Embed Size (px)

Citation preview

Financial Monitoring WorkshopFinancial Monitoring Workshop

Presenters: David O’Brien & Hitesh

Mohanlal

We will look at the accounting system of an organisation by stepping through profit and loss accounts, balance sheet, cash-flow, assets, liabilities and introduce you to the tools you need to gain a deeper understanding of the core financial drivers that affect your organisation's financial health.

Objective

Users of Financial Users of Financial InformationInformation

Management (i.e you)CreditorsShareholders or partnersTaxation Authorities

Profit & Loss Account

A profit and loss account provides a complete picture of the operating results of a business over the financial period, by detailing the amount of revenues and expenses and the results in a net profit or loss.

RevenuesRevenues

Revenues are inflows or other enhancements of service potential or future economic benefits arising from:

the provision of goods and services e.g sales

investments in or loans to another individual or entity e.g.

Interest or grants received

the holding and disposal of assets e.g. rent and proceeds of sale of assets

ExpensesExpenses

Expenses are consumption of or losses of service potential or future economic benefits arising from:

the use of goods and services e.g. property rates

the use of assets e.g. depreciation

the incurrence of a liability e.g. interest and income tax.

Workshop Exercise 1

Bank Charges REVENUE / EXPENSE

Interest Received REVENUE / EXPENSE

Wages Subsidy from Gov’t REVENUE / EXPENSE

Interest Paid REVENUE / EXPENSE

Rates REVENUE / EXPENSE

Depreciation REVENUE / EXPENSE

Sales REVENUE / EXPENSE

AccrualsAn accounting expense recognised in the books before it is paid for. It is a liability, and is usually current. These expenses are typically periodic and documented on a company's balance sheet due to the high probability that they will be paid.

E.g A telephone bill received on 15 July 2008 but relates to the period 1 June 2008 to 30 June 2008 for $77 would be included as an expense in the accounts for the year to 30 June 2008.

Prepayments

These are the opposite to accruals. An accounting expense recognised in the balance sheet after it is paid for. It is an asset, and is usually current. These expenses are typically periodic and documented on a company's balance sheet due to the high probability that they will be utilised.

Eg insurance paid for $2,000 for the period 1 January 2008 to 31 December 2008. In the accounts to 30 June 2008 $1,000 (50%) will be included as an insurance expense and $1,000 as a prepayment on the balance sheet.

Some Examples

A cheque banked 26 June 2008 for rent received on the building you own from 1 January to 31 December 2008. Year end is 30 June 2008.

Half of the amount banked would be revenue of the 30 June 2008 year and the other half would be a liability of the entity until 31 December 2008 because you are obligated to provide the building to the tenant until that time.

An invoice for printing of pamphlets/brochures is in the office at 30 June 2008 but has not been paid. The brochures were all distributed at a Trade Fair attended early June 2008.

The printing costs would all be an expense of the 30 June 2008 year because the brochures have been used in that period. If the brochures were for a Trade Fair in July 2008 and the amount involved was substantial then the printing expense would belong to the following year and the brochures would be an asset (stock on hand).

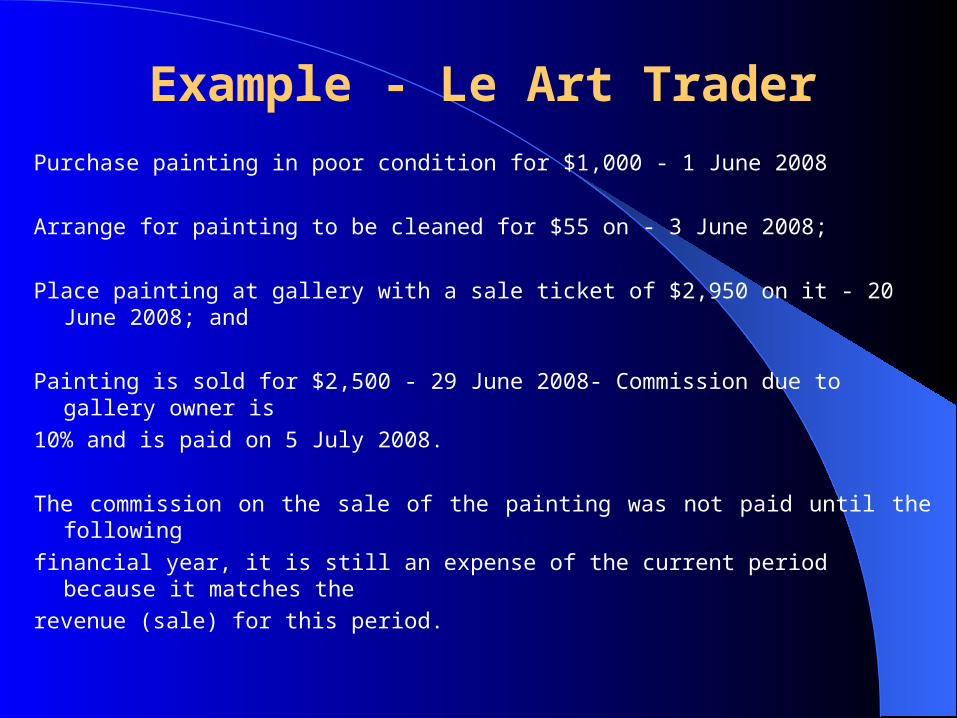

Example - Le Art Trader

Purchase painting in poor condition for $1,000 - 1 June 2008

Arrange for painting to be cleaned for $55 on - 3 June 2008;

Place painting at gallery with a sale ticket of $2,950 on it - 20 June 2008; and

Painting is sold for $2,500 - 29 June 2008- Commission due to gallery owner is

10% and is paid on 5 July 2008.

The commission on the sale of the painting was not paid until the following

financial year, it is still an expense of the current period because it matches the

revenue (sale) for this period.

Profit & Loss Account

Sale 2,500

less expenses

Purchase 1,000

Cleaning 55

Commission 250

1,305

NET PROFIT 1,195

Example - Le Art TraderExample - Le Art Trader

Balance SheetBalance Sheet

A balance sheet is a detailed. "snapshot" of the condition or financial health of a business on a specific date. Most businesses prepare a balance sheet at the end of its financial year, usually June 30; many businesses prepare them monthly or quarterly.

A balance sheet shows the A balance sheet shows the dollar amount of:dollar amount of:

Assetsi.e. what the business owns

Less

Liabilitiesi.e. what the business owes

equals

net worth i.e. what the owners, stakeholders or shareholders own.

Balance Sheet ClassificationsBalance Sheet ClassificationsAssets and liabilities are generally classified as

either:

Current

i.e. consumed or converted into cash or due and payable within 12 months of the end of the financial period or

Non-current

i.e. not to be consumed or converted into cash or not due and payable within 12 months of the end of the financial period.

Workshop ExerciseWorkshop Exercise Current/ Non Current

Trade Debtors $15,500

Bank Overdraft $(8,000)

Bank Deposit $25,000

Lease Liability:

< 1 year $(5,500)

> 2 years < 5 years $(20,000)

Accrued Charges ($16,000)

Bank loan ($15,000)

Cashflow StatementCashflow Statement

It is a statement that shows the net of

Inflows – cash that has come into the organisation.

Eg When a grant is received.

Outflows – cash that has left the organisation

Eg When salaries are paid

... It is not the same as Profit!!

Because ......Because ......

Some things are paid or received in cash but

not included in the profit and loss account.

Examples are:

Purchase of assets (balance sheet item)Depreciation charge (not a cash transaction)Accruals and prepayments (balance sheet

item)

Board InformationBoard InformationAs a board you should have the following

financial information: A budget prepared at the beginning of each

financial year which is reviewed periodically.

A monthly profit and loss account, balance sheet and cashflow forecast.

Comparison of budgets to actual figuresThe ability to identify differences between

actual and budget.

Question time

The Tea Trees

Theatre Company

Case Study