Embed Size (px)

Citation preview

1 Spectrum of Investment Avenues in India

Summer Training Project On

“Spectrum of Investment Avenues in India”

Submitted To

ANJUMAN I ISLAM’s ALLANA INSTITUTE OF MANAGEMENT STUDIES

Required For Partial Fulfilment of MMS Program

By

Shaikh Mohd. Jahir Munna Alli - 47

Under The Guidance Of

AHMAR BALBALE

(Channel Partner)

AM INVESTMENT

For The Academic Year

2009 – 2010

2 Spectrum of Investment Avenues in India

Declaration

I Mr. Shaikh Mohd. Jahir Munna Alli, student of

MMS (Specialization – Finance, Semester III) of

Anjuman-I-Islam‟s Allana Institute of Management

Studies hereby declare that I have completed this

Summer Internship project on “Spectrum of

Investment Avenues in India” in the academic year

2009 - 2010. The information submitted is true and

original to the best of my knowledge.

I further certify that I have no objection and grant the

rights to Anjuman-I-Islam‟s Allana Institute of

Management Studies or Mumbai University to publish

any chapter / Projects if they deem fit in journals or

magazines or newspapers without any permission.

Place : Mumbai

Date :

Name : Shaikh Mohd. Jahir Munna Alli.

Class : MMS – II, Sem – III

Roll No. : 47

Signature :

3 Spectrum of Investment Avenues in India

ACKNOWLEDGEMENT

If words are considered as a symbol of approval and token

of appreciation then let the words play the heralding role

expressing my gratitude.

I am indebted to the reviewer of the project Mr. Ahmer

Balbale, my project guide for his support and guidance. I

would sincerely like to thank him for all his efforts.

I am also grateful to Mr. Pradeep (Senior Manager – AM

Investment Ltd), Mr. Shamsher and Mr. Mahmood Balbale for

helping me understand the concept of various investment

and for providing their insights in the making of this project.

I would like to thank the University of Mumbai, for giving its

student a platform to stay abreast with changing business

scenario, with the help of theory as a base and practical as

a solution.

Last but not least, I would like to express my sincere thanks to

Dr. Vidya Hattangadi (Director, Allana Institute of

Management Studies, Mumbai) for her indirect help and all

other staff members of Allana Institute of Management

Studies for their co-operation and also my parents for giving

the best education.

4 Spectrum of Investment Avenues in India

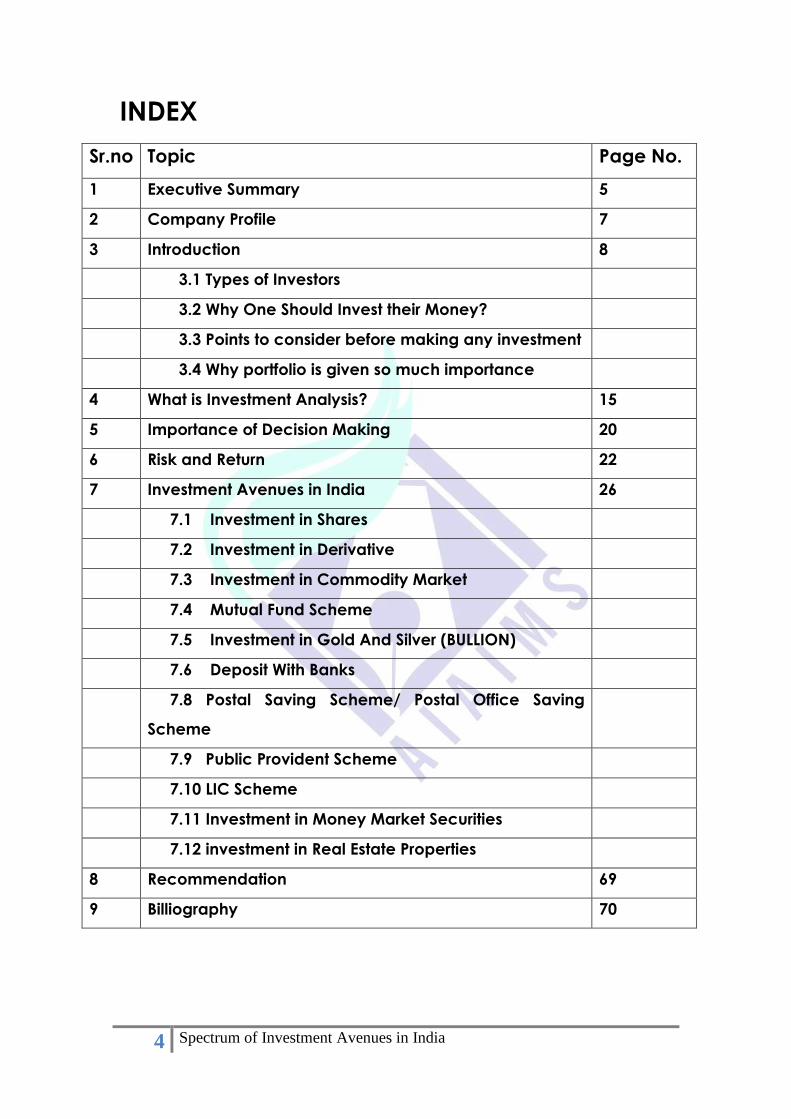

INDEX

Sr.no Topic Page No.

1 Executive Summary 5

2 Company Profile 7

3 Introduction 8

3.1 Types of Investors

3.2 Why One Should Invest their Money?

3.3 Points to consider before making any investment

3.4 Why portfolio is given so much importance

4 What is Investment Analysis? 15

5 Importance of Decision Making 20

6 Risk and Return 22

7 Investment Avenues in India 26

7.1 Investment in Shares

7.2 Investment in Derivative

7.3 Investment in Commodity Market

7.4 Mutual Fund Scheme

7.5 Investment in Gold And Silver (BULLION)

7.6 Deposit With Banks

7.8 Postal Saving Scheme/ Postal Office Saving

Scheme

7.9 Public Provident Scheme

7.10 LIC Scheme

7.11 Investment in Money Market Securities

7.12 investment in Real Estate Properties

8 Recommendation 69

9 Billiography 70

5 Spectrum of Investment Avenues in India

Executive Summary

There has been a phenomenal growth in the Indian capital

market in recent year. The number of investor has grown up to 30

millions. The Government of India has initiated a change in the

economic and financial policies of the country. The liberalised schemes

were announced with a view to overcome the foreign exchange crisis

due to adverse Balance of Payment in 1991.

The abolition of controller of capital issue and establishment of

Securities and Exchange Board of India (SEBI) which have significantly

contributed in changing investment scenario.

The need for investment arise not only for the institution but also

for the individual with surplus fund which they desire to invest for short

or long period with safety and fair return. For investors, various

alternative avenues of investment are available with specific features,

advantages and limitation and is suitability under certain

circumstances.

It‟s for the investor to find out the best alternative means of

Investment Avenue which is suitable for his needs and requirements.

Some investment avenues provide maximum safety but low return

while some investment avenues offers attractive return but limited

margin on safety, some avenues offer Tax benefit. One particular

avenue may be suitable for one investor while same may not be

suitable for other. Similarly some investor give more importance to

profitability i.e. Return on investment while other give more importance

to safety and security of the fund invested. In brief, every investor has

to find out one or more avenues for investment and act accordingly.

Every investment decision has become increasingly important in

recent days. Sound decisions are made on the basis of knowledge and

skills. There are several point needs to considers for investment decision.

There is no readymade formula which will always work. Investor should

realise that investment are made under condition of uncertainty. A

sound decision can be made if the investor is familiar with the various

alternatives investment available. An investment decision at any point

of time depends upon the individual‟s needs and preferences on one

hand and outlook for various types of securities and real property on

the other hand.

Most of Indian investor are still unaware of various investment

avenues available their features, advantages and disadvantages.

6 Spectrum of Investment Avenues in India

So, the problem definition of this project is as under:

a. Different types Investment Avenue in India

b. Risk and Return

7 Spectrum of Investment Avenues in India

Company Profile:

AM Investments is basically a small firm which deals in all types of small

and big business activities which can start form opening of an account

of a person who is interested in investing in shares giving them proper

guidance how to invest in shares and what are the terms and

conditions to it .It also deals in exports of soap products to the Gulf

countries mainly Dubai and supply semi-ripped mangoes to Akbar

allays in Mumbai.

It mainly concern with the deal of purchase and sale of shares with

Angel Broking connected with BSE On-Line trading System (BOLT).The

Angel Group is a member of the Bombay Stock Exchange (BSE),

National Stock Exchange (NSE) and the two leading Commodity

Exchanges in the country: NCDEX & MCX. Angel is also registered as a

Depository Participant with CDSL. AM Investment Business

would deal in Equity Trading Commodities, Portfolio Management

Services, Mutual Funds, Life Insurance, Personal Loans, Depository

Services, and Investment Advisory.

Angel Group mainly deals in the below:

Angel Broking Ltd,Angel Commodities Broking Ltd.,Angel Securities Ltd.

AM investment would deal in above of the investment in whole. But I

was mainly been associated with the Angel Broking Securities in the

firm and information regarding export and supply of mangoes to Akbar

allays. But the manager would give us all the information regarding the

investments as he used to suggest the investors those who felt that

shares are risky and the can lose money and he used to convince

them that they should not panic in such a situation but remain still. Even

when they are not been convinced by this he would suggest them to

invest in other government policies were no much risk is involved in it.

He would mainly insist us to sit on the BOLT and see how a change

takes place on the BOLT and to determine now further changes will

take place in it.

8 Spectrum of Investment Avenues in India

Introduction: Investors include individuals and institutional with surplus funds for short

and long run term investments. For all types of investors, alternative

investment avenues are easily available. Every avenue has certain

special features, advantages, limitations and suitability. It is for the

investors to select the best avenues for safe and profitable investment

of their savings/surplus funds. Some investment avenues provide

maximum safety but low return (e.g. GOI saving bonds or government

securities) while some others offer attractive return but limited safety

(e.g. Corporate Securities). Some more avenues offer tax benefits. One

particular avenue may be suitable/convenient to one investor while

the investors give importance to attractive return while others may give

priority to safety and security of the funds invested. In brief, every

investor has to find out one or more avenues for investment as per his

expectation and invest accordingly. One avenue may not necessarily

be convenient to all categories of investors.

Sometimes, an ordinary investor gets confused due to the availability of

varied investment avenues. He finds it difficult to select an avenue

which is most convenient to him. Moreover, the avenues for investment

are increasing rapidly in India. For example, mutual funds bring

availability of varieties of avenues; an investor actually enters in the

wonderland of investment. He keeps on moving in this wonderland in

order to find out the most convenient avenue for his investment. For this

he has to the relative merits and limitation of alternative avenues and

select one or two avenues to achieve his investment objective. An

investor can prepare a sound investment plan provided he is familiar

with various investment avenues. At present investment consultant (e.g.

M/S Blue-chip Corporate Investment Centre, Ltd.) are available. They

guide investors in the selection of most appropriate investment

avenues. In addition, door to door investment service is provided.

Hundreds of investors across India take benefits of such services free of

charge. Even investment agents provide detailed information on

different investment avenues and help the client in the selection of

appropriate avenues suitable to their specific requirements.

In addition, there are investment counsellors who undertake investment

counselling. They study the specific problems of individual investor and

guide him in his investment decisions. The counsellor knows details of

investment avenues and can suggest the avenues which will be most

suitable to a particular investor. This investment counselling service is

necessary in the present period when investment avenues are

increasing and an investor is not aware of details of investment

9 Spectrum of Investment Avenues in India

avenues. Faulty investment is always harmful to the investor as his

income from such investment may be low or he may not be able to

convert his investment into cash when urgently required. Here.

Investment counselling is useful. The investment counsellor is competent

to help and guide his clients in the right direction so as to avoid undue

risk in the investment. Even suitable changes in the investment avenues

can be suggested by the investment counsellor. He acts as a friend

and guide to his clients and offer them timely guidance. The relation

between the investor and his counsellor should be always cordial. In

India, there is urgent need of investment counselling particularly in

urban areas and big cities. The income of the people is increasing

rapidly so as the inflation. They have excess funds for profitable

investment. Here investment counselling is required. This suggests that

there is an ample scope of investment counselling in India.

10 Spectrum of Investment Avenues in India

Types of Investors:

Avenues for investment are the outlet or agencies useful for investment

of funds. Such investments are many but varied in character. Similarly,

investor are also quite large in number broadly classified into Individual

Investor and Institutional Investor.

o Individual Investor:

Individual investor are individual with surplus money (saving) to invest in

order to have some return on the investment made. This return may be

in the form of interest, dividend, bonus, shares or capital appreciation

of the investment made (short/long term Capital Gain). individual

investor include salaried people, retired employee, businessmen.

Housewives, Professional and so on. in India, an individual

in the 25-35 years age group may plan for purchase of a house and

vehicle, an individual belonging to the age group of 35-45 years may

plan for children‟s education and children‟s marriage, an individual in

his or her fifties would be planning for post-retirement life.

o Institutional Investor

Institutional investor include, financial agencies and other institutions

which desire to invest their surplus funds. Charitable/religious trust,

banks, insurance companies, cultural and educational institutions, etc.

can be treated as an institutional investor.

Moreover, all categories of investors are equally interested in safety,

liquidity and reasonable return on the fund invested.

In India, the avenues for investment are many and their numbers is

continuously increasing along with new development in the capital

market. In the olden days, people used to keep their saving in post

offices and in government securities. They used to purchase gold and

silver generally for occasion purpose. At present , these avenues have

lost their traditional importance as money can be invested more

profitably in the corporate securities, Public Provident Fund (PPF), UTI,

Mutual Funds and so on. The ample avenue give investor more choices

and benefit to the investor provided they have necessary knowledge ,

skill and experience for the selection of best avenues

11 Spectrum of Investment Avenues in India

Why one should invest their money? The answer to this question is very simple; one should invest their money

to get some income over it. Nowadays people also invest in some

securities for tax exemption under income tax act, people also invest

their money in order to compensate future expenses e.g child

education, children wedding, retirement, sickness, construction of

house – etc, which is nothing but personal objective of investor.

Points to consider before making any investment

o Investment Objective:

Before making any investment an investor should first set up his

personal objective than financial objective. Financial objective include

safety and security of the money invested (principal amount),

profitability (through interest and capital appreciation).Financial

objective should be given importance in the lights of personal

objective, because it is personal objective that is going to decide the

size of investment, type of investment and period of investment. Such

objective may be monetary/financial or personal in character. The

objective include safety and security of the funds invested (principal

amount), profitability (through interest, dividend and capital

appreciation) and liquidity (convertibility into cash as and when

required). These objective are universal in character as every investor

will like to have a fair balance of these three financial objectives. An

investor will not like to take undue risk about his principal amount even

when the interest is high and attractive.

o Period of Investment:

Period of investment relates to liquidity, therefore Period of investment

is one major consideration while selecting suitable avenue for

investment. Such period may be short (up to one year), medium (one

to three years) or long (more than three years). Return is more on

longer investment then shorter or medium investment. Example, LIC

policy is an investment for a very period as the investment id made for

the old age hence liquidity is low, whereas balance in the saving bank

account is a short term investment therefore liquidity is higher because

withdrawal is possible at any time as per need. People also invest in

share market on intra-day basis, that is the shortest period of investment

people can take exit from the market any time he want and vice

versa.

12 Spectrum of Investment Avenues in India

o Risk in investment:

It is the third factor that needs to be given importance before any

investment decision. Risk needs careful consideration while selecting

the avenue for investment. Risk is a normal feature in every investment,

as it is said “higher the risk, higher the return and lower the risk lower the

return”, the degree of risk and uncertainty may be more in some

investment avenues while it may be less in case of other avenues. In

addition, Liquidity risk, Inflation risk, Market Risk, Business Risk, Political

Risk, etc also connected with the investment made. Example – risk is

more, if the period of maturity of loan is longer. Similarly, the risk is less in

case of debt instrument (e.g. Debenture) and more in case of

ownership instrument (Equity Share). Certain type of risk is unavoidable

while some other can be estimated to some extent.

The objective of an investor should be to minimise the risk involved in

the investment and maximise the return out of the investment made.

There has to be proper balance between the risk involve and the return

available.

o Return on Investment:

An investor would like to have at least reasonable return on his

investment in terms of dividend, interest and capital appreciation. The

return is a reward of the risk undertaken and also for parting with

liquidity. Return on investment includes current income which is in the

form of interest or dividend earned on a yearly basis. The return on

investment is in the form of capital gains which may in the form of

increase in the market price of the investment. For example, a share of

Rs.10 may be available for Rs.25 at time of purchase. However, after 10

years, the market price of the same share mat reach to Rs.100, here,

Rs.75 (Rs.100 – Rs. 25) is the capital gain for the investor. He gets

dividend for a period of ten years and also capital gain at rate of Rs.75

per share.

o Miscellaneous Factors:

An investor has to consider some more factors while selecting a

suitable avenue for investment. Such factors are:

(i) Tax benefit available.

(ii) Availability of loan facility.

(iii) Initial investment amount and future marketability of

investment.

(iv) Capital appreciation.

(v) Availability of funds for investment and post retirement benefit

available.

13 Spectrum of Investment Avenues in India

(vi) Market standing of market borrowing agency.

(vii) Nomination facility and transfer of investment on the name of

close relative.

In short, selection of suitable avenue for investment depends on various

factors. An integrated approach on part of investor is necessary in this

regard. An investor also needs proper education, training and

guidance for the selection of most convenient avenues for his

investment. It is delicate decision which needs proper knowledge,

judgement and vision.

14 Spectrum of Investment Avenues in India

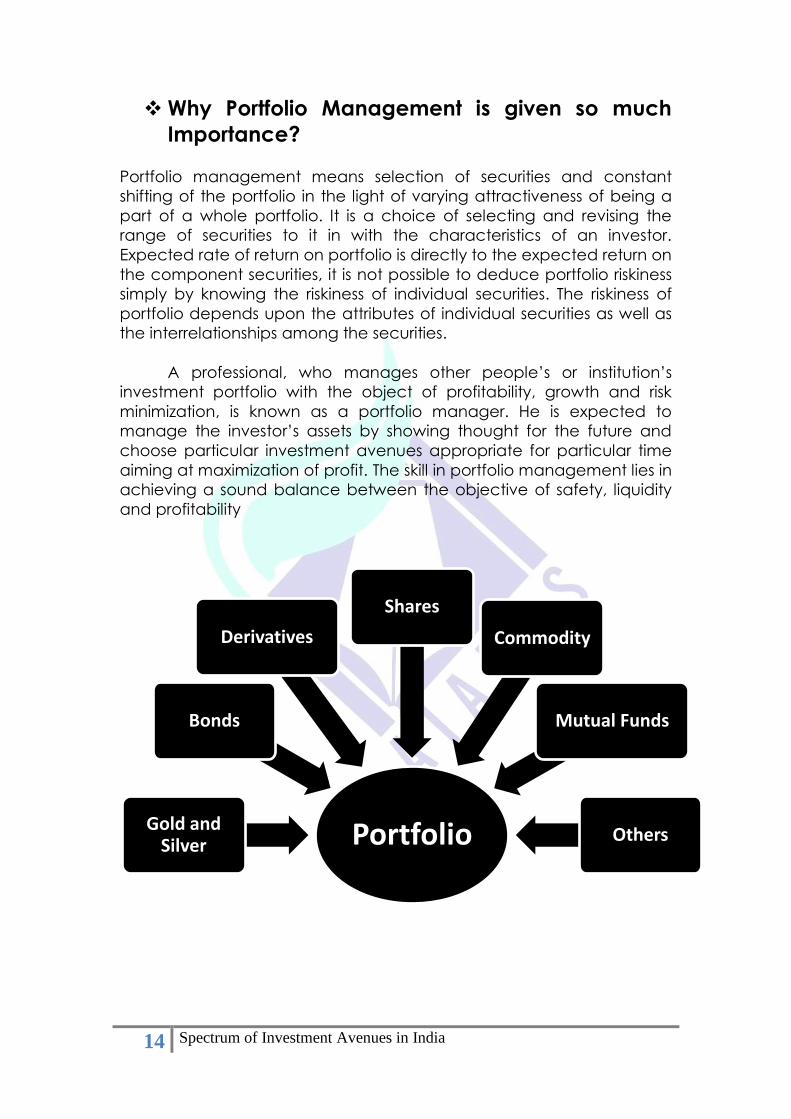

Why Portfolio Management is given so much

Importance?

Portfolio management means selection of securities and constant

shifting of the portfolio in the light of varying attractiveness of being a

part of a whole portfolio. It is a choice of selecting and revising the

range of securities to it in with the characteristics of an investor.

Expected rate of return on portfolio is directly to the expected return on

the component securities, it is not possible to deduce portfolio riskiness

simply by knowing the riskiness of individual securities. The riskiness of

portfolio depends upon the attributes of individual securities as well as

the interrelationships among the securities.

A professional, who manages other people‟s or institution‟s

investment portfolio with the object of profitability, growth and risk

minimization, is known as a portfolio manager. He is expected to

manage the investor‟s assets by showing thought for the future and

choose particular investment avenues appropriate for particular time

aiming at maximization of profit. The skill in portfolio management lies in

achieving a sound balance between the objective of safety, liquidity

and profitability

PortfolioGold and Silver

Bonds

Derivatives

Shares

Commodity

Mutual Funds

Others

15 Spectrum of Investment Avenues in India

What is Investment Analysis?

An investor has to analyse the securities available for investment.

Investment Analysis means to make a comparative study of the type of

industry, kind of security, fixed or variable securities. This helps to form

beliefs regarding future behaviour of price and stocks, the expected

return and risk associated with it. It helps investors regarding various

features such as liquidity, safety, income stability, capital appreciation,

tax incentive and legality. All investment decisions are to be made on

scientific analysis.

o FUNDAMENTAL ANALYSIS:

The primary purpose of any investment is to gain profit; it may be for

short or longer period. Therefore, fundamental analysis is a method of

finding out the future price of a security which an investor wants to buy.

The method of forecasting the future behaviour of investment, the rate

of return etc. is based on an analysis of the broad economic

environment in order to operates, a kind of industry to which it belongs

and the analysis of the internal working of the company through the

financial statement of the company which must be able to find out the

price movement of the shares and help to understand where to invest

their money effectively. The economy and industry would be necessary

to decide when, where and how much to invest. Thus, a look into the

monetary fiscal and demographic factors can give basic idea into the

trends in the economy.

Fundamental Analysis includes:

a) Economic Analysis

b) Industry Analysis

c) Company Analysi

a) Economic Analysis:

A study of economics forces which would give an idea about

future corporate earnings, payment of dividend, an interest to

investor is known as economic analysis. Some of the important

forces for economics analysis are: population, research and

technological developments, capital formation, natural

resources and raw material.

Population gives an idea of the kind of labour form available in

the country. Investor can invest on those industries amount of

16 Spectrum of Investment Avenues in India

share in the funds of the development of the country. Another

consideration of the investor is to invest in the company which

makes investment in capital goods or modernisation and

replacement of asset. The natural resources of the country are

responsible for its economic development. It is advisable to invest

in a company which utilises available natural resources of the

country.

Almost every piece of national legislation, substantial changes in

appropriation of funds by the government to specific

programme. Any changes in interest rate will have stimulating

impact on some companies. Investors should also get

knowledge of the present investment environment, the national

income figure, the wholesale price index, the agriculture and

industrial price indexes and the monetary policy and tax policy

for making economic analysis for making investment more

profitable.

b) Industry Analysis:

Industry analysis is the study of industries which are on the

upswing or growing. The ideal investment is the investment in

growing industry. There are certain industries which have been

growing in India. The recent examples are of entertainment and

computer software, petrochemical, bio-technology and capital

goods industries etc. Investment in these industries will definitely

gain in future.

Industry analysis should analyse and study of the following

factors.

1) Product line

2) Raw material and input

3) Capacity installed and utilised

4) Industry characteristics

5) Demand and market

6) Government policy with regards to industry

7) Labour and other industrial problems.

The investor should know the industry classification used in the

economy. It is also necessary to know the characteristics,

problems and practices in different industries. There is also need

to study the present and future development, operating

features, seasonal variation and competitiveness in order to

establish the proper perspective. In recent times the growth of

industries has been affected due to technological changes,

competitive pressure, population, etc

17 Spectrum of Investment Avenues in India

An investor should select few industries that are in the expansion

stages. Investment should not be made in the industries which

are in the pioneering stage. Similarly, industries that are in the

stagnation stage or declining stage its economic importance

should be avoided. Investor should select that company that

have developed a strong competitive position. It is difficult to

identify a good industry for investment. However an attempt to

analyze all the above factors should made by an investor.

An investor should measure the growth of the industry in terms of

Gross National Product. Those industries which are growing faster

than the growth if national income are useful for investment

purpose, and its growth rate is also useful for the investor to

analyse the prosperity and period between expansion and

growth. The economic and industry analysis is made in order to

have a broad idea of the forces affecting the investment.

c) Company Analysis:

The industry analysis helps to select few industries for investment

in securities. There are many companies in an industry. For

example \, is an investor want to invest in computer software

industry, then he has to select few companies from that industry.

There are thousands of listed companies from computer software

industry. Company analysis is the method to find out the worth of

the company. It is based on the analysis if the financial

statement of the company, it is the study of the variables which

influence the future price of a company‟s share. It is an

assessment of the company‟s competitive position, earning

capacity and profitability. It is a method of finding out the

intrinsic value of a company‟s share. This requires both internal as

well as external information.

The basic financial statements which are used as tools of

company analysis are the income statement, the balance sheet

and the statement of changes in financial position. While making

company analysis, investors should carefully judge that these

statements are correct, complete, consistent and comparable.

The most frequently used tools for company analysis are as

follows:

1) Ratio Analysis

2) Trend Analysis

3) Fund Flow Analysis

4) Common size Statement Analysis

5) Technical Analysis.

18 Spectrum of Investment Avenues in India

o TECHNICAL ANALYSIS:

Technical analysis is a study of market data in terms of factors affecting

supply and demand schedules, such as prices, volume of trading etc. it

is simple and quick method of forecasting behaviour of share prices.

The financial data and past behaviour of a company are presented on

charts and graphs in order to find out the history of price movement.

Technical analysis provides a simplified picture of price behaviour of

share. The analyst believe that the price of a share depends on

demand and supply in the stock market. They get the important

information about price and volume of a share in the stock market.

Investors, who use technical analysis, start checking the market action

of the share if it is favourable. They also examine the fundamental

factor and make sure that the company is sound and profitable.

Technical Analysis is based on certain assumption. These are

as follows:

1) The price of a security is related to demand and supply factor

operating in the market.

2) There are rational as well as irrational factors which affect the

supply and demand factors of a security.

3) The prices of securities behave in a manner that their movement

is continuous in a particular direction for some length of time.

4) Trend in the prices of securities have been seen to change when

there is shift in the demand and supply factors.

5) Whenever there are shifts in demand and supply, they can be

detected through charts prepared specially to show the action

of the market.

There are several way that technician think and act. At any given time,

many investor gain and many make loss. Technical analyst believe that

their method is simple and gives an investor a bird‟s eye view on the

future of security prices by measuring the past movement. They predict

the price behaviour through line chart, point charts, bar charts and

figure charts. There are large numbers of patterns which predict the

upward and downward swing in the market. This is not an accurate

method but it gives the general indication of the behaviour of prices in

the stock market.

19 Spectrum of Investment Avenues in India

Investment Decision

In order to enhance future wealth by generating income, each

individual has to make to separate decision. The first is saving decision.

It is concerned with the choice of how much of one‟s wealth consume

now and how much to consume later. The second is investment

decision, which relates the choice of portfolio or collection of assets

(instrument) for investment in which saving can be invested. Thus there

is a need for investment decision. The saving decision determine how

much to invest in securities, whereas, investment decision determine in

which securities or assets we can invest.

An individual may purchase a share of Rs. 1000 today in hopes of being

able to have Rs 1200 available for consuming a year from now with the

purpose in mind, think of an investment anything which is expected to

alter the owner‟s claim to consumption in present and future period.

The individual‟s purchase of share (investment) does this by reducing

consumption in the current period by Rs 1000 and by increasing

expected consumption by Rs 1200 in the future. In other words, there

are investment alternatives as well as investor‟s needs for which the

investment decision are necessary.

Investments are important as well as useful in the dynamic world. The

following factors provide investors to make investment decision:

(a) Increase in Income

(b) Retirement Benefit

(c) Contingency Arrangement

(d) Reduce Tax Liability

(e) If Basic Family Commitment such as Housing, Education,

Insurance, Marriage, Medical etc.

Individual have to decide from time to time about their saving and

investment on the basis of above factors. Basically, in making such

decisions, four things must be taken into account, which are as under

1) Available opportunities,

2) Preferences,

3) Market prices

4) Wealth.

20 Spectrum of Investment Avenues in India

Importance of Decision Making:

Investment is important in the context of present day conditions. The

following factors are responsible for making investment decision

increasingly important:

(a) Planning for retirement:

People retire at the age of 60. Individual have plan for their post

retirement life. Therefore, the earning from the employment should

be calculated and same portion of the earning should be saved.

The saving should be invested in such a manner that the investment

will appreciate sufficiently to provide stable income after retirement.

Thus, the investment decision is very important for an individual in

this respect.

(b) Tax saving:

Taxation is an important factor which influences the people to

invest. Individual manage to save and invest in such a manner

that their income tax is saved or minimised. Salaried people,

particularly, have to manage their investment in such a way that

their income tax will be saved or minimised. Investment in UIT,

ULIP, LIC NSC, post office deposits, PPF, mutual funds are eligible

for income tax relief to the investors. However, they have to take

investment decision in such a way that the investment will be

profitable, safe and the tax will be minimised.

(c) Interest rates:

Investors have to consider interest rates while making investment

decisions. As the objective of the investor is to maximise the

return on investment he will normally, select the investment which

will give the higher rate of interest. Thus, stability of interest is

important. However, a high rate of interest may not be the only

factor for selection of investment. The investor has to consider

other factor such as safety, liquidity, risk and legality of the

investment media. Interest rates may differ due to different

benefits offered by the investments. The investor has to take

proper decision on the basis of interest rates.

21 Spectrum of Investment Avenues in India

(d) Inflation:

In order to make the right choice of investments, investors have

to consider carefully the effect of inflation on their investment.

The investor has to consider an investment alternative which will

give a high rate of return in the form of interest to cover any

decrease in return due to inflation. Inflation has become a

continuous problem in India and hence, it is important for

investment decision making.

(e) Income:

Income level of investor goes on increasing due to inflation,

general increase in employment and other benefits and services.

If more income is generated investors find more revenues for

investment, however, investment decisions have become

important due to constant increase in income of the investors.

(f) Investment channels:

The growth and development of the country leads to greater

economic activities which provide large number of investment

channels. In India, investment opportunities and avenues have

increased due to liberalisation and free economy since 1991. This

has provided variety of investment opportunities. Thus, the

investors have the choice of variety of instruments. The investor

will have to try and achieve a proper investment mix between

high rate of return and stability of return to reap the benefit of

both. Therefore, investments decisions are important in modern

days.

An investor in order to fulfil his goals operates under certain constraints,

which are as follows:

Liquidity,

Age.

Need for regular income,

Time horizon,

Risk tolerance,

Tax liability.

The challenge in investment management lies in choosing the

appropriate investment which will meet the investment objectives of

the investor, subject to his constraints. Therefore, investment decision is

important from this point of view

22 Spectrum of Investment Avenues in India

Risk Return Analysis

Risk is a chance of loss. Investment risk exists where there is more than

one possible future return associated with an investment. If more than

one possible return exits and the investor has no idea of the

probabilities associated with the occurrence of any of the possible

future returns the situation is of complete investment uncertanity.

Investment certainly exists where there is only one possible return. The

investor is certain of the investment‟s return. Between the two extremes

of investment certainty and investment uncertainty lies the area of

investment risk. Under conditions of risk, investors realize that there is a

range of possible return and can associate some probability to each

possible return. This dispersion of possible returns represents risk. The

greater the dispersion of possible returns, on an investment, the greater

the risk.

The risks that equity shares can carry are:

Loss of dividend when no dividend is declared.

Low dividend i.e. dividend lower than bank‟s fixed deposit rates

of interest.

Stagnation or depreciation in the prices of shares and

Insolvency of the company.

o Types of Risk:

The various types of risks in investment may be classified as follows:

Default risk:

It is the risk of issuer of investment going bankrupt. An investor who

purchases shares or debentures will have to face the possibility of

default and bankruptcy of the company. In the case of fixed income

securities such as debentures or fixed deposits of companies, the

investor may take the care to see that the credit rating given to the

company, so that the risk can be minimized.

Business risk:

Business risk means the risk of a particular business failing thereby your

investment is lost. It is identifiable as the variation in the firm‟s earning

due to it‟s business or product line. The principle determinants of a firms

business risk are the variability of sales and it‟s operating leverage.

23 Spectrum of Investment Avenues in India

Operating leverage represents the firm‟s ability to translate increased

sales into increased profit. Business risk can be divided into two broad

categories, external and internal. External business risk is the result of

operating conditions imposed upon the firm by circumstances beyond

its control. Internal business risk is associated with the efficiency with

which a firm conducts its operations.

Financial risk:

The financial risk is function of the companies‟ capital structure or

financial leverage. The company may fall on financial grounds, if its

capital structure tends to make earnings unstable. Financial leverage

is the percent change in net earnings for a given result from the use of

debt financing in the capital structure. If a company uses a large

amount of debt, then it has contracted to pay a relatively large fixed

amount for its sources of capital. When the operating profits fall, the

company will have to pay large interest payments and the net profits

will fall even more. This is example of financial leverage. The like hood

of a company defaulting on its debt-servicing obligation is known as

financial risk.

Purchasing power risk:

The purchasing power risk of a security is the variation of real returns on

the security caused by inflation. Inflation reduces the purchasing

power of money over time. As price risk, the purchasing power of a

rupee falls and the real return on an investment may fall even though

the nominal return in current rupee rise. The impact of inflation is felt

greater in case of fixed income investments. On the other hand, in

case of fluctuating incomes like shares dividends, there is possibility of

the dividend rate being higher than the inflation rate. Thus, unless the

returns on your investments are higher than the inflation rate, your

investments are not profitable. The return on your investments after

adjusting for inflation is known as real rate of return.

Interest rate risk:

The earnings of companies and the performance of their shares are

sensitive to interest rates changes. Therefore, potential variability of

investment returns due to interest rate fluctuations is interest rate risk.

The prices of debt securities and all other securities with fixed payout

are dependent upon the level market interest rates. When interest rates

rise, bond values will generally fall. The degree of sensitivity to interest

rate changes will naturally differ from company to company.

24 Spectrum of Investment Avenues in India

Recently, companies have started issuing „floating rate bonds‟. The

rates of interest on these bonds are linked to some floating rate such as

„prime rate‟ or the banks minimum lending rate. When market interest

rate rise, the bond rate rises and when it fall, the bond rate also falls.

This is a good way of circumventing interest rate risk when interest

rates are on the rise. But in a situation where inflation is under control

and interest rates are on the decline, it is bond to be disadvantageous

to the investors.

Market risk:

The market risk means the variability in the rates of caused by the

market up swings or market down swings. It is caused by investor

reactions to tangible as well as intangible events in the market. Most

investors are quick to note about the security markets that returns on

securities tend to move together. That is, on a good day, the fact that

some stocks in the markets are rising seems to fuel enthusiasm, and

other sto7cks tend to rise also. On the other hand, when some stocks

begin to fall, others will also tend to fall as a mood of pessimism

pervades the market. This market psychology is the explanation of the

existence of market risk, while is the volatility of a security‟s return

attributable to changes in the level of market and have a high degree

of market risk, while others fluctuate very little as the market changes.

When a relatively small increase in the market usually accompanies a

relatively larger increase in the price of stock, the stock has a high

degree of market risk.

Liquidity risk:

Liquidity risk arises from the inability to convert an investment quickly

into cash. It refers to the ease with which a stock may be sold. If a stock

is highly liquid, it can be sold very quickly at a price which is more or

less equal to its previous market price. In a security market, liquidity risk

is function of the marketability of the security.

When an investor wants to sell a stock he is connected with its liquidity.

On the other hand, when an investor wants to buy a stock, he is

interested in its availability. A stock may be deemed to be easily, if it

can purchased quickly at a price more or less equal to its previous

price. A stock may be regarded as not easily available, if the purchaser

has to wait for quite sometimes to buy it at a price which is more or less

equal to the previous price. Alternatively, the purchaser, may, have to

offer a substantial premium in order to buy the stock quickly. Thus, the

lower marketability of stock gives a degree of liquidity risk that makes

the price of the stock a bit more uncertain.

25 Spectrum of Investment Avenues in India

Systematic and Unsystematic risk:

The fluctuation in an investment‟s return attribute to changes in broad

economic social or political factors which influence the return on

investment is systematic risk. It is that portion of total risk of security

which is caused by the influence of certain economic-wide factor like

money supply, inflation, level of government spending and monsoon

which have a bearing on the fortune of every company. Systematic risk

is undiversifiable risk and investors cannot avoid the risk arising from the

above factors.

Unsystematic risk is the variation in returns due to factors related to

the individual firm or security. It is that portion of the total risk which

arises from factors specific to particular firm such as plant breakdown,

labor strikes, sources of materials etc. It is possible to reduce

unsystematic risk by adding more securities the investor‟s portfolio. All

risky securities have some degree of unsystematic risk but combining

securities into diversified portfolios reduces unsystematic risk from the

portfolio. Therefore, unsystematic risk is often referred to as diversified

risk. The sum of systematic and unsystematic risks is equal to the total

risk of a security.

26 Spectrum of Investment Avenues in India

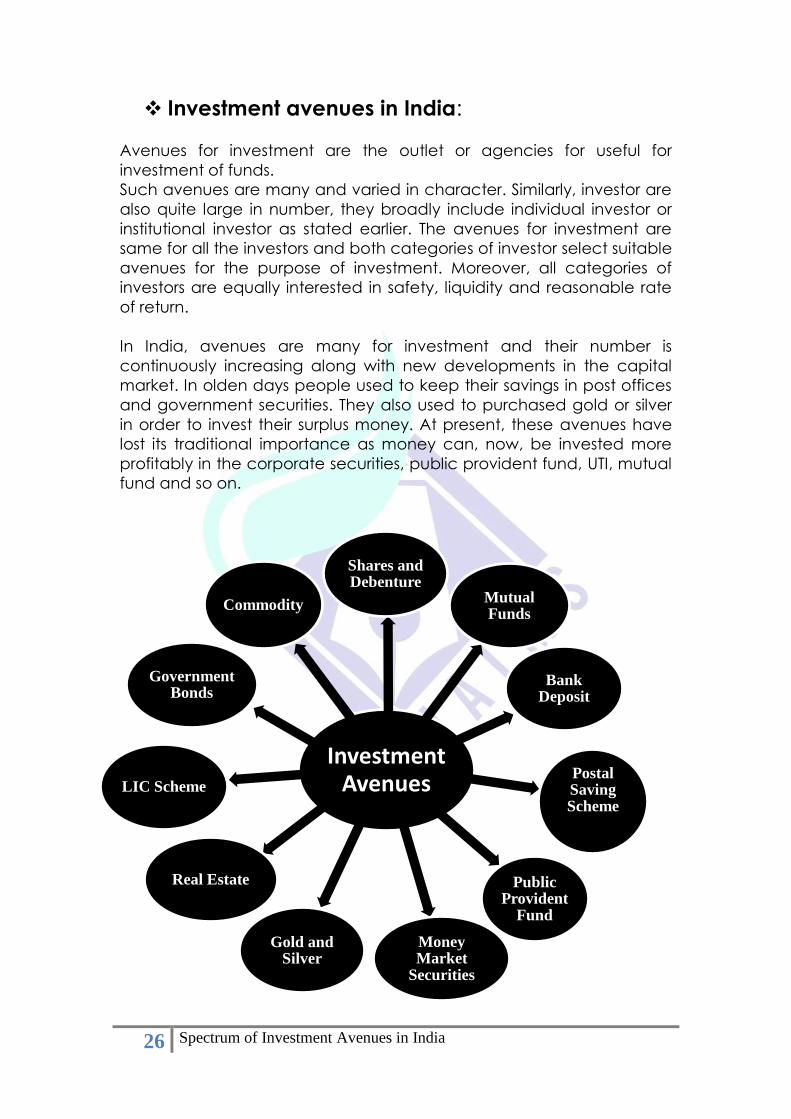

Investment avenues in India:

Avenues for investment are the outlet or agencies for useful for

investment of funds.

Such avenues are many and varied in character. Similarly, investor are

also quite large in number, they broadly include individual investor or

institutional investor as stated earlier. The avenues for investment are

same for all the investors and both categories of investor select suitable

avenues for the purpose of investment. Moreover, all categories of

investors are equally interested in safety, liquidity and reasonable rate

of return.

In India, avenues are many for investment and their number is

continuously increasing along with new developments in the capital

market. In olden days people used to keep their savings in post offices

and government securities. They also used to purchased gold or silver

in order to invest their surplus money. At present, these avenues have

lost its traditional importance as money can, now, be invested more

profitably in the corporate securities, public provident fund, UTI, mutual

fund and so on.

Investment Avenues

Shares and Debenture

Mutual Funds

Bank Deposit

Postal Saving Scheme

Public Provident

Fund

Money Market

Securities

Gold and Silver

Real Estate

LIC Scheme

Government Bonds

Commodity

27 Spectrum of Investment Avenues in India

Investment in share:

Joint stock companies collect their long term money/ fixed capital by

issuing share (equity/preference). This is called Stock Financing, share

are very popular amongst the investor class. Investment in share, are

risky as well as profitable. Transaction in share takes place in primary

and secondary markets. Large majority of investor prefer to invest their

money in shares through broker and other dealer operating on

commission basis. Purchasing of share is now easy and quick due to the

extensive use of computer and screen based trading based trading

system (STB‟s). Order can be registered on computers.

The shares are available for investment is classified into different

categories such as blue chip share, growth share, speculative share,

income share and so on. For proper investment in share the company

must be properly selected after studying the balance sheets and other

details of various companies. SHARE CERTIFICATE in physical form is no

more popular in India due to demat facility. It gives convenient in

handling and transfer of shares. For this, demat account can be

opened in the bank which provide depository service (e.g. ICICI

Demat).

o Advantage of investment in shares:

1) Equity shareholders get income in the form of dividend.

Companies offer attractive dividend to shareholder even when

the rate of dividend is flexible. Profitable and stable companies

offer good reward to their investors in the form of high rate of

dividend.

2) The liability of Equity shareholder is limited only to the extent of

their investment. Naturally, shareholder are not required to pay

anything more than the face value of the share purchased,

3) Shares are easily transferable and this facilitates easy transfer of

ownership at the option of shareholder. The transfer facility also

brings liquidity to the investment in shares.

4) The equity shareholders get an opportunity to participate in the

profitability of the company in the course of time. The profitable

companies also issue bonus share and rights shares from time to

time. Even the new shares issued by the companies are first

offered to existing shareholders. This pre-emptive right enables

28 Spectrum of Investment Avenues in India

existing shareholders to maintain their proportional ownership in

the additional share capital issued.

5) Listed equity share are actively quoted and traded on stock

exchanges. This marketability of equity shares brings liquidity to

the investment in share and also convenient to investors.

6) Equity shares carry Tax benefit. At present, dividend on the share

of Indian companies has been made tax free. However the

position may change as per the government policy.

7) Equity shareholders are the owner of the company with certain

power and voting rights. This enables them (collectively) to

exercise some control over the policies of the company.

8) Capital gain in equity investor is possible in the case of shares as

the price of the shares fluctuate along with the future prospect

of the company. Due to rise in the share price, there is a capital

appreciation and this offer extra benefit to the shareholders.

o Limitation of Investment in Shares:

1) Uncertainty of income/return: The return as regards investment in

shares is uncertain as it is linked with the profitability of the

company. The investment in share may prove to be the

unremunerative if the profit earn by the company is less.

2) Risky Investment: In the case of share, there is an element of

regards changing market values. The share price may go down

due to various reasons. This is bound to affect the investor

seriously. Secondly, selling at a low price bound to bring financial

loss. This suggests that investment is always risky.

3) Speculative activities are harmful: Speculative activities are quite

common as regards shares. However, such speculative deals

affect genuine investor and they may suffer loss even when they

are not directly involves in such speculative activities.

4) Future linked with company: In the case of shares, the future of

the shareholders is linked with the future of the company. The

return on investment will be attractive if the company makes

good profit. However, a shareholder may not get any return on

his investment if his company fails to get reasonably high profit.

29 Spectrum of Investment Avenues in India

Investment in Derivative: Derivative is a product whose value is derived from the value of one or

more basic variables, called bases (underlying asset, index, or

reference rate), in a contractual manner. The underlying asset can be

equity, FOREX, commodity or any other asset. According to Securities

Contracts (Regulation) Act, 1956 {SC(R)A}, derivatives is

A security derived from a debt instrument, share, loan, whether

secured or unsecured, risk instrument or contract for differences or any

other form of security. A contract which derives its value from the

prices, or index of prices, of underlying securities.

Derivatives are securities under the Securities Contract (Regulation) Act

and hence the trading of derivatives is governed by the regulatory

framework under the Securities Contract (Regulation) Act.

o Types of Derivative

There are mainly four types of derivatives i.e. Forwards, Futures, Options

and swaps.

Derivative

Forward

Future

Option

Calls

Puts

Swaps

Interest Rate Swap

Currency Swap

30 Spectrum of Investment Avenues in India

Forwards:

A forward contract is a customized contract between two entities,

where settlement takes place on a specific date in the future at

today's pre-agreed price.

Futures:

A futures contract is an agreement between two parties to buy or sell

an asset at a certain time in the future at a certain price. Futures

contracts are special types of forward contracts in the sense that the

former are standardized exchange -

traded contacts.

Options:

Options are of two types - calls and puts. Calls give the buyer the right

but not the obligation to buy a given quantity of the underlying asset,

at a given price on or before a given future date. Puts give the buyer

the right, but not the obligation to sell a given quantity of the

underlying asset at a given price on or before a given date.

Swaps:

Swaps are private agreements between two parties to exchange cash

flows in the future according to a prearranged formula. They can be

regarded as portfolios of forward contracts. The two commonly used

swaps are:

Interest rate swaps: These entail swapping only the interest

related cash flows between the parties in the same currency.

Currency swaps: These entail swapping both principal and

interest between the parties, with the cash flows in one direction

being in a different currency than those in the opposite direction.

Warrants:

Options generally have lives of upto one year, the majority of options

traded on options exchanges having a maximum maturity of nine

months. Longer-dated options are called warrants and are generally

traded over-the-counter.

31 Spectrum of Investment Avenues in India

LEAPS:

The acronym LEAPS means Long-Term Equity Anticipation Securities.

These are options having a maturity of upto three years.

Baskets:

Basket options are options on portfolios of underlying assets. The

underlying asset is usually a moving average or a basket of assets.

Equity index options are a form of basket options.

Swaptions:

Swaptions are options to buy or sell a swap that will become operative

at the expiry of the options. Thus a swaption is an option on a forward

swap. Rather than have calls and puts, the swaptions market has

receiver swaptions and payer swaptions. A receiver swaption is an

option to receive fixed and pay floating. A payer swaption is an option

to pay fixed and receive floating.

o Trading Participant in Derivative;

1) HEDGERS :

The process of managing the risk or risk management is called as

hedging. Hedgers are those individuals or firms who manage

their risk with the help of derivative products. Hedging does not

mean maximising of return. The main purpose for hedging is to

reduce the volatility of a portfolio by reducing the risk.

2) SPECULATORS :

Speculators do not have any position on which they enter into

futures and options Market i.e., they take the positions in the

futures market without having position in the underlying cash

market. They only have a particular view about future price of a

commodity, shares, stock index, interest rates or currency. They

consider various factors like demand and supply, market

positions, open interests, economic fundamentals, international

events, etc. to make predictions. They take risk in turn from high

returns. Speculators are essential in all markets – commodities,

equity, interest rates and currency. They help in providing the

market the much desired volume and liquidity.

32 Spectrum of Investment Avenues in India

3) ARBITRAGEURS :

Arbitrage is the simultaneous purchase and sale of the same

underlying in two different markets in an attempt to make profit

from price discrepancies between the two markets. Arbitrage

involves activity on several different instruments or assets

simultaneously to take advantage of price distortions judged to

be only temporary.

Arbitrage occupies a prominent position in the futures world. It is

the mechanism that keeps prices of futures contracts aligned

properly with prices of underlying assets. The objective is simply to

make profits without risk, but the complexity of arbitrage activity

is such that it is reserved to particularly well-informed and

experienced professional traders, equipped with powerful

calculating and data processing tools. Arbitrage may not be as

easy and costless as presumed.

o Advantages for investment in derivative;

1) Flexibility:

Derivatives can be used with respect to commodity price, interest and

exchange rates and equity price. They can be used in many ways.

2) Risk Reduction:

Derivatives can protect your business from huge losses. In fact,

derivatives allow you to cut down on non-essential risks.

3) Stable Economy:

Derivatives have a stabilizing effect on the economy by reducing the

number of businesses that go under due to volatile market forces.

o Disadvantages of Derivatives:

If derivatives are misused, they can boomerang on the company.

1) Credit Risk:

While derivatives cut down on the risks caused by a fluctuating market,

they increase credit risk. Even after minimizing the credit risk through

collateral, you still face some risk from credit protection agencies.

33 Spectrum of Investment Avenues in India

2) Crimes:

Derivatives have a high potential for misuse. They have been the

caused the downfall of many companies that used trade malpractices

and fraud.

3) Interest Rates:

Wrong forecasts can result in losses amounting to millions of dollars for

large companies; it can wipe out small businesses. You need to

accurately forecast the long term and short term interest rates,

something that many businesses cannot do.

o Minimizing Risks with Derivatives:

1) Future Exchanges:

Arrange the derivatives through future exchanges. You may need to

put in a lot of work here; you must keep track of all adjustments in the

market worth of the underlying asset.

2) Asset and Liability driven Transactions:

The transactions should be driven by asset and liability management.

You should not speculate based on future forecasts.

3) Derivative Policy:

A good derivative policy focuses more on cost management and less

on forecasting. It should aim for cutting down expenses and costs.

While dabbling in derivatives is risky if you choose to speculate,

derivatives can be an important tool for financial structuring and cost

management if you use them correctly. If you do not know how to start

investing in derivatives, you can consult a small business advisor or

financial consultant. Remember, if you do go for derivatives, always

play by the book and never try anything illegal.

34 Spectrum of Investment Avenues in India

Investment in Commodity Market

You may have your debt and equity funds in place, but investing in

commodities could just be the one element to improve your portfolio.

Commodity trading provides an ideal asset allocation, also helps you

hedge against inflation and buy a piece of global demand growth.

In 2003, the ban on commodity trading was lifted after 40 years in India.

Now, more and more people are interested in investing in this new

asset class. While price fluctuations in the sector could get rather

volatile depending on the category, returns are relatively higher.

However, as this is not a primary area of investment for most, there is a

lot of apprehension about when and how to invest.

o Why invest in commodities?

Commodities allow a portfolio to improve overall return at the same

level of risk. Ibbotson Associates, a leading US-based authority on asset

allocation estimates that commodities increased returns between 133

and 188 basis points, at no extra risk.

o Who should invest?

Any investor who wants to take advantage of price movements and

wishes to diversify his portfolio can invest in commodities. However,

retail and small investors should be careful while investing in

commodities as the swings are volatile and lack of knowledge may

result in loss of wealth.

Investors must understand the demand cycles that commodities go

through and should have a view on what factors may affect this.

Ideally, you should invest in select commodities that you can analyse

rather than speculate across products you have no idea about.

Investing in commodities should be undertaken as a kicker in your

portfolio and not as the first destination for your money.

35 Spectrum of Investment Avenues in India

o What is commodity trading?

It's an age-old phenomenon. Modern markets came up in the late 18th

century, when farming began to be modernised. Though the trade's

mechanisms have changed, the basics are still the same.

In common parlance, commodities means all types of products.

However, the Foreign Currency Regulation Act (FCRA) defines them as

'every kind of movable property other than actionable claims, money

and securities.'

Commodity trading is nothing but trading in commodity spot and

derivatives (futures). If you are keen on taking a buy or sell position

based on the future performance of agricultural commodities or

commodities like gold, silver, metals, or crude, then you could do so by

trading in commodity derivatives.

Commodity derivatives are traded on the National Commodity and

Derivative Exchange (NCDEX) and the Multi-Commodity Exchange

(MCX). Gold, silver, agri-commodities including grains, pulses, spices,

oils and oilseeds, mentha oil, metals and crude are some of the

commodities that these exchanges deal in.

Trading in commodities futures is quite similar to equity futures trading.

You could take a long position (where you buy a contract) or a short

position (where you sell it). Simply speaking, like in equity and other

markets, if you think prices are on their way up, you take a long position

and when prices are headed south you opt for a short position.

o What do you need to start trading?

Like equity markets, you have to fulfil the 'know your customer' norms

with a commodity broker. A photo identification, PAN and proof of

address are essential for registration. You will also have to sign the

necessary agreements with the broker.

o Is there a regulator for the commodity trading

market?

The Forward Markets Commission is the regulatory body for the

commodity market in India. It is the equivalent of the Securities and

Exchange Board of India (Sebi), which protects the interests of investors

in securities.

36 Spectrum of Investment Avenues in India

o What kind of products can be listed on the

commodity market?

All commodities produced in the agriculture, mineral and fossil sectors

have been sanctioned for futures trading. These include cereals, pulses,

ginned cotton, un-ginned

cotton, oilseeds, oils, jute, jute products, sugar, gur, potatoes, onions,

coffee, tea, petrochemicals, and bullion, among others.

o What are the risk factors?

Commodity trading is done in the form of futures and that throws up a

huge potential for profit and loss as it involves predictions of the future

and hence uncertainty and risk. Risk factors in commodity trading are

similar to futures trading in equity markets.

A major difference is that the information availability on supply and

demand cycles in commodity markets is not as robust and controlled

as the equity market.

o What are the factors that influence the commodity

prices in the market?

The commodity market is driven by demand and supply factors and

inventory, when it comes to perishable commodities such as

agricultural products and high demand products such as crude oil. Like

any market, the demand-supply equation influences the prices.

Variables like weather, social changes, government policies and global

factors influence the balance.

o What is the difference between directional trading

and day trading?

The key difference between commodity markets and stock markets is

the nature of products traded. Agricultural produce is unpredictable

and seasonal. During harvesting season, the prices of these

commodities is low as supply goes up. There are traders who use these

patterns to trade in the commodity market, and this is termed

directional trading.

37 Spectrum of Investment Avenues in India

Day trading in commodity markets is no different from day trading in

the equity market, where positions are bought in the morning and

squared off by the end of the day.

o How to keep updated?

Most commodity trading firms have a research team in place that

prepares commodity charts and conducts detailed study on the trends

of the commodity in question.

Investing strategies based on this research are usually provided to

clients.

They usually provide daily market reports before the market opens and

intra-day calls during trading hours, along with monthly and weekly

research reports.

38 Spectrum of Investment Avenues in India

Mutual Fund Scheme

“A mutual fund is formed by the coming together of a number of

investors who hand over surplus funds to a professional organisation to

manage their funds”.

UTI had virtual monopoly in the field of Mutual fund from 1964 to 1987.

After 1987, SBI (State Bank of India), Bank of India and other banks

financial institutions start their mutual funds (e.g. Kothari Pioneer Fund,

CRB Capital market and so on). They are given with recognition by

RBI/SEBI. Mutual funds, in general, are popular among the investing

class. Moreover, practically all mutual fund organisations are successful

in collecting crores of rupees from the investing class.

The main function of mutual fund is to mobilise the saving of the

general public and invest them in stock market securities. At present,

there is diversion of saving of the middle class investors from bank to

mutual funds. The government has thrown the field open to the private

sector and joint sector mutual funds.

More than 63 mutual funds are operating in India. The popular mutual

funds in India are as noted below:

1) HDFC Mutual Fund,

2) Birla Sun Life Mutual Fund,

3) Alliance Capital Mutual Fund,

4) Canbank Mutual Fund,

5) Pioneer ITI Mutual Fund,

6) Standard Chartered Mutual Fund,

7) Templetion India Income Fund,

8) Tata Mutual Fund,

9) Sundaram Mutual Fund,

10) Kotak Mutual Fund.

It may be noted that the investment scheme of Mutual fund are open-

ended or close-ended. In the open-ended scheme, there is no fixed

maturity period. Secondly, the investment can be encashed at any

time. The rate of conversion into cash will be the market rate available

on the day. The open-ended schemes of mutual fund are popular due

to these advantages. HDFC Prudence Fund is an example of an open-

ended and balanced fund.

In the close-ended scheme, the investment is for a fixed maturity

period. Encashment of the investment till maturity is not possible. This

means there is no liquidity to the investment as in the case of open-

39 Spectrum of Investment Avenues in India

ended schemes. The investors are paid back their invested money as

per the term agreed at the time of issue. The close-ended schemes of

mutual fund are no more popular with the mutual fund as well as with

the investors.

Mutual fund is a financial intermediary which collect saving of the

people for secured and profitable investment. The entire

income/profits of mutual fund are distributed among the investor in

proportion to their investment. Expenses of managing the fund are

charged to the fund. The mutual funds in India are registered as trusts

under the Indian Trust Act. The trustees are appointed and they look

after the management of the trust. They decide the investment policy

and give the benefit of professional investment through such mutual

fund. These funds are managed by financial and professional experts.

Naturally the saving collected from small investors is invested in a safe,

secured and profitable manner. This gives good income to the fund

and the investors are made party for sharing such income.

In brief, small investors get many benefits (and that to without any

botheration) due to the formation of mutual funds in India. Mutual fund

such as SBI mutual fund, LIC mutual fund, Indian Bank Mutual Fund, 20th

Century Mutual Fund, Shriram Mutual Fund, Tata Mutual fund, ICICI

Mutual Fund, BOI Mutual Fund are popular as they offer various service

and benefit to the investing class. Moreover, ordinary investor does not

have time, expertise and patience to take independent investment

decision on their own. Even the mutual funds starts by the public sector

banks (e.g. Canara Bank) are equally popular among the investor.

Mutual funds give wide publicity to their activities through press

advertisement in leading newspapers. UTI publishes such information on

monthly basis in the form of full page advertisement in the press.

o Benefit of Mutual Funds:

(1) Benefit of diversified and profitable investment:

Mutual Fund collects small saving of millions of people and pools

such savings for profitable investment. The funds collected are

invested in sound and profitable companies from different

industries. As a result the benefits are diversified and profitable

investments are available to small investors. Investment in mutual

funds is treated as liquid, reasonably safe and profitable

investment.

(2) Benefit of professional management:

40 Spectrum of Investment Avenues in India

Mutual fund is managed by trustees who are professional expert

in the field of finance, business and management. They frame

the investment policy for mutual fund. Naturally, carefully and

planned and sound investment decision are taken. The

investment made is safe as well as profitable. The benefit of such

professional management is passed on to every investor with the

mutual fund.

(3) Liquidity to the investment;

Mutual fund provides liquidity to the investment due to open-

ended investment schemes. The investor can sell his shares or

units in the market and recover his investment. Even repurchase

facility is also provided by mutual funds (e.g. UTI). This gives the

benefit of liquidity to the investors. The liquidity is not available in

the case of close-ended scheme of mutual funds. Here, the

investor has to wait till the maturity date. As a result, the

popularity of close-ended scheme is fast declining. However,

liquidity benefit is available in the open-ended scheme.

(4) Tax Benefit:

Tax benefits are given by the government to the investors of

mutual funds. This tax benefit relates to payment of income tax

on the income earned through such investment. The Tax relief

under 80L is one additional benefit available to investors of

mutual funds. In addition, investors can take tax benefit on the

amount invested in the scheme.

(5) Assured Allotment:

All application made to mutual funds for purchase of units are

normally honoured. This give the benefit of assured allotment to

the investors. Assured allotment avoids tension on part of the

investors. Loss of interest on application money is also avoided.

(6) Effective Regulation:

Mutual fund fund in India have to operate as per the guidelines

given by SEBI and also by the government or RBI from time to

time. There is supervision and control functioning of the mutual

funds. This is necessary for the protection of investors.

41 Spectrum of Investment Avenues in India

(7) Spread of Risk:

Mutual funds invest their funds in securities from different

industries. As a result, the risk in the portfolio management is

spread over a wider area. Some companies may incur losses but

such loss will be compensated by more profit of other companies

in which funds are invested.

(8) No Tension:

An investor gives his saving/surplus money to the mutual fund

and the fund looks after the investment of money collected from

such investors. The whole botheration of profitable and

diversified investment is given to the fund. In short, the investor

gets benefits without botheration and tension.

o Limitation of Investment in Mutual Funds:

(1) The investor are likely to come in difficulties If the Mutual funds (in

which funds are invested) is not managed efficiently. The rate of

return will go down and the investment may become risky.

(2) The investor has no direct control on their investment as the

investment policies are decided by the trustees.

(3) Investors of mutual funds are not given adequate information

about the functioning of their mutual funds. They gat the

information about irregularities, etc. when it is to late to introduce

remedial measures.

(4) The future of mutual fund investors is link with the future of mutual

funds. An investors may suffer because of mismanagement of

the mutual funds.

(5) The expectation (as regards return on investment) of investors

are fast growing in the case of mutual fund but the manager of

mutual funds find it hard to meet such high expectation of

investor.

42 Spectrum of Investment Avenues in India

o Scheme of Mutual Funds

Mutual funds have introduce many scheme for attracting investor and

also for collecting their saving. Such scheme include the following:

a) Open-Ended Scheme: Regular income scheme,

recurring investment scheme and cumulative growth

scheme.

b) Close-Ended Scheme: Dhanashree 1989, (LIC Mutual

Fund), IndJyoti, (Indian Bank Mutual Fund) and

Magnum Regular Income Scheme 1987 (SBI Mutual

Fund).

It may also be noted that basically there are 4 schemes by which

mutual fund collect money from the investor. Such schemes are:

a) Growth Scheme,

b) Income Scheme,

c) Balance Scheme

d) Money market scheme and

e) Tax Saving Scheme.

a) Growth Scheme:

Aim to provide capital appreciation over the medium to long

term. These schemes normally invest a majority of their funds in

equities and are willing to bear short-term decline in value for

possible future appreciation.

These Schemes are not for investors seeking regular income or

needing their money back in the short-term

Ideal for :

Investors in their prime earning years.

Investors seeking growth over the long-term.

b) Income Scheme:

Aim to provide regular and steady income to investors. These

schemes generally invest in fixed income securities such as bonds

and corporate debentures.

Ideal for : Capital appreciation in such schemes may be limited.

43 Spectrum of Investment Avenues in India

Retired people and others with a need for capital stability and

regular income.

Investors who need some income to supplement their earnings

c) Balanced Scheme: Aim to provide both growth and income by

periodically distributing a part of the income and capital gains

they earn. They invest in both shares and fixed income securities

in the proportion indicated in their offer documents. In a rising

stock market, the NAV of these schemes may not normally keep

pace, or fall equally when the market falls.

Ideal for :

Investors looking for a combination of income and moderate

growth.

d) Money Market Schemes:

Aim to provide easy liquidity, preservation of capital and

moderate income. These schemes generally invest in safer, short-