Embed Size (px)

Citation preview

1

Financial Distress: Lifecycle and Corporate Restructuring

SzeKee Koh, Lele Dai and Millicent Chang

The University of Western Australia

Abstract

Lifecycle theory suggests the unique firm lifecycle characteristics of birth, growth, maturity,

and decline and how these characteristics affect the decisions a firm makes, especially in

situations such as financial distress and the threat of bankruptcy. However because of these

lifecycle characteristics, when firms are faced with distress, managers may have limited

restructuring options. We examine how lifecycle characteristics affect the restructuring

strategies used by firms in financial distress such as: managerial, operational, asset and

financial strategies. We find evidence that distress firms’ access to different types of

restructuring strategies is limited by the lifecycle stage they are in. For example, mature firms

replace top level management while growth, mature and decline firms reduce dividend

payments and raise funds from external sources. Birth firms on the other hand are least able

to adopt restructuring strategies when in distress.

JEL classification: G33, G34

Keywords: Lifecycle Theory, Financial Distress, Restructuring

_______________________

The authors are from the University of Western Australia Business School (M250 (Accounting and Finance, 35

Stirling Highway, Crawley, Western Australia 6009). The authors also gratefully acknowledge the financial

support provided by the UWA Business School Research Development Grant.

2

1.0 Introduction

It has become commonly accepted in the managerial literature that as a firm grows and

matures, it moves through different stages of the corporate lifecycle (Miller & Friesen, 1984).

These stages differ in terms of firm characteristics and structure. The exact classification of

lifecycle stages varies, but common stages include; birth, growth, maturity, and decline

(Adizes, 2004). Firms in the birth phase are in the initial stage of starting up business

operations. These firms are action oriented and focused on expansion. During the growth

stage, firms have enjoyed some success and are experiencing strong business growth and cash

flows. Those that reach maturity are cash rich, financially oriented, with a focus on low risk

endeavours. Finally, firms in decline have limited investment opportunities and are largely

incapable of generating sufficient resources. As each lifecycle stage faces different

challenges, management decisions must be adjusted to take into account these differences.

Corporate finance theory, on the other hand, argues that states of financial distress, default

and bankruptcy present a fundamental stage in the lifecycle of firms (Wruck, 1990). The

survival of a firm is therefore not only dependent on its ability to remain profitable, to

maximise shareholder wealth and to avoid financial distress but also on its ability to make

decisions which take into consideration its stage in the lifecycle. As financial distress is a pre-

curser to bankruptcy, it needs to be addressed immediately and effectively. A firm’s ability to

take responsive action when it is in financial distress is a crucial factor in its recovery.

In this paper, the following question is addressed: How do firms in different lifecycle stages

approach corporate restructuring when faced with financial distress? It is expected that firms

experience financial distress before bankruptcy is filed. With the extreme nature and high

costs of bankruptcy, the implementation of correct restructuring strategies is an important

consideration for the firm and its shareholders. Since bankruptcy as a strategy is found to be

limited in its likelihood of success, it is imperative that preventative measures are taken when

managers recognise that the firm is in distress before the need to resort to bankruptcy.

Furthermore, bankruptcy is found to be costly both directly and indirectly and should be

avoided whenever possible (Moulton & Thomas 1993). Therefore, the importance of

restructuring strategies in a firm’s recovery from distress forms the motivation for this paper.

3

While it is clear that firms in each lifecycle stage exhibit different characteristics, there is

limited evidence on how these differences affect the choice of restructuring strategies. We

expect that these distinct lifecycle characteristics will influence management decisions when

firms recognise financial distress. These differences impact management decisions when

faced with distress as well as limit the restructuring options available. In particular, an

examination into how the lifecycle characteristics of birth, growth, maturity, and decline

stages affect managerial, operational and asset, and financial restructurings will be conducted.

Due to the lifecycle stage of a firm, certain restructuring strategies may not be available or

appropriate.

Using a sample of US firms, we find evidence to support lifecycle theory. When in distress, a

firm’s access to various types of restructuring strategies is limited by the lifecycle stage it is

in. Compared to birth firms, mature firms in distress are more likely to replace their

incompetent managers. Distress firms further on in the lifecycle hierarchy are also found to

be more likely to engage in operational and asset restructuring strategies relative to birth

firms. Growth, mature and decline firms are more likely to reduce dividend payments to

preserve investments and resources due to increased creditor pressure. Consistent with the

pecking order hypothesis, distress firms will raise external funding through the issuance of

common shares. We also found that none of the restructuring strategies we examined help the

firms to turn around within two years after distress. Therefore, even for those who have

access to the chosen restructuring strategy, there is no guarantee of recovery from distress.

The remainder of this paper is organised as follows. In Section 2 discusses past studies on the

lifecycle theory, financial distress and corporate turnaround strategies. In Section 3, we

present our hypotheses. In Section 4, we describe our data and sample selections. We present

our findings in Section 5 and our conclusions are presented in the final section.

4

2.0 Literature Review

2.1 Life Cycle Theory

Life cycle theory suggests that appropriate growth and capital capacity strategies depend on

the firm’s life cycle stage (Anthony and Ramesh, 1992). This life cycle stage may be viewed

as consisting essentially four main stages namely: (1) birth, (2) growth, (3) maturity, and (4)

decline; and each stage exhibits significant differences in terms of situation, organizational

strategy, structure, and decision making style (Miller & Friesen, 1984; Pashley and

Philippatos, 1990; Adizes, 2004). As a firm matures, its characteristics, business goals,

strengths and limitations will change reflecting the progression through the phases of

lifecycle theory. Firms tend to become bigger and more complex in organisational structure,

concentration of ownership becomes more dispersed and integration generally increases.

Strategic decision-making and their effectiveness will also differ depending on the lifecycle

of the firm. Mature and declining firms are less likely to take on innovative, risk-taking

strategies in comparison to firms in birth and growth. Theitart & Vivas (1984) suggest that

key factors affecting performance1 of each lifecycle stage differs. Marketing and product

differentiation are vital for the growth stage while mature firms depend on low cost

production and process efficiency. During decline, firms focus on controlling costs,

simplifying the production line, raising price, and cutting R&D expenses.

Birth

According to Miller & Friesen (1984), firms in the birth stage are small, dominated by their

owners (entrepreneurs), simple, informal in structure, undifferentiated, with highly

centralized power systems and considerable focus on innovation. Young firms face greater

uncertainty over future growth which results in higher book-to-market ratios and greater firm

specific risk (Pastor & Veronesi, 2003; Lubos & Peitro, 2003). These firms are in the initial

stages of operations and are struggling to remain viable amongst competition with older more

established firms. An entrepreneurial focus with a risk taking strategic approach usually

characterises the birth stage. The market therefore considers them riskier enterprises with

uncertain future cash flows and values them accordingly. For this reason, Quinn and

Cameron (1983) who categorize the four groups by their core strategy or decision making

style, label their birth stage as the “Creativity & Entrepreneurship” phase.

1 Performance as measured by % change in market share and cash-flow/revenue

5

Growth

Growth stage firms are medium sized organisations achieving rapid growth and multiple

shareholders. They are larger than birth firms and will begin to acquire subsidiaries in similar

industries. This is due to the fact that these firms would have experienced some initial success

and will be attempting to establish itself in the market by broadening the product market

scope into closely related areas. Mueller (1972) suggests that the typical growing corporation

will continue to decentralise its decision making structure with a downward shifting of

authority. As a result, managers will be delegated more decision making responsibility and

the separation of ownership and control will begin to emerge (Miller & Friesen 1984).

However, although a more team based management approach is taken, power remains quite

centralized at the upper levels of the organisation. Growth firms are also becoming more

formalised in structure and procedure with moderate levels of differentiation. Thietart &

Vivas (1984) argue that the ‘leadership’ strategy is adopted at the growth phase. An emphasis

will be placed on achieving rapid sales growth, amassing resources for economies of scale,

and broadening of operations to promote further growth. Quinn & Cameron (1983) name this

stage “Collectivity” for the emerging sense of a collective mission.

Maturity

Mature firms will have an even more dispersed ownership structure, be less innovative, have

formal bureaucratic systems, and slower or zero growth as sales become stabilised. Mueller

(1972) argues that internal fund flows will eventually outpace investment opportunities and

cost of capital will decrease as uncertainty is reduced. Markets will consider these firms to be

less risky as cash flows are stable and market position is established. Any investment

endeavours will be supported by existing operations. Firms in this stage will be very large in

size, have divisional organisational structure with high differentiation and sophisticated

systems. These formal structures are necessary to cope with the diverse needs of complex

business operations as well as heterogeneous markets. Mature firms face a competitive

environment and are usually conservative in their strategies. These firms will be enjoying a

size advantage over competitors and will be focused on efficiency rather than on innovation.

The main aim of firms in this stage is the smooth functioning of the business in a well-

defined market (Miller & Friesen 1984). For this reason, Thietart & Vivas (1984) argue that

mature firms pursue a ‘niche’ strategy. The increase in structure and emphasis on

formalisation lead Quinn & Cameron (1983) to name this stage “formalization and control”

6

where procedures and policies are institutionalized, goals are formalized, and flexibility is

reduced.

Decline

Finally as the name suggests, firms in decline are encroaching stagnation and suffer from low

profitability (Miller & Friesen 1984). Markets shrink, demand drops, and lack of innovation

lead to ever declining sales. Firms in this stage often resort to price cutting measures, the

consolidation of product lines, or the liquidation of subsidiaries to remain afloat. These firms

are forced to be risk averse in their strategies as they cannot sustain potential losses. The

dominant approach pursued by declining firms is a ‘harvest’ strategy where the main aim is

the collection of as much funds from existing operations as possible (Thietart & Vivas, 1984).

2.2 Financial Distress and Corporate Turnaround Strategies

Financial distress refers to a condition whereby a business or company cannot pay the owed

amounts on the due date. Chen, Weston, & Altman’s (1995) definition of distress is if a

firm’s liquidation of total assets is less than the total value of creditor claims. If prolonged,

this situation can lead to forced liquidation or bankruptcy. For this reason financial distress is

often referred to as the likelihood of bankruptcy which is found to be dependent on the

availability of liquidity and credit (Hendel, 1996).

Whitaker (1999) categorizes financial distress into categories. Distress due to poor

management (firm specific distress) and distress as a result of economic decline (common

factors). The argument is that if distress is the result of poor management, then the actions of

management in restructuring will be a more significant determinant of successful recovery.

Jensen (1989) argues that financial distress will trigger corrective action from management

which improves firm performance. Whitaker (1999) finds support for Jensen’s hypothesis and

argues that early financial distress will motivate managers to increase efficiency. Therefore

distress is actually beneficial to overall firm performance as it stimulates poorly managed

firms to improve. Based on Jenson and Whitaker, firms engaging in distress motivated

restructuring should show signs of performance improvement.

When a firm recognises that it is in danger of financial distress, it is vital that it responds

immediately by taking corrective measures to enhance efficiency and control costs. Lohrke,

Beheian, & Palmer (2004) for example, emphasise the importance of top management teams

7

during restructuring. They argue that a major determinant of successful turnaround is the

ability of management to select the appropriate strategy for recovery. However, restructuring

decisions are influenced not only by management teams and shareholders but also by

creditors who are found to exert significant power over financially distressed firms (Brown,

James & Mooradian, 1992 & 1994). When a firm is in distress, restructurings are usually met

with positive stock reactions2 which is a sign that they are considered to be necessary for the

firm to remain viable (Denis & Kruse, 2000).

When in financial distress, the affected firm usually faces a shortage of cash flows. In order

to generate liquid funds and decrease outflows, such firm can resort to cash reserves, reduce

inventory levels, extend trade credits, draw upon bank lines of credit, restructure debt

payments, raise equity, and sell assets (Whitaker, 1999).

Gibbs (1993) looks at the determinants of corporate restructuring and categorizes his findings

into two broad categories of theory; free cash flow and corporate governance. The free cash

flow hypothesis developed by Jensen (1986) proposes that management in firms with free

cash flow will be more likely to over-invest and over-diversify. These agency costs will

increase the likelihood of takeover treats which will lead to forced restructuring. Free cash

flow variables reflect the choice between retained and distributed earnings, investment

opportunities, operating cash flow, financial leverage, and diversification.

Corporate governance looks at the board of directors, management compensation,

concentration of equity ownership, and the managerial labour market. The argument is that

these factors will affect restructuring3 through their relevance to the level of monitoring and

limits to the discretionary power of managers. The argument is that the greater the proportion

of outside directors, the more effective the board will be in monitoring the actions of

managers and limiting agency costs (Gibbs, 1993). To summarise his results, Gibbs finds that

investment opportunity is negatively related to restructuring whilst financial leverage has a

positive relationship to restructuring. The positive relationship between investment

opportunity and restructuring is consistent with the free cash flow hypothesis. The

explanation provided is that decreasing investment potential leads to a higher risk of takeover

2 Average abnormal return of 0.59% over the two-day announcement period significant at the 10% level

3 Gibbs (1993) examines financial and portfolio restructuring. Financial restructuring refers to debt

recapitalization and portfolio restructuring refers to refocusing on the core business of the firm through

divestment and horizontal integration.

8

threats which results in a greater likelihood of takeover based restructuring. However, Gibbs

also finds that leverage has a positive relationship to restructuring which is inconsistent with

the free cash flow theory. According to the theory, firms with high levels of leverage limit the

ability of managers to over-invest and engage in self-serving behaviour. These firms are

restricted by their debt repayments as these obligations have to be met regularly. Thus, they

are prevented from engaging in overinvestment as free cash is low (Jensen, 1986). Broadly,

the determinants examined by Gibbs (1993) reflect the level of agency costs or the manager-

stockholder conflict, the investment opportunities available, and the level of leverage within

the firm. Lifecycle stages are expected to differ in both cash flow and corporate governance

which according to the findings of Gibbs should in turn affect restructuring.

Barket & Duhaime (1997) classify restructuring strategies into those that are strategic and

those that are operational. Operational restructuring refers to increasing efficiency and

productivity through cost cutting measures. Strategic restructuring is necessary when the

firm’s position relative to competitors is weak. In these cases, the managers need to focus on

changing the strategy, structure, and ideology to better adapt to a changing environment.

John, Lang, & Netter (1992) review annual reports and analyst reports and classify responses

to negative earnings into five groups: (1) Contraction policies, (2) Expansion policies, (3)

Change in market or pricing, (4) Change in production methods or management structure,

and (5) Other responses.4 They find that contraction policies such as sales, divestitures,

spinoffs, debt reductions, and plant shut downs are the most dominant form of restructuring.

Similarly, Chan, Weston & Altman (1995) find that the majority of restructuring takes on the

form of divestitures rather than investment. However, looking in the long run, there is some

weak evidence that sales and assets increased from restructuring decisions. Bowman & Singh

(1993) review the literature on corporate restructuring and develop a classification of

restructuring into three main groups. These are; portfolio restructuring, organisational

restructuring, and financial restructuring. Sudarsanam & Lai (2001) expand on this

classification to encompass: managerial, operational, asset, and financial restructuring.

4 The two main categories of interest for this paper are contraction and expansion policies. Contraction policies

refer to strategies which cut down the size of the firm through divestitures and the control of expenditure. In

times of financial distress it is often not viable for a firm to continue investing funds into all lines of business.

These unprofitable or costly branches of operations can be sold off to generate much needed funds which then

can be used to repay debt. Expansion policies increase the size of the firm by increasing investments, assets,

operations, or resources. These strategies look to pull themselves out of financial distress through synergistic

cost benefits and economies of scale.

9

Managerial Restructuring

Changes in top management are argued to be one of the main conditions for successful

turnarounds as they are a tangible signal to creditors that action is being taken by the

distressed firm (Hofer 1980). Incompetent managers may have been the cause of financial

distress through poor planning or inefficient decision making. Whitaker (1999) refers this as

firm-specific distress. These managers need to be replaced with management teams who can

accurately assess the source of distress and implement strategies necessary for successful

turnaround (Lohrke, Beheian, & Palmer 2004). Pearce & Robbins (1993) also stress the

importance of management in turning distressed firms around. They argue that a management

team lacking in the skills needed to respond efficiently and in a timely manner will result in

continued decline and the eventual failure of the company. Sudarsanam and Lai (2001)

suggest that creditors will only provide continued financial support if they are reassured that

management will be able to cope with distress. Denis & Kruse (2000) find that 36% of the

sample firms they study experience managerial turnover in top executives following

performance declines. Managerial restructuring includes replacement of senior management

and/or the Chief Executive Officer. Overall, managerial restructuring may be a crucial factor

in the turnaround process of a distressed firm.

Operational Restructuring

Operational restructuring refers to the efficiency/operating turnaround stage. This stage aims

to restore profitability by controlling costs and reducing overheads through the sale of surplus

fixed resources such as land, equipment, and offices. By decreasing input and maximising

output firms can generate cash flow (at least in the short term) and enhance efficiency. When

firms recognise distress, operational restructuring is usually the first strategy implemented.

However, although necessary, operational restructuring is primarily a short term fix used to

generate cash flow quickly. Sudarsanam & Lai (2001) argue that if used as a stand-alone

strategy, it may not be enough for recovery from distress. Past literature suggests that

operational restructuring in the form of purchases are less likely than sales. Nevertheless, if

productivity can be significantly improved, distressed firms may build new plants or invest in

more advanced technology and equipment.

Asset Restructuring

When a distressed firm sells off lines of businesses which are unprofitable or not at the core

operations of the company, it is considered to be engaging in asset restructuring. The aim of

10

this form of restructuring is to realign the focus of the firm by reducing unrelated

diversification and refocusing the business portfolio around core competencies (Shleifer &

Vishnny, 1992). Chang (1996) finds that poorly performing firms will be motivated to divest

lines of business which do not generate competitive advantages. Asset restructuring allows

the firm to re-evaluate its operations and reorganise business units into more efficient groups.

This form of restructuring is especially necessary if agency costs have resulted in over-

diversification by management. By selling underperforming businesses, resources can be

redeployed towards better uses so that asset restructuring is generally considered to be value

adding (Atanassov & Kim, 2009). Asset sales are limited by industry wide factors as highly

leveraged industries are less prone to sell assets. However, this form of restructuring is found

to play an important role for distressed firms as it both provides a source of funds and acts as

a mechanism for creditors to obtain control over assets (Brown, James & Mooradian, 1994).

Divestment of subsidiaries and divisions is argued to be the most common turnaround

strategy used by all but the smallest of firms as these firms are less likely to have subsidiaries

and non-essential business operations which they can afford to sell off (Sudarsanam & Lai,

2001).

Although contraction policies have been found to be the dominant form of restructuring

(John, Lang, & Netter 1992), asset restructuring could also refer to actions which increase the

size of the firm such as investments, strategic alliances, joint ventures, and licensing

agreements (Sudarsanam & Lai 2001). For example, acquisition of related businesses that fit

core competencies could help to increase the competitive advantage of distressed firms

through economies of scale. These restructuring strategies are risky however as they require

capital expenditure from firms already experiencing low cash flows. Since smaller firms will

generally have lower cash reserves, this form of restructuring may not be appropriate or

possible.

Financial Restructuring

Financial restructuring generally refers to changes in the firm’s capital structure in terms of

leverage. This seeks to reduce payment pressures through equity-based and debt-based

strategies. Where equity-based strategies may involve dividend cuts or issuance of shares as a

means to retain or generate funds, debt-based strategies involve the adjustment of interest,

maturity, or debt/equity ratio. DeAngelo & DeAngelo (1990) find that large firms are likely

to respond to distress with rapid and aggressive dividend reductions. Funds retained are then

11

able to be used to pay debt obligations. Share issues are another way in which distressed

firms can generate funds to support continued operations.

2.3 Restructuring Effectiveness

Past research have also examined factors which affect the success of completing certain

restructuring strategies. Moulton & Thomas (1993) find that firm size dominates all other

variables in predicting successful completion of the reorganization process. Large firms with

varied assets are more likely to successfully restructure as they are better able to survive

substantial losses, have more businesses to serve as the core, and have sufficient assets which

can be sold to provide cash for continued operations. Rate of decline or severity of financial

distress as measured by the number of years in which the firm had negative net income

during the six years prior to bankruptcy is also found to be a significant determinant of

restructuring success (Whitaker, 1999). Sudarsanam & Lai (2001) study a sample of

potentially bankrupt UK firms and find that recovery firms have more focus on growth and

external market strategies whereas non-recovery firms engage in fire-fighting actions. Using

logit and linear regressions, they find that recovered firms are more likely to engage in

investments and acquisitions in their restructuring decisions. This suggests that firms that

recover from distress are more expansionary, forward looking, and have an external market

focus. Non-recovered firms are found to be more internally focused and engage in short term

fire-fighting techniques of operational and financial restructuring. Barker and Duhaime

(1997) also argue that successful turnaround depends on the firm’s ability to change its

strategy, structure, and ideology rather than restructuring based on short term efficiency or

cost cutting tactics. They find that effective restructuring results from shifting the strategic

change to better suit the needs of the market and the competitive environment in which a firm

operates. Cost-cutting and layoffs are also found to be ineffectual strategies by Denis &

Kruse (2000) who find that improvements in operating performance are mostly attributable to

asset restructuring.

3.0 Hypotheses Development

As firms in the birth stage have highly centralised power structures (Miller & Friesen 1984),

it is more likely that the managers are also the owners. This suggests that there will be less

external pressure for a change in management when the firms are in distress and therefore

firms in the birth stage are less likely to engage in managerial restructuring. We would also

12

expect that birth and growth firms are less likely to have outside blockholders or to be

influenced by external shareholder pressures since there is a close manager-owner

connection. Kang & Shivdasani (1997) find that there exists a positive relationship between

outside blockholders and the probability of top management turnover in Japanese firms.

Bethel & Liebeskind (1993) also find that the prominence of managerial restructuring found

in the U.S. in the late 80’s was due outside pressure by blockholders. Based on these

arguments, the hypothesis is stated as:

H1: Firms in the birth stage are less likely to use managerial restructuring compared to firms

in growth, maturity, and decline stages.

Similarly, younger firms also engage in low levels of operational or asset restructuring due to

the limited range of product lines available to them. It has been argued that the greater the

diversification and the larger the size of a firm, the greater the capacity for change during the

turnaround process (Barker & Duhaime 1997). Furthermore, Brown, James, & Mooradian

(1994) argue that shareholders of distressed firms have little incentive to sell assets. It is up to

creditors to apply pressure on management to sell assets and generate funds so that debt

repayments can be made. Kang & Shivdasani (1997) examined Japanese firms and find

similar results where the probability of asset contractions increases with equity ownership by

a firm’s main bank. As was previously argued, younger firms have higher costs of debt

financing and would therefore be less likely to be subject to strong creditor pressure to sell

off investments.

Bowman & Singh (1993) argue that an increased equity stake of managers and board

members are negatively associated with portfolio restructuring. Their definition of portfolio

restructuring corresponds to asset restructuring in that it refers to significant changes in the

line of business through acquisition and divestiture. This suggests that younger firms with

more centralized ownership structures would engage in less portfolio/asset restructuring

given that the equity stake of managers is closely linked to that of owners. Birth and growth

firms are also more focused on business expansion. It is therefore likely that they would

attempt to seek other restructuring options during distress in order to maintain future growth

potential in the form of investments.

13

Since mature firms are more likely to have higher debt capacities and therefore more

creditors, asset restructuring should increase as a firm matures. This is confirmed by papers

which find that firms with greater amounts of debt are more likely to sell assets to repay debt

(Brown, James & Mooradian 1992), and those with close ties to outside banks and larger

blockholders engage in more asset sales (Kang & Shivdasani 1997).

Corresponding to the above arguments, Sudarsanam & Lai (2001) find that acquisition and

divestment (asset restructuring) is perhaps the most common turnaround strategy employed

by all but the smallest of firms. They argue that asset restructuring is especially important in

turnaround for firms in mature or declining product/markets. As we generally expect firm

size to increase with age, the hypothesis is stated as follows:

H2: Firms in the birth stage are less likely to use asset restructuring compared to firms in

growth, maturity, and decline stages.

During distress, firms in the birth stage will have less capacity for managerial, asset and

financial restructuring relative to firms in growth, maturity, and decline. This is due to the

highly centralized power structure, limited availability of non-core investments, and a high

cost of capital. These factors will force young firms to engage in high levels of operational

restructuring such as the sale of property, plant, and equipment to pull themselves out of

distress.

H3: Firms in the birth stage are more likely to use operational restructuring strategies

compared to firms in the growth, mature and decline stages.

In terms of financial restructuring, older and more established firms may be able to negotiate

debt restructuring more effectively than younger firms (Sudarsanam & Lai 2001). Younger

firms face greater uncertainties surrounding new ideas and products (Mueller 1972) which

results in greater difficulties in raising outside funds. This leads to young firms being subject

to higher costs of capital. Banks are also more likely to loosen financial constraints when

borrowing firms have collateral (Asquith, Gertner & Scharfstein 1994) which would be more

likely for mature firms who have good credit histories and a greater availability of capital.

Young firms are also less liquid and have smaller debt capacities relative to more mature

14

firms. This is confirmed by Bulan & Yan (2009) who find that on average, firms in the mature

stage of the lifecycle are older, larger, more profitable, and have higher leverage.

H4: Firms in the birth stage are less likely to use debt based financial restructuring

strategies compared to firms in the growth, maturity, and decline stages

With equity, dividend payout ratios are also dependent on a firm’s lifecycle stage. Mueller

(1972) argues that during the early stage of rapid growth, stockholders will want all of the

capital consumption allowances reinvested. This suggests that young firms will be paying

fewer dividends as funds will be allocated towards generating further expansion. When

growth potential declines, an ever increasing share of profits will go towards dividends.

DeAngelo & DeAngelo (1990) find that large firms respond to financial distress with rapid

and aggressive dividend reductions due to liquidity constraints.

H5: Firms in the birth stage are less likely to use equity based financial restructuring

strategies compared to firms in the growth, maturity, and decline stages.

4.0 Data

We investigate the implications of lifecycle theory of the firm on its choice of restructuring

strategies when faced with distress. In particular, our sample firms are constructed from U.S.

firm data available on CRSP and COMPUSTAT between 1995 and 2006. Our sample does

not include firms from the utilities and financials industries since these industries operate in a

more controlled environment and are distinct to firms in other industries. First, we classify

our firms into their lifecycle stages. Next, we identify firms that are financially distressed and

those that are not. Finally, we use a series of proxies to determine which restructuring

strategies are used by our sample firms.

Identification of lifecycle

First, we adopt Anthony and Ramesh’s (1992) method of classifying firms into the four

lifecycle classifications: birth, growth, maturity and decline. As a firm matures, growth will

slow down as sales stabilize and market saturation occurs. It makes sense that a firm will

maximise growth early in its lifecycle in order to create competitive advantages, acquire

market share, and build capacity (Anthony & Ramesh, 1992). Porter (1980) states that mature

firms will find investments less rewarding (relative to younger firms) which leads to

15

declining market growth. If investment opportunities decrease, capital expenditure will also

fall. More established firms will invest less into business operations and consequently more

will be paid out to shareholders as dividends. Dividend payouts will therefore increase as

firms grow older. Therefore, using univariate and multivariate ranking procedures, Anthony

and Ramesh classify firms into the four lifecycle categories based on the following four

lifecycle descriptors: annual dividends, scaled by income; percentage of sales growth; capital

expenditure as a proportion of firm value and age of firm.

1. Annual dividend as a percentage of income (DP)

��� � � �������� �100

2. Percent sales growth (SG)

��� � � �������� �100

3. Capital expenditure as a percentage of total value of the firm (CEV)

��� � � ������� �100

4. Age of the firm (AGE)

Where:

DIV t = common dividends in year t

IBED t = income before extraordinary items and discontinued operations in year t

SALES t = net sales in year t

CE t = capital expenditure in year t

VALUE t = market value of equity plus book value debt at year t

AGE t = number of years information is available for the firm on CRSP/Compustat

Industries differ in their dividend payment, sales growth, capital expenditure and age. We

control for the industry effect when grouping our firms into the four lifecycle categories. We

first calculate the four lifecycle descriptors for each year for each sample firm. Then for each

firm-year, median values of the descriptors (denoted MDP, MSG, MCEV, MAGE) are

16

computed using five years’ data (i.e., current year and prior four years). Next, using the

Fama-French 49 industry grouping, we split the median values of the descriptors (for each of

the industry) into quartiles and group the firms into the four lifecycle categories. Once a firm

year is assigned to a category, it is given a score (median values less than Q1 =1, median

values between Q1 and less than Q2 =2, median values between Q2 and less than Q3 =3 and

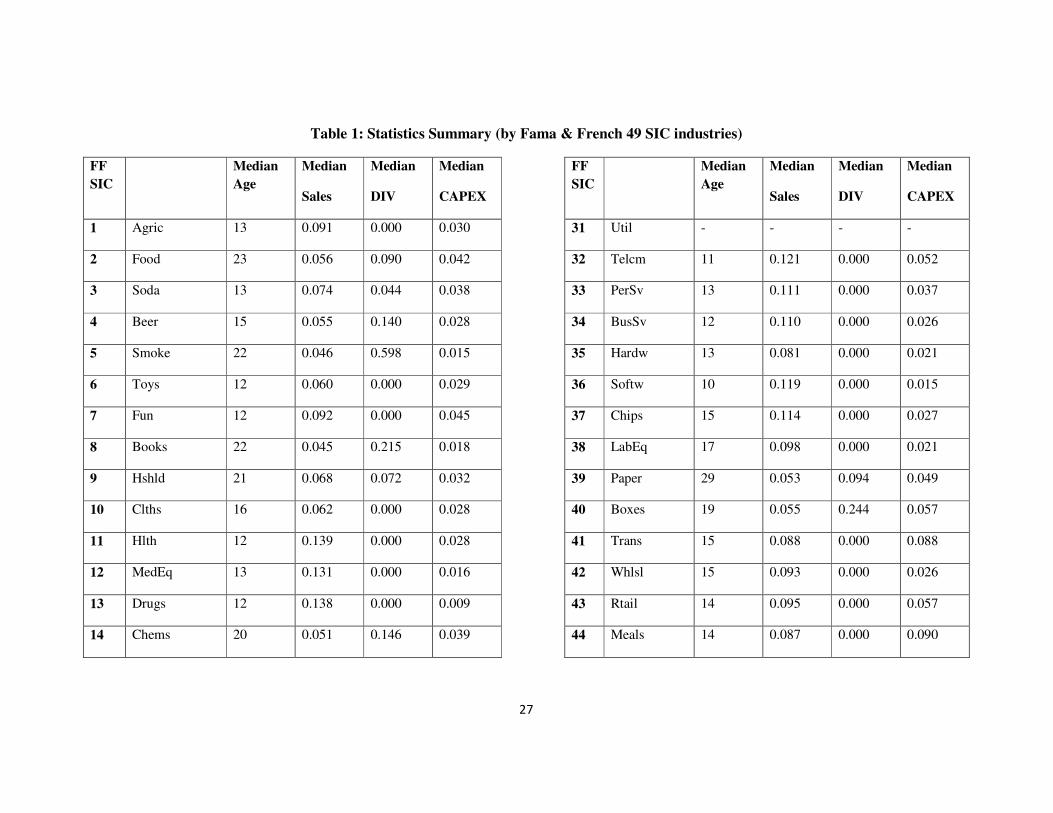

median values equal to Q3 and above =4). Table 1 presents the statistics summary for the

median values by Fama & French 49 SIC industries grouping.

[TABLE 1 ABOUT HERE]

We then sum up the scores for each firm year and further split all observations into quartiles

again. Firms are then finally categorised into the four lifecycle classifications: birth, growth,

maturity and decline, based on the cut-off values of the quartiles.

Identification of distress

Asquith, Gertner and Scharfstein (1994) argue that a firm is classified as being in distress if

in any two consecutive years, the firm’s earnings before interest, taxes, depreciation and

amortization (EBITDA) is less than its reported expense. Sudarsanam and Lai (2001) use

Taffler’s Z-score and adopt a positive, positive, negative approach to classify a firm being in

distress. They define a financially distress firm as one which has positive Z-scores in the two

previous years and a negative Z-score in the current year. Combining the two approaches, we

classify a firm to be financially distressed when it has two consecutive years of negative

EBITDA after a year of positive EBITDA. For example, firms classified as in distress in

1995 (the commencement of our sample period) have a positive EBITDA in 1993 and

negative EBITDAs in 1994 and 1995. Those firms that have positive EBITDA for all three

years (i.e., 1993 to 1995) are labelled as non-distress firms in 1995. Table 2 presents the

breakdown of the number of distress firms and non-distress firms by the four lifecycle

categories.

[TABLE 2 ABOUT HERE]

17

Figure 1 also shows the dispersion of distress firms across the sample period. An inspection

of Figure 1 shows that there was a sharp increase in distress firms over three general cycles:

the 1997/1998 Asian finacial crisis, the 2001/2002 tech-stock crash and the pre-2007/2008

Global Financial Crisis.

[FIGURE 1 ABOUT HERE]

Managerial Restructuring

We define a firm as engaging in managerial restructuring if it has replaced one of its top tier

management, being the Chief Executive Officer (CEO) or Managing Director (MD). We

obtained information on CEO or MD replacement from the S&P Executive Compensation

database. Similar to Atanassov and Kim (2009), managerial restructuring is taken to have

occurred if a CEO or MD changes during the distress period (i.e., year t). The reason for

leaving and age of the management is also examined to ensure that none of the replacements

are due to death, illness, or retirement.

Restructuring strategies: Operational /Asset

Operational and asset restructuring is generally the first broad strategy undertaken by firms.

We look at a number of operational and asset restructuring strategies including reducing

investments, reducing cost of goods sold, laying off employees and selling off assets.

Similar to Kang and Shivdasani (1997), a strategy to reduce investments (sell off assets) is

deemed to be taken by a firm if its investing activities - proxied by COMPUSTAT item

IVNCF (total (net) property, plant and equipment) falls more than 15% between year t-1 and

year t or year t+1, where t is the observed firm year; for distress firms, year t is also their year

of distress. For the strategy of reducing cost of goods sold, we follow Atanassov and Kim

(2009) where this strategy is implemented if its Cost of Goods Sold (scaled by Sales) is

initially above the industry median in year t-1 and falls to the bottom quartile of its industry’s

median in year t or year t+1. A firm is deemed to have undertaken the strategy of laying off

its employees if it has a more than 20% drop in the number of employees between year t-1

and year t or t+1 (Denis & Kruse, 2000).

18

Restructuring strategies: Financial

Financial restructuring typically includes cutting or omitting dividends, issuing new security

and exchanging debt for equity. Following Chen and Zhang (1998), a firm is deemed to have

undertaken the strategy to cut or omit dividends if it experiences more than a 25% drop in its

total dividends paid between year t-1 and year t or t+1. We define a firm to have issued

equity (debt) when the firm’s net equity (net debt) exceeds 5% of the book value of its total

asset at year t (Hovakimian, Hovakimian and Tehranian, 2004)

Table 3 describes the definition of the variables discussed above.

[TABLE 3 ABOUT HERE]

5.0 Analyses and Findings

Lifecycle theory, distress firms and restructuring strategies

We first examine if firms in the birth stage are less likely to use managerial restructuring

compared to firms in growth, maturity, and decline stages by running a logistic regression

where the dependent variable takes on the value of one if the CEO/MD has left the company

and zero otherwise.

iit

itititit

ititititit

nalInstitutio

etsLnTotalAssTobinsQFDDECLINEFDMATURE

FDGROWTHDECLINEMATUREGROWTHCEO

εα

αααα

ααααα

++

++++

++++=

10

9876

54321

**

*

Eqn (1)

GROWTH, MATURE and DECLINE are the lifecycle dummies that take the value 1 for the

respective lifecycle stages and zero otherwise. FD is the dummy for distress firm and takes

the value of 1 if a firm is distress and zero otherwise. We have also added three control

variables namely: TobinsQ (to control for the growth opportunities), LnTotalAssets (to

control for the firm size) and Institutional (to control for the institutional ownership in the

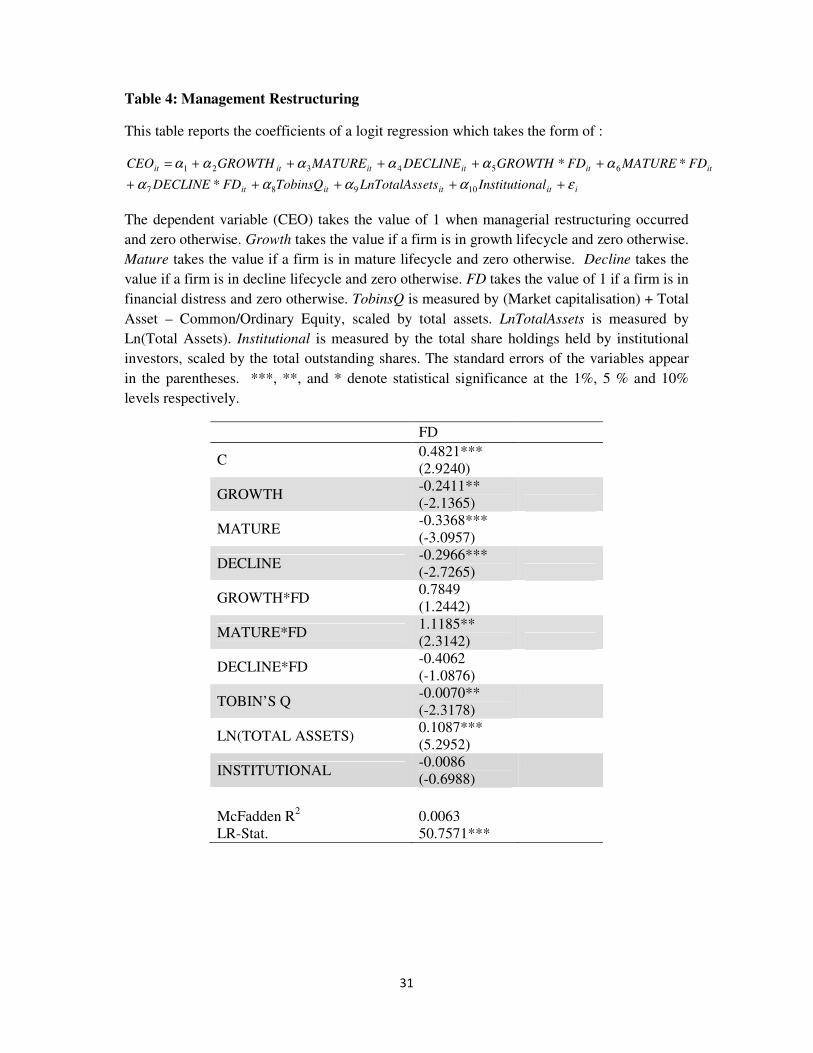

firm). Table 4 presents the results.

[TABLE 4 ABOUT HERE]

19

Since our research question seeks to answer if there is a systematic difference in the choice of

restructuring strategies undertaken by distress firms when they are in different lifecycle

stages, we focus our discussion on the interaction between lifecycle stage and distress. These

dummies allow us to separate the restructuring which occurs due to financial distress from the

normal strategies. In Table 4, we find that the FDMATURE* coefficient is 1.1185

(statistically significant at the 5% level). This is consistent with lifecycle theory. When

compared to firms in the birth stage, mature firms have more complex business operations.

Incompetent managers need to be replaced with others who can accurately assess the source

of distress and implement strategies necessary for a successful turnaround. The coefficients

of 0.7849 and -0.4062 for the growth and decline firms respectively are not statistically

significant. This suggests that there is no difference in the use of managerial restructuring

strategies between these two groups and the birth firms. Growth firms are likely to be still

dominated by the same top management/CEO since the birth stage, whereas it may be too late

to use such restructuring strategy for decline firms as it may be very difficult to employ new

management/CEO since the firms are close to filing bankruptcy.

We next examine if firms in the birth stage are less likely to use operational/asset

restructuring strategies compared to firms in growth, maturity, and decline stages by running

the following logistic regression:

iitit

itititit

itititit

nalInstitutioetsLnTotalAss

TobinsQFDDECLINEFDMATUREFDGROWTH

DECLINEMATUREGROWTHgstructurin

εαα

αααα

αααα

+++

++++

+++=

109

8765

4321

***

Re

Eqn (2)

We run the regression in Equation 2 four separate times, each time replacing the dependent

variable for the various operational/asset restructuring strategies: (1) reducing in investing

activities (INV), (2) reducing cost of goods sold (COGS), (3) laying off employees (EMP) and

(4) asset sales (ASSETS). Table 5 reports the findings.

[TABLE 5 ABOUT HERE]

Birth firms and growth firms are expected to have accumulated less resources than mature

and decline firms in the course of business. This is because these firms (birth and growth)

will be still pursuing a growth based strategy focused on expansion. It is therefore likely that

20

they will attempt to use other restructuring options during distress in order to maintain future

growth potential in the form of investments than engaging in operational or asset

restructuring. Furthermore, since birth and growth firms are more focused on business

expansion, they will have the least amount of non-essential property, plant, and equipment

with which they can sell or the less number of employees to lay off, even if they are in

distress. When we examine the regression result for firms to engage in operational/asset

restructuring strategies, all (except one) columns of Table 5 show that distress firms higher in

the lifecycle hierarchy are more likely to engage in operational/asset restructuring strategies

relative to birth firms; the coefficients ranging between 0.7361 and 1.5673 are all statistically

significant at the 1% level.

Financial restructuring typically includes issuing new securities, cutting/omitting dividends

and exchanging debt for equity. We examine if firms in the birth stage are less likely to use

financial restructuring strategies compared to firms in growth, maturity, and decline stages by

running the following logistic regression:

iitit

itititit

itititit

nalInstitutioetsLnTotalAss

TobinsQFDDECLINEFDMATUREFDGROWTH

DECLINEMATUREGROWTHgstructurin

εαα

αααα

αααα

+++

++++

+++=

109

8765

4321

***

Re

Eqn (3)

We run the regression in Equation 3 for three separate dependent variables: reduction of

dividend (DIV), issuing of debt (NetDebt) and issuing of equity (NetEquity). Table 6 presents

the results for the financial restructuring.

[TABLE 6 ABOUT HERE]

When examining Column 1 in Table 6, we find that compared to the distress birth firms, the

rest of the firms are more likely to engage in a reduction in dividends; the coefficients of

1.2456, 1.7517 and 1.4345 are all statistically significant at 1% level for the distress growth,

mature and decline firms. Distress growth and mature firms are more likely to reduce

dividend payments in order to preserve investments and resources so that future expansion is

not stymied. Decline firms in distress may be forced to decrease dividends due to increasing

21

creditor pressure. Comparing the above findings to the individual lifecycle dummies, in the

normal course of business, firms of all lifecycles are unlikely to engage in dividend cuts;

coefficients of -0.2512, -0.6244 and -0.7627 for growth, mature and decline respectively are

all statistically significant at 1% level. Dividend policies are often sticky. Firms will avoid

cutting or omitting dividends as this could give a wrong signal to the market that the firms are

performing poorly. However, when distress sets in, these firms will be forced to cut

dividends.

When firms are in distress, capital can be raised through the issuance of common shares. In

the Column 3 of Table 6, we find that all growth, mature and decline firms are more likely to

raise equity when in distress. In contrast, we find that they are less likely to raise external

funding using debt when in distress. The coefficients are between -0.5006 and 2.0717 and are

all statistically significant at 1% and 5% levels. This is consistent with the pecking order

hypothesis where firms will resort to raising external funds through issuance of equity when

in distress. A possible explanation for distress birth firms not raising new equity (relative to

the other firms) is that they have limited capacity; birth firms are not as well established as

the other firms and investors prefer firms with more established track records. As debt

financing is less transparent compared to equity, it is easier for distress birth firms to engage

in debt financing.

Restructuring Effectiveness

In the preceding section, we report evidence consistent with the lifecycle theory and that

firms are only likely to engage in certain restructuring strategies (depending on which stage

of the lifecycle they are in) when in distress. However, the ability to engage in a strategy does

not necessary mean that the distress firm will be able to turnaround its poor performance.

They may still continue to falter and may eventually find themselves filing for bankruptcy.

For the sample of distress firms only, we examine the success of the restructuring strategies

used. We define a “recovered” firm as one that has at least two consecutive years of positive

EBITDA after being previously classified as in distress. For example, a distress firm in 1995

22

is deemed to have turned around if its EBITDA is positive in 1996 and 1997. We run the

following logistic regression to examine the success of restructuring strategies for distress

firms:

iit

ititit

ititit

nalInstitutio

etsLnTotalAssTobinsQgsstructurinDECLINE

gsstructurinMATUREgsstructurinGROWTHery

εα

ααα

ααα

++

+++

++=

7

654

321

Re*

Re*Re*covRe

Eqn (4)

The dependent variable, Recovery, takes the value 1 if a distress firm recovers from distress

and zero otherwise. The interacted variables, Restructuring, represent the managerial,

operational/asset and financial restructuring strategies, examined in the previous section.

Table 7 presents the effectiveness of the restructuring strategies.

[TABLE 7 ABOUT HERE]

When examining the results in Table 7, we find that none of the restructuring strategies

appear to have any impact. However, we find that distress growth and mature firms that

raised external funds by issuing equities are less likely to recover from distress, relative to the

distress birth firms who used the same strategy; the coefficients for the growth and mature

firms are -1.1145and -1.2313, statistically significant at 5% and 1% respectively. Compared

to the distress growth and mature firms, it is likely birth firms are not as distressed. After all,

birth firms are in their infancy and in the commencement of their business operations. Since

birth firms are more likely to be dominated and managed by their owners, these managers-

owners certainly have more incentives to make sure the firms turn round as they are more

likely to have personal funds in the firms. Finally, we also find a weak evidence to suggest

that mature firms that replaced their incompetent managers are less likely to have a successful

turnaround from their financial distress. Given the complexity of their business operations, it

is unlikely for the new manager to turn the firms around within the short time-span of 2 years.

6.0 Conclusions

When firms suffer from poor operating performance, shareholders may pressure management

to undertake restructuring actions to improve firm performance. Creditors also may demand

23

corrective measures, especially when debt covenants are violated. While the decision on

which corrective measures to be used is decided by the management, management may be

limited in their measures, depending on which lifecycle stage the firm is in.

We examine the implications of the lifecycle theory on how a distress firm chooses its

restructuring strategies. We find evidence that distress firms’ access to different types of

restructuring strategies is limited by the lifecycle stages they are in: there are systematic

differences between firms in different lifecycles when choosing a restructuring strategy.

However, even for those able to implement restructuring strategies, there is no guarantee that

the strategies are successful.

24

References

Adizes, I 2004, Managing Corporate Lifecycles, 2nd edn, Adizes Institute.

Anthony, J & Ramesh, K 1992, 'Association Between Accounting Performance Measures and

Stock Prices: A Test of the Lifecycle Hypothesis', Journal of Accounting and Economics,

15(2-3), 203-227.

Asquith, P, Gertner, R & Scharfstein, D 1994, 'Anatomy of Financial Distress: An

Examination of Junk-Bond Issuers', The Quarterly Journal of Economics, 109 (3), 625-

658.

Atanassov, J & Kim, H 2009, 'Labor and Corporate Governance: International Evidence from

Restructuring Decisions', The Journal of Finance, 64(1), 341-373.

Barker, V & Duhaime, I 1997, 'Strategic Change in the Turnaround Process: Theory and

Empirical Evidence', Strategic Management Journal, 18(1), 13-38.

Bethel, J. E.& Liebeskind, J., The Effects of Ownership Structure on Corporate

Restructuring, Strategic Management Journal, 14, Summer 1993, 15-31.

Bowman, E & Singh, H 1993, 'Corporate Restructuring: Reconfiguring the Firm', Strategic

Management Journal, 14, 5-14.

Brown, D, James, C & Mooradian, R 1992, 'The Information Content of Distressed

Restructurings Involving Public and Private Debt Claims', Journal of Financial

Economics, 33, 93-118.

Brown, D, James, C & Mooradian, R 1994, 'Asset Sales by Financially Distressed Firms',

Journal of Corporate Finance, 1(2), 233-257.

Bulan, L. & Yan, Z., 2009, ‘The pecking order of Financing in the Firm’s Life Cycle’,

Banking and Finance Letters, 1 (3), 129-40.

Chang, SJ 1996, 'Evolutionary Perspective on Diversification and Corporate Restructuring:

Entry, Exit, and Economic Performance During 1981-1989', Strategic Management

Journal, 17 (8), 587-611.

Chen, N. & Zhang, F., 1998, ‘Risk and Return of Value Stocks’, Journal of Business, 71 (4),

501-35

Chen, Y, Weston, F & Altman, E 1995, 'Financial Distress and Restructuring Models',

Financial Management, 24(2), 57-75.

DeAngelo, H & DeAngelo, L 1990, 'Dividend Policy and Financial Distress: An Empirical

Investigation of Troubled NYSE Firms', The Journal of Finance, 45(5), 1415-1431.

25

Denis, D & Kruse, T 2000, 'Managerial Discipline and Corporate Restructuring Following

Performance Declines', Journal of Financial Economics, 55, 391-424.

Gibbs, P 1993, 'Determinants of Corporate Restructuring: The Relative Importance of

Corporate Governance, Takeover Threat, and Free Cash Flow', Strategic Management

Journal, 14(1), 51-68.

Hendel, I 1996, 'Competition Under Financial Distress', The Journal of Industrial Economics,

44(3), 309-324.

Hofer, C 1980, 'Turnaround Strategies', Journal of Business Strategy, 1(1), 19-31.

Hovakimian, A., Hovakimian, G., Tehranian, H., 2004. Determinants Of Target Capital

Structure: The Case Of Dual, Debt And Equity Issues, Journal of Financial Economics, 71

(3), 517-540.

Jensen, M 1986, 'Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers',

American Economic Review, 76, 323-329.

Jensen, M 1989, 'The Eclipse of the Public Corporation', Harvard Business Review, 5, 61-74.

John, K, Lang, L & Netter, J 1992, 'The Voluntary Restructuring of Large firms in Response

to Performance Decline', The Journal of Finance, 47(3), 891-917.

Kang, J-K & Shivdasani, A 1997, 'Corporate Restructuring during Performance Declines in

Japan', Journal of Financial Economics, 102, 510-546.

Lohrke, F, Bedeian, A & Palmer, T 2004, 'The Role of Top Management Teams in

Formulating and Implementing Turnaround Strategies: A Review and Research Agenda',

International Journal of Management Reviews, 5-6 (2), 63-90.

Lubos, P & Peitro, V 2003, 'Stock Valuation and Learning About Profitability', Journal of

Finance, 58, 1749-1989.

Miller, D & Friesen, PH 1984, 'A Longitudinal Study of the Corporate Life Cycle',

Management Science, 30 (10), 1161-1183.

Moulton, W & Thomas, H 1993, 'Bankruptcy as a Deliberate Strategy: Theoretical

Considerations and Empirical Evidence', Strategic Management Journal, 14(2), 125-135.

Mueller, D 1972, 'A Life Cycle Theory of the Firm', The Journal of Industrial Economics,

20(3), 199-219.

Pashley, M & Philippatos, G 1990, 'Voluntary Divestitures and Croporate Life-cycle: Some

Empirical Evidence', Applied Econmics, 22, 1181-1196.

Pastor, L. & P. Veronesi 2003, ‘Stock Valuation and learning about profitability” Journal of

Finance, 58, 1749-89

26

Pearce, J. A. II, & Robbins, D. K. (1993). Toward improved theory and research on business

turnaround. Journal of Management, 19(3), 613–637.

Porter, ME 1980, Competitive Strategy: Techniques for Analysing Industries and

Competitors, Free Press, New York.

Quinn, R & Cameron, K 1983, 'Organizational Lifecycles and Shifting Criteria of

Effectiveness: Some Preliminary Evidence', Management Science, 29 (1), 33-51.

Shleifer, A & Vishny, R 1992, 'Liquidation Values and Debt Capacity: A Market Equilibrium

Approach', Journal of Finance, 47(4), 1343-1366.

Sudarsanam, S & Lai, J 2001, 'Corporate Financial Distress and Turnaround Strategies: An

Empirical Analysis', British Journal of Management, 12, 183-199.

Thietart, R & Vivas, R 1984, 'An Empirical Investigation of Success Strategies for

Businesses Along the Product Life Cycle', Management Science, 30(12), 1405-1423.

Whitaker, R 1999, 'The Early Stages of Financial Distress', Journal of Economics and

Finance, 23(2), 123-133.

Wruck, K 1990, ‘Financial distress, reorganization, and organizational Efficiency’, Journal of

Financial Economics, 27, 419-444.

27

Table 1: Statistics Summary (by Fama & French 49 SIC industries)

FF

SIC

Median

Age

Median

Sales

Median

DIV

Median

CAPEX

FF

SIC

Median

Age

Median

Sales

Median

DIV

Median

CAPEX

1 Agric 13 0.091 0.000 0.030 31 Util - - - -

2 Food 23 0.056 0.090 0.042 32 Telcm 11 0.121 0.000 0.052

3 Soda 13 0.074 0.044 0.038 33 PerSv 13 0.111 0.000 0.037

4 Beer 15 0.055 0.140 0.028 34 BusSv 12 0.110 0.000 0.026

5 Smoke 22 0.046 0.598 0.015 35 Hardw 13 0.081 0.000 0.021

6 Toys 12 0.060 0.000 0.029 36 Softw 10 0.119 0.000 0.015

7 Fun 12 0.092 0.000 0.045 37 Chips 15 0.114 0.000 0.027

8 Books 22 0.045 0.215 0.018 38 LabEq 17 0.098 0.000 0.021

9 Hshld 21 0.068 0.072 0.032 39 Paper 29 0.053 0.094 0.049

10 Clths 16 0.062 0.000 0.028 40 Boxes 19 0.055 0.244 0.057

11 Hlth 12 0.139 0.000 0.028 41 Trans 15 0.088 0.000 0.088

12 MedEq 13 0.131 0.000 0.016 42 Whlsl 15 0.093 0.000 0.026

13 Drugs 12 0.138 0.000 0.009 43 Rtail 14 0.095 0.000 0.057

14 Chems 20 0.051 0.146 0.039 44 Meals 14 0.087 0.000 0.090

28

15 Rubbr 16 0.064 0.000 0.055 45 Banks - - - -

16 Txtls 24 0.025 0.000 0.053 46 Insur - - - -

17 BldMt 28 0.077 0.065 0.045 47 RlEst - - - -

18 Cnstr 18 0.140 0.000 0.017 48 Fin - - - -

19 Steel 17 0.069 0.000 0.058 49 Other 16 0.086 0.000 0.025

20 FabPr 21 0.076 0.000 0.056

21 Mach 18 0.081 0.000 0.030

22 ElcEq 20 0.064 0.000 0.030

23 Autos 19 0.078 0.106 0.055

24 Aero 19 0.078 0.106 0.055

25 Ships 38 0.074 0.044 0.051

26 Guns 17 0.018 0.000 0.024

27 Gold 15 0.038 0.000 0.061

28 Mines 14 0.091 0.135 0.053

29 Coal 11.5 0.053 0.000 0.065

30 Oil 17 0.158 0.000 0.118

29

Table 2: Breakdown of the number of distress firm years and non-distress firms years

by the four lifecycle categories

Distress Firms Non-Distress Firms Total

Birth 157 4190 4347

Growth 328 7660 7988

Mature 387 8559 8946

Decline 263 8770 9032

Total 1134 29179 30313

30

Table 3: Definition of Variables

This table presents the definition of the variables employed in this paper.

Dependent Variables

CEOit = Dummy variable where it is equal to one if the CEO of the firm is replaced

and zero otherwise.

INVit = Dummy variable where it is equal to one if the firm experiences more than

15% decrease in investment activities from year t-1 to year t or t+1 and zero

otherwise.

COGSit = Dummy variable where it is equal to one if the firm’s [Cost of good

sold/Sales] is initially above the industry median at year t-1 and falls to the

bottom quartile of its industry in year t or year t+1 and zero otherwise.

EMPit = Dummy variable where it is equal to one if the firm experiences more than

20% drop in the number of employees from year t-1 to year t or t+1 and

zero otherwise.

ASSETSit = Dummy variable where it is equal to one if the firm experiences more than

15% drop in its total property, plant and equipment (net) from year t-1 to

year t or t+1 and zero otherwise.

DIVit = Dummy variable where it is equal to one if the firm experiences more than

25% drop in its total dividends from year t-1 to year t or t+1 and zero

otherwise.

NetDebtit = Dummy variable where it is equal to one if Net Debt exceeds 5% of the

book value of total asset at year t or t+1 and zero otherwise. Net Debt is

measured by Compustat item: DLTIS (Data 111) less DLTR (Data 114).

Net Equityit = Dummy variable where it is equal to one if Net Equity exceeds 5% of the

book value of total asset at year t or t+1 and zero otherwise. Net Debt is

measured by Compustat item: SSTK (Data 108) less PRSTKC (Data 115).

Independent Variables

Toibn’s Qit

= Market capitalisation) + Total Asset – Common/Ordinary Equity, scaled by

total assets at year t.

LnTotal Assetsit

= Natural logarithm of company i's total asset at year t.

Institutionalit = The proportion of shares held by institutional investors reported in file s13

at year t.

31

Table 4: Management Restructuring

This table reports the coefficients of a logit regression which takes the form of :

iitititit

itititititit

nalInstitutioetsLnTotalAssTobinsQFDDECLINE

FDMATUREFDGROWTHDECLINEMATUREGROWTHCEO

εαααα

αααααα

+++++

+++++=

10987

654321

*

**

The dependent variable (CEO) takes the value of 1 when managerial restructuring occurred

and zero otherwise. Growth takes the value if a firm is in growth lifecycle and zero otherwise.

Mature takes the value if a firm is in mature lifecycle and zero otherwise. Decline takes the

value if a firm is in decline lifecycle and zero otherwise. FD takes the value of 1 if a firm is in

financial distress and zero otherwise. TobinsQ is measured by (Market capitalisation) + Total

Asset – Common/Ordinary Equity, scaled by total assets. LnTotalAssets is measured by

Ln(Total Assets). Institutional is measured by the total share holdings held by institutional

investors, scaled by the total outstanding shares. The standard errors of the variables appear

in the parentheses. ***, **, and * denote statistical significance at the 1%, 5 % and 10%

levels respectively.

FD

C 0.4821***

(2.9240)

GROWTH -0.2411**

(-2.1365)

MATURE -0.3368***

(-3.0957)

DECLINE -0.2966***

(-2.7265)

GROWTH*FD 0.7849

(1.2442)

MATURE*FD 1.1185**

(2.3142)

DECLINE*FD -0.4062

(-1.0876)

TOBIN’S Q -0.0070**

(-2.3178)

LN(TOTAL ASSETS) 0.1087***

(5.2952)

INSTITUTIONAL -0.0086

(-0.6988)

McFadden R2 0.0063

LR-Stat. 50.7571***

32

Table 5: Operational Restructuring / Asset Restructuring This table reports the coefficients of a logit regression which takes the form of :

iititititit

ititititit

nalInstitutioetsLnTotalAssTobinsQFDDECLINEFDMATURE

FDGROWTHDECLINEMATUREGROWTHgstructurin

εααααα

ααααα

++++++

++++=

109876

54321

**

*Re

The dependent variable (Restructuring) takes the value of 1 when operational (asset)

restructurings occurred and zero otherwise. The restructurings include reducing in investing

activities (INV), reducing cost of goods sold (COGS), laying off employees (EMP) and asset

sales (ASSETS). Definitions of the restructurings are in Table 2. Growth takes the value if a

firm is in growth lifecycle and zero otherwise. Mature takes the value if a firm is in mature

lifecycle and zero otherwise. Decline takes the value if a firm is in decline lifecycle and zero

otherwise. FD takes the value of 1 if a firm is in financial distress and zero otherwise.

TobinsQ is measured by (Market capitalisation) + Total Asset – Common/Ordinary Equity,

scaled by total assets. LnTotalAssets is measured by Ln(Total Assets). Institutional is

measured by the total share holdings held by institutional investors, scaled by the total

outstanding shares. The standard errors of the variables appear in the parentheses. ***, **,

and * denote statistical significance at the 1%, 5 % and 10% levels respectively.

INV COGS EMP ASSETS

C 1.1489***

(22.2152)

-1.8518***

(17.8514)

-0.0387

(-0.5817)

0.25488**

(4.4088)

GROWTH 0.0198

(0.4658)

-0.0215

(-0.2516)

-0.1861***

(-3.5982)

-0.0448

(-0.9433)

MATURE 0.1869**

(4.3985)

0.0037

(0.0439)

-0.2574***

(-4.9541)

0.0799*

(1.7026)

DECLINE 0.2479***

(5.7451)

-0.0190

(-0.2160)

-0.2617***

(-4.8824)

0.2366***

(4.9588)

GROWTH*FD 1.4396***

(7.0413)

0.7193***

(4.0950)

1.3461***

(10.2747)

1.5673***

(11.3586)

MATURE*FD 1.1751***

(6.4825)

0.2714

(1.4120)

1.4749***

(11.8700)

1.3254***

(10.5539)

DECLINE*FD 1.1072***

(4.7295)

0.7361***

(3.7037)

1.3289***

(8.7588)

1.0781***

(6.9902)

TOBIN’S Q -0.0003

(-1.5053)

0.0000

(0.1251)

-0.0001

(-1.0731)

-0.0002**

(-2.0628)

LN(TOTAL ASSETS) -0.0933***

(-13.3508)

-0.1765***

(11.7543)

-0.2288***

(-22.9595)

-0.2439***

(-29.1921)

INSTITUTIONAL 0.0001**

(2.2010)

0.0002***

(3.3362)

-0.0064*

(-1.8956)

0.0007

(1.0037)

McFadden R2 0.0138 0.0209 0.0573 0.0568

LR-Stat. 452.1484*** 241.0682*** 1343.2100*** 1645.6120***

33

Table 6: Financial Restructuring

This table reports the coefficients of a logit regression which takes the form of :

iititititit

ititititit

nalInstitutioetsLnTotalAssTobinsQFDDECLINEFDMATURE

FDGROWTHDECLINEMATUREGROWTHgstructurin

εααααα

ααααα

++++++

++++=

109876

54321

**

*Re

The dependent variable (Restructuring) takes the value of 1 when financial restructurings

occurred and zero otherwise. The restructurings include dividend cuts (DIV), issue of debt

(NetDebt) and issue of equity (NetEquity). Definitions of the restructurings are in Table 2.

Growth takes the value if a firm is in growth lifecycle and zero otherwise. Mature takes the

value if a firm is in mature lifecycle and zero otherwise. Decline takes the value if a firm is

in decline lifecycle and zero otherwise. FD takes the value of 1 if a firm is in financial

distress and zero otherwise. TobinsQ is measured by (Market capitalisation) + Total Asset –

Common/Ordinary Equity, scaled by total assets. LnTotalAssets is measured by Ln(Total

Assets). Institutional is measured by the total share holdings held by institutional investors,

scaled by the total outstanding shares. The standard errors of the variables appear in the

parentheses. ***, **, and * denote statistical significance at the 1%, 5 % and 10% levels

respectively.

DIV NetDebt NetEquity

C 0.6879***

(6.8299)

-0.5011***

(-9.5213)

-1.7984***

(-21.4868)

GROWTH -0.2512***

(-2.8805)

-0.3044***

(-7.0061)

-0.4659***

(-6.9203)

MATURE -0.6244***

(-7.5450)

-0.4741***

(-10.8175)

-0.8813***

(-12.0733)

DECLINE -0.7627***

(-9.5786)

-0.4155***

(-9.3513)

-1.4572***

(-16.7136)

GROWTH*FD 1.2456***

(3.0042)

-0.3013**

(-2.1116)

1.2707***

(8.7514)

MATURE*FD 1.7517***

(5.6077)

-0.4839***

(-3.2606)

1.4694***

(9.9279)

DECLINE*FD 1.4345***

(4.8616)

-0.5006***

(-2.8514)

2.0717***

(11.5711)

TOBIN’S Q 0.0002

(1.1338)

0.0000

(0.4627)

0.0010**

(2.3130)

LN(TOTAL ASSETS) -0.1937***

(-16.4640)

-0.0433***

(-5.8534)

-0.0433***

(-3.4434)

INSTITUTIONAL 0.0027

(0.9661)

0.0000

(-1.3190)

0.0002***

(7.1979)

McFadden R2 0.0479 0.0071 0.0475

LR-Stat. 652.8526*** 213.7014*** 617.3404***

34

Table 7: Effectiveness of the Restructuring Strategies

This table reports the coefficients of a logit regression which takes the form of :

iititit

itititit

nalInstitutioetsLnTotalAssTobinsQ

gsstructurinDECLINEgsstructurinMATUREgsstructurinGROWTHery

εααα

αααα

++++

+++=

765

4321 Re*Re*Re*covRe

The dependent variable (Recovery) takes the value of 1 when a financial distress firm return to profit (measured by Earnings before Interest, Tax, depreciation

and amortisation) within 2 years followed the distress year; and zero otherwise. Growth takes the value if a firm is in growth lifecycle and zero otherwise.

Mature takes the value if a firm is in mature lifecycle and zero otherwise. Decline takes the value if a firm is in decline lifecycle and zero otherwise. The

restructurings include managerial, operational/assets and financial restructurings. Definitions of the restructurings are in Table 2. TobinsQ is measured by

(Market capitalisation) + Total Asset – Common/Ordinary Equity, scaled by total assets. LnTotalAssets is measured by Ln(Total Assets). Institutional is

measured by the total share holdings held by institutional investors, scaled by the total outstanding shares. The standard errors of the variables appear in the

parentheses. ***, **, and * denote statistical significance at the 1%, 5% and 10% levels respectively.

CEO INV COGS EMP ASSETS DIV NetDebt NetEquity

C -1.7642

(-1.5200)

-1.8066***

(-6.1193)

-1.8722***

(-7.5213)

-1.7756***

(-6.6102)

-1.8937***

(-6.9198)

-1.7877***

(-2.7097)

-1.9046***

(-7.7345)

-1.7135***

(-6.6556)

GROWTH*RESTRUCTURING -1.0473

(-1.5582)

-0.1389

(-0.5652)

0.5782

(0.7842)

-0.1562

(-0.5809)

-0.1442

(-0.5861)

0.6315

(1.0369)

0.2161

(0.5878)

-1.1145**

(-2.0423)

MATURE*RESTRUCTURING -1.0368*

(-1.6958)

0.0608

(0.2611)

-0.2964

(-0.2265)

0.1385

(0.5924)

0.1944

(0.8641)

0.5404

(1.0620)

0.5739

(1.5683)

-1.2313***

(-2.6202)

DECLINE*RESTRUCTURING -0.1044

(-0.1428)

-0.0315

(-0.1188)

-0.8360

(-0.7593)

-0.2075

(-0.6782)

0.1088

(0.3959)

0.0144

(0.0229)

0.2119

(0.4614)

0.0289

(0.0647)

TOBIN’S Q 0.0090

(1.0011)

0.0001

(0.8353)

0.0000

(0.5765)

0.0001

(0.7071)

0.0001

(0.8508)

0.0124**

(1.9656)

0.0000

(0.8085)

0.0001

(0.8945)

LN(TOTAL ASSETS) 0.3218*

(1.7233)

0.1889***

(3.3819)

0.1981***

(3.5417)

0.1820***

(3.1852)

0.1973***

(3.4969)

0.2032*

(1.7155)

0.1927***

(3.4914)

0.1854***

(3.2350)

INSTITUTIONAL 0.5208

(0.7022)

0.0012

(0.5177)

0.0012

(0.5361)

0.0014

(0.5854)

0.0012

(0.5382)

0.0809

(1.5583)

0.0013

(0.5607)

0.0012

(0.5025)

McFadden R2 0.0881 0.0184 0.0196 0.0183 0.0202 0.0989 0.0213 0.0346

LR-Stat. 10.2591 14.8193** 15.8277** 14.3043** 16.3203** 15.2450** 17.2008*** 27.9626***

35

Figure 1: Distress Firms (by lifecycle) from 1995 to 20006

0

10

20

30

40

50

60

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Nu

mb

er o

f F

irm

s

birth

growth

mature

decline