Embed Size (px)

Citation preview

Financial Inclusion in ASEANPresentation for the ASEAN Working Group on Financial Inclusion

Kuala Lumpur, Malaysia, January 21, 2016

Jose De Luna Martinez

World Bank Group

Contents

I. Financial inclusion around the world

II. Financial inclusion in ASEAN

- Ownership of accounts

- Use of accounts

- Payments

- Savings, credit, and financial resilience

III. Final remarks

Global Findex measures financial inclusion in a systematic and

comparable manner

Methodology Global Findex (2014 )

• Survey based on face-to-face and phone interviews (150,000 people).

• Respondents were randomly selected.

• Data is weighted to ensure a nationally representative sample for each

economy.

• Adults age 15+

• Account: percentage of respondents who report having an account at a

bank or another financial institution or report personally using a mobile

money service in the past 12 months.

Key Definitions

Financial inclusion

around the world

Ownership of accounts, saving, and borrowing

Global Findex reveals that between 2011 and 2014, 700 million

adults worldwide became account holders

Source: Global Findex database. (p.p.) percentage points.

Indicator 2011 2014 Change

(p.p.)

Ownership of account 50.6 61.5 10.9

With debit card 30.5 40.0 9.5

With credit card 14.9 17.6 2.7

Saved at a financial institution 22.6 27.4 3.8

Borrowed from a financial institution 9.1 10.7 1.6

Selected World Financial Inclusion Indicators

(% of adults age 15+)

• The number of adults without an account dropped by 20% to 2 billion in 2014.

• The increase in account ownership was driven by the growth in account

penetration of developing economies and innovations in technology, particularly

mobile money.

Source: Global Findex database. p.p. percentage points.

Adults with an account (%) in 2014Change

2014/2011

(p.p.)

14

8

4

12

3

14

10

World

62

Despite the progress that has been achieved in the past, there

are still disparities among regions

2011

2014

71

38

71

41

30

36

60World

56

Adults saving any money in 2014

(%)

In 2014, 56% of adults around the world reported having saved

Sou

rce:

Glo

bal F

inde

xda

taba

se.

But only 27% of adults saved at a financial institution

World

42

Adults borrowing from any source in the past year

(% of adults)

According to Findex, 42% of adults reported that they borrowed

money in the past 12 months

Source: Global Findex database.

But only 11% of adults borrowed through a financial institution

Financial inclusion in ASEAN

Ownership, education, gender, income, and rural

Adults with an account

(%)

In ASEAN, 50% of adults reported having an account in 2014

ASEAN

50

2011 2014

Source: Global Findex database. Lao PDR data is 2011.

The share of adults with an account increased by 8 percentage points,

from 42% in 2011 to 50% in 2014.

Female and male adults with an account (%) in 2014

In ASEAN as a group, there is practically no gender gap in

account ownership

ASEAN

Male

Female

In ASEAN, 49% of men and 48% of women reported having an account

Source: Global Findex database. Lao PDR data is 2011.

Adults in poorest 40% of households

with an account (%)

In ASEAN, account penetration among poorest 40% is 38%

The gap between the richest 60% and the poorest 40% is 15 percentage

points.

With

account

Without

account

ASEAN

38

Source: Global Findex database. Lao PDR data is 2011.

Adults in rural areas with account

(%)

36% of adults in rural areas reported having an account

Account penetration in rural areas in high income OECD economies is 2.6

times ASEAN’s.

ASEAN

36

Source: Global Findex database. Lao PDR data is 2011.

Use of account

Deposits, withdrawals, debit card, and credit card

Frequency of deposits by account holder

Adults with an account by number of deposits in a typical month (%)

In ASEAN in 2014, 56% of adults with an account at a financial

institution reported making at least one deposit

The difference with high income OECD economies is 28 percentage points.

Source: Global Findex database. Lao PDR data is 2011. Note: The categories do not sum to 100% because of “don’t know” and “refuse” answers.

None 1-2 3 or more

Frequency of withdrawals by account holder

Adults with an account by number of withdrawals in a typical month (%)

And 50% of adults with an account at a financial institution reported

making at least one withdrawal per month

Among ASEAN countries there is a broad range between 8% and 82% of adults

reporting withdrawals in a typical month

Source: Global Findex database. Lao PDR data is 2011. Note: The categories do not sum to 100% because of “don’t know” and “refuse” answers.

None 1-2 3 or more

Adults with a financial institution account by

most common mode of withdrawal used

(%)

In ASEAN, 53% of adults with an account at a financial institution

reported using an ATM to withdraw money

And 34% of adults with account used a bank teller to make withdrawals

Source: Global Findex database. OECD data is 2011. Note: The categories do not sum to 100% because of “don’t know” and “refuse” answers. Other includes bank agent and

retail stores.

ATM Bank teller Other

In ASEAN, 30% of adults reported having a debit card

However, only half of the people with a debit card made use of it in the last

12 months

Source: Global Findex database. Lao PDR data is 2011.

Adults with a debit card

(as % of all adults)

ASEAN

30

Adults that used debit card

(as % of all adults)

ASEAN

15

Adults with a credit card

(as % of all adults)

In ASEAN, 9% of the people has a credit card

And 90% of them used it in the last 12 months

Source: Global Findex database. Lao PDR data is 2011.

ASEAN

9

Adults that used credit card

(as % of all adults)

ASEAN

8

Payments

Wages, government transfers, utility bills, remittances, and use of internet

Adults receiving wage payments by method

In ASEAN, 71% of adults reported receiving their wages in

cash

The ratio of ASEAN to high-income OECD economies of people

receiving wages in cash is 6 times

Source: Global Findex database. Into an accountIn cash

In ASEAN, 69% of adults that reported receiving government

transfers did so in cash

However, some countries are moving towards cashless government

transfers schemes

Source: Global Findex database.

ASEAN

69

Adults that receive government transfers in cash

(% of adults receiving government transfers)

Utility payments

Adults paying utility bills in cash in 2014

(as % of all adults)

In ASEAN, 89% of adults reported paying utility bills in cash

The ratio of adults paying bills in cash in ASEAN to high-income OECD

economies is 3 times

Source: Global Findex database.

ASEAN

89

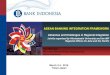

How adults sent remittances?

(%)

Source: Global Findex database.

Note: Respondents could report using more than one method.

In ASEAN, 61% of adults that sent remittances used cash and

33% used informal channels to do their transactions

In cashMoney transfer operator

Financial institutionMobile phone

Source: Global Findex database.

Note: Respondents could report using more than one method.

In ASEAN, most adults received remittances in cash

In cashMoney transfer operator

Financial institutionMobile phone

Means to receive remittances

(%)

Use of internet to make payments

Adults who used internet to pay bills or buy things (% of all adults)

Source: Global Findex database.

No use of

internet

Use of

internet

In ASEAN, 8% of adults reported using internet to make payments

Saving, credit and financial

resilienceSaving, borrowing, mortgage, and emergency funds

Adults saving any money

(%)

Source: Global Findex database and UNCDF.

Other

In ASEAN, a large number of adults still save their money at home

or at informal groups

Financial

institution

Semi-

formal

Sources of borrowing used by adults in ASEAN

(% of total borrowers)

Source: Global Findex database and UNCDF. Note: Respondents could report borrowing from more than one source.

In ASEAN, family and friends are the main source of funds for

adults borrowing

Financial

institution

Family &

friends

Semi-

formal

Other

Adults able to raise emergency funds by main source

(%)

Source: Global Findex database.

Note: Other includes “other sources” and “don’t know” and “refuse” answers.

The main source for emergency funds is family or friends

SavingsFamily or

friends

Work loanOther

Financial

institution

Informal

Final remarks

Conclusions, ASEAN FI goals, and WB’s role

Conclusions

• Between 2011 and 2014, ASEAN has achieved a substantial increase in

financial inclusion.

• However, 264 million (59%) of adults 15+ in ASEAN still remained

unbanked.

• With the expansion of the middle-income class in ASEAN, the demand for

access to finance and credit is expected to continue to grow.

• Many countries in ASEAN have a large opportunity for increasing

financial inclusion.

• For households in ASEAN, cash still constitutes the main means for

executing financial transactions (payment of wages, government

transfers, payment of bills, receiving and sending remittances).

• A large number of adults with accounts at financial institutions still prefer

to conduct and settle their transactions in cash.

• Use of debit and credit cards is relatively low across ASEAN when

compared to other regions in the world.

• In ASEAN, a large number of adults that save money still do not use

financial institutions.

• A large number of adults in ASEAN see their relatives and employers as

the main source of borrowing, not financial institutions.

• Digital financial inclusion remains limited in ASEAN.

• Overall, there is a need to scale up the “usage” of accounts for adults

with accounts at financial institutions.

• There are large opportunities for advancing financial inclusion by paying

wages and disbursing government transfers through financial institutions.

Conclusions

Adults with an account (%)

Source: Global Findex database and World Bank staff estimates.

75

Baseline

Findex

trend

ASEAN potential goal for account ownership in 2020: Findex

trend 67% or optimistic scenario 75%

Gap between 60% richest and 40% poorest less than 5 pp (baseline 15 pp)

Optimistic

scenario

67

50

2020

2014

Account ownership and savings in ASEAN

Source: Global Findex database and World Bank staff estimates.

Financial inclusion remains a challenge for ASEAN

% of adults that saved at a financial institution

% o

f a

du

lts w

ith

an

ac

co

un

t

How can the WBG help?

New graphic: bicycle spokes?

Client

Financing

Analytical services

andadvisory

Technical assistance

Diagnostic assessment

Practical knowledge

Data

Loans/grants

Credits

Guarantees

Risk management products

Amend regulations

Formulate national

strategies

Develop financial

products

Annexes

Source: Global Findex database. Note: The categories do not sum to 100% because of “don’t know” and “refuse” answers.

Adults by reported likelihood of being able to

raise emergency funds in 2014

(%)

Globally, 76% of adults reported that it would be possible to come

up with an amount equivalent to 5% of the GNI per capita

In OECD countries, 83% of adults reported that it would be possible to come up

with these funds, while in developing countries 74% did

Very

possible

Somewhat

possible

Not very

possible

Not at all

possible

Account penetration by age group

(%)

The relative age group gap in ASEAN is very small, less than 1

percentage point

47% of adults age 25+ and 46% of adults age 15-24 reported having an

account in a financial institution

Age 25+Age 15-24

ASEAN

Source: Global Findex database. Lao PDR data is 2011.

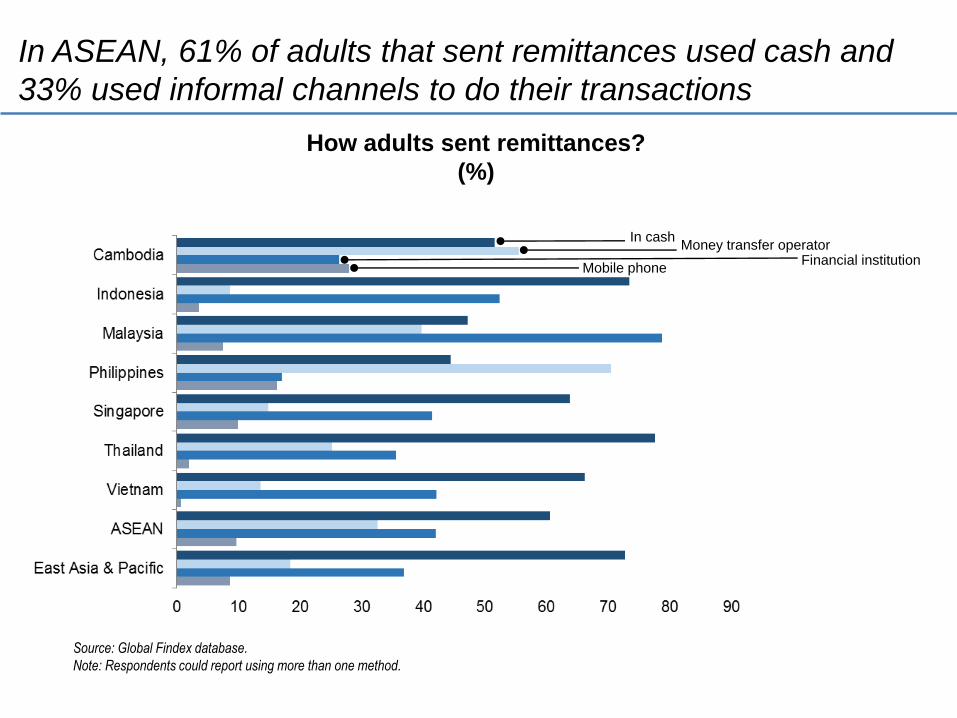

Account ownership for adults with

primary education

(%)

Account ownership among adults with primary education is 30%

ASEAN

30

Source: Global Findex database.

Lao PDR data is 2011. Singapore and high-income OECD economies did not report data on accounts for adults with primary education.

Reasons for saving

Adults saving for specified purpose in the past year

(% of savers)

Source: Global Findex database.

Note: Respondents could report saving for more than one purpose.

For education

The main reason for saving in ASEAN is for old age, followed

by for education

For business

For old age

Purpose of borrowing

(% of borrowers)

Source: Global Findex database. Note: Respondents could report borrowing for more than one purpose.

For education

In ASEAN, the main reason for borrowing is for health or

medical purposes

For business

For health or medical purposes

Use of mobile phones to access financial

institution accounts

Adults with a financial institution account with use of mobile phone access in 2014

(as % of all adults)

Only 5% of adults access their accounts with a mobile phone

In high-income OECD economies 21% of adults access their accounts

using a mobile phone

Source: Global Findex database.

Did not use mobile

phone to access

account

Used mobile phone

to access account

Agricultural payment recipients

Adults receiving cash payments for agricultural products

(% of recipients)

In ASEAN, 99% of adults who received agriculture payments

did so in cash

In high-income OECD economies no adult reported receiving cash

payments for agricultural activities

Source: Global Findex database.

Adults with an outstanding mortgage

(%)

Source: Global Findex database. Data for Lao PDR is 2011.

In ASEAN, 10% of adults reported having an outstanding

mortgage

No

mortgage

Mortgage

Adults paying school fees in cash in the

past

(%)

In ASEAN, 87% of adults reported paying school fees in cash

Source: Global Findex database.

ASEAN

87

Saving at a financial institution

(% of adults)

Source: Global Findex database and World Bank staff estimates.

ASEAN potential goal for saving at a financial institution in 2020:

Findex trend 36% or optimistic scenario 43%

43

Baseline

Findex

trend

Optimistic

scenario

36

24

2020

2014

Borrowed from a financial institution

(% of adults)

Source: Global Findex database and World Bank staff estimates.

ASEAN potential goal for borrowing from a financial institution in

2020: Findex trend 25% or optimistic scenario 32%

32

Baseline

Findex

trend

Optimistic

scenario

25

17

2020

2014

![Financial Inclusion: General Overview, Central Banks …...Financial Inclusion [General Overview] •Financial inclusion or inclusive financing is the delivery of financial services](https://img.pdfslide.us/doc/110x75/5e95eef43708446e852354fe/financial-inclusion-general-overview-central-banks-financial-inclusion-general.jpg)