Embed Size (px)

Citation preview

Financial Planning for Expatriates: A Global View with a Spotlight on German-US Legal and Tax Considerations

Friday, March 16, 2012 Sofitel Redwood City, San Francisco223 Twin Dolphin Drive Redwood City, CA 94065

Jörg Kemkes, Managing DirectorBridgehouseTax, Atlanta

Alex Knight, PartnerHabif, Arogeti & Wynne, LLP

Kristin Mäckel, Senior Tax ManagerHabif, Arogeti & Wynne, LLP

Presenters

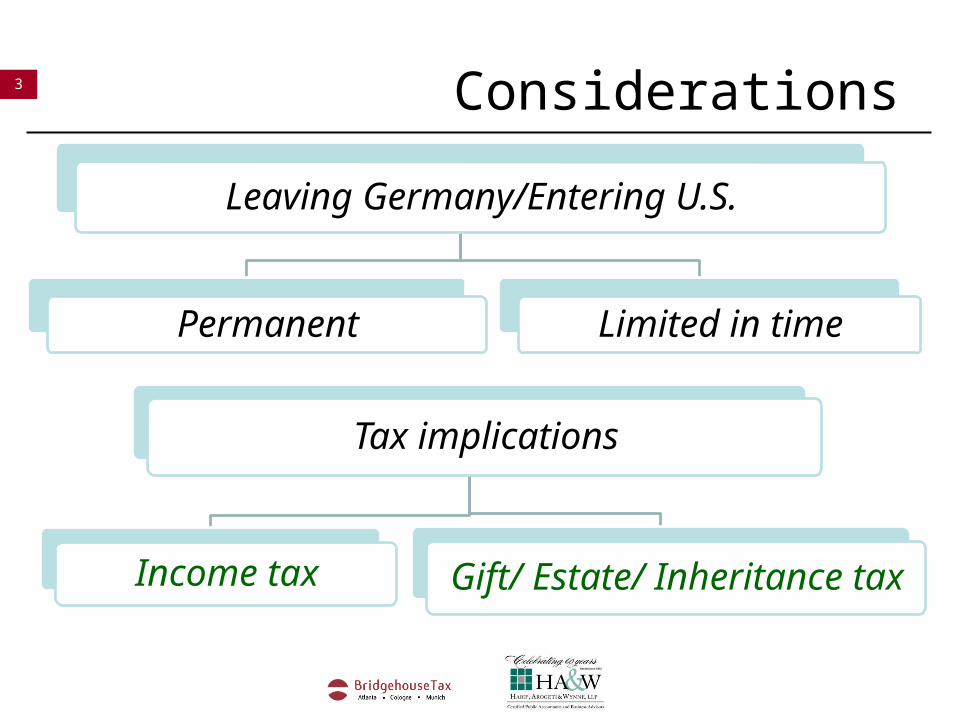

3 Considerations

Leaving Germany/Entering U.S.

Permanent Limited in time

Tax implications

Income tax Gift/ Estate/ Inheritance tax

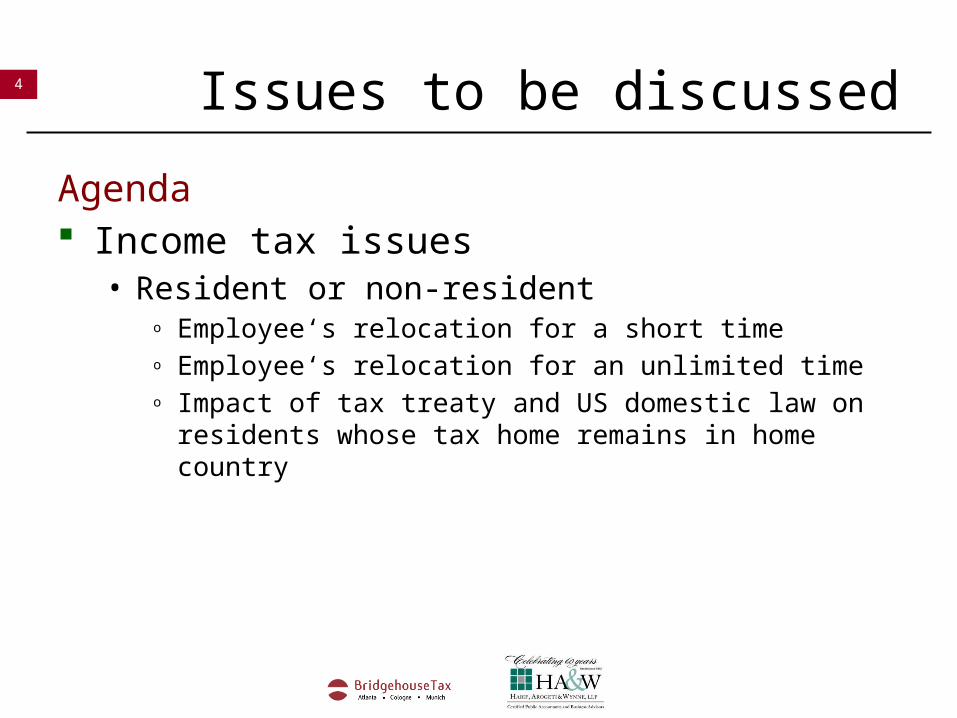

4 Issues to be discussed

Agenda Income tax issues

• Resident or non-residento Employee‘s relocation for a short timeo Employee‘s relocation for an unlimited timeo Impact of tax treaty and US domestic law on residents whose

tax home remains in home country

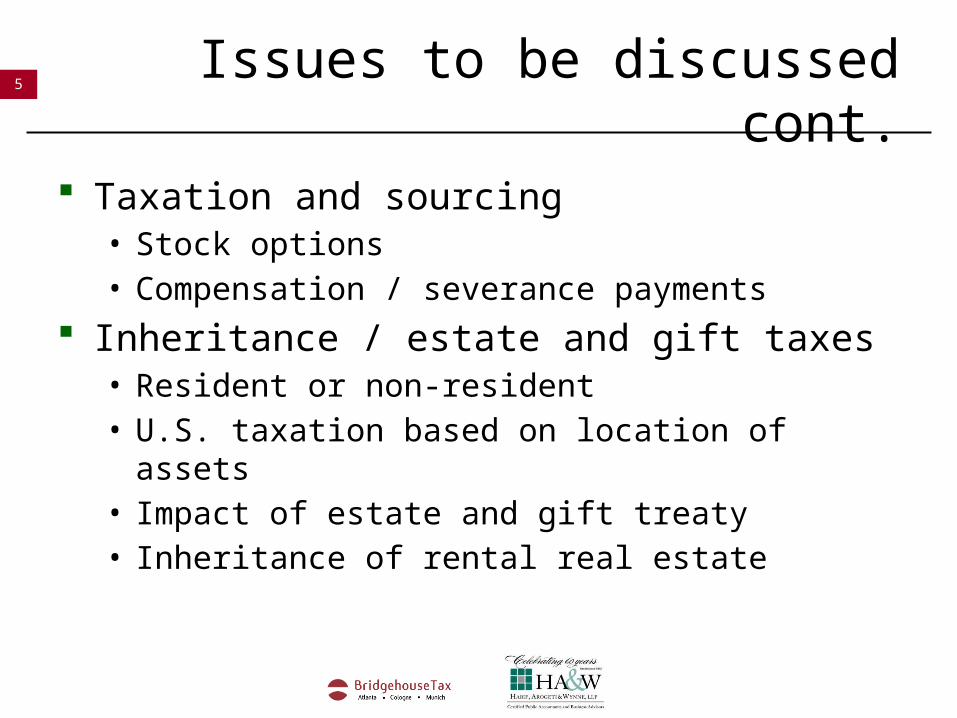

5 Issues to be discussed cont.

Taxation and sourcing• Stock options• Compensation / severance payments

Inheritance / estate and gift taxes • Resident or non-resident• U.S. taxation based on location of assets• Impact of estate and gift treaty• Inheritance of rental real estate

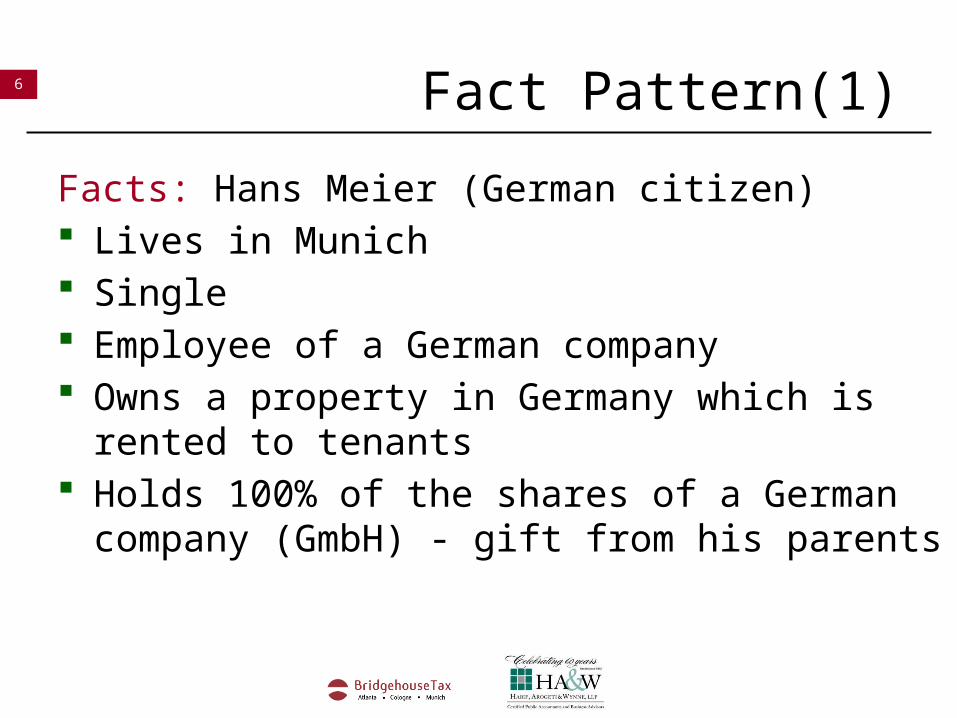

6 Fact Pattern(1)

Facts: Hans Meier (German citizen) Lives in Munich Single Employee of a German company Owns a property in Germany which is rented to

tenants Holds 100% of the shares of a German company

(GmbH) - gift from his parents

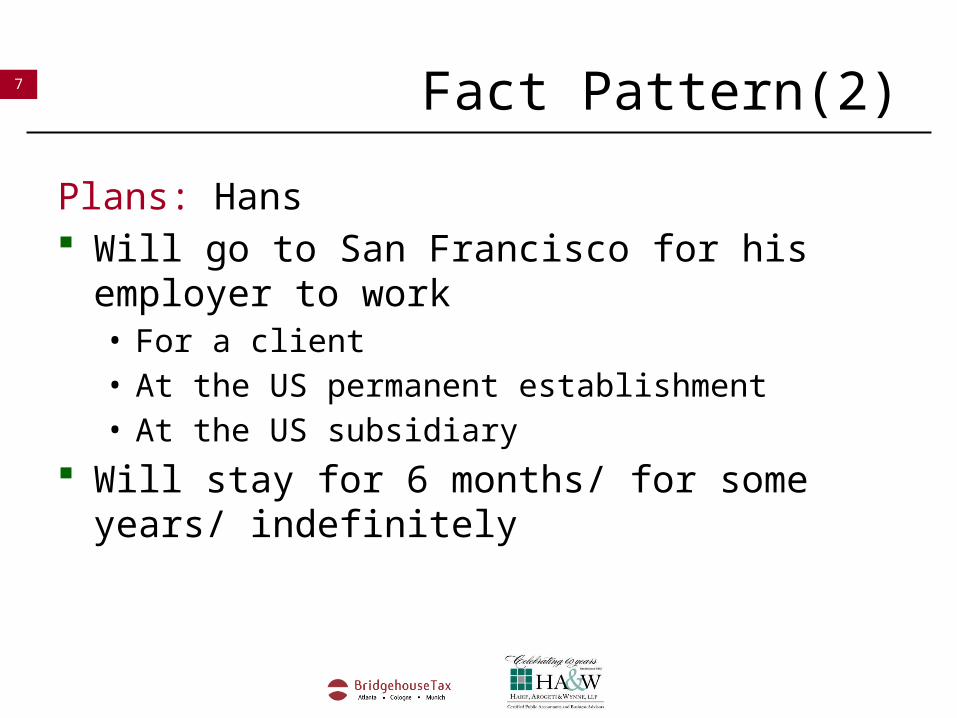

7 Fact Pattern(2)

Plans: Hans Will go to San Francisco for his employer to work

• For a client• At the US permanent establishment• At the US subsidiary

Will stay for 6 months/ for some years/ indefinitely

8 Fact Pattern(3)

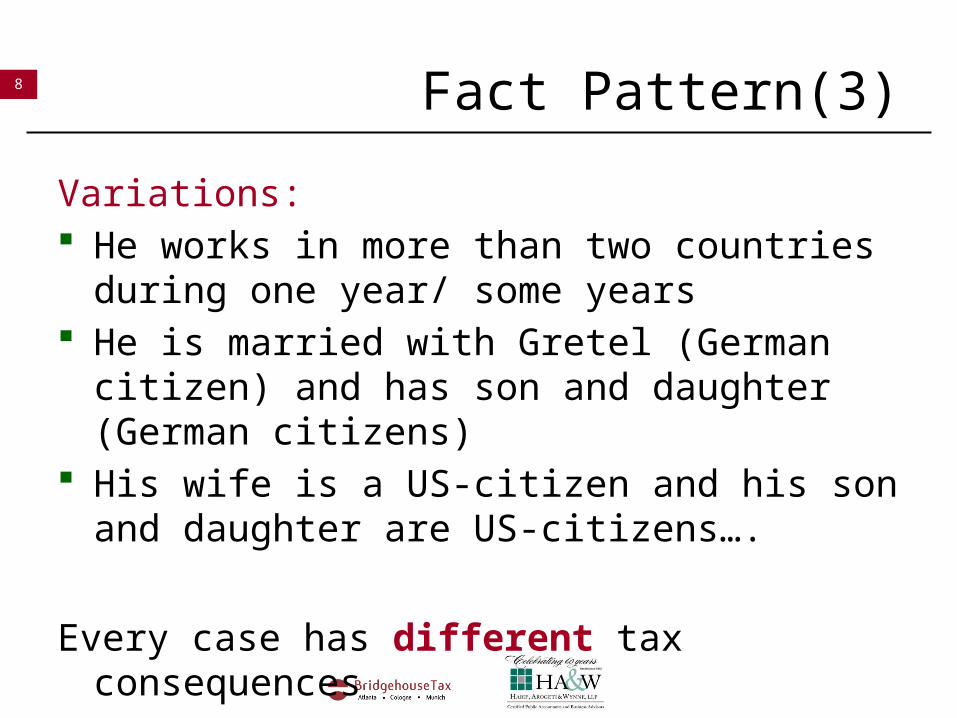

Variations: He works in more than two countries

during one year/ some years He is married with Gretel (German citizen) and has

son and daughter (German citizens) His wife is a US-citizen and his son and daughter

are US-citizens….

Every case has different tax consequences

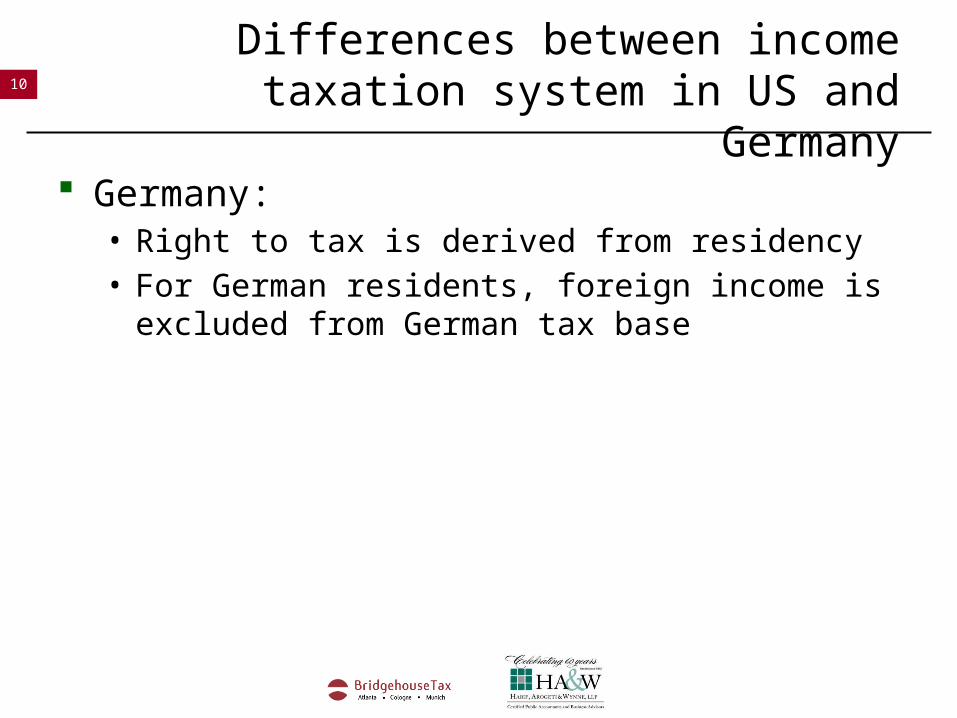

9Differences between income taxation

system in US and Germany

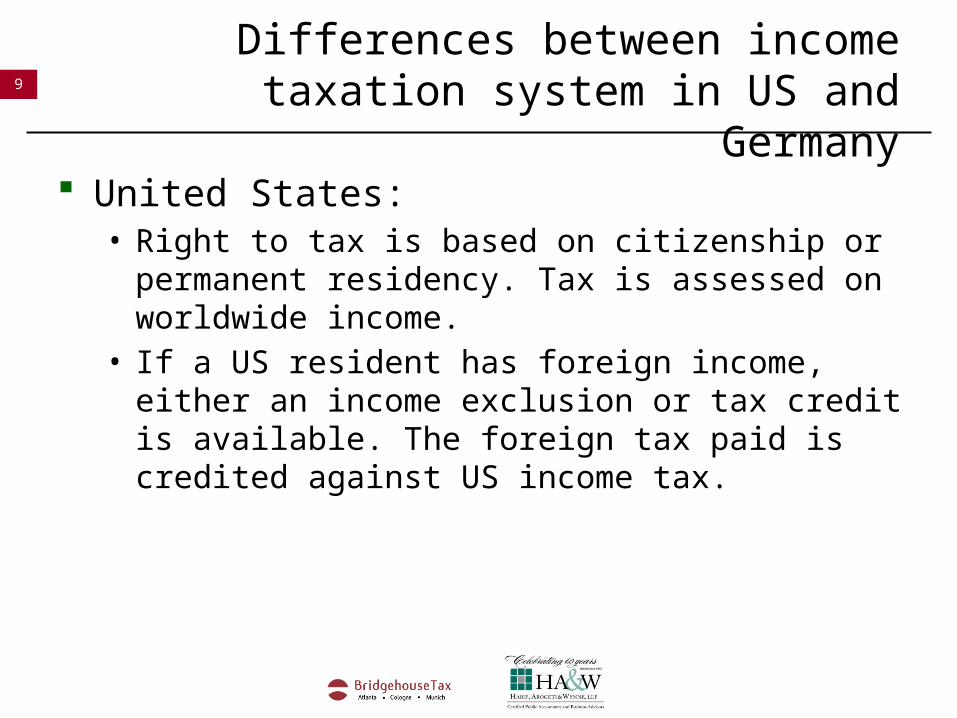

United States:• Right to tax is based on citizenship or permanent

residency. Tax is assessed on worldwide income.• If a US resident has foreign income, either an income

exclusion or tax credit is available. The foreign tax paid is credited against US income tax.

10Differences between income taxation

system in US and Germany

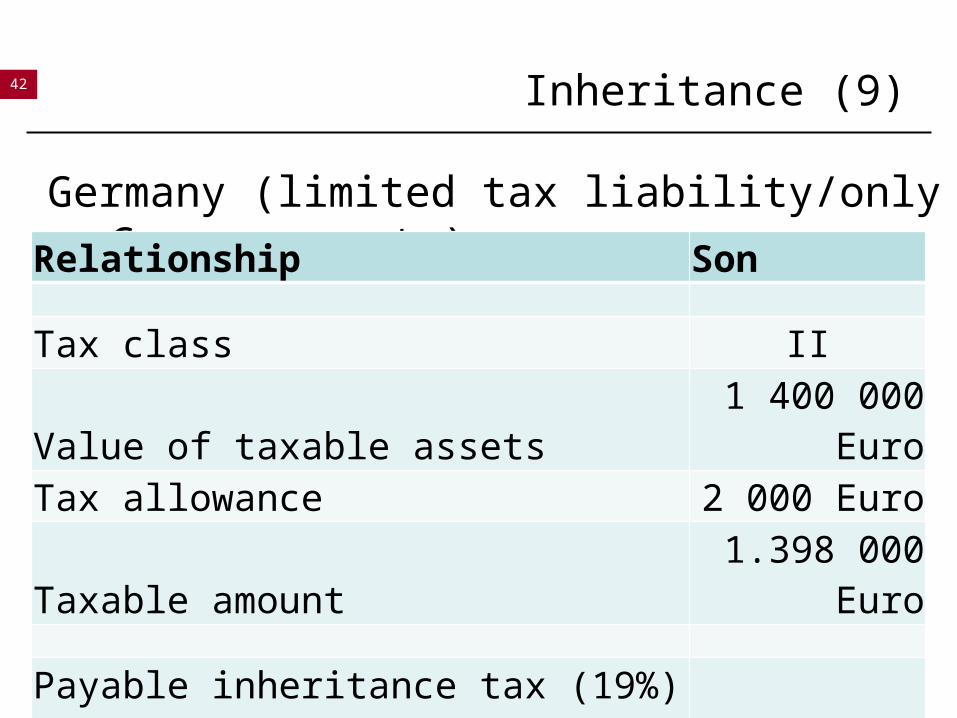

Germany:• Right to tax is derived from residency• For German residents, foreign income is excluded from

German tax base

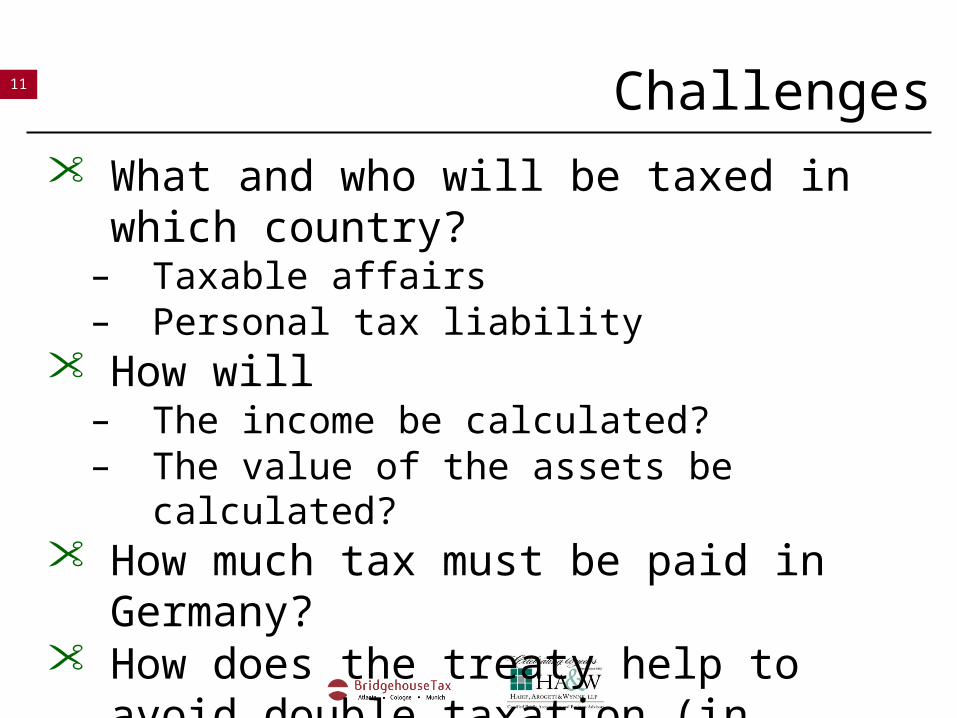

11 Challenges

What and who will be taxed in which country?

– Taxable affairs– Personal tax liability

How will– The income be calculated?– The value of the assets be calculated?

How much tax must be paid in Germany? How does the treaty help to avoid double

taxation (in Germany and the USA)

12

INCOME TAX

Employees‘ relocation

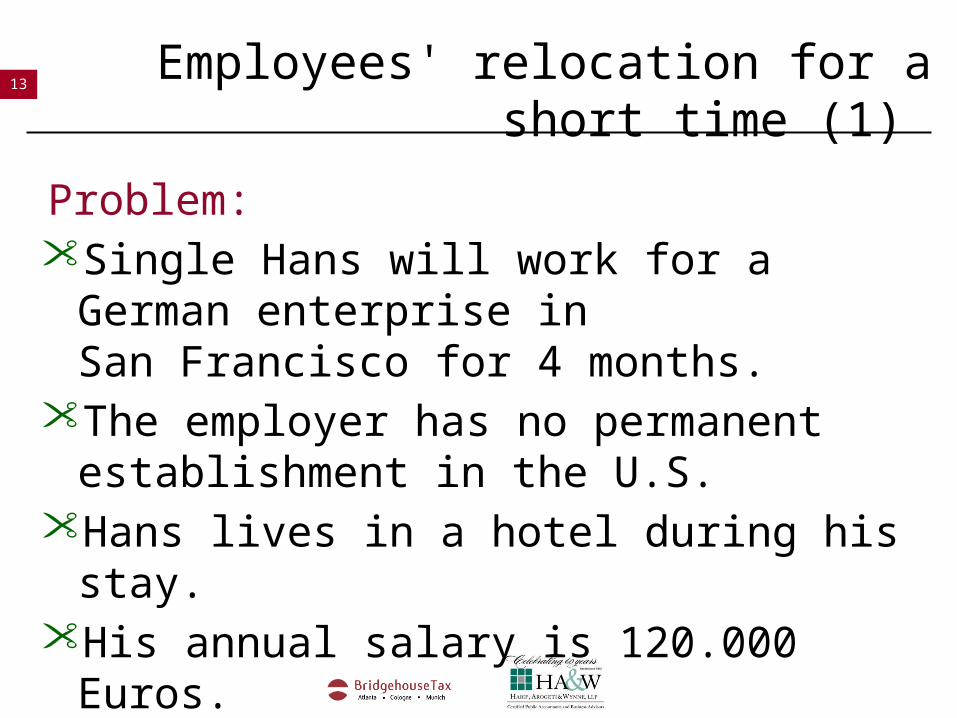

13 Employees' relocation for a short time (1)

Problem:Single Hans will work for a German enterprise

in San Francisco for 4 months.

The employer has no permanent establishment in the U.S.

Hans lives in a hotel during his stay. His annual salary is 120.000 Euros. He has no other income.

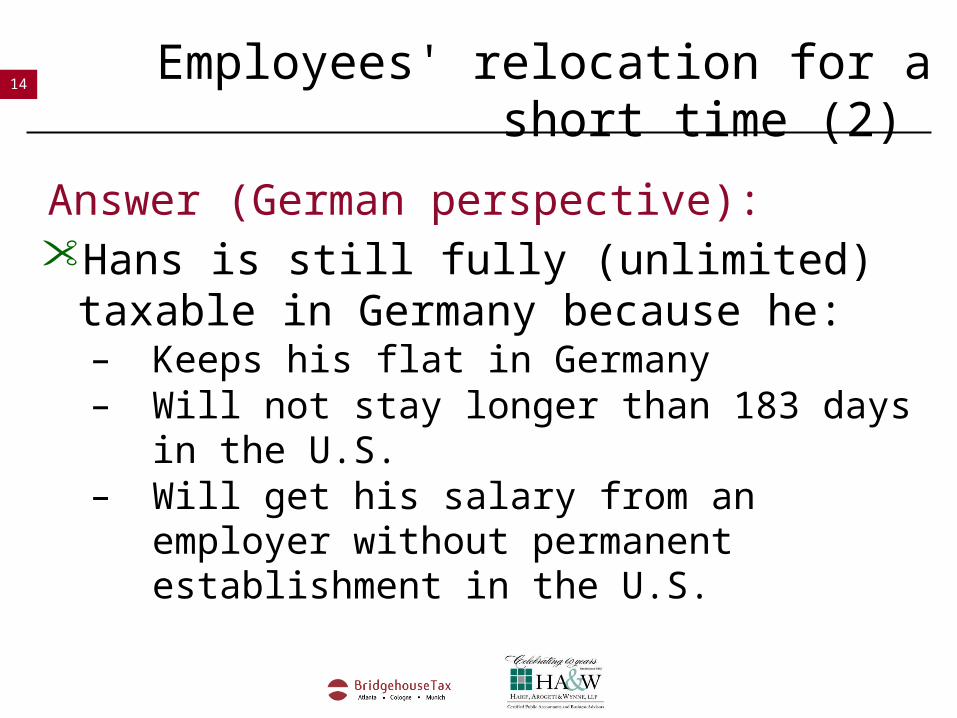

14 Employees' relocation for a short time (2)

Answer (German perspective):Hans is still fully (unlimited) taxable in

Germany because he:– Keeps his flat in Germany– Will not stay longer than 183 days in the U.S.– Will get his salary from an employer without

permanent establishment in the U.S.

15 Employees’ relocation for a short time (3)

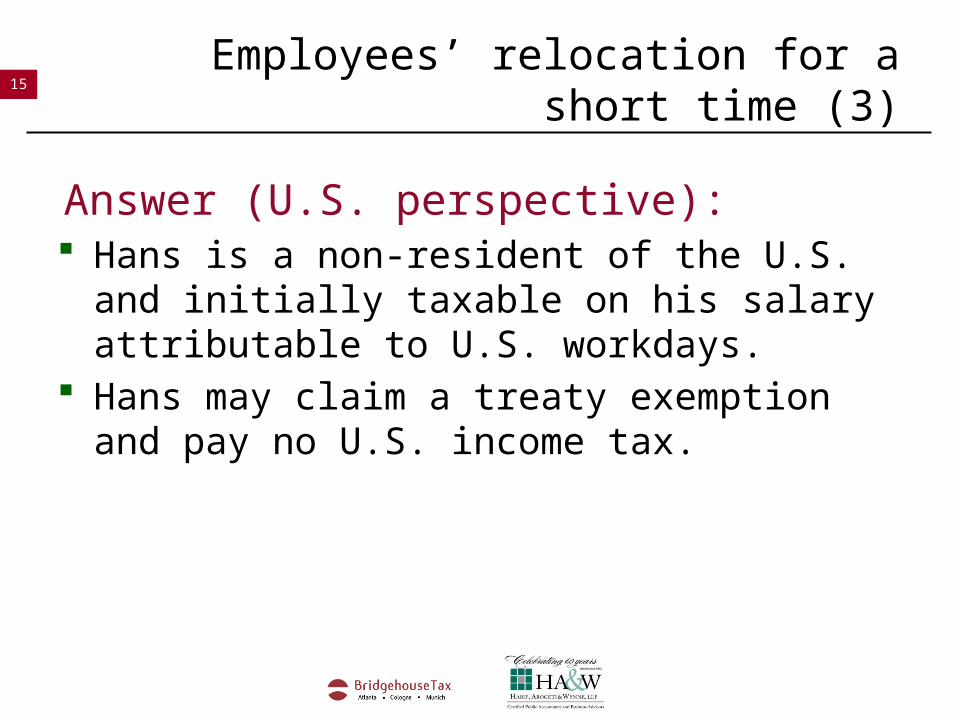

Answer (U.S. perspective): Hans is a non-resident of the U.S. and initially

taxable on his salary attributable to U.S. workdays.

Hans may claim a treaty exemption and pay no U.S. income tax.

16 Employees' relocation for an unlimited time (4)

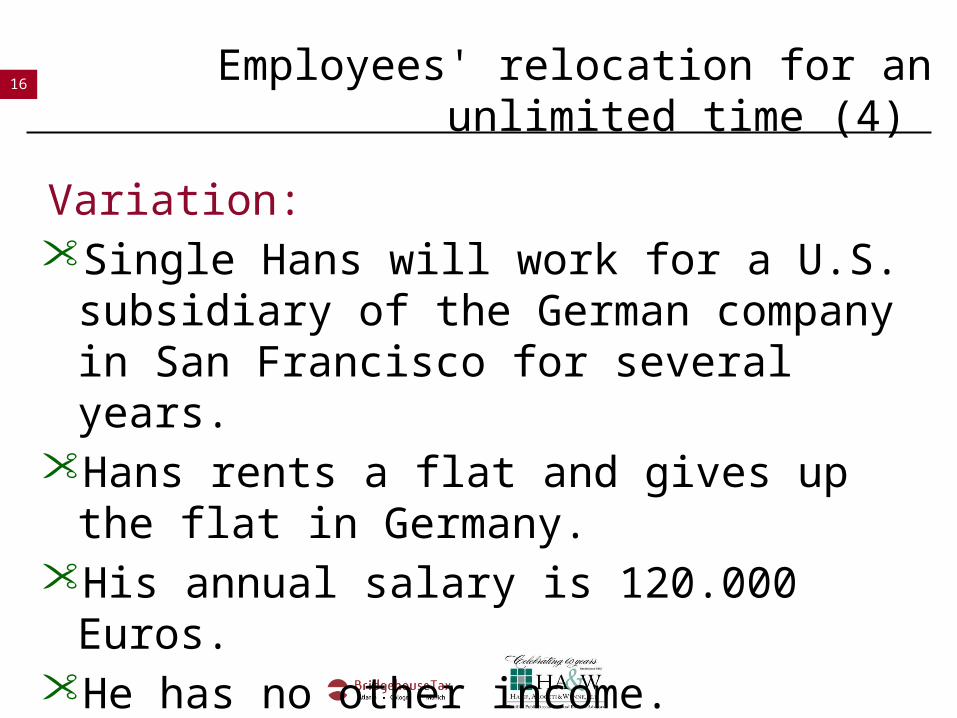

Variation:Single Hans will work for a U.S. subsidiary of

the German company in San Francisco for several years.

Hans rents a flat and gives up the flat in Germany.

His annual salary is 120.000 Euros. He has no other income.

17 Employees' relocation for an unlimited time (5)

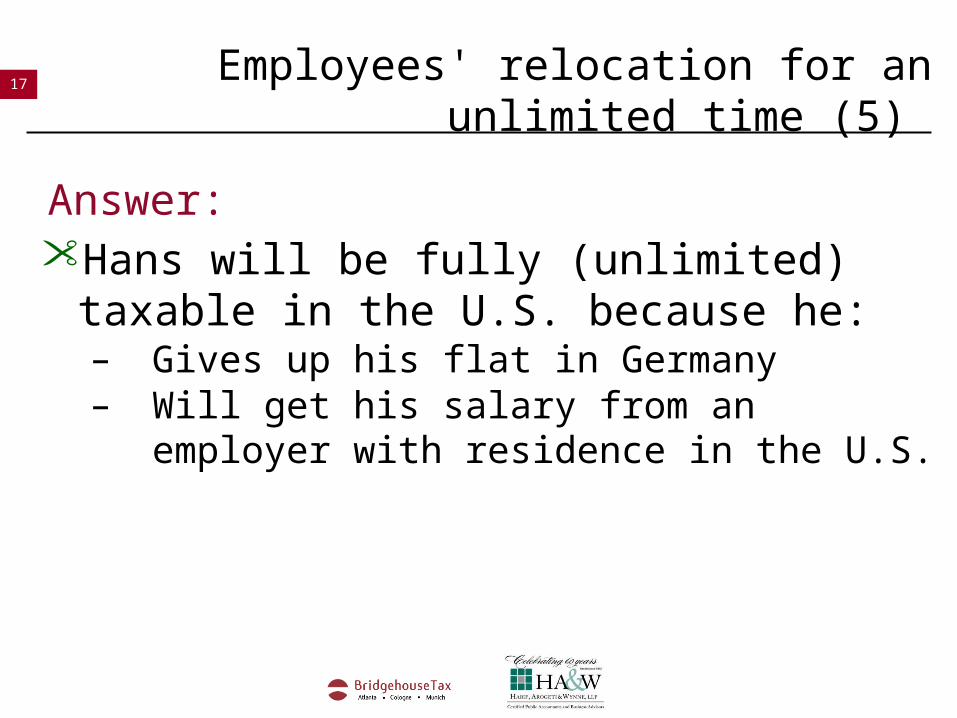

Answer:Hans will be fully (unlimited) taxable in the

U.S. because he:– Gives up his flat in Germany– Will get his salary from an employer with

residence in the U.S.

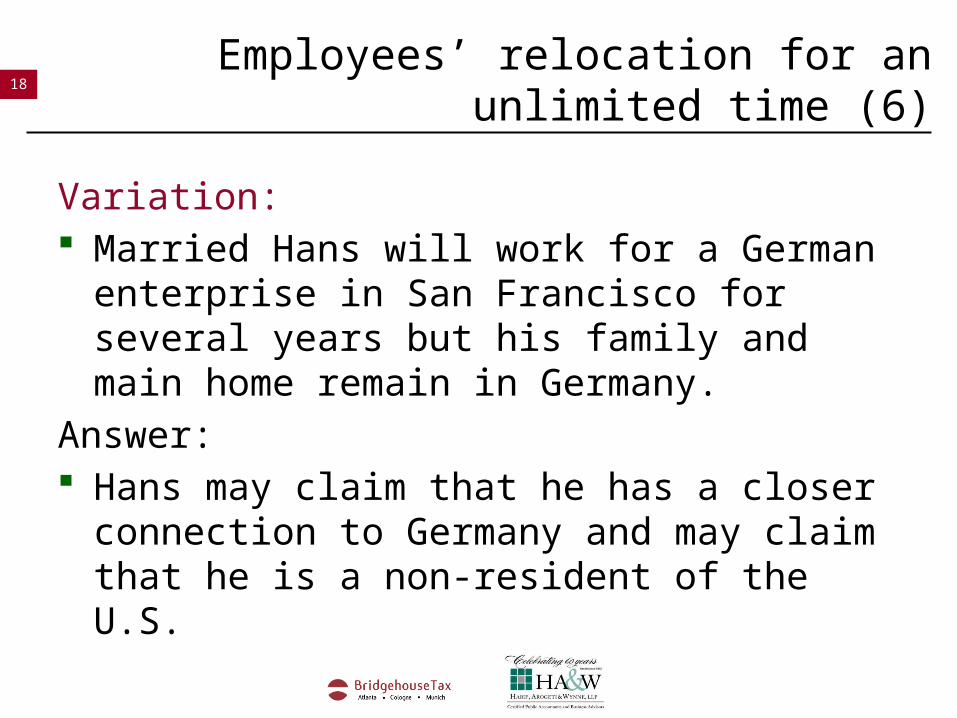

18 Employees’ relocation for an unlimited time (6)

Variation: Married Hans will work for a German enterprise

in San Francisco for several years but his family and main home remain in Germany.

Answer: Hans may claim that he has a closer connection

to Germany and may claim that he is a non-resident of the U.S.

19

INCOME TAX

Stock incentives

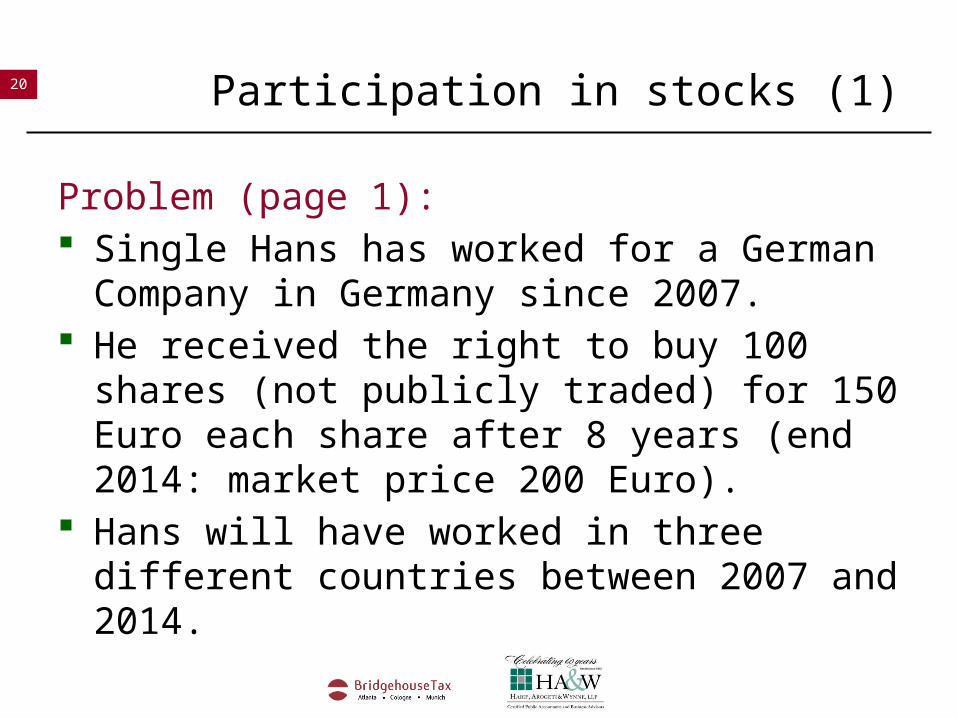

20 Participation in stocks (1)

Problem (page 1): Single Hans has worked for a German Company

in Germany since 2007. He received the right to buy 100 shares (not

publicly traded) for 150 Euro each share after 8 years (end 2014: market price 200 Euro).

Hans will have worked in three different countries between 2007 and 2014.

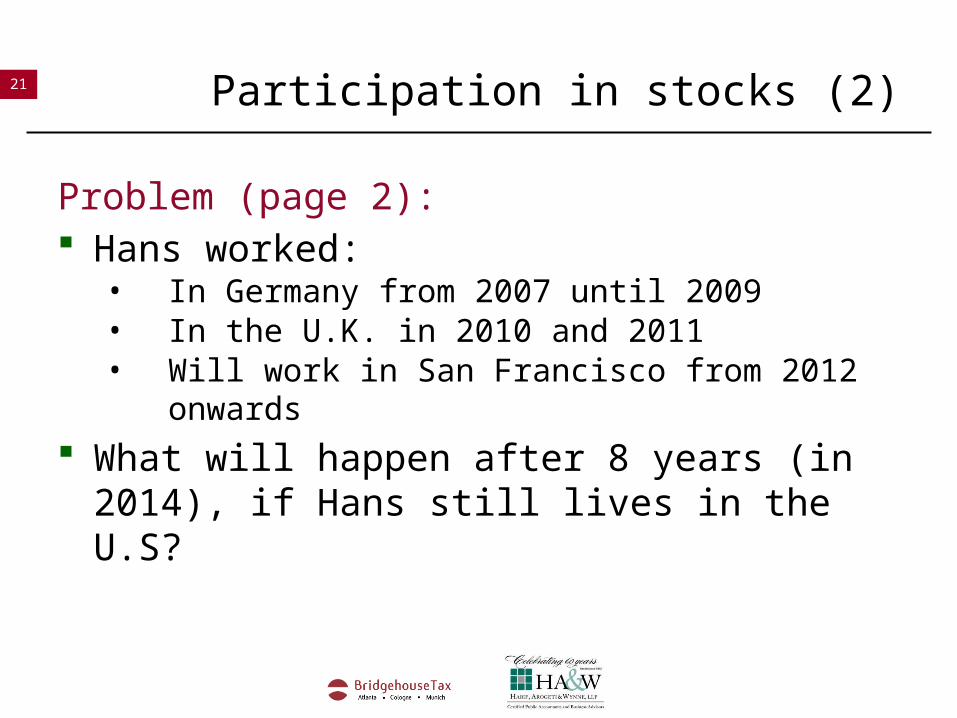

21 Participation in stocks (2)

Problem (page 2): Hans worked:

• In Germany from 2007 until 2009 • In the U.K. in 2010 and 2011• Will work in San Francisco from 2012 onwards

What will happen after 8 years (in 2014), if Hans still lives in the U.S?

22 Participation in stocks (3)

Answer: The benefit for Hans (difference between the

purchase price 150 and the market price 200) is subject to tax. The benefit (50*100) will be split pro rata over the time period 2007 to 2014.

That means (simplified): • Taxable in Germany 3/8• Taxable in the UK 2/8• Taxable in the U.S. 3/8

23

INCOME TAX

Compensation/severance payments

24 Compensation payment (1)

Problem: Single Hans (German citizen) has been working for

a German Company in San Francisco since 2005. • He leaves the Company in 2012. • He receives an additional payment. • He goes back to Germany

25 Compensation payment (2)

Challenges: Two countries will want to tax the payment

• U.S. (country of employment) • Germany (country of residence)

Considerations• What was the reason for the payment?• In which country is Hans a resident in the year in which

he receives the compensation?

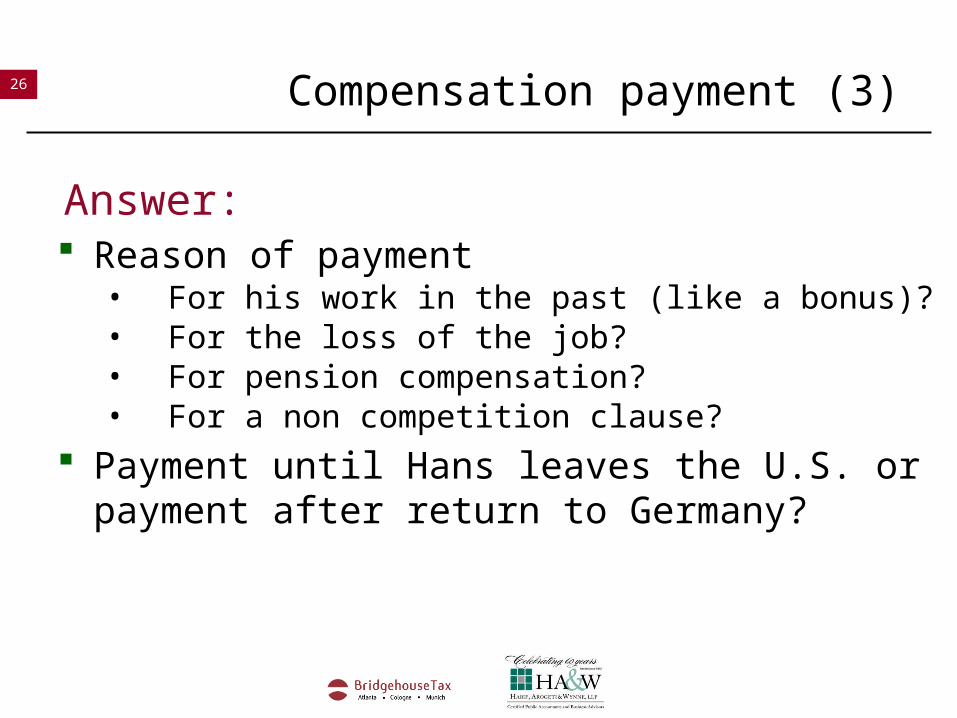

26 Compensation payment (3)

Answer: Reason of payment

• For his work in the past (like a bonus)?• For the loss of the job?• For pension compensation?• For a non competition clause?

Payment until Hans leaves the U.S. or payment after return to Germany?

27 Compensation payment (4)

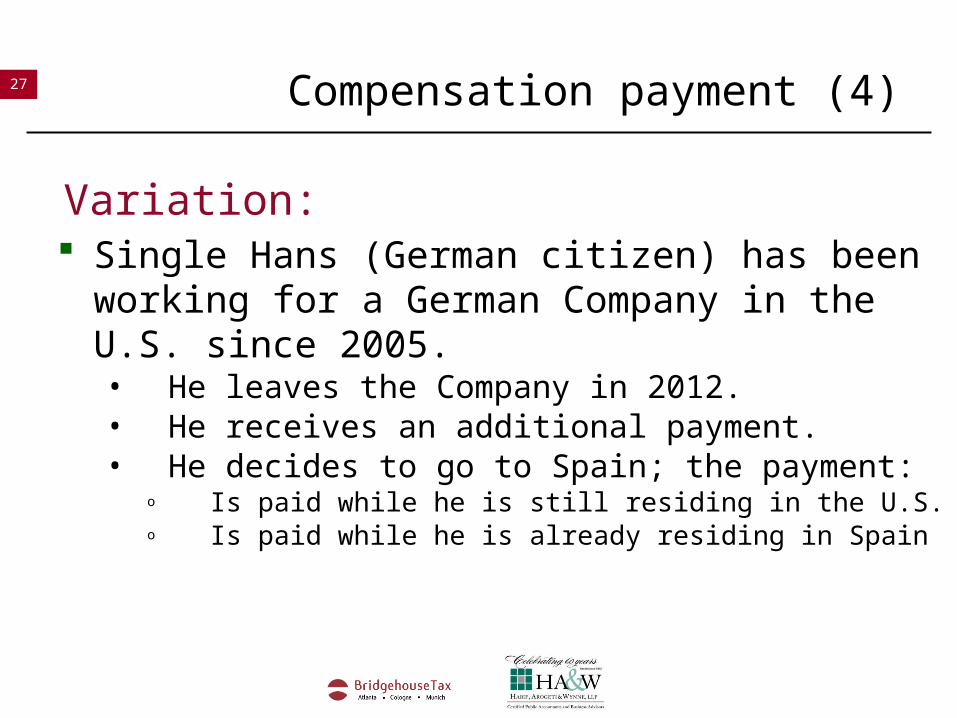

Variation: Single Hans (German citizen) has been working for

a German Company in the U.S. since 2005. • He leaves the Company in 2012. • He receives an additional payment. • He decides to go to Spain; the payment:

o Is paid while he is still residing in the U.S.o Is paid while he is already residing in Spain

28 Compensation payment (5)

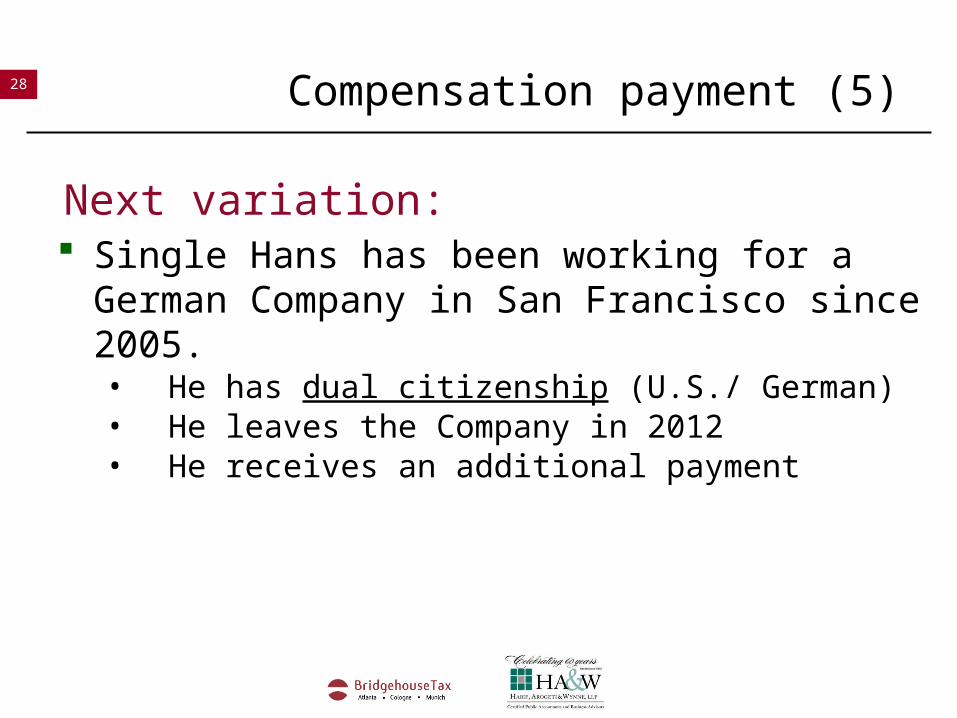

Next variation: Single Hans has been working for a German

Company in San Francisco since 2005. • He has dual citizenship (U.S./ German)• He leaves the Company in 2012 • He receives an additional payment

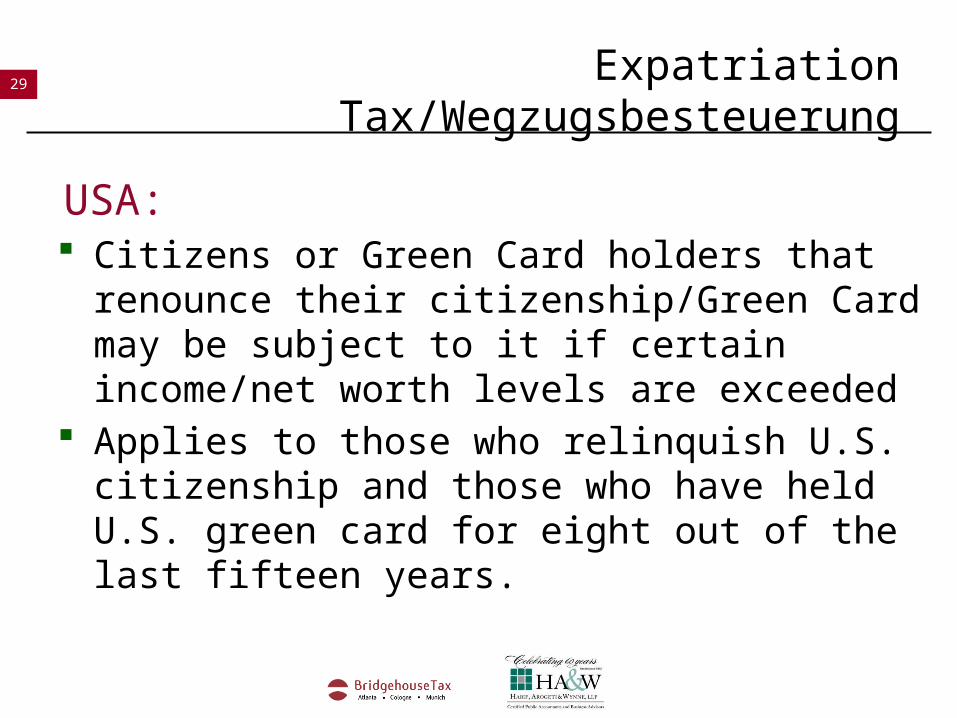

29 Expatriation Tax/Wegzugsbesteuerung

USA: Citizens or Green Card holders that renounce their

citizenship/Green Card may be subject to it if certain income/net worth levels are exceeded

Applies to those who relinquish U.S. citizenship and those who have held U.S. green card for eight out of the last fifteen years.

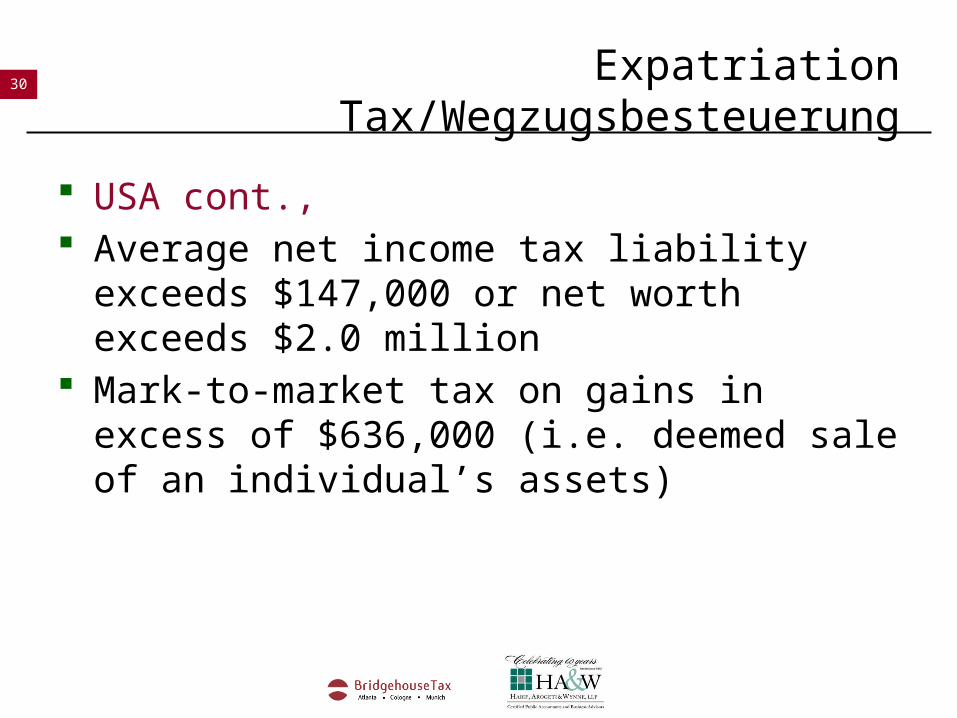

30 Expatriation Tax/Wegzugsbesteuerung

USA cont., Average net income tax liability exceeds

$147,000 or net worth exceeds $2.0 million Mark-to-market tax on gains in excess of

$636,000 (i.e. deemed sale of an individual’s assets)

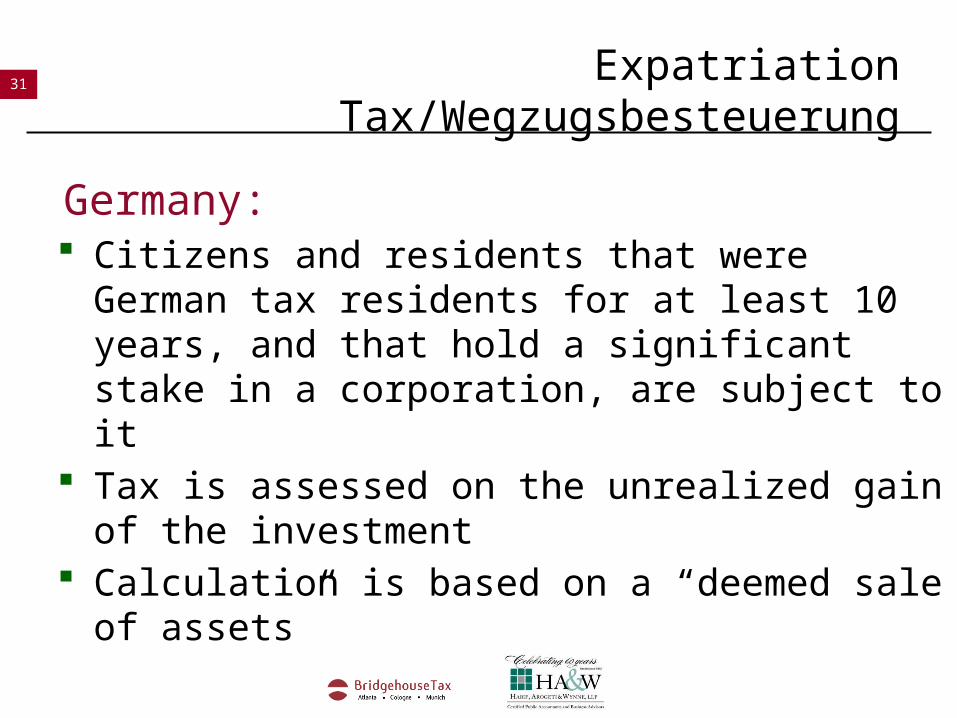

31 Expatriation Tax/Wegzugsbesteuerung

Germany: Citizens and residents that were German tax

residents for at least 10 years, and that hold a significant stake in a corporation, are subject to it

Tax is assessed on the unrealized gain of the investment

Calculation is based on a “deemed sale of assets”

32

GIFT/ INHERITANCE TAX

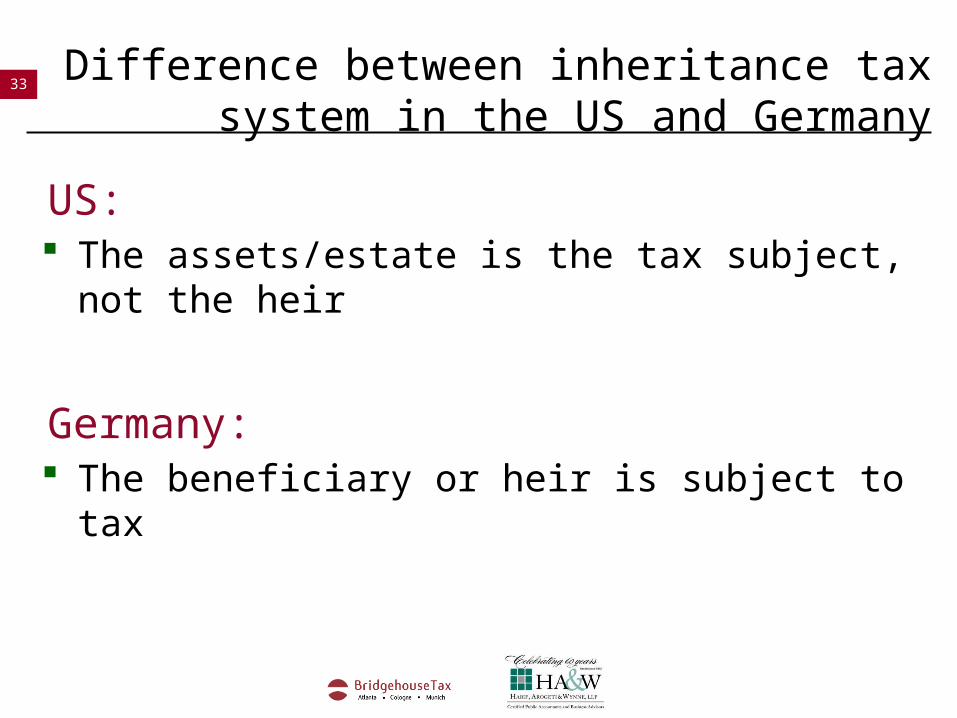

33Difference between inheritance tax system in

the US and Germany

US: The assets/estate is the tax subject, not the heir

Germany: The beneficiary or heir is subject to tax

34 Gift/Inheritance (1)

Problem (page 1): Hans (German/American citizen) has been living

with his wife in San Francisco for 30 years. In 2008, his mother Gerda (American citizen)

passed away in Los Angeles. The mother was the owner of four buildings in

Germany, which are rented to tenants. Two of these were gifted to Hans in 1990, one of these in 2002.

35 Gift/Inheritance (2)

Problem (page 2): The German CPA prepared all German tax

declarations but never informed Hans that he has to fulfill tax obligations in the U.S., too.

Some weeks after his mother, Gerda, died Hans has sought help of a US/ German law firm to prepare a will which considered US and German implications.

After thoroughly checking the case, the following issues needed to be discussed:

36 Gift/Inheritance (3)

Answer: What relief is available in the U.S. for not filing the

gift tax declarations? How is the rental income taxed going forward? Is it possible to claim a tax credit for prior years? How to avoid late penalties?

37 Inheritance (4)

Variation 1: Hans (German/ American citizen) has been living

with his wife in San Francisco for 30 years. In 2008 his mother, Gerda (German citizen), passed

away in Munich, Germany. She was the owner of four buildings in Germany, which are rented to tenants

She also owns a second home in San Francisco for the family.

Compare limited and unlimited tax liability

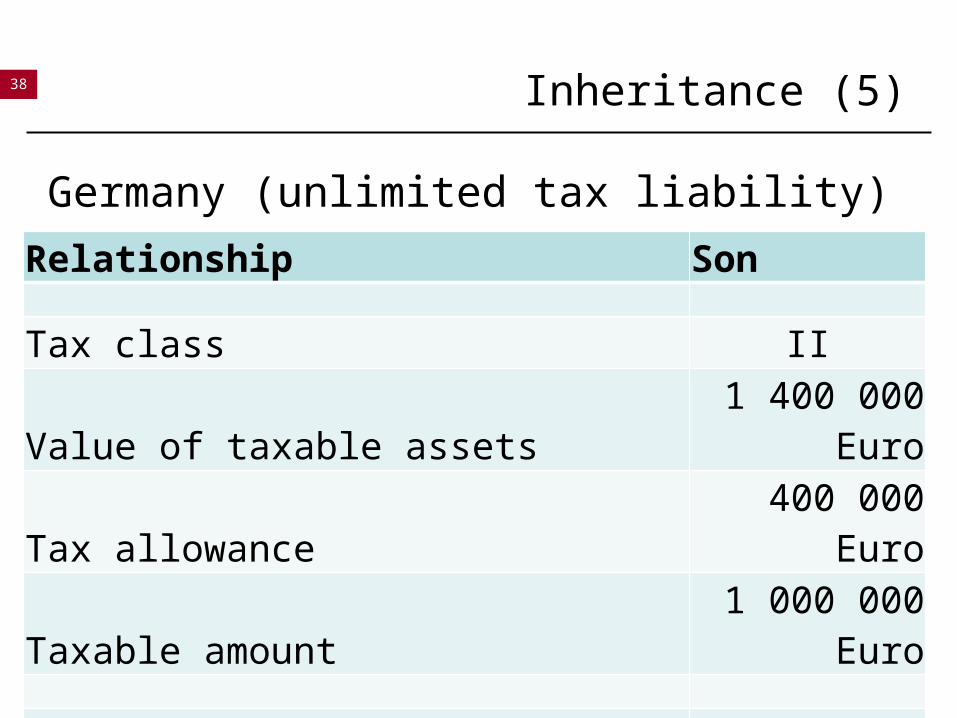

38 Inheritance (5)

Germany (unlimited tax liability)

Relationship Son

Tax class IIValue of taxable assets 1 400 000 EuroTax allowance 400 000 EuroTaxable amount 1 000 000 Euro

Payable inheritance tax (19%)(tax credit allowed for US estate taxes paid)

190 000 Euro

39 Inheritance (6)

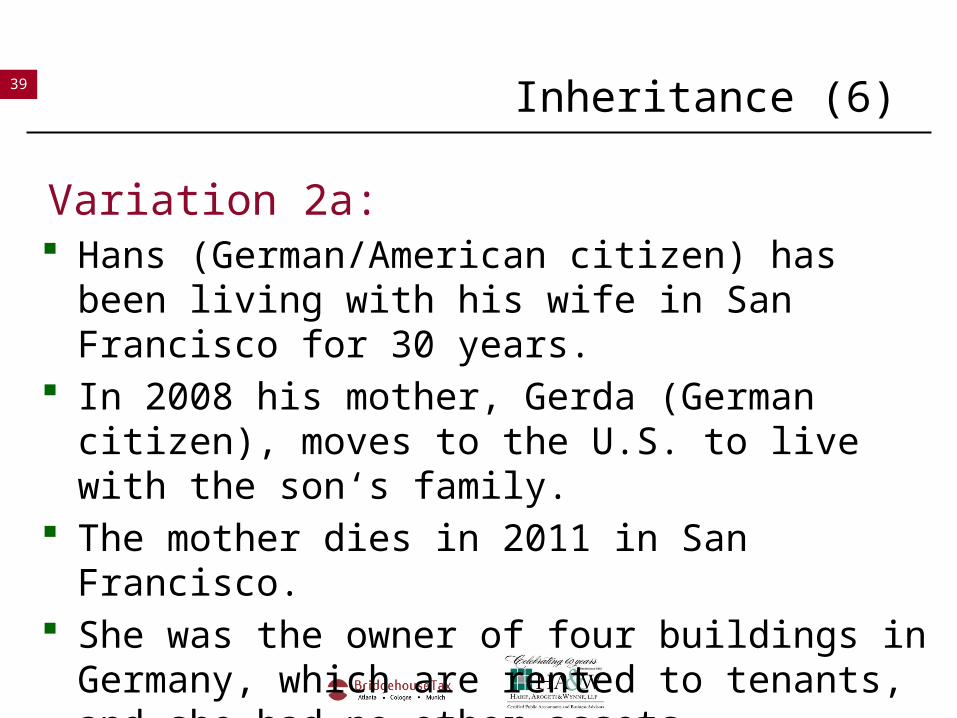

Variation 2a: Hans (German/American citizen) has been living

with his wife in San Francisco for 30 years. In 2008 his mother, Gerda (German citizen), moves

to the U.S. to live with the son‘s family. The mother dies in 2011 in San Francisco. She was the owner of four buildings in Germany,

which are rented to tenants, and she had no other assets.

40 Inheritance (7)

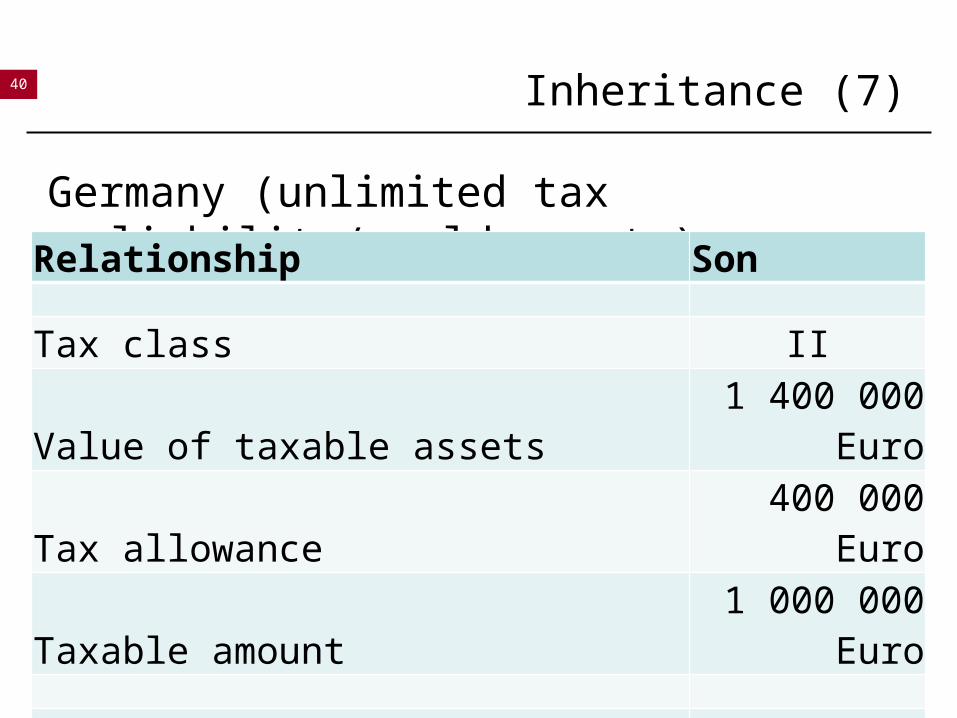

Germany (unlimited tax liability/world assets)

Relationship Son

Tax class IIValue of taxable assets 1 400 000 EuroTax allowance 400 000 EuroTaxable amount 1 000 000 Euro

Payable inheritance tax (19%) 190 000 Euro

41 Inheritance (8)

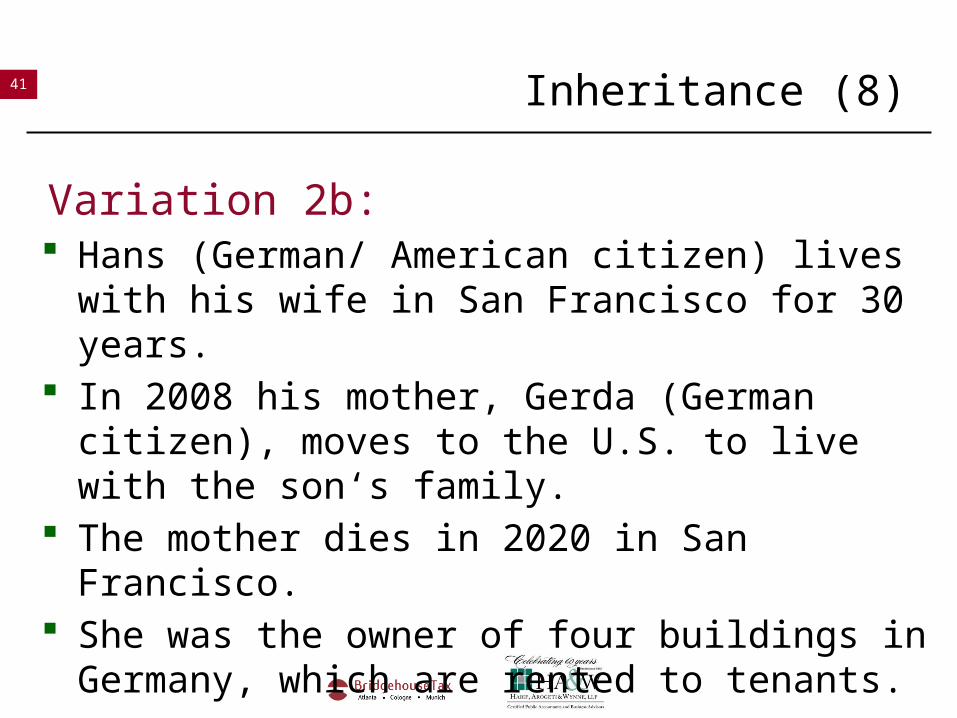

Variation 2b: Hans (German/ American citizen) lives with his wife

in San Francisco for 30 years. In 2008 his mother, Gerda (German citizen), moves

to the U.S. to live with the son‘s family. The mother dies in 2020 in San Francisco. She was the owner of four buildings in Germany,

which are rented to tenants.

42 Inheritance (9)

Germany (limited tax liability/only German assets)

Relationship Son

Tax class IIValue of taxable assets 1 400 000 EuroTax allowance 2 000 EuroTaxable amount 1.398 000 Euro

Payable inheritance tax (19%)(will be credited in the U.S.) 265 620 Euro

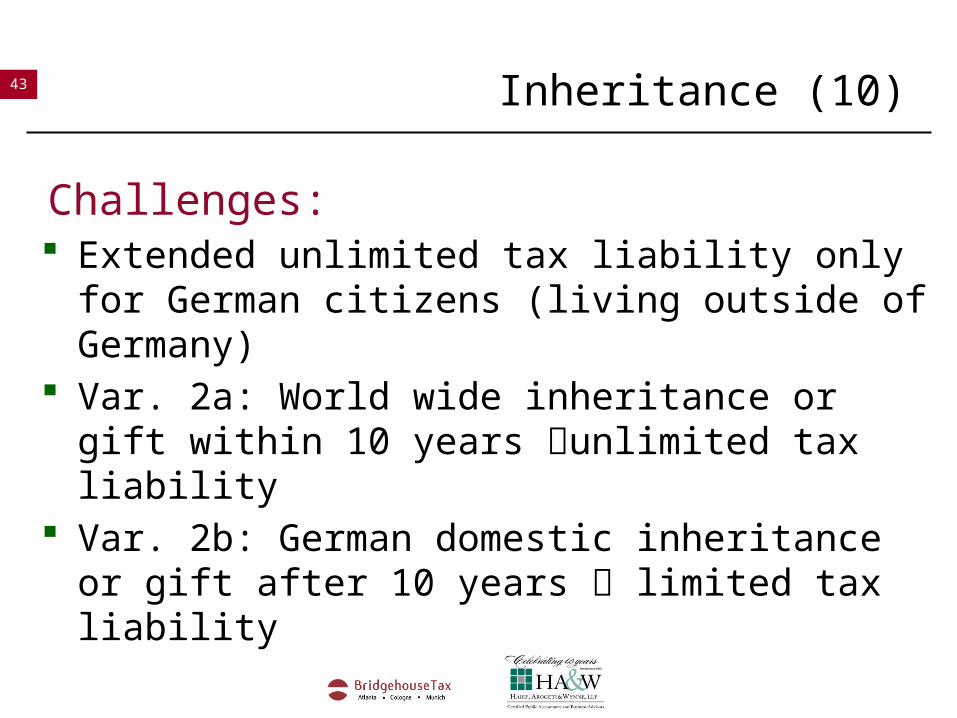

43 Inheritance (10)

Challenges: Extended unlimited tax liability only for German

citizens (living outside of Germany) Var. 2a: World wide inheritance or gift within 10

years unlimited tax liability Var. 2b: German domestic inheritance or gift after 10

years limited tax liability

44 ContactBridgehouseTax AtlantaThe Proscenium, Suite 17751170 Peachtree Street, NEAtlanta, GA 30309-7675U.S.A.www.bridgehousetax.us

Jörg KemkesT +1 404 898 9122F +1 404 506 9930E [email protected]

Habif, Arogeti & Wynne LLP5 Concourse Parkway, Suite 1000Atlanta, GA 30328U.S.A.www.hawcpa.com

Alex KnightT +1 404 898 7428M +1 770 367 3178E [email protected]

Kristin MäckelT +1 770 353 8606M +1 678 793 4204E [email protected]

![TAXATION OF EXPATRIATES - B.D Jokhakar & Co. · Taxation of Expatriates TABLE OF CONTENTS Sr. No. Topic Page number ... (10CC)] Expatriates coming into India and working in various](https://img.pdfslide.us/doc/110x75/5b3ffd287f8b9aff118cca0c/taxation-of-expatriates-bd-jokhakar-co-taxation-of-expatriates-table-of.jpg)

![The Redwood gazette. (Redwood Falls, Minn.), 1925-06-17, [p ]. · 2019-10-27 · THE REDWOOD GAZETTE, REDWOOD FALLS, MINNESOTA The Redwood Gazette prints wedding an- nouncements or](https://img.pdfslide.us/doc/110x75/5fa04f2ead664330d06ddb4a/the-redwood-gazette-redwood-falls-minn-1925-06-17-p-2019-10-27-the.jpg)