Embed Size (px)

Citation preview

FINA

RELIA

PROBLEMS WITH

EXPENSE

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ANCIAL STATEME

ABILITY UNDER IF

PROBLEMS WITH

EXPENSE RECOGNITION

Dr Jacek Welc:

0

: Problems with Expense Recognition

ENT

FRS:

PROBLEMS WITH

RECOGNITION

Dr Jacek Welc:

RECOGNIZING EXPENSES

RELATED TO INVENTORY AND

RECEIVABLE ACCOUNTS

Financial Statement Reliability under IFRS: Problems with Expense Recognition

PART 1:

RECOGNIZING EXPENSES

RELATED TO INVENTORY AND

RECEIVABLE ACCOUNTS

1

: Problems with Expense Recognition

RECOGNIZING EXPENSES

RELATED TO INVENTORY AND

RECEIVABLE ACCOUNTS

ACCOUNTING FOR INVENTORY

According to IAS 2 (Inventory),

historical cost (either a purchase or a production).

Par. 10 of IAS 2 specifies three components of inventory cost:

���� Costs of purchase,

���� Costs of conversion,

���� Other costs incurred in bringing the inventories to their present location and condition.

Par. 11 of IAS 2 states that the

and other taxes (other than those subsequently recoverable by t

authorities), transport, handling and other costs directly attributable to the acquisition of

finished goods, materials and services.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

FOR INVENTORY UNDER IFRS

), inventories are accounted for primarily on the basis of their

(either a purchase or a production).

Par. 10 of IAS 2 specifies three components of inventory cost:

Other costs incurred in bringing the inventories to their present location and condition.

Par. 11 of IAS 2 states that the costs of purchase comprise the purchase price, import duties

and other taxes (other than those subsequently recoverable by the entity from the taxing

authorities), transport, handling and other costs directly attributable to the acquisition of

finished goods, materials and services.

2

: Problems with Expense Recognition

are accounted for primarily on the basis of their

Other costs incurred in bringing the inventories to their present location and condition.

comprise the purchase price, import duties

he entity from the taxing

authorities), transport, handling and other costs directly attributable to the acquisition of

ACCOUNTING FOR INVENTORY UNDER IFRS

According to par. 12 of IAS 2, the

production (e.g. direct labor and direct m

manufacturing costs (fixed and variable production overheads) that are incurred in

converting materials into finished goods.

Inclusion of the overheads in inventory costs calls for an

into various items of inventory. However,

production levels. This means that in periods, when the production volume is unusually low,

the costs of unused capacity should be

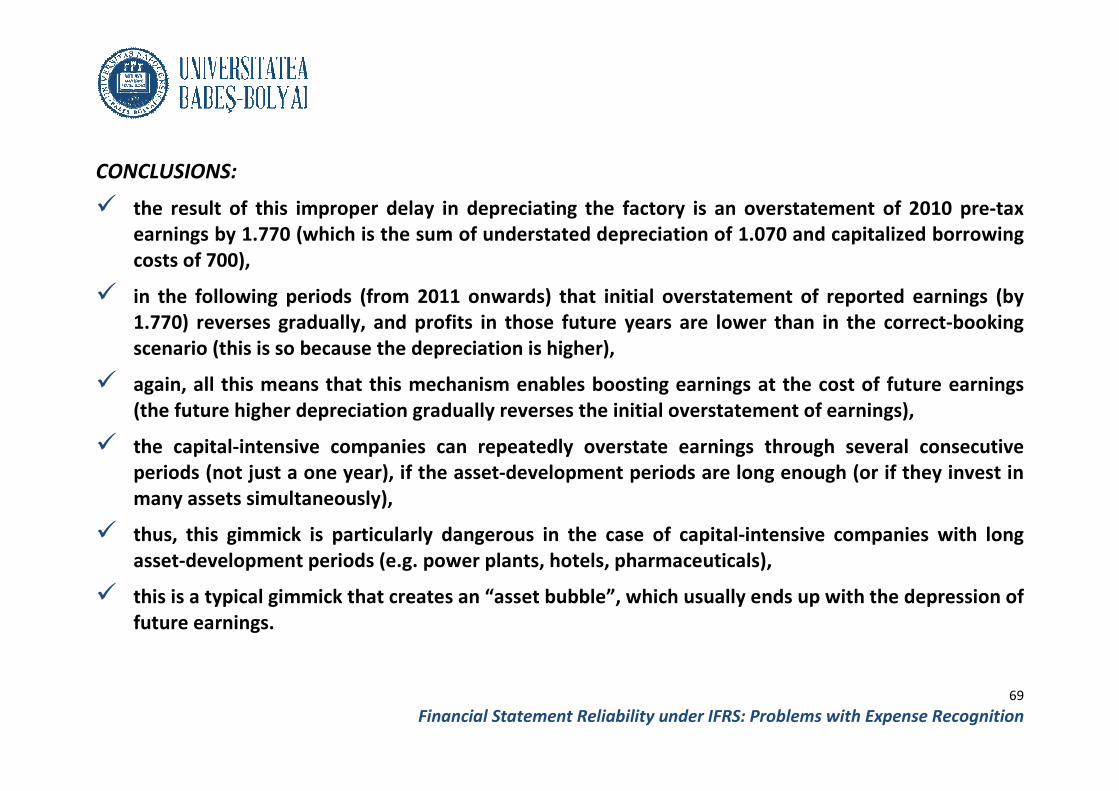

within the carrying value of inventory).

Other costs can be included in inventory only if they are incurred in bringing the inventories

to their present location and condition (e.g. some borrowing costs, related to inventories

with unusually long production periods). For example, according to par. 16 of IAS

of “inefficiencies” (e.g. abnormal amounts of wasted materials or labor)

included in the inventory cost.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR INVENTORY UNDER IFRS

According to par. 12 of IAS 2, the costs of conversion are directly related to the units of

production (e.g. direct labor and direct materials) plus a systematic

manufacturing costs (fixed and variable production overheads) that are incurred in

converting materials into finished goods.

Inclusion of the overheads in inventory costs calls for an allocation of the total overheads

into various items of inventory. However, the cost allocation should be based on

. This means that in periods, when the production volume is unusually low,

used capacity should be expensed as incurred (instead of being capitalized

within the carrying value of inventory).

can be included in inventory only if they are incurred in bringing the inventories

to their present location and condition (e.g. some borrowing costs, related to inventories

with unusually long production periods). For example, according to par. 16 of IAS

of “inefficiencies” (e.g. abnormal amounts of wasted materials or labor)

PROBLEM 1: Allocation of c

the basis of “normal produ

observable and objectively determinable

PROBLEM 1 (cont.): Misallocation (e.g. over

inventory) of those costs may result in serious distortions of

reported inventories and earnings3

: Problems with Expense Recognition

are directly related to the units of

allocation of indirect

manufacturing costs (fixed and variable production overheads) that are incurred in

of the total overheads

allocation should be based on normal

. This means that in periods, when the production volume is unusually low,

(instead of being capitalized

can be included in inventory only if they are incurred in bringing the inventories

to their present location and condition (e.g. some borrowing costs, related to inventories

with unusually long production periods). For example, according to par. 16 of IAS 2 the costs

of “inefficiencies” (e.g. abnormal amounts of wasted materials or labor) should not be

n of costs of conversion must be done on

roduction levels”, which are not directly

observable and objectively determinable

Misallocation (e.g. over-capitalization in

inventory) of those costs may result in serious distortions of

reported inventories and earnings

ACCOUNTING FOR INVENTORY UNDER IFRS

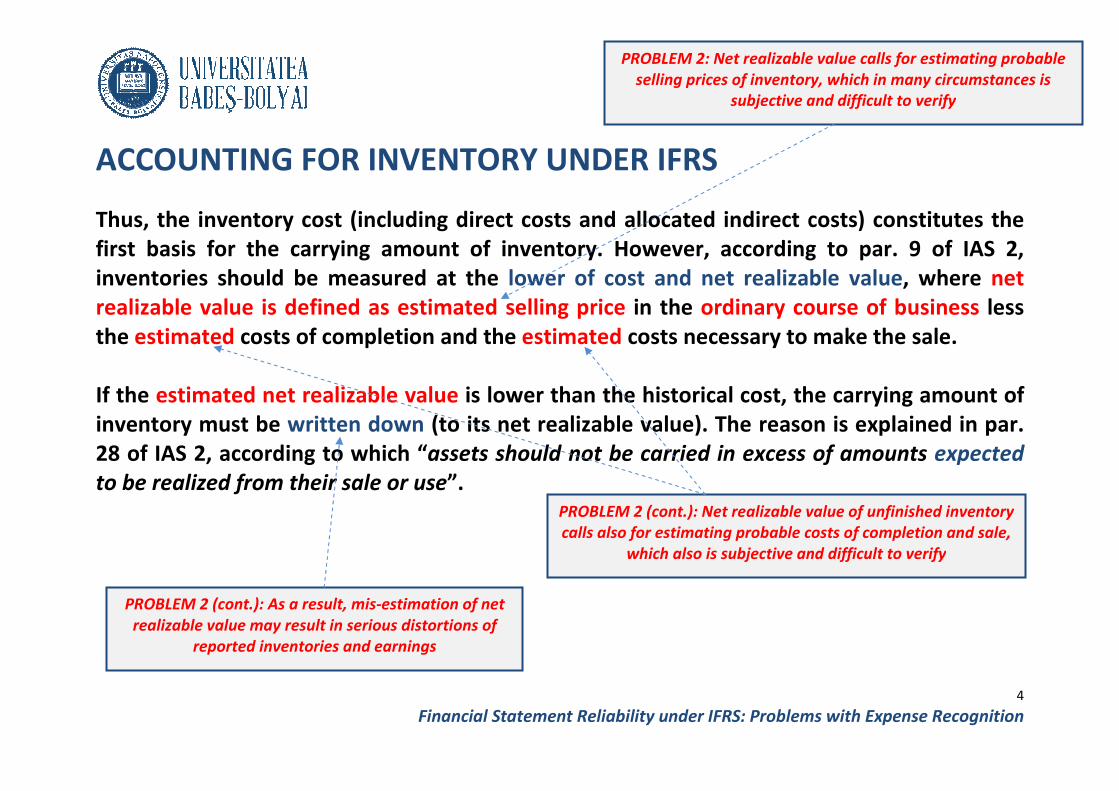

Thus, the inventory cost (including direct costs and allocated indirect costs) constitutes the

first basis for the carrying amount of inventory. However, according to par. 9 of IAS 2,

inventories should be measured at the

realizable value is defined as estimated selling price

the estimated costs of completion and t

If the estimated net realizable value

inventory must be written down

28 of IAS 2, according to which “

to be realized from their sale or use

PROBLEM 2 (cont.): As a result, mis-estimation of net

realizable value may result in serious distortions of

reported inventories and earnings

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR INVENTORY UNDER IFRS

Thus, the inventory cost (including direct costs and allocated indirect costs) constitutes the

first basis for the carrying amount of inventory. However, according to par. 9 of IAS 2,

inventories should be measured at the lower of cost and net realizable v

realizable value is defined as estimated selling price in the ordinary course of business

costs of completion and the estimated costs necessary to make the sale.

estimated net realizable value is lower than the historical cost, the carrying amount of

written down (to its net realizable value). The reason is explained in par.

28 of IAS 2, according to which “assets should not be carried in excess of amounts

to be realized from their sale or use”.

PROBLEM 2: Net realizable value calls for estimating probable

selling prices of inventory, which in many circumstanc

subjective and difficult to verify

PROBLEM 2 (cont.): Net realizable value of unfinished

calls also for estimating probable costs of completion and sale,

which also is subjective and difficult to verify

estimation of net

realizable value may result in serious distortions of

reported inventories and earnings

4

: Problems with Expense Recognition

Thus, the inventory cost (including direct costs and allocated indirect costs) constitutes the

first basis for the carrying amount of inventory. However, according to par. 9 of IAS 2,

lower of cost and net realizable value, where net

ordinary course of business less

costs necessary to make the sale.

is lower than the historical cost, the carrying amount of

ts net realizable value). The reason is explained in par.

assets should not be carried in excess of amounts expected

Net realizable value calls for estimating probable

selling prices of inventory, which in many circumstances is

subjective and difficult to verify

Net realizable value of unfinished inventory

calls also for estimating probable costs of completion and sale,

which also is subjective and difficult to verify

ACCOUNTING FOR INVENTORY UNDER IFRS

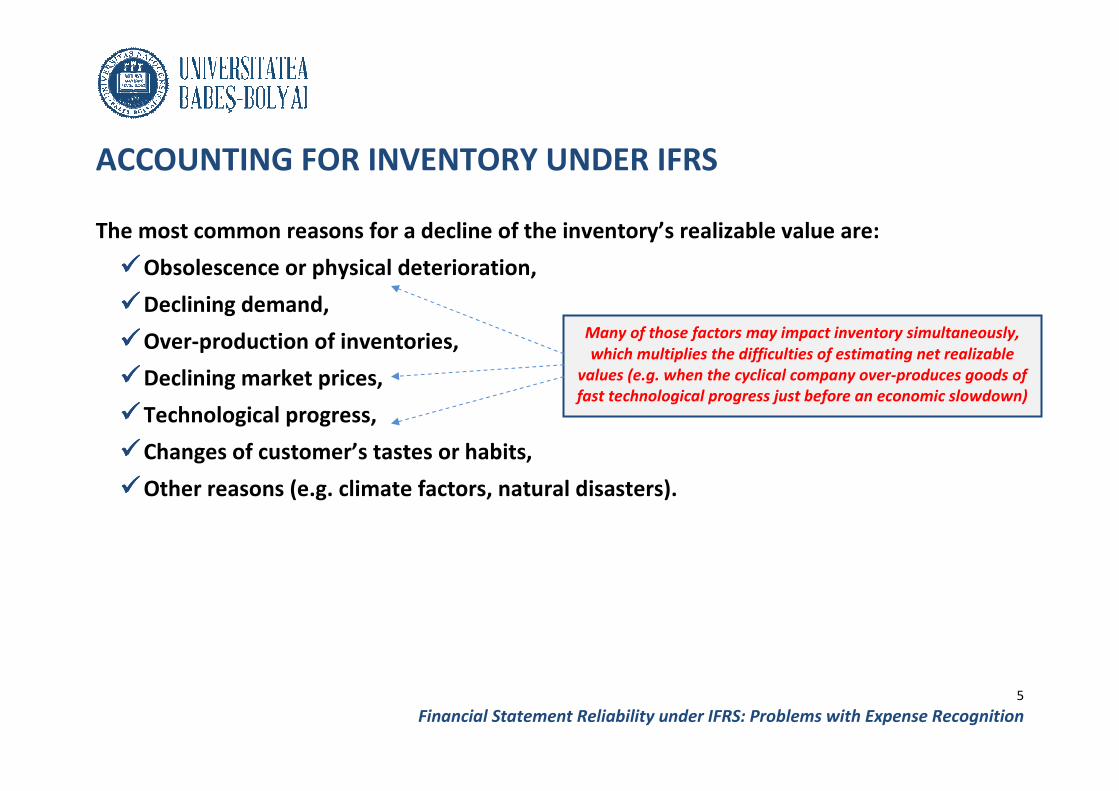

The most common reasons for a decline of the inventory’s realizable value are:

���� Obsolescence or physical deterioration,

���� Declining demand,

���� Over-production of inventories,

���� Declining market prices,

���� Technological progress,

���� Changes of customer’s tastes or habits,

���� Other reasons (e.g. climate factors

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR INVENTORY UNDER IFRS

The most common reasons for a decline of the inventory’s realizable value are:

Obsolescence or physical deterioration,

production of inventories,

Changes of customer’s tastes or habits,

Other reasons (e.g. climate factors, natural disasters).

Many of those factors may impact inventory simultaneously,

which multiplies the difficulties of estimating net realizable

values (e.g. when the cyclical company over

fast technological progress just before an economic slowdown)

5

: Problems with Expense Recognition

The most common reasons for a decline of the inventory’s realizable value are:

Many of those factors may impact inventory simultaneously,

which multiplies the difficulties of estimating net realizable

values (e.g. when the cyclical company over-produces goods of

fast technological progress just before an economic slowdown)

ACCOUNTING FOR INVENTORY UNDER IFRS

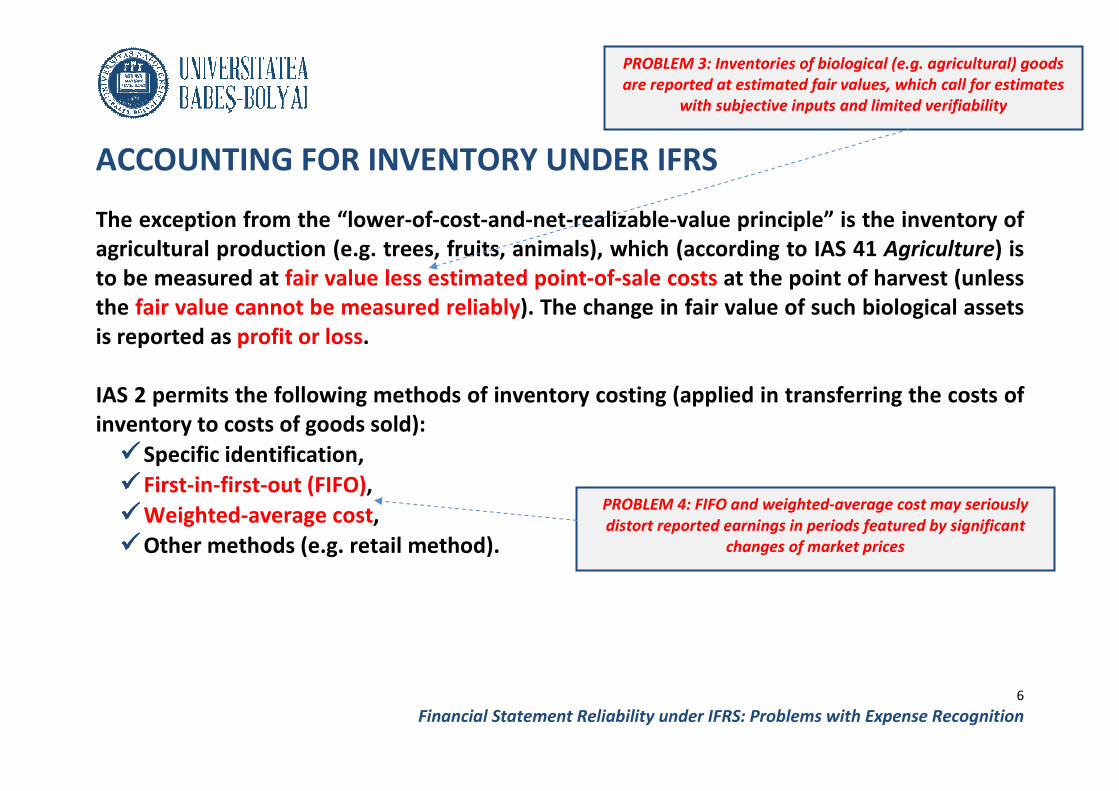

The exception from the “lower-

agricultural production (e.g. trees, fruits, animals), which (according to IAS 41

to be measured at fair value less estimated point

the fair value cannot be measured rel

is reported as profit or loss.

IAS 2 permits the following methods of inventory costing (applied in transferring the costs of

inventory to costs of goods sold):

���� Specific identification,

���� First-in-first-out (FIFO),

���� Weighted-average cost,

���� Other methods (e.g. retail method).

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR INVENTORY UNDER IFRS

-of-cost-and-net-realizable-value principle” is the inventory of

agricultural production (e.g. trees, fruits, animals), which (according to IAS 41

fair value less estimated point-of-sale costs at the point of harvest (unless

cannot be measured reliably). The change in fair value of such biological assets

IAS 2 permits the following methods of inventory costing (applied in transferring the costs of

inventory to costs of goods sold):

Other methods (e.g. retail method).

PROBLEM 3: Inventories of

are reported at estimated fair values, which call for estimates

with subjective inputs and limited verifiability

PROBLEM 4: FIFO and weighted

distort reported earnings in periods featured by significant

changes of market prices

6

: Problems with Expense Recognition

ple” is the inventory of

agricultural production (e.g. trees, fruits, animals), which (according to IAS 41 Agriculture) is

at the point of harvest (unless

). The change in fair value of such biological assets

IAS 2 permits the following methods of inventory costing (applied in transferring the costs of

Inventories of biological (e.g. agricultural) goods

are reported at estimated fair values, which call for estimates

with subjective inputs and limited verifiability

FIFO and weighted-average cost may seriously

distort reported earnings in periods featured by significant

changes of market prices

SELECTED PRACTICAL

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

���� PROBLEM 1: allocation of indirect costs of conversion, based on

production levels – if the production volume is unusually low (significantly

below the normal level), the increased unit manufacturing costs, resulting from

unused capacity, should be expensed as incurred (instead of being capitalized

in a carrying amount of inventory). If, i

such costs, it may temporarily overstate reported inventory and earnings (as

illustrated in Example 1).

directly observable and must be determined, which may be pr

companies with highly variable production volumes.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

allocation of indirect costs of conversion, based on

if the production volume is unusually low (significantly

), the increased unit manufacturing costs, resulting from

unused capacity, should be expensed as incurred (instead of being capitalized

in a carrying amount of inventory). If, in such periods, the company

such costs, it may temporarily overstate reported inventory and earnings (as

illustrated in Example 1). The problem is that normal production levels are not

directly observable and must be determined, which may be pr

companies with highly variable production volumes.

7

: Problems with Expense Recognition

PROBLEMS WITH ACCOUNTING FOR

Practical problems related to inventory, resulting directly from IFRS regulations:

allocation of indirect costs of conversion, based on normal

if the production volume is unusually low (significantly

), the increased unit manufacturing costs, resulting from

unused capacity, should be expensed as incurred (instead of being capitalized

n such periods, the company capitalizes

such costs, it may temporarily overstate reported inventory and earnings (as

The problem is that normal production levels are not

directly observable and must be determined, which may be problematic for

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

���� PROBLEM 2: estimation of

values of inventories fall below their carrying amounts

must be written down to net realizable values

an income statement).

reported inventories and earnings

illustrated in Example 2

future selling prices are not directly observable

multiple subjective inputs) and are difficult to verify

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

estimation of net realizable values – if estimated net realizable

of inventories fall below their carrying amounts, the

must be written down to net realizable values (with resulting loss reported in

. If estimated net realizable values are overstated

reported inventories and earnings will be temporarily overstated as well

2). The problem is that for many goods the probable

are not directly observable, must be estimated (often wi

multiple subjective inputs) and are difficult to verify.

8

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

Practical problems related to inventory, resulting directly from IFRS regulations:

estimated net realizable

, the carrying amounts

(with resulting loss reported in

alues are overstated, the

overstated as well (as

for many goods the probable

estimated (often with

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

���� PROBLEM 3: accounting for

agricultural industries) are reported at their

to-period changes in fair values

fair values are overstated, the reported inventories and earnings will be

temporarily overstated as well. The problem is that for many

agricultural goods (e.g. a young forest, which will be commercially marketable

far in the future, e.g. in 25

must be estimated (usually

verify.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

accounting for biological assets – the biological inventories (e.g. in

agricultural industries) are reported at their estimated fair values

period changes in fair values reported in an income statement. If estimated

are overstated, the reported inventories and earnings will be

temporarily overstated as well. The problem is that for many

(e.g. a young forest, which will be commercially marketable

far in the future, e.g. in 25-30 years) the fair values are not directly observable,

usually with multiple subjective inputs) and are difficult to

9

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

Practical problems related to inventory, resulting directly from IFRS regulations:

the biological inventories (e.g. in

fair values, with period-

reported in an income statement. If estimated

are overstated, the reported inventories and earnings will be

temporarily overstated as well. The problem is that for many unfinished

(e.g. a young forest, which will be commercially marketable

are not directly observable,

with multiple subjective inputs) and are difficult to

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting

���� PROBLEM 4: impact of FIFO and weighted

inventories and earnings

significantly and fast, and these growth

mismatch between a measurement bases for sales revenues and cost of goods

sold emerges (particularly under FIFO and when there are many “layers” of

inventories from prior purchases). This is so because sales revenues may

already reflect increased

be based on lower (old) prices from purchases made long ago.

effect is a temporary overstatement of reported earnings (which fades away

when “fresher” layers of inventories become the costs o

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Practical problems related to inventory, resulting directly from IFRS regulations

impact of FIFO and weighted-average cost on reported

inventories and earnings – when the purchase prices of inventories

and these growths are reflected in rising sales prices,

mismatch between a measurement bases for sales revenues and cost of goods

sold emerges (particularly under FIFO and when there are many “layers” of

inventories from prior purchases). This is so because sales revenues may

reflect increased (new) market prices, while cost of goods sold may still

be based on lower (old) prices from purchases made long ago.

effect is a temporary overstatement of reported earnings (which fades away

when “fresher” layers of inventories become the costs of goods sold).

10

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

directly from IFRS regulations:

average cost on reported

when the purchase prices of inventories grow

are reflected in rising sales prices, the

mismatch between a measurement bases for sales revenues and cost of goods

sold emerges (particularly under FIFO and when there are many “layers” of

inventories from prior purchases). This is so because sales revenues may

market prices, while cost of goods sold may still

be based on lower (old) prices from purchases made long ago. The resulting

effect is a temporary overstatement of reported earnings (which fades away

f goods sold).

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Other problems related to inventory (not resulting directly from IFRS)

���� PROBLEM 5: computation of unit product costs

with a mass production, the initial cost of inventory (and then the cost of goods

sold) is computed by dividing total manufacturing costs (

costs of conversion) by a production volume.

data are derived from internal do

the company deliberately (or by a mistake) overstate the

volume, the resulting unit costs will be understated (with the

understatement of cost of goods sold and related overstatement of reported

earnings), until the physical inventory count

recorded inventories.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Other problems related to inventory (not resulting directly from IFRS)

computation of unit product costs – in manufacturing industries

production, the initial cost of inventory (and then the cost of goods

sold) is computed by dividing total manufacturing costs (costs of purchase +

costs of conversion) by a production volume. However, the production volume

data are derived from internal documents (e.g. weekly production reports).

the company deliberately (or by a mistake) overstate the reported

volume, the resulting unit costs will be understated (with the

understatement of cost of goods sold and related overstatement of reported

physical inventory count detects the non

11

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

Other problems related to inventory (not resulting directly from IFRS):

in manufacturing industries

production, the initial cost of inventory (and then the cost of goods

costs of purchase +

However, the production volume

cuments (e.g. weekly production reports). If

reported production

volume, the resulting unit costs will be understated (with the following

understatement of cost of goods sold and related overstatement of reported

the non-existent but

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Other problems related to inventory (not resulting directly from IFRS)

���� PROBLEM 6: recording cost of goods sold

company records two events: recognizes revenues (with corresponding

increase in receivables or cash) and recognizes cost of goods sold associated

with the goods that were sold (with corresponding decrease in inventory). The

failure (deliberate or by e

recognizing sales revenues

expenses and overstating earnings

the non-existent but recorded inventories

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

her problems related to inventory (not resulting directly from IFRS)

recording cost of goods sold – when products are sold

company records two events: recognizes revenues (with corresponding

increase in receivables or cash) and recognizes cost of goods sold associated

with the goods that were sold (with corresponding decrease in inventory). The

(deliberate or by en error) to record costs of goods sold

revenues, results in overstating inventory, understating

expenses and overstating earnings (until the physical inventory count

existent but recorded inventories), as illustrated in Example 3.

12

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

her problems related to inventory (not resulting directly from IFRS):

hen products are sold, the

company records two events: recognizes revenues (with corresponding

increase in receivables or cash) and recognizes cost of goods sold associated

with the goods that were sold (with corresponding decrease in inventory). The

to record costs of goods sold, while

results in overstating inventory, understating

physical inventory count detects

d in Example 3.

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Other problems related to inventory (not resulting directly from IFRS)

���� PROBLEM 7: artificial sale

artificially and temporarily

a “friendly” company, it

inventories (with immediate profit

the same price (so that

company, but may bring the temporary overstatement of earnings reported

a selling company). This is illustrated in Example 4.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

INVENTORY UNDER IFRS

Other problems related to inventory (not resulting directly from IFRS)

artificial sale-and-buyback transactions – if a

and temporarily boost its reported earnings, and if

“friendly” company, it may arrange a two-way transaction

with immediate profit) and then a buyback of

(so that the transaction may be neutral for a “friendly”

company, but may bring the temporary overstatement of earnings reported

a selling company). This is illustrated in Example 4.

13

: Problems with Expense Recognition

SELECTED PRACTICAL PROBLEMS WITH ACCOUNTING FOR

Other problems related to inventory (not resulting directly from IFRS):

company wants to

and if it finds or creates

way transaction: a sale of

buyback of this inventory for

may be neutral for a “friendly”

company, but may bring the temporary overstatement of earnings reported by

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

EXAMPLE 1: MISALLOCATION OF

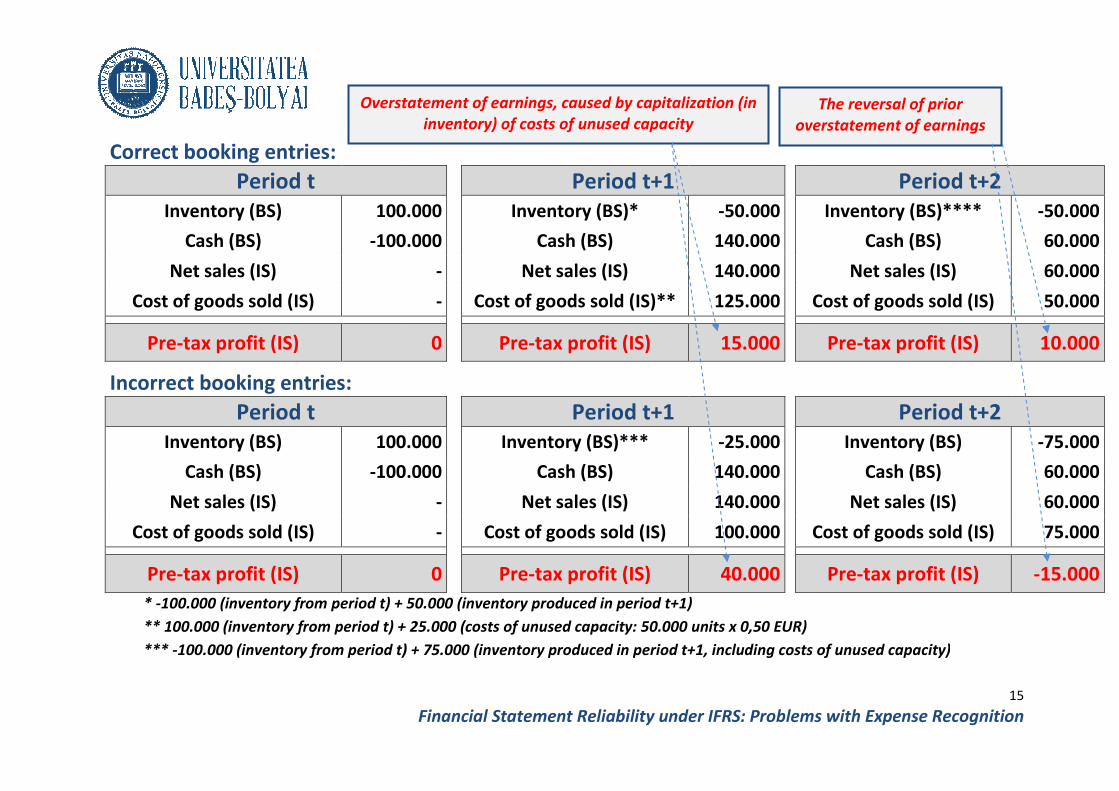

Basic data about company X are as follows:

• „normal” production level equals 100.000 units per year,

• fixed indirect manufacturing costs equal 50.000 EUR per year,

• variable (direct and indirect) manufacturing costs equal 0,50 EUR per unit,

• „standard” unit production costs equal 1 EUR (0,50 + 50.000 / 100.000),

• volume of production is: 100.000 units in period t and 50.000 units in period t+1

(when the company entered a cyclical economic slo

• actual unit costs in period t+1 equal 1,

• the unit selling price is 1,

“poor times” (periods t+1 and t+2),

• in period t+1 the company sold 100.000 units of

• in period t+2 the company sold 50.000 units of goods manufactured in

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

ALLOCATION OF INDIRECT MANUFACTURING (CONVERSION) COSTS

Basic data about company X are as follows:

„normal” production level equals 100.000 units per year,

fixed indirect manufacturing costs equal 50.000 EUR per year,

direct) manufacturing costs equal 0,50 EUR per unit,

„standard” unit production costs equal 1 EUR (0,50 + 50.000 / 100.000),

volume of production is: 100.000 units in period t and 50.000 units in period t+1

(when the company entered a cyclical economic slowdown),

actual unit costs in period t+1 equal 1,50 EUR (0,50 + 50.000 / 50.000),

the unit selling price is 1,40 EUR in “good times” (period t), but drops to 1,

s t+1 and t+2),

in period t+1 the company sold 100.000 units of goods manufactured in period t,

in period t+2 the company sold 50.000 units of goods manufactured in

14

: Problems with Expense Recognition

REPORTED INVENTORIES ON

INDIRECT MANUFACTURING (CONVERSION) COSTS

direct) manufacturing costs equal 0,50 EUR per unit,

„standard” unit production costs equal 1 EUR (0,50 + 50.000 / 100.000),

volume of production is: 100.000 units in period t and 50.000 units in period t+1

50 EUR (0,50 + 50.000 / 50.000),

0 EUR in “good times” (period t), but drops to 1,20 EUR in

goods manufactured in period t,

in period t+2 the company sold 50.000 units of goods manufactured in period t+1.

Correct booking entries:

Period t

Inventory (BS) 100.000

Cash (BS) -100.000

Net sales (IS)

Cost of goods sold (IS)

Pre-tax profit (IS)

Incorrect booking entries:

Period t

Inventory (BS) 100.000

Cash (BS) -100.000

Net sales (IS)

Cost of goods sold (IS)

Pre-tax profit (IS)

* -100.000 (inventory from period t) + 50.000 (inventory produced in period t+1)

** 100.000 (inventory from period t) + 25.000 (costs of unused capacity: 50.000 units x 0,50 EUR)

*** -100.000 (inventory from period t) + 75.000 (inventory produced in

Overstatement of earnings, caused by capitalization (in

Financial Statement Reliability under IFRS: Problems with Expense Recognition

Period t+1

100.000

Inventory (BS)* -50.000

100.000

Cash (BS) 140.000

-

Net sales (IS) 140.000

-

Cost of goods sold (IS)** 125.000

0

Pre-tax profit (IS) 15.000

Period t+1

100.000

Inventory (BS)*** -25.000

100.000

Cash (BS) 140.000

-

Net sales (IS) 140.000

-

Cost of goods sold (IS) 100.000

0

Pre-tax profit (IS) 40.000

100.000 (inventory from period t) + 50.000 (inventory produced in period t+1)

** 100.000 (inventory from period t) + 25.000 (costs of unused capacity: 50.000 units x 0,50 EUR)

100.000 (inventory from period t) + 75.000 (inventory produced in period t+1, including costs of unused capacity)

overstatement of earnings

Overstatement of earnings, caused by capitalization (in

inventory) of costs of unused capacity

15

: Problems with Expense Recognition

Period t+2

Inventory (BS)**** -50.000

Cash (BS) 60.000

Net sales (IS) 60.000

Cost of goods sold (IS) 50.000

Pre-tax profit (IS) 10.000

Period t+2

Inventory (BS) -75.000

Cash (BS) 60.000

Net sales (IS) 60.000

Cost of goods sold (IS) 75.000

Pre-tax profit (IS) -15.000

period t+1, including costs of unused capacity)

The reversal of prior

overstatement of earnings

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

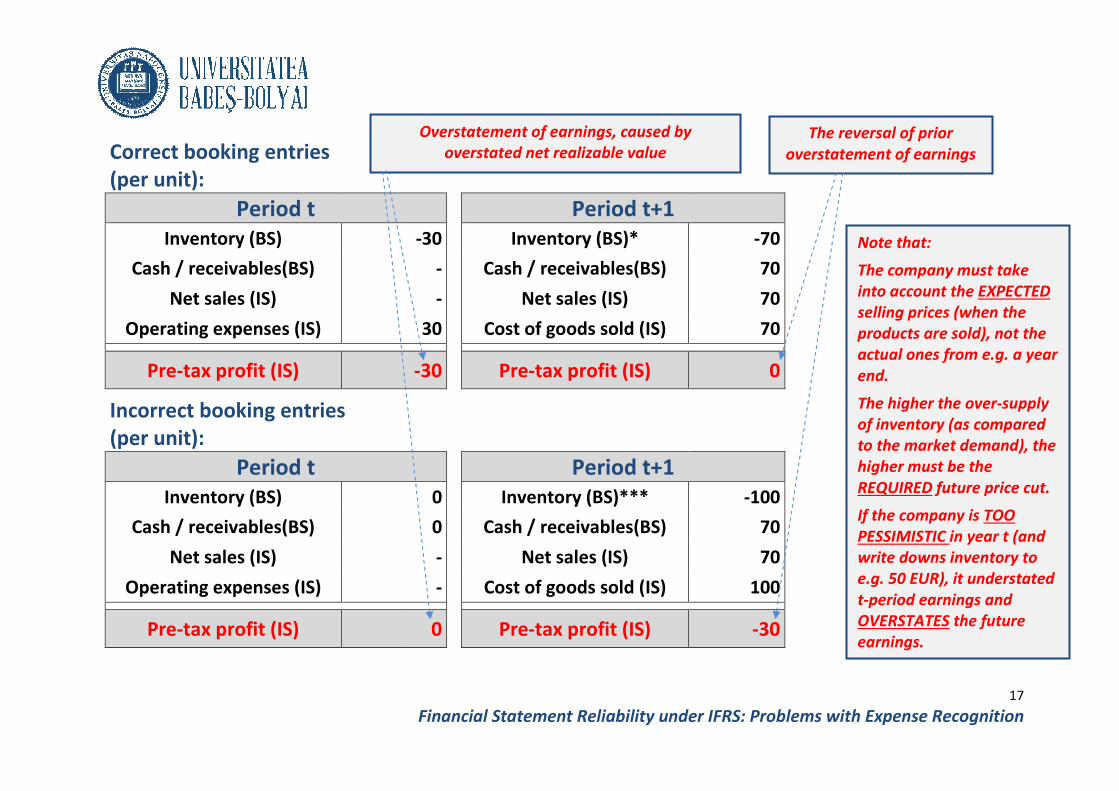

EXAMPLE 2: MIS-ESTIMATION OF NET REALIZABLE VALUE

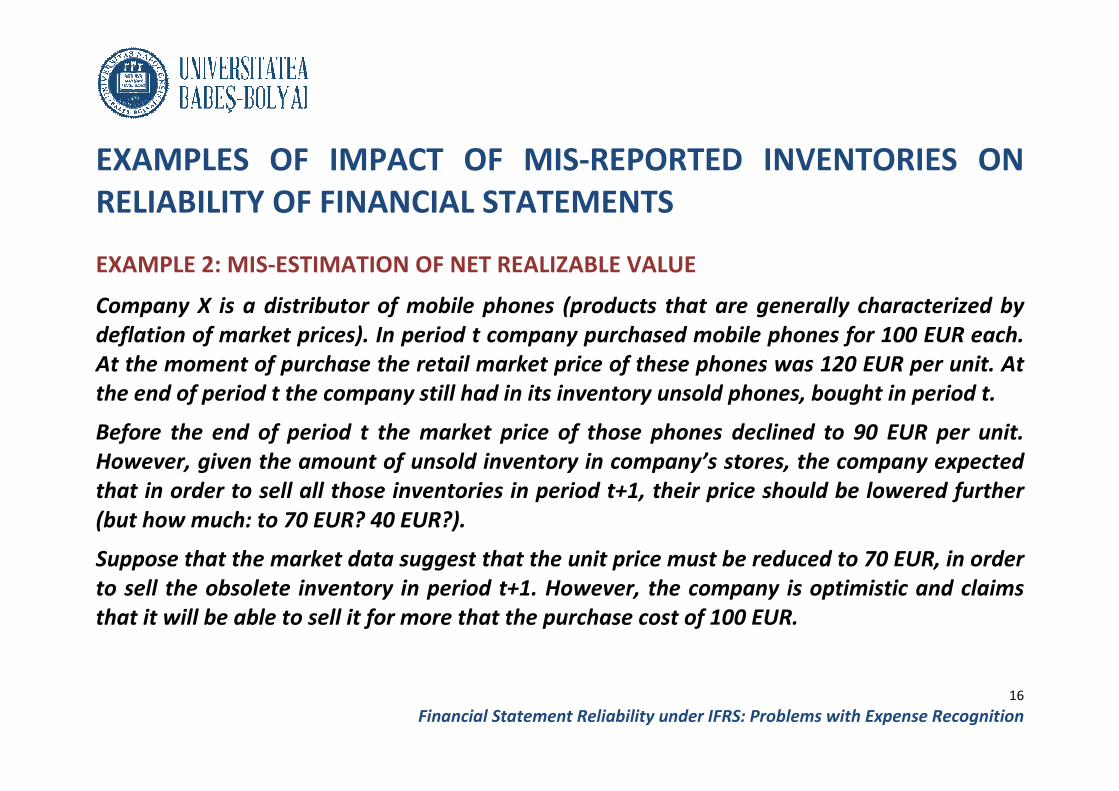

Company X is a distributor of mobile phones (products that are genera

deflation of market prices). In period t company

At the moment of purchase the retail market price of these phones was 120 EUR per unit. At

the end of period t the company still had in its inventory unsold phones, bought in period t.

Before the end of period t the market price of those phones declined to 90 EUR per unit.

However, given the amount of unsold inventory in company’s stores, the company expected

that in order to sell all those inventories in period t+1, their price should b

(but how much: to 70 EUR? 40 EUR?).

Suppose that the market data suggest

to sell the obsolete inventory in period t+1

that it will be able to sell it for more that the purchase cost of 100 EUR.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

ESTIMATION OF NET REALIZABLE VALUE

Company X is a distributor of mobile phones (products that are genera

). In period t company purchased mobile phones for 100 EUR each.

At the moment of purchase the retail market price of these phones was 120 EUR per unit. At

the end of period t the company still had in its inventory unsold phones, bought in period t.

Before the end of period t the market price of those phones declined to 90 EUR per unit.

However, given the amount of unsold inventory in company’s stores, the company expected

that in order to sell all those inventories in period t+1, their price should b

(but how much: to 70 EUR? 40 EUR?).

market data suggest that the unit price must be reduced to 70 EUR

to sell the obsolete inventory in period t+1. However, the company is optimistic and claims

sell it for more that the purchase cost of 100 EUR.

16

: Problems with Expense Recognition

REPORTED INVENTORIES ON

Company X is a distributor of mobile phones (products that are generally characterized by

mobile phones for 100 EUR each.

At the moment of purchase the retail market price of these phones was 120 EUR per unit. At

the end of period t the company still had in its inventory unsold phones, bought in period t.

Before the end of period t the market price of those phones declined to 90 EUR per unit.

However, given the amount of unsold inventory in company’s stores, the company expected

that in order to sell all those inventories in period t+1, their price should be lowered further

that the unit price must be reduced to 70 EUR, in order

. However, the company is optimistic and claims

Correct booking entries

(per unit):

Period t

Inventory (BS)

Cash / receivables(BS)

Net sales (IS)

Operating expenses (IS)

Pre-tax profit (IS)

Incorrect booking entries

(per unit):

Period t

Inventory (BS)

Cash / receivables(BS)

Net sales (IS)

Operating expenses (IS)

Pre-tax profit (IS)

Financial Statement Reliability under IFRS: Problems with Expense Recognition

Period t+1

-30

Inventory (BS)* -70

-

Cash / receivables(BS) 70

-

Net sales (IS) 70

30

Cost of goods sold (IS) 70

-30

Pre-tax profit (IS) 0

Period t+1

0

Inventory (BS)*** -100

0

Cash / receivables(BS) 70

-

Net sales (IS) 70

-

Cost of goods sold (IS) 100

0

Pre-tax profit (IS) -30

The reversal of prior

overstatement of earnings

Overstatement of earnings, caused by

overstated net realizable value

17

: Problems with Expense Recognition

The reversal of prior

overstatement of earnings

Note that:

The company must take

into account the EXPECTED

selling prices (when the

products are sold), not the

actual ones from e.g. a year

end.

The higher the over-supply

of inventory (as compared

to the market demand), the

higher must be the

REQUIRED future price cut.

If the company is TOO

PESSIMISTIC in year t (and

write downs inventory to

e.g. 50 EUR), it understated

t-period earnings and

OVERSTATES the future

earnings.

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

EXAMPLE 3: NON-RECOGNITION OF COST OF GOODS SOLD

In period t the company purchased 1.000 units of merchandise for 10

t+1 the company sold 500 units of this inventory for 12

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

RECOGNITION OF COST OF GOODS SOLD

In period t the company purchased 1.000 units of merchandise for 10 EUR per unit. In period

0 units of this inventory for 12 EUR per unit (for cash).

18

: Problems with Expense Recognition

REPORTED INVENTORIES ON

EUR per unit. In period

EUR per unit (for cash).

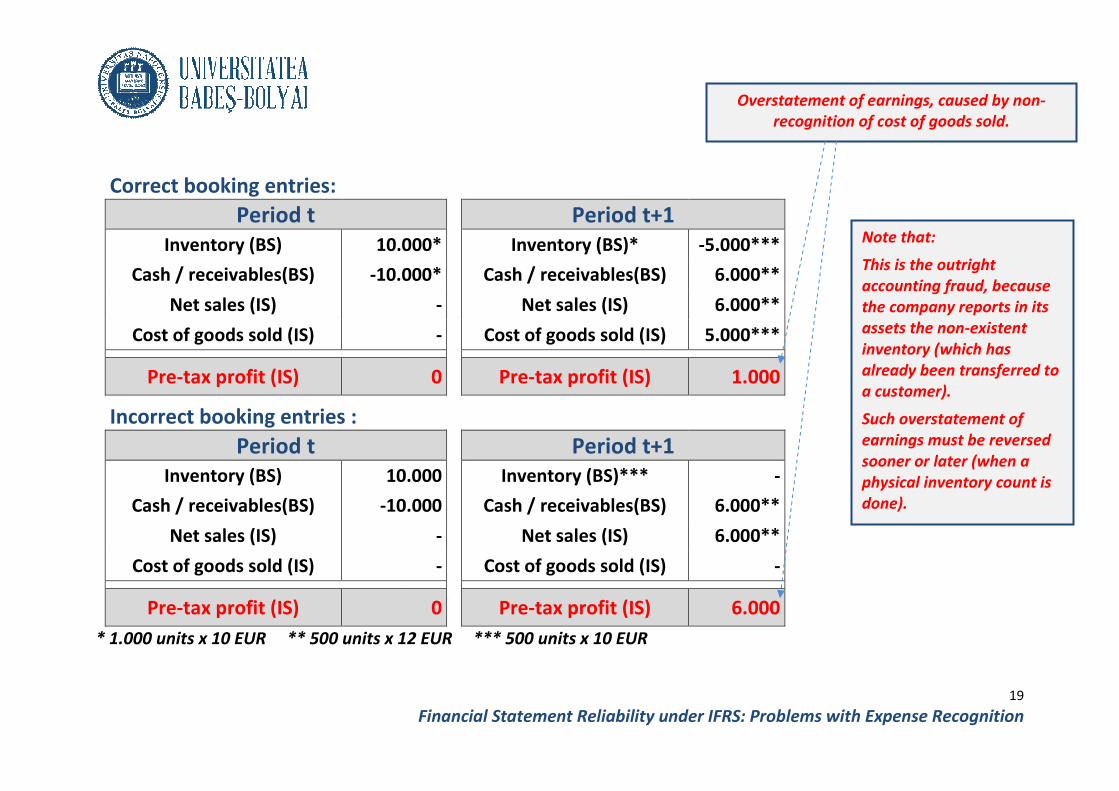

Correct booking entries:

Period t

Inventory (BS) 10.000*

Cash / receivables(BS) -10.000

Net sales (IS)

Cost of goods sold (IS)

Pre-tax profit (IS)

Incorrect booking entries :

Period t

Inventory (BS) 10

Cash / receivables(BS) -10.000

Net sales (IS)

Cost of goods sold (IS)

Pre-tax profit (IS)

* 1.000 units x 10 EUR ** 500 units x 12 EUR *** 500 units x 10 EUR

Financial Statement Reliability under IFRS: Problems with Expense Recognition

Period t+1

10.000*

Inventory (BS)* -5.000***

10.000*

Cash / receivables(BS) 6.000**

-

Net sales (IS) 6.000**

-

Cost of goods sold (IS) 5.000***

0

Pre-tax profit (IS) 1.000

Period t+1

0.000

Inventory (BS)*** -

10.000

Cash / receivables(BS) 6.000**

-

Net sales (IS) 6.000**

-

Cost of goods sold (IS) -

0

Pre-tax profit (IS) 6.000

** 500 units x 12 EUR *** 500 units x 10 EUR

Overstatement of earnings, caused by non

recognition of cost of goods sold.

19

: Problems with Expense Recognition

Overstatement of earnings, caused by non-

recognition of cost of goods sold.

Note that:

This is the outright

accounting fraud, because

the company reports in its

assets the non-existent

inventory (which has

already been transferred to

a customer).

Such overstatement of

earnings must be reversed

sooner or later (when a

physical inventory count is

done).

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

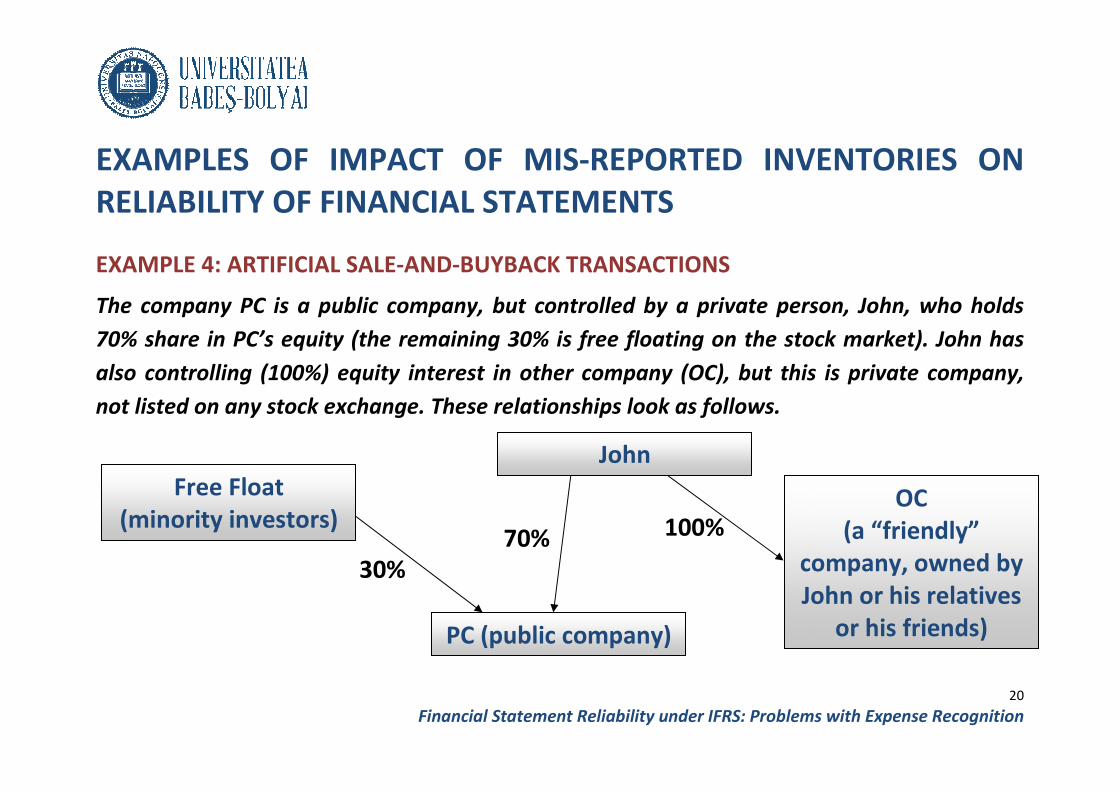

EXAMPLE 4: ARTIFICIAL SALE-AND

The company PC is a public company, but controlled by

70% share in PC’s equity (the remaining 30% is free floating on the stock market). John has

also controlling (100%) equity interest in other company (OC), but this is private company,

not listed on any stock exchange

Free Float

(minority investors)

30%

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

AND-BUYBACK TRANSACTIONS

The company PC is a public company, but controlled by a private person, John, who holds

remaining 30% is free floating on the stock market). John has

also controlling (100%) equity interest in other company (OC), but this is private company,

not listed on any stock exchange. These relationships look as follows.

company, owned by

John

PC (public company)

30%

70% 100%

John

20

: Problems with Expense Recognition

REPORTED INVENTORIES ON

private person, John, who holds

remaining 30% is free floating on the stock market). John has

also controlling (100%) equity interest in other company (OC), but this is private company,

OC

(a “friendly”

company, owned by

John or his relatives

or his friends)

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

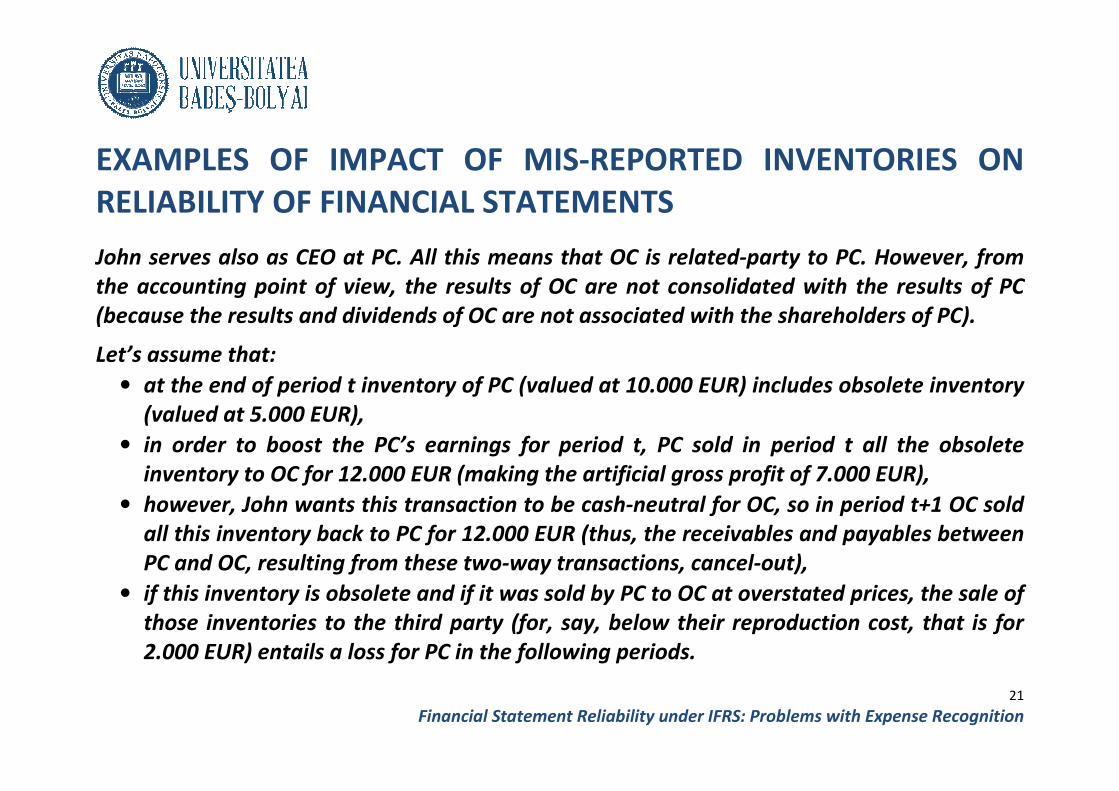

John serves also as CEO at PC.

the accounting point of view, the results of OC are not consolidated with the results of PC

(because the results and dividends of OC are not associated with the shareholders of PC).

Let’s assume that:

• at the end of period t inventory of PC (valued at 10.000 EUR) includes obsolete inventory

(valued at 5.000 EUR),

• in order to boost the PC’s earnings for period t, PC sold in period t all the obsolete

inventory to OC for 12.000 EUR (making the

• however, John wants this transaction to be cash

all this inventory back to PC for 12.000 EUR (

PC and OC, resulting from these two

• if this inventory is obsolete and if it was sold by PC to OC at overstated prices, the sale of

those inventories to the third party (for, say, below their reproduction cost, that is for

2.000 EUR) entails a loss for PC in the

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

John serves also as CEO at PC. All this means that OC is related-party to PC. However, from

the accounting point of view, the results of OC are not consolidated with the results of PC

(because the results and dividends of OC are not associated with the shareholders of PC).

at the end of period t inventory of PC (valued at 10.000 EUR) includes obsolete inventory

in order to boost the PC’s earnings for period t, PC sold in period t all the obsolete

inventory to OC for 12.000 EUR (making the artificial gross profit of 7.000 EUR),

however, John wants this transaction to be cash-neutral for OC, so in period t+1 OC sold

all this inventory back to PC for 12.000 EUR (thus, the receivables and payables between

, resulting from these two-way transactions, cancel-out),

if this inventory is obsolete and if it was sold by PC to OC at overstated prices, the sale of

those inventories to the third party (for, say, below their reproduction cost, that is for

a loss for PC in the following periods.

21

: Problems with Expense Recognition

REPORTED INVENTORIES ON

party to PC. However, from

the accounting point of view, the results of OC are not consolidated with the results of PC

(because the results and dividends of OC are not associated with the shareholders of PC).

at the end of period t inventory of PC (valued at 10.000 EUR) includes obsolete inventory

in order to boost the PC’s earnings for period t, PC sold in period t all the obsolete

gross profit of 7.000 EUR),

neutral for OC, so in period t+1 OC sold

, the receivables and payables between

if this inventory is obsolete and if it was sold by PC to OC at overstated prices, the sale of

those inventories to the third party (for, say, below their reproduction cost, that is for

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

PC (public company)

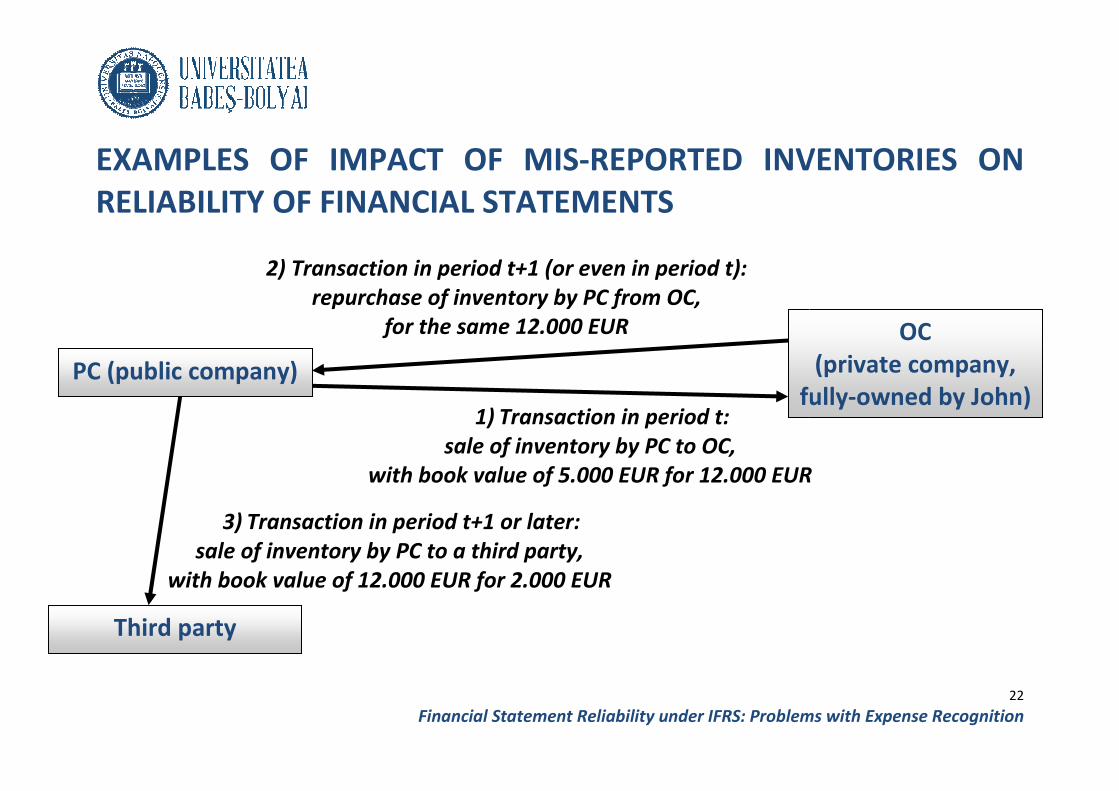

2) Transaction

repurchase of inventory by PC from OC

for

with book value of 5.000 EUR for 12.000 EUR

Third party

3) Transaction in period t+1 or later

sale of inventory by PC to

with book value of 12.000 EUR for

Financial Statement Reliability under IFRS: Problems with Expense Recognition

EXAMPLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

fully

Transaction in period t+1 (or even in period t):

repurchase of inventory by PC from OC,

for the same 12.000 EUR

1) Transaction in period t:

sale of inventory by PC to OC,

with book value of 5.000 EUR for 12.000 EUR

in period t+1 or later:

sale of inventory by PC to a third party,

.000 EUR for 2.000 EUR

22

: Problems with Expense Recognition

REPORTED INVENTORIES ON

OC

(private company,

fully-owned by John)

with book value of 5.000 EUR for 12.000 EUR

Effect of this related-party transaction of PC’s results:

Period t

Net sales to OC (IS) /

Receivables (BS) 12.000

Costs of goods sold (IS) /

Inventory (BS) 5.000

Profit before taxes (IS) 7.000

Impact on inventory -5.000

PC’s results without this related-party transaction:

Period t

Net sales to OC (IS) /

Receivables (BS) 0

Costs of goods sold (IS) /

Inventory (BS) 0

Profit before taxes (IS) 0

Impact on inventory 0

Artificial sale of inventory

results in

overstatement by 7.000

Financial Statement Reliability under IFRS: Problems with Expense Recognition

party transaction of PC’s results:

Period t+1

12.000

Inventory (IS) /

Payables (BS) 12.000

5.000

Costs of goods sold (IS) /

Inventory (BS) -

Costs of goods sold (IS) /

7.000

Profit before taxes (IS) 0

Profit before taxes (IS)

5.000

Impact on inventory 12.000

party transaction:

Period t+1

Inventory (IS) /

Payables (BS) 0

Costs of goods sold (IS) /

Inventory (BS) -

Costs of goods sold (IS) /

Profit before taxes (IS) 0

Profit before taxes (IS)

Impact on inventory 0

Artificial sale of inventory

results in earnings

overstatement by 7.000

Buyback of inventory brings

it back to the balance sheet

(at overstated value)

23

: Problems with Expense Recognition

Period t+2

Net sales (IS) /

Receivables (BS) 2.000

Costs of goods sold (IS) /

Inventory (BS) 12.000

Profit before taxes (IS) -10.000

Impact on inventory -12.000

Period t+2

Net sales (IS) /

Receivables (BS) 2.000

Costs of goods sold (IS) /

Inventory (BS) 5.000

Profit before taxes (IS) -3.000

Impact on inventory -5.000

Reversal of prior

overstatement of earnings

(by 7.000)

EXAMPLES OF IMPACT OF MIS

RELIABILITY OF FINANCIAL STATEMENTS

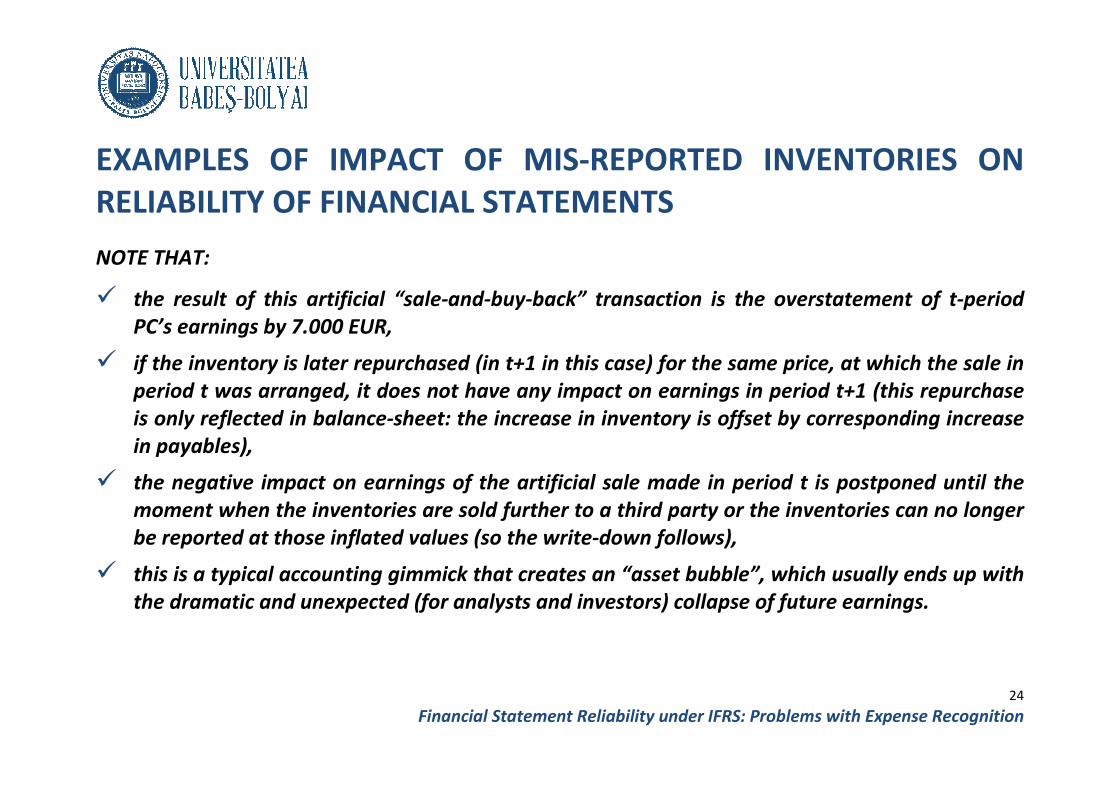

NOTE THAT:

� the result of this artificial “sale

PC’s earnings by 7.000 EUR,

� if the inventory is later repurchased (in t+1 in this case) for the same price, at which the sale in

period t was arranged, it does not have

is only reflected in balance-sheet: the increase in inventory

in payables),

� the negative impact on earnings of the artificial sale made in period t is postponed until the

moment when the inventories are sold further to

be reported at those inflated values (so the write

� this is a typical accounting gimmick that creates an “asset bubble”, which usually ends up with

the dramatic and unexpected (for analysts and investors) collapse of future earnings.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

PLES OF IMPACT OF MIS-REPORTED INVENTORIES ON

RELIABILITY OF FINANCIAL STATEMENTS

the result of this artificial “sale-and-buy-back” transaction is the overstatement of t

if the inventory is later repurchased (in t+1 in this case) for the same price, at which the sale in

period t was arranged, it does not have any impact on earnings in period t+1 (this repurchase

sheet: the increase in inventory is offset by corresponding increase

the negative impact on earnings of the artificial sale made in period t is postponed until the

moment when the inventories are sold further to a third party or the inventories can no longer

those inflated values (so the write-down follows),

gimmick that creates an “asset bubble”, which usually ends up with

the dramatic and unexpected (for analysts and investors) collapse of future earnings.

24

: Problems with Expense Recognition

REPORTED INVENTORIES ON

back” transaction is the overstatement of t-period

if the inventory is later repurchased (in t+1 in this case) for the same price, at which the sale in

impact on earnings in period t+1 (this repurchase

is offset by corresponding increase

the negative impact on earnings of the artificial sale made in period t is postponed until the

third party or the inventories can no longer

gimmick that creates an “asset bubble”, which usually ends up with

the dramatic and unexpected (for analysts and investors) collapse of future earnings.

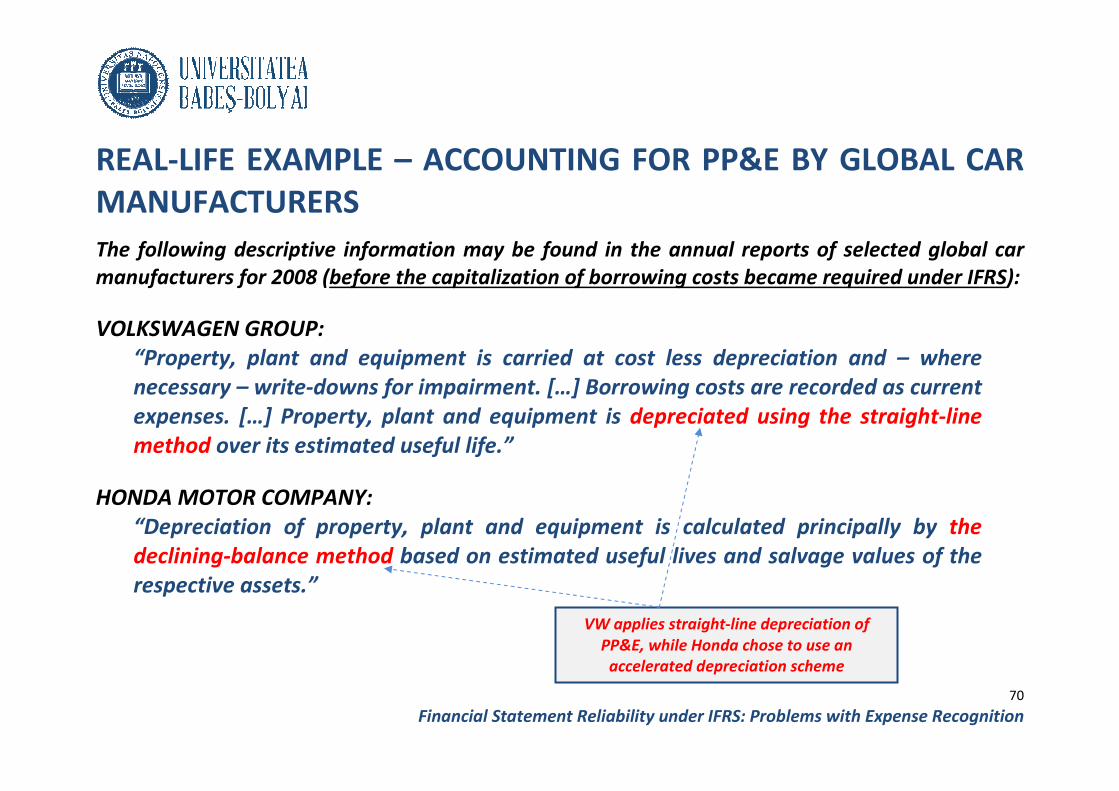

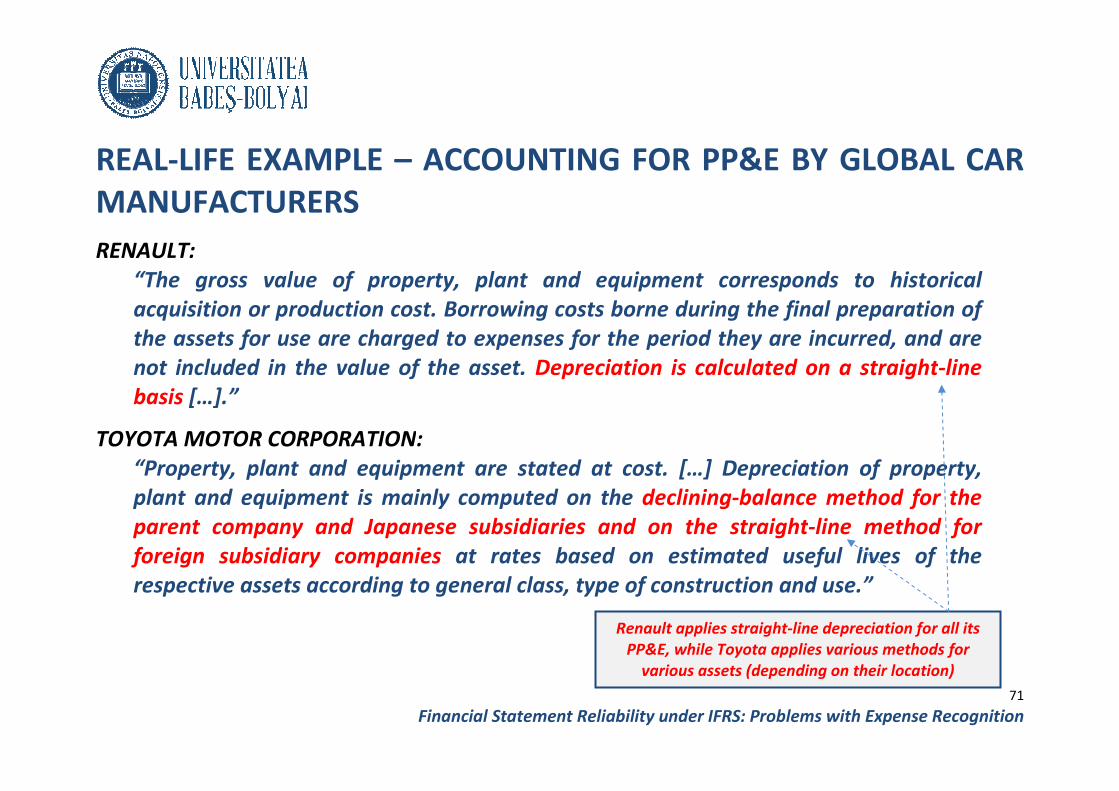

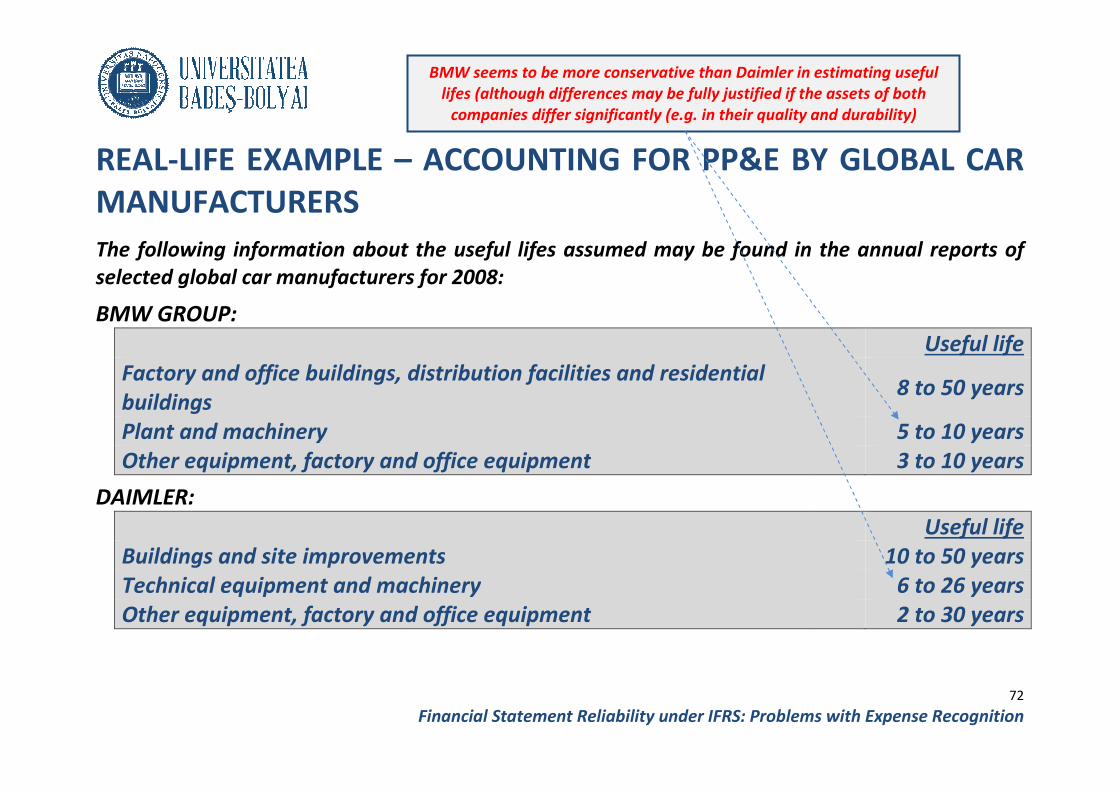

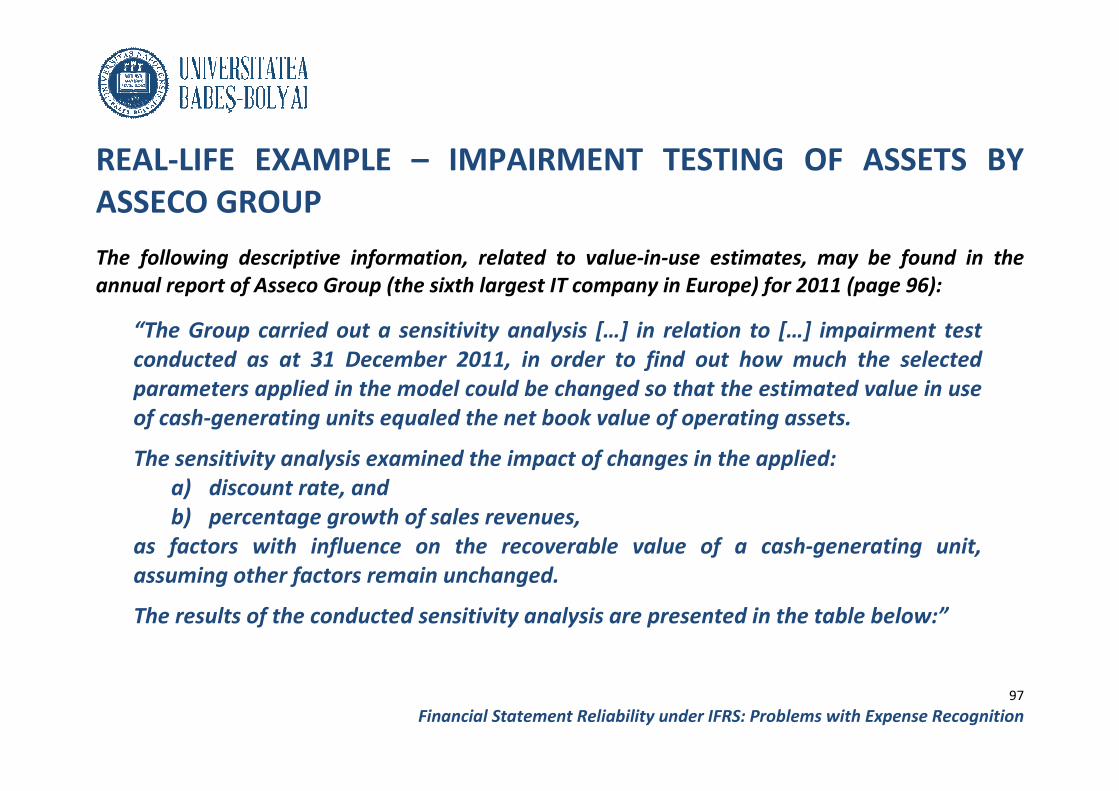

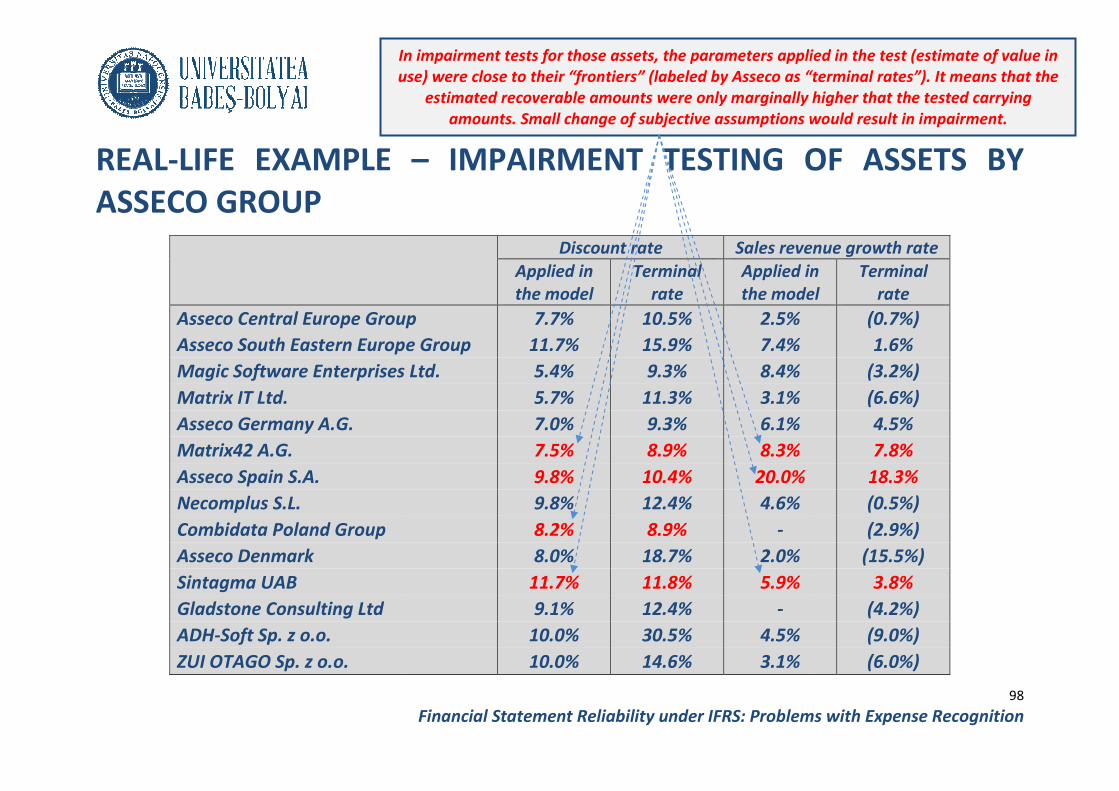

REAL-LIFE EXAMPLE –

OF RENAULT AND PEUGEOT

The following descriptive information may be found in the Annual Report

“Inventories are stated at the lower of cost or net realizable value. Cost corresponds

acquisition cost or production cost, which includes direct and indirect production expenses,

and a share of manufacturing overheads based on a normal level of activity. The normal

level of activity is assessed site by site, in order to determine the sha

excluded in the event of below

Inventories are valued under the FIFO (First In First Out) method.

When the net realizable value is lower than the value under the FIFO method, impairment

equal to the difference is recorded.”

The inventory-related numerical data, disclosed in the annual reports

following analysis of company’s revenues, earnings and inventories:

Financial Statement Reliability under IFRS: Problems with Expense Recognition

– INVENTORY IMPAIRMENT ALLOWANCES

AND PEUGEOT

information may be found in the Annual Report of Renault

“Inventories are stated at the lower of cost or net realizable value. Cost corresponds

acquisition cost or production cost, which includes direct and indirect production expenses,

and a share of manufacturing overheads based on a normal level of activity. The normal

level of activity is assessed site by site, in order to determine the share of fixed costs to be

excluded in the event of below-normal activity.

Inventories are valued under the FIFO (First In First Out) method.

When the net realizable value is lower than the value under the FIFO method, impairment

recorded.”

related numerical data, disclosed in the annual reports of Renault Group

following analysis of company’s revenues, earnings and inventories:

25

: Problems with Expense Recognition

INVENTORY IMPAIRMENT ALLOWANCES

of Renault for 2009:

“Inventories are stated at the lower of cost or net realizable value. Cost corresponds to

acquisition cost or production cost, which includes direct and indirect production expenses,

and a share of manufacturing overheads based on a normal level of activity. The normal

re of fixed costs to be

When the net realizable value is lower than the value under the FIFO method, impairment

of Renault Group, enable the

REAL-LIFE EXAMPLE –

OF RENAULT AND PEUGEOT

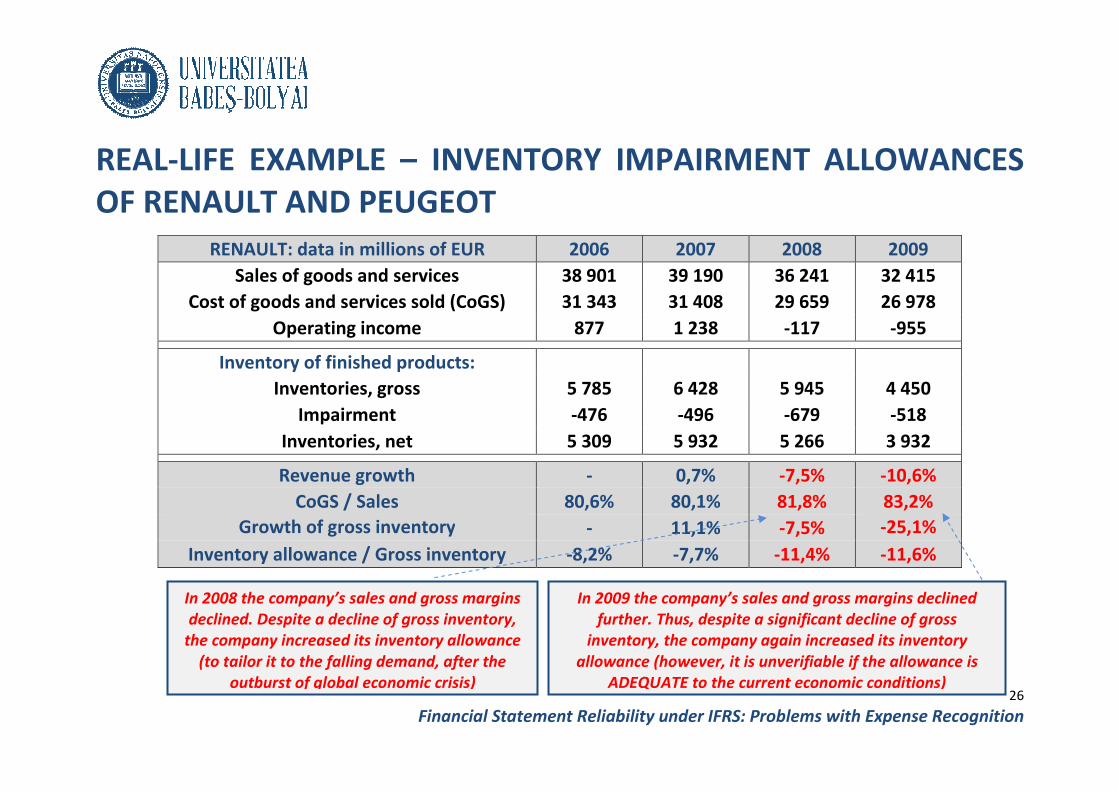

RENAULT: data in million

Sales of goods and services

Cost of goods and services sold

Operating income

Inventory of finished products

Inventories, gross

Impairment

Inventories, net

Revenue growth

CoGS / Sales

Growth of gross inventory

Inventory allowance / Gross inventory

In 2008 the company’s sales and gross margins

declined. Despite a decline of gross inventory,

the company increased its inventory allowance

(to tailor it to the falling demand, after the

outburst of global economic crisis)

Financial Statement Reliability under IFRS: Problems with Expense Recognition

– INVENTORY IMPAIRMENT ALLOWANCES

AND PEUGEOT

millions of EUR 2006 2007 2008

Sales of goods and services 38 901 39 190 36 241

Cost of goods and services sold (CoGS) 31 343 31 408 29 659

Operating income 877 1 238 -117

Inventory of finished products:

Inventories, gross 5 785 6 428 5 945

-476 -496 -679

Inventories, net 5 309 5 932 5 266

Revenue growth - 0,7% -7,5%

80,6% 80,1% 81,8%

Growth of gross inventory - 11,1% -7,5%

Inventory allowance / Gross inventory -8,2% -7,7% -11,4%

In 2008 the company’s sales and gross margins

declined. Despite a decline of gross inventory,

the company increased its inventory allowance

demand, after the

outburst of global economic crisis)

In 2009 the company’s sales and gross margins declined

further. Thus, despite a significant decline of gross

inventory, the company again increased its inventory

allowance (however, it is unverifiable if the allowance is

ADEQUATE to the current economic conditions)26

: Problems with Expense Recognition

INVENTORY IMPAIRMENT ALLOWANCES

2008 2009

36 241 32 415

29 659 26 978

117 -955

5 945 4 450

679 -518

5 266 3 932

7,5% -10,6%

81,8% 83,2%

7,5% -25,1%

11,4% -11,6%

In 2009 the company’s sales and gross margins declined

further. Thus, despite a significant decline of gross

inventory, the company again increased its inventory

unverifiable if the allowance is

ADEQUATE to the current economic conditions)

REAL-LIFE EXAMPLE –

OF RENAULT AND PEUGEOT

The following descriptive information may be found in the Annual Report

“Inventories are stated at the lower of cost and net realizable value, in accordance with

IAS 2 - Inventories.

Cost is determined by the first

indirect variable production expenses, plus fixed production expenses based on the normal

capacity of the production facility. As inventories do not take a substantial period of time

to get ready for sale, their cost does not include any borrowing costs.

The net realizable value of inventories intended to be sold corresponds to their selling

price, as estimated based on market conditions and any relevant external information

sources, less the estimated costs necessary to complete the sale (such as variable direct

selling expenses, refurbishment costs not billed to customers for used vehicles and other

goods).”

As in Renault’s case, the inventory

Peugeot enable the following analysis of company’s revenues, earnings and inventories:

Financial Statement Reliability under IFRS: Problems with Expense Recognition

– INVENTORY IMPAIRMENT ALLOWANCES

LT AND PEUGEOT

information may be found in the Annual Report of Peugeot

at the lower of cost and net realizable value, in accordance with

Cost is determined by the first-in-first-out (FIFO) method and includes all direct and

indirect variable production expenses, plus fixed production expenses based on the normal

capacity of the production facility. As inventories do not take a substantial period of time

for sale, their cost does not include any borrowing costs.

The net realizable value of inventories intended to be sold corresponds to their selling

estimated based on market conditions and any relevant external information

imated costs necessary to complete the sale (such as variable direct

selling expenses, refurbishment costs not billed to customers for used vehicles and other

he inventory-related numerical data, disclosed in the annual

enable the following analysis of company’s revenues, earnings and inventories:

The company uses wide range of information (also

with a qualitative nature) when estimating the net

realizable values for its products

27

: Problems with Expense Recognition

INVENTORY IMPAIRMENT ALLOWANCES

of Peugeot for 2009:

at the lower of cost and net realizable value, in accordance with

out (FIFO) method and includes all direct and

indirect variable production expenses, plus fixed production expenses based on the normal

capacity of the production facility. As inventories do not take a substantial period of time

The net realizable value of inventories intended to be sold corresponds to their selling

estimated based on market conditions and any relevant external information

imated costs necessary to complete the sale (such as variable direct

selling expenses, refurbishment costs not billed to customers for used vehicles and other

related numerical data, disclosed in the annual reports of

enable the following analysis of company’s revenues, earnings and inventories:

The company uses wide range of information (also

with a qualitative nature) when estimating the net

realizable values for its products

REAL-LIFE EXAMPLE –

OF RENAULT AND PEUGEOT

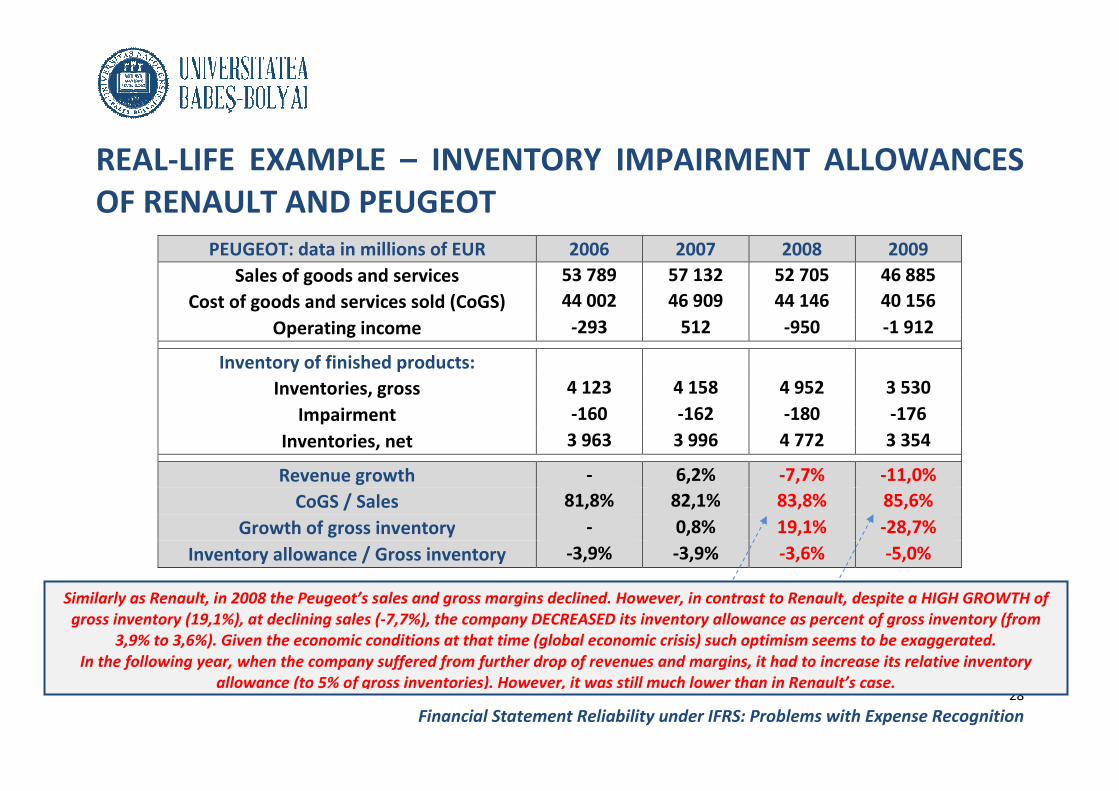

PEUGEOT: data in million

Sales of goods and services

Cost of goods and services sold

Operating income

Inventory of finished products

Inventories, gross

Impairment

Inventories, net

Revenue growth

CoGS / Sales

Growth of gross inventory

Inventory allowance / Gross inventory

Similarly as Renault, in 2008 the Peugeot’s sales and gross margins declined. However, in contrast to Renault, despite a HIGH GROWTH of

gross inventory (19,1%), at declining sales (-7,7%), the company DECREASED its inventory allowance as percent of gross inventory (fro

3,9% to 3,6%). Given the economic conditions at that time (global economic crisis) such optimism seems to be exaggerated.

In the following year, when the company suffered from further drop of revenues and margins, it had to increase its relative

allowance (to 5% of gross inventories). However, it was still much lower than in Renault’s case.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

– INVENTORY IMPAIRMENT ALLOWANCES

OF RENAULT AND PEUGEOT

millions of EUR 2006 2007 2008

Sales of goods and services 53 789 57 132 52 705

Cost of goods and services sold (CoGS) 44 002 46 909 44 146

Operating income -293 512 -950

Inventory of finished products:

Inventories, gross 4 123 4 158 4 952

-160 -162 -180

Inventories, net 3 963 3 996 4 772

Revenue growth - 6,2% -7,7%

81,8% 82,1% 83,8%

Growth of gross inventory - 0,8% 19,1%

Inventory allowance / Gross inventory -3,9% -3,9% -3,6%

Renault, in 2008 the Peugeot’s sales and gross margins declined. However, in contrast to Renault, despite a HIGH GROWTH of

7,7%), the company DECREASED its inventory allowance as percent of gross inventory (fro

3,9% to 3,6%). Given the economic conditions at that time (global economic crisis) such optimism seems to be exaggerated.

In the following year, when the company suffered from further drop of revenues and margins, it had to increase its relative

allowance (to 5% of gross inventories). However, it was still much lower than in Renault’s case.28

: Problems with Expense Recognition

INVENTORY IMPAIRMENT ALLOWANCES

2008 2009

52 705 46 885

44 146 40 156

950 -1 912

4 952 3 530

180 -176

4 772 3 354

7,7% -11,0%

83,8% 85,6%

19,1% -28,7%

3,6% -5,0%

Renault, in 2008 the Peugeot’s sales and gross margins declined. However, in contrast to Renault, despite a HIGH GROWTH of

7,7%), the company DECREASED its inventory allowance as percent of gross inventory (from

3,9% to 3,6%). Given the economic conditions at that time (global economic crisis) such optimism seems to be exaggerated.

In the following year, when the company suffered from further drop of revenues and margins, it had to increase its relative inventory

allowance (to 5% of gross inventories). However, it was still much lower than in Renault’s case.

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

Accounts receivable (receivables) are defined as amounts due from customers for goods or

services provided in the normal course of business.

accounts are credit sales transactions (i.e. sales with deferred payment terms)

that the receivables-related accounting abuses are often twin to revenue

(discussed in Module 1), such as

brought about by premature revenue recognition or

However, receivables (like other assets)

exceed their recoverable amounts.

collection problems, e.g. delays or total defaults,

by its customers. These estimates, often labeled as

extent similar in nature to allowances for impaired inventories

extent exposed to subjective judgments, because usually no any observable inputs are

available (such as current market prices

inventories). As a result, allowances for bad debts

compared to impairments of other assets

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

(receivables) are defined as amounts due from customers for goods or

services provided in the normal course of business. Thus, the main source for receivable

sales transactions (i.e. sales with deferred payment terms)

related accounting abuses are often twin to revenue

(discussed in Module 1), such as overstatements of revenues (and related receivables)

premature revenue recognition or by recognizing fictitious sales.

(like other assets) should not be reported at carrying

exceed their recoverable amounts. Thus, accountants must make estimates of expected

, e.g. delays or total defaults, related to receivables

. These estimates, often labeled as “allowance for bad debts

similar in nature to allowances for impaired inventories. However, they are to a larger

extent exposed to subjective judgments, because usually no any observable inputs are

available (such as current market prices or price forecasts, which are available

allowances for bad debts are much more prone to manipulations, as

compared to impairments of other assets.

PROBLEM 8: Accounting for receivable accounts calls

for estimating uncollectible accounts, which usually

is heavily subjective and difficult

29

: Problems with Expense Recognition

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

(receivables) are defined as amounts due from customers for goods or

Thus, the main source for receivable

sales transactions (i.e. sales with deferred payment terms). This means

related accounting abuses are often twin to revenue-recognition abuses

overstatements of revenues (and related receivables)

recognizing fictitious sales.

should not be reported at carrying values which

estimates of expected

related to receivables owed to a company

d debts”, are to some

However, they are to a larger

extent exposed to subjective judgments, because usually no any observable inputs are

or price forecasts, which are available for many

are much more prone to manipulations, as

Accounting for receivable accounts calls

for estimating uncollectible accounts, which usually

is heavily subjective and difficult to verify

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

It is also worth noting that not all the overdue accounts must be automatically written down

(e.g. when the company cooperates with a customer for a long time and it always pay after a

deadline). In contrast, some receivables which are not overdue, may qua

write-off (e.g. “fresh” receivable accounts from a sale to a bankrupt customer).

If accountants are too optimistic and

assets (receivables) and earnings will be overstated.

excessive write-downs of receivables

(“cookie-jar reserves”)

The two methods are usually applied in adjusting the gross values of receivable accounts to

their recoverable amounts:

(1) Aging-the-accounts method

uncollectible accounts receivable based on the length of time the end

outstanding accounts have been unpaid,

(2) Percentage-of-sales method

uncollectible accounts receivable based on the historical relationship between bad

debts and gross credit sales.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

It is also worth noting that not all the overdue accounts must be automatically written down

(e.g. when the company cooperates with a customer for a long time and it always pay after a

In contrast, some receivables which are not overdue, may qua

off (e.g. “fresh” receivable accounts from a sale to a bankrupt customer).

accountants are too optimistic and underestimate the values of the

and earnings will be overstated. However, similarly as for inventories,

downs of receivables in “good times” may be easily reverted in bad periods

The two methods are usually applied in adjusting the gross values of receivable accounts to

accounts method – procedure for the computation of the adjustment for

uncollectible accounts receivable based on the length of time the end

outstanding accounts have been unpaid,

sales method – procedure for computing the adjustment for

uncollectible accounts receivable based on the historical relationship between bad

debts and gross credit sales. 30

: Problems with Expense Recognition

ACCOUNTING FOR RECEIVABLE ACCOUNTS UNDER IFRS

It is also worth noting that not all the overdue accounts must be automatically written down

(e.g. when the company cooperates with a customer for a long time and it always pay after a

In contrast, some receivables which are not overdue, may qualify for a full-blown

off (e.g. “fresh” receivable accounts from a sale to a bankrupt customer).

the bad-debt reserves,

However, similarly as for inventories,

be easily reverted in bad periods

The two methods are usually applied in adjusting the gross values of receivable accounts to

procedure for the computation of the adjustment for

uncollectible accounts receivable based on the length of time the end-of-period

dure for computing the adjustment for

uncollectible accounts receivable based on the historical relationship between bad

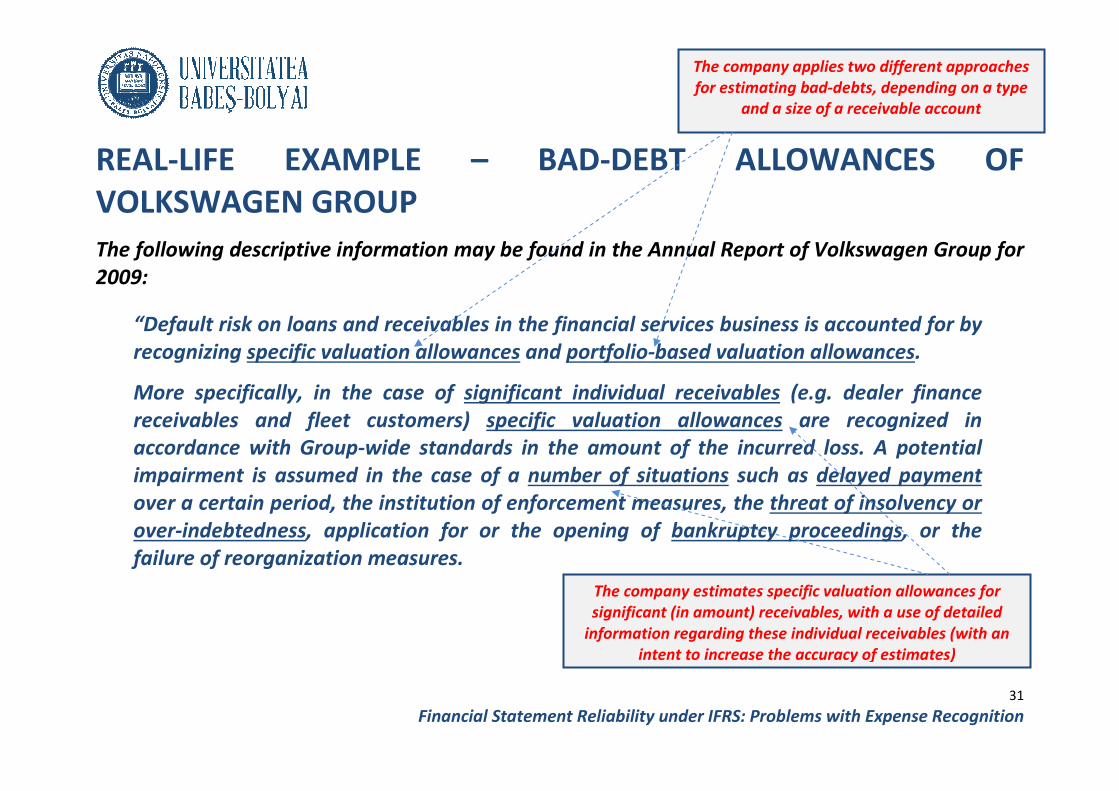

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

The following descriptive information may be found in the Annual Report of Volk

2009:

“Default risk on loans and receivables in the financial services business is accounted for by

recognizing specific valuation allowances

More specifically, in the case of

receivables and fleet customers)

accordance with Group-wide standards in the amount of the incurred loss. A potential

impairment is assumed in the case of a

over a certain period, the institution of enforcement measures, the

over-indebtedness, application for or the opening of

failure of reorganization measures.

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES OF

VOLKSWAGEN GROUP

The following descriptive information may be found in the Annual Report of Volk

Default risk on loans and receivables in the financial services business is accounted for by

specific valuation allowances and portfolio-based valuation allowances

More specifically, in the case of significant individual receivables (e.g. dealer finance

receivables and fleet customers) specific valuation allowances are recognized in

wide standards in the amount of the incurred loss. A potential

impairment is assumed in the case of a number of situations such as

over a certain period, the institution of enforcement measures, the threat of insolvency or

, application for or the opening of bankruptcy proceedings

failure of reorganization measures.

The company applies two different approaches

for estimating bad

and a size of a receivable account

The company estimates specific valuation allowances for

significant (in amount) receivables, with a use of detailed

information regarding these individual receivables (with an

intent to increase the accuracy of estimates)

31

: Problems with Expense Recognition

DEBT ALLOWANCES OF

The following descriptive information may be found in the Annual Report of Volkswagen Group for

Default risk on loans and receivables in the financial services business is accounted for by

based valuation allowances.

(e.g. dealer finance

are recognized in

wide standards in the amount of the incurred loss. A potential

such as delayed payment

threat of insolvency or

bankruptcy proceedings, or the

The company applies two different approaches

for estimating bad-debts, depending on a type

e of a receivable account

cific valuation allowances for

significant (in amount) receivables, with a use of detailed

information regarding these individual receivables (with an

intent to increase the accuracy of estimates)

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

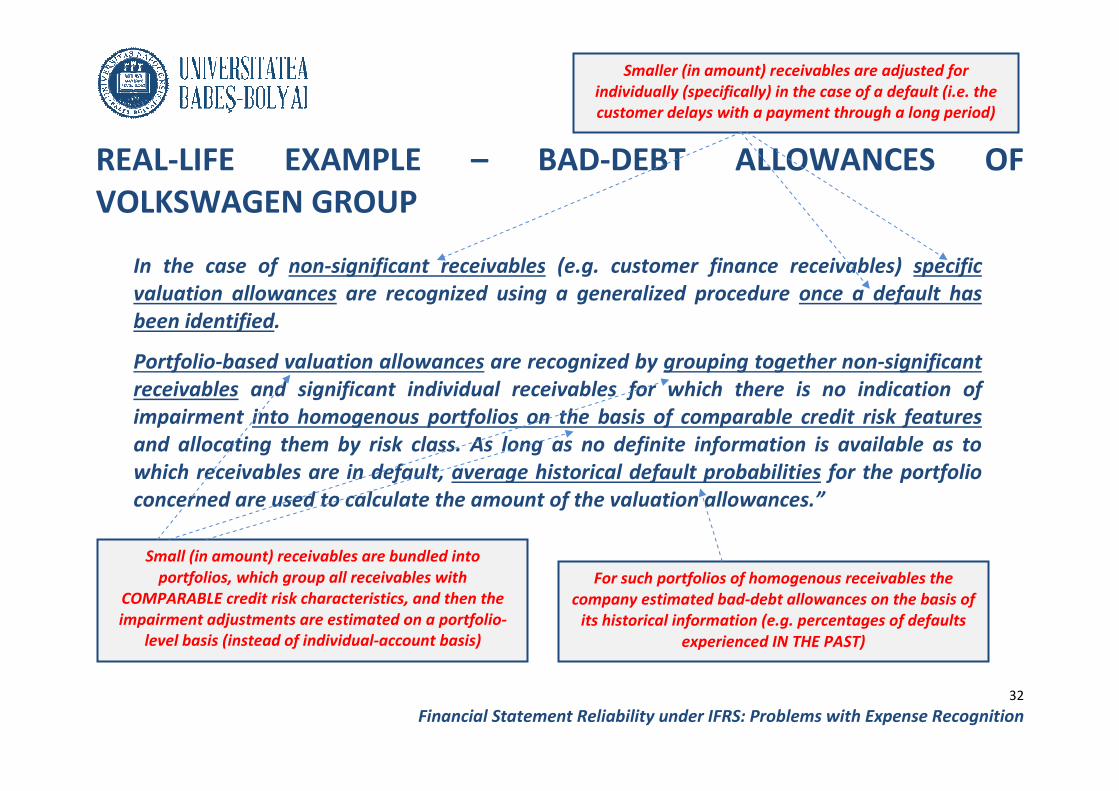

In the case of non-significant receivables

valuation allowances are recognized using a generalized procedure

been identified.

Portfolio-based valuation allowances

receivables and significant individual receivables for which there is no indication of

impairment into homogenous portfolios on the basis of comparable credit risk features

and allocating them by risk class. As long as no definite information is available as to

which receivables are in default,

concerned are used to calculate the amount of the valuation allowances.

Small (in amount) receivables are bundled into

portfolios, which group all receivables

COMPARABLE credit risk characteristics, and then the

impairment adjustments are estimated on a portfolio

level basis (instead of individual-account basis)

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES OF

VOLKSWAGEN GROUP

significant receivables (e.g. customer finance receivables)

are recognized using a generalized procedure once a default has

based valuation allowances are recognized by grouping together non

and significant individual receivables for which there is no indication of

into homogenous portfolios on the basis of comparable credit risk features

and allocating them by risk class. As long as no definite information is available as to

receivables are in default, average historical default probabilities

concerned are used to calculate the amount of the valuation allowances.

Smaller (in amount) receivables are adjusted for

individually (specifically) in the case of a default (i.e. the

customer delays with a payment through a long period)

Small (in amount) receivables are bundled into

portfolios, which group all receivables with

COMPARABLE credit risk characteristics, and then the

impairment adjustments are estimated on a portfolio-

account basis)

For such portfolios of homogenous receivables the

company estimated bad-debt allowances on

its historical information (e.g. percentages of defaults

experienced IN THE PAST)

32

: Problems with Expense Recognition

DEBT ALLOWANCES OF

(e.g. customer finance receivables) specific

once a default has

grouping together non-significant

and significant individual receivables for which there is no indication of

into homogenous portfolios on the basis of comparable credit risk features

and allocating them by risk class. As long as no definite information is available as to

average historical default probabilities for the portfolio

concerned are used to calculate the amount of the valuation allowances.”

Smaller (in amount) receivables are adjusted for

individually (specifically) in the case of a default (i.e. the

customer delays with a payment through a long period)

For such portfolios of homogenous receivables the

debt allowances on the basis of

its historical information (e.g. percentages of defaults

experienced IN THE PAST)

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

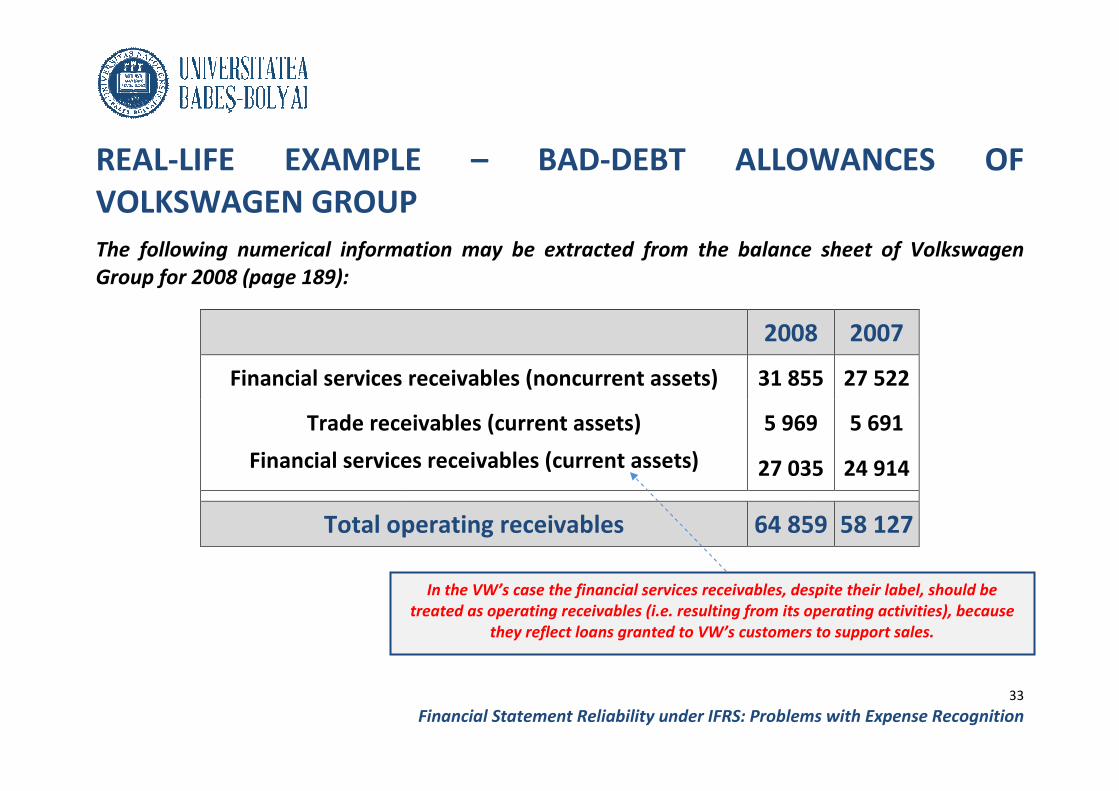

The following numerical information may be extracted from the balance sheet of Volkswagen

Group for 2008 (page 189):

Financial services receivables (noncurrent assets)

Trade receivables (current assets)

Financial services receivables (current assets)

Total operating receivables

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES OF

VOLKSWAGEN GROUP

The following numerical information may be extracted from the balance sheet of Volkswagen

2008

Financial services receivables (noncurrent assets) 31 855

Trade receivables (current assets) 5 969

Financial services receivables (current assets) 27 035

Total operating receivables 64 859

In the VW’s case the financial services receivables, despite their label, should be

treated as operating receivables (i.e. resulting from its operating activities), because

they reflect loans granted to VW’s customers to support sales.

33

: Problems with Expense Recognition

DEBT ALLOWANCES OF

The following numerical information may be extracted from the balance sheet of Volkswagen

2008 2007

31 855 27 522

5 969 5 691

27 035 24 914

64 859 58 127

In the VW’s case the financial services receivables, despite their label, should be

treated as operating receivables (i.e. resulting from its operating activities), because

they reflect loans granted to VW’s customers to support sales.

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

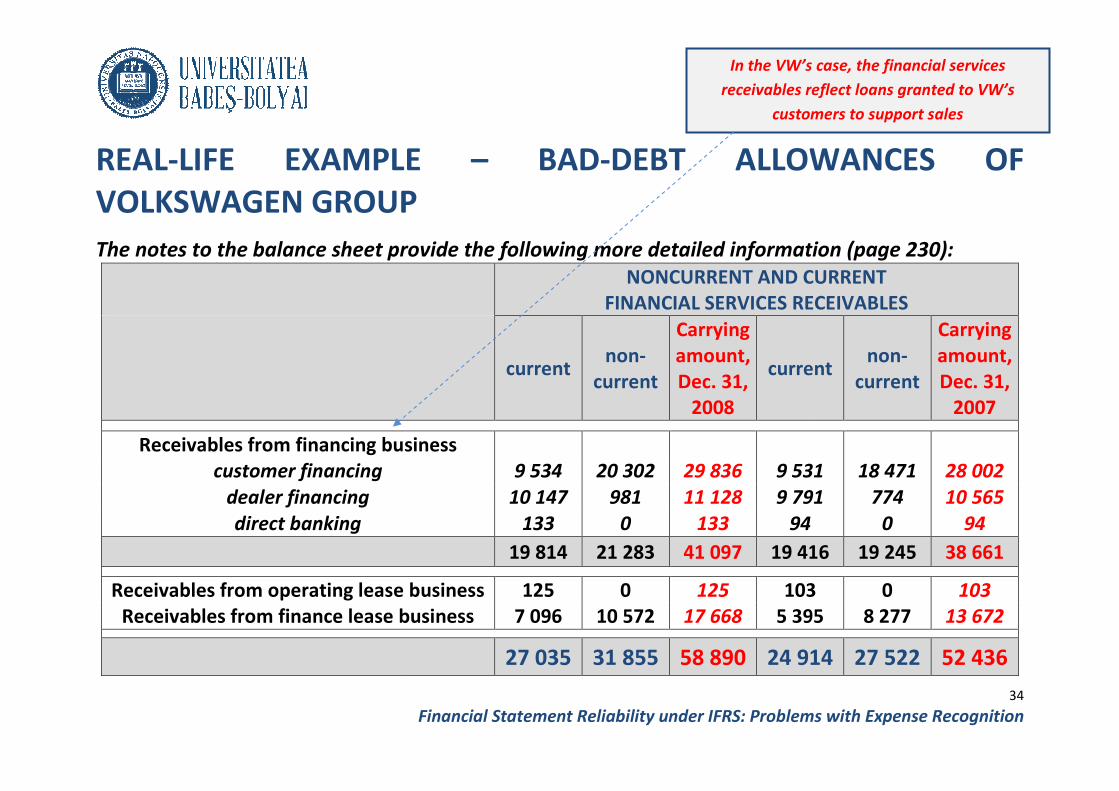

The notes to the balance sheet provide the following more detailed information (page 230)

Receivables from financing business

customer financing

dealer financing

direct banking

Receivables from operating lease business

Receivables from finance lease business

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES OF

VOLKSWAGEN GROUP

The notes to the balance sheet provide the following more detailed information (page 230)

NONCURRENT AND CURRENT

FINANCIAL SERVICES RECEIVABLES

current non-

current

Carrying

amount,

Dec. 31,

2008

current

Receivables from financing business

9 534 20 302 29 836 9 531

10 147 981 11 128 9 791

133 0 133 94

19 814 21 283 41 097 19 416

Receivables from operating lease business 125 0 125 103

business 7 096 10 572 17 668 5 395

27 035 31 855 58 890 24 914

In the VW’s case, the financial services

receivables reflect loans granted to VW’s

customers to support sales

34

: Problems with Expense Recognition

DEBT ALLOWANCES OF

The notes to the balance sheet provide the following more detailed information (page 230):

NONCURRENT AND CURRENT

FINANCIAL SERVICES RECEIVABLES

current non-

current

Carrying

amount,

Dec. 31,

2007

531 18 471 28 002

9 791 774 10 565

94 0 94

19 416 19 245 38 661

103 0 103

5 395 8 277 13 672

24 914 27 522 52 436

the VW’s case, the financial services

receivables reflect loans granted to VW’s

customers to support sales

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

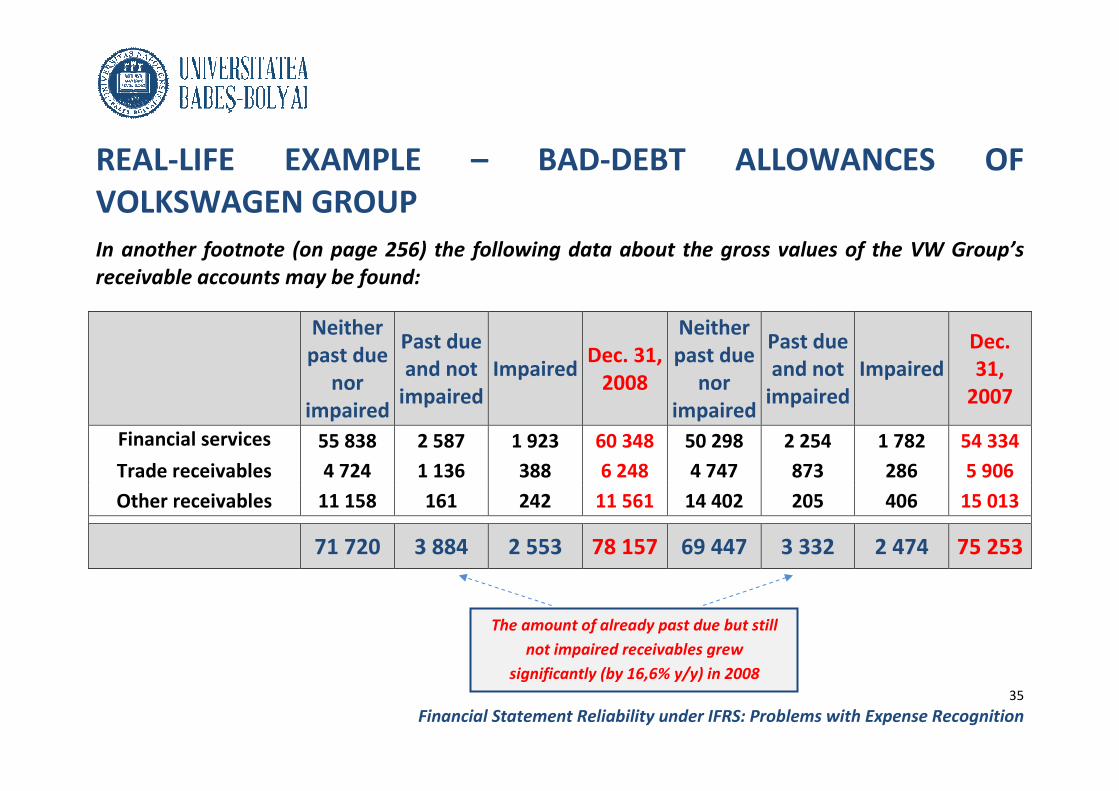

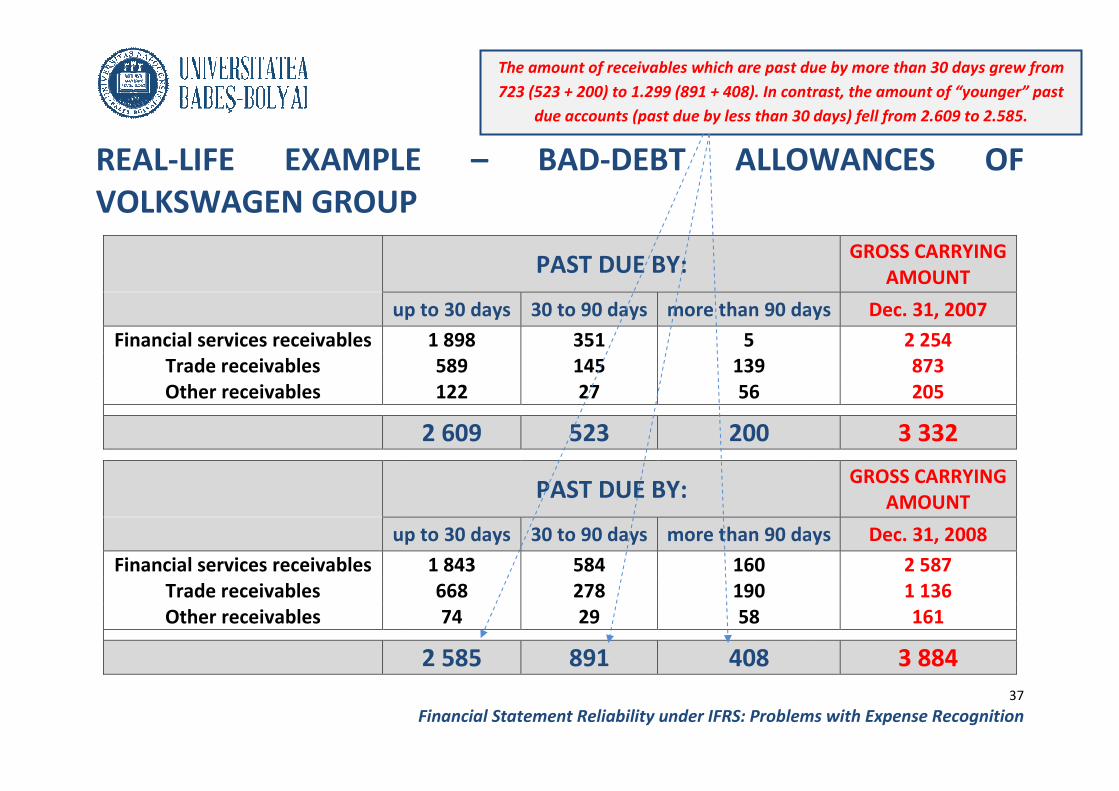

In another footnote (on page 256

receivable accounts may be found

Neither

past due

nor

impaired

Past due

and not

impaired

Financial services

receivables

55 838

Trade receivables 4 724

Other receivables 11 158

71 720

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES OF

VOLKSWAGEN GROUP

n page 256) the following data about the gross values

may be found:

Past due

and not

impaired

Impaired Dec. 31,

2008

Neither

past due

nor

impaired

Past due

and not

impaired

2 587 1 923 60 348 50 298 2 254

1 136 388 6 248 4 747 873

161 242 11 561 14 402 205

3 884 2 553 78 157 69 447 3 332

The amount of already past due but still

not impaired receivables grew

significantly (by 16,6% y/y) in 2008

35

: Problems with Expense Recognition

DEBT ALLOWANCES OF

gross values of the VW Group’s

Past due

and not

impaired

Impaired

Dec.

31,

2007

2 254 1 782 54 334

873 286 5 906

205 406 15 013

3 332 2 474 75 253

REAL-LIFE EXAMPLE

VOLKSWAGEN GROUP

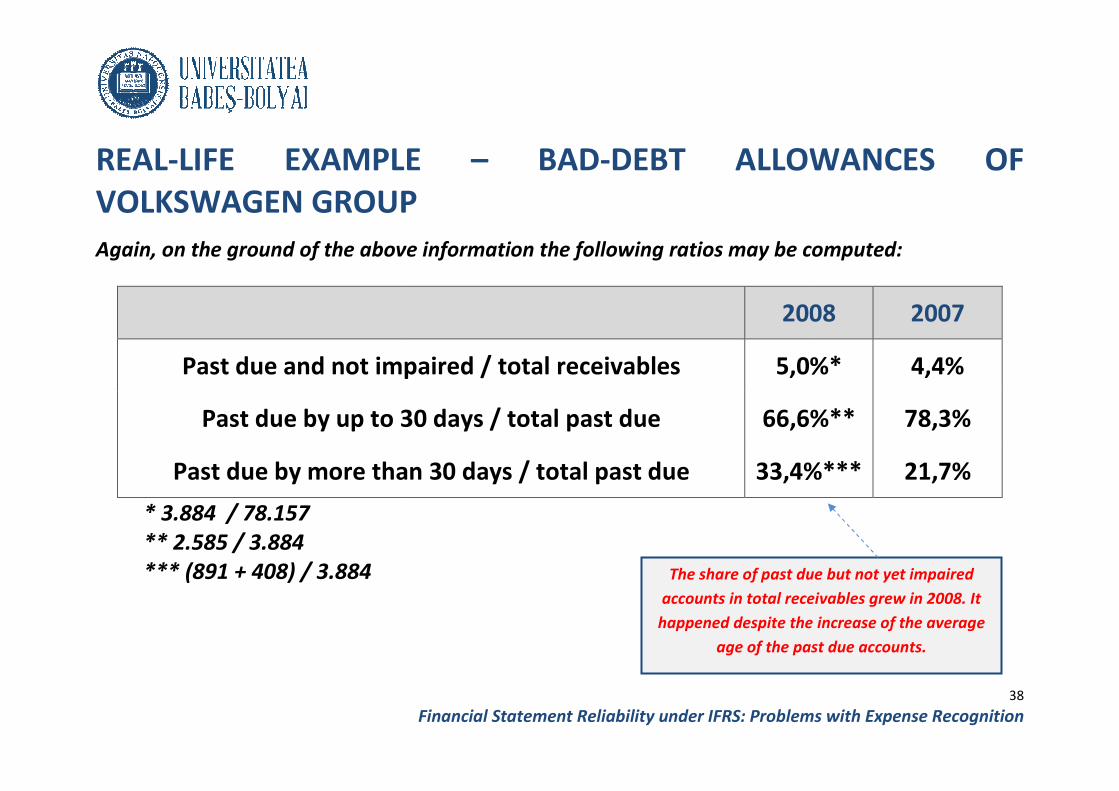

On the ground of the above information the following ratios may be computed

All past due (impaired and not impaired) /

total receivables

Past due and impaired / total past due

* (3.884 + 2.553) / 78.157

** (3.332 + 2.474) / 75.253

*** 2.553 / (3.884 + 2.553)

**** 2.474 / (3.332 + 2.474)

The notes (on page 257) offer

receivables which are past due and not impaired:

Financial Statement Reliability under IFRS: Problems with Expense Recognition

LIFE EXAMPLE – BAD-DEBT ALLOWANCES

VOLKSWAGEN GROUP

On the ground of the above information the following ratios may be computed

2008

All past due (impaired and not impaired) /

total receivables 8,2%*

Past due and impaired / total past due 39,7%***

** (3.332 + 2.474) / 75.253

*** 2.553 / (3.884 + 2.553)

**** 2.474 / (3.332 + 2.474)

the following more insightful data about the age structure of

receivables which are past due and not impaired:

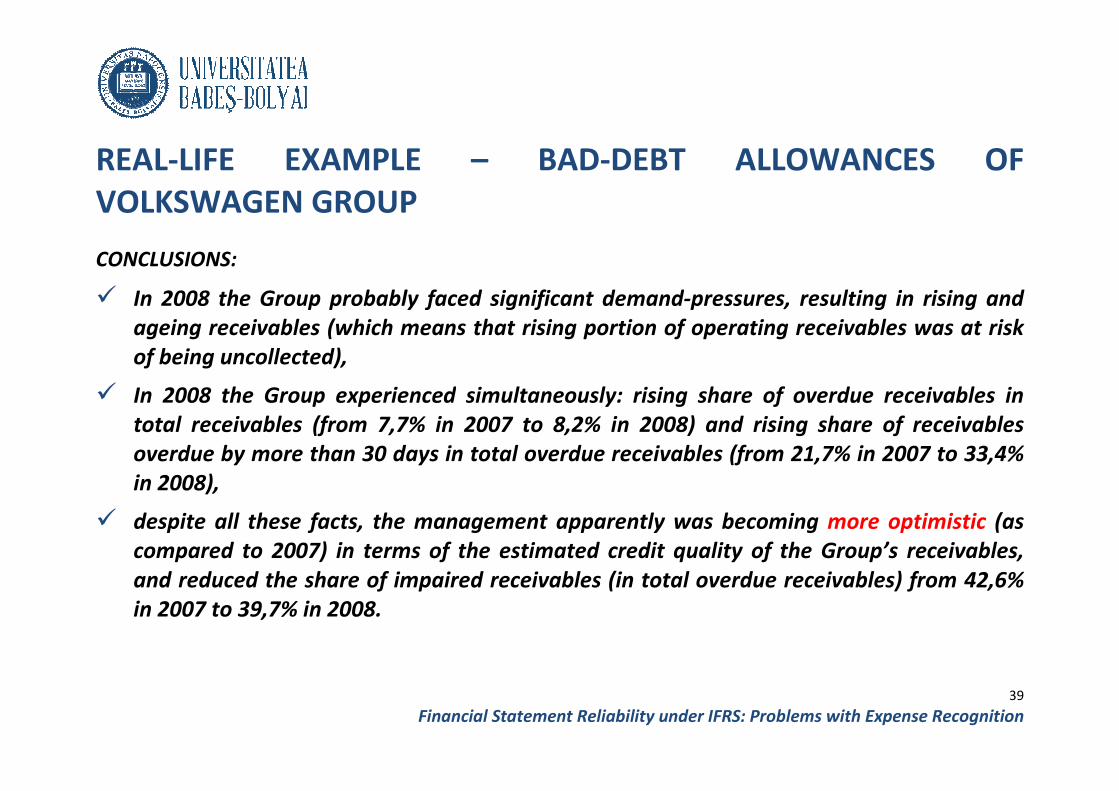

The share of past due accounts in total

receivables grew in 2008. Despite it, the share

of past due and impaired in total past due fell.

36

: Problems with Expense Recognition

DEBT ALLOWANCES OF

On the ground of the above information the following ratios may be computed:

2008 2007

8,2%* 7,7%**

39,7%*** 42,6%****

more insightful data about the age structure of