Embed Size (px)

Citation preview

Financial Management Common Core Solution Business Use Cases September 30, 2016

2 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

Table of Contents Purpose ................................................................................................................................................................................... 4

End-to-End Business Processes ............................................................................................................................................... 4

Service Area, Function and Activity Listing ............................................................................................................................. 4

Business Scenarios .................................................................................................................................................................. 4

Business Use Cases.................................................................................................................................................................. 5

Federal Financial Management Inventory of Business Use Cases and Scenarios ................................................................... 5

Federal Financial Management Business Use Case Demonstration Threads ....................................................................... 14

Federal Financial Management Business Use Cases ............................................................................................................. 23

1 Budget Formulation-to-Execution ..................................................................................................................................... 24

1.1 Budget Authority Set-Up ............................................................................................................................................. 24

1.2 Spending Authority from Offsetting Collections (Reimbursables) .............................................................................. 27

1.3 Budget Authority Transfers ......................................................................................................................................... 30

2 Acquire-to-Dispose ............................................................................................................................................................. 33

2.1 Property, Plant, and Equipment (PP&E) Assets .......................................................................................................... 33

2.2 Bulk Purchases ............................................................................................................................................................ 38

2.3 Complex Systems ........................................................................................................................................................ 42

3 Request-to-Procure ............................................................................................................................................................ 48

3.1 Procurement Within a Single Fiscal Year .................................................................................................................... 48

3.2 Procurement Across Fiscal Years Using Multi-Year Funds .......................................................................................... 52

3.3 Single Award from Multiple Purchase Requests ......................................................................................................... 56

4 Procure-to-Pay ................................................................................................................................................................... 59

4.1 Expenditures Within a Single Fiscal Year .................................................................................................................... 59

4.2 Expenditures Across Fiscal Years Using Multi-Year Funds with Invoicing Options ..................................................... 64

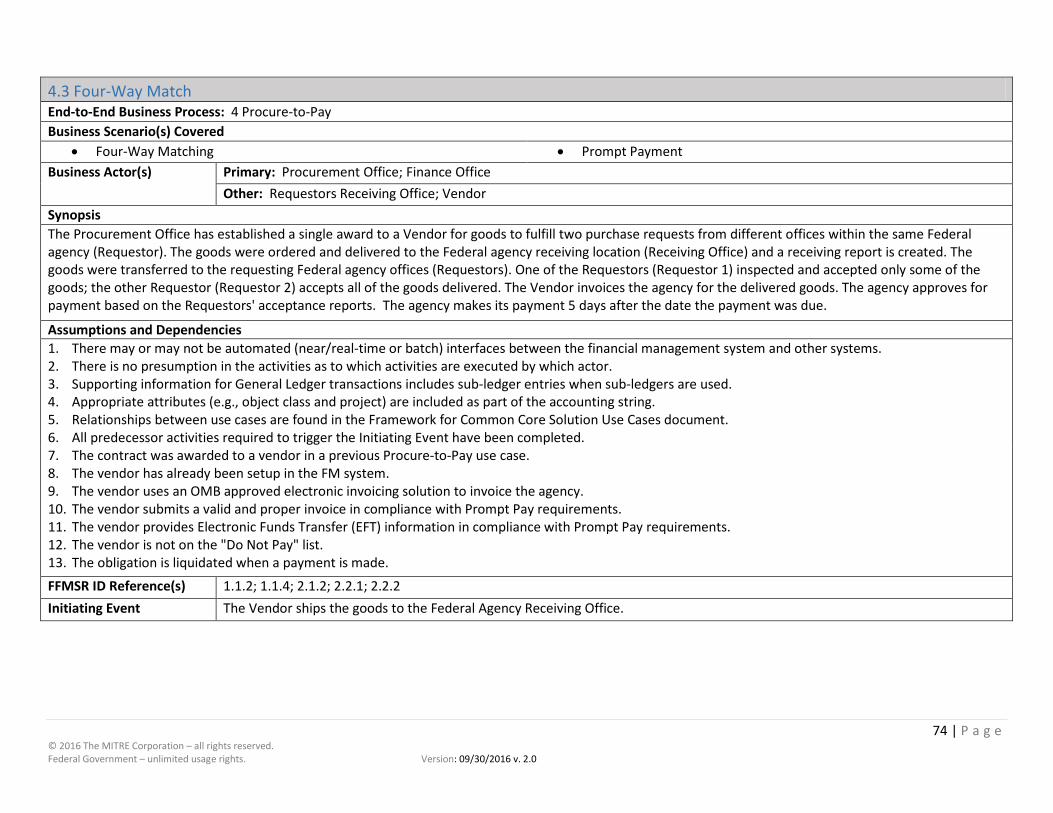

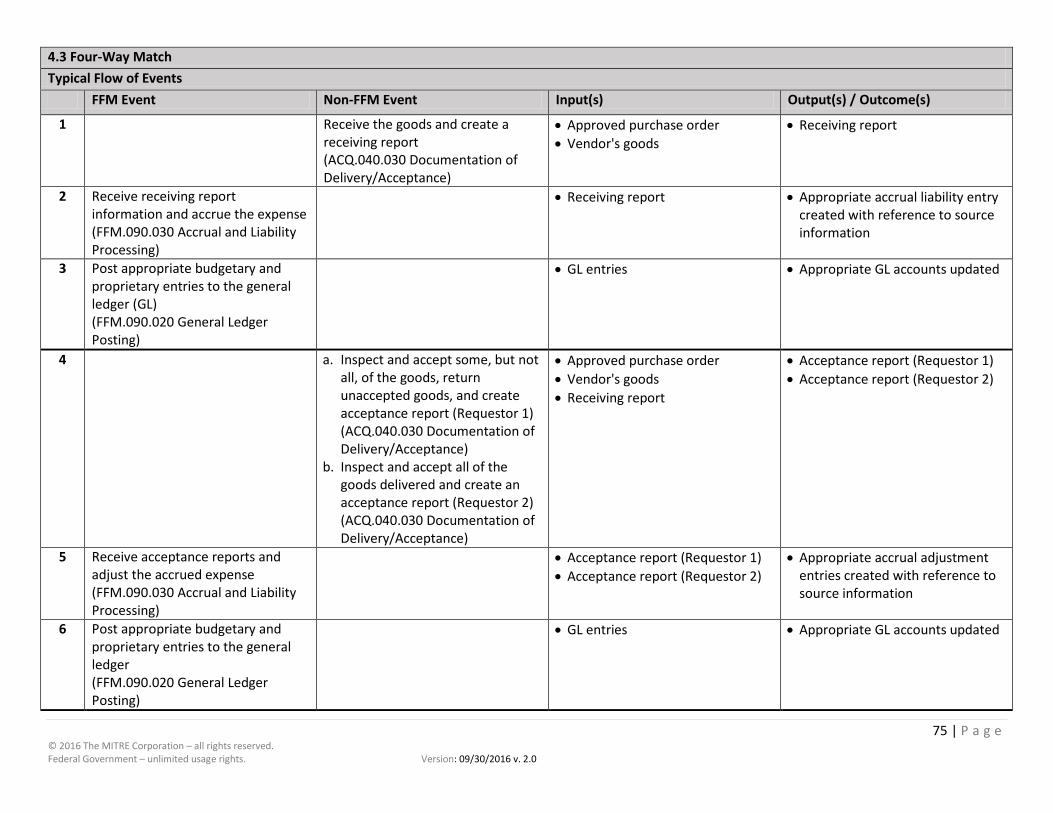

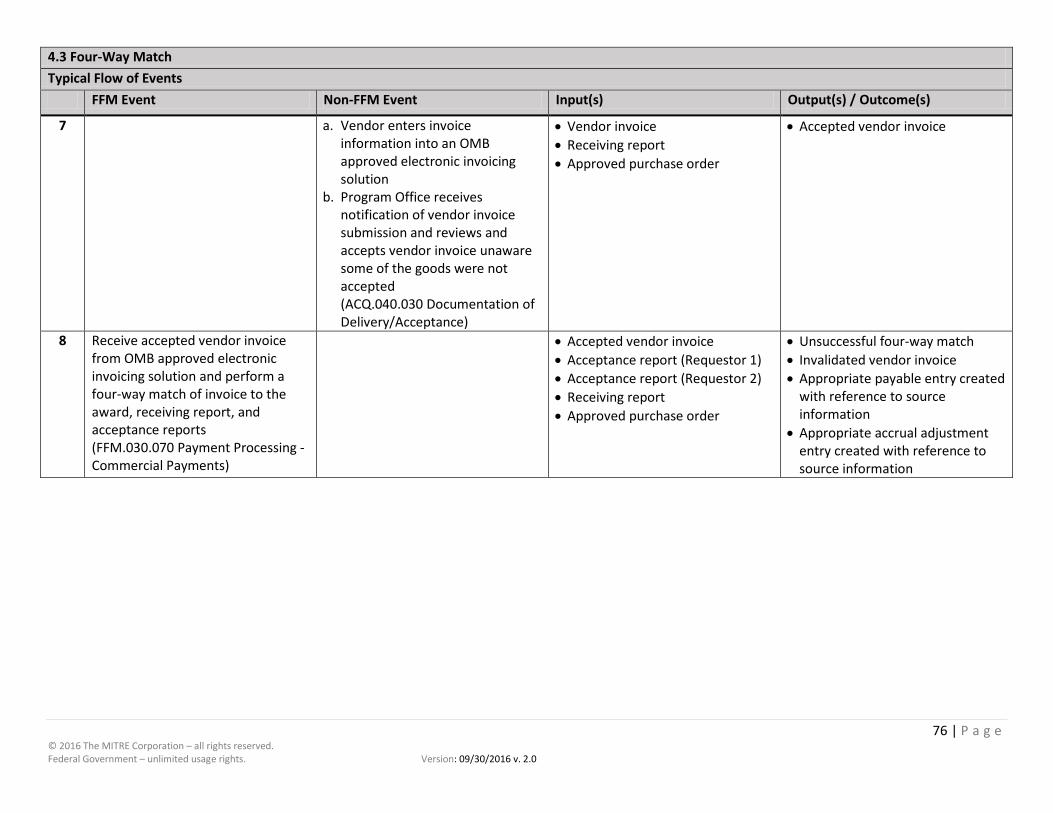

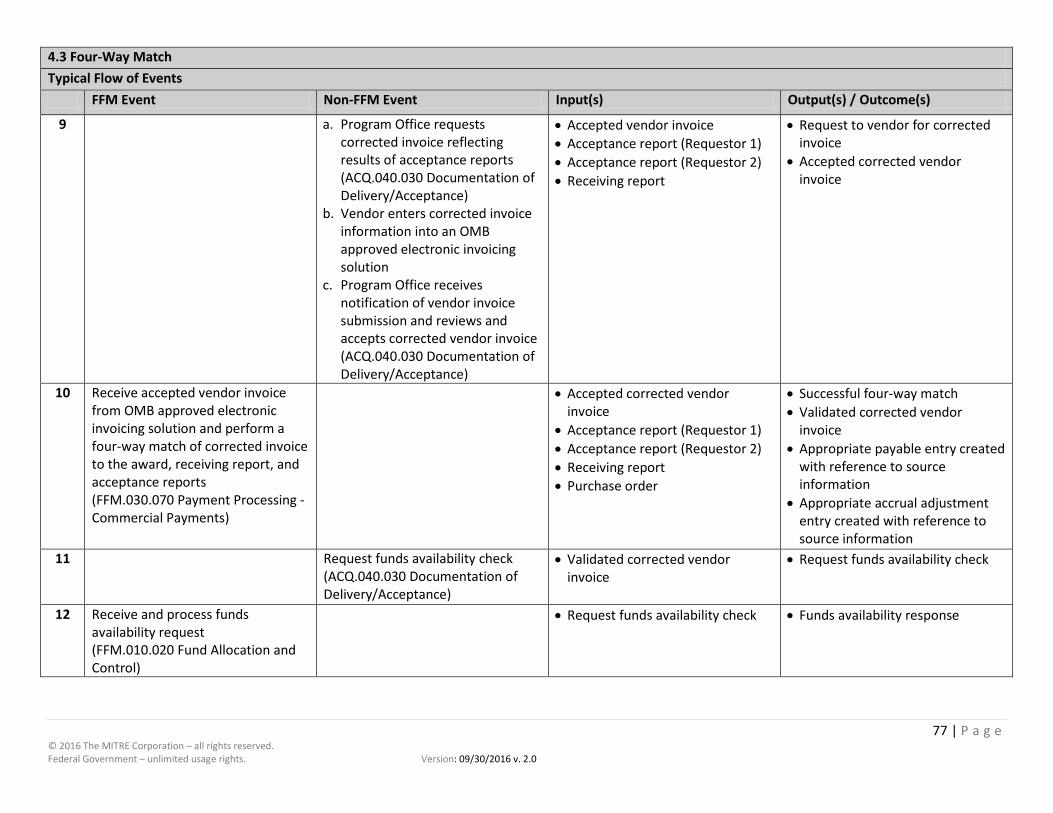

4.3 Four-Way Match ......................................................................................................................................................... 74

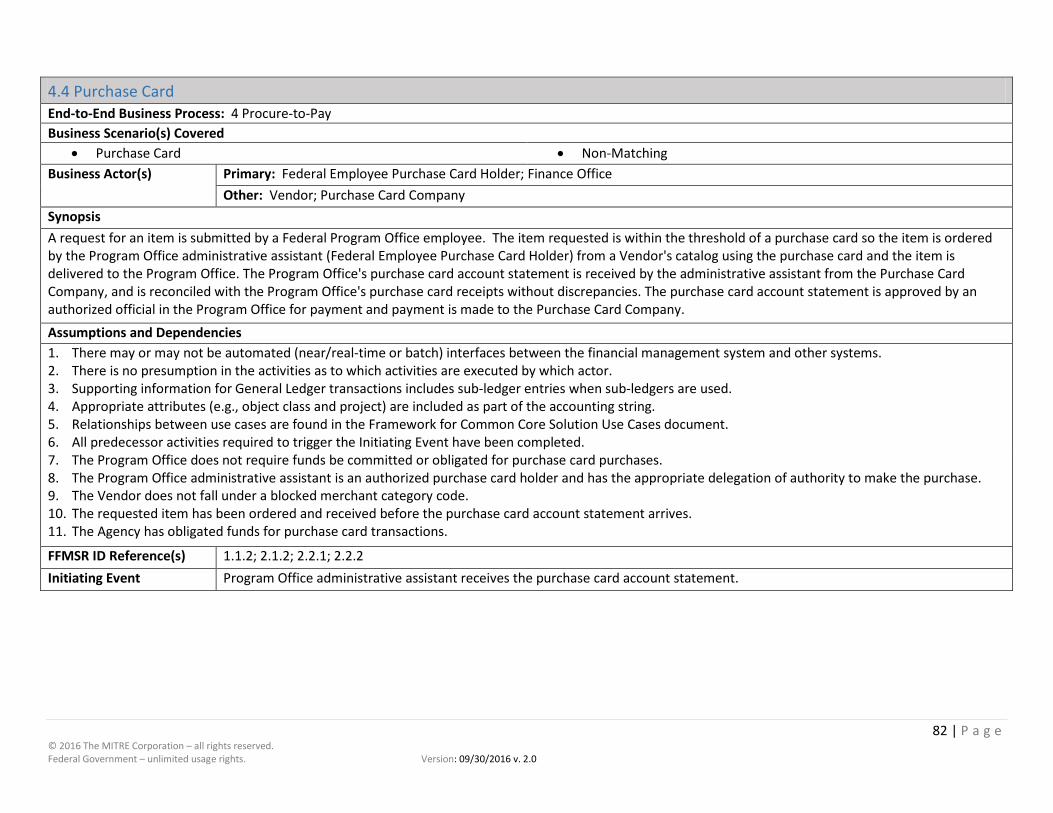

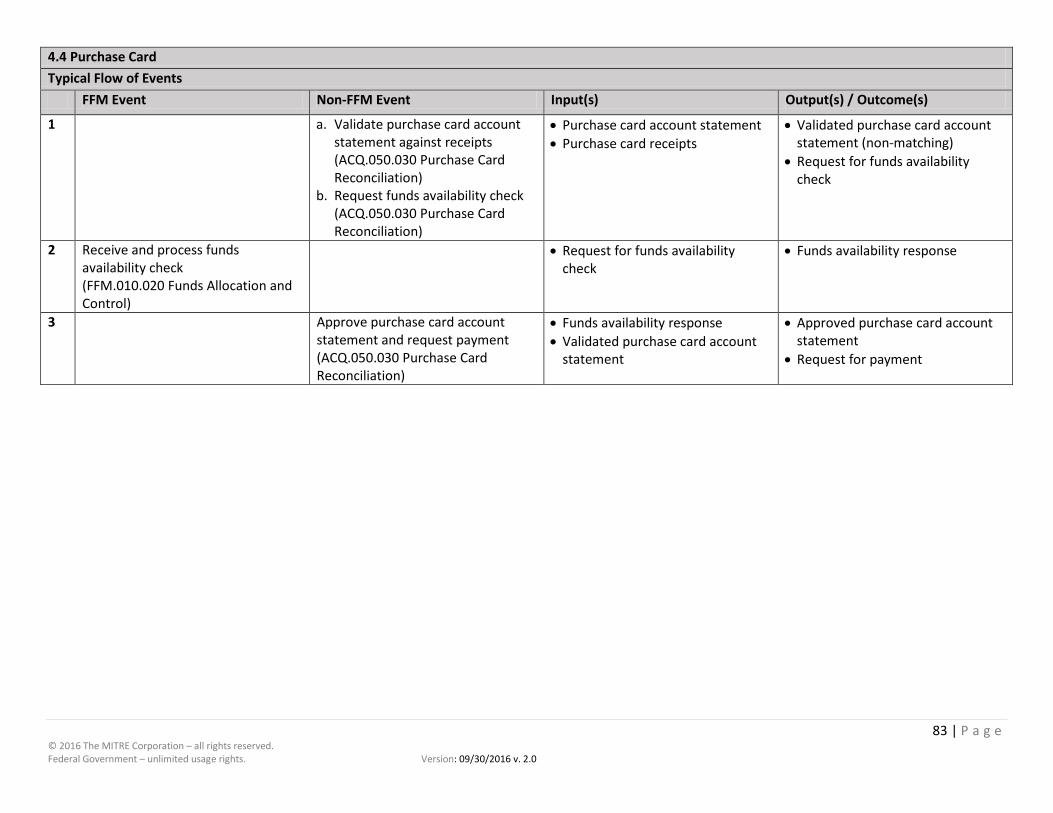

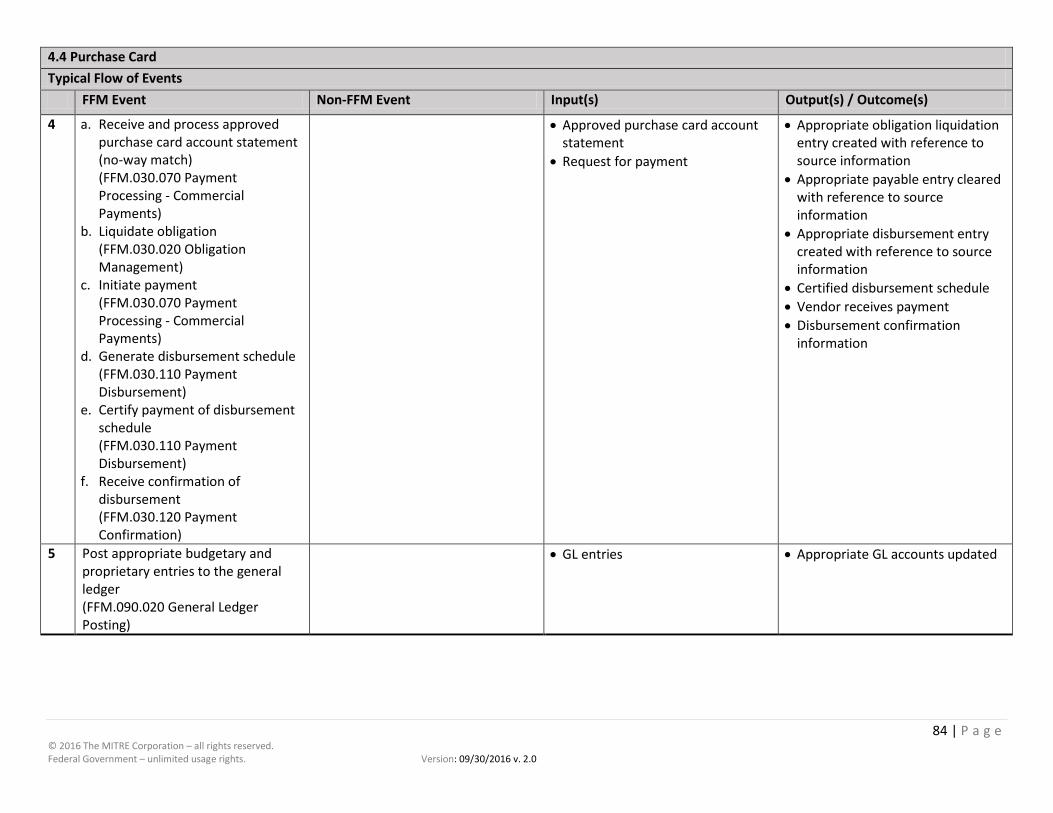

4.4 Purchase Card ............................................................................................................................................................. 82

5 Bill-to-Collect ...................................................................................................................................................................... 86

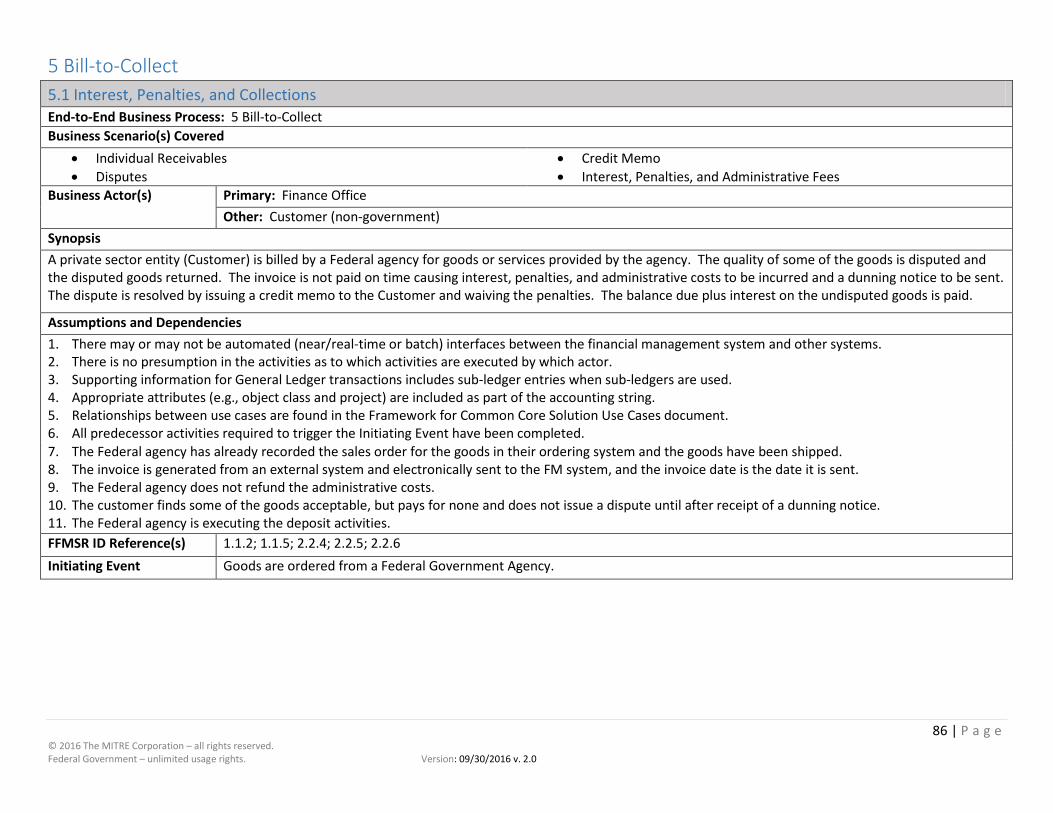

5.1 Interest, Penalties, and Collections ............................................................................................................................. 86

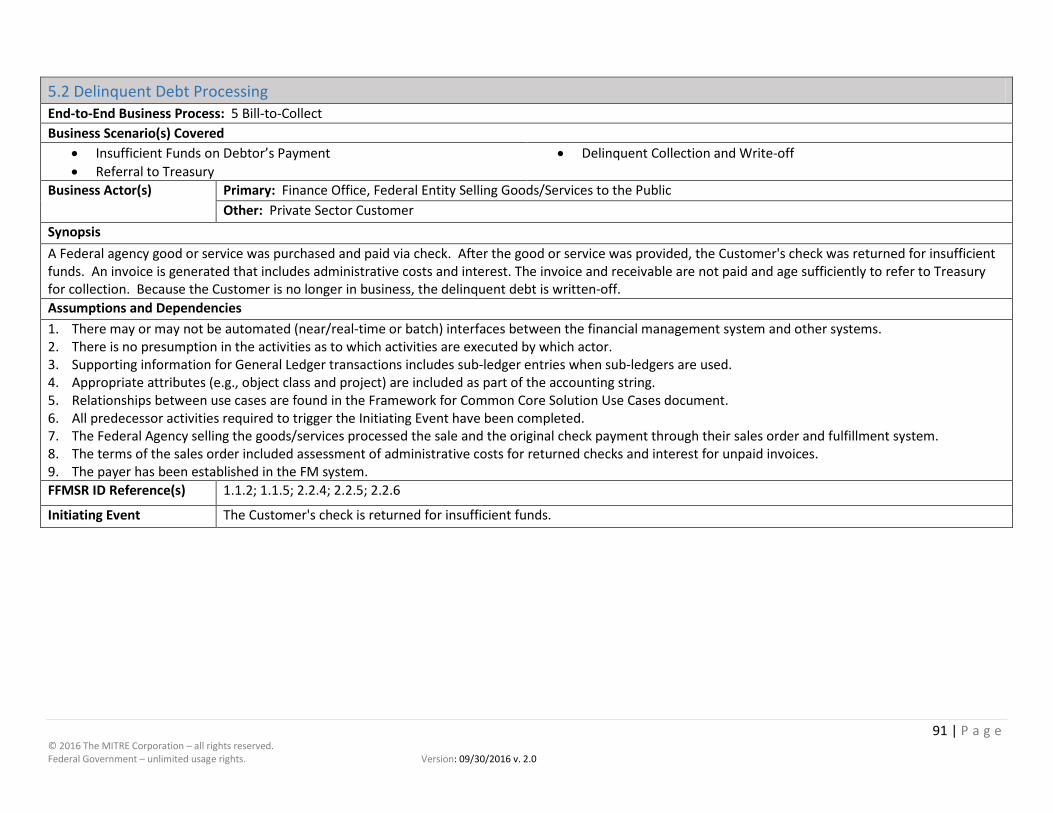

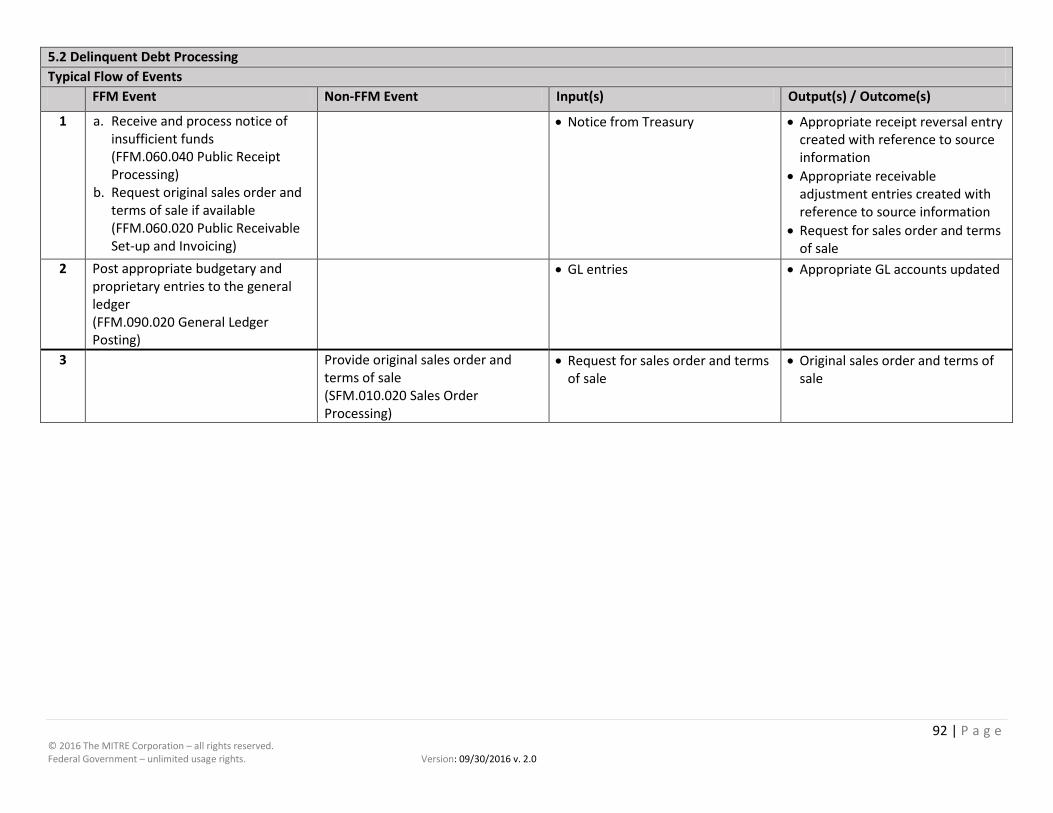

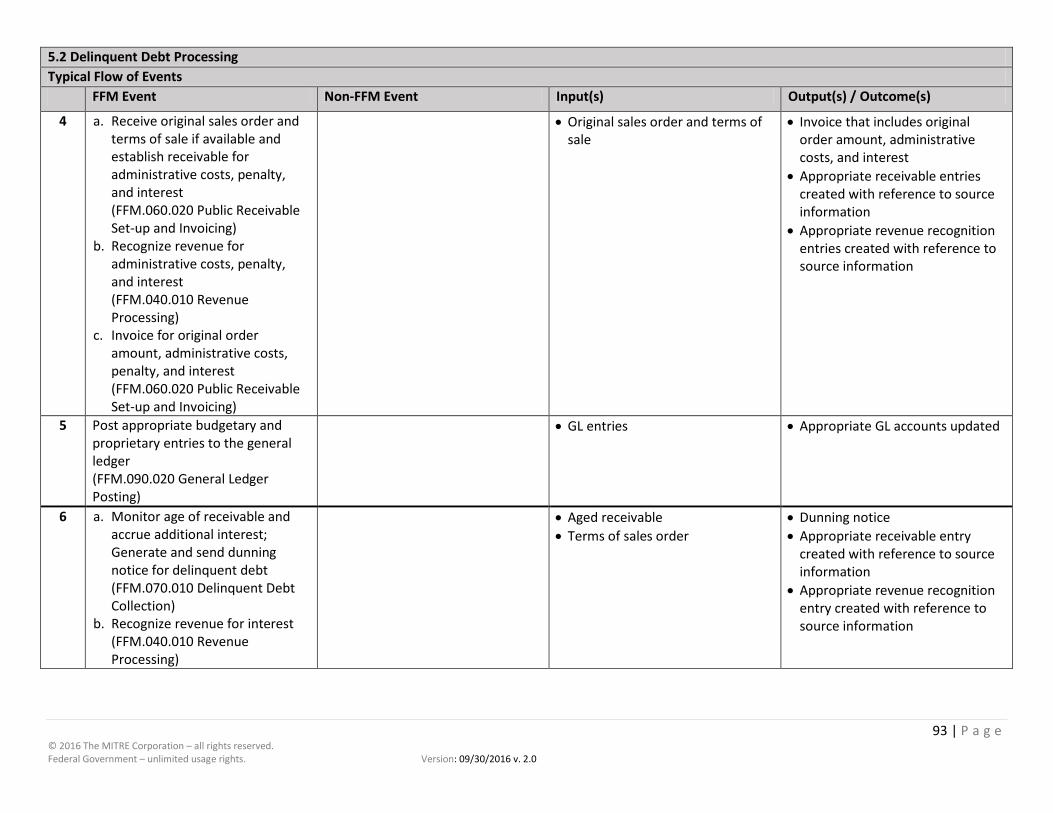

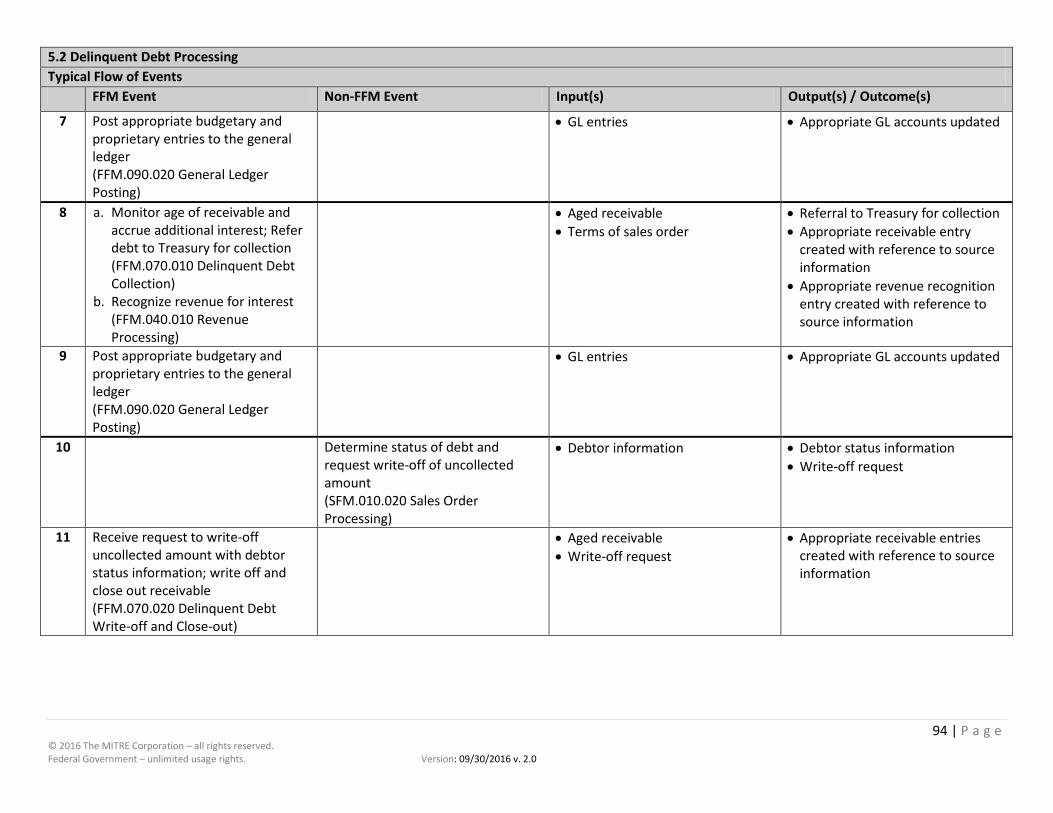

5.2 Delinquent Debt Processing ........................................................................................................................................ 91

6 Record-to-Report ............................................................................................................................................................... 96

6.1 Period End Adjustments and Reporting ...................................................................................................................... 96

6.2 Consolidated Financial Statements ............................................................................................................................. 99

7 Agree-to-Reimburse (Reimbursable Management)......................................................................................................... 102

7.1 Federal to Federal Reimbursable Agreement ........................................................................................................... 102

3 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

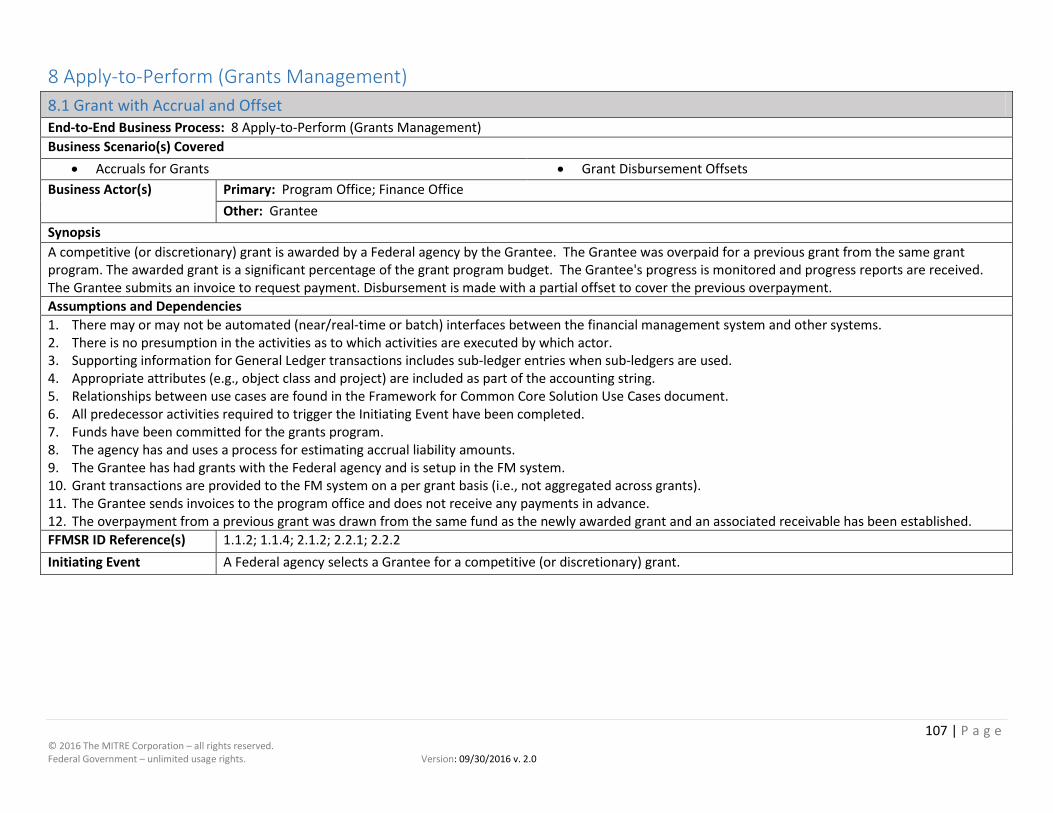

8 Apply-to-Perform (Grants Management) ........................................................................................................................ 107

8.1 Grant with Accrual and Offset .................................................................................................................................. 107

8.2 Administrative Grant Closeout.................................................................................................................................. 112

9 Hire-to-Retire ................................................................................................................................................................... 114

9.1 Post Payroll ............................................................................................................................................................... 114

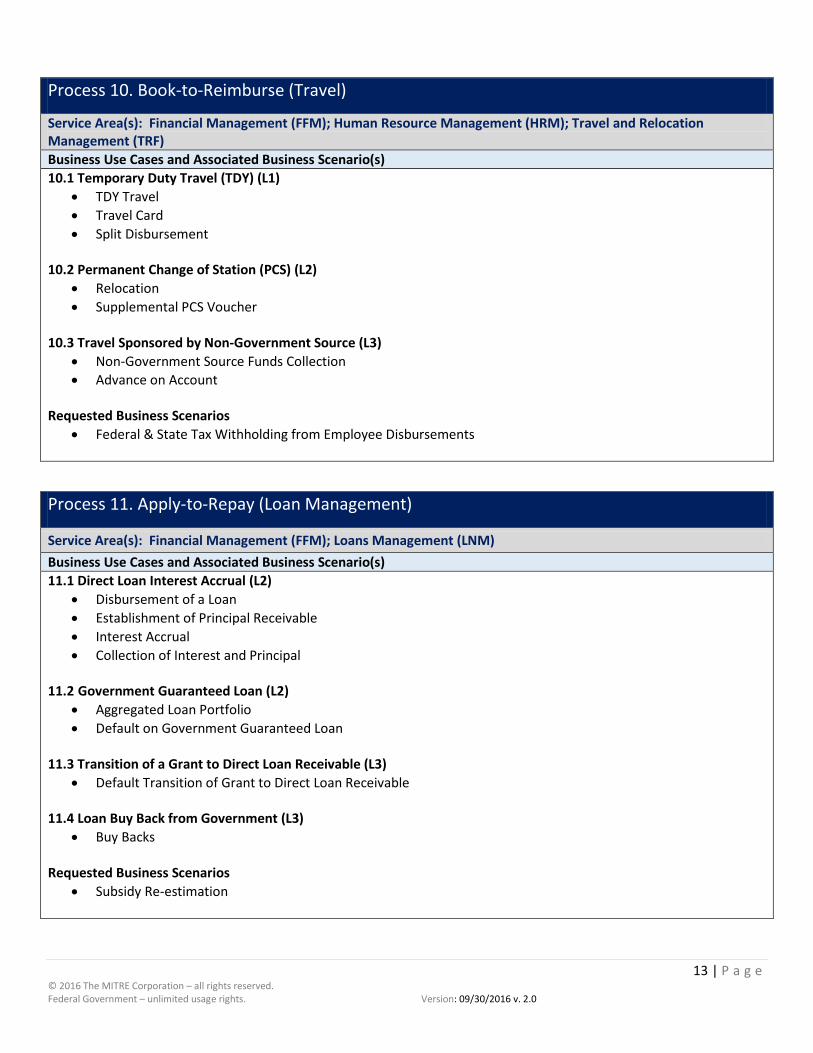

10 Book-to-Reimburse (Travel) ........................................................................................................................................... 119

10.1 Temporary Duty (TDY) Travel .................................................................................................................................. 119

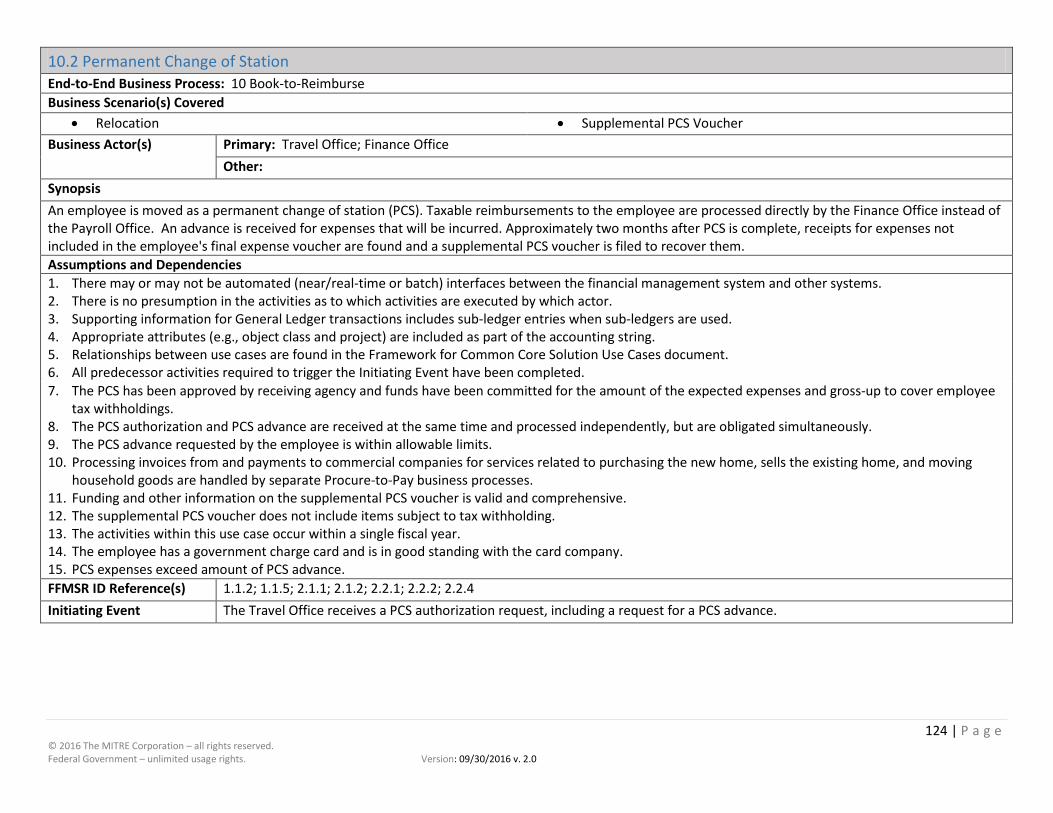

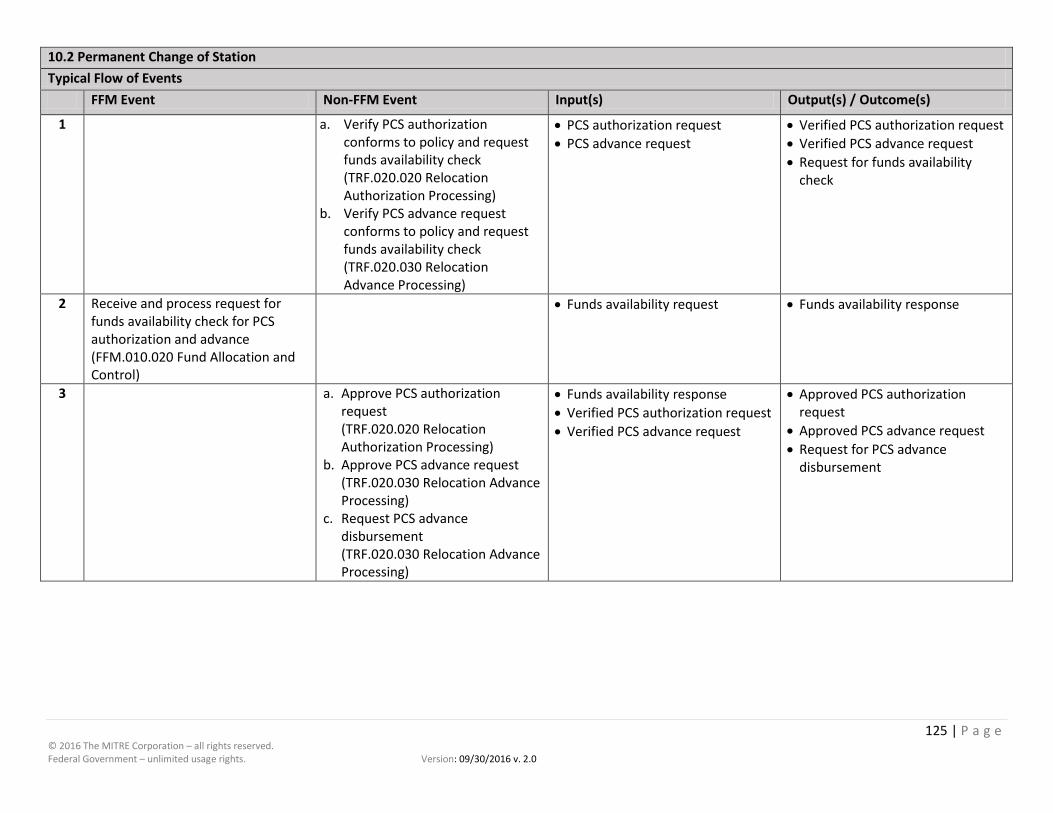

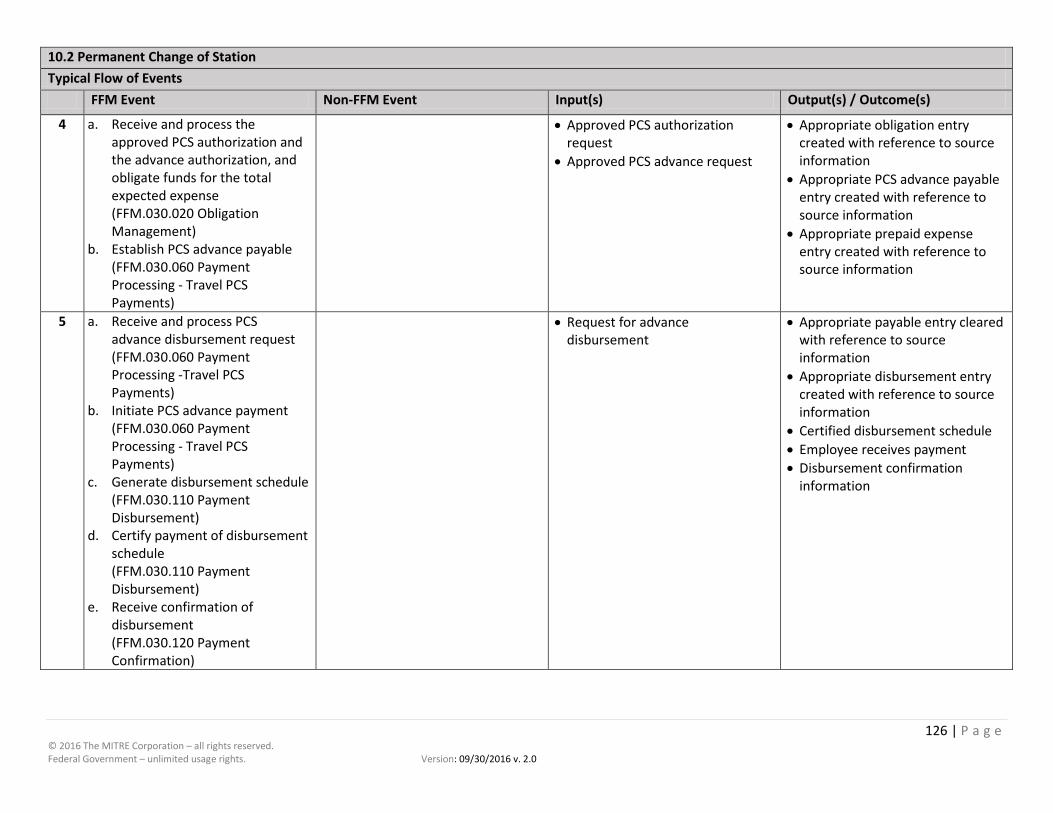

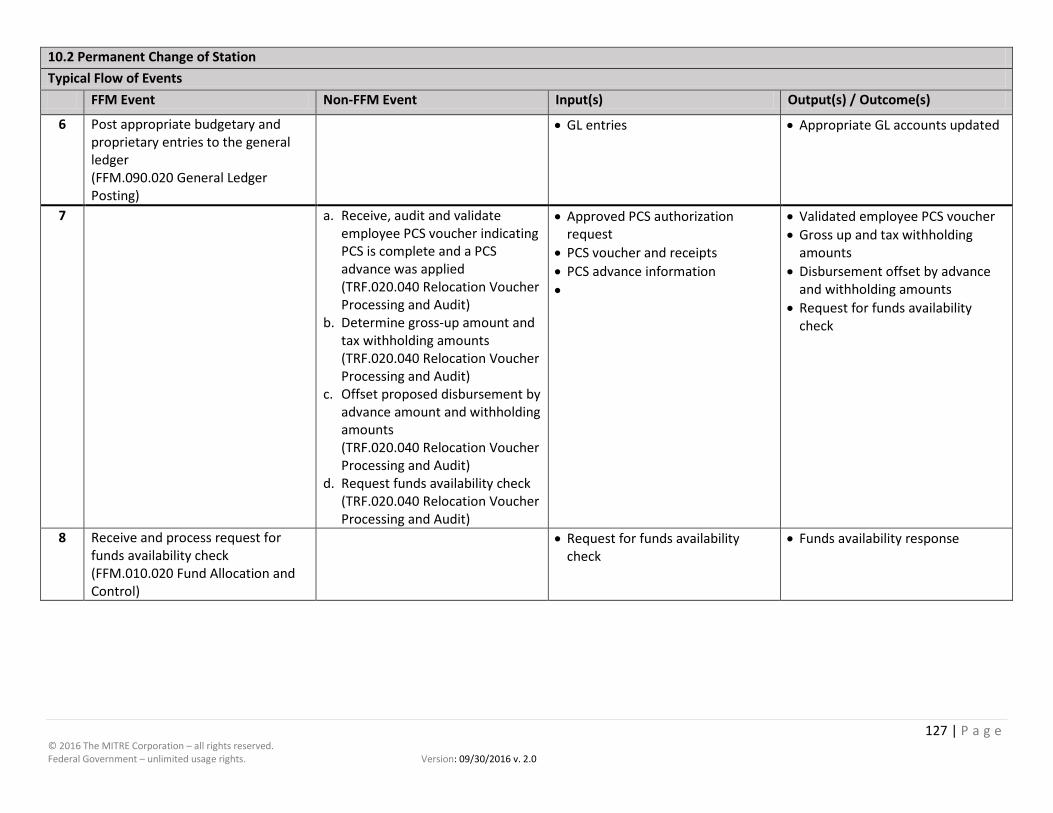

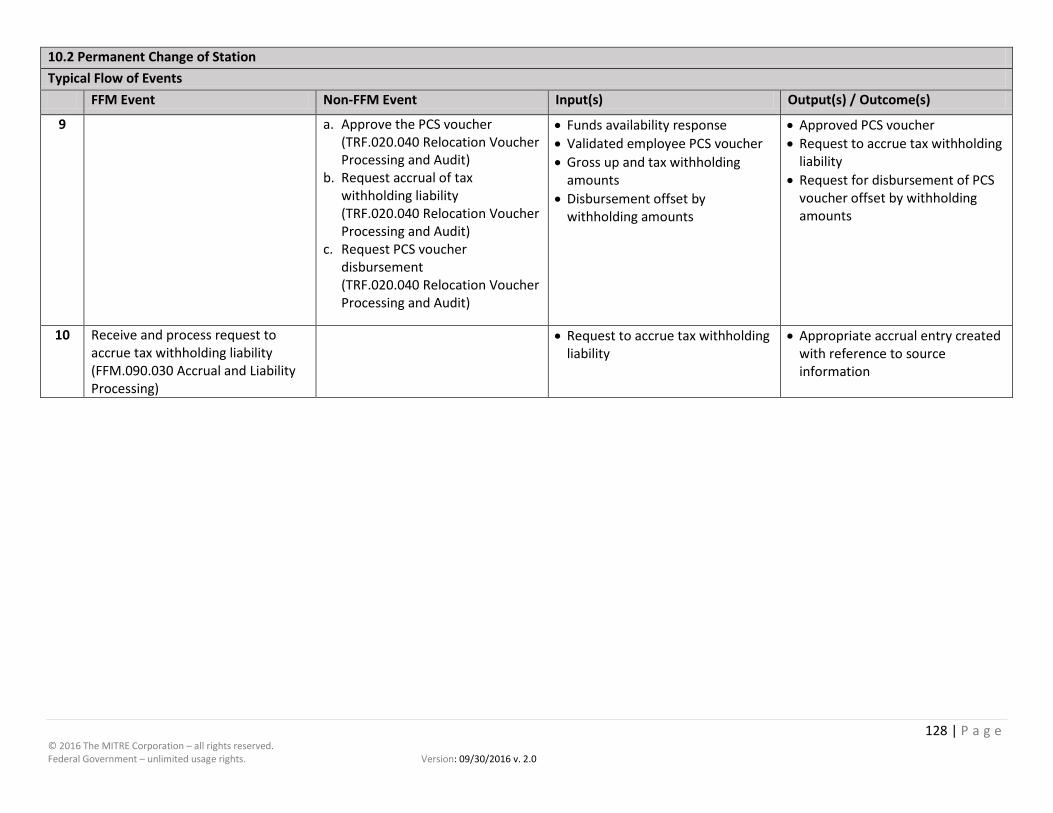

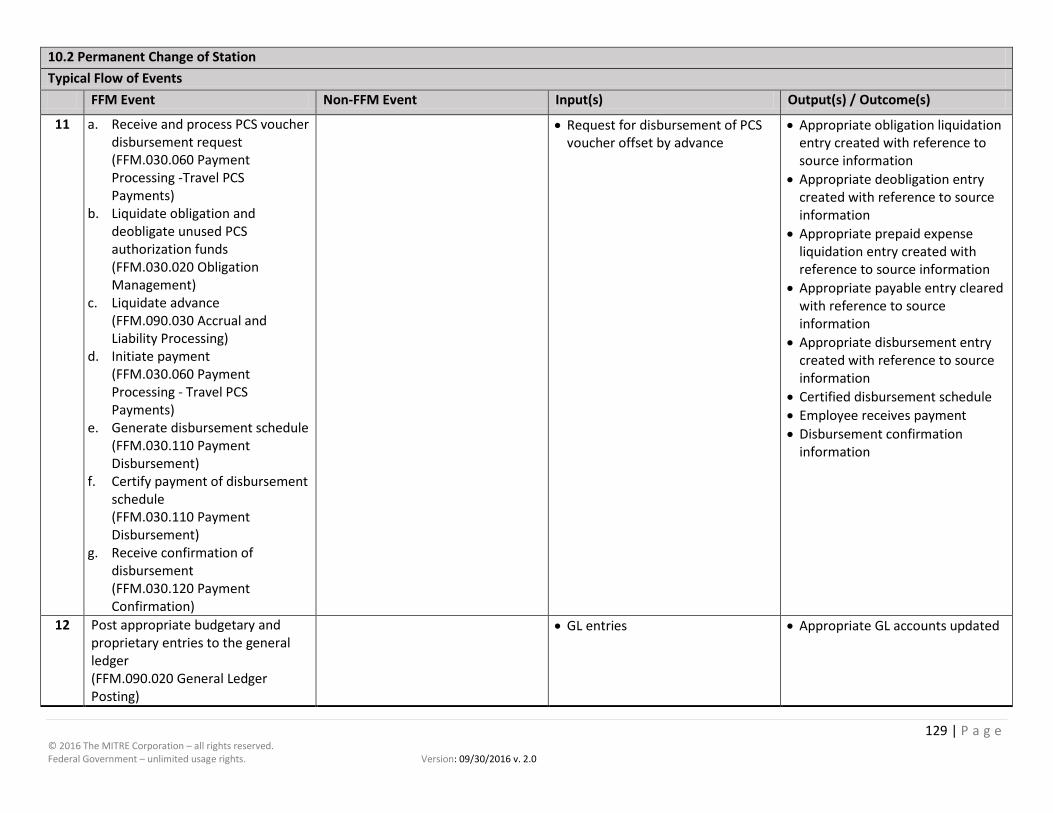

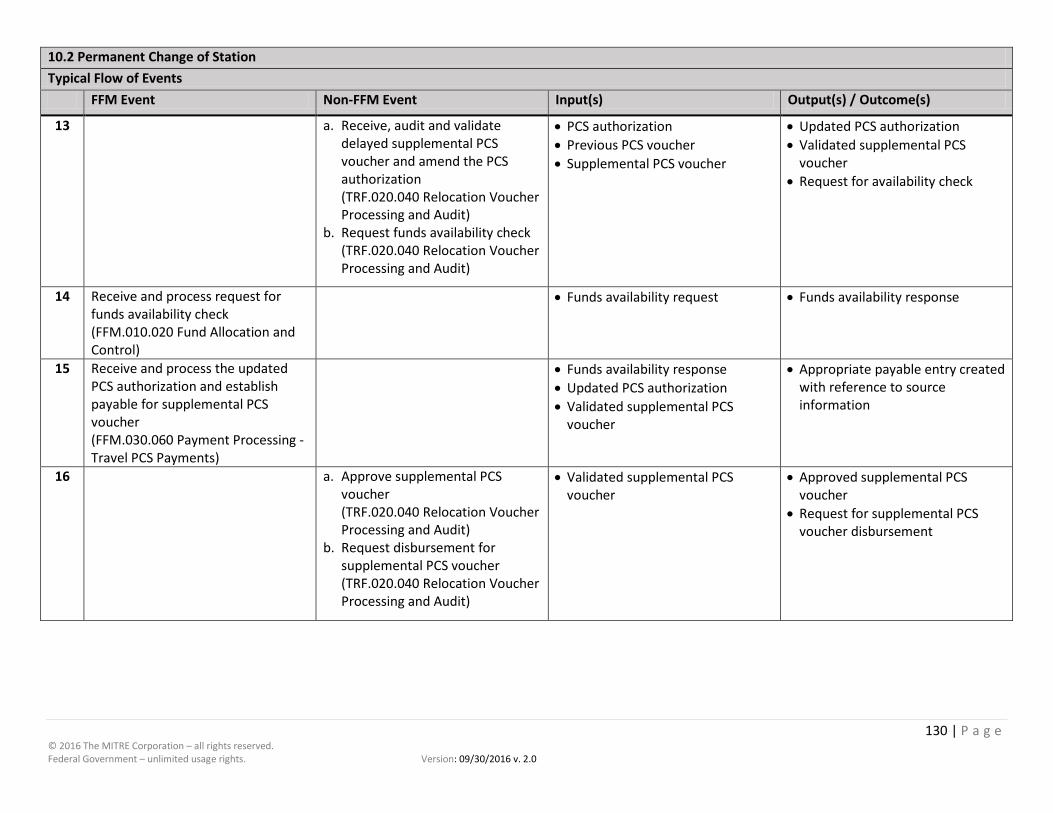

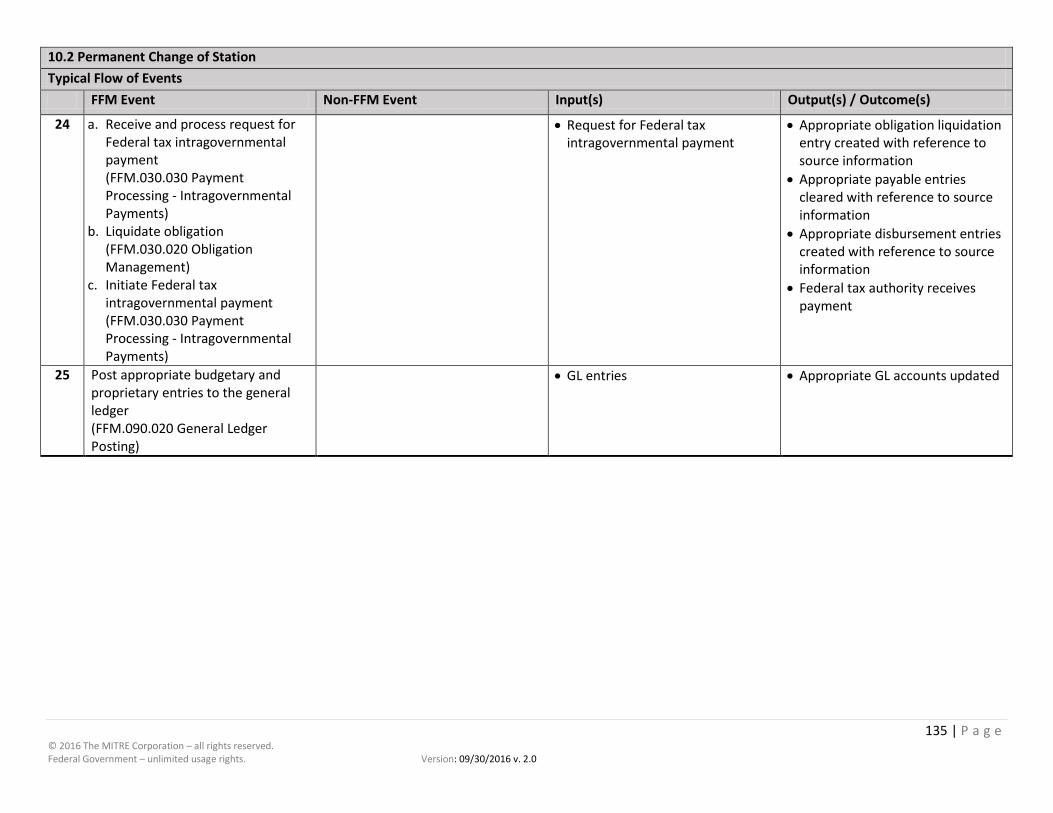

10.2 Permanent Change of Station ................................................................................................................................. 124

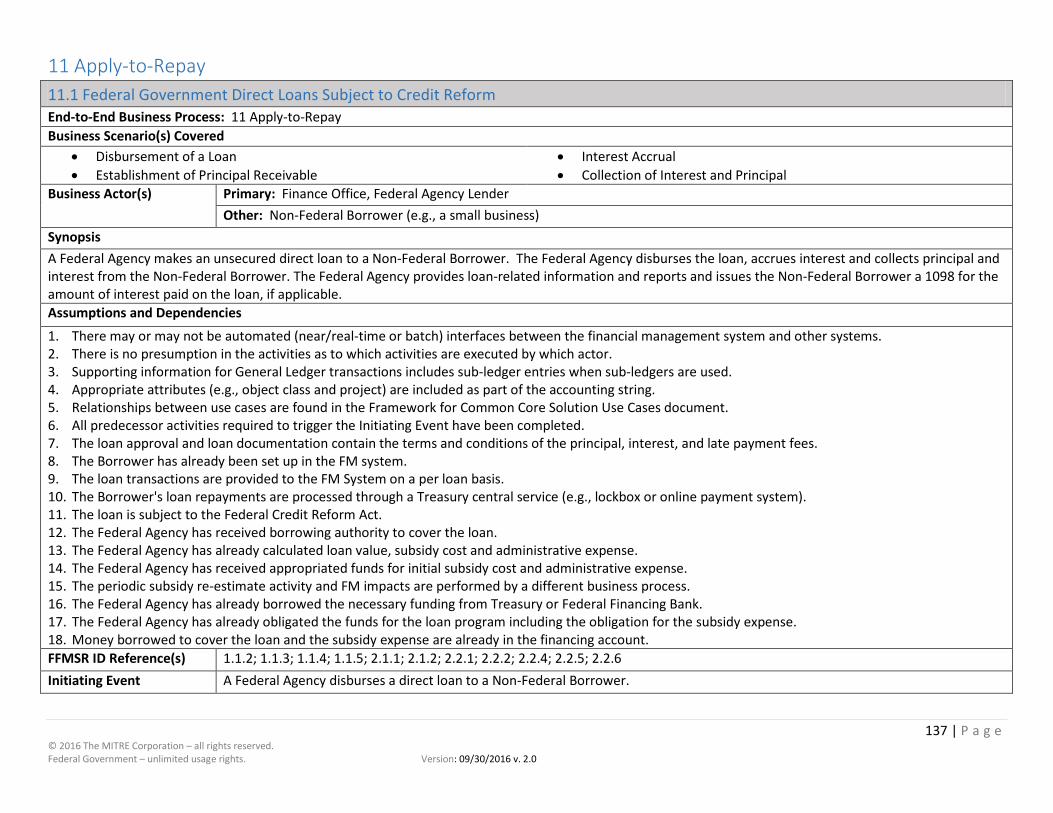

11 Apply-to-Repay .............................................................................................................................................................. 137

11.1 Federal Government Direct Loans Subject to Credit Reform ................................................................................. 137

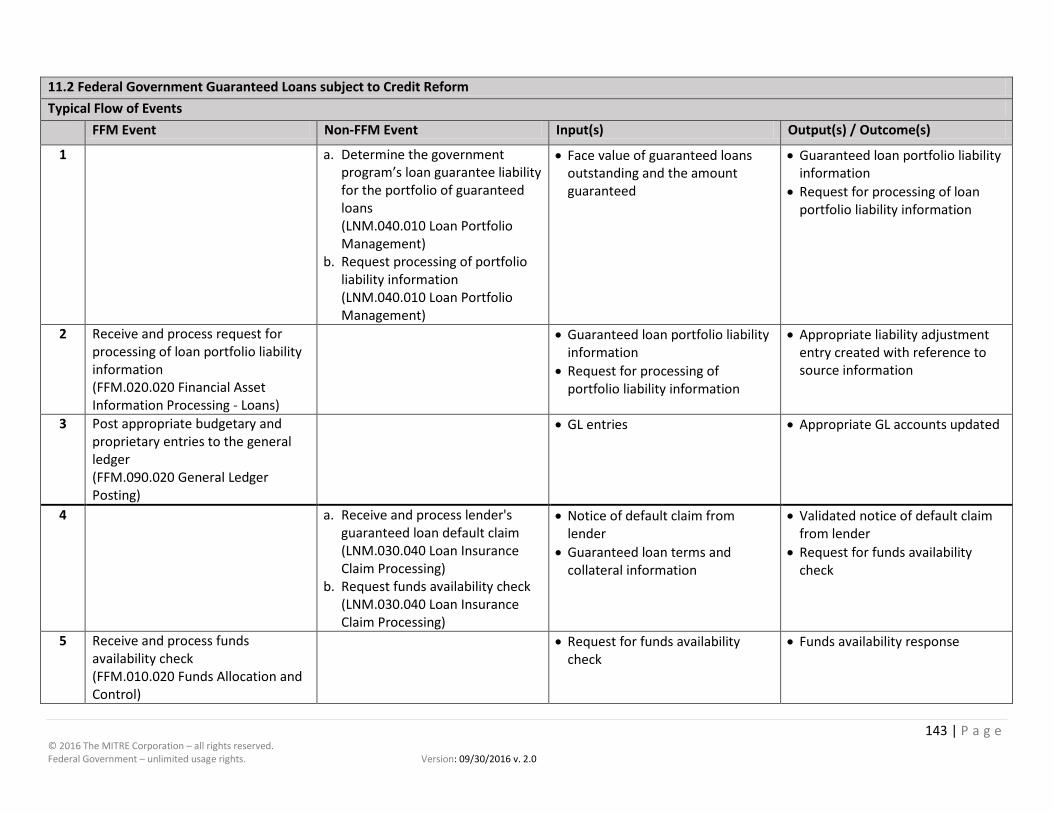

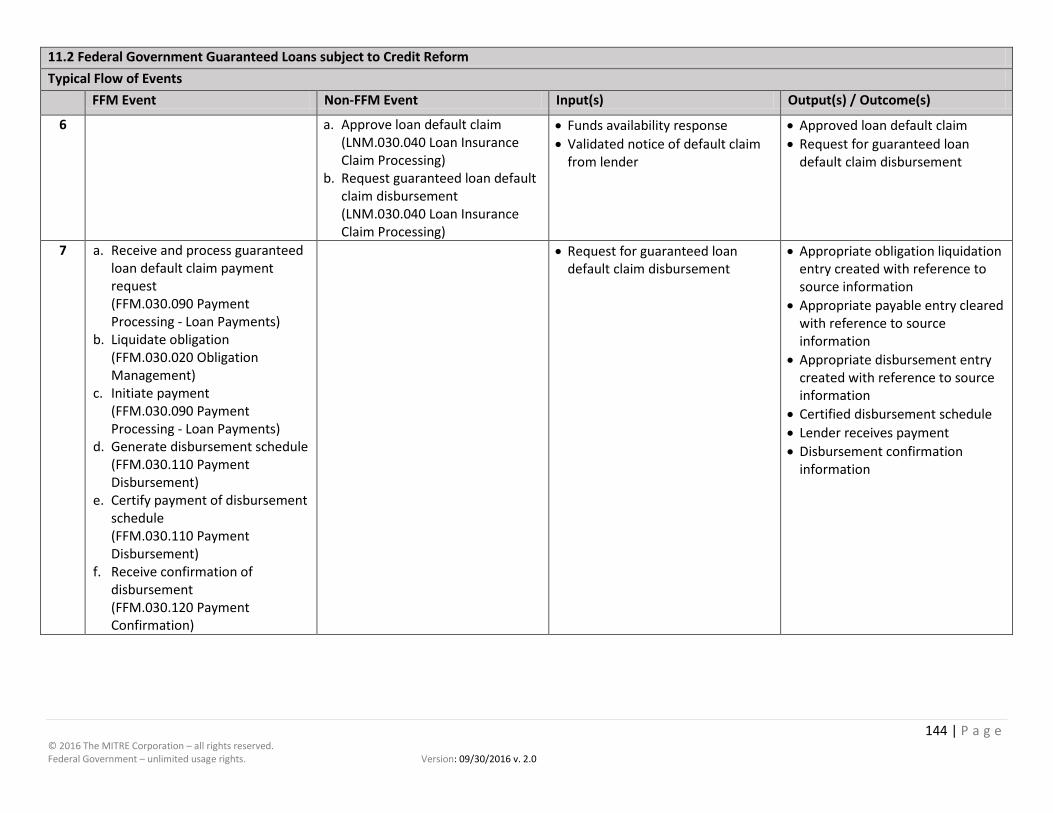

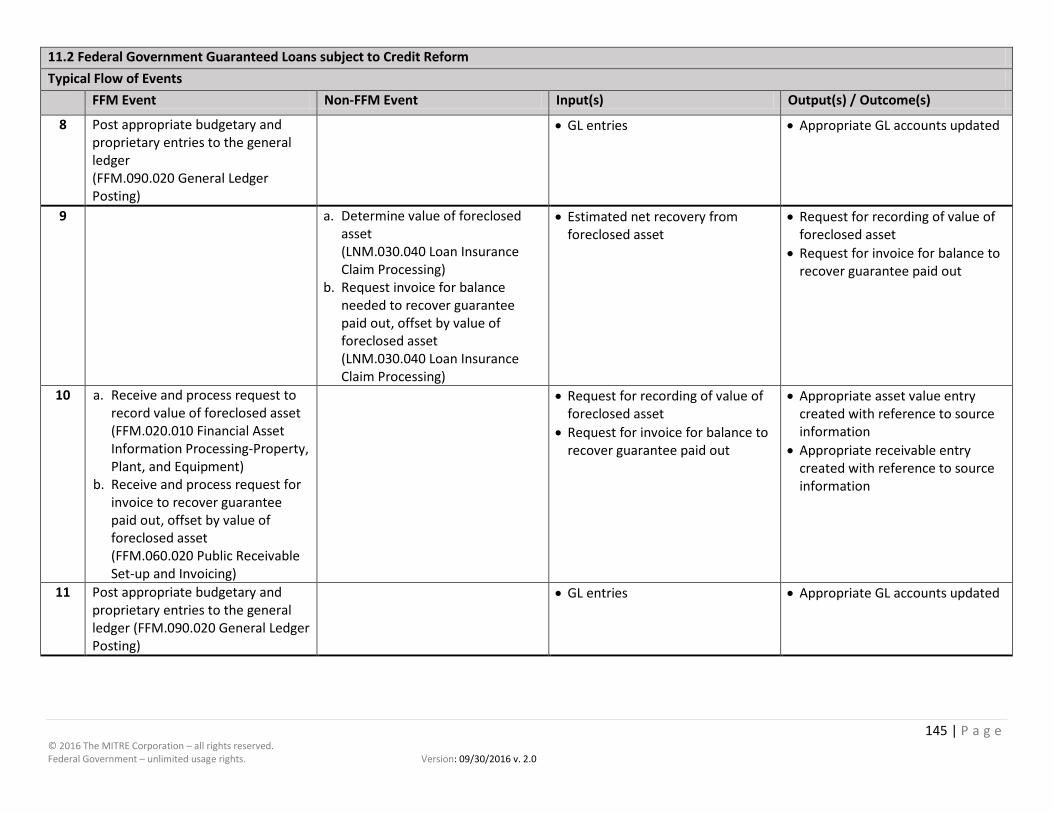

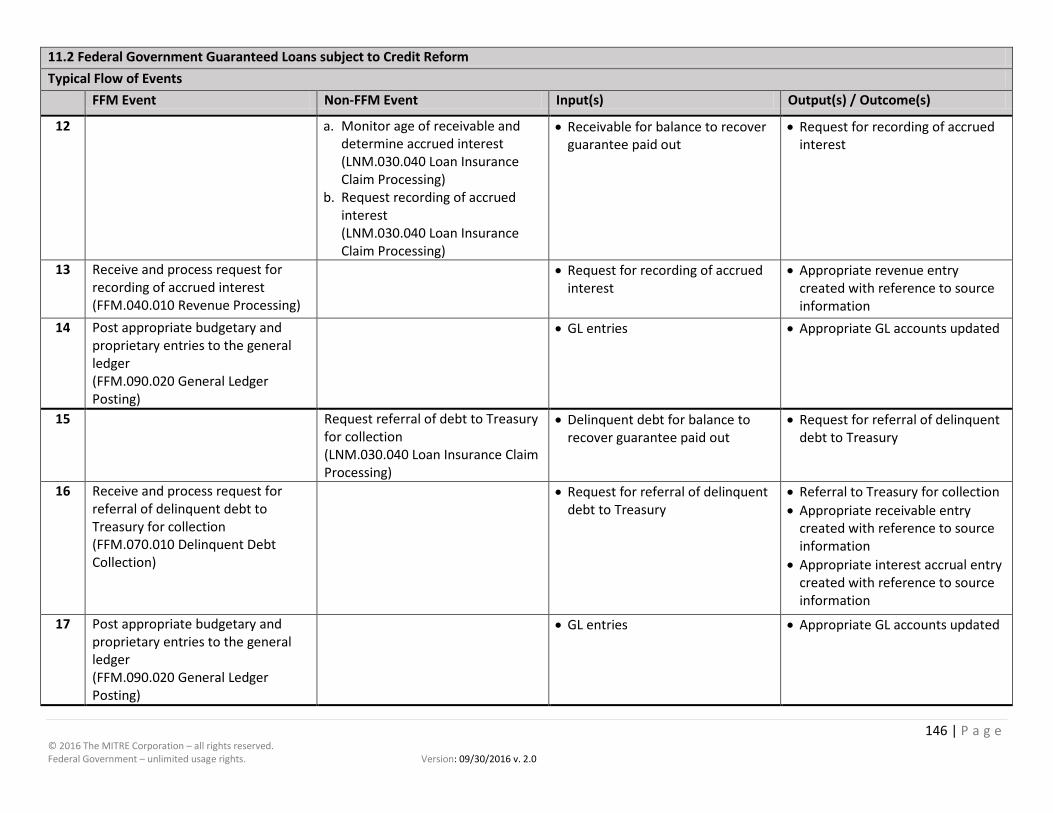

11.2 Federal Government Guaranteed Loans subject to Credit Reform ........................................................................ 142

Table of Figures Figure 1 Use Case Dependencies .......................................................................................................................................... 14 Figure 2 Use Case Demonstration Threads and End-to-End Processes ................................................................................ 15

4 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

Purpose The Federal Financial Management (FFM) Business Use Cases were developed as a tool to improve financial management, regardless of what system and agency user or who is providing the service. The Office of Financial Innovation and Transformation (FIT) initially leveraged the use cases for discussions between designated Federal Shared Service Providers (FSSPs) and prospective customers to better align customer needs with solutions. During the use case development process, stakeholders said that there are broader applications for these documents.

The purpose of this document is to introduce the key components used to develop the FFM Business Use Cases and provide an inventory of the FFM Business Use Cases and associated Business Scenarios developed to date.

End-to-End Business Processes An End-to-End Business Process identifies a start-to-finish outcome required by the business unit customer of mission support services (e.g., a program office). The End-to-End Business Process provides the context for executing financial management services. The list of End-to-End Business Processes used to develop the FFM Business Use Cases are:

1) Budget Formulation-to-Execution 2) Acquire-to-Dispose 3) Request-to-Procure 4) Procure-to-Pay 5) Bill-to-Collect 6) Record-to-Report

7) Agree-to-Reimburse 8) Apply-to-Perform 9) Hire-to-Retire 10) Book-to-Reimburse 11) Apply-to-Repay

Service Area, Function and Activity Listing Service Areas are the administrative and support domains which provide services that enable service customers (e.g., program offices) to deliver on their mission and accomplish End-to-End Business Processes. A Service Function is a further breakdown of an administrative or mission-support Service Area into categories of services provided to service customers. Within a Service Function, Service Activities are the processes that provide identifiable outputs/outcomes to service customers.

Most of the End-to-End Business Processes require integration across multiple Service Areas/Functions/Activities to achieve the business outcome. In addition to Financial Management, the other Services Areas contributing to the completion of each End-to-End Business Process are identified in the Federal Financial Management Inventory of Business Use Cases and Scenarios.

Business Scenarios Business Scenarios identify differing situations or conditions that occur when executing an End-to-End Business Process and reflect the scope and complexity of Federal government agency missions. Business Scenarios also define various business conditions that would cause the FFM solution functionality to be exercised in a different order or with different business information. For example, the Procure-to-Pay Business Scenario for a complex software system is different than for a purchase card. Business Scenarios are categorized as follows:

• Level 1 (L1): Affects most Federal agencies and/or impacts a large transaction volume or dollar value within the Federal government

• Level 2 (L2): Affects multiple Federal agencies and requires some specialized processing from the service consumer or auditor perspective

• Level 3 (L3): Affects a few Federal agencies and requires unique processing, but is mandated by legislation.

5 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

Business Use Cases Within an End-to-End Business Process, Business Use Cases are formed by combining Business Scenarios and Service Areas/Functions/Activities. Business Use Cases:

• identify the interactions between Service Areas/Functions/Activities.

• identify the business events to be accomplished and the business information expected to be provided/received/processed.

• are agnostic of whether the events in the Business Use Case are automated, semi-automated or manually accomplished.

Federal Financial Management Inventory of Business Use Cases and Scenarios The list of FFM Business Use Cases developed to date, and the Business Scenarios included in each Business Use Case, are presented in the tables that follow. Also included in the tables is the list of Requested Business Scenarios which have been identified for potential inclusion in future Business Use Cases.

Process 1. Budget Formulation-to-Execution

Service Area(s): Budget Formulation (BFM); Financial Management (FFM) Business Use Cases and Associated Business Scenario(s) 1.1 Budget Authority Set-Up (L1)

• Funds Control at Appropriation, Apportionment, Allotment, Allocation, Suballocation 1, and Suballocation 2 Levels

• Accounting Segments of Treasury Account Symbol/Fund, Organization, Program, Project, and Activity • Discretionary Appropriated Funds • Single Year, Multi-Year, and No Year Appropriations • Program Allocation Exceeding Organization Allotment

1.2 Spending Authority from Offsetting Collections (Reimbursables) (L1)

• Reimbursable Authority • Revolving Funds

1.3 Budget Authority Transfers (L1)

• Appropriation Transfers • Non-Expenditure Transfers

1.4 Special Authorities (L3)

• Special Authority from Off Setting Collections • Donation Revenues, Foreign and Domestic • Borrowing Authority • Contract Authority • Special Limitations from Budget Formulation • Parent-Child Funds Allocation Transfer • Cash Equivalent Transfers • Direct and Guaranteed Loan Authority • Liquidating Accounts

Requested Business Scenarios

6 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

• Continuing Resolution • Borrowing Authority

7 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

Process 2. Acquire-to-Dispose

Service Area(s): Acquisition (ACQ); Financial Management (FFM); Property Management (PRM) Business Use Cases and Associated Business Scenario(s) 2.1 Property, Plant, and Equipment (PP&E Assets) (L1)

• Acquiring a PP&E Asset • Leasing a PP&E Asset • Depreciation of a PP&E Asset • Disposing of a PP&E Asset • Replacing an Asset

2.2 Bulk Purchases (L1)

• Bulk Purchases • Transfers between Department Components

2.3 Complex Systems (L2)

• Complex Systems • Internal Use Software • Work in Progress • Increase Life and Value of Asset • Enhancing an Asset

2.4 Real Property (L3)

• Heritage Assets • Stewardship Land • Construction in Progress • Capitalization of Labor Costs • Environmental Hazardous Substances on/in Property • Impairment • Construction in Abeyance

Requested Business Scenarios

• Impairments, Lost/Stolen Items, and Excessed Items • Property Below the Capitalization Threshold • Operating Lease Arrangement • Leasehold Improvements • Bulk Purchase Capitalization Criteria Policies for purchases • Transfer of Funds Between the Warehouse and the Program Office • Bulk Purchases of COTS Software • Multiple Software Package Distribution • Useful Life of Software • Recurring Software Amortization • Software Under Construction • Scientific Equipment Under Construction • Real Property Under Construction • Real Property

8 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

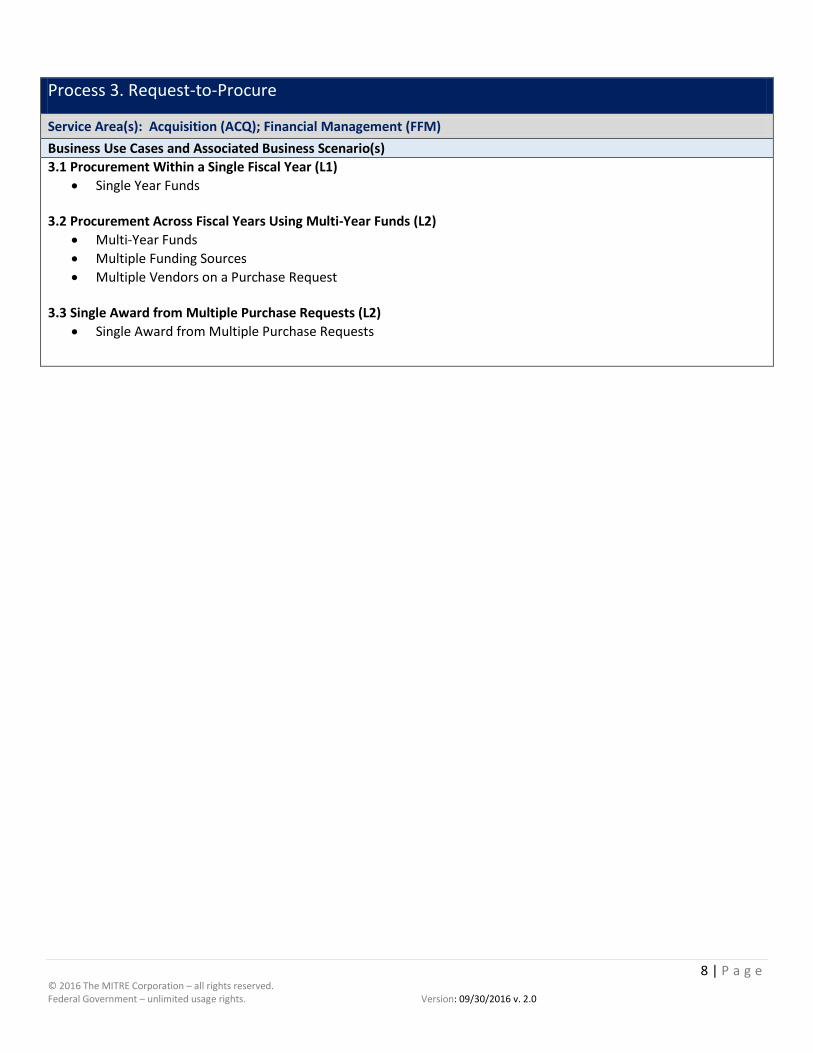

Process 3. Request-to-Procure

Service Area(s): Acquisition (ACQ); Financial Management (FFM) Business Use Cases and Associated Business Scenario(s) 3.1 Procurement Within a Single Fiscal Year (L1)

• Single Year Funds 3.2 Procurement Across Fiscal Years Using Multi-Year Funds (L2)

• Multi-Year Funds • Multiple Funding Sources • Multiple Vendors on a Purchase Request

3.3 Single Award from Multiple Purchase Requests (L2) • Single Award from Multiple Purchase Requests

9 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

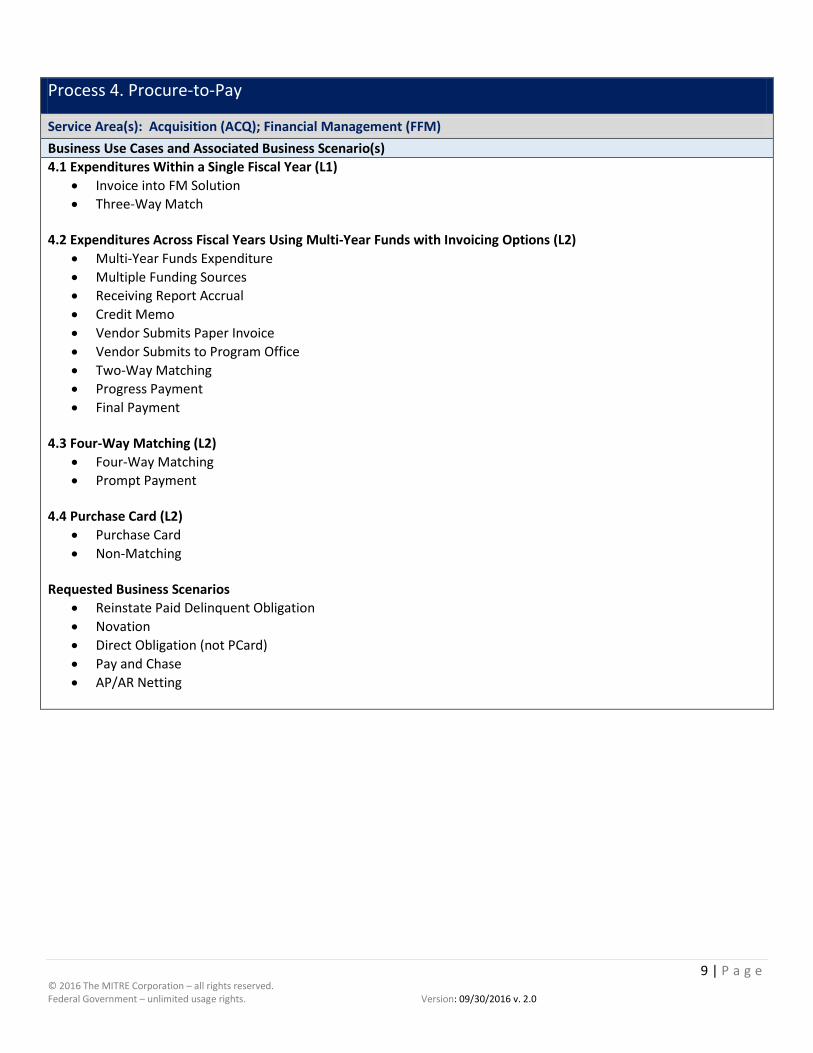

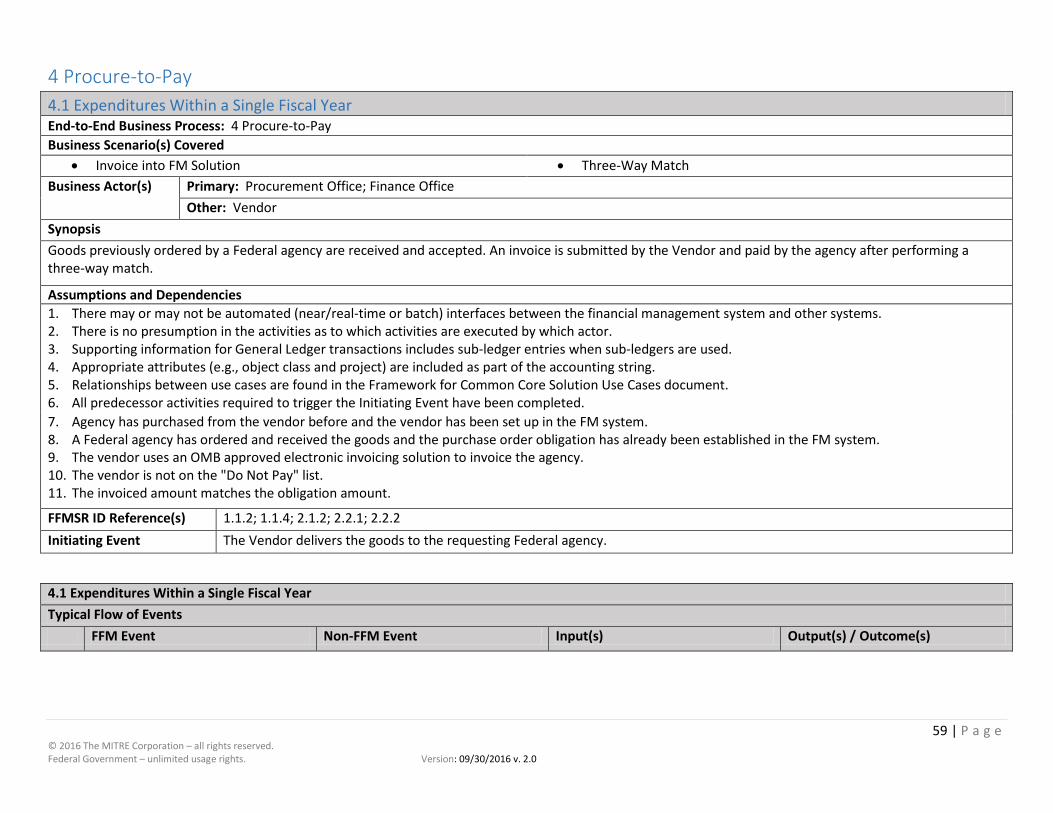

Process 4. Procure-to-Pay

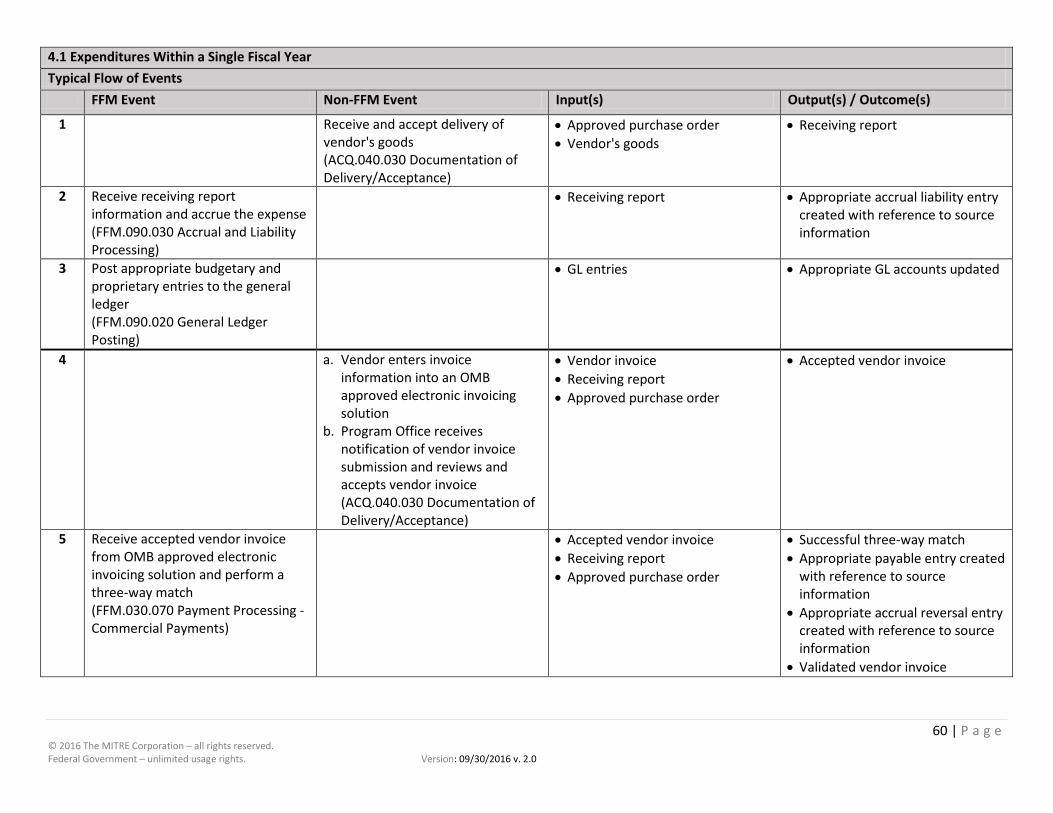

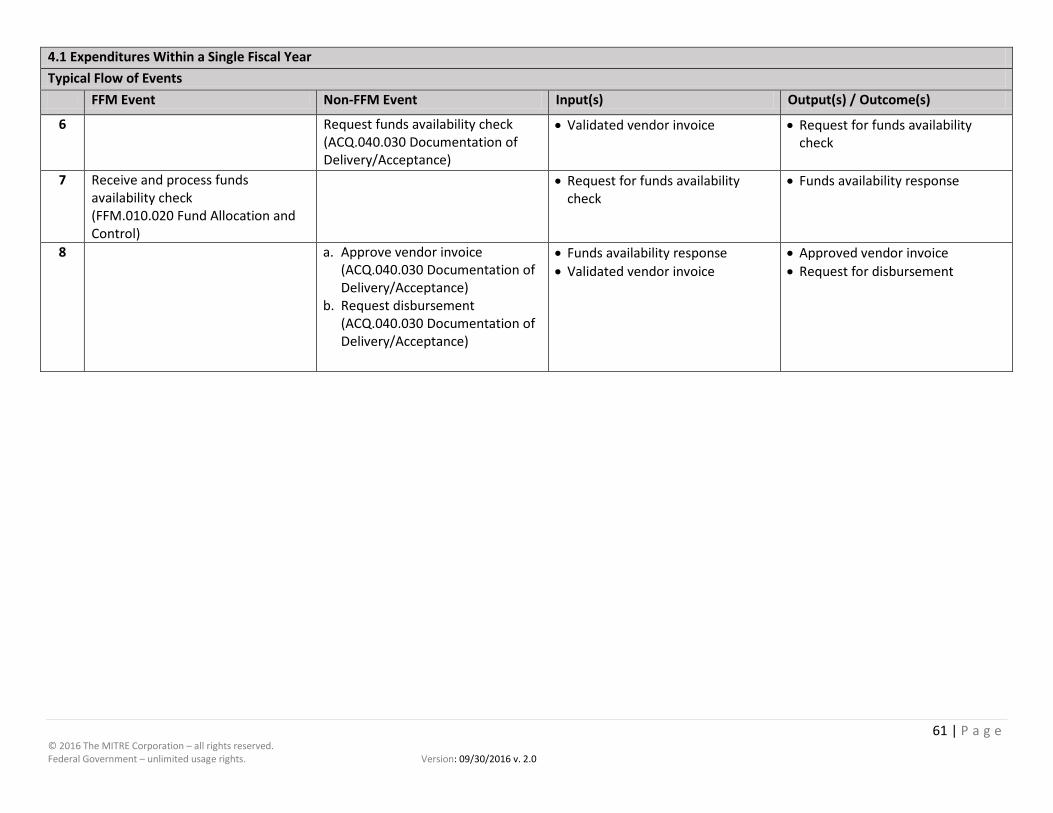

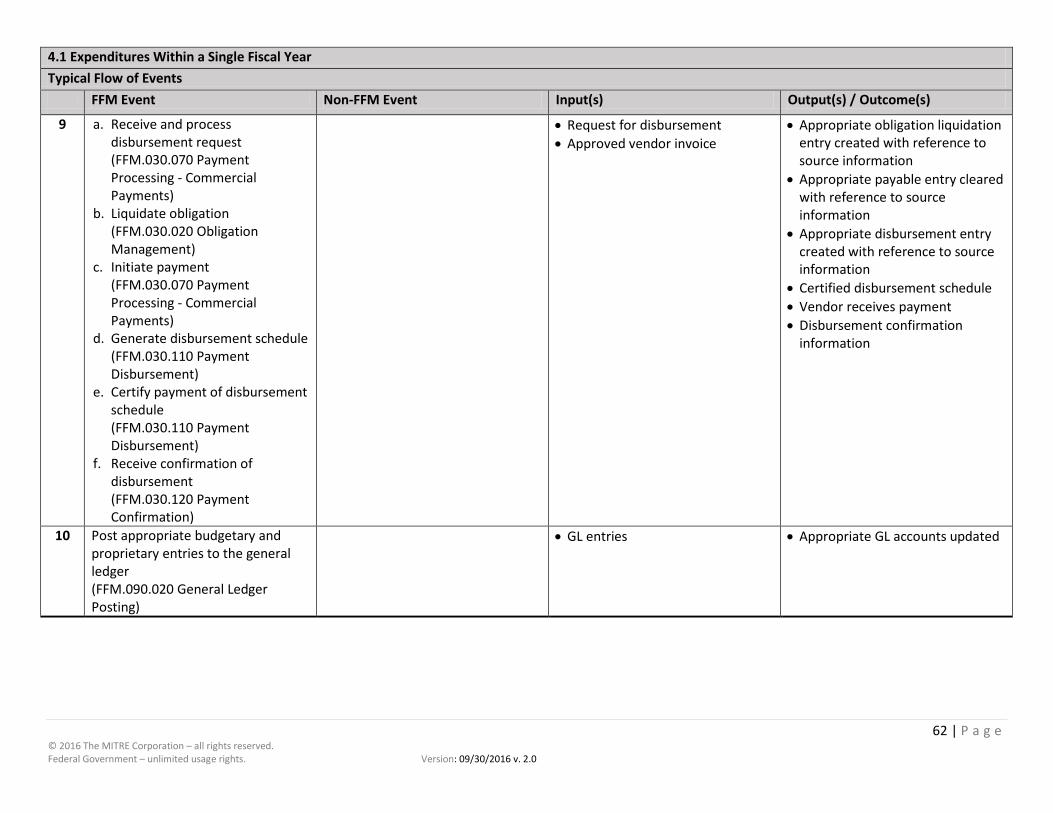

Service Area(s): Acquisition (ACQ); Financial Management (FFM) Business Use Cases and Associated Business Scenario(s) 4.1 Expenditures Within a Single Fiscal Year (L1)

• Invoice into FM Solution • Three-Way Match

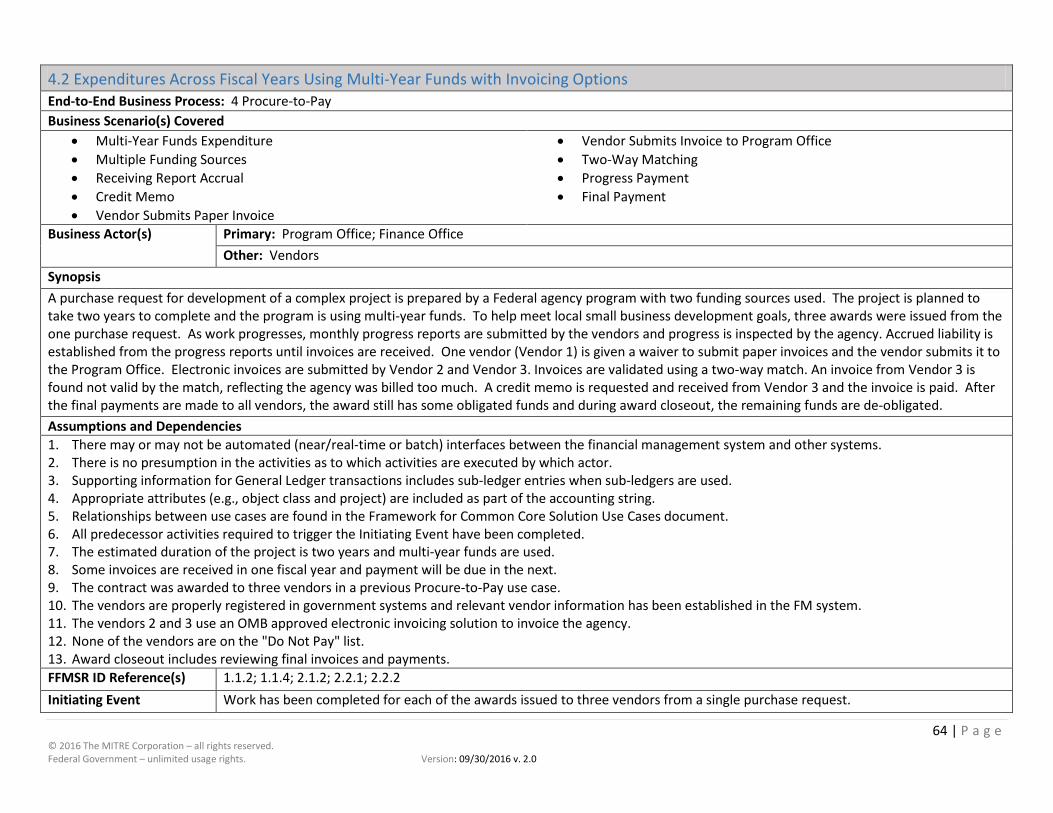

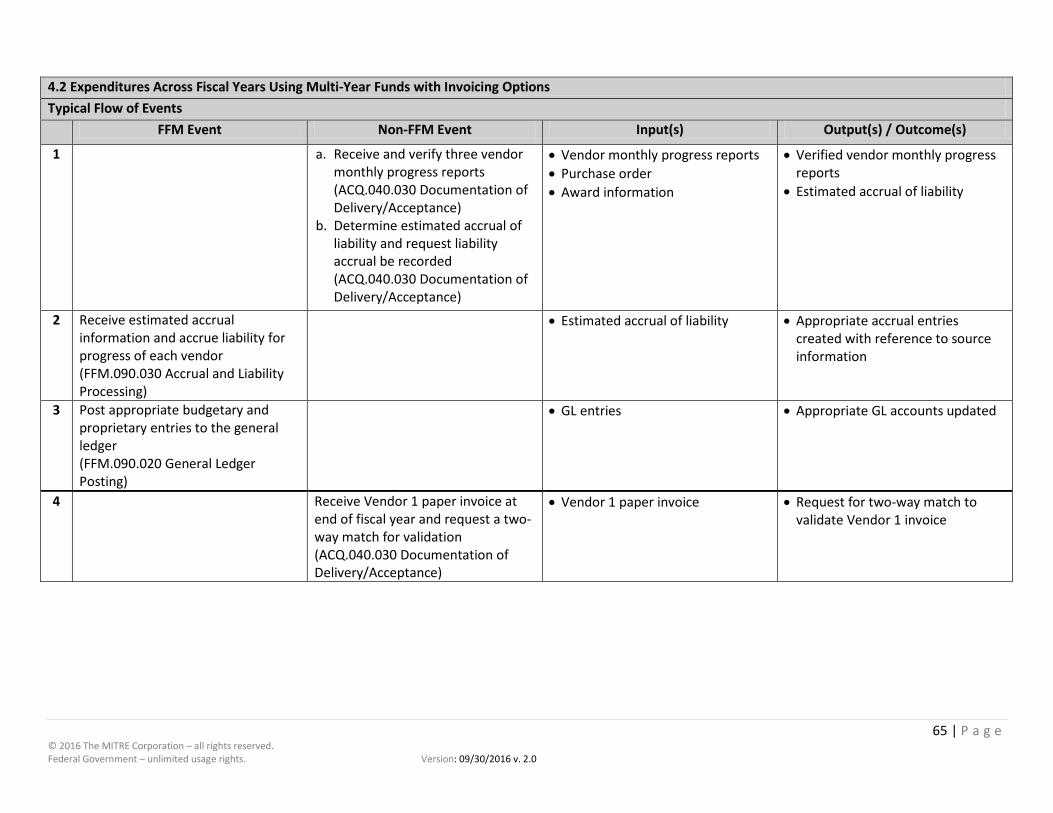

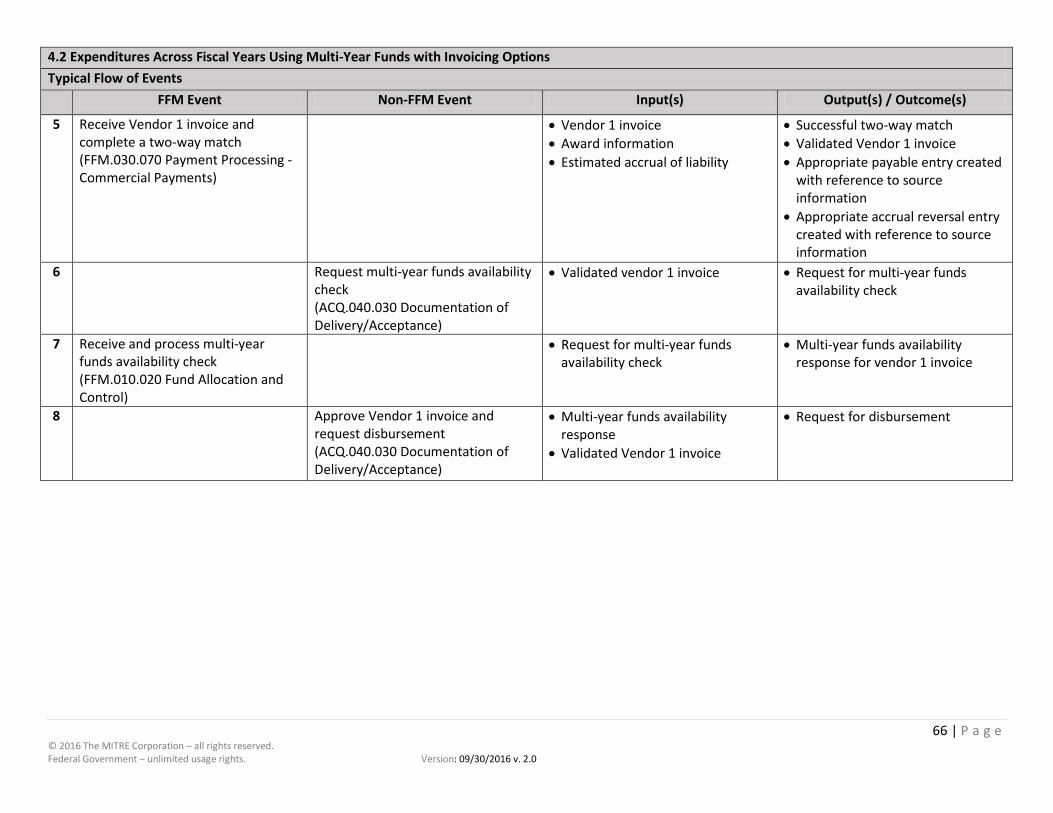

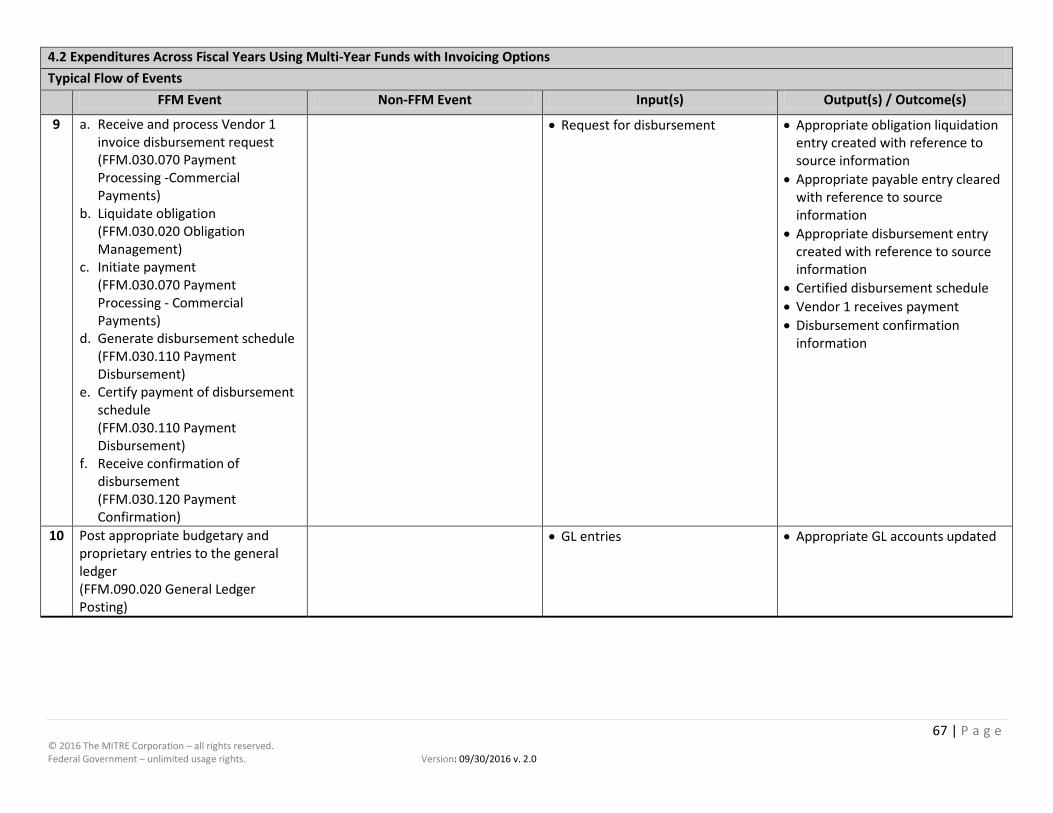

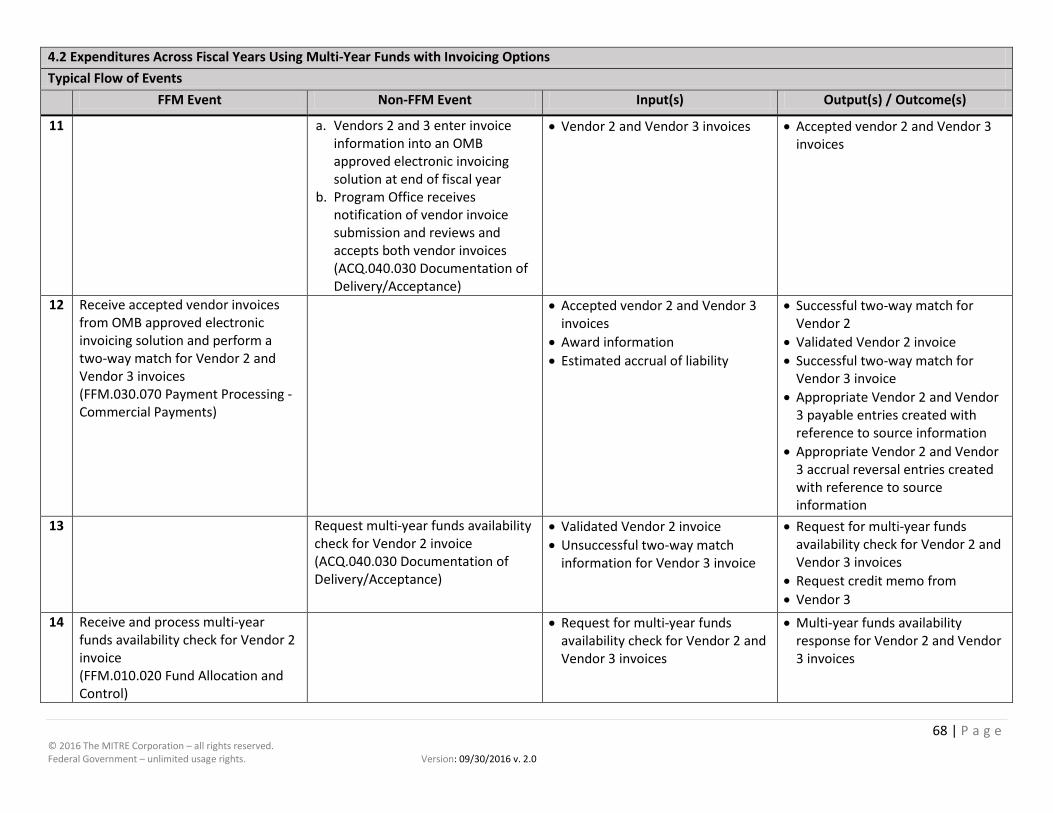

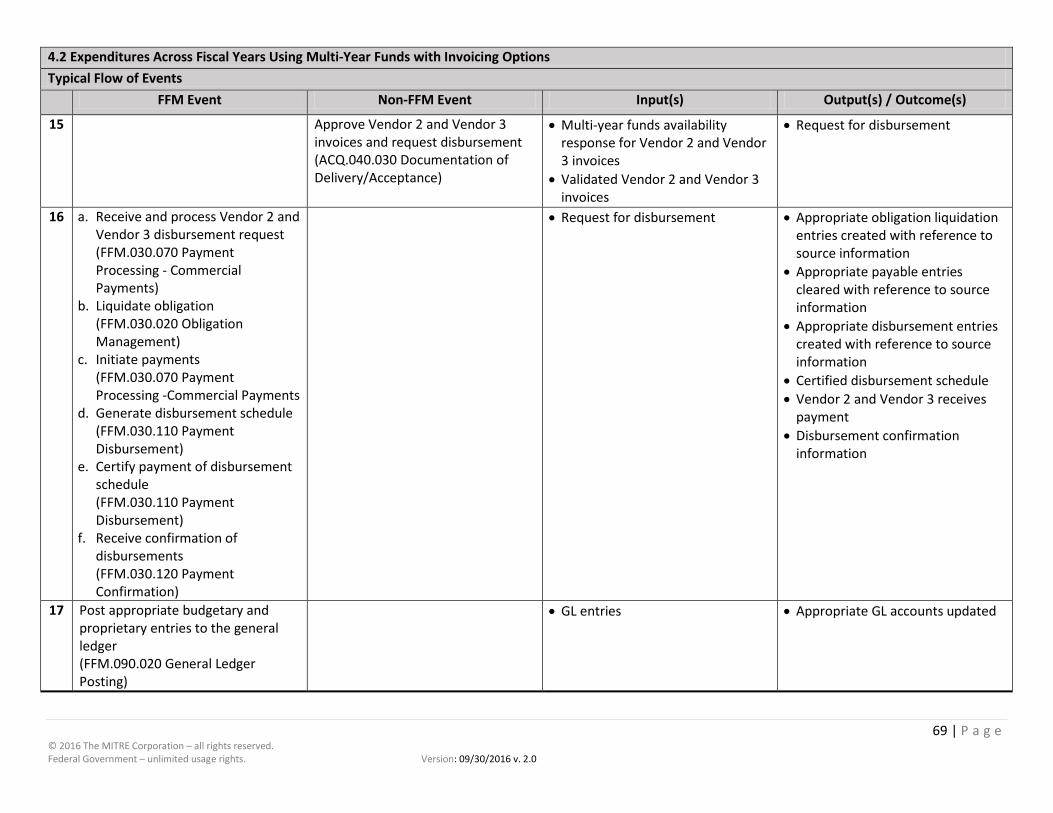

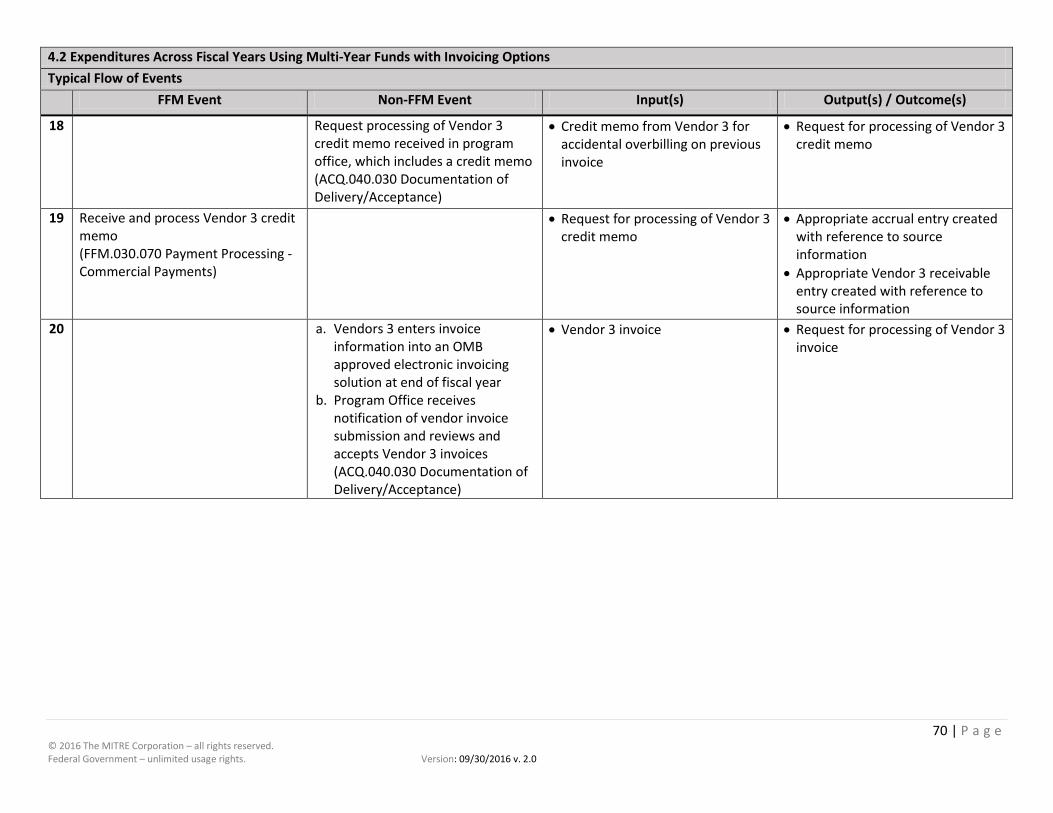

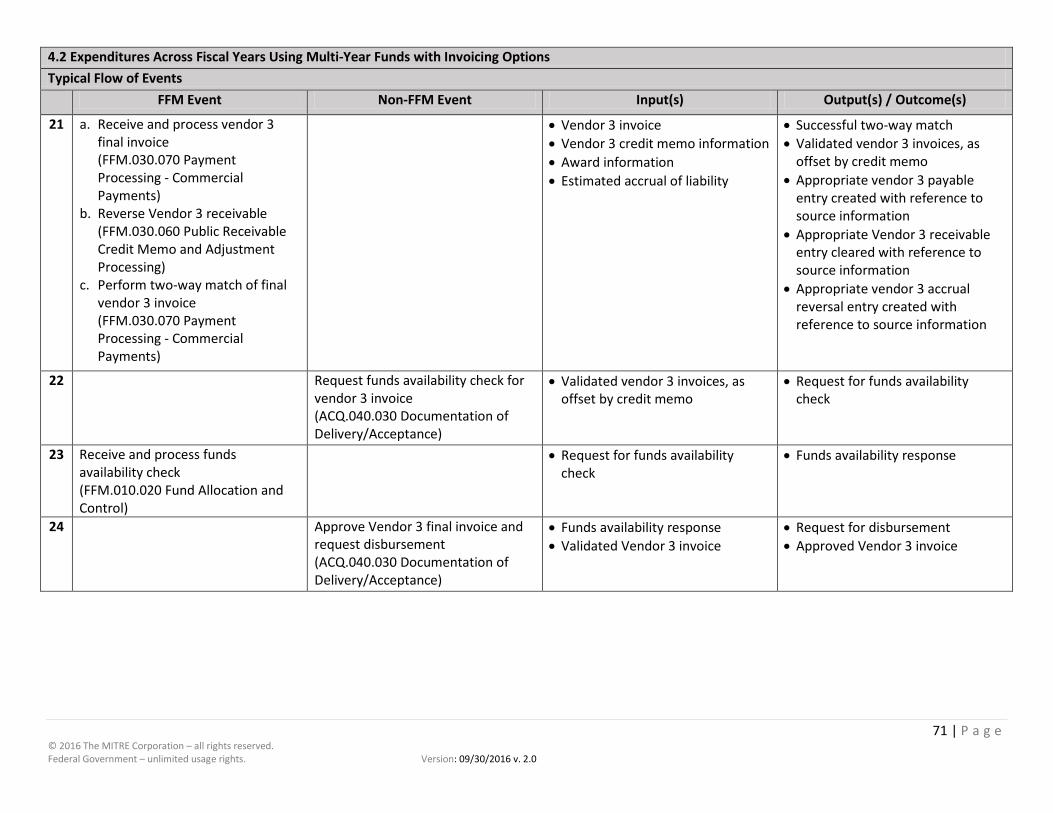

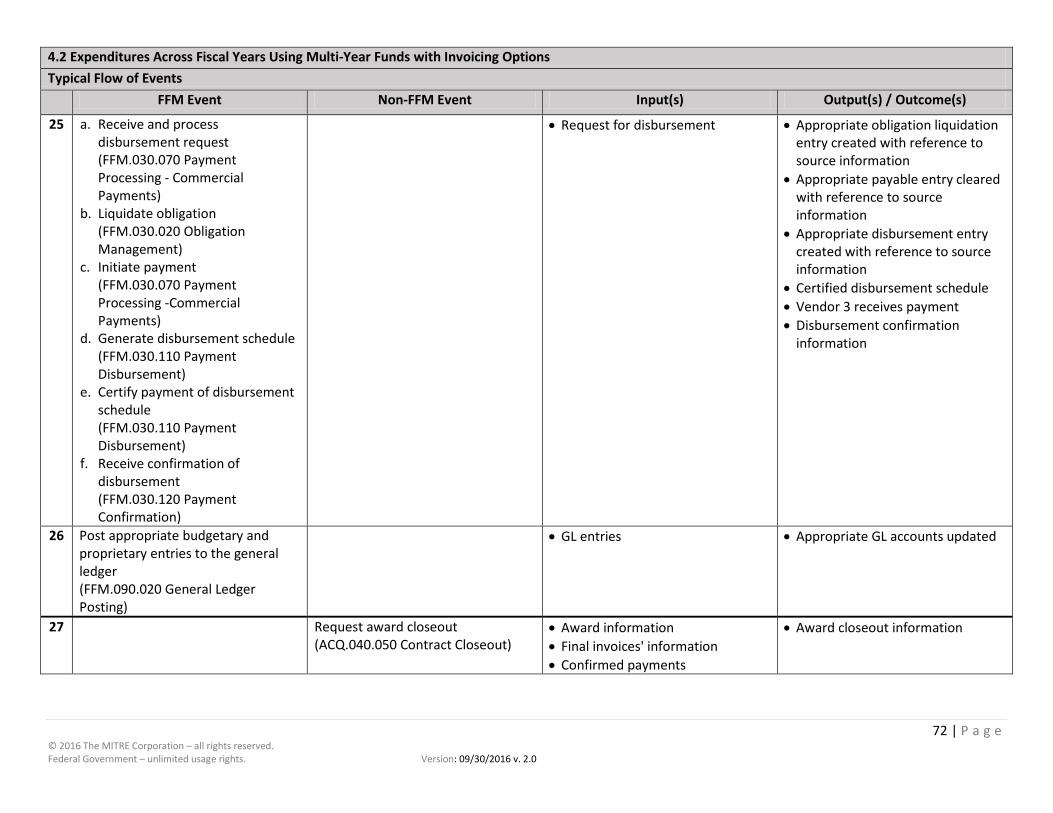

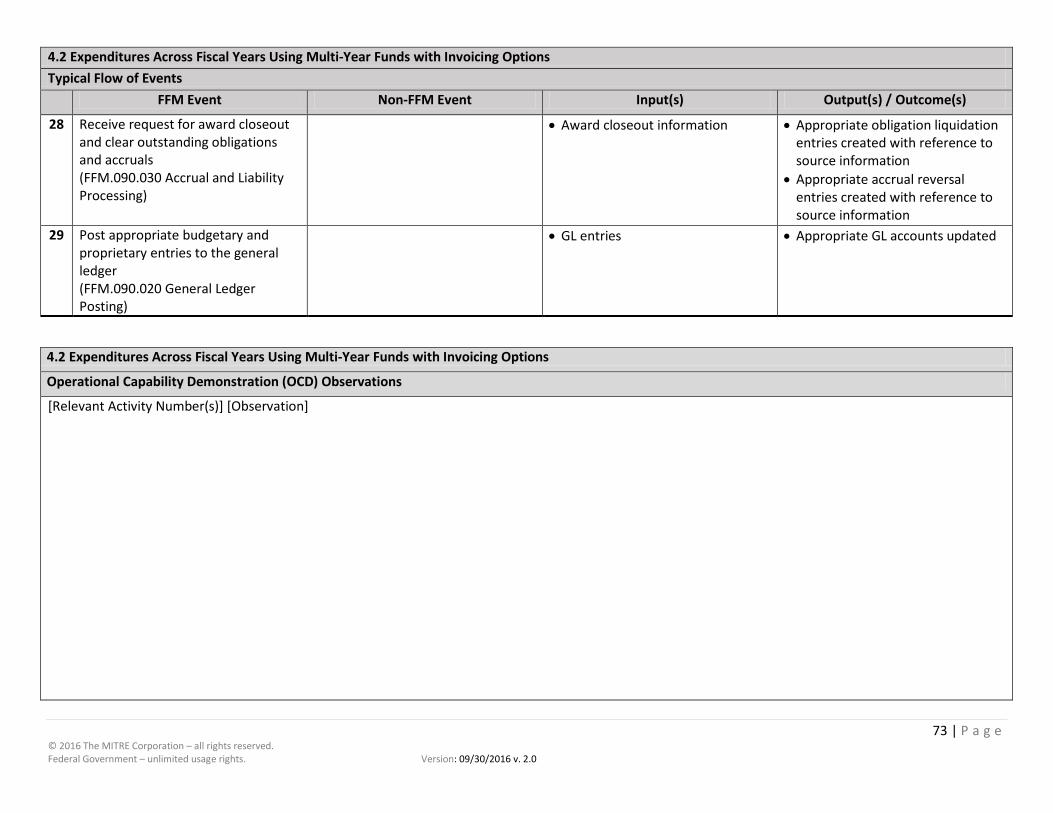

4.2 Expenditures Across Fiscal Years Using Multi-Year Funds with Invoicing Options (L2)

• Multi-Year Funds Expenditure • Multiple Funding Sources • Receiving Report Accrual • Credit Memo • Vendor Submits Paper Invoice • Vendor Submits to Program Office • Two-Way Matching • Progress Payment • Final Payment

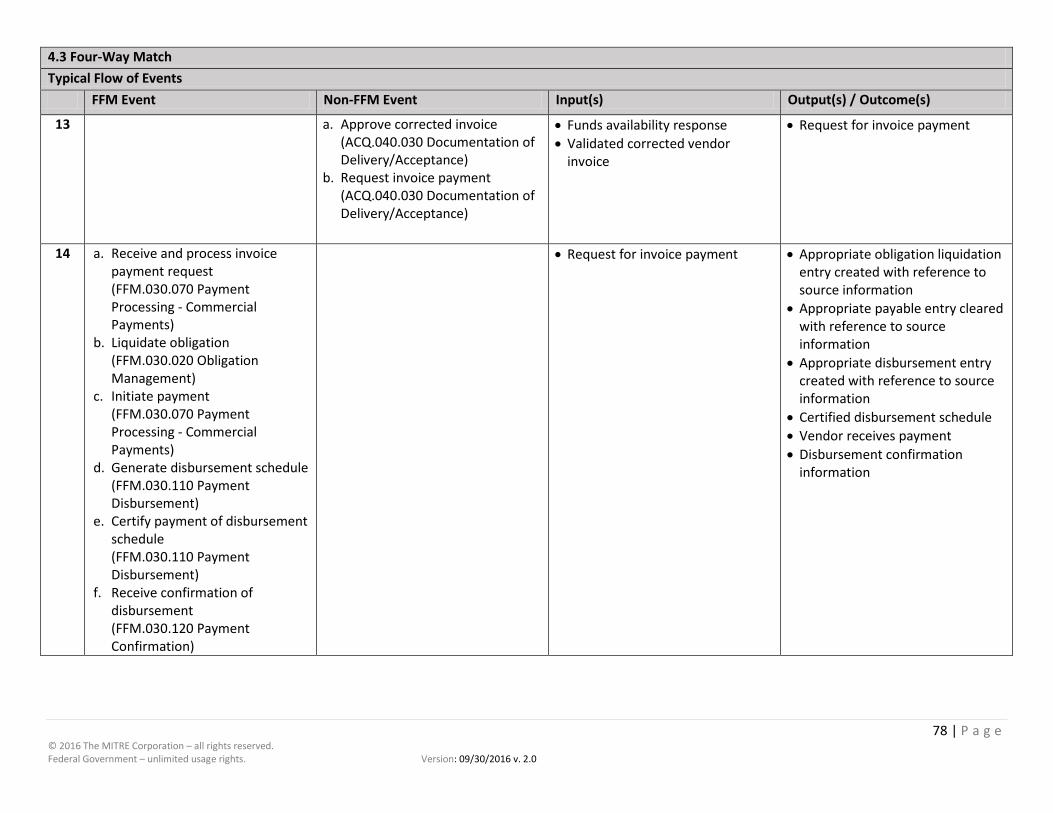

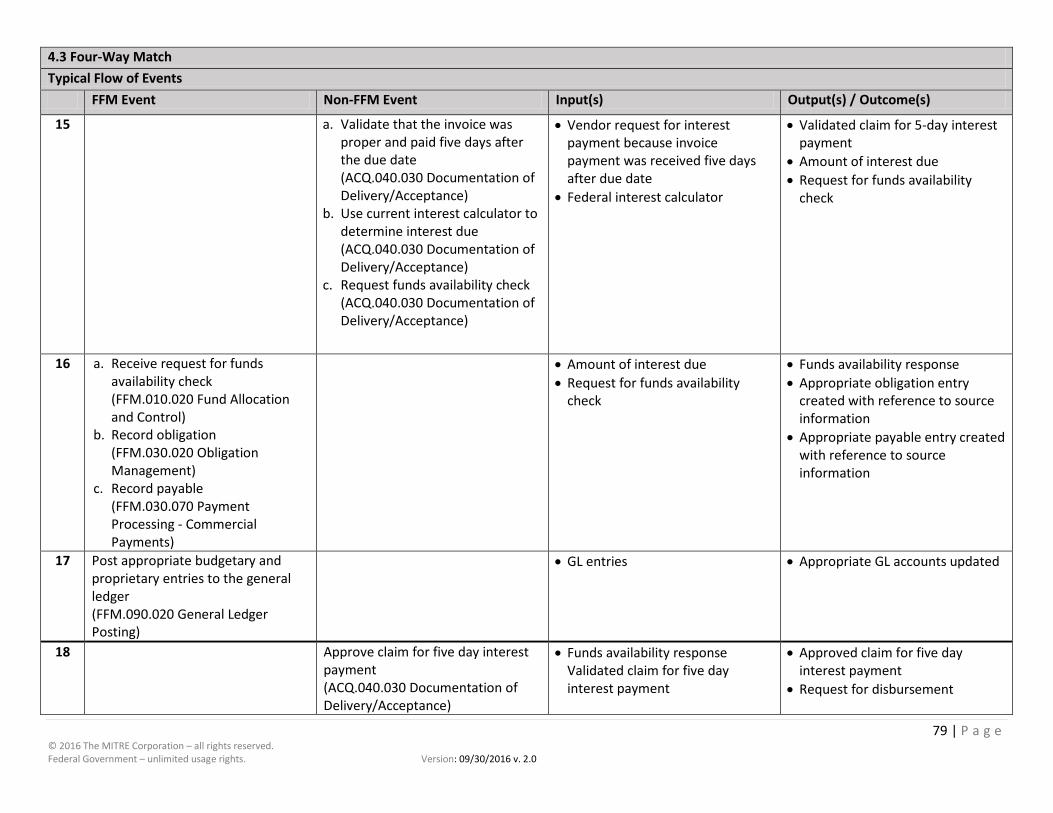

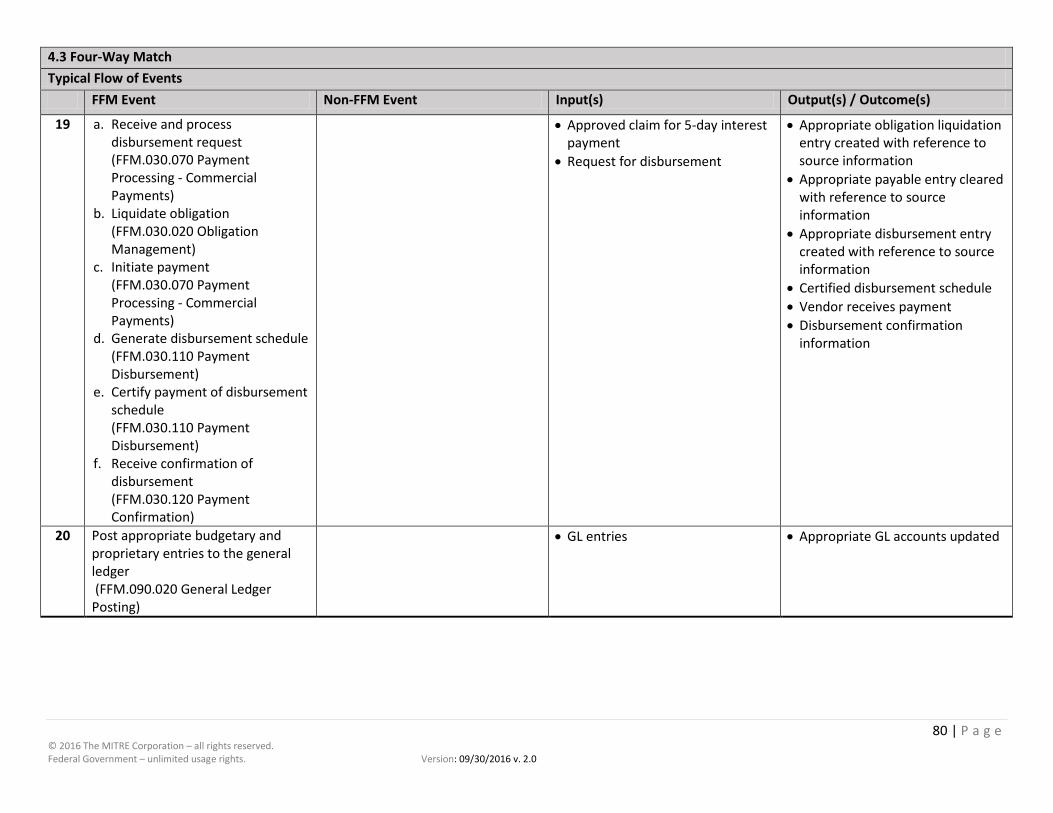

4.3 Four-Way Matching (L2)

• Four-Way Matching • Prompt Payment

4.4 Purchase Card (L2)

• Purchase Card • Non-Matching

Requested Business Scenarios • Reinstate Paid Delinquent Obligation • Novation • Direct Obligation (not PCard) • Pay and Chase • AP/AR Netting

10 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

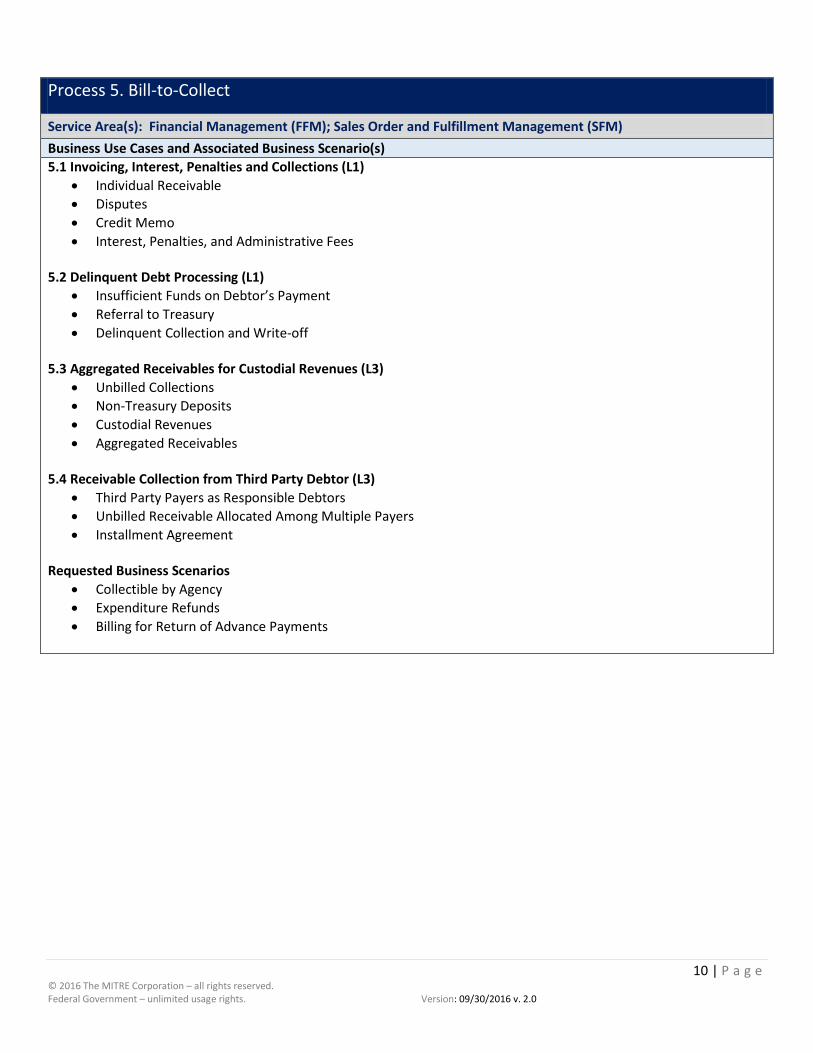

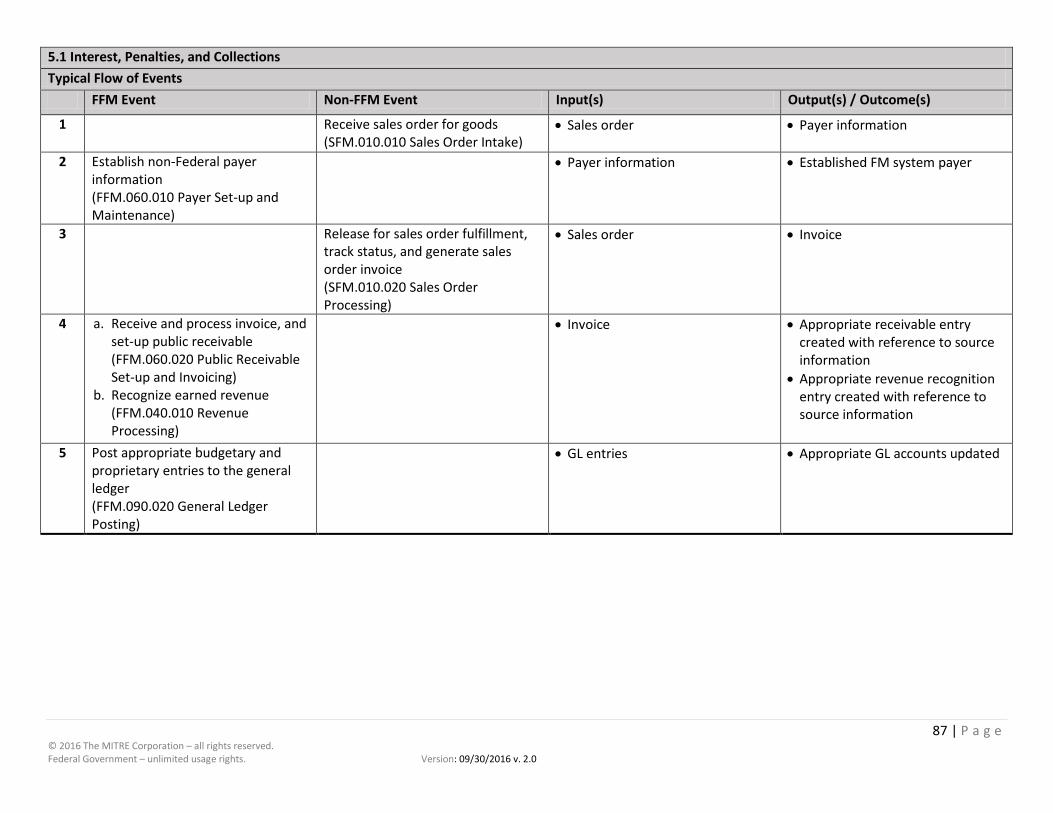

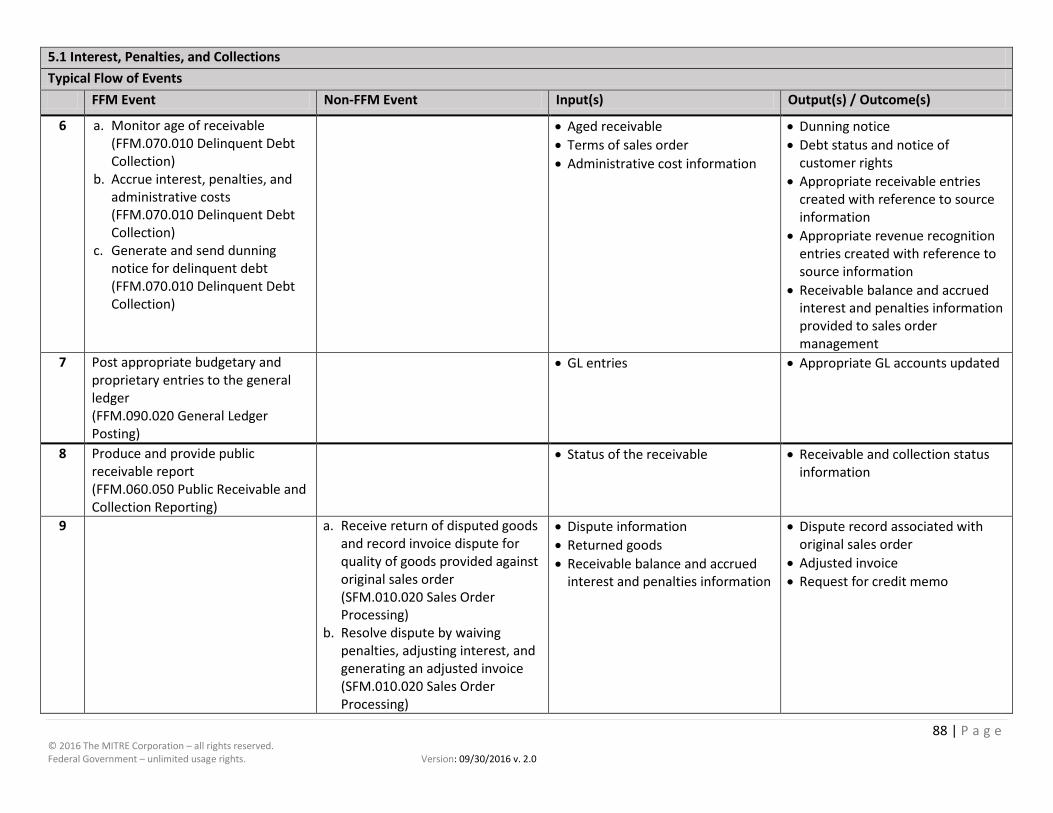

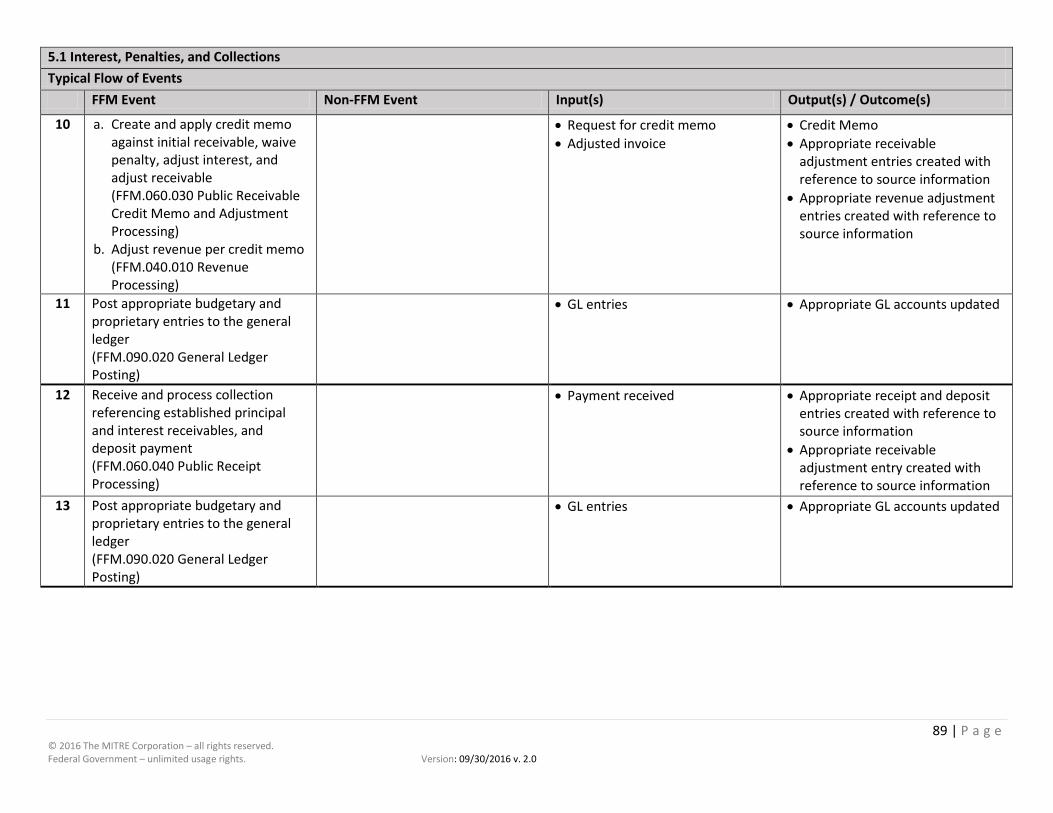

Process 5. Bill-to-Collect

Service Area(s): Financial Management (FFM); Sales Order and Fulfillment Management (SFM) Business Use Cases and Associated Business Scenario(s) 5.1 Invoicing, Interest, Penalties and Collections (L1)

• Individual Receivable • Disputes • Credit Memo • Interest, Penalties, and Administrative Fees

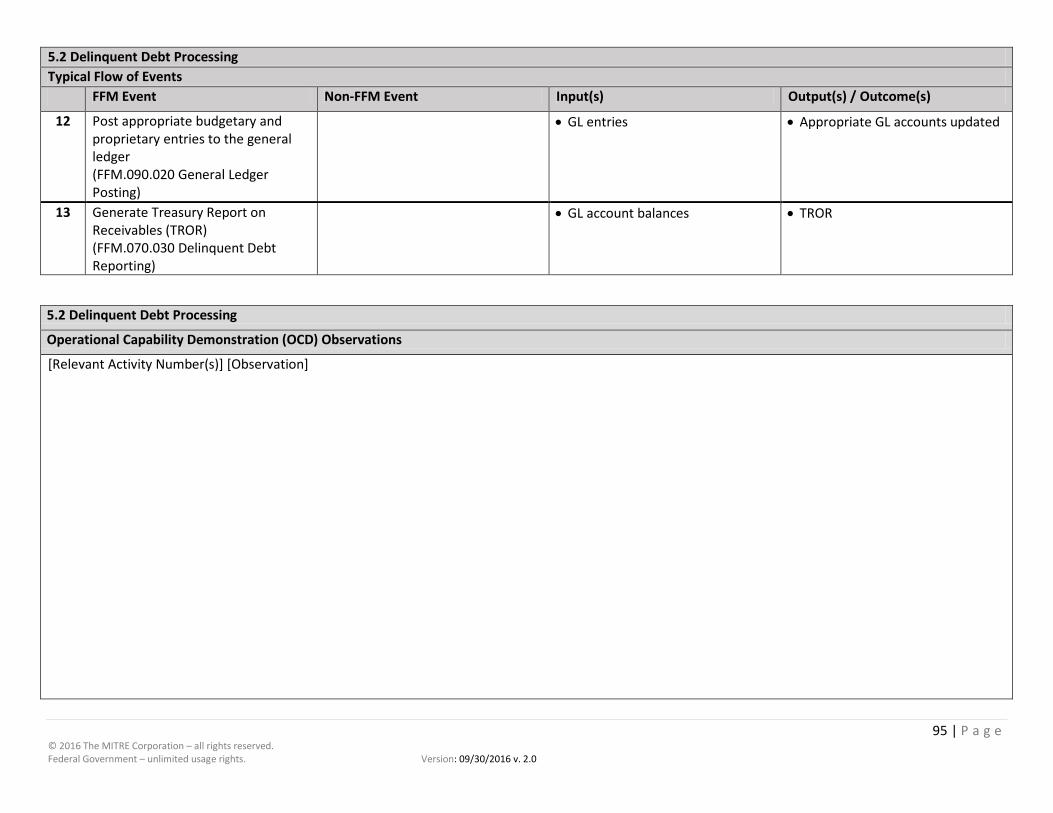

5.2 Delinquent Debt Processing (L1)

• Insufficient Funds on Debtor’s Payment • Referral to Treasury • Delinquent Collection and Write-off

5.3 Aggregated Receivables for Custodial Revenues (L3)

• Unbilled Collections • Non-Treasury Deposits • Custodial Revenues • Aggregated Receivables

5.4 Receivable Collection from Third Party Debtor (L3)

• Third Party Payers as Responsible Debtors • Unbilled Receivable Allocated Among Multiple Payers • Installment Agreement

Requested Business Scenarios • Collectible by Agency • Expenditure Refunds • Billing for Return of Advance Payments

11 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

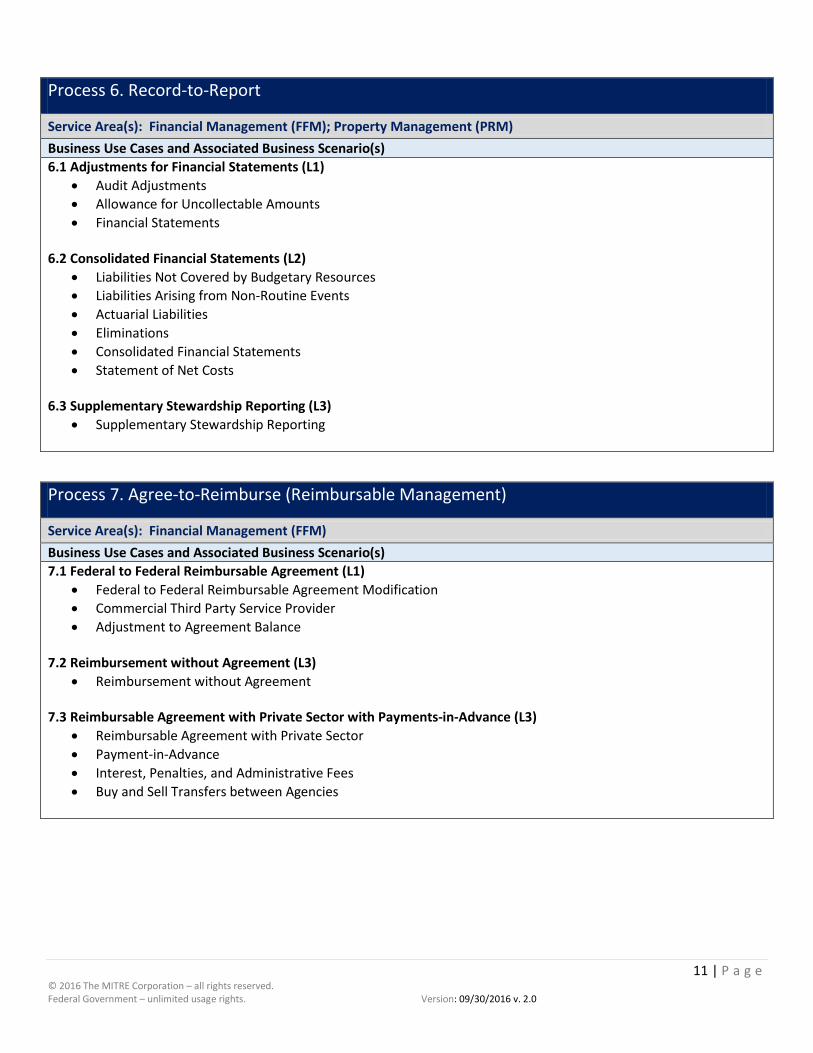

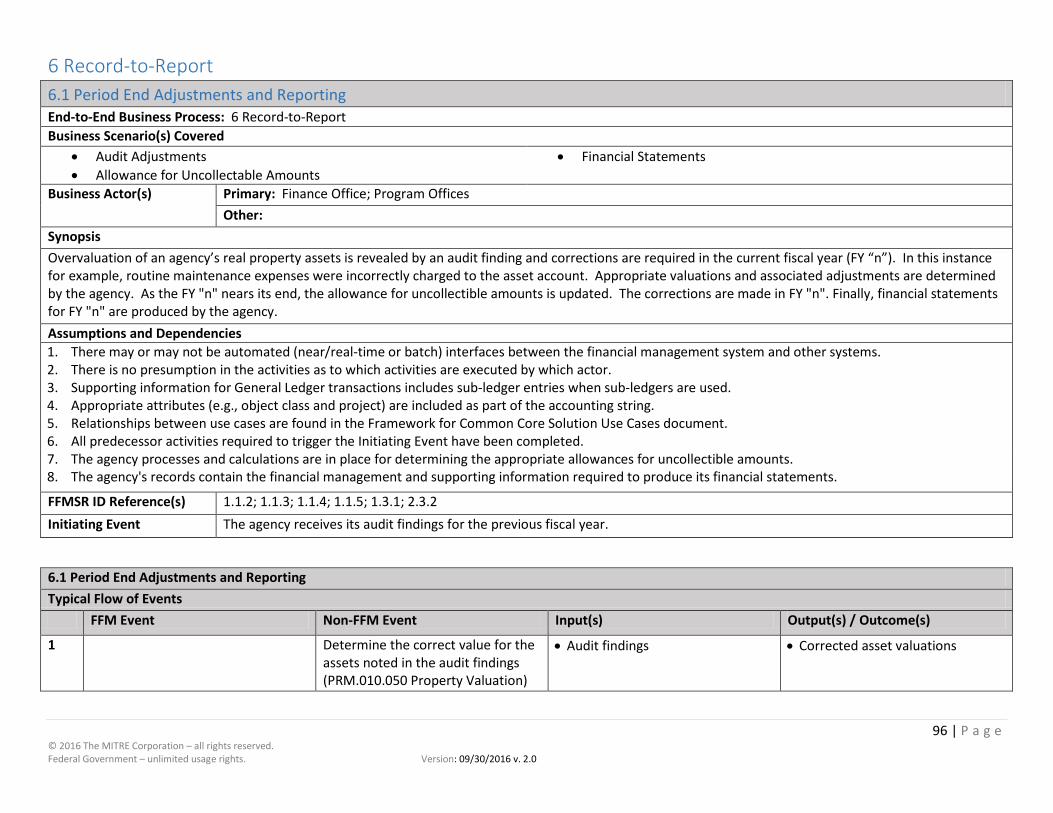

Process 6. Record-to-Report

Service Area(s): Financial Management (FFM); Property Management (PRM) Business Use Cases and Associated Business Scenario(s) 6.1 Adjustments for Financial Statements (L1)

• Audit Adjustments • Allowance for Uncollectable Amounts • Financial Statements

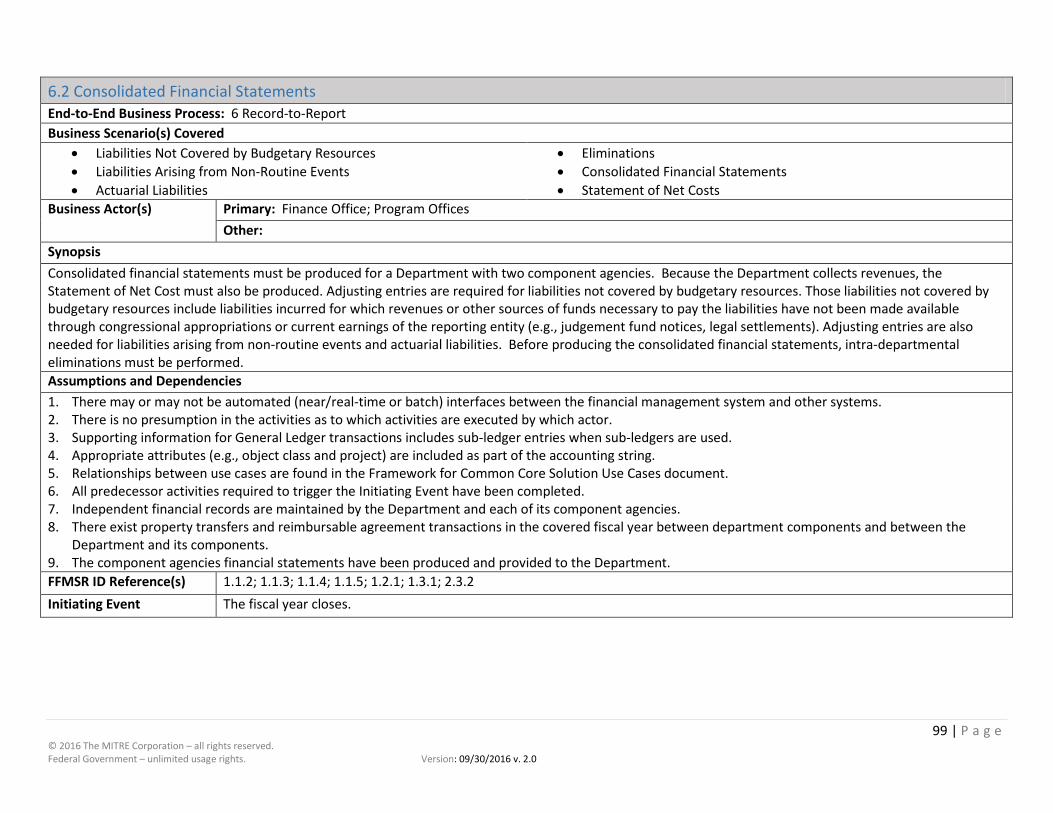

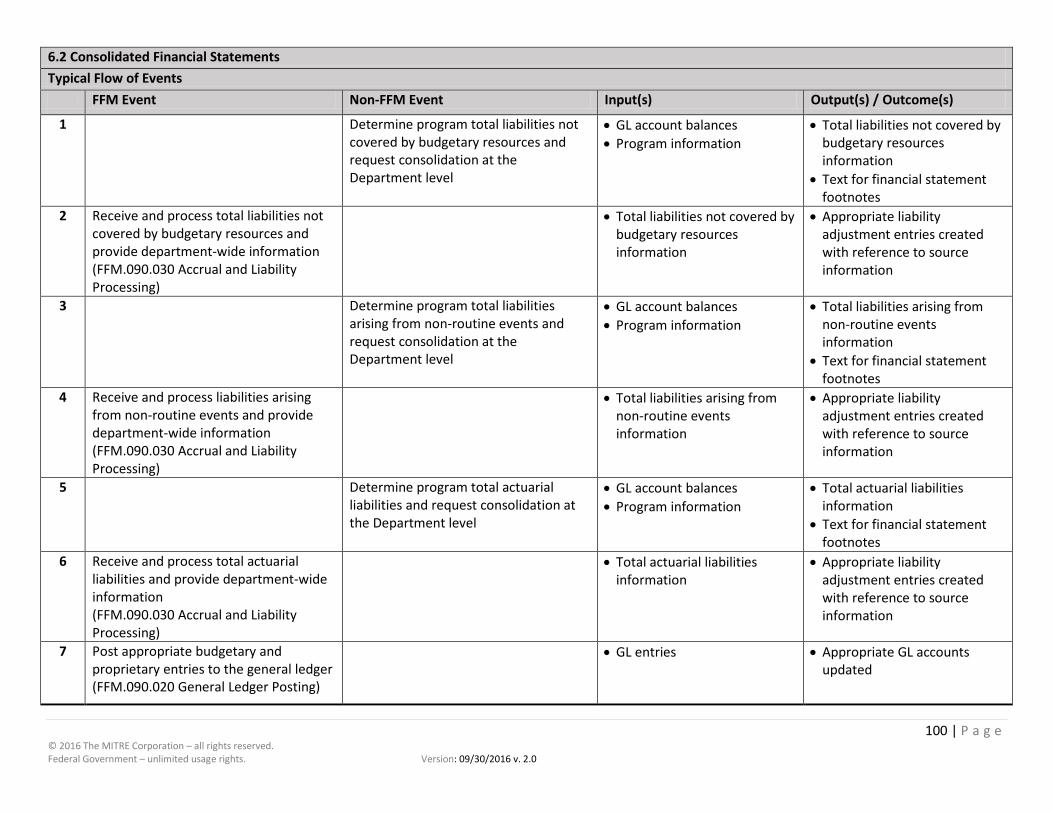

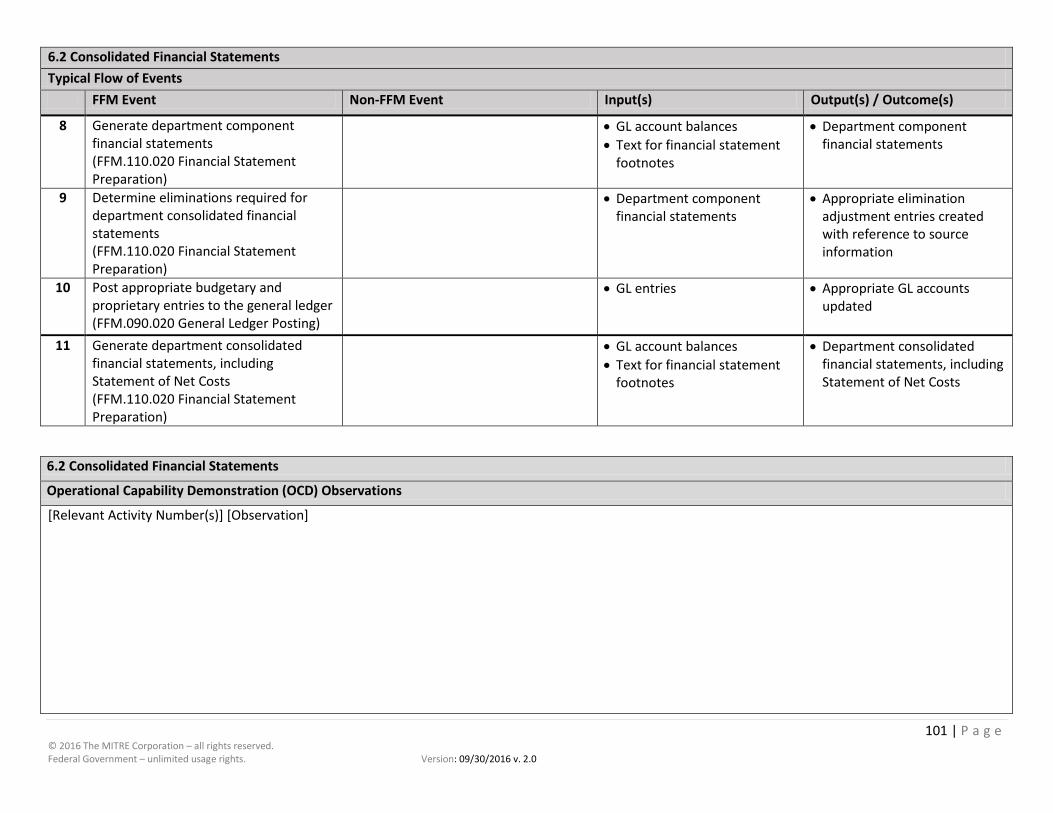

6.2 Consolidated Financial Statements (L2)

• Liabilities Not Covered by Budgetary Resources • Liabilities Arising from Non-Routine Events • Actuarial Liabilities • Eliminations • Consolidated Financial Statements • Statement of Net Costs

6.3 Supplementary Stewardship Reporting (L3)

• Supplementary Stewardship Reporting

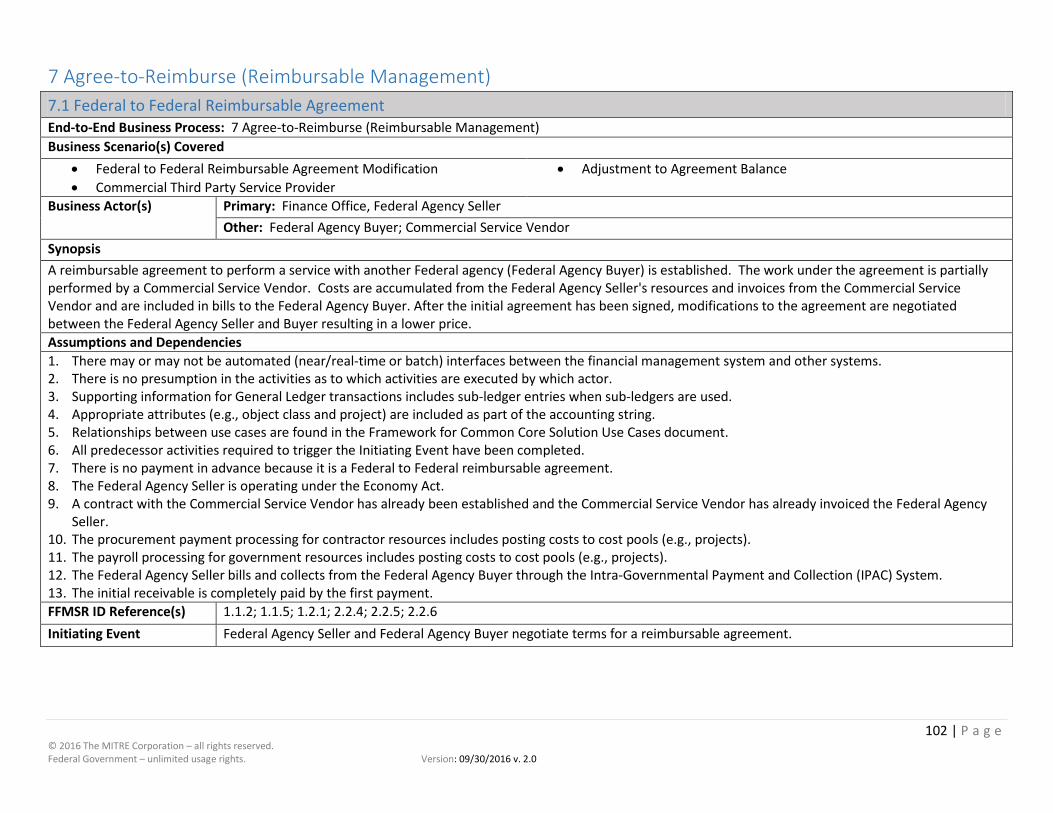

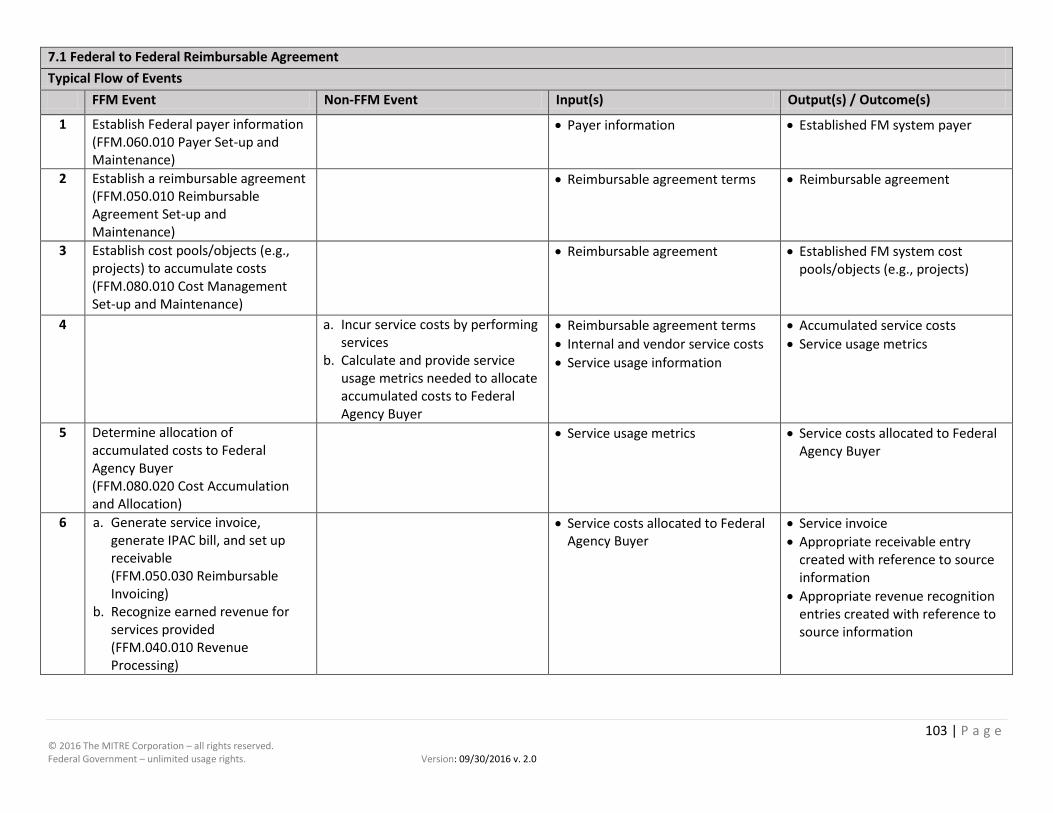

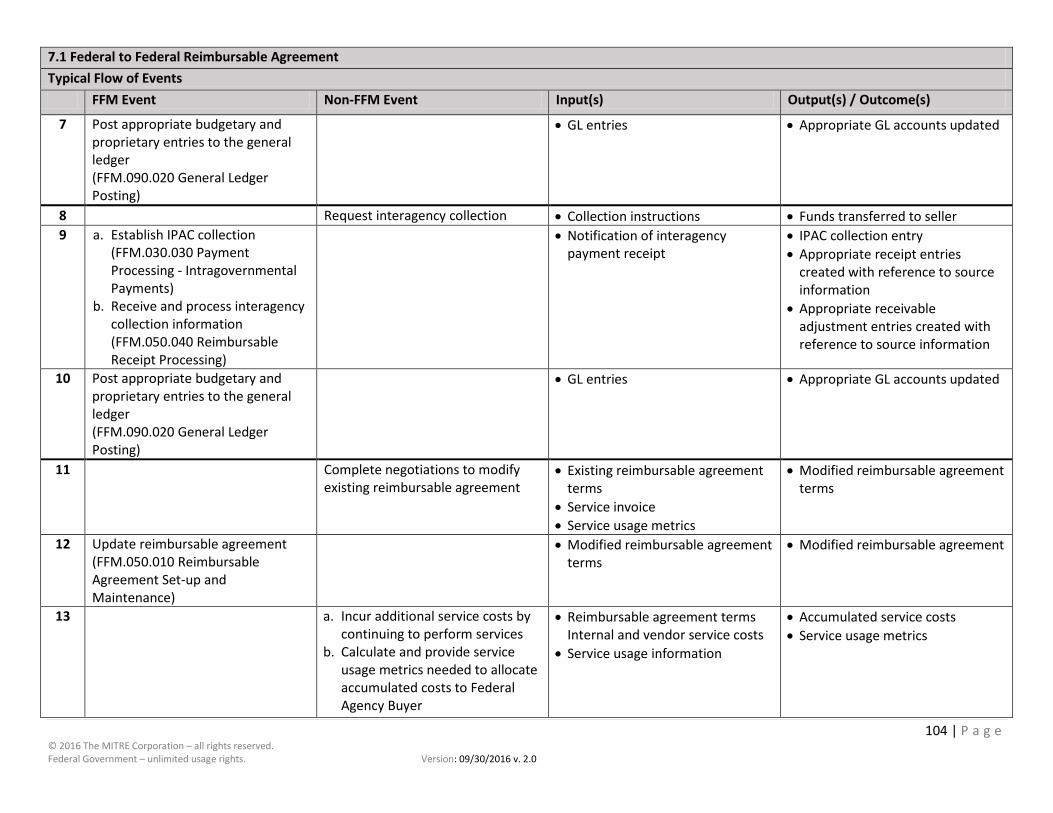

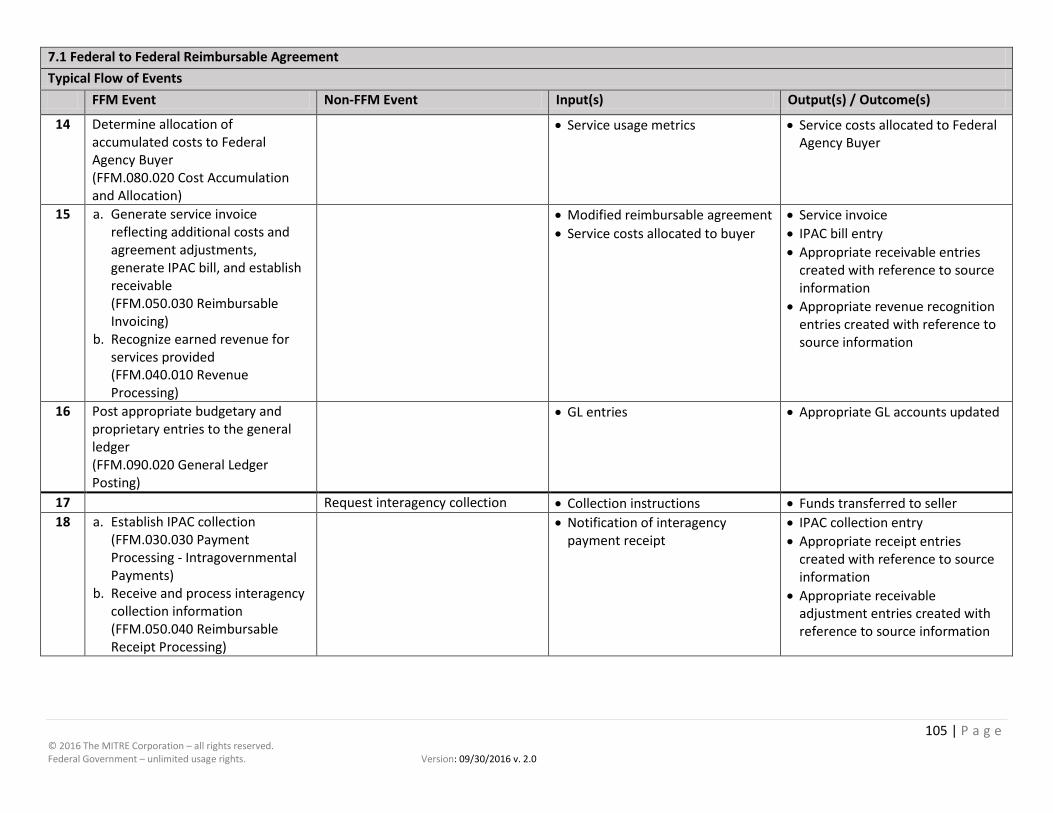

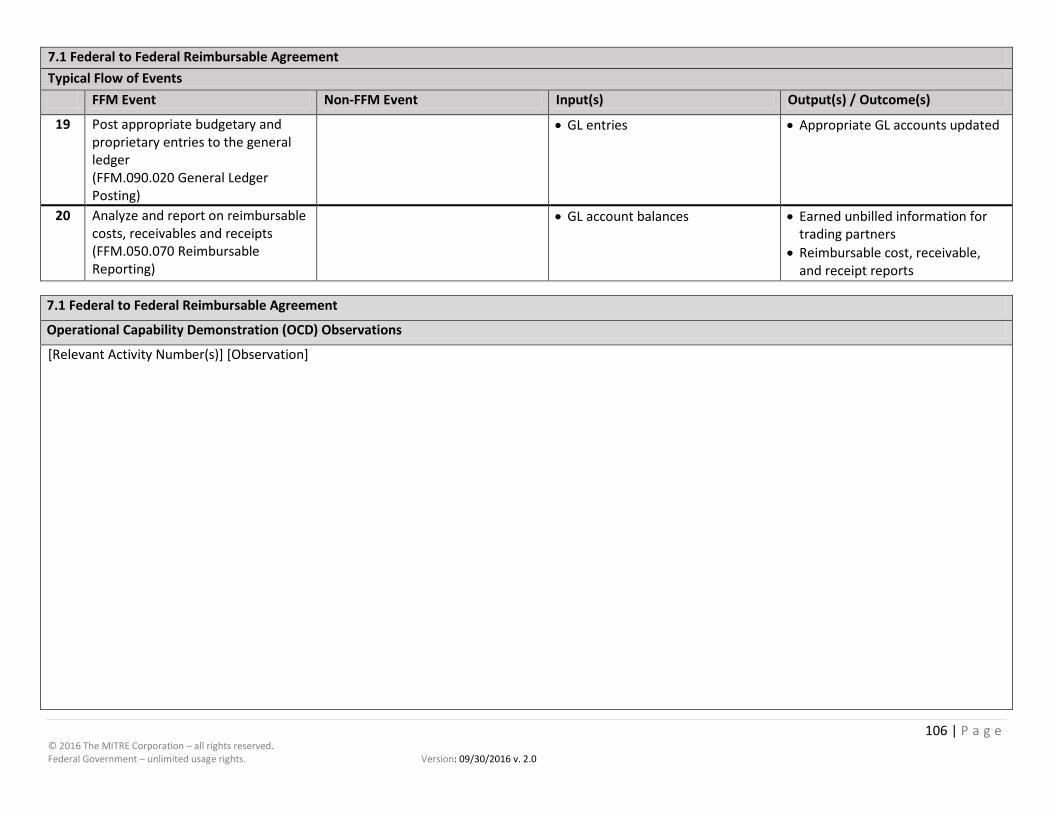

Process 7. Agree-to-Reimburse (Reimbursable Management)

Service Area(s): Financial Management (FFM) Business Use Cases and Associated Business Scenario(s) 7.1 Federal to Federal Reimbursable Agreement (L1)

• Federal to Federal Reimbursable Agreement Modification • Commercial Third Party Service Provider • Adjustment to Agreement Balance

7.2 Reimbursement without Agreement (L3)

• Reimbursement without Agreement 7.3 Reimbursable Agreement with Private Sector with Payments-in-Advance (L3)

• Reimbursable Agreement with Private Sector • Payment-in-Advance • Interest, Penalties, and Administrative Fees • Buy and Sell Transfers between Agencies

12 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

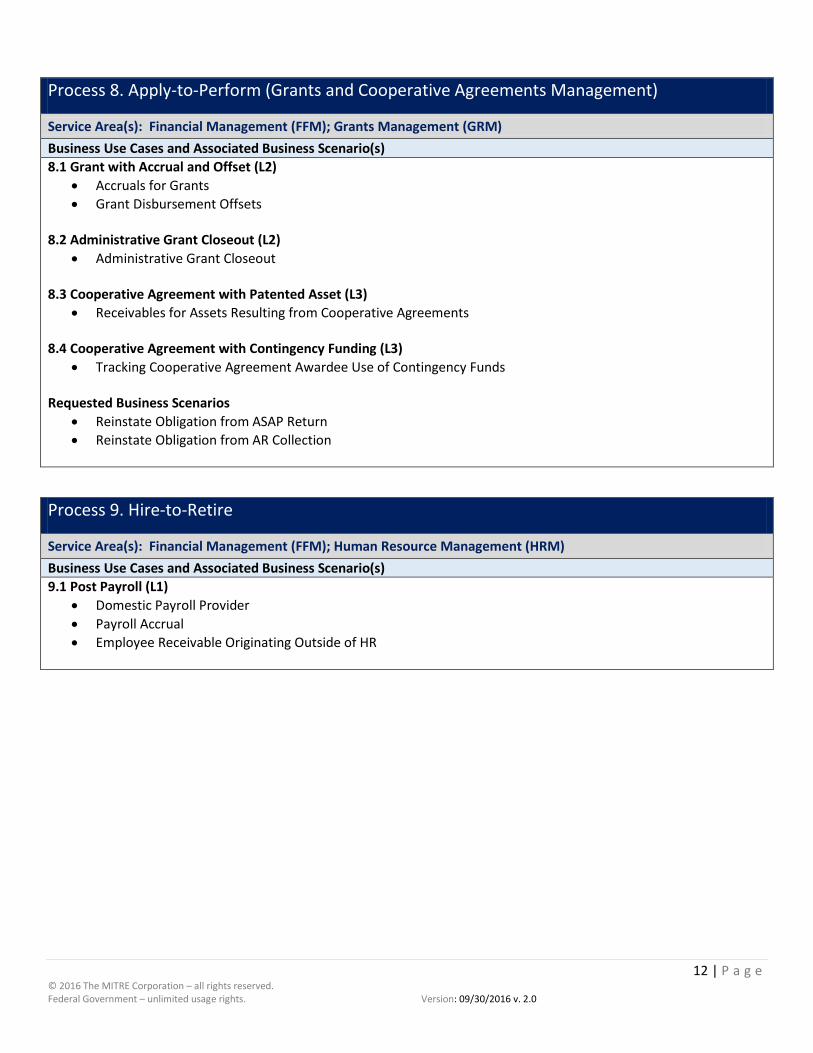

Process 8. Apply-to-Perform (Grants and Cooperative Agreements Management)

Service Area(s): Financial Management (FFM); Grants Management (GRM) Business Use Cases and Associated Business Scenario(s) 8.1 Grant with Accrual and Offset (L2)

• Accruals for Grants • Grant Disbursement Offsets

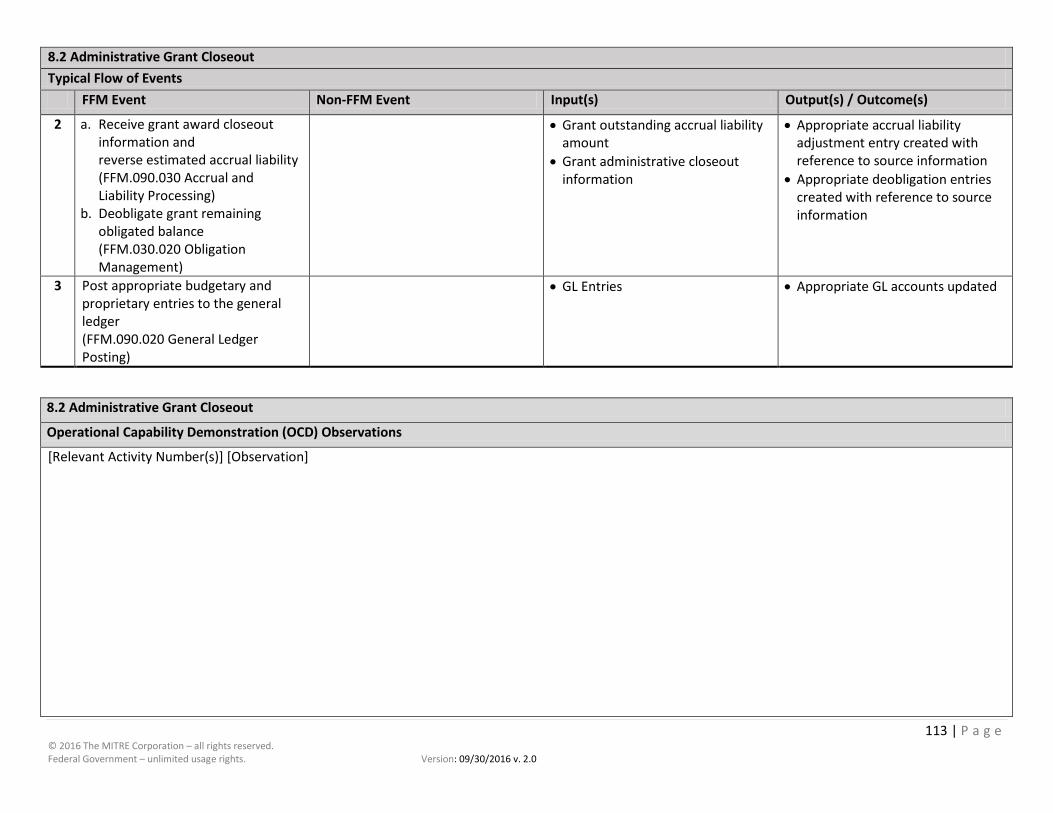

8.2 Administrative Grant Closeout (L2)

• Administrative Grant Closeout 8.3 Cooperative Agreement with Patented Asset (L3)

• Receivables for Assets Resulting from Cooperative Agreements 8.4 Cooperative Agreement with Contingency Funding (L3)

• Tracking Cooperative Agreement Awardee Use of Contingency Funds Requested Business Scenarios

• Reinstate Obligation from ASAP Return • Reinstate Obligation from AR Collection

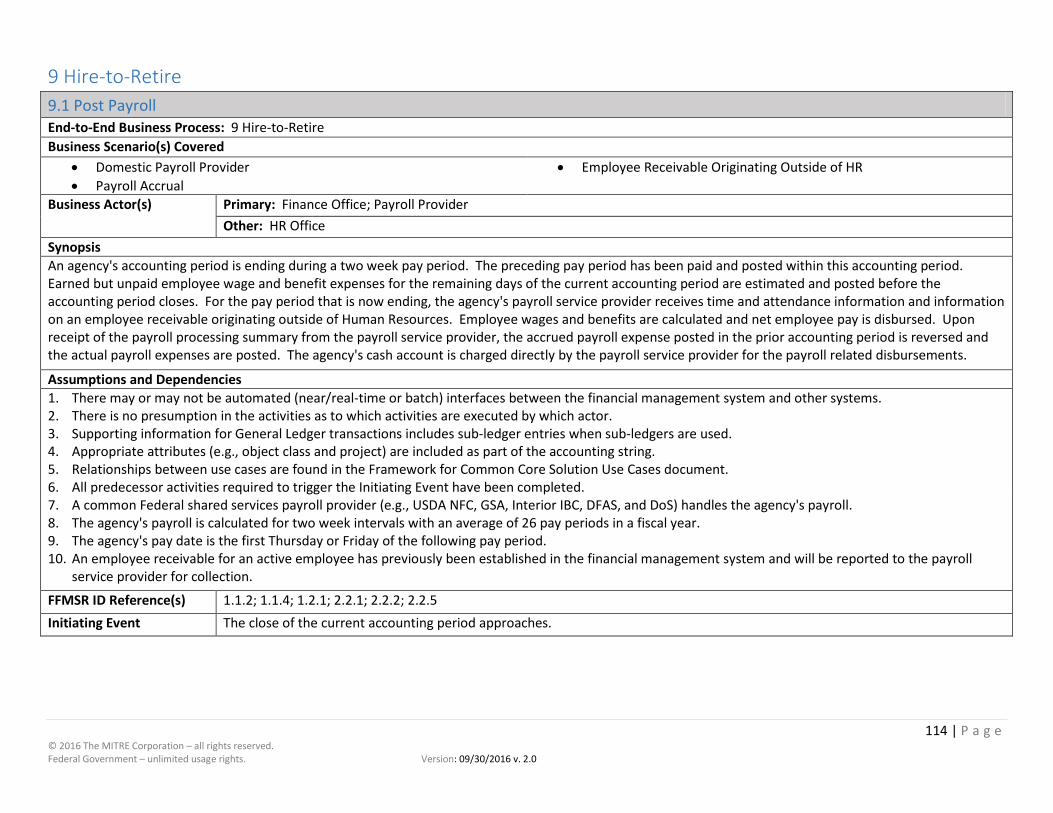

Process 9. Hire-to-Retire

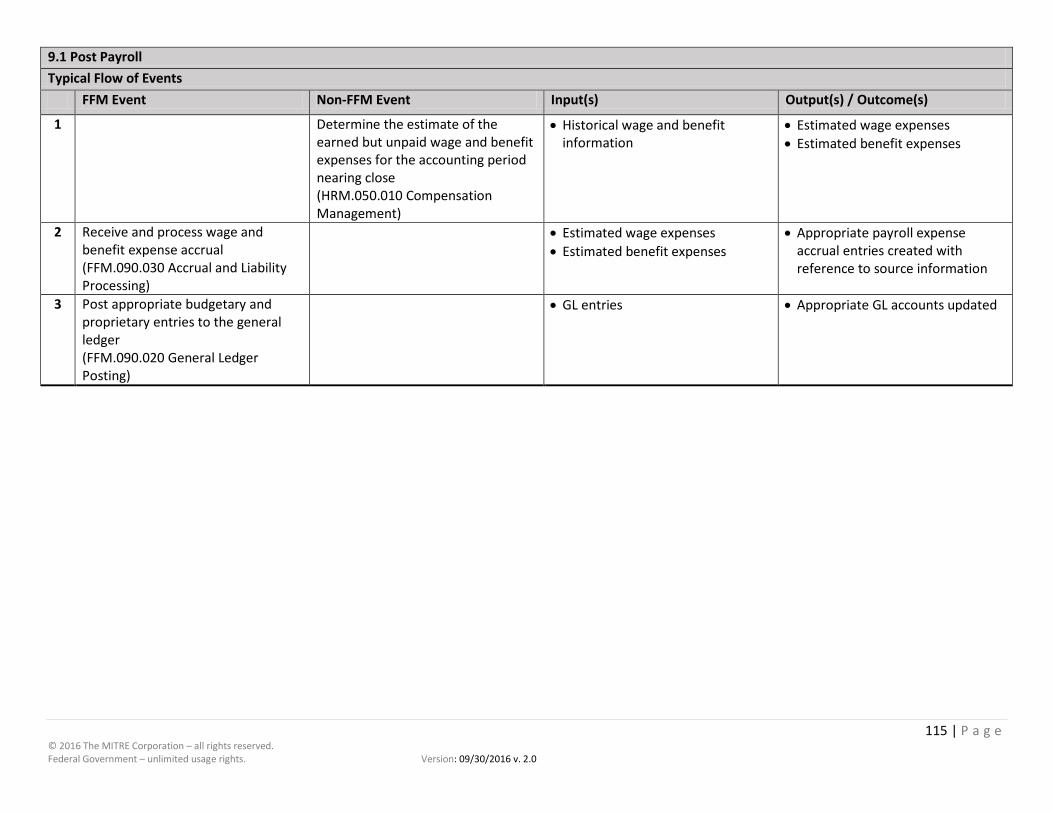

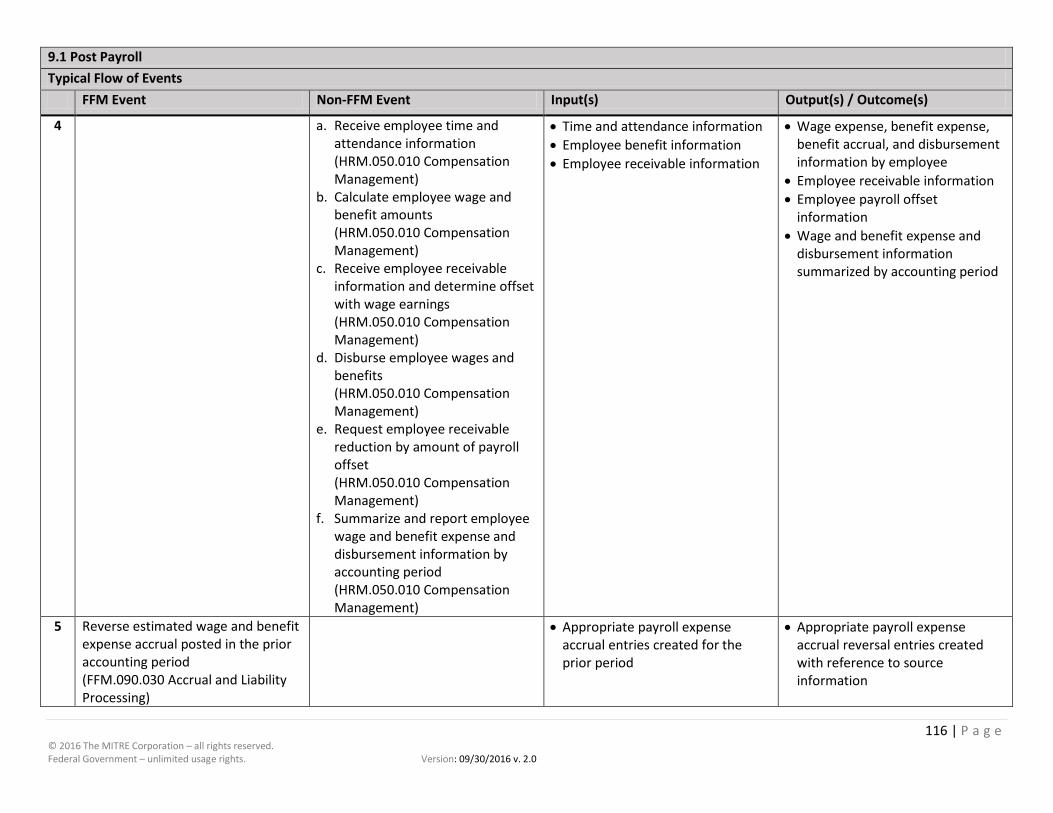

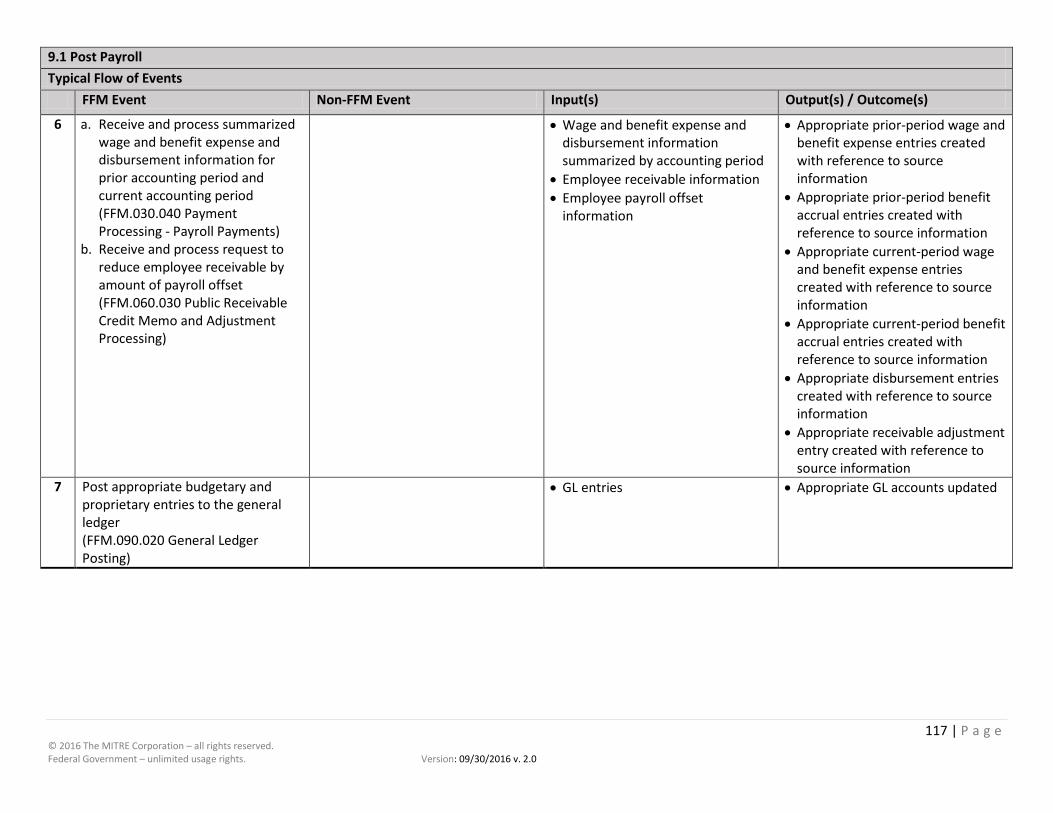

Service Area(s): Financial Management (FFM); Human Resource Management (HRM) Business Use Cases and Associated Business Scenario(s) 9.1 Post Payroll (L1)

• Domestic Payroll Provider • Payroll Accrual • Employee Receivable Originating Outside of HR

13 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

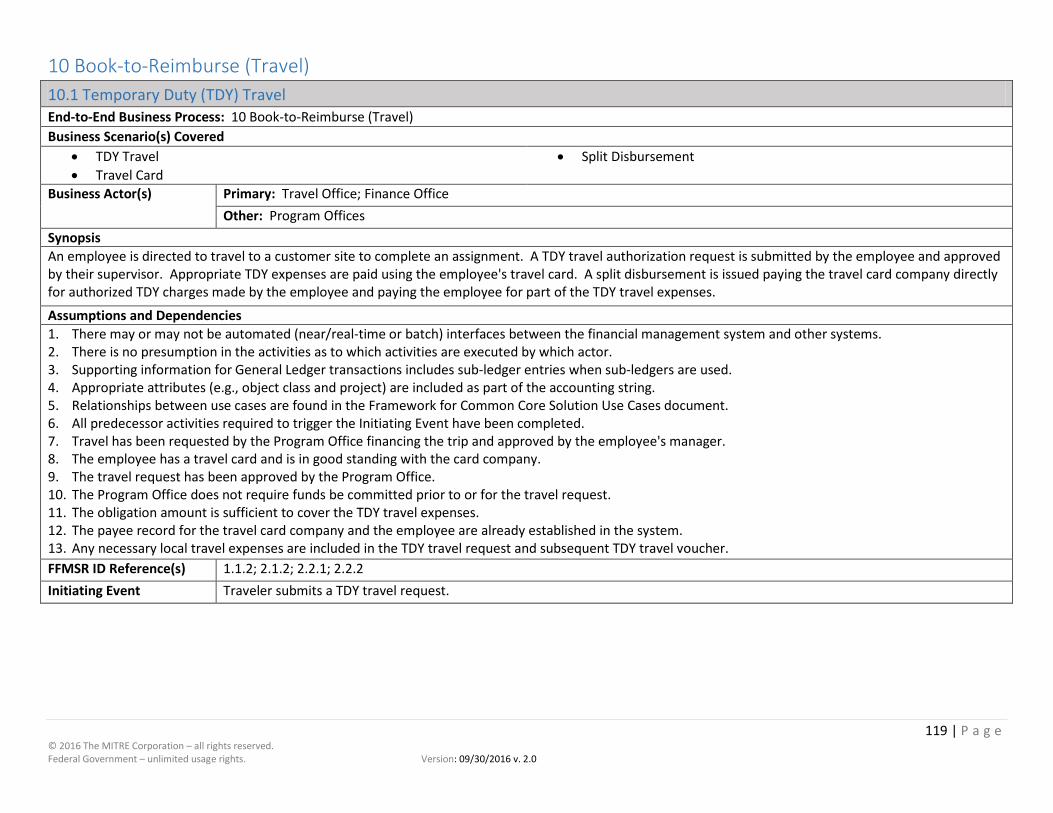

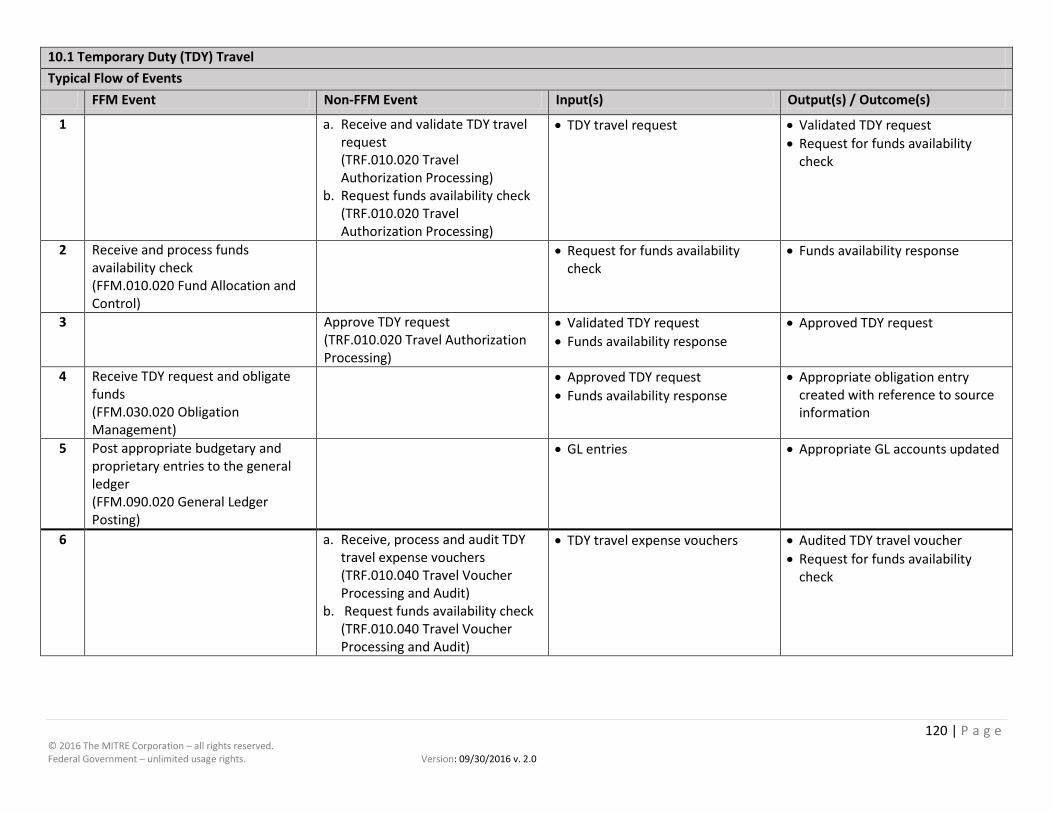

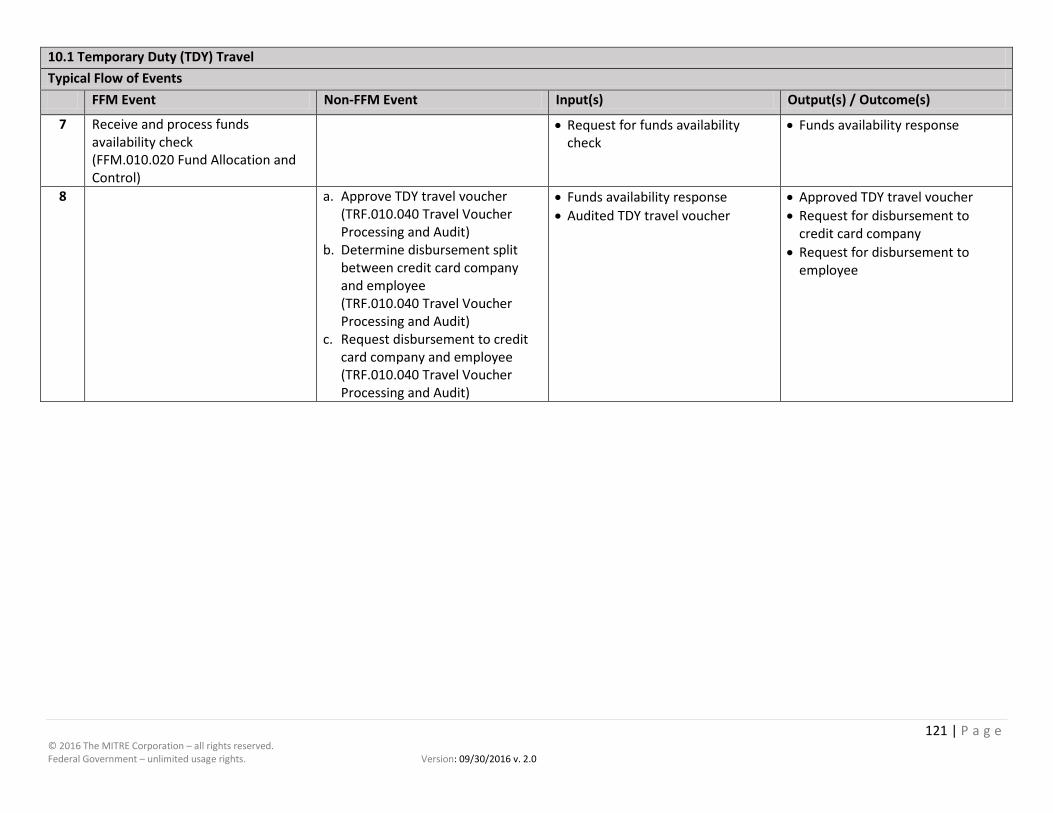

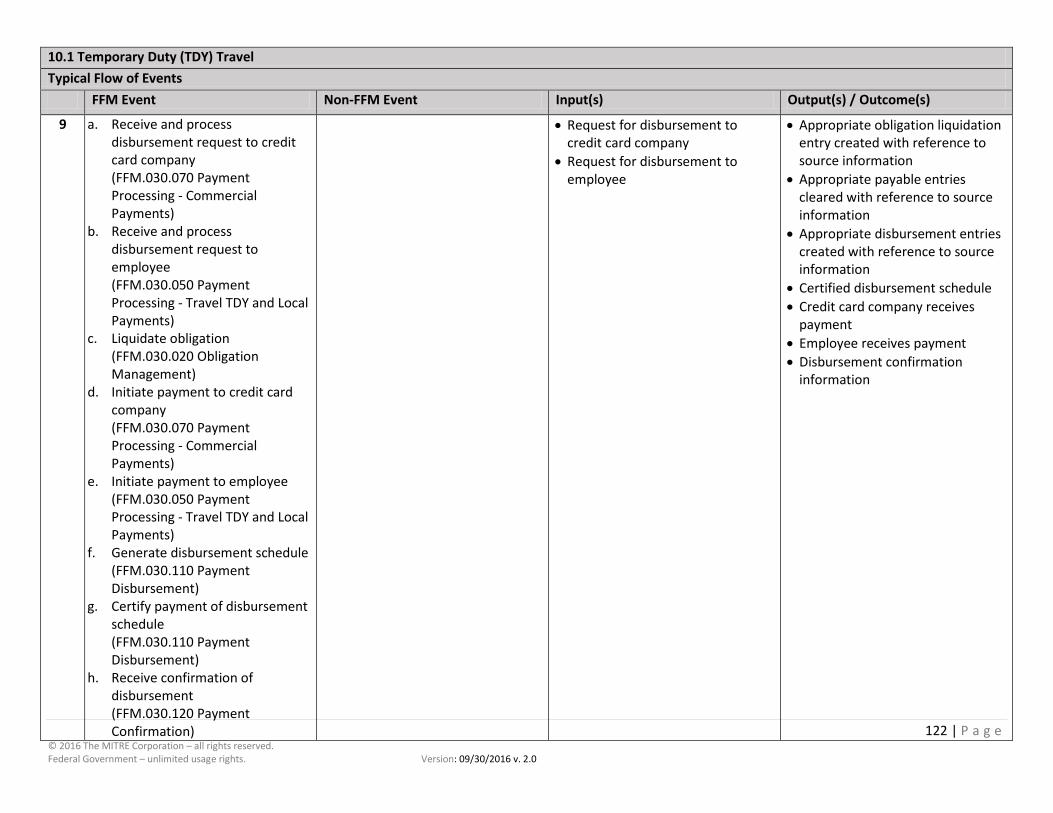

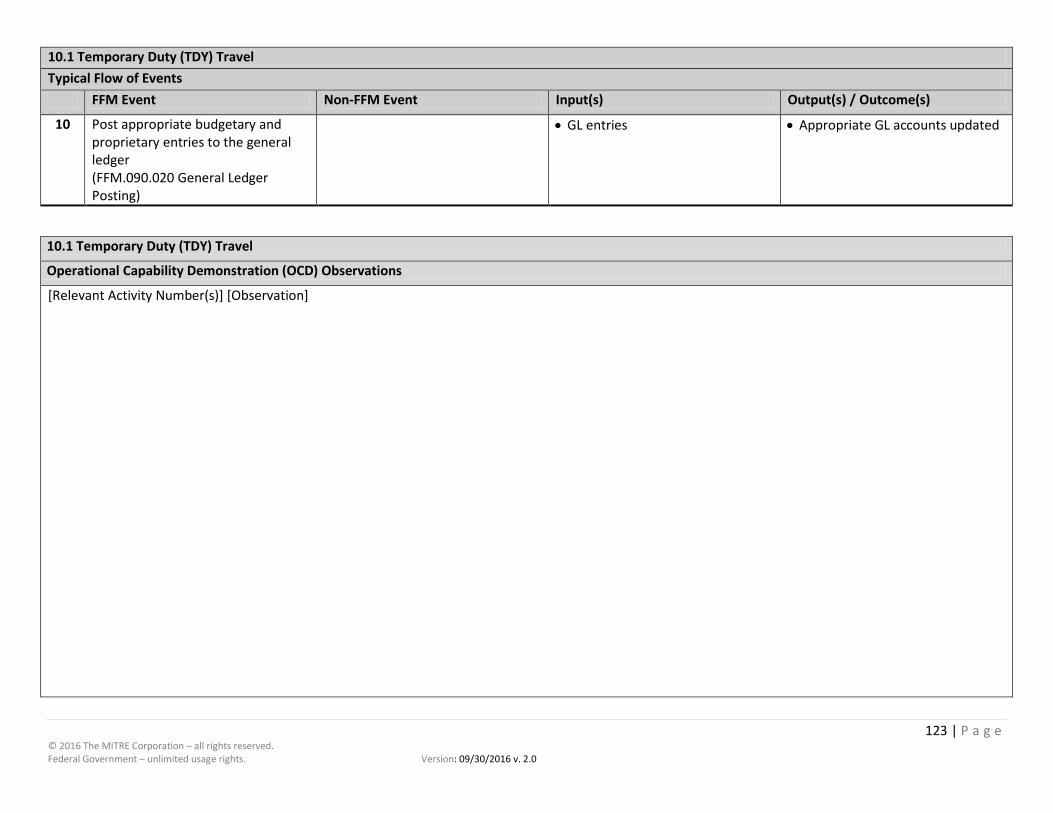

Process 10. Book-to-Reimburse (Travel)

Service Area(s): Financial Management (FFM); Human Resource Management (HRM); Travel and Relocation Management (TRF) Business Use Cases and Associated Business Scenario(s) 10.1 Temporary Duty Travel (TDY) (L1)

• TDY Travel • Travel Card • Split Disbursement

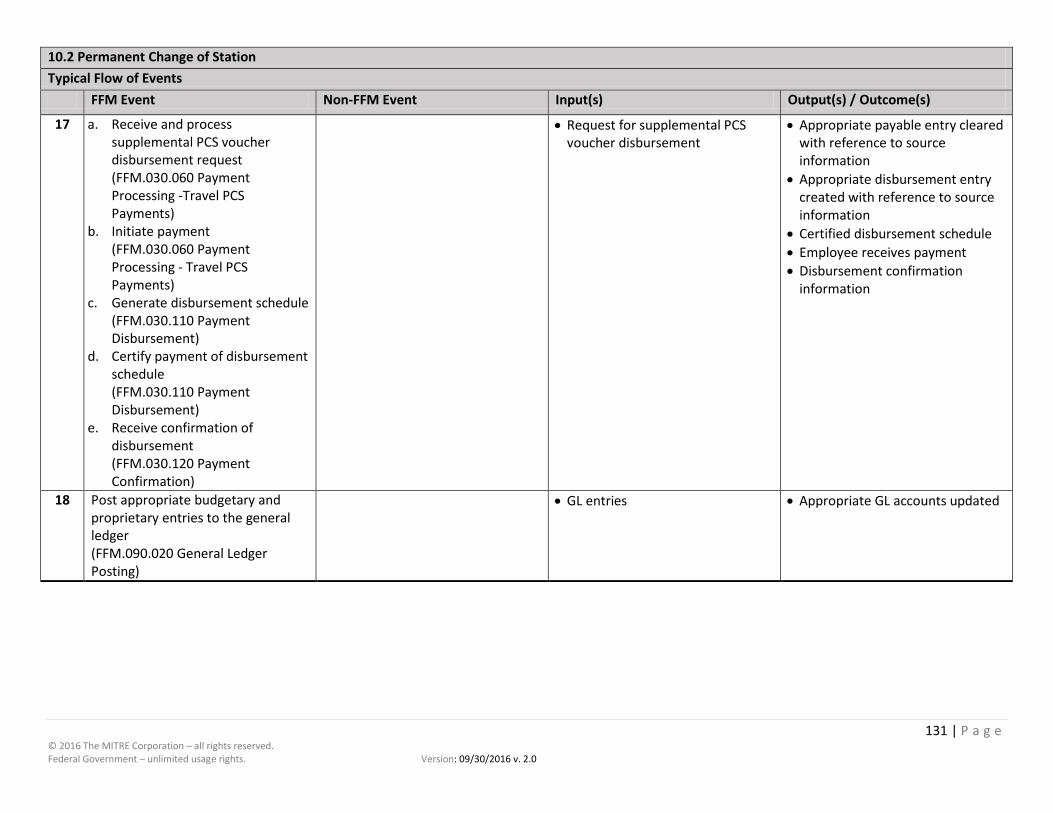

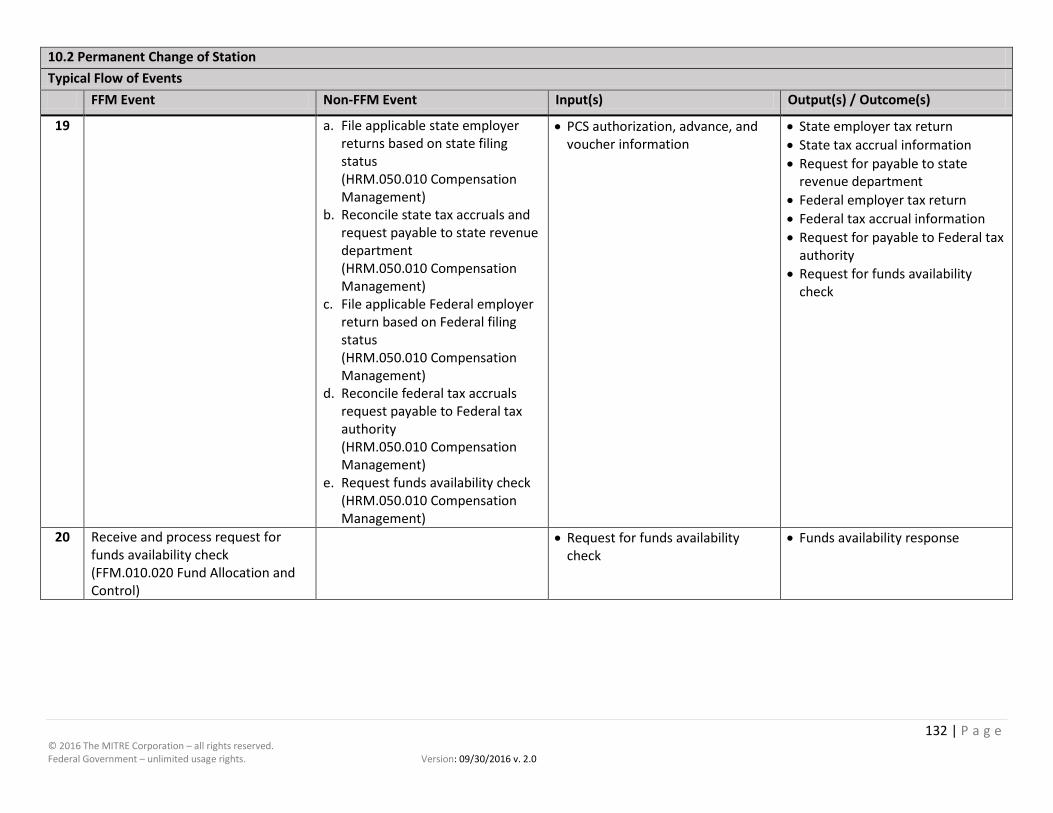

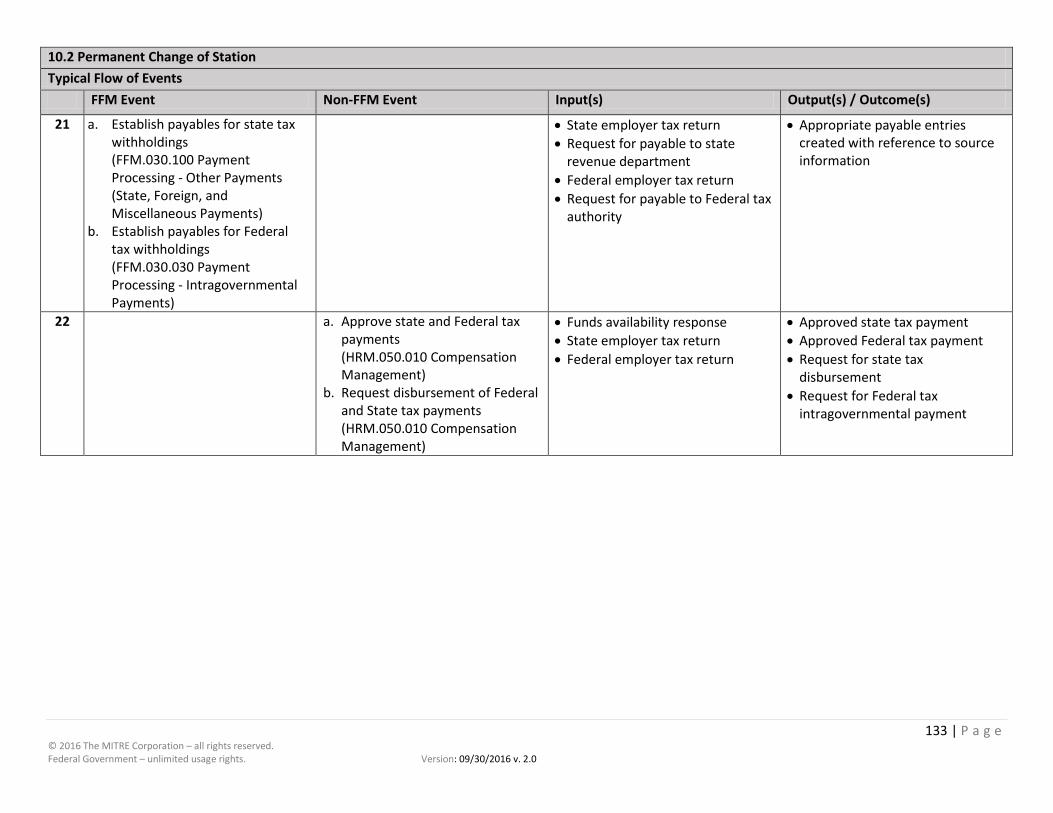

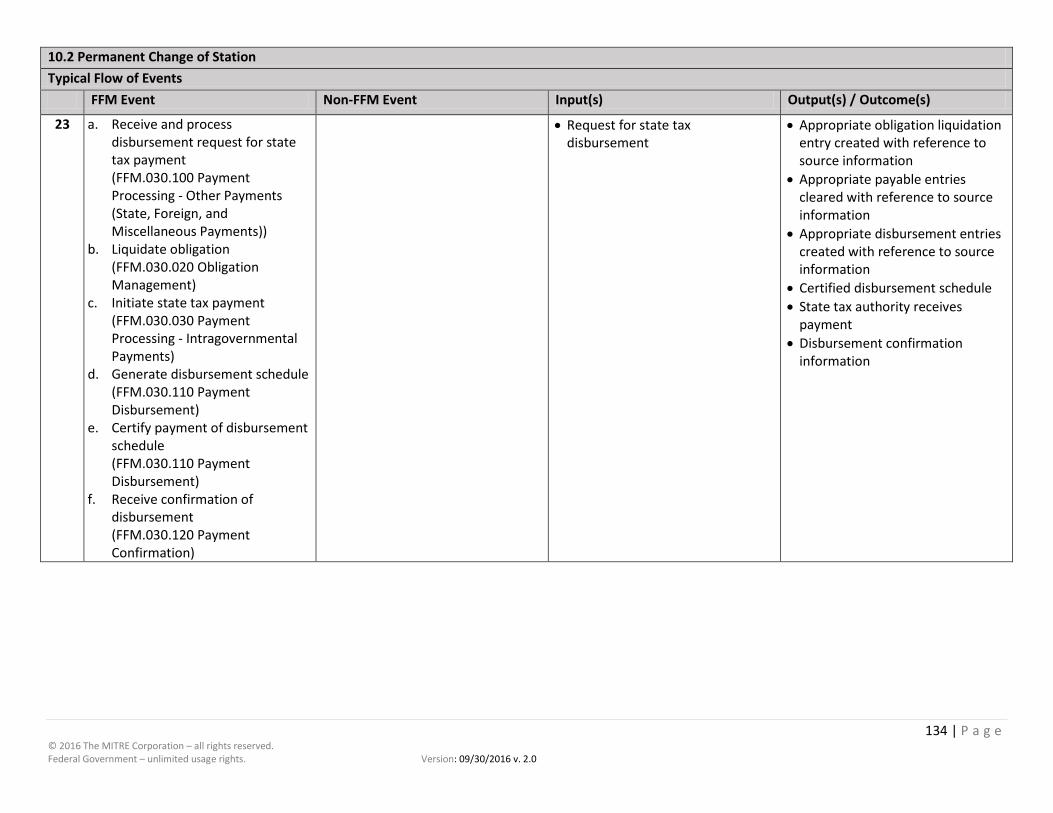

10.2 Permanent Change of Station (PCS) (L2)

• Relocation • Supplemental PCS Voucher

10.3 Travel Sponsored by Non-Government Source (L3)

• Non-Government Source Funds Collection • Advance on Account

Requested Business Scenarios

• Federal & State Tax Withholding from Employee Disbursements

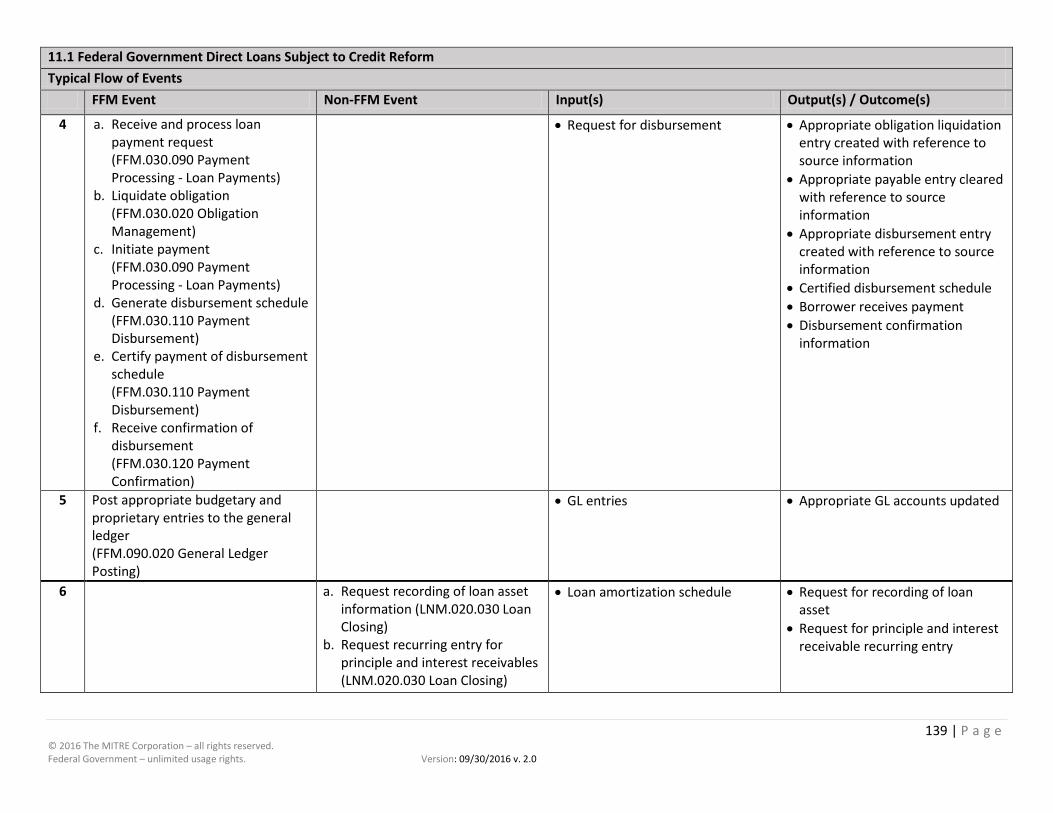

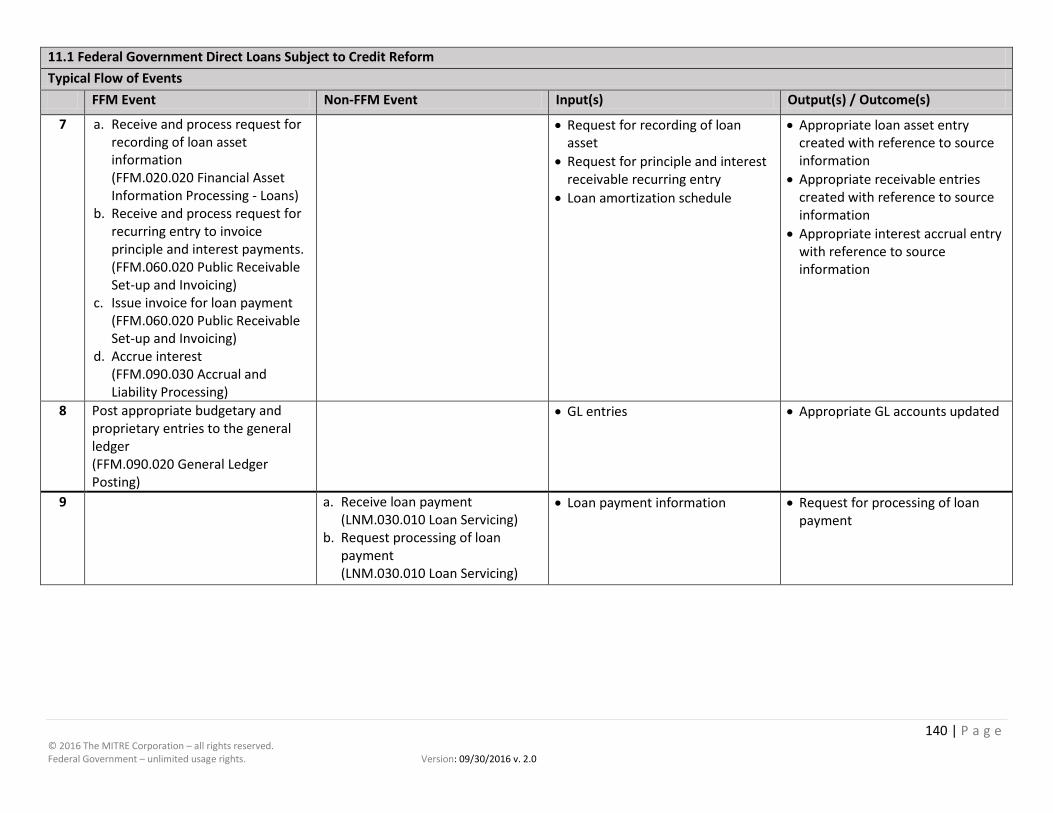

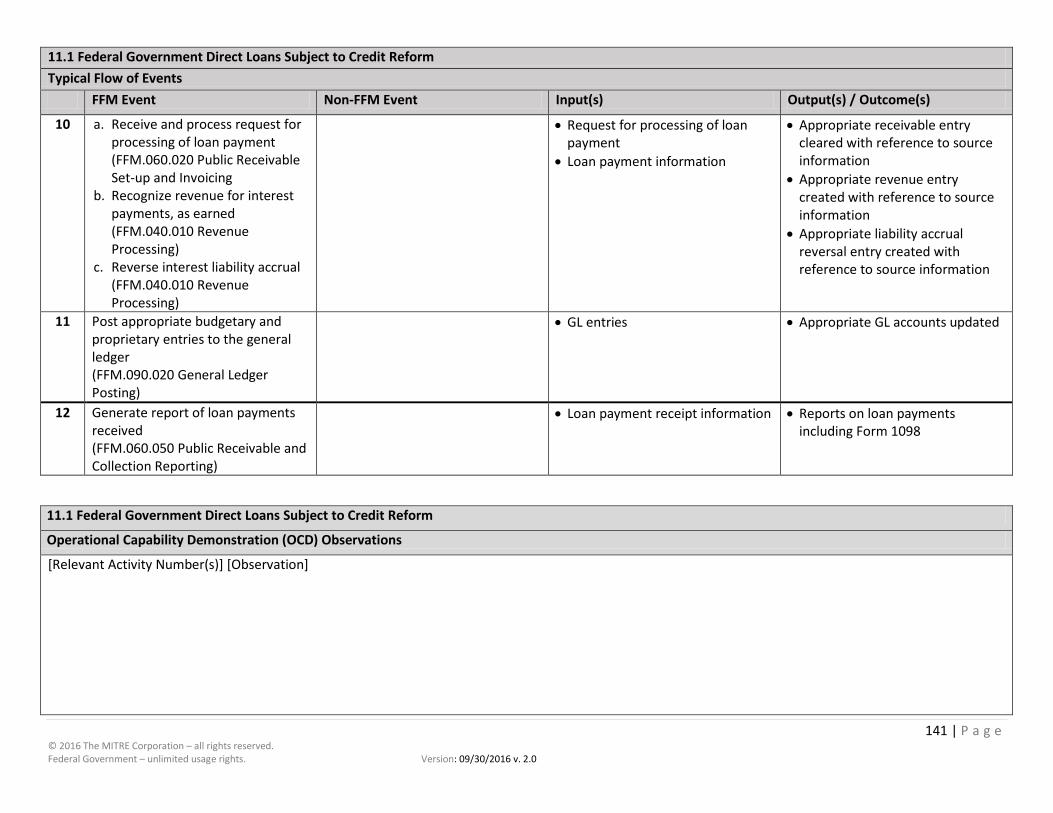

Process 11. Apply-to-Repay (Loan Management)

Service Area(s): Financial Management (FFM); Loans Management (LNM) Business Use Cases and Associated Business Scenario(s) 11.1 Direct Loan Interest Accrual (L2)

• Disbursement of a Loan • Establishment of Principal Receivable • Interest Accrual • Collection of Interest and Principal

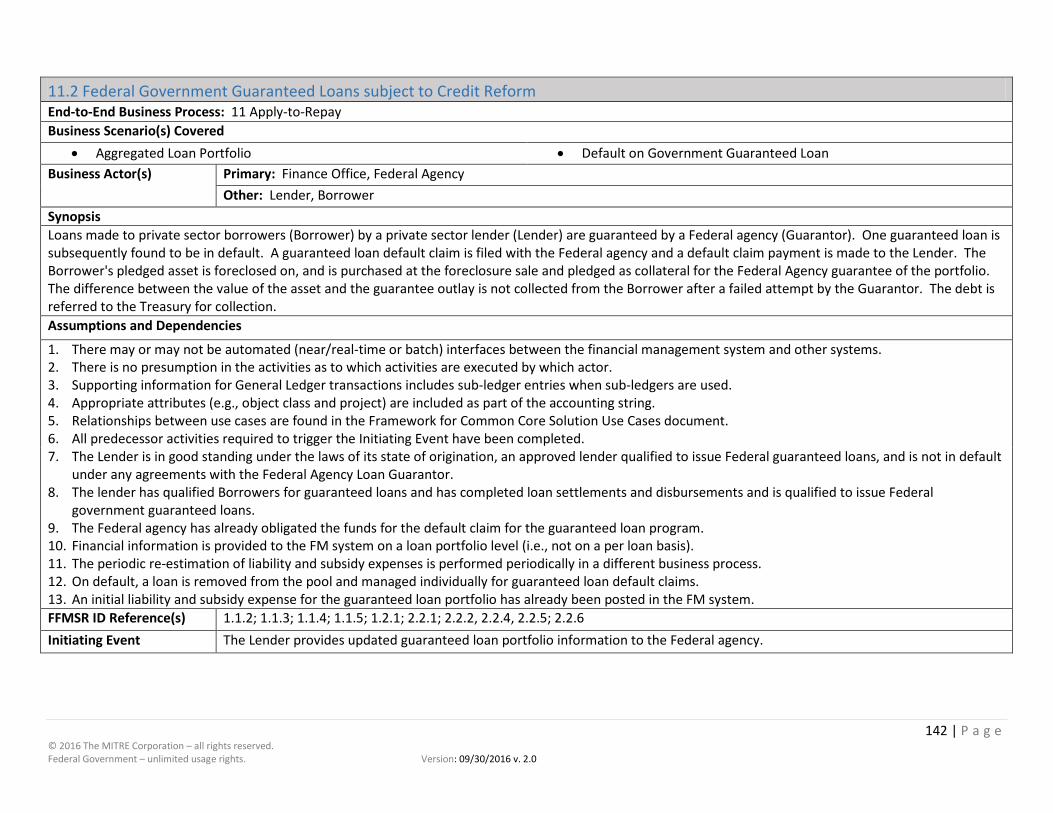

11.2 Government Guaranteed Loan (L2)

• Aggregated Loan Portfolio • Default on Government Guaranteed Loan

11.3 Transition of a Grant to Direct Loan Receivable (L3)

• Default Transition of Grant to Direct Loan Receivable 11.4 Loan Buy Back from Government (L3)

• Buy Backs Requested Business Scenarios

• Subsidy Re-estimation

14 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

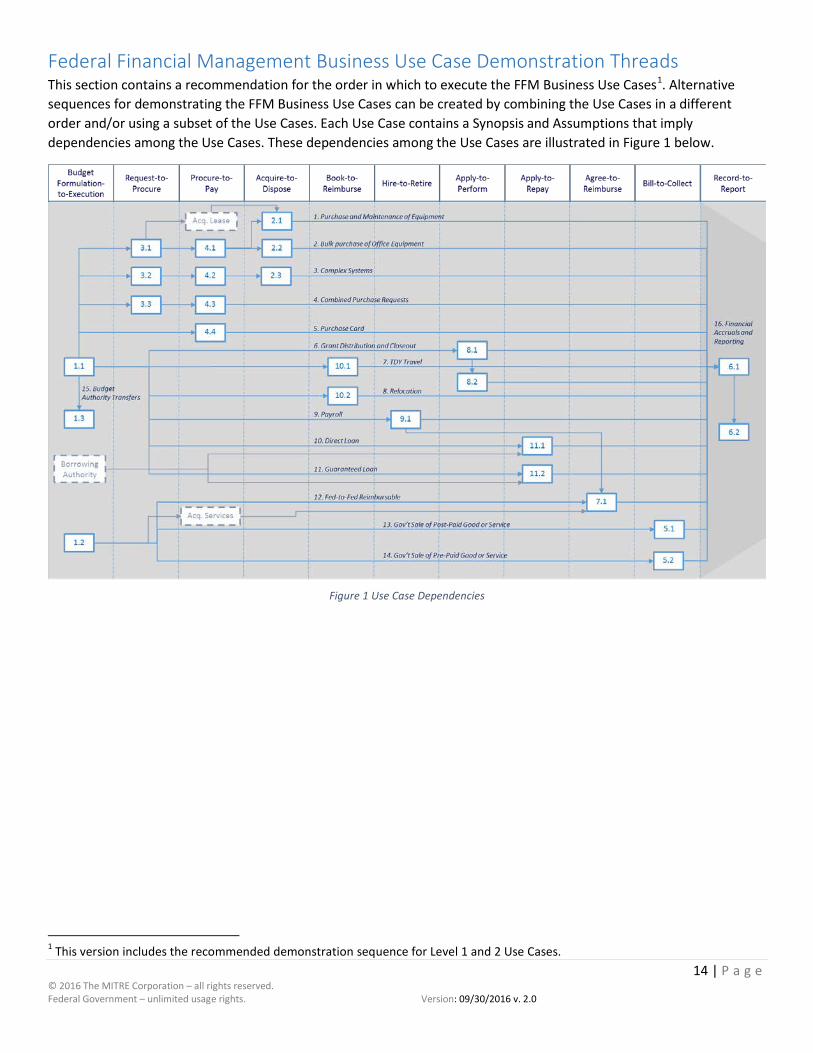

Federal Financial Management Business Use Case Demonstration Threads This section contains a recommendation for the order in which to execute the FFM Business Use Cases1. Alternative sequences for demonstrating the FFM Business Use Cases can be created by combining the Use Cases in a different order and/or using a subset of the Use Cases. Each Use Case contains a Synopsis and Assumptions that imply dependencies among the Use Cases. These dependencies among the Use Cases are illustrated in Figure 1 below.

Figure 1 Use Case Dependencies

1 This version includes the recommended demonstration sequence for Level 1 and 2 Use Cases.

15 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

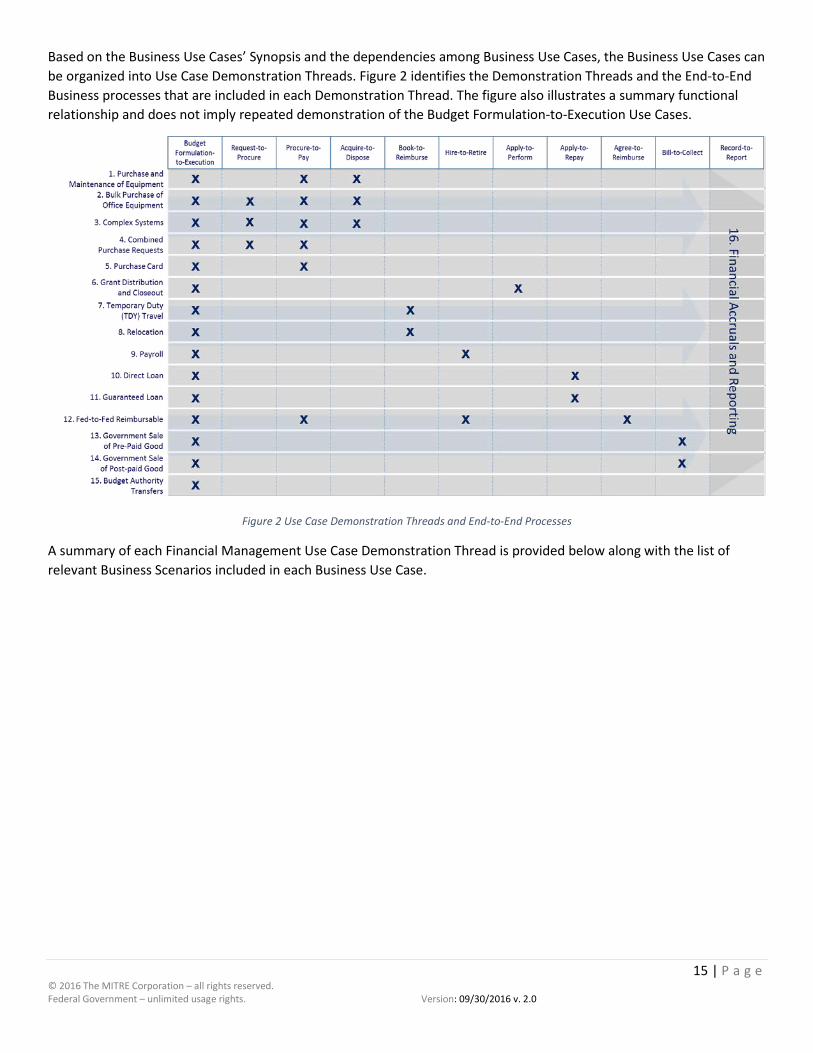

Based on the Business Use Cases’ Synopsis and the dependencies among Business Use Cases, the Business Use Cases can be organized into Use Case Demonstration Threads. Figure 2 identifies the Demonstration Threads and the End-to-End Business processes that are included in each Demonstration Thread. The figure also illustrates a summary functional relationship and does not imply repeated demonstration of the Budget Formulation-to-Execution Use Cases.

Figure 2 Use Case Demonstration Threads and End-to-End Processes

A summary of each Financial Management Use Case Demonstration Thread is provided below along with the list of relevant Business Scenarios included in each Business Use Case.

16 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

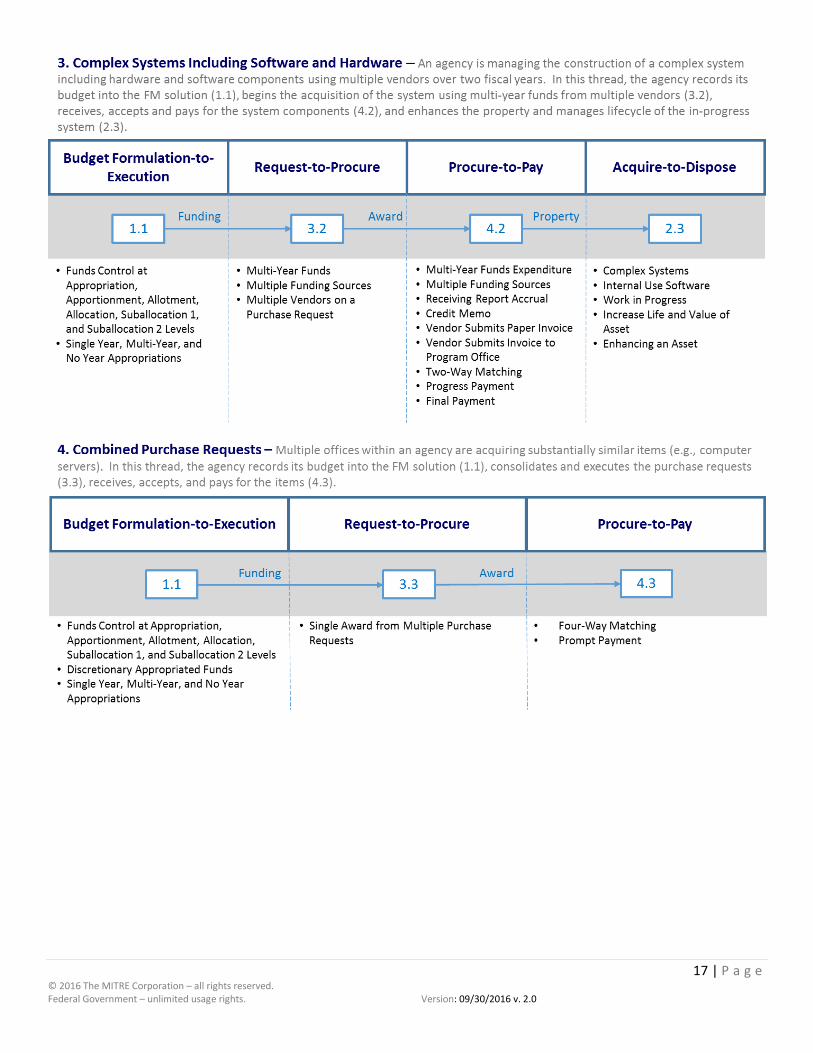

17 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

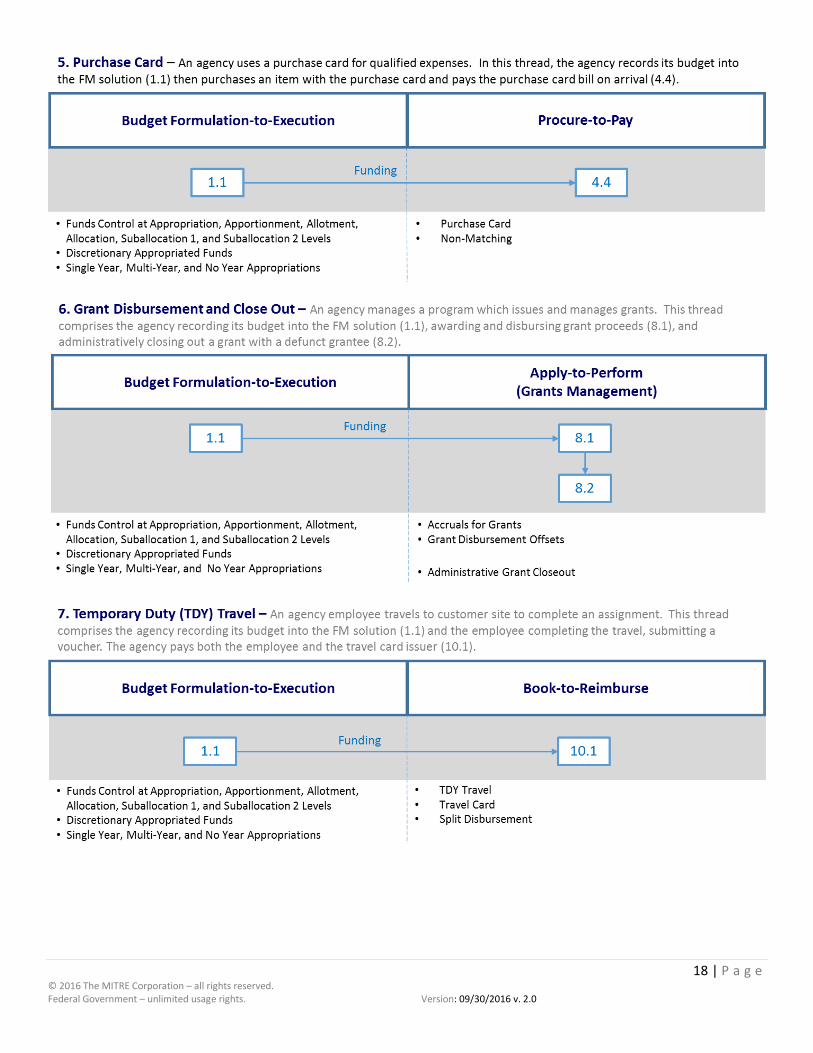

18 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

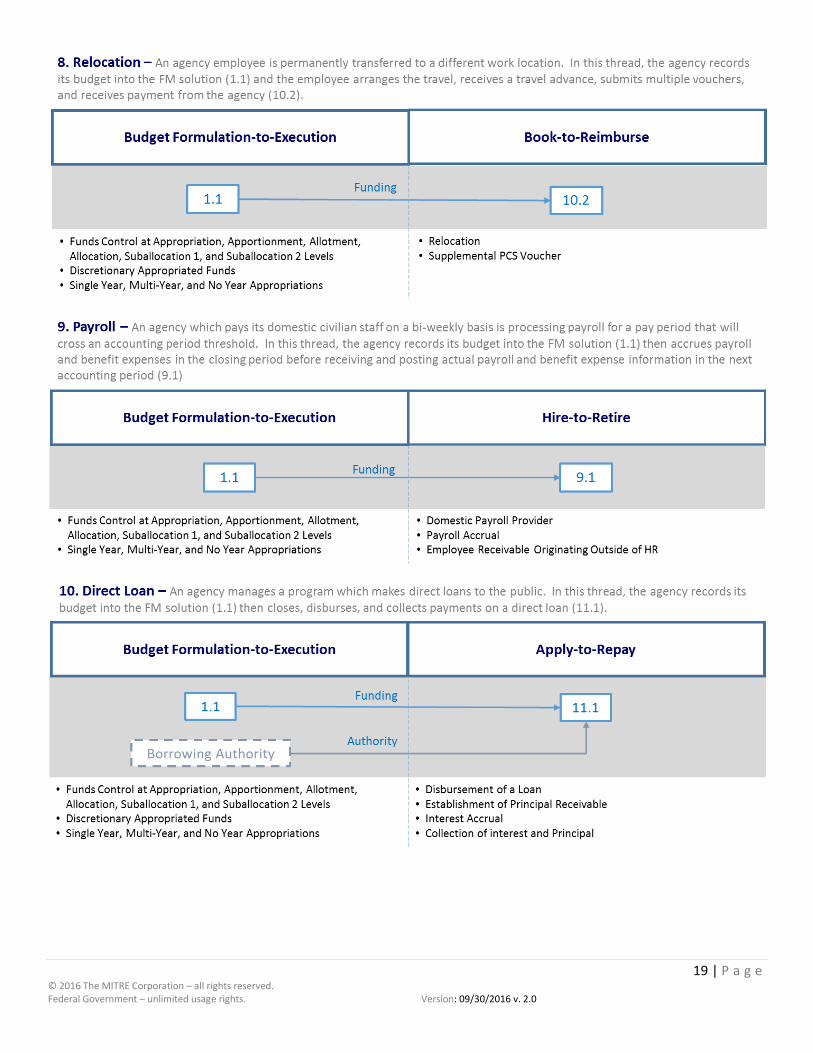

19 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

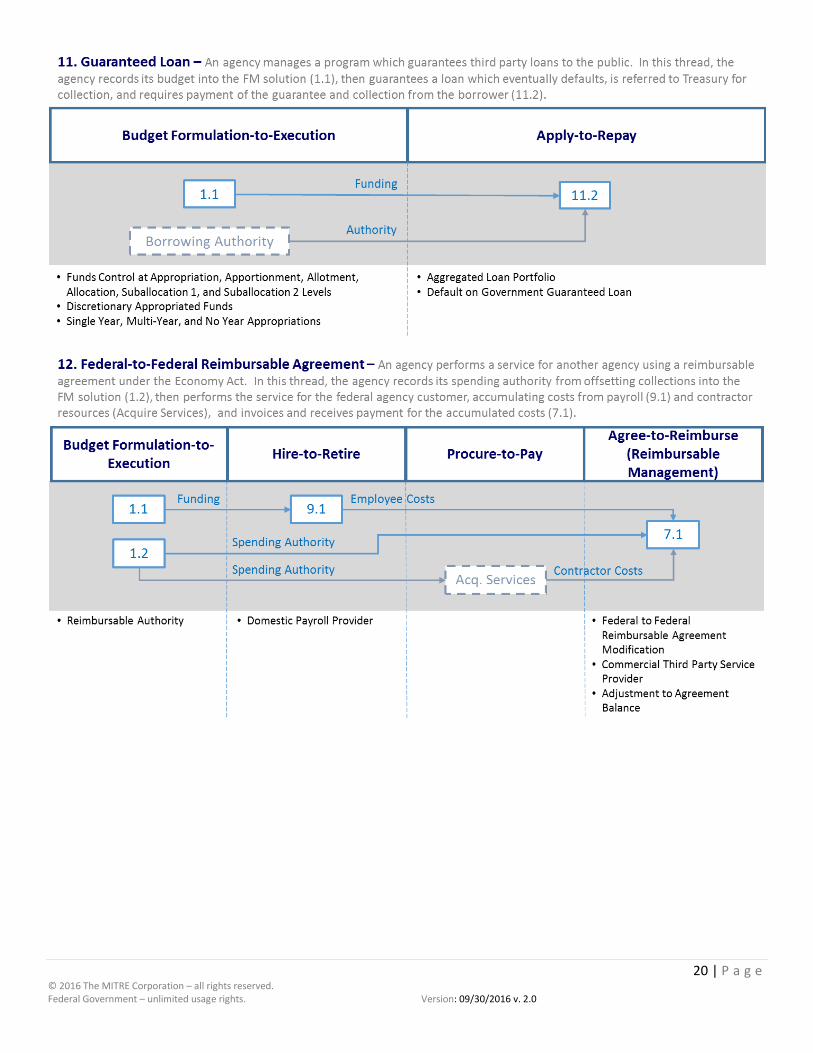

20 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

21 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

22 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

23 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

Federal Financial Management Business Use Cases The sections below contain the FFM Business Use Cases. The content of the FFM Business Use Case is defined below.

Section 1 of each Business Use Case provides the following information:

a) Use Case Number and Name The Use Case Number correlates to an End-to-End Business Process (e.g., 1.1 Budget Authority Set-up is a Business Use Case under End-to-End Business Process 1 Budget Formulation-to-Execution)

b) End-to-End Business Process Number and Name c) Business Scenario(s) Covered d) Business Actor(s)

There are two categories of business actors, primary and other. Primary business actors are those who execute most of the events. The actors are named in general terms. The actor names in specific agencies or departments may differ. Other business actors are actors that support the primary business actors.

e) Synopsis The Synopsis provides a summary of the events that take place within the Business Use Case.

f) Assumptions and Dependencies These include assumptions about events that have occurred prior to the first event identified in the Use Case or outside of the Use Case and dependencies on events accomplished in other Use Cases. There are a number of common assumptions that are established for all Use Cases. Additional assumptions or dependencies are included if needed for the specific Use Case.

g) Initiating Event The event that triggers the initiation of the Use Case.

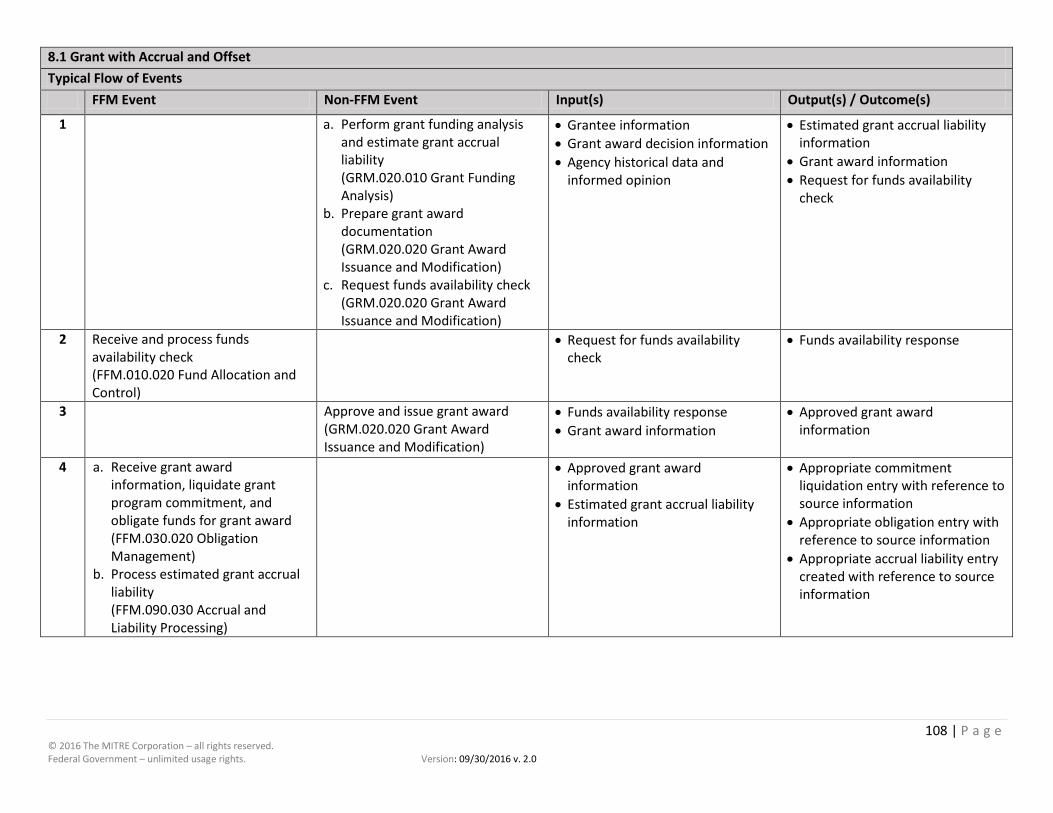

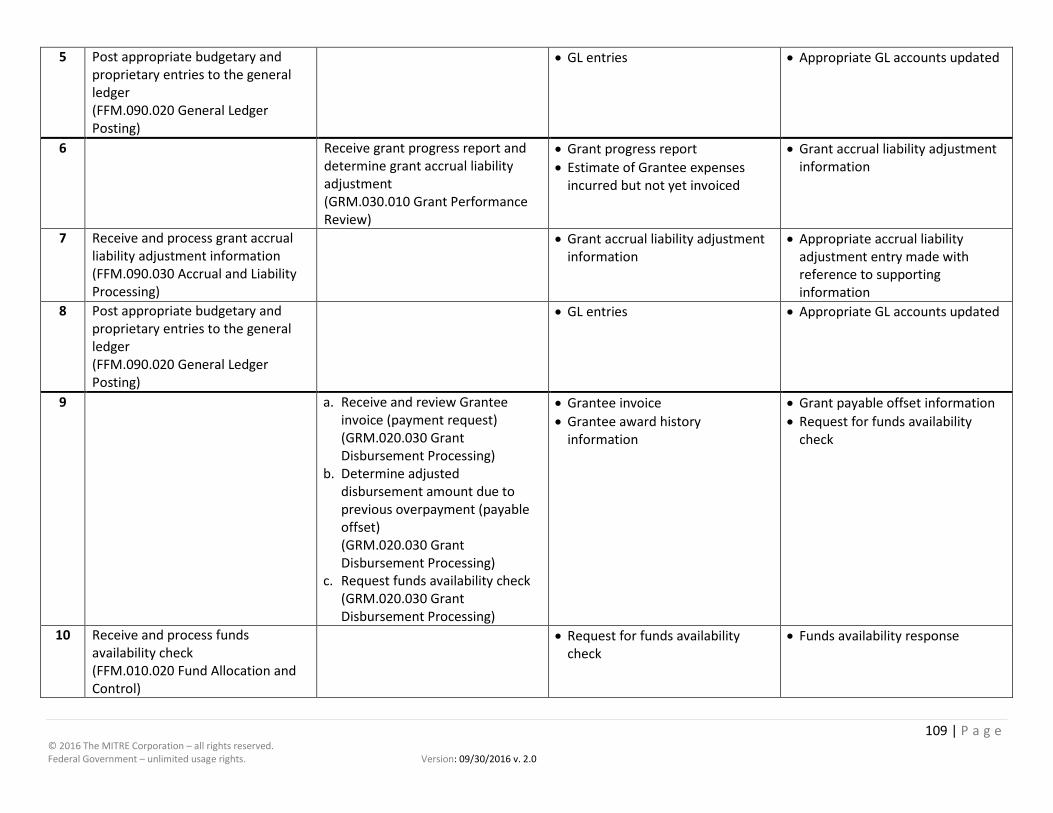

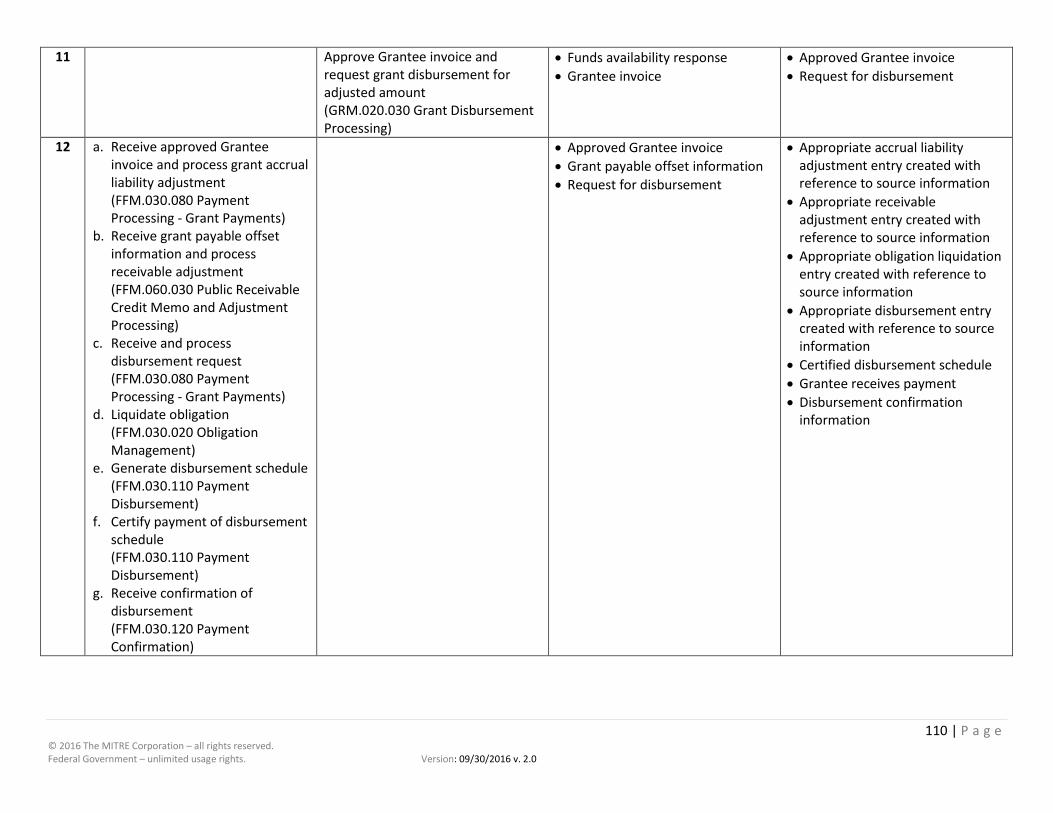

Section 2: Typical Flow of Events

This section includes the Federal Financial Management (FFM) and Non-FFM events that may occur to complete the Business Scenario(s) included in the Business Use Case. The non-FFM events are provided for business context. Also included are the inputs and outputs or outcomes that one would expect occur during or as a result of the event.

24 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

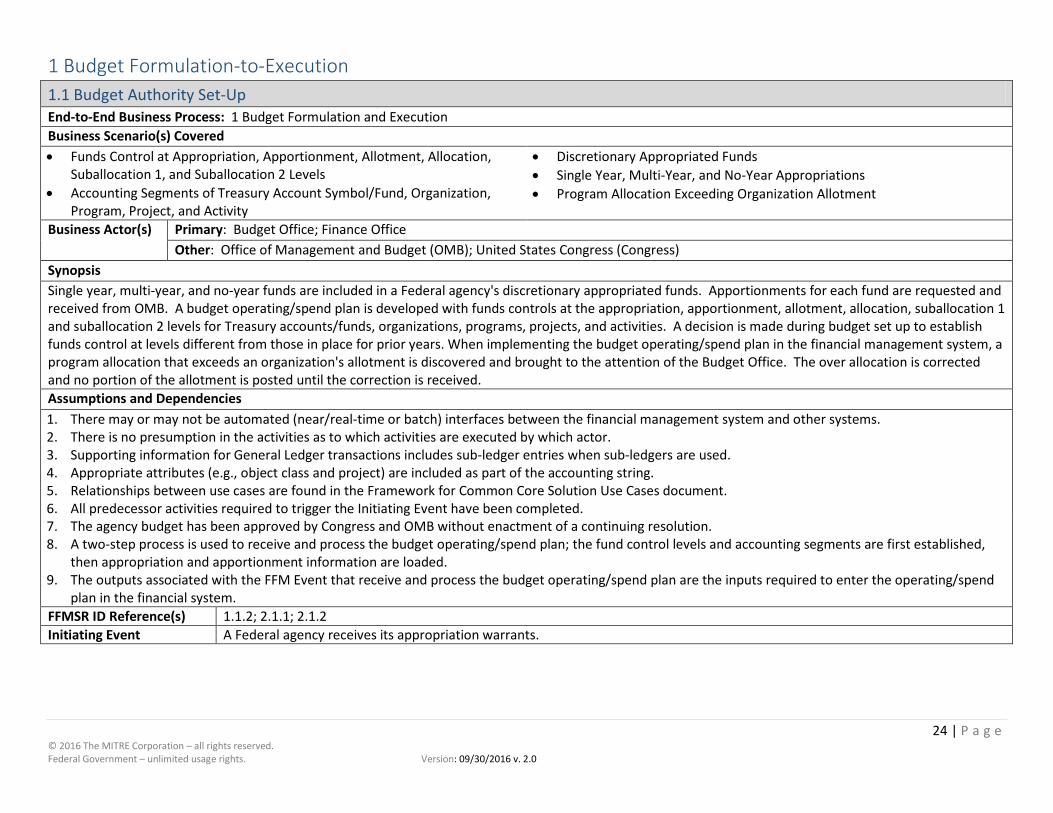

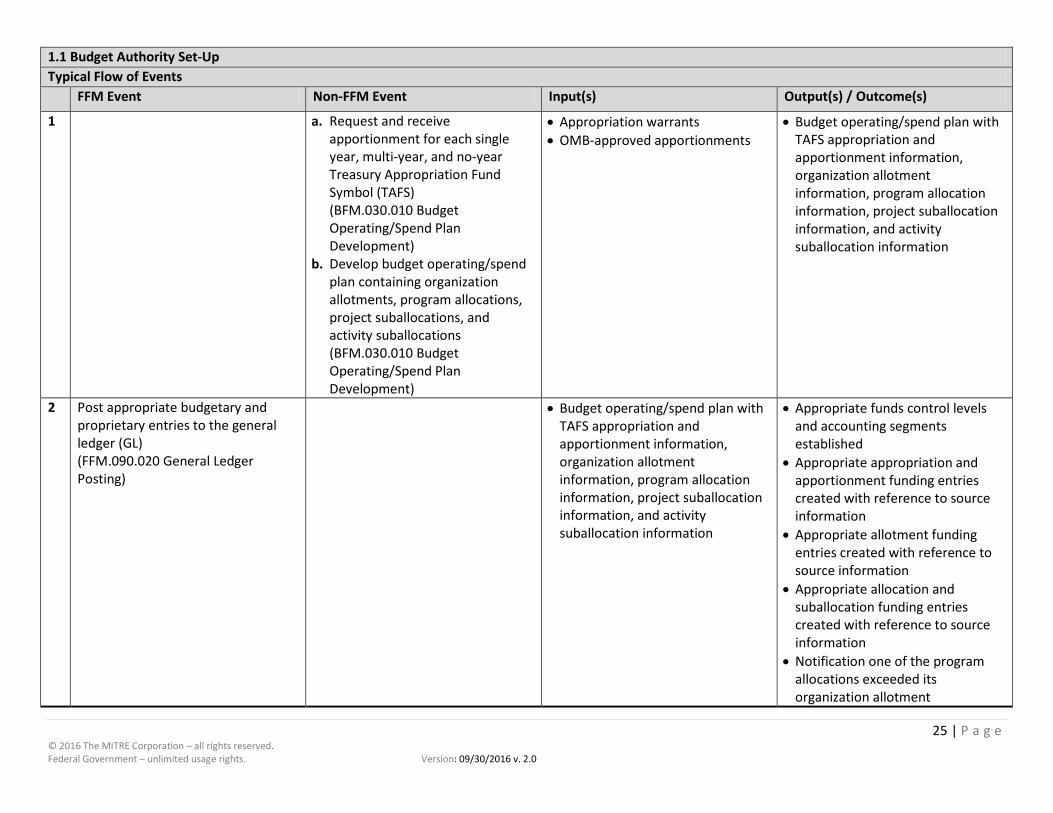

1 Budget Formulation-to-Execution 1.1 Budget Authority Set-Up End-to-End Business Process: 1 Budget Formulation and Execution Business Scenario(s) Covered • Funds Control at Appropriation, Apportionment, Allotment, Allocation,

Suballocation 1, and Suballocation 2 Levels • Accounting Segments of Treasury Account Symbol/Fund, Organization,

Program, Project, and Activity

• Discretionary Appropriated Funds • Single Year, Multi-Year, and No-Year Appropriations • Program Allocation Exceeding Organization Allotment

Business Actor(s) Primary: Budget Office; Finance Office Other: Office of Management and Budget (OMB); United States Congress (Congress)

Synopsis Single year, multi-year, and no-year funds are included in a Federal agency's discretionary appropriated funds. Apportionments for each fund are requested and received from OMB. A budget operating/spend plan is developed with funds controls at the appropriation, apportionment, allotment, allocation, suballocation 1 and suballocation 2 levels for Treasury accounts/funds, organizations, programs, projects, and activities. A decision is made during budget set up to establish funds control at levels different from those in place for prior years. When implementing the budget operating/spend plan in the financial management system, a program allocation that exceeds an organization's allotment is discovered and brought to the attention of the Budget Office. The over allocation is corrected and no portion of the allotment is posted until the correction is received. Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The agency budget has been approved by Congress and OMB without enactment of a continuing resolution. 8. A two-step process is used to receive and process the budget operating/spend plan; the fund control levels and accounting segments are first established,

then appropriation and apportionment information are loaded. 9. The outputs associated with the FFM Event that receive and process the budget operating/spend plan are the inputs required to enter the operating/spend

plan in the financial system. FFMSR ID Reference(s) 1.1.2; 2.1.1; 2.1.2 Initiating Event A Federal agency receives its appropriation warrants.

25 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

1.1 Budget Authority Set-Up Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Request and receive apportionment for each single year, multi-year, and no-year Treasury Appropriation Fund Symbol (TAFS) (BFM.030.010 Budget Operating/Spend Plan Development)

b. Develop budget operating/spend plan containing organization allotments, program allocations, project suballocations, and activity suballocations (BFM.030.010 Budget Operating/Spend Plan Development)

• Appropriation warrants • OMB-approved apportionments

• Budget operating/spend plan with TAFS appropriation and apportionment information, organization allotment information, program allocation information, project suballocation information, and activity suballocation information

2 Post appropriate budgetary and proprietary entries to the general ledger (GL) (FFM.090.020 General Ledger Posting)

• Budget operating/spend plan with TAFS appropriation and apportionment information, organization allotment information, program allocation information, project suballocation information, and activity suballocation information

• Appropriate funds control levels and accounting segments established

• Appropriate appropriation and apportionment funding entries created with reference to source information

• Appropriate allotment funding entries created with reference to source information

• Appropriate allocation and suballocation funding entries created with reference to source information

• Notification one of the program allocations exceeded its organization allotment

26 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

1.1 Budget Authority Set-Up Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

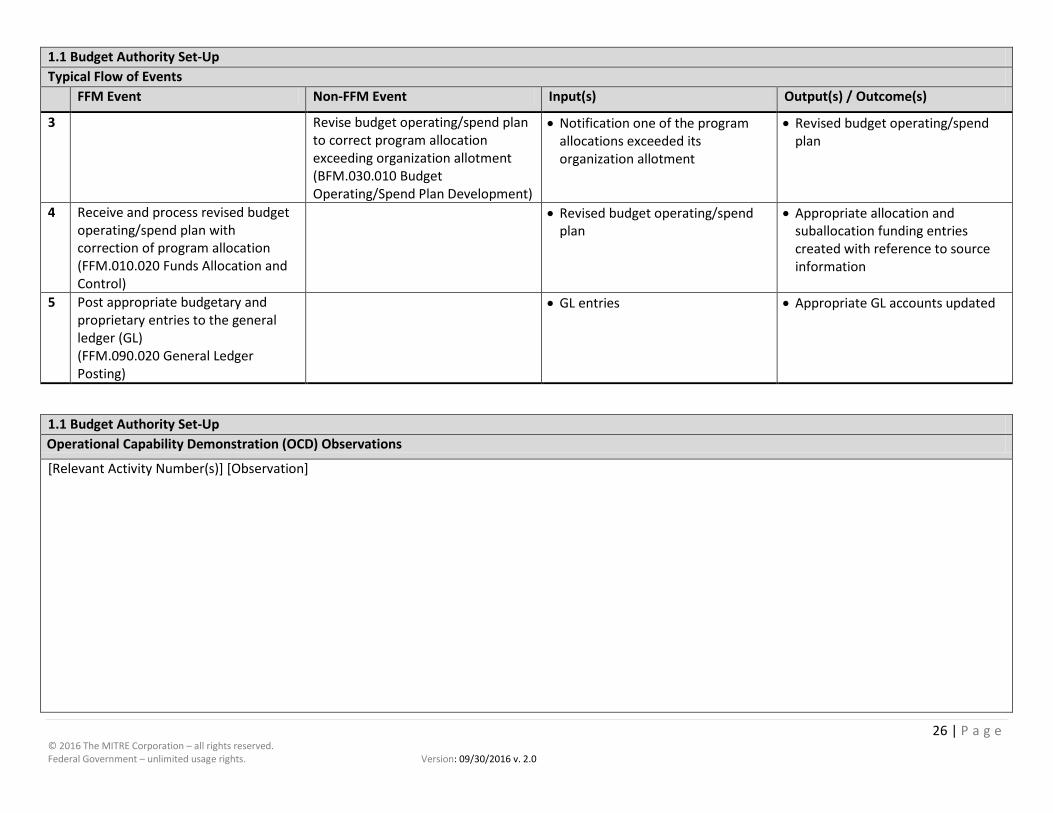

3 Revise budget operating/spend plan to correct program allocation exceeding organization allotment (BFM.030.010 Budget Operating/Spend Plan Development)

• Notification one of the program allocations exceeded its organization allotment

• Revised budget operating/spend plan

4 Receive and process revised budget operating/spend plan with correction of program allocation (FFM.010.020 Funds Allocation and Control)

• Revised budget operating/spend plan

• Appropriate allocation and suballocation funding entries created with reference to source information

5 Post appropriate budgetary and proprietary entries to the general ledger (GL) (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

1.1 Budget Authority Set-Up Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

27 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

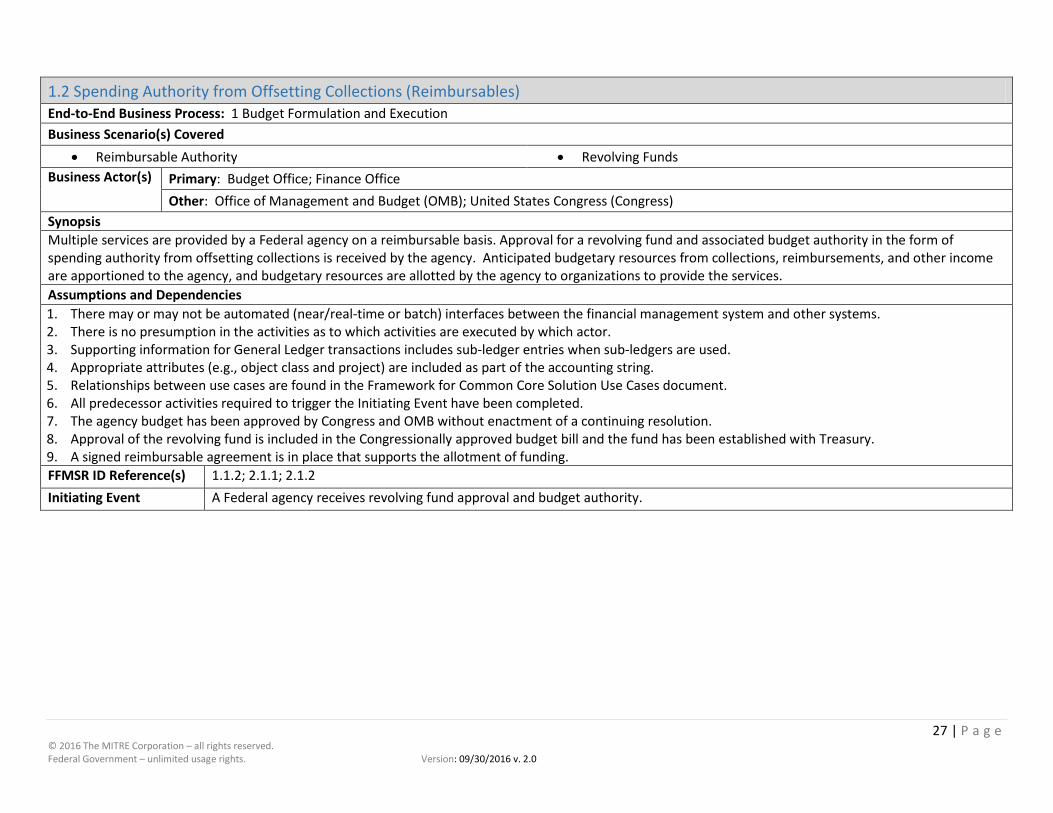

1.2 Spending Authority from Offsetting Collections (Reimbursables) End-to-End Business Process: 1 Budget Formulation and Execution Business Scenario(s) Covered

• Reimbursable Authority • Revolving Funds Business Actor(s) Primary: Budget Office; Finance Office

Other: Office of Management and Budget (OMB); United States Congress (Congress) Synopsis Multiple services are provided by a Federal agency on a reimbursable basis. Approval for a revolving fund and associated budget authority in the form of spending authority from offsetting collections is received by the agency. Anticipated budgetary resources from collections, reimbursements, and other income are apportioned to the agency, and budgetary resources are allotted by the agency to organizations to provide the services. Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The agency budget has been approved by Congress and OMB without enactment of a continuing resolution. 8. Approval of the revolving fund is included in the Congressionally approved budget bill and the fund has been established with Treasury. 9. A signed reimbursable agreement is in place that supports the allotment of funding. FFMSR ID Reference(s) 1.1.2; 2.1.1; 2.1.2 Initiating Event A Federal agency receives revolving fund approval and budget authority.

28 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

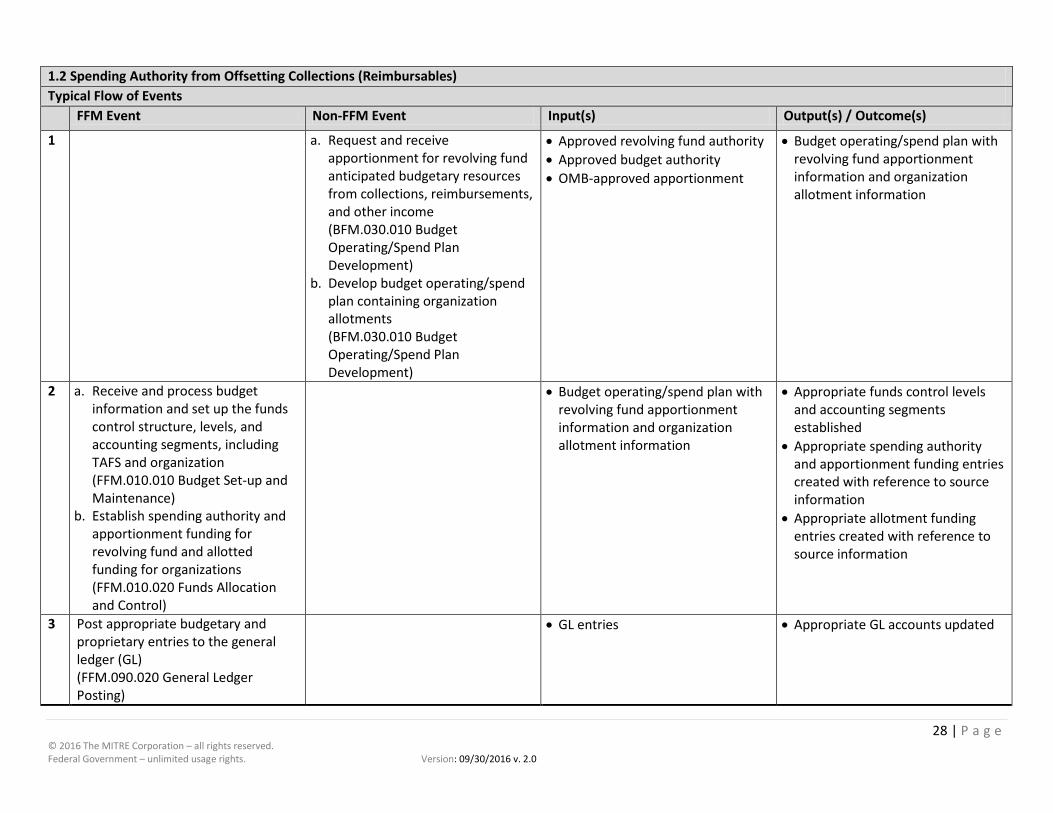

1.2 Spending Authority from Offsetting Collections (Reimbursables) Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Request and receive apportionment for revolving fund anticipated budgetary resources from collections, reimbursements, and other income (BFM.030.010 Budget Operating/Spend Plan Development)

b. Develop budget operating/spend plan containing organization allotments (BFM.030.010 Budget Operating/Spend Plan Development)

• Approved revolving fund authority • Approved budget authority • OMB-approved apportionment

• Budget operating/spend plan with revolving fund apportionment information and organization allotment information

2 a. Receive and process budget information and set up the funds control structure, levels, and accounting segments, including TAFS and organization (FFM.010.010 Budget Set-up and Maintenance)

b. Establish spending authority and apportionment funding for revolving fund and allotted funding for organizations (FFM.010.020 Funds Allocation and Control)

• Budget operating/spend plan with revolving fund apportionment information and organization allotment information

• Appropriate funds control levels and accounting segments established

• Appropriate spending authority and apportionment funding entries created with reference to source information

• Appropriate allotment funding entries created with reference to source information

3 Post appropriate budgetary and proprietary entries to the general ledger (GL) (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

29 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

1.2 Spending Authority from Offsetting Collections (Reimbursables)

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

30 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

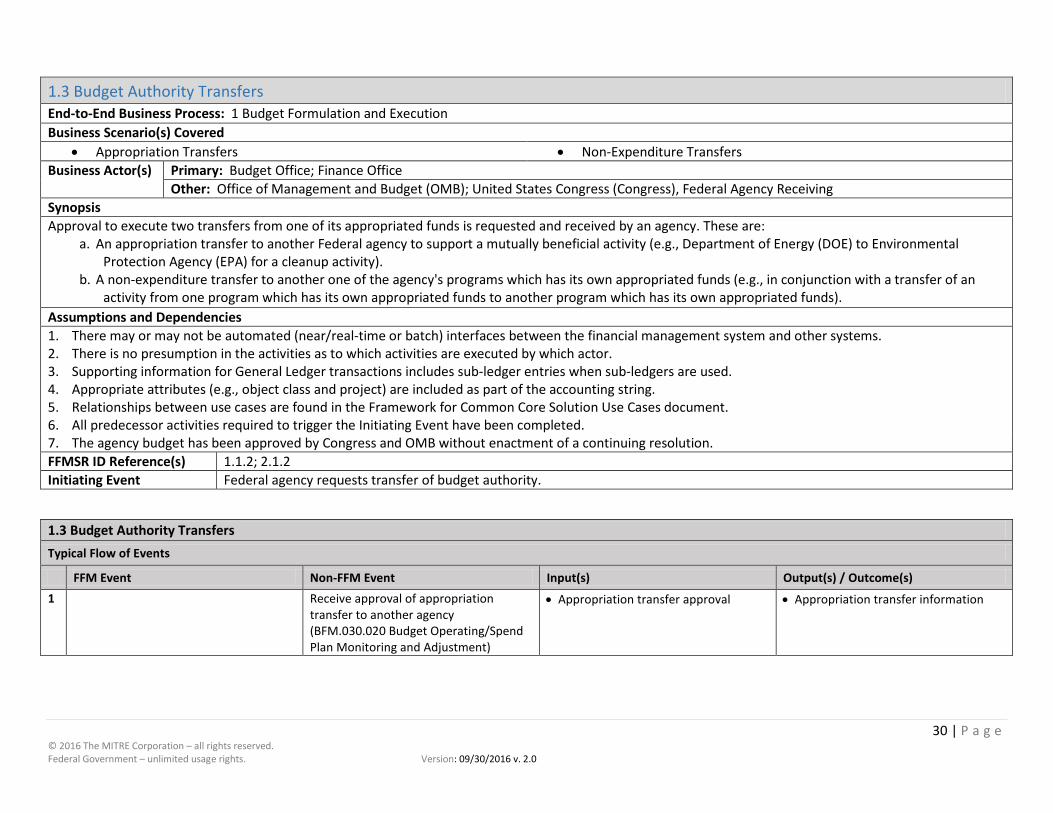

1.3 Budget Authority Transfers End-to-End Business Process: 1 Budget Formulation and Execution Business Scenario(s) Covered

• Appropriation Transfers • Non-Expenditure Transfers Business Actor(s) Primary: Budget Office; Finance Office

Other: Office of Management and Budget (OMB); United States Congress (Congress), Federal Agency Receiving Synopsis Approval to execute two transfers from one of its appropriated funds is requested and received by an agency. These are:

a. An appropriation transfer to another Federal agency to support a mutually beneficial activity (e.g., Department of Energy (DOE) to Environmental Protection Agency (EPA) for a cleanup activity).

b. A non-expenditure transfer to another one of the agency's programs which has its own appropriated funds (e.g., in conjunction with a transfer of an activity from one program which has its own appropriated funds to another program which has its own appropriated funds).

Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The agency budget has been approved by Congress and OMB without enactment of a continuing resolution. FFMSR ID Reference(s) 1.1.2; 2.1.2 Initiating Event Federal agency requests transfer of budget authority.

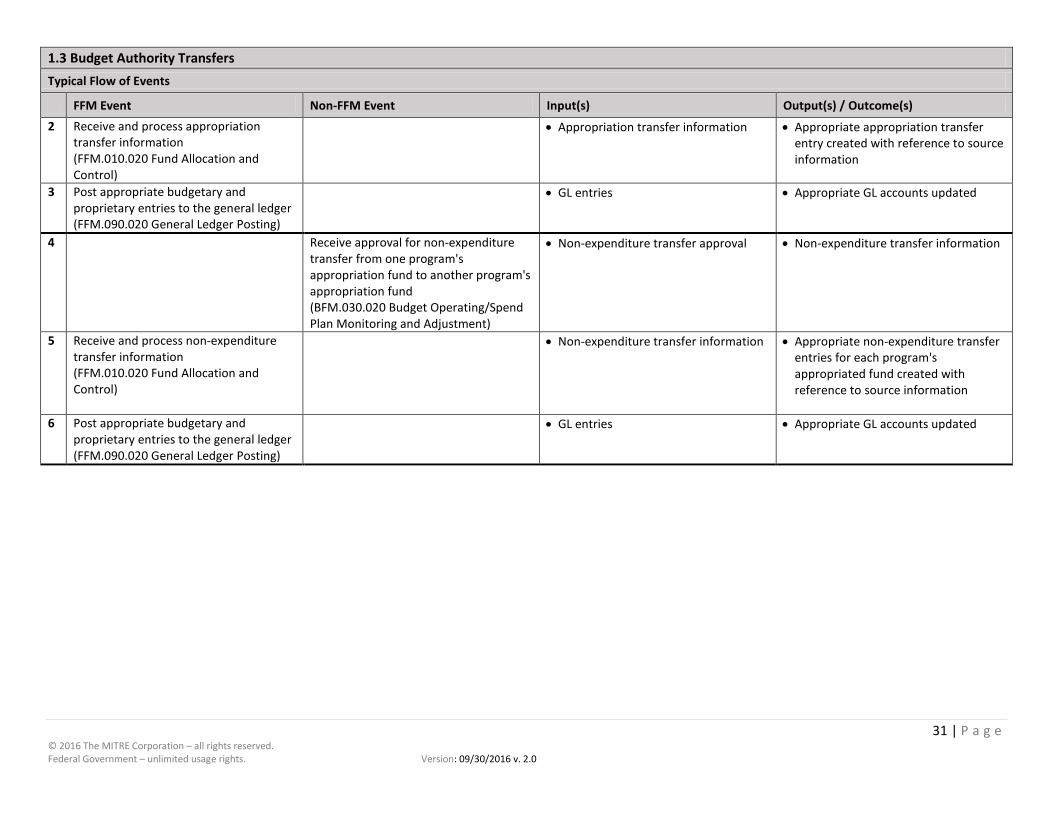

1.3 Budget Authority Transfers Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s) 1 Receive approval of appropriation

transfer to another agency (BFM.030.020 Budget Operating/Spend Plan Monitoring and Adjustment)

• Appropriation transfer approval • Appropriation transfer information

31 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

1.3 Budget Authority Transfers Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s) 2 Receive and process appropriation

transfer information (FFM.010.020 Fund Allocation and Control)

• Appropriation transfer information • Appropriate appropriation transfer entry created with reference to source information

3 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

4 Receive approval for non-expenditure transfer from one program's appropriation fund to another program's appropriation fund (BFM.030.020 Budget Operating/Spend Plan Monitoring and Adjustment)

• Non-expenditure transfer approval • Non-expenditure transfer information

5 Receive and process non-expenditure transfer information (FFM.010.020 Fund Allocation and Control)

• Non-expenditure transfer information • Appropriate non-expenditure transfer entries for each program's appropriated fund created with reference to source information

6 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

32 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

1.3 Budget Authority Transfers

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

33 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

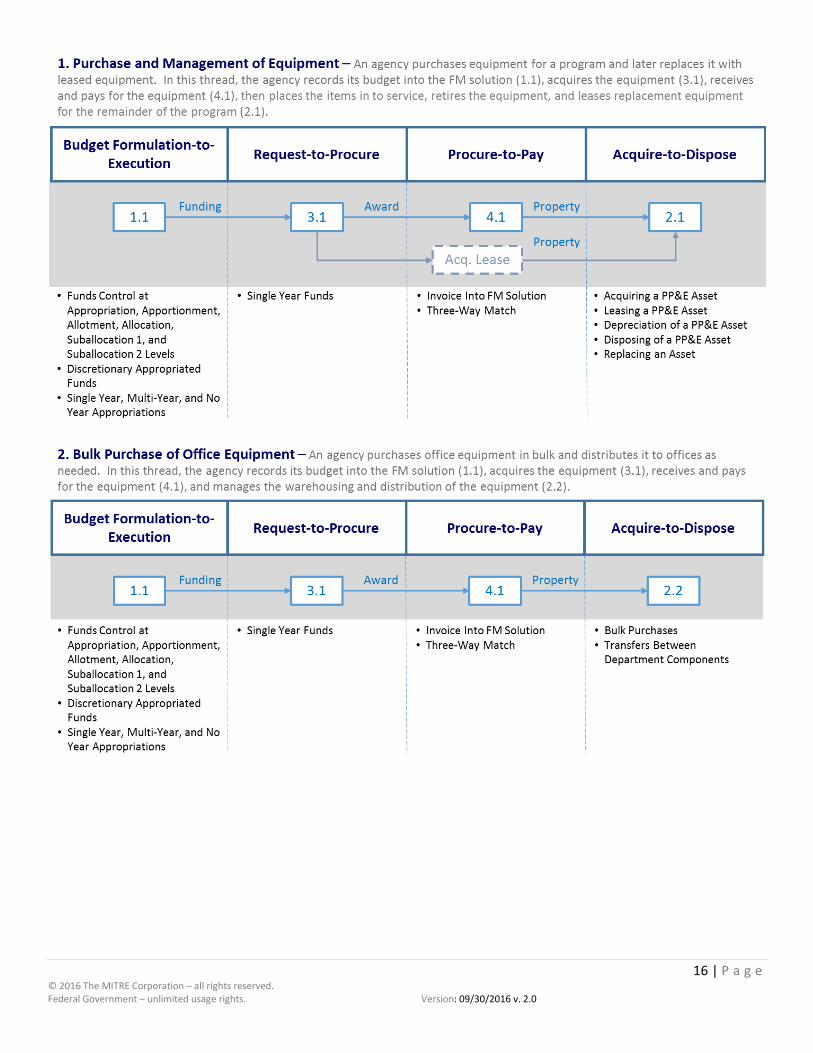

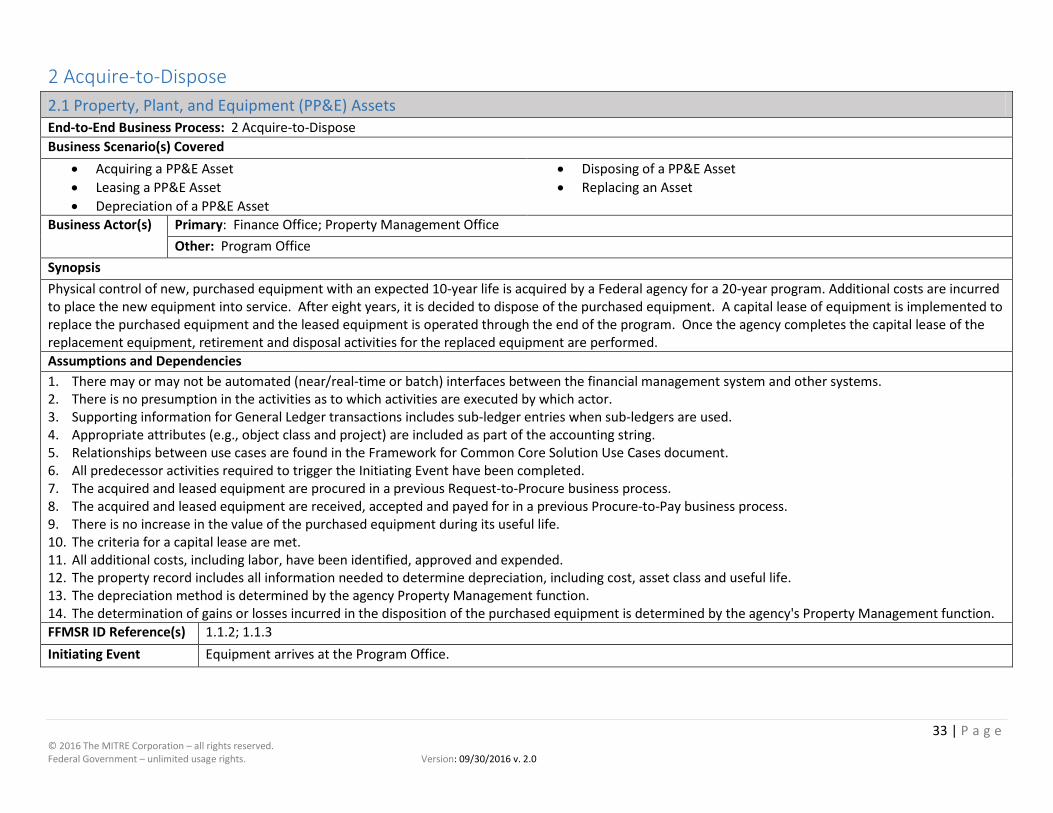

2 Acquire-to-Dispose 2.1 Property, Plant, and Equipment (PP&E) Assets End-to-End Business Process: 2 Acquire-to-Dispose Business Scenario(s) Covered

• Acquiring a PP&E Asset • Leasing a PP&E Asset • Depreciation of a PP&E Asset

• Disposing of a PP&E Asset • Replacing an Asset

Business Actor(s) Primary: Finance Office; Property Management Office Other: Program Office

Synopsis Physical control of new, purchased equipment with an expected 10-year life is acquired by a Federal agency for a 20-year program. Additional costs are incurred to place the new equipment into service. After eight years, it is decided to dispose of the purchased equipment. A capital lease of equipment is implemented to replace the purchased equipment and the leased equipment is operated through the end of the program. Once the agency completes the capital lease of the replacement equipment, retirement and disposal activities for the replaced equipment are performed. Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The acquired and leased equipment are procured in a previous Request-to-Procure business process. 8. The acquired and leased equipment are received, accepted and payed for in a previous Procure-to-Pay business process. 9. There is no increase in the value of the purchased equipment during its useful life. 10. The criteria for a capital lease are met. 11. All additional costs, including labor, have been identified, approved and expended. 12. The property record includes all information needed to determine depreciation, including cost, asset class and useful life. 13. The depreciation method is determined by the agency Property Management function. 14. The determination of gains or losses incurred in the disposition of the purchased equipment is determined by the agency's Property Management function. FFMSR ID Reference(s) 1.1.2; 1.1.3 Initiating Event Equipment arrives at the Program Office.

34 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

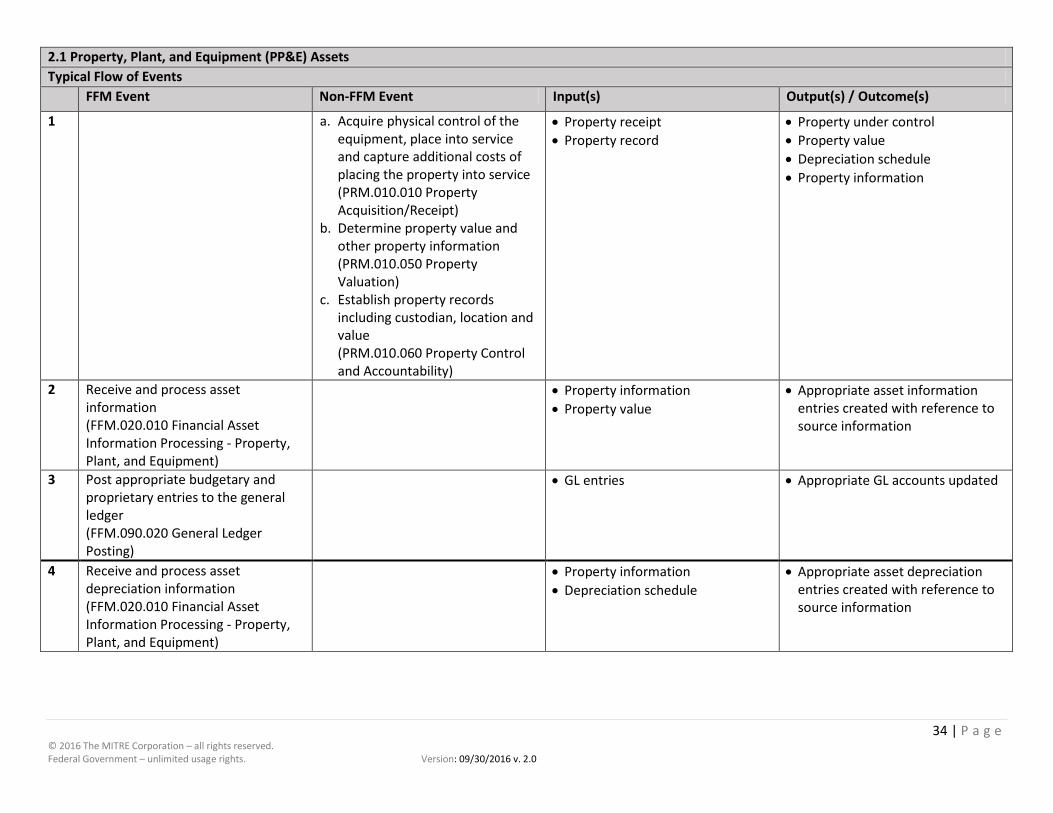

2.1 Property, Plant, and Equipment (PP&E) Assets Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Acquire physical control of the equipment, place into service and capture additional costs of placing the property into service (PRM.010.010 Property Acquisition/Receipt)

b. Determine property value and other property information (PRM.010.050 Property Valuation)

c. Establish property records including custodian, location and value (PRM.010.060 Property Control and Accountability)

• Property receipt • Property record

• Property under control • Property value • Depreciation schedule • Property information

2 Receive and process asset information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Property information • Property value

• Appropriate asset information entries created with reference to source information

3 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

4 Receive and process asset depreciation information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Property information • Depreciation schedule

• Appropriate asset depreciation entries created with reference to source information

35 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

2.1 Property, Plant, and Equipment (PP&E) Assets Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

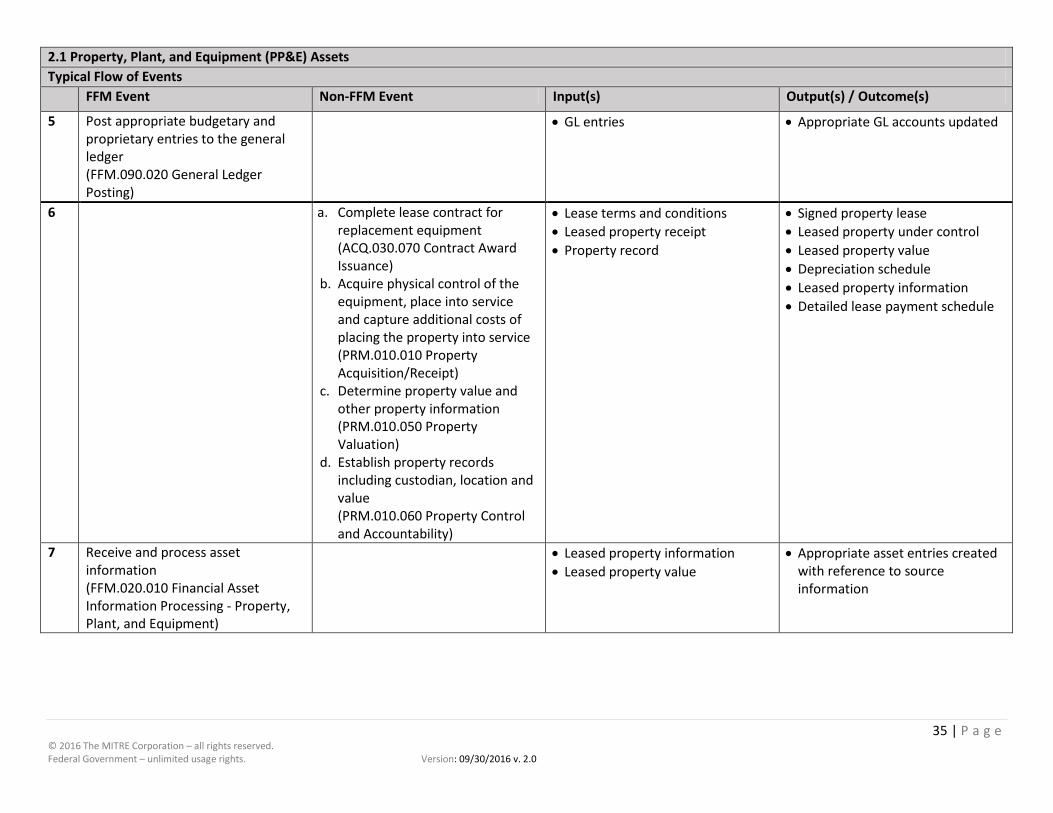

5 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

6 a. Complete lease contract for replacement equipment (ACQ.030.070 Contract Award Issuance)

b. Acquire physical control of the equipment, place into service and capture additional costs of placing the property into service (PRM.010.010 Property Acquisition/Receipt)

c. Determine property value and other property information (PRM.010.050 Property Valuation)

d. Establish property records including custodian, location and value (PRM.010.060 Property Control and Accountability)

• Lease terms and conditions • Leased property receipt • Property record

• Signed property lease • Leased property under control • Leased property value • Depreciation schedule • Leased property information • Detailed lease payment schedule

7 Receive and process asset information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Leased property information • Leased property value

• Appropriate asset entries created with reference to source information

36 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

2.1 Property, Plant, and Equipment (PP&E) Assets Typical Flow of Events FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

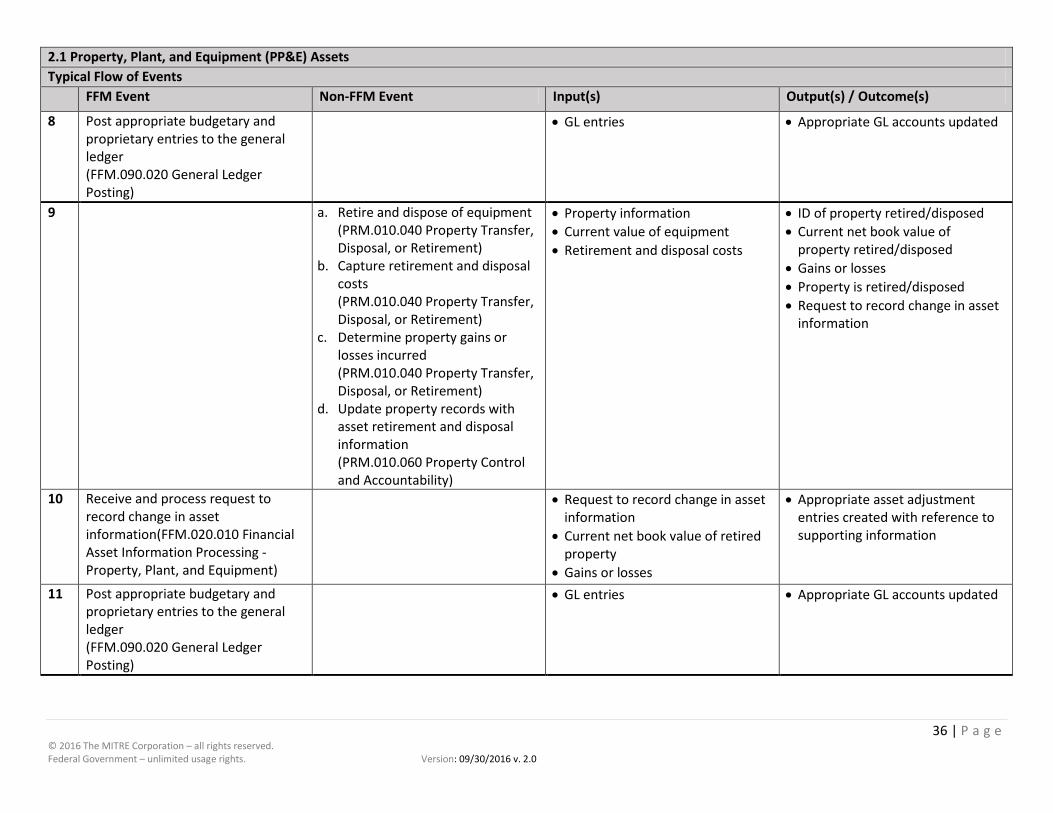

8 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

9 a. Retire and dispose of equipment (PRM.010.040 Property Transfer, Disposal, or Retirement)

b. Capture retirement and disposal costs (PRM.010.040 Property Transfer, Disposal, or Retirement)

c. Determine property gains or losses incurred (PRM.010.040 Property Transfer, Disposal, or Retirement)

d. Update property records with asset retirement and disposal information (PRM.010.060 Property Control and Accountability)

• Property information • Current value of equipment • Retirement and disposal costs

• ID of property retired/disposed • Current net book value of

property retired/disposed • Gains or losses • Property is retired/disposed • Request to record change in asset

information

10 Receive and process request to record change in asset information(FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Request to record change in asset information

• Current net book value of retired property

• Gains or losses

• Appropriate asset adjustment entries created with reference to supporting information

11 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

37 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

2.1 Property, Plant, and Equipment (PP&E) Assets

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

38 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

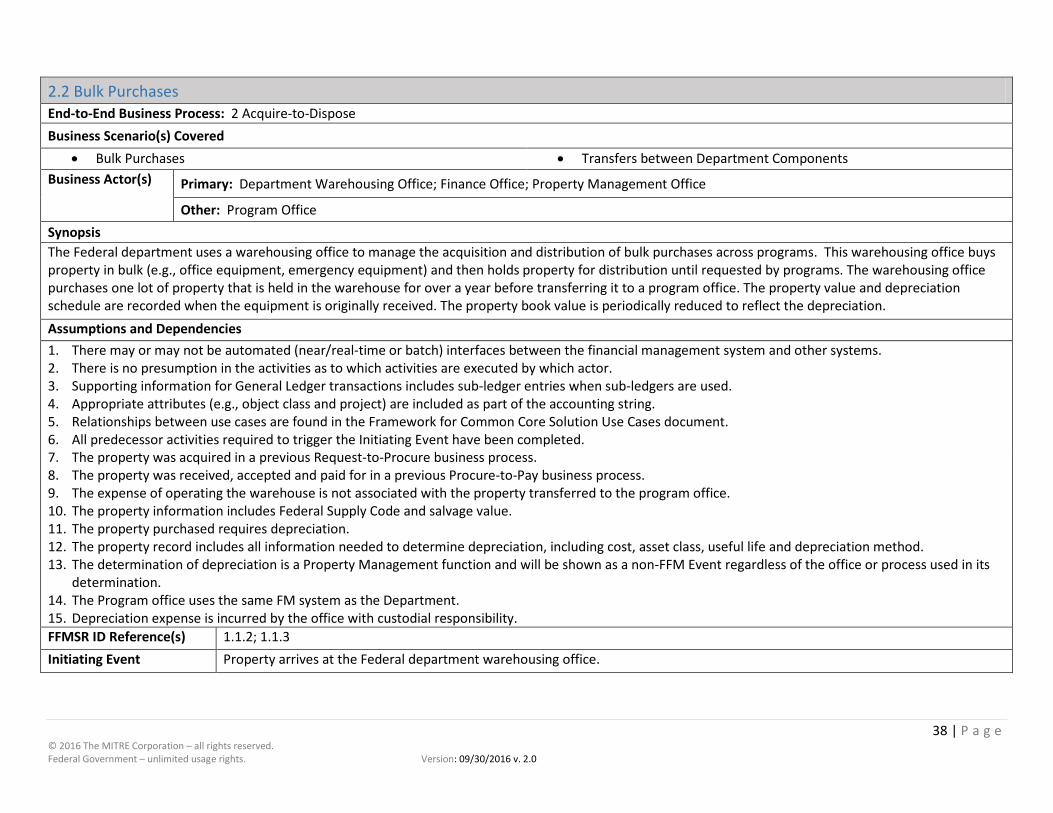

2.2 Bulk Purchases End-to-End Business Process: 2 Acquire-to-Dispose Business Scenario(s) Covered

• Bulk Purchases • Transfers between Department Components Business Actor(s) Primary: Department Warehousing Office; Finance Office; Property Management Office

Other: Program Office Synopsis The Federal department uses a warehousing office to manage the acquisition and distribution of bulk purchases across programs. This warehousing office buys property in bulk (e.g., office equipment, emergency equipment) and then holds property for distribution until requested by programs. The warehousing office purchases one lot of property that is held in the warehouse for over a year before transferring it to a program office. The property value and depreciation schedule are recorded when the equipment is originally received. The property book value is periodically reduced to reflect the depreciation. Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The property was acquired in a previous Request-to-Procure business process. 8. The property was received, accepted and paid for in a previous Procure-to-Pay business process. 9. The expense of operating the warehouse is not associated with the property transferred to the program office. 10. The property information includes Federal Supply Code and salvage value. 11. The property purchased requires depreciation. 12. The property record includes all information needed to determine depreciation, including cost, asset class, useful life and depreciation method. 13. The determination of depreciation is a Property Management function and will be shown as a non-FFM Event regardless of the office or process used in its

determination. 14. The Program office uses the same FM system as the Department. 15. Depreciation expense is incurred by the office with custodial responsibility. FFMSR ID Reference(s) 1.1.2; 1.1.3 Initiating Event Property arrives at the Federal department warehousing office.

39 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

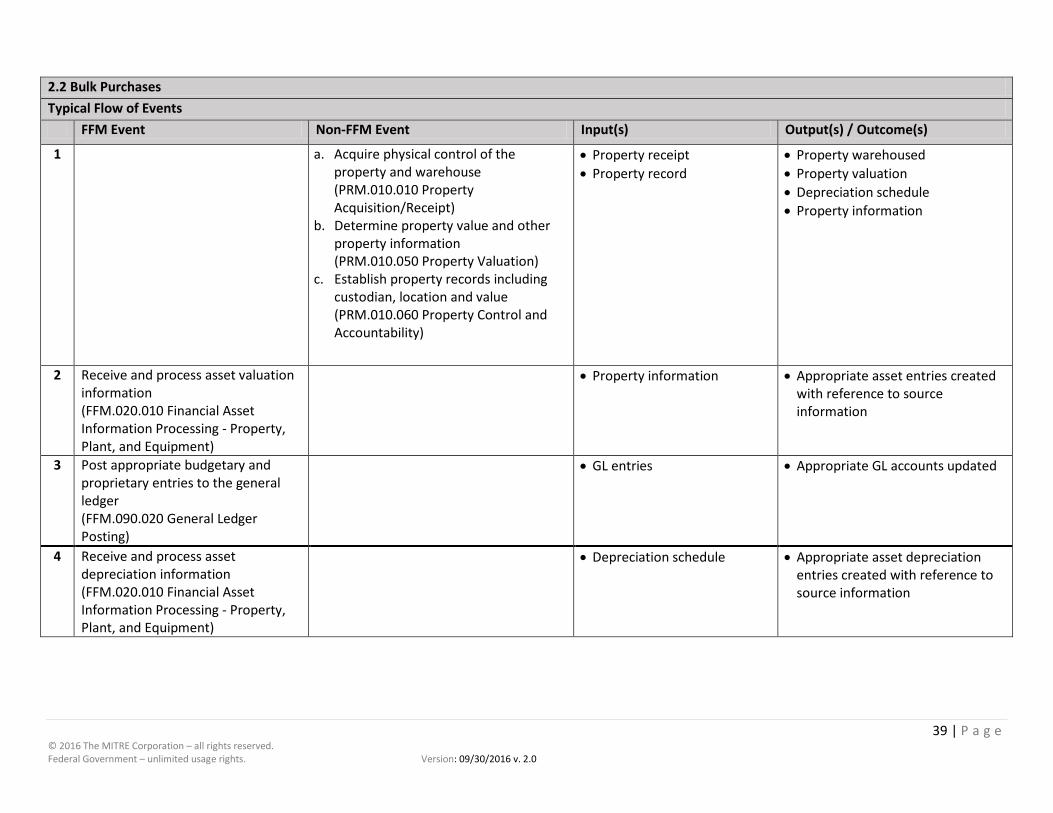

2.2 Bulk Purchases Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Acquire physical control of the property and warehouse (PRM.010.010 Property Acquisition/Receipt)

b. Determine property value and other property information (PRM.010.050 Property Valuation)

c. Establish property records including custodian, location and value (PRM.010.060 Property Control and Accountability)

• Property receipt • Property record

• Property warehoused • Property valuation • Depreciation schedule • Property information

2 Receive and process asset valuation information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Property information • Appropriate asset entries created with reference to source information

3 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

4 Receive and process asset depreciation information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Depreciation schedule • Appropriate asset depreciation entries created with reference to source information

40 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

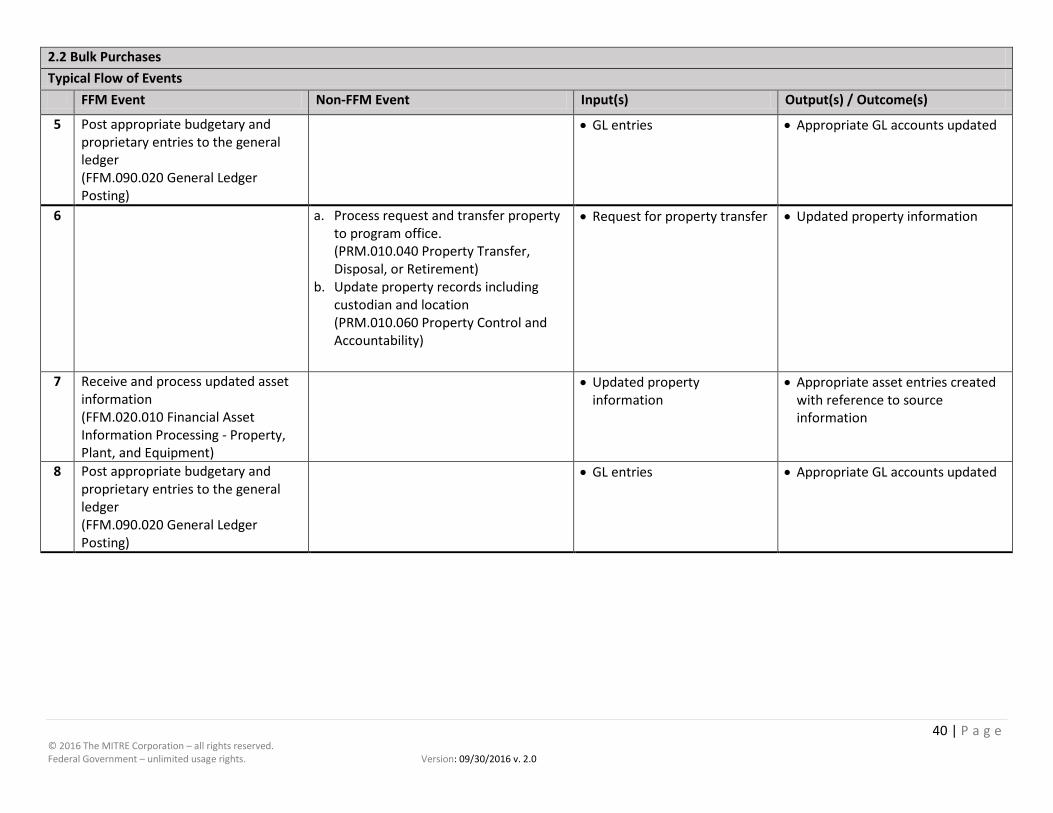

2.2 Bulk Purchases Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

5 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

6 a. Process request and transfer property to program office. (PRM.010.040 Property Transfer, Disposal, or Retirement)

b. Update property records including custodian and location (PRM.010.060 Property Control and Accountability)

• Request for property transfer • Updated property information

7 Receive and process updated asset information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Updated property information

• Appropriate asset entries created with reference to source information

8 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

41 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

2.2 Bulk Purchases

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

42 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

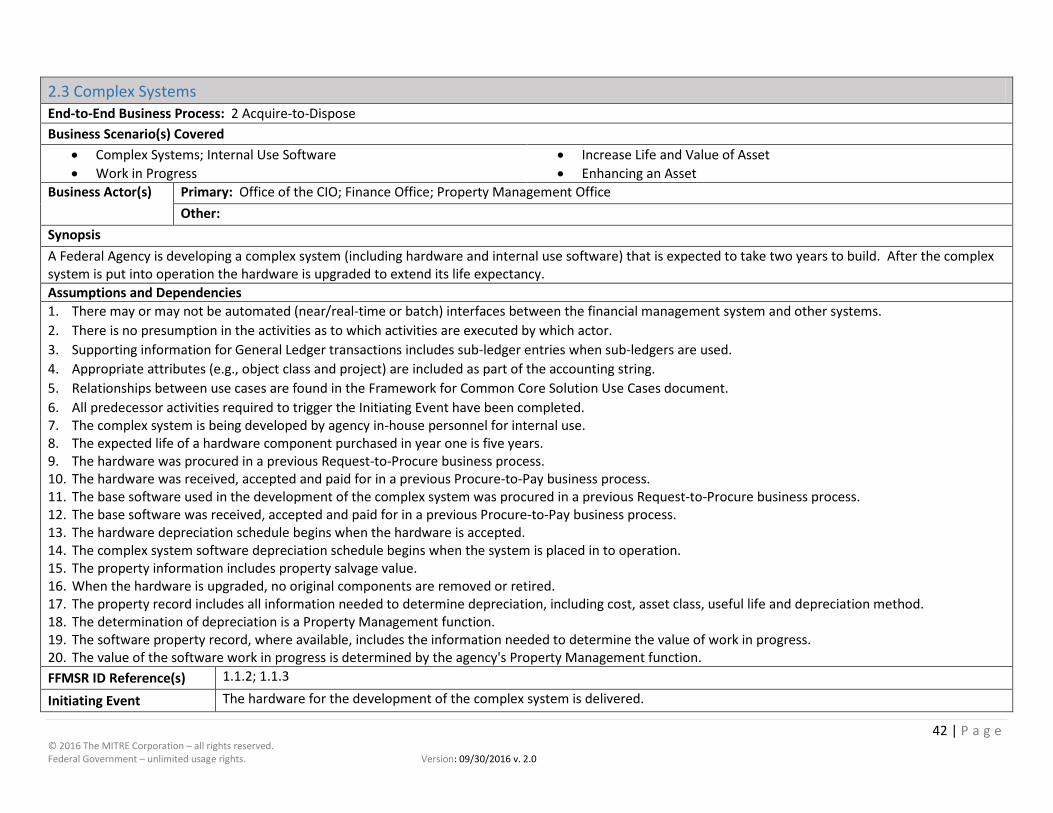

2.3 Complex Systems End-to-End Business Process: 2 Acquire-to-Dispose Business Scenario(s) Covered

• Complex Systems; Internal Use Software • Work in Progress

• Increase Life and Value of Asset • Enhancing an Asset

Business Actor(s) Primary: Office of the CIO; Finance Office; Property Management Office Other:

Synopsis A Federal Agency is developing a complex system (including hardware and internal use software) that is expected to take two years to build. After the complex system is put into operation the hardware is upgraded to extend its life expectancy. Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. The complex system is being developed by agency in-house personnel for internal use. 8. The expected life of a hardware component purchased in year one is five years. 9. The hardware was procured in a previous Request-to-Procure business process. 10. The hardware was received, accepted and paid for in a previous Procure-to-Pay business process. 11. The base software used in the development of the complex system was procured in a previous Request-to-Procure business process. 12. The base software was received, accepted and paid for in a previous Procure-to-Pay business process. 13. The hardware depreciation schedule begins when the hardware is accepted. 14. The complex system software depreciation schedule begins when the system is placed in to operation. 15. The property information includes property salvage value. 16. When the hardware is upgraded, no original components are removed or retired. 17. The property record includes all information needed to determine depreciation, including cost, asset class, useful life and depreciation method. 18. The determination of depreciation is a Property Management function. 19. The software property record, where available, includes the information needed to determine the value of work in progress. 20. The value of the software work in progress is determined by the agency's Property Management function. FFMSR ID Reference(s) 1.1.2; 1.1.3

Initiating Event The hardware for the development of the complex system is delivered.

43 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

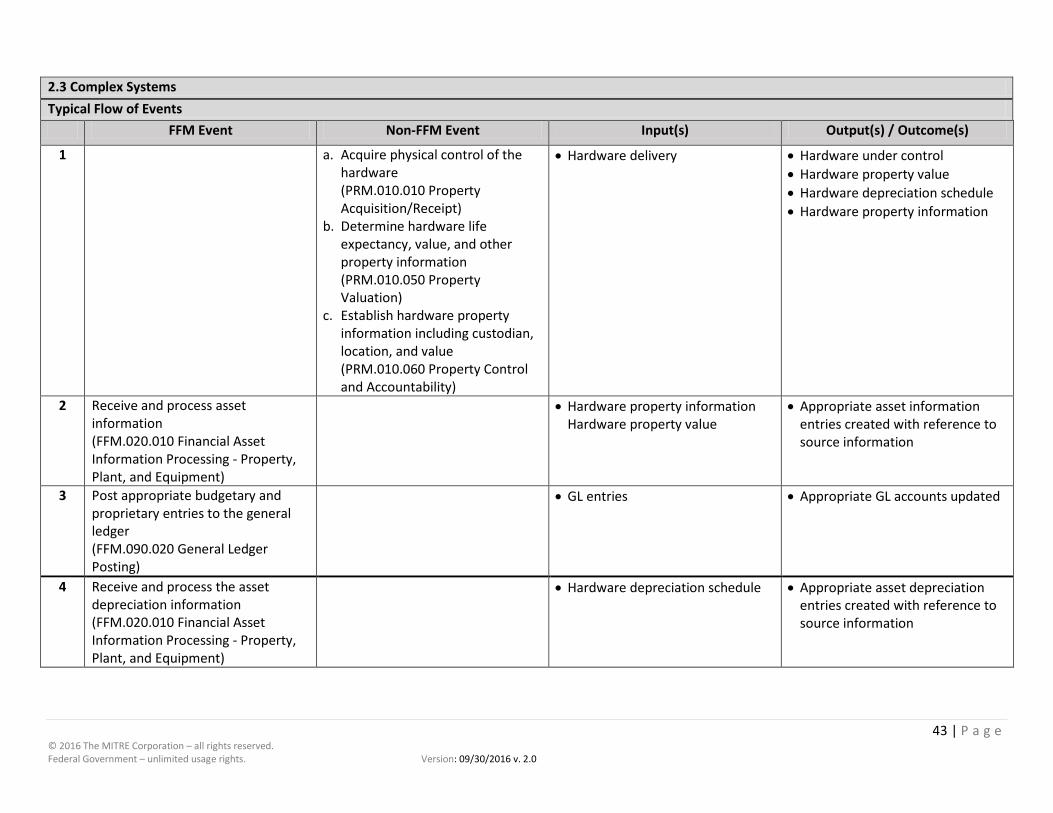

2.3 Complex Systems Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Acquire physical control of the hardware (PRM.010.010 Property Acquisition/Receipt)

b. Determine hardware life expectancy, value, and other property information (PRM.010.050 Property Valuation)

c. Establish hardware property information including custodian, location, and value (PRM.010.060 Property Control and Accountability)

• Hardware delivery • Hardware under control • Hardware property value • Hardware depreciation schedule • Hardware property information

2 Receive and process asset information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Hardware property information Hardware property value

• Appropriate asset information entries created with reference to source information

3 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

4 Receive and process the asset depreciation information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Hardware depreciation schedule • Appropriate asset depreciation entries created with reference to source information

44 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

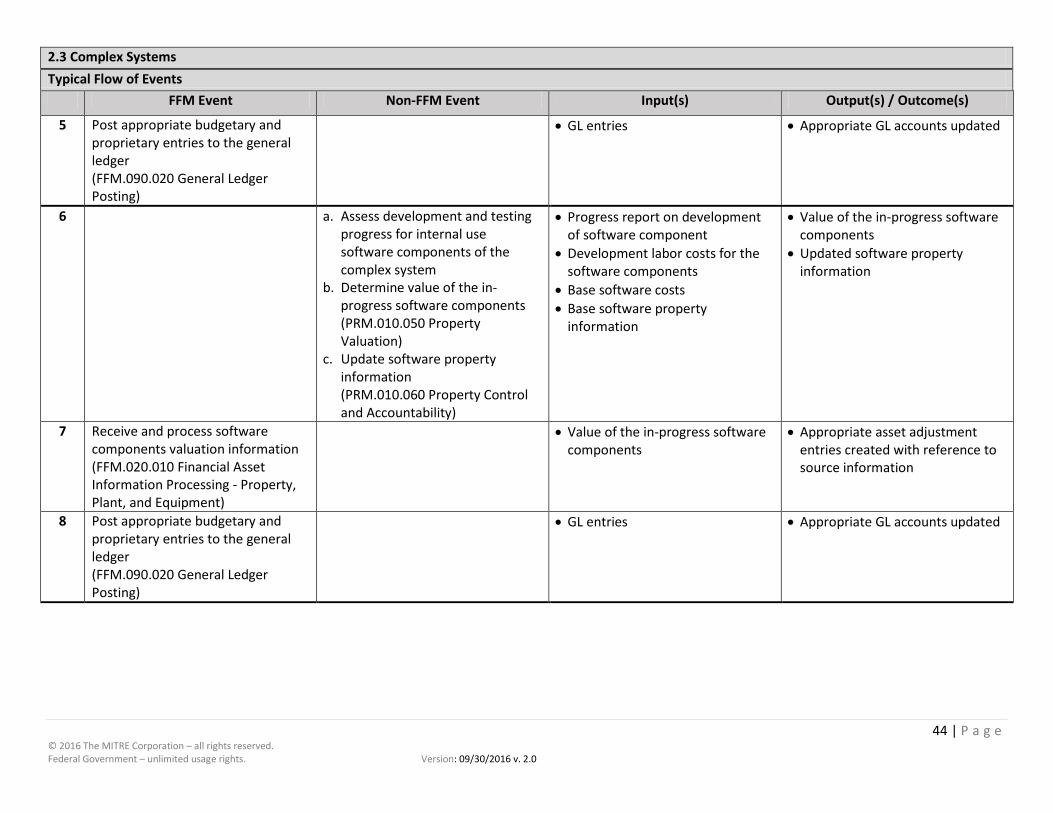

2.3 Complex Systems Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

5 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

6 a. Assess development and testing progress for internal use software components of the complex system

b. Determine value of the in-progress software components (PRM.010.050 Property Valuation)

c. Update software property information (PRM.010.060 Property Control and Accountability)

• Progress report on development of software component

• Development labor costs for the software components

• Base software costs • Base software property

information

• Value of the in-progress software components

• Updated software property information

7 Receive and process software components valuation information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Value of the in-progress software components

• Appropriate asset adjustment entries created with reference to source information

8 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

45 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

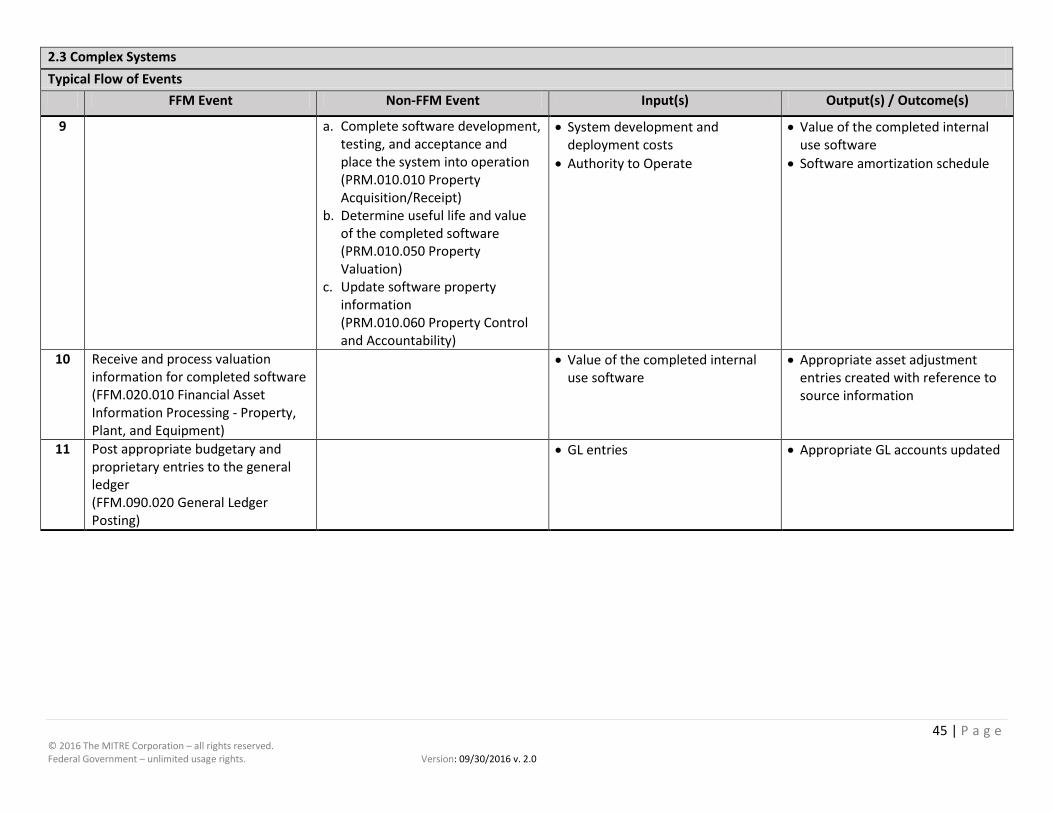

2.3 Complex Systems Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

9 a. Complete software development, testing, and acceptance and place the system into operation (PRM.010.010 Property Acquisition/Receipt)

b. Determine useful life and value of the completed software (PRM.010.050 Property Valuation)

c. Update software property information (PRM.010.060 Property Control and Accountability)

• System development and deployment costs

• Authority to Operate

• Value of the completed internal use software

• Software amortization schedule

10 Receive and process valuation information for completed software (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Value of the completed internal use software

• Appropriate asset adjustment entries created with reference to source information

11 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

46 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

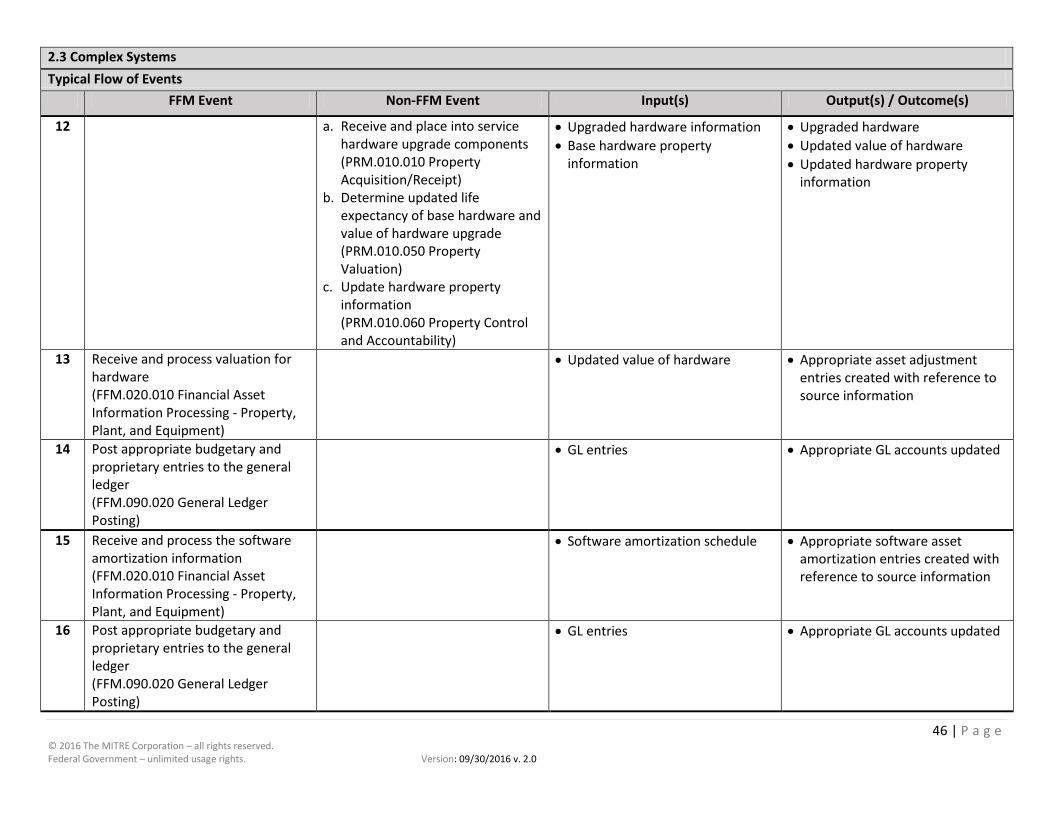

2.3 Complex Systems Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

12 a. Receive and place into service hardware upgrade components (PRM.010.010 Property Acquisition/Receipt)

b. Determine updated life expectancy of base hardware and value of hardware upgrade (PRM.010.050 Property Valuation)

c. Update hardware property information (PRM.010.060 Property Control and Accountability)

• Upgraded hardware information • Base hardware property

information

• Upgraded hardware • Updated value of hardware • Updated hardware property

information

13 Receive and process valuation for hardware (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Updated value of hardware • Appropriate asset adjustment entries created with reference to source information

14 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

15 Receive and process the software amortization information (FFM.020.010 Financial Asset Information Processing - Property, Plant, and Equipment)

• Software amortization schedule • Appropriate software asset amortization entries created with reference to source information

16 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

47 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

2.3 Complex Systems

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

48 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

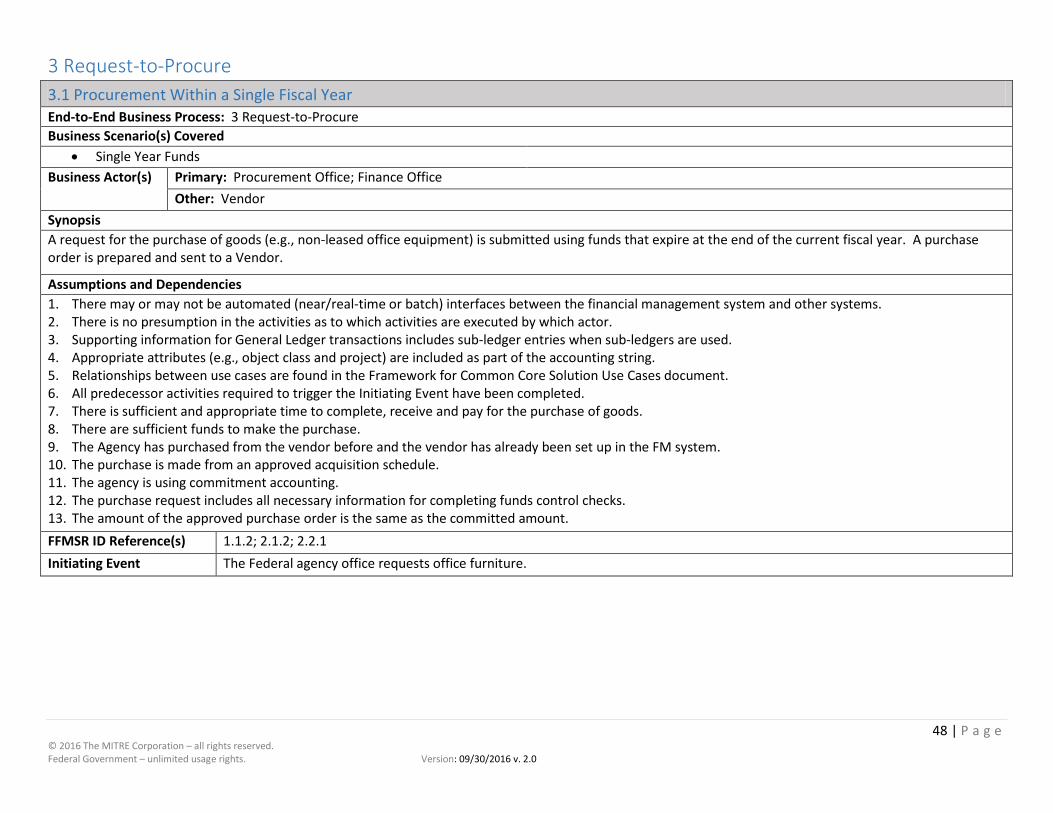

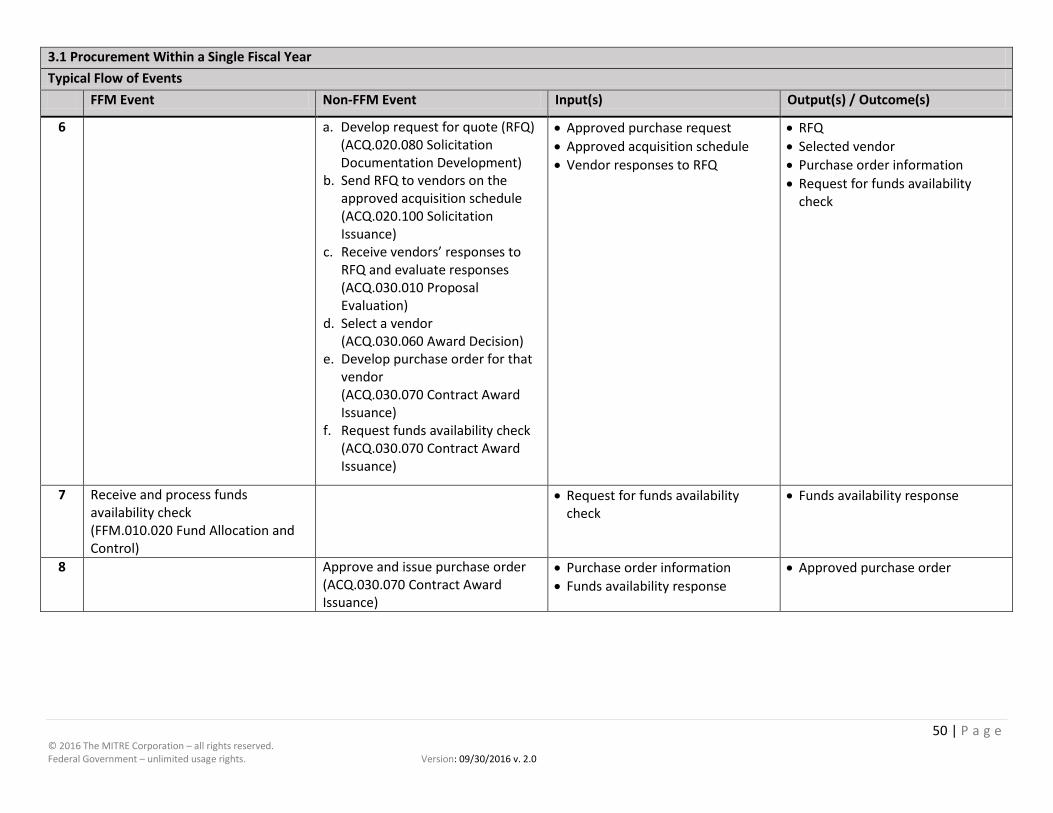

3 Request-to-Procure 3.1 Procurement Within a Single Fiscal Year End-to-End Business Process: 3 Request-to-Procure Business Scenario(s) Covered

• Single Year Funds Business Actor(s) Primary: Procurement Office; Finance Office

Other: Vendor Synopsis A request for the purchase of goods (e.g., non-leased office equipment) is submitted using funds that expire at the end of the current fiscal year. A purchase order is prepared and sent to a Vendor.

Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. There is sufficient and appropriate time to complete, receive and pay for the purchase of goods. 8. There are sufficient funds to make the purchase. 9. The Agency has purchased from the vendor before and the vendor has already been set up in the FM system. 10. The purchase is made from an approved acquisition schedule. 11. The agency is using commitment accounting. 12. The purchase request includes all necessary information for completing funds control checks. 13. The amount of the approved purchase order is the same as the committed amount. FFMSR ID Reference(s) 1.1.2; 2.1.2; 2.2.1 Initiating Event The Federal agency office requests office furniture.

49 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

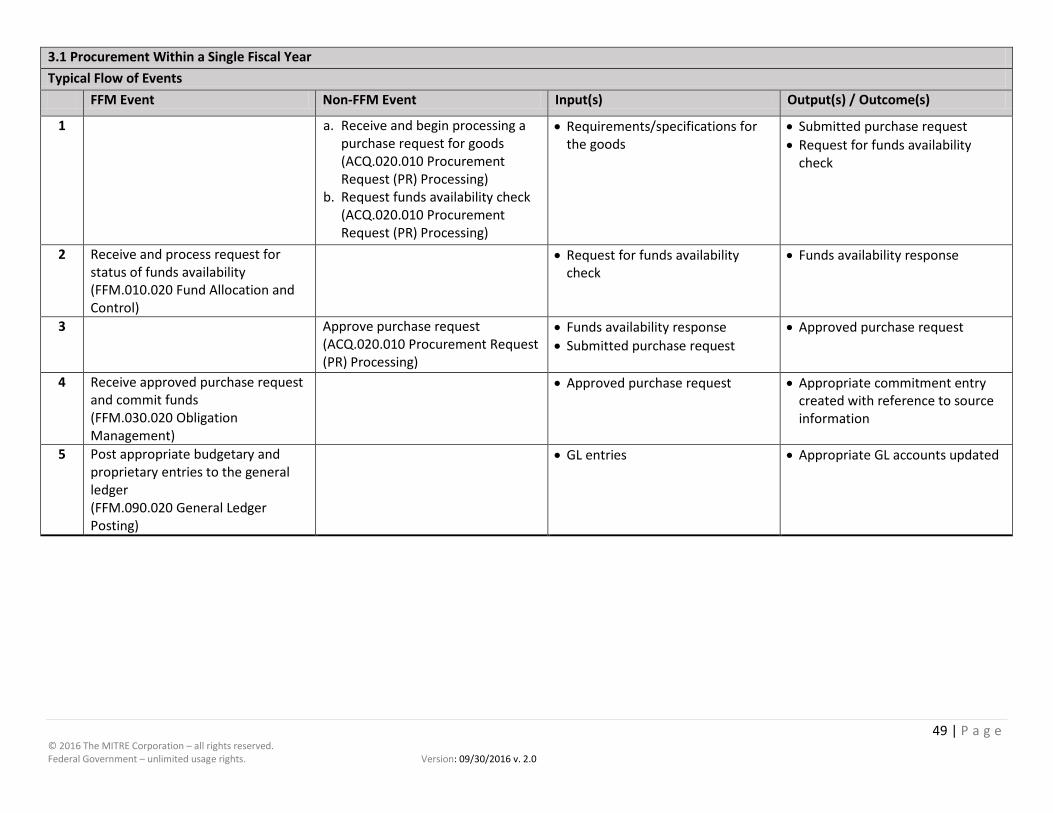

3.1 Procurement Within a Single Fiscal Year Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Receive and begin processing a purchase request for goods (ACQ.020.010 Procurement Request (PR) Processing)

b. Request funds availability check (ACQ.020.010 Procurement Request (PR) Processing)

• Requirements/specifications for the goods

• Submitted purchase request • Request for funds availability

check

2 Receive and process request for status of funds availability (FFM.010.020 Fund Allocation and Control)

• Request for funds availability check

• Funds availability response

3 Approve purchase request (ACQ.020.010 Procurement Request (PR) Processing)

• Funds availability response • Submitted purchase request

• Approved purchase request

4 Receive approved purchase request and commit funds (FFM.030.020 Obligation Management)

• Approved purchase request • Appropriate commitment entry created with reference to source information

5 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

50 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

3.1 Procurement Within a Single Fiscal Year Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

6 a. Develop request for quote (RFQ) (ACQ.020.080 Solicitation Documentation Development)

b. Send RFQ to vendors on the approved acquisition schedule (ACQ.020.100 Solicitation Issuance)

c. Receive vendors’ responses to RFQ and evaluate responses (ACQ.030.010 Proposal Evaluation)

d. Select a vendor (ACQ.030.060 Award Decision)

e. Develop purchase order for that vendor (ACQ.030.070 Contract Award Issuance)

f. Request funds availability check (ACQ.030.070 Contract Award Issuance)

• Approved purchase request • Approved acquisition schedule • Vendor responses to RFQ

• RFQ • Selected vendor • Purchase order information • Request for funds availability

check

7 Receive and process funds availability check (FFM.010.020 Fund Allocation and Control)

• Request for funds availability check

• Funds availability response

8 Approve and issue purchase order (ACQ.030.070 Contract Award Issuance)

• Purchase order information • Funds availability response

• Approved purchase order

51 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

3.1 Procurement Within a Single Fiscal Year Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

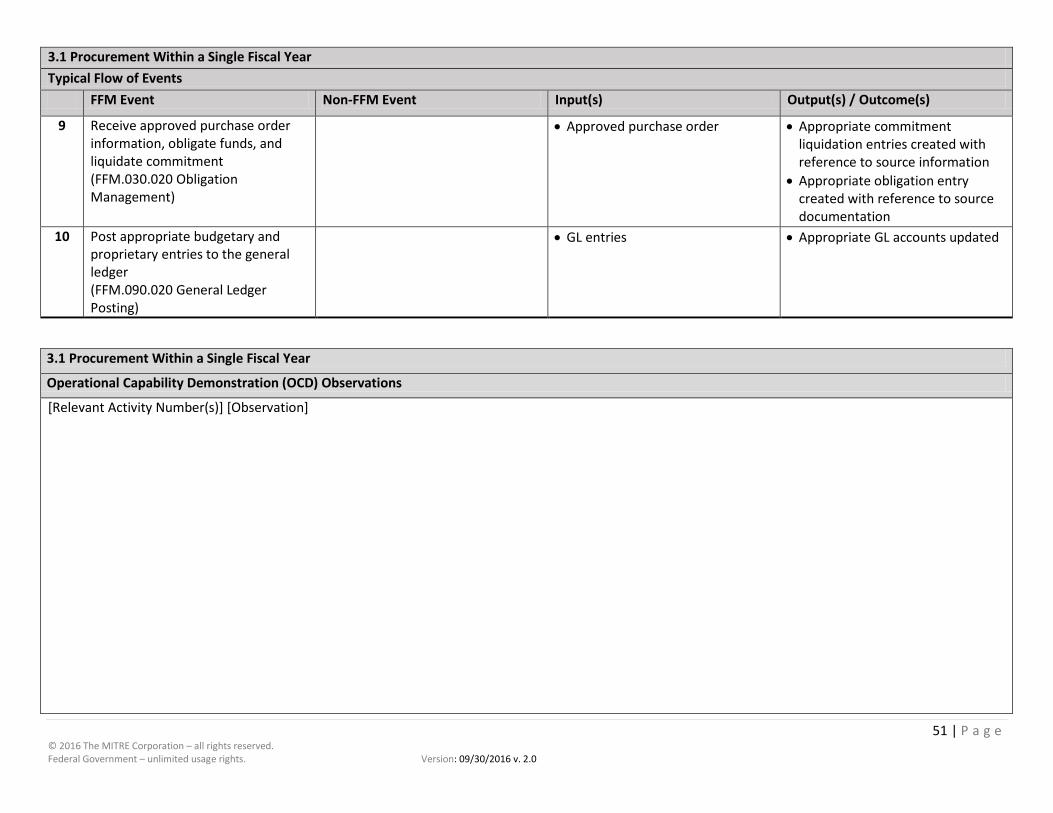

9 Receive approved purchase order information, obligate funds, and liquidate commitment (FFM.030.020 Obligation Management)

• Approved purchase order • Appropriate commitment liquidation entries created with reference to source information

• Appropriate obligation entry created with reference to source documentation

10 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

3.1 Procurement Within a Single Fiscal Year

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

52 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

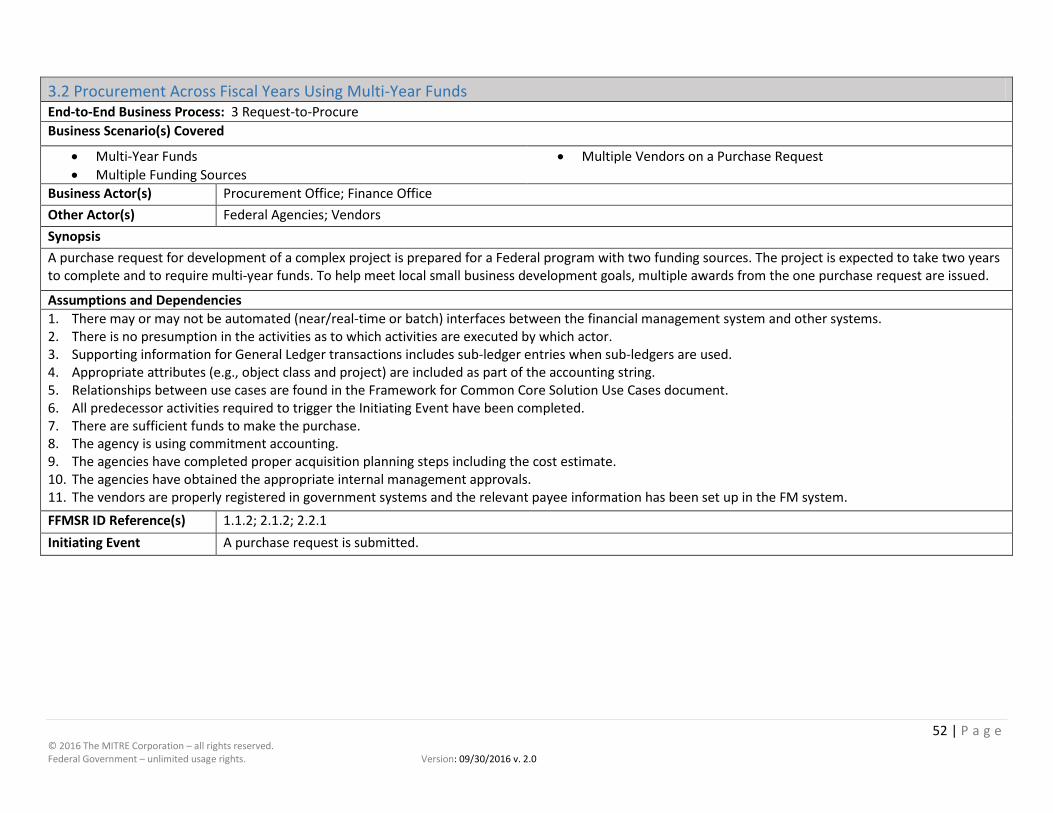

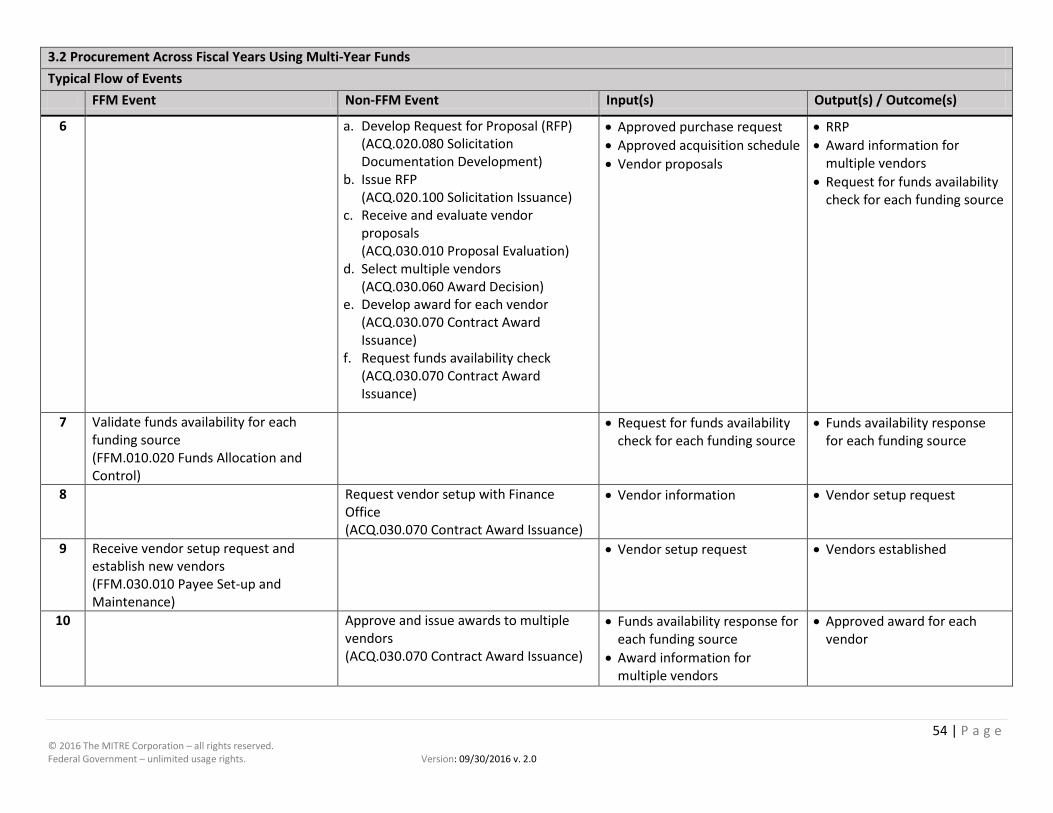

3.2 Procurement Across Fiscal Years Using Multi-Year Funds End-to-End Business Process: 3 Request-to-Procure Business Scenario(s) Covered

• Multi-Year Funds • Multiple Funding Sources

• Multiple Vendors on a Purchase Request

Business Actor(s) Procurement Office; Finance Office Other Actor(s) Federal Agencies; Vendors Synopsis A purchase request for development of a complex project is prepared for a Federal program with two funding sources. The project is expected to take two years to complete and to require multi-year funds. To help meet local small business development goals, multiple awards from the one purchase request are issued.

Assumptions and Dependencies 1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. There are sufficient funds to make the purchase. 8. The agency is using commitment accounting. 9. The agencies have completed proper acquisition planning steps including the cost estimate. 10. The agencies have obtained the appropriate internal management approvals. 11. The vendors are properly registered in government systems and the relevant payee information has been set up in the FM system. FFMSR ID Reference(s) 1.1.2; 2.1.2; 2.2.1 Initiating Event A purchase request is submitted.

53 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

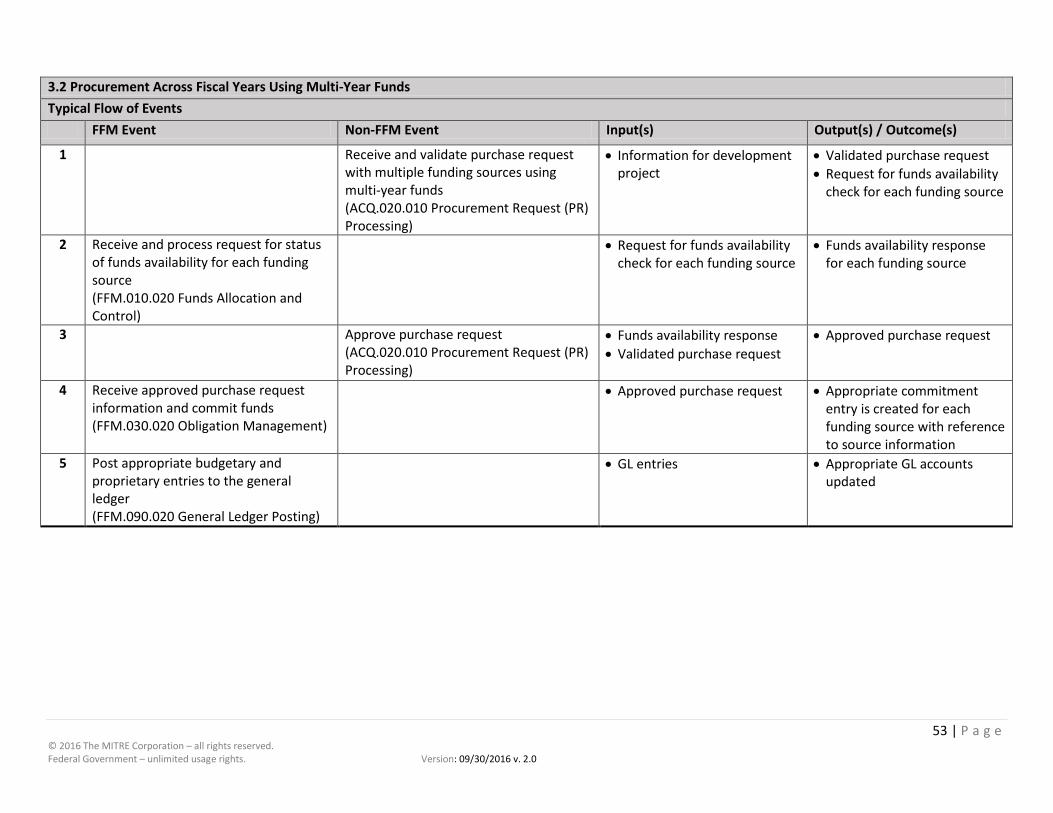

3.2 Procurement Across Fiscal Years Using Multi-Year Funds Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 Receive and validate purchase request with multiple funding sources using multi-year funds (ACQ.020.010 Procurement Request (PR) Processing)

• Information for development project

• Validated purchase request • Request for funds availability

check for each funding source

2 Receive and process request for status of funds availability for each funding source (FFM.010.020 Funds Allocation and Control)

• Request for funds availability check for each funding source

• Funds availability response for each funding source

3 Approve purchase request (ACQ.020.010 Procurement Request (PR) Processing)

• Funds availability response • Validated purchase request

• Approved purchase request

4 Receive approved purchase request information and commit funds (FFM.030.020 Obligation Management)

• Approved purchase request • Appropriate commitment entry is created for each funding source with reference to source information

5 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

54 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

3.2 Procurement Across Fiscal Years Using Multi-Year Funds Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

6 a. Develop Request for Proposal (RFP) (ACQ.020.080 Solicitation Documentation Development)

b. Issue RFP (ACQ.020.100 Solicitation Issuance)

c. Receive and evaluate vendor proposals (ACQ.030.010 Proposal Evaluation)

d. Select multiple vendors (ACQ.030.060 Award Decision)

e. Develop award for each vendor (ACQ.030.070 Contract Award Issuance)

f. Request funds availability check (ACQ.030.070 Contract Award Issuance)

• Approved purchase request • Approved acquisition schedule • Vendor proposals

• RRP • Award information for

multiple vendors • Request for funds availability

check for each funding source

7 Validate funds availability for each funding source (FFM.010.020 Funds Allocation and Control)

• Request for funds availability check for each funding source

• Funds availability response for each funding source

8 Request vendor setup with Finance Office (ACQ.030.070 Contract Award Issuance)

• Vendor information • Vendor setup request

9 Receive vendor setup request and establish new vendors (FFM.030.010 Payee Set-up and Maintenance)

• Vendor setup request • Vendors established

10 Approve and issue awards to multiple vendors (ACQ.030.070 Contract Award Issuance)

• Funds availability response for each funding source

• Award information for multiple vendors

• Approved award for each vendor

55 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

3.2 Procurement Across Fiscal Years Using Multi-Year Funds Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

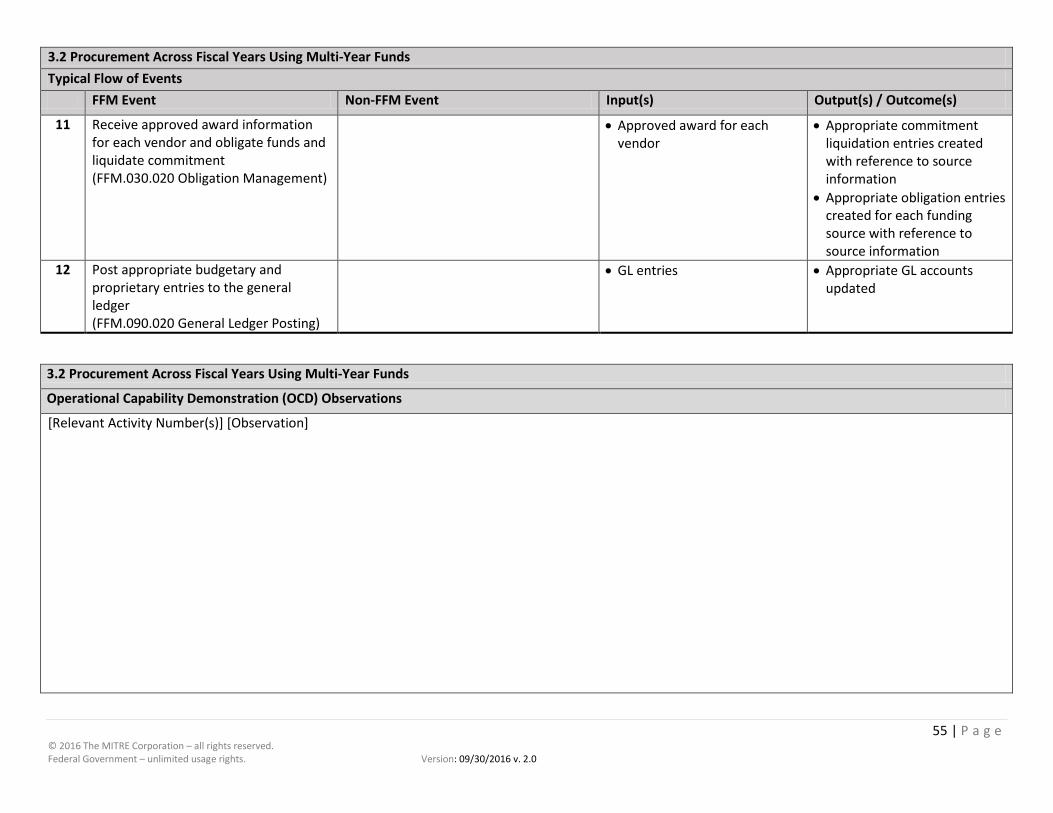

11 Receive approved award information for each vendor and obligate funds and liquidate commitment (FFM.030.020 Obligation Management)

• Approved award for each vendor

• Appropriate commitment liquidation entries created with reference to source information

• Appropriate obligation entries created for each funding source with reference to source information

12 Post appropriate budgetary and proprietary entries to the general ledger (FFM.090.020 General Ledger Posting)

• GL entries • Appropriate GL accounts updated

3.2 Procurement Across Fiscal Years Using Multi-Year Funds

Operational Capability Demonstration (OCD) Observations

[Relevant Activity Number(s)] [Observation]

56 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

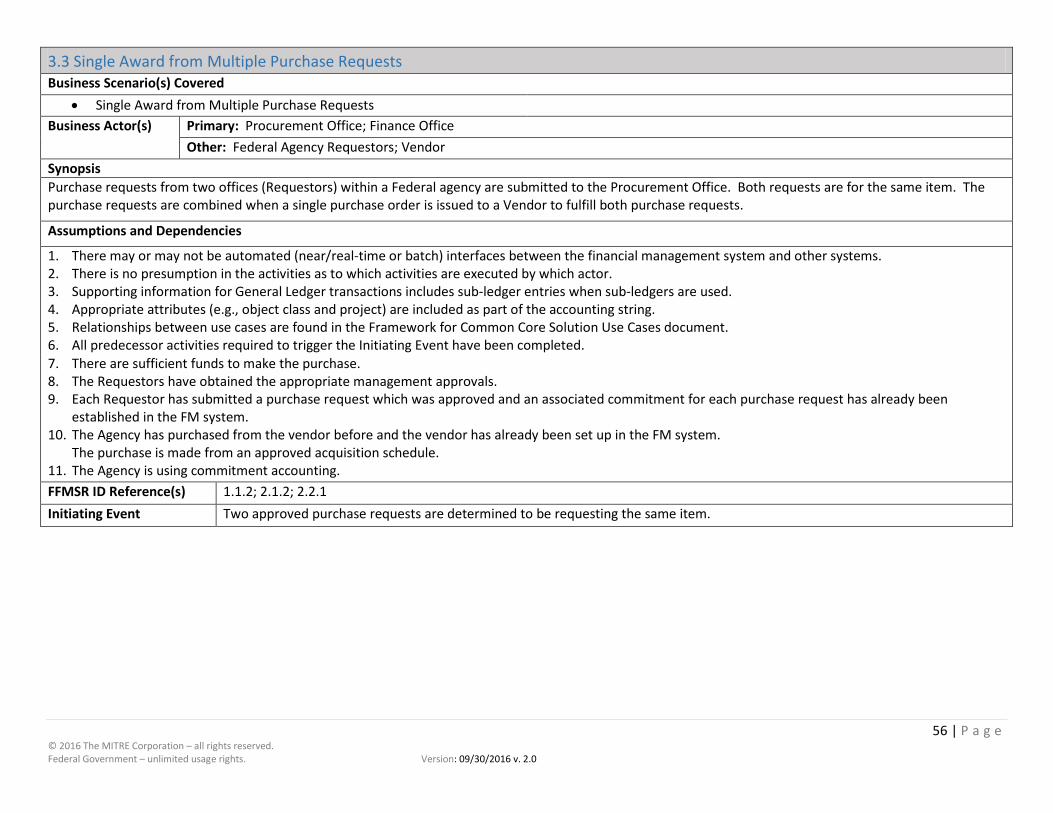

3.3 Single Award from Multiple Purchase Requests Business Scenario(s) Covered

• Single Award from Multiple Purchase Requests Business Actor(s) Primary: Procurement Office; Finance Office

Other: Federal Agency Requestors; Vendor Synopsis Purchase requests from two offices (Requestors) within a Federal agency are submitted to the Procurement Office. Both requests are for the same item. The purchase requests are combined when a single purchase order is issued to a Vendor to fulfill both purchase requests.

Assumptions and Dependencies

1. There may or may not be automated (near/real-time or batch) interfaces between the financial management system and other systems. 2. There is no presumption in the activities as to which activities are executed by which actor. 3. Supporting information for General Ledger transactions includes sub-ledger entries when sub-ledgers are used. 4. Appropriate attributes (e.g., object class and project) are included as part of the accounting string. 5. Relationships between use cases are found in the Framework for Common Core Solution Use Cases document. 6. All predecessor activities required to trigger the Initiating Event have been completed. 7. There are sufficient funds to make the purchase. 8. The Requestors have obtained the appropriate management approvals. 9. Each Requestor has submitted a purchase request which was approved and an associated commitment for each purchase request has already been

established in the FM system. 10. The Agency has purchased from the vendor before and the vendor has already been set up in the FM system.

The purchase is made from an approved acquisition schedule. 11. The Agency is using commitment accounting. FFMSR ID Reference(s) 1.1.2; 2.1.2; 2.2.1 Initiating Event Two approved purchase requests are determined to be requesting the same item.

57 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

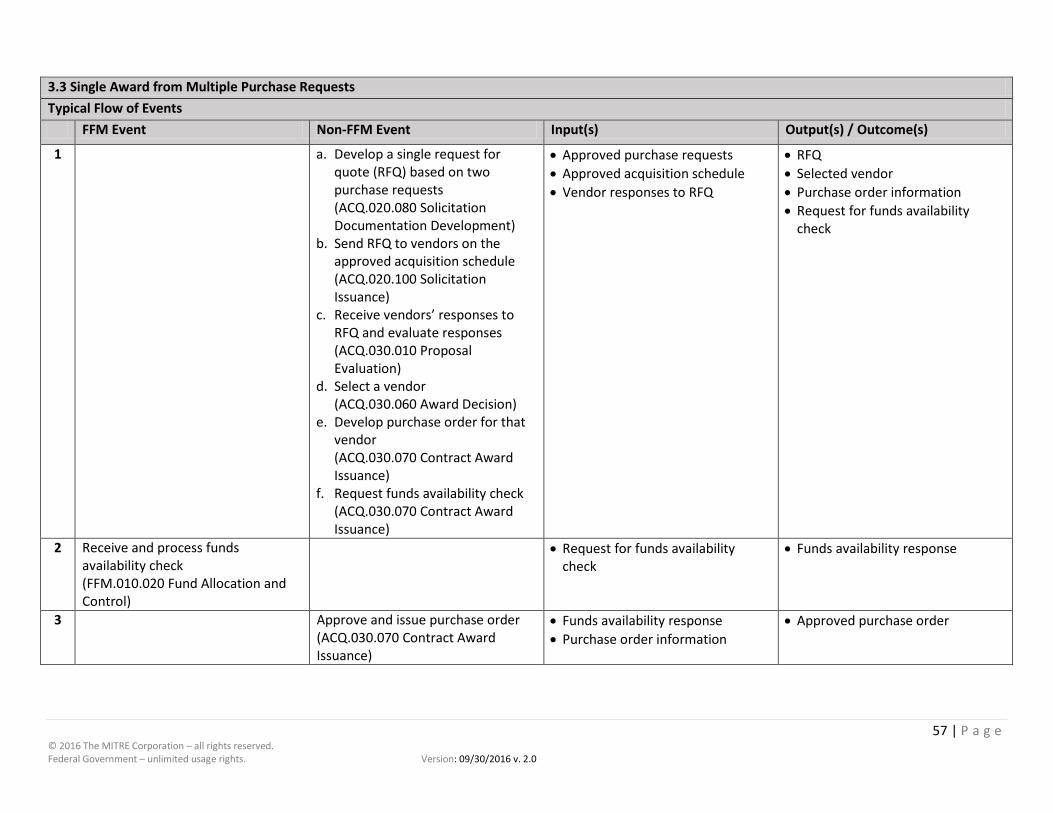

3.3 Single Award from Multiple Purchase Requests Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

1 a. Develop a single request for quote (RFQ) based on two purchase requests (ACQ.020.080 Solicitation Documentation Development)

b. Send RFQ to vendors on the approved acquisition schedule (ACQ.020.100 Solicitation Issuance)

c. Receive vendors’ responses to RFQ and evaluate responses (ACQ.030.010 Proposal Evaluation)

d. Select a vendor (ACQ.030.060 Award Decision)

e. Develop purchase order for that vendor (ACQ.030.070 Contract Award Issuance)

f. Request funds availability check (ACQ.030.070 Contract Award Issuance)

• Approved purchase requests • Approved acquisition schedule • Vendor responses to RFQ

• RFQ • Selected vendor • Purchase order information • Request for funds availability

check

2 Receive and process funds availability check (FFM.010.020 Fund Allocation and Control)

• Request for funds availability check

• Funds availability response

3 Approve and issue purchase order (ACQ.030.070 Contract Award Issuance)

• Funds availability response • Purchase order information

• Approved purchase order

58 | P a g e © 2016 The MITRE Corporation – all rights reserved. Federal Government – unlimited usage rights. Version: 09/30/2016 v. 2.0

3.3 Single Award from Multiple Purchase Requests Typical Flow of Events

FFM Event Non-FFM Event Input(s) Output(s) / Outcome(s)

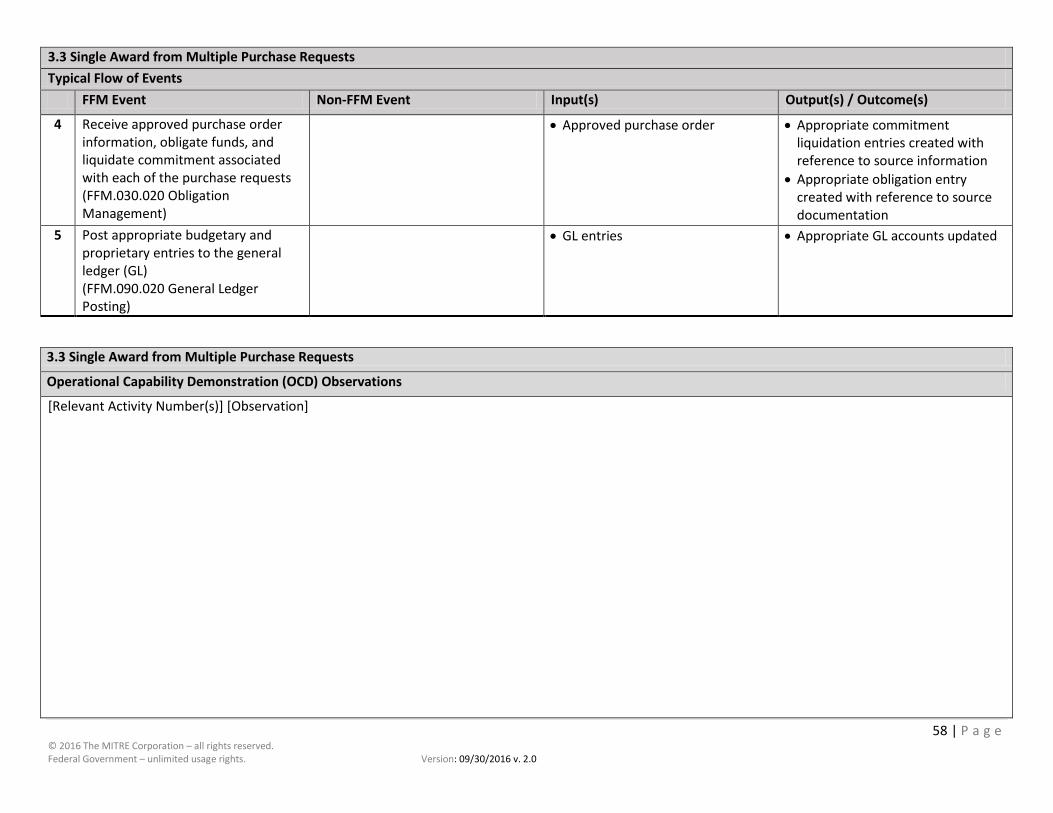

4 Receive approved purchase order information, obligate funds, and liquidate commitment associated with each of the purchase requests (FFM.030.020 Obligation Management)

• Approved purchase order • Appropriate commitment liquidation entries created with reference to source information

• Appropriate obligation entry created with reference to source documentation