Embed Size (px)

Citation preview

Finance Act’ 2011

Service TaxPuneet Agrawal,

B. Com (H), CA, LLBPartner

ATHENA LAW ASSOCIATES

1

Public debate on negative list

• Currently, services defined u/s 65(105) are taxed• Public debate on taxing services based on a small negative list

initiated

04/19/23

Scope of New and Amended Services

04/19/23

COVERAGE

04/19/23

S. No

Particulars Effective date

Source of Legislation

1. New Services 01st May, 11

Notification 29/2011-ST dated 25.04.11

2. Amendment in scope of existing services

01st May, 11

Notification 29/2011-ST dated 25.04.11

3. Other changes in the Act

08th April, 2011

Passing of Finance Act

4. Notifications Specific dates

Respective notifications

INTRODUCTION OF

NEW SERVICES

04/19/23

New Services

1. Service provided by a restaurant - Section 65(105)(zzzzv)

2. Service for short term accommodation – Section 65 (105)(zzzzw)

Service provided by a restaurant

Section 65(105)(zzzzv)

04/19/23

Service provided by a restaurant

• Service by Air Conditioned Restaurants having license to serve liquor - Vide Section 65(105)(zzzzv)

– Taxable service means any service provided or to be provided– to any person– by a restaurant having:

» facility of air condition» license to serve liquor

– in relation to serving of food or beverage, including alcoholic beverages

04/19/23

Service provided by a restaurant

• TRU letter clarifies [Annexure A]• Restaurants provide a number of services normally in

combination with the meal and/or beverage for a consolidated charge.

• These services relate to the use of:– restaurant space and furniture, – air-conditioning, – well-trained waiters,– linen,– cutlery and crockery, – music, live or otherwise, or a dance floor. Contd…

04/19/23

Service provided by a restaurant

TRU letter (Annexure A)• Para 1.4: The new levy is directed at services provided by high-end

restaurants that are airconditioned and have license to serve liquor. Such restaurants provide conditions and ambience in a manner that service provided may assume predominance over the food in many situations.

• It should not be confused with mere sale of food at any eating house, where such services are materially absent or so minimal that it will be difficult to establish that any service in any meaningful way is being provided.

• Abatement provision – 30%. • Taxable only if served in the restaurant.

04/19/23

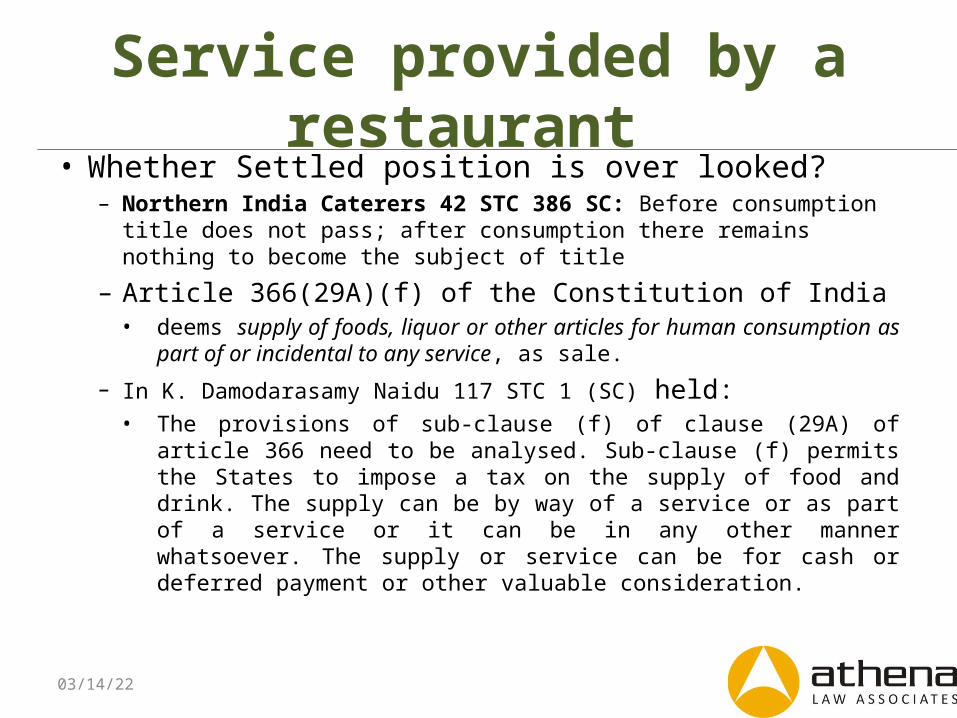

Service provided by a restaurant • Whether Settled position is over looked?

– Northern India Caterers 42 STC 386 SC: Before consumption title does not pass; after consumption there remains nothing to become the subject of title

– Article 366(29A)(f) of the Constitution of India• deems supply of foods, liquor or other articles for human

consumption as part of or incidental to any service, as sale.

– In K. Damodarasamy Naidu 117 STC 1 (SC) held:• The provisions of sub-clause (f) of clause (29A) of article 366 need

to be analysed. Sub-clause (f) permits the States to impose a tax on the supply of food and drink. The supply can be by way of a service or as part of a service or it can be in any other manner whatsoever. The supply or service can be for cash or deferred payment or other valuable consideration.

04/19/23

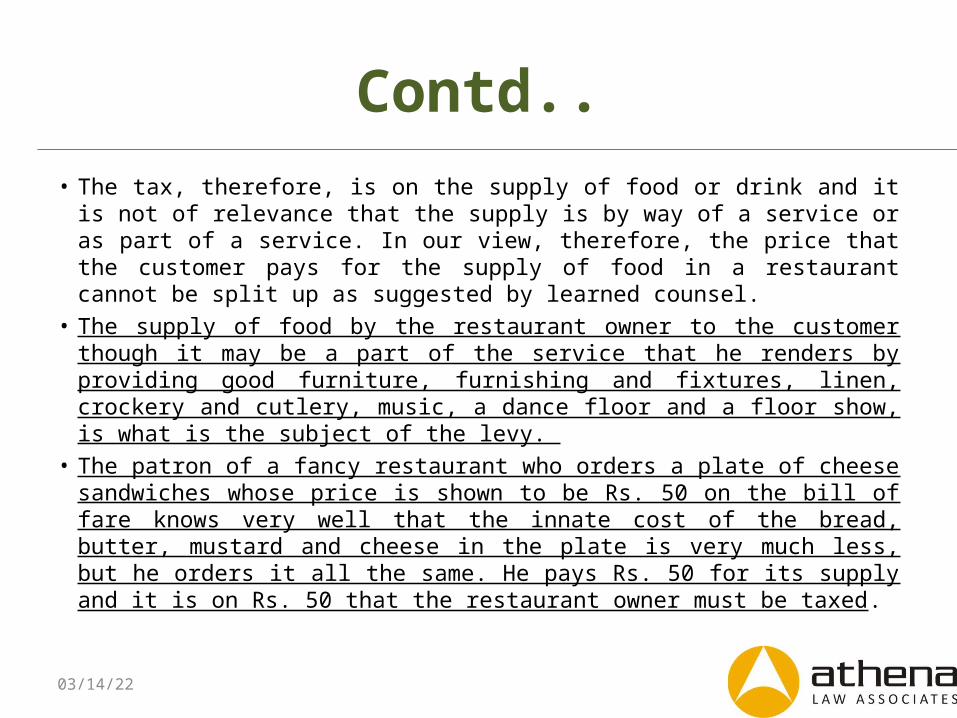

Contd..• The tax, therefore, is on the supply of food or drink and it is not of

relevance that the supply is by way of a service or as part of a service. In our view, therefore, the price that the customer pays for the supply of food in a restaurant cannot be split up as suggested by learned counsel.

• The supply of food by the restaurant owner to the customer though it may be a part of the service that he renders by providing good furniture, furnishing and fixtures, linen, crockery and cutlery, music, a dance floor and a floor show, is what is the subject of the levy.

• The patron of a fancy restaurant who orders a plate of cheese sandwiches whose price is shown to be Rs. 50 on the bill of fare knows very well that the innate cost of the bread, butter, mustard and cheese in the plate is very much less, but he orders it all the same. He pays Rs. 50 for its supply and it is on Rs. 50 that the restaurant owner must be taxed.

04/19/23

Abatement (1/2006-ST)

– Abatement - 70%– Abatement – no option to exclude value of goods

and materials sold and without allowing Cenvat credit

04/19/23

IssuesIssue Response (Circular No. 139/8/2011-TRU)

More than one restaurants belonging to the same entity. Only one satisfy both the criteria

Restaurants, which are clearly demarcated and separately named, the one which satisfy both the criteria is only liable to service tax.

Services provided by taxable restaurant in other parts of the hotel e.g. swimming pool, or an open area attached to a restaurant

Services provided in other parts of the hotel e.g. swimming pool, or an open area attached to the restaurant are also liable to Service Tax as these areas become extensions of the restaurant

Serving by way of room service No. Service is not provided in the premises of the restaurant

Is VAT includible in value for charging service tax

No

Tip to any member of the staff Not includible

04/19/23

Service providedfor

short term accommodation

04/19/23

Service for short term accommodation

– Service provided to any person– Service provided by:

• Hotel• Inn• Guest house• Club or campsite• By whatever name called

– For providing of accommodation for a continuous period less than 3 months

04/19/23

Service for short term accommodation

– If the declared tariff is less than Rs. 1000 per day – exemption [31/2011-ST]

– “declared tariff”:• Includes charges for all amenities provided in the unit

of accommodation like furniture, air-conditioner, refrigerators etc.,

• but does not include any discount offered on the published charges for such unit

04/19/23

Abatement (1/2006-ST)

– Abatement - 50%– Abatement – no option to exclude value of goods

and materials sold and without allowing Cenvat credit

04/19/23

IssuesIssues Response (Circular No. 139/8/2011-TRU)

Is the tax payable on declared tariff or actual amount charged. Declared tariff-Rs 1100, amount charged-Rs. 800

On Rs. 800

Separate declared tariff for separate classes, say-corporate etc

If classes clearly categorised, can be classwise

Does declared tariff include cost of meals Where the declared tariff includes the cost of food or beverages, declared tariff includes cost of meals

off-season prices If separate tariff season-wise, then the declared tariff or that season would apply

Is luxury tax included for determining declared tariff or the actual room rent

For the purpose of service tax, luxury tax has to be excluded from the taxable value

04/19/23

AMENDMENT IN

EXISTING SERVICES

04/19/23

Amendment in existing Services

• Scope of existing Services Expanded

1. Authorized Service Station’s Services - Section 65(105)(zo)

2. Service provided by Club or Association -Section 65(105)(zzze) expanded to include such service provided to non members as well which was earlier restricted to its members only.

3. Services by legal professionals - Section 65 (105) (zzzzm) -

04/19/23

Amendment in existing Services

5. Commercial Training or Coaching Service – Section 65(105)(zzc) – expanded to include all coaching and training that is not recognized by law irrespective of whether the institute is providing any other course(s) recognized by law

6. Life Insurance Service – Section 65(105)(zx) - expanded to include all services, including in relation to management of investments.

7. Business Support Service – Section 65(105)(zzzq) – expanded to include operational or administrative assistance of any kind.

8. Health Service – Section 65(105)(zzzzo) – Scope of service is modifed but service has been fully exempted

04/19/23

Authorized Service Station’s Services Section 65(105)(zo)

04/19/23

Authorized Service Station’s Services

• The definition of “Authorised Service Station” defined under Section 65(9) is omitted

• Amended taxable service:• (zo) to any person, by any other person, in relation

to any service for repair, reconditioning, restoration or decoration or any other similar service, of any motor vehicle other than 3 wheeler scooter auto-rickshaw and motor vehicle meant for goods carriage

04/19/23

Authorized Service Station’s Services

• The existing service is being substituted with a new definition to cover:

– Services provided by any person i.e. whether authorized service station or otherwise;

– All motor vehicles, other than vehicles used for goods transport and three wheeler auto-rickshaws; and

– Repair, re-conditioning or restoration - which are already taxable – and services of decoration and any other related services.

Refer TRU Letter

• Parts if any sold would remain out of the charge in view of Notification 12/2003-ST.

04/19/23

Service provided by Club or Association

Service provided by Club or Association

• Old provision(zzze)» to its members, by any club or association in relation to

provision of services, facilities or advantages for a subscription or any other amount;

• New provision» To its members or any other person, by any club … … … …

… … … … … … … … …

• If a club primarily provides services to its members, then services to non members are also taxable.

04/19/23

Service provided by Club or Association

• TRU clarification:– 4.1 Services provided by a club or association to its members

are already subjected to tax since 2005. When a member avails the facilities for his guest, he is already covered by the existing definition as the services are paid for by the member and not by the guest. However a number of clubs or associations allow non-members to use their facilities in their own capacity for a separate charge. Clubs also entertain members of other affiliated clubs. Such services are proposed to be brought within the revised definition.

04/19/23

Services by legal professionals

04/19/23

Services by legal professionals

• Old provision for taxable Service:– (zzzzm) to a business entity, by any other business entity, in relation to advice,

consultancy or assistance in any branch of law, in any manner:Provided that any service provided by way of appearance before any court, tribunal or authority shall not amount to taxable service.

• Amendment (i) to any person, by a business entity, in relation to advice, consultancy or assistance

in any branch of law, in any manner;(ii) to any business entity, by any person, in relation to representational services before any

court, Tribunal or authority;(iii) to any business entity, by an arbitral Tribunal, in respect of arbitration.

(19b) “business entity” includes an AOP/BOI/company/firm but does not include an individual

04/19/23

Services by legal professionals

- The scope of the existing service is being expanded to include:

• Services of advice, consultancy or assistance provided by a business entity to individuals as well;

• Representational services provided by any person to a business entity; and

• Services provided by arbitrators to business entities.- Services provided by individuals to other individual

will remain outside the levy.- Stayed till 23.05.11 by Delhi HC (WPC 2792/2011)

and Gauhati HC04/19/23

CA/CS/CWA Service

• Exemption on representation service withdrawn [25/2006-ST]

Notification No.33/2011 - ST F. No. 334/3/ 2011 TRU Dated 25th April, 2011

04/19/23

Commercial Training or Coaching Service

04/19/23

Commercial Training or Coaching Service

– Old definition of “commercial training or coaching centre”:

» means any institute or establishment providing commercial training or coaching for imparting skill or knowledge or lessons on any subject or field other than the sports, with or without issuance of a certificate and includes coaching or tutorial classes but does not include preschool coaching and training centre or any institute or establishment which issues any certificate or diploma or degree or any educational qualification recognised by law for the time being in force;

• Underlined are omitted – vide finance bill

04/19/23

Commercial Training or Coaching Service

• Effect of changes:– Presently, where an institute which provides any degree

recognized under law, the institute as a whole is outside the purview of service tax even with respect to a course not recognized under law.

– Under proposed changes - No exclusion for institutes providing any course recognized by law.

04/19/23

Exemption

• Exemption from levy of service tax for the followings:• any preschool coaching and training; • any coaching or training leading to grant of a certificate or

diploma or degree or any educational qualification which is recognised by any law for the time being in force; to pre school training and to courses recognized by law.‑

Notification No.33/2011 - ST F. No. 334/3/ 2011 TRU Dated

25th April, 2011

04/19/23

Issue

• Institutes imparting education– INST. OF CHARTERED FIN. ANALYSTS OF INDIA 2009 (14)

S.T.R. 220 (Tri. – Bang)– CENTRE FOR DEV. OF ADVANCED COMPUTING 2009 (14)

S.T.R. 165 (Tri. – Bang)– MAGNUS SOCIETY 2009 (13) S.T.R. 509 (Tri. – Bang)

04/19/23

Life Insurance Service

04/19/23

Life Insurance Service

• Old taxable service– to a policyholder or any person, by an insurer, including re-

insurer carrying on life insurance business in relation to the risk cover in life insurance;

• Amended taxable service– to a policyholder or any person, by an insurer, including re-

insurer carrying on life insurance business.

04/19/23

Life Insurance Service

– The scope of this service is proposed to be expanded to cover all services, including in relation to management of investments.

• Unlike now where in non ULIP policies, only risk portion of the life insurance policy is chargeable to service tax, it is proposed to charge service tax on the total amount of the premium which is not invested.

• Thus amount retained for risk cover, commission and expenses, etc would be chargeable to tax.

• An option to charge tax @ 1.5% is also given R6(7A) of STR.

04/19/23

Value [Rule 7(7A) of STR]

Case Break up of investment given

Value Pay @1.5% of gross premium

Premium (risk + investment)

Yes Premium less amount invested

No

Premium (risk + investment)

No Not determinable

Yes

Premium (risk only)

NA Full premium No

04/19/23

Business support service

Business support service

– It is proposed to rephrase the clause ‘operational assistance in marketing’ with “operation and administrative assistance”.

– The proposed clause would have wider scope and thus services of routine administration, even if not related to marketing would be chargeable to tax.

04/19/23

Health Service

Exemption

• Fully exempted vide Notification No.30/2011 - Service Tax F. No. 334/3/ 2011 TRU Dated 25th April, 2011

04/19/23

Rate of service Tax - Air Travel Service

• Incase of domestic Travel– The upper ceiling of service tax in case of domestic travel by

economy class has been increased from Rs. 100 to Rs. 150– Other classes would be chargeable to tax flat @10.3%.

• In case of international travel – If by economy class, ceiling of service tax has been raised from

Rs. 500 to Rs. 750.– On other than economy class, tax would continue to be

charged at 10.3%.

Notification 4/2011, Effective date – 01.04.2010

04/19/23

Assessment/ Penalty etc

04/19/23

Assessment (S. 73) – old provisions

Sec. issue option effect

73 (1A) andProviso to 73 (2)

(1A) Where any service tax has not been levied by reason of fraud/collusion etc, with intent to evade payment of service tax, by a person to whom a SCN is served

such person may pay:-service tax -Interest, and -penalty equal to twenty-five per cent of the service tax within thirty days of the receipt of the notice.

Proceedings deemed completed

04/19/23

Now omitted

Assessment (S. 73) – new provisions

Sec. issue option effect

73 (4A)

•During course of investigation/ audit/ verification – found that service tax has not been paid •True and complete details available in specified records•No SCN issued

• may pay the amount of such- service tax, -Interest, and -Penalty = 1% p.m. / max 25%• And inform excise officer

•No SCN would be issued•Proceedings deemed completed

04/19/23

specified records" means records including computerised data as are required to be maintained by an assessee in accordance with any law, or where there is no such requirement - the invoices recorded by the assessee in the books of account

Penalty provisions-S.78Sec. Situation Particulars Penalty

(S.78)Comments

78 (1)

•Service tax has not been levied by reason of fraud/ collusion with intent to evade service tax •SCN issued and adjudicated

True and complete particulars of transaction not available in specified records

Pay penalty = service tax

•Earlier - 100% - 200% of tax evaded•No remission u/s 80

Proviso

•Service tax has not been levied by reason of fraud/ collusion with intent to evade service tax •SCN issued and adjudicated

True and complete particulars of transaction available in specified records

Pay penalty = 50% of service tax

•If paid within 30 days of adjudicationPenalty = 25% of service tax •(For small service providers 90 days)•Remission possible u/s 80

04/19/23

Penalty – u/s 76/ 77

Period Penalty MaximumEarlier 2% p.m. / Rs. 200 per day

(whichever higher)100% of tax

Now 1% p.m. / Rs. 100 per day (whichever higher)

50% of tax

04/19/23

Section 77 – Miscellaneous penalty – Non registration/ non maintenance of accounts/ Non issuance of invoice/ Other offences for which no separate penalty – Earlier – Rs. 5,000Now – Rs. 10,000

Interest

Sec. Normal

Small taxpayer

75 Rate of interest 18% 15%Small taxpayer means – Where SCN issued – during any of the F.Y. covered by SCN, taxable value did not exceed 60 LakhOtherwise - taxable value did not exceed 60 Lakh in the preceding F.Y.

04/19/23

Power to Search

S. 82 Authorisation Search by Old law CCE AC/DC or by CCENew Law Jt. CCE Superintendent or

CCE himself

04/19/23

S. 88 - Liability under Act to be first charge.—• Notwithstanding anything to the contrary contained in any

Central Act or State Act, • any amount of duty, penalty, interest, or any other sum

payable under this Chapter, • shall, save as otherwise provided in section 529A of the

Companies Act, and the Recovery of Debts Due to Banks and the Financial Institutions Act and the Securitisation and Reconstruction of Financial Assets and the Enforcement of Security Interest Act, 2002

• be the first charge on the property of the assessee or the person as the case may be.

04/19/23

S. 89 - Prosecution

Offence No. 1Whoever(a) provides any taxable service chargeable to service tax under sub-section (1) of section 68 or receives any taxable service chargeable to tax under sub-section (2) of said section, without an invoice issued in accordance with the provisions of this Chapter or the rules made thereunder; or

04/19/23

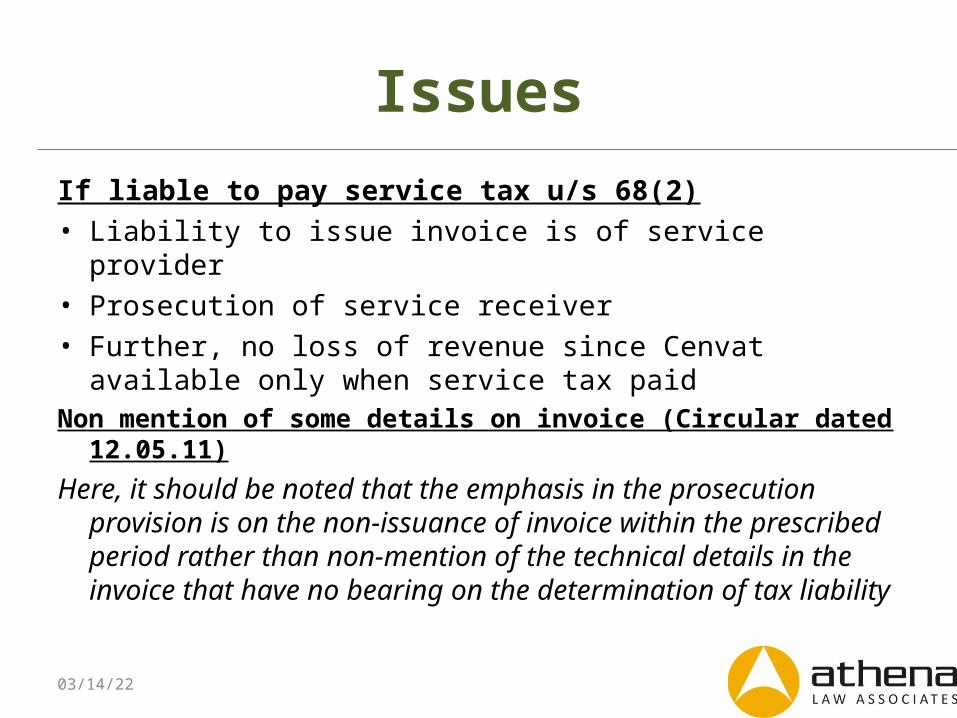

Issues

If liable to pay service tax u/s 68(2)• Liability to issue invoice is of service provider• Prosecution of service receiver• Further, no loss of revenue since Cenvat available only when

service tax paidNon mention of some details on invoice (Circular dated 12.05.11)

Here, it should be noted that the emphasis in the prosecution provision is on the non-issuance of invoice within the prescribed period rather than non-mention of the technical details in the invoice that have no bearing on the determination of tax liability

04/19/23

Purpose of prosecution provisions

• While minor technical omissions or commissions have been made punishable with simple penal measures (under section 77), prosecution is meant to contain and tackle certain specified serious violations

• Circular dated 12.05.11

04/19/23

Offence No. 2

• avails and utilises credit of taxes or duty without actual receipt of taxable service or excisable goods

• either fully or partially in violation of the rules made under the provisions of this Chapter

Invoice shopping without receipt of actual services/ goods Credit must be taken AND utilised

04/19/23

Offence No. 3•maintains false books of account or •fails to supply any information which he is required to supply •Or supplies false information (unless with a reasonable belief, the burden of proving which shall be upon him, that the information supplied by him is true)

Mis-statement as to material particularsIt should be noted that the offence in relation to maintenance of false books of accounts or failure to supply the required information or supplying of false information, should be in material particulars have a bearing on the tax liability [Circular dated 12.05.11]

04/19/23

Offence No. 4

• collects any amount as service tax • but fails to pay the amount so collected • beyond a period of six months from the date on which such

payment becomes due

Issues• Payment becomes due even if payment not received• Mere non payment not covered• Only after collection, if there is non payment

04/19/23

Punishment

First time offender1. in the case of an offence where the amount exceeds fifty lakh rupees - with imprisonment upto three yearsMinimum - six months (can be waived only if there exists special and adequate reasons)2. in cases involving less than 50 Lakh - upto 1 yr3. No prosecution below 10 lakh (unless contg offence)- Circular•These monetary limits are of tax effect because of offence

Subsequent offender – upto 3 yrs

04/19/23

Prosecution

Special reasons for non prosecution• Age of offender/ first time offence/ levy of penalty/ accused being

secondary offender• Are not special reasons

In case of company/ Firm etc 9AA of CEA–• Every person responsible for conduct of business shall be liable for

prosecution• He may prove that without knowledge or that he exercised due

diligence• If consent/ connivance of manager/Director/ Secretary or other

officer – they shall be liable for prosecution

04/19/23

Presumption of culpability S 9C of CEA

• In any prosecution - the Court shall presume the existence of such mental state

• Accused may prove that he had no such mental state with respect to the act charged as an offence in that prosecution.

• Explanation. — In this section, “culpable mental state” includes intention, motive, knowledge of a fact, and belief in, or reason to believe, a fact.

• For the purposes of this section, a fact is said to be proved only when the Court believes it to exist beyond reasonable doubt and not merely when its existence is established by a preponderance of probability.

04/19/23

Re-categorisation of the services for the purpose of

Export of service Rules/Import Rules[Notification 12/2011 ST and 13/2011 ST, effective date 01st April 2011]

04/19/23

Re-categorisation

• Index• Category (i)- situation of immovable property • Category (ii)- place of performance• Category (iii)- place of recipient

• Due to re-categorisation of services, criteria for a service to qualify as export/ import would change.

04/19/23

re-categorisationS. No. Head of service Old category New category

1. Preferential location and similar services (iii) (i)

2. Rail Travel Agent (iii) (ii)

3. Health service (iii) (ii)

4. Credit rating agency (ii) (iii)

5. Market research agency (ii) (iii)

6. Technical testing and analysis (ii) (iii)

7. Goods transport agency (ii) (iii)

8. Transport of goods by air (ii) (iii)

9. Opinion poll (ii) (iii)

10. Transport of goods by rail (ii) (iii)

11. Restaurant service (new service) - (i)

12. Short term accommodation service (new service) - (i)

04/19/23

Consequential exemption1. Since transportation of goods by road/ air/ rail has been brought in

category (iii), if a person in India receives service of transportation of goods from one foreign destination to another destination outside India, the said service has been specifically exempted.

[Notification 8/2011 ST, effective date 01st April 2011] 2. Freight for transport of goods by air, to the extent included in customs

value would also not be chargeable to service tax. [Notification 9/2011 ST, effective date 01st April 2011]

04/19/23

Exemption to SEZ [Notification 17/2011 ST, effective date 01st March 2011]

• Exemption notification No. 9/2009 has been superseded vide this notification

• various anomalies which earlier existed are sought to be corrected.

• The exemption would partly work as outright exemption and partly by way of refund.

• The notification has overcome the problem created by the decision in Jindal Drug case Final Order No. 900A to 1143 A-2009 EX(DB)(12.08.09) (Tribunal)

• Services consumed in SEZ get outright exemption

04/19/23

Other Exemption

• Notification No. 5/2011, Effective date 01st March 2011– Exhibitor of business exhibitions organizing business exhibitions outside India

have been exempted from service tax.– Thus, if clients of India avail services of such organizer, but unable to pay in

foreign currency, the services would be exempt from tax notwithstanding that the said service would not qualify as export of service.

04/19/23

Packaged Software

Case 1• Value under section 4A of CE• Don’t pay service tax [notification 53/2010-ST]Case 2• Value of media pack – section 4 • Pay service tax on value of right to use

04/19/23

![ATHENA - Coordinate System Document...[RD02] ATHENA Mission Requirements Document (MRD), ATHENA-ESA-URD-0010 [RD03] ATHENA Product Tree, ATHENA-ESA-PT-0001 [RD04] Ariane 5 User’s](https://img.pdfslide.us/doc/110x75/5ff23cd84225de2c7f4f21b6/athena-coordinate-system-document-rd02-athena-mission-requirements-document.jpg)