Embed Size (px)

Citation preview

1 Keirns

Exchange Rate Stability and Economic Growth in Virtual Economies

Garrett Keirns

Department of Economics, Xavier University, Cincinnati, USA

May 2013

2 Keirns

Abstract

Empirical evidence suggests that exchange rate volatility has historically mitigated economic growth.

The goal of this paper is to confirm this hypothesis as well as apply it to the new virtual economy. Using

data gathered from previous studies I present the argument that the economic relationship that exists

between exchange rate volatility and economic growth in the “brick and mortar” economy is also

present in the virtual economy. I define the virtual economy as the sum of all financial transactions that

take place online. I then present the case of Bitcoin, a new virtual currency, and show how the

hypotheses proposed in the first stage of the paper are translating themselves into reality.

Keywords: Bitcoin, currency, cryptography, fiat, finance, risk, volatility

Contents

1. What factor does exchange rate stability play in economic growth? Does a

decrease in volatility increase productivity?

2. What is the virtual economy? How does capital flow through the internet?

3. What is Bitcoin? What is Bitcoin’s role in the virtual economy?

4. Can the insights gained from volatility research in traditional economies

be translated to the Bitcoin economy?

5. Beyond Bitcoin: The Future of Cryptographic Currencies.

6. Conclusion

3 Keirns

What factor does exchange rate stability play in economic growth? Does a

decrease in volatility increase productivity?

Empirical evidence suggests that exchange rate volatility has historically mitigated economic

growth. Volatility skews investors’ expectations of the future making it more profitable to have a “wait

and see” approach to developments of a market that they are trying to enter. For example, if investor A

wants to purchase a fixed income security in market X but is unable to hedge his exchange rate risk his

total return on his investment is unknown because he cannot accurately predict what the exchange rate

will be. Many institutional investors are bound to report their earning in a particular currency so

convertibility between currencies is important. The objective of a great deal of economic research is

quantifying what type of impact that the volatility of an exchange rate will have on an economy. This is

useful from a policy standpoint because governments and central banks can use this information to

formulate monetary policies that reduce volatility, such as adopting floating exchange rate regimes and

curbing inflation through currency repurchases.

Exchange rate volatility is usually measured as the average deviation from an average exchange

rate measured over a specific period of time. Thus, a currency that typically trades in a broad range from

its moving average is considered more volatile than a currency that trades in a narrow range. The cause

of this is market forces. Like any other tradable commodity, currency prices are an equilibrium of supply

(people trying to sell a currency) and demand (people trying to buy a currency). If buyers and sellers do

not have similar needs in a currency market then that market will be more volatile. Liquidity provided by

market makers makes markets less volatile because the market makers are willing to compromise with

buyers and sellers and take on additional exchange rate risk in return for the ability to make a profit in

the market when conditions (parity between buyers and sellers) improve.

As stated earlier, I draw upon previous empirical research to formulate my hypothesis that

decreasing exchange rate volatility will have a positive effect on an economy. I draw on real world

studies that look into the relationship of exchange rate volatility and foreign direct investment. Some of

the papers focus on the effects of exchange rate volatility in a specific country such as the work of

Amaghionyeodiwe (2009) and his study on the impact of foreign exchange rate volatility on foreign

direct investment in Nigeria. Other papers are broader in scope such as the paper published by the

European Central Bank in 2007 on exchange rate volatility and growth in small open economies at the

EMU periphery. In the case of the Nigerian economy, there was found to be a strong relationship

between the variability of the Naira (NGN) to major world currencies and the amount of FDI in the

country. The ECB paper also concluded that exchange rate stability is a sign of a healthy economy and

will therefore attract more outside investment which will further develop the economy. A paper

published by Aranyarat (2011) looks at the effect of foreign exchange rate volatility and foreign direct

investment in Thailand. The author found that volatility is statistically significant for machinery and

transportation, chemicals, food, and finance.

4 Keirns

What is the virtual economy? How does capital flow through the internet?

Just as money circulates in the traditional “brick and mortar” economy as bills, paper notes and

electronically, money flows through the internet creating a virtual economy. The virtual economy is the

sum of all financial transactions that take place online. For example, a purchase of clothes on eBay

would be considered a transaction that takes place in the virtual economy. The virtual economy is not

limited to just commerce. Players of online-video games often trade inside the game and settle debts on

the internet using real money. Remittance payments across borders that are settled entirely

electronically are also considered to be part of the virtual economy. Actually, any transaction that can

take place remotely and without either party having to physically meet the other person could be

considered to be counted in the virtual economy. The growth of the internet has stimulated the growth

of these types of transactions. Growth of the virtual economy over the past few years has been

exponential as a greater share of commerce has become electronic. Services such as PayPal,

Moneybookers, and Skrill allow users to transfer money over the internet using credit cards and bank

balances. Many banks now offer free instant inter-bank transfers to account holders. The whole

financial landscape is becoming much more high-tech allowing money to move much more quickly than

before.

Like the brick and mortar economy, capital moves through the virtual economy in predictable

flows. Consumers move money from banks or credit cards onto the internet to merchants who in turn

return that money back into the banking system to cover their costs of doing business. Some of that

money remains online to pay for virtual infrastructure such as web hosting costs and online advertising

costs. For video-gamers, money moves from offline to online in order to pay for virtual goods and is then

either returned to the brick and mortar economy or kept online. The same is true for remittance

payments, money that is obtained from doing work in the brick and mortar economy is brought online

and then sent to the receiving party usually being transferred offline again to be used to pay for living

expenses.

An interesting aspect of the virtual economy is that the electronic nature of transactions means

that more information about transactions is recorded and can be analyzed. In the brick and mortar

economy many transactions go unrecorded because of the use of cash or because people decide not to

record the transaction. Being electronic, the virtual economy captures more information than the brick

and mortar economy allowing a greater depth of information for dissecting and analyzing economic

phenomena such as capital flows.

What is Bitcoin? What is Bitcoin’s role in the virtual economy?

Bitcoin acts as a decentralized internet currency that facilitates online trade. Bitcoins are

“mined” meaning that a network of computers solves complex algorithms that process transactions on

the Bitcoin network in return for receiving new Bitcoins. These Bitcoins are created in a predictable

pattern thus mitigating inflationary concerns. There will only be 21,000,000 Bitcoins created. The

network regulates the number of Bitcoins created by changing the difficulty of the algorithms that are

required to receive new Bitcoins. This is called “network difficulty.” If there is a sudden influx of

5 Keirns

processing power on the network difficulty will increase thus maintaining the predictable mining of new

Bitcoins. Currently, as March 2013, there are 11 million Bitcoins in circulation. Bitcoins are mined in

“blocks.” When the complex algorithms of the block are solved the computer providing the processing

power receives a certain number of Bitcoins. Currently a mined block will yield 25 Bitcoins (BTC).

However, in the past that number was greater and in the future the number will shrink until all the

Bitcoins have been mined. At the point when all Bitcoins are mined, processing power on the network

will be compensated by paying out transaction fees. Below is a chart1 depicting the total number of

Bitcoins that will be in circulation. All 21 million Bitcoins will be mined by the year 2030; at that time

traditional Bitcoin mining will become obsolete and the network will switch to a fee-only infrastructure.

The creation of the Bitcoin is credited to a pseudonymous developer named Satoshi Nakamoto.

In a 2008 paper he describes his vision of a peer-to-peer, electronic payments system written in an

open-source code. The production of transfer is based on public-key encryption. Essentially, each Bitcoin

is assigned an encrypted code that can only be recognized by the central log that keeps track of each

transaction. This central log is known as the blockchain and is being constantly updated as new

transactions take place. A copy of the blockchain is archived and all transactions are recorded. Bitcoins

can be received using a Bitcoin wallet. A wallet is software that recognizes the encrypted keys and is

able to synchronize with the blockchain, thus confirming transactions that take place.

The value of a Bitcoin is determined by the free market. Many Bitcoins are traded on centralized

exchanges. Exchanges act as the intermediary between Bitcoins and fiat currencies such as US Dollars

1 Taken from www.bitcointalk.org

6 Keirns

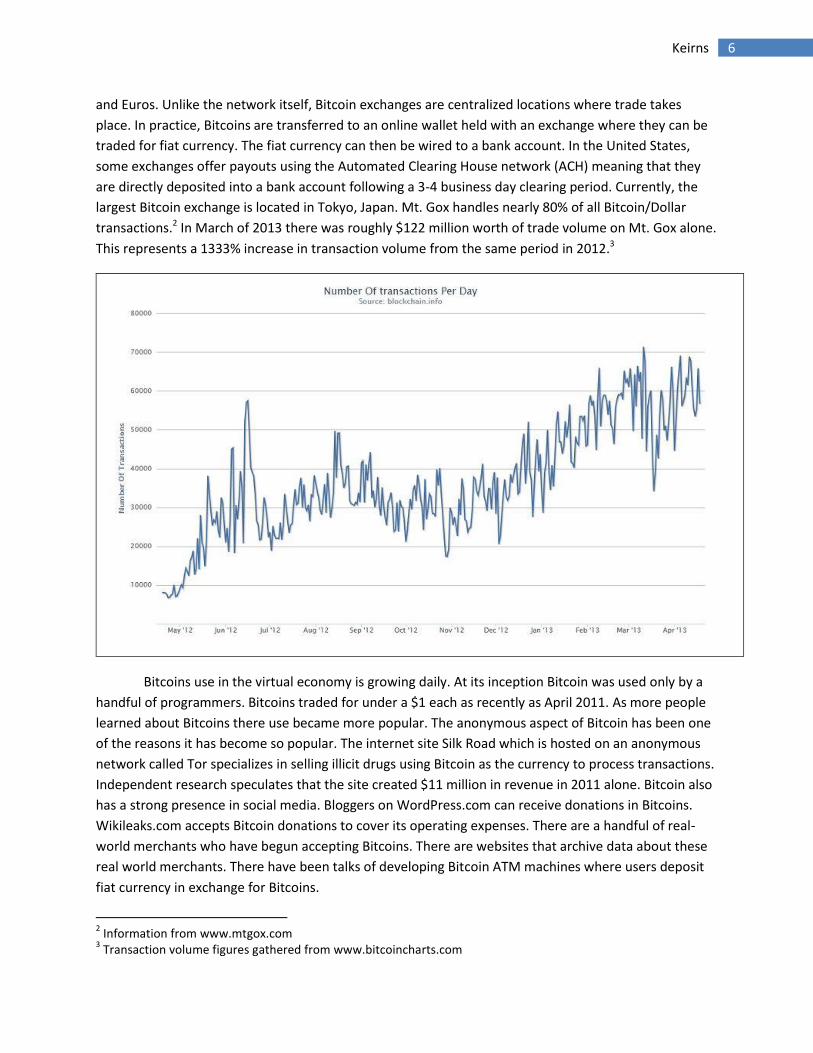

and Euros. Unlike the network itself, Bitcoin exchanges are centralized locations where trade takes

place. In practice, Bitcoins are transferred to an online wallet held with an exchange where they can be

traded for fiat currency. The fiat currency can then be wired to a bank account. In the United States,

some exchanges offer payouts using the Automated Clearing House network (ACH) meaning that they

are directly deposited into a bank account following a 3-4 business day clearing period. Currently, the

largest Bitcoin exchange is located in Tokyo, Japan. Mt. Gox handles nearly 80% of all Bitcoin/Dollar

transactions.2 In March of 2013 there was roughly $122 million worth of trade volume on Mt. Gox alone.

This represents a 1333% increase in transaction volume from the same period in 2012.3

Bitcoins use in the virtual economy is growing daily. At its inception Bitcoin was used only by a

handful of programmers. Bitcoins traded for under a $1 each as recently as April 2011. As more people

learned about Bitcoins there use became more popular. The anonymous aspect of Bitcoin has been one

of the reasons it has become so popular. The internet site Silk Road which is hosted on an anonymous

network called Tor specializes in selling illicit drugs using Bitcoin as the currency to process transactions.

Independent research speculates that the site created $11 million in revenue in 2011 alone. Bitcoin also

has a strong presence in social media. Bloggers on WordPress.com can receive donations in Bitcoins.

Wikileaks.com accepts Bitcoin donations to cover its operating expenses. There are a handful of real-

world merchants who have begun accepting Bitcoins. There are websites that archive data about these

real world merchants. There have been talks of developing Bitcoin ATM machines where users deposit

fiat currency in exchange for Bitcoins.

2 Information from www.mtgox.com

3 Transaction volume figures gathered from www.bitcoincharts.com

7 Keirns

Can the insights gained from volatility research in traditional economics be

translated to the Bitcoin economy?

Many of the empirical studies on exchange rate volatility point to the fact that excessive

volatility has the effect of decreasing economic growth. The excessive volatility has the effect of

decreasing FDI inflows which are necessary in helping small economies develop. I hypothesize that the

same is true for Bitcoin. Thus, excessive volatility of the Bitcoin exchange rate will have a negative

effect on the growth of the Bitcoin economy and will mitigate Bitcoin’s utility as a medium of

exchange. To further explain this we first need to understand the difference between Bitcoin and

traditional fiat currencies. We also need to understand the causes of exchange rate volatility. A fiat

currency is any currency created by a government. It usually gains its legal tender status from the fact

that it can be used to pay taxes. Fiat currencies do not have any other backing other than the faith and

credit of the issuing country. Many governments hand over the power to create and destroy fiat

currencies to a semi-independent central bank. The bank creates monetary policy and decides the

direction that the currency will take. Consumers and producers rely on traditional fiat currencies for

three things 1.) a unit of account, 2.) a store of value, and 3.) a medium of exchange. Sometimes,

however, a central bank caves into pressure from the government to pursue policies that satisfy short-

term desires instead of upholding the integrity of the currency for future generations. Mismanagement

of the currency supply skews investors’ expectations and usually leads to a devaluing of the currency in

the form of inflation. Less likely is a scenario when holders of a currency believe that a currency will

appreciate in value and therefore the incentive to hold the currency is greater than spending, this causes

deflation.

Volatility occurs in currency markets when central banks mismanage the money supply. This

causes a rational fear in investors who want to maintain the real value of their assets. Panic buying and

selling can occur after a central bank announces its intentions of the future value of a currency. The

excessive buying and selling cannot be matched with others who want to take on the same trades,

therefore creating a greater deviation from the normal trading price. This deviation is known as

volatility. In the developed world this is usually not a problem because central bankers have sufficient

independence from political pressures and are well educated in maintaining a façade of integrity in their

money supply. However, in smaller and more developing countries there is a pressure to cave in to

political pressures and overlook long term integrity in exchange for a short term fix. Furthermore, in

these less developed countries there is less economic diversification. This has the effect of amplifying

economic shocks.

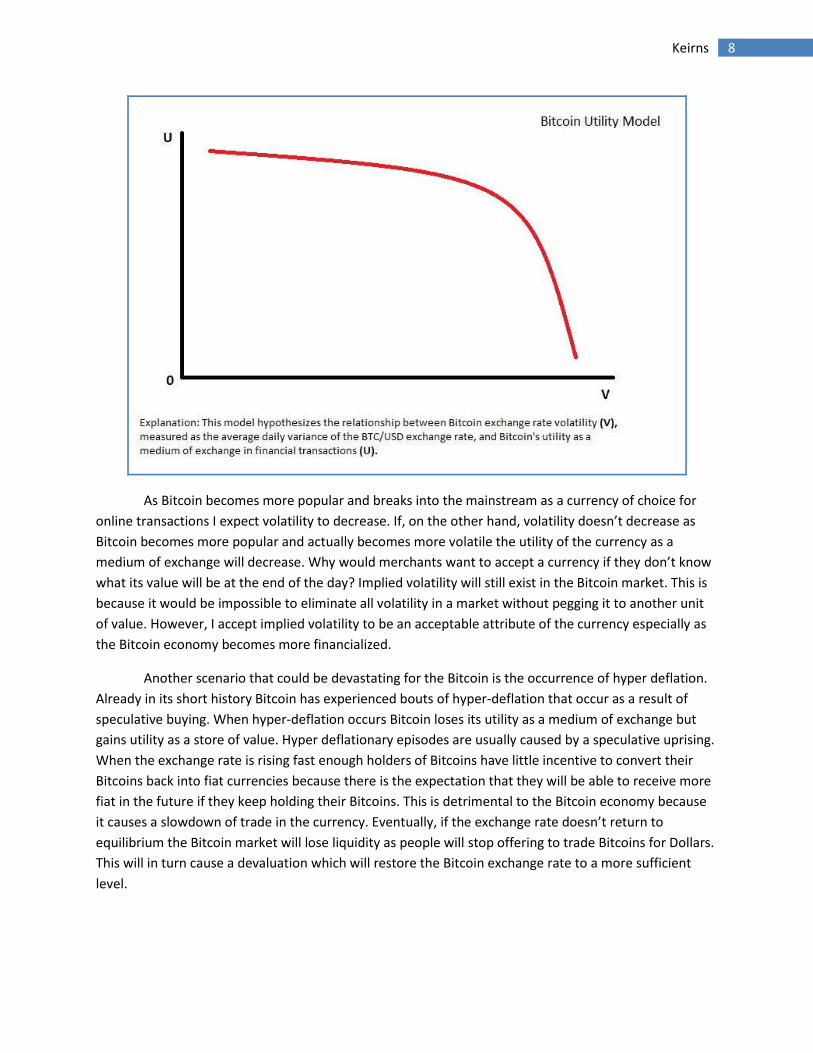

Bitcoin is similar to fiat currencies in that it can be used as a unit of account, store of value, and

medium of exchange. The utility of the Bitcoin is entirely dependent upon creating maintaining an

efficient market between Bitcoins and fiat currencies. An efficient market is one in which volatility is

contained in a narrow and predictable range. The model below explains this concept graphically:

8 Keirns

As Bitcoin becomes more popular and breaks into the mainstream as a currency of choice for

online transactions I expect volatility to decrease. If, on the other hand, volatility doesn’t decrease as

Bitcoin becomes more popular and actually becomes more volatile the utility of the currency as a

medium of exchange will decrease. Why would merchants want to accept a currency if they don’t know

what its value will be at the end of the day? Implied volatility will still exist in the Bitcoin market. This is

because it would be impossible to eliminate all volatility in a market without pegging it to another unit

of value. However, I accept implied volatility to be an acceptable attribute of the currency especially as

the Bitcoin economy becomes more financialized.

Another scenario that could be devastating for the Bitcoin is the occurrence of hyper deflation.

Already in its short history Bitcoin has experienced bouts of hyper-deflation that occur as a result of

speculative buying. When hyper-deflation occurs Bitcoin loses its utility as a medium of exchange but

gains utility as a store of value. Hyper deflationary episodes are usually caused by a speculative uprising.

When the exchange rate is rising fast enough holders of Bitcoins have little incentive to convert their

Bitcoins back into fiat currencies because there is the expectation that they will be able to receive more

fiat in the future if they keep holding their Bitcoins. This is detrimental to the Bitcoin economy because

it causes a slowdown of trade in the currency. Eventually, if the exchange rate doesn’t return to

equilibrium the Bitcoin market will lose liquidity as people will stop offering to trade Bitcoins for Dollars.

This will in turn cause a devaluation which will restore the Bitcoin exchange rate to a more sufficient

level.

9 Keirns

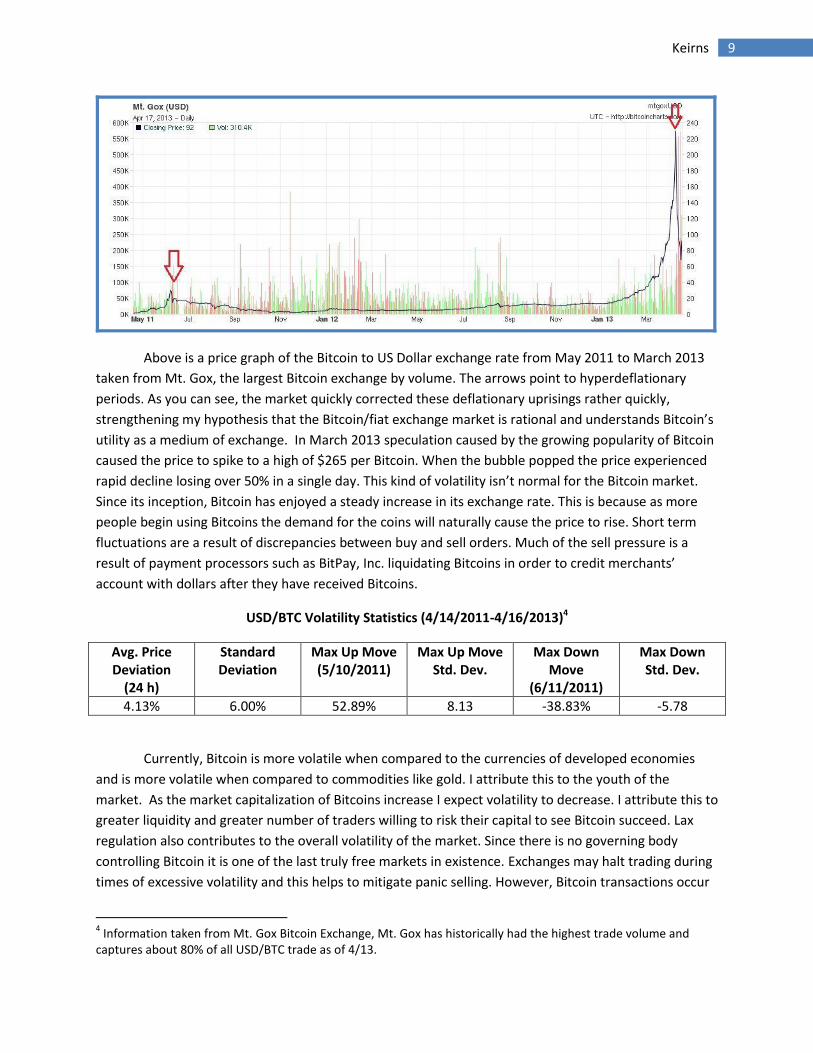

Above is a price graph of the Bitcoin to US Dollar exchange rate from May 2011 to March 2013

taken from Mt. Gox, the largest Bitcoin exchange by volume. The arrows point to hyperdeflationary

periods. As you can see, the market quickly corrected these deflationary uprisings rather quickly,

strengthening my hypothesis that the Bitcoin/fiat exchange market is rational and understands Bitcoin’s

utility as a medium of exchange. In March 2013 speculation caused by the growing popularity of Bitcoin

caused the price to spike to a high of $265 per Bitcoin. When the bubble popped the price experienced

rapid decline losing over 50% in a single day. This kind of volatility isn’t normal for the Bitcoin market.

Since its inception, Bitcoin has enjoyed a steady increase in its exchange rate. This is because as more

people begin using Bitcoins the demand for the coins will naturally cause the price to rise. Short term

fluctuations are a result of discrepancies between buy and sell orders. Much of the sell pressure is a

result of payment processors such as BitPay, Inc. liquidating Bitcoins in order to credit merchants’

account with dollars after they have received Bitcoins.

USD/BTC Volatility Statistics (4/14/2011-4/16/2013)4

Avg. Price Deviation

(24 h)

Standard Deviation

Max Up Move (5/10/2011)

Max Up Move Std. Dev.

Max Down Move

(6/11/2011)

Max Down Std. Dev.

4.13% 6.00% 52.89% 8.13 -38.83% -5.78

Currently, Bitcoin is more volatile when compared to the currencies of developed economies

and is more volatile when compared to commodities like gold. I attribute this to the youth of the

market. As the market capitalization of Bitcoins increase I expect volatility to decrease. I attribute this to

greater liquidity and greater number of traders willing to risk their capital to see Bitcoin succeed. Lax

regulation also contributes to the overall volatility of the market. Since there is no governing body

controlling Bitcoin it is one of the last truly free markets in existence. Exchanges may halt trading during

times of excessive volatility and this helps to mitigate panic selling. However, Bitcoin transactions occur

4 Information taken from Mt. Gox Bitcoin Exchange, Mt. Gox has historically had the highest trade volume and

captures about 80% of all USD/BTC trade as of 4/13.

10 Keirns

with relatively little government scrutiny. Going forward I believe that the financial landscape of the

Bitcoin economy will become increasingly sophisticated. Since one of the catalysts to mainstream

adoption will be a decrease in volatility, growth in the area of Bitcoin financial derivatives will help drive

larger volumes of trade onto the network. There already exist ways of hedging exchange rate risk such

as the MPex securities exchange5 and the ICBIT Bitcoin Exchange and Futures Market. Currently, these

markets are relatively illiquid and hedging positions is expensive because of the high volatility. However,

as the BTC/USD market becomes more mature these types of contracts will become invaluable for

merchants who want to enter the Bitcoin economy but previously haven’t been able to because they

cannot handle the exchange rate risk.

Beyond Bitcoin: The Future of Cryptographic Currencies.

Even if Bitcoin ultimately doesn’t succeed the lessons it has taught us about virtual

decentralized currencies will prove invaluable going forward. The Bitcoin model can easily be copied and

there are already competing virtual currencies such as LiteCoin6 and DevCoin7. One of the main factors

that has set Bitcoin apart from previous virtual currencies is that it relies on advanced cryptography. This

cryptography, once reserved only for highly advanced computers, was used by governments to transfer

internal wires with the objective of maintaining secrecy. With the advent of the internet and the

development of the micro-processor this once esoteric technology is becoming a household staple.

The applications of Bitcoin are numerous. Application developers have already created

numerous apps that integrate Bitcoins. It is now very easy to have Bitcoins loaded onto a smartphone.

The transactions that take place on smartphones utilize new Quick Response (QR) code technology. This

makes transacting money as simple as taking a picture of a pixelated box image. Transaction processing

costs using this technology are cheaper and quicker than traditional credit card networks such as Visa,

MasterCard, and Discover.

Bitcoin’s utility brings up serious questions about regulation in the realm of financial

transactions. Given Bitcoin’s anonymity aspects there is the possibility that Bitcoins can be used to

evade taxes and conduct other illegal activity. Many exchanges are required to adhere to strict Anti-

Money Laundering (AML) and Know Your Customer (KYC) guidelines to prevent the transfer of funds

derived from illegal activities. However, given the decentralized nature of a network operating in

multiple jurisdictions this poses considerable problems to governments worldwide trying to control the

flow of illegal funds. An interesting example of Bitcoin’s independence from governmental regulation

takes place in Argentina. As of March 2013, the government of Argentina has restricted the flow of US

Dollars into the economy in an effort to curb Argentine Peso (ARS) inflation. This has created a vibrant

underground market for the US Dollar which is still the currency of choice for the real estate market. The

5 MPex.co is a Bitcoin securities exchange run by Romanian mathematician Mircea Popescu. The site provides put

and call options on various USD/BTC strikes. 6 Litecoin.org

7 From Devcoin official site

11 Keirns

“Dolar Blue” is the price at which a US Dollar can be bought unregulated merchants in Argentina and the

exchange rate is considerably higher than official published figures. This has caused some Argentinians

seeking US Dollars to use Bitcoins. Argentinians will find traders willing to accept Pesos for Bitcoins and

will then trade Bitcoins for US Dollars, effectively bypassing the government’s efforts at currency

controls.

Governments that exercise excess control over citizens will have a hard time with Bitcoin. In

countries such as China and Iran Bitcoins are being used to purchase products from countries like the

United States. In the United States, there is the possibility that citizens can use Bitcoins to conduct

business with merchants in countries that the government has blacklisted. Potentially, if these types of

activities develop, Bitcoin could undermine trade agreements and economic pacts between nations. This

is what makes the legality of Bitcoin so unclear. In March 2013, FinCEN, a department of the United

States Treasury, released a statement outlining the steps that users of virtual currencies must take to

maintain compliance with the US government. Users who purchase virtual currencies to buy goods or

services are not required to file any paperwork with the government. However, individuals involved in

the selling of virtual currencies to others are required to file as a Money Service Business (MSB) with a

number of local authorities. With the registration is the understanding that individuals conducting this

type of business will comply with AML and KYC protocol.

The future of the virtual economy is bright with potential. In the future, Bitcoin may not be the

currency that defines the virtual economy but it will certainly go down as the catalyst that started the

revolution. The challenges that face Bitcoin are numerous. Governments will assert that they are the

only entities with the sovereign authority to maintain currencies and may try to illegalize Bitcoin and its

imitators. The traditional banking cartel will try hard to maintain its dominance and will work hard to

discourage integration between the banking system and Bitcoin. Given these circumstances, however, I

believe that virtual currencies will ultimately succeed because at their core they are beneficial to

promoting human trade and interaction.

12 Keirns

Bibliography

Academic Papers

Aranyarat, Chonnikarn. The Effect of Exchange Rate Volatility on Foreign Direct Investment and Portfolio

Flows to Thailand. Chulalongkorn University. N.p., n.d. Web.

Barber, Simon, Xavier Boyen, Elaine Shi, and Ersin Uzun. "Bitter to Better —How to Make Bitcoin a Better Currency." Palo Alto Research Center, University of California, Berkeley(2012).

Nakamoto, Satoshi. "Bitcoin: A Peer-to-Peer Electronic Cash System." (n.d.): n. pag. Web.

OSINUBI, Tokunbo S., and Lloyd A. AMAGHIONYEODIWE. "FOREIGN DIRECT INVESTMENT AND

EXCHANGE RATE VOLATILITY IN NIGERIA." International Journal of Applied Econometrics and

Quantitative Studies 6.2 (2009): n. pag. Web.

SCHNABL, GUNTHER. "EXCHANGE RATE VOLATILITY AND GROWTH IN EMERGING EUROPE AND EAST

ASIA." CESIFO WORKING PAPER NO. 2023 (2007): n. pag.

Vergil, Hasan. "Exchange Rate Volatility in Turkey and Its Effect on Trade Flows." Journal of Economic

and Social Research 4.1 (n.d.): 83-99.

Internet Sources

"Bitcoin." Wikipedia. Wikimedia Foundation, 05 May 2012. Web. 03 May 2012.

<http://en.wikipedia.org/wiki/Bitcoin>.

"Bitcoin Charts." Bitcoin Charts. N.p., n.d. Web. 24 Apr. 2013

"Bitcoin Forum - Index." Bitcoin Forum - Index. N.p., n.d. Web. 24 Apr. 2013.https://bitcoin.it/

"Home Most Recently Mined Blocks in the Bitcoin Block Chain." Bitcoin Block Explorer. N.p., n.d. Web. 24

Apr. 2013.

"Powerful." CampBX Bitcoin Trading Platform. N.p., n.d. Web. 24 Apr. 2013.

"Trade with Confidence on the World's Largest Bitcoin Exchange!" Mt.Gox. N.p., n.d. Web. 24 Apr. 2013.

13 Keirns

Donations Accepted: 1N8HpkUomTJrjdrZ6caRcazWgkJf51KBgN

![Final Paper - Plymouth State Universityjupiter.plymouth.edu/~megp/TAR Page/Final Paper[1].pdf · 2007. 6. 2. · Title: Final Paper Author: HP_Owner Subject: Final Paper Created Date:](https://img.pdfslide.us/doc/110x75/5ffae7a1f34bf038954031d4/final-paper-plymouth-state-megptar-pagefinal-paper1pdf-2007-6-2-title.jpg)

![Final Paper Group 2[1] 8 5](https://img.pdfslide.us/doc/110x75/55680330d8b42a242a8b493d/final-paper-group-21-8-5.jpg)