Embed Size (px)

Citation preview

SHRIMP PANEL

January 19, 2016Miami, FL

THE SHRIMP PANEL

2

John Sackton Sree Alturi

Bill Hoenig Robbins McIntosh

Alan WeitzerMike Seidel

Ray Jones Brendan Curran

David Pearce

SandroCoglitore

Overview• 2014-2015 shrimp production recovered– Lower prices for shrimp, difficulties for farmers– Expanded demand, rebound in US use of shrimp

in 2014 and 2015• 2016: Disease Issues may limit growth– Production for US market focused on large sizes– Competition from China will be factor– First Half of year may see light production

• Total Global Production is Likely to be Flat

3

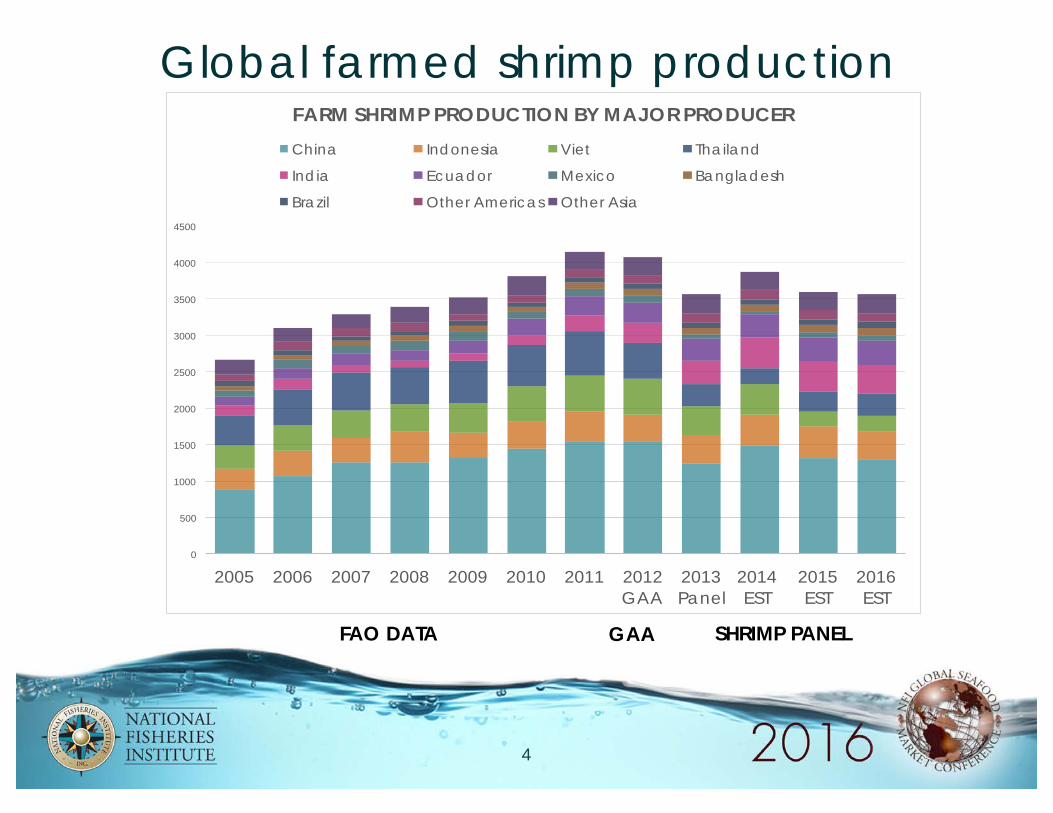

Global farmed shrimp production

FAO DATA GAA SHRIMP PANEL

4

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2005 2006 2007 2008 2009 2010 2011 2012 GAA

2013 Panel

2014 EST

2015 EST

2016 EST

FARM SHRIMP PRODUCTION BY MAJOR PRODUCERChina Indonesia Viet Thailand

India Ecuador Mexico Bangladesh

Brazil Other Americas Other Asia

Farmed Shrimp Exports

Note: China, Indo, Malaysia may include double-countingData: GTIS

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

2010 2011 2012 2013 2014 2015 Est

Exports of Six Major Shrimp Producers THAILAND INDIA ECUADOR CHINA INDONESIA MALAYSIA

5

US demand

US Customs Data

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

2011 2012 2013 2014 2015

POUN

DS

US Imports of Shrimp, All Types Jan-Nov THAILAND INDIA INDONESIA ECUADOR VIETNAM CHINA (MAINLAND)

MEXICO MALAYSIA PERU HONDURAS GUYANA PANAMA

NICARAGUA BANGLADESH GUATEMALA OTHER

6

Growth of shrimp volume may level off in 2016

• Production, major global exports, and US imports all show same pattern:– Losses due to disease in 2012, 2013– Recovery in volume in 2014 – Maintenance of volume in 2015

• 2016 US Imports will depend on India, Ecuador, and Indonesia, supplemented by Thailand, Vietnam, and Mexico.

Should production falter there are few places to make it up with expansion, as happened in 2014.

7

Shrimp disease from EMS to EHP• Recovery of shrimp volume in 2014-2015

largely due to new production areas; plus more control of EMS

• However deepening disease issues could mean a risk of decrease in overall supplies

• Extent of disease impacted producing areas is not likely to expand

• Current hot spots: White spot in India; EHP in China, EMS in Central America

8

How Should Buyers Understand Shrimp Diseases

• Disease issues occur in every growing area• Impacts include reduced growth, mortality,

higher costs • EMS is seen as an environmental problem,

not simply an animal mortality problem• EMS/EHP solutions include animal husbandry,

pond and environmental management; where these are poor, disease impacts will continue

9

10

No growth in supply forecast for 2016

Panel Global Production Estimates

10

0

500

1000

1500

2000

2500

3000

3500

4000

2014 EST 2015 EST 2016 EST

CHINA INDONESIA VIET THAILAND INDIA ECUADOR

MEXICO BANGLADESH BRAZIL OTHER AMERICAS OTHER ASIA

Why do our projections differ from 7.7% Annual growth rate at GAA

• We are forecasting slightly decreasing supplies in the first half of the year from 2 of the 3 major producers: Indonesia and India.

• Ecuador Should Remain Flat• This will not be fully compensated for by growth in

Thailand, Mexico, or Vietnam.• Between September 2015 and January 2016, the

evidence of production difficulties due to disease, weather and in some cases delayed reaction to low prices, has become more pronounced.

1111

India

2010-2014 Indian Gov’t Data; 2015-2016 Panel Estimates

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 Panel 2014 EST 2015 EST 2016 EST

000'

S M

ETRI

C TO

NS

12

Indonesia / Vietnam / Malaysia

Data from FAO, Panel Estimates

0

100

200

300

400

500

600

700

2010 2011 2012 2013 PANEL

2014 EST 2015 EST 2016 EST

000'

S M

ETRI

C TO

NS

INDONESIA VIETNAM MALAYSIA

13

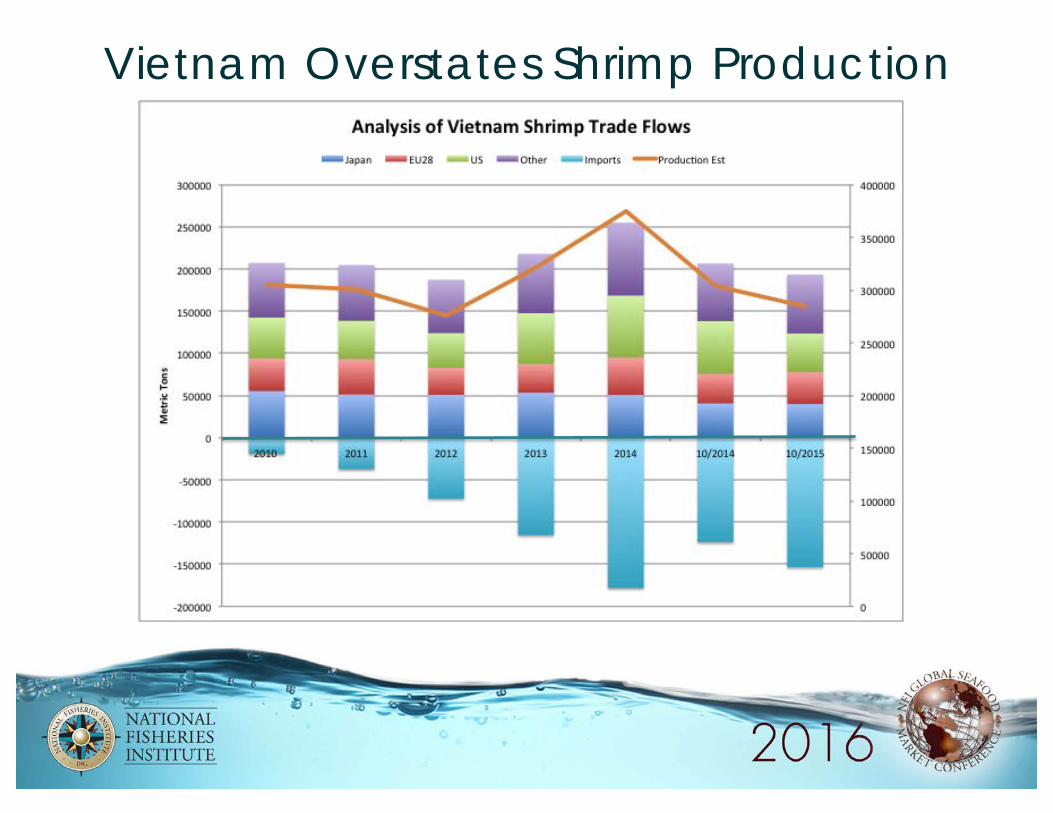

Vietnam Overstates Shrimp Production

Thailand

Data from Industry Estimates, Thai Frozen Food Assoc., Gov’t Data

0

100

200

300

400

500

600

700

2010 2011 2012 2013 Panel 2014 EST 2015 EST 2016 EST

000'

S M

ETRI

C T

ON

S

15

China production

Industry Estimates Based on Feed Sales

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013Panel 2014EST 2015EST 2016EST

000's

Metricto

ns

China

16

Ecuador

Government Export Data 2010-2014; Industry Estimates 2015-2016

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

2010 2011 2012 2013Panel 2014EST 2015EST 2016EST

000's

metricto

ns

EcuadorProduction

17

18

Mexico and Central America

Government and Industry Data

0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013Panel 2014EST 2015EST 2016EST

000'smetricto

ns

MexicoandCentralAmericaMexico Honduras Nicaragua Guatamala Panama

US Gulf production

Source: NMFS

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2010 2011 2012 2013 2014 2015*

000'

S PO

UND

S Gulf Domestic Shrimp Landings

FL AL MS LA TX

19

US share of total exports

Source: GTIS

20

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

India Ecuador Thailand Indonesia Malaysia China Vietnam

Percent Shipped to US by Major Exporters2011 2012 2013 2014 08/2015

20

Summary of Asian production outlook

Shrimp Panel Industry Estimates

1600

1700

1800

1900

2000

2100

2200

2300

0

500

1000

1500

2000

2500

2011 2012 2013 2014 2015 Est 2016 Est

000'

s M

etric

Tons

Asian production declined in 2015 and will be flat or barely higher in 2016

THAILAND VIETNAM INDIA INDONESIA CHINA MALAYSIA TOTAL

21

Panel estimates shrimp production declined in 2015, and will barely recover in 2016

Industry and Panelist estimates; 2011-2012 FAO data; 2013-2016 Panel

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2011 2012 2013 2014 2015 2016

000'

S M

ETRI

C T

ON

S

Panel Predictions for 2016 Major Country Production THAILAND INDIA INDONESIA ECUADOR VIETNAM MEXICO TOTALS

22

EU warmwater shrimp imports declined 6.5% thru Sept 2015

Source: Eurostat

155

160

165

170

175

180

185

190

195

200

2013 2014 2015

000'

MET

RIC

TO

NS

EU Warmwater Shrimp Imports

23

Japan

Japan Customs Data

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

2010 2011 2012 2013 2014 11/2014 11/2015

MET

RIC

TO

NS

Japan Farmed Shrimp Imports (Major Countries) VIETNAM INDIA INDONESIA CHINA THAILAND MYANMAR

MALAYSIA PHILIPPINES BANGLADESH SRI LANKA ECUADOR

24

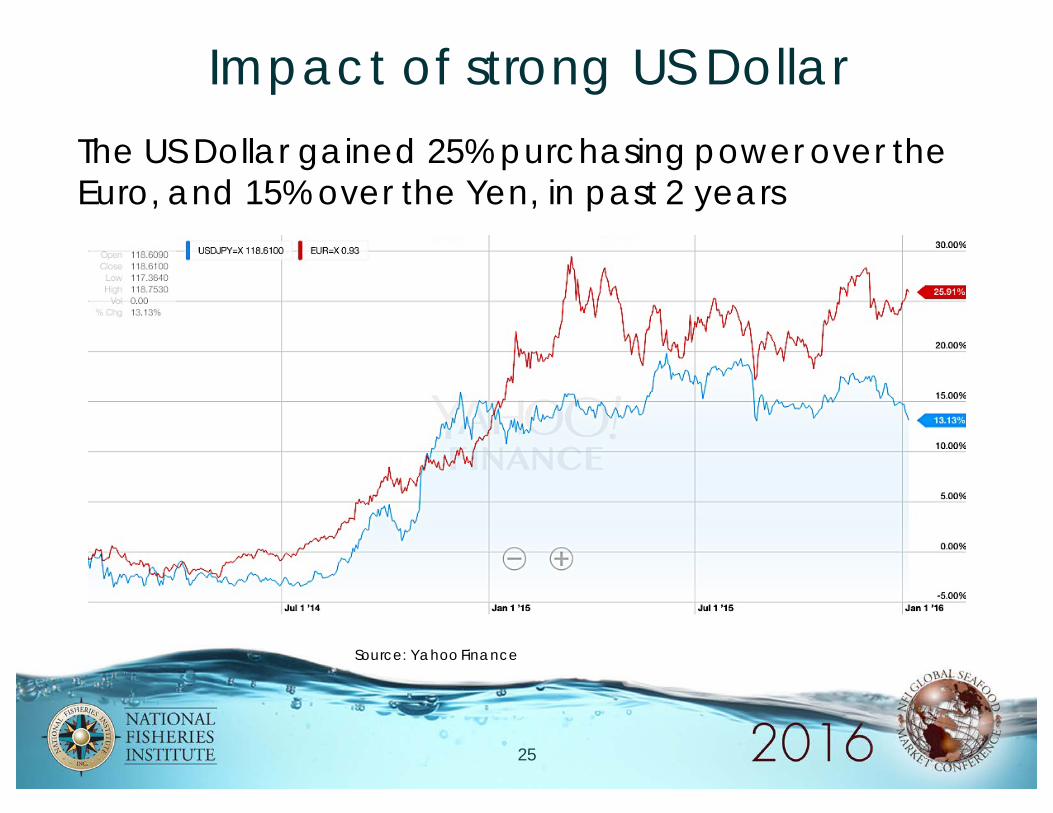

Impact of strong US DollarThe US Dollar gained 25% purchasing power over the Euro, and 15% over the Yen, in past 2 years

Source: Yahoo Finance

25

Relative market shareStrong dollar has allowed US to Increase global share of shrimp at same time total production is declining

Seafood Datasearch, Panel Estimates, Gov’t Trade Data

38.5%

47.6%

44.2%

46.8%

34.6%

28.4%

35.8%

33.8%

26.9%

24.0%

19.9% 19.3%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2013 2014 08/2014 08/2015

Relative Global Market Share from Major Farmed Shrimp ProducersUS EU JAPAN

26

Market risk factors other than supply

• China (Vietnam) demand– Crackdown on Gray Market– Change in demand for imports

• Continued Currency Volatility• El Niño impacts make production more

uncertain:– Ecuador, Central America, Indonesia

27

US retail demand• US retail demand for shrimp accelerated in

2015 with higher sales volume, lower prices,and more household penetration.

28

US retail demand

Source: retail scan data via Nielsen

250,000,000

260,000,000

270,000,000

280,000,000

290,000,000

300,000,000

310,000,000

$1,800,000,000

$1,900,000,000

$2,000,000,000

$2,100,000,000

$2,200,000,000

$2,300,000,000

$2,400,000,000

$2,500,000,000

CY 2011 CY 2012 CY 2013 CY 2014 52 Wk Nov 2015

VO

LUM

E IN

PO

UND

SAXI

S TITL

E

SALE

S IN

DO

LLA

RSA

XIS T

ITLE

All Retail: Shrimp Sales and VolumeDOLLAR SALES VOLUME LBS

29

2015 est(sept)

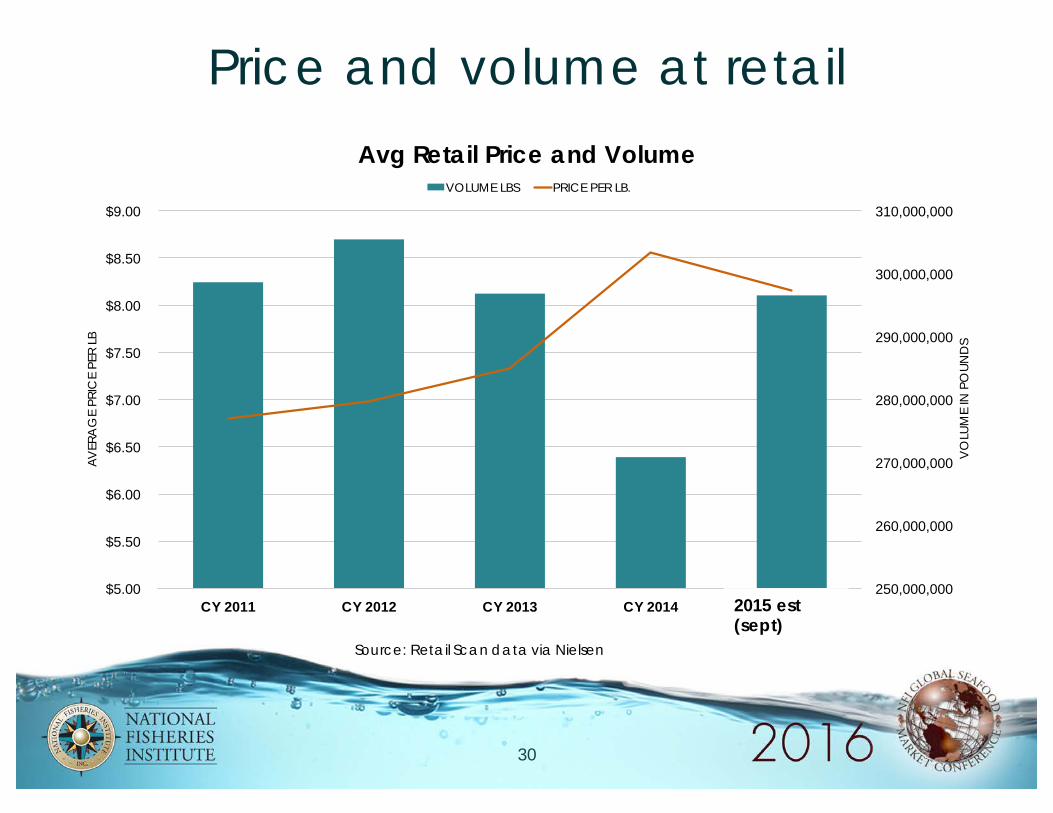

Price and volume at retail

Source: Retail Scan data via Nielsen

250,000,000

260,000,000

270,000,000

280,000,000

290,000,000

300,000,000

310,000,000

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

$8.00

$8.50

$9.00

CY 2011 CY 2012 CY 2013 CY 2014 52 Wk Nov 2015

VO

LUM

E IN

PO

UND

S

AVER

AG

E PR

ICE

PER

LB

Avg Retail Price and Volume VOLUME LBS PRICE PER LB.

30

2015 est(sept)

Shrimp household penetration

Source: Retail Scan Data via Nielsen

46.346.2

44.8

43.5

45.1

$6.79 $6.98

$7.33

$8.56

$8.16

42.0

42.5

43.0

43.5

44.0

44.5

45.0

45.5

46.0

46.5

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

CY 2011 CY 2012 CY 2013 CY 2014 52 Wk Nov 2015

PERC

ENT

OF

HO

USEH

OLD

S BU

YIN

G A

T RE

TAIL

AV

G D

OLL

ARS

PER

LB

Household Penetration and Shrimp Avg Retail Price PRICE PER LB. HOUSEHOLD PERCENT

31

2015 est(sept)

Retail momentum continued into December

• Favorable retail trends continued into December• For 12 weeks ending 12/21 vs Year Ago

– Dollar sales +4%– Unit sales +16%– Non-promoted unit price -16%

• For the 52 week period ending 12/21– Dollar sales +7%– Unit sales +14%– Non-promoted unit price -6.5%

• Retailer promotions on shrimp have improved

Source: Industry Estimates; Nielsen

32

US foodservice demand• Favorable trends in foodservice in 2015• Foodservice buyers sensitive to price

changes– Independent restaurants adjust size up or down– Long term trend to prefer large sizes

33

A 10-year trend of shrimp sizing sold by foodservice

Data Source: Collection of data from foodservice and shrimp suppliers

Most radical changes are growth in 16/20, 21/25, 26/30 and declines in 36/40, 51/60 and 71/90.

Above chart depicts “share” of sizes sold. Sizes less than U-15, 91-110, 110-130,130-150, 200-300 and 300-500 are not shown as each independently represent <2% of share with no radical gains/losses in the ten year period 2006-2015. Due to rounding some summarized data might be slightly +/- 100%.

34

Price changes impact customer behavior

Data Source: Collection of data from foodservice and shrimp suppliers. Price changes UB reports.

Between 2006 and 2015 share in the 51-90 range declines by 26 points; while 26/30 share grows 17 points, 21/25 grows 11 points and 16/20 grow 5 points. 41/50 stays constant.

2008:Share reduced 8 points in 41-60 range and did not move to 61-90 count range. Share shifts to 21-35 range.

2009:As prices drop, share loss of 7 points in 36-50 range. Share shifts to 21-30 range. 2010 & 2011: Nominal shifts throughout all sizes. 2012:As prices drop, share of 26/30 and 36/40 decline and 21/25 and 31/35 increase. 2013:Even while prices increase 26/30 and 31/35 share increase 2-3 times, while 21/25 lose share.2014:As prices further increase share shifts from larger sizes to smaller sizes.2015:Large price drops provide 3x growth for 16-25 range.

35

Certain customer types tend to shift shrimp sizes more than others

• Foodservice Independent Operators classified asCasual, Family, and Mexican seem to shift size the most,particularly influenced by market price changes.

• Foodservice Independent Operators classified as FineDining, as well as Italian have the largest share of 16-20,and tend not to shift sizes when markets change.

• 21-25 and 26-30 have gained the most appeal forFoodservice Operators classified as Casual, includingRegional and National Chains.

36

Larger shrimp have declined more in price since 2014

Source: Urner Barry

2.5

3.5

4.5

5.5

6.5

7.5

8.5

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

$/LB

. HSLO % Change Log Scale

HSLO ASIAN, WHITE, 16-20 COUNT HSLO ASIAN, WHITE, 21-25 COUNT HSLO C&SA, WHITE, 41-50 COUNT HSLO C&SA, WHITE, 61-70 COUNT

Over time, large sizes have adjusted lower; in current dollars

-50% -40% -30% -20% -10%

0% 10% 20% 30% 40% 50% 60%

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

HSLO % Change Log Scale HSLO ASIAN, WHITE, 16-20 COUNT HSLO ASIAN, WHITE, 21-25 COUNT HSLO C&SA, WHITE, 41-50 COUNT HSLO C&SA, WHITE, 61-70 COUNT

Over time, large sizes have adjusted lower; in current dollars

37

Indications of Holiday, Lent expectations

• What have been preliminary feedback onholiday sales at retail and foodservice?

• What are expectations for Lent

38

What are the critical dates and markers for 2016 shrimp availability

• First half– Indonesia production– Ecuador production– Lack of Central American production

• April / May:– Volume of production• India, Thailand

• June:– China (strength and size of first harvest) and Vietnam

production• Second half of year:– India, Thailand, Vietnam, Mexico

39

Price Ladder

Source: Urner Barry Comtell

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

$7.50

$8.00

HLSO U-15 HLSO 16-20 HLSO 21-25 HLSO 26-30

HLSO 31-35 HLSO 41-50 HLSO 51-60

40

Ecuador Head-on

Source: Urner Barry Comtell

1.95

2.45

2.95

3.45

3.95

4.45

4.95

5.45

5.95

HEAD-ON 30-40 HEAD-ON 40-50 HEAD-ON 60-70

41

Questions for 2016• US shrimp demand–Retail promotions– Foodservice traffic

• Timing of Heavy Production– First half vs. second half

42

Audience Questions (1)• What is your role in the Shrimp Industry

– Importer– Producer– Buyer– Distributor– Retail user– Foodservice user– Other

43

Audience Questions (2)• Which represents the biggest unknown

factor about 2016 shrimp market– Total global production– Impact of disease– Impact of Weather, El Nino– China’s economic performance– Strength of US currency– Strength of consumer demand– Competitiveness of Japan and Europe

44

Audience Questions (3)• What factors most concern you about the

seafood/shrimp business climate in 2016– Another supply shock– Price volatility– US economic recession, lack of demand– Increased costs of financing, importing– Political interference with trade– Overseas economic turmoil– None of the above

45

Audience Questions (4)• What changes do you see in shrimp /

seafood in 2016– US Consumption will Grow– US Consumption will Decline– Import sources of Shrimp will Resemble 2015– Import sources of Shrimp will Change in 2016

46

Time for Questions & Discussion

47

![[XLS] · Web view9789681663926 33648 1 91000 9789681666583 36077 1 17000 9788437061726 70270 1 124000 9789872302221 78120 1 38000 9788495939173 41233 1 160000 9788416830350 253541](https://img.pdfslide.us/doc/110x75/5bb449e909d3f28c2a8cb5b4/xls-web-view9789681663926-33648-1-91000-9789681666583-36077-1-17000-9788437061726.jpg)