Embed Size (px)

Citation preview

The Big BOP-PER An Analysis of America’s Balance of Payments and Strategy for Political and Economic Realignment

A thesis submitted to the Center for Global Affairs at New York University in partial fulfillment of

the requirements for the degree of Master of Science in Global Affairs

By: Steven L. Avary Concentration: Private Sector

Thesis Advisor: Carolyn Kissane, Ph.D. New York, NY

Fall, 2014

Abstract: An opportunity has arisen that has the potential to reshape international relations and

global economics significantly. The key driver for this opportunity is the resurgence of the

American Energy Industry. This analysis argues that with changes to three key areas: foreign

policy as executed by the Executive Branch, rescinding mandates and more prudent fiscal

policies alleviating market distortions in the energy sector by the Legislative Branch and

promoting bills that facilitates energy sector growth, and illuminating a narrative and modifying

Central Bank interest rate policy as it relates to energy price inflation, should provide wide

spread benefits to the U.S. Implications are incorporated into Game Theoretic permutations,

with anticipated outcomes for America of greater leverage globally, resulting in reduced

commitment of blood and treasure to hazardous regions, risk mitigation, a reduction in its twin

deficits -- trade and budget, and enhancements in its energy and transportation infrastructure,

while also enhancing America’s aggregate economic base.

1

Table of Contents

INTRODUCTION ............................................................................................................................................. 3

AGNOSTICS AND EVANGELISTS ................................................................................................................... 10

EXTERNALITIES ........................................................................................................................................ 10

LEVELIZED COST OF ENERGY ................................................................................................................... 12

TRADEOFFS ............................................................................................................................................. 13

POLICY SHIFTS ............................................................................................................................................. 15

EXECUTIVE BRANCH ................................................................................................................................ 15

International Relations Theory ........................................................................................................... 16

Hegemonic Stability Theory ............................................................................................................ 16

Realists ............................................................................................................................................ 17

Liberals ............................................................................................................................................ 18

Central Limit Theorem .................................................................................................................... 20

LEGISLATIVE BRANCH .............................................................................................................................. 21

Fiscal .................................................................................................................................................... 21

Expenditures ................................................................................................................................... 24

Reallocation ................................................................................................................................ 27

Taxes ............................................................................................................................................... 29

Carbon ......................................................................................................................................... 29

Cap & Trade................................................................................................................................. 29

Renewable Externality ................................................................................................................ 30

Tax credits and DD&A ................................................................................................................. 31

LIFO ............................................................................................................................................. 32

Legislation ........................................................................................................................................... 34

Law .................................................................................................................................................. 34

Energy Policy and Conservation Act of 1975 .............................................................................. 34

Energy Policy Act of 2005 ............................................................................................................ 35

Energy Independence and Security Act of 2007 ......................................................................... 36

2

Bills .................................................................................................................................................. 37

North American Energy Infrastructure Act ................................................................................. 37

Keystone XL ................................................................................................................................. 38

North Atlantic Energy Security Act ............................................................................................. 39

CENTRAL BANK ........................................................................................................................................ 40

Picturesque ......................................................................................................................................... 42

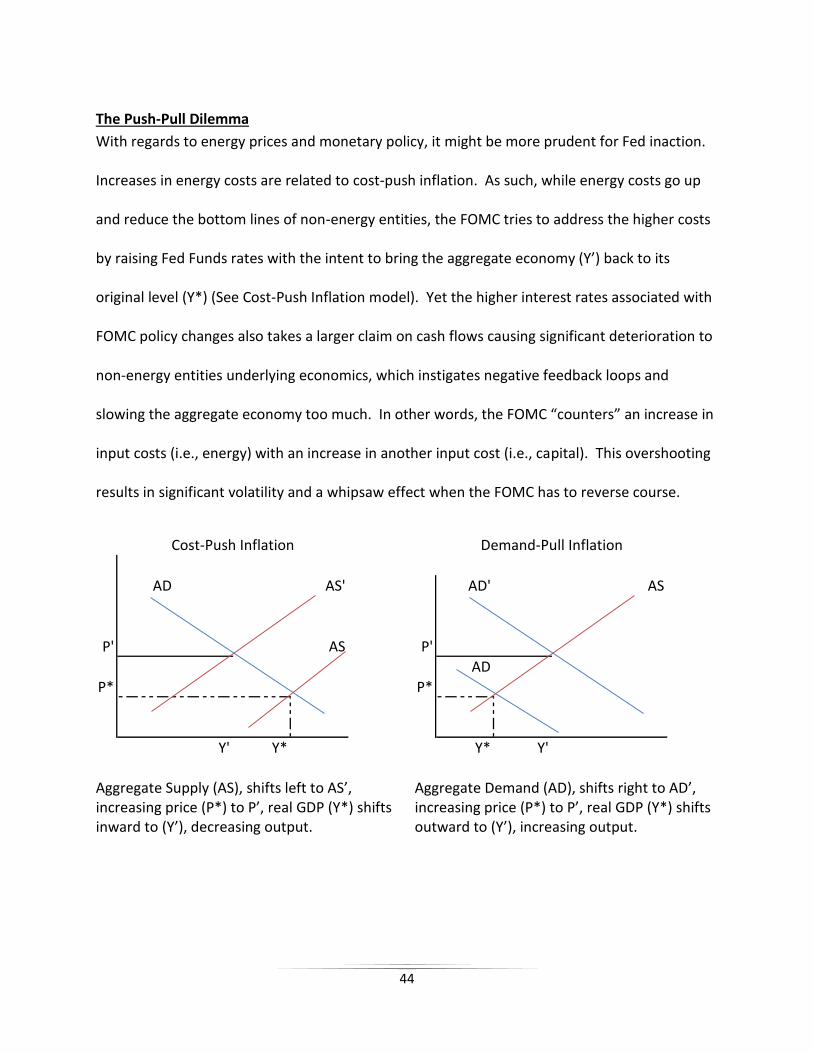

The Push-Pull Dilemma ....................................................................................................................... 44

Secrets of the Temple ......................................................................................................................... 45

Minute Minutiae ................................................................................................................................. 46

Of The Core, and The Core, and The Core ...................................................................................... 46

Collide-a-scope ................................................................................................................................ 47

50 shades of grey ............................................................................................................................ 48

ECONOMIC FUNDAMENTALS ...................................................................................................................... 49

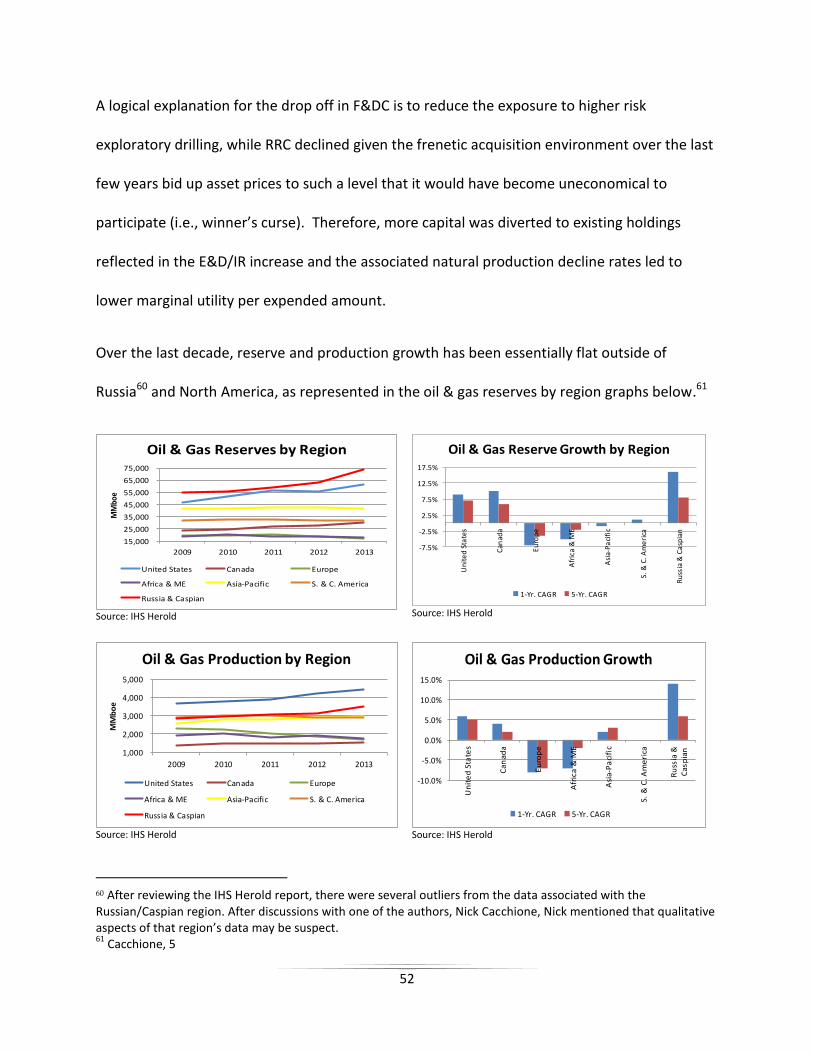

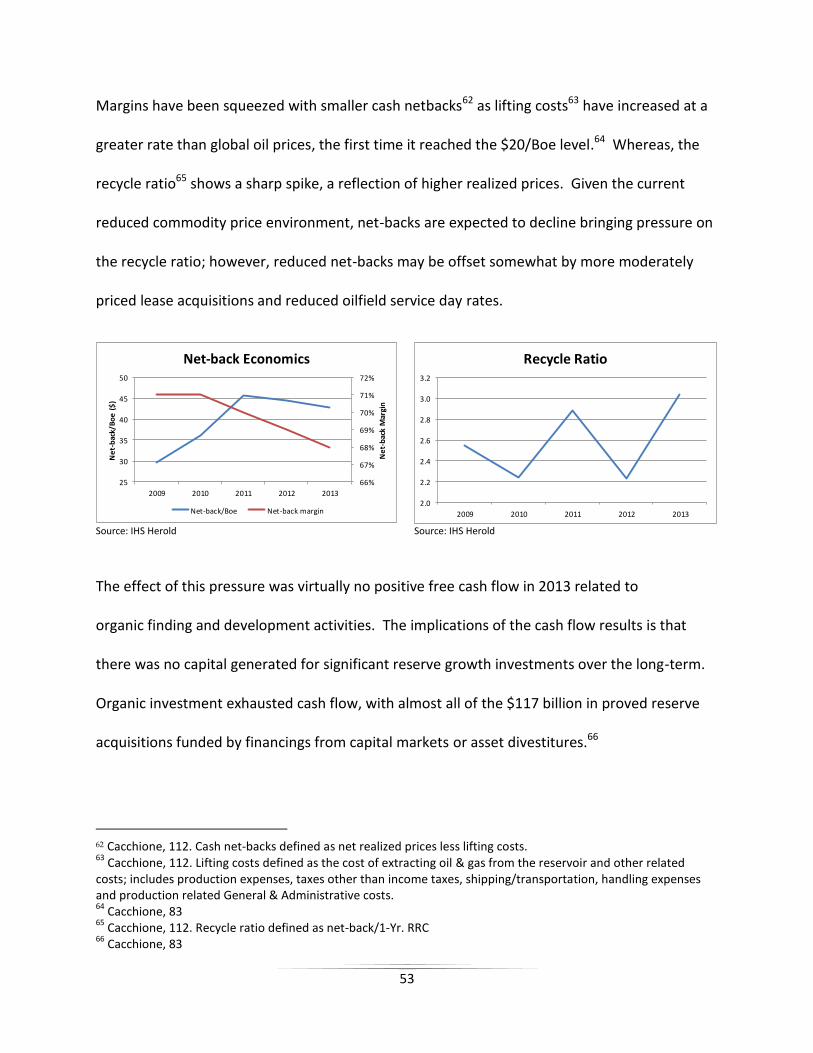

TIME SERIES ANALYSIS ............................................................................................................................ 51

CAPITAL DISCIPLINE ................................................................................................................................ 55

PRICES ..................................................................................................................................................... 56

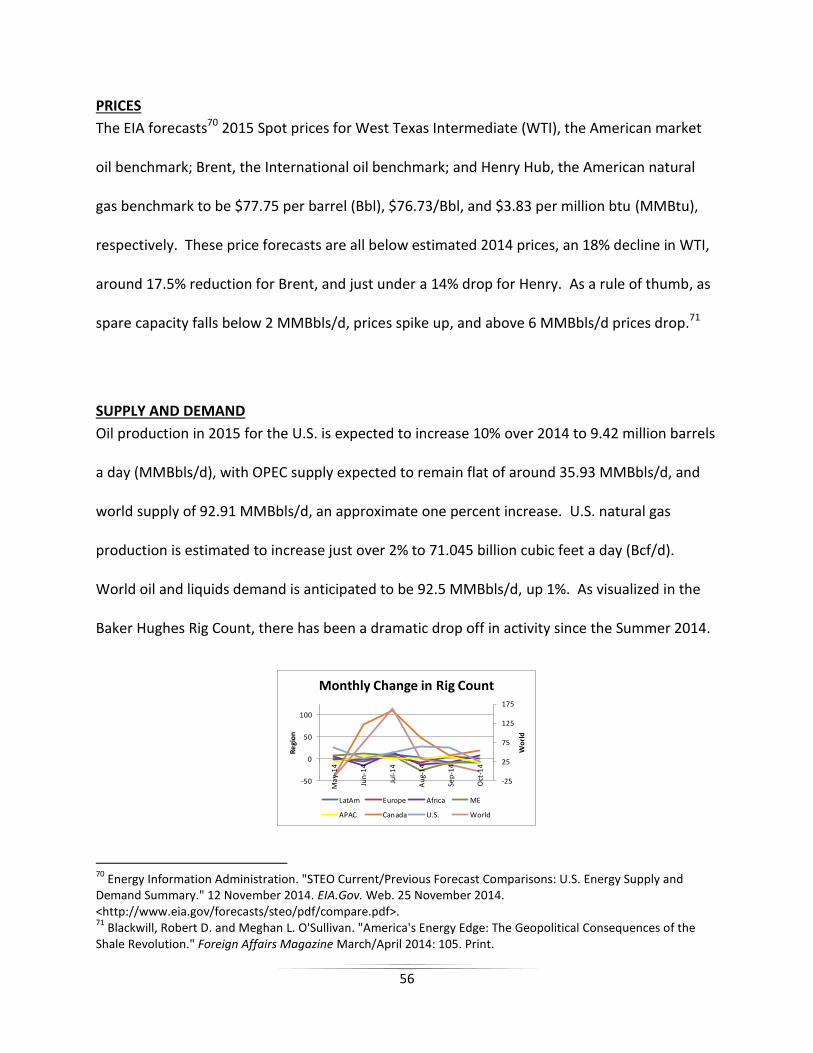

SUPPLY AND DEMAND ............................................................................................................................ 56

IMPLICATIONS ............................................................................................................................................. 57

FISCAL PHYSICAL ..................................................................................................................................... 58

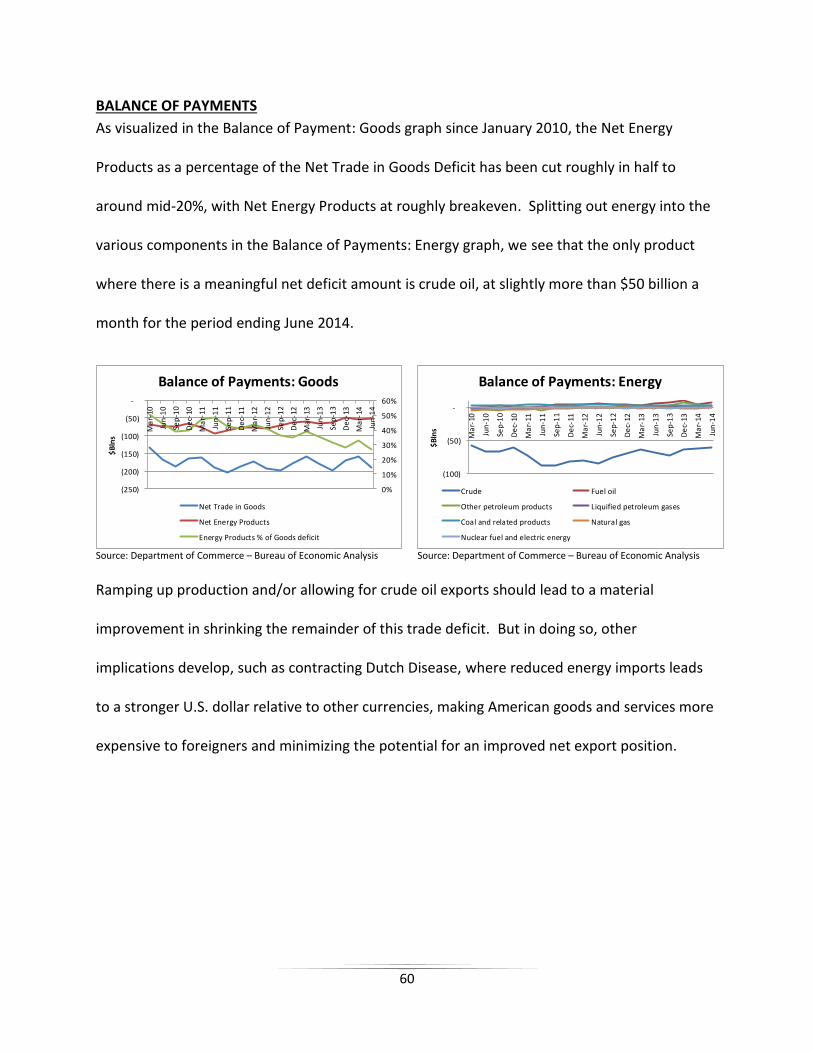

BALANCE OF PAYMENTS ......................................................................................................................... 60

CENTRAL BANK ........................................................................................................................................ 61

Taylor Made ........................................................................................................................................ 61

Deriving the Derivative ....................................................................................................................... 61

GAME THEORY ........................................................................................................................................ 62

Players ................................................................................................................................................. 62

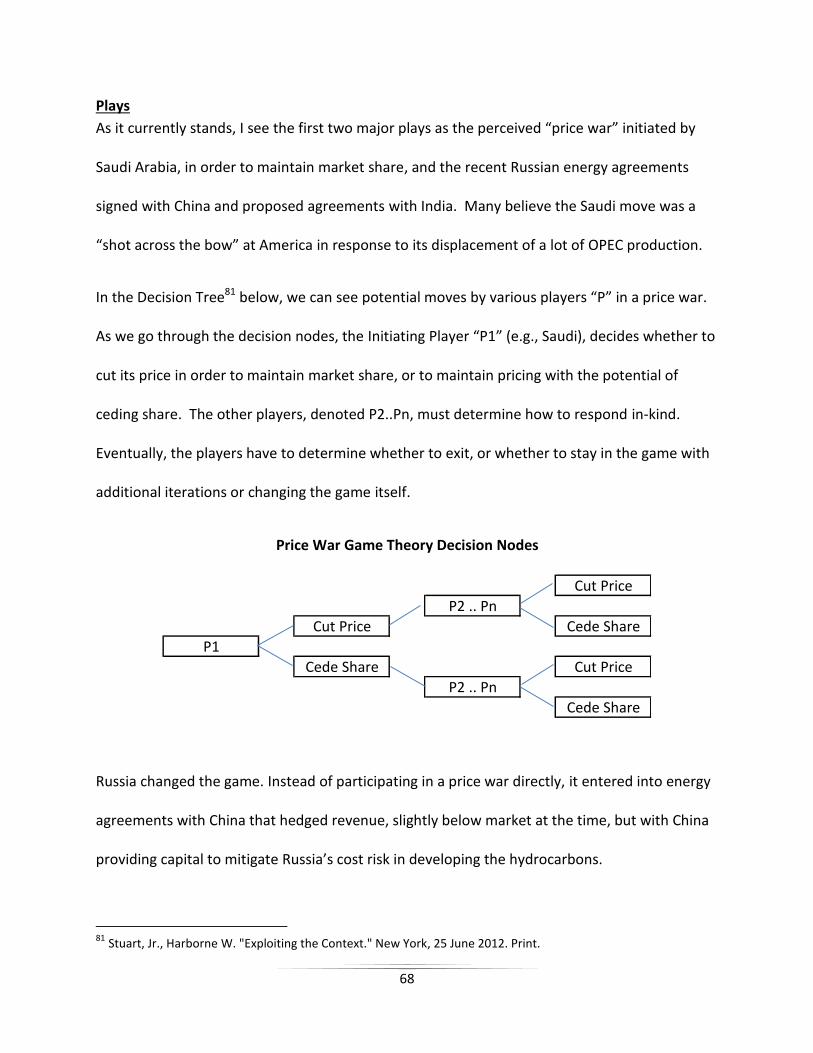

Plays .................................................................................................................................................... 68

Payoffs ................................................................................................................................................. 71

CONCLUSION ............................................................................................................................................... 73

BIBLIOGRAPHY ............................................................................................................................................ 75

ACKNOWLEDGMENTS ................................................................................................................................. 81

3

INTRODUCTION

Politics is what drives the process in the establishment of policy parameters and culminates in

economic outcomes. Yet, due to various special interests, personal agendas, or

misunderstanding of cause and effect of market dynamics, both government and central bank

policies are interjected into the energy sector that distorts the market away from the optimal

position, its natural equilibrium; thus, leading to unintended consequences and suboptimal

outcomes. While American energy policy is often advertised as comprehensive in nature or

taking an “Agnostic” position showing no preferential treatment, in reality it is driven by

“Evangelists,” individuals that promote one form of energy over the other and subordinate

other forms in the belief they have the one true gospel. Given its innate attributes, proponents

of the competing energy sources need to be sensitive to stakeholders’ concerns and take a

more holistic perspective that of striking a proper balance with the triple bottom line of people,

planet and profit.

Much of the focus over the last decade has been greater government support for alternative

energy sources. In certain cases, some of these energy sources do not have strong enough

economic fundamentals currently without government intervention. An argument can be

made to provide government support to infant industries while they are getting established.

However, much of the industries supported by the government, such as solar and wind power,

has been around for many years. As such, the self-sufficiency of such sources over the long-

term comes into question. If so, I make the claim that it is inappropriate to continue

4

government support in its current form, and limited resources should be released and

reallocated for more viable projects.

The objective of this paper is to argue that with a more accommodative policy for the domestic

energy sector, that there may be an improvement in the United States’ Balance of Payment

(BOP) position, and more productive and beneficial political and economic relationships

through realignment (PER). Greater accommodation refers to reducing or eliminating

encumbrances (e.g., mandates) and market frictions (e.g., subsidies) imposed by the federal

government. It also means that Central Bank (i.e., the Federal Reserve (Fed)) policy will be

appropriate with respect to addressing energy price inflation pressures. Political and economic

relationships need reassessment and a more robust foreign policy posture should be taken by

incorporating certain tenets of the main schools of international relations theory, Realists and

Liberals, without strict adherence to a specific philosophy. Indeed, I provide my own personal

philosophy, the Central Limit Theorem, a hybrid approach. In essence, much of my argument is

to allow for more optionality into the system, which provides more flexibility to maneuver as

the situation dictates rather than to be constrained by a silo oriented mentality.

I preface my comments that this thesis will be examined from the perspective of the

advancement of America’s position of the interrelated areas of international relations and

economics. I believe the United States should seize this opportunity through leveraging its

energy assets via revisiting its energy policies, with government remaining Agnostic amongst

5

the various energy sources. I will accede at first glance it might appear that I am an Evangelist

for hydrocarbon-based sources. I am a proponent of American Energy in all its forms. With this

understanding, the majority of the focus will be on hydrocarbon sources as a function of my

greater familiarity with the source, its predominance in the marketplace, and its ability for

greater scalability over a shorter timeframe. In addition, there are greater gaps in technology

necessary to make other forms more economically viable at this time, although there have

been tremendous strides over the last few years (See Levelized Cost of Energy). The greater

focus on hydrocarbons initially is given its “lower hanging fruit” position and in general more

competitive cost structure that is to be complemented by alternative energy sources. In

aggregate, I am encouraging rapid expansion of an “All the Above” energy policy within the

context of a holistic cost/benefit and strategic perspective.

I begin the analysis by introducing the ideological personalities that drive the energy debate,

Evangelists, and layout a key area, Externalities, which are major drivers in supporting an

energy source over another. Then I introduce a metric, Levelized Cost of Energy (LCOE), which

helps provide an assessment of energy sources. Finally, I incorporate into the discussion a

resolution to the differences by suggesting a holistic approach, that it comes down to a series of

Tradeoffs.

Next, I transition to highlighting certain Policy Shifts recommended for the Executive Branch,

the Legislative Branch, and the Central Bank. For the Executive Branch, I suggest in making

6

changes to foreign policy with adoption of more clear guidelines using templates from

international relations theory, Hegemonic Stability Theory, the Realist and Liberal schools, and

my personal default position, the Central Limit Theorem. Other than commodity price risk,

geopolitical issues are arguably the most prominent risk of energy, the most consequential

industry across the globe, and it is essential that the proper approach is implemented in

navigating the obstacles.

In general, I recommend that the policy shifts from the political branches, the Executive and

Legislative, rescind policies I believe are detrimental, and facilitate various bills or other policy

instruments that encourage growth. The prudence of a diverse energy strategy is best captured

by Winston Churchill in a speech to Parliament, “On no one quality, on no one process, on no

one country, on no one route, and no one field must we be dependent. Safety and certainty in

oil lie in variety and variety alone.” Critical to America’s energy security is to follow such a

strategy, updated to include an All the Above approach to energy sources and technology,

within resource constraints and parameters aforementioned, that should be maximized.

I then turn to the other political entity, the Legislative Branch. I argue for changes in Fiscal

Policy and Legislation. I suggest the American people and economy would be better served by

eliminating distortions the Legislature causes in the market by misallocating resources, by

allowing taxpayer money to be made in investments in general, and to favored energy sources

specifically. Furthermore, I discuss distortions and shortcomings of Taxes dealing with

7

externalities. Other tax issues include policy changes proposed by the Obama Administration

that would result in an undue burden on hydrocarbon sources while supporting renewables in

the Tax Credits and DD&A, and LIFO sections, and propose a solution to the LIFO debate. In the

Legislation section, I highlight existing laws, the Energy Policy and Conservation Act of 1975, the

Energy Policy Act of 2005, and the Energy Independence and Security Act of 2007. In these

laws, I mention rescinding mandates (e.g., ethanol) and economic distortions (e.g., subsidies).

Recent Bills are also addressed that promote energy and economic growth and closer strategic

positions with our allies, which are included in the North American Energy Infrastructure,

Keystone XL, and Energy Security Acts.

For the Central Bank, I make the case that the Fed does not adhere to its stated position of

“core inflation” as the triggering mechanism for changes in interest rates to address inflationary

pressures. I provide empirical research to support my argument that the Fed’s interest rate

policy is flawed, and recommend policy shifts. These recommendations are based on changing

perceptions about monetary policy actions associated with energy prices with the objective of

mitigating volatile swings between perceived inflationary pressures and economic contractions

over the long-term, which provides the Fed with greater flexibility in balancing its dual mandate

of price stability (inflation management) and maximum employment. Empirical analysis

includes visualizing the influence of energy prices on rate moves and the effects over a time

series included in the Picturesque section. This lack of comprehension, and not allowing the

market to adjust naturally to a new equilibrium, has led to dire outcomes. Fed intervention is

8

not a solution to the problem; rather it introduces another problem into the system, causing

the unintended consequence of significant volatility and economic deterioration, only to have

to reverse the decision later to counter effects of prior rate moves.

The Push-Pull Dilemma describes the problem with assuming all forms of inflation are equal.

Secrets of the Temple, the Temple being a nickname for the Fed, describe discussions I had with

a Fed economist as it relates to my inflation differential arguments and its effects. To support

my claims, I reviewed meeting minutes of the Federal Open Market Committee (FOMC), the

group within the Fed that makes interest rate policy decisions. My findings are included in the

Minute Minutiae subsection, and focus on three key points that they made interest rate

increases as implemented with changes in the Fed Funds rate, despite the following: various

core inflation metrics were relatively stable; that the increases were made even while

acknowledging the impact that higher energy prices were having on the overall economy; and,

even though the risks between price stability and maximum employment were deemed in

balance. These subjects are addressed in of The Core, and The Core, and The Core; Collide-a-

scope; and, 50 shades of grey, respectively.

In order for the U.S. to capitalize on its energy assets to further its position, it is necessary to be

cognizant of its feasibility based on what is underpinning such a policy. This viability is

addressed in the Economic Fundamentals section, discussing such drivers as economic growth,

supply and demand, and the expected pricing environment. I provide a significant amount of

9

data in the Time Series section mentioning capital investment, and asset and production

growth, with additional granularity provided on per unit operating economic statistics.

In the Implications section, I describe how all the aforementioned items translate to its fiscal

health in Fiscal Physical. America’s Energy Renaissance has contributed greatly in international

trade, reducing its reliance on energy imports as reflecting in its Balance of Payments.

Eliminating mandates prohibiting export of energy products, specifically that of crude oil, and

facilitating growth in the Liquid Natural Gas (LNG) market through expedited permitting and

enabling exports, should further reduce the trade deficit. The Fed effect is spelled out in Taylor

Made, a modified application of the Taylor Rule, a tool often used as a benchmark to set rates.

In Deriving the Derivative, I explain the impact between an absolute and relative rate of change.

Game Theory incorporates potential Plays and Payoffs of key Players in response to actions

taken by others in the pursuit of maximizing their own positions. I discuss certain key issues in

order to compete with Australia, Brazil, Canada, Mexico, members of OPEC and Russia.

Throughout, I intersperse the commentary of other ancillary benefits from utilizing these policy

shifts, such as an enhanced infrastructure, freeing up transportation sources, and potentially

mitigating concerns of a highly contested method for enhanced recovery.

10

AGNOSTICS AND EVANGELISTS

Perhaps the most contentious issue surrounding the energy industry is from what source

supplies the market, with the argument largely focused on the negative externalities of carbon

emission produced by petroleum, natural gas and coal (hydrocarbons). Individuals and groups

that support one form of energy supply over another I describe as Evangelists, and it is that

group that drives policy. Others that have no preference outside of such issues as cost/benefit,

accessibility, and security are deemed Agnostics. I believe America’s energy policy should take

an All the Above Agnostic approach, limiting interference in promoting one form of energy over

another. Historically, government has been a poor asset allocator, with the market better at

assessing where to allocate limited resources.

EXTERNALITIES

Negative externalities are costs borne by a third party involuntarily. In the energy industry, the

most prominent one is pollution in the form of carbon emission. Other common externalities of

hydrocarbon energy sources are waste disposal, soil and water degradation, seismic activity

and cave-ins and depletion of resources associated with the extractive operations.

Negative externalities of non-hydrocarbon based sources are largely ignored in the energy

debate, and come in such forms as aesthetics, safety concerns and business disruption, cultural

activity interference and effects on wildlife.

11

For example, an offshore wind project off the coast of Massachusetts, Cape Wind, was

described as “visual pollution.”1 Other negative externalities, such as tourism and fishing

disruption, anxieties over depressed property values and associated obstructed views, as well

as concerns by a local Indian tribe over disturbing ancient burial grounds, are largely

downplayed by wind power Evangelists.2

Avian deaths caused by turbine blade strikes are frequent, which may result in a change in the

balance of the local ecosystem, such as overpopulation by rodentia, which could spread

diseases and destruction of property and crops.3 A recent court ruling may internalize the cost

of bird deaths.4 In addition to monetary fines, the ruling requires Duke to take the following

measures when birds are in the vicinity:

Cut back flora where prey may hide; and

Stop wind turbines

If the turbines are not turning, they are not making money. When in motion, wind turbines

generate a vortex that distorts planes’ signatures making them indistinguishable on air

controllers’ radar screens.5 This motion also leads to turbulence, which may require planes to

1 Seelye, Katherine Q. "Koch Brother Wages 12-Year Fight Over Wind Farm." New York Times 22 October 2013:

A12. <http://www.nytimes.com/2013/10/23/us/koch-brother-wages-12-year-fight-over-wind-farm.html?pagewanted=all&_r=0>.

2 Courtney. Cape Cod's Offshore Wind Farm: Yay [sic] or Nay? 29 April 2010. 2013.

<http://thegreenists.com/energy-saver/cape-cods-offshore-wind-farm-yay-or-nay/5699>. 3 Avary, Steven L. "Wind Power: Evaluating Cost Economics." 2014. 2. Print.

<https://www.linkedin.com/profile/view?id=2506829&trk=nav_responsive_tab_profile>. 4 Cappielo, Dina. Guilty plea in bird deaths at wind farms a first. 23 November 2013. 2013.

<http://www.myfoxny.com/story/24050658/guilty-plea-in-bird-deaths-at-wind-farms-a-first>. 5 Irvine, Chris. "Wind farms could pose danger to planes without new air traffic control radar." The Telegraph 25

May 2009. <http://www.telegraph.co.uk/travel/travelnews/5383658/Wind-farms-could-pose-danger-to-planes-without-new-air-traffic-control-radar-system.html>.

12

alter their paths.6 Consequently, the alteration causes more financial burdens for the airplane

and greater carbon emissions incurred with the consumption of additional jet fuel.

LEVELIZED COST OF ENERGY

One of the more frequent metrics of comparison between energy for electricity prices is the

LCOE, which is a discounted financial cost figure over the economic life of the project

incorporating capital costs, fixed and variable operating and maintenance (O&M) costs, fuel

input costs and carbon tax where relevant, and an assumed utilization rate.7 Joskow called this

metric flawed when comparing hydrocarbon versus renewable energy source technologies, as it

treats electricity generation as a “homogenous product governed by the law of one price,” that

it does not take into account volatility in the value of supply varying significantly over the year.8

However, he bases his argument on the assumption that demand is perfectly price inelastic

(i.e., transaction price insensitive), which might hold at a specific point in time, but unlikely over

a prolonged period as new energy supply is introduced. Other costs may come in the form of

externalities, opportunity costs (i.e., the best alternative’s value), and market distortions

through government intervention.9

6 Burnett, III, James H. boston.com. 10 June 2012. 2013. Web.

<http://www.boston.com/ae/movies/articles/2012/06/10/spin_a_good_yarn/>. 7 Avary, Steven L. "Wind Power: Evaluating Cost Economics." 2014. 1. Print

8 Joskow, Paul L. "Comparing the Cost of Intermittent and Dispatchable Electricity Generating Technologies."

American Economic Review: Papers & Proceedings 101.3 (2011): 239. Web. <https://www.aeaweb.org/articles.php?doi=10.1257/aer.101.3.238>.

9 Avary, Steven L. "Wind Power: Evaluating Cost Economics." 2014. 1. Print

13

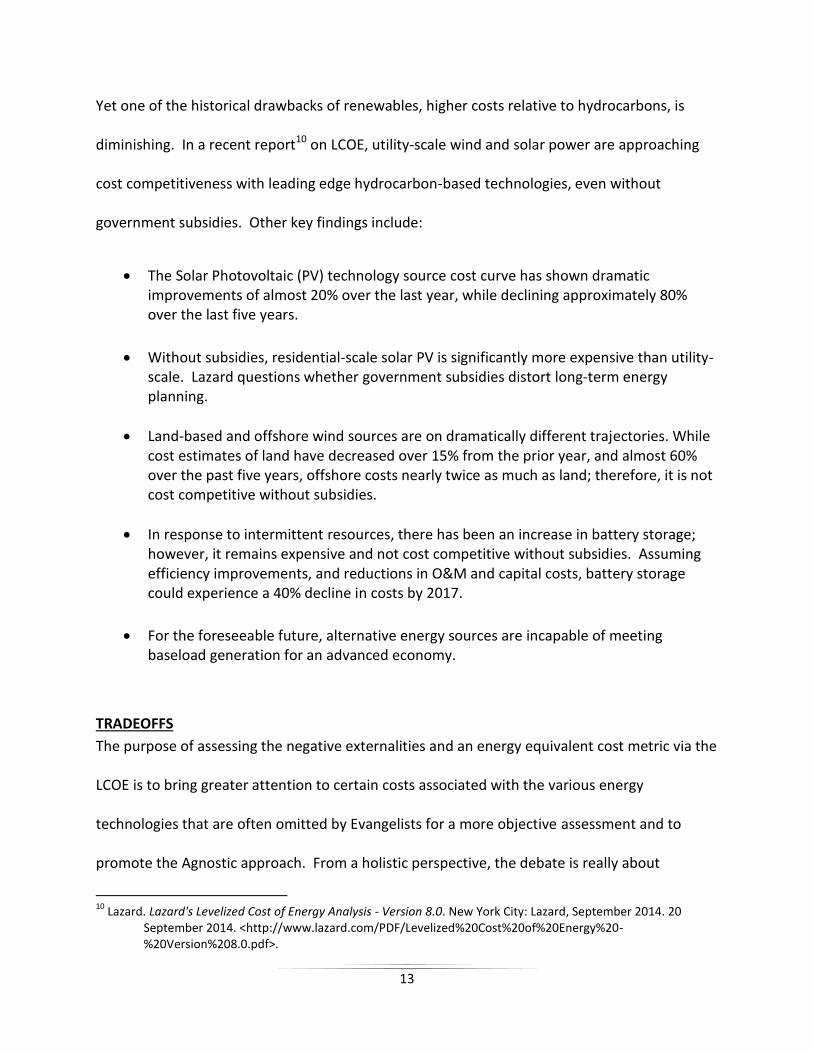

Yet one of the historical drawbacks of renewables, higher costs relative to hydrocarbons, is

diminishing. In a recent report10 on LCOE, utility-scale wind and solar power are approaching

cost competitiveness with leading edge hydrocarbon-based technologies, even without

government subsidies. Other key findings include:

The Solar Photovoltaic (PV) technology source cost curve has shown dramatic improvements of almost 20% over the last year, while declining approximately 80% over the last five years.

Without subsidies, residential-scale solar PV is significantly more expensive than utility-scale. Lazard questions whether government subsidies distort long-term energy planning.

Land-based and offshore wind sources are on dramatically different trajectories. While cost estimates of land have decreased over 15% from the prior year, and almost 60% over the past five years, offshore costs nearly twice as much as land; therefore, it is not cost competitive without subsidies.

In response to intermittent resources, there has been an increase in battery storage; however, it remains expensive and not cost competitive without subsidies. Assuming efficiency improvements, and reductions in O&M and capital costs, battery storage could experience a 40% decline in costs by 2017.

For the foreseeable future, alternative energy sources are incapable of meeting baseload generation for an advanced economy.

TRADEOFFS

The purpose of assessing the negative externalities and an energy equivalent cost metric via the

LCOE is to bring greater attention to certain costs associated with the various energy

technologies that are often omitted by Evangelists for a more objective assessment and to

promote the Agnostic approach. From a holistic perspective, the debate is really about

10

Lazard. Lazard's Levelized Cost of Energy Analysis - Version 8.0. New York City: Lazard, September 2014. 20 September 2014. <http://www.lazard.com/PDF/Levelized%20Cost%20of%20Energy%20-%20Version%208.0.pdf>.

14

tradeoffs, netting out the various externalities against other factors like direct and indirect

financial costs and benefits, accessibility, dispacthability (i.e., on/off flexibility in response to

demand) and intermittency (i.e., demand dispatch inability or unpredictability).

15

POLICY SHIFTS

The key drivers in enhancing America’s position in addressing its global standing, tackling its

twin deficits, and providing a more robust economic base utilizing energy assets are through

policy shifts from the Executive Branch, Legislative Branch, and the quasi-governmental Federal

Reserve.

EXECUTIVE BRANCH

One of the roles for the executive branch is leading foreign policy. As the focal point of this

area, it is of great importance to have a clearly defined policy, the resources to enable it, and

decisive in its implementation. Given the current state of affairs, the Administration appears

disengaged and uncertain, rebuffing traditional allies and embracing those players that at times

have been hostile to the U.S., leading to a state of confusion. Instead of using successful

established patterns and “measuring twice and cutting once,” there are too many instances of

tailoring “by the seat of their pants,” with an “ill-suited” policy as a consequence. Saudi Prince

al-Waleed bin Talal stated, “The U.S. has to have a foreign policy. Well defined, well structured.

You don’t have it right now, unfortunately. It’s just complete chaos.”11

The world is looking for leadership. Yet when Ian Bremmer poses the question as to whom

would assume the mantle, he said “no one.”12 He bases this conclusion stating, “none has

political and economic muscle to remake the status quo.”13

11 Stephens, Bret. "Obama Survival Manual, Intl. Edition: If you think 2014 has been a year of unraveling and

disorder, just wait." The Wall Street Journal 13 October 2014. <http://online.wsj.com/articles/bret-stephens-obama-survival-manual-intl-edition-1413242790>.

12 Bremmer, Ian. Every Nation for Itself: Winners and Losers in a G-Zero World. New York: Penguin Group, 2012: 4.

Print 13

Bremmer, 10

16

International Relations Theory

In the process of executing foreign policy, it is important to have a “playbook” to provide

guidance in initiating and responding to actions as the circumstances dictate. International

relations are politics translated to the global forum; therefore, implementing and executing the

correct policy while assuming the appropriate posture is essential. Given the high stakes,

seeking guidance from the various international relations theorists and incorporating empirical

support in decision-making is critical with such criteria as constructing an overarching objective,

and applying certain tenets from the respective schools of thought.

Hegemonic Stability Theory

It is my belief that circumstances associated with these particular times suggest adherence to

the Hegemonic Stability Theory (HST), the overarching objective for international relations. The

world seems adrift, with little to no global leadership, leaving a vacuum for “bad actors” who

feel empowered to create chaos, death and destruction. This environment results in significant

geopolitical risk with a requisite for risk premiums in capital and assets.

The key tenet of HST is that a single nation-state that dominates the world, or a hegemon, will

exercise leadership via diplomatic channels, persuasion, or coercion; thus, providing a more

stable system globally.14 For instance, the period often referred to as Pax Britannica, a

timeframe of roughly a century ending at the beginning of World War I, was generally a time of

relative peace and prosperity across the globe. Britain utilized its powerful navy to secure

maritime routes that enabled for greater trade in goods and to project its influence to quell

uprisings.

14 Goldstein, Joshua S., International Relations. New York: Pearson-Longman. 2005. 107

17

Realists

The Realist School of International Relations takes a hard power, state-centric position, focusing

on safety, with a wealth maximizing economy utilized to fund a powerful military. Amassing

absolute power is critical, yet enhancing relative power is the interim goal on the path to be the

global hegemon.15 Yet, Mearsheimer comments that given certain geographical physical

characteristics, mainly water, would make it impossible to be a global hegemon, and any

aspirants would be constrained to be a regional hegemon.16 As I perceive it, perhaps the

biggest weakness of certain Realist ideology is when taken to the extreme, certain stances may

come across as belligerent, reducing the probability of building a broad coalition, limiting

responses to unilateral acts.

Geographical constraints notwithstanding, I am not convinced that a country is limited to

regional hegemony. For instance, at minimum, the United States would be considered a

regional hegemon, yet China and Russia may counterbalance each other in their respective

region. I suggest that America might position itself somewhere between a regional and global

hegemon, such as a “multi-hemispheric” hegemon excluding the sphere surrounding both

China and Russia.

15 Mearsheimer, John J., The Tragedy of Great Power Politics. New York: W.W. Norton & Company. 2001: 1-402 16

Mearsheimer, 84

18

Liberals

The main theme proposed by Complex Interdependence suggests a soft power approach that

promotes interconnectedness of mutually beneficial relationships in economic and national

security interests.17 This interdependence may help advance America’s interests with broader

and deeper ties with states and organizations that share certain worldviews. This perspective

leads us to reexamine ties to other parties that could at best be described as strained if not an

outright hostile relationship which resulted or could result in negative consequences. Just like

tending a growing tree, America may have to prune some of these relationships so that more

resources are diverted to those that foster a healthier organism.

However, a weakness of interdependence as characterized in the International Organization

Model is that there are constraints placed on the actors, limiting full capacity utilization given

the systems’ processes and procedures.18 When such occasions arise, America should reach

out to find a solution. While a broadly accepted diplomatic solution is preferable, there may be

times it would be more prudent to proceed down a different path. For instance, while most

countries are in favor of reducing carbon emissions, the effect of the Kyoto Protocol was of

little consequence. Signatories to the agreement breached their emissions limitations. Still

17 Keohane, Robert O. and Joseph S. Nye, Jr. Power and Interdependence. Pearson-Longman, February 20, 2011: 1-

294. Print 18

Keohane, 46-47

19

America, a non-ratifier, was able to achieve much of the objective via a market-based solution

(i.e., natural gas displacing coal).19

Because of significant shifts in foreign policy over the last few years, America is often described

as a state with a diminishing power position, although the fundamentals of a strong power base

are still intact. Such a view is described as the Eroding Hegemon Model (EH), and where it

occurs regime change follows.20 Perceptions of this weakened position is evidenced in current

events, with Russia taking a more belligerent stance, escalating activities rarely seen since the

fall of the Soviet Union.21

This EH model buttresses my position on HST, as I believe that states’ innate goal is to be the

global hegemon if given the opportunity and resources. If the U.S. will not step up, someone

else will make an attempt. Aggressive actions taken by certain global players, especially that of

China (e.g., Taiwan, South China Sea) and Russia (e.g., South Ossetia, Crimea), supports this

argument.

19 Lieberman, Ben. "What Americans Need to Know About the Copenhagen Global Warming Conference." Special

Report #71 on Climate Change. 2009. Web. 28 November 2014. <http://www.heritage.org/research/reports/2009/11/what-americans-need-to-know-about-the-copenhagen-global-warming-conference>.

20 Keohane, 36-37

21 Fox News. Russia has never flown bomber patrols over Gulf of Mexico before, US official claims. 13 November

2014. Web. 30 November 2014. <http://www.foxnews.com/world/2014/11/13/russian-defense-ministry-says-bomber-patrols-will-reach-gulf-mexico/>.

20

Central Limit Theorem

Rarely have there been situations where the goals of the two main schools of International

Relations, Liberals and Realists, have overlapped to such an extent. At this moment, the Liberal

tenet of interconnectedness and Realist’s strong economy that bolsters the military and

facilitates hegemonic aspirations are not mutually exclusive. My belief is in a hybrid of these

two schools,22 neither implementing policy based solely on soft power, nor that of hard power,

rather a default position of semi-hard power that focuses on more diplomatic measures yet

sealed with a “firm handshake.” The reasoning for this approach is that each situation is

different, and requires the flexibility to move along the continuum as the situation dictates.

A hybrid model is substantiated by a report23 that “hard power” is decreasing in the eyes of

public opinion, though relying on “soft power” may cause a vacuum leaving the opportunity for

bad actors to impose deleterious actions.

Incorporating international relations theory from the various schools is an important tool in

providing direction. While each situation faced is different, many of the same themes

encountered over history are repeated. Examining the features of similar situations and the

outcomes can help navigate obstacles to achieve the intended result.

22

Avary, Steven L. "Central Limit Theorem: A Treatise on International Relations Reconcilement." 14 April 2014. 12-14. Print <https://www.linkedin.com/profile/view?id=2506829&trk=nav_responsive_tab_profile>. 23

Fordham, Tina M., et al. Taking it to the streets: What the New Vox Populi Risk Means for Politics, the Economy and Markets. New York: Citi GPS: Global Perspectives & Solutions, 2014: 40. Web <https://ir.citi.com/MLFFG3mEHO39FBGJhaYs8f02RBUr5gk4DwtUNhgcMXG%2Bi%2FGKPG8GW8VegMsWPk40v5U3DEmh%2Bjo%3D>.

21

LEGISLATIVE BRANCH

With respect to the legislature, the key areas to be addressed are changes to the dichotomous

branches of fiscal policy, taxing and spending, eliminating mandates, and promoting bills

focused on facilitating energy growth.

Fiscal

My objective for changes in fiscal policy is to reduce the distortions caused by government

intervention. Furthermore, given that capital flows to where it is treated best, my objectives

include creation of a more hospitable environment through a more prudent tax policy in the

United States, making it more competitive with the rest of the world. Government

intervention, through excessive burdens of regulatory overreach or taxation, or by misallocating

resources through subsidies or government funding and loan guarantees, inserts a wedge, or

Dead Weight Loss (DWL), leading to economic frictions.

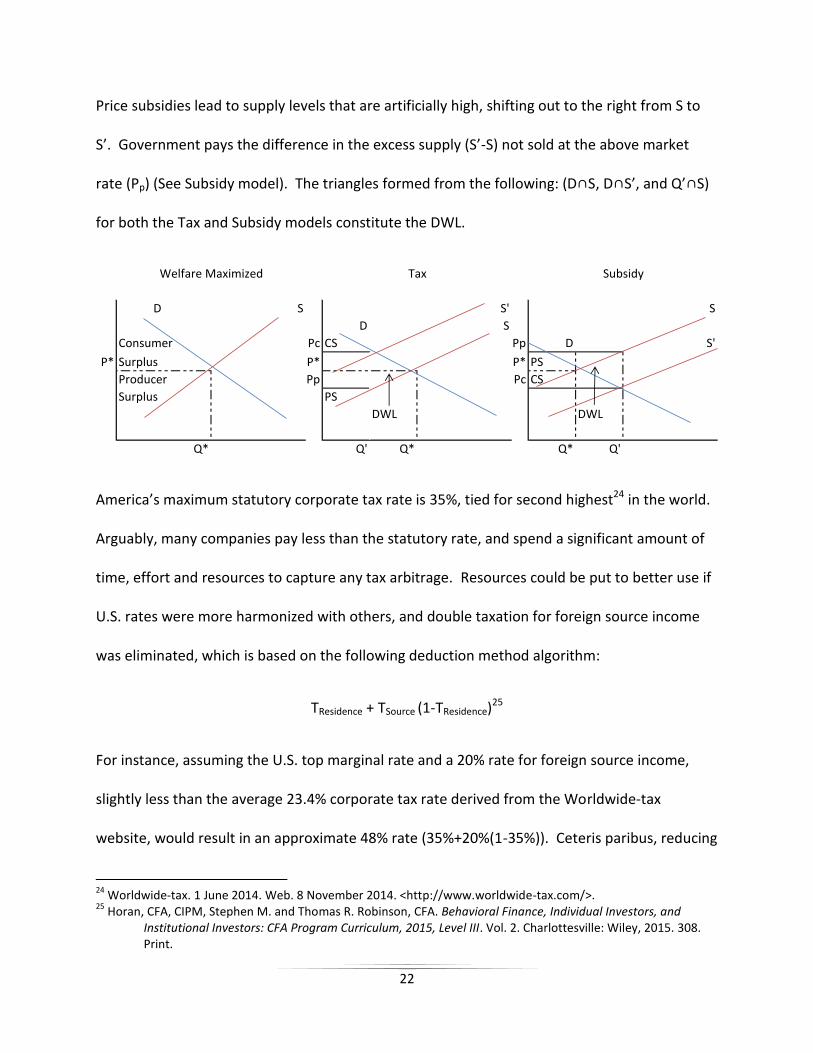

As shown in the models that follow, welfare is maximized amongst the various parties where

the Supply Curve (S) and Demand Curve (D) are in natural equilibrium at Price (P*) ∩ Quantity

(Q*). Producer Surplus (PS) is the amount the supplier receives in excess of its costs, and is the

area above S up to P*. Consumer Surplus (CS) is the amount a buyer saves, and is the area

below D down to P* (See Welfare Maximized model).

Disequilibria caused by government intervention reduce welfare by a loss of surplus by one or

both parties without a corresponding offset to the other party. Price distortions with a tax on

goods erodes welfare at CS from P* to Price to the consumer (Pc), and PS declines from P* to

Price to producer (Pp). S shifts upward to the left (S’) and reduces Q* to Q’ (See Tax model).

22

Price subsidies lead to supply levels that are artificially high, shifting out to the right from S to

S’. Government pays the difference in the excess supply (S’-S) not sold at the above market

rate (Pp) (See Subsidy model). The triangles formed from the following: (D∩S, D∩S’, and Q’∩S)

for both the Tax and Subsidy models constitute the DWL.

America’s maximum statutory corporate tax rate is 35%, tied for second highest24 in the world.

Arguably, many companies pay less than the statutory rate, and spend a significant amount of

time, effort and resources to capture any tax arbitrage. Resources could be put to better use if

U.S. rates were more harmonized with others, and double taxation for foreign source income

was eliminated, which is based on the following deduction method algorithm:

TResidence + TSource (1-TResidence)25

For instance, assuming the U.S. top marginal rate and a 20% rate for foreign source income,

slightly less than the average 23.4% corporate tax rate derived from the Worldwide-tax

website, would result in an approximate 48% rate (35%+20%(1-35%)). Ceteris paribus, reducing

24

Worldwide-tax. 1 June 2014. Web. 8 November 2014. <http://www.worldwide-tax.com/>. 25

Horan, CFA, CIPM, Stephen M. and Thomas R. Robinson, CFA. Behavioral Finance, Individual Investors, and Institutional Investors: CFA Program Curriculum, 2015, Level III. Vol. 2. Charlottesville: Wiley, 2015. 308. Print.

D S S' S

D S

Consumer Pc CS Pp D S'

P* Surplus P* P* PS

Producer Pp Pc CS

Surplus PS

DWL DWL

Q* Q' Q* Q* Q'

Welfare Maximized Tax Subsidy

23

the rate, and eliminating the double taxation would result in the following tax savings benefit

for foreign source income: 48%-TSource, which can be reinvested and provide a multiplier effect

of P (1+r)N.

A more prudent and robust fiscal policy would include accelerated depreciation, depletion, and

amortization (DD&A) schedules, tax holidays and special tax benefits, such as a higher rate for

deductions or credits, for repatriated funds that are devoted to research and development,

capital investment, personnel training and hiring, and for certain infrastructure project

investments. The accelerated DD&A provides the benefit of the time value of money of tax

shields for capital investment, and tax holidays would incentivize corporations to repatriate

funds from overseas to reinvest in the U.S.

24

Expenditures

At the heart of the American Government’s desire to make such expenditures is to increase

aggregate demand through Keynesian Economics with the objective to increase Real (i.e.,

inflation adjusted) Gross Domestic Product (GDP), the final value of all goods and services

produced in a country, represented by the GDP Expenditure Model below:

GDP = C+I+G+X-M

Defined as:

C = Consumers

I = Industrial

G = Government

X = Exports

M = Imports

With the various financings and the principal-agent relationship, there arise the attendant risks

of moral hazard, adverse selection and risk compensation. Briefly, moral hazard is the

additional risk someone undertakes if another party (i.e., principal) bears the risk burden. This

situation is seen frequently in financings where management (i.e., agent) is imprudent in such

areas as spending or operations. Moral hazard can be an ex-ante or ex-post risk. The central

feature of adverse selection is information asymmetry, where one party has a more complete

picture with their access to better information, allowing them to be in a better negotiating

situation than the other. The information asymmetry can manifest itself as risk compensation,

the requisite return based on the perceived level of risk. If the perception of this risk is

incorrect, it can lead to the asset associated with the risk to be overpriced significantly.

25

Government funding of various energy projects via a portfolio managed by the Department of

Energy (DOE) has taken center stage over the last few years. “Crony capitalism” has distorted

the funding process, with critical objectivity and robust financial analysis often secondary.

Thus, the triple net goal of people, planet, and profit is frequently supplanted with biases

toward energy source, individual companies or individuals that are well connected (e.g., George

Kaiser and Solyndra), often in exchange for quid pro quo support of various political parties,

policies or candidates. Given certain biases, and that the DOE personnel do not have “direct

skin in the game” in the form of personal capital at risk, which is commonplace in the private

sector; and, with limited concern over job security should the investment underperform, there

is not as great an incentive to be more thorough with due diligence. One of the most astute

comments I ever heard about reviewing business plans was, “All business plans have two things

in common, the numbers always go up, and they are always wrong.” The Prudent-Person Rule

is a legal maxim in the private sector restricting investing to those opportunities that have

assumptions scrutinized and significant iterative stress tests of the financial projections are

undertaken. Consequences of financial imprudence are reflected in the demise of Long-Term

Capital Management (LTCM), a highly sophisticated hedge fund with Nobel laureates on its

payroll. LTCM utilized a strategy based on correlations amongst different assets based on a

normal statistical distribution. The key question not addressed was what happens to

correlations when there is a kurtosis distribution, a situation where there is an extreme event?

LTCM’s failure is described as a result of the breakdown in asset correlations, where asset

prices moved differently than anticipated. The DOE exposed taxpayer money to the big solar

thermal project Ivanpah. One of the investors for this project is Google, led by Chairman Eric

26

Schmidt, who is very close to the current Administration. While the U.S. provided a $1.6 billion

construction loan, Ivanpah has recently approached the DOE again for money in the form of a

grant of around $500 million in which to pay off some of the loan. Purportedly, the need to

come hat and hand was due to unexpected weather, the sun did not shine enough.26 DOE

meet intermittency risk, perhaps the most prominent risk with many alternative energy

sources. Providing a grant would throw good money after bad, and the grant structure is “free

money” to the organization; therefore, no payoff to the American taxpayer.

Other than magnitude, essentially the only real differences between LTCM and Ivanpah was

with regards to “Other People’s Money” (OPM). LTCM’s was with money volunteered by

investors, while the DOE’s was taken involuntarily from taxpayers. As LTCM resides in the

annals of history, the DOE’s misallocation of taxpayer money continues unabated.

Should government continue to make investments, consideration of the position in the capital

structure is of significant importance. At no time should the government use taxpayer money

to take an equity position. Not only does this expose the portfolio to residual equity risk, but

also with a portfolio conflict where the government could have an outsized influence over the

entity and industry, clearing a path not available to others and coercing potential customers to

the government backed entity. Typically, companies or projects that seek government

financing are at a stage of maturity where they do not generate sufficient or stable enough cash

26

La Jeunesse, William. World's largest solar plant applying for federal grant to pay off federal loan. New York, 8 November 2014. Web. 29 November 2014. <http://www.foxnews.com/politics/2014/11/08/world-largest-solar-plant-applying-for-federal-grant-to-pay-off-its-federal/>.

27

flows to support a typical loan structure. Providing government guarantees, which prices the

instrument on the full faith and credit of the U.S. Government, exposes taxpayers to absorb the

loss in the event of a default by the issuer.

Reallocation

While my preference is to eliminate government involvement where possible, I am pragmatic in

the sense that there will always be some given entrenched interests. Therefore, I make the

case for reallocating involvement to areas I believe mitigate much of the risk to taxpayer money

as well as focusing on areas that have broad applications with a potential material impact. It is

my belief the key focus should be in research and development (R&D). In so doing, several risk

factors are minimized including direct commodity price, operational and business model. Also,

if funding was provided in staged tranches, with future funding based on meeting certain

milestones, such a structure should incentivize for a more focused approach on continuous

improvement and in a timely manner. It should also limit throwing good money after bad, and

alleviate concerns of moral hazard, risk compensation and adverse selection. Such an approach

should also reduce crony capitalism as well as the asymmetrical payoffs of privatized profits and

socialized losses. Focusing on R&D would imply the key risk remaining is technology, an area

where the U.S. has an absolute and comparative advantage over all the other market

participants. The focus should be on broad-based issues, such as carbon capture and

sequestration (CCS) for hydrocarbon-based energy sources, and battery storage, the “holy grail”

solution addressing intermittency limitations of alternative sources. The CCS issue may also be

beneficial as a source of enhanced hydrocarbon recovery with its reinjection into hydrocarbon

28

reservoirs, which might moderate the need to frac. Other areas that might be addressed

includes infrastructure spending such as upgrades to the electric grid, making it more resilient

and secure, and allowing for better interconnectedness permitting the ability to transmit from

one region to another to address supply and demand issues, as well as upgrades to the railway

infrastructure, midstream, and ports, reducing the burden on the transportation of goods.

Investment should boost the qualitative factors of America’s infrastructure, which ranks 15th,

12th, and 24th, out of 144 countries for railway, seaports, and electric supply, respectively27

In some of these infrastructure projects, it might make sense for public/private partnerships

with the understanding that funds will not be diverted to illusory “make work” government

interests, that labor is not limited to those individuals under collective bargaining agreements,

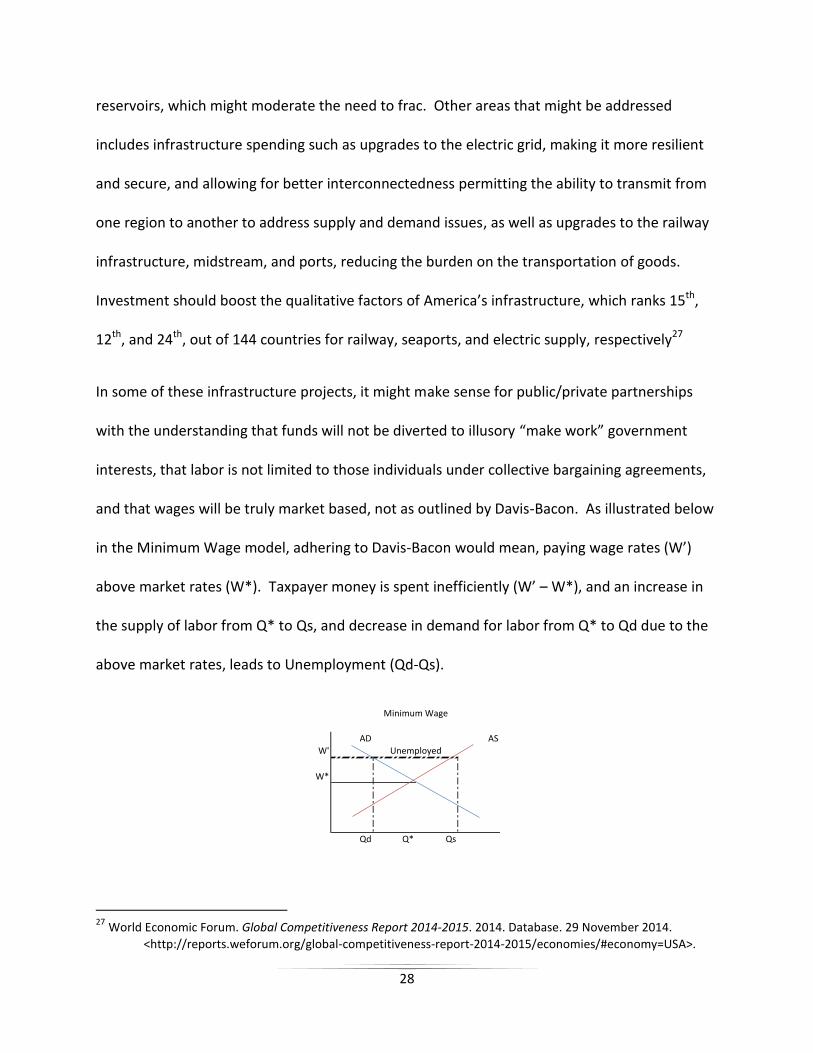

and that wages will be truly market based, not as outlined by Davis-Bacon. As illustrated below

in the Minimum Wage model, adhering to Davis-Bacon would mean, paying wage rates (W’)

above market rates (W*). Taxpayer money is spent inefficiently (W’ – W*), and an increase in

the supply of labor from Q* to Qs, and decrease in demand for labor from Q* to Qd due to the

above market rates, leads to Unemployment (Qd-Qs).

27 World Economic Forum. Global Competitiveness Report 2014-2015. 2014. Database. 29 November 2014.

<http://reports.weforum.org/global-competitiveness-report-2014-2015/economies/#economy=USA>.

AD AS

W'

W*

Qd Q* Qs

Minimum Wage

Unemployed

29

Taxes

With regards to tax policy, I am focusing on responding to debates about introducing new tax

structures, such as carbon or cap & trade, and renewable externality, and modifications to tax

credits and tax accounting methodologies for DD&A and LIFO.

Carbon

All energy sources have negative externalities that result in society having to bear some of the

costs. Various mechanisms have been proposed in which the goal is for the producer to

internalize the negative externality costs. One of the most frequently mentioned is inserting a

carbon tax. The tax is based on a per energy heating unit (i.e., Btu) produced. However, as

noted by the EIA,28 carbon emission is not uniform across source per Btu, ranging from 117

pounds of CO2 per million Btu for natural gas to 228.6 for anthracite coal. Therefore, such a tax

system would be “inequitable” solely from a per unit of carbon emitted perspective. For a coal-

fired electric utility, four different types of coal with different CO2 level content might be

consumed including anthracite (228.6), bituminous (205.7), lignite (215.4) or subbituminous

(214.3). Should there be a switching amongst the different sources of coal or if the facility

allows for switching amongst the different hydrocarbon sources, keeping track for assessing an

equitable carbon tax would be onerous, if not impossible.

Cap & Trade

Although not technically categorized as a tax is Cap & Trade, a mechanism where certain

producers limit supply, while “trading” their excess emission volumes available to other

28

U.S. Energy Information Administration. "How much carbon dioxide is produced when different fuels are burned?" 14 June 2014. U.S. Energy Information Administration. Web. 20 November 2014. <http://www.eia.gov/tools/faqs/faq.cfm?id=73&t=11>.

30

producers of carbon, thereby pushing up prices and limiting supply. The “tax” is transferred to

the purchaser, permitting it to emit additional CO2 volumes previously available to the seller.

Thus, this system in and of itself does not really reduce carbon emissions, it transfers it. A

cousin to Cap & Trade is renewable identification numbers (RINs), a tracking system imposed by

the Environmental Protection Agency (EPA) to confirm refiners use enough ethanol. In addition

to holding a RIN directly, should they not fulfill the requirement, RINs can be purchased from

others. This system has been gamed, with counterfeit RIN numbers valued in the millions of

dollars.29

Renewable Externality

For non-hydrocarbon source energy, rarely is a cost for negative externalities mentioned as part

of the debate. The recent charges filed against Duke set a precedent, and may result in

applying a similar “negative externality” tax across the board. Just as it would for

hydrocarbons, trying to derive the cost in which to assess the tax would be very difficult.

Would it be an actual hard count, or an estimate for such categories as bird kills? If so, would

there be a uniform set price per bird, or would there be different values assessed for birds that

are more endangered?

Regardless of method, eventually the consumer is the one that picks up the tax in the form of

higher prices, with the largest burden allocated between the consumer and the supplier based

on each party’s price inelasticity.

29 Loris, Nicholas D. The Ethanol Mandate: Don't Mend It, End It. Washington, D.C.: The Heritage Foundation

Backgrounder No. 2811, June 12, 2013. 3. Web. <http://report.heritage.org/bg2811>.

31

Tax credits and DD&A

After reviewing the President’s Budget Proposal,30 it is biased in its support of renewable

sources of energy at the expense of fossil-fuel sources. Tax credits are proposed for the

modification and permanent extension for the Renewable Electricity Production Tax Credit for

the 10-year period 2013-2023 of approximately $24.7 billion. Whereas, the proposal calls for

the repeal of several tax accounting related issues for fossil-fuel preferences over the same

period of an aggregate $48 billion, including expensing intangible drilling costs of an estimated

$13.7 billion, percentage depletion for oil & natural gas wells of $11.1 billion and domestic

manufacturing deduction for oil & natural gas production of $19.4 billion. DD&A is a cost

recovery method to incentivize continuous reinvestment by reducing taxes in a current period.

It is available to all companies, and the rates at which the cost recovery is allocated based on

the economic life of the assets. This tax shield reduces period taxes based on the formula

DD&A x Tax Rate. Taxes are not eliminated; rather they are deferred, allowing the funds

otherwise utilized for tax payments to be reinvested, expanding the economy. The value of the

tax shield is provided as (Annual DD&A x Tax Rate)/(1+r)t, with “r” representing the rate of

return for the invested funds and “t” representing time. As denoted mathematically,

lengthening “t” reduces the value of the tax shield to the company. Expensing items in the

period incurred accelerates the value of the tax shield rather than having it allocated over the

useful economic life as per DD&A tax schedules.

30

Joint Committee on Taxation. Estimated Budget Effects of the Revenue Provisions Contained in The President's Fiscal Year 2014 Budget Proposal: Fiscal Years 2013-2014. Washington, D.C.: Congress of the United States, 2013. Web. <https://www.jct.gov/publications.html?func=startdown&id=4520>.

32

LIFO

A catalyst for eliminating the Last-In First-Out (LIFO) inventory valuation method is the desire to

harmonize accounting standards, the U.S.’s Generally Accepted Accounting Principles (GAAP)

with that of International Financial Reporting Standards (IFRS), which is the most frequently

used standard outside of America. IFRS does not allow a provision for LIFO; therefore, any

attempts to be fully compliant would eliminate this method.

The appeal of LIFO is that the prices allocated to inventory sold are from the most recent units

purchased. In a normal price-increasing environment, this method allows higher priced

inventory to offset revenues and lowering taxable income, while also increasing after-tax cash

flow. As such, it is a better way in which to match current period economics, more closely

taxing “real income” rather than “nominal income” and its associated inflation.31 This inventory

method is prevalent in the energy industry, reflecting its volatile price nature. The budget

proposal includes $78.3 billion for repeal of LIFO for all industries. The LIFO Reserve, the

accumulated net income difference between using LIFO and the First-In First-Out (FIFO) method

for energy companies amounted to less than $15 billion,32 which comprises 37% of the total

LIFO reserve for all industries. In the context of the national budget, this figure is trivial, yet

when viewed alongside alternative energy sources, (e.g., wind and solar) that do not carry

inventory, it is apparent elimination of LIFO would change the competitive landscape amongst

the different energy sources.

31 The Committee for a Responsible Federal Budget. The Tax Break-Down: LIFO Accounting. Washington, D.C., 22

August 2013. Web. <http://crfb.org/blogs/tax-break-down-lifo-accounting>. 32

The Committee for a Responsible Federal Budget

33

Other consequences of LIFO repeal are expressed by the Vice President of Tax of a company,

stating that a LIFO liquidation would not result in additional revenue to the company, rather

deferred taxes would come due, and “In effect the repeal of LIFO is going after our equity.”33

Furthermore, a Director of Tax at PricewaterhouseCoopers, asserts that the termination of LIFO

may affect a company’s net operating losses (NOLs), an accumulation of period losses, which

are used to offset future taxable income.34 Should such a situation arise, impairment of NOLs

would cause a write-down of this asset, reducing reported income.

While potential funds received by the government through LIFO conversion are immaterial in

its overall budget, it has significant impact for the entities that adopted it. There may be an

exclusion for LIFO repeal as a requisite for harmonization. The IRS provides a provision in the

tax code where under certain circumstances, conformity requirement can be relaxed, providing

a potential solution in IFRS discussions.35 If LIFO is repealed, there should be a method in which

to alleviate the damage. Thus, I propose the following: grandfather existing inventories based

on LIFO at a time certain, with new inventory purchases based on the other inventory method

(e.g., FIFO) at a time certain. Amortization of the inventory costs between the two methods

will be done on a pro rata basis, resulting in a gradual transition to be fully compliant with IFRS

without as severe an immediate tax impact.

33

Leone, Marie. "Sucking the LIFO Out of Inventory: The government sees billions of dollars in potential tax revenues sitting on the shelves of company warehouses." CFO Magazine 15 July 2010. 4. Web. <http://ww2.cfo.com/accounting-tax/2010/07/sucking-the-lifo-out-of-inventory/>.

34 Leone, 5

35 Cuomo, CPA, Jason and Mark Lamonte. Is the End of LIFO Near? New York, NY: Moody's Investors Service, 2010.

8. Print

34

Legislation

My discussion about legislation is focused on eliminating biases of various energy sources

through fiscal measures and mandates. In addition, I identified bills with provisions to promote

American Energy growth. Some key legislation that I believe should be amended or aspects

repealed include the Energy Policy and Conservation Act of 1975, the Energy Policy Act of 2005

and the Energy Independence Act of 2007. Additional commentary is provided to explain my

logic not already discussed in other sections.

Law

Energy Policy and Conservation Act of 1975 (EPCA)

Mandate:

Prohibition of crude oil exports

Commentary – the goals of crude export prohibition was to limit foreign imports and conserve

domestic crude stocks in response to the energy crisis in 1973, when OPEC cut off supply due to

America’s support of Israel in the Yom Kippur War.

Neither limiting foreign imports, nor conserving domestic crude was achieved. Rather, it

caused inefficiencies in the market, such as the mismatch between various grades of domestic

crudes available with that of domestic refinery capability.36 Steps have been taken to erode

this restriction with the recent approval of condensate, a high quality of crude that needs little

36 Clayton, Blake. "The Case for Allowing U.S. Crude Oil Exports: Policy Innovation Memorandum No. 34."

The Council on Foreign Relations (2013). Web. 15 November 2014. <http://www.cfr.org/oil/case-allowing-us-crude-oil-exports/p31005>.

35

refining, for export shipment.37 A loophole was found in the law based on how crude and

certain forms of condensate are defined, opening a new pathway and limiting the effectiveness

of the existing ban. Should the President decide to pass on rescinding the mandate, if declared

in the national interest by Congress, there is a provision in EPCA that allows Congress to lift the

ban by amending EPCA.38

Energy Policy Act of 2005

Fiscal:

Guarantees for greenhouse gas innovative technologies, and funding 80% of project

costs for nuclear facilities

Grants for biomass every year over the life of the law

Subsidies for wind and other alternative energy sources

“Financial Backstop” with standby support for delays in new nuclear reactors

Mandates:

Renewable fuels (e.g., ethanol) to be blended in motor fuels

Exclusive use of alternative fuels by Federal Fleet vehicles

Commentary - A key selling point for biofuels is to minimize carbon emission, but “the great

majority of biofuels do not lead to significant net energy gain and cannot therefore lay claim to

being carbon neutral.”39 Exclusive source use is express bias and limits optionality in finding the

37 Berthelsen, Christian and Lynn Cook. "U.S. Ruling Loosens Four-Decade Ban On Oil Exports: Shipments of

Unrefined American Oil Could Begin as Early as August." The Wall Street Journal 14 June 2014. Web. 27 November 2014. <http://online.wsj.com/articles/u-s-ruling-would-allow-first-shipments-of-unrefined-oil-overseas-1403644494>.

38 Ebinger, Charles and Heather L. Greenley. Changing Markets: Economic Opportunities from Lifting the U.S. Ban

on Crude Oil Exports. Washington D.C.: Brookings Institute: Energy Security Initiative, 2014: xi. Print. 25 September 2014. <http://www.brookings.edu/~/media/research/files/reports/2014/09/09%208%20facts%20about%20crude%20oil%20production/crude%20oil%20exports%20web.pdf>.

39Walker, D.A. "Biofuels - for better or worse?" Annals of Applied Biology (2010): 320. Print. 10 November 2014.

36

most affordable energy source funded with taxpayer money. In addition, ethanol damages

traditional car engines when exceeding the 10% (E10) “blend wall.”40

Energy Independence and Security Act of 2007

Fiscal:

Loan program for battery technology

Grants for electric transportation technology

Mandates:

Vehicle electrification

Reduce petroleum consumption and increase alternative fuels by Federal agencies

Biofuels volume floor (i.e., Renewable Fuel Standard)

Commentary – the mandate provides price supports with the volume floor with prices above

market when it is oversupplied. Given the biofuel requirement, when crops used in biofuel and

foodstuffs are in short supply, this leads to food price inflation, and potential civil unrest due to

food scarcity. Also, as discussed in Energy Policy Act of 2005, there is express source bias.

40

Loris, 2-3

37

Bills

The bills that I focused on is the legislation that addressed the following areas: facilitating

Keystone XL, the centerpiece of American Energy Infrastructure Policy, more comprehensive

acts for energy infrastructure, particularly that of midstream assets, and bills that provided for

quicker permitting and enabling for energy exports.

North American Energy Infrastructure Act (NAEIA) A House bill41 was passed in June 2014 that addresses one of the key holdups in building out

America’s energy infrastructure, getting approval for cross-border segments in pipeline and

electric transmission, which was submitted for consideration to the Senate with its pending

bill42 introduced in September 2014. NAEIA requires authorization for construction,

connection, or maintaining the segments, from the Secretary of State for pipelines and

Secretary of Energy for electric transmission. In so doing, a Presidential Permit or Executive

Order is not required; thus, bypassing President Obama who has intimated that he would not

pass Keystone XL. While the authorized parties are members of the Administration and may be

under pressure not to approve it, they may be reluctant to prevent approval given their

respective constituencies and future career aspirations.

41

North American Energy Infrastructure Act. No. H.R. 3301. 113th, 2d Session. Washington, D.C.: 25 June 2014. Web. 15 November 2014. <https://www.govtrack.us/congress/bills/113/hr3301>. 42

North American Energy Infrastructure Act. No. S. 2823. 113th, 2d Session. Washington, D.C.: 16 September 2014. Web. 15 November 2014 <https://www.govtrack.us/congress/bills/113/s2823/text>.

38

Keystone XL

The House of Representatives passed H.R. 568243 in November 2014 approving the

construction, connection, operation and maintenance of the pipeline, including a provision for

any required rerouting within Nebraska and needing authorization by the state. The bill was

forwarded to the Senate, and missed passage by one vote that same month. With the

changeover in the Senate in January 2015, I anticipate that it will come up for another vote and

will pass in the Senate. President Obama is expected to veto the bill, and the Senate will take

another vote on whether to overrule the President’s veto. Should this situation arise, at this

juncture, I think it is too close to call on the overrule vote. Even so, it is my belief it is not

whether “if” Keystone will pass, but “when.” If not in 2015, I anticipate its passage in 2017.

Of note, the bill addresses one of the key tools utilized by the Administration to stall the project

by a myriad of environmental reviews and consultations, stating that the Environmental Impact

Statement issued in January 2014 will satisfy fully requirements of the National Environmental

Policy Act of 1969, and any other requisite reviews or consultations by Federal agencies. In

addition, this bill limits legal judicial review challenges to a Federal agency for acting on it to the

U.S. Court of Appeals, D.C. circuit.

43 Keystone XL Pipeline. No. H.R. 5682. 113

th, 2d Session. Washington, D.C.: 14 November 2014. Web. 15

November 2014. <https://www.govtrack.us/congress/bills/113/hr5682/text>.

39

North Atlantic Energy Security Act (NAESA) This Senate Bill44 proposed in July 2014 is designed to promote domestic energy efforts with

such features as:

Reducing the need for imports of natural gas, directly reducing the trade deficit;

Creating and supporting millions of new jobs across the United States;

Adding billions to GDP;

Generating additional Federal, State, and local government tax revenues; and

Revitalizing the manufacturing sector with abundant and affordable feedstocks

Some of the key matters for passing this bill include the significant amount of flaring or venting

of natural gas while extracting petroleum where there is insufficient natural gas infrastructure,

such as pipelines and gathering systems. The bill provides the Secretary of the Interior with

additional authority for approval of this infrastructure on Federal and Indian lands, and allows

the Secretary to increase the royalties from such lands.

In addition, the NAESA provides for a date certain of no later than 45 days after an application

is submitted for the approval of LNG exportation. Also included is expedited approval for

natural gas exportation to Ukraine, NATO member countries and Japan. This act would help

solidify relations with our allies, and mitigate concerns of Petropolitic supply disruptions

perpetrated by Russia.

44 North Atlantic Energy Security Act. No. S. 2592. 10 July 2014. Web. 14 November 2014

<https://www.govtrack.us/congress/bills/113/s2592/text>.

40

CENTRAL BANK

In general, the Fed’s dual mandate of price stability and maximum employment has an inverse

relationship. The three key tools utilized by the Fed to achieve this objective are open market

operations, reserve requirements and interest rate policy. Open market operations are when

the Fed transacts in the financial market by purchasing treasury securities. In doing so, due to

the inverse relationship between price and yield for bonds, the transactions reduce interest

rates and increase demand for credit that stimulates the economy. The term Quantitative

Easing (QE) is a form of open market operations with an added twist of including non-treasury

securities (e.g., mortgage-backed) with additional procedures in which to manipulate interest

rates. Reducing reserve requirements frees up funds of lenders previously held on account at

the Fed, allowing lenders to extend credit to customers with the goal of expanding the

economy. Interest rate policy via setting the Fed Funds rate has been the most frequently used

tool historically, with the significant QE expansion a relatively recent phenomenon. The Central

Bank section will focus on interest rate policy.

41

The Taylor Rule is often recommended as a rule of thumb for setting the nominal Fed Funds

Rate, incorporating a real rate based on risk pricing and an inflation risk premium. This rule is

represented by the following algorithm with assumed values in brackets based on long-term

trends:

i = r* + π + a1(π - π*) + a2(g - g*)

Defined as:

I = Target Fed Funds Rate

r* = Average real interest rate [2%]

π = Inflation rate [PCE]

π* = Target inflation rate [2%]

g = Real Gross Domestic Product (GDP) growth rate

g* = Average GDP growth rate [3%]

(a1, a2) = Parameter weights [50% each]

As can be seen by the formula and parameter weights, the Fed’s goal is to have a balanced

approach, a Goldilocks range for an economy that is not too hot and not too cold allowing for

moderate sustained growth. With any interest rate move, there is a lag time before the effects

of the move begin to show up in the data. The exact amount of time is subject to debate, but is

generally believed to be at least six to nine months.

As part of the Fed’s mandate, inflation takes a prominent role in monetary policy. Although the

Fed is chartered as an apolitical body, Fed Governors are political appointees, and it would be

naïve to assume that certain biases are never encountered when setting monetary policy. The

most frequently used tool by the Fed in policy actions is changes in interest rates by the Federal

42

Open Market Committee (FOMC). When assessing energy’s impact on inflation, the FOMC

communicates that it strips out the effects of the more volatile food and energy components,

and focuses on “core inflation.”

Picturesque

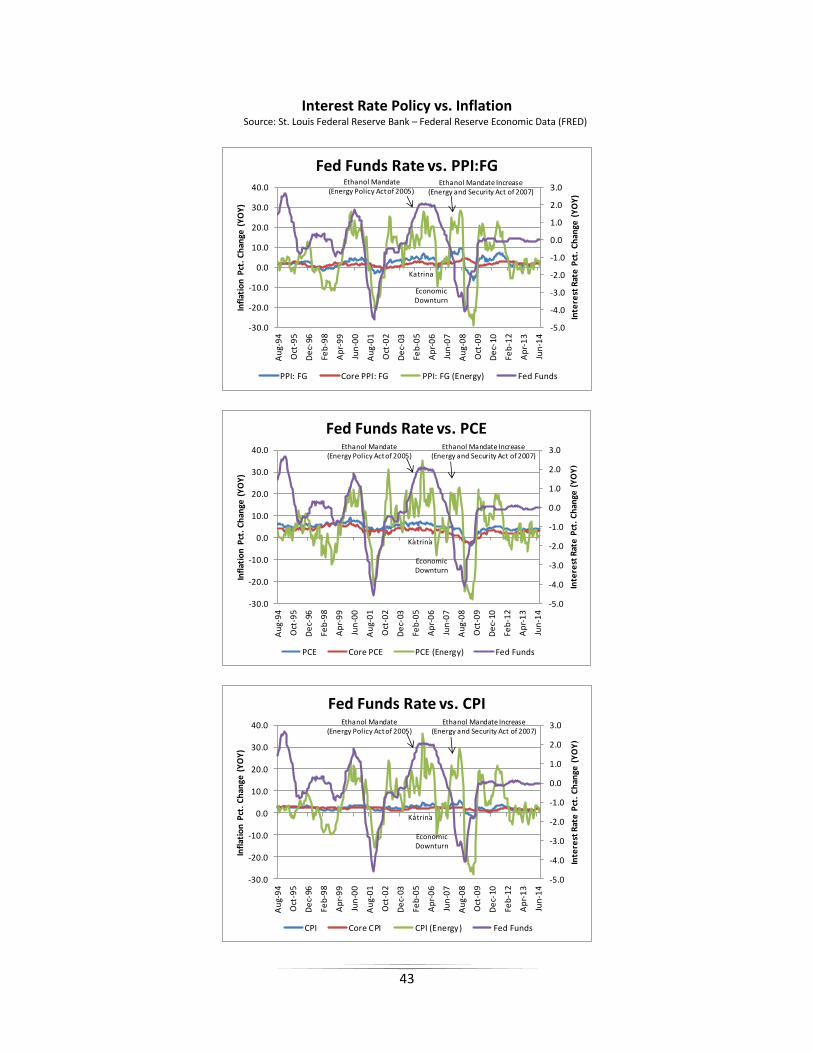

When assessing interest rate policy as it relates to taming inflation, I utilized three major

inflation measures, a subindex of the Producer Price Index (PPI): Finished Goods (FG); the

Personal Consumption Expenditure Price Index (PCE); and, the Consumer Price Index (CPI). As

inflationary pressures generally show up in the production process in a timelier manner, PPI

often serves as an early warning indicator. The most widely followed inflation measure is the

CPI, yet due to certain features such as different weightings between CPI and PCE, and PCE

making adjustments to relative prices and the substitution effect of goods and services, PCE is

the favored index utilized by the Fed in setting rates. As discussed, the FOMC states that it

focuses on core inflation measures. Yet when using an ocular test for interest rate policy in

response to the aforementioned inflation measures, it would appear that the FOMC does not

adhere to this guideline (See Interest Rate Policy vs. Inflation graphs). Changes in headline PPI:

FG, CPI and PCE, as well as their respective Core subindices, are relatively moderate, even

though there are wide swings in the Fed Funds Rate, closely mirroring the volatility in energy

price inflation, as represented by subindices (e.g., PCE (Energy)) of the respective inflation

measures. Based on this observation, I conclude the FOMC’s actions do not follow its

communicated guidance of adhering to fluctuations in core inflation measures as the triggering

mechanism in changing interest rates, rather energy price inflation dominates policy actions.

43

Interest Rate Policy vs. Inflation Source: St. Louis Federal Reserve Bank – Federal Reserve Economic Data (FRED)

-5.0

-4.0