Embed Size (px)

Citation preview

1 | P a g e

CLASH FOR THE INDIAN SKIES…

INDIGO VS SPICEJET VS JET AIRWAYS

“A PROJECT ON COMPARATIVE STUDY OF INDIAN LOW COST CARRIER

(LCC) WITH RESPECT TO INDIGO, SPICEJET, AND JET AIRWAYS”

SUBMITTED BY

PRIYA AWASTHI (01)

SELWYN MASCARENHAS (16)

PALLAVI PATIL (25)

SAAD SIDDIQUI (36)

SUBMITTED TO

DR. PROF. SUHAS RANE

For A Course On

STRATEGIC MANAGEMENT

2 | P a g e

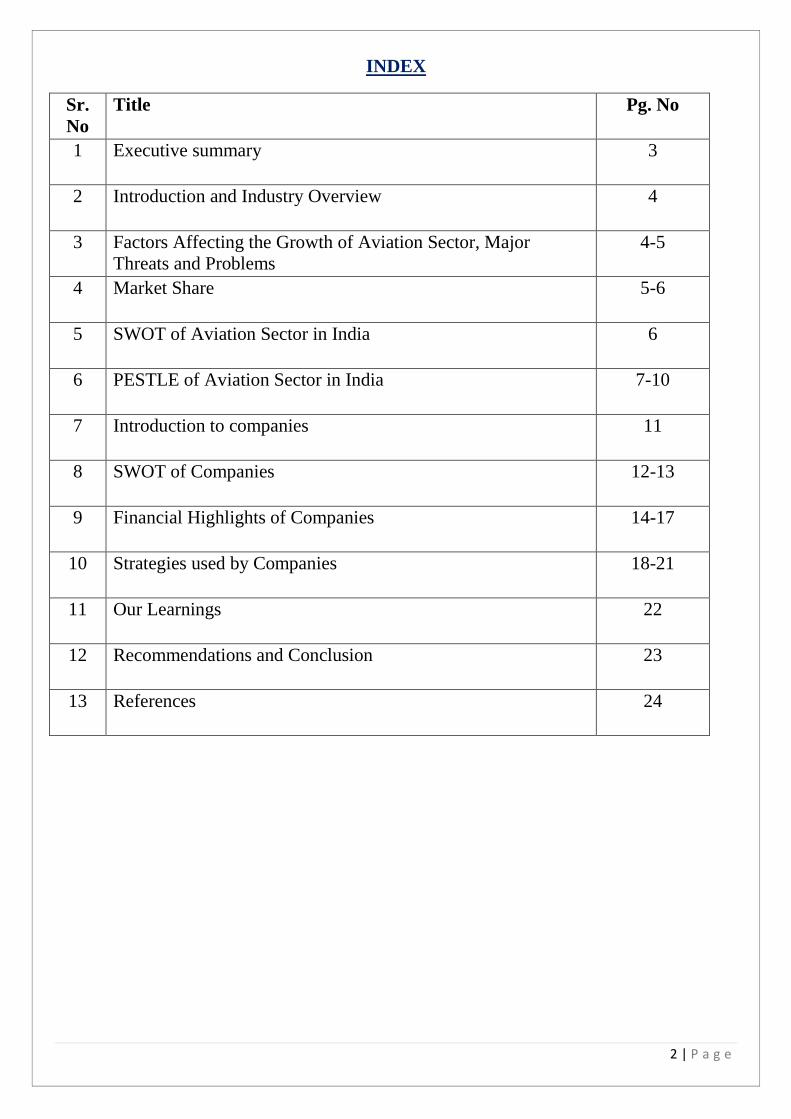

INDEX

Sr.

No

Title Pg. No

1 Executive summary 3

2 Introduction and Industry Overview 4

3 Factors Affecting the Growth of Aviation Sector, Major

Threats and Problems

4-5

4 Market Share 5-6

5 SWOT of Aviation Sector in India 6

6 PESTLE of Aviation Sector in India 7-10

7 Introduction to companies 11

8 SWOT of Companies 12-13

9 Financial Highlights of Companies 14-17

10 Strategies used by Companies 18-21

11 Our Learnings 22

12 Recommendations and Conclusion 23

13 References 24

3 | P a g e

EXECUTIVE SUMMARY

The project undertaken is a comparative study of Indian low cost carriers (LCC) with

respect to Indigo, Spicejet, and Jet Airways. The project provides information on the

various aspects of LCC. It covers the various strategies used by the companies and their

financial performance. It also provides various suggestions to the stakeholders.

4 | P a g e

INTRODUCTION

India is the 9th largest aviation market in

the world with a size of around Rs. 107200

crores and is aiming to become the 3rd

largest by 2020.

Indian aviation industry promises huge

growth potential due to large and growing

middle class population, rapid economic

growth, higher disposable incomes, rising

aspirations of the middle class and overall low penetration levels.

Civil aviation industry in India is experiencing a new era of expansion driven by

factors such as low cost carriers, modern airports, foreign direct investments in

domestic airlines, etc.

The air transport in India has attracted FDI of over Rs. 3812.3 crores from April

2000 to February 2015.

INDUSTRY OVERVIEW

In May 2016, domestic air passenger traffic rose 21.63% to 0.867 crore from 0.713

crore during the same month of the last year.

In March 2016, total aircraft movements at all Indian airports stood at 1,60,830

which was 14.9% higher than March 2015.

Indian domestic air traffic is expected to cross 10 crores passengers by FY 2017,

compared to 8.1 crores passengers in 2015, as per Centre for Asia Pacific Aviation

(CAPA).

India is among the five fastest growing aviation markets globally with 27.5 crore

new passengers.

The airlines operating in India are projected to record a collective operating profit of

Rs. 8,100 crores in fiscal year 2016, according to Crisil Ltd.

http://www.india-aviation.in/pages/view/38/an_overview.html

FACTORS AFFECTING THE GROWTH OF THE AVIATION SECTOR

From an over- regulated and under- managed sector, the aviation industry in India

has now changed to a more open, liberal and investment – friendly sector, especially

after 2004. Some major factors contributing to this are:

Higher Household Incomes

Strong Economic Growth

Entry of Low Cost Carriers (LCC)

Increased FDI inflows in domestic airlines

5 | P a g e

Increased tourist inflow

Surging Cargo movement

Cutting Edge Information Technology (IT) Interventions

Focus on Regional Connectivity

Modern Airports

Sustained Business Growth and

Supporting Government Policies

MAJOR THREATS

The continuous rise in the price of fuel is a major threat.

A terrorist attack anywhere in the world can negatively impact air travel.

Government intervention can lead to new costly rules.

A global economic slowdown negatively impacts leisure, optional and

business travel.

PROBLEMS FACED BY THE AVIATION SECTOR

High operational costs

Cut throat competition

High service tax and other charges

High foreign exchange rate

http://www.mapsofindia.com/my-india/business/in-indias-burgeoning-aviation-sector-

safety-is-the-key-word

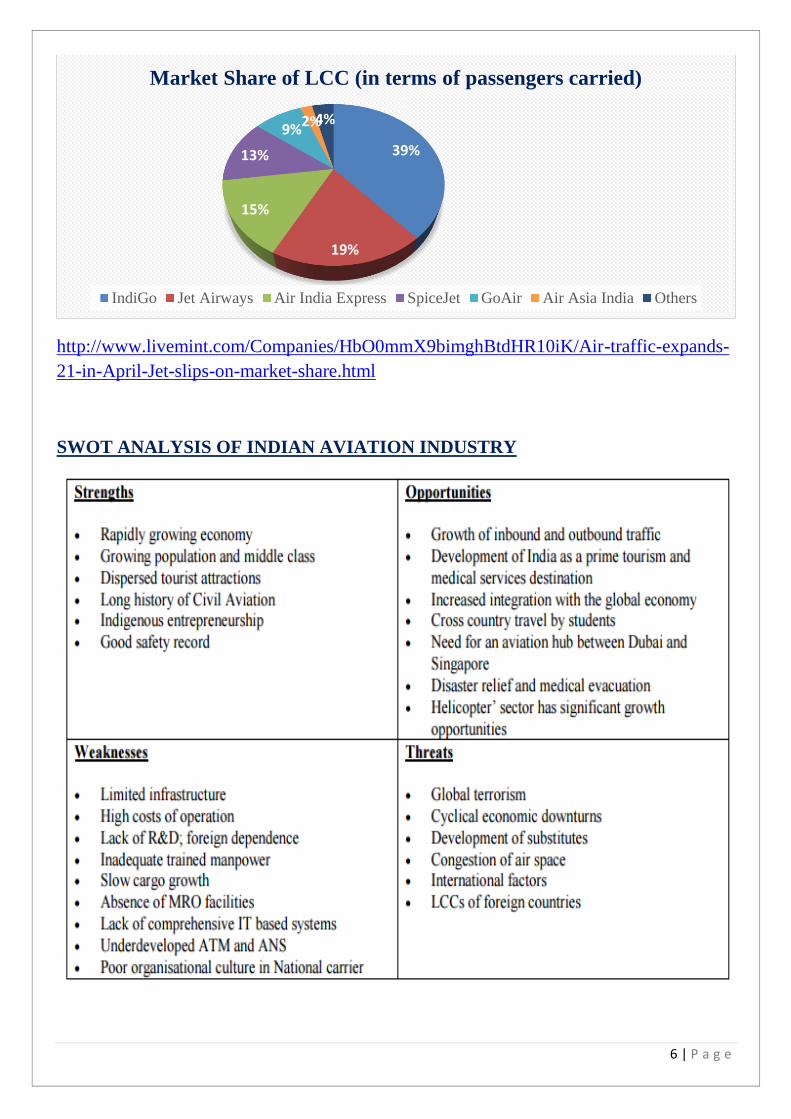

NUMBER OF LOW COST AIRLINES IN INDIA

Sr

No. No. of Players Company Logo

Market

Share

1 IndiGo Airline

38.7%

2 Jet Airways

18.9%

3 Air India Express

15.1%

4 SpiceJet Airline

12.9%

5 GoAir Airline

8.5%

6 Air Asia India

2.1%

7 Others 3.8%

6 | P a g e

http://www.livemint.com/Companies/HbO0mmX9bimghBtdHR10iK/Air-traffic-expands-

21-in-April-Jet-slips-on-market-share.html

SWOT ANALYSIS OF INDIAN AVIATION INDUSTRY

39%

19%

15%

13%

9%2%4%

Market Share of LCC (in terms of passengers carried)

IndiGo Jet Airways Air India Express SpiceJet GoAir Air Asia India Others

7 | P a g e

PESTLE ANALYSIS OF INDIAN AVIATION INDUSTRY

POLITICAL FACTORS:

National Civil Aviation Policy (NCAP) 2016 –

Objectives:

Establish an integrated eco-system which will lead to significant growth of civil

aviation sector, which in turn would promote tourism, increase employment and

lead to a balanced regional growth.

Ensure safety, security and sustainability of aviation sector through the use of

technology and effective monitoring.

Enhance regional connectivity through fiscal support and infrastructure

development.

Enhance ease of doing business through deregulation, simplified procedures and e-

governance.

Promote the entire aviation sector chain in a harmonized manner covering cargo,

MRO, general aviation, aerospace manufacturing and skill development.

1. Open Sky Agreement:

US – No restrictions

UK – Few restrictions

ASEAN and 100 other countries – Limited restrictions regarding landing points,

traffic rights, seasons, capacity, etc.

2. FDI limits:

100% FDI limits is permitted for green field airport projects.

Upto 74% FDI is permitted for existing airport.

3. Taxation Policy:

According to a survey conducted by FICCI-EY on civil aviation sector title ‘Indian

Aviation: Waiting on the runway’, 57% respondents said ‘High Taxation’ is a major

deterrent to growth of aviation industry.

Huge amount of taxes on aviation sector has led to thin profit margins and increases

the cost of ticket by almost 20% (approx.)

Taxes on ATF (which constitutes 30% - 35 % of the operational cost of LCC in

India) – Central Government levies 14% excise duty, 10 % custom duty and States

levy sales tax at weighted average rate of 22.1%

Also with the implementation of GST, the service tax rate which is currently

applicable on air tickets (15%) will increase to a minimum 18%

http://www.taxindiaonline.com/RC2/inside2.php3?filename=bnews_detail.php3

&newsid=2152

8 | P a g e

Impact-

Positive impact on the civil aviation sector, LCC will be benefitted from the new

policy with increased demand for air transport.

Integration of all the related sectors like MRO, aerospace manufacturing, etc. and

skill development programs will strengthen the aviation sector and bring down cost

of maintenance.

Open sky agreements will open up the aviation sector to intense competition which

will make sure only the most efficient LCC will survive.

Increase in FDI limits will help the LCC with much needed capital and

technological know-how.

High taxes will continue to make a dent in the profits of the airlines.

ECONOMIC FACTORS:

India has emerged as the fastest growing major economy in the world as per the Central

Statistics Organization (CSO) and International Monetary Fund (IMF). According to the

Economic Survey 2015-16, the Indian economy will continue to grow more than 7 per

cent in 2016-17.

The improvement in India’s economic fundamentals has accelerated in the year 2015 with

the combined impact of strong government reforms, RBI's inflation focus supported by

benign global commodity prices.

http://www.ibef.org/economy/indian-economy-overview

1. Inflation:

Consumer prices in India went up 6.07 percent year-on-year in July of 2016. It was

the highest figure since August of 2014, as food cost rose further.

Higher inflation affects the purchasing power of consumers. Higher inflation is

usually negative for aviation sector.

http://www.tradingeconomics.com/india/inflation-cpi

2. Employment:

Unemployment rate in India as on 14th August, 2016 was 9.3 % - Urban (11.4%)

Rural (8.3%).

Decrease in unemployment rates affects the overall economy positively.

http://unemploymentinindia.cmie.com/

3. Growing Middle Class Income:

India’s economic growth and rising disposable income of the middle class is

expected to create significant demand for passenger air travel.

9 | P a g e

Impact –

Growth in economy will increase the Per Capita National Income (for FY 2014-15 it

stood at Rs. 86879) and Per Capita Disposable Income (for FY 2014-15 it stood at

Rs. 58208; based on 30% average personal tax rate) which can have a positive

impact on LCC.

http://pib.nic.in/newsite/PrintRelease.aspx?relid=136214

Increasing inflation may affect the purchasing power of consumers thereby

discouraging them to use LCC.

Increase in middle class income will lead to demand for LCC as more number of

people will option for flying than use railways in order to save time.

SOCIAL FACTORS:

1. Attitude to Work & Leisure:

Changing attitudes towards work and leisure has helped LCC to grab on the

changing trend. People no more use air travel as luxury but more as a necessity to

save time.

2. Security Issues & Terrorism:

Recent terrorist attacks on Brussels Airport & Istanbul Ataturk Airport has

questioned the safety of air travel. Under these circumstances, it is of paramount

importance that airlines as well as airports and all other players in the airline

industry improve their safety standards and ramp up their security checks.

3. Population Demographics:

It has been noted that ‘Age’ and ‘Income’ are two very important factors that affect

the demand for air travel. 64% of India’s population is in 15-59 age group. Also,

35.4% are in lower middle class bracket while 11.4% are in upper middle class

bracket. This certainly means there is a huge potential to be tapped by LCC in India.

Impact –

Changing attitude will help LCC to cash on the changing trend by using various

innovative strategies and thereby increase their topline.

Attacks on airport creates fear in the mind of people and may have a slight impact

on the demand for LCC but the regular users seem unfazed.

The population demographics on India is such that 64% of it is in the 15-59 age

group. Young people prefer air travel.

10 | P a g e

TECHNOLOGICAL FACTORS:

Technology has been a cornerstone of aviation industry ever since the dawn of aviation –

commencing with the conquering of ‘flights’ to becoming a key enabler for

communications, business innovation, and business models.

Indian LCC are upgrading their technology in order to face the stiff competition in

the already competitive industry.

This includes using software to optimize flight planning for minimum fuel burning

routes and altitudes and also by making use of latest fuel saving technology.

New technologies at airports like advance baggage handling system, accepting

mobile boarding pass on a passenger’s smartphone, notifications of schedule

changes are being published in real time to passenger, etc.

Impact –

Fuel saving technologies will reduce the cost and increase profitability.

Increase in customer satisfaction.

LEGAL FACTORS:

In the recent past, a number of legal changes have been implemented in India, such

as minimum wage increase, increase in FDI, liberalization of aviation sector from

the shackles of cumbersome taxes and laws, etc.

The cabinet has cleared new civil aviation policy which replaced 5/20 condition

with 0/20 rule which means any airline with 20 planes in its fleet can go for

international flights.

Impact –

Entry of more airlines (especially foreign LCC) is expected.

Indian LCC can now fly on international routes without waiting for 5 years.

Increase in FDI will help the domestic LCC with capital and technological know-

how.

ENVIRONMENTAL FACTORS:

The environmental impact of aviation occurs because aircraft engines emit heat, noise,

particulates and gases which contribute to climate change and global warming. The global

aviation industry produces 2% of all human induced CO2 emissions. Alternative fuels,

particularly sustainable biofuels, have been identified as excellent candidates for helping

achieve the industry target of reducing 50% of the emissions by 2050.

11 | P a g e

INTRODUCTION TO COMPANIES

Particular Indigo SpiceJet Jet Airways

Commenced On 8th April 2006; 10

years ago

23 May 2005; 11

years ago

5th May 1993; 23

years ago

Founder Rakesh Gangwal and

Rahul Bhatia

Ajay Singh Naresh Goyal

Destinations 40 (35 Domestic & 5

abroad)

41 (35 Domestic & 6

abroad)

68 (48 Domestic & 20

abroad)

Headquarters Gurgaon, India Gurgaon, India Mumbai, India

Fleet

(Aircraft)

Airbus 320-200

Airbus 320 neo

(109 aircrafts)

Boeing737-700

Boeing737-800

Boeing737-900ER

Bombardier Dash 8

Q400

(36 aircraft)

Airbus A330-200/300

ATR 72-500/600

Boeing 737-900ER

(116 aircraft)

Services Offers only economy

class

Offers economy class

& Spice Max Class

(extra legroom,

premium economy)

Offers 3 classes:

First Class

Premiere Class

Economy Class

Vision To be India’s largest

and fastest growing

airline through 3

things:

Affordable

fares

On time

performance

and

Hassle free

travel

experience

To ensure that flying

is no longer only for

CEO’s and business

travelers, but for

everyone.

Organization vision is

to become the “best

airline in the world’’

and to come in the top

5 preferred airlines.

Mission To provide quality

and reliable air travel

facilities to the young,

price conscious, first

time travelers.

To become India’s

preferred low-cost

airline, delivering the

lowest air fares with

the highest consumer

value, to price

sensitive consumers

Most preferred

domestic airline in

India.

12 | P a g e

SWOT ANALYSIS OF THE COMPANIES

JET AIRWAYS

STRENGTHS

Trusted Airline by the Corporates

Biggest Indian Airline company

with over 13,000 employees

Operations in over 75 Indian

cities and over 400 flights daily

WEAKNESSES

Competition from the LCC’s and

other competitors means market

share growth is tough

OPPORTUNITIES

Has presence in every segment

Increasing number of people

opting to travel by airlines

THREATS

Fuel cost makes up 40% of

operating expenses which is

going up gradually, labor aviation

regulations, etc.

Unfavorable Govt. policies and

aviation regulations

INDIGO AIRLINES

STRENGTHS

Strong backing of the promoters

and is one of the largest low cost

carriers in India

Only LCC to make consistent

profits

Good advertising has increased its

brand recall

WEAKNESSES

Does not fly to as many routes as

its competitors

Still has to establish itself on

international destinations

OPPORTUNITIES

Opening up of International

routes

Largest Market share among

LCC’s in Indian Market

Middle class taking to the skies

THREATS

Fuel cost makes up 40% of

operating expenses which is

going up gradually, labor aviation

regulations, etc.

Plenty of new LCC’s to compete

with

13 | P a g e

SPICEJET AIRLINES

STRENGTHS

Has a reach to around 35 Indian

destinations

LCC segment is ever growing in

the country

One of the largest low cost

carriers in India

WEAKNESSES

Low market share due to presence

of significant competition

Has limited destinations and no

international presence

OPPORTUNITIES

Middle class taking it to the skies

International tie-ups would boost

the brand image and reach

THREATS

Fuel cost makes up 40% of

operating expenses which is

going up gradually, labor aviation

regulations, etc.

Strong competition in LCC

segment

14 | P a g e

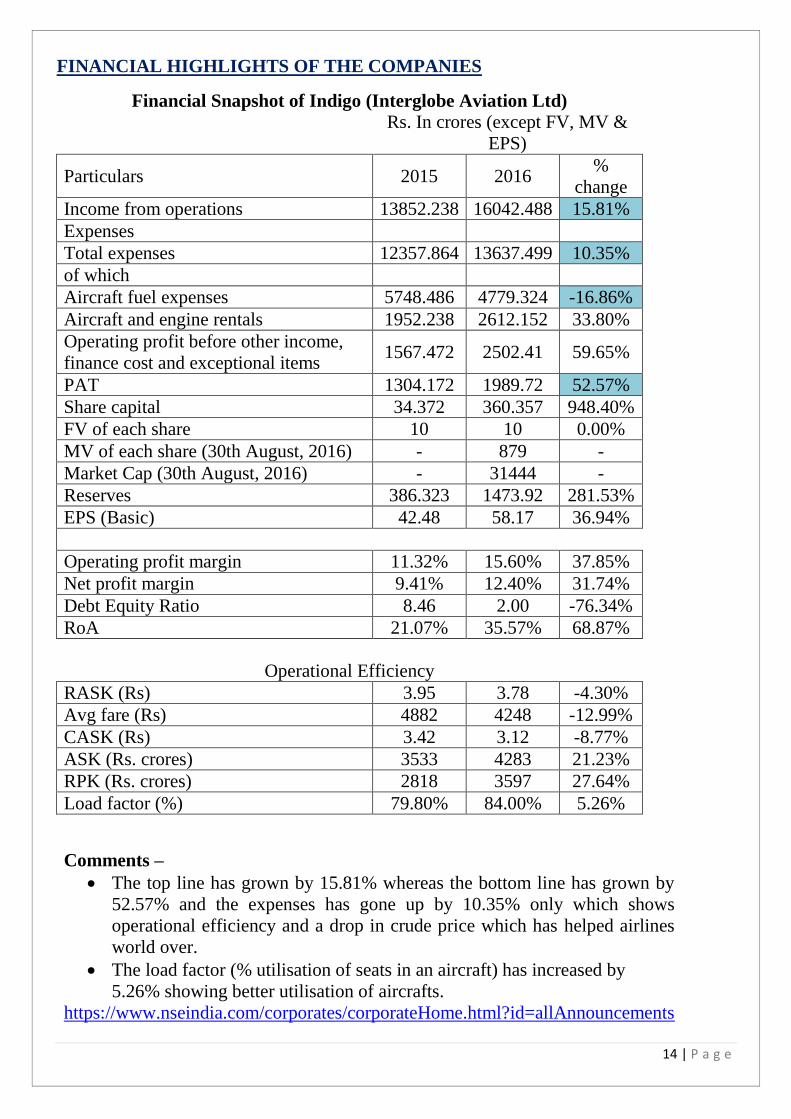

FINANCIAL HIGHLIGHTS OF THE COMPANIES

Financial Snapshot of Indigo (Interglobe Aviation Ltd)

Rs. In crores (except FV, MV &

EPS)

Particulars 2015 2016 %

change

Income from operations 13852.238 16042.488 15.81%

Expenses

Total expenses 12357.864 13637.499 10.35%

of which

Aircraft fuel expenses 5748.486 4779.324 -16.86%

Aircraft and engine rentals 1952.238 2612.152 33.80%

Operating profit before other income,

finance cost and exceptional items 1567.472 2502.41 59.65%

PAT 1304.172 1989.72 52.57%

Share capital 34.372 360.357 948.40%

FV of each share 10 10 0.00%

MV of each share (30th August, 2016) - 879 -

Market Cap (30th August, 2016) - 31444 -

Reserves 386.323 1473.92 281.53%

EPS (Basic) 42.48 58.17 36.94%

Operating profit margin 11.32% 15.60% 37.85%

Net profit margin 9.41% 12.40% 31.74%

Debt Equity Ratio 8.46 2.00 -76.34%

RoA 21.07% 35.57% 68.87%

Operational Efficiency

RASK (Rs) 3.95 3.78 -4.30%

Avg fare (Rs) 4882 4248 -12.99%

CASK (Rs) 3.42 3.12 -8.77%

ASK (Rs. crores) 3533 4283 21.23%

RPK (Rs. crores) 2818 3597 27.64%

Load factor (%) 79.80% 84.00% 5.26%

Comments –

The top line has grown by 15.81% whereas the bottom line has grown by

52.57% and the expenses has gone up by 10.35% only which shows

operational efficiency and a drop in crude price which has helped airlines

world over.

The load factor (% utilisation of seats in an aircraft) has increased by

5.26% showing better utilisation of aircrafts.

https://www.nseindia.com/corporates/corporateHome.html?id=allAnnouncements

15 | P a g e

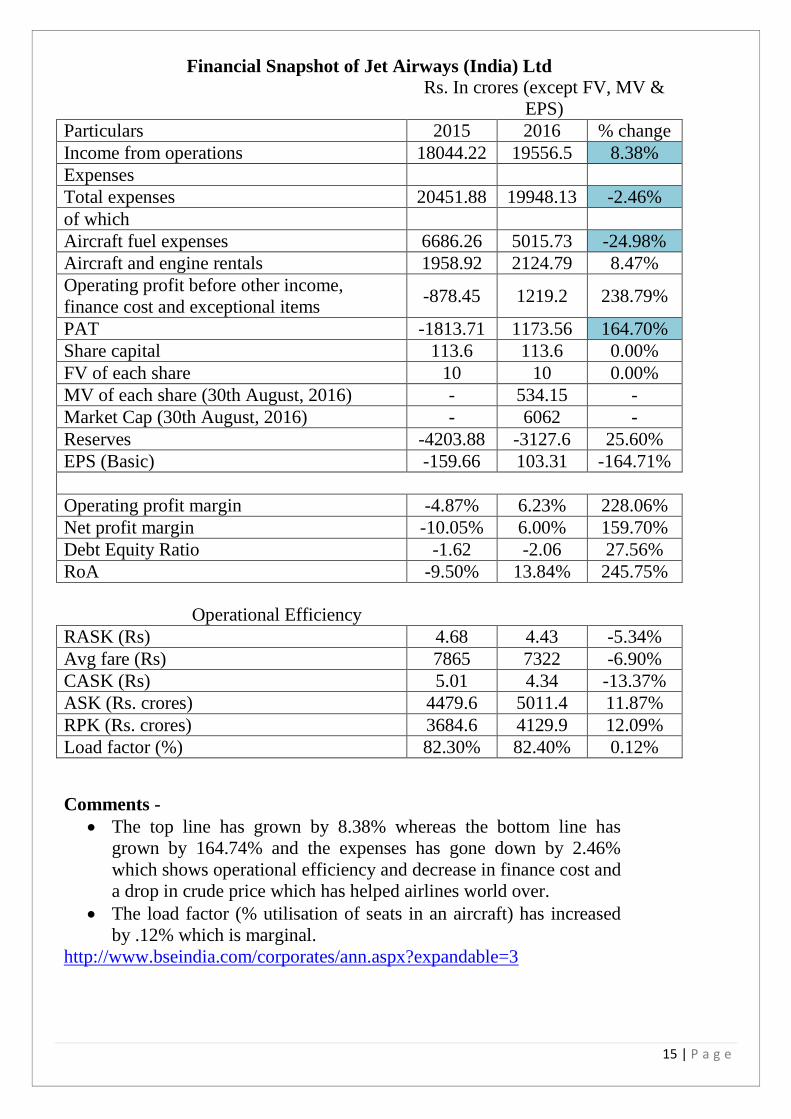

Financial Snapshot of Jet Airways (India) Ltd

Rs. In crores (except FV, MV &

EPS)

Particulars 2015 2016 % change

Income from operations 18044.22 19556.5 8.38%

Expenses

Total expenses 20451.88 19948.13 -2.46%

of which

Aircraft fuel expenses 6686.26 5015.73 -24.98%

Aircraft and engine rentals 1958.92 2124.79 8.47%

Operating profit before other income,

finance cost and exceptional items -878.45 1219.2 238.79%

PAT -1813.71 1173.56 164.70%

Share capital 113.6 113.6 0.00%

FV of each share 10 10 0.00%

MV of each share (30th August, 2016) - 534.15 -

Market Cap (30th August, 2016) - 6062 -

Reserves -4203.88 -3127.6 25.60%

EPS (Basic) -159.66 103.31 -164.71%

Operating profit margin -4.87% 6.23% 228.06%

Net profit margin -10.05% 6.00% 159.70%

Debt Equity Ratio -1.62 -2.06 27.56%

RoA -9.50% 13.84% 245.75%

Operational Efficiency

RASK (Rs) 4.68 4.43 -5.34%

Avg fare (Rs) 7865 7322 -6.90%

CASK (Rs) 5.01 4.34 -13.37%

ASK (Rs. crores) 4479.6 5011.4 11.87%

RPK (Rs. crores) 3684.6 4129.9 12.09%

Load factor (%) 82.30% 82.40% 0.12%

Comments -

The top line has grown by 8.38% whereas the bottom line has

grown by 164.74% and the expenses has gone down by 2.46%

which shows operational efficiency and decrease in finance cost and

a drop in crude price which has helped airlines world over.

The load factor (% utilisation of seats in an aircraft) has increased

by .12% which is marginal.

http://www.bseindia.com/corporates/ann.aspx?expandable=3

16 | P a g e

Financial Snapshot Spicejet Ltd

Rs. In crores (except FV, MV

& EPS)

Particulars 2015 2016 %

change

Income from operations 5172.734 5020.396 -2.95%

Expenses

Total expenses 5986.376 4773.505 -20.26%

of which

Aircraft fuel expenses 2409.622 1391.959 -42.23%

Aircraft and engine rentals 864.388 805.447 -6.82%

Operating profit before other income,

finance cost and exceptional items -743.311 314.567 142.32%

PAT -748.409 343.505 145.90%

Share capital 599.45 599.45 0.00%

FV of each share 10 10 0.00%

MV of each share (30th August, 2016) - 58.2 -

Market Cap (30th August, 2016) - 3486 -

Reserves -

2214.467

-

1810.162 18.26%

EPS (Basic) -13.38 4.36 -

132.59%

Operating profit margin -14.37% 6.27% 143.60%

Net profit margin -14.47% 6.84% 147.29%

Debt Equity Ratio -1.03 -1.46 41.81%

RoA -43.37% 19.63% 145.27%

Operational Efficiency

RASK (Rs) 3.75 4.1 9.33%

Avg fare (Rs) 3824 3598 -5.91%

CASK (Rs) 4.22 3.79 -10.19%

ASK (Rs. crores) 1456.5 1290.9 -11.37%

RPK (Rs. crores) 1187.1 1174.7 -1.04%

Load factor (%) 81.00% 91.00% 12.35%

Comments –

The top line has gone down by -2.95% whereas the bottom line has grown by

145.90% and the expenses has gone down by 20.26% which shows operational

efficiency a drop in crude price which has helped airlines world over.

The load factor (% utilisation of seats in an aircraft) has increased by 12.35% which

is marginal.

https://www.nseindia.com/corporates/corporateHome.html?id=allAnnouncements

17 | P a g e

21.07%

-9.50%

-43.37%

35.57%

13.84%19.63%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

Indigo Jet Airways Spice Jet

Operating profit margin (in %)

2014-15 2015-16

9.41%

-10.05%

-14.47%

12.40%

6.00% 6.84%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Indigo Jet Airways Spice Jet

Net profit margin (in %)

2014-15 2015-16

21.07%

-9.50%

-43.37%

35.57%

13.84% 19.63%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

Indigo Jet Airways Spice Jet

RoA (in %)

2014-15 2015-16

18 | P a g e

STRATEGIES USED BY COMPANIES

Pricing Strategies –

Comparison of Ticket Price (One-way trip, Cheapest possible rates, Inclusive of taxes)

All figures in Rs.

Route Indigo Spicejet Jet Airways

Mumbai – Delhi 3170 3450 3870

Mumbai – Chennai 2450 2950 3150

Mumbai – Kolkata 4650 5130 5270

Mumbai – Bengaluru 2450 3250 2800

Mumbai – Hyderabad 2300 2550 2250

Mumbai – Cochin 2950 4000 5000

Mumbai – Ahmedabad 2300 2450 1700

Mumbai - Goa 2450 2500 2650

o All the rates are obtained from the websites of the respective airlines and

reflect one-week prior booking rates.

o Rates are subject to changes.

Comments –

i. It is observed that Indigo provides cheapest rates for almost all the areas

served.

ii. Jet Airways has the highest ticket prices but it also provides food and other

amenities.

iii. Spicejet is in the middle with average ticket pricing and adds on like extra leg

space, food, etc.

INDIGO AIRLINES:

It is a ‘No Frills’ airline i.e. it does not provide any luxury but does its work of

transporting people from one place to another safely and on time.

They have only 1 type of Aircraft (A-320-232) which results in greater flexibility by

using the same crew from pilots to flights attendants.

They also avoid the D-Check which is done after every 8 years of operations by

leasing the aircrafts for 5-6 years and new renewal later on. This mean no airplane

remains out of service at any time.

They use latest fuel saving technologies to reduce the cost of operations.

They also don’t provide meals during short distance flights (1.5 hours or less).

19 | P a g e

SPICEJET:

Spice Jet has started using ‘Pricing Stimulation’ as well as ‘Dual Fleet’ strategies.

Under ‘Pricing Stimulation’, Spicejet provides steep discounts to frequent users as

well as non-users in order to grab the market share.

It is also reducing maintenance cost to boost profitability.

Spicejet is also using dual fleet strategy where Bombardier Q400 aircraft are being

used for high frequency shorter routes while Boeing 737 aircraft are being used for

long distance routes with more passengers.

JET AIRWAYS:

A strategic partnership with ETIHAD Airways provides Jet with new codeshares

and additional capital.

Jet Airways provides economical as well as luxury class travel to its customer,

hence, executives prefer Jet Airways.

The profitability of Jet has soared on the back of low fuel prices.

Jet has one of the highest aircraft utilization rate at 12.7 hours a day.

Jet Airways has started cost cutting program and focused on improving results

by not entering the discount war led by Spicejet.

Marketing Strategies -

JET AIRWAYS

INDIGO

SPICEJET

20 | P a g e

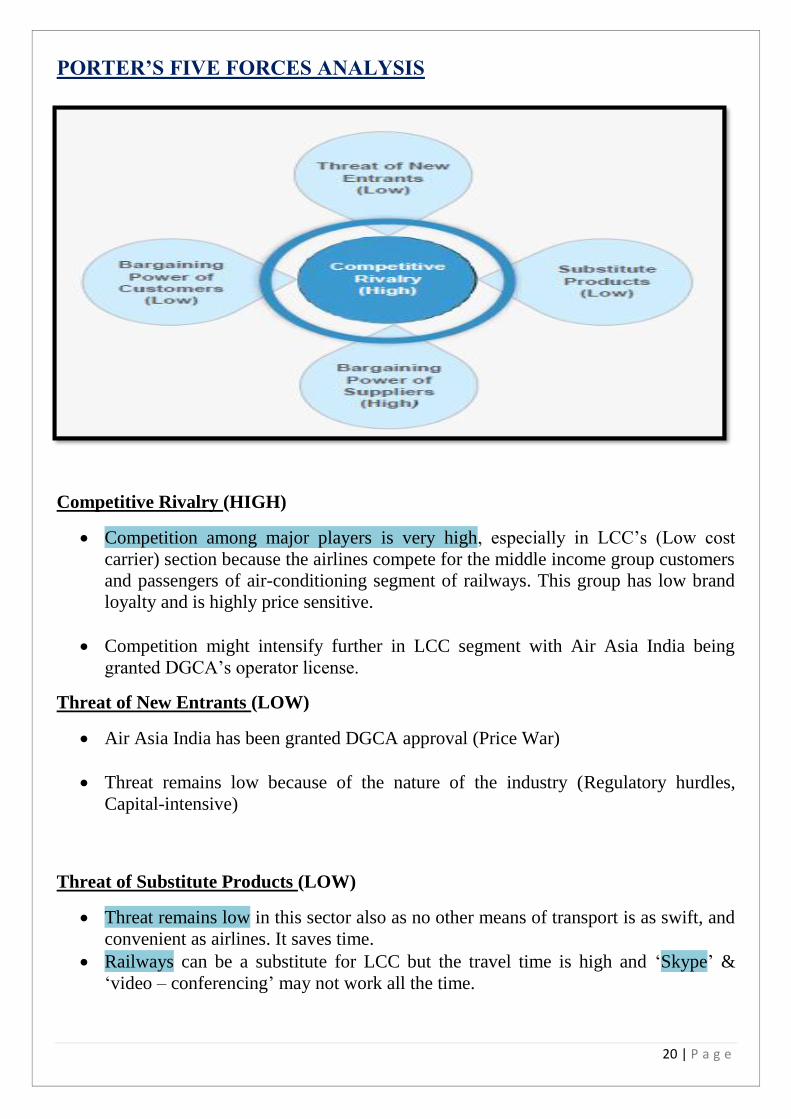

PORTER’S FIVE FORCES ANALYSIS

Competitive Rivalry (HIGH)

Competition among major players is very high, especially in LCC’s (Low cost

carrier) section because the airlines compete for the middle income group customers

and passengers of air-conditioning segment of railways. This group has low brand

loyalty and is highly price sensitive.

Competition might intensify further in LCC segment with Air Asia India being

granted DGCA’s operator license.

Threat of New Entrants (LOW)

Air Asia India has been granted DGCA approval (Price War)

Threat remains low because of the nature of the industry (Regulatory hurdles,

Capital-intensive)

Threat of Substitute Products (LOW)

Threat remains low in this sector also as no other means of transport is as swift, and

convenient as airlines. It saves time.

Railways can be a substitute for LCC but the travel time is high and ‘Skype’ &

‘video – conferencing’ may not work all the time.

21 | P a g e

Bargaining Power of Suppliers (HIGH)

Bargaining power of suppliers remain high as there are only few fuel and aircraft

suppliers.

Talent pool of pilots, engineers and other staff is also limited.

Bargaining Power of Customers (LOW)

Bargaining power of customers remains low as the demand for low cost air travel is

quite high.

The costs of switching airplanes and services offered hardly differ with each other.

Source: Source: Central Asia-Pacific Aviation, TechSci Research

Note: *(Notes w.r.t airlines)

KANO MODEL –

Attributes Indigo Spicejet Jet Airways

Basic 1.Flight won’t be

cancelled

2.Guaranteed seat

3.Transporting safely

from destination A to

B

1.Flight won’t be

cancelled

2.Guaranteed seat

3.Transporting safely

from destination A to

B

1.Flight won’t be

cancelled

2.Guaranteed seat

3.Transporting safely

from destination A to

B

Performance 1.No frills

2.On time service

3.Cheap fare

4.Comfortable seats

1.No frills

2.More legroom for

Spice Max class

3.Average fare

1.Services like food

and entertainment

2.All three classes

available i.e.

Economy, First,

Business.

3.Comparatively

higher fare

Delight 1.Festive offers

2.Food of very good

quality and tasty (for

flights > 1.5 hours)

3.Cabin crew is very

warm and punctual

1.Festive offers

2.Loyalty points

1.Exotic dining

experience

2.Premium services

like more legroom,

beautiful ambience,

etc.

22 | P a g e

LEARNINGS –

Indigo is ruling the Indian skies and will continue to do so, at least in near future.

Indigo was able to break even in the 3rd year of its operations, a feat in itself, and

has been profitable ever since, a claim few can boast of.

All this has been possible because of the strategic plans implemented by the

management like using a single type of aircraft, going for top quality executives,

having single ‘Economy’ class seats, having maintenance contracts with Airbus so

as to keep the safety standards high, etc.

Under the new management, Spicejet is looking for turnaround and its going strong

with back to back profits in all the quarters of FY 2015-16.

With deep discounting strategies, its gaining market share of other players.

Spicejet is also paying off its debt to reduce the interest cost.

Jet Airways had a spectacular FY 2015-16 as it managed to post net profit after 5

years and has been aggressive with its own strategies.

Partnership with Etihad has boosted the balance sheet and Jet Airways is trying to

grab the premium segment by providing luxurious services.

It is also paying off its loan in order to reduce its huge interest cost.

In an industry where profit margins are thin, INDIGO remains ‘the king’ whereas

SPICEJET is ‘the dark horse’ catching up with the leaders and JET AIRWAYS ‘the

knight’ that has a presence not only in domestic market, but also in international

market.

23 | P a g e

RECOMMENDATIONS –

To Airlines-

Airlines should not indulge in unethical practices like increasing air fare during

festive seasons to exorbitant levels.

All safety standards should be strictly adhered to as per international standards.

Crew members should be regularly trained on customer service.

Passengers should be compensated properly in case of flight delays.

Passengers should be kept updated regarding their schedule.

Cost cutting measures should be implemented to boost profitability.

To Government and Regulatory Authority –

Taxes should be rationalized.

Taxes on aviation fuel and services need to be reduced in order to make Indian LCC

competitive in international market.

DGCA should take speedy decisions on licensing of operators.

Budget food stalls should be opened on airports.

Airport infrastructure in non-metro cities needs to be improved.

Consumer complaint redressal should be quick and appropriate.

Regulatory hurdles should be removed.

CONCLUSION –

We conclude that, an industry bogged by heavy taxes and regulatory hurdles, stiff

competition and thin profit margins, no customer loyalty yet high customer expectations, it

is a classic case of survival of the fittest and INDIGO is leading the pack on all the fronts.

But it must be noted that under the new management, Spicejet has managed to shut its

doomsayers, and become profitable once again. Jet Airways is also catching up to its rivals

and with the liberalization of regulations under new aviation policy, new LCC are entering

the market increasing the competition and putting pressure on the profit margin.

Time will tell who won in the ‘Clash for the Indian skies’.

24 | P a g e

REFERENCES –

http://www.india-aviation.in/pages/view/38/an_overview.html

http://www.tradingeconomics.com/india/inflation-cpi

http://www.mapsofindia.com/my-india/business/in-indias-burgeoning-aviation-sector-

safety-is-the-key-word

http://www.livemint.com/Companies/HbO0mmX9bimghBtdHR10iK/Air-traffic-expands-

21-in-April-Jet-slips-on-market-share.html

http://www.taxindiaonline.com/RC2/inside2.php3?filename=bnews_detail.php3&newsid=

2152

http://www.tradingeconomics.com/india/inflation-cpi

All the financial data was sourced from - BSE India, NSE India, and respective websites

of the company.

http://www.bseindia.com/corporates/ann.aspx?expandable=3

https://www.nseindia.com/corporates/corporateHome.html?id=allAnnouncements

Glossary

LCC Low cost carrier

RASK Revenue per Available Seat Kilometer

CASK Cost per Available Seat Kilometer

ASK Available Seat Kilometers

RPK Revenue passenger Kilometers

DGCA Directorate General of Civil Aviation