Embed Size (px)

Citation preview

A&A Update

Bill Miller, KPMG

Justin Jackson, Ohio National Financial Services

November 10, 2017

2© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

• ASU 2016-01, Recognition and measurement of financial assets and liabilities

• ASU 2016-13, Financial Instruments – Credit Losses

• Targeted Improvements to the Accounting for Long-Duration Contracts

• NAIC Insurance Data Security Model Law

• Statutory Accounting Update

ASU 2016-01, Recognition and measurement of financial assets and financial liabilities

4© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Main Changes

Available for Sale - equity investments

Cost method vs measurement alternative

Financial liabilities (fair value option)

Deferred taxes, presentation and other disclosures

5© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

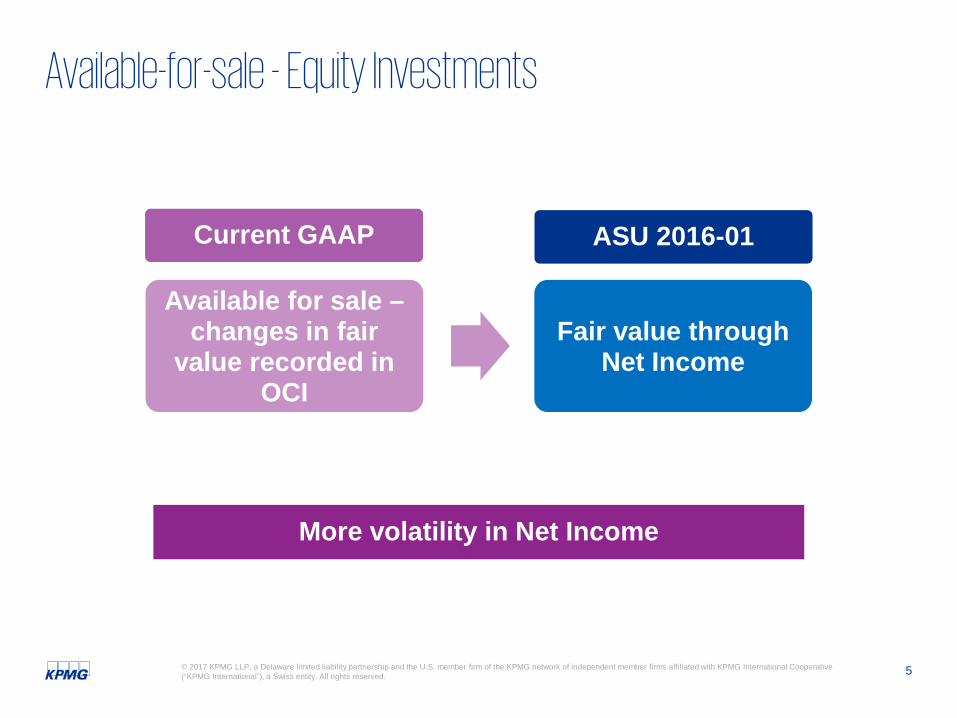

Available-for-sale - Equity Investments

Available for sale –changes in fair

value recorded in OCI

Fair value throughNet Income

Current GAAP ASU 2016-01

More volatility in Net Income

6© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Cost method vs measurement alternative

Cost methodMeasurement

alternative may be elected

Cost minus impairment

Cost minus impairment +/- changes in

observable prices

Current GAAP ASU 2016-01

Eliminates cost method, but an exception to full FV available

7© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Measurement alternative - +/- Changes in observable prices

Changes in observable prices must be

From “orderly transactions”

In the same or “similar” investment of

the same issuer

Potential challenges• Is the transaction orderly? • What to do if transaction is not orderly?• Identifying observable prices• Determining if an investment is similar

8© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Effective date

• Public Business Entities: Fiscal years beginning after December 15, 2017 (including interim periods within those fiscal years)

• For All Other Entities: Fiscal years beginning after December 15, 2018 and interim periods in fiscal years beginning after December 15, 2019

Effective Date

• Entities that are not public business entities:may adopt for fiscal years beginning after December 15, 2017 (including interim periods within those fiscal years)

• All entities: may early adopt the provisions related to the recognition of changes in fair value of financial liabilities

Early Adoption

ASU 2016-13, Financial Instruments – Credit Losses

10© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

ASU 2016-13, Financial Instruments – Credit Losses

■ Effective date■ Scope ■ Current Expected Credit Losses (CECL) Model

– Main areas of change– Measurement and methodologies

■ Available-for-sale credit loss model■ Transition■ Transition Resource Group

11© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Effective Date

— Fiscal years beginning after December 15, 2019 and interim periods within those years

SEC filers that are Public Business Entities

— Fiscal years beginning after December 15, 2018

Early adoption

— Fiscal years beginning after December 15, 2020 and interim periods within those years

Non-SEC filers that are Public Business Entities

— Fiscal years beginning after December 15, 2020 and interim periods thereafter

All of entities

12© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Scope

■ Loans■ Loan commitments■ Financial guarantees (not insurance contracts)■ Trade receivables■ Reinsurance receivables■ Lease receivables recognized by a lessor■ Receivables that result from revenue transactions■ Loans made by a NFP entity to meet its mission (programmatic loans)■ Debt securities classified as held-to-maturity■ Debt securities classified as available-for-sale

■ Equity instruments■ Financial instruments measured at FV through NI■ Loans and receivables between entities under common control ■ Policy loan receivables of an insurance entity■ Loans made to participants by defined contribution employee benefit plans■ Pledge receivables of a not-for-profit entity

In scope

CECL

Out of scope

13© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Main areas of change - CECL

No probability threshold

Expected lifetime loss estimate

Estimate future economic conditions

Applies to HTM securities

14© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CECL – Measurement overview

Historical loss

experience adj. for asset

specific attributes

Reasonable and

supportable forecasts

Adjustments for current economic conditions

Estimate of current

expected credit losses

??

15© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

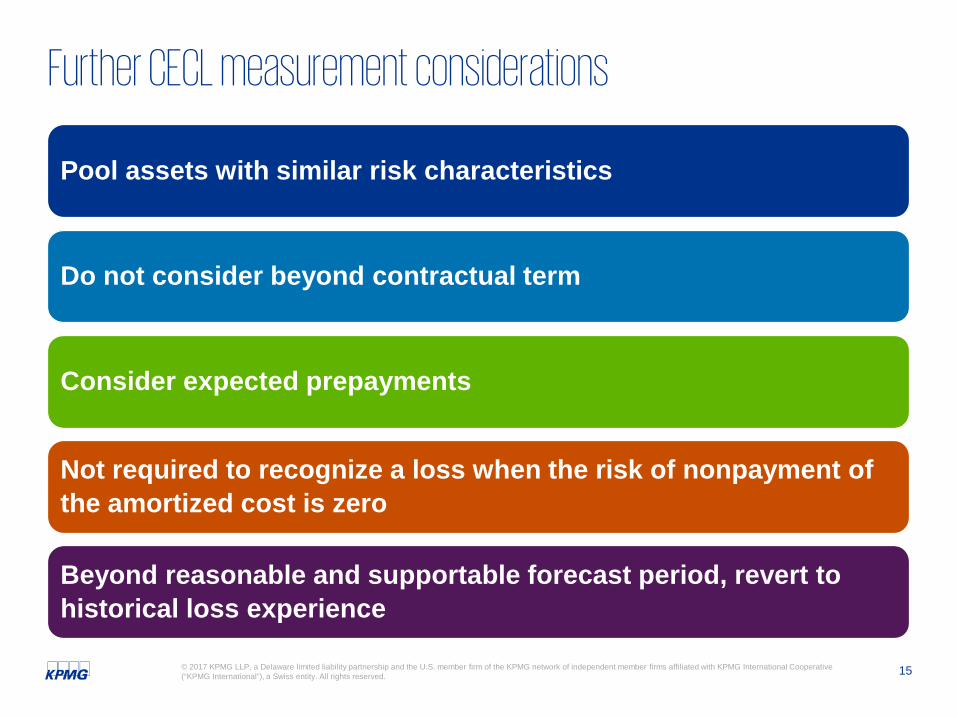

Further CECL measurement considerations

Pool assets with similar risk characteristics

Do not consider beyond contractual term

Consider expected prepayments

Not required to recognize a loss when the risk of nonpayment of the amortized cost is zero

Beyond reasonable and supportable forecast period, revert to historical loss experience

16© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

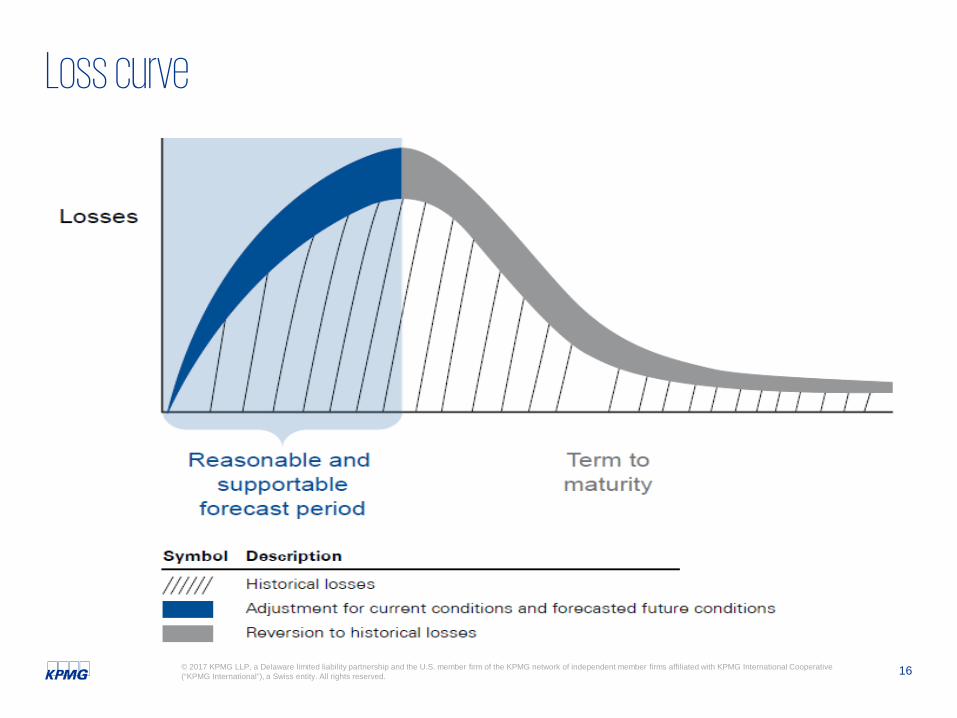

Loss curve

17© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Potential for diversity

Judgment would be needed

• DCFA• Loan loss• Vintage• Other

If other, which one?

Immediate or straight line?

What is reasonable & supportable?

How long?

Methodology

Reasonable and supportable forecasts

Revert back to historical losses (adjusted for asset attributes but

not economic conditions)

18© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

AFS credit loss model - Main areas of change

Allowance

Reversals

Floor

Cannot consider length of time fair value is below amortized cost

19© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Qualitative disclosures about how an entity

estimates expected losses, including changes in credit

loss expectations

Rollforward of the allowance for expected credit losses

for financial assets measured at amortized cost

and FV-OCI

Current credit quality indicators that are disclosed under current GAAP would be disaggregated by year of

origination (vintage disclosures)

A discussion of the type of collateral and extent to

which collateral secures an entity’s financial assets

Reconciliation between the purchase price and the par

value of PCD financial assets at the time of

purchase

Disclosures

AFS debt securities

■ Retain current disclosure requirements, updated for the general principles regarding disclosing credit risk

20© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transition

Previously impaired debt securities• Prospective• Certain amounts in AOCI will continue to be accreted in

interest income

PCD financial assets• Assets to which Subtopic 310-30 (including by

analogy) was applied – reclass as PCD at adoption• Gross up the allowance at adoption date• Prospective interest income will be recognized based

on EIR determined after the adjustment for credit losses made on the adoption date

Cumulative effect adjustment to the statement of financial position as of the beginning of the first reporting period

Insurance: Targeted Improvements to the Accounting for Long-Duration Contracts

22© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Insurance Contracts – FASB Initiatives

Short-Duration Contracts (Final

Standard ASU 2015-09 Issued May 2015)

Focused efforts on targeted improvements

to disclosures

No change to current U.S. GAAP model for

recognition and measurement

Long-Duration Contracts (Exposure

Draft Issued September 2016)

Focused efforts on targeted improvements to both accounting and

disclosures

Change to current U.S. GAAP model for

recognition, measurement,

presentation and disclosure

23© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Feedback from comment letters discussed in February 2017

Proposed ASU issued in September 2016

Long-duration Insurance Contracts – Timeline

Redeliberations begin in August 2017

Public roundtable meeting held in April 2017

Legend to matters that have been redeliberated:

FASB affirmed previous decisions

FASB revised previous decisions as highlighted

Unmarked items have not yet been redeliberated or affirmed. Marked affirmed or revised decisions apply only to nonparticipating traditional and limited payment contracts; participating contracts and market-risk benefits have not yet been redeliberated.

24© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

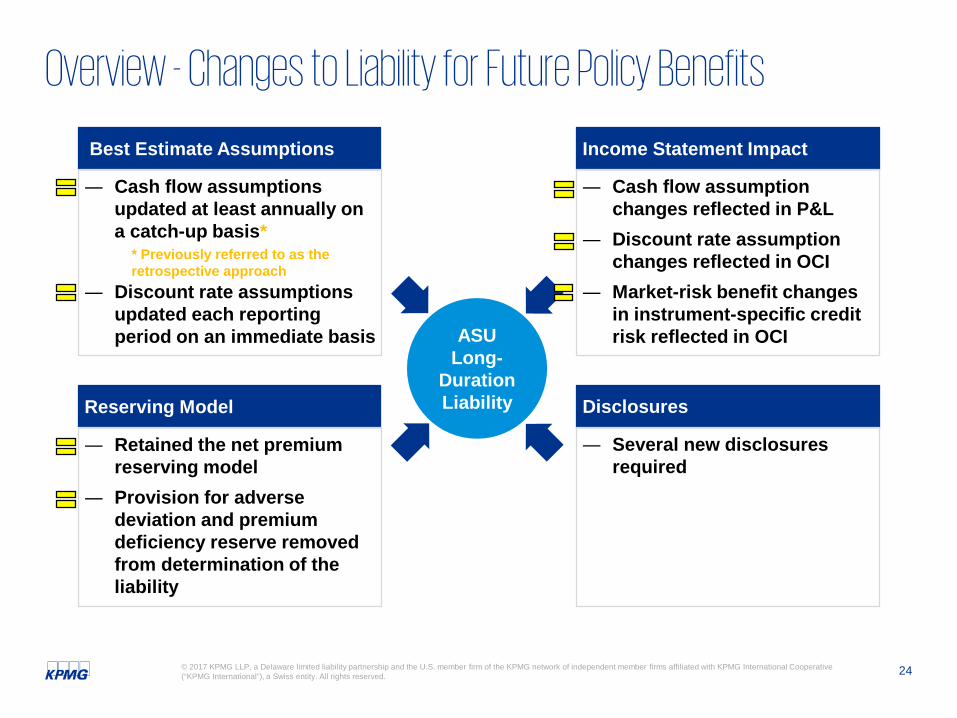

ASU Long-

Duration Liability

Best Estimate Assumptions

Reserving Model

Income Statement Impact

Disclosures

― Cash flow assumptions updated at least annually on a catch-up basis*

― Discount rate assumptions updated each reporting period on an immediate basis

― Retained the net premium reserving model

― Provision for adverse deviation and premium deficiency reserve removed from determination of the liability

― Cash flow assumption changes reflected in P&L

― Discount rate assumption changes reflected in OCI

― Market-risk benefit changes in instrument-specific credit risk reflected in OCI

― Several new disclosures required

Overview - Changes to Liability for Future Policy Benefits

* Previously referred to as the retrospective approach

25© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Unlocking of assumptions is meant to provide more relevant estimates of future policy benefit reservesKey Changes:—Updated at least annually in the same

quarter every year, but more frequently if experience warrants

—Unlocked and updated on a catch-up basis (previously the retrospective approach) through net income

Cash Flow Assumptions

Unlocking of the discount rate better reflects the market environment of the liabilitiesKey Changes:—Updated at each reporting date—Unlocked and updated on an immediate

basis in other comprehensive income

Discount Rate

Reflected in the Net Premium % Not Reflected in the Net Premium %

Assumption Changes

26© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

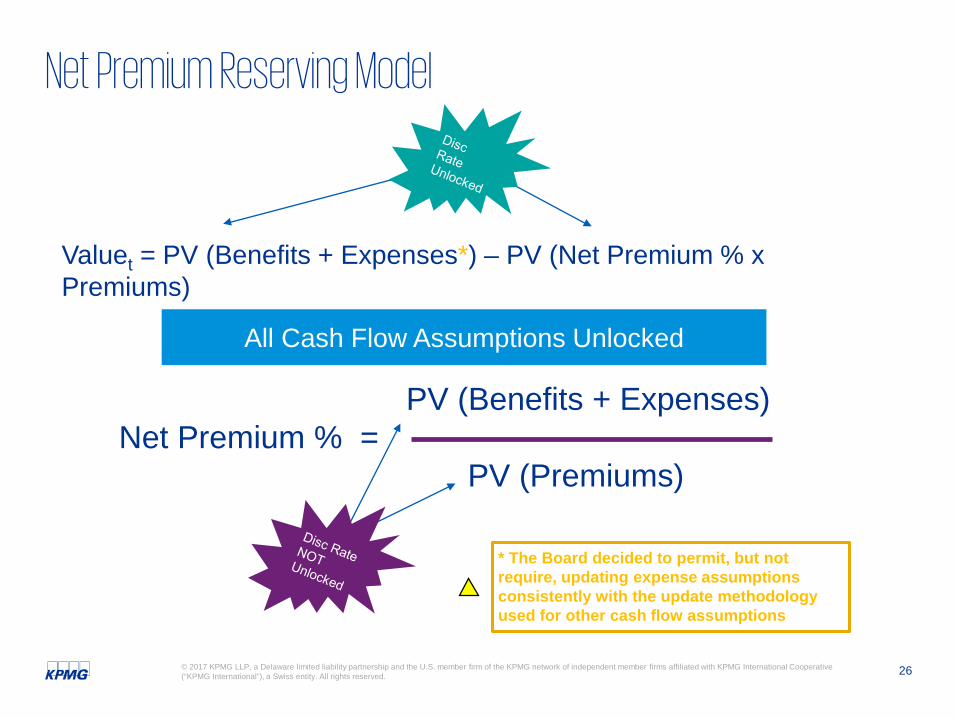

Net Premium Reserving Model

Valuet = PV (Benefits + Expenses*) – PV (Net Premium % x Premiums)

PV (Benefits + Expenses)Net Premium % =

PV (Premiums)

All Cash Flow Assumptions Unlocked

* The Board decided to permit, but not require, updating expense assumptions consistently with the update methodology used for other cash flow assumptions

27© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

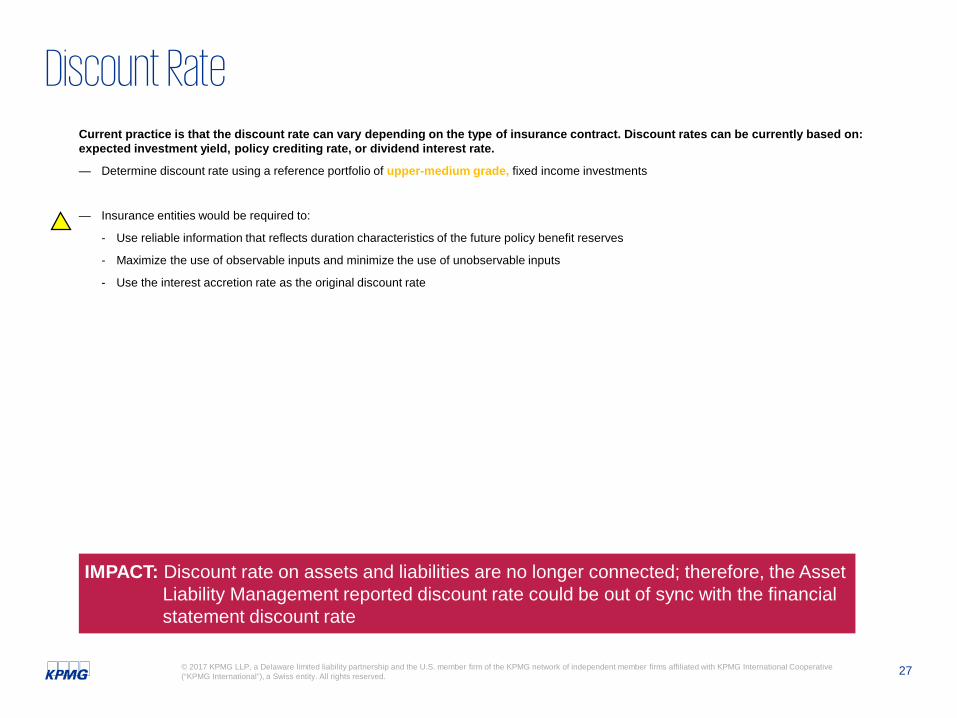

Discount RateCurrent practice is that the discount rate can vary depending on the type of insurance contract. Discount rates can be currently based on: expected investment yield, policy crediting rate, or dividend interest rate.

— Determine discount rate using a reference portfolio of upper-medium grade, fixed income investments

— Insurance entities would be required to:

- Use reliable information that reflects duration characteristics of the future policy benefit reserves

- Maximize the use of observable inputs and minimize the use of unobservable inputs

- Use the interest accretion rate as the original discount rate

IMPACT: Discount rate on assets and liabilities are no longer connected; therefore, the Asset Liability Management reported discount rate could be out of sync with the financial statement discount rate

28© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

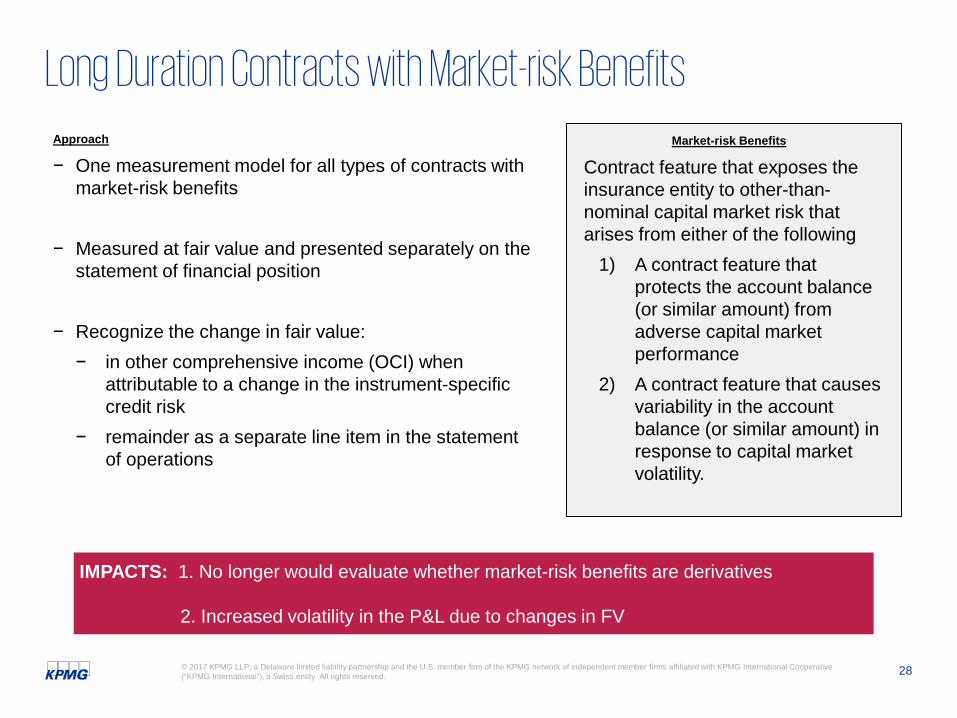

Long Duration Contracts with Market-risk BenefitsApproach

− One measurement model for all types of contracts with market-risk benefits

− Measured at fair value and presented separately on the statement of financial position

− Recognize the change in fair value: − in other comprehensive income (OCI) when

attributable to a change in the instrument-specific credit risk

− remainder as a separate line item in the statement of operations

Market-risk Benefits

Contract feature that exposes the insurance entity to other-than-nominal capital market risk that arises from either of the following

1) A contract feature that protects the account balance (or similar amount) from adverse capital market performance

2) A contract feature that causes variability in the account balance (or similar amount) in response to capital market volatility.

IMPACTS: 1. No longer would evaluate whether market-risk benefits are derivatives

2. Increased volatility in the P&L due to changes in FV

29© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

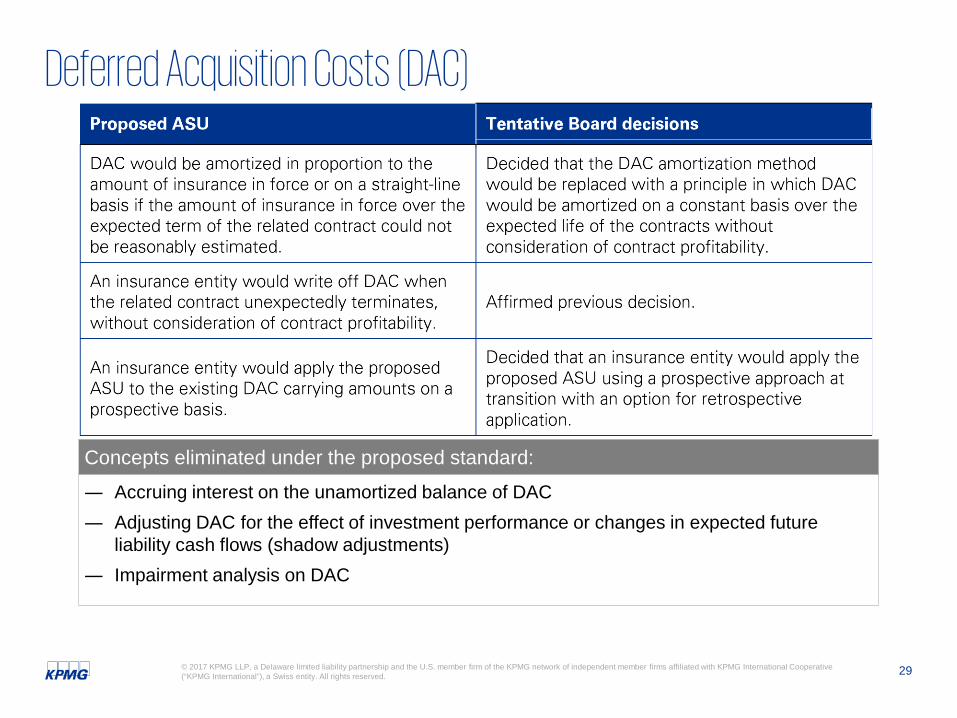

Deferred Acquisition Costs (DAC)

― Accruing interest on the unamortized balance of DAC― Adjusting DAC for the effect of investment performance or changes in expected future

liability cash flows (shadow adjustments) ― Impairment analysis on DAC

Concepts eliminated under the proposed standard:

30© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

DisclosuresAdditional disaggregated disclosures for the future policy benefit reserves and DAC would include rollforwards of opening and closing balances and quantitative and qualitative information about significant inputs, judgments and assumptions used in the measurement of the liabilities for future policy benefits and DAC.

— Provides a principle for determining how to disaggregate the new disclosures to provide meaningful information without requiring a large amount of insignificant detail or aggregation of items with significantly different characteristics.

— Provides examples of disaggregation characteristics (e.g., type of coverage, etc.).

— Consider how information about future policy benefit reserves or DAC has been disaggregated for other purposes when determining which categories would be the most relevant and useful.

— Clarifies that the aggregation of the disclosures would at a minimum be consistent with segment-related disclosures.

IMPACT: The proposed ASU would significantly expand the disclosure requirements for long-duration contracts in the annual and interim financial statements.

31© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transition Requirements

The FASB has not discussed an effective date

Effective Date

− Difference between fair value and carrying value at the transition date, excluding changes in instrument-specific credit risk, recognized in opening retained earnings

− Cumulative effect of changes in instrument-specific credit risk recognized in accumulated OCI

Market-Risk Benefits

− Apply to existing carrying amounts at the transition date, adjusted to remove amounts in OCI (shadow DAC)

− Apply to other balances amortized consistently with deferred acquisition costs (e.g., sales inducements)

Deferred Acquisition Costs

− Information required for a change in accounting principle, but on a disaggregated basis consistent with recurring disclosure disaggregation

− Qualitative and quantitative information about transition adjustments when net premiums exceed gross premiums and additional liability for a universal life-type or investment contract is recorded

Disclosures During the Year of Adoption

− Apply to existing carrying amounts at the transition date, adjusted to remove related amounts in accumulated OCI (prospective basis)

− Option to apply the guidance retrospectively, with a cumulative adjustment to opening retained earnings

Future Policy Benefit Reserves

NAIC Insurance Data Security Model Law

33© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

NAIC Passes Insurance Data Security Model LawOn October 24, 2017, the NAIC adopted the Insurance Data Security Model Law, which creates rules for insurers, agents and other licensed entities covering data security, investigation and notification of breach.

— Purpose is to establish standards for data security and standards for the investigation of and notification to the Commissioner of a Cybersecurity Event applicable to Licensees.

— “Cybersecurity Event” means an event resulting in unauthorized access to, disruption or misuse of, an Information System or information stored on such Information System.

— Effective date will vary based on when individual states adopt, but upon that date, Licensees will have one year from the effective date to implement Section 4 (Information Security Program) and two years from the effective date to implement Section 4F (Oversight of Third-Party Service Provider Arrangements)

If a Licensee is in compliance with N.Y. Comp. Codes R. & Regs. tit.23, 500, Cybersecurity Requirements for Financial Services Companies, effective March 1, 2017, such Licensee is also in compliance with this Act.

34© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

NAIC Passes Insurance Data Security Model Law (cont.)Section 4: Information Security Program

A. Implementation of an Information Security Program

B. Objectives of Information Security Program

C. Risk Assessment

D. Risk Management

E. Oversight by Board of Directors

F. Oversight of Third-Party Service Provider Arrangements

G. Program Adjustments

H. Incident Response Plan

I. Annual Certification to Commissioner of Domiciliary State

Section 5: Investigation of a Cybersecurity Event

Section 6: Notification of a Cybersecurity Event

Section 7: Power of Commissioner

Section 8: Confidentiality

Section 9: Exceptions

Statutory Accounting Update

36© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

InvestmentsMoney Market Mutual Funds (SSAP No. 2) – Adopted— Reclassified to cash equivalents— Measured at fair value— Effective December 31, 2017Accounting for ETFs (SSAP No. 26) – Adopted— Removed from the definition of a bond— Measured at fair value — May elect to use the systematic value approach, if certain conditions are metAVR and IMR (SSAP No. 26) – Adopted— Clarify OTTI to be recorded either entirely in AVR or IMR— Effective upon adoption (August 6, 2017)Bank Loans (SSAP No. 26) – Exposed— Revised definition to include bank loans issued directly by insurer— Potential separate reporting on schedule DMortgage Loans (SSAP No. 37) – Adopted— Mortgage acquired through assignment, syndication or participation – In scope— Real estate funds or securitization of assets – Out of scope— Effective upon adoption (June 8, 2017)

37© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Investments (continued)Derivatives (SSAP No. 86)— Impact of future settlement premiums on option value – Exposed

- Treatment of initial cost to acquire derivative contracts— Derivative contracts related to variable annuity products – Ongoing discussions

- Issue Paper proposes hedge accounting treatment for certain limited derivative contracts

- Discussions focused on:— Dynamic hedging strategies— Amortization or accretion period for unrecognized gains or losses — Recognition of unrealized gains and losses— Ability to apply current accounting, in certain situations

Derivatives (SSAP No. 86)— Variation margin – Exposed

- Recognize as unrealized gains or losses until maturity, termination or expiration- Report collateral separately on the balance sheet

38© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Investments (continued)Repurchase and reverse repurchase agreements (SSAP No. 103R) – Adopted— New disclosures

- General information- Detailed information for agreements accounted for as secured borrowing and

sales transitions— Effective December 31, 2017NAV as a practical expedient to fair value (Exposed)— Allow the use of NAV when:

- Specifically permitted by an SSAP- No readily determinable fair value FV and an investment company or real estate fund that

measures FV using NAV and issues financial statements following measurement principles of an investment company

Mid-Year reporting of investment schedules — Adopted by SAPWG and AP&P— Discussions are on-going at the E Committee

39© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Other Accounting TopicsGuaranty Fund Credits (SSAP No. 35) – Adopted— Allowed discounting of guaranty fund assessments resulting from insurers that wrote long-term care

contracts— Allows expected renewals of short-term contracts for long term care assessments when determining:

- Premium tax credit- Policy surcharge assets

— Effective January 1, 2017Risk Transfer (SSAP No. 61R and 62R) – Exposed— SSAP No. 61R

- Additional guidance to determine if a contract is proportional or non-proportional and if significant loss is transferred for non-proportional reinsurance contracts

- Clarified that provisions that limit reinsurer’s losses should be reflected as a reduction in claims and losses ceded

- Additional disclosures— SSAP No. 62R

- Clarified that provisions that limit reinsurer’s losses should be reflected as a reduction in claims and losses ceded

- Prohibition of reserve credit for non-proportional reinsurance unless the aggregate attachment point has been penetrated

40© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Other Accounting Topics (continued)U.S. GAAP disclosures for short-duration contracts (SSAP No. 55 and 65) – Adopted— SSAP No. 55 – disclose significant changes in methodologies and assumptions— SSAP No. 65 – disclose amount of interest accretion recognized in statement

of income— Effective upon adoption (April 8, 2017)Goodwill limitations (SSAP No. 68) – Exposed— Proposed 5 options for admissibility of goodwill

- Decrease admissibility limit from 10% to 5%- Limit admissibility based on percentage of the dollar amount of goodwill remaining after the initial

10% limitation based on amount of capital held by the parent- Limit to the asset or net asset value of the SCA- Eliminate admissibility- No change to current admissibility

High Deductible Disclosures (SSAP No. 65) – Adopted— Gross amount of loss reserves— Amounts that have been billed and are recoverable on paid claims— Collateral pledged related to deductible and paid recoverables— Unsecured high deductible (amount and percentages)— Highest 10 unsecured high deductible amounts by counterparty — Effective upon adoption (June 8, 2017)

41© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Projects to WatchLeases – Exposed— Revisions consider new U.S. GAAP guidance for leases

- Retain concept of operating leases - Revisions are significant but are not intended to result in significant changes to current statutory

accounting Credit Losses (CECL)— Considering adoption of new U.S. GAAP accounting— Expect to have discussion later this year

42© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Principles Based Reserving (PBR)— Completed a pilot project

- Made changes to address inconsistencies within VM-20 - Made changes to VM-31 to streamline actuarial report

— Life PBR Exemption - Ordinary premium of less than $300 million (or $600 million for a group)- Total Adjusted Capital of at least 450 %- Unqualified actuarial opinion on reserves- No universal life policies issued or assumed with material secondary guarantees, after January 1,

2020— Adopted changes to Life PBR exemption to

- Exclude small companies from requirement to meet the 450 percent risk-based capital;

- Allow certain companies that fall below the 450 percent RBC requirement, to seek an exemption from their commissioner;

- Clarify that companies cannot have material Universal Life with Secondary Guarantees policies on or after January 1, 2020; and

- Exclude the following from the ordinary life premium threshold of $300 million:— premiums for preneed life contracts; and— transfers of reserves in-force as of the effective date of a reinsurance

assumed transaction.

43© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Regulatory UpdateInvestment RBC— Discussed updated bond factors for Life insurers

- Suggested starting point for P&C and Health insurers — Real Estate

- Proposal to change base factor from 15% to 10%— Federal Home Loan Banks

- Proposal to change 1.3% to zero for collateral held for FHLB advancesNAIC Group Capital Calculation – inventory method based on RBC aggregation— Existing legal entity requirements, not new standards— Treatment of different typed of entities:

- Insurers that are not subject to RBC formula, non insurance entities, entities with no capital requirements and;

- Captives that:— Exclusively self-insure— Do not assume XXX/AXXX business— Assume XXX/AXXX business

— Treatment of permitted and prescribed practices — Scalars for capital from non-U.S. jurisdictions

Thank You

© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 712774

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

![binary heap, d-ary heap, binomial heap, amortized analysis ... · Amortized Complexity [amortizovaná složitost] In an amortized analysis , the time required to perform a sequence](https://img.pdfslide.us/doc/110x75/5ed29bc1016d386359233e54/binary-heap-d-ary-heap-binomial-heap-amortized-analysis-amortized-complexity.jpg)