Embed Size (px)

Citation preview

26/03/15 1 Корпоративная презентация Медси

Financial and Operating Results for 2014

March 2015

26/03/15 2 Корпоративная презентация Медси

OVERVIEW

26/03/15 3 Корпоративная презентация Медси

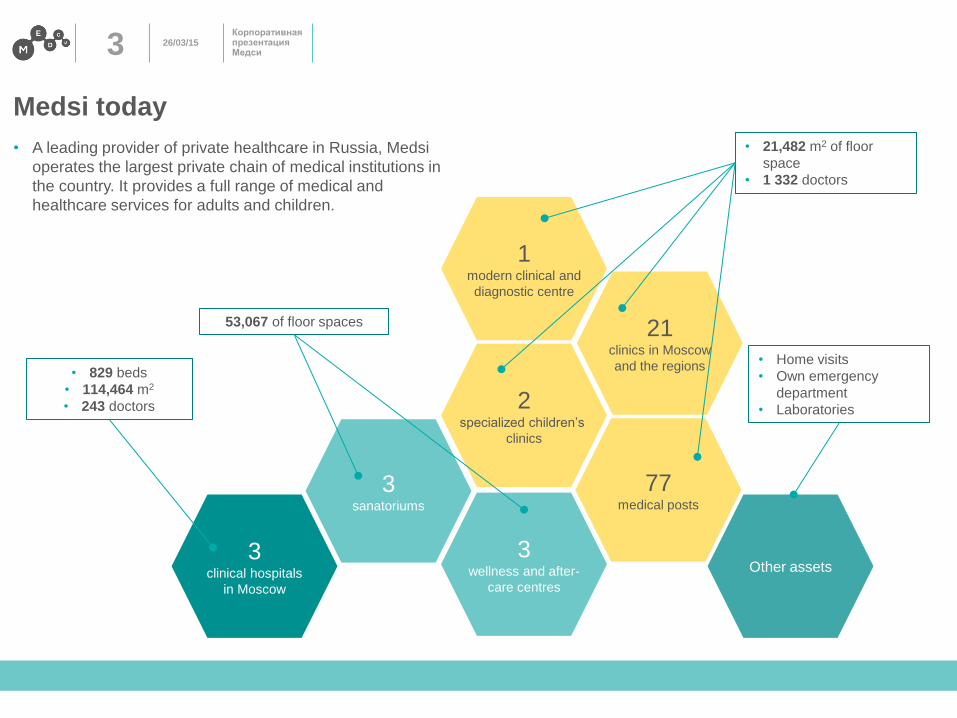

Medsi today

1

modern clinical and

diagnostic centre

21 clinics in Moscow

and the regions

2 specialized children’s

clinics

77 medical posts

3 sanatoriums

Other assets

53,067 of floor spaces

• 21,482 m2 of floor

space

• 1 332 doctors

• 829 beds

• 114,464 m2

• 243 doctors

• Home visits

• Own emergency

department

• Laboratories

3 wellness and after-

care centres

3 clinical hospitals

in Moscow

• A leading provider of private healthcare in Russia, Medsi

operates the largest private chain of medical institutions in

the country. It provides a full range of medical and

healthcare services for adults and children.

26/03/15 4 Корпоративная презентация Медси

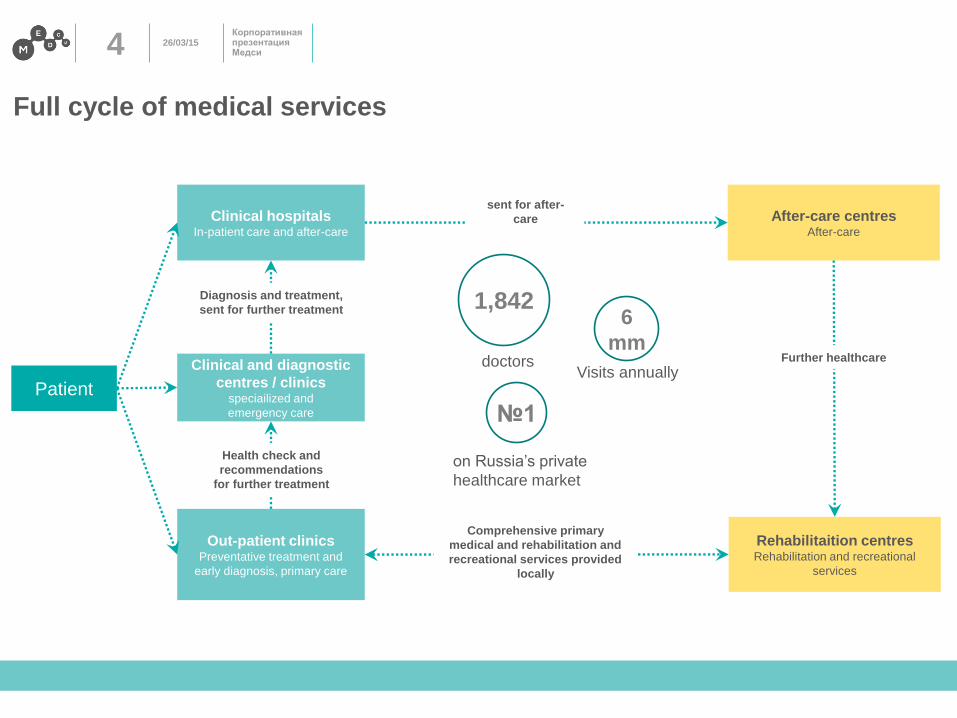

Full cycle of medical services

Clinical hospitals In-patient care and after-care

Clinical and diagnostic

centres / clinics speciailized and

emergency care

Out-patient clinics Preventative treatment and

early diagnosis, primary care

Patient

After-care centres After-care

Rehabilitaition centres Rehabilitation and recreational

services

Health check and

recommendations

for further treatment

Diagnosis and treatment,

sent for further treatment

sent for after-

care

Further healthcare

Comprehensive primary

medical and rehabilitation and

recreational services provided

locally

6

mm

1,842

Visits annually doctors

№1

on Russia’s private

healthcare market

26/03/15 5 Корпоративная презентация Медси

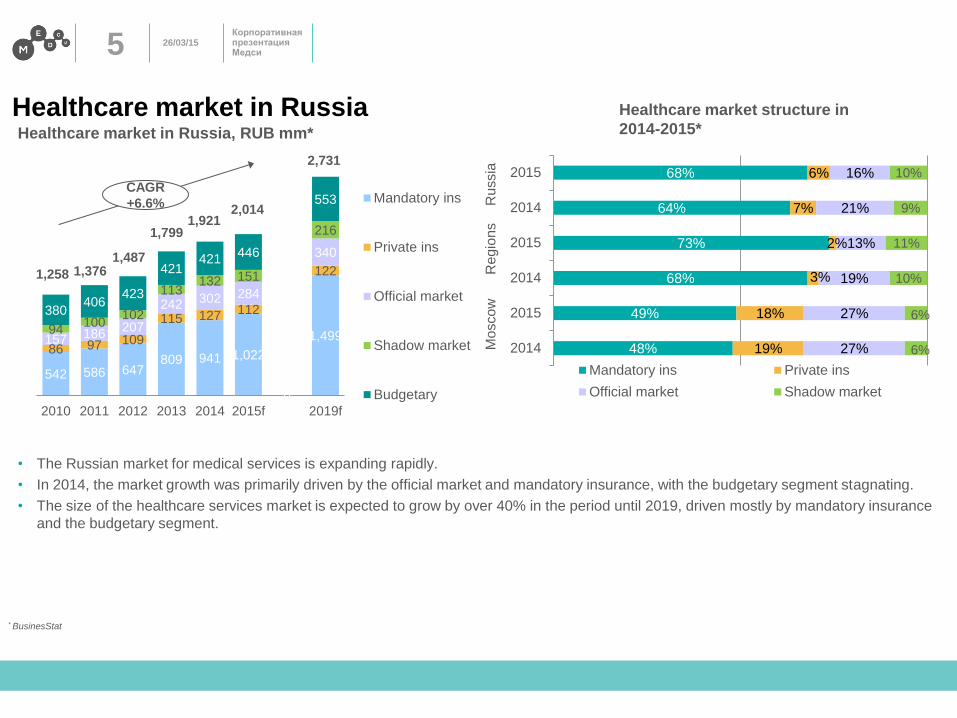

Healthcare market in Russia

542 586 647 809 941 1,022

1,499 86 97 109

115 127 112

122

157 186 207

242 302 284

340

94 100

102

113 132 151

216

380 406

423

421 421

446

0

553

2010 2011 2012 2013 2014 2015f 2019f

Mandatory ins

Private ins

Official market

Shadow market

Budgetary

1,258

CAGR

+6.6%

Healthcare market in Russia, RUB mm*

• The Russian market for medical services is expanding rapidly.

• In 2014, the market growth was primarily driven by the official market and mandatory insurance, with the budgetary segment stagnating.

• The size of the healthcare services market is expected to grow by over 40% in the period until 2019, driven mostly by mandatory insurance

and the budgetary segment.

* BusinesStat

Mo

sco

w

Re

gio

ns

Healthcare market structure in

2014-2015*

48%

49%

68%

73%

64%

68%

19%

18%

3%

2%

7%

6%

27%

27%

19%

13%

21%

16%

6%

6%

10%

11%

9%

10%

2014

2015

2014

2015

2014

2015

Mandatory ins Private ins

Official market Shadow market

Ru

ssia

2,731

2,014 1,921

1,799

1,487 1,376

26/03/15 6 Корпоративная презентация Медси

RESULTS FOR 2014

26/03/15 7 Корпоративная презентация Медси

• In January 2014 Medsi launched a new strategy aimed at improving the quality and range of services, and enhancing

operational efficiency.

• Medsi redesigned management system, granting additional powers to 11 key assets that have became independent

centers of financial responsibility and development. Each of the key assets has operational and medical departments.

• The Group optimized the remuneration system for medical staff, management of the key assets and top-managers. The

proportion of the variable compensation pools was increased and is now linked to the assets' financial performance.

• Medsi launched the automation of business processes in order to make a unified healthcare information system, a

universal resource management system and a unified sales management system for each of the key assets.

• The Group continued to develop partnerships with leading foreign healthcare providers and equipment manufacturers to

supply state-of-the-art equipment to its clinics, adopt best international practices, introduce technology and quality

standards into MEDSI's operations, and provide training to its medical staff.

• Medsi launched a major strategic investment project the construction of a new clinical and diagnostic centre (CDC) on

Krasnaya Presnya, which will comprise polyclinics with in-patient facilities for children and adults, equipped with state-of-

the-art medical equipment. The new centre is expected to be opened in Q2 2015.

• Elena Brusilova was appointed president of the Medsi Group of Companies on November 27, 2014.

MEDSI launched a new strategy, large investment program and projects aimed at

improving business efficiency

2014 January

February

March

April

May

June

July

August

September

October

November

December

2015

Key events in 2014

26/03/15 8 Корпоративная презентация Медси

44%

65% 62%

In-patient Clinics Centre onBelorusskaya

In-patient 12.4%

Centre on Belorusskaya

20.4%

Clinics 58.5%

Other 8.6%

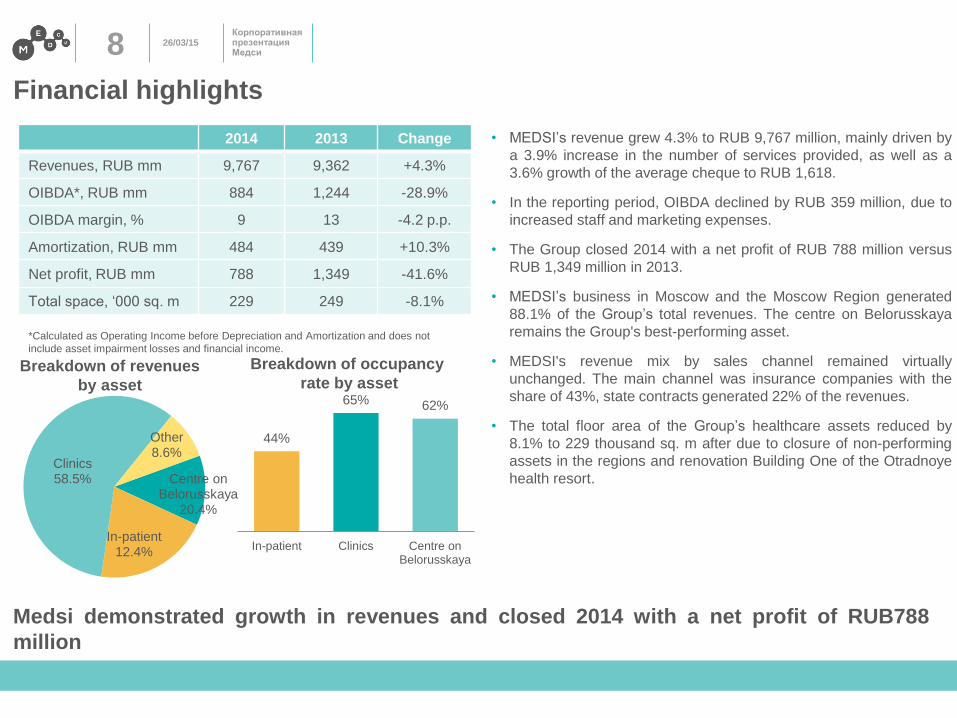

Financial highlights

2014 2013 Change

Revenues, RUB mm 9,767 9,362 +4.3%

OIBDA*, RUB mm 884 1,244 -28.9%

OIBDA margin, % 9 13 -4.2 p.p.

Amortization, RUB mm 484 439 +10.3%

Net profit, RUB mm 788 1,349 -41.6%

Total space, ‘000 sq. m 229 249 -8.1%

• MEDSI’s revenue grew 4.3% to RUB 9,767 million, mainly driven by

a 3.9% increase in the number of services provided, as well as a

3.6% growth of the average cheque to RUB 1,618.

• In the reporting period, OIBDA declined by RUB 359 million, due to

increased staff and marketing expenses.

• The Group closed 2014 with a net profit of RUB 788 million versus

RUB 1,349 million in 2013.

• MEDSI’s business in Moscow and the Moscow Region generated

88.1% of the Group’s total revenues. The centre on Belorusskaya

remains the Group's best-performing asset.

• MEDSI's revenue mix by sales channel remained virtually

unchanged. The main channel was insurance companies with the

share of 43%, state contracts generated 22% of the revenues.

• The total floor area of the Group’s healthcare assets reduced by

8.1% to 229 thousand sq. m after due to closure of non-performing

assets in the regions and renovation Building One of the Otradnoye

health resort.

Medsi demonstrated growth in revenues and closed 2014 with a net profit of RUB788

million

Breakdown of revenues

by asset

Breakdown of occupancy

rate by asset

*Calculated as Operating Income before Depreciation and Amortization and does not

include asset impairment losses and financial income.

26/03/15 9 Корпоративная презентация Медси

1,155 4,276

16,336

1,233 4,287

25,631

Centre on Belorusskaya Clinics Hospitals

2013 2014

Operational highlights

Occupancy rate

Visits, thousand/Hospitalization*

1,531 1,618 1,249 1,332 7,298 7,693

Average cheque, RUB>>

Insurance companies

45%

Corporate clients 23%

Individuals 21%

State contracts

11%

Breakdown of visits by client type

+1 p.p. +5 p.p.

+0.1% +6.8%

43%

64% 57%

44%

65% 62%

Hospitals Clinics Centre on Belorusskaya

2013 2014

Insurance companies

42%

Corporate clients 11%

Individuals 24%

State contracts

22% Other 1%

Breakdown of revenue by client type

+56.9%

*only for in-patient.

* Occupancy rate is calculated as a ratio of number of visits to their maximum possible.

+1 p.p.

26/03/15 10 Корпоративная презентация Медси

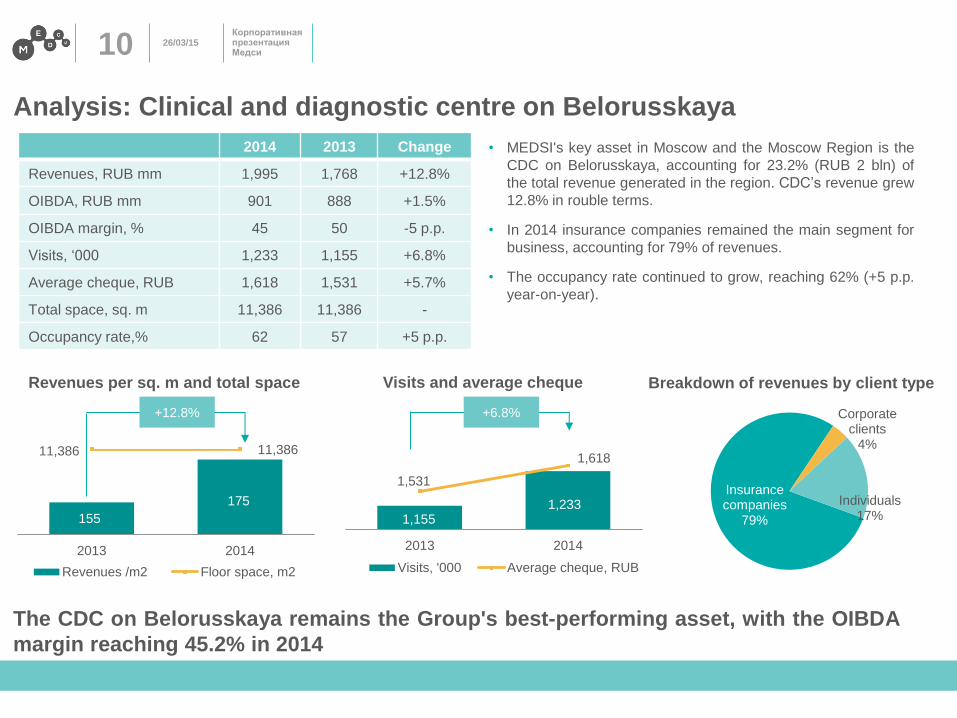

Analysis: Clinical and diagnostic centre on Belorusskaya

2014 2013 Change

Revenues, RUB mm 1,995 1,768 +12.8%

OIBDA, RUB mm 901 888 +1.5%

OIBDA margin, % 45 50 -5 p.p.

Visits, ‘000 1,233 1,155 +6.8%

Average cheque, RUB 1,618 1,531 +5.7%

Total space, sq. m 11,386 11,386 -

Occupancy rate,% 62 57 +5 p.p.

The CDC on Belorusskaya remains the Group's best-performing asset, with the OIBDA

margin reaching 45.2% in 2014

• MEDSI's key asset in Moscow and the Moscow Region is the

CDC on Belorusskaya, accounting for 23.2% (RUB 2 bln) of

the total revenue generated in the region. CDC’s revenue grew

12.8% in rouble terms.

• In 2014 insurance companies remained the main segment for

business, accounting for 79% of revenues.

• The occupancy rate continued to grow, reaching 62% (+5 p.p.

year-on-year).

Visits and average cheque

155

175

11,386 11,386

2013 2014

Revenues /m2 Floor space, m2

Revenues per sq. m and total space

+12.8% +6.8%

Insurance companies

79%

Corporate clients

4%

Individuals 17%

Breakdown of revenues by client type

1,155 1,233

1,531

1,618

2013 2014

Visits, '000 Average cheque, RUB

26/03/15 11 Корпоративная презентация Медси

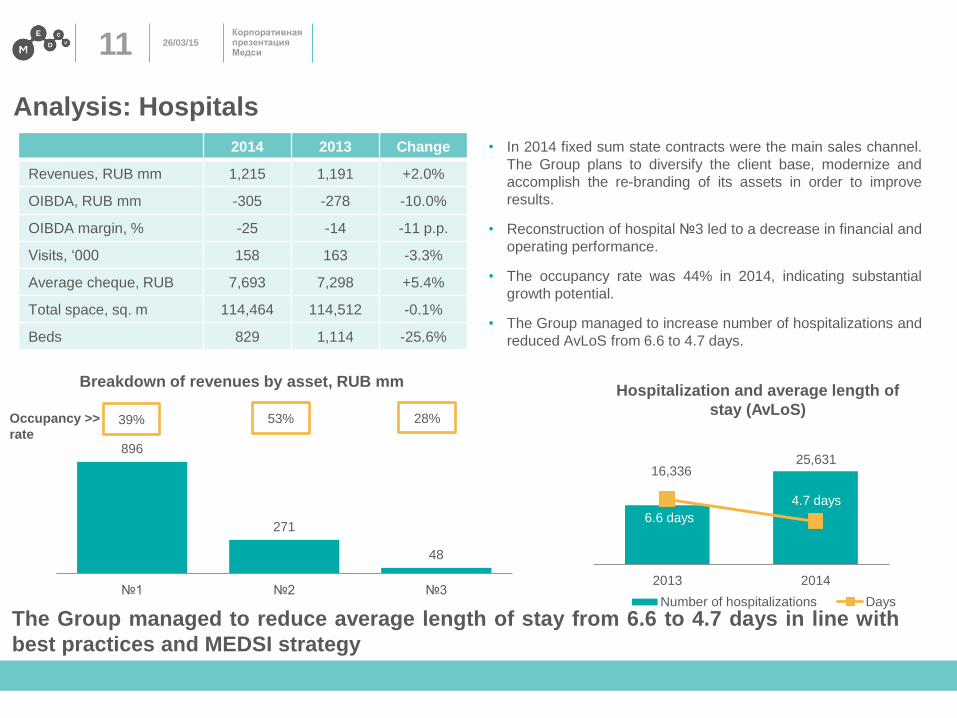

Analysis: Hospitals

2014 2013 Change

Revenues, RUB mm 1,215 1,191 +2.0%

OIBDA, RUB mm -305 -278 -10.0%

OIBDA margin, % -25 -14 -11 p.p.

Visits, ‘000 158 163 -3.3%

Average cheque, RUB 7,693 7,298 +5.4%

Total space, sq. m 114,464 114,512 -0.1%

Beds 829 1,114 -25.6%

• In 2014 fixed sum state contracts were the main sales channel.

The Group plans to diversify the client base, modernize and

accomplish the re-branding of its assets in order to improve

results.

• Reconstruction of hospital №3 led to a decrease in financial and

operating performance.

• The occupancy rate was 44% in 2014, indicating substantial

growth potential.

• The Group managed to increase number of hospitalizations and

reduced AvLoS from 6.6 to 4.7 days.

Breakdown of revenues by asset, RUB mm

The Group managed to reduce average length of stay from 6.6 to 4.7 days in line with

best practices and MEDSI strategy

896

271

48

№1 №2 №3

Occupancy >>

rate 39% 53% 28%

Hospitalization and average length of

stay (AvLoS)

16,336 25,631

2013 2014

Number of hospitalizations Days

4.7 days

6.6 days

26/03/15 12 Корпоративная презентация Медси

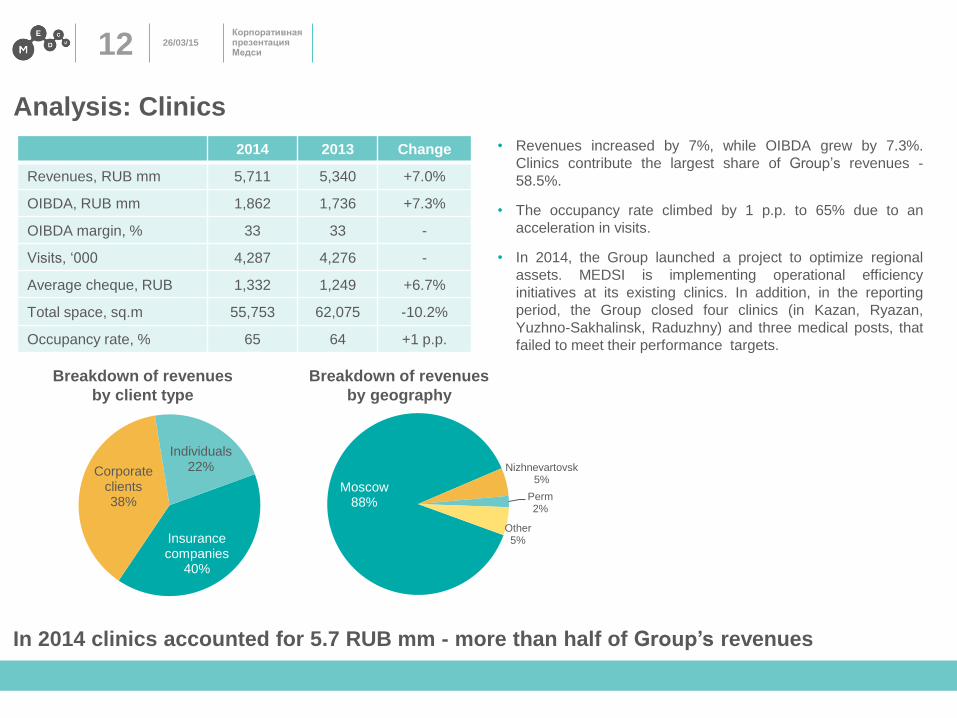

Moscow 88%

Nizhnevartovsk 5%

Perm 2%

Other 5%

Analysis: Clinics

2014 2013 Change

Revenues, RUB mm 5,711 5,340 +7.0%

OIBDA, RUB mm 1,862 1,736 +7.3%

OIBDA margin, % 33 33 -

Visits, ‘000 4,287 4,276 -

Average cheque, RUB 1,332 1,249 +6.7%

Total space, sq.m 55,753 62,075 -10.2%

Occupancy rate, % 65 64 +1 p.p.

• Revenues increased by 7%, while OIBDA grew by 7.3%.

Clinics contribute the largest share of Group’s revenues -

58.5%.

• The occupancy rate climbed by 1 p.p. to 65% due to an

acceleration in visits.

• In 2014, the Group launched a project to optimize regional

assets. MEDSI is implementing operational efficiency

initiatives at its existing clinics. In addition, in the reporting

period, the Group closed four clinics (in Kazan, Ryazan,

Yuzhno-Sakhalinsk, Raduzhny) and three medical posts, that

failed to meet their performance targets.

In 2014 clinics accounted for 5.7 RUB mm - more than half of Group’s revenues

Insurance companies

40%

Corporate clients 38%

Individuals 22%

Breakdown of revenues

by client type

Breakdown of revenues

by geography

26/03/15 13 Корпоративная презентация Медси

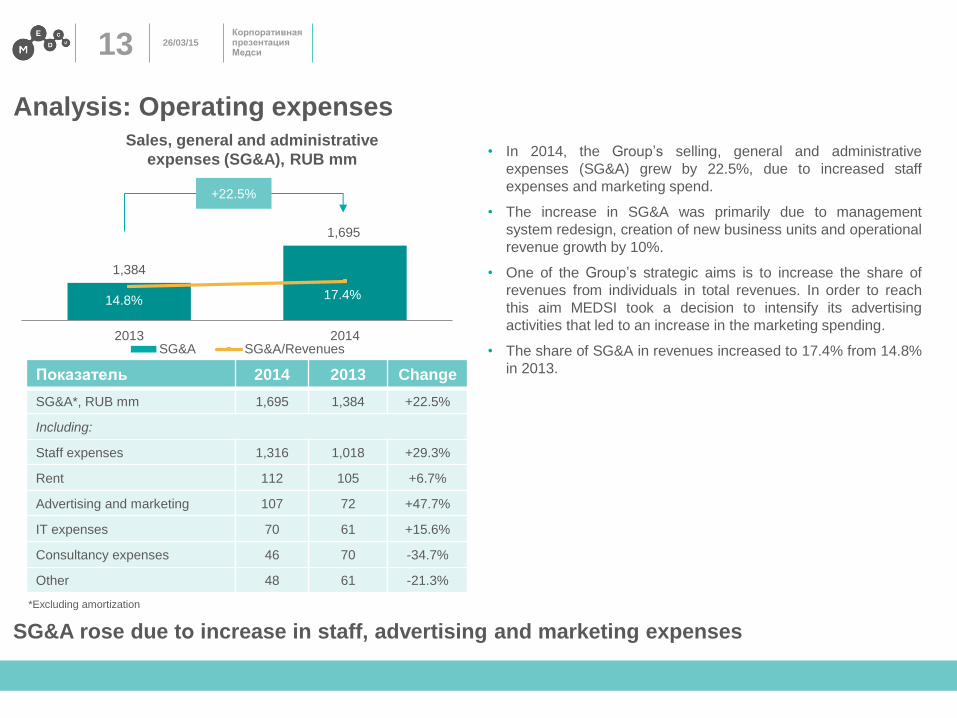

Analysis: Operating expenses

1,384

1,695

14.8% 17.4%

2013 2014SG&A SG&A/Revenues

Sales, general and administrative

expenses (SG&A), RUB mm

+22.5%

Показатель 2014 2013 Change

SG&A*, RUB mm 1,695 1,384 +22.5%

Including:

Staff expenses 1,316 1,018 +29.3%

Rent 112 105 +6.7%

Advertising and marketing 107 72 +47.7%

IT expenses 70 61 +15.6%

Consultancy expenses 46 70 -34.7%

Other 48 61 -21.3%

• In 2014, the Group’s selling, general and administrative

expenses (SG&A) grew by 22.5%, due to increased staff

expenses and marketing spend.

• The increase in SG&A was primarily due to management

system redesign, creation of new business units and operational

revenue growth by 10%.

• One of the Group’s strategic aims is to increase the share of

revenues from individuals in total revenues. In order to reach

this aim MEDSI took a decision to intensify its advertising

activities that led to an increase in the marketing spending.

• The share of SG&A in revenues increased to 17.4% from 14.8%

in 2013.

SG&A rose due tо increase in staff, advertising and marketing expenses

*Excluding amortization

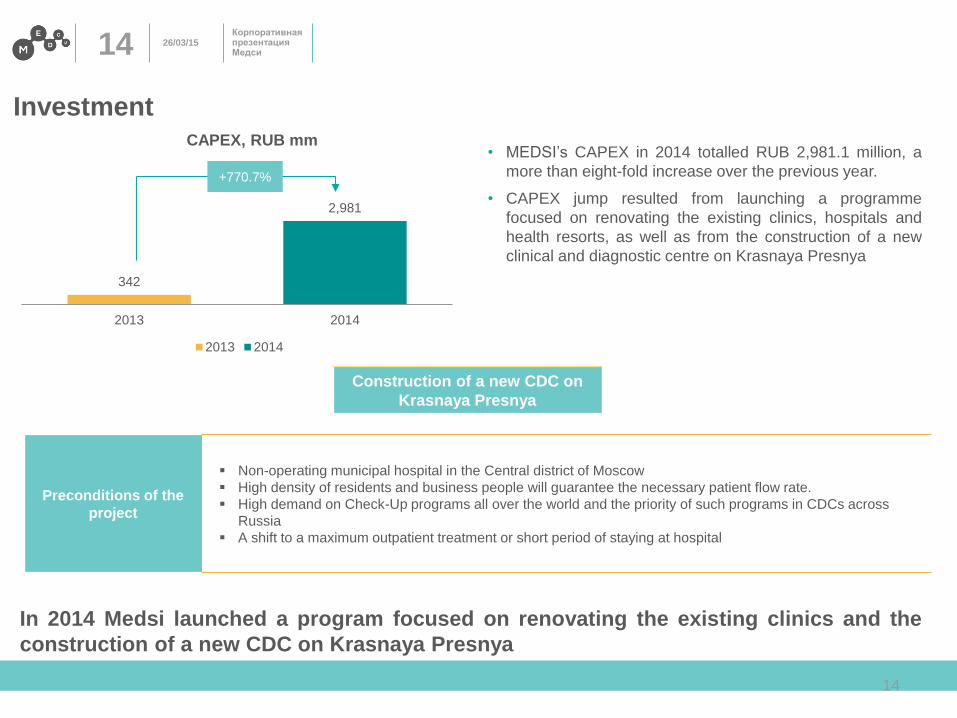

26/03/15 14 Корпоративная презентация Медси

14

342

2,981

2013 2014

2013 2014

Investment

+770.7%

• MEDSI’s CAPEX in 2014 totalled RUB 2,981.1 million, a

more than eight-fold increase over the previous year.

• CAPEX jump resulted from launching a programme

focused on renovating the existing clinics, hospitals and

health resorts, as well as from the construction of a new

clinical and diagnostic centre on Krasnaya Presnya

CAPEX, RUB mm

Construction of a new CDC on

Krasnaya Presnya

In 2014 Medsi launched a program focused on renovating the existing clinics and the

construction of a new CDC on Krasnaya Presnya

Preconditions of the

project

Non-operating municipal hospital in the Central district of Moscow

High density of residents and business people will guarantee the necessary patient flow rate.

High demand on Check-Up programs all over the world and the priority of such programs in CDCs across

Russia

A shift to a maximum outpatient treatment or short period of staying at hospital

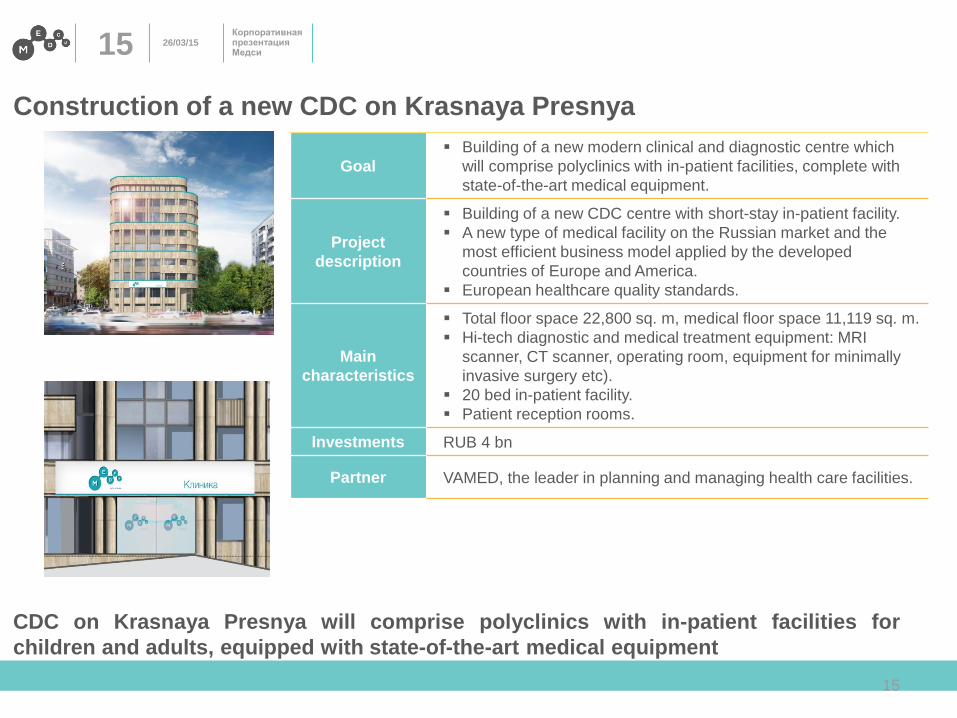

26/03/15 15 Корпоративная презентация Медси

15

Goal

Building of a new modern clinical and diagnostic centre which

will comprise polyclinics with in-patient facilities, complete with

state-of-the-art medical equipment.

Project

description

Building of a new CDC centre with short-stay in-patient facility.

A new type of medical facility on the Russian market and the

most efficient business model applied by the developed

countries of Europe and America.

European healthcare quality standards.

Main

characteristics

Total floor space 22,800 sq. m, medical floor space 11,119 sq. m.

Hi-tech diagnostic and medical treatment equipment: MRI

scanner, CT scanner, operating room, equipment for minimally

invasive surgery etc).

20 bed in-patient facility.

Patient reception rooms.

Investments RUB 4 bn

Partner VAMED, the leader in planning and managing health care facilities.

CDC on Krasnaya Presnya will comprise polyclinics with in-patient facilities for

children and adults, equipped with state-of-the-art medical equipment

Construction of a new CDC on Krasnaya Presnya

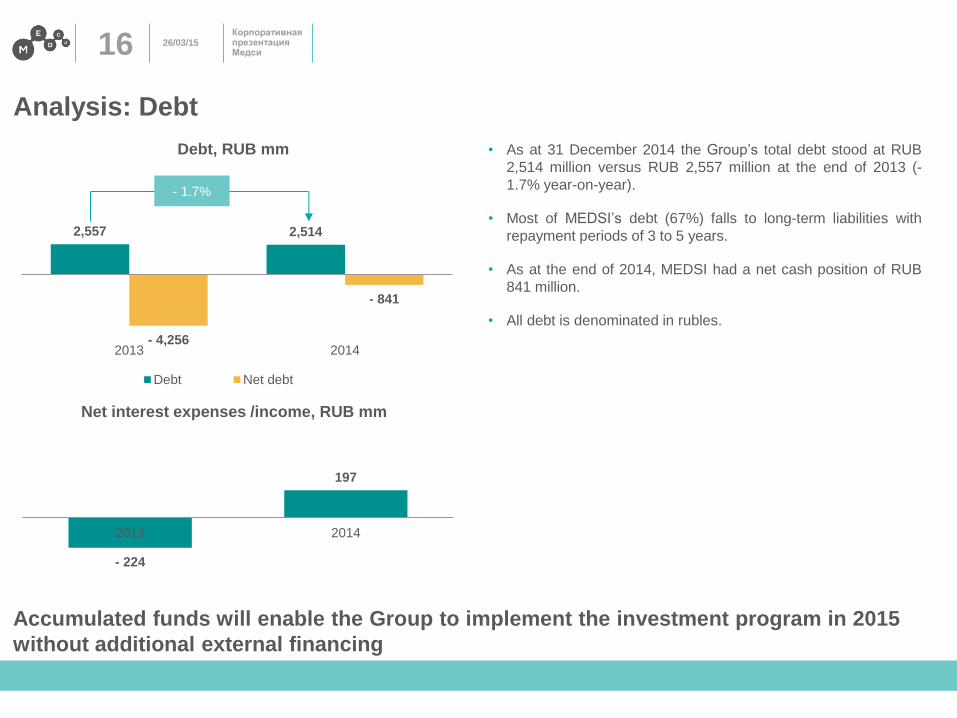

26/03/15 16 Корпоративная презентация Медси

Analysis: Debt

2,557 2,514

- 4,256

- 841

2013 2014

Debt Net debt

Debt, RUB mm

- 1.7%

- 224

197

2013 2014

Net interest expenses /income, RUB mm

• As at 31 December 2014 the Group’s total debt stood at RUB

2,514 million versus RUB 2,557 million at the end of 2013 (-

1.7% year-on-year).

• Most of MEDSI’s debt (67%) falls to long-term liabilities with

repayment periods of 3 to 5 years.

• As at the end of 2014, MEDSI had a net cash position of RUB

841 million.

• All debt is denominated in rubles.

Accumulated funds will enable the Group to implement the investment program in 2015

without additional external financing

26/03/15 17 Корпоративная презентация Медси

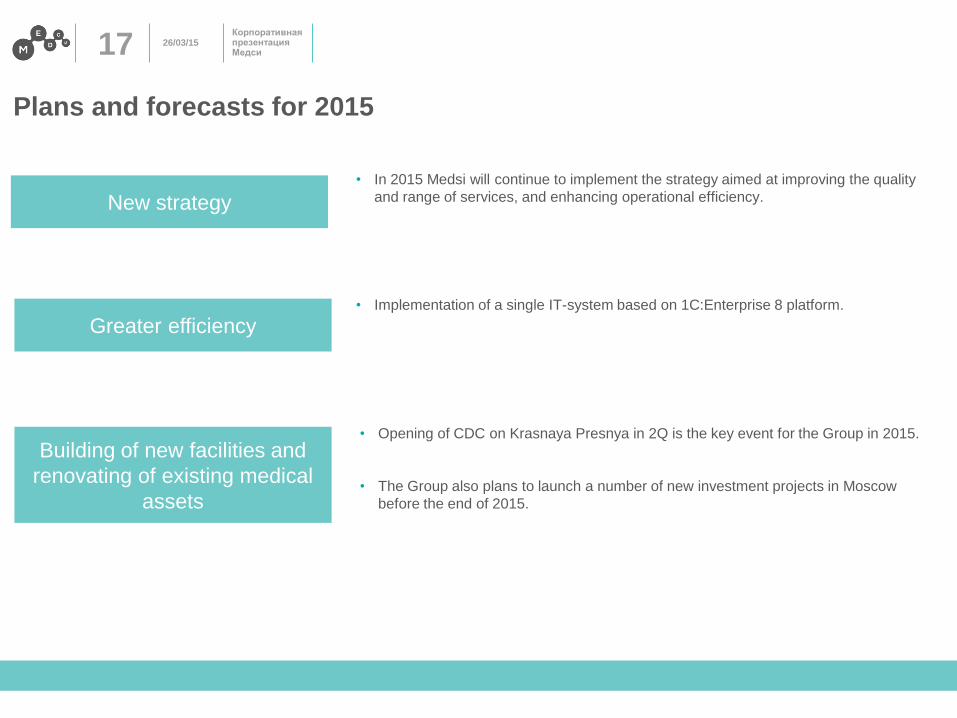

Plans and forecasts for 2015

Building of new facilities and

renovating of existing medical

assets

• Opening of CDC on Krasnaya Presnya in 2Q is the key event for the Group in 2015.

• The Group also plans to launch a number of new investment projects in Moscow

before the end of 2015.

New strategy

Greater efficiency

• In 2015 Medsi will continue to implement the strategy aimed at improving the quality

and range of services, and enhancing operational efficiency.

• Implementation of a single IT-system based on 1C:Enterprise 8 platform.