Embed Size (px)

Citation preview

It’s not just account-ing for the num-bers, but account-

ing for the functionsand activities that pro-duce the numbers.

In today’s multi-faceted and multidis-ciplinary economic environ-ment, organizationalmanagement has placed evermore emphasis on increasingresults with fewer resourcesthrough evaluation of the econ-omy, efficiency, and effective-ness of the organization’s opera-tions. While the financial auditprovides an after-the-fact opin-ion that financial statementspresent fairly the company’sfinancial position, there is noassurance that the company’soperations are conducted in themost economical, efficient, andeffective manner. It is these veryoperations that produce thetransactions and numbers thatultimately become the financialstatement amounts. However,normally very little is done bythe financial auditors, other thana management report primarilyconcerned with observed weak-nesses in internal controls,regarding the state of operationsthat produce such financial

results. The operational review,combined with financial auditprocedures, is the tool used toperform such an evaluation.

In many organizations today,top management is seeking waysto become competitive andmaintain market position—ormerely to survive. Managershave sensed that many of theirorganizational systems are detri-mental to progress and have heldthem back from achieving orga-nizational, departmental, andindividual goals and objectives.These are the very systems thatare supposed to be helpful; forexample:

1. Planning systems—long- andshort-term—that resulted indocumented plans but not inactual results;

2. Budget systems that becamecostly in terms of allocatingresources effectively and con-trolling costs in relation toresults;

3. Organizationalstructures that createdunwieldy hierarchies,which produced sys-tems of unnecessarypolicing and control;4. Cost accountingstructures that

obscured true product costsand resulted in pricing thatconstrained competitiveness;

5. Management systems thatproduced elaborate computersystems and reporting withoutenhancing the effectiveness ofoperations;

6. Sales functions and forecaststhat resulted in selling thoseproducts that maximized salescommissions but may nothave been the products man-agement desired to produceand sell; and

7. Operating practices that per-petuated outmoded systems(“We’ve always done it thatway”) rather than promotedbest practices.

Performing an operationalreview together with or separatefrom the financial audit is a toolto make these systems helpful asintended and direct the organiza-tion toward its goals. Theoreti-cally, organizations and work

It’s not just accounting for the numbers. It’saccounting for the functions and activities that pro-duce the numbers. That’s why simply doing afinancial audit may not give you a clear picture ofthe company’s operations. © 2007 Wiley Periodicals, Inc.

Rob Reider

Financial Audits: Taking an Operational

View

featur

e artic

le

19

© 2007 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com).DOI 10.1002/jcaf.20304

jcaf_966.qxp 4/11/07 6:47 AM Page 19

20 The Journal of Corporate Accounting & Finance / May/June 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

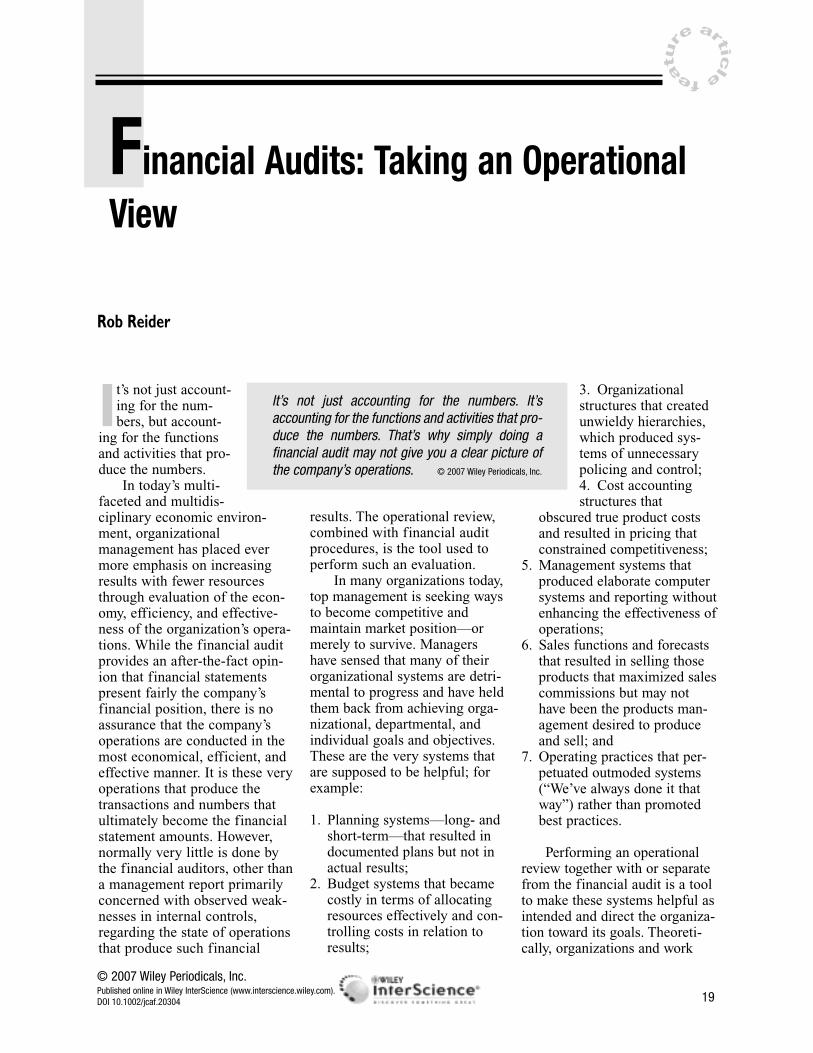

Operational Areas

Although the primary focus of the operational review is on the manner in which scarce resources are used by theorganization, considering the sources and uses of resources and the policies and procedures used to deal withundesirable operating conditions, there are specific operational areas that need to be addressed, including:

1. Sales of Products or Services

• Are sales made to quality customers with the right products at the right time?• Does each sale make a contribution to profits?• Are all costs compared to the sale, such as product costs (direct material and labor), assignment of product-related

activity costs (e.g., manufacturing processes, quality control, shipping, and receiving), functional costs (e.g., purchasing, accounts payable, billing, and accounts receivable), and customer costs (e.g., marketing, selling,support services, and customer service)?

• Do sales relate to an agreed-upon sales forecast? Is the company selling the right products to the right cus-tomers?

• Do sales integrate with an effective production scheduling and control system?2. Manufacturing or Production of Services

• Are sales orders entered into an effective production control system, which ensures that all sales orders areentered into production in a timely manner to ensure on-time, quality deliveries?

• Is work-in-process kept to a minimum so that only real customer orders are being worked on rather thanbuilding up finished goods inventory?

• Are the most efficient and economical production methods used to ensure that the cost of the product is keptto its realizable minimum?

• Are direct materials and labor used most efficiently so that waste, reworks, and rejects are kept to a mini-mum?

• Are nondirect labor (and material) costs such as quality control, supervision and management, repairs andmaintenance, material handling, and so on kept to a minimum?

3. Billing, Accounts Receivable, and Collections

• Are bills sent out in a timely manner—at the time of shipment or before?• Are accounts receivable processing procedures the most efficient and economical?• Is the cost of billing, accounts receivable processing, and collection efforts more than the amount of the

receivable or the net profit on the sale?• Is the number and amount of accounts receivable continually analyzed for minimization?• Are any customers paying directly or through electronic funds transfer at the time of shipping or delivery?• Are bills and accounts receivable in amounts exceeding the cost of processing excluded from the system?• Has consideration been given to reducing or eliminating these functions?

4. Inventory—Raw Materials and Finished Goods

• Are raw materials and finished goods inventories kept to a minimum?• Are raw materials delivered into production on a just-in-time basis?• Are finished goods completed in production just in time for customer delivery?• Is the company working toward getting out of these inventory businesses?

5. Purchasing, Accounts Payable, and Payments

• Are all items that are less than the cost of purchasing excluded from the purchasing system—with an effi-cient system used for these items? (continued)

Exhibit 1

jcaf_966.qxp 4/11/07 6:47 AM Page 20

units within the organizationshould operate in an economic,efficient, and effective manner atall times. If such were the case,operational review techniqueswould be applied on an ongoingbasis. However, with the passageof time, good intentions and ini-tially helpful systems tend todeteriorate. Operational reviewsare then necessary to help getthe organization back on trackby pinpointing operational defi-ciencies, developing practicalrecommendations, and imple-menting positive changes. Mak-ing such operational reviews partof the financial audit processhelps to improve overall com-pany operations as well as pro-duce improved financial results.The results of operations cannotbe separated from financialresults.

Theoretically, managers atall levels should be heldaccountable for using the scarceresources entrusted to them toachieve maximum results at theleast possible costs. Althoughmanagement should embraceoperational review concepts andapply them as they proceed, thisis rarely the case. More typically,management has to be sold onthe value of operational reviewsas part of the financial audit oras a separate engagement for thecertified public accountant.While the financial audit may beseen as a cost center to theorganization or as a necessaryevil that disrupts operationswhile the audit is being per-formed, operational review pro-cedures that improve operationsand reduce or eliminate costscan be seen as a profit center.

In selling the benefits ofconducting an operationalreview, as part of the financialaudit or separately, it is impor-tant to stress that unlike othertechniques that cost time andmoney, such as a financial audit,for uncertain results, operationalreviews pay for themselves. Ineffect, the operational reviewenvironment becomes a profitcenter instead of a financialaudit cost center. Although thereare no guarantees, a successfuloperational review should resultin at least five to ten times itscost in annual savings. These arenot one-time savings, but ongoing—that is, savings yearafter year. With the success of anoperational review, managementmay quickly realize that themore operational review proce-dures accomplished and the

The Journal of Corporate Accounting & Finance / May/June 2007 21

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Operational Areas (continued)

• Are all repetitive high-volume and high-cost items (e.g., raw materials and manufacturing supplies) negotiatedby purchasing with vendors as to price, quality, and timeliness?

• Does the production system automatically order repetitive items as an integrated part of the production con-trol system?

• Has consideration been given to reduce these functions for low- and high-ticket items, leading toward thepossible elimination of these functions?

• Does the company consider paying any vendors on a shipment or delivery basis as part of its vendor negotia-tion procedures?

6. Other Costs and Expenses—General, Administrative, and Selling

• Are all other costs and expenses kept to a minimum? Remember, an unnecessary dollar not spent is a dollardirectly to the bottom line.

• Are selling costs directed toward customer service and strategic plans rather than maximizing salespeople’scompensation?

• Is there a system in effect that recognizes and rewards the reduction of expenses rather than the rewarding ofbudget increases?

• Are all non-value-added functions (e.g., management and supervision, office processing, paperwork, and soon) evaluated as to reduction and elimination?

Exhibit 1

jcaf_966.qxp 4/11/07 6:47 AM Page 21

more recommended economiesand efficiencies implemented,the greater the savings andresults. In addition, the residualcapability for performing opera-tional reviews remains in thearea under review, so operationspersonnel can continue to applyoperational review concepts onan ongoing basis.

Keep in mind that the intentof the operational review is notto be critical of present opera-tions—which is the case manytimes with a financial audit andits accompanying managementletter—but to review operationsand develop a program of bestpractices and continuous positiveoperational improvements byworking with management andstaff personnel. This can be

accomplished most effectivelyby working with operations per-sonnel in areas where they rec-ognize deficiencies and are will-ing to cooperate. The concept ofoperational reviews should besold as an internal program ofreview directed toward improvedeconomies and efficiencies thatwill produce increased opera-tional results—either as part ofthe financial audit or as a sepa-rate service. CPAs must deter-mine to what extent to includeoperational review procedureswithin the scope of the financialaudit as a service to the clientand as a way to make theirfinancial audit services moreunique.

The operational reviewprocess should start at the top of

the organization. That is, topmanagement should define andcommunicate its strategic plansfor the company, including areasof expansion, retrenchment, andstatus quo. At the same time,management members shouldidentify the businesses they wantto be in, the businesses they donot want to be in, their basicbusiness principles and beliefsystems, and their desires foreach function within the organi-zation.

For instance, top manage-ment may define a desire for thesales function, which has histori-cally sold whatever it could tocustomers, to become a moreintegral part of the planningprocess and other functions suchas manufacturing and

22 The Journal of Corporate Accounting & Finance / May/June 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

Some Basic Business Principles

Each organization must determine the basic principles that guide its operations. These principles become the foun-dation on which the company bases its desirable operational practices. Examples of such business principlesinclude the following:

• Produce the best-quality product at the least possible cost.• Set selling prices realistically, so as to sell the entire product that can be produced within the constraints of the

production facilities.• Build trusting relationships with critical vendors; keeping them in business is keeping the company in business.• The company is in the customer service and cash conversion businesses.• Do not spend a dollar that doesn’t need to be spent; a dollar not spent is a dollar to the bottom line. Control

costs effectively; there is more to be made here than increased sales.• Manage the company; do not let it manage the managers. Provide guidance and direction, not crises.• Identify the company’s customers and develop marketing and sales plans with the customers in mind. Produce

for the company’s customers, not for inventory. Serve the customers by providing what they need, not by sellingthem what the company produces.

• Do not hire employees unless they are absolutely needed—and only when they multiply the company’s effective-ness so that the company makes more from them than if they did it themselves.

• Keep property, plant, and equipment to the minimum necessary to maintain customer demand.• Plan for the realistic, but develop contingency plans for the positive unexpected.

Exhibit 2

jcaf_966.qxp 4/11/07 6:47 AM Page 22

engineering. In defining theirdesires, members of manage-ment may identify attributessuch as the following:

• sales forecasts more realisti-cally related to actual cus-tomers and products to besold;

• a larger percentage of thesales forecast (at least 80percent) matched by realcustomer orders;

• sales efforts driven by man-agement’s identification inthe planning process of what

to sell, to whom, and at whatquantity;

• a sales forecast with a highpercentage of real customerorders that allows the com-pany’s production to bebased on customer ordersand expected deliverytimes, at a specified qualitylevel;

• a sales function that isgeared more toward provid-ing customer service thantoward making sales thatmaximize sales personnel’scompensation; and

• a sales function that workswithin the company’s planstogether with the other func-tions of the company, suchas manufacturing, engineer-ing, purchasing, accounting,and marketing.

With the clear identificationand communication of manage-ment’s desires, each function hasa clear idea as to where it is head-ing and the basis for its evalua-tion. The purpose of the opera-tional review then becomes one ofa helping agent, assisting each

The Journal of Corporate Accounting & Finance / May/June 2007 23

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

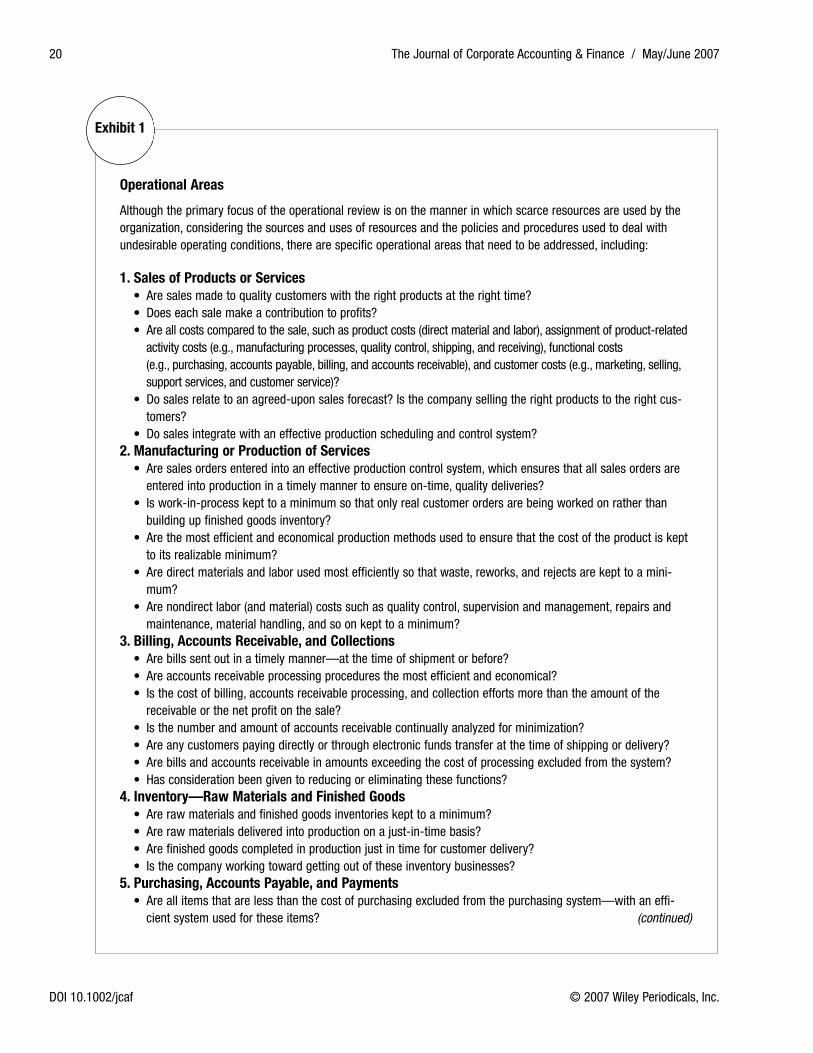

Financial Audits Versus Operational Reviews

Among the differences between financial audits and operational reviews, using operational review concepts, is thatthe reviewer is less concerned with determining whether purchase requisitions and orders and suppliers’ invoicesreflect proper approvals, as in a financial audit, but more concerned with such operational aspects as whether:

• the materials were really needed,• quantities used or purchased were reasonable,• there was avoidable waste and exposure to damage or loss, and• requisitioners exercised undue influence over purchasing by designating sources of purchase.

For example, a typical financial audit step may be to determine whether vendor purchase requisitions and invoiceshave been properly approved. However, when looking at the operational aspects of vendor purchases, the reviewermay ask:

• Were materials really needed?

For example, were materials mistakenly ordered that could not be used, owing to changes in production specifica-tions, because the product specifications unit failed to communicate with the purchasing department?• Were quantities used or purchased reasonable?

For example, assuming the materials were usable, were goods bought for inventory above calculated safety stocklevels because of the fear of incurring a stock-out?• Was there avoidable waste and exposure to damage or loss?

For example, were steel components and parts that were susceptible to rust bought and stored in an outside yard,owing to an overcrowded inside storeroom?• Did the requisitioner exercise undue influence by stating specific sources or brands?

For example, did the requisitioner specify a Dell microcomputer or a Xerox copier when a less expensive brandwould do just as well?

Exhibit 3

jcaf_966.qxp 4/11/07 6:47 AM Page 23

function to achieve its stated goalsand objectives as related to man-agement’s desires. The perform-ance of the operational review isthus less a critical evaluation ofwhat a particular function is doingand more an appraisal of whatneeds to be done to help the func-tion achieve its goals and becomethe best it can.

As the operational reviewteam works with each functionwithin the organization, it assiststhat function to understand whatit needs to do to become what itshould be. As best practices andimprovements are recommendedand implemented, each functionmoves toward its proper place

within the organization—and thecompany becomes a learningorganization, both by functionand overall.

In today’s organizationalatmosphere of cost cutting,downsizing, re-engineering andso on, the operational reviewmust be sensitive in its approachso as to maintain needed serv-ices in the most economical,efficient, and effective manner.Whereas management may befocusing on reducing costs,operations may be focusing onan increase in providing qualityservices. The review team mustbe careful to maintain a properperspective so that it directs its

efforts toward overall organiza-tional goals as well as the indi-vidual requirements of eachfunction.

As you plan your operationalreview, consult the exhibits inthis article for guidelines.Exhibit 1 discusses specificoperational areas you need toaddress. Exhibit 2 helps yourorganization determine the basicbusiness principles that guide itsoperations. Exhibit 3 discussesthe differences between financialaudits and operational reviews.And Exhibit 4 summarizes someother differences between finan-cial audits and operationalreviews.

24 The Journal of Corporate Accounting & Finance / May/June 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

Financial Audit Versus Operational Reviews: More Differences

Some of the other differences between a conventional financial audit and an operational review are summarizedbelow.

Financial Audit Versus Operational Review

Characteristic Financial Audit Operational Review

1. Purpose Express opinion on financial condition Analyze and improve methods and performance2. Scope Fiscal financial records Business operations3. Skills Accounting Interdisciplinary4. Time orientation To the past To the future 5. Precision Absolute Relative6. Audience Stockholders, public Internal management7. Necessity Legally required At option of management8. Standards GAAP, GAAS* Economy, efficiency, effectiveness9. Opinion Required Not required

10. Audit results Opinions, financial statements Recommendations to management11. Focus Financial statements presented fairly Operational positive improvements12. Viewpoint Financial Management13. Success Unqualified opinion Management adoption of recommendations

*GAAP = generally accepted accounting principles.GAAS = generally accepted auditing standards.

Exhibit 4

jcaf_966.qxp 4/11/07 6:47 AM Page 24

The Journal of Corporate Accounting & Finance / May/June 2007 25

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Rob Reider, CPA, MBA, PhD, is the president of Reider Associates, a management and organizational con-sulting firm located in Santa Fe, New Mexico, which he founded in 1976. He has been a consultant tonumerous large, medium, and small businesses in both the private and public sectors. He is the courseauthor and sought-after discussion leader and presenter for more than 20 different workshops and semi-nars that are conducted nationally for various organizations and associations. He has conducted more than1,000 such seminars throughout the country and has received the American Institute of Certified PublicAccountants’ Outstanding Discussion Leader of the Year Award. He is also the author of the following pro-fessional management books published by John Wiley & Sons, Inc.:• Operational Review: Maximum Results at Efficient Costs (text and workbook),• Benchmarking Strategies: A Tool for Profit Improvement,• Improving the Economy, Efficiency, and Effectiveness of Not-for-Profits, and• Managing Cash Flow: An Operational Focus (coauthor with Peter B. Heyler).He is also the author of the work of fiction Road to Oblivion: The Footpath Back Home, a novel of discov-ery that looks at life after being downsized.

For more information about Rob Reider and Reider Associates, visit www.reiderassociates.com or e-mail him at [email protected].

jcaf_966.qxp 4/11/07 6:47 AM Page 25