Embed Size (px)

DESCRIPTION

all about banking

Citation preview

Casco, Malamion, Rama 1

BANKING INSTITUTIONSBank of the Philippine Islands (BPI)

December 10, 2013

Casco, Malamion, Rama 2

Philippine Banking SystemHistory of Banks in the PhilippinesHistory of Bank of the Philippine Islands

INTRODUCTION

December 10, 2013

Casco, Malamion, Rama 3

PHILIPPINE BANKING SYSTEM

The Philippine banking system continued to deliver a remarkable performance in 2012 amid the ongoing fragilities in the global financial landscape on sustained implementation of deep reforms particularly on ensuring greater stability of the domestic banking system.

December 10, 2013

Casco, Malamion, Rama 4

PHILIPPINE BANKING SYSTEM During 2012, there were 9,410 operating

banks consisting of 696 head offices and 8,714 branches and other offices.

Banks accounted for 34.7% (unchanged) of all financial institution under the effective supervision of the Bangko Sentral ng Pilipinas. The slight increase in share was due to the increase in the number of bank branches during the year.

December 10, 2013

Casco, Malamion, Rama 5

BANKING HISTORY

Obras Pias - first organized credit institutions.

1869 opening of the Suez Canal facilitated trade

between the Philippines and Europe. Chartered Bank of India, Australia and China

(now known as the Standard Chartered Bank) and the Hong Kong and Shanghai Banking Corporation (HSBC) opened their respective branches in Manila.

December 10, 2013

Casco, Malamion, Rama 6

BANKING HISTORY 1883

Madrid-based Banco Peninsular Ultamarino also established a branch in the country; but ceased operations after four years.

End of the Spanish regime El Banco Español Filipino de Isabel (now the Bank

of Philippine Islands or BPI), which was given the sole mandate under a Spanish Royal Decree of 1854 to issue banknotes called Pesos Fuertes;

the Chartered Bank of India, a branch of the HSBC;

the Monte de Piedad;and the Banco Peninsular Ultamarino de Madrid.

December 10, 2013

Casco, Malamion, Rama 7

BANKING HISTORY During the American colonial period

American Bank was first to open a branch in 1901.

20th century the Americans established the Guaranty

Trust Corporation (GTC) and International Banking Corporation (IBC)

1918 Manila branch of the Yokohama Specie

Bank was given a license to do business in the Philippines.

December 10, 2013

Casco, Malamion, Rama 8

BANKING HISTORY 1919 – 1930

Asia Banking Corporation, the Chinese-American Bank of Commerce of Peking, China, and the National City Bank of New York opened branches in the Philippines.

Bank of the Philippine Islands was the only significant bank controlled by local interests.

Philippine National Bank (PNB) was established in 1916 with the Philippine Government as the majority stockholder. It empowered the PNB to issue bank notes and act as a depositary of government funds.

December 10, 2013

Casco, Malamion, Rama 9

BANKING HISTORY During the Commonwealth period (1935-

1946) Bank of Taiwan and the Nederlandsche Indische

Handelsbanks were established in the Philippines.

1939 government created the Agricultural and

Industrial Bank Philippine Bank of Communications: first bank

with genuine Filipino private capital; temporarily closed at the outbreak of the Second World War.

only Filipino-owned and Japanese banks were allowed to operate during World War II.

December 10, 2013

Casco, Malamion, Rama 10

BANKING HISTORY 1942

Nampo Kaihatsu Kinko (or the Southern Development Bank) opened a Manila branch

1945 National City Bank of New York: granted

the first license to reopen. Chartered Bank of India, Australia, and

China, HSBC, and Nederlandsche Indische Handelsbanks were likewise granted the license to reopen.

December 10, 2013

Casco, Malamion, Rama 11

BANKING HISTORY 1947

Bank of America, NT & SA (Bank of America) of San Francisco, California, was allowed to establish a branch in Manila.

1949 Central Bank of the Philippines started its

operations, the banking system consisted of seven commercial banks, three thrift banks, the sole government specialized bank, the Agricultural and Industrial Bank, and seven foreign bank branches.

December 10, 2013

Casco, Malamion, Rama 12

BANKING HISTORY General Banking Act (GBA) became

effective on January 3, 1949. 1952

Rural Banks Act was enacted. 1954

Agricultural and Industrial Bank merged with the Reconstruction and Rehabilitation Fund to form the Development Bank of the Philippines (DBP).

Law on Secrecy of Bank Deposits which discouraged private hoarding by encouraging the public to deposit their money in banking institutions.

December 10, 2013

Casco, Malamion, Rama 13

BANKING HISTORY 1963

created the Philippine Deposit Insurance Commission (PDIC).

1971 Joint International Monetary Fund-Central

Bank of the Philippines Banking Survey Commission was created. The Commission studied the banking system and proposed several measures that resulted in the promulgation of Presidential Decree Nos. 71 (amending the General Banking Act) and 72 (amending the Central Bank Act).

December 10, 2013

Casco, Malamion, Rama 14

BANKING HISTORY 1980s

significant circular issued by the Central Bank was Circular No. 905 (issued in 1983), which lifted the interest rate ceilings imposed by the Usury Law.

1990s classified into foreign exchange

liberalization, financial liberalization, and the passage of the General Banking Law of 2000.

2000s Republic Act 8791, the General Banking Law

of 2000, was enacted.

December 10, 2013

Casco, Malamion, Rama 15

BANK OF THE PHILIPPINE ISLANDS HISTORY

1828 A first attempt to establish a colonial

bank when King Ferdinand VII called for the creation of a public bank in the Philippines.

1829 Urbiztondo established the bank in the

Royal Custom House in the fortress town of Intramuros.

Named the bank El Banco Español Filipino de Isabel 2 in honor of the reigning queen of Spain.

December 10, 2013

Casco, Malamion, Rama 16

BANK OF THE PHILIPPINE ISLANDS HISTORY

1852 granted the authority to issue pesos

fuertes, or 'strong pesos,’ the first paper money in the Philippines.

Bank changed its name after Isabel II was dethroned in 1869, becoming more simply El Banco Español Filipino.

1897 Banco Español Filipino opened its first

branch office, Iloilo. December 10, 2013

Casco, Malamion, Rama 17

BANK OF THE PHILIPPINE ISLANDS HISTORY

1912 While the change in the company's

name--authorized in 1907--came only this year, it nevertheless adopted the name of Bank of the Philippine Islands (BPI).

opened its second branch office in Zamboanga.

1949 BPI lost its money-issuing privileges

altogether. BPI was converted to a private bank.

December 10, 2013

Casco, Malamion, Rama 18

BANK OF THE PHILIPPINE ISLANDS HISTORY

1969 Bank's relationship with the Ayala family

and businesses strengthened after Ayala Corporation took a majority share in BPI.

1974 Much of BPI's growth came through a

stream of acquisitions with its purchase of the Peoples Bank and Trust Company.

December 10, 2013

Casco, Malamion, Rama 19

BANK OF THE PHILIPPINE ISLANDS HISTORY

1982 BPI acquired Commercial Bank and Trust

Company, which specialized in the middle market, in 1981.

Purchase of Ayala Investment and Development Corporation.

acquired Philsec, boosting its new investment banking wing, and Makati Leasing and Financing. The latter purchase helped strengthen its own leasing arm, which was launched in 1980 and made BPI the first Philippine bank to offer leasing facilities.

December 10, 2013

Casco, Malamion, Rama 20

BANK OF THE PHILIPPINE ISLANDS HISTORY

1984 The People's Development Bank

acquisition formed the basis of BPI's new subsidiary, BPI Agricultural Bank.

1985 Company added Family Bank, at the

time a major mortgage and savings bank in the Philippines.

Purchase of Asian International Bank, based in New York.

December 10, 2013

Casco, Malamion, Rama 21

BANK OF THE PHILIPPINE ISLANDS HISTORY

1981 first in the country to offer access

via Automated Teller Machines (ATM). 1983

Express Teller system, the first in the country to provide 24-hour access to banking services.

1987 introduced the Philippines first debit-

card system.December 10, 2013

Casco, Malamion, Rama 22

BANK OF THE PHILIPPINE ISLANDS HISTORY

1991 introduced its Express Banking Centers.

1995 purchase of First Cavite Savings.

1996 adding CityTrust Banking Corporation.

1998 launched a 24-hour call center providing

a broad range of banking services over the telephone.

December 10, 2013

Casco, Malamion, Rama 23

BANK OF THE PHILIPPINE ISLANDS HISTORY 1999

BPI began talks for a three-way merger with two other prominent Filipino banks, FarEast Bank and Trust Company and Union Bank.

In November 1999 FarEast agreed to be acquired by BPI for $1.2 billion.

2000 first Filipino bank to launch its own online bank,

BPI Direct. acquired FGU Insurance Corporation, Universal

Reinsurance Corporation, Ayala Life Assurance, Ayala Health Care and Ayala Plans.

Philippines' first "bancassurance" company.

December 10, 2013

Casco, Malamion, Rama 24

BANK OF THE PHILIPPINE ISLANDS HISTORY

2001 FGU merged with FEB Mitsui Marine,

creating BPI/MS Insurance Corporation. 2003

BPI spun off its re-insurance operations into a merger with Malayan Reinsurance Corporation, forming Universal Malayan Reinsurance Corporation.

Bought up DBS Bank Philippines.

December 10, 2013

Casco, Malamion, Rama 25

BANK OF THE PHILIPPINE ISLANDS HISTORY

One of the most financially sound of all Philippine banks, posting steady increases in its net earnings despite the Asian economic crisis that occurred in the early 2000s.

After more than 150 years in existence, BPI remained a top player in the Philippines banking market.

December 10, 2013

Casco, Malamion, Rama 26December 10, 2013

Casco, Malamion, Rama 27

Entities that Introduce Funds into the Economy

Bank Organization and Operation

Classification of Banks

Number and Types of Banks Supervised by BSP

Functions of a Bank

Minimum Capitalization Requirement

List of Banks

Laws and Circulations

Bangko Sentral ng Pilipinas (BSP)

Monetary Board

Philippine Depository Insurance Corporation

“Close Now, Hear Later” Scheme

Reserves

Bank of the Philippine Islands Products and Services

Bank of the Philippine Islands Subsidiaries

OVERVIEW OF PHILIPPINE BANKING INDUSTRY

December 10, 2013

Casco, Malamion, Rama 28

ENTITIES THAT INTRODUCE FUNDS INTO THE ECONOMY

Banks Entities engaged in the lending of funds obtained in

the form of deposits. Quasi – Banks

Entities engaged in the borrowing of funds through the issuance, endorsement or assignment with recourse or acceptance of deposit substitutes.

Financial Intermediaries Persons or entities whose principal functions include

the lending, investing or placement of funds on evidences of indebtedness or equity deposited with them, acquired by them or otherwise coursed through them, either for their own account or for the account of others.

December 10, 2013

Casco, Malamion, Rama 29

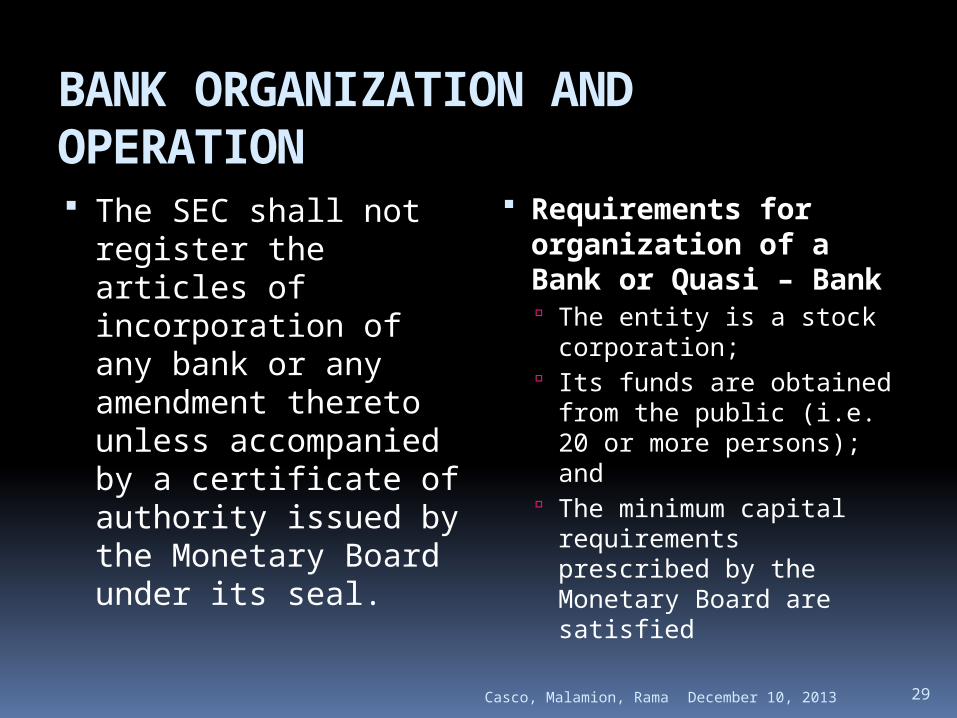

BANK ORGANIZATION AND OPERATION The SEC shall not

register the articles of incorporation of any bank or any amendment thereto unless accompanied by a certificate of authority issued by the Monetary Board under its seal.

Requirements for organization of a Bank or Quasi – Bank The entity is a stock

corporation; Its funds are obtained

from the public (i.e. 20 or more persons); and

The minimum capital requirements prescribed by the Monetary Board are satisfied

December 10, 2013

Casco, Malamion, Rama 30

CLASSIFICATION OF BANKS Universal Banks

Primarily governed by the General Banking Law (GBL), can exercise the powers of an investment house and invest in non-allied enterprises and have the highest capitalization requirement.

Commercial Banks Ordinary banks

governed by the GBL which have a lower capitalization requirement than universal banks and can neither exercise the powers of an investment house nor invest in non-allied enterprises.December 10, 2013

Casco, Malamion, Rama 31

CLASSIFICATION OF BANKS Thrift Banks

These are a) Savings and

mortgage banks; b) Stock savings and

loan associations; c) Private

development banks, which are primarily governed by the Thrift Banks Act

Rural Banks Mandated to make

needed credit available and readily accessible in the rural areas on reasonable terms and which are primarily governed by the Rural Banks Act of 1992.

December 10, 2013

Casco, Malamion, Rama 32

CLASSIFICATION OF BANKS Cooperative

Banks majority shares are

owned and controlled by cooperatives primarily to provide financial and credit services to cooperatives. It shall include cooperative rural banks. They are governed primarily by the Cooperative Code.

Islamic Banks Banks whose

business dealings and activities are subject to the basic principles and rulings of Islamic Shari’ a, such as the Al Amanah Islamic Investment Bank of the Philippines which was created by RA 6848.December 10, 2013

Casco, Malamion, Rama 33

NUMBER AND TYPES OF BANKS SUPERVISED BY BSP

December 10, 2013

Casco, Malamion, Rama 34

NUMBER AND TYPES OF BANKS SUPERVISED BY BSP

December 10, 2013

Casco, Malamion, Rama 35

FUNCTIONS OF A BANK Deposit Loan and Discount Exchange Trust Advisory

December 10, 2013

Casco, Malamion, Rama 36

MINIMUM CAPITALIZATION REQUIREMENT

December 10, 2013

Casco, Malamion, Rama 37

LIST OF BANKS

Universal Banks Commercial Banks Bank of the Philippine Islands BDO Unibank, Inc. Deutsche Bank AG Development Bank of the

Philippines East West Banking

Corporation Land Bank of the Philippines Philippine National Bank Security Bank Corporation Standard Chartered Bank The Hongkong & Shanghai

Banking Corporation

Asia United Bank Corporation

Bank of America, N. A. Bank of Commerce BDO Private Bank, Inc. Citibank, N. A. JP Morgan Chase Bank, N.

A. Korea Exchange Bank Maybank Philippines, Inc. Philippine Bank of

Communications Philippine Veterans Bank

December 10, 2013

Casco, Malamion, Rama 38

LIST OF BANKS

Thrift Banks Rural Banks Allied Savings Bank Bataan Development Bank BDO Elite Savings Bank, Inc. BPI Direct Savings Bank, Inc. BPI Family Savings Bank, Inc. BPI Globe BanKo, Inc., A

Savings Bank China Bank Savings, Inc. Citibank Savings, Inc. City Savings Bank, Inc. Equicom Savings Bank, Inc.

Liberty Bank (A Rural Bank), Inc.

Lipa Bank, Inc. (A Rural Bank)

Maharlika Rural Bank, Inc. Malaybalay Rural Bank,

Inc. Rural Bank of Bustos, Inc.

December 10, 2013

Casco, Malamion, Rama 39

LIST OF BANKS

Cooperative Banks Offshore Banking Units in the Philippines

Bataan Cooperative Bank Bukidnon Cooperative

Bank Cooperative Bank of

Aurora Cooperative Bank of

Cagayan Cooperative Bank of Cebu

BNP Paribas J. P. Morgan International

Finance, Limited Taiwan Cooperative Bank

December 10, 2013

Casco, Malamion, Rama 40

LAWS AND CIRCULATIONS

General Banking Laws

Special Banking Laws

General Banking Law (R.A. No. 8791)

New Central Bank Act (R.A. No. 7653)

New Rural Banks Act (R.A. No. 7353)

Private Development Banks Act (R.A. No. 4093)

Savings and Loan Association Act (R.A. No. 3779)

Thrift Banks Act (R.A. No. 7906)

December 10, 2013

Casco, Malamion, Rama 41

LAWS AND CIRCULATIONS

Secrecy of Bank Deposits Law (R.A. No. 1405)

Unclaimed Balances Law (Act No. 3936)

Philippine Deposit Insurance Corporation Act (R.A. No. 3591)

Anti – Money Laundering (RA 9194)

Foreign Currency Deposit Act (R.A. No. 6426) December 10, 2013

Casco, Malamion, Rama 42

BANGKO SENTRAL NG PILIPINAS (BSP) It is the central bank of the Republic

of the Philippines. Established on 3 July 1993 pursuant to

the provisions of the 1987 Philippine Constitution and the New Central Bank Act of 1993.

The BSP enjoys fiscal and administrative autonomy from the National Government in the pursuit of its mandated responsibilities.

December 10, 2013

Casco, Malamion, Rama 43

BANGKO SENTRAL NG PILIPINAS (BSP) Primary objectives:

To maintain price stability conducive to a balanced and sustainable growth of the economy.

To promote and maintain monetary stability and the convertibility of the peso.

Responsibilities: To provide policy directions in the areas of money,

banking, and credit To supervise bank operations To regulate the operations of finance companies and

non-bank financial institutions performing quasi-banking functions, and similar institutions (Sec. 3)

December 10, 2013

Casco, Malamion, Rama 44

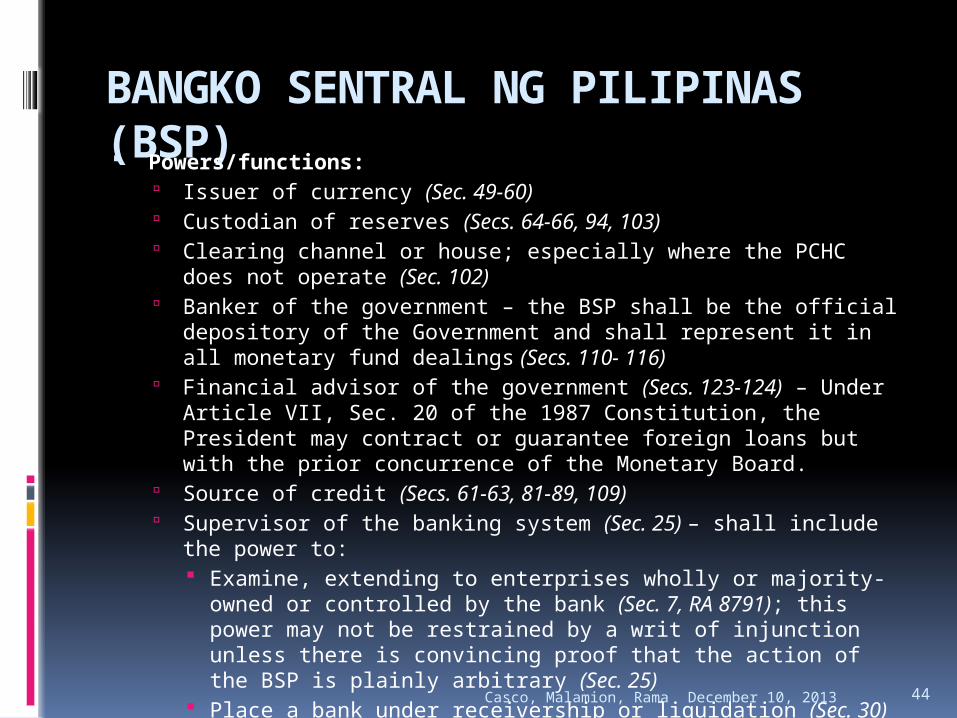

BANGKO SENTRAL NG PILIPINAS (BSP) Powers/functions:

Issuer of currency (Sec. 49-60) Custodian of reserves (Secs. 64-66, 94, 103) Clearing channel or house; especially where the PCHC does not

operate (Sec. 102) Banker of the government – the BSP shall be the official depository

of the Government and shall represent it in all monetary fund dealings (Secs. 110- 116)

Financial advisor of the government (Secs. 123-124) – Under Article VII, Sec. 20 of the 1987 Constitution, the President may contract or guarantee foreign loans but with the prior concurrence of the Monetary Board.

Source of credit (Secs. 61-63, 81-89, 109) Supervisor of the banking system (Sec. 25) – shall include the

power to: Examine, extending to enterprises wholly or majority-owned or

controlled by the bank (Sec. 7, RA 8791); this power may not be restrained by a writ of injunction unless there is convincing proof that the action of the BSP is plainly arbitrary (Sec. 25)

Place a bank under receivership or liquidation (Sec. 30) Initiate criminal prosecution of erring officers of banks

Government agent (Secs. 117-122)

December 10, 2013

Casco, Malamion, Rama 45

MONETARY BOARD The body by which the powers and functions

of the Bangko Sentral are exercised.

Composition: Seven (7) members consisting of:

Chairman: Governor of the BSP A member of the cabinet to be designated

by the President of the Philippines Five (5) members who shall come from the

private sector, all of whom shall serve full-time.

December 10, 2013

Casco, Malamion, Rama 46

PHILIPPINE DEPOSITORY INSURANCE CORPORATION

PDIC is a government – run Philippine insurance fund. It was established on June 22, 1963 by Republic Act 3591. It guarantees increasing maximum deposit insurance coverage to P500, 000.

December 10, 2013

Casco, Malamion, Rama 47

“Close Now, Hear Later” Scheme Sec. 29 of the Central Bank Act does not

contemplate prior notice and hearing before a bank is placed under receivership. It is enough that such action is made the subject of a subsequent judicial review. The purpose of the scheme is to protect the depositors, creditors, stockholders and general public (Central Bank vs. CA, 220 SCRA 536).

Only stockholders representing the majority of the capital stock of a bank have the personality to file a petition for certiorari to be filed within 10 days from receipt by the board of directors of the institution of the order directing receivership, liquidation or conservatorship.

December 10, 2013

Casco, Malamion, Rama 48

RESERVES any part of stockholders' equity,

except for basic share capital. Reserves are amounts that are retained in the business and not distributed to the owners.

December 10, 2013

Casco, Malamion, Rama 49

RESERVES

Primary reserves Secondary reserves

The minimum amount of cash required to operate a bank. Primary reserves also include the legal reserves that are housed in a Federal Reserve or other correspondent bank. Checks that have not been collected are included in this amount as well.

Assets that are invested in safe, marketable, short-term securities such as Treasury bills when the demand for loans is low. Secondary reserves provide a supplemental measure of low-risk liquidity. They earn interest and can be useful in adjusting a bank's reserve totals.

December 10, 2013

Casco, Malamion, Rama 50

RESERVES

Investment reserves It is used to identify any assets that an

investor or a company have held in check to cover losses incurred when certain investments contained in the portfolio experience some sort of downturn in value. One of the more common examples of an investor making use of an investment reserve is an insurance company.

December 10, 2013

Casco, Malamion, Rama 51

BANK OF THE PHILIPPINE ISLANDS PRODUCTS AND SERVICES

PRODUCTS SERVICES

Deposit Loans Credit Cards ATM/ Debit Cards Prepaid and Gift Cards Remittance Asset Management Insurance Pre – need

Online Banking Phone Banking Mobile Banking Branch Banking ATM Banking Express Deposit

Machines Bills Payment Foreign Exchange

December 10, 2013

Casco, Malamion, Rama 52

BANK OF THE PHILIPPINE ISLANDS SUBSIDIARIES

December 10, 2013

Casco, Malamion, Rama 53

Financial Reporting RequirementsManual of AccountsAccounting Entries

ACCOUNTING OF BANKING INSTITUTIONS

December 10, 2013

Casco, Malamion, Rama 54

BANK OF THE PHILIPPINE ISLANDS ACCOUNTING STANDARDS/ GUIDELINES

The BPI Group adopted the following amendments to existing standards and interpretations approved by the FRSC which are effective for the BPI Group beginning January 1, 2012:

PAS 12 (Amendment), Income Taxes - Deferred Tax (effective January 1, 2012)

PFRS 7 (Amendment), Financial Instruments: Disclosures - Derecognition (effective July 1, 2011)

December 10, 2013

Casco, Malamion, Rama 55

BANK OF THE PHILIPPINE ISLANDS ACCOUNTING STANDARDS/ GUIDELINES

New standards, amendments and interpretations to existing standards that are not yet effective and not early adopted by the BPI Group PAS 1 (Amendment), Financial Statement Presentation

- Other Comprehensive Income (effective July 1, 2012) PAS 19 (Amendment), Employee Benefits (effective

January 1, 2013) PAS 28 (Revised), Investments in Associates and Joint

Ventures (effective January 1, 2013) PAS 32 (Amendment), Financial Instruments:

Presentation – Asset and Liability Offsetting (effective January 1, 2014).

December 10, 2013

Casco, Malamion, Rama 56

BANK OF THE PHILIPPINE ISLANDS ACCOUNTING STANDARDS/ GUIDELINES

New standards, amendments and interpretations to existing standards that are not yet effective and not early adopted by the BPI Group PFRS 9, Financial Instruments (effective January

1, 2015). PFRS 10, Consolidated Financial Statements

(effective January 1, 2013) PFRS 12, Disclosures of Interests in Other

Entities (effective January 1, 2013) PFRS 13, Fair Value Measurement (effective

January 1, 2013)

December 10, 2013

Casco, Malamion, Rama 57

IAS 30 - Disclosures in the Financial Statements of Banks and Similar Financial Institutions

Objective of IAS 30

The objective of IAS 30 is to prescribe appropriate presentation and disclosure standards for banks and similar financial institutions (hereafter called 'banks'), which supplement the requirements of other Standards. The intention is to provide users with appropriate information to assist them in evaluating the financial position and performance of banks, and to enable them to obtain a better understanding of the special characteristics of the operations of banks.

December 10, 2013

Casco, Malamion, Rama 58

IAS 30 - Disclosures in the Financial Statements of Banks and Similar Financial Institutions Presentation and disclosure

A bank's income statement should group income and expenses by nature. [IAS 30.9]

A bank's income statement or notes should report the following specific amounts: [IAS 30.10] interest income interest expense dividend income fee and commission income fee and commission expense net gains/losses from securities dealing net gains/losses from investment securities net gains/losses from foreign currency dealing other operating income loan losses general administrative expenses other operating expenses.

December 10, 2013

Casco, Malamion, Rama 59

IAS 30 - Disclosures in the Financial Statements of Banks and Similar Financial Institutions

A bank's balance sheet should group assets and liabilities by nature and list them in liquidity sequence. [IAS 30.18] IAS 30.19 sets out the specific line items requiring disclosure.

IAS 30.13 and IAS 30.23 include guidelines for the limited circumstances in which income and expense items or asset and liability items are offset.

A bank must disclose the fair values of each class of its financial assets and financial liabilities as required by IAS 32 and IAS 39. [IAS 30.24]

December 10, 2013

Casco, Malamion, Rama 60

IAS 30 - Disclosures in the Financial Statements of Banks and Similar Financial Institutions

Disclosures are also required about: specific contingencies and commitments

(including off-balance sheet items) requiring disclosure [IAS 30.26]

specified disclosures for the maturity of assets and liabilities [IAS 30.30]

concentrations of assets, liabilities and off-balance sheet items [IAS 30.40]

losses on loans and advances [IAS 30.43] general banking risks [IAS 30.50] assets pledged as security [IAS 30.53].

December 10, 2013

Casco, Malamion, Rama 61

MANUAL OF ACCOUNTS – Statement of Financial Position

Asset Accounts Cash on hand Checks and other cash

items (COCI) Due from Bangko Sentral ng

Pilipinas (BSP) Due from Other Banks Financial Assets Held for

Trading (HFT) Financial Assets Designated

at Fair Value through Profit or Loss (DFVPL)

Available-for-Sale (AFS) Financial Assets

Held-to-Maturity (HTM) Financial Assets

Investments in Non-Marketable Equity Securities (INMES)

Loans and Receivables Sales Contract Receivable (SCR) Equity Investment in

Subsidiaries, Associates and Joint Venture

Bank Premises, Furniture, Fixture and Equipment

Real and Other Properties Acquired (ROPA)

Non-Current Assets Held for Sale

Goodwill Deferred Tax Asset Other Assets

December 10, 2013

Casco, Malamion, Rama 62

MANUAL OF ACCOUNTS – Statement of Financial Position

Liability Accounts

Deposit Liabilities Financial Liabilities Held

for Trading Financial Liabilities

Designated at Fair Value through Profit or Loss (DFVPL)

Due to Other Banks Bills Payable Bonds Payable Derivatives Liabilities Unsecured Subordinated

Debt (USD)

Margin Deposits on Letters of Credit

Due to Bangko Sentral ng Pilipinas (BSP)

Due to Philippine Deposit Insurance Corporation (PDIC)

Income Tax Payable Other Taxes and Licenses

Payable Accrued Other Expenses Unearned Income Other LiabilitiesDecember 10, 2013

Casco, Malamion, Rama 63

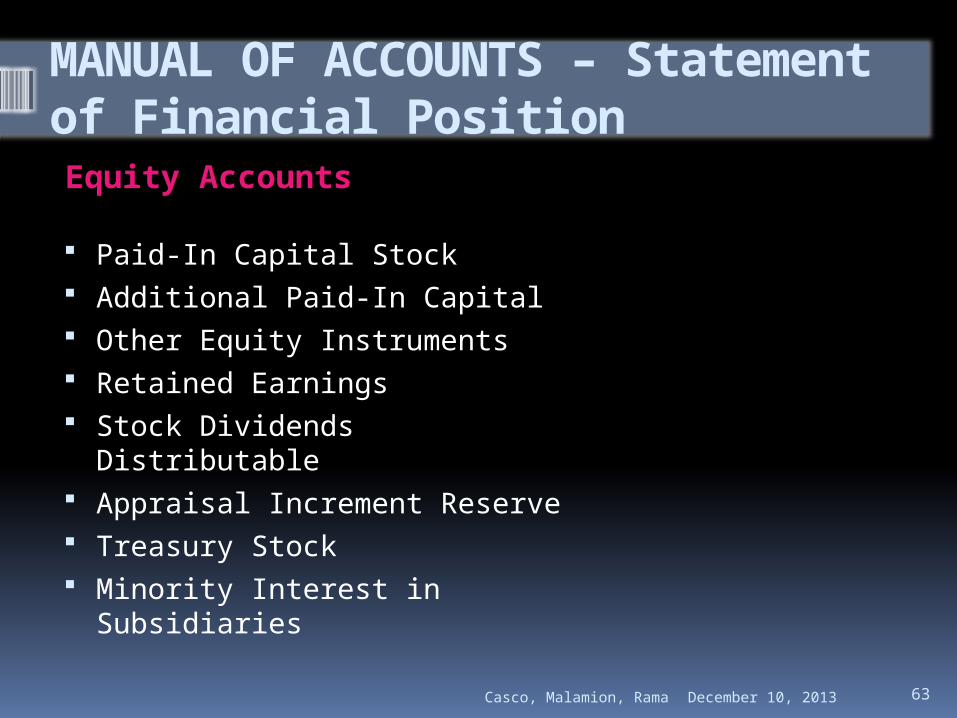

MANUAL OF ACCOUNTS – Statement of Financial PositionEquity Accounts

Paid-In Capital Stock Additional Paid-In Capital Other Equity Instruments Retained Earnings Stock Dividends

Distributable Appraisal Increment Reserve Treasury Stock Minority Interest in

SubsidiariesDecember 10, 2013

Casco, Malamion, Rama 64

MANUAL OF ACCOUNTS – Statement of Financial Performance Interest Income Interest Expense Provision for Losses on

Accrued Interest Income from Financial Assets

Dividend Income Fees and Commissions Income Gains/(Losses) on Financial

Assets and Liabilities Held for Trading (HFT)

Gains/(Losses) on Financial Assets and Liabilities Designated at Fair Value through Profit or Loss (DFVPL)

Foreign Exchange Profit/(Loss) Gains/(Losses) from Fair Value

Adjustment in Hedge Accounting

Gains/(Losses) from Sale/Derecognition of Non-Financial Assets

Other Income Compensation/Fringe Benefits Taxes and Licenses Fees and Commissions

Expenses Other Administrative

Expenses Depreciation/Amortization Recovery on Charged-Off

Assets Share in the Profit/(Loss) of

Unconsolidated Subsidiaries Share in the Profit/(Loss) of

Joint Ventures Income Tax Expense

December 10, 2013

Casco, Malamion, Rama 65

BANK’S CAPITAL IS DIVIDED INTO:TIER 1 CAPITAL TIER 2 CAPITAL A term used to

describe the capital adequacy of a bank.

It is a core capital, this includes equity capital and disclosed reserves.

Includes instruments that can't be redeemed at the option of the holder.

It is a supplementary bank capital that includes items such as revaluation reserves, undisclosed reserves, hybrid instruments and subordinated term debt.

December 10, 2013

Casco, Malamion, Rama 66

Computation:

Tier 1 Capital = Permanent shareholders’ equity + Disclosed reserves (including retained earnings) – Goodwill

Tier 2 Capital = General provisions/general loan-loss reserves + Revaluation reserves + Hybrid (debt/equity) capital instruments + Subordinated term debt+ Undisclosed reserves – Investments in unconsolidated financial subsidiaries – Investments in the capital of other financial institutions

December 10, 2013

Casco, Malamion, Rama 67

ACCOUNTING ENTRIESDEPOSIT (Liability Account)

Cash DepositCash

XXXDeposit Account

XXX

December 10, 2013

Casco, Malamion, Rama 68

ACCOUNTING ENTRIES Check Deposit Due from BSP XXX

Deposit AccountXXX

Deposit Account (issuer) XXXDeposit Account (depositor)

XXX

Manager’s Check XXXDeposit AccountXXX

December 10, 2013

Casco, Malamion, Rama 69

ACCOUNTING ENTRIESLOANS / RECEIVABLES

In CashLoan Account Receivable

XXXManager’s Check

XXX

Credited in the Current AccountLoan Account Receivable

XXXDeposit Account – Manager

XXX

December 10, 2013

Casco, Malamion, Rama 70

ACCOUNTING ENTRIES Interbank Loans

Interbank Loan Receivable XXXDue from BSP XXX

Collections for Payment of LoansCash (Deposit Account) XXX

Loan Account Receivable XXX

December 10, 2013

Casco, Malamion, Rama 71

ACCOUNTING ENTRIES Inward

Due from Foreign Bank XXXDeposit Account (remitter) XXX

OutwardDeposit Account (remitter) XXX

Due from Foreign Bank XXX

December 10, 2013

Casco, Malamion, Rama 72

ACCOUNTING ENTRIESPAYMENT MADE BY CREDITOR TO

SETTLE HIS ACCOUNT

Other Banks’ Checks Due from BSP XXX

Accounts Payable XXX

Due from BSP XXXDeposit Account XXX

December 10, 2013

Casco, Malamion, Rama 73

ACCOUNTING ENTRIES On-us Checks Deposit Account (issuer) XXX

Accounts PayableXXX

Deposit Account (issuer) XXXDeposit AccountXXX

December 10, 2013

Casco, Malamion, Rama 74

ACCOUNTING ENTRIESINTEREST EARNED ON THE DEPOSIT

Interest Expense XXXDeposit Account

XXX

December 10, 2013

Casco, Malamion, Rama 75

ACCOUNTING ENTRIESLOANS GRANTED BY A FOREIGN

CURRENCY DEPOSIT UNIT TO THE BSP

Loans to BSP XXXCash on Hand

XXX

December 10, 2013