page is a subpage of the Veda website, with links on the

Veda homepage that are subordinate to those for the my credit file website.21

52. The complainants contend that websites are not comparable to brochures.

14 Veda’s submission to the OAIC, 20 April 2015, 2-3, [1.4].

21 Veda’s submission to the OAIC, 20 April 2015, 5-6, [3.4]-[3.5].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 18

‘Websites are amorphous, are navigated via hyperlinks and can consist of many dozens of separate pages.’15

Findings in relation to prominence issue

The Veda website

53. Veda claims that the primary site for information about its paid services is its my credit file website,

which is the website that also contains the free credit report information. The your credit and identity

web page is a subpage of the Veda website. As I understand it, the Veda website at the relevant time re-

directed customers to the my credit file website if the appropriate link ‘Get Your Credit Report’ was

clicked on, but the Veda website did not otherwise contain or provide links to free credit reporting

information.

54. I have reviewed various links from the Veda website homepage around the time the complaint was

made. The following web pages were linked to the Veda website homepage and made reference to paid

services that include accessing ‘your credit report’ but did not provide any information about accessing

credit reports free of charge:

I. https://web.archive.org/web/20140707102041/http://www.veda.com.au/yourcreditandidentity/pr

oduct-comparison (link from Veda homepage by clicking onto buttons ‘Get your credit score’ and

‘Get identity watch’ as at 7 July 2014) (figure 3)

15 Complainants’ submission in reply to the OAIC, 15 June 2015, 10, [33].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 19

Figure 3 — link from Veda homepage by clicking onto buttons ‘Get your credit score’ and ‘Get identity watch’

II. https://web.archive.org/web/20140712112900/http://www.veda.com.au/yourcreditandidentity/ch

eck (link from Veda homepage by clicking onto buttons ‘Check your credit file and Veda score’ /

‘Understand your credit file and Veda score’, as at 12 July 2014) (figure 4)

Figure 4 — link from Veda homepage by clicking onto buttons ‘Check your credit file and Veda score’ /

‘Understand your credit file and Veda score’

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 20

III. https://web.archive.org/web/20140712151905/http://www.veda.com.au/yourcreditandidentity/im

prove/improving-your-veda-score (link from Veda homepage by clicking onto button ‘Tips to

improve your credit file and Veda score’, as at 12 July 2014) (figure 5).

Figure 5 — link from Veda homepage by clicking onto button ‘Tips to improve your credit file and Veda score’

55. From these web pages, I could not discern any information about accessing credit reporting information

free of charge, despite my attempts to investigate through a series of optional click-throughs to other

pages on the Veda website.

56. The word ‘prominent’ is not defined in the Privacy Act and in the absence of any legislative intention to

the contrary, it may be ascribed its ordinary natural meaning. According to the Macquarie Dictionary the

word ‘prominent’ means in the relevant context ‘standing out so as to be easily seen; conspicuous; very

noticeable’.16

57. I agree with the complainants — brochures are not websites. Websites are not generally read in the

same front-to-back and left-to-right way as brochures. Users may enter the site from a subpage rather

than the home page, and may never go to the home page of a website.17 Veda’s contention that

providing free credit reporting information on only one web page is sufficient does not appear to take

this into account.

16 Macquarie Dictionary, Macquarie Dictionary Online, 6th ed (October 2013) < https://www.macquariedictionary.com.au/>.

https://www.macquariedictionary.com.au/features/word/search/?word=transfer&search_word_type=Dictionary>.

17 See for example, Sarah Morton. (November 2012). Writing Brochure Copy versus Website Copy, Sarah Morton Copywriter. (Accessed 15 August 2016). <https:sarahmortoncopwriter.com.au/writing-brochure-copy-versus-webiste-copy>.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 21

58. Keeping in mind the ordinary meaning of the word ‘prominent’, I am of the view that Veda has not met

the requirements of paragraph 19.3(a) of the CR code in relation to the information Veda has made

available about its fee-based services on its Veda website.

The ‘my credit file’ website

59. A review of the home page on the my credit file website shows if a class member scrolls down the web

page through a list of fee-for-service options, they will be alerted by a button with the words ‘Free file,

find out more’ that they may be able to access a free copy of their credit report (figure 2).

60. The words ‘Free File’ are in white text against a light red background and the button is readily viewable

and identifiable. I also note that a statement setting out the circumstances in which a free credit report

can be obtained is displayed on the same page, to the left of the ‘Free File’ button. The information is

directly below information about Veda’s fee-based service.

61. It is therefore apparent that information made available on the my credit file website about Veda’s fee-

based services also provides information about individuals’ right under the Privacy Act to access their

credit reports free of charge.18 The complainants argue that this information was at the relevant time not

‘prominently stated’ for the purposes of paragraph 19.3(a) of the CR code.

62. Examining the layout of the my credit file website home page as it was at the time the complaint was

made (figures 2 and 6), I note the following:

the statement about free access to credit reports (the relevant statement) is located below the

‘fold’ (that is, below that part of the web page that is visible without scrolling)

the text of the relevant statement is in Arial font, size 10

to the right side of the relevant statement appear the words ‘Free File, Find out more’ within a

large light red luminescent rectangle

the text directly above the relevant statement, stating that “for less than $1.55 a week, you can

better manage one of your most important assets” is in bold Helvetica font, size 13.5, and in

colour

to the right side of this text is a smaller rectangle (button) of a dark red colour featuring the words

‘Buy Now’.

18 <www.mycreditfile.com.au>; <www.mycreditfile.com.au/products-and-pricing>; <www.mycreditfile.com.au/personal/veda-

alert.dot>,

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 22

Figure 6

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 23

63. The home page of the ‘my credit file’ website, displays a series of colour photographs and two ‘buy now’

buttons (figure 6). The ‘Free File’ button, although large and colourful, is below the ‘fold’ and does not

come into view until the page is scrolled. It is not able to be seen on the web page at first instance (prior

to scrolling). In other words, it is not noticeable on the face of it, and in my view does not have the

necessary degree of prominence needed to meet the requirement of ‘prominently stated’ under

paragraph 19.3(a) of the CR code.

64. I therefore find that Veda has not met the requirements of paragraph 19.3(a) of the CR code in relation

to the information Veda has made available about its fee-based services on its ‘my credit file’ website. I

am of the view that Veda has engaged in conduct constituting an interference with the privacy of

individuals who are members of the class identified in the complaint.

The online access issue

65. The complainants also allege that access to a free credit report on the Veda and ‘my credit file’ websites

is not as available and as easy to identify and access as credit reports accessed through its paid services,

in breach of paragraph 19.3(b) of the CR code.19

66. Paragraph 19.3(b) of the CR code states that if a CRB has a service whereby an individual may obtain

their credit reporting information for a fee, the CRB must take reasonable steps to ensure that its

service, whereby individuals may obtain their credit reporting information free of charge, is as available

and easy to identify and access as its fee-based service.

67. In reference to the ‘my credit file’ website shown in figures 1 and 2, the complainants contend that a

free file is not as easy to access and identify as Veda’s fee-based service because:

o the reference to the free service is much further down the page

o unlike Veda’s fee-for-service options which provide for direct access via an online application

form, access to a free credit report requires access seekers to fill in an enquiries form at first

instance. The ordering form and instructions are subsequently emailed to the access seeker to

complete.20

68. The complainants also refer to the ‘’your credit and identity’ web page on the Veda website which

compares a number of Veda paid products including Starter, Access, ID and Plan. According to the

complainants the web page does not mention the option of free access to a credit report. They state

that it would be reasonable for a person looking at this web page to assume that these four products

were the only choices (figures 7 and 8).21

19 Initial representative complaint about Veda Advantage to the OAIC, 15 August 2014, 1.

20 First representative complaint about Veda Advantage to the OAIC, 15 August 2014, 3.

21 First representative complaint about Veda Advantage to the OAIC, 15 August 2014, 3.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 24

Figure 7.

Figure 8: the ‘your credit and identity’ web page after scrolling down.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 25

69. The complainants state that there are several links to the ‘your credit and identity’ web page and none of

the linked pages refer to the option of free access to a credit report.22

70. Veda does not accept that it did not comply with paragraph 19.3(b) of the CR Code. It argues that

paragraph 19.3(b) requires an assessment of what a reasonable person would be expected to implement

in the circumstances, and does not require Veda to treat its paid services and its service providing access

to free reports identically. Veda contends that rather, what is required is ‘reasonable substantial parity’ in

the availability of, identification of, and access to, free reports, having regard to all the circumstances.23

Current position

71. I acknowledge that since the first representative complaint was lodged, Veda has amended how it makes

information about its service providing access to credit reports free of charge available on its ‘my credit

file’ website. It has moved information about free credit reports to a horizontal level equivalent to the

Veda website’s first reference to a paid service, so that a viewer no longer has to scroll right down the

web page to view information about how to access a credit report free of charge. It has also amended its

‘your credit and identity’ web page on the Veda website so an initial comparison of Veda products

(‘Compare Our Products’) at the top of the web page includes a ‘free file’ option.24

72. Nonetheless, the current presentation mode of Veda’s websites is not relevant to the issues that I have to

decide here. My findings must be based on the steps Veda had in place at the time the complaint was

lodged. It must also be said that all the current website presentations show what could have been done

earlier. They do not, by any necessary implication, demonstrate that what was done earlier was in

contravention of the Act or the CR code.

73. My findings in relation to the online access issue are as follows.

Findings in relation to online access issue

74. Veda contends that it met the ‘reasonable steps’ standard mandated at paragraph 19.3 of the CR Code, by

making both free and paid services prominently identifiable, available and accessible from the homepage

of its ‘my credit file’ website.

75. The complainants argue that the requirement under paragraph 19.3 that Veda’s free service be ‘as

available’, ‘as easy to identify’ and ‘as easy to access’ as its fee-based service, “demands equivalence

22 Initial representative complaint about Veda Advantage, 15 August 2014, 3.

23 Veda’s submission to the OAIC, 20 April 2015, 2, [1.2]-[1.4].

24 https://www.veda.com.au/yourcreditandidentity/product-comparison.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 26

between the free service and the fee service of the three mandated outcomes: availability, ease of

identification, and ease of access”.25

76. In determining whether Veda has fulfilled its paragraph 19.3 obligations I must also consider the overall

objects of the Privacy Act including the facilitation of an efficient credit reporting system while ensuring

that the privacy of individuals is respected; and that the protection of the privacy of individuals must be

balanced with the interests of entities in carrying out their functions or activities.26

Reasonable steps

77. Paragraph 19.3 of the CR code names s 20R of the Privacy Act as its source. The explanatory

memorandum to the Privacy Amendment (Enhancing Privacy Protection) Bill 2012 (‘explanatory

memorandum’) states:

This provision [s 20R] is based on the obligations set out in, and the structure of, APP 12, modified to apply specifically to credit reporting bodies. It is generally intended that access to credit reporting information should occur on the same terms as access to personal information held by an APP entity27.

78. Though the APPs do not apply to a credit reporting body in relation to personal information that is credit

reporting information28, the APP guidelines may provide some guidance in relation to what may be

considered ‘reasonable steps’.

79. ‘Reasonable steps’ is not defined in the Privacy Act, but I accept that the steps required to be taken do not

have to be exhaustive; rather reasonable where ‘reasonable’ means appropriate in the circumstances.29 It

is, however, the responsibility of the APP entity to be able to justify that its conduct was reasonable, and

that reasonable steps were taken. 30

Google search results

80. Veda contends that the results returned from internet search engines are highly relevant in assessing

what constitutes ‘reasonable steps’ under paragraph 19.3(b) of the CR code given that the standard

practices of internet users seeking information is to search via internet search engines rather than by

reviewing web pages.31

25 Complainants’ reply to Veda’s submission, 15 June 2015, 5, [14].

26 Privacy Act 1988 (Cth), s 2A.

27 Explanatory memorandum, Privacy Amendment (Enhancing Privacy Protection) Bill 2012

28 Privacy Act 1988 (Cth), s 20A(2).

29 Office of the Australian Information Commissioner, Australian Privacy Principles Guidelines, B.99.

30 Office of the Australian Information Commissioner, Australian Privacy Principles Guidelines, B.105, B.108.

31 Veda’s submission to the OAIC, 20 April 2015, [1.5].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 27

81. Search engines such as Google allow internet users to search for information of interest by entering

search terms into the search box on the search engine’s website or on users’ toolbars. A search will

produce both advertisements (‘sponsored links’)32 and ‘organic search results’ (i.e. the main search results

not influenced by advertising). Organic search results are ranked in order of relevance to the search terms

entered by the user.

82. In its 20 April 2015 submission Veda uses the example of a Google search conducted on 14 April 2015 on

the search phrase ‘credit report’ which returned a link to the ‘my credit file’ website under the heading

‘Order a Free Credit Report’. This link took the user directly to a web page titled ‘How to get your credit

report free of charge’ (figure 9).

Figure 9.

32 On a web page, advertisements are labelled ‘Ad’ or ‘Ads’ and are listed separately to the organic search results. They are triggered by

keywords supplied by the advertiser to the search provider, using an AdWords program. When a user enters search terms into the search engine that match the keywords of an advertiser, the search results will display the triggered sponsored links. Organisations like Veda using sponsored links pay the search provider every time a user clicks on the sponsored link.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 28

83. Veda contends that search results like this ‘clearly demonstrate that Veda has taken reasonable steps to

ensure that its service whereby individuals may obtain their credit reporting information free of charge

is as available and easy to identify and access as its fee-based service’.33

84. The complainants argue that it is not a ‘reasonable step’ to “trust in a Google search as providing parity

of availability, ease of identification and ease of access” between paid services and those services

provided free of charge.34

85. I agree that there are some difficulties with Veda’s contention. Firstly, search results will vary between

different devices and different users on different days. Searches of the same keywords - ‘credit report’ –

on 16 December 2014 (figure 10) and 5 May 2015 (figure 11), produced different search results, for

example.

33 Veda submission to the OAIC, 20 April 2015, 5-6, [3.4]-[3.6].

34 Complainants’ reply to Veda’s submission, 15 June 2015, 8, [22].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 29

Figure 10

86. For example, in contrast to the search results provided on 14 April 2015, the first Veda result returned

on the 5 May 2015 search by the complainants was http://www.veda.com.au/yourcredit and

identity/tips-mythbusters/fags/how-can-I-check-my-credit-history (figure 10). This web page did not

refer to free credit reports, providing only options for paid services.35

35 Complainant representatives’ response to Veda submission of 20 April 2015, 8, [22]-[25].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 30

Figure 11.

87. This is not surprising. Different search results may be obtained even when the same key words are

searched. This may be due to variances in a user’s physical location or in the search history of different

devices, or the keyword search being performed by different Google data centres.36

88. Secondly, I note the searches conducted by Veda to illustrate the relevance of Google search results to it

meeting its obligations under paragraph 19.3(b) of the CR code were undertaken sometime after the

date of the complaint. Their relevance as to what results might have been produced around the time of

the complaint is accordingly limited.

89. Thirdly, and perhaps most importantly, there is no information before me which indicates that Veda has

actually taken any steps to produce the search results it highlights in its submission.

36 McEvoy, M. (2015). 7 Reasons Google Search Results Vary Dramatically. Web Presence Solutions. Accessed 22 August 2016.

www.webpresencesolutions.net/7-reasons-google-search-results-vary-dramatically/>; Snipes, Susan. (2012). SEO Under Scrutiny: Reasons your Google search results are different than mine. Q Digital Studio. Accessed 19 August 2016. < <http://www.qdigitalstudio.com/library/reasons-your-google-search-results-are-different-than-mine>; Sullivan, Rob.(n.d.) SEO Questions – Why Do I See Different Google Results Than My Clients? Internet Seer. Accessed 19 August 2016. < http://www.internetseer.com/services/article.xtp?id=37037>.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 31

90. A business may maximise its exposure via organic search results through a process known as ‘search

engine optimisation’ to ensure that it appears first in the organic search results.37 This is a form of search

engine marketing and involves optimising each page of a website to include keyword phrases in headers,

sub headers, web page text, hyperlinks and, where appropriate, in image file names and alt tags, which

provide a text alternative to an image.

91. Veda engages from time to time in search engine optimisation strategies to market to individuals and/or

business customers.38 However, there is no evidence that Veda engaged in any search engine optimisation

strategies to try to bring its service of free access to credit reports to the attention of access seekers.

There is no information which suggests that Veda did anything by way of website optimisation to promote

its service whereby individuals may obtain their credit reports free of charge.

92. For this reason, I give little weight to the results returned from internet search engines in determining this

matter.

‘my credit file’ website

93. In its letter to the complainants dated 14 May 2014, Veda outlines the online process an access seeker

may take to access a free credit report:

(a) On Veda’s main website and landing page <www.veda.com.au>, a consumer can see information

about access to credit reports as well as other Veda services (figure 12).

37Search engine optimisation discussed by Katzmann J in Veda Advantage Limited v Malouf Group Enterprises Pty Limited [2016] FCA

255 (21 March 2016).

38 Noted in Veda Advantage Limited v Malouf Group Enterprises Pty Limited [2016] FCA 255 (21 March 2016), [12].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 32

Figure 12.

(b) When a consumer clicks on GET YOUR CREDIT REPORT, they are taken to Veda’s ‘My Credit File’

website which includes information about credit reports as well as a large ‘free file’ button (figure 13)

Figure 13.

(c) Clicking on the large red button brings consumers to the free credit file page. Very clear instructions

on how to order your free credit file are provided (figure 14).

(d) A consumer enters in details and the ordering form and instructions are emailed to the consumer to

complete (figure 15).39

39Veda letter to the complainants, 14 May 2014, 3-6.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 33

Figure 14.

Figure 15.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 34

94. Veda, in support of its contention that its free and paid services in relation to access to credit reports are

of “reasonable substantial parity”, points out that the ‘Free File’ button is prominent and physically close

to the information regarding Veda’s paid services (figures 6 and 7).40 I have discussed the issue of

prominence at [56]-[63].

95. The complainants note that the position of the ‘Free File’ button is, however, much further down the

web page (i.e. below the ‘fold line’). By this I take it to mean that the complainants are contending that

information about free credit reports is less easily identified or accessible than information about Veda’s

paid services because access seekers have to scroll further down the web page.

96. Veda argues that:

The ‘fold line’ is irrelevant, as reasonable, substantial parity is achieved by having both types of reports

prominently identified, available and accessible via the internet at the same place, being the ‘My Credit File’

home page. Nothing further is required.41

97. Secondary sources in the form of research findings suggest that although the concept of a fold was

important in early web history, nowadays people do scroll and it is not as integral to web advertising

today.42 Research findings on whether scrolling is an impediment to users are mixed.43 There is research

that indicates users’ attention is generally caught above the fold44, while other studies have found that

users spend more time on actual web content as they move down the page45. What does seem to be an

accepted finding amongst researchers is that users’ behaviour has changed over the years since the

inception of the personal computer and they are more likely to scroll than previously. Research has also

indicated that web designers are now being encouraged to design a page that encourages users to scroll

rather than to navigate away from the page.46

40 Veda’s submission to the OAIC, 20 April 2015, 2, [1.4].

41 Veda’s submission to the OAIC, 20 April 2015, 2-3, [1.4].

42 Motive, The Motive Web Design Glossary, (updated August 2009) <www.motive.co.nz/glossary/fold.php.

43 Mixed research findings noted by Matt Keogh (February 2015, updated June 2016) Does It Matter if Users Need to Scroll? Liquid Light. https://www.liquidlight.co.uk/blog/article/does-it-matter-if-users-need-to-scroll>. See also Haile, Tony. (March 2014). What You Think You know About the Web is Wrong? Time. http://time.com/12933/what-you-think-you-know-about-the-web-is-wrong/.

44 Schade, Amy. (February 2015). The Fold Manifesto: Why the Page Fold Still Matters. Nielsen Norman Group. <https://www.nngroup.com/articles/page-fold-manifesto>. Highlighted by Matt Keogh (February 2015, updated June 2016) Does It Matter if Users Need to Scroll? Liquid Light. https://www.liquidlight.co.uk/blog/article/does-it-matter-if-users-need-to-scroll>.

45 Josh. (August 2013). Scroll behaviour across the web. Chartbeat Blog. <blog.chartbeat.com/2013/08/12scroll-behavour-across-the-web>. Highlighted by Matt Keogh (February 2015, updated June 2016) Does It Matter if Users Need to Scroll? Liquid Light. https://www.liquidlight.co.uk/blog/article/does-it-matter-if-users-need-to-scroll>.

46 Schade, Amy. (February 2015) The Fold Manifesto: Why the Page Fold Still Matters, Nielsen Norman Group <https://www.nngroup.com/articles/page-fold-manifesto>. See also Cao, Jerry. (October 2015). The New Rules for Scrolling in Web Design. DesignMode. <designmode.com/scrolling-web-design.>

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 35

98. There is no doubt that scrolling is an extra action, but the issue here is, does having to scroll down to

information about how to access a free credit report lessen its availability or the ease with which this

information may be identified or accessed?

99. I accept that the images on a web page are not, unlike television for example, transitory; a viewer can

generally take as long as they wish to review the contents of the page.47 It is therefore difficult to see

how scrolling down half a page on the same web page could be seen to lessen the availability of the free

credit reporting information or lessen the ease with which it is accessed, within the ordinary meaning of

the word (i.e. access meaning ‘the opportunity to approach or enter a place’48). Nonetheless, as I noted

at paragraphs [56]-[63], information that is not viewable at first instance on a screen is not as prominent

as information that is instantly viewable on screen. For information to be as identifiable as other

information, it must be as easily recognisable. In my view, the information made available on the ‘my

credit file’ website does not enable access seekers to identify Veda’s free-based service as easily as its

fee-based services, and in this regard I find that Veda has not complied with paragraph 19.3(b) of the CR

code.

Veda’s www.veda.com.au website

100. The complainants also claim that the web page www.veda.com.au/yourcreditandidentity linked to

Veda’s main website, at the relevant time, compared a number of Veda’s paid products (Starter, Access,

ID and Plan) which included a service to provide customers with their credit report (figure 16). The

complainants contend that the web page did not include any information which identified a service for

customers to access their credit report free of charge. The complainants contend that:

It would be reasonable for a person looking at this web page to assume that these four products were the only

options.49

47 See Australian Competition and Consumer Commission v Hillside (Australia New Media) Pty Ltd trading as Bet365 [2015] FCA 1007

for support of this view.

48 Macquarie Dictionary, Macquarie Dictionary Online, 6th ed (October 2013) < https://www.macquariedictionary.com.au/>. https://www.macquariedictionary.com.au/features/word/search/?word=transfer&search_word_type=Dictionary>.

49 Complainants’ representative complaint to the OAIC, 15 August 2014, 3.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 36

Figure 16.

101. Veda contends that this web page, as well as its Veda home page and ‘my credit file’ website, had links

to Veda’s credit policy “which clearly sets out how individuals can obtain free access to their credit

reporting information”50.

102. I accept that nowadays a majority of class members have a reasonable understanding of how to

navigate the web. Clicking-through to other pages does not necessarily mean that something is less

accessible. Nonetheless, at the relevant time the digital pathway from Veda’s ‘my credit and identity’

web page to information embedded in Veda’s credit policy about accessing credit reports free of charge

was lengthy and not user-friendly. In order to navigate successfully, an access seeker would need to

already be aware that information about access to Veda’s free service could be found within Veda’s

credit policy.

103. Having to discern how to access a credit report free of charge by firstly being aware that the

information was embedded in a ‘credit policy’ page, and then clicking through to that page, is not as

easy as being presented with that information on the home or landing page. I therefore consider that

the Veda website does not enable access seekers to identify Veda’s free-based service as easily as its

fee-based service, and I find that Veda has not complied with paragraph 19.3(b) of the CR code in this

regard.

50 Veda response to the complainants, 14 May 2014, (Appendix C to Representative complaint about Veda Advantage dated 15

August 2014).

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 37

104. The complainants further contend that Veda’s free service is not as easy to access and is not as

available as the paid service. To access the free service, access seekers needed to submit an ‘enquiries

form’ through Veda’s portal. I note from a review of the web pages at the relevant time51 that clicking

on the ‘’Free File, find out more’ button on the ‘my credit file’ home page took access seekers to a page

titled ‘How to get your credit report free of charge’. To obtain a free copy of their credit report, access

seekers had to complete the Veda Free Credit File Form. Certain identification details (name, phone

number, email address, state, and ‘yes/no’ to marketing) needed to be submitted on an online ‘order

form’. Once this form was submitted, access seekers would ‘immediately receive’ by email another form

to request a free copy of their credit report (figure 15).

105. Veda confirms this process in its 14 May 2014 response to the complainants, which is outlined at

paragraph [93].

106. In contrast, individuals accessing Veda’s paid services at the relevant time, could apply directly online

for their credit report. There was no additional requirement to complete an enquiries form and receive

further email instructions from Veda on how to apply for their credit report.

107. In its 14 May 2014 response to the complainants, Veda advises that it is investing in “a new portal

aligning processes and requirements for free reports with those available for paid services”. Veda states:

Customers seeking a free report will have the same straight through process as applies for paid reports, that is,

they will be able to type-in their information onto an online application form.

108. It is evident that at the relevant time a further step had to be undertaken to obtain a credit report free

of charge. Customers accessing a credit report through Veda’s paid services, on the other hand, could

readily apply online. The online process for paid access was evidently more accessible than that for free

access. Veda accepts that the ‘same straight through process’ as applied to paid reports did not apply to

reports accessed free of charge.52

109. I accept that Veda was at the relevant time “making efforts to streamline the process for requesting a

free credit report”, but I have no substantive information available to me which explains why the online

process for access to free credit reports was implemented differently from the outset, or why there was

such a lag in addressing the variance between the access processes of the paid and unpaid services. I

note that there were “some teething problems with some of the new IT infrastructure” and “an

unprecedented demand for free credit reports”.53

110. In ‘S’ and Veda Advantage Information Services and Solutions Limited54, which the complainants

helpfully referred to, I considered whether or not Veda had taken reasonable steps to ensure that

51 https://web.archive.org/web/20140731202413/http://www.veda.com.au/mcfpage.

52 Veda’s response to the complainant’s complaint, 14 May 2014.

53 Veda’s response to the complainant’s complaint, 14 May 2014.

54 [2012] AICmr 33 at [61].

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 38

personal information contained in the complainant’s credit file or report was ‘accurate, up-to-date,

complete and not misleading’ as required under s 18G, a former provision of the Privacy Act which

existed prior to the 12 March 2014 reforms. In making an assessment of the ‘reasonable steps’ I

relevantly considered:

• the size and nature of an organisation such as Veda and how Veda's practices may impact on a large

number of individuals and credit providers, and

• the ease with which any particular step can be implemented.

111. In their response to Veda’s 20 April 2015 submission, the complainants point out that:

Veda has not shown that it would be arduous or costly to implement practices that provide equivalent

availability, ease of identification of, and ease of access to free credit reporting information to the

availability, ease of identification of, and ease of access to fee-based credit reporting information.

We submit that given Veda’s size and nature, the large number of individuals affected, the object of the

Act and Code to make credit reports freely available to enable errors and omissions to be rectified, the

ease of access to and prominence of Veda’s fee-based services the Commissioner should find that Veda has

not complied with paragraph 19.3(b) of the CR code.55

112. I note that Veda is by its own admission ‘the leading provider of credit information in Australia’. As a

credit reporting body, it claims a market share of 96% with a database of 16.5 million credit-active

Australians.56 It was put on notice about the ‘sizeable changes’57 arising from the 2014 legislative

reforms well before the passing of the Privacy Amendment (Enhancing Privacy Protection) Act 2012, and

was, or should have been aware, of the impact of the changes on its customers58. The onus was on Veda

to justify that it took reasonable steps (as were appropriate in the circumstances) to ensure its free

service was as available and as easy to access as its fee-based services. I am not satisfied that it did so. In

my view, Veda did not meet its obligations under paragraph 19.3(b) of the CR code in this regard.

55 Complainant’s reply to Veda’s submission, 9, [28]-[29].

56 Explanatory Memorandum, Privacy Amendment (enhancing Privacy Protection) Bill 2012, citing Veda Advantage ‘About Us’, accessed 23 July 2009 from <http://www.vedaadvantage.com/about-veda/au_our-data.dot>.

57 Veda response to the complainants, 14 May 2014, (Appendix C to representative complaint about Veda Advantage dated 15 August 2014).

58 See for example, Explanatory Memorandum, Privacy Amendment (enhancing Privacy Protection) Bill 2012, citing Veda Advantage responds to ALRC Privacy Review proposal in Wot News, accessed 23 July 2009 from <http://wotnews.com.au/like/veda_advantage_responds_to_the_alrc_privacy_review_proprosal/1666111>.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 39

The phone access issue

113. The complainants allege that access seekers are not able to obtain a credit report free of charge from

Veda over the phone, while credit reports can be obtained over the phone via Veda’s paid services.59

114. The complainants contend that this is a breach of paragraph 19.3(b) of the CR code which relevantly

states that the CRB must take reasonable steps to ensure that its service whereby individuals may obtain

their credit report free of charge is as available and easy to identify and access as its fee-based service.60

115. The complainants state:

The phone number for Veda … leads to a message that states a free copy of your credit report can be

obtained by visiting the Veda website. There is an option to get a paid copy of a credit report over the

phone, but there is no option to get a free credit report over the phone.61

116. The complainants detail the experiences of an access seeker’s attempts to order a free credit report

over the phone:

In their automated section it asks you whether you are seeking your credit report. On following the prompts,

it takes you to a pre-recorded message that explains that you are entitled to receive a free credit report

every 12 months, and within 90 days of a credit application. It then continues to explain that you can order

the free credit report online or by sending specific information to a postal address.

You are then prompted to go through to a customer service operator. When requesting the free credit

report, I was told by the operator that it could not be done through her and that I could only order the

‘express’ report for $67.62

117. The access seeker’s second attempt to order a free credit report went as follows:

This time the customer service operator that picked up said that I could only receive the free report if I had

internet (which I had told both that I did not have). She said that if I did not have internet the only other

option open to me was to purchase an express report for $67, as it is "easier and better" than the free report

anyway. When I pressed her why I couldn't get a free one on the phone she said that it was a Veda process,

they could only sell the 'express' credit reports on the phone, nothing else.

She also noted that if I purchased the express report I would get all the updates for free. I questioned back to

her, "Are you saying that if I don't have the internet I cannot get a free credit report like I was told I could".

59 Initial representative complaint to the OAIC, 15 August 2014, 1-3.

60 Initial representative complaint to the OAIC, 15 August 2014, 1-3.

61 Initial representative complaint to the OAIC, 15 August 2014, 1-3..

62 Complainant’s reply to Veda’s submission, Attachment 2, ‘Veda Shadow Shopping’, 5 May 2015.

Financial Rights Legal Centre Inc. & Others and Veda Advantage Information Services and Solutions Ltd │ 40

She said "That is up to you, if you don't have the internet you don't have any other option but to buy the

express credit report".63

118. The complainants contend these experiences highlight that in contrast to accessing a credit report by

phone through a paid service, requesting a credit report free of charge by phone is not an option, i.e. an

access seeker is limited to ordering online or making a request by post. In other words, the complainants