Embed Size (px)

Citation preview

Final Report

PSA Tape Market in Europe“A State of the Industry”

Prepared for:Afera

July 31st, 2007

Confidential

F R A N K F U R T • C H I C A G O • D E T R O I T • G R E E N B A Y • S H A N G H A I • B E I J I N G

2Confidential

Background and ObjectivesBackground and Objectives

3Confidential

Afera needs to determine the Western European PSA tape production volume and future perspectives.Afera needs to determine the Western European PSA tape production volume and future perspectives.

Afera, the European Association for the Self Adhesive Tape Industry, seeks for a better understanding of the 2006 Western European PSA tape production.

Afera leadership has commissioned a market study to the Martec Group primarily focused on the 2006 tape production volume in Western Europe.

• Martec has interviewed Afera members across Western Europe regarding their estimations, industry trends and developments

50 interviews with active, associated and affiliated members have been conducted in total

• The primary objective of this study was to generate the production size (volume and value) and growth (5-year forecast) by key tape segment, substrate and adhesive type including:

Tape Type - Industrial Tapes, Industrial Specialty Tapes and Healthcare Tapes Substrate - Film, Paper, Woven fabric, Foil and Foam Adhesive Type - Solvent-based, Water-based and others such as hot melts and

UV&EB • Martec conducted a similar focused effort in the US with member companies of the PSTC

to confirm the 2005 PSA tape production For the European study, Martec has confronted member companies of Afera with a

similar tape segmentation to that used in US, which was generally accepted amongst members – this segmentation will facilitate comparisons between regions

4Confidential

Other information needs of secondary importance were as follows:

• Trends in each tape segment, adhesive usage, substrate usage and in end-use markets

• How is the value chain in each tape segment structured?

• Is there a threat coming from Asia/China and/or Eastern Europe?

• How does the REACH legislation affect the PSA tape industry?

• Is e-commerce something that the PSA tape industry is considering to implement?

• Is the compliance with current regulations, e.g. providing material safety data sheets for the automotive industry a challenge/problem for the industry?

• Is the current re-positioning of several players within the industry (e.g. tape manufacturers going for vertical integration, converters going to private labelling, etc.) a positive or negative aspect?

Bridging upon the success of the 2005 PSTC industry effort, Martec employed a 3-step research process to drive the information collection process.

• Afera introduced the study and Martec to members via mass communication providing Martec with a contact list of members to include in the survey

• Martec developed a production size (m²) template by segment and subsegment

• Martec scheduled telephone interviews with Afera members in order to discuss the production size template

The study was based upon a qualitative methodology designed to capture appropriate production size metrics.The study was based upon a qualitative methodology designed to capture appropriate production size metrics.

5Confidential

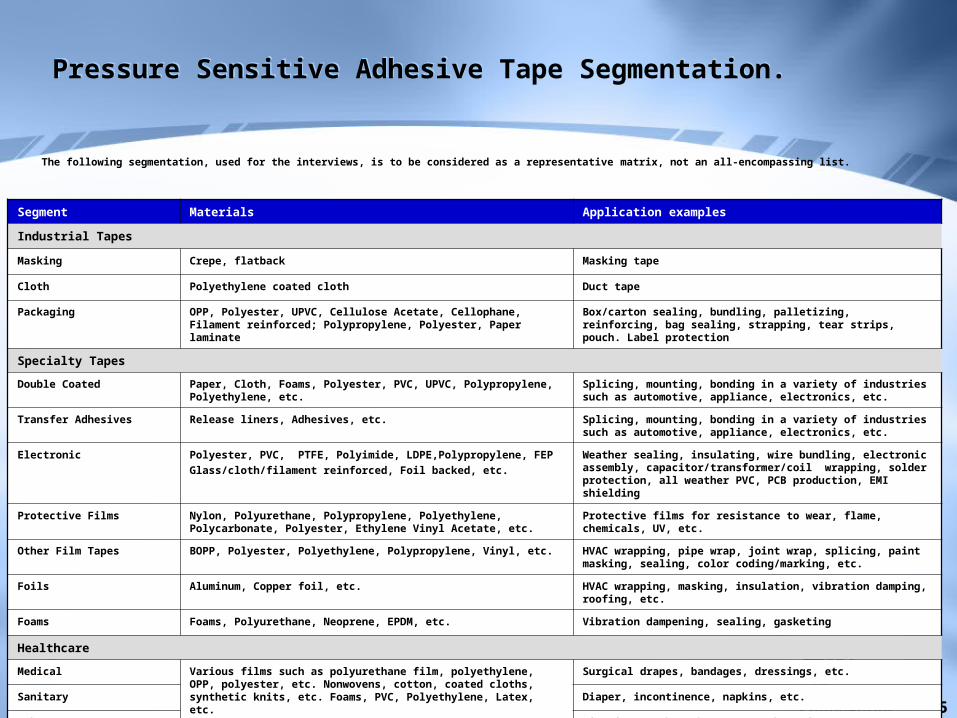

The following segmentation, used for the interviews, is to be considered as a representative matrix, not an all-encompassing list.

Pressure Sensitive Adhesive Tape Segmentation. Pressure Sensitive Adhesive Tape Segmentation.

Segment Materials Application examples

Industrial Tapes

Masking Crepe, flatback Masking tape

Cloth Polyethylene coated cloth Duct tape

Packaging OPP, Polyester, UPVC, Cellulose Acetate, Cellophane, Filament reinforced; Polypropylene, Polyester, Paper laminate

Box/carton sealing, bundling, palletizing, reinforcing, bag sealing, strapping, tear strips, pouch. Label protection

Specialty Tapes

Double Coated Paper, Cloth, Foams, Polyester, PVC, UPVC, Polypropylene, Polyethylene, etc.

Splicing, mounting, bonding in a variety of industries such as automotive, appliance, electronics, etc.

Transfer Adhesives Release liners, Adhesives, etc. Splicing, mounting, bonding in a variety of industries such as automotive, appliance, electronics, etc.

Electronic Polyester, PVC, PTFE, Polyimide, LDPE,Polypropylene, FEP

Glass/cloth/filament reinforced, Foil backed, etc.

Weather sealing, insulating, wire bundling, electronic assembly, capacitor/transformer/coil wrapping, solder protection, all weather PVC, PCB production, EMI shielding

Protective Films Nylon, Polyurethane, Polypropylene, Polyethylene, Polycarbonate, Polyester, Ethylene Vinyl Acetate, etc.

Protective films for resistance to wear, flame, chemicals, UV, etc.

Other Film Tapes BOPP, Polyester, Polyethylene, Polypropylene, Vinyl, etc. HVAC wrapping, pipe wrap, joint wrap, splicing, paint masking, sealing, color coding/marking, etc.

Foils Aluminum, Copper foil, etc. HVAC wrapping, masking, insulation, vibration damping, roofing, etc.

Foams Foams, Polyurethane, Neoprene, EPDM, etc. Vibration dampening, sealing, gasketing

Healthcare

Medical Various films such as polyurethane film, polyethylene, OPP, polyester, etc. Nonwovens, cotton, coated cloths, synthetic knits, etc. Foams, PVC, Polyethylene, Latex, etc.

Surgical drapes, bandages, dressings, etc.

Sanitary Diaper, incontinence, napkins, etc.

Other Nicotine patches, hormone patches, foot care, etc.

6Confidential

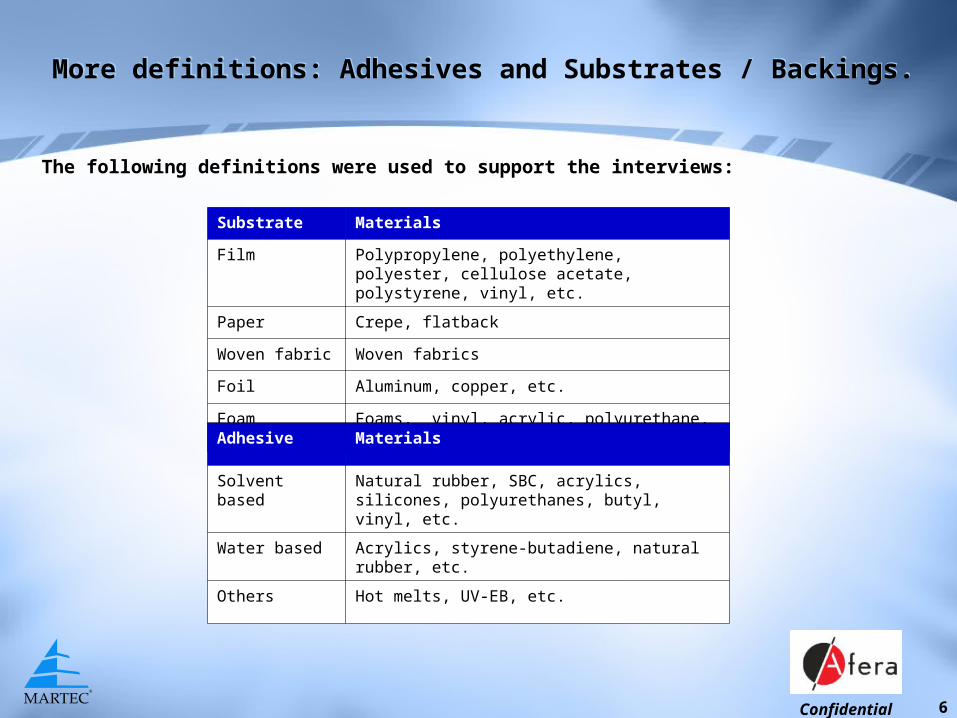

The following definitions were used to support the interviews:

More definitions: Adhesives and Substrates / Backings. More definitions: Adhesives and Substrates / Backings.

Substrate Materials

Film Polypropylene, polyethylene, polyester, cellulose acetate, polystyrene, vinyl, etc.

Paper Crepe, flatback

Woven fabric Woven fabrics

Foil Aluminum, copper, etc.

Foam Foams, vinyl, acrylic, polyurethane, silicone, etc.

Adhesive Materials

Solvent based Natural rubber, SBC, acrylics, silicones, polyurethanes, butyl, vinyl, etc.

Water based Acrylics, styrene-butadiene, natural rubber, etc.

Others Hot melts, UV-EB, etc.

7Confidential

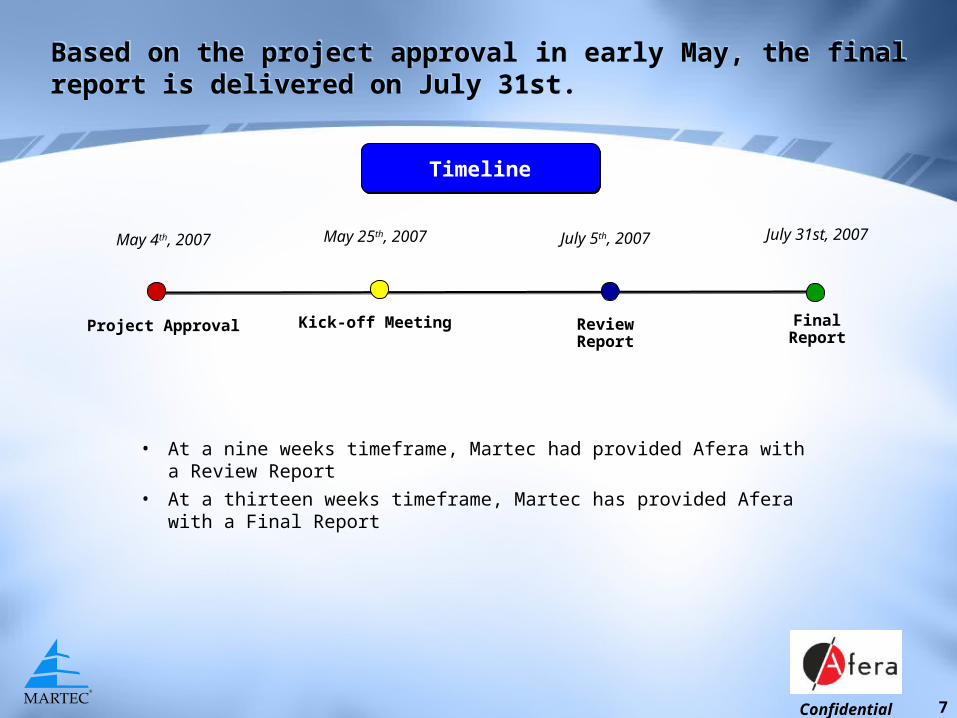

July 31st, 2007

FinalReport

May 4th, 2007

Project Approval

Based on the project approval in early May, the final report is delivered on July 31st.Based on the project approval in early May, the final report is delivered on July 31st.

TimelineTimeline

July 5th, 2007

ReviewReport

• At a nine weeks timeframe, Martec had provided Afera with a Review Report

• At a thirteen weeks timeframe, Martec has provided Afera with a Final Report

May 25th, 2007

Kick-off Meeting

8Confidential

FindingsFindings

9Confidential

Members interviewed across Western Europe included tape manufacturers, adhesive manufacturers, converters, paper and equipment manufacturers serving the tape industry.

Most respondents accepted and agreed with the tape segmentation presented, although some referred to “consumer tapes” and “packaging tapes” as subsegments that should in fact have a segment of their own.

• According to the members, the main reason for “packaging tapes” potentially being a segment on its own is its share of the total PSA tape production, i.e. approx. 80% of industrial tapes which corresponds with ~ 60% of total

• Some companies referred to their end-markets as determining factor for tape segmentation and classification, e.g. automotive, electronic, etc.

Many companies are only active in “niche applications” which made it almost impossible for them to estimate the total production.

• Particularly larger European tape manufacturers such as Tesa, Scapa Tapes, etc. who participate in the industrial and/or specialty tapes segments mostly, were able to give their estimations of the total production volume

The majority of the member companies who have participated in the survey are positioned within the Industrial and Specialty Tapes segments.

The majority of the member companies who have participated in the survey are positioned within the Industrial and Specialty Tapes segments.

10Confidential

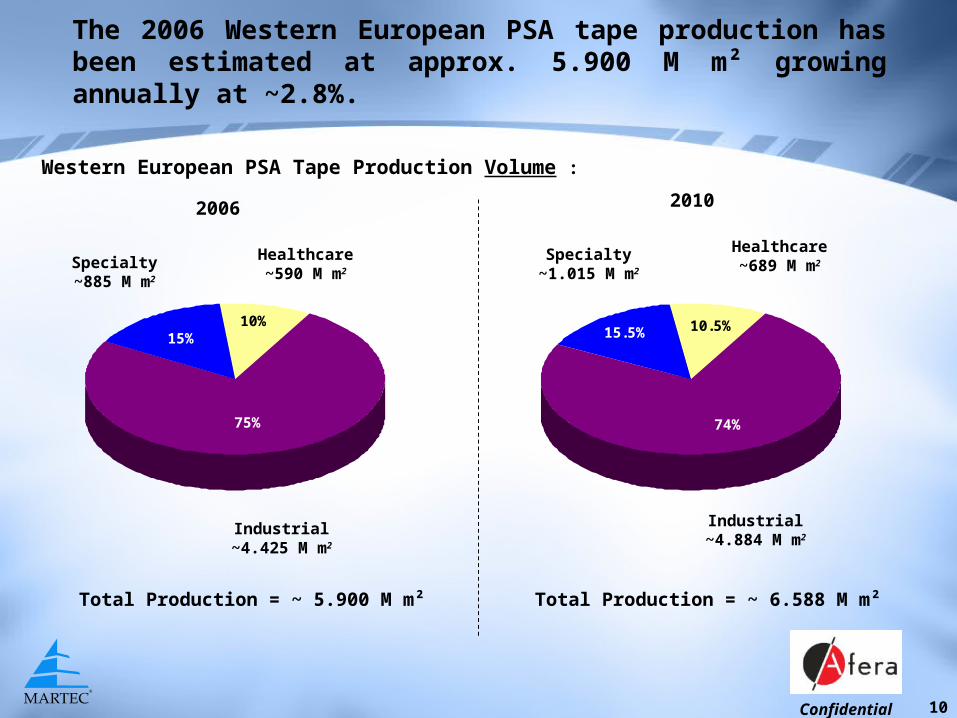

The 2006 Western European PSA tape production has been estimated at approx. 5.900 M m² growing annually at ~2.8%.

75%

15%10%

Healthcare~590 M m2

Industrial~4.425 M m2

Specialty~885 M m2

20102006

Total Production = ~ 5.900 M m²

74%

15.5% 10.5%

Total Production = ~ 6.588 M m²

Healthcare~689 M m2

Industrial~4.884 M m2

Specialty~1.015 M m2

Western European PSA Tape Production Volume :

11Confidential

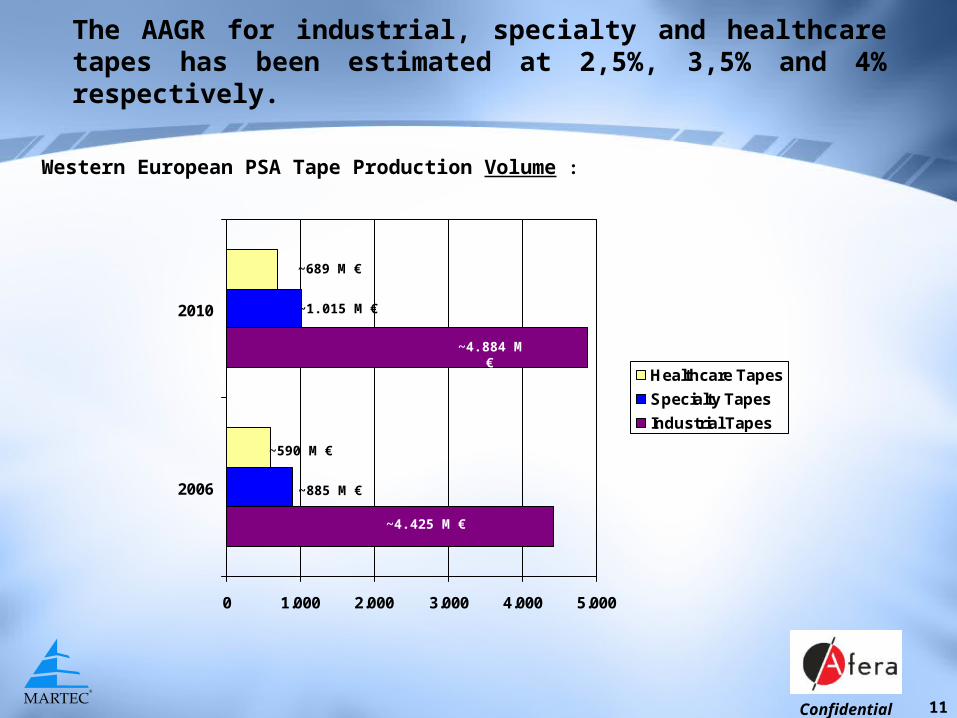

The AAGR for industrial, specialty and healthcare tapes has been estimated at 2,5%, 3,5% and 4% respectively.

Western European PSA Tape Production Volume :

0 1.000 2.000 3.000 4.000 5.000

2006

2010

Healthcare Tapes

Specialty Tapes

Industrial Tapes

~689 M €

~1.015 M €

~4.884 M €

~590 M €

~885 M €

~4.425 M €

12Confidential

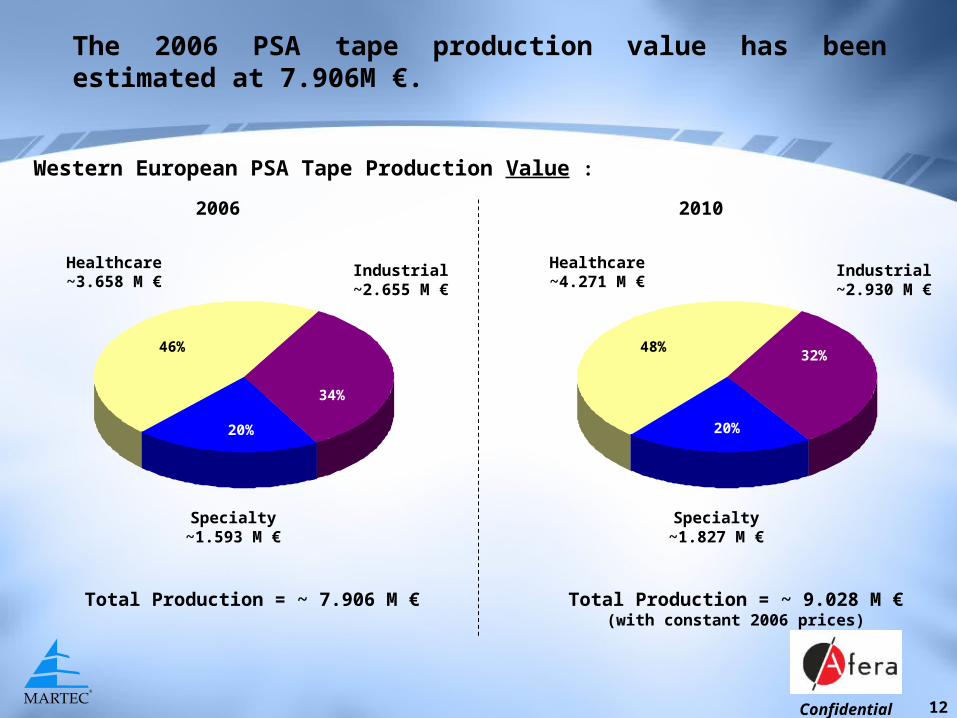

The 2006 PSA tape production value has been estimated at 7.906M €.

34%

20%

46%

Healthcare~3.658 M €

Industrial~2.655 M €

Specialty~1.593 M €

2006

Total Production = ~ 7.906 M €

Western European PSA Tape Production Value :

32%

20%

48%

Healthcare~4.271 M €

Industrial~2.930 M €

Specialty~1.827 M €

2010

Total Production = ~ 9.028 M €(with constant 2006 prices)

13Confidential

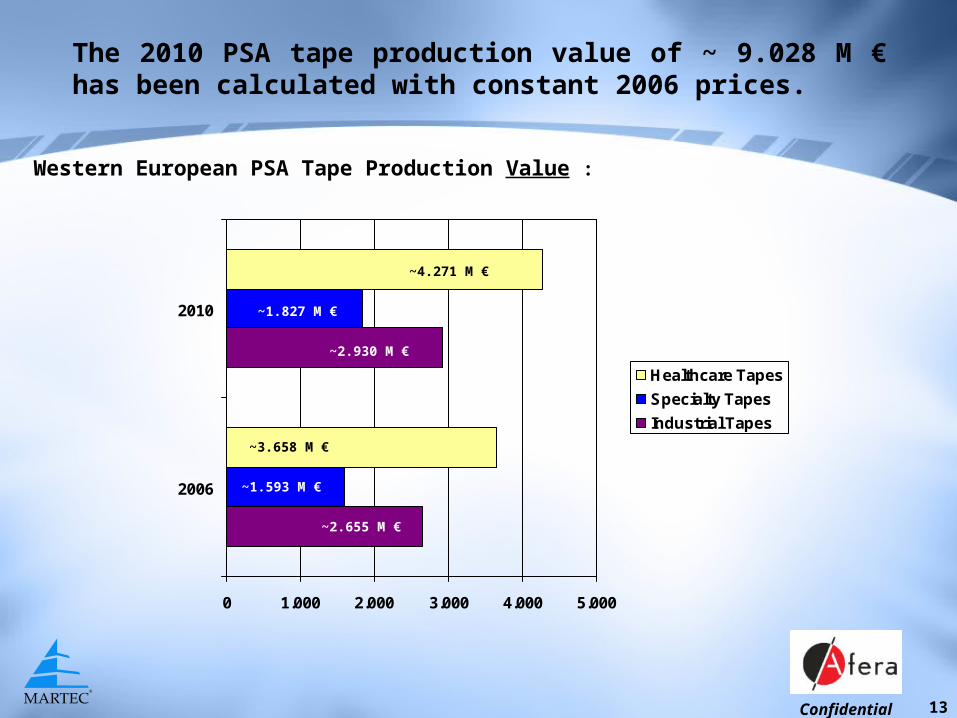

The 2010 PSA tape production value of ~ 9.028 M € has been calculated with constant 2006 prices.

Western European PSA Tape Production Value :

0 1.000 2.000 3.000 4.000 5.000

2006

2010

Healthcare Tapes

Specialty Tapes

Industrial Tapes

~4.271 M €

~1.827 M €

~2.930 M €

~3.658 M €

~1.593 M €

~2.655 M €

14Confidential

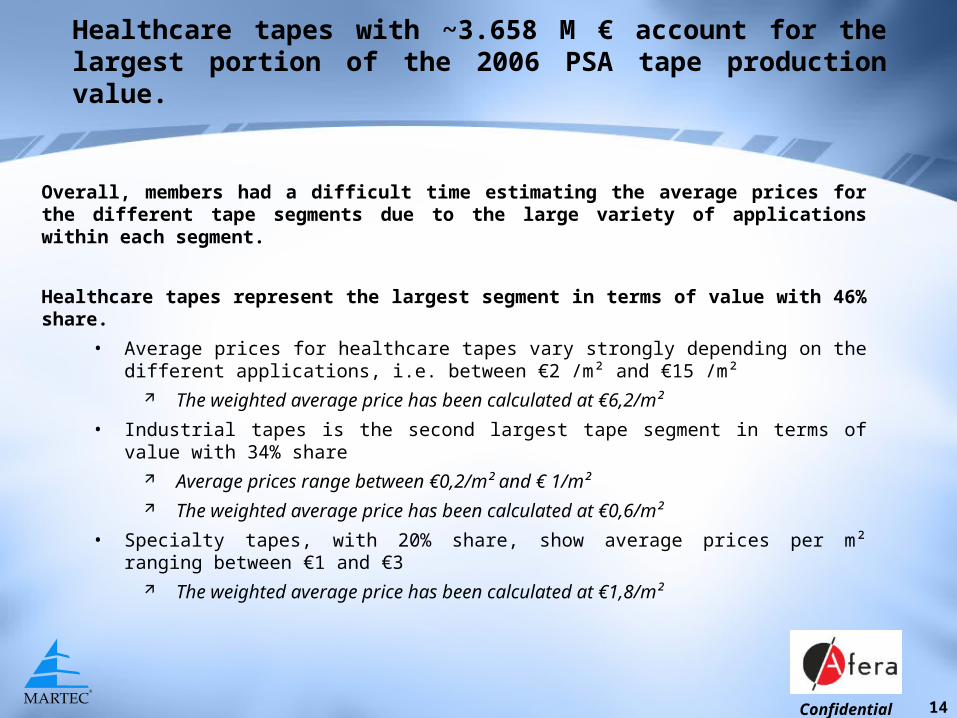

Healthcare tapes with ~3.658 M € account for the largest portion of the 2006 PSA tape production value.

Overall, members had a difficult time estimating the average prices for the different tape segments due to the large variety of applications within each segment.

Healthcare tapes represent the largest segment in terms of value with 46% share.

• Average prices for healthcare tapes vary strongly depending on the different applications, i.e. between €2 /m² and €15 /m²

The weighted average price has been calculated at €6,2/m²

• Industrial tapes is the second largest tape segment in terms of value with 34% share Average prices range between €0,2/m² and € 1/m² The weighted average price has been calculated at €0,6/m²

• Specialty tapes, with 20% share, show average prices per m² ranging between €1 and €3 The weighted average price has been calculated at €1,8/m²

15Confidential

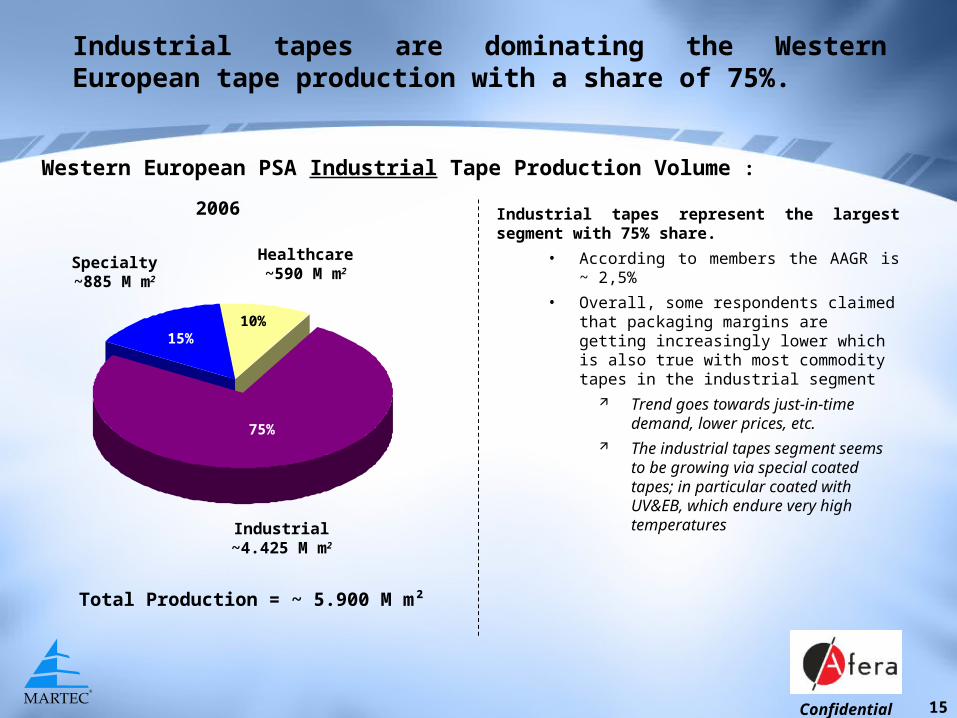

Industrial tapes are dominating the Western European tape production with a share of 75%.

75%

15%10%

Healthcare~590 M m2

Industrial~4.425 M m2

Specialty~885 M m2

2006

Total Production = ~ 5.900 M m²

Western European PSA Industrial Tape Production Volume :

Industrial tapes represent the largest segment with 75% share.

• According to members the AAGR is ~ 2,5%

• Overall, some respondents claimed that packaging margins are getting increasingly lower which is also true with most commodity tapes in the industrial segment

Trend goes towards just-in-time demand, lower prices, etc.

The industrial tapes segment seems to be growing via special coated tapes; in particular coated with UV&EB, which endure very high temperatures

16Confidential

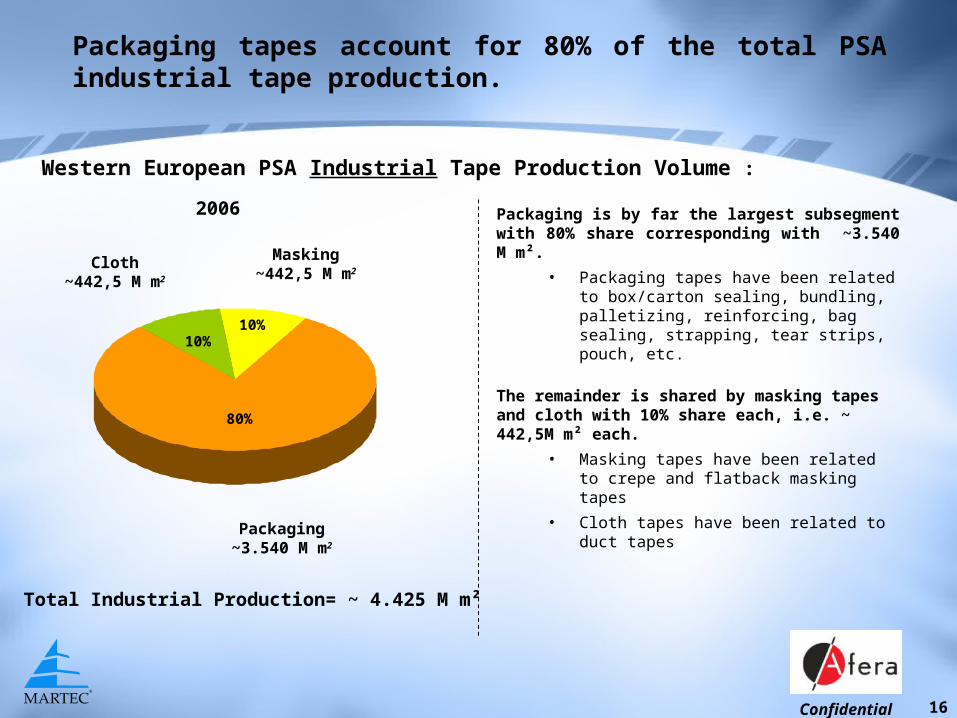

Packaging tapes account for 80% of the total PSA industrial tape production.

80%

10%10%

Masking~442,5 M m2

Packaging~3.540 M m2

Cloth~442,5 M m2

2006

Total Industrial Production= ~ 4.425 M m²

Western European PSA Industrial Tape Production Volume :

Packaging is by far the largest subsegment with 80% share corresponding with ~3.540 M m².

• Packaging tapes have been related to box/carton sealing, bundling, palletizing, reinforcing, bag sealing, strapping, tear strips, pouch, etc.

The remainder is shared by masking tapes and cloth with 10% share each, i.e. ~ 442,5M m² each.

• Masking tapes have been related to crepe and flatback masking tapes

• Cloth tapes have been related to duct tapes

17Confidential

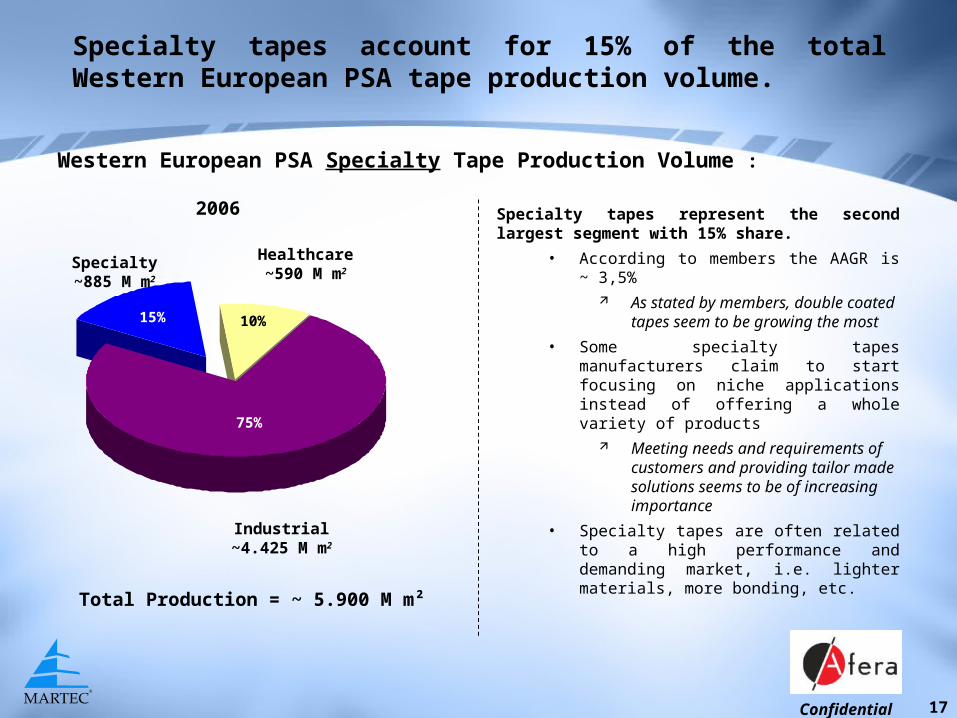

Specialty tapes account for 15% of the total Western European PSA tape production volume.

75%

15% 10%

Healthcare~590 M m2

Industrial~4.425 M m2

Specialty~885 M m2

2006

Total Production = ~ 5.900 M m²

Western European PSA Specialty Tape Production Volume :

Specialty tapes represent the second largest segment with 15% share.

• According to members the AAGR is ~ 3,5% As stated by members, double coated

tapes seem to be growing the most

• Some specialty tapes manufacturers claim to start focusing on niche applications instead of offering a whole variety of products

Meeting needs and requirements of customers and providing tailor made solutions seems to be of increasing importance

• Specialty tapes are often related to a high performance and demanding market, i.e. lighter materials, more bonding, etc.

18Confidential

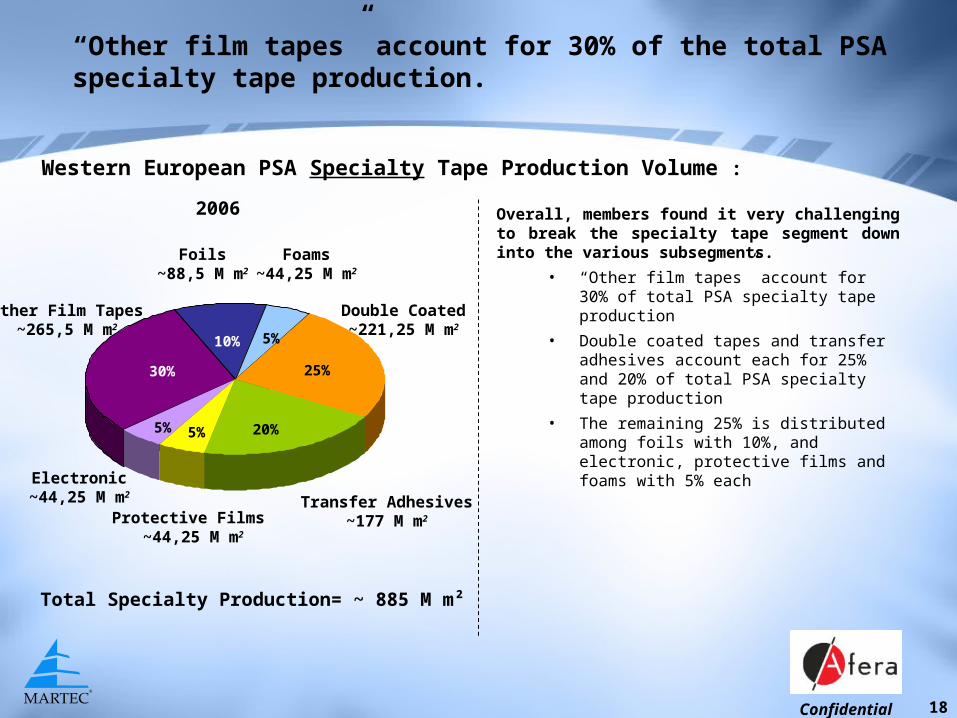

“Other film tapes” account for 30% of the total PSA specialty tape production.

5%10%

30% 25%

5% 20%5%

Foams~44,25 M m2

Transfer Adhesives~177 M m2

Other Film Tapes~265,5 M m2

2006

Total Specialty Production= ~ 885 M m²

Western European PSA Specialty Tape Production Volume :

Overall, members found it very challenging to break the specialty tape segment down into the various subsegments.

• “Other film tapes” account for 30% of total PSA specialty tape production

• Double coated tapes and transfer adhesives account each for 25% and 20% of total PSA specialty tape production

• The remaining 25% is distributed among foils with 10%, and electronic, protective films and foams with 5% each

Electronic~44,25 M m2

Double Coated~221,25 M m2

Foils~88,5 M m2

Protective Films ~44,25 M m2

19Confidential

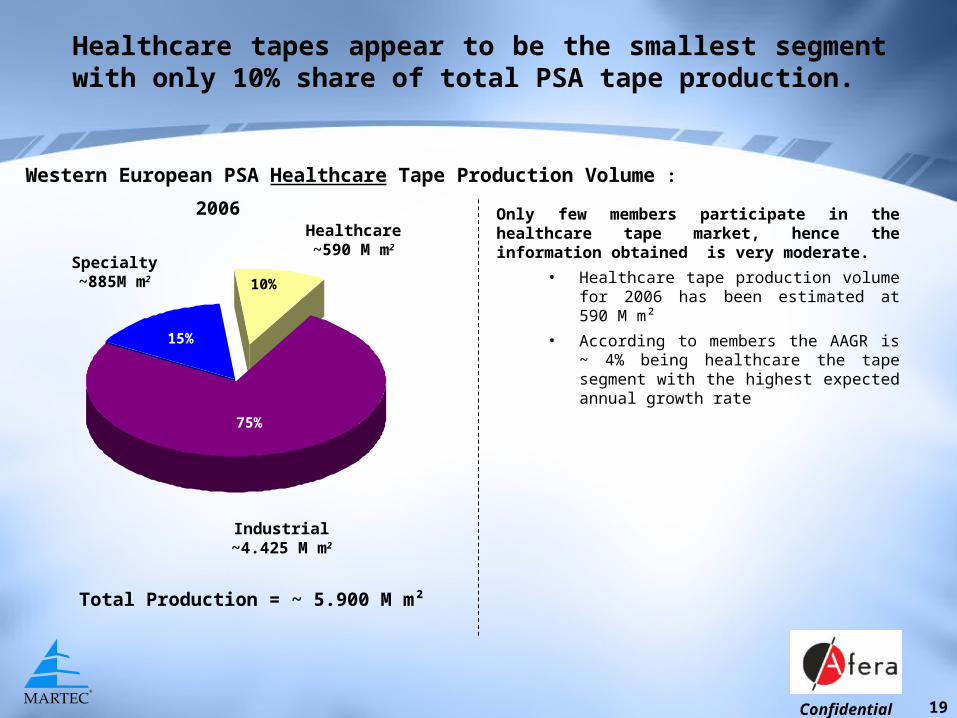

Healthcare tapes appear to be the smallest segment with only 10% share of total PSA tape production.

75%

15%

10%

Healthcare~590 M m2

Industrial~4.425 M m2

Specialty~885M m2

2006

Total Production = ~ 5.900 M m²

Western European PSA Healthcare Tape Production Volume :

Only few members participate in the healthcare tape market, hence the information obtained is very moderate.

• Healthcare tape production volume for 2006 has been estimated at 590 M m²

• According to members the AAGR is ~ 4% being healthcare the tape segment with the highest expected annual growth rate

20Confidential

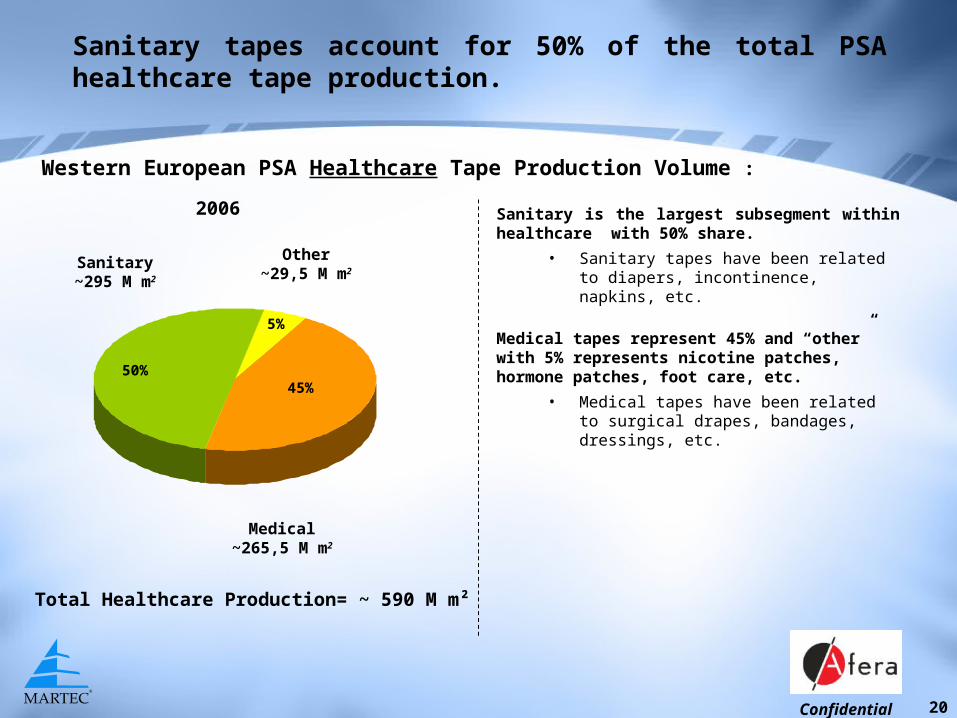

Sanitary tapes account for 50% of the total PSA healthcare tape production.

45%50%

5%

Other~29,5 M m2

Medical~265,5 M m2

Sanitary~295 M m2

2006

Total Healthcare Production= ~ 590 M m²

Western European PSA Healthcare Tape Production Volume :

Sanitary is the largest subsegment within healthcare with 50% share.

• Sanitary tapes have been related to diapers, incontinence, napkins, etc.

Medical tapes represent 45% and “other” with 5% represents nicotine patches, hormone patches, foot care, etc.

• Medical tapes have been related to surgical drapes, bandages, dressings, etc.

21Confidential

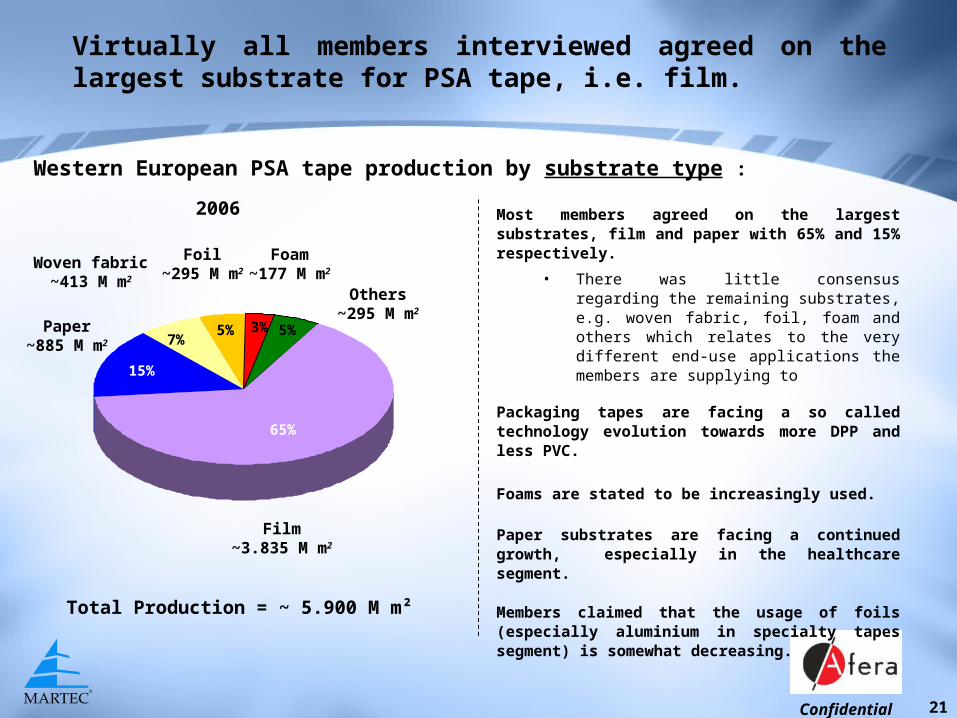

Virtually all members interviewed agreed on the largest substrate for PSA tape, i.e. film.

Western European PSA tape production by substrate type :

Most members agreed on the largest substrates, film and paper with 65% and 15% respectively.

• There was little consensus regarding the remaining substrates, e.g. woven fabric, foil, foam and others which relates to the very different end-use applications the members are supplying to

Packaging tapes are facing a so called technology evolution towards more DPP and less PVC.

Foams are stated to be increasingly used.

Paper substrates are facing a continued growth, especially in the healthcare segment.

Members claimed that the usage of foils (especially aluminium in specialty tapes segment) is somewhat decreasing.

2006

3% 5%

65%

5%

15%

7%

Total Production = ~ 5.900 M m²

Foam~177 M m2

Film~3.835 M m2

Paper~885 M m2

Others~295 M m2

Woven fabric~413 M m2

Foil~295 M m2

22Confidential

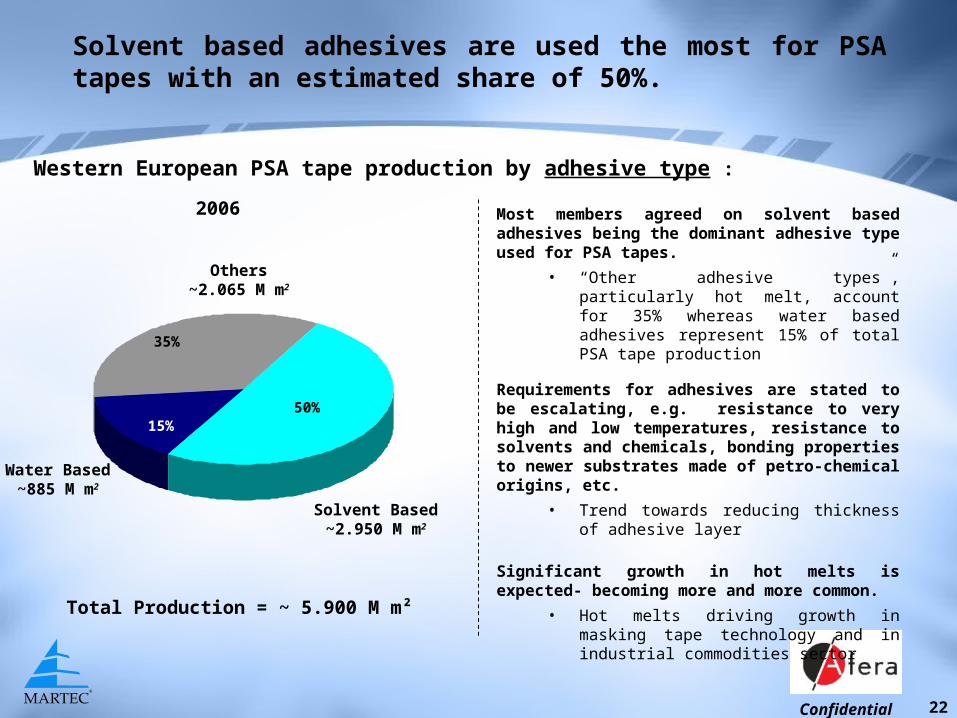

Solvent based adhesives are used the most for PSA tapes with an estimated share of 50%.

Western European PSA tape production by adhesive type :

Most members agreed on solvent based adhesives being the dominant adhesive type used for PSA tapes.

• “Other adhesive types”, particularly hot melt, account for 35% whereas water based adhesives represent 15% of total PSA tape production

Requirements for adhesives are stated to be escalating, e.g. resistance to very high and low temperatures, resistance to solvents and chemicals, bonding properties to newer substrates made of petro-chemical origins, etc.

• Trend towards reducing thickness of adhesive layer

Significant growth in hot melts is expected- becoming more and more common.

• Hot melts driving growth in masking tape technology and in industrial commodities sector

2006

50%15%

35%

Total Production = ~ 5.900 M m²

Others~2.065 M m2

Solvent Based~2.950 M m2

Water Based~885 M m2

23Confidential

Is there a threat coming from Asia/China and/or Eastern Europe?

• Virtually all members agreed on a threat coming from Asia with cheaper products Some companies claim that Asian tape manufacturers are starting to learn how to

produce cheap products with better quality Majority of threat though is expected to affect the industrial tapes segment , i.e.

packaging/ commodity tapes, not such a threat in the specialty tapes segment

• No member has commented on any threat coming from Eastern European companies

How does the REACH legislation affect the PSA tape industry?

• Respondents claimed that the REACH legislation is supposed to be in place, but it is not yet clear how it will affect the PSA tape manufacturers

The legislation is stated not to be structured enough yet and still in the process of many changes

• Many members commented that it will affect the raw material suppliers mostly, but if these do not comply with the legislation the tape manufactures might be forced to switch suppliers

Is e-commerce something that the PSA tape industry is considering to implement?

• While e-commerce options do not seem to be popular at present, most members expect that it will be slowly implemented in the future

Qualitative Questions.Qualitative Questions.

24Confidential

Is the compliance with current regulations, e.g. providing material safety data sheets for the automotive industry a challenge/problem for the industry?

• According to members interviewed, the Western Europe PSA tape industry is the most regulated in the world

This relates to more environmentally friendly products complying with stricter regulations but also higher prices and hence less competitiveness

– Some respondents are willing to take on this to maintain the reputation of European quality

Current regulations in Europe require that raw material suppliers (chemical suppliers) have to register their end-use applications, many smaller companies can not afford to register their products because it is stated to be very expensive

Qualitative Questions (cont’d).Qualitative Questions (cont’d).

25Confidential

Is the current re-positioning of several players within the industry (e.g. tape manufacturers going for vertical integration, converters going to private labelling, etc.) a positive or negative aspect?

• Overall, most respondents were not aware on any re-positioning of ‘industry players’ Being vertically integrated is seen as something that some companies just

naturally do, e.g. some tape manufacturers make their own adhesives, some tape manufactures sell to converters that put their private label on the converted product and also will sell unfinished converted product as well – this is seen as common practice by most respondents

• Some smaller tape manufacturers believe the dominance of some larger tape producers in the marketplace is excessive, hence the only way for them to sustain is via vertical integration /fusing with other players

Qualitative Questions (cont’d).Qualitative Questions (cont’d).

This concludes our presentation of findings.Thank you.

The Martec Group