Embed Size (px)

Citation preview

Finance for Non-Finance

People

Session 3

Date: 19 March 2015

Facilitator: Deborah Richards

Community Action Southwark

At Cambridge House

www.casouthwark.org.uk

Session Objectives

By the end of the session, participants will be able to:

prepare a Receipts and Payments Account and a

Statement of Assets and Liabilities (SoAL)

explain what a Statement of Financial Activities (SOFA)

explain the difference between a Receipts and Payments

Account and a SOFA

identify debtors, creditors, accruals and prepayments

adjust Receipts and Payments figures to produce a

SOFA

prepare a Balance Sheet

3

Final/Statutory Accounts

Prepared each year

Presented to Annual General Meetings (AGM).

Prepared in accordance with legal requirements

(hence why they are also called statutory accounts).

Primarily of historical value.

They take time, usually months, to prepare.

By which time they are of limited use for

managing the organisation.

By law, must be accurate.

4

Why we Prepare

Final Accounts (1)

1. Legal Requirements:-

o Charities Acts 2011 and Charities (Accounts and Reports)

Regulations 2008 and Companies Act 2006 & 2011

to satisfy funding bodies - councils, trustees, donors -

that their funds are being spent strictly in accordance

with any conditions

2. Constitutional requirements:-

o To satisfy the independent examiner/auditor that proper

books of account have been maintained and that the

charity is abiding to it’s constitution.

5

Why we Prepare

Final Accounts (2)

3. To satisfy other users of accounts:-

o Members

o Her Majesty's Revenue and Customs (HMRC)

o Employees and Volunteers, Trade Unions

o Financial guarantors, Creditors, Banks, Loan

companies etc.

4. To provide information to the management

committee/trustees or directors.

6

Different Types of Accounts

Presentation (1)

There are two main ways of presenting the final

accounts for charities:-

1. Receipts and Payments Accounts, together with the Statement of Assets and Liabilities (SoAL)

2. Statement of Financial Activities (SOFA) together with a Balance Sheet

Note: Trading, Profit and Loss Accounts are not

appropriate for voluntary organisations, whether

they are companies or not.

7

Some Definitions

Receipts – monies (whether notes, coins, cheques, or electonic fund

transfers) actually received.

Payments - monies (whether notes, coins, cheques, or electonic fund

transfers) actually paid out.

Incoming Resources (Income) – monies (as above) actually

received, plus monies owing to the organisation at year-end.

Resources Expended (Expenditure) – monies (as above)

actually paid out, plus monies owed by the organisation at year-end.

8

Fund Accounting

Charity law requires that all the funds of a charity be identified in one (or

more) of three categories. They are determined according to the terms

and conditions under which they were given to or obtained by the

charity.

Endowment funds: funds to be retained by the charity. (Also

called Capital Funds)

Restricted Funds: funds which can only be used for specific

purposes, usually defined by the donor .

Unrestricted Funds: funds available for spending on the objects

of the charity as the trustees see fit.

9

Endowment Funds

Permanent Endowment Funds are funds which have been

given to a charity to be held as capital with no power to convert the

funds to income.

These may be in the form of cash or other assets.

o Although the capital must be retained for the benefit of the charity, any

investment income will be available to be applied by the charity unless

otherwise specified by the terms of the trust.

Expendable Endowment Funds are funds which have been

given to a charity to be held as capital where the trustees do have a

discretionary power to convert them into income.

o They should be treated as capital until converted to income.

10

Restricted Funds

Whichever way a charity presents its end-of-year accounts,

endowment, restricted and unrestricted funds, must always

be accounted for on a fund by fund basis.

Restricted income funds may be grouped together for

presentation in the accounts, but

detailed records must be kept of each fund,

must be broken down in the notes to the accounts

Trustees will be in breach of trust if they use restricted

income other than for the purpose(s) for which are given.

Any interest or investment income arising from a

restricted income fund must be added back to the fund.

11

Methods of Book-keeping

There are two methods of bookkeeping: Receipts & Payments and Accruals

Accounting.

1. Receipts & Payments basis - You are using this method

if:-

you are recording money coming in but do not include the amounts

people owe you as part of your income.

and

if you keep track of expenses at the time you pay them, rather than

at the time you first receive the bills.

o This method is also referred to as Cash Accounting or a Cash

basis.

12

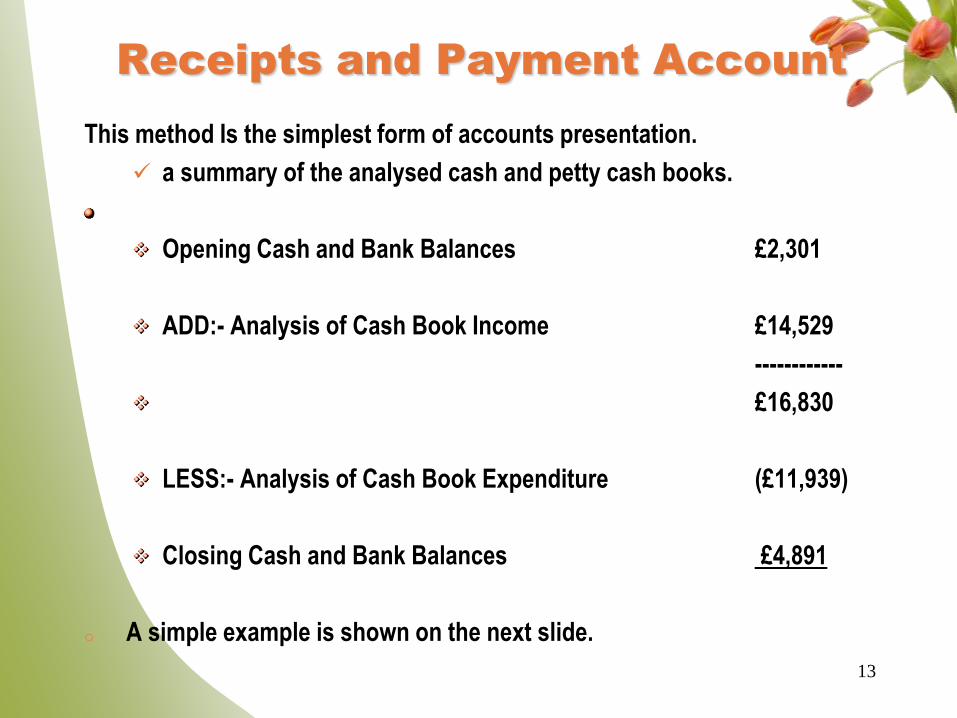

Receipts and Payment Account

This method Is the simplest form of accounts presentation.

a summary of the analysed cash and petty cash books.

Opening Cash and Bank Balances £2,301

ADD:- Analysis of Cash Book Income £14,529

------------

£16,830

LESS:- Analysis of Cash Book Expenditure (£11,939)

Closing Cash and Bank Balances £4,891

o A simple example is shown on the next slide.

13

14

RECEIPTS & PAYMENTS

Flower Pot Trust

Receipts & Payments Account

for the year ended 31 December 20XX

Receipts

Rent 10290

Grants 1000

Donations 2130

Bank Interest 100

Total Receipts 13520

Payments

Salary & NI 12400

Rent & Utilities 2710

Insurance 340

Printing & Stationery 90

Telephone & Postage 250

Publicity 40

Volunteers Expenses 250

Course Materials 850

Repairs/Renewals 60

Training 150

Trips 1300

Accountancy Fee 80

Other Expenditure 520

Total Payments 19040

Net Receipts/(Payments) (5520)

Cash and bank balance at start of period 11220

Cash and bank balance at end of period 5700

Flower Pot Trust

Statement of Assets and Liabilities

As At 31 December 20XX

Cash and Bank Deposits 5700

Liabilities 2570

Advantages of Receipts and

Payments Accounts

Easier to use and more straightforward than accruals

accounting

No specialist accounting knowledge is required

Double entry book-keeping isn’t needed

Can legally be used by charities which are not registered

companies for their end of year accounts

provided their income is less than £250,000 a year

15

Disadvantages of Receipts and

Payments Accounts

Only explains the differences between the opening and closing cash and

bank balances.

Does not take into account monies owed (debtors) to the

organisation or monies owed (creditors) by the organisation

Does not show any assets (i.e. furniture, stock) or liabilities

Note. The Statement of Assets and Liabilities on the next slide

goes some way towards reducing these two disadvantages

o Does not show the “true and fair view” required by the Companies Acts

therefore cannot be used by limited companies for their end of

year accounts

however small their income is

This includes charitable companies 16

Statement of Assets and

Liabilities (SOAL)

A Statement of Asset and Liabilities (SOAL) should always accompany a

Receipts and Payments Account

It lists

the assets an organisation owns or is owed

o The amount of Cash at bank and in hand (petty cash)

o Fixed assets

e.g. Computer equipment, with values

o Debtors

o Creditors

17

Receipts and Payments

Accounts Pack (CC16)

The Charity Commission provides a template for Receipts and Payments

accounts, together with a set of guidance notes.

See http://www.charity-commission.gov.uk/publications/cc16.aspx

o CC16a, the Receipts and Payments Accounts template is available as a

pdf file, or, more usefully, in an Excel format

o CC16b, are the pdf guidance notes,

o Although the use of this pack is not compulsory, if your charity is one

that can legally prepare Receipts and Payments Accounts, you are

strongly advised to use it.

You can then be certain that your accounts will meet the legal

requirements

18

Exercise 1 - Receipts and

Payments Account

Case Study:- Paradise Estate Tenants

Association

Exercise:- Produce a R&P Account plus

SoAL for the above from the

information provided

19

Receipts & Payments Basis vs.

Accrual Basis Book-keeping (2)

2. Accruals basis - You are using this method if:-

You record income at the time a sale is made or the time a grant is

due, not at the time you actually receive the money.

and

You enter expenses when you receive the bill, not when you pay it.

o In practice, most voluntary organisations keep records on a receipts and

payments basis.

o For those groups which need Final (Statutory) Accounts prepared on an

accruals basis, but keep their books on a receipts and payments basis,

the books will have to be adjusted to take account of monies owed and

owing both for the year in question and for the preceding and following

years.

o We will go through these adjustments during this session. 20

The Accruals Concept (1)

One of the basic ideas that runs through accountancy

is the Accruals (or Matching) Concept.

This means we match up all income and

expenditure to the accounting period in which

they were earned or incurred.

When we prepare accounts for a period of

time (typically a year), we should therefore

only concern ourselves with the income and

expenditure that relates directly to the period

in question.

21

The Accruals Concept (2)

o This means we need to:

a) Identify what income was actually "earned"'

during the

accounting period (rather than what money was

received and banked).

and

b) Identify what expenditure was actually

incurred during the period (rather than what

payments were made).

22

The Accruals Concept (3)

Incoming Resources - represents the amount of money

received in the accountancy period, adjusted for:

monies received in advance (for example Grants)

monies due but not received by the organisation at the end of each

accounting period (for example customers who have been invoiced)

Resources Expended - represents the amount of money paid in

the year, adjusted for:

bills owing at the start and end of the year (i.e. Utilities, HMRC)

bills paid where not all of the bill relates to the current financial year

(i.e. Insurance) .

23

Accruals Accounts (1)

The Charity Commission provides two templates for Accruals

accounts, CC17a and CC39a together with guidance notes.

CC17a, is available as a pdf file, or in an Excel format

See

http://www.charitycommission.gov.uk/Publications/cc17.

aspx

o CC17b, are the pdf guidance notes,

o CC17a is suitable for charities wishing to analyse their

expenditure by charitable activity, e.g. voluntary income,

activities for generating funds, investment income etc.

24

The Accruals Accounts (2)

The other template provided for Accruals accounts, CC39a also has a set of

guidance notes.

See http://www.charitycommission.gov.uk/Publications/cc17.aspx

o CC39a, the Receipts and Payments Accounts template , is available as a

pdf file, or, more usefully, in Excel format

o CC39b, are the pdf guidance notes

CC39a - suitable for charities wishing to analyse their financial reporting

using natural categories. These are the types of income and expenditure

headings which should be found in the entity's financial records e.g.

grant income, donations, salary costs, premises costs etc.

25

Statement Of Financial Activities

(SOFA)

The Charities’ SORP - introduced a new accounting format called a

Statement of Financial Activities (SOFA)

o Sets out the accounting rules and practises which all charities, whether

registered or not, are expected to follow when preparing end of year

accounts.

o This change recognised that an Income and Expenditure Account

(which is derived from the Profit and Loss Account for commercial

enterprises) is not well suited for use by charities, and can sometimes be

misleading.

o The SOFA effectively does away with surpluses and deficits and

concentrates on showing all incoming resources, all resources

expended and all changes in funds from one year to another.

26

The Charities SORP

Accounting and Reporting by Charities: Statement of

Recommended Practice (SORP) (Revised 2015)

The Charity Commission and the Office of the Scottish

Charity Regulator, as the joint SORP-making body for

charities, have developed two SORPS:-

1. Financial Reporting Standard for Smaller Entities

(FRSSE)

2. Financial Reporting Standard applicable in the UK

and Republic of Ireland (FRS 102).

Recommended that charities speak with their auditor,

independent examiner or advising accountant to explore

which standard is best for them.

For further information on which one to chose:

http://www.charitiessorp.org/

27

28

STATEMENT OF FINANCIAL ACTIVITIESUnrestricted Restricted Endowment Total Previous Year

Funds Funds Funds Funds Totals

Incoming Resources

Resources Expended

Net Incoming/(Outgoing) Resources before transfers

Gross Transfers Between Funds

Net Movement in Funds

Total Funds Brought Forward

Total Funds Carried Forward

Where Do We Get the Information

From To Prepare the SOFA?

When we prepare a SOFA, we prepare it for the year:- i.e.:

12 months from 1st April 20xx to 31st March 20xy.

o We therefore need all the Incoming Resources (Income) and Resources

Expended (Expenditure) relating to that year.

o The information can be obtained from:

The Receipts and Payments Account

Cash (Received and Paid) Analysis Book

Petty Cash Analysis Book

Invoices that we have not yet paid (creditors) that relate to that

year.

Monies other people owe us (debtors) that relate to that year.

Monies we have paid in advance of the accounting period

29

Adjusting Receipts & Payments to Produce

Incoming Resources & Resources Expended

The Receipts and Payments for the year are easily obtained by summarising

the analysis books, but to convert the Receipts and Payments into

Incoming Resources and Resources Expended, we need to do three

things:-

1. Identify anything else which belongs to the year just

ended and bring it in

2. Identify anything which does not belong to the year

just ended and take it out

3. After we have done this, we need to identify all

expenditure on fixed assets and replace it with a

depreciation charge.

30

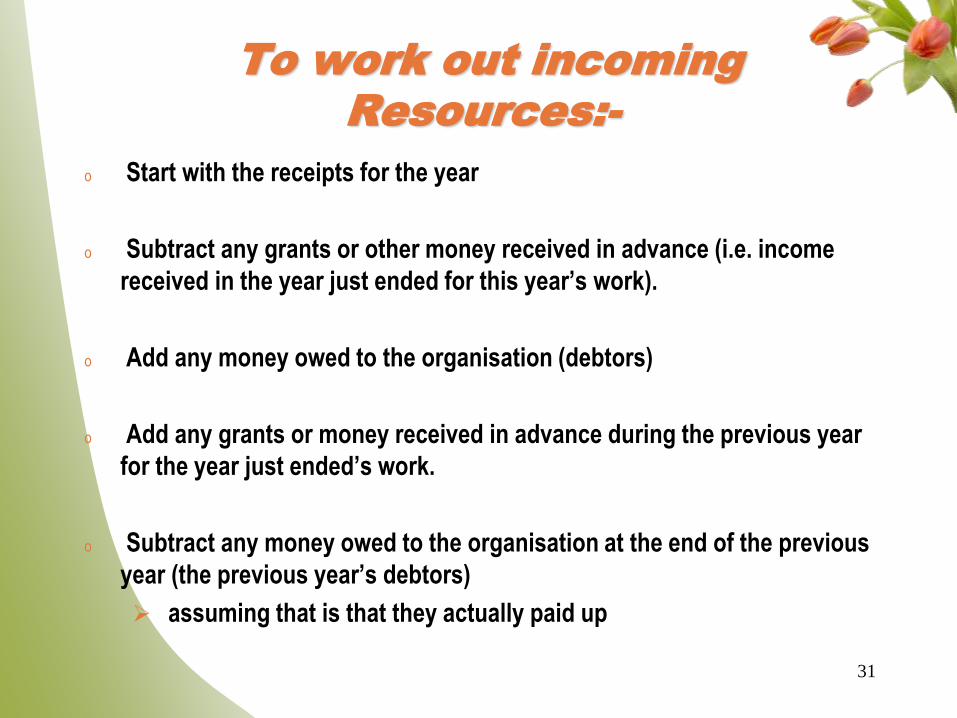

To work out incoming

Resources:-

o Start with the receipts for the year

o Subtract any grants or other money received in advance (i.e. income

received in the year just ended for this year’s work).

o Add any money owed to the organisation (debtors)

o Add any grants or money received in advance during the previous year

for the year just ended’s work.

o Subtract any money owed to the organisation at the end of the previous

year (the previous year’s debtors)

assuming that is that they actually paid up

31

To work out Resources

Expended:-

o Start with payments for the year

o Add any money owed by the organisation (creditors and accruals)

o Subtract any payments made in advance (i.e. money paid out in the year

just ended for this year’s work)

o Subtract any money owed by the organisation at the end of the previous

year (i.e. the previous year’s creditors and accruals)

(assuming that is that you actually paid up)

32

Adjustment for depreciation:-

Depreciation is a calculated figure charged to Resources

Expended to write off Fixed Assets over their useful life. o Two methods :-

1. the straight line method

2. the reducing balance method.

o Subtract any payments made to purchase

fixed assets (above your capitalisation level)

o Add back the depreciation charge

not only for the fixed assets purchased in the

year

but also for all the fixed assets purchased in

previous years.

33

Exercise 2 - Adjusting Receipts and Payments to

produce Incoming Resources and Resources

Expended

o We’ll continue using the Paradise Estate Residents Association as our

case study. CaseStudyResourcesIn&Out

o To do the adjustments, use the prepared spread-sheet named

“WorkingSheet” in the Excel Workbook named “SOFAWorkingSheet”

SOFAWorkingSheet

o SOFAWorkingSheetAnswer

34

Exercise 3 – Preparing the SOFA

o We do this using the answers from the previous exercise.

o We also know that the Paradise Estates Tenants Association

has (as yet) no endowments

brought forward £0 from the previous year

spent £3,092 out of a total capital grant of £3,100 which was restricted

the depreciation charge in the year was £245, which will also be a charge to

the restricted funds

Case Study:- CaseStudySOFA

Exercise:- SOFABlank

Answers:- SOFAAnswers

35

Balance Sheet

o The object of a balance sheet is to show a record of the assets and

liabilities of an organisation at a point in time

a particular date, usually the last day of the financial year.

o This is the wealth of an organisation at that date.

o Contrast the Balance Sheet with the SOFA, which attempts to

summarise the group’s activities over a period of time (i.e. Incoming

Resources, Resources Expended) for the year ended 31st. March 20xy),

rather than at a point in time (i.e. Balance Sheet as at 31st. March 20xy)

o A simple example of a balance sheet is shown on the next slide

36

37

FLOWER POT TRUST

BALANCE SHEET

as at 31 DECEMBER 20XX

At Cost Depreciation Net Book Value

Fixed Assets:- £2,000 (£500) £1,500

Current Assets:-

Stock £0

Debtors/Prepayments £8,370

Cash at Bank £5,000

Cash in Hand £700

£14,070

Current Liabilities:-

Creditors £2,000

Accruals £570

(£2,570)

Net Current Assets £11,500

Net Assets £13,000

Funds:-

Restricted Funds £3,000

Unrestricted Funds £10,000

£13,000

Assets (1)

There are 2 types of assets: Fixed Assets and Current Assets.

Fixed Assets have

a useful life of more than one year.

cost a significant amount

are depreciated over their useful life.

Current Assets can, in principle, be converted into cash in a

relatively short time

liquid assets

Include, in order of liquidity

Stock

Debtors

Prepayments

Bank Accounts

Cash in Hand

38

Assets (2)

Stock

Some voluntary groups may have stock: examples would be groups

running bars, and printing organisations (e.g. stock of paper or value of

finished publications).

Bank Account

The balances held in the current, deposit or any other bank accounts at

the end of the accounting period are included on the balance sheet.

The bank reconciliation figure should be used.

Cash in Hand

This is the amount of money in the petty cash tin at the balance sheet

date.

39

Debtors and Prepaid Expenses

Debtors

These might be people who have been invoiced for services/activities, but

have not yet paid.

Sometimes it may be a funder who has agreed to give the organisation a

grant but have not yet released the money.

In both examples we have "earned" the money during the period, so we

need to include the amounts in our incoming resources.

Prepaid Expenses are amounts which we have paid out for a future period.

They don't relate to the period in question so we need to deduct them from

our expenditure.

A common example of prepaid expenses is an insurance premium,

which is usually paid for the whole year.

o Debtors and Prepaid Expenses form part of our Assets (on the Balance Sheet)

because they are favourable balances.

40

Liabilities

Liabilities are divided between current liabilities and other

liabilities.

Current Liabilities are short term liabilities which will

be paid within one year of the balance sheet date.

Current Liabilities include:

Creditors, Accruals and Bank Overdrafts

Other Liabilities include any long term loans the

organisation may have taken out.

With long term loans it is important to establish when the

loan is likely to be repaid.

41

Creditors and Accrued Expenses (1)

Creditors

These will be bills in our unpaid invoices file, such as stationery

bills, electricity bills etc.

We need to include these amounts in our accounts because we

have already incurred this expenditure even though we haven't

yet paid out the money.

o Another type of creditor occurs when money has been received in

advance (for a future period).

For example, a funder may send us a grant cheque for a project that

hasn't started yet.

If we decided to abandon the project, we would have to pay this

grant back.

Any grant received in advance needs to be deducted from our

incoming resources for the period.

42

Creditors and Accrued Expenses (2)

Accrued Expenses: Sometimes we know we have

incurred expenditure even though we haven't actually

received a bill yet.

We may not even know how much we will have to pay,

but if we can make a reasonable estimate we can include

this in our expenditure as well.

Common examples of this are the cost of telephone calls

or gas and electricity for which we only receive bills

every three months.

o Creditors and Accrued Expenses form part of our Liabilities

because they are unfavourable balances.

43

Charity Funds

Charity Funds are

the amount of money your organisation is worth (on

paper) after collecting all its money in and paying off all

its debts.

the sum of all the annual surplus and deficits over the

years.

o Charity Funds are usually made up of three elements:-

Restricted Funds

Unrestricted Funds (including Designated Funds)

Endowments Funds

44

Reserves

o Reserves are monies set aside for specific purposes from the

Unrestricted Fund.

Examples include:-

to replace equipment

for major repairs

The advantage of reserves is to help management identify how

much is allocated for future costs and how much they may have left

to play with.

o For charitable voluntary organisations, reserves are monies set aside

from the Unrestricted Funds against unforeseen events – a “rainy day

fund”.

The size of the reserves should be fixed by the risks the

organisation faces.

https://www.gov.uk/government/uploads/system/uploads/attachment

_data/file/303074/cc19text.pdf 45

Exercise 4 – Preparing the Balance Sheet

o Using information contained in the previous two

exercises, we can now prepare the balance sheet.

Most of the information for the balance sheet

actually comes from the adjustments we made to

the Receipts and Payments Account

Case Study:- Balance Sheet

Exercise:- Balance Sheet

Answers:- Balance Sheet Answers

46

Final Accounts and External

Scrutiny (1)

Each year, all organisations have to produce Final Accounts.

o For the majority, an external scrutiny is also required in order to fulfil a

legal requirement or a condition of grant aid.

o The Management Committee must make sure it knows which

requirements apply to their organisation and appoint a suitable person to

do this work

o Some organisations are obliged to use a Registered Auditor.

This is someone who is qualified to audit company accounts and is

regulated by one of the professional bodies such as the Institute of

Chartered Accountants.

47

Final Accounts and External

Scrutiny (2)

o A full audit is needed for :

Larger Limited Companies

Charities whose Incoming Resources or Resources

Expended is over £500,000 per year, or if total assets

(before liabilities) exceed £3.26m, and the charity’s gross

income is more than £250,000.

Organisations whose funders make it a condition of

grant aid that full audited accounts must be presented

Organisations whose constitution specifies a full audit

48

Final Accounts and External

Scrutiny (3)

o Most unincorporated charities and voluntary organisations and charities that

are Limited Companies, with income between £25,000 and £500,000 a year

can opt to use an Independent Examiner.

This is someone independent of the organisation that the Management

Committee believes has the required ability and practical experience to

carry out a competent examination.

o For more information on the external scrutiny requirements for charities, go to

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/30

0889/cc15btext.pdf

o As part of the Receipts and Payments Accounts Pack CC16a and the Accruals

Accounts Packs CC17a & CC39a, the Charity Commission also provides

templates for the Independent Examiner’s Report (IER). http://www.charity-

commission.gov.uk/library/ier.pdf

49

Independent Examination or Audit?

50

Content of Final Accounts

o Depending on the size and legal status of an organisation, the annual

accounts can consist of anything from a single page of figures to a hefty

document containing a lot of information.

o A typical set for a charitable voluntary organisation will contain the

following:

Financial Statements covering both the year's transactions and the

position at the year end, which may be:

a Receipts & Payments Account and a Statement of Assets and

Liabilities (SoAL)

or a Statement of Financial Activities (SOFA) and a Balance

Sheet

Notes providing further detail and explanatory information

The Auditor's, Accountant's or Independent Examiner's Report

51

The Trustees Annual Report (TAR) (1)

o The written report which should accompany the Financial

Statements is nowadays seen as at least as important as

the Financial Statements themselves

o As part of the Receipts and Payments Accounts Pack

CC16a and the Accruals Accounts Pack CC39a, the Charity

Commission provides templates for the Trustees’ Annual

Report (TAR) http://www.charity-

commission.gov.uk/library/tar.pdf and a set of guidance

notes

The report template and guidance notes are the same in

both packs

o These templates are intended for smaller charities only. 52

The Trustees Annual Report (TAR) (2)

o An Annual Report for a charitable voluntary organisation will,

depending on the size of the organisation, contain some or all of the

following:

Legal, administrative and other information

Name, address, and registered number of charity

Financial Review on the year

Details of its constitution, trust deed or memorandum and

articles, its charitable objects and its investment powers.

Names and addresses of accountants, solicitors, investment

and other professional advisers.

Names of charity’s trustees with dates of

election/appointment plus method election/appointment

Policies on reserves, awarding grants and making

investments

A review of its major risks

A report on its activities and achievements 53