Embed Size (px)

Citation preview

VIRTUAL COACHING CLASSES ORGANISED BY BOS, ICAI

FINAL LEVEL

PAPER 1: FINANCIAL REPORTING

TOPIC: IND AS 20 ACCOUNTING FOR GOVERNMENT GRANTS & DISCLOSURE OF GOVERNMENT ASSISTANCE

Faculty: CA (Dr.) Alok K. Garg

© The Institute of Chartered Accountants of India

Date: 12 September 2021

12 September 2021 1

Agenda

Objective and Scope

Government Grants

Recognition and Accounting

Non Monetary Grants

Presentation

Repayment

Government Assistance

Key Differences

Disclosures

12 September 2021 © The Institute of Chartered Accountants of India 3

Objective

The objective of this Standard is to prescribe the accounting treatment for government grants and disclosures relating to government grants and other forms of government assistance.

Scope

■ Applicable to Govt grants and other form of Govt Assistance except:

This Standard does not apply to:

■ Income Tax related assistance e.g. Income Tax holidays

■ Biological Asset (Ind AS 41)

■ Government participation

■ Accounting of govt grant reflecting

the effect for changing prices

Definition – Govt & Govt Grants

Government: refers to

the Central Government,

State Government,

Government agencies

and similar bodies,

whether local, national or

international

Government grants are

assistance by government

in the form of transfers of

resources to an entity in

return for past or future

compliance with certain

conditions relating to the

operating activities of the

entity.

Government Grants exclude those govt assistance which can not have a value &

cannot distinguished from normal trading transactions.

Government Grants

Grants received from Govt against reimbursement of

expense/against expenses/fulfilment of certain conditions

Apply Ind AS 20

Examples of Government Grants

■ Subsidy given by the govt for procurement of material

■ Free allotment of Land by the government

■ Forgivable Loan is government grant when entity meets terms of forgiveness of loan.

■ Interest free loan or at concessional rate

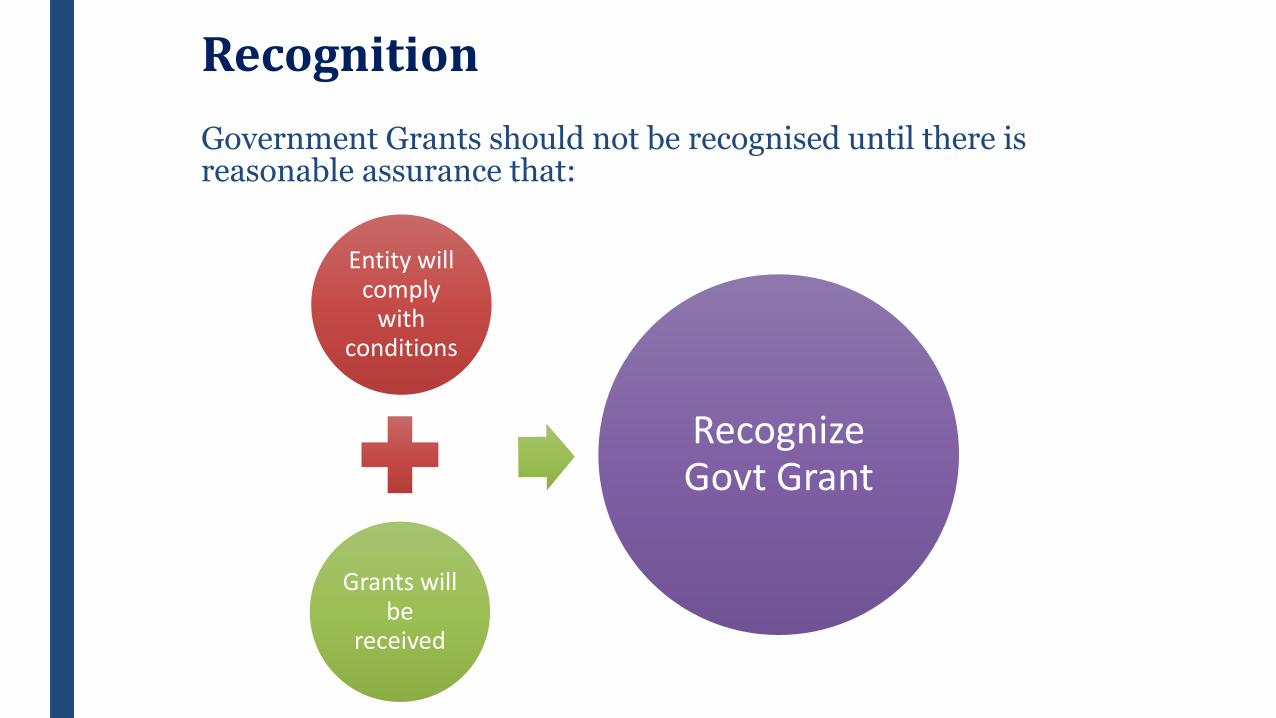

Government Grants should not be recognised until there is reasonable assurance that:

Recognition

Entity will

comply

with

conditions

Grants will

be

received

Recognize

Govt Grant

Recognised in Profit & Loss for the period in which expense for which grant received had been recognised on a systematic manner.

Related Contingent Liability or Contingent Asset is treated in accordance with Ind AS 37

Accounting

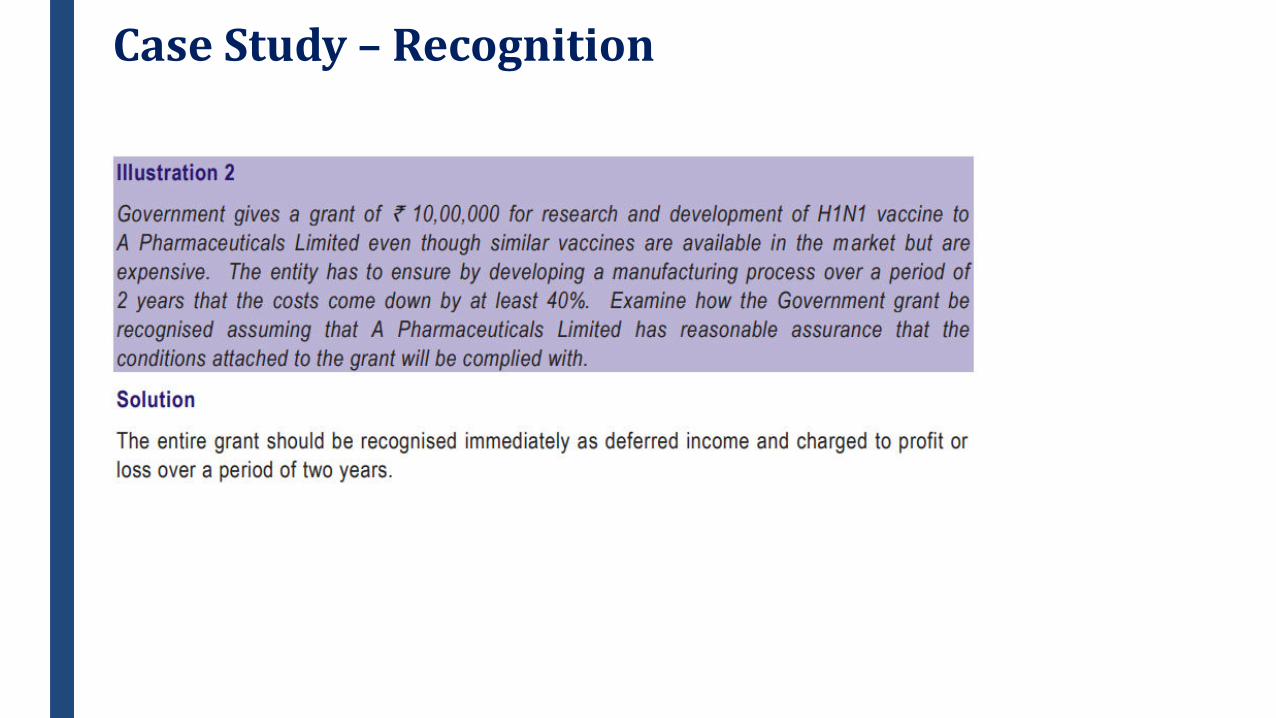

Case Study – Recognition

Case Study – Recognition

Case Study – Recognition

Non-Monetary Grant

Case Study – Grants related to Non-Monetary Assets

Presentation

Grants related to Assets

Either presented

in BS by setting

up grant as

“Deferred income”

Or, Deducted

from the carrying

value of the

asset

Grants related to Income

Either presented

separately as

“Other Income”

under P&L

Or, Deducted in

reporting the

related expense

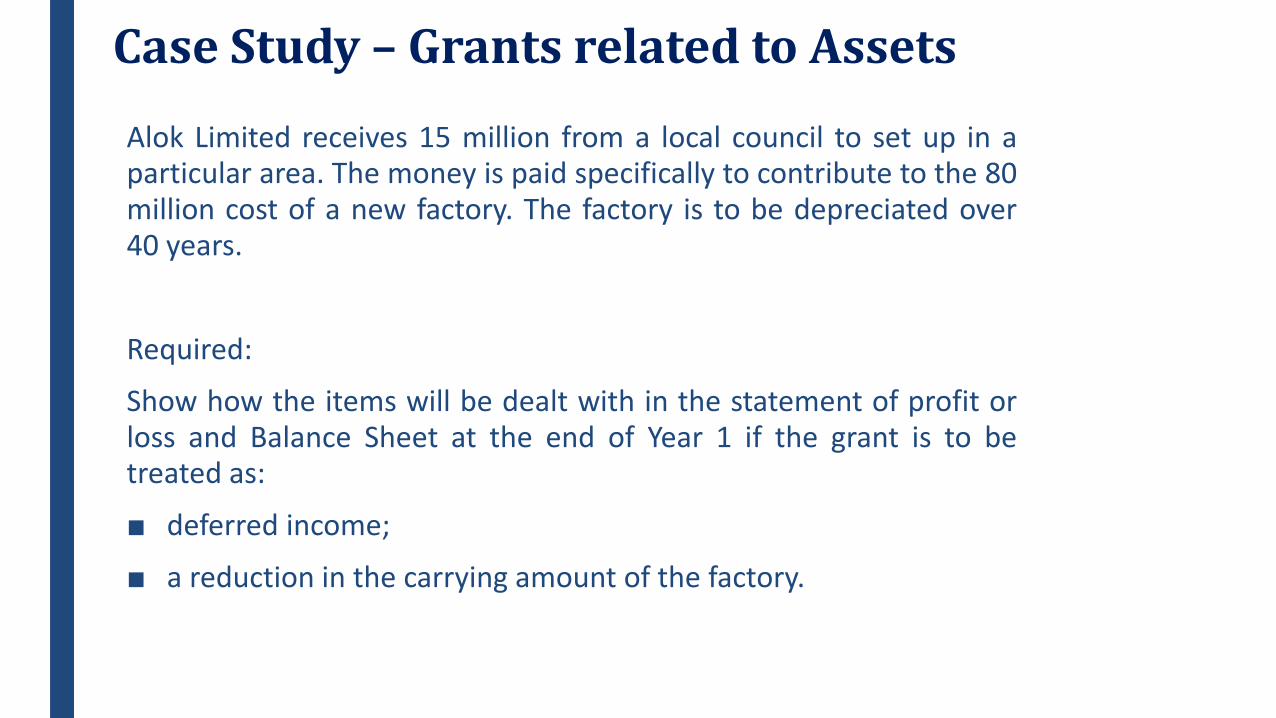

Case Study – Grants related to Assets

Alok Limited receives 15 million from a local council to set up in a

particular area. The money is paid specifically to contribute to the 80

million cost of a new factory. The factory is to be depreciated over

40 years.

Required:

Show how the items will be dealt with in the statement of profit or

loss and Balance Sheet at the end of Year 1 if the grant is to be

treated as:

■ deferred income;

■ a reduction in the carrying amount of the factory.

Solution – Grants related to Assets

(a) Deferred income Approach

Statement of profit or loss Rs’ 000

Depreciation of factory (2,000)

Government grant 375

Balance Sheet Rs’ 000

Tangible non-current assets

Property (80 million – 2 million) 78,000

Non-current liabilities:

Deferred income 14,250

Current liabilities:

Deferred income 375

Solution – Grants related to Assets

(b) Reduction in carrying amount

Statement of profit or loss Rs’ 000

Depreciation of factory

((80 million – 15 million) ÷ 40) (1,625)

Balance Sheet Rs’ 000

Tangible non-current assets

Property (65,000,000 – 1,625,000) 63,375

Case Study - Grants related to Income

The Govt of Haryana reimbursed the OPD expense of Kedanta

Hospital which is treating COVID patient amounting to Rs. 1 Crore

pertaining to FY 2019-20. Advise the treatment of such support from

the government.

Analysis:

Such amount is required to be recognized in P&L either as an Other

Income or it will be reduced from OPD expenses.

Case Study - Grants related to Income

Repayment of Government Grants

Accounted as change in Accounting Estimate

Grant Related to Income

- First, Against unamortised

deferred Credit

- Then, Balance to be

recognised immediately in P&L

Grants Related to Asset

Repayment of a grant related to

an asset shall be recognised by

increasing the carrying amount

of the asset or reducing the

deferred income balance by the

amount repayable, as the case

may be. The cumulative

additional depreciation that

would have been recognised in

P&L to date in the absence of

the grant shall be recognised

immediately in P&L.

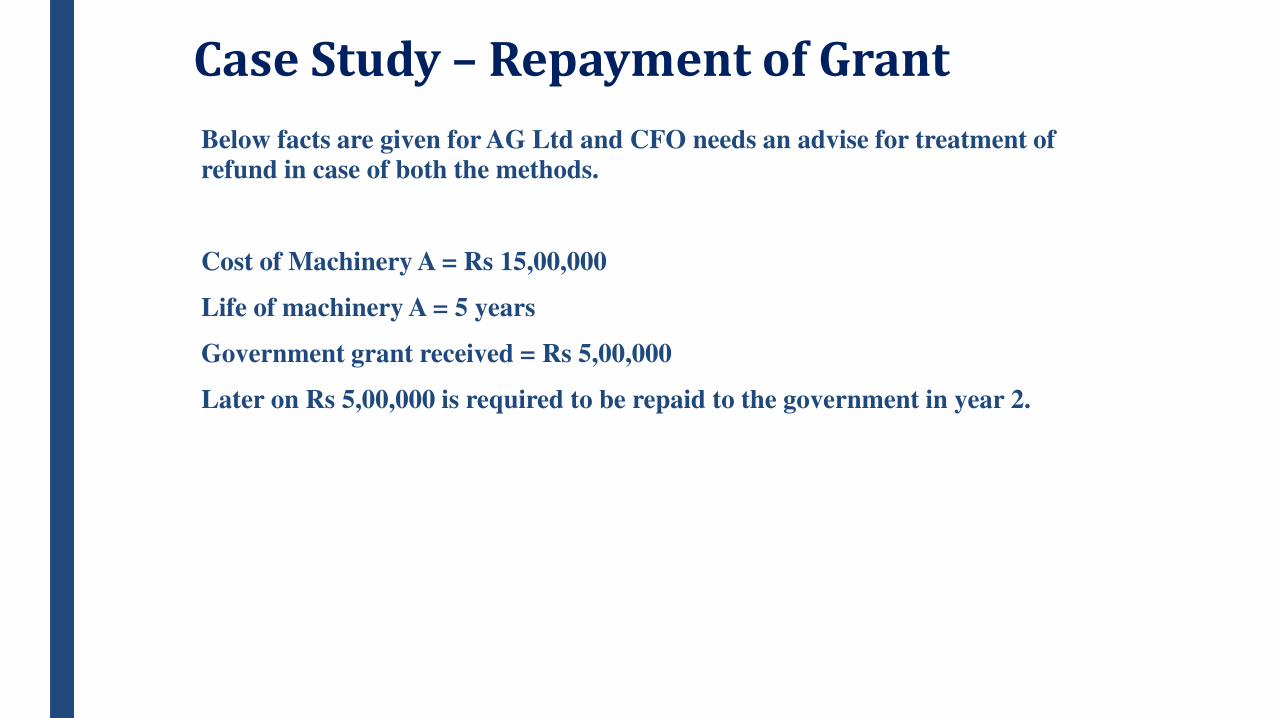

Case Study – Repayment of Grant

Below facts are given for AG Ltd and CFO needs an advise for treatment of

refund in case of both the methods.

Cost of Machinery A = Rs 15,00,000

Life of machinery A = 5 years

Government grant received = Rs 5,00,000

Later on Rs 5,00,000 is required to be repaid to the government in year 2.

Solution – Repayment of Grant

Method 1:

Cost of Machinery A= Rs 15,00,000

Deferred income = Rs 5,00,000

Depreciation charged in year 1 = 15,00,000 / 5 = Rs 3,00,000

Deferred income credited in P&L = Rs 5,00,000 / 5 = Rs 1,00,000

Balance of Machinery A at the end of year 1 = Rs 12,00,000

Deferred income balance at the end of year 1 = Rs 4,00,000

In year 2, Rs 5,00,000 is to be returned back to the government and accordingly, Rs 4,00,000

will be reduced from deferred income balance and Rs 1,00,000 will be debited in P&L.

Balance of Machinery A at the end of year 2 = 12,00,000 – 3,00,000 = Rs 9,00,000

Solution - Repayment of Grant

Method 2:

Cost of Machinery A = Rs 15,00,000 – Rs 5,00,000 = Rs 10,00,000

Closing balance at the end of year 1 = Rs 10,00,000 – Rs 2,00,000 = Rs 8,00,000

Since Rs 5,00,000 was paid back to the government, this amount will be added to the cost of

machinery.

Therefore, balance in Machinery A= 8,00,000 + 5,00,000 = 13,00,000

Depreciation p.a. in absence of government grant= 15,00,000 / 5 = Rs 3,00,000

Depreciation to be charged at the end of year 2

= (3,00,000 X 2) – 2,00,000 (already charged in year 1) = Rs 4,00,000

Carrying value of Machinery A at the end of Year 2 after all adjustments

= 13,00,000 – 4,00,000 = Rs 9,00,000

Loans from Government

Forgivable Loan

A forgivable loan from government, for which the government has undertaken to waive repayment under certain prescribed conditions, is treated as a government grant when there is reasonable assurance that the entity will meet the terms for forgiveness of the loan.

Loans from Government

Loan at a below-market rate of interest

The benefit of a government loan at a below-market rate of interest is treated as a government grant.

The loan shall be recognized and measured in accordance with Ind AS 109 Financial Instruments.

The benefit of the below-market rate of interest shall be measured as the difference between the initial carrying value of the loan determined in accordance with Ind AS 109 and the proceeds received.

Government Assistance

Assistance which cannot reasonably have a value placed on it. Transactions which cannot be distinguished from normal trading transactions. E.g. Government procurement policy resulting in a portion of the entity’s sales. Action by government designed to provide an economic benefit specific to an entity or range of entities qualifying under certain criteria. E.g. Technical or marketing advice, Government procurement. Disclosure if necessary so that the financial statements are not misleading.

Disclosure Requirements

Disclosures

Accounting policy for measurement and Presentation.

Nature and Extent of Grants recognised in FS.

Indications of Other Form of Government Assistance.

Unfulfilled Conditions & Other Contingencies attached to the amount recognised.

30

Comparison –Ind AS Vs AS

Particulars Ind AS 20 AS 12

Govt Assistance

Ind AS 20 also deals with Government assistance

However, AS 12 does not deal with such government assistance.

Non Monetary Assets

There is an option to value non monetary assets received as a government grant at fair value or nominal value.

Non-monetary assets, given at a concessional rate should be accounted for at their acquisition cost and if given free should be recorded at a nominal value.

Govt grants & promoter’s contribution

Credit to shareholder’s funds is prohibited

Certain government grants are like promoter’s contribution and hence must be credited to capital reserve, thereby treating it as a part of shareholder’s funds.

Forgivable Loans

The guidance for inclusion of forgivable loan as government grant is specified under Ind AS 20.

No such guidance

Loans at below market rates

Loans received from a government that have a below-market rate of interest should be recognized and measured in accordance with Ind AS 109

No such guidance

Key differences

32

Comparison –Ind AS Vs IFRS

There is no difference between Ind AS and

IFRS

12 September 2021 © The Institute of Chartered Accountants of India 34

THANK YOU

Presented by :

CA (Dr.) Alok Kumar Garg

CA, CS, Dip. IFRS (ACCA) UK, CIFRS (ICAI), B.Com (Hons.)