Embed Size (px)

Citation preview

Fin 4200 Project

Jessi Sagner

11/15/11

All Option information is outlined in appendix A

Option Strategy

The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

to maturity. This is similar to a straddle except the times to maturity are different. I have named it the

“ladle” strategy because the scenario graph (included in the appendix) resembles a soup ladle. For the

strategy I went long a $65 November Call Option and long a $65 December Put Option. This would be a

good neutral risk strategy because there is limited loss (because both the put and call carry a limited

loss), some limited gains when the put is in the money, and unlimited gains when the call is in the

money. This strategy allows people who are risk averse to break even as soon as the stock price rises to

above $79.32 (the current stock price) and to make a profit as soon as the stock price drops to about

$48 as the graph illustrates. All loses in between those two numbers are limited. Also, the delta of this

strategy is 92.45% showing that the overall portfolio is deep in the money and would be a wise a

strategy to pursue.

Graph in Appendix B

Black Scholes Formula

a. Determining Volatility

My calculated historical volatility from 40 days of data came out to 35%. I also calculated the

implied volatilities of eight options using Derivagem . The calculated volatilities are shown in the table

below:

Maturity Month Type of Option Strike Price Implied Volatility

November Call $90 (Out of the Money) 32.61%

November Call $65 (In the Money) 84.63%

November Put $55 (Out of the Money) 73.21%

November Put $87.5 (In the Money) 32.65%

December Call $85 (Out of the Money) 25.75%

December Call $80 (At the Money) 29.12%

December Put $65 (Out of the Money) 43.34%

December Put $87.5 (In the Money) 26.56%

Most of the volatilities are between 25% and 45%, however there are two major outliers

(73.21% and 84.63%) which are taken from a November call and put option respectively. I believe the

main cause for these inconsistencies are how far from “at the money” they are compared to the other

options. While most of the options have strike prices within about $10 from the stock price these two

options are $15 and $25 from the stock price. The reason that the out of the money put option in

November has a much higher volatility than the out of the money put option in December is because

dividends will be paid in November.

My calculated historical volatility seems to be relatively accurate with respect to the majority of

the implied volatilities (which lay between 25% and 45%). The historical number of 35% is exactly in the

middle of these to numbers, which leads me to believe it is a good measure of comparison when

deciding what percentage to use to calculate my option prices.

The average of these implied volatilities and my historical calculation comes out to 42.5%. I have

chosen to discard the biggest outlier (84.63%) which gives me a new average of 37.23%. Because my

historical volatility was accurate and right in the middle of the majority of the volatilities, I feel this

average is much more likely volatility and I feel more comfortable using the average without the major

outlier.

b. Pricing Options

The following table illustrates the calculated option price versus the actual option price. An

explanation of the information is found below.

Maturity Month

Type of Option

Strike Price Black-Scholes

Option Price

Market Option Price

Difference in Black-Scholes vs. Market

Price

November Call $90 (Out of the Money)

$.11 $.07 $.04

November Call $65 (In the Money)

$14.01 $14.55 -$.54

November Put $55 (Out of the Money)

$.0000009 $.03 -$.03

November Put $87.5 (In the Money)

$21.00 $22.5 -$1.5

December Call $85 (Out of the Money)

$1.31 $.79 $.52

December Call $80 (At the Money)

$2.94 $2.63 $.35

December Put $65 (Out of the Money)

$.105 $.51 -$.405

December Put $87.5 (In the Money)

$11.46 $11.55 -$.09

I used Derivagem to calculate option prices and compared those to the actual option prices. The

difference between the calculated and actual option prices can lead us to some observations about

using the Black Scholes Method to price options. Some consistencies found when pricing these options

are as follows: all puts were undervalued; all “in the money” options were undervalued; all out of the

money call options (including the “at the money” because in reality it is slightly “out of the money”)

were over-valued. With those biases being stated, the formula still comes within an acceptably accurate

range (all but one are within $1 from the actual price) and can be a reliable source for option pricing –

especially when one keeps in mind the small biases the formula creates.

Binomial Option Pricing & Early Exercise

Maturity Month

Type of Option

Strike Price Black Scholes Option Price

Market Option Price

Binomial Option Price

Difference Between B.S.

and BOPM

November Call $90 (Out of the Money)

$.11 $.07 $.11

$0

November Call $65 (In the Money)

$14.01 $14.55 $14.01 $0

November Put $55 (Out of the Money)

$.0000009 $.03 $.0000006 $.0000003

November Put $87.5 (In the Money)

$21.54 $22.5 $21.55 $.01

December Call $85 (Out of the Money)

$1.31 $.79 $1.30 $.01

December Call $80 (At the Money)

$2.94 $2.63 $2.95

$.01

December Put $65 (Out of the Money)

$.105 $.51 $.104 $.001

December Put $87.5 (In the Money)

$11.46 $11.55 $11.47 $.01

I used 500 steps to calculate the option price using the Binomial Option Pricing Method. The calculated

Binomial Option Prices are basically equivalent to the ones calculated using the Black-Scholes method.

The value of early exercise was determined up to the tenth step only.

There is a very small difference (if any) between all of the Black-Scholes option prices versus the

Binomial Option Pricing Method Option prices. Because BOPM takes in to consideration dividends while

Black-Scholes does not, the ‘slim-to-none’ differences between the two show that there was no case in

which it was best to exercise the option early

The Greeks

The following is a brief description of what each of the Greek symbols measure with respect to options.

Delta: measures the amount of change in the value of an option due to a change in the value of the

stock.

Gamma: measures the amount of change in delta due to a change in the value of the stock.

Vega: measures the change in the value of an option due to a change in volatility.

Theta: measures the change in the value of an option due to a change in time.

Rho: measures the change in a value of an option due to a change in interest rate.

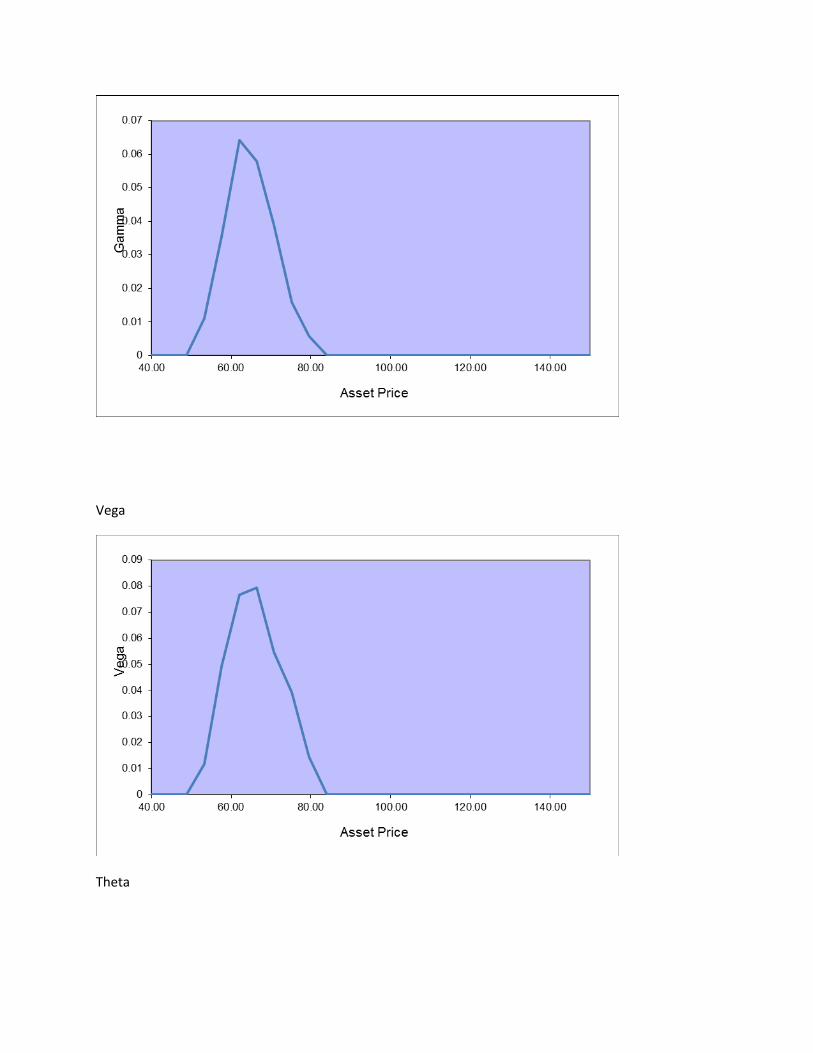

Please refer to the appendix C to see the full set of examples of these “Greek” graphs calculated from

my options. Graphs for Volatility and Time to Maturity are in appendix D. The general shapes of all of

these graphs are described below.

Graphing Delta:

When the asset price is out of the money (both for calls and puts) delta moves to zero. This is because

when an option is out of the money it will expire worthless and no matter what it the value of the call

will not change as the asset price changes as long as the asset price remains out of the money. As the

asset price moves to at the money, delta increases to .5 (for calls) or decreases to -.5 (for puts). The

reason for the .5 is because the stock has about a 50/50 chance of moving either to in the money of out

of the money so the option value is somewhat receptive to changes in the underlying stock price. In the

money options consist of a delta of about 1 (or -1 for puts). As an option moves in the money it is very

likely that it will end up being exercised, as the option gets deeper in the money the option value gets

greater and greater, so, the value of the option is receptive to changes in stock price creating a larger

delta (1).

Graphing Gamma:

When an option is either very deep out of the money, or very deep in the money, gamma is zero. This is

because delta does not change at those two points. When you are already deep in the money it doesn’t

matter if you go even deeper, you still have a delta of one. The same is true for deep out of the money,

it doesn’t matter how deep or “shallow” you go, delta is still zero. Delta does change though when an

option price nears the strike price (is at the money). This causes a peak in the gamma graph at the

money. As the option moves away from the strike price in either direction gamma begins to decrease

because delta is less responsive to changes in underlying stock price.

Graphing Vega:

As volatility increases, the most affected options are at the money. This is because as volatility increases

or decreases option price is very affected and can fluctuate in either direction, causing a large vega.

When a call option is out of the money, it doesn’t matter how far out of the money it is because you

have downside protection so therefore vega goes right to zero. In the money call options are affected a

little bit more than out of the money options because as volatility increases you have unlimited gains,

but you could also be moving out of the money creating a loss. So, the change in the value of an in the

money call option is relatively sensitive to a change in volatility, but not nearly as much so as at the

money options are. The opposite argument is true for in and out of the money puts.

Graphing Theta:

As time changes, the most affected options are at the money. When you have an at the money option it

experiences the greatest time decay leading to a large theta. Out of the money calls and in the money

puts experience very little time decay (it takes a very short amount of time to go from a small strike

price to zero) so their theta is near zero. For in the money calls and out of the money puts theta is

between the previous two scenarios. Each day the option gets closer to exercise (and in the case of ITM

calls/OTM puts they will be exercised) the more value it is losing because of time decay and time value

of money. So a shorter time for ITM options is better because you want to exercise and get the money

from the position instead of letting the option lose value.

Graphing Rho:

Out of the money options tend to have a rho around zero. This is because changing interest rates don’t

really affect OTM options since you wouldn’t exercise them regardless of the interest rate. As you move

to at the money and then further in the money, and options rho increases in the absolute sense (puts

move from zero to larger negative numbers all the way to -1). The more money you have (the more in

the money your option is) the more it will grow with respect to interest rates. So the deeper in the

money the option is the more sensitive it is to changes in interest rates which in turn increases the

option’s rho.

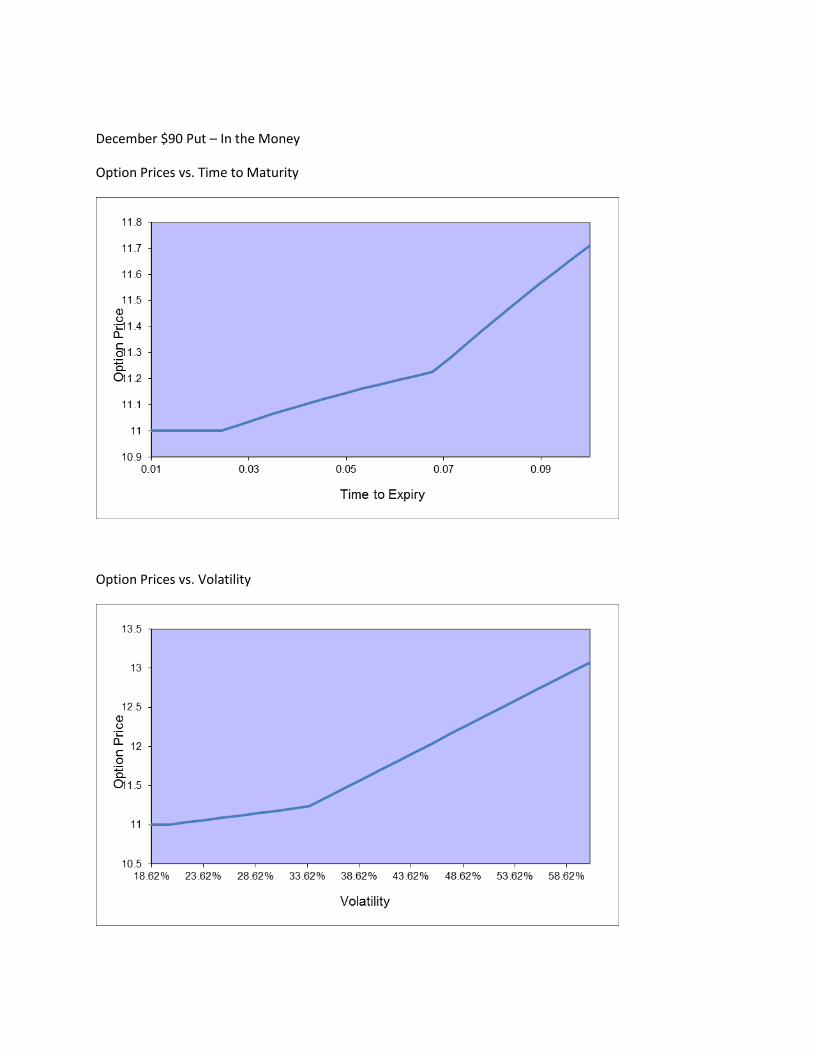

Volatility:

The volatility versus option price graph of at, in, and, out of the money options shows a direct

relationship between option price and volatility. As the option price increases so does volatility. The out

of the money option does not increase in price until it hits about 30% volatility and then has a constant

slop until 50% at which point it takes off and the option price increases drastically. As the option price is

increases it is become less and less out of the money which is why it becomes affected by volatility. The

in the money option has a constant volatility until about 33% at which point the graph slowly increases

with the option price. When an option becomes more in the money it is more sensitive to changes in

volatility which is why as the price increases so does volatility. The at the money option has a straight

slope and does not falter as option price increases. As an at the money call option price increases it

continually becomes closer to in the money which is why the graph increases at a constant rate.

Time to Maturity:

All three types of options show an increase in option price over time – some of these (OTM)

shows a slower increase, but an increase none the less. As you increase time to maturity all options

become more valuable. The reason behind this is when you increase time to maturity you increase all

the opportunities you have to exercise your option. With American options you not only have your

expiration date on which you can exercise, but every day in between. So with every gained opportunity

(day, hour, minute, second) you get an increase in that options value.

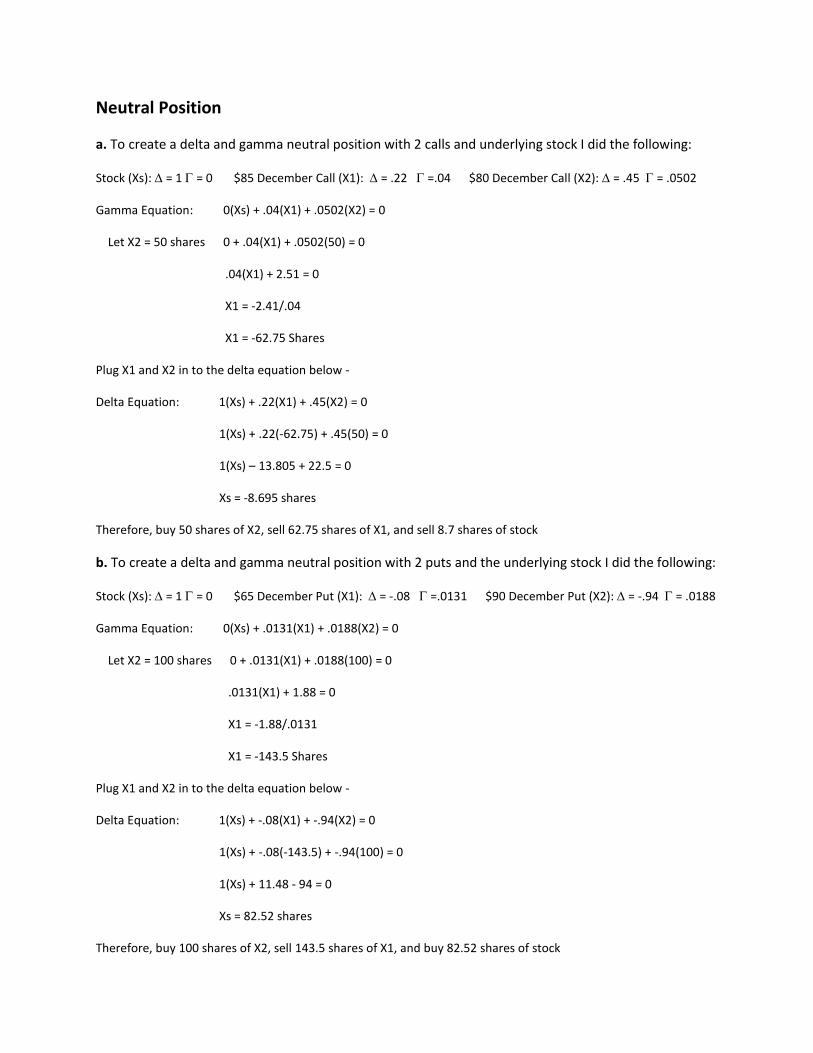

Neutral Position

a. To create a delta and gamma neutral position with 2 calls and underlying stock I did the following:

Stock (Xs): = 1 = 0 $85 December Call (X1): = .22 =.04 $80 December Call (X2): = .45 = .0502

Gamma Equation: 0(Xs) + .04(X1) + .0502(X2) = 0

Let X2 = 50 shares 0 + .04(X1) + .0502(50) = 0

.04(X1) + 2.51 = 0

X1 = -2.41/.04

X1 = -62.75 Shares

Plug X1 and X2 in to the delta equation below -

Delta Equation: 1(Xs) + .22(X1) + .45(X2) = 0

1(Xs) + .22(-62.75) + .45(50) = 0

1(Xs) – 13.805 + 22.5 = 0

Xs = -8.695 shares

Therefore, buy 50 shares of X2, sell 62.75 shares of X1, and sell 8.7 shares of stock

b. To create a delta and gamma neutral position with 2 puts and the underlying stock I did the following:

Stock (Xs): = 1 = 0 $65 December Put (X1): = -.08 =.0131 $90 December Put (X2): = -.94 = .0188

Gamma Equation: 0(Xs) + .0131(X1) + .0188(X2) = 0

Let X2 = 100 shares 0 + .0131(X1) + .0188(100) = 0

.0131(X1) + 1.88 = 0

X1 = -1.88/.0131

X1 = -143.5 Shares

Plug X1 and X2 in to the delta equation below -

Delta Equation: 1(Xs) + -.08(X1) + -.94(X2) = 0

1(Xs) + -.08(-143.5) + -.94(100) = 0

1(Xs) + 11.48 - 94 = 0

Xs = 82.52 shares

Therefore, buy 100 shares of X2, sell 143.5 shares of X1, and buy 82.52 shares of stock

Arbitrage Strategy

This arbitrage consists of a December out of the money call option, underlying stock, and the

riskless security. S =$ 79.32 x = $85 C = $1.31 R = .99 t = .0833

The following formula proves the arbitrage strategy:

C = S- XR^-t

1.31 = 79.32 – 85(.0=99)^-.0833

1.31 = [79.32 – 85.07] -1

1.31 = -79.32 + 85.07

1.

31 < 5.75

Arbitrage Table:

This arbitrage only makes sense if you have a very bearish view on the market. You begin with a

negative cash flow because the option is out of the money to begin with. If stock price at maturity (St)

ends up greater than the strike price (x) your total cash flow is zero. This is because you only receive the

difference between St and x, and x from lending at the risk free rate, while you have to pay someone

back the stock price at maturity because you used it to short sell the stock at time zero. However, if the

stock price at maturity is less than the strike price you end up with a positive cash flow. The positive

cash flow is a result of paying St for short selling the stock at time zero and gaining back x from lending it

at time zero.

This isn’t a very good arbitrage because you begin with a negative cash flow and in one scenario end up

with a zero cash flow at time T (maturity). So, unless you are sure that the market will go down it would

be unwise to pursue this arbitrage strategy.

0 St>x 90>85 St<x 60<85

Buy Call -1.31 90-85 = 5 0

Short Sell Stock 79.32 -90 -60

Lend XR^-t -85.07 85 85

Total: -7.06 0 15

Appendix:

A.

Chosen Option's Information

1 2 3 4 5 6 7 8

Expiration Month November November November November December December December December

Option Type Call Call Put Put Call Call Put Put

Strike Price $90 $65 $55 $100 $85 $80 $65 $90

in/at/out Out In Out In In At Out In

Option Price $0.07 $14.55 $0.03 $22.50 $0.79 $2.63 $0.51 $11.55

Delta 0.02 0.92 -0.01 -0.99 0.22 0.45 -0.08 -0.94

Gamma 0.0125 0.0151 0.0051 0.004 0.04 0.0502 0.0131 0.0188

Vega 0.0084 0.0197 0.0025 0.0163 0.0774 0.1017 0.0402 0.0297

Theta 0.0109 0.0723 0.0069 0.0103 0.0283 0.0411 0.0226 0.0093

Rho 0.0581 1.5052 -0.0183 -2.3998 1.6174 3.5535 -0.7064 -5.5719

Interest Rate 0.00% 0.00% 0.00% 0.00% 0.05% 0.05% 0.05% 0.05%

Dividends 0.55 0.55 0.55 0.55 0 0 0 0

B.

Option Strategy Scenario Graph

C.

December $90 Put (In the Money)

Delta

Gamma

Vega

Theta

Rho

C.

December $85 Call Option:

Delta

Gamma

Vega

Theta

Rho

C.

December $85 Call Option:

Delta

Gamma

Vega

Theta

Rho

C.

December $80 Call (At the Money)

Delta

Gamma

Vega

Theta

Rho

C.

December $65 Put (Out of the Money)

Delta

Gamma

Vega

Theta

Rho

C.

Delta vs. Asset Price Graphs

Delta vs. Asset Price $65 December Put (out of the money)

Delta vs. Asset Price $90 December Put (in the money)

Delta vs. Asset Price $80 December Call (at the money)

Delta vs. Asset Price $85 December Call (out of the money)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

65.00 70.00 75.00 80.00 85.00 90.00 95.00

Delta

Asset Price

D.

December $65 Put – Out of the Money

Option Price vs. Time to Expiration

Option Price vs. Volatility

December $90 Put – In the Money

Option Prices vs. Time to Maturity

Option Prices vs. Volatility

December $80 Call – At the Money

Option Prices vs. Time to Maturity

Option Prices vs. Volatility