Embed Size (px)

Citation preview

GHIFinancial overview, trends and opportunities

29 March 2017

Market overview

3© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

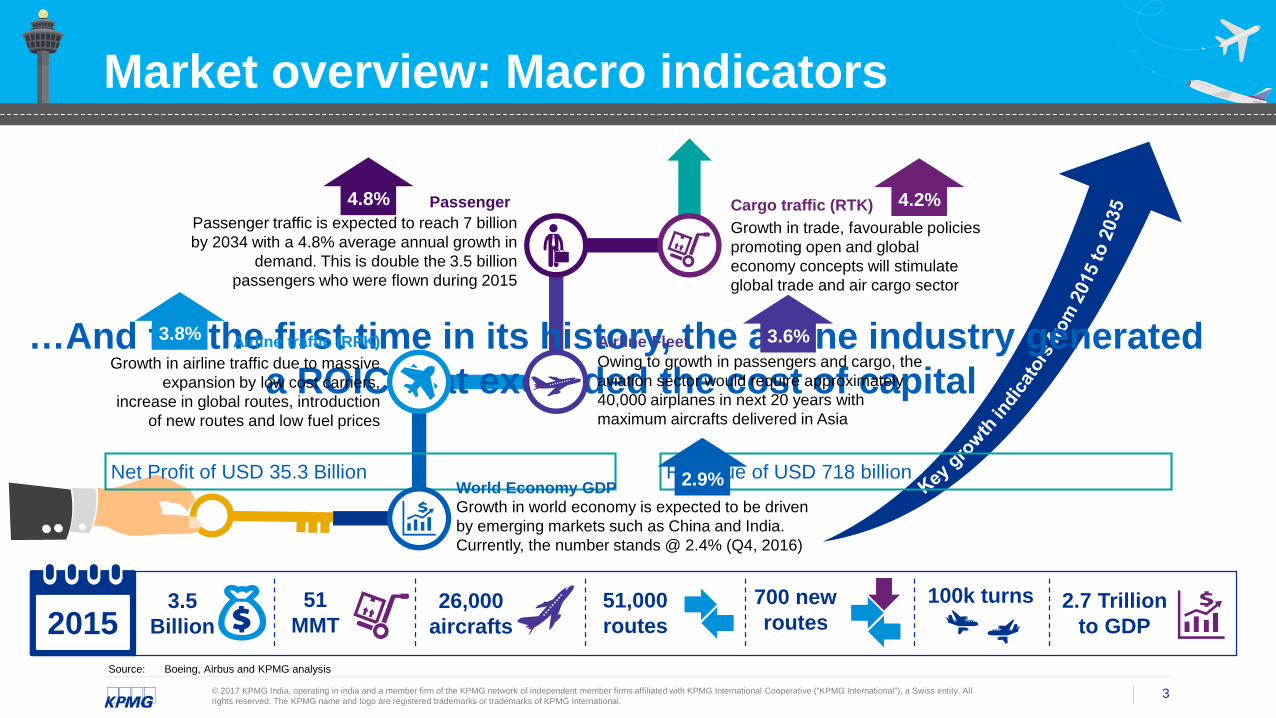

Market overview: Macro indicators

Source: Boeing, Airbus and KPMG analysis

…And for the first time in its history, the airline industry generated a ROIC that exceeded the cost of capital

Net Profit of USD 35.3 Billion Revenue of USD 718 billion

Passenger4.8%Passenger traffic is expected to reach 7 billion by 2034 with a 4.8% average annual growth in

demand. This is double the 3.5 billion passengers who were flown during 2015

Cargo traffic (RTK) 4.2%Growth in trade, favourable policies promoting open and global economy concepts will stimulate global trade and air cargo sector

Airline traffic (RPK)3.8%Growth in airline traffic due to massive

expansion by low cost carriers, increase in global routes, introduction

of new routes and low fuel prices

Airline Fleet 3.6%Owing to growth in passengers and cargo, the aviation sector would require approximately 40,000 airplanes in next 20 years with maximum aircrafts delivered in Asia

2.9%World Economy GDPGrowth in world economy is expected to be driven by emerging markets such as China and India. Currently, the number stands @ 2.4% (Q4, 2016)

20153.5

Billion51

MMT26,000

aircrafts51,000 routes

700 new routes

100k turns 2.7 Trillion to GDP

4© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

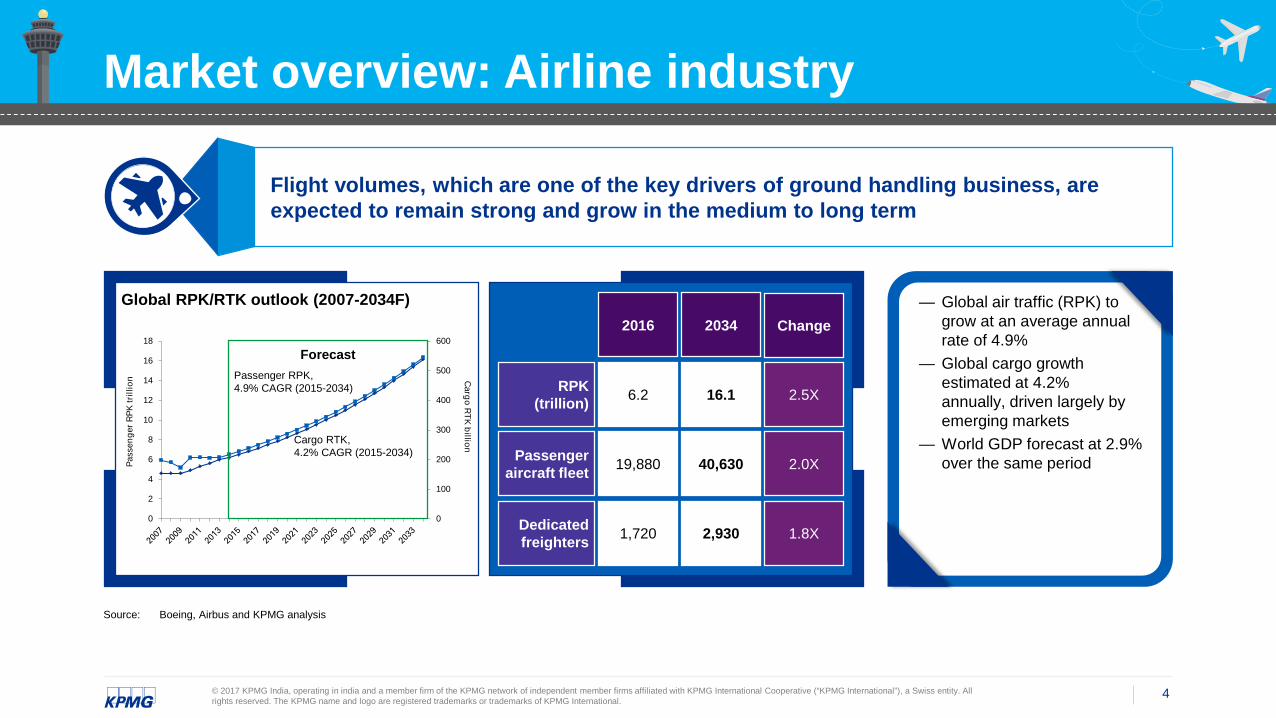

Market overview: Airline industry

— Global air traffic (RPK) to grow at an average annual rate of 4.9%

— Global cargo growth estimated at 4.2% annually, driven largely by emerging markets

— World GDP forecast at 2.9% over the same period

Flight volumes, which are one of the key drivers of ground handling business, are expected to remain strong and grow in the medium to long term

Global RPK/RTK outlook (2007-2034F)

0

100

200

300

400

500

600

0

2

4

6

8

10

12

14

16

18

Cargo R

TK billion

Pass

enge

r RPK

trill

ion

ForecastPassenger RPK,4.9% CAGR (2015-2034)

Cargo RTK,4.2% CAGR (2015-2034)

2016 2034 Change

RPK (trillion)

Passenger aircraft fleet

Dedicated freighters

6.2 16.1 2.5X

19,880 40,630 2.0X

1,720 2,930 1.8X

Source: Boeing, Airbus and KPMG analysis

5© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

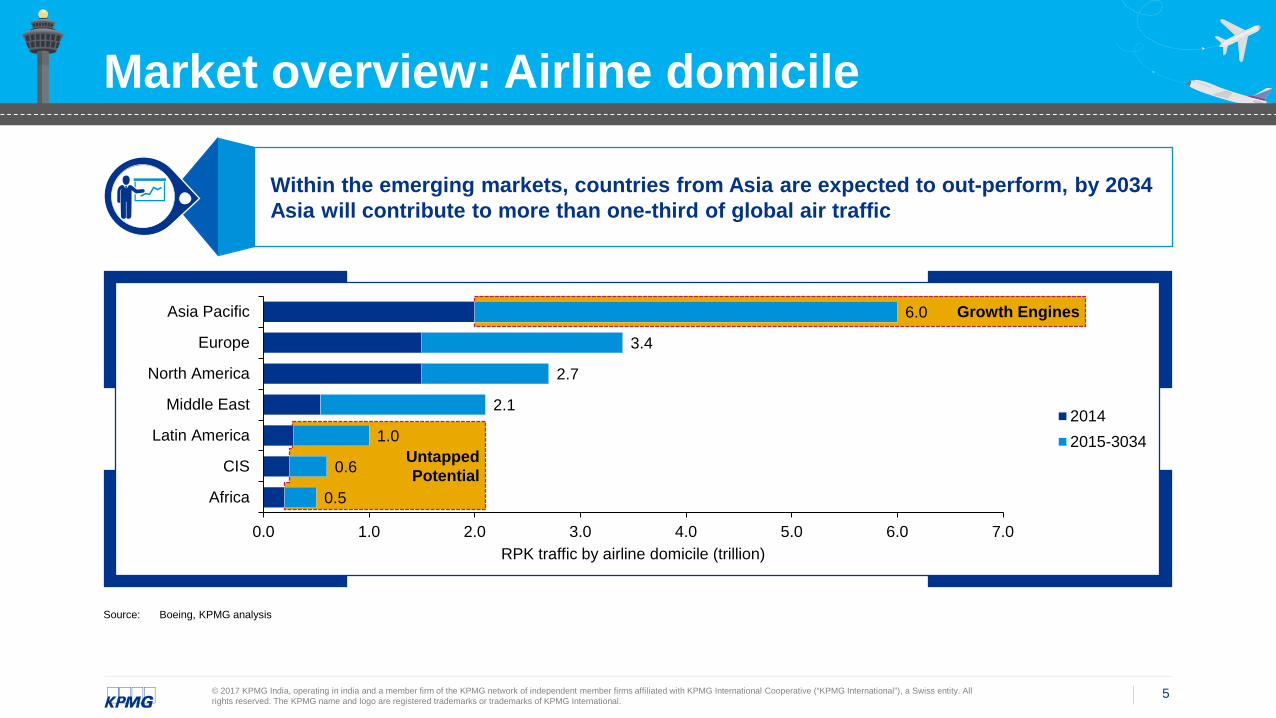

Market overview: Airline domicile

Within the emerging markets, countries from Asia are expected to out-perform, by 2034 Asia will contribute to more than one-third of global air traffic

Source: Boeing, KPMG analysis

Growth Engines

UntappedPotential

0.5

0.6

1.0

2.1

2.7

3.4

6.0

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

Africa

CIS

Latin America

Middle East

North America

Europe

Asia Pacific

RPK traffic by airline domicile (trillion)

20142015-3034

6© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

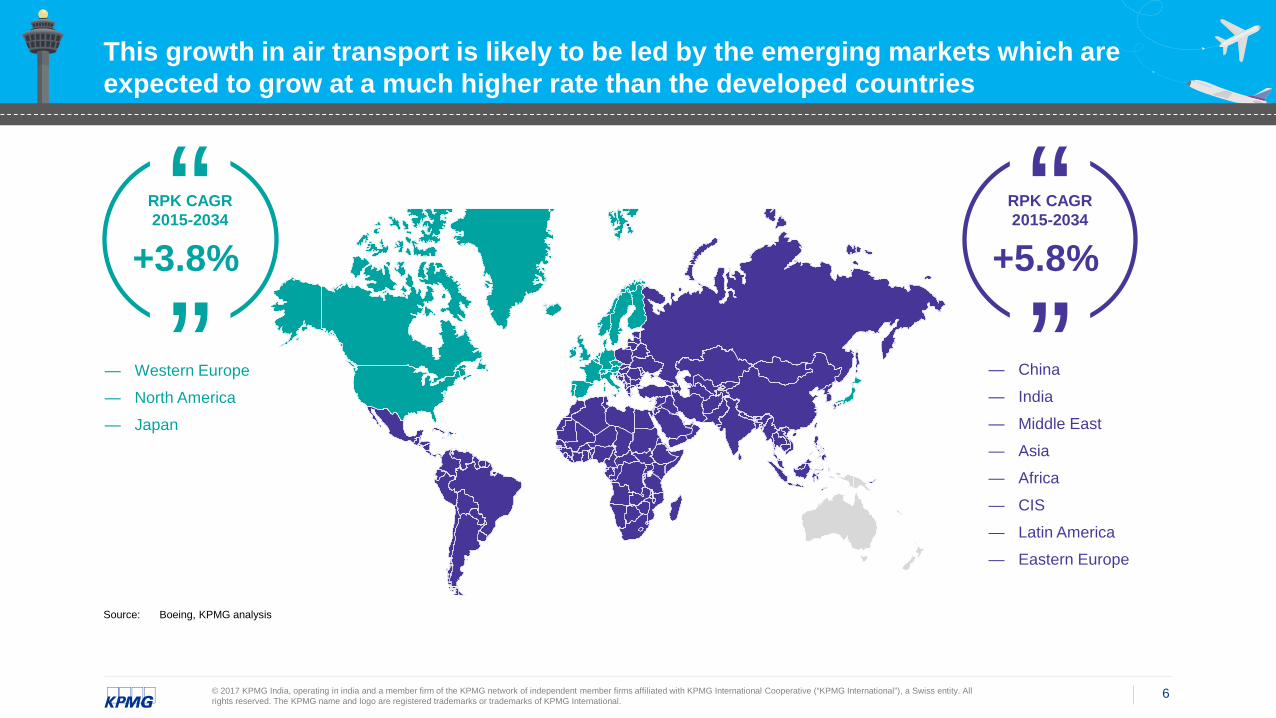

This growth in air transport is likely to be led by the emerging markets which are expected to grow at a much higher rate than the developed countries

““RPK CAGR2015-2034

+3.8%““RPK CAGR

2015-2034

+5.8%

— Western Europe

— North America

— Japan

— China

— India

— Middle East

— Asia

— Africa

— CIS

— Latin America

— Eastern Europe

Source: Boeing, KPMG analysis

7© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

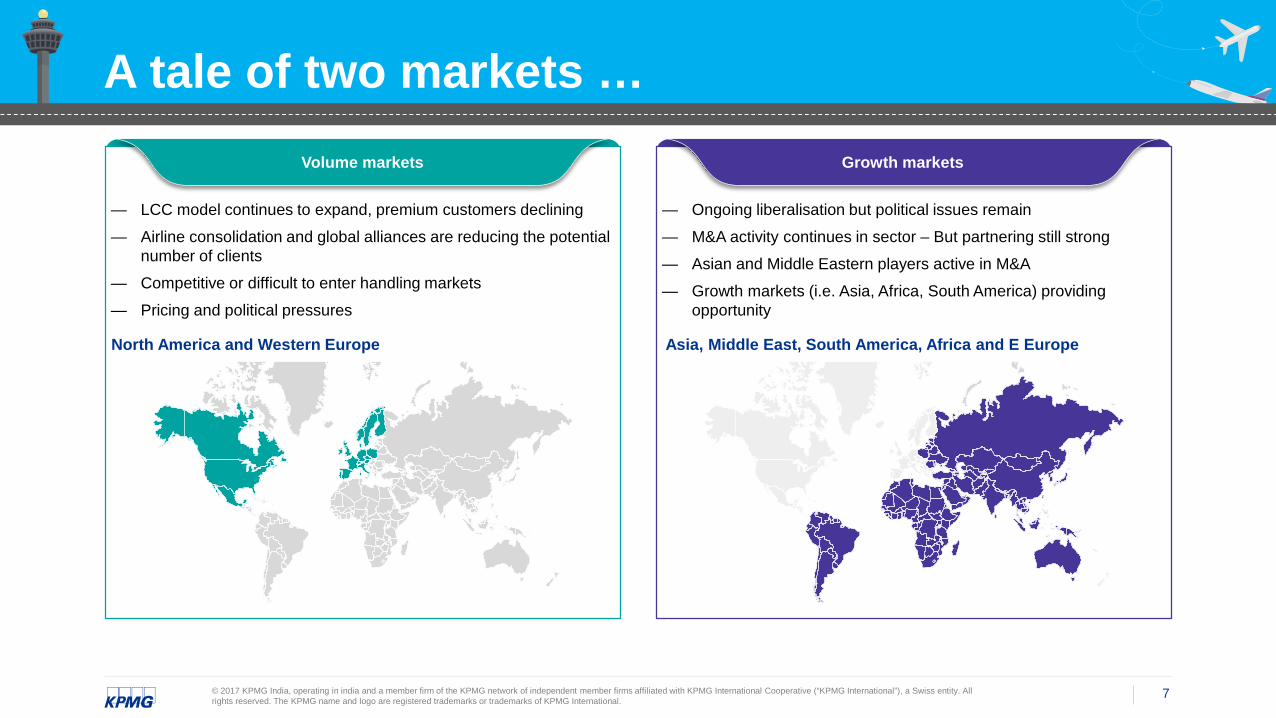

A tale of two markets …

— LCC model continues to expand, premium customers declining

— Airline consolidation and global alliances are reducing the potential number of clients

— Competitive or difficult to enter handling markets

— Pricing and political pressures

— Ongoing liberalisation but political issues remain

— M&A activity continues in sector – But partnering still strong

— Asian and Middle Eastern players active in M&A

— Growth markets (i.e. Asia, Africa, South America) providing opportunity

Volume markets Growth markets

North America and Western Europe Asia, Middle East, South America, Africa and E Europe

8© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

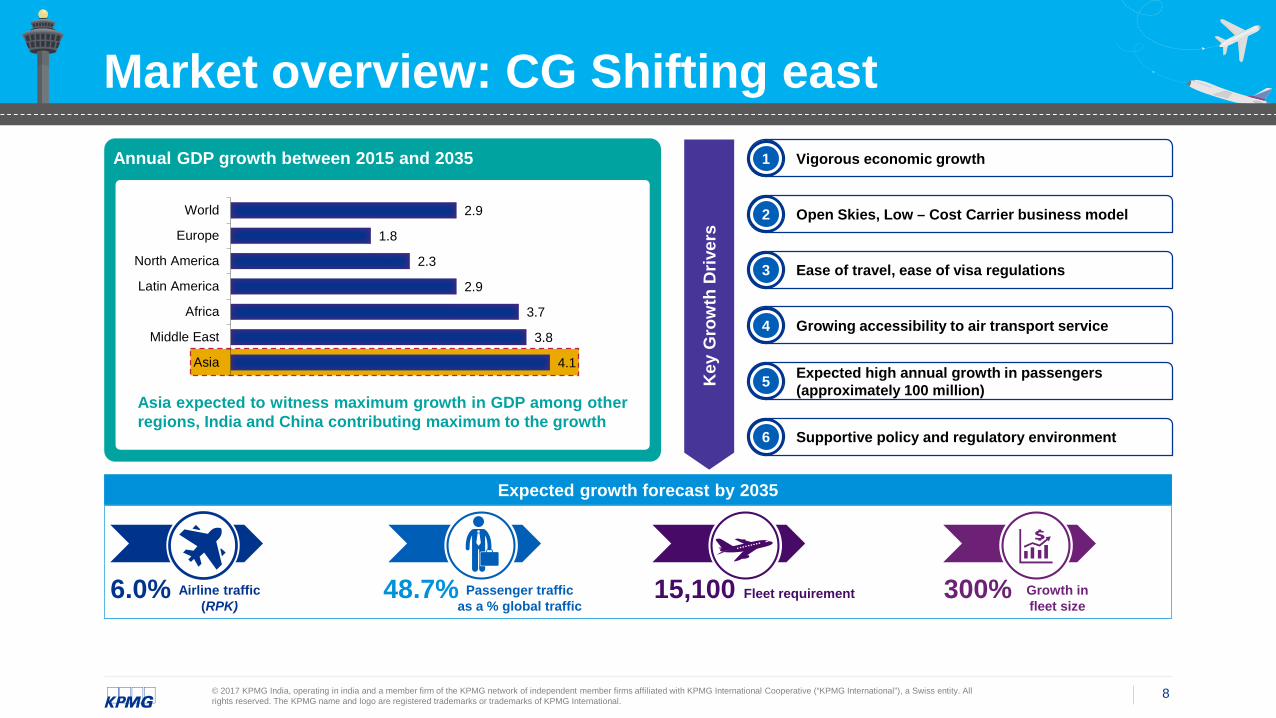

Market overview: CG Shifting eastAnnual GDP growth between 2015 and 2035

4.1

3.8

3.7

2.9

2.3

1.8

2.9

Asia

Middle East

Africa

Latin America

North America

Europe

World

Asia expected to witness maximum growth in GDP among otherregions, India and China contributing maximum to the growth

Vigorous economic growth1

Key

Gro

wth

Driv

ers

Open Skies, Low – Cost Carrier business model2

Ease of travel, ease of visa regulations3

Growing accessibility to air transport service4

Expected high annual growth in passengers (approximately 100 million)5

Supportive policy and regulatory environment6

Expected growth forecast by 2035

Airline traffic (RPK)

Passenger traffic as a % global traffic

Fleet requirement Growth in fleet size

6.0% 48.7% 15,100 300%

9© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

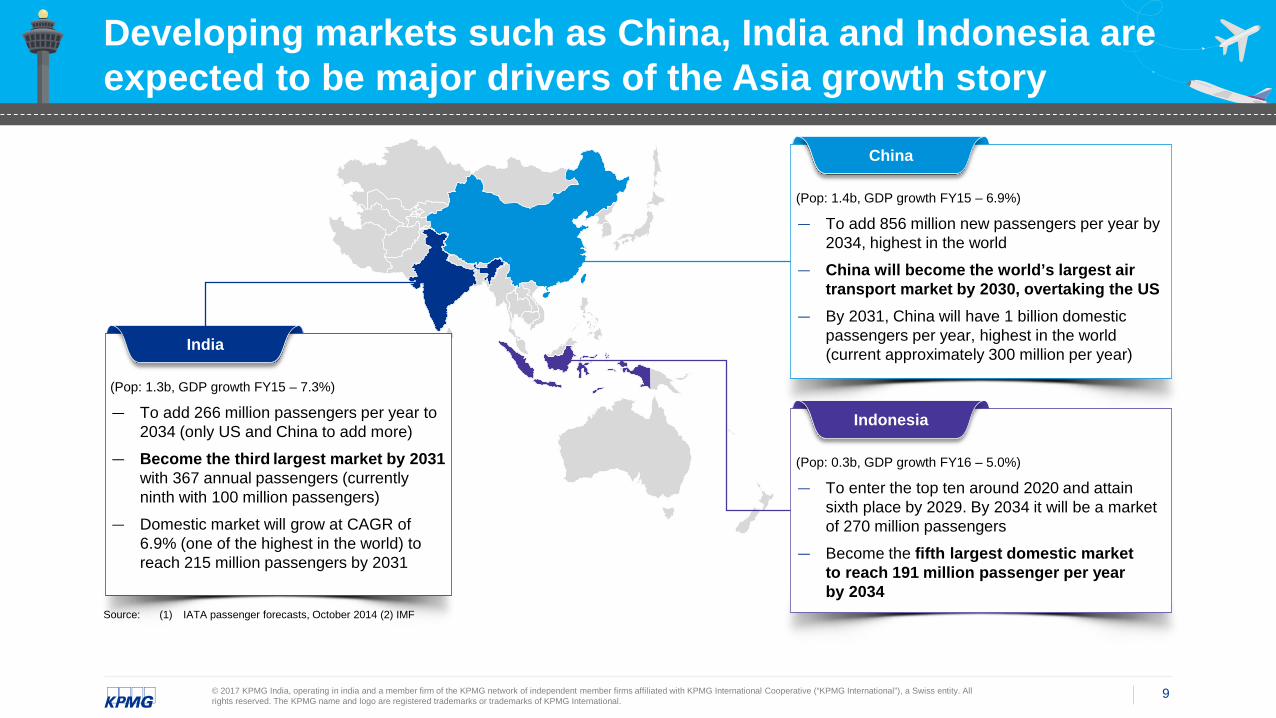

Developing markets such as China, India and Indonesia are expected to be major drivers of the Asia growth story

(Pop: 1.3b, GDP growth FY15 – 7.3%)

— To add 266 million passengers per year to 2034 (only US and China to add more)

— Become the third largest market by 2031with 367 annual passengers (currently ninth with 100 million passengers)

— Domestic market will grow at CAGR of 6.9% (one of the highest in the world) to reach 215 million passengers by 2031

India

(Pop: 1.4b, GDP growth FY15 – 6.9%)

— To add 856 million new passengers per year by 2034, highest in the world

— China will become the world’s largest air transport market by 2030, overtaking the US

— By 2031, China will have 1 billion domestic passengers per year, highest in the world (current approximately 300 million per year)

China

(Pop: 0.3b, GDP growth FY16 – 5.0%)

— To enter the top ten around 2020 and attain sixth place by 2029. By 2034 it will be a market of 270 million passengers

— Become the fifth largest domestic market to reach 191 million passenger per year by 2034

Indonesia

Source: (1) IATA passenger forecasts, October 2014 (2) IMF

10© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

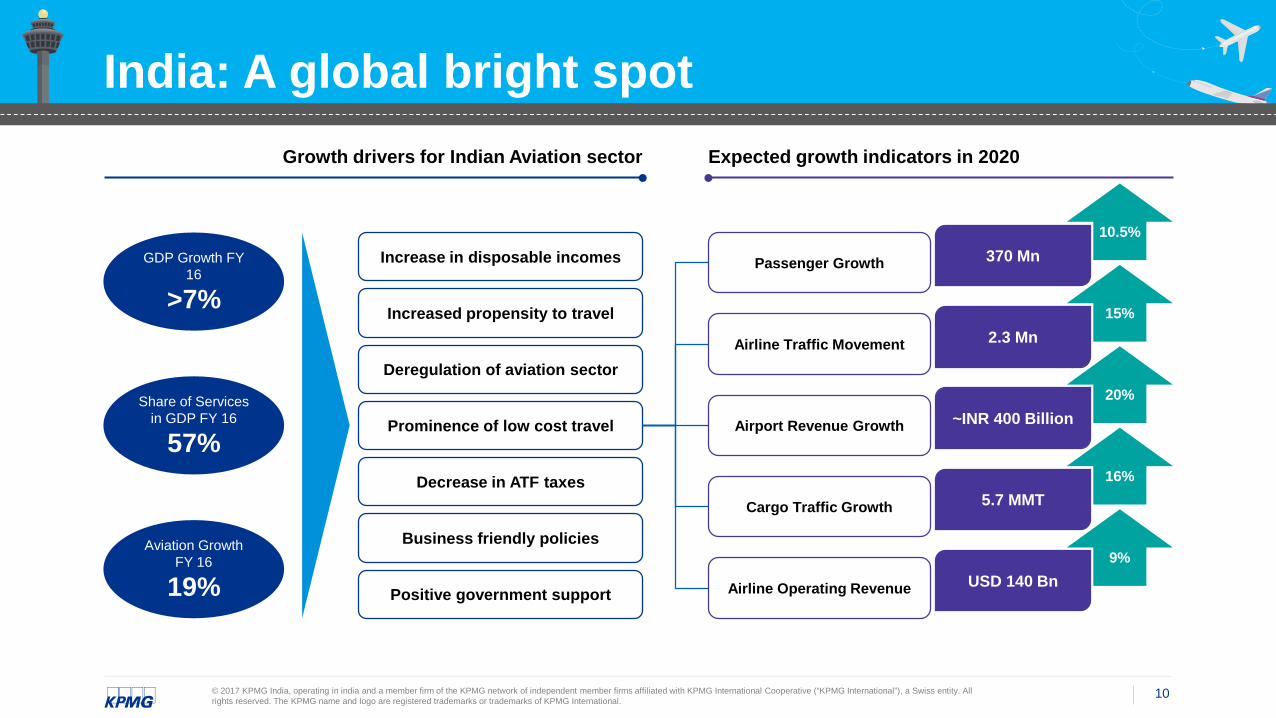

India: A global bright spot

370 Mn10.5%

5.7 MMT16%

~INR 400 Billion20%

2.3 Mn15%

USD 140 Bn9%

Passenger Growth

Cargo Traffic Growth

Airport Revenue Growth

Airline Traffic Movement

Airline Operating Revenue

Increase in disposable incomes

Increased propensity to travel

Deregulation of aviation sector

Prominence of low cost travel

Decrease in ATF taxes

Business friendly policies

Positive government support

GDP Growth FY 16

>7%

Share of Services in GDP FY 16

57%

Aviation Growth FY 16

19%

Growth drivers for Indian Aviation sector Expected growth indicators in 2020

11© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

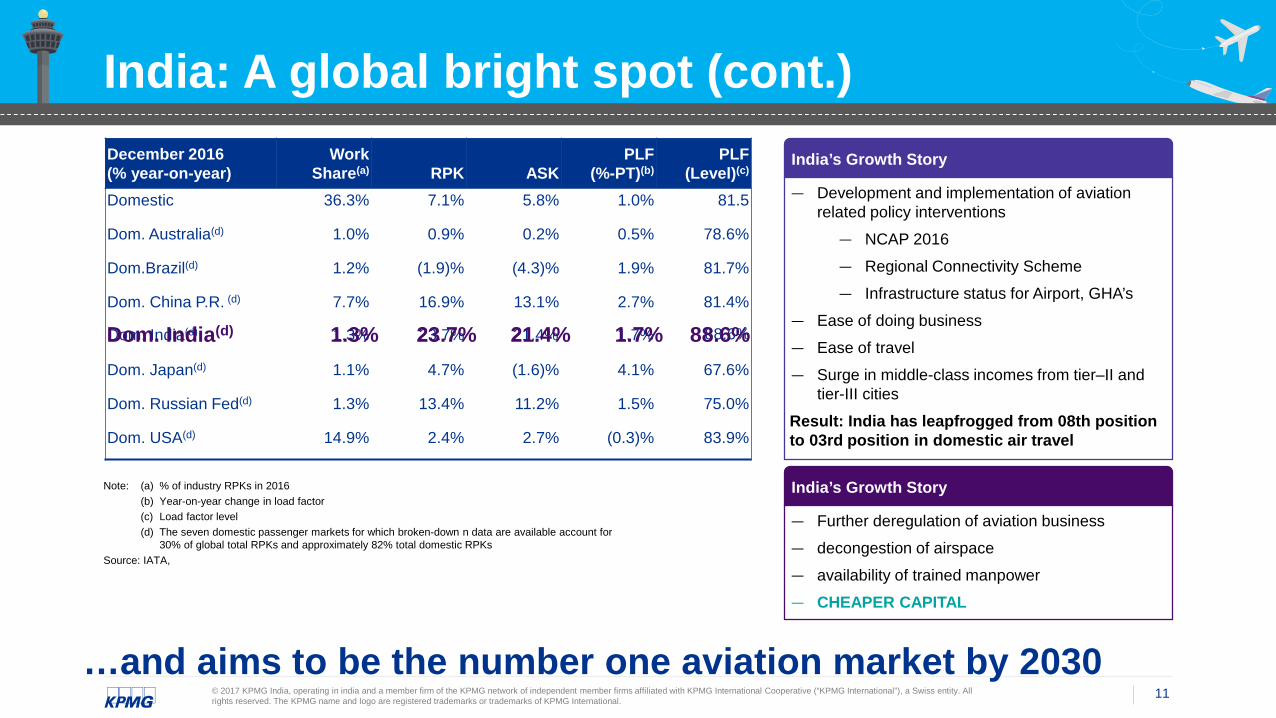

December 2016(% year-on-year)

WorkShare(a) RPK ASK

PLF(%-PT)(b)

PLF(Level)(c)

Domestic 36.3% 7.1% 5.8% 1.0% 81.5

Dom. Australia(d) 1.0% 0.9% 0.2% 0.5% 78.6%

Dom.Brazil(d) 1.2% (1.9)% (4.3)% 1.9% 81.7%

Dom. China P.R. (d) 7.7% 16.9% 13.1% 2.7% 81.4%

Dom. Japan(d) 1.1% 4.7% (1.6)% 4.1% 67.6%

Dom. Russian Fed(d) 1.3% 13.4% 11.2% 1.5% 75.0%

Dom. USA(d) 14.9% 2.4% 2.7% (0.3)% 83.9%

India: A global bright spot (cont.)India’s Growth Story

— Development and implementation of aviation related policy interventions

— NCAP 2016

— Regional Connectivity Scheme

— Infrastructure status for Airport, GHA’s

— Ease of doing business

— Ease of travel

— Surge in middle-class incomes from tier–II and tier-III cities

Result: India has leapfrogged from 08th position to 03rd position in domestic air travel

India’s Growth Story

— Further deregulation of aviation business

— decongestion of airspace

— availability of trained manpower

— CHEAPER CAPITAL

Note: (a) % of industry RPKs in 2016(b) Year-on-year change in load factor(c) Load factor level(d) The seven domestic passenger markets for which broken-down n data are available account for

30% of global total RPKs and approximately 82% total domestic RPKsSource: IATA,

Dom. India(d) 1.3% 23.7% 21.4% 1.7% 88.6%Dom. India(d) 1.3% 23.7% 21.4% 1.7% 88.6%

…and aims to be the number one aviation market by 2030

12© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

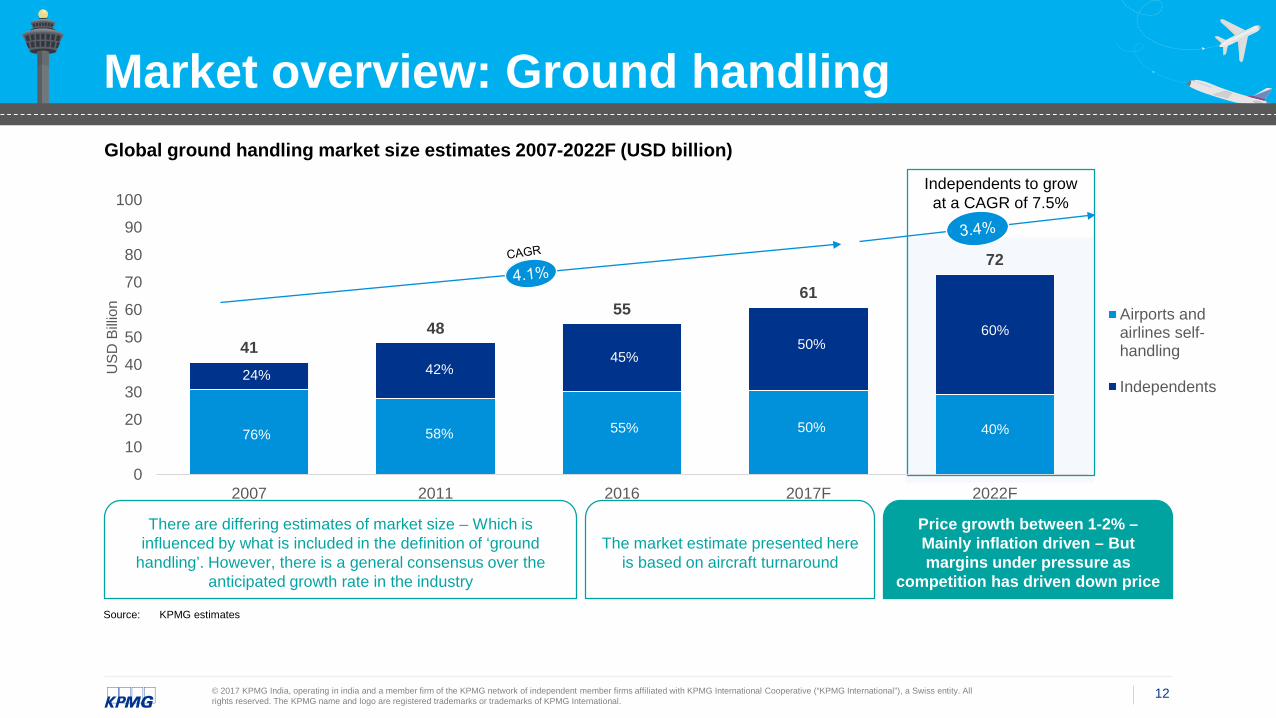

Market overview: Ground handlingGlobal ground handling market size estimates 2007-2022F (USD billion)

Independents to grow at a CAGR of 7.5%

Source: KPMG estimates

There are differing estimates of market size – Which is influenced by what is included in the definition of ‘ground

handling’. However, there is a general consensus over the anticipated growth rate in the industry

The market estimate presented here is based on aircraft turnaround

Price growth between 1-2% –Mainly inflation driven – But margins under pressure as

competition has driven down price

4148

5561

72

0

10

20

30

40

50

60

70

80

90

100

2007 2011 2016 2017F 2022F

USD

Billi

on Airports andairlines self-handling

Independents

60%

40%

50%

50%55%

45%42%

58%

24%

76%

13© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

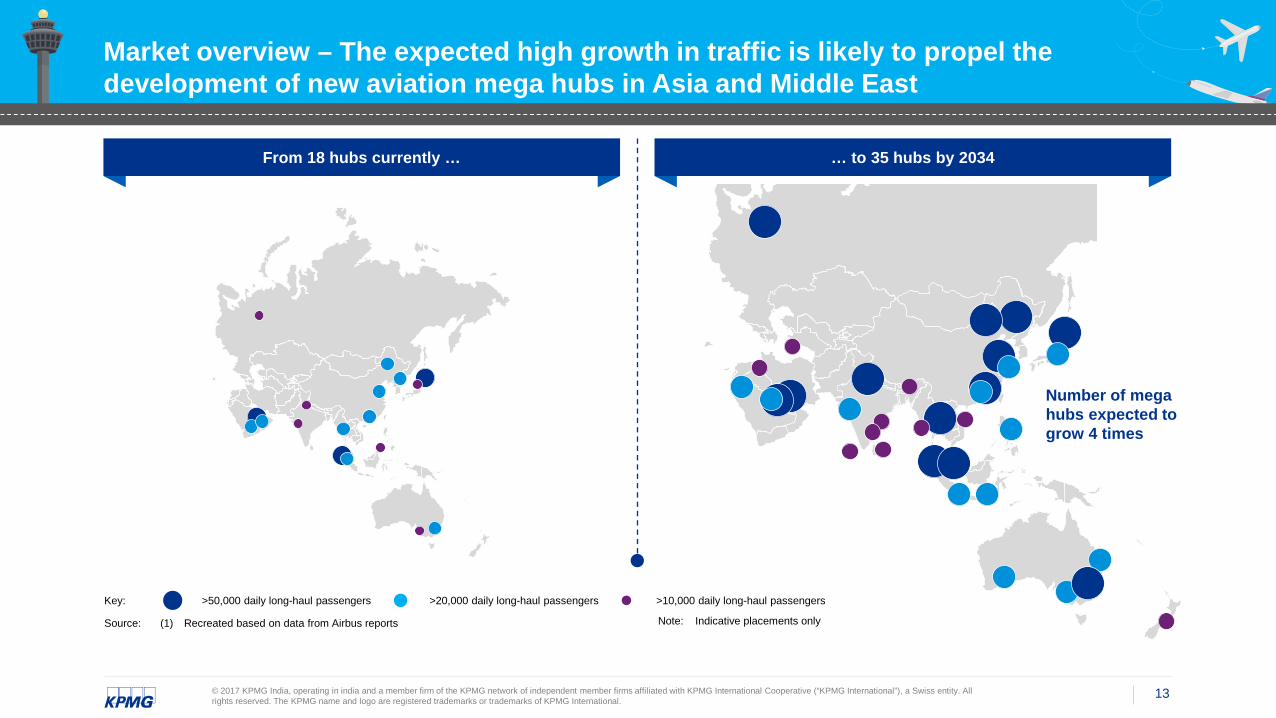

Market overview – The expected high growth in traffic is likely to propel the development of new aviation mega hubs in Asia and Middle East

Source: (1) Recreated based on data from Airbus reports Note: Indicative placements only

From 18 hubs currently …

>50,000 daily long-haul passengersKey: >20,000 daily long-haul passengers >10,000 daily long-haul passengers

Number of mega hubs expected to grow 4 times

… to 35 hubs by 2034

14© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

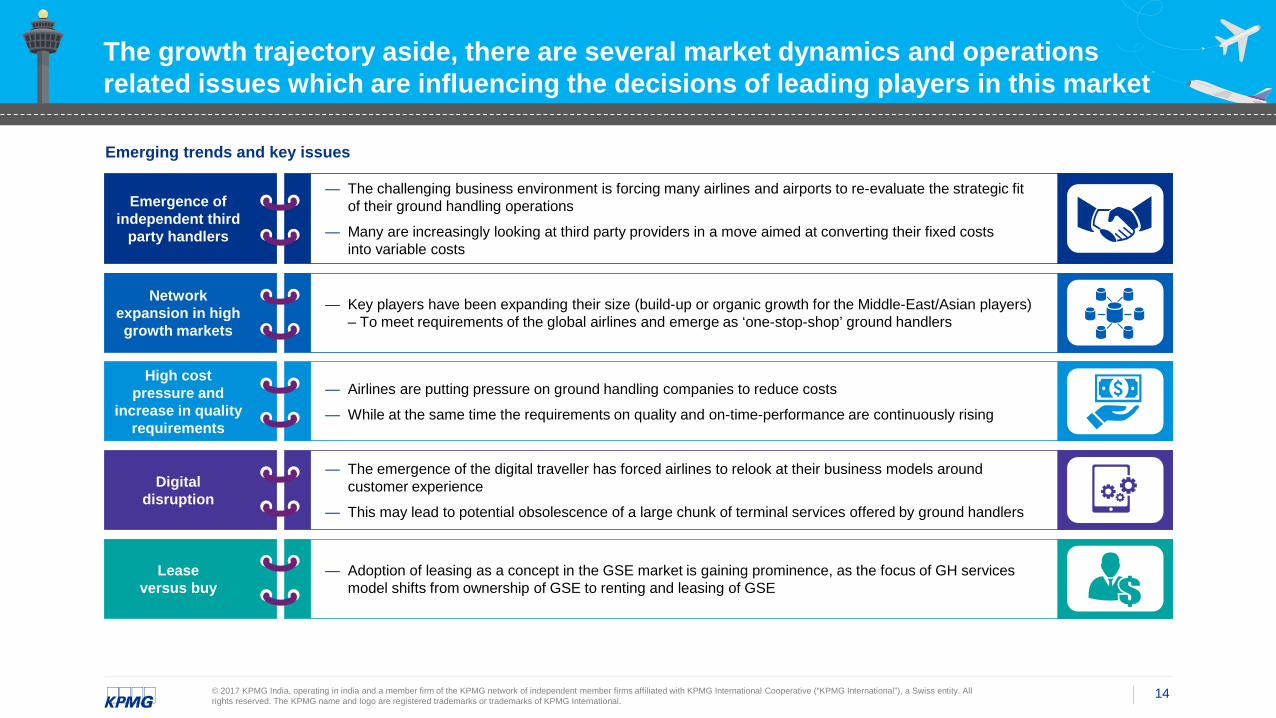

The growth trajectory aside, there are several market dynamics and operations related issues which are influencing the decisions of leading players in this market

Emerging trends and key issues

Emergence of independent third

party handlers

— The challenging business environment is forcing many airlines and airports to re-evaluate the strategic fitof their ground handling operations

— Many are increasingly looking at third party providers in a move aimed at converting their fixed costsinto variable costs

— Key players have been expanding their size (build-up or organic growth for the Middle-East/Asian players)– To meet requirements of the global airlines and emerge as ‘one-stop-shop’ ground handlers

Networkexpansion in high growth markets

— Airlines are putting pressure on ground handling companies to reduce costs

— While at the same time the requirements on quality and on-time-performance are continuously rising

High costpressure and

increase in quality requirements

— The emergence of the digital traveller has forced airlines to relook at their business models aroundcustomer experience

— This may lead to potential obsolescence of a large chunk of terminal services offered by ground handlers

Digitaldisruption

— Adoption of leasing as a concept in the GSE market is gaining prominence, as the focus of GH servicesmodel shifts from ownership of GSE to renting and leasing of GSE

Leaseversus buy

15© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

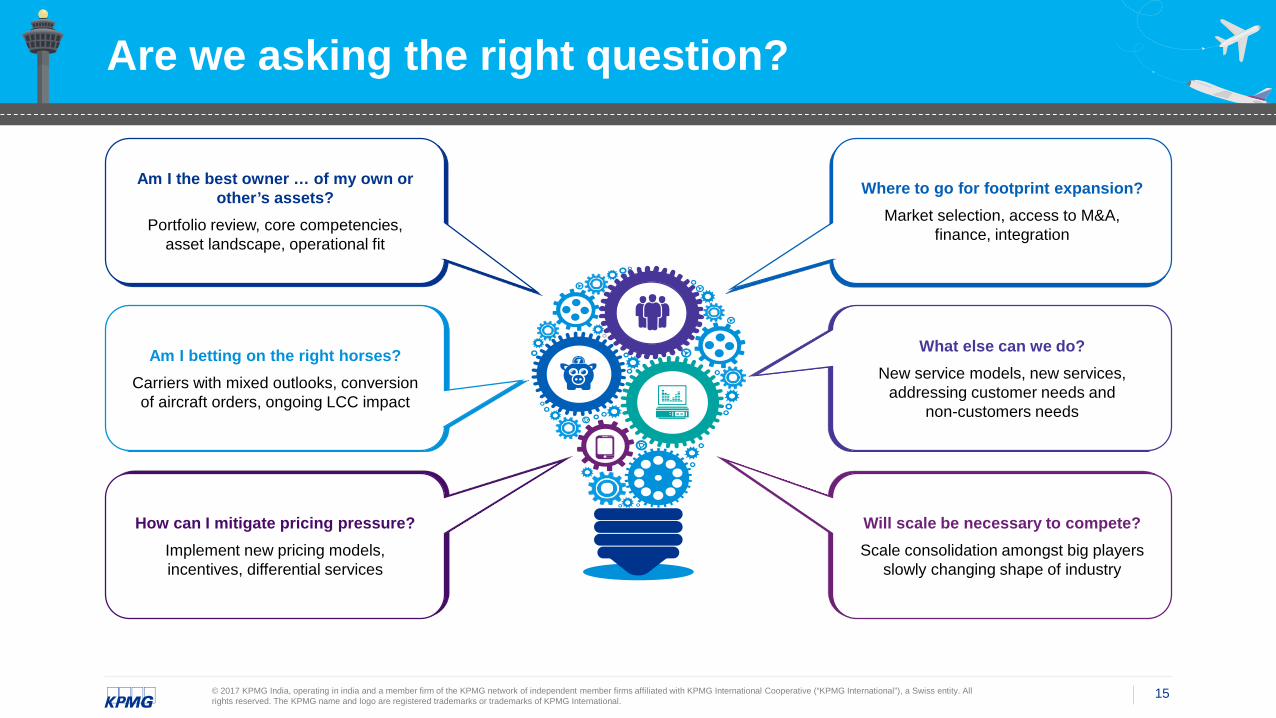

Are we asking the right question?

What else can we do?New service models, new services,

addressing customer needs andnon-customers needs

How can I mitigate pricing pressure?Implement new pricing models, incentives, differential services

Am I betting on the right horses?Carriers with mixed outlooks, conversion of aircraft orders, ongoing LCC impact

Where to go for footprint expansion? Market selection, access to M&A,

finance, integration

Am I the best owner … of my own or other’s assets?

Portfolio review, core competencies, asset landscape, operational fit

Will scale be necessary to compete?Scale consolidation amongst big players

slowly changing shape of industry

Winter is coming!…with a new friend

17© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

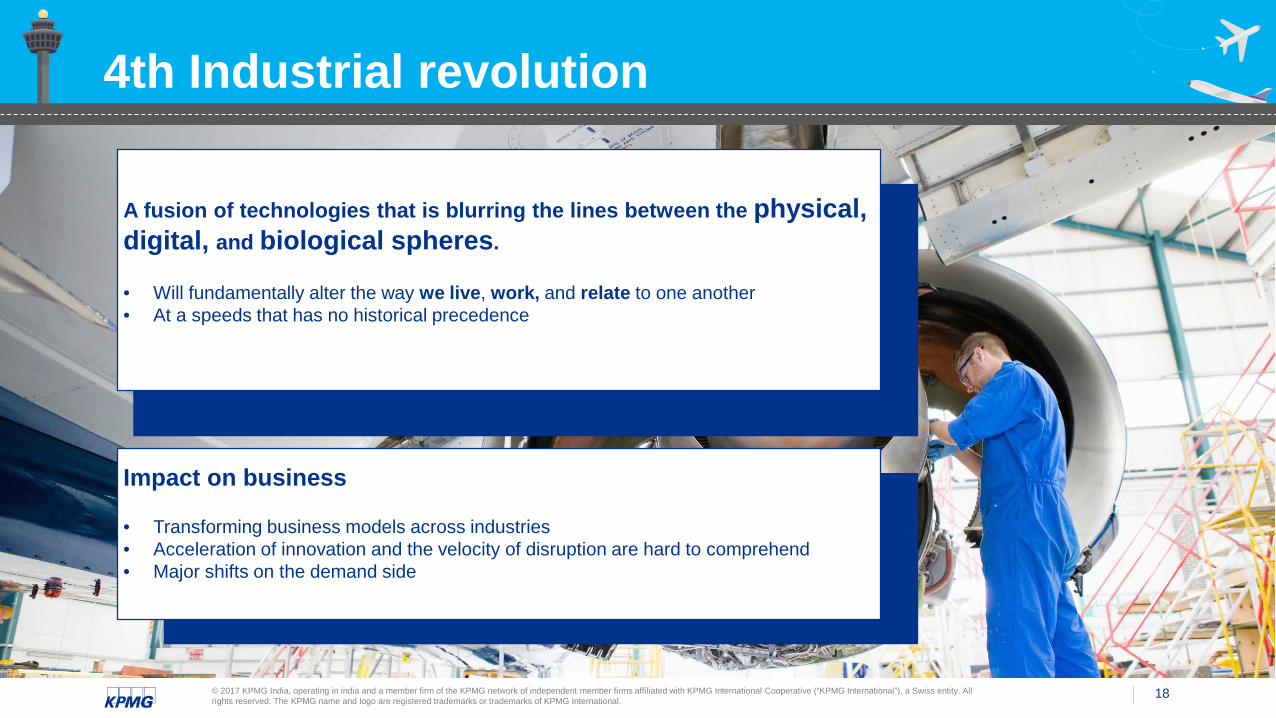

4th Industrial revolution

18© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

4th Industrial revolution

A fusion of technologies that is blurring the lines between the physical, digital, and biological spheres.

• Will fundamentally alter the way we live, work, and relate to one another• At a speeds that has no historical precedence

Impact on business

• Transforming business models across industries• Acceleration of innovation and the velocity of disruption are hard to comprehend• Major shifts on the demand side

20© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

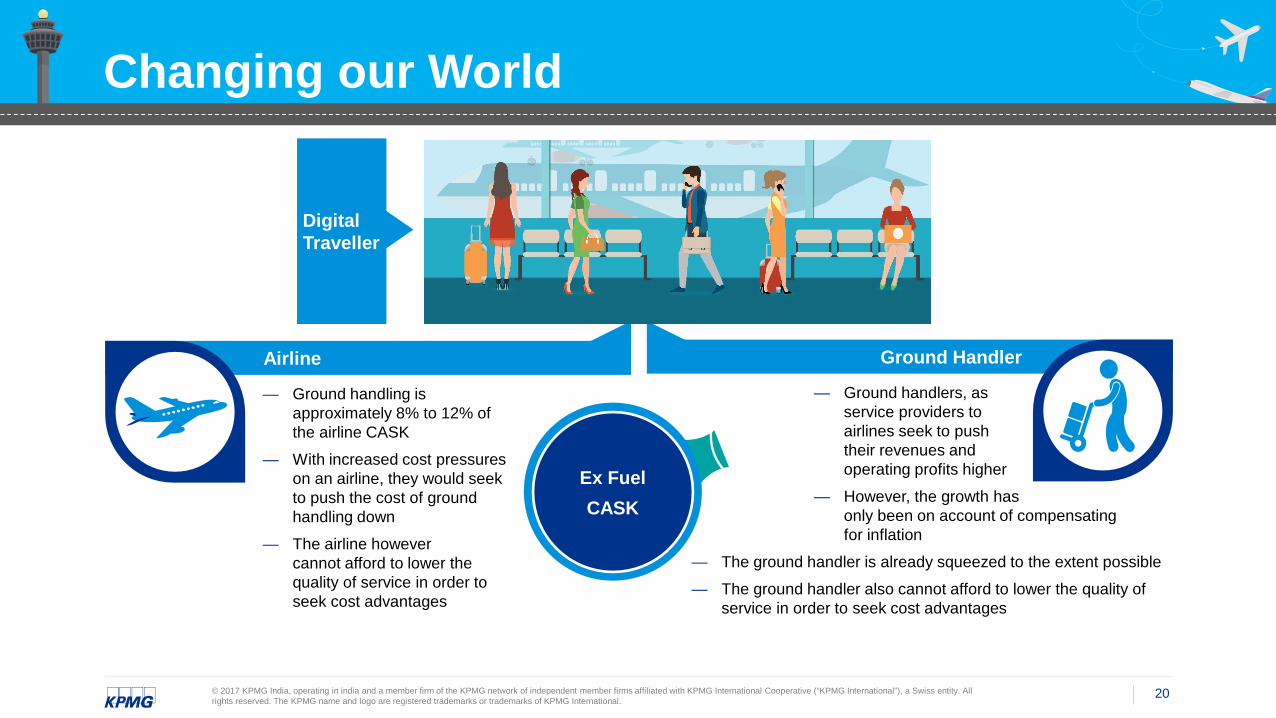

Ground handling 8-12%

Changing our World

Ex FuelCASK

— Ground handling is approximately 8% to 12% of the airline CASK

— With increased cost pressures on an airline, they would seek to push the cost of ground handling down

— The airline however cannot afford to lower the quality of service in order to seek cost advantages

Airline

— Ground handlers, asservice providers toairlines seek to pushtheir revenues andoperating profits higher

— However, the growth hasonly been on account of compensating for inflation

— The ground handler is already squeezed to the extent possible

— The ground handler also cannot afford to lower the quality of service in order to seek cost advantages

Ground Handler

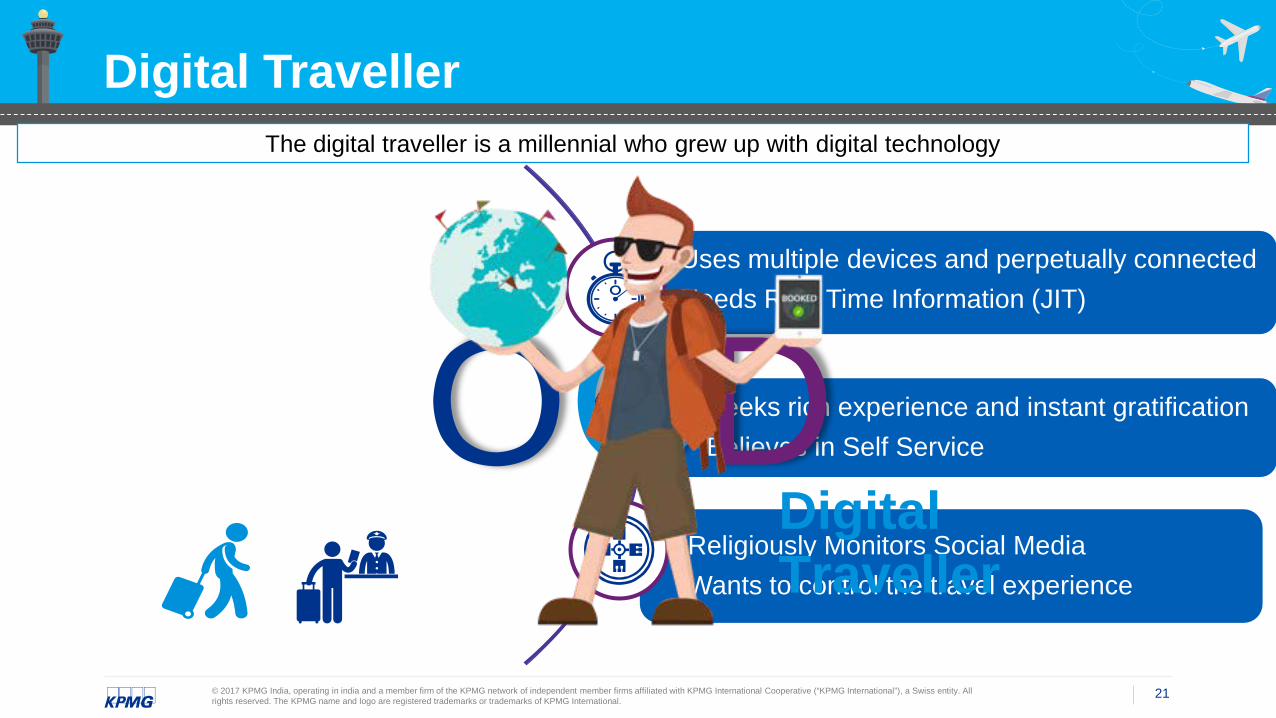

Digital Traveller

21© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Religiously Monitors Social MediaWants to control the travel experience

Uses multiple devices and perpetually connectedNeeds Real Time Information (JIT)

Digital Traveller

Seeks rich experience and instant gratificationBelieves in Self ServiceOCD

Digital Traveller

The digital traveller is a millennial who grew up with digital technology

22© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

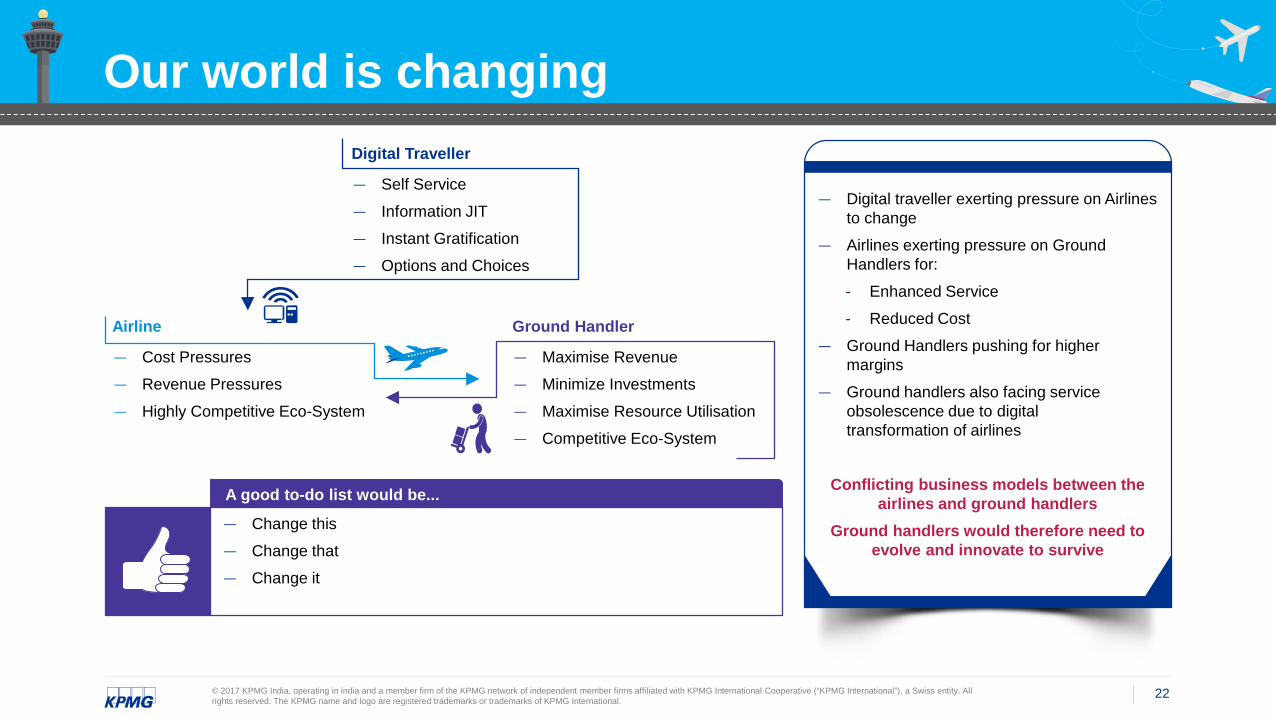

Our world is changing

— Digital traveller exerting pressure on Airlines to change

— Airlines exerting pressure on Ground Handlers for:

- Enhanced Service

- Reduced Cost

— Ground Handlers pushing for higher margins

— Ground handlers also facing service obsolescence due to digital transformation of airlines

Conflicting business models between the airlines and ground handlers

Ground handlers would therefore need to evolve and innovate to survive

A good to-do list would be...

— Change this

— Change that

— Change it

— Self Service

— Information JIT

— Instant Gratification

— Options and Choices

Digital Traveller

— Cost Pressures

— Revenue Pressures

— Highly Competitive Eco-System

Airline

— Maximise Revenue

— Minimize Investments

— Maximise Resource Utilisation

— Competitive Eco-System

Ground Handler

23© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Warming up to the winter

Cue Cards

Managed Service Provider

Alliances between Ground Handlers

Change Business Model to Tech Based

Service Provision

Monetize additional revenue streams such as training

…and many more transformational ideas

24© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

To keep warm (survive)…

Digital revolution is coming and is coming fast …

Customer Experience is the new Operational Excellence

25© 2017 KPMG India, operating in india and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

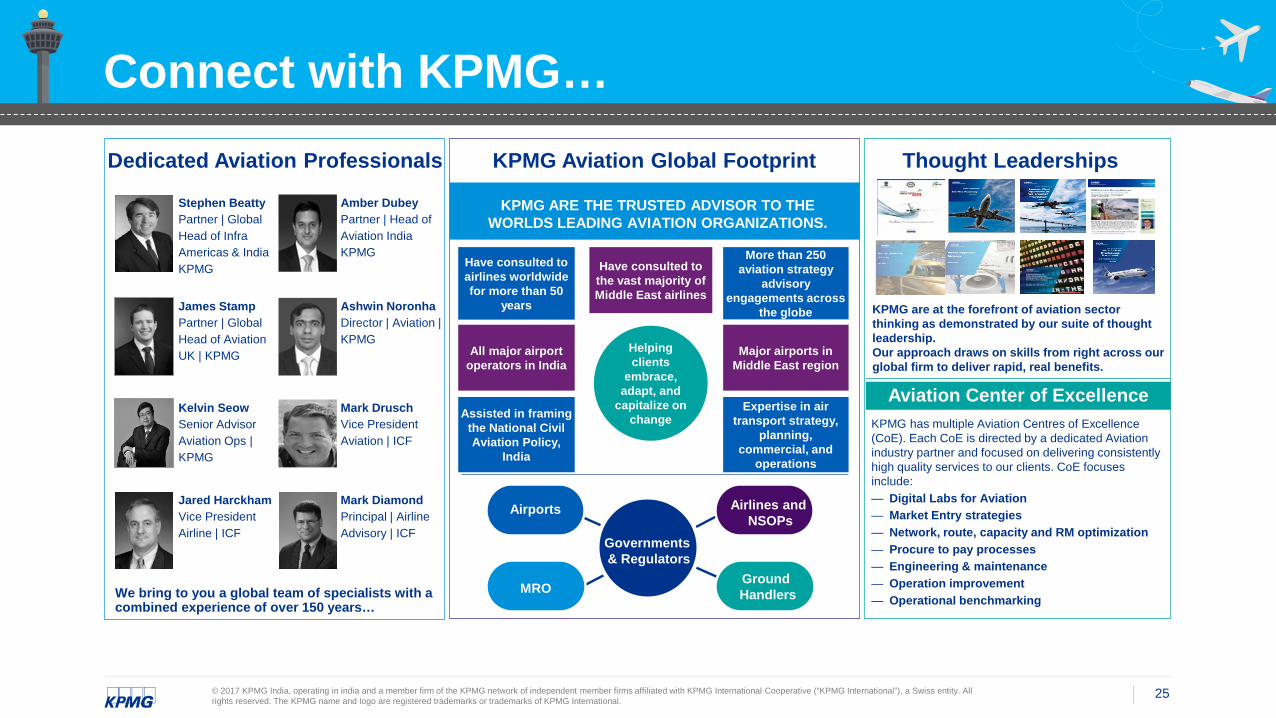

Connect with KPMG… Thought LeadershipsKPMG Aviation Global Footprint

Helping clients

embrace, adapt, and

capitalize on change

Have consulted to the vast majority of Middle East airlines

Assisted in framing the National Civil Aviation Policy,

India

Have consulted to airlines worldwide for more than 50

years

Major airports in Middle East region

More than 250 aviation strategy

advisory engagements across

the globe

Expertise in air transport strategy,

planning, commercial, and

operations

All major airport operators in India

Dedicated Aviation Professionals

Aviation Center of Excellence

We bring to you a global team of specialists with a combined experience of over 150 years…

KPMG are at the forefront of aviation sector thinking as demonstrated by our suite of thought leadership.Our approach draws on skills from right across our global firm to deliver rapid, real benefits.

Stephen BeattyPartner | Global Head of Infra Americas & IndiaKPMG

James StampPartner | Global Head of Aviation UK | KPMG

Kelvin SeowSenior Advisor Aviation Ops | KPMG

Ashwin NoronhaDirector | Aviation | KPMG

Mark DiamondPrincipal | Airline Advisory | ICF

Jared Harckham Vice President Airline | ICF

Mark DruschVice President Aviation | ICF

Amber DubeyPartner | Head of Aviation IndiaKPMG

KPMG ARE THE TRUSTED ADVISOR TO THE WORLDS LEADING AVIATION ORGANIZATIONS.

Governments & Regulators

Airports Airlines and NSOPs

MROGround Handlers

KPMG has multiple Aviation Centres of Excellence (CoE). Each CoE is directed by a dedicated Aviation industry partner and focused on delivering consistently high quality services to our clients. CoE focuses include: — Digital Labs for Aviation— Market Entry strategies — Network, route, capacity and RM optimization — Procure to pay processes— Engineering & maintenance— Operation improvement — Operational benchmarking

Thank you

T: +911246691000M:+919871933711F: +911243074300E: [email protected]

Amber Dubey

Partner and Head Aerospace and Defense

KPMG in India

Kelvin Seow

Sr. AdvisorAerospace and Defence

KPMG in India

Ashwin Noronha

DirectorAerospace and Defence

KPMG in India

Rohit Tomar

ManagerAerospace and Defence

KPMG In India

Contact us

T: +911246691000

F: +911243074300E: [email protected]

T: +911246691000M:+919810757773F: +911243074300E: [email protected]

T: +911246691000

F: +911243074300E: [email protected]