Embed Size (px)

Citation preview

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 1/47

1.1 INTRODUCTION OF THE STUDY

Running a successful small business requires adept navigation of the many choices created

by an ever changing market place. Cost Volume Profit Analysis (CVPA) is an effective

tool that can help its user answer important questions you may have about pricing your

products and services, whether or not to invest in additional capital items, and which

products and services to emphasize.

Fixed Semi-Variable and Variable Costs:

Before the CVPA can be used, fixed, semi-variable and variable costs must be determined.

Determining these costs is a very useful tool in itself, but that's another white paper.

Fixed costs are those costs that your business incurs regardless of sales volume. These are

costs such as rent, insurance, and annual business licensing fees. Sales volume, not

exceeding your current capacity, has no effect.

Variable costs are those costs that are directly affected by sales volume. These include

items such as cost-of-goods sold, sales commissions, and travel expenses, if you are a

service provider that travels as a result of service provision.

Semi-variable costs, as you have determined by now, are those costs that increase with

sales volume but not directly as with variable costs. An example of a semi-variable cost for

an auto body shop might be equipment maintenance expense. At some point, equipment

begins to break down if not maintained at a level consistent with increased use. Therefore,

in order to avoid equipment breakdown due to hyper-use, the business owner must spend

additional funds on maintaining equipment.

Break-Even:

There are several benefits to using CVPA. First, it shows what the break-even point, in

units or dollars, for a given product or service is, given a specified sales price. Break-even

is the point at which sales revenue covers all fixed costs for the year plus all variable costs

up to that sales point. .

CVP analysis can be used for analyzing price sensitivity.

1

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 2/47

Contribution Margin

Determining the contribution margin for your business is an additional benefit of CVPA.

Contribution margin is simply the amount of each sales dollar left after all variable costs

have been covered. It is that portion of the sales dollar that can be devoted to covering

fixed costs.

Knowing your overall contribution margin is beneficial because it can be compared to

prior periods to determine if it is trending positively or negatively. Additionally,

contribution margin analysis can be applied to individual products, product lines, services,

or service lines. Knowing the contribution margin of a particular product or service can

help determine if carrying that product or performing that service over another is the best

decision. Moreover, understanding contribution margin is very helpful in developing the

best pricing strategy for your business.

One final benefit to knowing how to determine contribution margin is that it can point out

your most profitable products or services, even though sales may indicate something

different.

Operating Leverage

Operating leverage is the degree to which a business uses fixed costs to generate profit.

The greater the degree of fixed cost reliance, the greater the increase in profits during a

sales up-trend and the greater the loss in a sales down-trend.

As fixed assets usually carry fixed costs, financed payments for the equipment, additional

insurance, etc., investing in additional equipment is something our auto body shop owner

will want to seriously consider if the up-ward sales trend she is experiencing is something

she believes to a be long-term phenomenon. If she believes the sales up-trend to indeed be

long-term, then investing in additional fixed assets may be just the thing for her to do.

CVPA is one tool our auto body shop owner can use to help her determine what to do in

this situation. By using her break-even model and considering contribution margins, she

2

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 3/47

can perform sensitivity analyses to help her determine whether or not to increase her

operating leverage in an effort to take advantage of a sales up-trend.

Summary:

CVPA is a tool that can be used to help answer questions you may have about pricing your

products and services, whether or not to invest in additional capital items, and which

products and services to emphasize. While there is no one magic bullet, CVPA is a nice

tool to have in your business analysis bag to help you make good decisions when

answering these types of questions.

3

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 4/47

1.2 NEED OF THE STUDY

The study is carried out mainly to make profit planning by forecasting activity level

in order to gain or maintain specified amount of profit. It also present cost data for control

purposes. It also facilitates the company to take make or buy decision. It also helps to

analyze the profitability of a multiple-product firm with a constant sales mix. This analysis

is important to select the best alternative method yielding highest contribution.

This study helps the company to determine changes in profit due to changes in

sales volume. Sales required to meet proposed expenditure also determined in this study.

CVP analysis is often used to develop an understanding of the

overall operations of an organization.

4

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 5/47

1.3 OBJECTIVES OF THE STUDY

Primary objective

To study the Cost-Volume-Profit analysis of WABCO-TVS (INDIA)

LIMITED.

Secondary objectives

1. To analyze how the change in selling price and change in cost affect

the profit position of the company.

2. To find out the breakeven point of sales and margin of safety that helps

in taking policy decision like reduction in price to face the competitors.

3. To predict profit over a wide range of volume.

4. To determine the optimum mix of the company.

5. To estimate the volume to be produced for obtaining a desired profit

5

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 6/47

1.4 SCOPE OF THE STUDY

This study is performed by using the annuity report of WABCO-TVS(INDIA)

LTD. The analysis done are Breakeven analysis, profit volume, etc., these calculation

cover the major areas like contribution margin, profit, margin of safety. This would be

useful for company to make new strategy to compete in the market by adopting various

controlling techniques in the process of manufacturing.

This study was conducted on cost volume profit analysis and on each and every

variables. This study to help to forecast profit fairly and accurately as it is essential to

know the relationship between profits and costs.

This study assists in evaluation of performance for the purpose of control and also

assists in formulating policies by showing the effect of different price structure on costs

and profits.

6

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 7/47

2.1 INDUSTRY PROFILE

The global auto component industry could be the next big success story after software,

pharmaceuticals, BPO and textiles. The size of the global auto component industry is

approximately $1 trillion. The leading auto component manufacturers (OEM) in the world

are Ford Motors ,General Motors (GM), Delphi Corporation, Caterpillar, International

Truck and Engine Corporation and Cummins. The US is the world’s biggest auto

component market. In 2002 it imported auto component worth $69 bn.

Currently, the automotive component industry is an important sector of the Indian

economy and a major foreign exchange earner for the country. There are around 400 major

players in the auto component sector. The automotive component industry manufactures a

wide range of parts including casting, forging, finished, semi-finished components,

assemblies, and subassemblies for all types of vehicle products in India.

Evolution of Indian auto component industry

The Indian auto component Industry has always been rising over the Indian Automobile

industry. The component industry started out small in the 1940’s supplying components to

Hindustan Motors and premier automobiles. In the 1950’s the arrival of Telco, Bajaj, and

Mahindra & Mahindra led to steadily increasing production.

In the 1980’s with Maruti, the growth suddenly accelerated. Boom time for auto

components industry started with the arrival of India’s “people’s car” - the Maruthi. As

Maruthi became India’s best selling car, the path of India auto component industry took anupswing. Export figures also climbed. Low costs of labor and raw materials resulted in

exports taking a quantum jump.

The new car required components that would adhere to its stringent quality standards. It

virtually gave birth to a variety of new age auto component manufacturers who

manufactured components that combined the best to technology with quality.

7

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 8/47

The influx of foreign auto majors ranging from Mercedes Benz, Ford, and General Motors

to Daewoo few years ago presented a world of opportunity for the industry. The auto

components industry responded with huge capacity expansion and modernization

programs. Growth in the commercial vehicle and the passenger car segments has been 20

percent year on year and 40 percent year on year from year 2000 onwards

.

India’s automotive component industry manufactures the entire range of parts required by

the domestic automobile industry and currently employs about 250000 persons. Auto

component manufacturers supply to two kinds of buyers-original equipment manufacturers

(OEM) and the replacement market is characterized by the presence of several small-scalesuppliers who score over the organized players in terms of excise duty exemptions and

lower overheads.

Global trends and challenges

The World trade and investment in automotive and parts has become liberalized with

tariffs going down internationally. MNC assembler source parts from cheapest quality

source in any part of the world. Local suppliers are being linked into the global supply

chain and they have to compete with regional players. Rapid changes in information and

communication technology are reshaping the way auto industry is doing business

The globalization offers a great opportunity for the Indian auto component manufacturers.

There are certain strengths of the industry that attracts the global buyers and there are

certain weaknesses, which can eliminate the local auto parts manufacturers, and the

advantage shall go to global manufacturers who shall have local capabilities in India.

Indian auto component industry strengths

The component industry in India has significant cost advantages primarily due to lower

labor cost in India. This labor cost advantage translates to overall cost advantages of 20-

8

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 9/47

30% over the counter parts from other developed despite lower labor productivity. Since

tier I suppliers control the global component industry the cost advantages should be

leveraged into attracting these global players to set up manufacturing base in India. This

low cost labor is not a factor for long-term competitiveness, and improvement in scale,

quality, technology and investment in critical process, are necessary to sustain the cost

competitiveness.

In spite of several handicaps there are a number of favorable factors, which are

1. Trained and killed human resources2. Wide industry base manufacturing 97% of component required

3. Growing entrepreneurship

4. Growing domestic market

5. Expanding global markets

6. Transnationalisation of world economy

7. Investment by non-resident Indians

8. Economic liberalization

Evolving industry structure

The Indian automotive vehicle market has recovered from the downturn and is expected to

witness a healthy growth at least for the next 3 years. This is a high degree of correlation

between the automotive vehicle and the automotive component industry sales. The growth

in the component market is likely to be driven by an important in the demand for

automotive vehicles.

In 1999, the component business in India was estimated at $2.81 bn. Of this, original

equipment(OE) had a share of 60 percent. The replacement market accounted for the

remaining 40 percent. In the next few years, the aftermarket is expected to growth faster

than OE component market. This is primarily because the old vehicle population is

registering a significant rise. The effect is likely to be nullified as the average life span of

9

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 10/47

auto parts is expected to go up due to improved quality of components. Subsequently, the

ratio is likely to stabilize as in the case of developed markets.

Production

While analyzing 54 automotive country markets, it is found that 96% of global vehicle

sales and 99% of global vehicles production have been made. Indian auto component

industry is wide(over 420 firms in the organized sector producing practically all

components and more than 10000 firms in small unorganized sector, in tierized format)

and has been one of the fastest growing segments of automotive industry, growing by over 28% in nominal terms, between 1995-98. During the year 2003-2004, the sector has

recorded a growth of 25.06% by recording a production of the order of Rs.30,640 crores.

During the year 2004-05, the output of the auto component industry is expected to be

around Rs. 36300 crores.

Growth of automobile component industries

The growth of automobile components industries is closely linked to the growth of

automotive industry as substantial quantity produced is supplied by auto components

industry to original equipment manufactures (OEMs), keeping in line with the decline in

the growth rate in the automotive as a whole, auto components industry has also registered

slow growth during last 2-3 years. The production during 2000-2001 was of the order

Rs.17174 crores compared to Rs.1999-2000 registering growth of 5%.

10

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 11/47

2.2 COMPANY PROFILE

WABCO-TVS (INDIA) Limited was a joint venture between TVS Group and WABCO Vehicle

Control System. But it has acquired all the shares from TVS and now it has 75% shares and

remaining to the public. It was formerly known as Sundaram Clayton Limited, Brakes Division.

It began its operations in Chennai in 1962, in collaboration with Clayton Dewandre Holdings plc,

UK.

WABCO-TVS (INDIA) Limited has pioneered the manufacture of air-assisted and air brake

systems for commercial vehicles in INDIA. With a commitment of total satisfaction tocustomers, the company has achieved a share of business in the OE (Original Equipment)

segment greater than 85% and a market share in the after-market greater than 75%.

WTIL have plants at Ambattur-Chennai, Jamshedpur and mahindra world city-Chennai adopting

rigorous TQM processes and standards, WTIL’s brakes division registered a turnover of $135

million in 2007-2008.

The Research and Development center is full-fledged and state-of-the-art to facilitate design,

development, simulation and testing. A team of professional engineers powered with the best

production facilities gear up to translate design competence into excellence in manufacturing

through concepts such as cellular manufacturing and operation standards

TQM

WABCO-TVS have a solid foundation in its domestic market leadership and pioneering R&D

efforts. Comprehensive TQM (Total Quality Management) practices enable WABCO-TVS in

being a competitive world-class manufacturer in terms of quality, cost and timely delivery of

products.

11

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 12/47

Process Management

WABCO-TVS, have committed to total customer satisfaction. Cellular manufacturing gives

them the flexibility to respond in tune to customer needs. Comprehensive integration of the

supply chain through implementation of ERP (Enterprise-Wide Resource Planning) programme

has further enhanced WABCO-TVS (INDIA) Limited's responsiveness.

Employees

TEI (Total Employee Involvement) forms the base of WABCO-TVS quest for excellencethrough TQM. WABCO-TVS is poised to achieve breakthroughs by realizing the importance of

the need to continuously honing the expertise of our human resources and learning from the best

practices across the world. Training is imparted not only to employees but also to suppliers.

WABCO-TVS (INDIA) Limited supplies original equipment fitments for vehicles manufactured

by Ashok Leyland, TATA Motors, Vehicle Factory (Jabalpur), and Bharat Earthmovers, TAFE,

Volvo, SUTLEJ, CATERPILLAR, Eicher Motors, Swaraj Mazda, Force Motors, Mahindra &

Mahindra, Tata Cummins (Engines) and a host of other trailer manufacturers.

A complete product range

WTIL manufacturers an entire range of air brake actuation components comprising several

varieties of compressors, re services, air dryers, controlling and regulating valves, brake

chambers, spring brake actuators and a host of auxiliaries such as hoses, couplings and

switches. WTIL manufacturers a growing range of vacuum brake equipment for light

commercial vehicles. WTIL also offers a range of repair kits to service its products in the

after market.

WTIL is the first Indian company to manufacturer the next generation braking system:

Anti – Lock brake System (ABS) and Anti-Spin Regulation (ASR) developed with total in-

house design technology. ABS is a result of years of extensive research and it dramatically

12

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 13/47

improves vehicle stability under adverse road conditions, thus enhancing safely and steer

ability.

Milestones on the road to excellence

A commitment to enhancing customer satisfaction through continuous improvement and

total employee involvement has led WTIL to one of its most significant milestones so far –

The Deming Award. WTIL’s brakes division was awarded the prestigious Deming Prize

by the union of Japanese and engineers (JUSE) for having “achieved distinctive

performance improvements through the applications of company-wide quality control”.The examination procedures and selection process being exacting and elaborate; WTIL

considers it a matter of pride that it is only the fourth organization in the world outside

Japan to win this prize and the very first in India.

In 2002, WTIL’s brakes division was awarded the Japan quality medal for “continual

application of TQM for priority issue to achieve business results”. It is the second

company outside Japan outside Japan and the very first in India to win this prestigious

award. WTIL has a solid foundation in its domestic market leadership and pioneering

R&D efforts. With this, WTIL aims to be a competitive world class manufacturer in terms

of quality, cost and timely delivery through comprehensive world –class practices.

Not with standing, WTIL believes that winning the demand award and Japan quality medal

is still only the beginning of a conscious and continuous search for new level of excellence.

13

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 14/47

3 REVIEW OF LITERATURE

A literature review is a “critical analysis of a segment of a published body of knowledge

through summery, classification and comparison of prior research studies, reviews of

literature and theoretical articles”.

Literature review is the process of developing an insight into both conceptual and research

based studies available in the area and the topic chosen. The objectives of such review are

to understand the importance of the topic and find out the research gaps if any in the

chosen area.

Michael J. McCarthy(1994)

The present study reveals that variable cost is always vary with the variables.The cost of

the cabin flight crew is a step-variable cost--the number of flight attendants assigned to a

flight will vary with the number of passengers on the flight. The only true variable costs

are the costs of meals and an almost inconsequential increase in fuel consumption.

Therefore, adding one passenger to a flight brings in additional revenue but has very little

effect on total cost. Consequently, airlines have been stuffing more and more seats into

their aircraft.

GM corp (1992)

In the early 1990s, General Motors Corp. laid off tens of thousands of its hourly workers

who would nevertheless continue to receive full pay under union contracts. GM entered

into an agreement with one of its suppliers, Android Industries, Inc., to use laid-off GMworkers. GM agreed to pay the wages of the workers who would be supervised by Android

Industries. In return, Android subtracted the wages from the bills it submitted to GM under

their current contract. This reduction in contract price is pure profit to GM, since GM

would have had to pay the laid-off workers in any case.

14

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 15/47

Dorina BUDUGAN, (1989)

The study reveals that alternative method of full costing method.This is the direct costing

method employed to calculate costs, which is based on those costs that are closely and

directly connected to the operation volume. This method is actually more than a cost

calculation method; it is a short-term earnings calculation method, which makes these costs

a useful company management tool. This paper is designed to explain, by means of

concrete examples, the way in which operation conditions changes influence the earnings

estimated by means of the cost-volume-profit analysis, as well as the implications of these

changes on the decisions to make.

Kee, Robert (2007)

Cost-volume-profit (CVP) analysis is a mathematical representation of the economics of

producing a product. The relationships between a product's revenue and cost functions

expressed within the CVP model are used to evaluate the financial implications of a wide

range of strategic and operational decisions. CVP analysis may be used to determine the

trade-offs in profitability and risk from alternative product design and production

possibilities. In effect, CVP is a quantitative model for developing much of the financial

information relevant for evaluating resource allocation decisions.

Horngren(1994)

Cost Volume Profit analysis (CVP) is one of the most hallowed, and yet one of the

simplest, analytical tools in management accounting. In a general sense, it provides a

sweeping financial overview of the planning process . That overview allows managers to

examine the possible impacts of a wide range of strategic decisions. Those decisions can

include such crucial areas as pricing policies, product mixes, market expansions or

contractions, outsourcing contracts.

Steven, Grahame (2005)

Cost/volume/profit (CVP) analysis can be used to determine how many products must be

sold in order to break even or reach a target profit and also to calculate the margin of safety

15

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 16/47

for a business proposal Panel 1 contains the formulas for these calculations. Although the

information it provides is extremely useful, CVP analysis can also offer a valuable insight

into the business issues that underpin a venture.

Metzger, Lawrence M. (1993)

An important result of this search for better data is more accurate and relevant costing

information that is useful for decision making. This article will describe the use of data

developed in an ABC system as it applies to the multiproduct cost-volume-profit (CVP)

analysis model. Data derived under ABC can be integrated into traditional decision-making

techniques.

16

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 17/47

4 RESEARCH METHODOLOGY

4.1 DEFINITION

According to Clifford woody research comprises defining and redefining problems,

formulating hypothesis or suggested solutions correcting, organizing and evaluating data

making deductions and reaching conclusions and at last testing the conclusions to

determine whether they fit the formulated hypothesis.

It can be defined as an organized, systematic, scientific inquiry or investigation in to a

specific problem undertaken with the purpose of finding answers or solutions to it.

It is the process of finding solution to a problem after the thorough study and analysis of

situational factors.

Research can be a means to an end or and it end itself.

Research design is needed in the following cases.

• Identify the difficult issues

• Gather relevant information

• Analyzing the data in the case that would help decision making

• Implementing the right course of action, decision making is the process

of choosing and want the alternative solution to resolve their problem.

• Research helps to generate better alternative for effective decision

making.

4.2 RESEARCH DESIGN:

A research design is the arrangement of conditions for collection and analysis of data in a

manner that aims to combine relevance to the research purpose with economy in

procedure.

17

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 18/47

4.3 NATURE OF RESEARCH:

Analytical research:

This type of research is used where the researcher has to use facts or information that is

already available and analyze these to make a critical evaluation.

4.4 SOURCES OF DATA:

Secondary data:

It refers to the information or facts actually collected. Such data are collected with the

objective of understanding the past status of any variable or the data collected and reported

by some source is assessed and used for the objective of the study.

Since this study requires use of secondary data only, this data has been collected from the

Annual report.

18

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 19/47

4.5 TOOLS AND TECHNIQUES USED

• contribution

• P/V Ratio

• Breakeven point

• Margin of safety

• Operating leverage

Marginal cost:

CIMA define marginal cost as “The cost of one unit of product or service which would be

avoided if that unit were not produced or provided”.

Marginal costing:

CIMA define marginal costing as “The accounting system in which variable costs are

charged to the cost units and fixed costs of the period are written –off in full against the

aggregate contribution. Its special value is in decision-making”.

We all know that profit is balancing figure of sales over costs, i.e., Sales-cost=Profit. This

knowledge is not sufficient for management for discharging the functions of planning and

control, etc. The cost is further divided according to its behaviour, i.e., fixed cost and

variable cost. The age old equation can be written as

Sales – (Fixed cost + Variable cost) = profit.

Marginal costing is a management technique of dealing with cost of data. It is based

primarily on the behavioural study of cost.

19

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 20/47

Absorption costing, i.e., the costing technique, which does not recognize the difference

between fixed costs and variable costs does not adequately cater to the needs of

management. The statements prepared under absorption costing do elaborately explain

past profit, past losses and the costs incurred in past, but these statements do not help when

it comes to predict about tomorrow’s result. A conventional income statement cannot tell

what the profit or loss will be if the volume is increased or decreased. These days, there is

a cut-throat competition in market and management has got to know its cost structure

thoroughly. Marginal costing provides this vital information to management and it helps in

the discharge of its functions like cost control, profit planning performance evaluation and

decision-making.

I) Contribution

Contribution is the difference between the sales and the marginal cost of sales and the

marginal cost of sales and it contribute towards fixed expenses and profit.

Contribution can be represented as :

II) Profit Volume (P/V) Ratio

The profit volume ratio is one of the most important ratios for studying the profitability of

operations of a business and establishes the relationship between contribution and sales.

20

Contribution = Selling Price – Marginal Cost

Contribution = Fixed Expenses + Profit

Contribution – Fixed Expenses = Profit

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 21/47

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 22/47

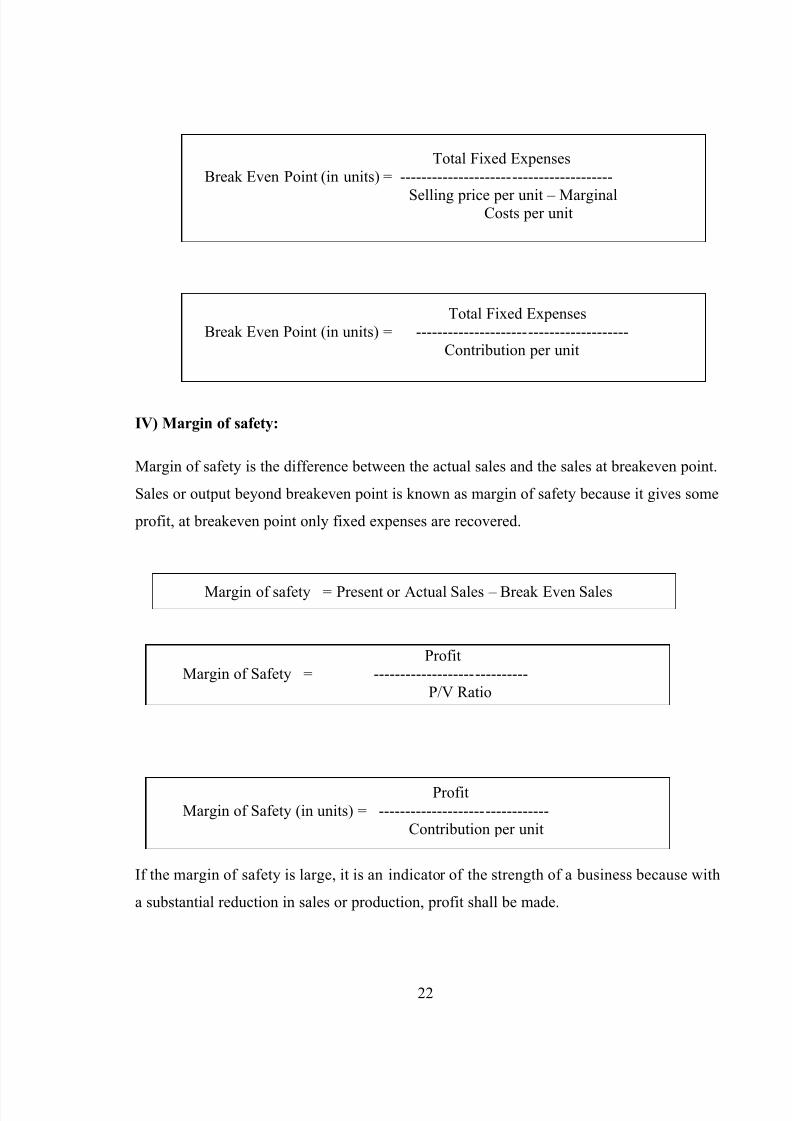

Total Fixed ExpensesBreak Even Point (in units) = ----------------------------------------

Selling price per unit – MarginalCosts per unit

Total Fixed ExpensesBreak Even Point (in units) = ----------------------------------------

Contribution per unit

IV) Margin of safety:

Margin of safety is the difference between the actual sales and the sales at breakeven point.

Sales or output beyond breakeven point is known as margin of safety because it gives some

profit, at breakeven point only fixed expenses are recovered.

Margin of safety = Present or Actual Sales – Break Even Sales

ProfitMargin of Safety = -----------------------------

P/V Ratio

ProfitMargin of Safety (in units) = --------------------------------

Contribution per unit

If the margin of safety is large, it is an indicator of the strength of a business because with

a substantial reduction in sales or production, profit shall be made.

22

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 23/47

4.6 LIMITATION OF THE STUDY

1. Fixed costs do not always remain constant.

2. Variable costs do not always vary proportionately

3. Breakeven analysis of doubtful validity when the business is selling many

products with profit margin.

4. Only a limited amount of information can be presented in a single breakeven chart.

If we have to study the changes of fixed costs, variable costs and selling prices, a

number of charts will have to be drawn up.

5. The chart becomes very complicated and difficult to understand for a layman, if the

number of lines or curves depicted on the graph is large.

23

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 24/47

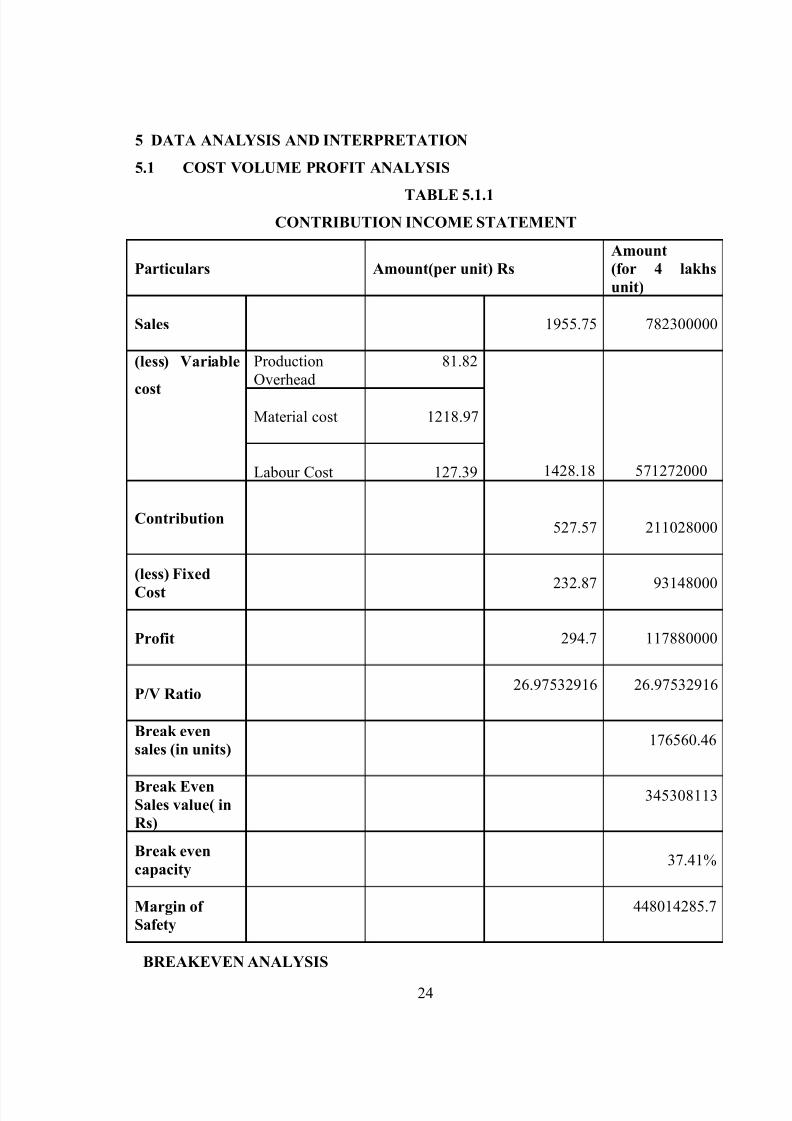

5 DATA ANALYSIS AND INTERPRETATION

5.1 COST VOLUME PROFIT ANALYSIS

TABLE 5.1.1

CONTRIBUTION INCOME STATEMENT

BREAKEVEN ANALYSIS

24

Particulars Amount(per unit) Rs

Amount

(for 4 lakhs

unit)

Sales 1955.75 782300000

(less) Variable

cost

ProductionOverhead

81.82

1428.18 571272000

Material cost 1218.97

Labour Cost

127.39

Contribution527.57 211028000

(less) Fixed

Cost 232.87 93148000

Profit 294.7 117880000

P/V Ratio26.97532916 26.97532916

Break even

sales (in units)176560.46

Break EvenSales value( in

Rs)

345308113

Break even

capacity37.41%

Margin of

Safety

448014285.7

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 25/47

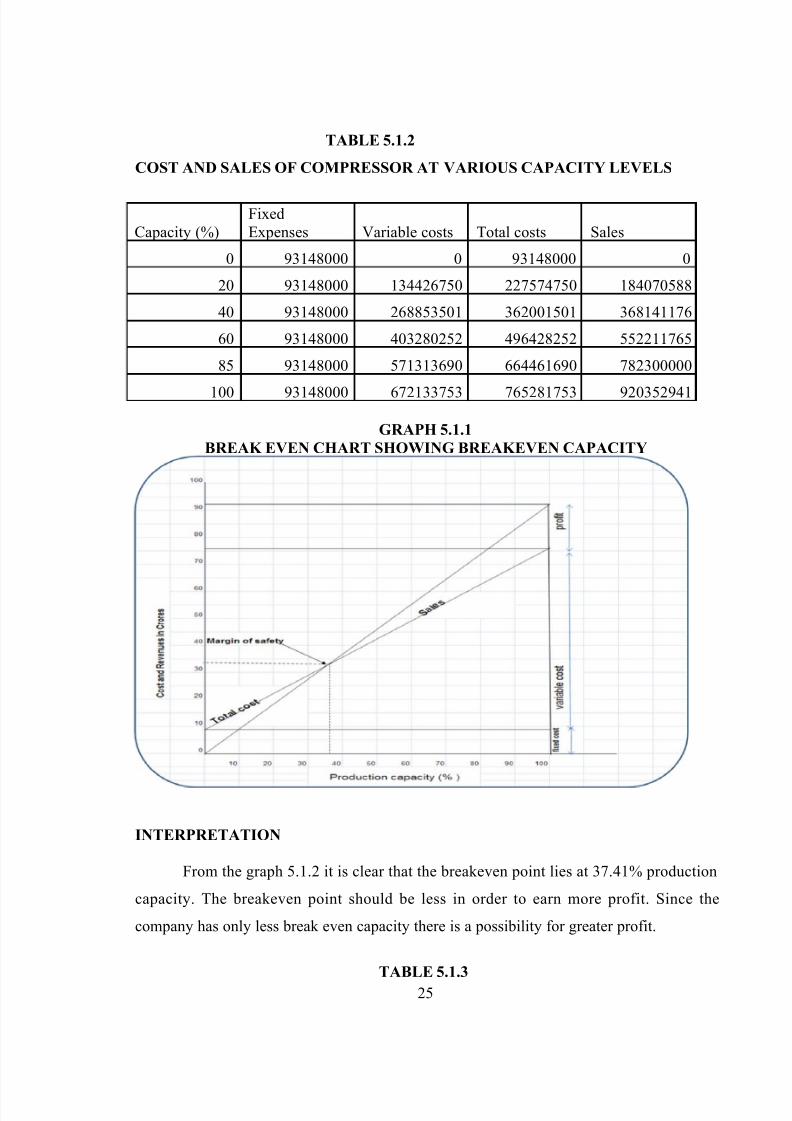

TABLE 5.1.2

COST AND SALES OF COMPRESSOR AT VARIOUS CAPACITY LEVELS

Capacity (%)FixedExpenses Variable costs Total costs Sales

0 93148000 0 93148000 0

20 93148000 134426750 227574750 184070588

40 93148000 268853501 362001501 368141176

60 93148000 403280252 496428252 552211765

85 93148000 571313690 664461690 782300000

100 93148000 672133753 765281753 920352941

GRAPH 5.1.1

BREAK EVEN CHART SHOWING BREAKEVEN CAPACITY

INTERPRETATION

From the graph 5.1.2 it is clear that the breakeven point lies at 37.41% production

capacity. The breakeven point should be less in order to earn more profit. Since the

company has only less break even capacity there is a possibility for greater profit.

TABLE 5.1.3

25

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 26/47

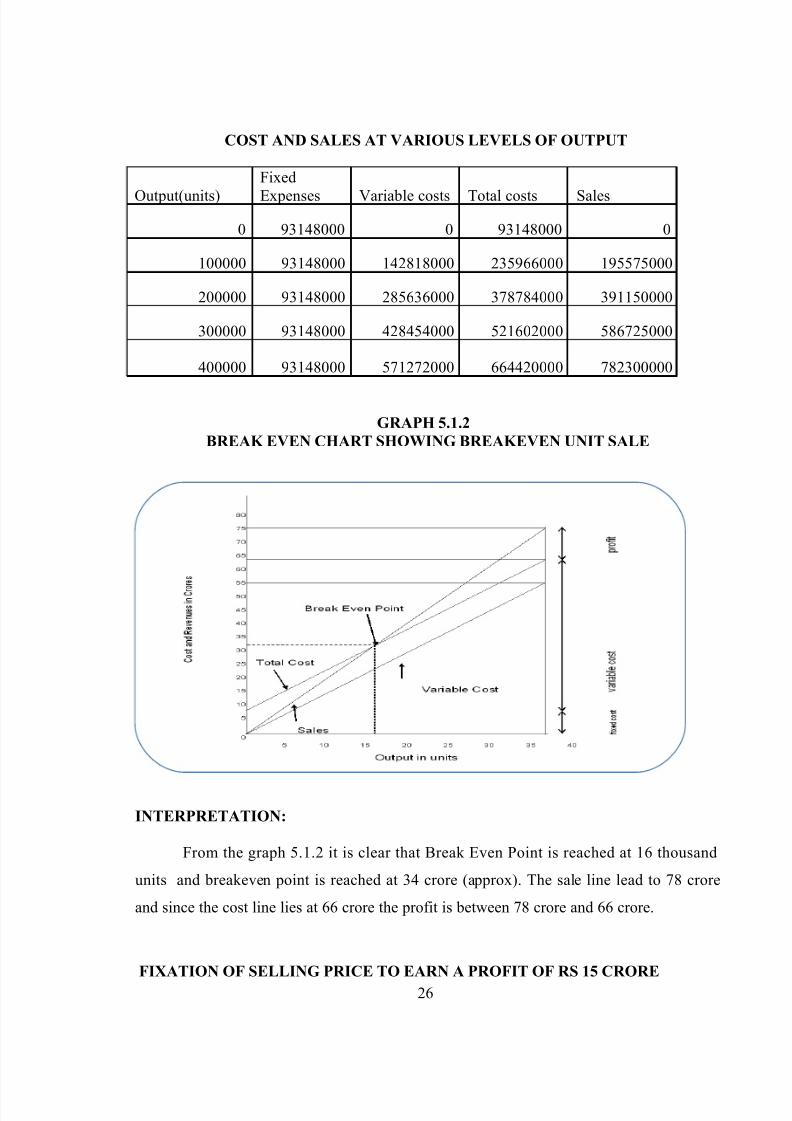

COST AND SALES AT VARIOUS LEVELS OF OUTPUT

Output(units)

Fixed

Expenses Variable costs Total costs Sales

0 93148000 0 93148000 0

100000 93148000 142818000 235966000 195575000

200000 93148000 285636000 378784000 391150000

300000 93148000 428454000 521602000 586725000

400000 93148000 571272000 664420000 782300000

GRAPH 5.1.2

BREAK EVEN CHART SHOWING BREAKEVEN UNIT SALE

INTERPRETATION:

From the graph 5.1.2 it is clear that Break Even Point is reached at 16 thousand

units and breakeven point is reached at 34 crore (approx). The sale line lead to 78 crore

and since the cost line lies at 66 crore the profit is between 78 crore and 66 crore.

FIXATION OF SELLING PRICE TO EARN A PROFIT OF RS 15 CRORE

26

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 27/47

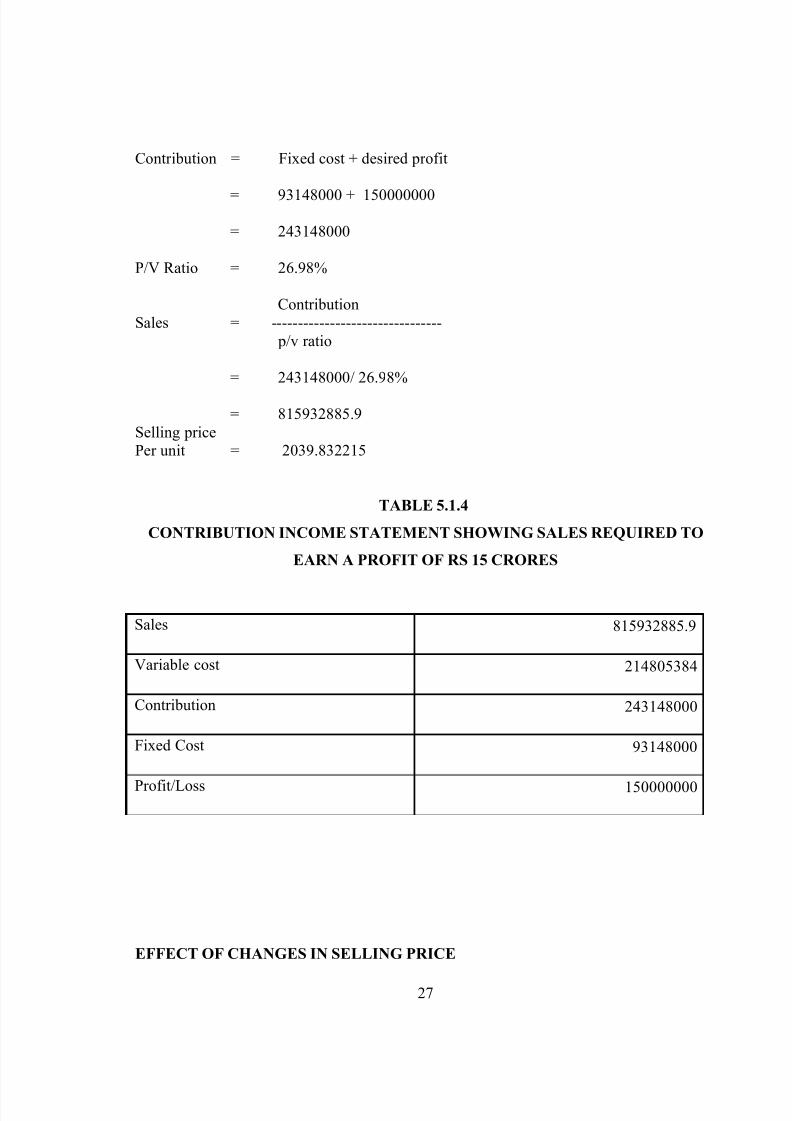

Contribution = Fixed cost + desired profit

= 93148000 + 150000000

= 243148000

P/V Ratio = 26.98%

ContributionSales = --------------------------------

p/v ratio

= 243148000/ 26.98%

= 815932885.9Selling pricePer unit = 2039.832215

TABLE 5.1.4

CONTRIBUTION INCOME STATEMENT SHOWING SALES REQUIRED TO

EARN A PROFIT OF RS 15 CRORES

Sales 815932885.9

Variable cost 214805384

Contribution 243148000

Fixed Cost 93148000

Profit/Loss 150000000

EFFECT OF CHANGES IN SELLING PRICE

27

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 28/47

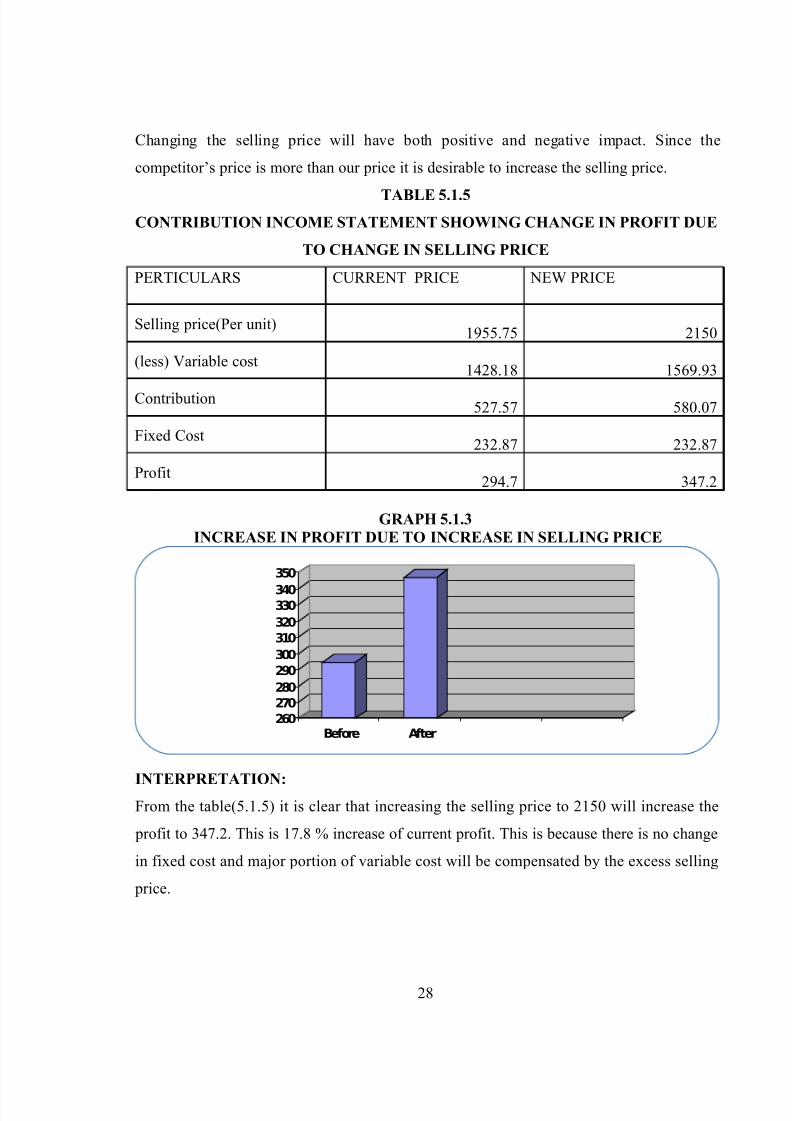

Changing the selling price will have both positive and negative impact. Since the

competitor’s price is more than our price it is desirable to increase the selling price.

TABLE 5.1.5

CONTRIBUTION INCOME STATEMENT SHOWING CHANGE IN PROFIT DUE

TO CHANGE IN SELLING PRICE

PERTICULARS CURRENT PRICE NEW PRICE

Selling price(Per unit)1955.75 2150

(less) Variable cost

1428.18 1569.93

Contribution527.57 580.07

Fixed Cost232.87 232.87

Profit294.7 347.2

GRAPH 5.1.3

INCREASE IN PROFIT DUE TO INCREASE IN SELLING PRICE

260

270

280

290

300

310

320

330340

350

Before After

INTERPRETATION:From the table(5.1.5) it is clear that increasing the selling price to 2150 will increase the

profit to 347.2. This is 17.8 % increase of current profit. This is because there is no change

in fixed cost and major portion of variable cost will be compensated by the excess selling

price.

28

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 29/47

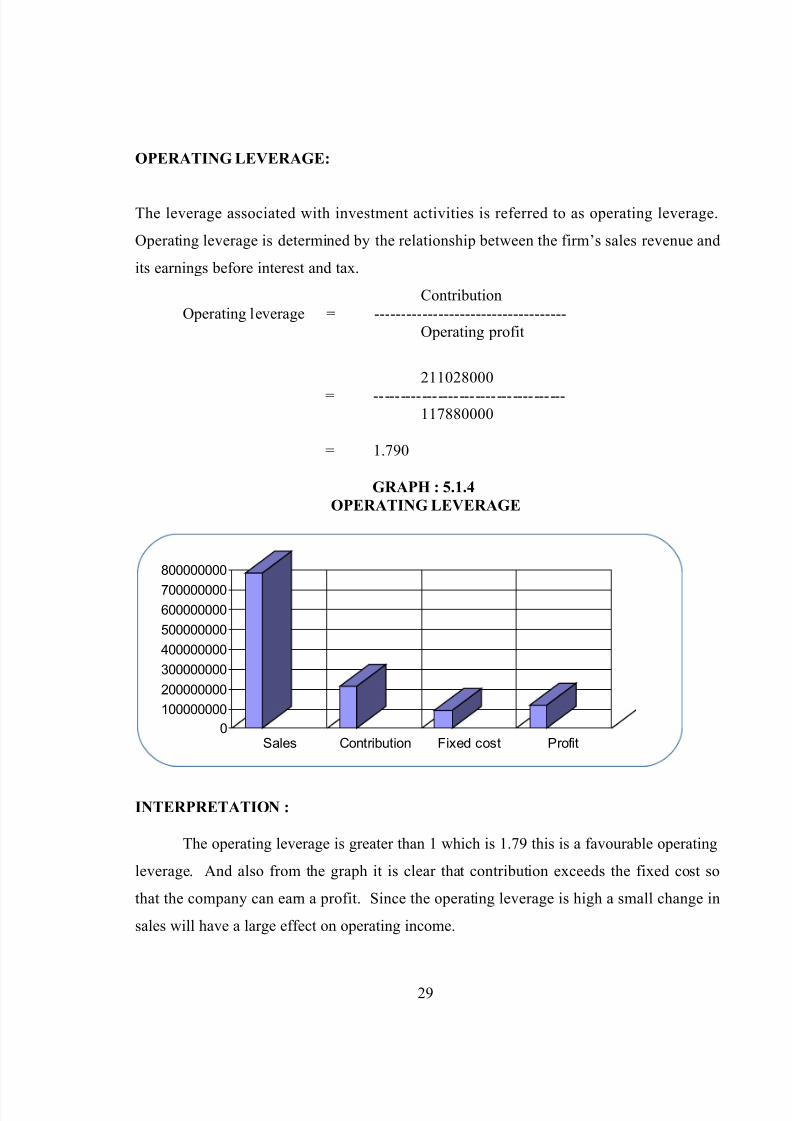

OPERATING LEVERAGE:

The leverage associated with investment activities is referred to as operating leverage.

Operating leverage is determined by the relationship between the firm’s sales revenue and

its earnings before interest and tax.

ContributionOperating leverage = ------------------------------------

Operating profit

211028000

= ------------------------------------117880000

= 1.790

GRAPH : 5.1.4

OPERATING LEVERAGE

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000

800000000

Sales Contribution Fixed cost Profit

INTERPRETATION :

The operating leverage is greater than 1 which is 1.79 this is a favourable operating

leverage. And also from the graph it is clear that contribution exceeds the fixed cost so

that the company can earn a profit. Since the operating leverage is high a small change in

sales will have a large effect on operating income.

29

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 30/47

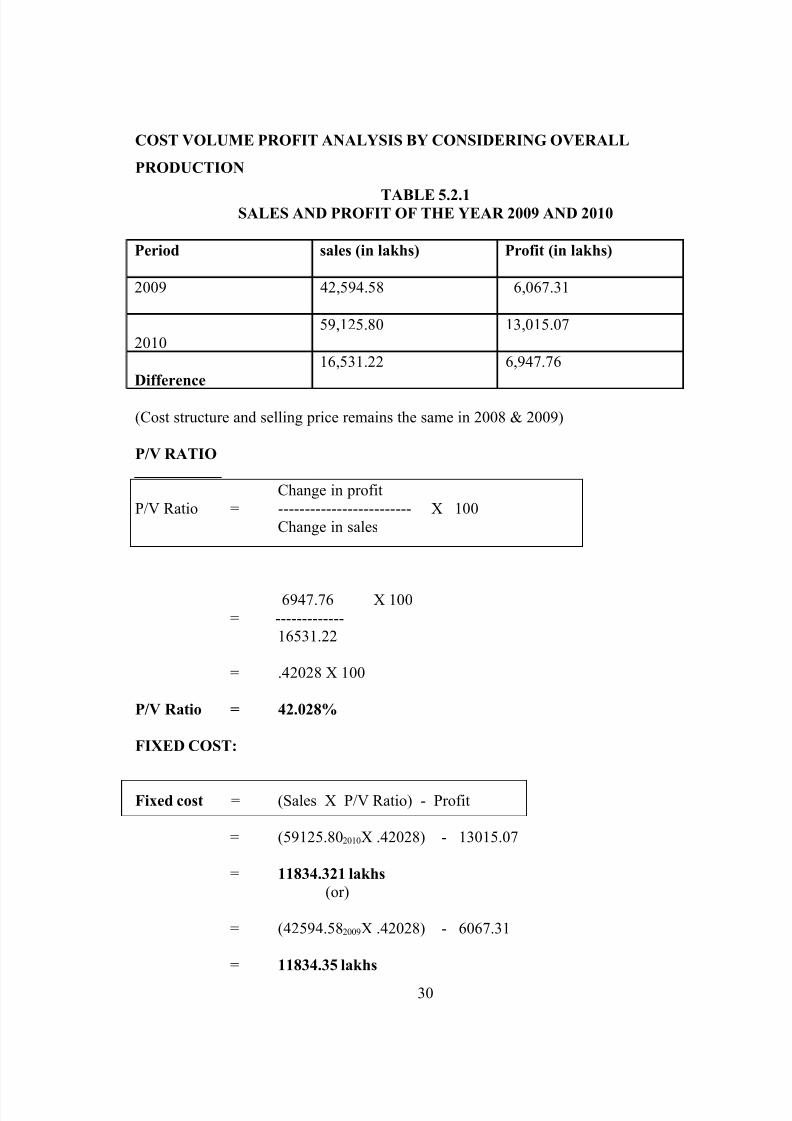

COST VOLUME PROFIT ANALYSIS BY CONSIDERING OVERALL

PRODUCTION

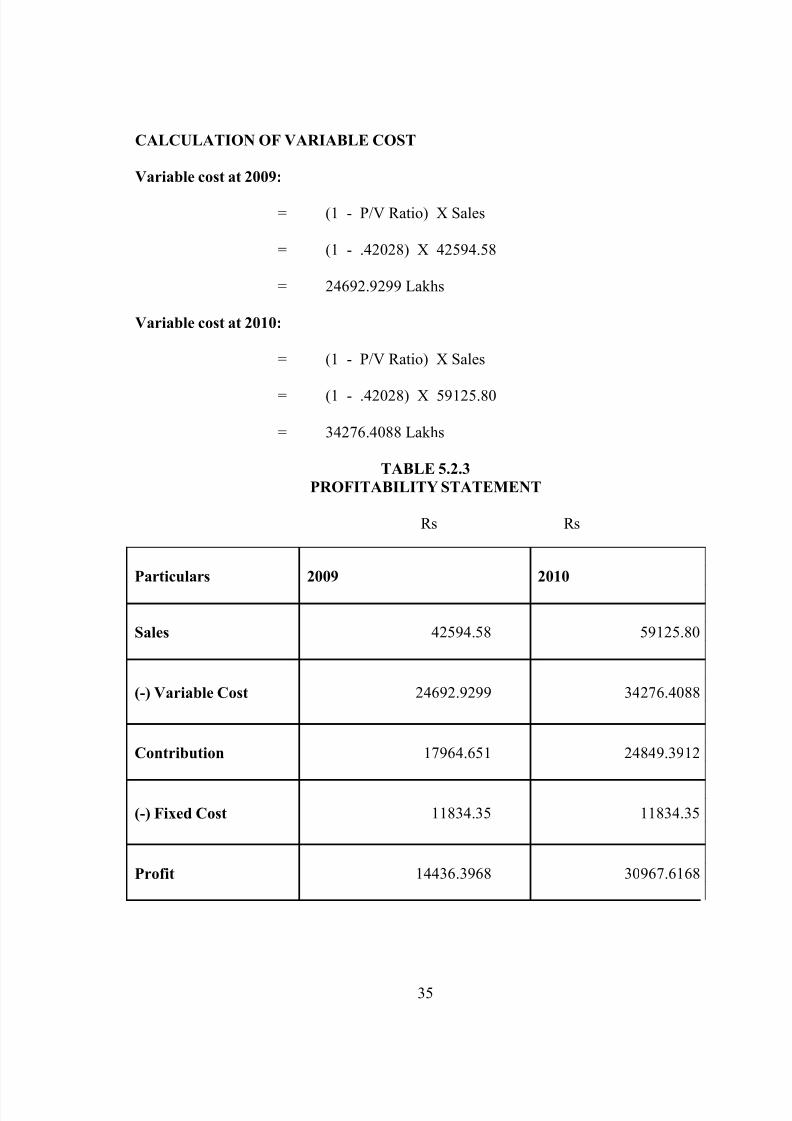

TABLE 5.2.1SALES AND PROFIT OF THE YEAR 2009 AND 2010

Period sales (in lakhs) Profit (in lakhs)

2009 42,594.58 6,067.31

201059,125.80 13,015.07

Difference

16,531.22 6,947.76

(Cost structure and selling price remains the same in 2008 & 2009)

P/V RATIO

Change in profit

P/V Ratio = ------------------------- X 100Change in sales

6947.76 X 100= -------------

16531.22

= .42028 X 100

P/V Ratio = 42.028%

FIXED COST:

Fixed cost = (Sales X P/V Ratio) - Profit

= (59125.802010X .42028) - 13015.07

= 11834.321 lakhs

(or)

= (42594.582009X .42028) - 6067.31

= 11834.35 lakhs

30

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 31/47

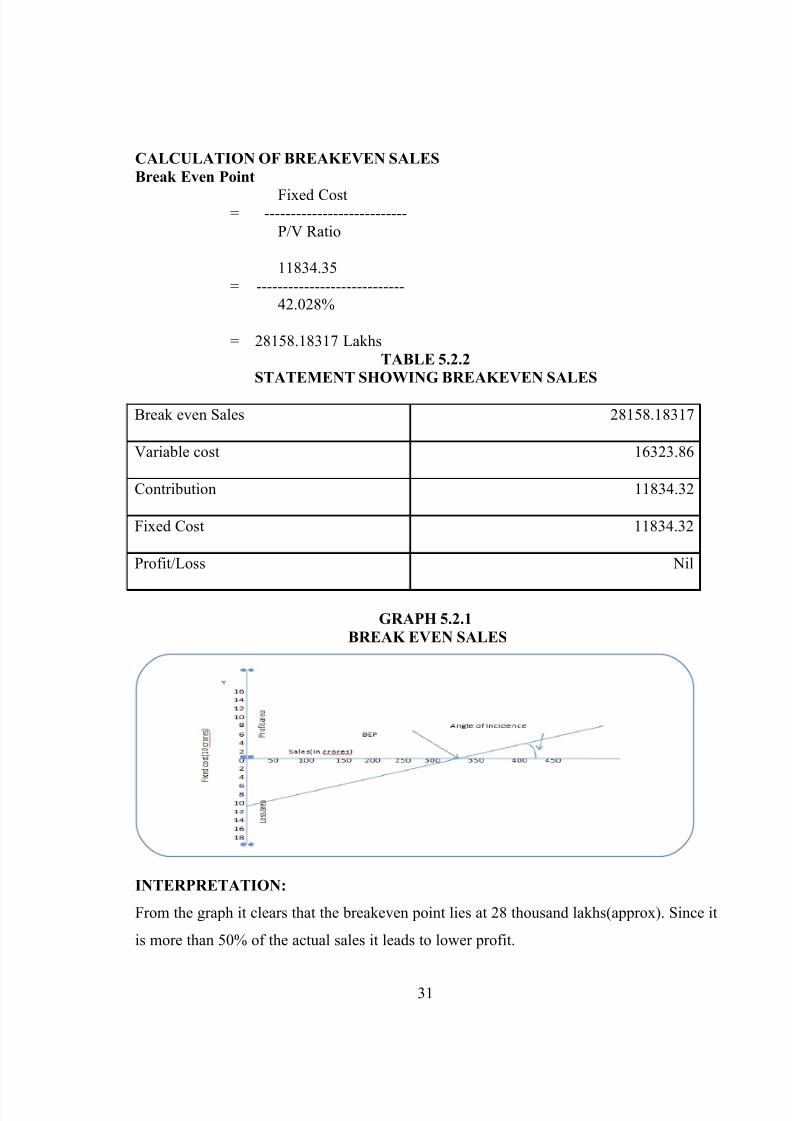

CALCULATION OF BREAKEVEN SALES

Break Even Point

Fixed Cost= ---------------------------

P/V Ratio

11834.35= ----------------------------

42.028%

= 28158.18317 LakhsTABLE 5.2.2

STATEMENT SHOWING BREAKEVEN SALES

Break even Sales 28158.18317

Variable cost 16323.86

Contribution 11834.32

Fixed Cost 11834.32

Profit/Loss Nil

GRAPH 5.2.1

BREAK EVEN SALES

INTERPRETATION:

From the graph it clears that the breakeven point lies at 28 thousand lakhs(approx). Since it

is more than 50% of the actual sales it leads to lower profit.

31

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 32/47

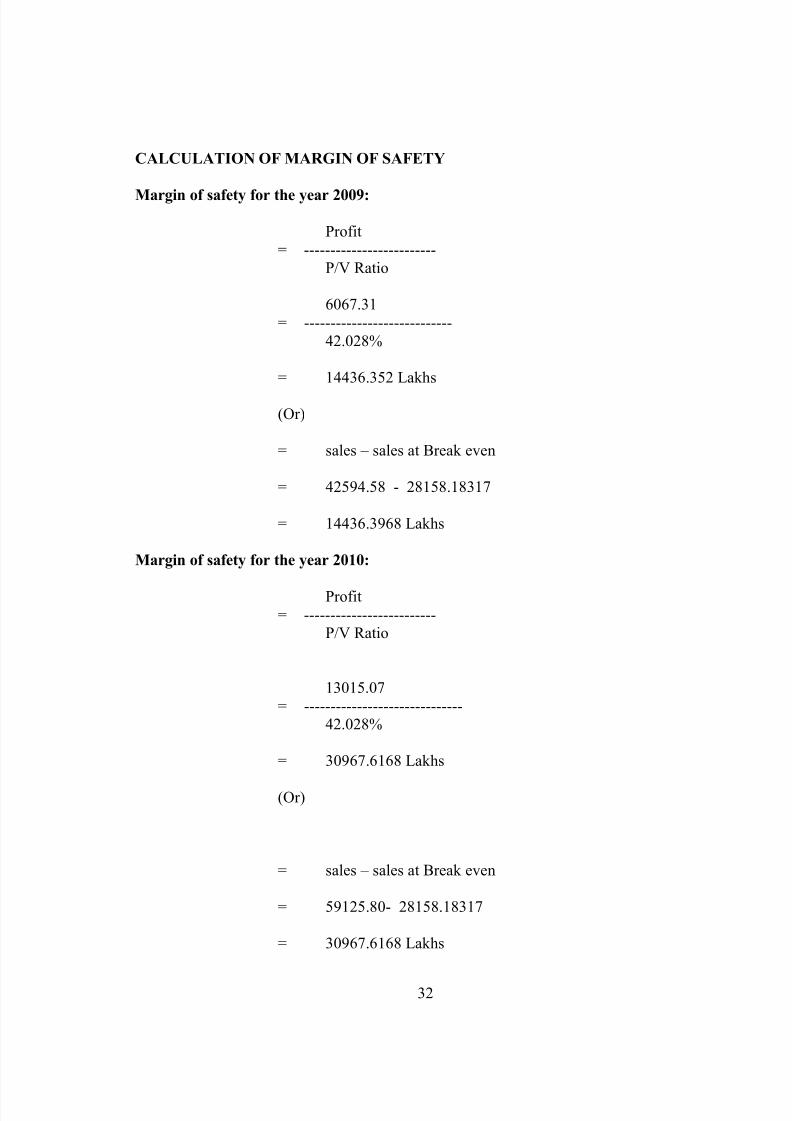

CALCULATION OF MARGIN OF SAFETY

Margin of safety for the year 2009:

Profit= -------------------------

P/V Ratio

6067.31= ----------------------------

42.028%

= 14436.352 Lakhs

(Or)

= sales – sales at Break even

= 42594.58 - 28158.18317

= 14436.3968 Lakhs

Margin of safety for the year 2010:

Profit= -------------------------

P/V Ratio

13015.07= ------------------------------

42.028%

= 30967.6168 Lakhs

(Or)

= sales – sales at Break even

= 59125.80- 28158.18317

= 30967.6168 Lakhs

32

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 33/47

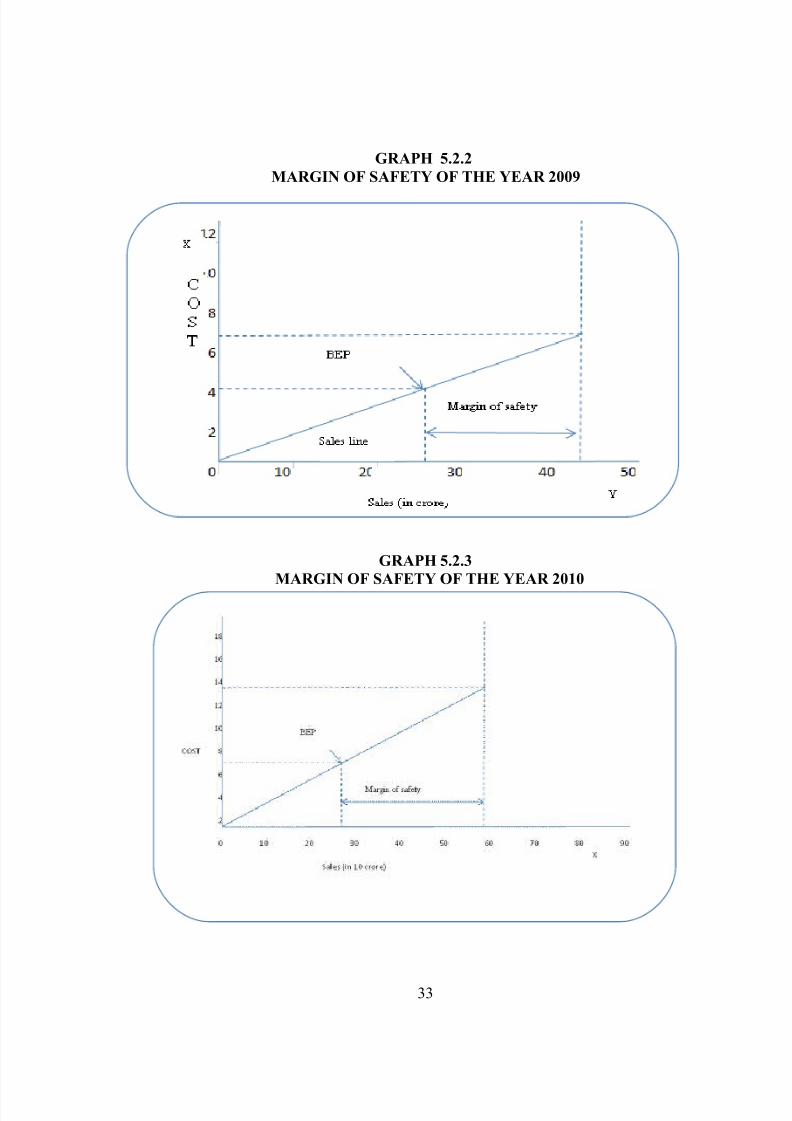

GRAPH 5.2.2

MARGIN OF SAFETY OF THE YEAR 2009

GRAPH 5.2.3

MARGIN OF SAFETY OF THE YEAR 2010

33

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 34/47

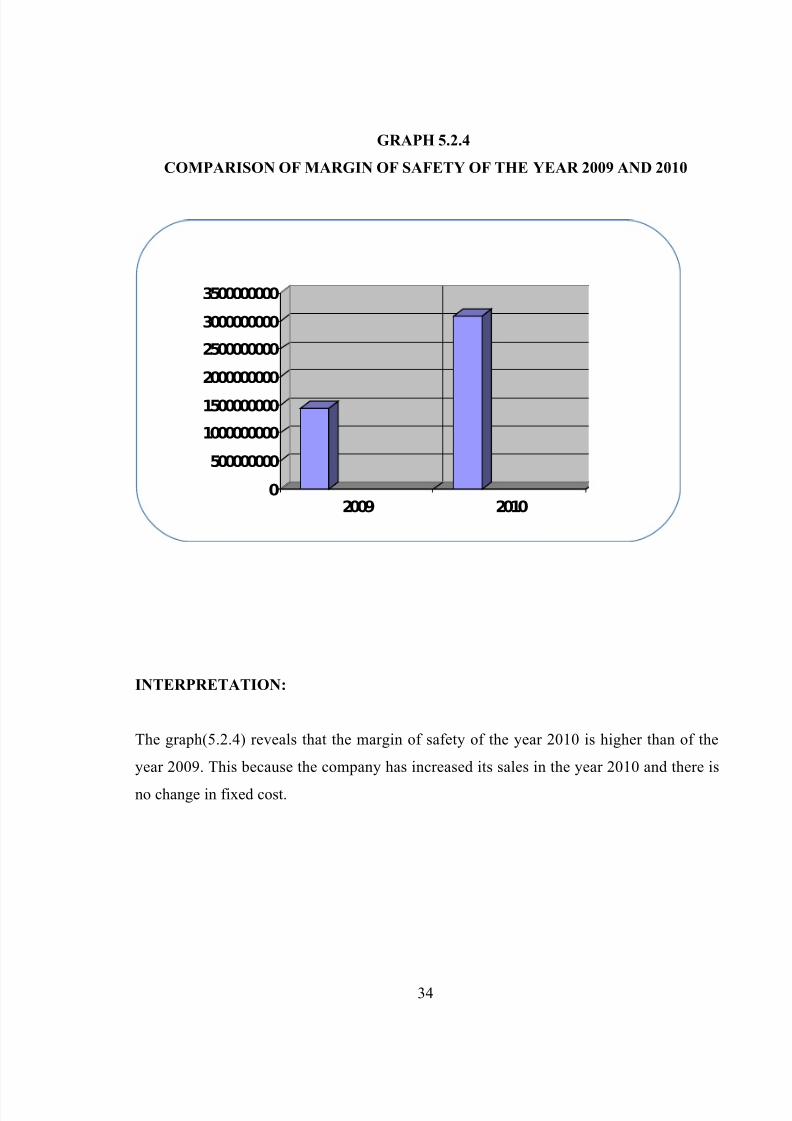

GRAPH 5.2.4

COMPARISON OF MARGIN OF SAFETY OF THE YEAR 2009 AND 2010

0

500000000

1000000000

1500000000

2000000000

2500000000

3000000000

3500000000

2009 2010

INTERPRETATION:

The graph(5.2.4) reveals that the margin of safety of the year 2010 is higher than of the

year 2009. This because the company has increased its sales in the year 2010 and there is

no change in fixed cost.

34

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 35/47

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 36/47

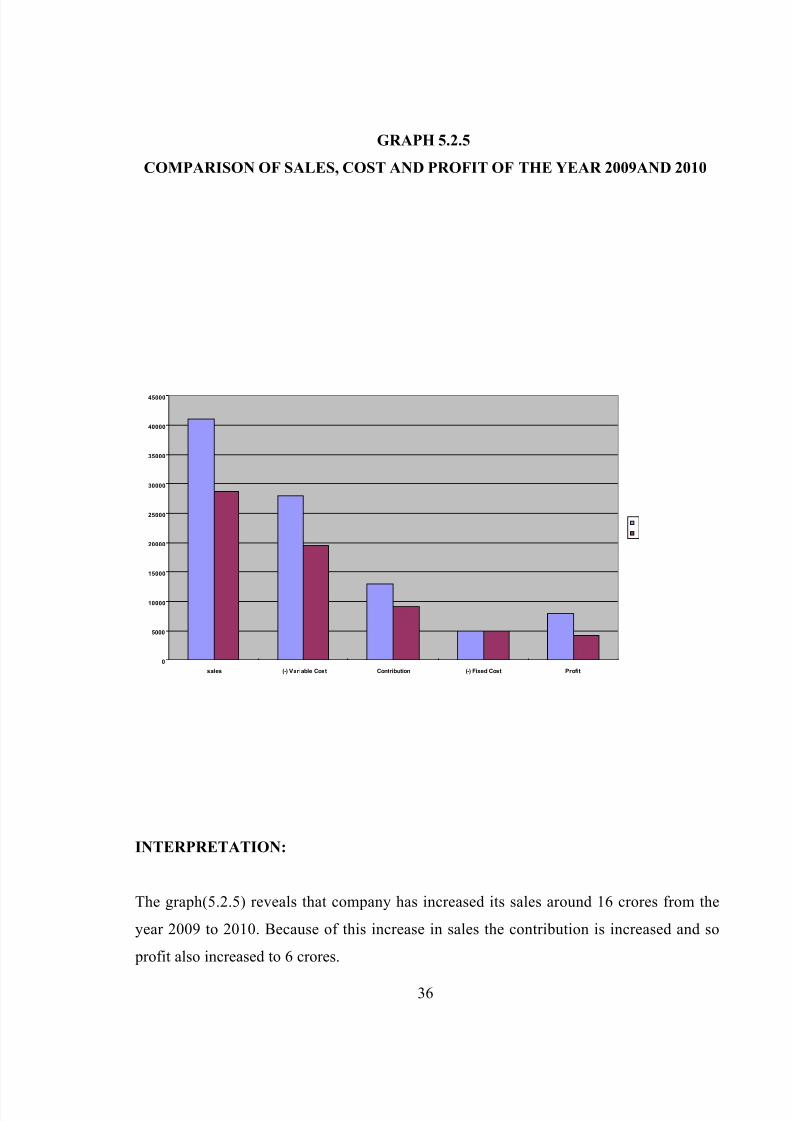

GRAPH 5.2.5

COMPARISON OF SALES, COST AND PROFIT OF THE YEAR 2009AND 2010

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

sales (-) Variable Cost Contribution (-) Fixed Cost Profit

INTERPRETATION:

The graph(5.2.5) reveals that company has increased its sales around 16 crores from the

year 2009 to 2010. Because of this increase in sales the contribution is increased and so

profit also increased to 6 crores.

36

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 37/47

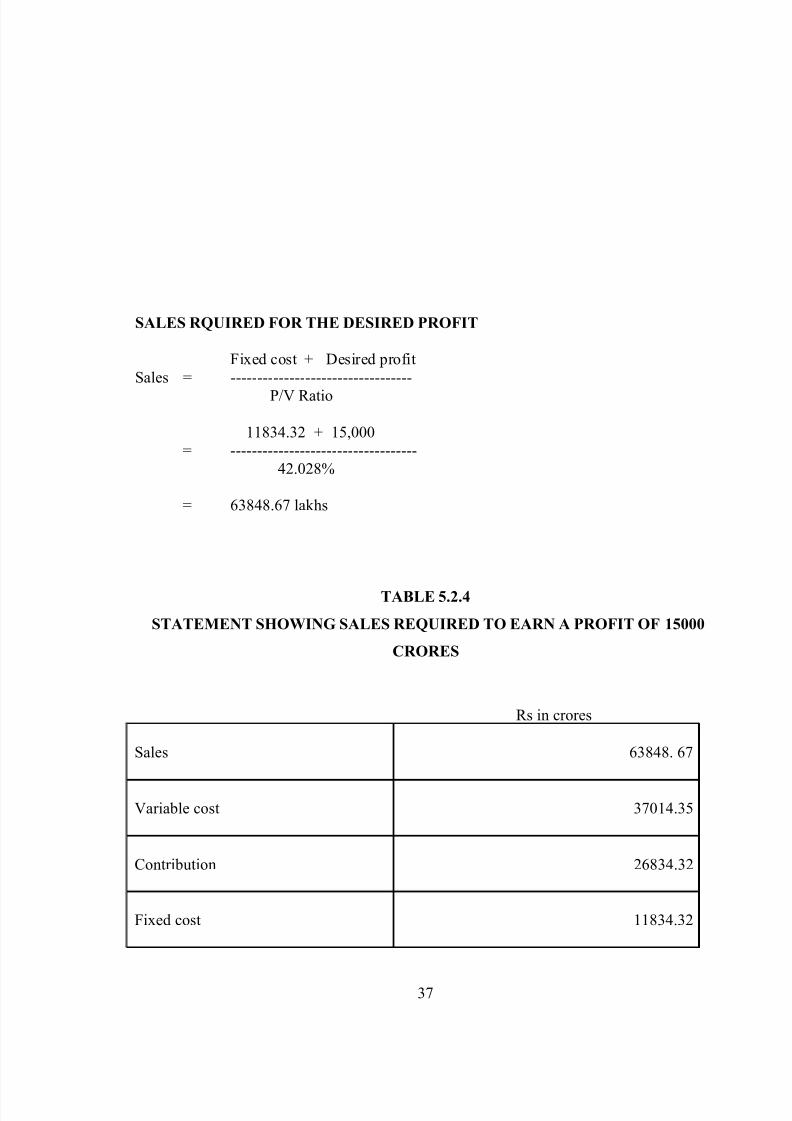

SALES RQUIRED FOR THE DESIRED PROFIT

Fixed cost + Desired profitSales = ----------------------------------

P/V Ratio

11834.32 + 15,000= -----------------------------------

42.028%

= 63848.67 lakhs

TABLE 5.2.4

STATEMENT SHOWING SALES REQUIRED TO EARN A PROFIT OF 15000

CRORES

Rs in crores

Sales 63848. 67

Variable cost 37014.35

Contribution 26834.32

Fixed cost 11834.32

37

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 38/47

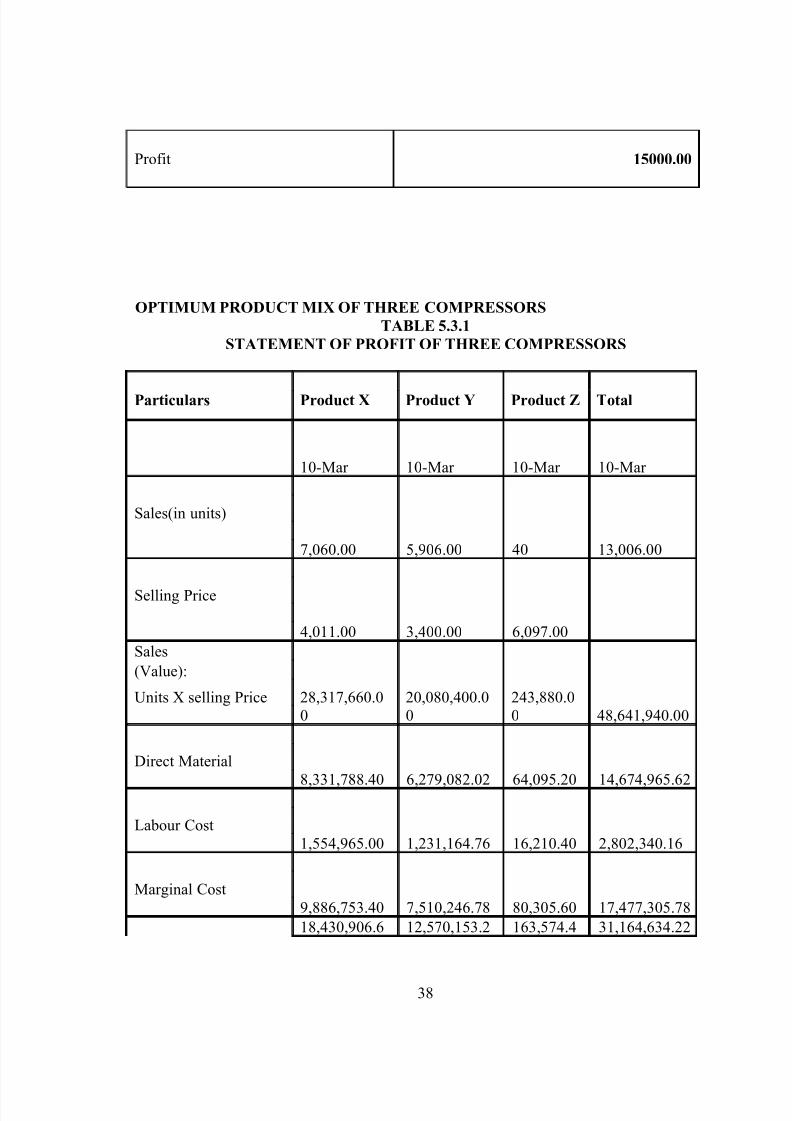

Profit 15000.00

OPTIMUM PRODUCT MIX OF THREE COMPRESSORS

TABLE 5.3.1

STATEMENT OF PROFIT OF THREE COMPRESSORS

Particulars Product X Product Y Product Z Total

10-Mar 10-Mar 10-Mar 10-Mar

7,060.00 5,906.00 40 13,006.00

Sales(in units)

4,011.00 3,400.00 6,097.00

Selling Price

Sales

28,317,660.00

20,080,400.00

243,880.00 48,641,940.00

(Value):

Units X selling Price

8,331,788.40 6,279,082.02 64,095.20 14,674,965.62

Direct Material

1,554,965.00 1,231,164.76 16,210.40 2,802,340.16Labour Cost

9,886,753.40 7,510,246.78 80,305.60 17,477,305.78Marginal Cost

18,430,906.6 12,570,153.2 163,574.4 31,164,634.22

38

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 39/47

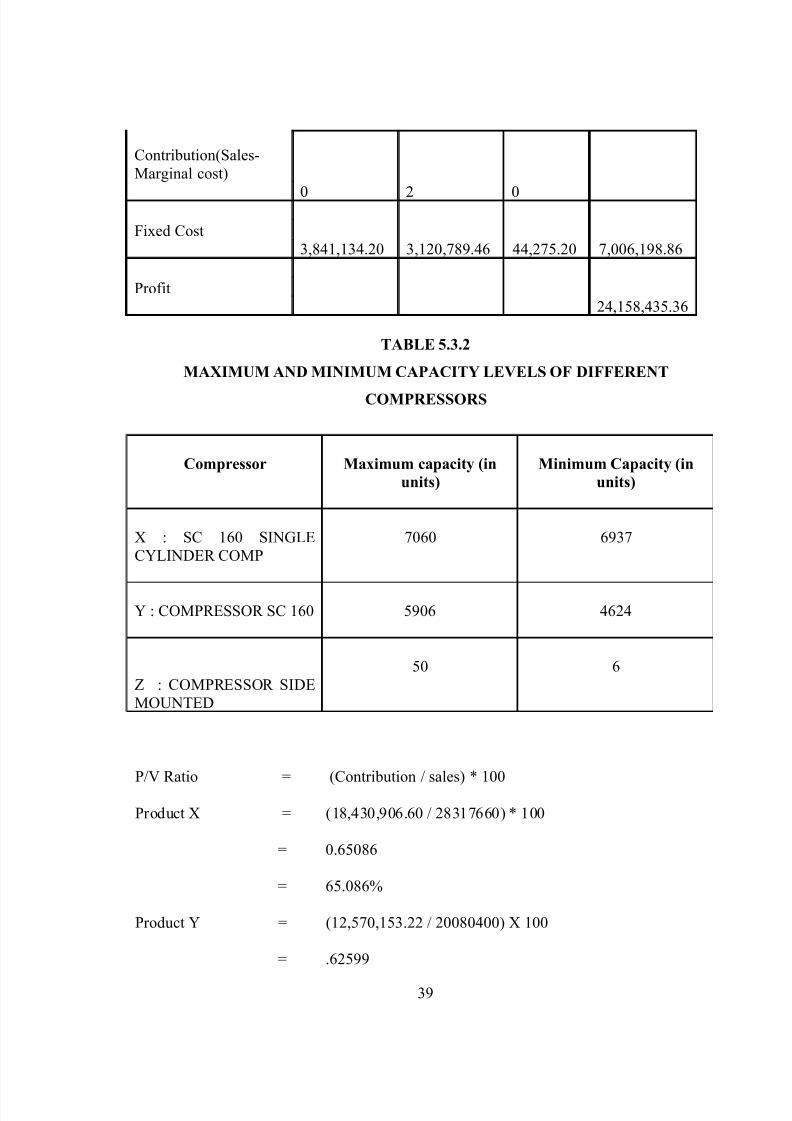

0 2 0

Contribution(Sales-Marginal cost)

3,841,134.20 3,120,789.46 44,275.20 7,006,198.86Fixed Cost

24,158,435.36Profit

TABLE 5.3.2

MAXIMUM AND MINIMUM CAPACITY LEVELS OF DIFFERENT

COMPRESSORS

Compressor Maximum capacity (in

units)

Minimum Capacity (in

units)

X : SC 160 SINGLECYLINDER COMP

7060 6937

Y : COMPRESSOR SC 160 5906 4624

Z : COMPRESSOR SIDEMOUNTED

50 6

P/V Ratio = (Contribution / sales) * 100

Product X = (18,430,906.60 / 28317660) * 100

= 0.65086

= 65.086%

Product Y = (12,570,153.22 / 20080400) X 100

= .62599

39

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 40/47

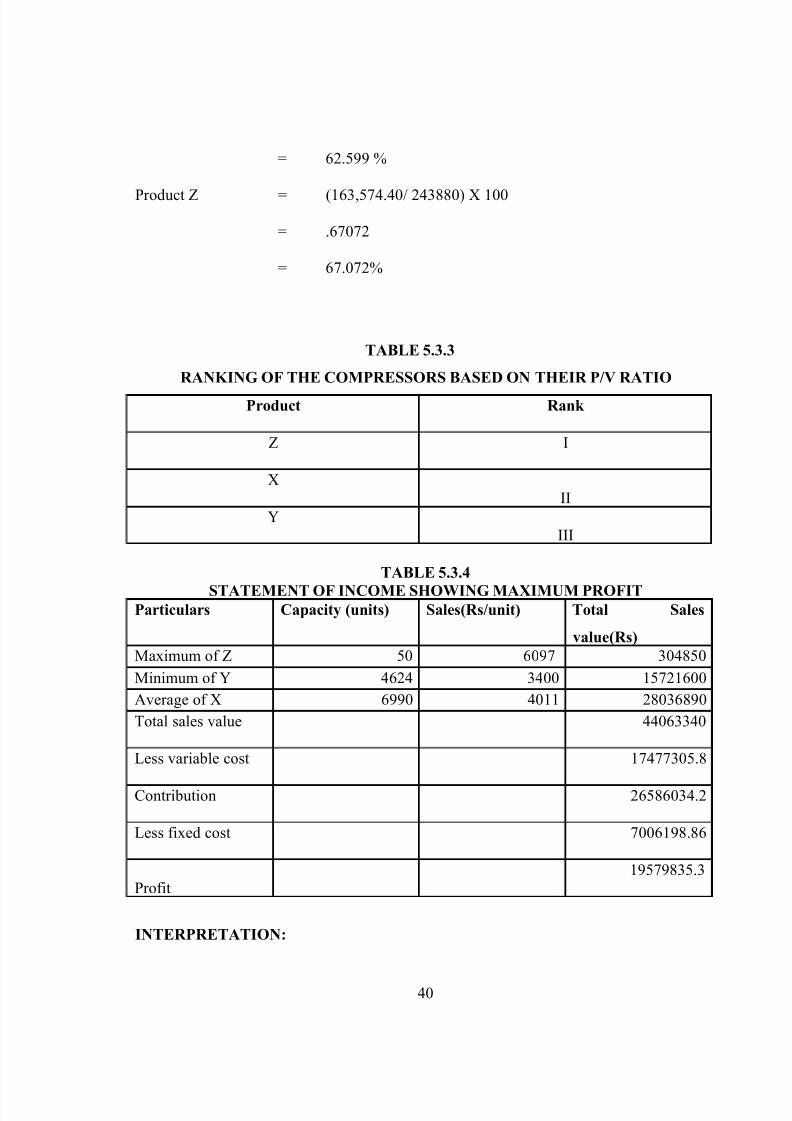

= 62.599 %

Product Z = (163,574.40/ 243880) X 100

= .67072

= 67.072%

TABLE 5.3.3

RANKING OF THE COMPRESSORS BASED ON THEIR P/V RATIO

Product Rank

Z I

XII

YIII

TABLE 5.3.4

STATEMENT OF INCOME SHOWING MAXIMUM PROFITParticulars Capacity (units) Sales(Rs/unit) Total Sales

value(Rs)

Maximum of Z 50 6097 304850

Minimum of Y 4624 3400 15721600

Average of X 6990 4011 28036890

Total sales value 44063340

Less variable cost 17477305.8

Contribution 26586034.2

Less fixed cost 7006198.86

Profit19579835.3

INTERPRETATION:

40

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 41/47

From the above table(5.3.4) it is clear that product Z has highest contribution. And then X

followed by Y. In order to earn more profit te company should boost up te sale of product

Z. Since the maximum production capacity of Z is only 50 units the company should

produce all the 50 units. And since the contribution of product Y is comparatively less than

other products it should produced at its minimum level. And te product X can be produced

at the normal level. By doing so the company can earn a profit of Rs 19579835.3.

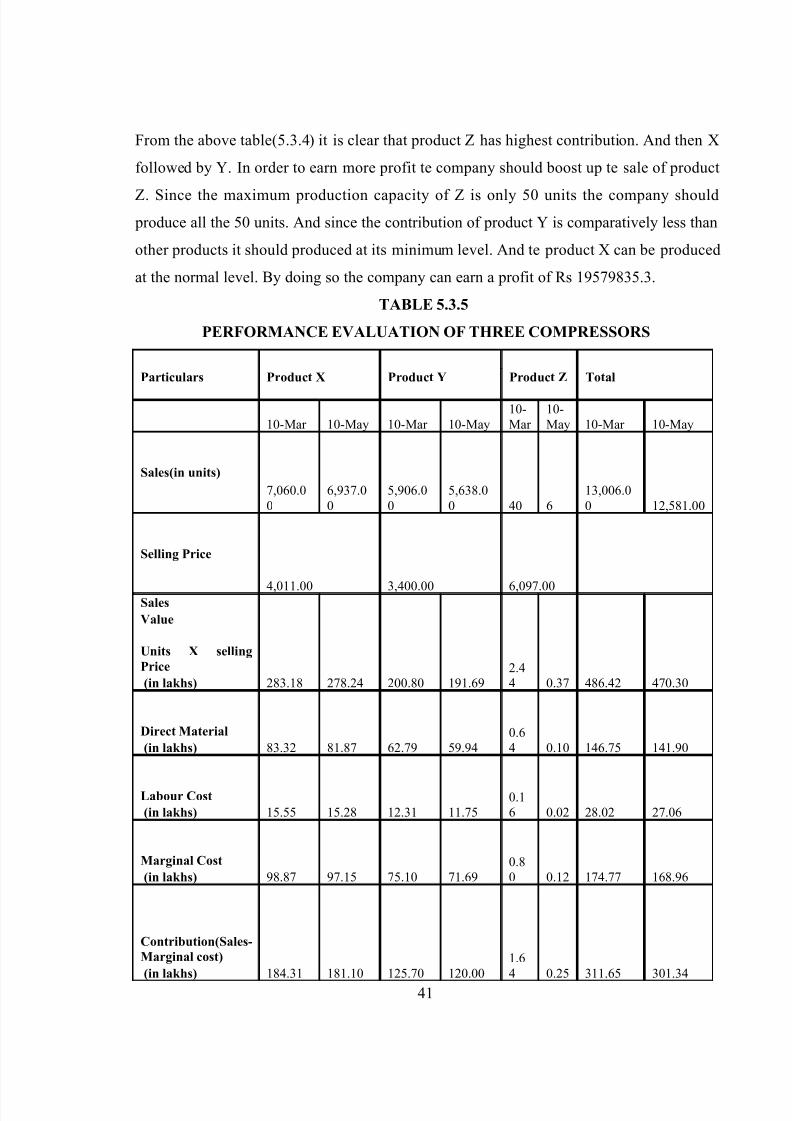

TABLE 5.3.5

PERFORMANCE EVALUATION OF THREE COMPRESSORS

Particulars Product X Product Y Product Z Total

10-Mar 10-May 10-Mar 10-May10-Mar

10-May 10-Mar 10-May

7,060.00

6,937.00

5,906.00

5,638.00 40 6

13,006.00 12,581.00

Sales(in units)

4,011.00 3,400.00 6,097.00

Selling Price

Sales

283.18 278.24 200.80 191.692.44 0.37 486.42 470.30

Value

Units X selling

Price

(in lakhs)

83.32 81.87 62.79 59.940.64 0.10 146.75 141.90

Direct Material

(in lakhs)

15.55 15.28 12.31 11.750.16 0.02 28.02 27.06

Labour Cost

(in lakhs)

98.87 97.15 75.10 71.690.80 0.12 174.77 168.96

Marginal Cost

(in lakhs)

184.31 181.10 125.70 120.001.64 0.25 311.65 301.34

Contribution(Sales-

Marginal cost)

(in lakhs)

41

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 42/47

38.41 37.74 31.21 29.790.44 0.07 70.06 67.60

Fixed Cost

(in lakhs)

241.58 233.74

Profit

(in lakhs)

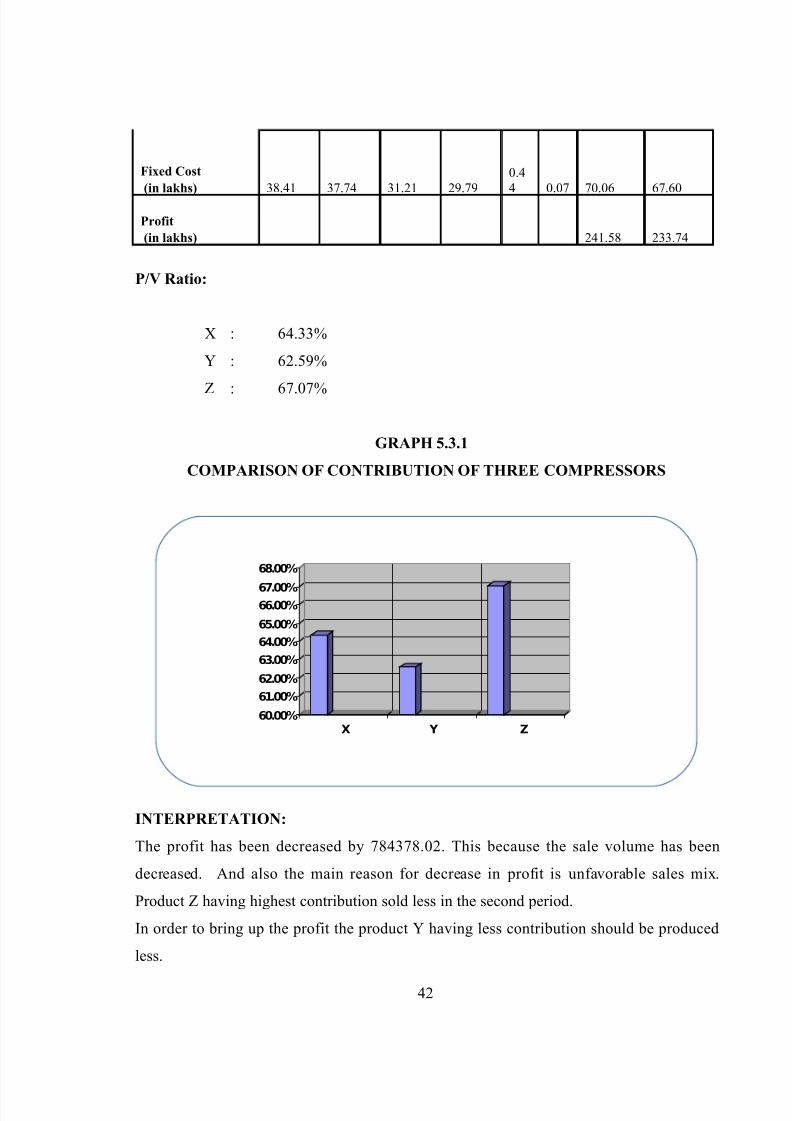

P/V Ratio:

X : 64.33%

Y : 62.59%

Z : 67.07%

GRAPH 5.3.1

COMPARISON OF CONTRIBUTION OF THREE COMPRESSORS

60.00%

61.00%

62.00%

63.00%

64.00%

65.00%

66.00%67.00%

68.00%

X Y Z

INTERPRETATION:

The profit has been decreased by 784378.02. This because the sale volume has been

decreased. And also the main reason for decrease in profit is unfavorable sales mix.

Product Z having highest contribution sold less in the second period.

In order to bring up the profit the product Y having less contribution should be produced

less.

42

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 43/47

6. FINDINGS, SUGGESTIONS AND CONCLUSION

6.1 FINDINGS

1. It was found that breakeven capacity of the production of capacitor lies at 37.41%

of overall production capacity.

2. The breakeven sale volume of capacitor lies at 16 thousand units.

3. Increasing the selling price to 2150 will increase the profit to 347.2. This is 17.8 %

increase of current profit. This is because there is no change in fixed cost and major

portion of variable cost will be compensated by the excess selling price.

4. The operating leverage of the company regarding production of capacitor is 1.790.

It shows positive sign of the company.

5. It was found that breakeven sale of overall production is Rs 28 thousand lakhs.

6. Margin of safety of the year 2010 is higher than the year 2009

7. The company has earned a profit of additional 6 crores in the year 2010 than in the

year 2009

8. The item Z (COMPRESSOR SIDE MOUNTED) has higher contribution than other

items X ( SC 160 SINGLE CYLINDER COMPRESSOR) and Y (COMPRESSOR

SC 160)

9. Because of unfavourable sales mix the profit has been reduced to 1.96 crore.

43

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 44/47

6.2 SUGGESTIONS

From the findings it was found that the breakeven capacity of capacitors is 37.41%. Since

it is less than 50% the company can continue the production of capacitors and it has to

take measures to control the variable cost by concentrating on single product..

Since the company is following JIT( Just In Time) principle for manufacturing(i.e.,

production based on demand) it is highly risk for the company to increase the profit by

increasing the sales. So in order to increase the profit the company can increase the selling

price maximum to the competitor’s price.

Because of unfavourable sales mix of the compressors the profit of the company has been

reduced to 1.96 crores. So in order to overcome the loss the product COMPRESSOR SIDE

MOUNTED should be given importance, followed by the item SC 160 SINGLE

CYLINDER COMPRESSOR and then the item COMPRESSOR SC 160.

44

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 45/47

6.3 CONCLUSION

The cost volume profit analysis is very much important for the company to know about

the relationship between the cost volume and profit. In the competitive world it is verymuch important for the company to know about its profit position.

It is a powerful tool to analyze how the change in selling price and change in cost

affect the profit position of the company, not only that it also helps to determine the

optimum mix of the company.

Cost volume profit analysis helps the management in profit planning. profit of the firm

wabco-tvs can be increased by increase the output , selling price or reducing the cost ,

since the company can produce products on demand basis it’s concluded that by

increasing the selling price company can earn more profit.

45

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 46/47

TEXTBOOKS REFERRED:

1. Brealey, Richard A., and Stewart C. Myers. 1991. Principles of Corporate Finance.

4th ed. New York: McGraw-Hill.2. Brigham, Eugene F. 1995. Fundamentals of Financial Management. 7th ed.

Orlando, FL: Dryden Press.

3. Chan, Y.L., and Y. Yuan. 1990. "Dealing With Fuzziness in Cost-Volume-Profit

Analysis." Accounting and Business Research 20 (78): 83-95.

4. Cheung, J.K., and J. Heaney. 1990. "A Contingent-Claim Integration of Cost-

Volume-Profit Analysis with Capital Budgeting." Contemporary Accounting

Research 6 (Spring): 738-760.

5. Drucker, Peter F. 1995. "The Information Executives Truly Need." Harvard

Business Review 73 (January-February): 54-62.

6. Michael J. McCarthy, “Airline Squeeze Play: More Seats, Less Legroom,” The

Wall Street Journal, April 18, 1994,pp. B1 and B6.

WEBSITES REFERRED:

1. www.wabco-tvs.com

2. www.wikipedia.com

3. www.moneycontrol.com

4. www.wabco-auto.com

5. www.financialexpress.com

46

8/7/2019 final(sat)

http://slidepdf.com/reader/full/finalsat 47/47

![GB - Triax fibre optic [SAT] 2015 -final](https://img.pdfslide.us/doc/110x75/55c5d673bb61ebfb5d8b4568/gb-triax-fibre-optic-sat-2015-final.jpg)