Embed Size (px)

Citation preview

Finance 300Financial Markets

Lecture 4

Professor J. Petry, Fall, 2002©

http://www.cba.uiuc.edu/jpetry/Fin_300_fa02/http://webboard.cites.uiuc.edu/

2

HousekeepingKeep your eyes on the calendar from the web-site.

• mid-term is 9/17 covering chapters 1-3—a week from today! • equity analysis project begins now.

– Teams today.– Sign-up after 1:00 pm Thursday at Prof Oltheten’s office 225DKH

Know material both in text and in my notes. • There is generally a very high degree of overlap. • You will NOT be tested on readings at end of chapters.• Notice that in this chapter in particular, the material is the

same, but the order is slightly different.

3

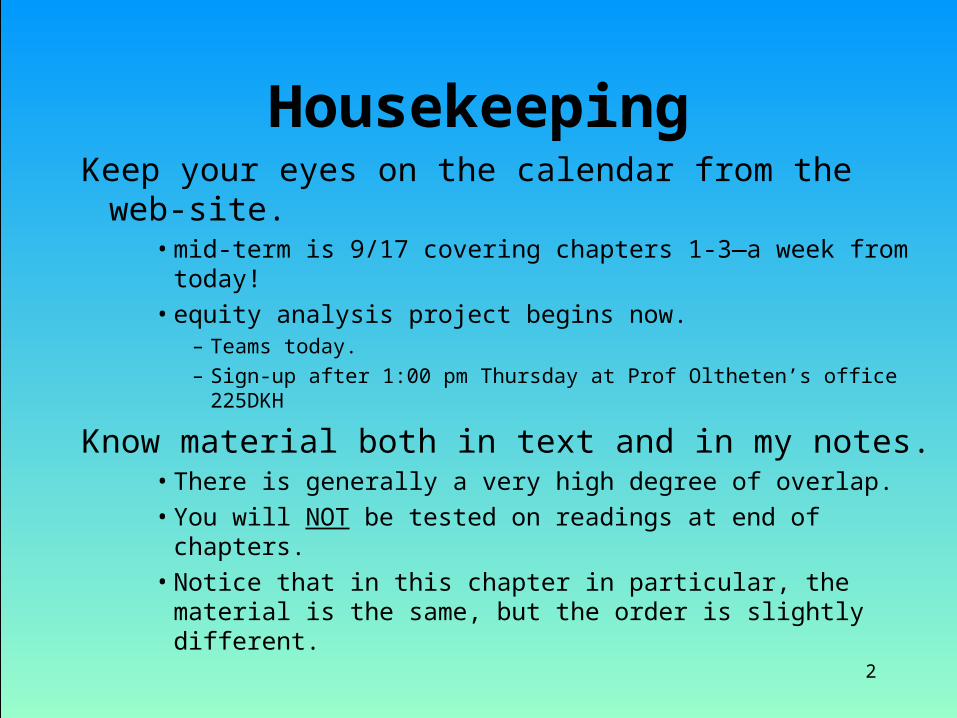

Capital Asset Pricing Model (CAPM)• First developed by Harry Markowitz in the 1950s• Is now a fundamental underlying principle of financial

analysis, and earned him a Nobel Prize• Attempts to quantify the relationship between risk and

return• States that risk is either market risk (systematic risk,

undiversifiable risk), or firm specific risk (diversifiable risk).

• Because individuals can diversify away firm specific risk, the only thing they should care about is market risk.

4

Risk Premium for stock pRisk Premium for stock p Market Risk PremiumMarket Risk Premium

ii= risk free rate, i.e. the stock’s expected return if the= risk free rate, i.e. the stock’s expected return if the market’s excess return is zeromarket’s excess return is zero

ßßpp(E(R(E(RMM)-r)-rff)) = the component of return due to= the component of return due to

movements in the market indexmovements in the market index

E((RE((RMM)- r)- rff)) = 0 = 0 rf

fMpfp rRERE r )(

Capital Asset Pricing Model (CAPM)

5

Capital Asset Pricing Model (CAPM)• The risk of a stock is fully defined by its “Beta”, and the

return to a stock should be directly proportional to its Beta.

• Beta is a market sensitivity index.• B > 1 means stock is highly sensitive to market moves

– If B =1.5, a market move of 10% would result in 15% move for this particular stock (aggressive stock pick)

• B=1 means stock is right in line with overall market sensitivity• 0<B<1 means stock moves mute the moves of the overall market

– If B = .5, a market move of 10% would result in a 5% move of the individual stock

• B<0 means the stock moves in the opposite direction of the market (and provides an opportunity to hedge)

6

Capital Asset Pricing Model (CAPM)• Beta is found running a regression between market returns and the

individual assets returns—the market model. The slope of this regression is the “characteristic line” for the stock, the slope of which is the stock’s beta.

• The Beta of a portfolio is found by taking a weighted average of the betas of the stocks making up the portfolio. (know how to calculate this)

• While you cannot diversify away market risk, you can control your exposure to that risk via choice of beta.

• Assume we have:– Risk Free Rate = 3.2%– S&P Average Rate of Return = 11.2%– Risk Premium = 8.0%

• The graphical representation of CAPM would look like:

7

Security Market Line

0

5

10

15

20

25

0 0.5 1 1.5 2

Systematic Risk (ß)

E(R

)

Market Portfolio11.2%

Risk Free Rate3.2%

Risk Premium8.0%

Where should the above labels go on the graph?

8

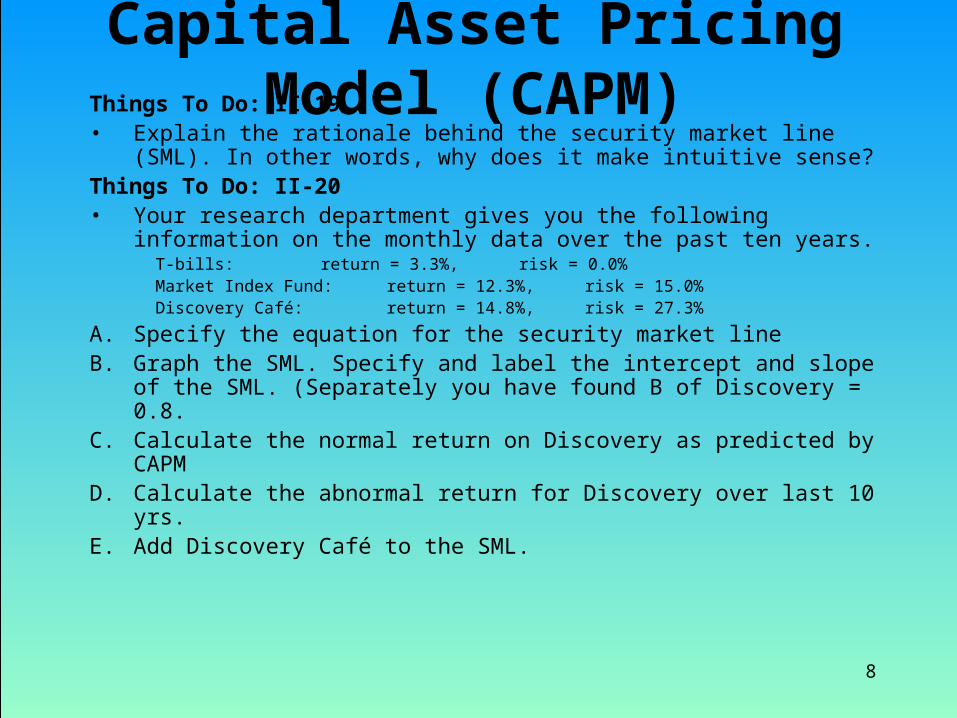

Capital Asset Pricing Model (CAPM)Things To Do: II-19• Explain the rationale behind the security market line (SML). In other

words, why does it make intuitive sense?Things To Do: II-20• Your research department gives you the following information on the

monthly data over the past ten years.T-bills: return = 3.3%, risk = 0.0%Market Index Fund: return = 12.3%, risk = 15.0%Discovery Café: return = 14.8%, risk = 27.3%

A. Specify the equation for the security market lineB. Graph the SML. Specify and label the intercept and slope of the SML.

(Separately you have found B of Discovery = 0.8.C. Calculate the normal return on Discovery as predicted by CAPMD. Calculate the abnormal return for Discovery over last 10 yrs. E. Add Discovery Café to the SML.

9

Chapter III-Equity & Equity Markets

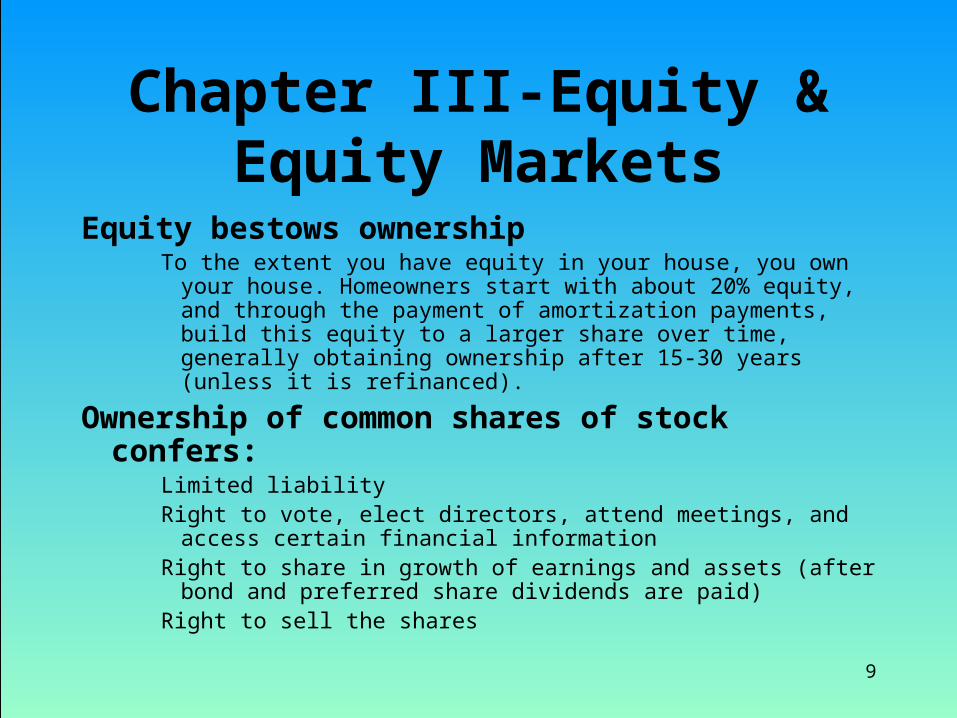

Equity bestows ownershipTo the extent you have equity in your house, you own your house.

Homeowners start with about 20% equity, and through the payment of amortization payments, build this equity to a larger share over time, generally obtaining ownership after 15-30 years (unless it is refinanced).

Ownership of common shares of stock confers:Limited liabilityRight to vote, elect directors, attend meetings, and access certain

financial informationRight to share in growth of earnings and assets (after bond and

preferred share dividends are paid)Right to sell the shares

10

Chapter III-Equity & Equity MarketsEquity

Authorized sharesThe maximum number of shares the firm may offer under the terms of its charter

Outstanding sharesThe total number of shares authorized and sold by the firm

Treasury sharesShares the corporation has repurchased and holds (guess where?). Treasury

shares carry no voting rights and do not earn dividends.

Classified StockCommon Stock may be separated into different classifications, generally labelled

Class A, Class B, Class C, etc. The differences between classes are often voting rights and payment of dividends. Each firm has its own methods and definitions which must be investigated.

11

Chapter III-Equity & Equity MarketsDividends

A distribution to stockholders, usually in cash, or sometimes in shares. Dividend payments are determined by Board of Directors, generally done quarterly, but is not required.

Declaration DateThe day the BOD officially declares the dividend. This announcement includes the

dividend amount, the record date, and the pay date.

Record DateThe date on which you must be the registered holder of the shares in order to

receive the dividend

Ex-dividend DateThe date at which the price of the stock trades without the dividend, generally about

4 days before the “date of record”. If you buy the stock before the ex-date, you will own it in time to receive the dividend.

12

Chapter III-Equity & Equity MarketsPayable Date

The date the dividend is actually paid out.

Things to Do (like question):You buy 10,000 shares of Caterpillar (CAT) on January 10 at $80, sell

$4,000 shares on January 11 at 79-1/2, and sell the remaining 6,000 shares on January 17 at $82. Caterpillar paid a dividend of $.50 with an ex-date of January 11 and a pay-date of February 12.

A. How much in dividends do you receive?B. What is the holding period return on this investment (assume no

commission)?

13

Chapter III-Equity & Equity MarketsStock Splits and Consolidations

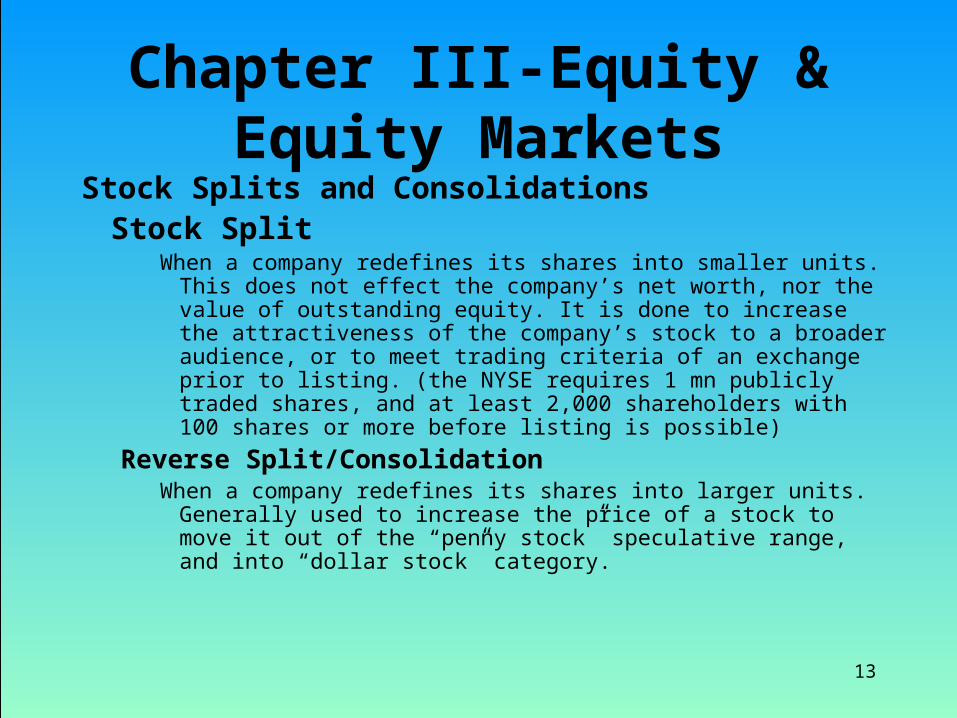

Stock SplitWhen a company redefines its shares into smaller units. This does not

effect the company’s net worth, nor the value of outstanding equity. It is done to increase the attractiveness of the company’s stock to a broader audience, or to meet trading criteria of an exchange prior to listing. (the NYSE requires 1 mn publicly traded shares, and at least 2,000 shareholders with 100 shares or more before listing is possible)

Reverse Split/ConsolidationWhen a company redefines its shares into larger units. Generally used to

increase the price of a stock to move it out of the “penny stock” speculative range, and into “dollar stock” category.

14

Chapter III-Equity & Equity MarketsSecurities and Exchange Commission

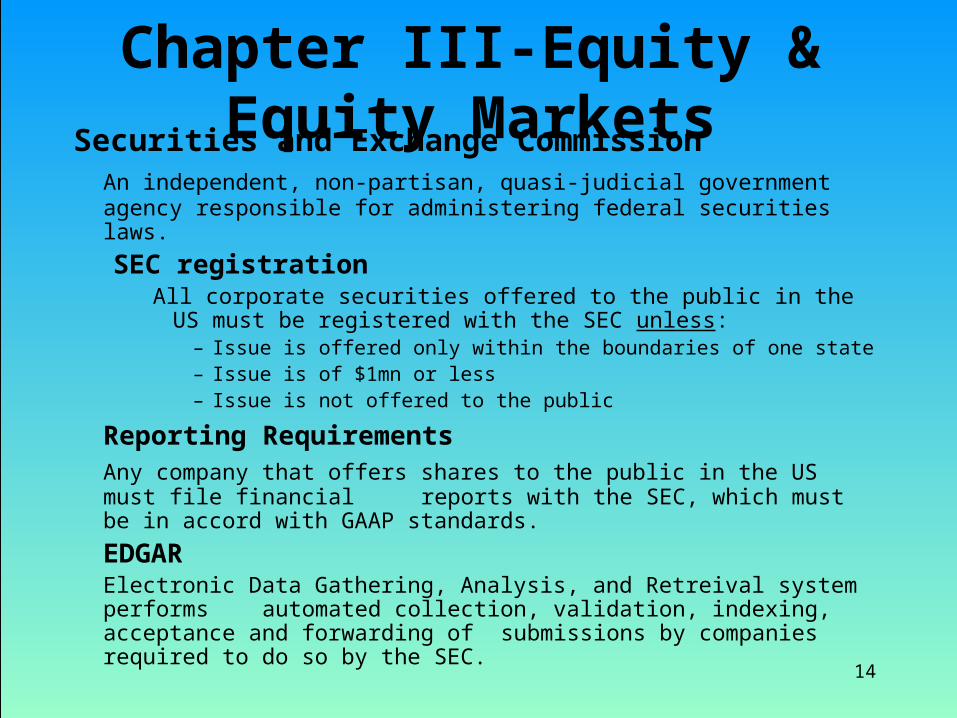

An independent, non-partisan, quasi-judicial government agency responsible for administering federal securities laws.

SEC registrationAll corporate securities offered to the public in the US must be registered

with the SEC unless:– Issue is offered only within the boundaries of one state– Issue is of $1mn or less– Issue is not offered to the public

Reporting RequirementsAny company that offers shares to the public in the US must file

financial reports with the SEC, which must be in accord with GAAP standards.

EDGARElectronic Data Gathering, Analysis, and Retreival system performs

automated collection, validation, indexing, acceptance and forwarding of submissions by companies required to do so by the SEC.

15

Chapter III-Equity & Equity MarketsPrimary Markets

Initial Public OfferingsThe first time a firm sells shares to the public

Seasoned OfferingAn issue of new shares to the public by a firm that is already

publicly owned

UnderwriterBrokerage firm or investment bank that assists in development of a

new issue (sets the price, markets the issue).

Registration StatementInformation provided by a firm to the SEC and public as a part of its

IPO. Contains information about the firm, management, markets and the security, as well as certified financial statements.

16

Chapter III-Equity & Equity MarketsPrimary Markets

Red Herring

A preliminary prospectus, which can be circulated while the Registration Statement is being approved, is not an offer to sell, nor does it have a price. Hot Issue

When an IPO immediately begins trading at a higher price in the secondary market than the public offer price. Demand exceeds supply for the issue.

17

Chapter III-Equity & Equity MarketsPrimary Markets

Private Placements

When the entire issue is offered to accredited investors (generally institutional investors) rather than to the general public. No SEC registration is required. Corporate and financial information is circulated through a Private Placement Memorandum instead of a prospectus. Accredited Investors

Defined by the SEC as those who are able to analyze the risk and return characteristics of an offering and have the financial resources to bear those risks.

18

Chapter III-Equity & Equity MarketsPrimary Markets

RightsSubscription right is a distribution to existing shareholders

of a negotiable right to buy newly issued shares of the company at a subscription price. The subscription price is often below the offer price at which the stock is offered to the general public.

A right usually has a life of a few weeks, and during this time, trades on the secondary market.

Things to Do (like question):Ferengi Exports Inc (QRK) issues new stock with a

subscription price of $28. Under the terms of the offering four rights are required to subscribe to one new share. Is existing shares of QRK are trading at $32, where should QRK rt trade?

19

Chapter III-Equity & Equity MarketsPrimary Markets

American Depository Receipts (ADRs) and Shares (ADSs)Means to facilitate the holding of foreign stocks by Americans

American Depository Shares (ADSs) or Sponsored ADRsA negotiable receipt representing common stock of a foreign

company held in trust by a foreign bank. ADS holders are registered with the issuing firm as shareholders and have equal rights with other shareholders. Firm must provide quarterly and annual reports in English and distribute dividends in dollars.American Depository Receipts (ADRs) (Unsponsored ADR)

A negotiable reciept representing common stock of a foreign firm held in trust in a US bank. ADR holders are entitled to dividends and capital gains. The issuing firm is not involved in the issuance of the ADR. The US bank is the registered owner of the shares, and is responsible for translating earnings statements, etc

20

Chapter III-Equity & Equity MarketsSecondary Markets

Stock ExchangeAn organized market where member brokers buy and sell securities for

themselves and their clients.

SeatTo trade securities on an exchange you must be a member or sit on the

exchange. The number of seats are fixed, and can be bought and sold for a market determined price.

Listing RequirementsOnly issued listed with the exchange may be traded. Each exchange has

specific listing requirements. An issue may be listed on more than one exchange.

Board Lot (Round Lot)Refers to the trading unit defined by the exchange. Odd or Broken lots

carry a higher sales commission or trade at less advantageous prices than Board Lots.

21

Chapter III-Equity & Equity MarketsMarket Concepts & Terminology

Continuous MarketMarket prices are determined continuously through the hours the

market is open.

Call MarketOrders are collected for the next auction, which take place at regular

intervals during the day. Each auction determines the market clearing price or fix.

TransparencyThe absence of closed door deals. All market participants are fully and

rapidly informed, keep profit-making from private information to a minimum.

Execution CostThe difference between the execution price of a security and the price

that would have existed in the absence of that trade.

22

Chapter III-Equity & Equity MarketsMarket Concepts & Terminology

Information Based TradeA trade made because an informed trader believes she has information

not yet reflected in the absence of that trade.

Informationless TradeA trade made by a liquidity trader to reallocate her portfolio, not based

on a real or perceived informational advantage.

23

Chapter III-Equity & Equity MarketsBrokers & Dealers

BrokerAn agent of an investing client; the broker takes no position in the

securities she trades.

DealerA dealer maintains her own positions in the securities traded, thereby

supplying immediacy. Immediacy is the ability to trade as soon as the order hits the floor rather than wait for the coincidence of buyers and sellers.

Market MakerA dealer who guarantees that she will always stand ready to buy and to

sell shares in the stock in which she makes a market. This insures there is always a market for the issue. Market makers always have a bid (at which she will buy) and an ask (at which she will sell), providing a continuous auction market.

24

Chapter III-Equity & Equity MarketsBrokers & Dealers

SpecialistThe dealer designated by the exchange as the only market maker on

the floor of the exchange for specifically assigned stocks. The specialist executes orders for other brokers, and is required to maintain fair and orderly markets.

The specialist also opens the market by examining the orders which have accumulated overnight, and setting the opening price such that the market will clear at the opening bell. Thus the market is continuous from during the course of trading hours, but opens with a call market in which the opening price is fixed.