Embed Size (px)

Citation preview

Financial Insights: MONY’s Smart Assets Course

Buy-Sell Agreements

MONY Life Insurance Company and MONY Securities Corporation are members of The MONY Group

2

Buy-Sell Planning: SMART Business Succession/Transition Strategies Buy-Sell Planning involves an orderly business sale...

…To family, partners or co-shareholders, or outsiders …Considering the tax, financial, and emotional needs …Of the buyer …And of the seller and /or his or her family

3

Buy-Sell vs. Business SuccessionThe Difference

Succession Planning: May be accomplished by a sale, gift, or bequest at death Main Objective: To continue the business

Buy-Sell Planning: Always involves a sale of a business interest Main Objective: To convert an owner’s business interest

into cash

4

The Buy-Sell Agreement A contract between identified buyer(s) and seller(s),

obligating the buyer to buy and the seller to sell.

“Trigger events” are specified in the contract.

The contract fixes the price (by dollar amount or formula) and terms of the sale

Having a “funding plan” in place is critical!

Proper buy-sell planning helps eliminate uncertainty

for owners, buyers, and sellers!

5

Possible Triggering Events

Retirement

Disability

Death

Termination of Employment

Divorce

Bankruptcy

6

Business Survival Rates:Not Encouraging!

Only 30% of businesses survive a transition to the next generation*

Death or disability of an owner are two of the most destabilizing events to a business’s future

*Kennesaw State University Study, 1998

7

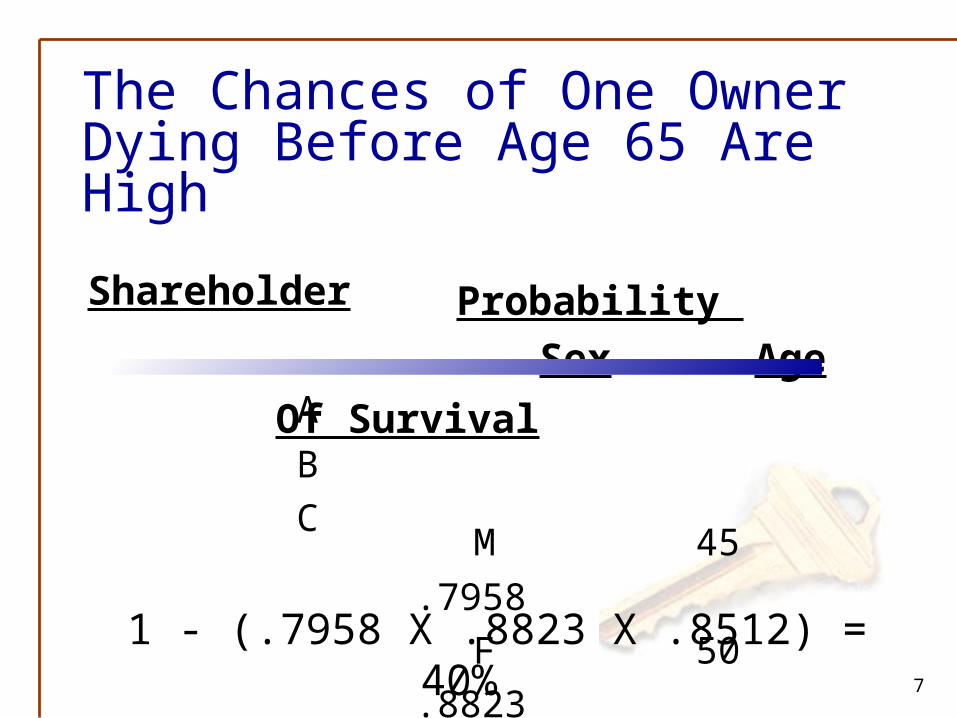

The Chances of One Owner Dying Before Age 65 Are High

Shareholder

A B C

Probability

Sex Age Of Survival

M 45 .7958 F 50 .8823

M 55 .8512

1 - (.7958 X .8823 X .8512) = 40% Source: 1985 Society of Actuaries Disability Termination Study

8

The Chances of a 90+ Day Disability are Also High

1 - (.8281 X .8189 X .8731) = 41%Source: 1985 Society of Actuaries Disability Termination Study

Shareholder

ABC

Sex

MFM

Age

455055

Probability Of No Disability

.8281

.8189

.8731

9

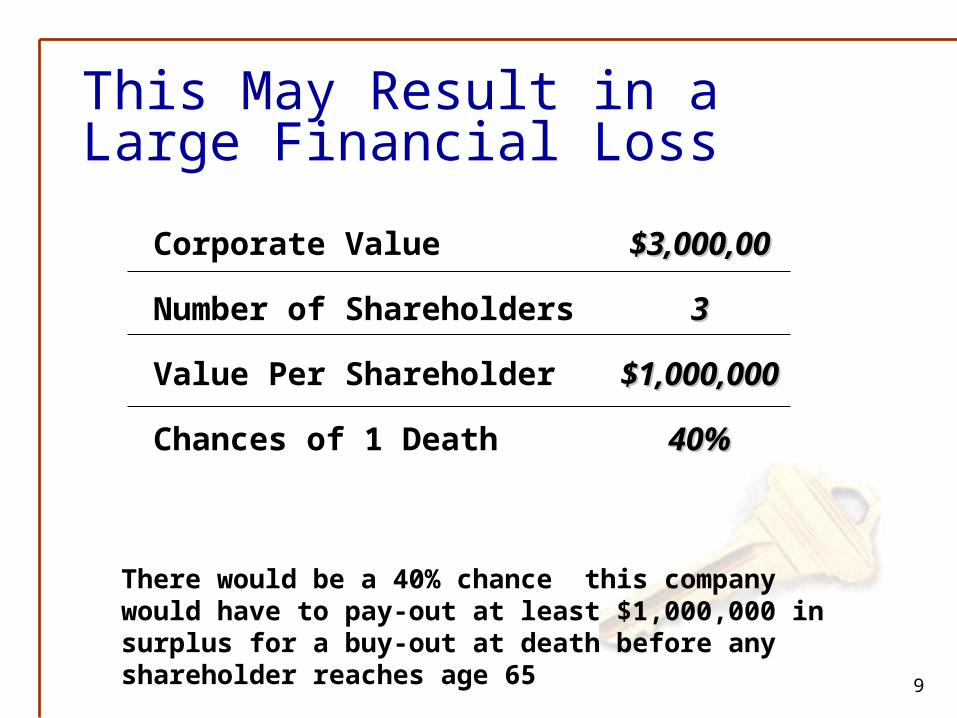

There would be a 40% chance this company would have to pay-out at least $1,000,000 in surplus for a buy-out at death before any shareholder reaches age 65

Corporate Value

Number of Shareholders

Value Per Shareholder

Chances of 1 Death

$3,000,00$3,000,00

33

$1,000,000$1,000,000

40%40%

This May Result in a Large Financial Loss

10

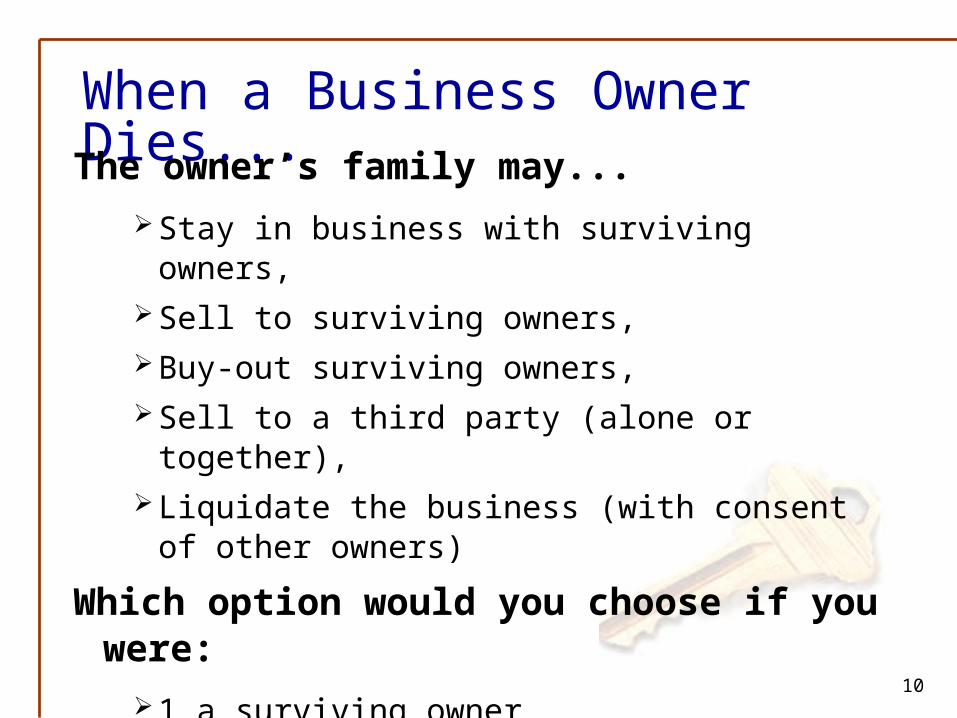

When a Business Owner Dies...The owner’s family may...

Stay in business with surviving owners, Sell to surviving owners, Buy-out surviving owners, Sell to a third party (alone or together), Liquidate the business (with consent of other owners)

Which option would you choose if you were:

1 a surviving owner 2 the decedent’s family?

11

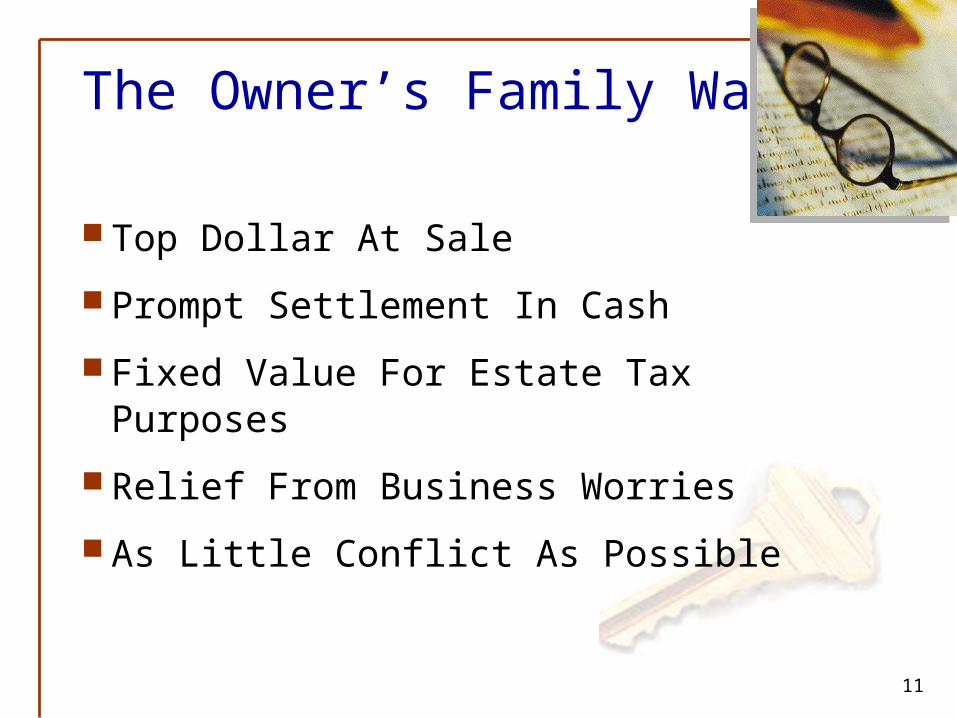

The Owner’s Family Wants

Top Dollar At Sale

Prompt Settlement In Cash

Fixed Value For Estate Tax Purposes

Relief From Business Worries

As Little Conflict As Possible

12

The Surviving Owners Want

Full Control At Sale

Business Continuation

Minimum Payments

Smooth And Prompt Transition

No Interference from Heirs

Uninterrupted Access to Credit

13

Everyone Can Lose!!!

Without an Agreement

Possible: Liquidation Litigation Loss of Value Conflict and Delay Bad Feelings and Unhappiness

14

With an Agreement Everyone Can Benefit!!!

Smooth and orderly transition

Binding value for estate tax purposes

Agreeable price and terms

Avoidance of conflicts

No forced liquidation

A known plan reduces trepidation & turmoil

Certainty vs. uncertainty can make all the difference!

15

Professional Corporations--Special Considerations

Sale must be made to other qualified professionals-- CPAs Attorneys Engineers Physicians

Often, “goodwill value” is not accounted for, and there are few hard assets in the corporation

PCs are typically valued differently from other business structures--perhaps only 1x-3x annual income!

16

Professional Corporations--Implications

…Buy-sell proceeds may not be sufficient to support retirement, disability income needs, or surviving family in the event of a buy-out at death.

Integrating buy-sell planning with overall retirement, disability, and survivor-income needs is especially important!

17

Family-Owned Businesses--Special Considerations

Not all children may be active in the business

Children may not be ready to run business when it suddenly becomes necessary

A surviving spouse may still depend on income derived from the business

Estate “equalization” may be an issue

18

Family-Owned Businesses--Special Solutions

Intra-family buy-sell agreements can be part of a solution

Equalization of the estate among children can be addressed using non business assets

Non-family key employees may be given incentives to stay, such as “golden handcuffs” benefit programs

Integrating buy-sell planning with overall retirement, disability, and survivor-income & estate planning is especially important!

19

Basic Types of Buy-Sell Arrangements

1. Entity Buy Out

2. Cross Purchase

3. Wait-&-See (a.k.a. combination or hybrid)

20

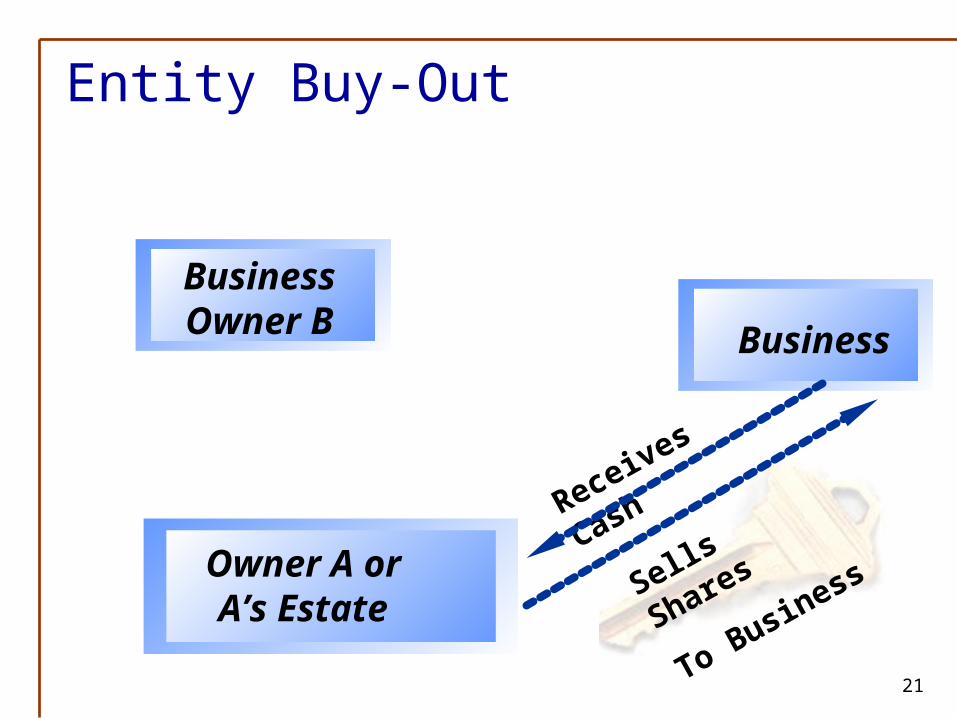

Entity Buy-Out

The business purchases the business interest from the withdrawing owner or his/her estate upon triggering the agreement.

21

Entity Buy-Out

Sells Shares

To Business

Receives Cash

Owner A or A’s Estate

Business

Business Owner B

22

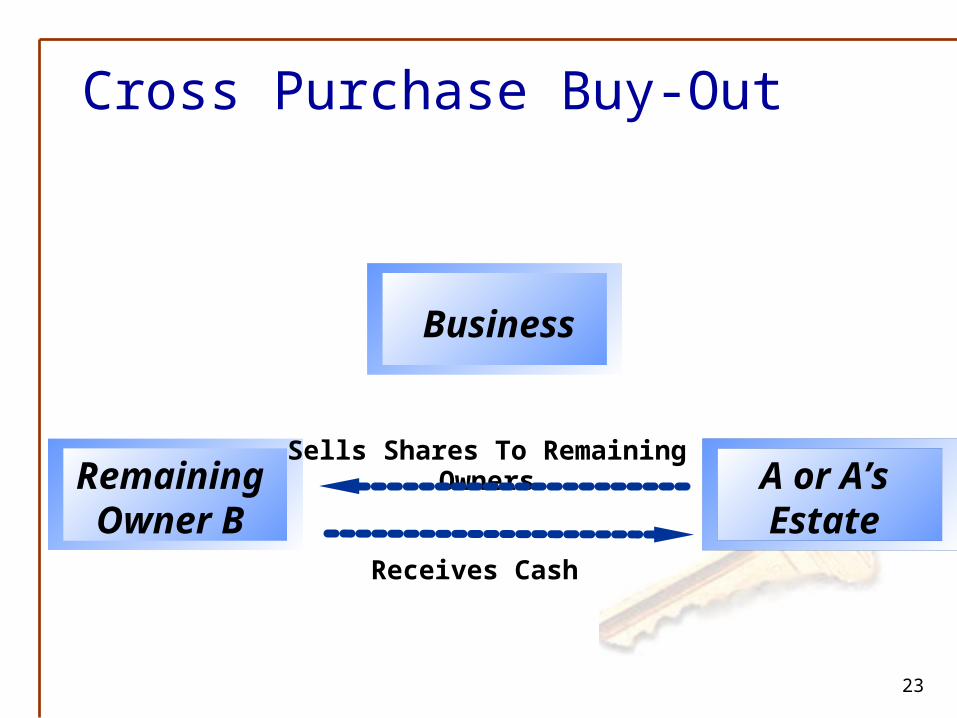

The remaining owners purchase the business interest from the withdrawing owner or his/her estate upon triggering the agreement.

Cross Purchase Buy-Out

23

Cross Purchase Buy-Out

Sells Shares To Remaining Owners

Receives Cash

Remaining Owner B

Business

A or A’s Estate

24

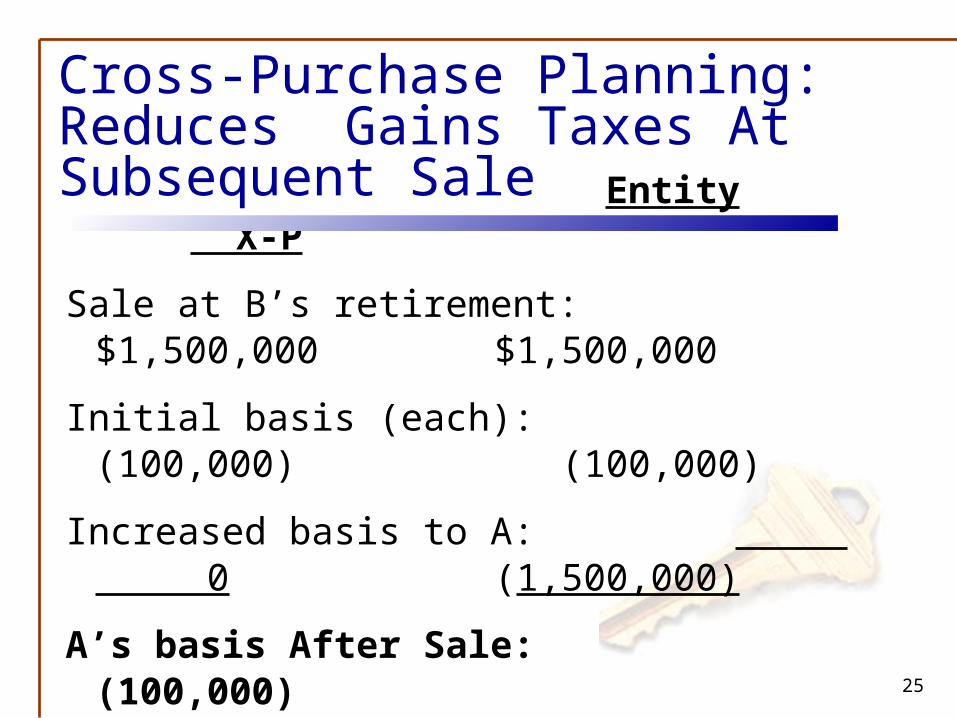

Case Study: Cost Basis ComparisonEntity Buy-Out vs. Cross-Purchase

Bob and Abby started ABC, Corp. many years agowith $100,000 each.

Current Value of business: $3,000,000.

Bob retires in 2001; buy-sell agreement is triggered.

Bob’s share is purchased for $1,500,000

Abby runs the business and sells it in 2009 (8 years later) for $6,000,000.

25

Cross-Purchase Planning: Reduces Gains Taxes At Subsequent Sale

Entity X-P

Sale at B’s retirement: $1,500,000 $1,500,000

Initial basis (each): (100,000) (100,000)

Increased basis to A: 0 (1,500,000)

A’s basis After Sale: (100,000) ( 1,600,000)

Sale price $ 6,000,000 $ 6,000,000

Taxable capital gain: $5,900,000 $ 4,400,000

26

Wait-&-See Buy-Sell: A Combination Agreement

Buy-Sell contains option for either corporate OR personal purchase of withdrawing/deceased’s shares

Funding is cross-owned outside the corporation. (ie; A owns assets which will pay for B’s interest)

Provides flexibility to help meet needs when triggering event occurs.

27

Which Type is Right? Entity:

Less complex to arrange Funded with corporate assets May be best choice if business will NOT be sold after an owner’s death

Cross-Purchase: Increased cost basis to survivors Can fine-tune ownership % No Corp. AMT or excess surplus worries Often the best choice for family businesses

Wait-&-See Maximum flexibility at execution + captures advantages of each No effective difference to owner/estate doing the selling

28

Buy and Sell Essentials

Written Agreement

Accurate Valuation

Adequate Funding

29

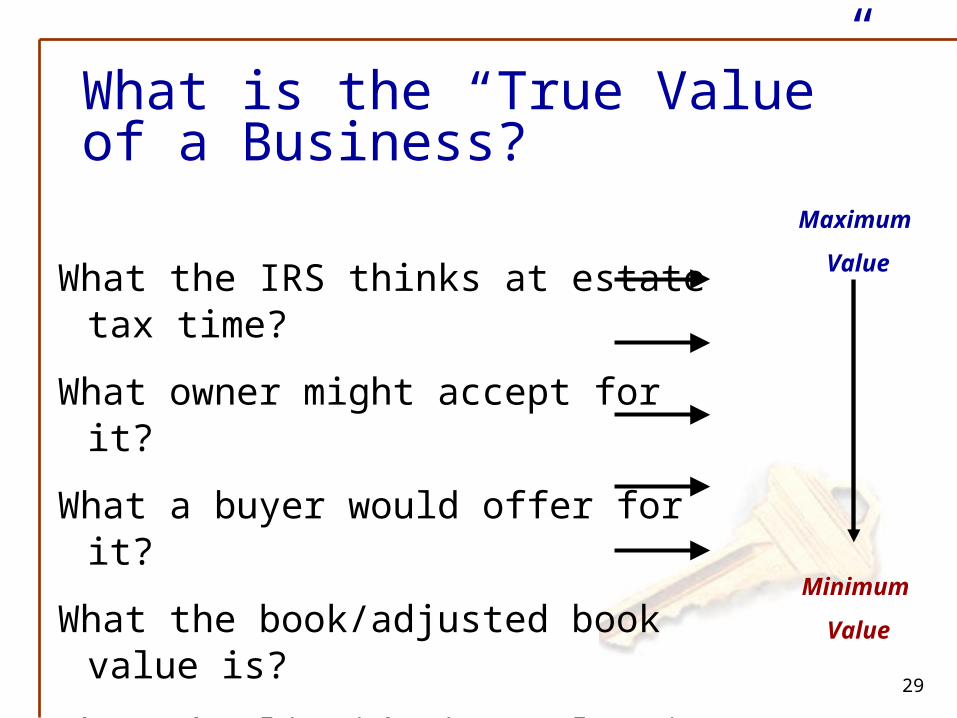

What the IRS thinks at estate tax time?

What owner might accept for it?

What a buyer would offer for it?

What the book/adjusted book value is?

What the liquidation value is?

What is the “True Value” of a Business?

Maximum

Value

Minimum

Value

30

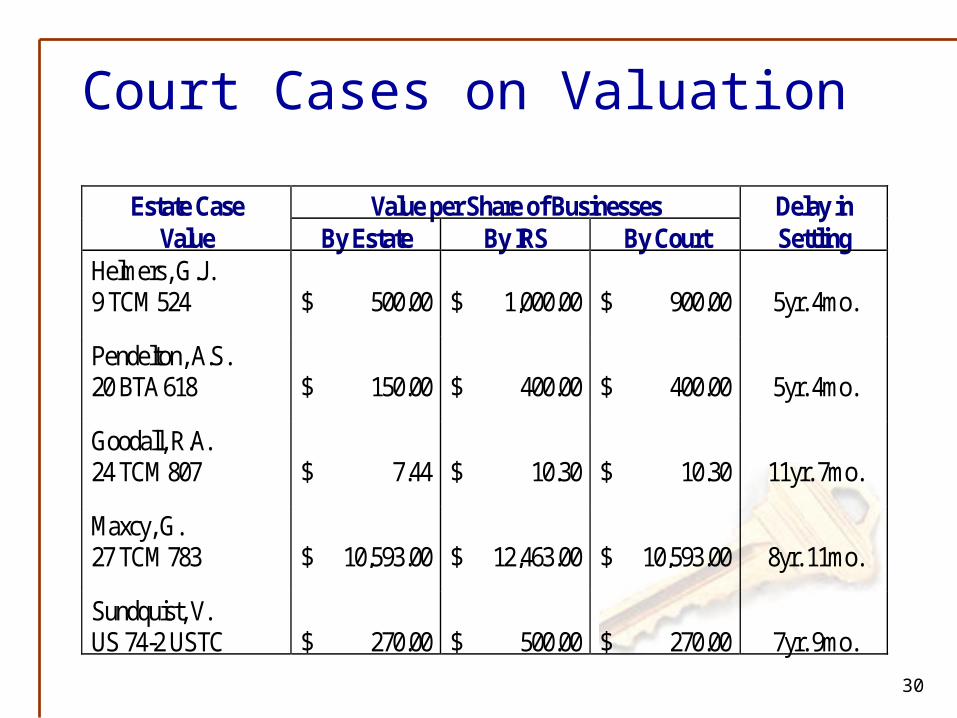

Court Cases on Valuation

Estate Case Value per Share of Businesses Delay inValue By Estate By IRS By Court Settling

Helmers, G.J.9 TCM 524 $ 500.00 $ 1,000.00 $ 900.00 5yr. 4mo.

Pendelton, A.S.20 BTA 618 $ 150.00 $ 400.00 $ 400.00 5yr. 4mo.

Goodall, R.A.24 TCM 807 $ 7.44 $ 10.30 $ 10.30 11yr. 7mo.

Maxcy, G.27 TCM 783 $ 10,593.00 $ 12,463.00 $ 10,593.00 8yr. 11mo.

Sundquist, V.US 74-2 USTC $ 270.00 $ 500.00 $ 270.00 7yr. 9mo.

31

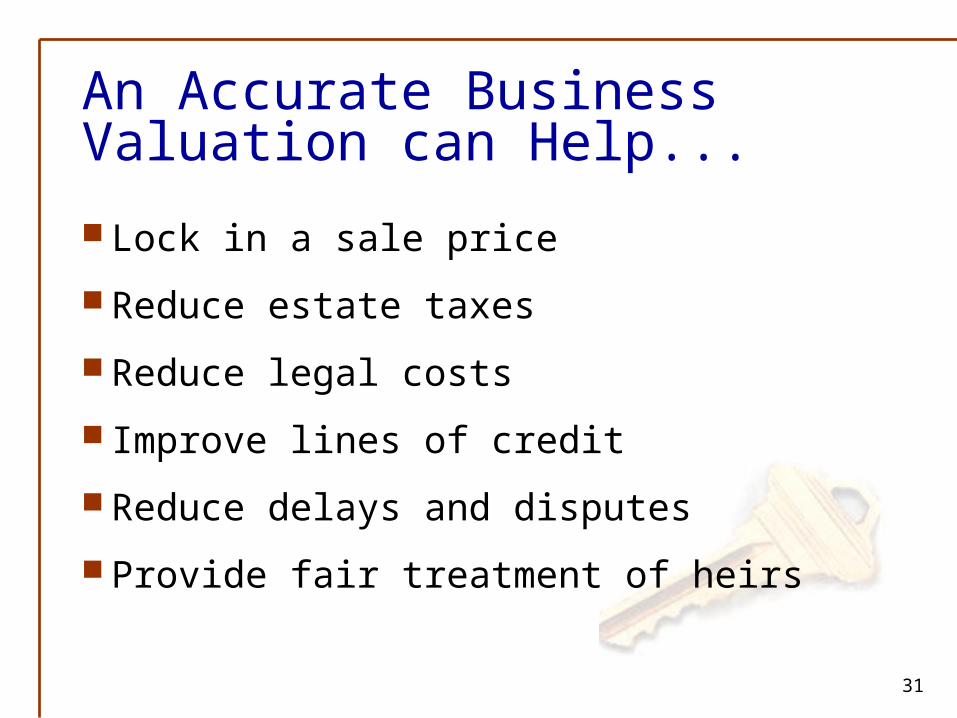

An Accurate Business Valuation can Help...

Lock in a sale price

Reduce estate taxes

Reduce legal costs

Improve lines of credit

Reduce delays and disputes

Provide fair treatment of heirs

32

Buy and Sell Essentials

Written Agreement

Accurate Valuation

Adequate Funding

Review periodically; update as needed

33

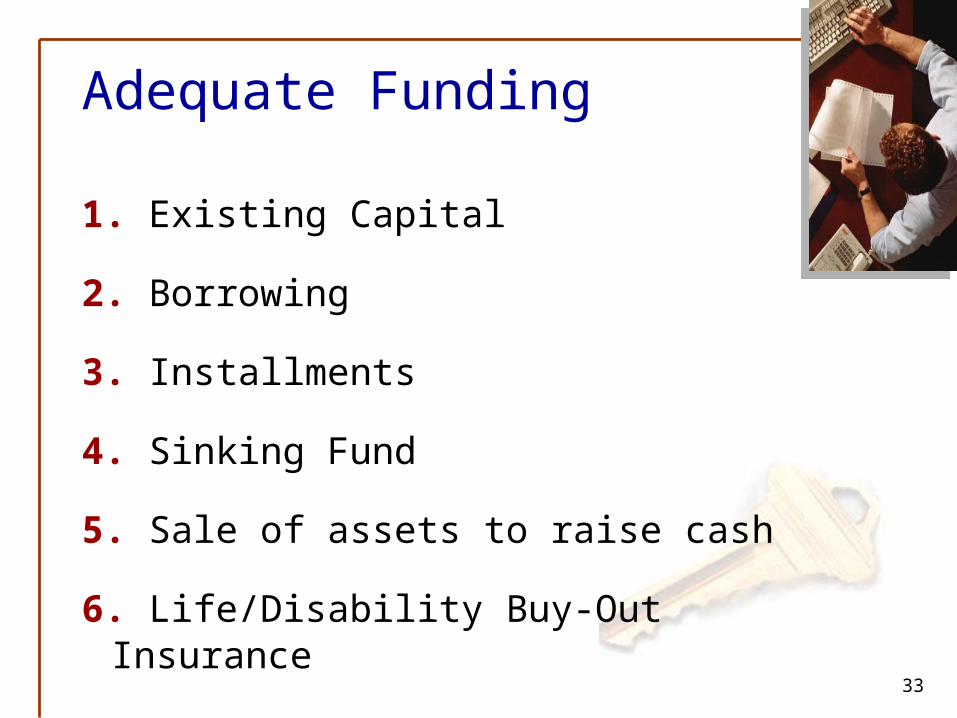

Adequate Funding

1. Existing Capital

2. Borrowing

3. Installments

4. Sinking Fund

5. Sale of assets to raise cash

6. Life/Disability Buy-Out Insurance

34

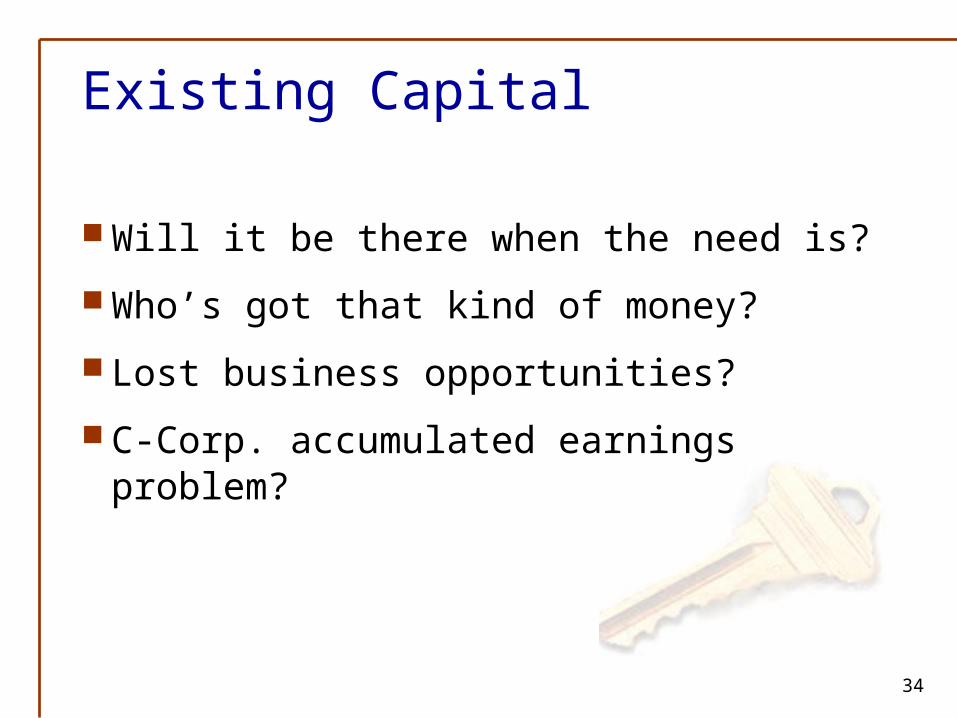

Existing Capital

Will it be there when the need is?

Who’s got that kind of money?

Lost business opportunities?

C-Corp. accumulated earnings problem?

35

Borrowing

Will buyer qualify?

Can borrower repay?

High interest charges?

EXPENSIVE!

36

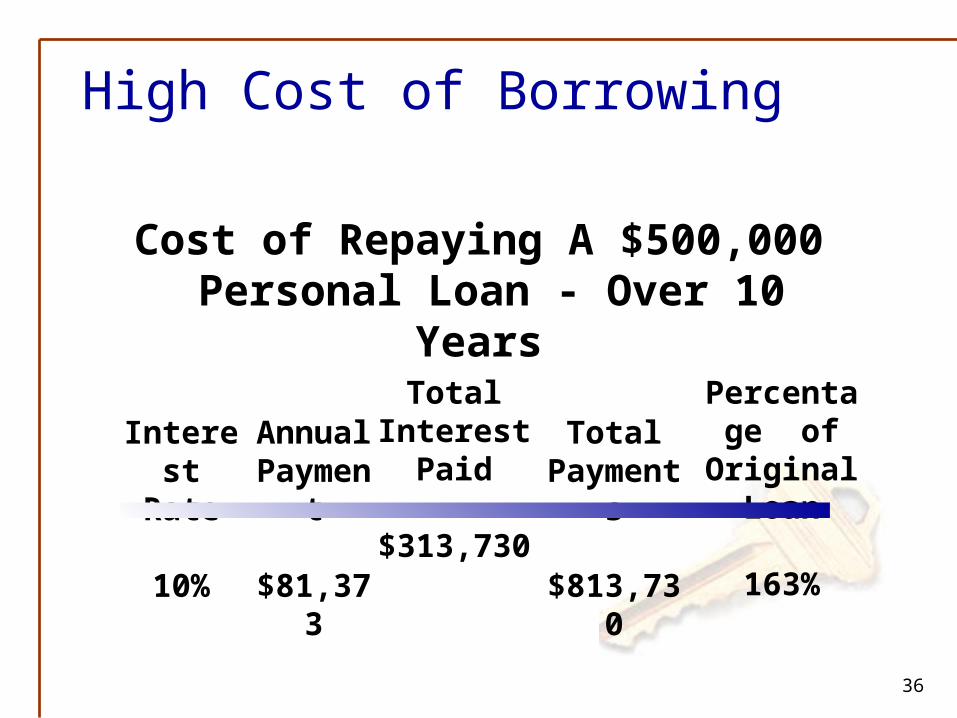

High Cost of Borrowing

Cost of Repaying A $500,000 Personal Loan - Over 10 Years

Percentage of Original

Loan

163%

Interest Rate

10%

Annual Payment

$81,373

Total Interest

Paid

$313,730

Total Payments

$813,730

37

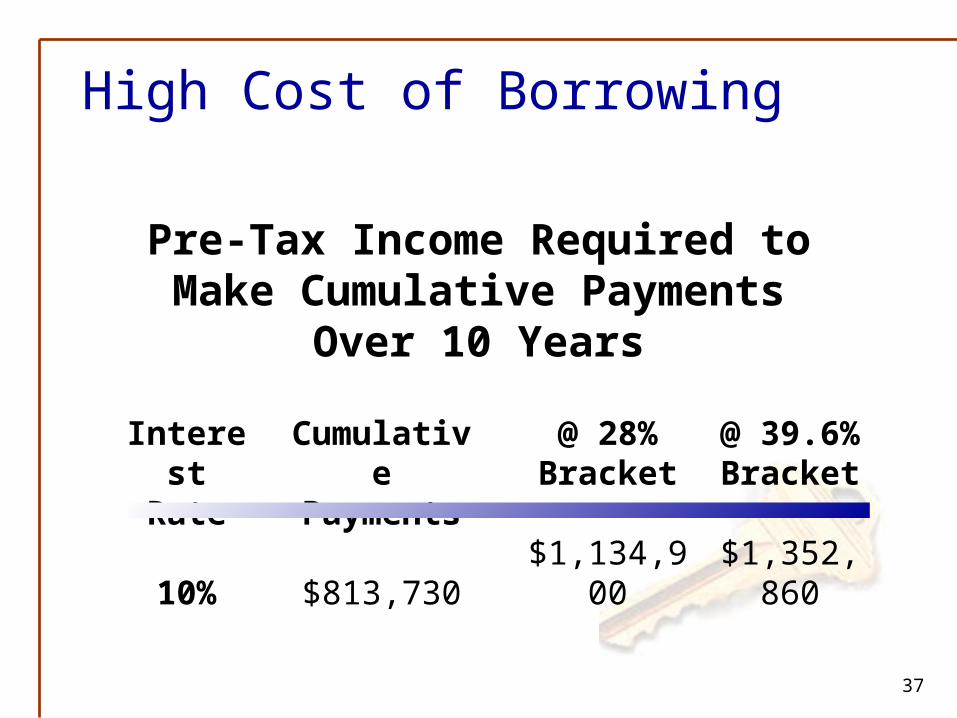

High Cost of Borrowing

Pre-Tax Income Required to Make Cumulative Payments Over 10 Years

Interest Rate

10%

CumulativePayments

$813,730

@ 28% Bracket

$1,134,900

@ 39.6% Bracket

$1,352,860

38

High Cost of Borrowing

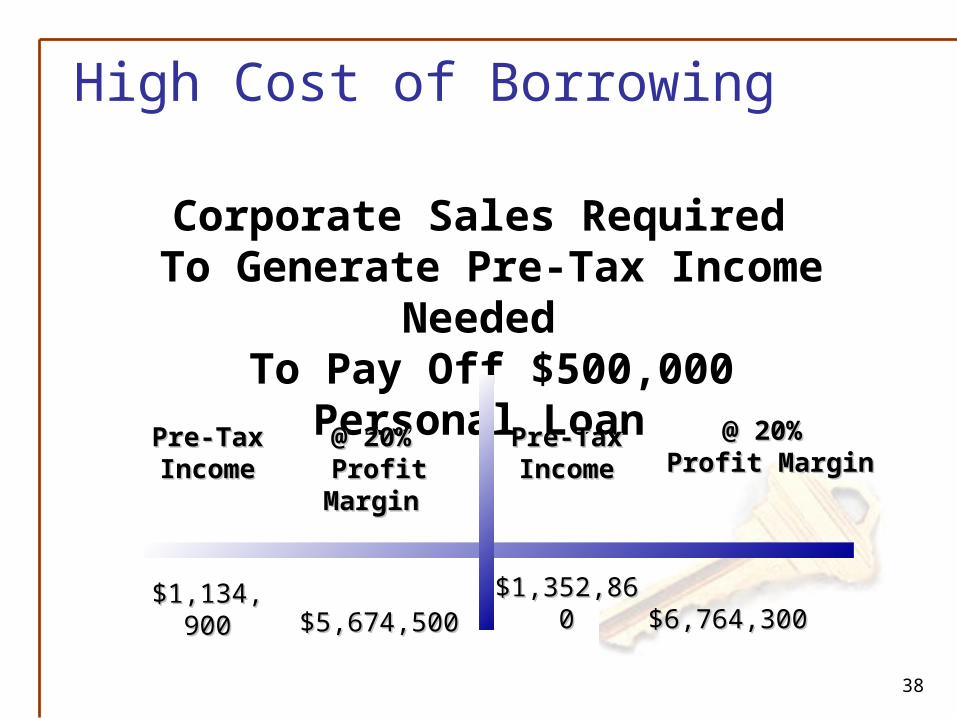

Corporate Sales Required To Generate Pre-Tax Income Needed To Pay Off $500,000 Personal Loan

Pre-Tax Pre-Tax IncomeIncome

$1,134,900$1,134,900

@ 20%@ 20% Profit Margin Profit Margin

$5,674,500$5,674,500

Pre-Tax Pre-Tax IncomeIncome

$1,352,860$1,352,860

@ 20%@ 20% Profit Margin Profit Margin

$6,764,300$6,764,300

39

Installment Payments

Can buyer afford it?

Will buyer default?

Installments may outlast business?

False sense of security?

40

Sinking Fund

Lost Business opportunities?

Will money be on time?

Corporate income tax due on accumulations?

C-Corp. accumulated earnings problem?

41

Sale of Assets

Forced sale is NOT conducive to best price!

Will it cover the need?

Was it desirable from a business perspective?

42

Life & DBO Insurance

1. Easy to use

2. Cost-effective AND those costs are known in advance

3. Helps eliminate risk

4. Provides an income tax free death/disability benefit

5. Premium can be waived during disability w/purchase of appropriate rider (life ins.)

6. Can provide tax-deferred accumulation to help fund RETIREMENT buyout at the same time (life ins.)

7. Premiums must be paid and owners must be insurable

43

Funding Using Insurance:Paying the Premium

Business can pay…one way or another Directly, in entity arrangement Split dollar Executive bonus or double bonus

Make premiums deductible

44

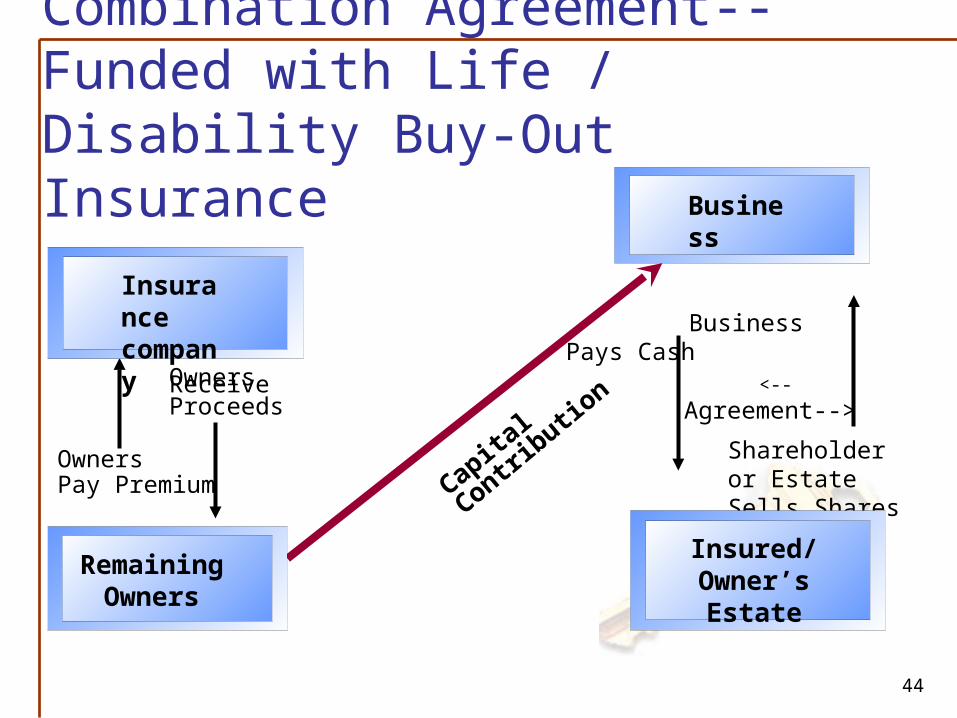

Owners Receive Proceeds

Owners Pay Premium

Shareholder or Estate Sells Shares

Business Pays Cash

<--Agreement-->

Capital

Contributio

n

Combination Agreement--Funded with Life / Disability Buy-Out Insurance

Insurance company

Business

Remaining Owners

Insured/ Owner’s Estate

45

Business Succession Arrangement

Insurance helps stabilize a business by providing funds that can help---

Pay income and estate taxes Provide working capital Meet payroll Pay suppliers and creditors Expand, diversifying, reorganizing Replace key employees Buy unmarketable shares

46

Buy-Sell Life Insurance

What If It Were Tax Deductible?

47

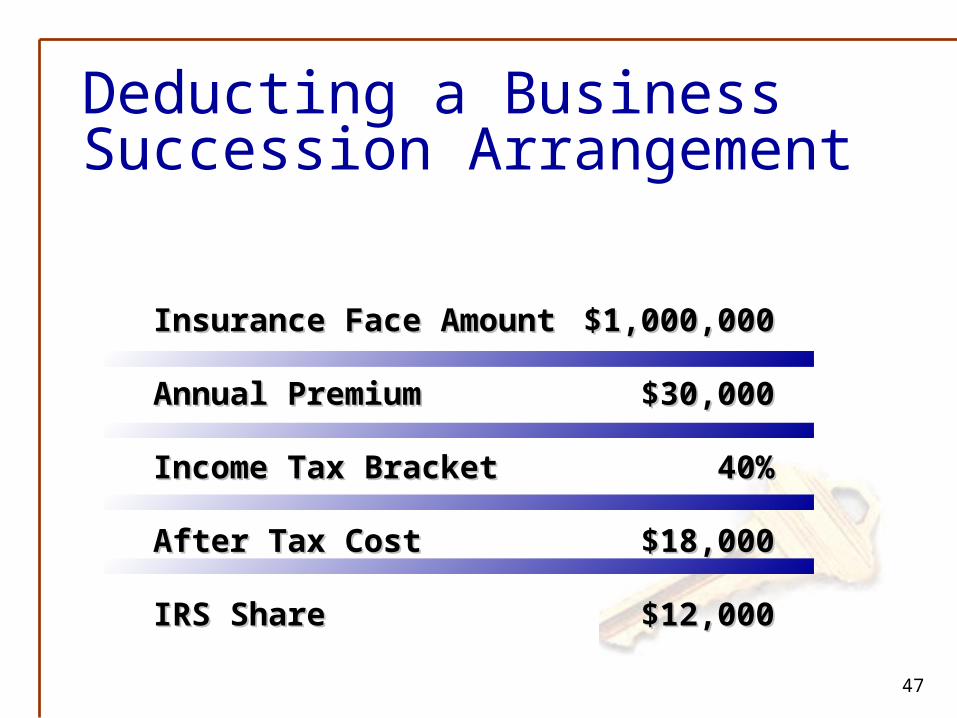

Insurance owned by your profit sharing plan lowers your costs…

Deducting a Business Succession Arrangement

Insurance Face AmountInsurance Face Amount

Annual PremiumAnnual Premium

Income Tax BracketIncome Tax Bracket

After Tax CostAfter Tax Cost

IRS ShareIRS Share

$1,000,000$1,000,000

$30,000$30,000

40%40%

$18,000$18,000

$12,000$12,000

48

Deducting a Business Succession Arrangement

What if the insurance were on the life of your business partner?

Purpose:

To help fund a buy and sell arrangement at death.

49

Pure Death

Benefit

Annual Premium

Cash Value

Deducting a Business Succession Arrangement

Insurance Company

Profit Sharing Plan Account of Shareholder #1 (Insures Shareholder #2)

Shareholder #1Pays Tax on PS58Receives Death Benefitincome tax free

50

CashStock

Pays TaxesProvides Income

Deducting a Business Succession Arrangement

Shareholder #1Buys Stock From Estate Of Shareholder #2

Estate OfShareholder #2Receives Cash for Stock

51

Deducting a Business Succession Arrangement

Living Buy Out At Retirement

Each shareholder’s profit sharing account can also tap the cash value of the insurance it owns to buy the shares of a withdrawing or retiring shareholder.

52

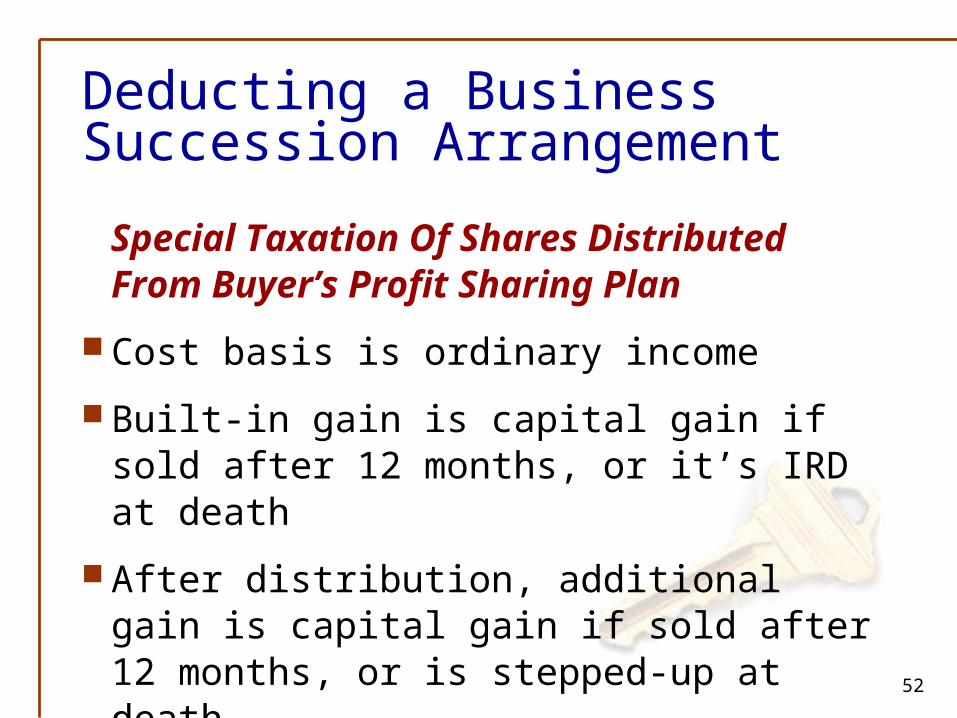

Deducting a Business Succession Arrangement

Special Taxation Of Shares Distributed From Buyer’s Profit Sharing Plan

Cost basis is ordinary income

Built-in gain is capital gain if sold after 12 months, or it’s IRD at death

After distribution, additional gain is capital gain if sold after 12 months, or is stepped-up at death

53

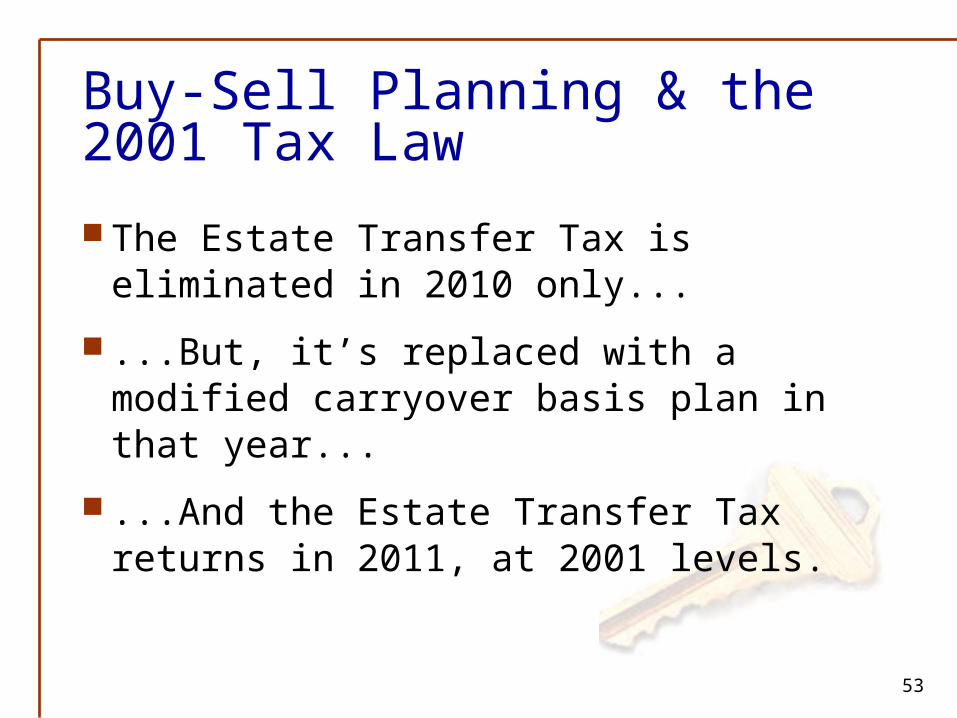

Buy-Sell Planning & the 2001 Tax Law

The Estate Transfer Tax is eliminated in 2010 only...

...But, it’s replaced with a modified carryover basis plan in that year...

...And the Estate Transfer Tax returns in 2011, at 2001 levels.

54

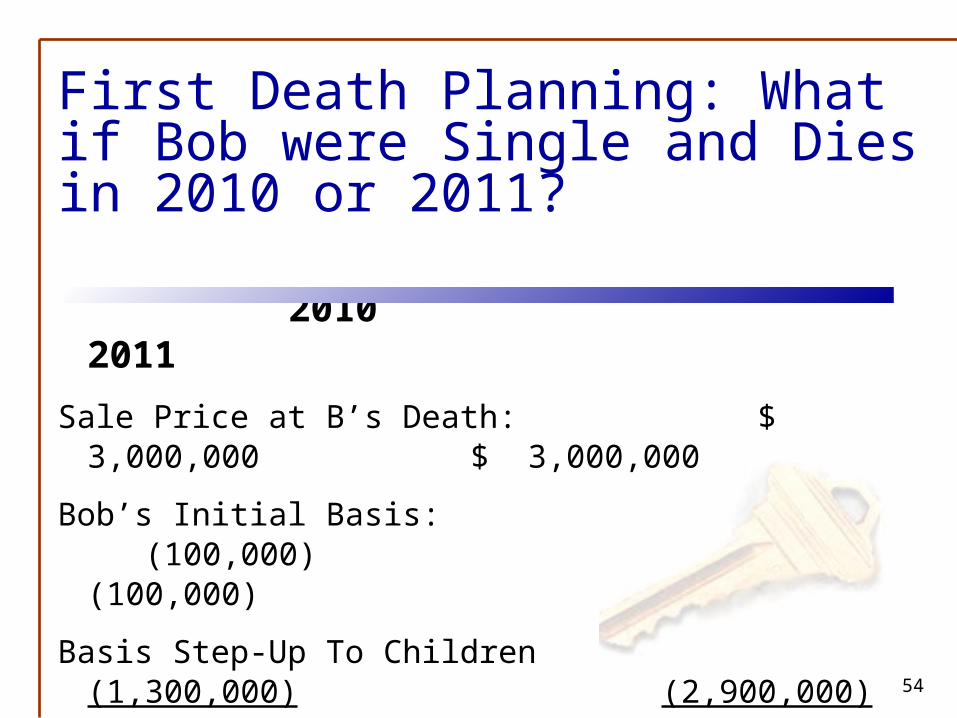

First Death Planning: What if Bob were Single and Dies in 2010 or 2011?

2010 2011

Sale Price at B’s Death: $ 3,000,000 $ 3,000,000

Bob’s Initial Basis: (100,000) (100,000)

Basis Step-Up To Children (1,300,000) (2,900,000)

Taxable Gain $ 1,600,000 $ - 0 - -- versus --

Taxable Estate Repealed $ 3,000,000

55

First Death Planning: Transfer Costs On Buy-Sell At Bob’s Death

Year 2010 “Sunrise”

Gains Tax on $1,600,000

Federal Gains Tax $320,000

State Gains Tax 80,000

Federal Estate Tax - 0 -

State Death Tax 182,000

Total Taxes $582,000

Year 2011 “Sunset”

Estate Tax on $3,000,000

Federal Gains Tax $ - 0 -

State Gains Tax - 0 -

Federal Estate Tax 763,000

State Death Tax 182,000

Total Taxes $ 945,000

56

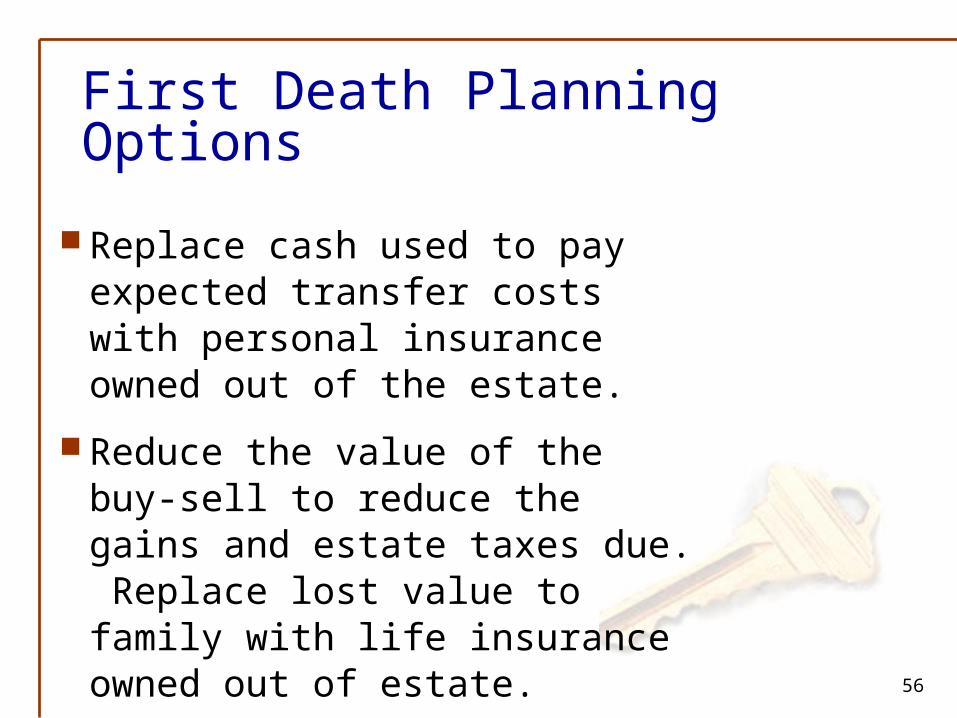

First Death Planning Options

Replace cash used to pay expected transfer costs with personal insurance owned out of the estate.

Reduce the value of the buy-sell to reduce the gains and estate taxes due. Replace lost value to family with life insurance owned out of estate.

57

Buy-Sell Agreements: Thinking outside the Box

What if an owner has no co-owners? Agreement with key employees? Agreement with competitor? Sale using business broker or M & A firm?

58

Sale to An Outside Buyer --Prepare 2-5 Years in Advance!

Consider a professional valuation

Consider co-owners’ exit strategies

Focus on profitability

Keep running the business!

59

A Buy-Sell Agreement is a Good Idea When...

There is a high degree of financial risk for the family of the retired / disabled / deceased owner

It’s important to guarantee a market at retirement, death or disability for the sale of an otherwise unmarketable business interest

It’s important to fix the value of the business for federal estate tax purposes

60

A Buy-Sell Agreement is a Good Idea When...

A surviving owner is unable or unwilling to remain in business with the deceased/withdrawing owner’s heirs

It’s important to prevent outsiders from taking over the business

The owner / owner’s estate needs cash and the business is unable to provide it

61

Buy-Sell Planning:Critical Components

A written agreement Address ALL appropriate contingencies Provide for valuation Address funding

Type of agreement is a secondary issue… but, when appropriate, consider opportunities!

Business Succession:Buy-Sell Planning

MONY Life Insurance Company and MONY Securities Corporation are members of The MONY Group