Embed Size (px)

Citation preview

Filing at a Glance Company: Mutual of Enumclaw Insurance Company

Product Name: Businessowners

State: Oregon

TOI: 05.0 CMP Liability and Non-Liability

Sub-TOI: 05.0002 Businessowners

Filing Type: Form/Rate/Rule

Date Submitted: 05/18/2016

SERFF Tr Num: ENUX-130575485

SERFF Status: Closed-Approved

State Tr Num: ENUX-130575485

State Status: Review completed

Co Tr Num: 01926

Effective DateRequested (New):

On Approval

Effective DateRequested (Renewal):

On Approval

Author(s): Brianne Dahl, Donna Wilson

Reviewer(s): Lorna Keyes (primary), David Dahl

Disposition Date: 06/20/2016

Disposition Status: Approved

Effective Date (New): 06/20/2016

Effective Date (Renewal): 06/20/2016

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

General Information

Company and Contact

Filing Fees

State Specific

Project Name: Hotel/Motel Endorsement Status of Filing in Domicile: Pending

Project Number: 01926 Domicile Status Comments:

Reference Organization: Reference Number:

Reference Title: Advisory Org. Circular:

Filing Status Changed: 06/20/2016

State Status Changed: 06/20/2016 Deemer Date:

Created By: Brianne Dahl Submitted By: Brianne Dahl

Corresponding Filing Tracking Number:

Filing Description:

With this filings we are adding the ISO classifications for Hotel/Motel risks. We are adding a new hotel/motel enhancementendorsement option as well as making some editorial and clarification revisions to a few additional rules. Refer to theexplanatory memo for additional details.

Filing Contact InformationDonna Wilson, Commercial ProductManager

1460 Wells Street

Enumclaw, WA 98022

800-366-5551 [Phone] 3237 [Ext]

866-546-0223 [FAX]

Filing Company InformationMutual of Enumclaw InsuranceCompany

1460 Wells Street

Enumclaw, WA 98022

(360) 825-2591 ext. [Phone]

CoCode: 14761

Group Code: 333

Group Name:

FEIN Number: 91-0217580

State of Domicile: Oregon

Company Type:

State ID Number:

Fee Required? No

Retaliatory? No

Fee Explanation:

Have you reviewed the General Instructions attached as a separate pdf at the bottom of the General Instructions page?: yesDid you read the instructions regarding how to enter the form number and edition date in the Forms Schedule tab?: yesDid you realize Oregon does not respond to Status Requests thru SERFF?: yesPlease confirm that you have read the Fraud Bulletin 2010-3 located at:http://www.cbs.state.or.us/external/ins/bulletins/bulletin2010-03.pdf: yesFor PC files: Mandatory requirement as stated in the product standards: You must attach under the SupportingDocumentation tab any Oregon approved amendments that will be used to bring the filed forms into compliance with Oregonlaws. For example: Fraud Warning, Domestic Partnership, Cancellation/Non-renewal. This would include an endorsementapproved for an advisory organization. Confirm that this has been done.: yes

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

Correspondence Summary DispositionsStatus Created By Created On Date SubmittedApproved Lorna Keyes 06/20/2016 06/20/2016

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

Disposition

Disposition Date: 06/20/2016

Effective Date (New): 06/20/2016

Effective Date (Renewal): 06/20/2016

Status: Approved

Comment: Department of Consumer and Business ServicesDivision of Financial Regulation – Product Regulation - Rates and Forms

Invitation to Comment on Quality of Service from the Division of Financial Regulation

We strive to provide excellent customer service at all times and invite you to provide written comment regarding your filing experience.

Instructions for submitting a filing are on our website at http://www.oregon.gov/DCBS/insurance/insurers/rates-forms/Pages/rates-forms.aspx or contained withinSERFF under the Filing Rules tab. Filings that contain errors may be returned without having been accepted for review. Filing errors that are considered include: formnumbers that do not match, forms attached under the wrong tab, or missing required documents. If we allow the company to correct a filing error it must be correctedwithin 24 hours or the filing will be rejected for “no response”.

If we contact you about compliance-related issues or corrections that need to be made to your filing, we must receive your complete response within 10 calendar days.

Any disapproval for reasons other than filing errors must be supported by our product standards. If you believe we have failed to meet our performance objectives oryou believe we have provided outstanding performance, please let us know. We value your comments and will use this information to improve our service.

You may request that your comments be kept confidential; however, be aware that confidential feedback limits our ability to follow up, as your concerns cannot beshared with staff. If you are not requesting confidentially, please include the SERFF or state tracking number with your comments.

Please explain if the Division met its objective. Was your experience positive?

Comments:

Thank you,Eric Cutler, CPCU, CIC, AINS, LPCSDivision of Financial Regulation

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

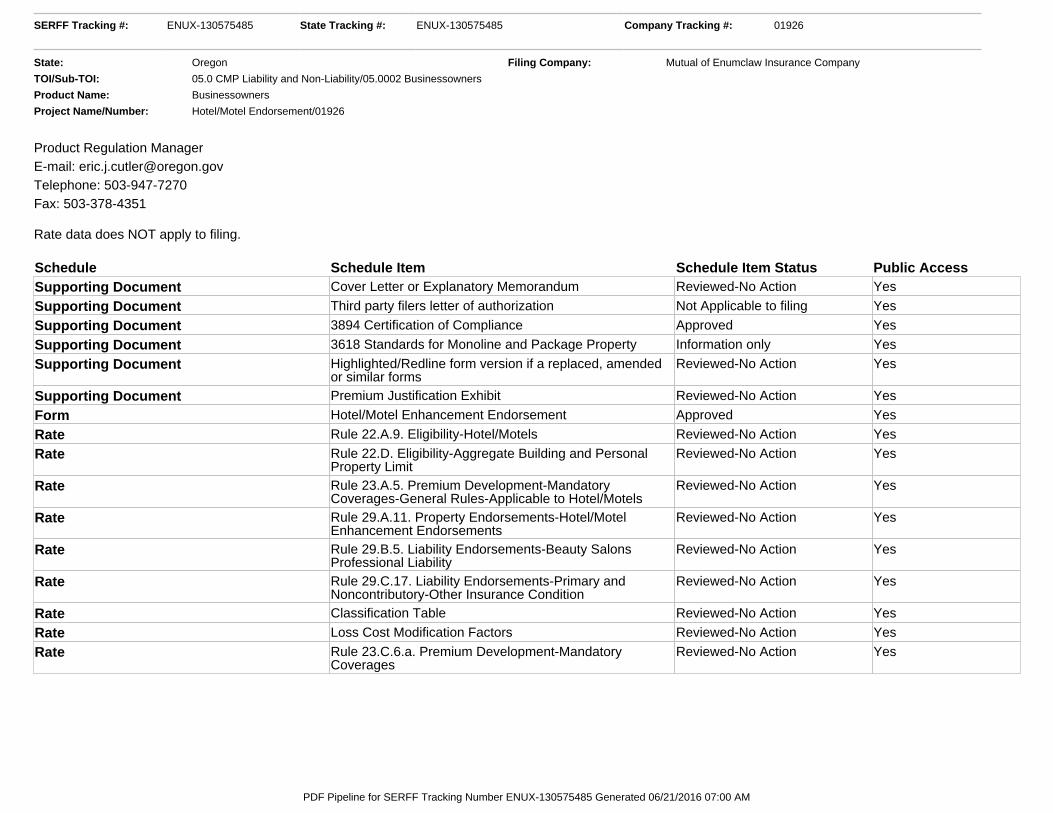

Product Regulation ManagerE-mail: [email protected]: 503-947-7270Fax: 503-378-4351

Rate data does NOT apply to filing.

Schedule Schedule Item Schedule Item Status Public AccessSupporting Document Cover Letter or Explanatory Memorandum Reviewed-No Action Yes

Supporting Document Third party filers letter of authorization Not Applicable to filing Yes

Supporting Document 3894 Certification of Compliance Approved Yes

Supporting Document 3618 Standards for Monoline and Package Property Information only Yes

Supporting Document Highlighted/Redline form version if a replaced, amendedor similar forms

Reviewed-No Action Yes

Supporting Document Premium Justification Exhibit Reviewed-No Action Yes

Form Hotel/Motel Enhancement Endorsement Approved Yes

Rate Rule 22.A.9. Eligibility-Hotel/Motels Reviewed-No Action Yes

Rate Rule 22.D. Eligibility-Aggregate Building and PersonalProperty Limit

Reviewed-No Action Yes

Rate Rule 23.A.5. Premium Development-MandatoryCoverages-General Rules-Applicable to Hotel/Motels

Reviewed-No Action Yes

Rate Rule 29.A.11. Property Endorsements-Hotel/MotelEnhancement Endorsements

Reviewed-No Action Yes

Rate Rule 29.B.5. Liability Endorsements-Beauty SalonsProfessional Liability

Reviewed-No Action Yes

Rate Rule 29.C.17. Liability Endorsements-Primary andNoncontributory-Other Insurance Condition

Reviewed-No Action Yes

Rate Classification Table Reviewed-No Action Yes

Rate Loss Cost Modification Factors Reviewed-No Action Yes

Rate Rule 23.C.6.a. Premium Development-MandatoryCoverages

Reviewed-No Action Yes

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

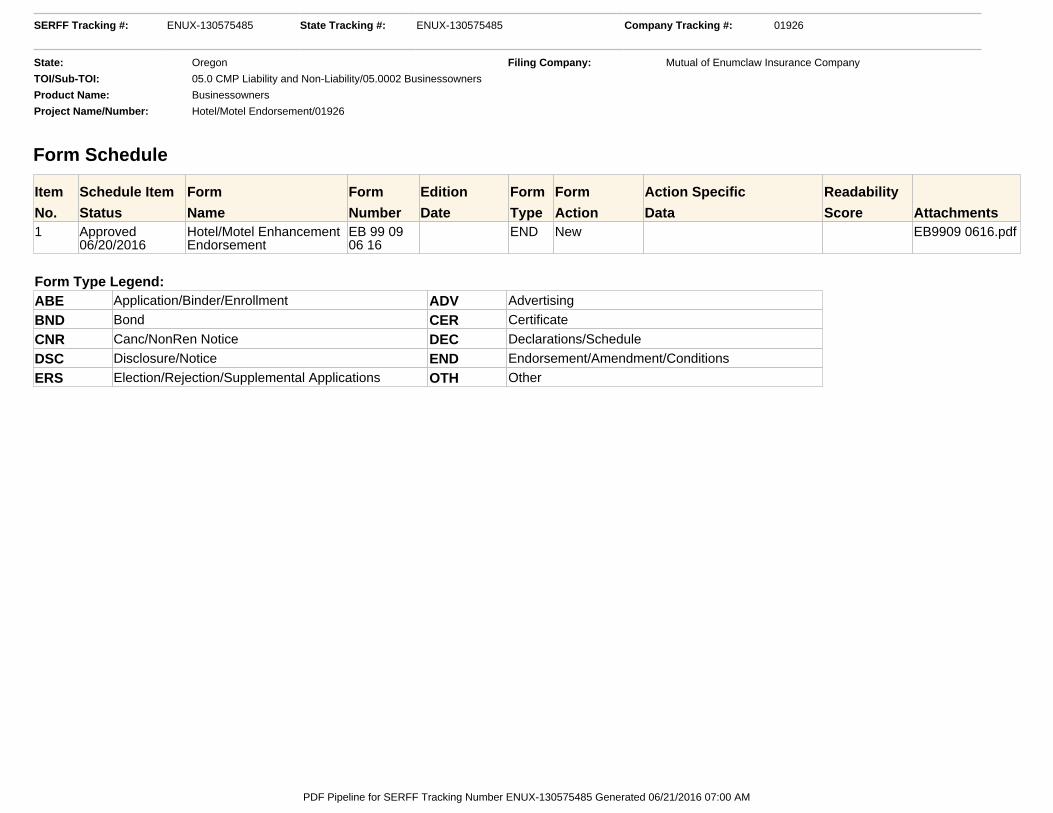

Form Schedule

Item

No.

Schedule Item

Status

Form

Name

Form

Number

Edition

Date

Form

Type

Form

Action

Action Specific

Data

Readability

Score Attachments1 Approved

06/20/2016Hotel/Motel EnhancementEndorsement

EB 99 0906 16

END New EB9909 0616.pdf

Form Type Legend:ABE Application/Binder/Enrollment ADV Advertising

BND Bond CER Certificate

CNR Canc/NonRen Notice DEC Declarations/Schedule

DSC Disclosure/Notice END Endorsement/Amendment/Conditions

ERS Election/Rejection/Supplemental Applications OTH Other

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

Rate Information Rate data does NOT apply to filing.

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

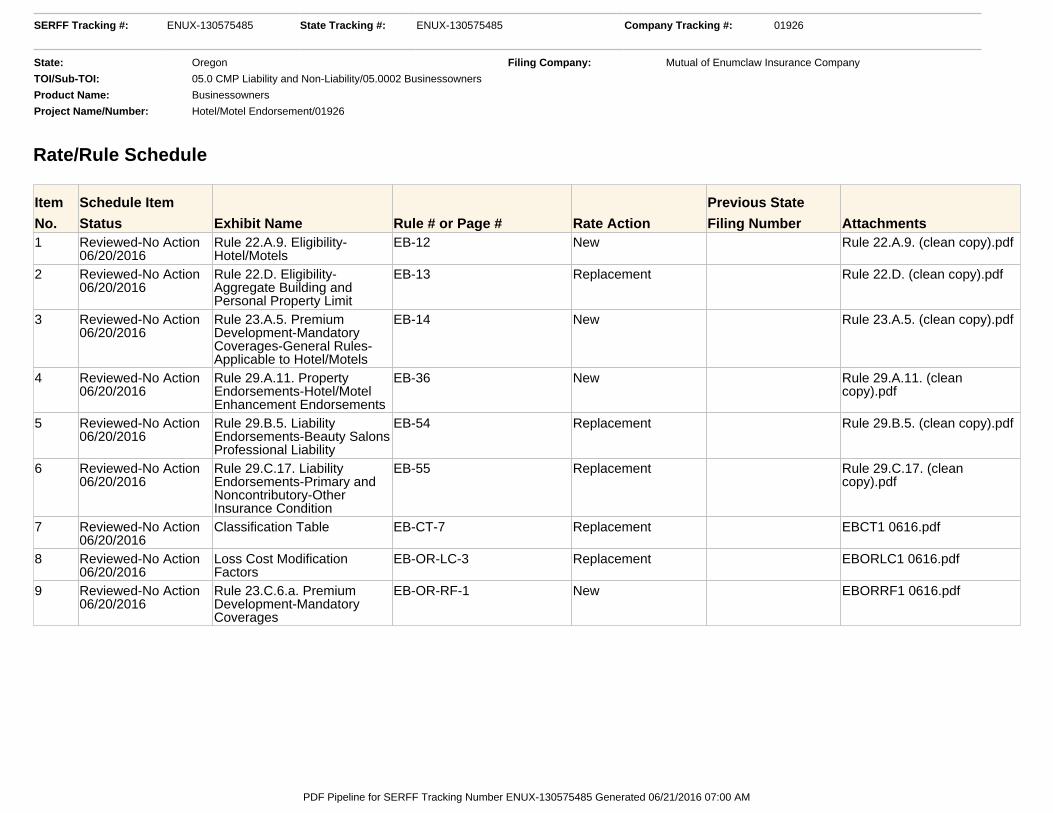

Rate/Rule Schedule

Item

No.

Schedule Item

Status Exhibit Name Rule # or Page # Rate Action

Previous State

Filing Number Attachments1 Reviewed-No Action

06/20/2016Rule 22.A.9. Eligibility-Hotel/Motels

EB-12 New Rule 22.A.9. (clean copy).pdf

2 Reviewed-No Action06/20/2016

Rule 22.D. Eligibility-Aggregate Building andPersonal Property Limit

EB-13 Replacement Rule 22.D. (clean copy).pdf

3 Reviewed-No Action06/20/2016

Rule 23.A.5. PremiumDevelopment-MandatoryCoverages-General Rules-Applicable to Hotel/Motels

EB-14 New Rule 23.A.5. (clean copy).pdf

4 Reviewed-No Action06/20/2016

Rule 29.A.11. PropertyEndorsements-Hotel/MotelEnhancement Endorsements

EB-36 New Rule 29.A.11. (cleancopy).pdf

5 Reviewed-No Action06/20/2016

Rule 29.B.5. LiabilityEndorsements-Beauty SalonsProfessional Liability

EB-54 Replacement Rule 29.B.5. (clean copy).pdf

6 Reviewed-No Action06/20/2016

Rule 29.C.17. LiabilityEndorsements-Primary andNoncontributory-OtherInsurance Condition

EB-55 Replacement Rule 29.C.17. (cleancopy).pdf

7 Reviewed-No Action06/20/2016

Classification Table EB-CT-7 Replacement EBCT1 0616.pdf

8 Reviewed-No Action06/20/2016

Loss Cost ModificationFactors

EB-OR-LC-3 Replacement EBORLC1 0616.pdf

9 Reviewed-No Action06/20/2016

Rule 23.C.6.a. PremiumDevelopment-MandatoryCoverages

EB-OR-RF-1 New EBORRF1 0616.pdf

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

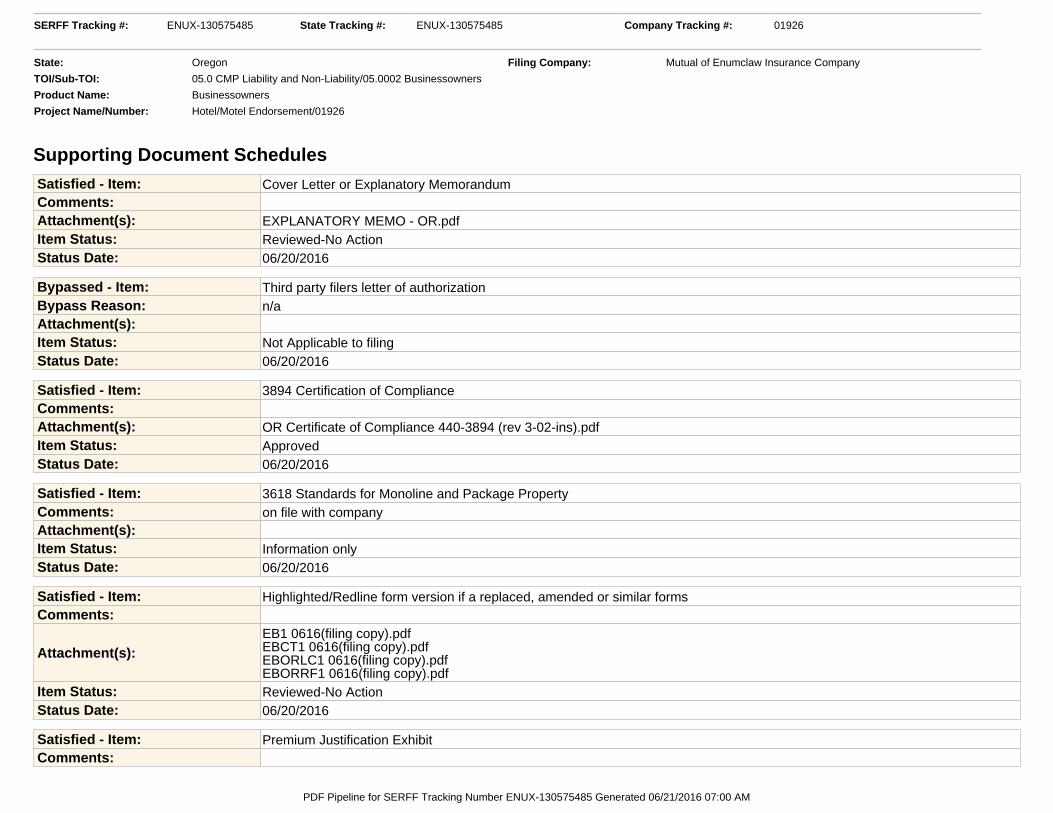

Supporting Document Schedules Satisfied - Item: Cover Letter or Explanatory MemorandumComments:Attachment(s): EXPLANATORY MEMO - OR.pdfItem Status: Reviewed-No ActionStatus Date: 06/20/2016

Bypassed - Item: Third party filers letter of authorizationBypass Reason: n/aAttachment(s):Item Status: Not Applicable to filingStatus Date: 06/20/2016

Satisfied - Item: 3894 Certification of ComplianceComments:Attachment(s): OR Certificate of Compliance 440-3894 (rev 3-02-ins).pdfItem Status: ApprovedStatus Date: 06/20/2016

Satisfied - Item: 3618 Standards for Monoline and Package PropertyComments: on file with companyAttachment(s):Item Status: Information onlyStatus Date: 06/20/2016

Satisfied - Item: Highlighted/Redline form version if a replaced, amended or similar formsComments:

Attachment(s):EB1 0616(filing copy).pdfEBCT1 0616(filing copy).pdfEBORLC1 0616(filing copy).pdfEBORRF1 0616(filing copy).pdf

Item Status: Reviewed-No ActionStatus Date: 06/20/2016

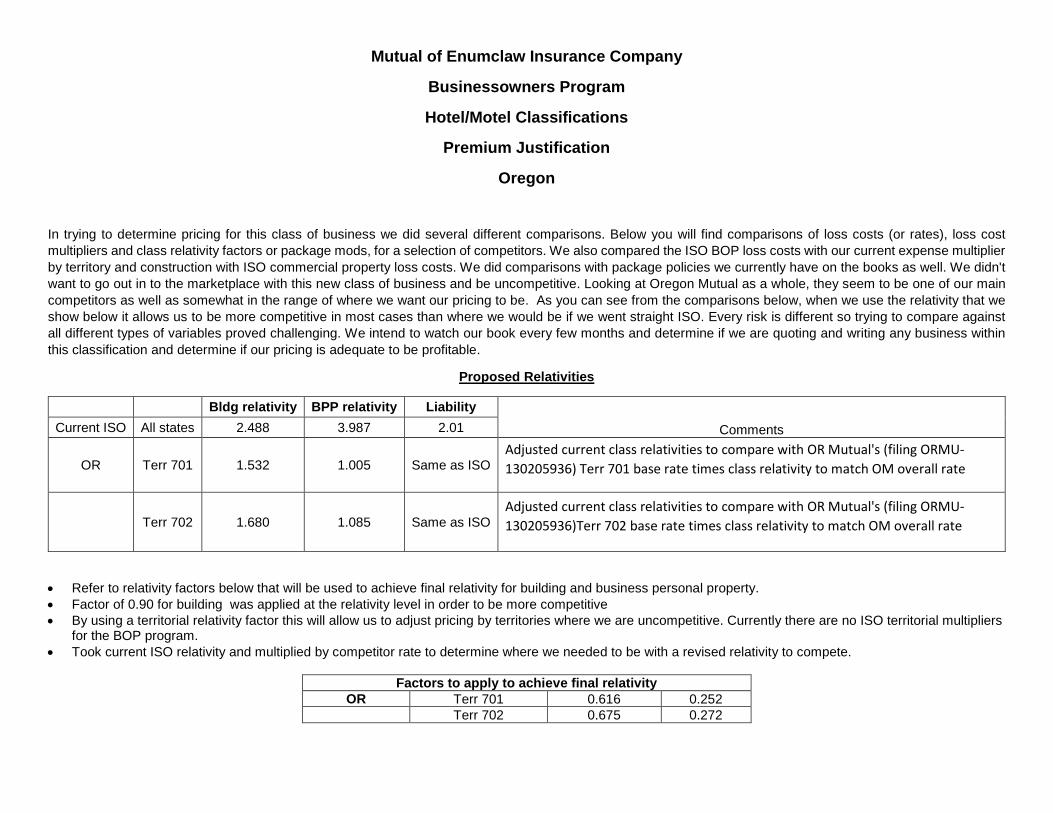

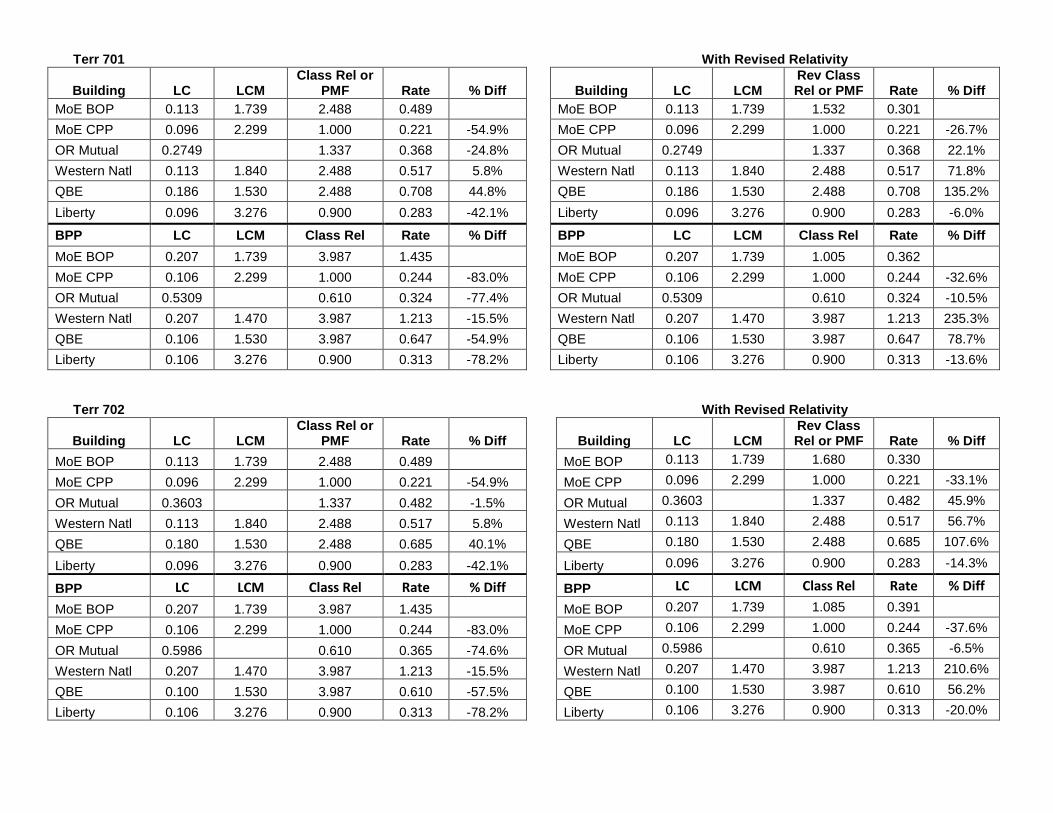

Satisfied - Item: Premium Justification ExhibitComments:

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

Attachment(s): Premium justification exhibit - OR.pdfItem Status: Reviewed-No ActionStatus Date: 06/20/2016

SERFF Tracking #: ENUX-130575485 State Tracking #: ENUX-130575485 Company Tracking #: 01926

State: Oregon Filing Company: Mutual of Enumclaw Insurance Company

TOI/Sub-TOI: 05.0 CMP Liability and Non-Liability/05.0002 Businessowners

Product Name: Businessowners

Project Name/Number: Hotel/Motel Endorsement/01926

PDF Pipeline for SERFF Tracking Number ENUX-130575485 Generated 06/21/2016 07:00 AM

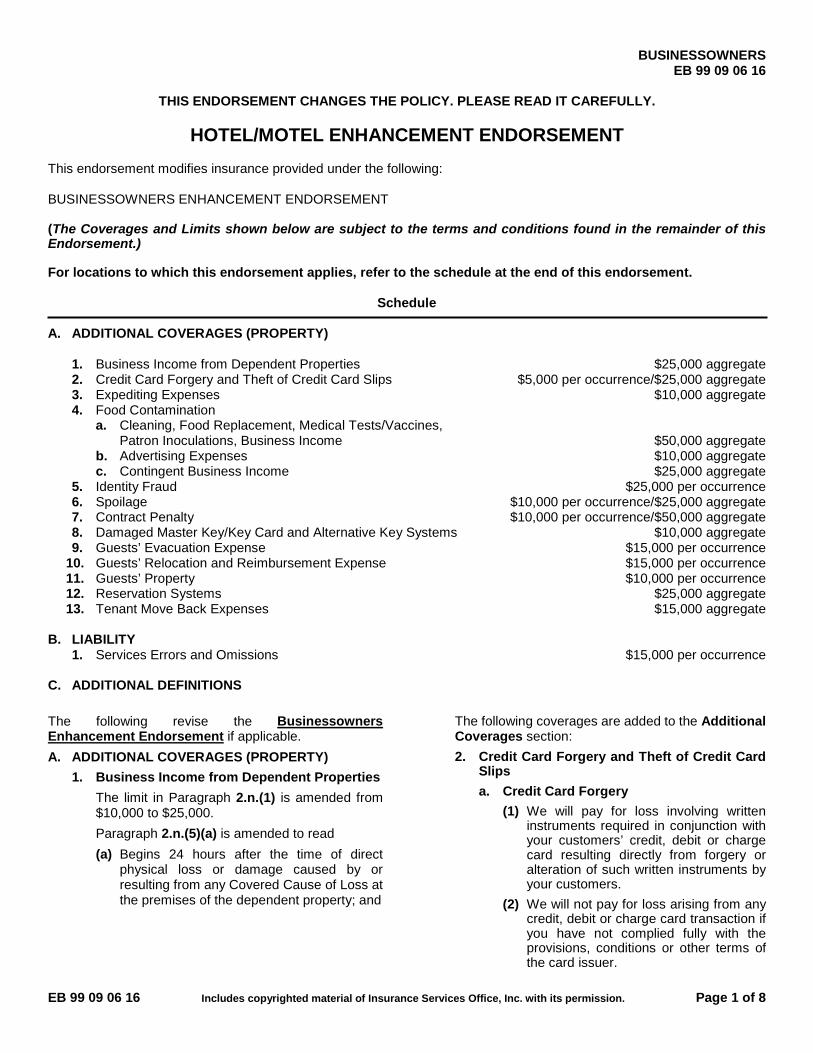

BUSINESSOWNERS EB 99 09 06 16

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 1 of 8

HOTEL/MOTEL ENHANCEMENT ENDORSEMENT

This endorsement modifies insurance provided under the following: BUSINESSOWNERS ENHANCEMENT ENDORSEMENT (The Coverages and Limits shown below are subject to the terms and conditions found in the remainder of this Endorsement.) For locations to which this endorsement applies, refer to the schedule at the end of this endorsement.

Schedule A. ADDITIONAL COVERAGES (PROPERTY)

1. Business Income from Dependent Properties $25,000 aggregate 2. Credit Card Forgery and Theft of Credit Card Slips $5,000 per occurrence/$25,000 aggregate 3. Expediting Expenses $10,000 aggregate 4. Food Contamination

a. Cleaning, Food Replacement, Medical Tests/Vaccines, Patron Inoculations, Business Income $50,000 aggregate

b. Advertising Expenses $10,000 aggregate c. Contingent Business Income $25,000 aggregate

5. Identity Fraud $25,000 per occurrence 6. Spoilage $10,000 per occurrence/$25,000 aggregate 7. Contract Penalty $10,000 per occurrence/$50,000 aggregate 8. Damaged Master Key/Key Card and Alternative Key Systems $10,000 aggregate 9. Guests’ Evacuation Expense $15,000 per occurrence

10. Guests’ Relocation and Reimbursement Expense $15,000 per occurrence 11. Guests’ Property $10,000 per occurrence 12. Reservation Systems $25,000 aggregate 13. Tenant Move Back Expenses $15,000 aggregate

B. LIABILITY

1. Services Errors and Omissions $15,000 per occurrence C. ADDITIONAL DEFINITIONS The following revise the Businessowners Enhancement Endorsement if applicable. A. ADDITIONAL COVERAGES (PROPERTY)

1. Business Income from Dependent Properties The limit in Paragraph 2.n.(1) is amended from $10,000 to $25,000. Paragraph 2.n.(5)(a) is amended to read (a) Begins 24 hours after the time of direct

physical loss or damage caused by or resulting from any Covered Cause of Loss at the premises of the dependent property; and

The following coverages are added to the Additional Coverages section: 2. Credit Card Forgery and Theft of Credit Card

Slips a. Credit Card Forgery

(1) We will pay for loss involving written instruments required in conjunction with your customers’ credit, debit or charge card resulting directly from forgery or alteration of such written instruments by your customers.

(2) We will not pay for loss arising from any credit, debit or charge card transaction if you have not complied fully with the provisions, conditions or other terms of the card issuer.

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 2 of 8

(3) All loss caused by any person or in which that person is involved, whether the loss involves one or more instruments, is considered one occurrence.

b. Theft of Credit Card Slips (1) We will pay for loss of written instruments

required in conjunction with any credit, debit, or charge card at the described premises resulting directly from theft, meaning any act of stealing, disappearance or destruction.

(2) We will not pay for loss: (a) Resulting from accounting or

arithmetical errors or omissions; or (b) Due to the giving or surrendering of

property in any exchange or purchase.

(3) You must keep records of all written instruments so we can verify the amount of any loss or damage.

(4) All loss: (a) Caused by one or more persons; or (b) Involving a single act or series of

related acts; is considered one occurrence.

c. We will not pay for loss or damage in any one occurrence until the amount of loss or damage exceeds $100. We will then pay the amount of loss or damage in excess of $100 up to $5,000 subject to an Annual Policy Aggregate of $25,000.

3. Expediting Expenses a. We will pay necessary expediting expenses

you incur during the “period of restoration” that you would not have incurred if there had been no direct physical loss or damage to property at the described premises, including personal property in the open (or in a vehicle) within 1,000 feet, caused by or resulting from a Covered Cause of Loss.

b. Expediting Expense means the following reasonable and necessary additional expenses: (1) Overtime wages; (2) Extra Cost of express or rapid means of

transportation; (3) Costs to make temporary repairs; (4) Costs to expedite permanent repair or

replacement of damaged property; (5) Additional costs to provide training on

replacement equipment that you incur in order to meet the completion date of any project performed for a client or customer which is required in a written

contract or agreement that was executed prior to loss or damage.

c. The most we will pay for loss or damage under this Additional Coverage in any one annual policy period is $10,000. No Deductible applies to this Additional Coverage.

4. Food Contamination a. If your business at the described premises is

ordered closed by the Board of Health or any other governmental authority as a result of the discovery or suspicion of "food contamination", we will pay: (1) Your expense to clean your equipment

as required by the Board of Health or any other governmental authority;

(2) Your cost to replace the food which is, or is suspected to be, contaminated;

(3) Your expense to provide necessary medical tests or vaccinations for your infected employees. However, we will not pay for any expense that is otherwise covered under a Workers Compensation Policy;

(4) The loss of “Business Income” you sustain due to the necessary suspension of your "operations" at a described premises. The coverage for Business Income will begin 24 hours after you receive notice of closing from the Board of Health or any other governmental authority.

(5) Reasonable expenses incurred for inoculation of your restaurant patrons by a licensed medical professional because of “food contamination” alleged by such patrons to have been caused by ingestion of your food. However, this coverage does not apply to you, your employees or, unless they are an affected patron, members of either’s household.

(6) Additional advertising expenses you incur to restore your reputation.

The most we will pay for all loss in any one annual policy period under paragraphs a.(1) through a.(5) is $50,000. The most we will pay for all loss in any one annual policy period under paragraph a.(6) is $10,000. With respect to paragraphs a.(1) through a.(3), a.(5) and a.(6), we will not pay for loss or damage in any one occurrence until the amount of loss or damage exceeds $500. We will then pay the amount of loss or damage in excess of $500 up to the limit of insurance for

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 3 of 8

each applicable coverage noted in the paragraphs mentioned.

b. We will pay the loss of “Business Income” you sustain as a direct result of an “announcement” of “food borne illness”. (1) “Announcement” means a declaration by

a Board of Health or any other governmental authority having jurisdiction, or a publication or broadcast by the media, of the discovery or suspicion of “food contamination” at a location of the same type, trade name and operation. Any and all “announcements” concerning the same event or a series of related events, regardless of the number of locations or individuals affected, shall be considered one “announcement”. Any such “announcement” must occur during the policy period.

(2) “Food borne illness” means an incidence of food poisoning to one or more customers of a location of the same type, trade name and operation as a result of: (a) Tainted food purchased by the

location; (b) Food which has been improperly

stored, handled or prepared; or (c) A communicable disease transmitted

through one or more of the employees of the location.

The most we will pay for all loss in any one annual policy period under paragraph b. is $25,000.

c. These limits are in excess of any other “food contamination” or “food borne illness” coverage available.

d. We will not pay any fines or penalties levied against you by the Board of Health or any other governmental authority as a result of the discovery or suspicion of “food contamination” at the described premises.

5. Identity Fraud a. We will pay for “expenses” incurred by an

insured, as the direct result of any one “identity fraud” commenced during the policy period.

b. Any act or series of acts committed by any one person or in which any one person is concerned or implicated is considered to be one “identity fraud”, even if a series of acts continues into a subsequent policy period.

c. The following exclusions apply to this coverage. We do not cover:

(1) “Expenses” incurred due to any fraudulent, dishonest or criminal act by an insured or any person acting in concert with an insured, or by any authorized representative of an insured, whether acting alone or in collusion with others.

(2) Loss other than “expenses”. d. We will not pay for loss or damage in any one

occurrence until the amount of loss or damage exceeds $250. We will then pay the amount of loss or damage in excess of $250 up to $25,000.

6. Spoilage a. We will pay for loss of “perishable stock” due

to spoilage resulting from: (1) Breakdown or Contamination, meaning:

(a) Change in temperature or humidity resulting from mechanical breakdown or mechanical failure of refrigerating, cooling or humidity control apparatus or equipment, only while such apparatus or equipment is at the described premises shown in the Schedule; or

(b) Contamination by a refrigerant, only while the refrigerating apparatus or equipment is at the described premises shown in the Schedule. Mechanical breakdown and mechanical failure do not mean power interruption, regardless of how or where the interruption is caused and whether or not the interruption is complete or partial.

(2) Power Outage, meaning change in temperature or humidity resulting from complete or partial interruption of electrical power, either on or off the described premises, due to conditions beyond your control.

b. We will not pay for loss or damage caused by or resulting from: (1) The disconnection of any refrigerating,

cooling or humidity control system from the source of power.

(2) The deactivation of electrical power caused by the manipulation of any switch or other device used to control the flow of electrical power or current.

(3) The inability of an Electrical Utility Company or other power source to provide sufficient power due to: (a) Lack of fuel; or (b) Governmental order.

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 4 of 8

(4) The inability of a power source at the described premises to provide sufficient power due to lack of generating capacity to meet demand.

(5) Breaking of any glass that is a permanent part of any refrigerating, cooling or humidity control unit.

c. The most we will pay for loss or damage in any one occurrence under this Additional coverage is $10,000 subject to an Annual Policy Aggregate of $25,000. This limit is excess over any other spoilage coverage available. The Business Personal Property deductible, as shown in the Commercial Property Coverage Part Declarations, applies to this Additional Coverage.

7. Contract Penalty a. We will pay to cover contract penalties you

are assessed as a result of any written clause in your contract for failure to timely deliver your product or service according to contract terms, provided the contract was executed prior to the loss or damage. The penalties must solely result from direct physical loss or damage by a Covered Cause of Loss to covered Property.

b. The most we will pay for loss or damage in any one occurrence under this Additional Coverage is $10,000 subject to an Annual Policy Aggregate of $50,000. No Deductible applies to this Additional Coverage.

8. Damaged Master Key/Key Card and Alternative Key Systems a. We will pay to cover any consequential loss

you actually incur caused by a Covered Cause of Loss to replace keys or key-cards and adjust locks to accept new keys or key-cards or, if required, to replace locks, including the cost of their installation, necessitated by the loss of or damage to master or grand master keys or key-cards, including any card programmers, card-readers, computers, related alarms, transceivers, powers supplies and any other electronic or mechanical apparatus needed to make the card keys work.

b. The most we will pay under this Additional Coverage for all loss or damage in any one annual policy period is $10,000. No Deductible applies to this Additional Coverage.

9. Guests’ Evacuation Expense

a. We will reimburse you for reasonable and necessary expenses that you incur to evacuate a described premises because of imminent danger to the life or safety of your “guest” posed by a Covered Cause of Loss.

b. We will not reimburse you for any: (1) Planned evacuation or drill; or (2) Strike, bomb threat or false fire alarm,

unless the order to evacuate the described premises is issued by a civil authority having jurisdiction.

c. The most we will pay for loss or damage in any one occurrence under this Additional Coverage is $15,000. No Deductible applies to this Additional Coverage.

10. Guests’ Relocation and Reimbursement Expense a. We will pay for the actual and reasonable

expense you incur to reimburse your “guest” whose prearranged lodging accommodations at the premises described in the Declarations cannot be honored due to direct physical loss or damage to Covered Property at a described premises caused by or resulting from a Covered Cause of Loss.

b. We will reimburse you only for: (1) Reasonable actual expenses you incur

beyond the cost of lodging accommodations at the described premises to secure other comparable hotel lodging accommodations for your “guest”; and

(2) Reasonable extra expenses you incur to provide transportation for your “guest” between your hotel to the location where comparable accommodations are secured.

Such expenses are limited to the amount of time each “guest” is scheduled to stay at the insured’s lodging, or as limited in Paragraph c.

c. If you do not resume all or part of your “operations” at the premises described in the Declarations as quickly as possible, we will pay based on the length of time it would have taken to resume “operations” as quickly as possible.

d. The coverage period for this Additional Coverage: (1) Begins on the date the:

(a) Described premises becomes uninhabitable; and

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 5 of 8

(b) “Guests” prearranged lodging accommodations are scheduled to commence or are interrupted, whichever is later; and

(2) Ends on the earliest of the following: (a) The last date for which “guests” are

scheduled to stay at the premises described in the Declarations during the period of uninhabitability; or

(b) The date the damaged property at the covered location should be repaired, rebuilt or replaced with reasonable speed and similar quality.

(c) For each person, 14 days after the date you began to incur such expenses on behalf of that person.

e. The most we will pay for loss or damage in any one occurrence under this Additional Coverage is $15,000. However, in no event will we reimburse you more than $1,000 for any one “guest”. No Deductible applies to this Additional Coverage.

11. Guests’ Property a. We will pay those sums that you become

legally obligated to pay as damages because of loss or destruction of, or damage to any property, other than that specified in Paragraph b., belonging to your “guests” while the property is at the premises or in your possession. If you are sued for refusing to pay for loss of or damage to “guests’ property”, and you have our written consent to defend against the suit, we will pay for any reasonable legal expenses that you incur and pay in that defense. The amount that we will pay is in addition to the applicable limit of insurance shown in the Schedule of this endorsement.

b. We will not pay for loss or damage: (1) Resulting from any dishonest or criminal

act that you or any of your partners or members commit, whether acting alone or in collusion with other persons.

(2) Resulting from liability you assume under any written agreement. However, this exclusion does not apply under Paragraph b.(2), to any written agreement entered into with a “guest” for loss of or damage to property for which you may be liable by law, if the written agreement:

(a) Is made before the “occurrence” which results in the loss or damage; and

(b) Does not increase the amount for which you are legally liable by more than $1,000.

(3) To property resulting from fire, however caused.

(4) To property in a “guest’s” quarters including any wall safe or other container used for safekeeping.

(5) To property resulting from the spilling, upsetting or leaking of any food or liquid.

(6) To property while in your care and custody for laundering or cleaning.

(7) Resulting from your release of any other person or organization from legal liability.

(8) To samples or articles carried or held for sale or delivery after sale.

(9) To any vehicle, including: (a) Its equipment and accessories; and (b) Any property contained in or on a

vehicle. c. We will not pay for loss or damage in any one

occurrence until the amount of loss or damage exceeds $250. We will then pay the amount of loss or damage in excess of $250 up to $10,000. However, in no event will we reimburse you more than $1,000 for any one “guest”.

d. “Occurrence”: With respect to the provisions of this endorsement for Guests’ Property only, “occurrence” means: (1) An individual act or event; (2) The combined total of all separate acts or

events whether or not related; or (3) A series of acts or events whether or not

related; (4) committed by a person acting alone or in

collusion with other persons, or not committed by any person, during the policy period shown in the Declarations, before such policy period or both.

12. Reservation Systems a. We will pay for the actual loss of “Business

Income” you sustain due to direct physical loss or damage at the premises of a dependent reservation system caused by or resulting from any Covered Cause of Loss.

b. If you do not resume “operations”, or do not resume “operations” as quickly as possible,

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 6 of 8

we will pay based on the length of time it would have taken to resume “operations” as quickly as possible.

c. For the purpose of this Additional Coverage, dependent reservation system means property located within the coverage territory owned or operated by others, excluding travel agencies, whom you depend on to book reservations to the described premises.

d. The coverage period for “Business Income” under this Additional Coverage: a. Begins 24 hours after the time of direct

physical loss or damage caused by or resulting from any Covered Cause of Loss at the premises of the dependent reservation system; and

b. Ends on the date when the property at the premises of the dependent reservation system should be repaired, rebuilt or replaced with reasonable speed and similar quality.

e. The most we will pay under this Additional Coverage for all loss or damage in any one annual policy period is $25,000.

f. This Additional Coverage does not apply to any loss otherwise covered under the Business Income from Dependent Properties Additional Coverage.

13. Tenant Move Back Expenses a. If a Covered Cause of Loss occurs to covered

Building Property during the policy term which requires your commercial tenants to temporarily vacate part of the building, we will pay your actual expense to reimburse: (1) The tenants’ cost of reestablishing utility

services, less any refunds from discontinued service at your covered building;

(2) The move back costs of assembling and setting up tenants’ fixtures and equipment at your covered building; and

(3) Unpacking and reshelving tenants’ “stock” and supplies at your covered building.

b. The most we will pay under this Additional Coverage for all loss or damage in any one annual policy period is $15,000.

The following revises the Businessowners Coverage Form. A. The following is added to Section II – Liability,

Paragraph A. – Coverages: 1. Services Errors and Omissions Coverage

a. Insuring Agreement

(1) We will pay those sums that the insured becomes legally obligated to pay as damages because of an error or omission by you or any of your “employees” or by any concessionaire trading under your name in providing facilities, goods or services. We will have the right and duty to defend the insured against any “suit” seeking those damages. However, we will have no duty to defend the insured against any “suit” seeking damages for errors and omissions to which this insurance does not apply. We may, at our discretion, investigate the circumstances of any error or omission and settle any claim or “suit” that may result. But: (a) The most we will pay for the sum of

all damages under this Services Errors And Omissions Coverage because of all services errors and omissions is $15,000 in any one annual policy period starting with the beginning of the policy period shown in the Declarations. This Limit of Insurance applies separately to each premises described in the Declarations;

(b) We will not pay for loss or damage in any one occurrence until the amount of loss or damage exceeds $250. We will then pay the amount of loss or damage in excess of $250 up to $15,000; and

(c) Our right and duty to defend end when we have used up the applicable Limit of Insurance in the payment of judgments or settlements, or exhausted our limits, under this Services Errors And Omissions Coverage.

(2) This insurance applies only to errors in the providing of facilities, goods or services that take place, or omissions in providing such goods, facilities or services that should have taken place, in the “coverage territory” and during the policy period.

b. Exclusions This insurance does not apply to: (1) Intentional error or intentional failure to

provide any services. (2) “Bodily injury”, “property damage” or

“personal and advertising injury”. (3) Discrimination based on a “guest’s” or

invitee’s race, color, national origin,

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 7 of 8

religion, gender, marital status, age, sexual orientation or preference, physical or mental condition or residence location.

c. With respect to this Services Errors And Omissions Coverage, the Duties In The Event Of Occurrence, Offense, Claim Or Suit Condition is replaced by the following: (1) If a claim is made or “suit” is brought

against any insured, you must: (a) Immediately record the specifics of

the claim or “suit” and the date received; and

(b) Notify us as soon as practicable. You must see to it that we receive written notice of the claim or “suit” as soon as practicable.

(2) You and any other involved insured must: (a) Immediately send us copies of any

demands, notices, summonses or legal papers received in connection with the claim or “suit”;

(b) Authorize us to obtain records and other information;

(c) Cooperate with us in our investigation or settlement of the claim or defense against the “suit”; and

(d) Assist us, upon our request, in the enforcement of any right against any person or organization which may be liable to the insured because of an error or omission to which this insurance may apply.

(3) No insured will, except at that insured’s own cost, voluntarily make a payment, assume any obligation, or incur any expense without our consent.

C. ADDITIONAL DEFINITIONS 1. “Expenses”:

a. With respect to the provisions of this endorsement for Identity Fraud coverage only, “expenses” means: (1) Costs for notarizing fraud affidavits or

similar documents for financial institutions or similar credit grantors or credit agencies that have required that such affidavits be notarized.

(2) Costs for certified mail to law enforcement agencies, credit agencies,

financial institutions or similar credit grantors.

(3) Loan application fees for re-applying for a loan or loans where the original application is rejected solely because the lender received incorrect credit information.

(4) Reasonable attorney fees incurred, with our prior consent, for: (a) Defense of lawsuits brought against

the insured by merchants or their collection agencies.

(b) The removal of any criminal or civil judgments wrongly entered against an insured, and

(c) Challenging the accuracy or completeness of any information in a consumer credit report.

(5) Charges incurred for long distance telephone calls to merchants, law enforcement agencies, financial institutions or similar credit grantors, or credit agencies to report or discuss an actual “identity fraud”.

2. “Food contamination” means an incidence of food poisoning to one or more of your customers as a result of: (a) Tainted food you purchased; (b) Food which has been improperly stored,

handled or prepared; or (c) A communicable disease transmitted through

one or more of your employees. 3. “Guest” means a person or group of persons in a

single reservation who have checked-in for lodging at the described premises.

4. “Guests’ property” means “money”, “securities” and other tangible property having intrinsic value that belongs to your “guest”.

5. “Identity fraud” means the act of knowingly transferring or using, without lawful authority, a means of identification of an insured with the intent to commit, or to aid or abet, any unlawful activity that constitutes a violation of any local, state or federal law.

6. “Perishable Stock” means personal property: a. Maintained under controlled conditions for its

preservation; and b. Susceptible to loss or damage if the

controlled conditions change.

EB 99 09 06 16 Includes copyrighted material of Insurance Services Office, Inc. with its permission. Page 8 of 8

SCHEDULE OF LOCATIONS Loc. No. Bldg. No. Street City State Zip

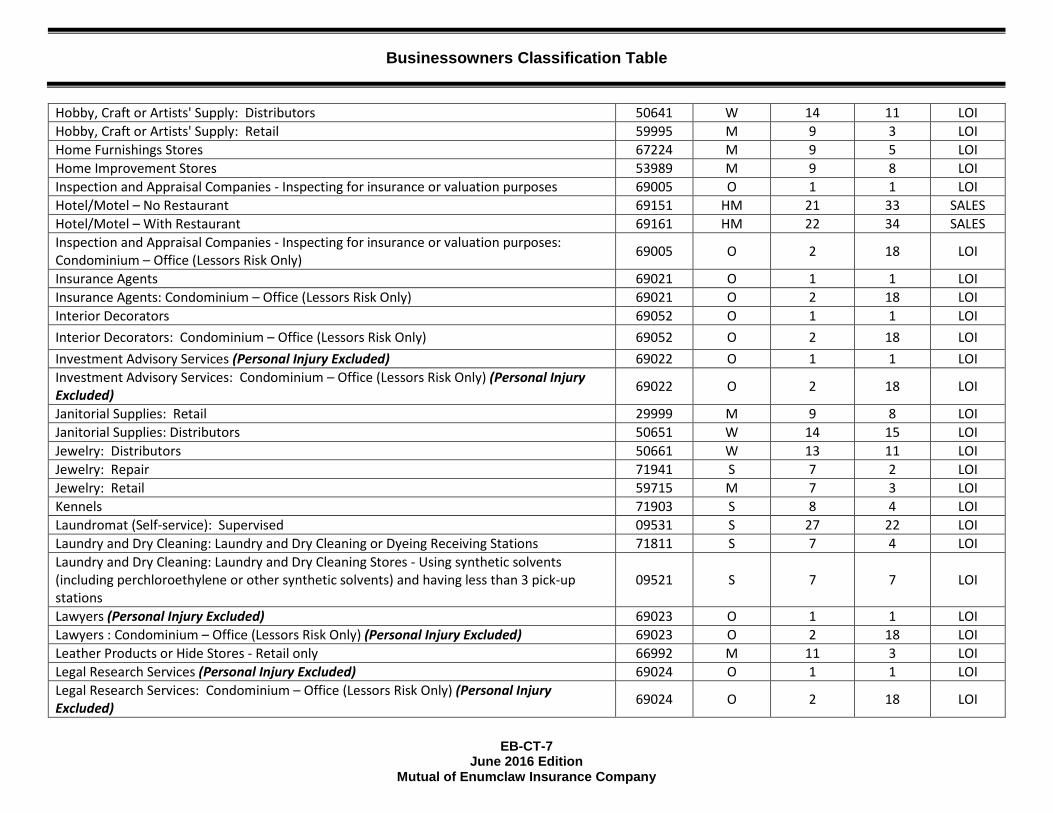

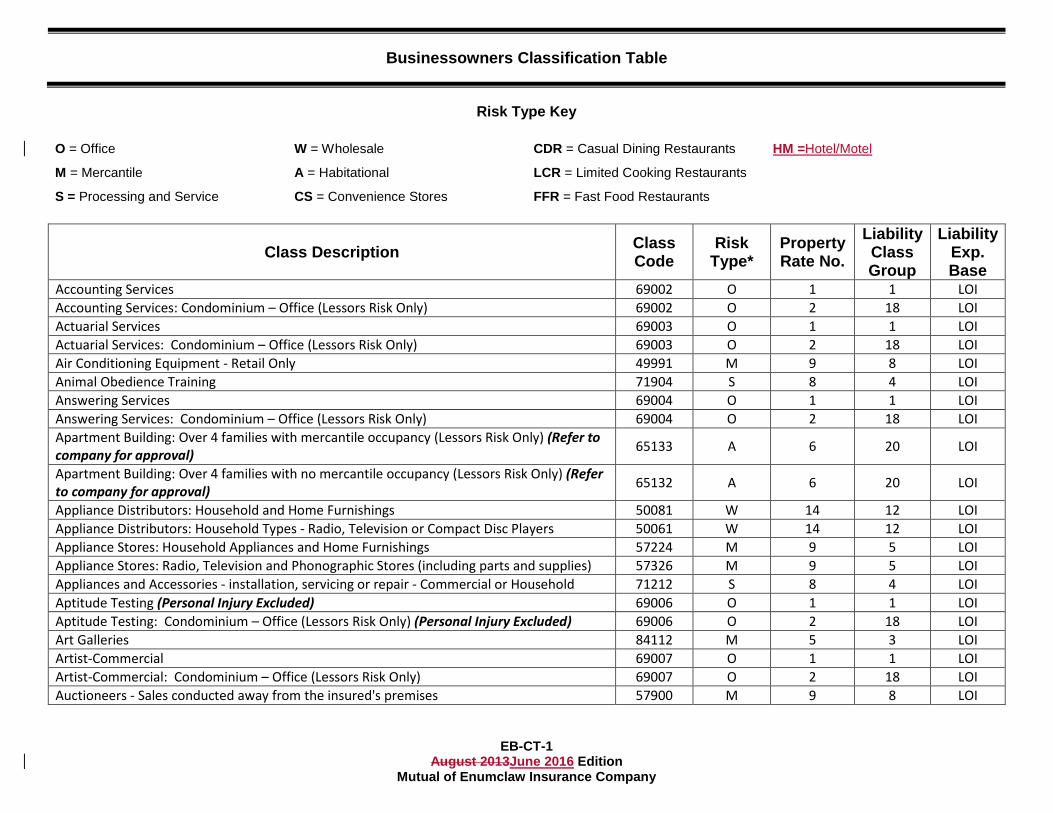

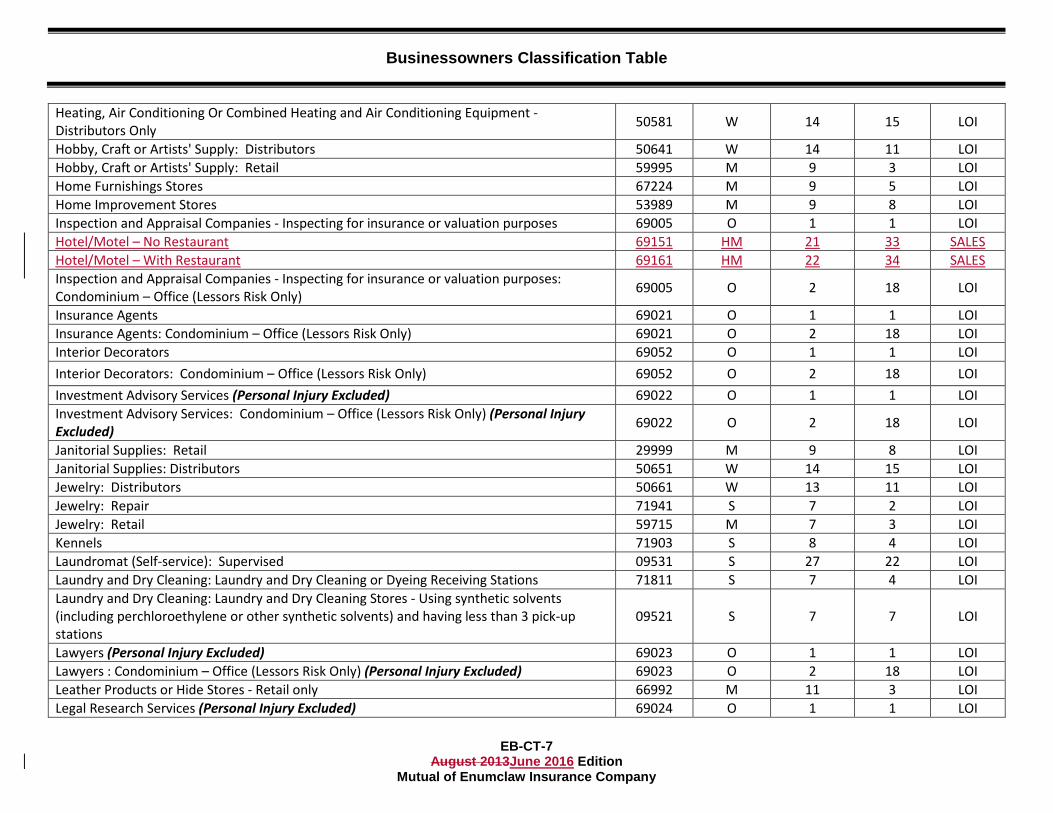

Businessowners Classification Table

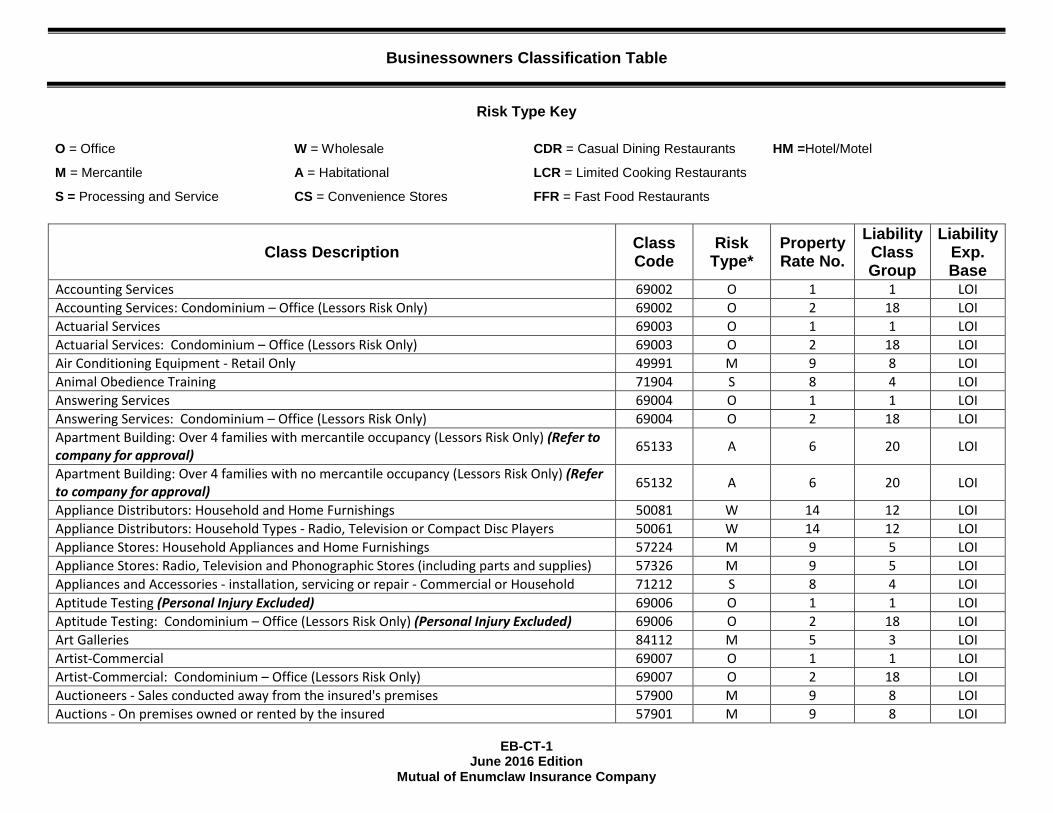

EB-CT-1

June 2016 Edition Mutual of Enumclaw Insurance Company

Risk Type Key

O = Office W = Wholesale CDR = Casual Dining Restaurants HM =Hotel/Motel

M = Mercantile A = Habitational LCR = Limited Cooking Restaurants

S = Processing and Service CS = Convenience Stores FFR = Fast Food Restaurants

Class Description Class Code

Risk Type*

Property Rate No.

Liability Class Group

Liability Exp. Base

Accounting Services 69002 O 1 1 LOI Accounting Services: Condominium – Office (Lessors Risk Only) 69002 O 2 18 LOI Actuarial Services 69003 O 1 1 LOI Actuarial Services: Condominium – Office (Lessors Risk Only) 69003 O 2 18 LOI Air Conditioning Equipment - Retail Only 49991 M 9 8 LOI Animal Obedience Training 71904 S 8 4 LOI Answering Services 69004 O 1 1 LOI Answering Services: Condominium – Office (Lessors Risk Only) 69004 O 2 18 LOI Apartment Building: Over 4 families with mercantile occupancy (Lessors Risk Only) (Refer to company for approval) 65133 A 6 20 LOI

Apartment Building: Over 4 families with no mercantile occupancy (Lessors Risk Only) (Refer to company for approval) 65132 A 6 20 LOI

Appliance Distributors: Household and Home Furnishings 50081 W 14 12 LOI Appliance Distributors: Household Types - Radio, Television or Compact Disc Players 50061 W 14 12 LOI Appliance Stores: Household Appliances and Home Furnishings 57224 M 9 5 LOI Appliance Stores: Radio, Television and Phonographic Stores (including parts and supplies) 57326 M 9 5 LOI Appliances and Accessories - installation, servicing or repair - Commercial or Household 71212 S 8 4 LOI Aptitude Testing (Personal Injury Excluded) 69006 O 1 1 LOI Aptitude Testing: Condominium – Office (Lessors Risk Only) (Personal Injury Excluded) 69006 O 2 18 LOI Art Galleries 84112 M 5 3 LOI Artist-Commercial 69007 O 1 1 LOI Artist-Commercial: Condominium – Office (Lessors Risk Only) 69007 O 2 18 LOI Auctioneers - Sales conducted away from the insured's premises 57900 M 9 8 LOI Auctions - On premises owned or rented by the insured 57901 M 9 8 LOI

Businessowners Classification Table

EB-CT-7

June 2016 Edition Mutual of Enumclaw Insurance Company

Hobby, Craft or Artists' Supply: Distributors 50641 W 14 11 LOI Hobby, Craft or Artists' Supply: Retail 59995 M 9 3 LOI Home Furnishings Stores 67224 M 9 5 LOI Home Improvement Stores 53989 M 9 8 LOI Inspection and Appraisal Companies - Inspecting for insurance or valuation purposes 69005 O 1 1 LOI Hotel/Motel – No Restaurant 69151 HM 21 33 SALES Hotel/Motel – With Restaurant 69161 HM 22 34 SALES Inspection and Appraisal Companies - Inspecting for insurance or valuation purposes: Condominium – Office (Lessors Risk Only) 69005 O 2 18 LOI

Insurance Agents 69021 O 1 1 LOI Insurance Agents: Condominium – Office (Lessors Risk Only) 69021 O 2 18 LOI Interior Decorators 69052 O 1 1 LOI Interior Decorators: Condominium – Office (Lessors Risk Only) 69052 O 2 18 LOI Investment Advisory Services (Personal Injury Excluded) 69022 O 1 1 LOI Investment Advisory Services: Condominium – Office (Lessors Risk Only) (Personal Injury Excluded) 69022 O 2 18 LOI

Janitorial Supplies: Retail 29999 M 9 8 LOI Janitorial Supplies: Distributors 50651 W 14 15 LOI Jewelry: Distributors 50661 W 13 11 LOI Jewelry: Repair 71941 S 7 2 LOI Jewelry: Retail 59715 M 7 3 LOI Kennels 71903 S 8 4 LOI Laundromat (Self-service): Supervised 09531 S 27 22 LOI Laundry and Dry Cleaning: Laundry and Dry Cleaning or Dyeing Receiving Stations 71811 S 7 4 LOI Laundry and Dry Cleaning: Laundry and Dry Cleaning Stores - Using synthetic solvents (including perchloroethylene or other synthetic solvents) and having less than 3 pick-up stations

09521 S 7 7 LOI

Lawyers (Personal Injury Excluded) 69023 O 1 1 LOI Lawyers : Condominium – Office (Lessors Risk Only) (Personal Injury Excluded) 69023 O 2 18 LOI Leather Products or Hide Stores - Retail only 66992 M 11 3 LOI Legal Research Services (Personal Injury Excluded) 69024 O 1 1 LOI Legal Research Services: Condominium – Office (Lessors Risk Only) (Personal Injury Excluded) 69024 O 2 18 LOI

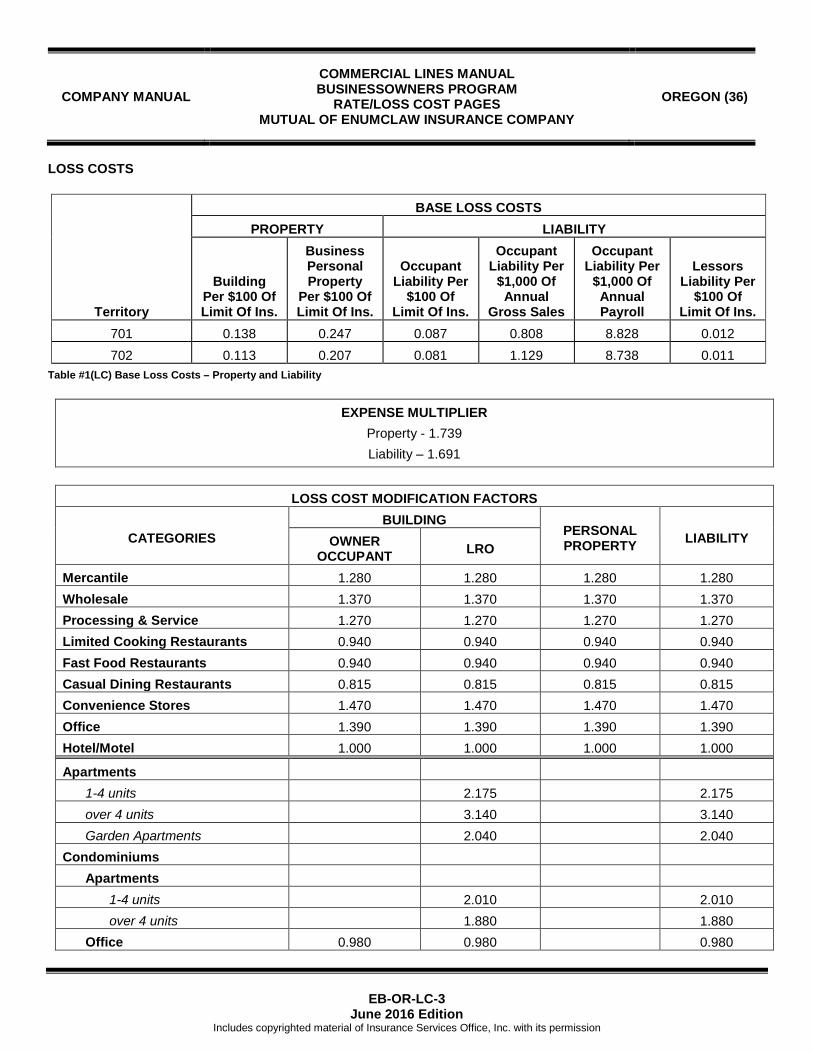

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

RATE/LOSS COST PAGES MUTUAL OF ENUMCLAW INSURANCE COMPANY

OREGON (36)

EB-OR-LC-3

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

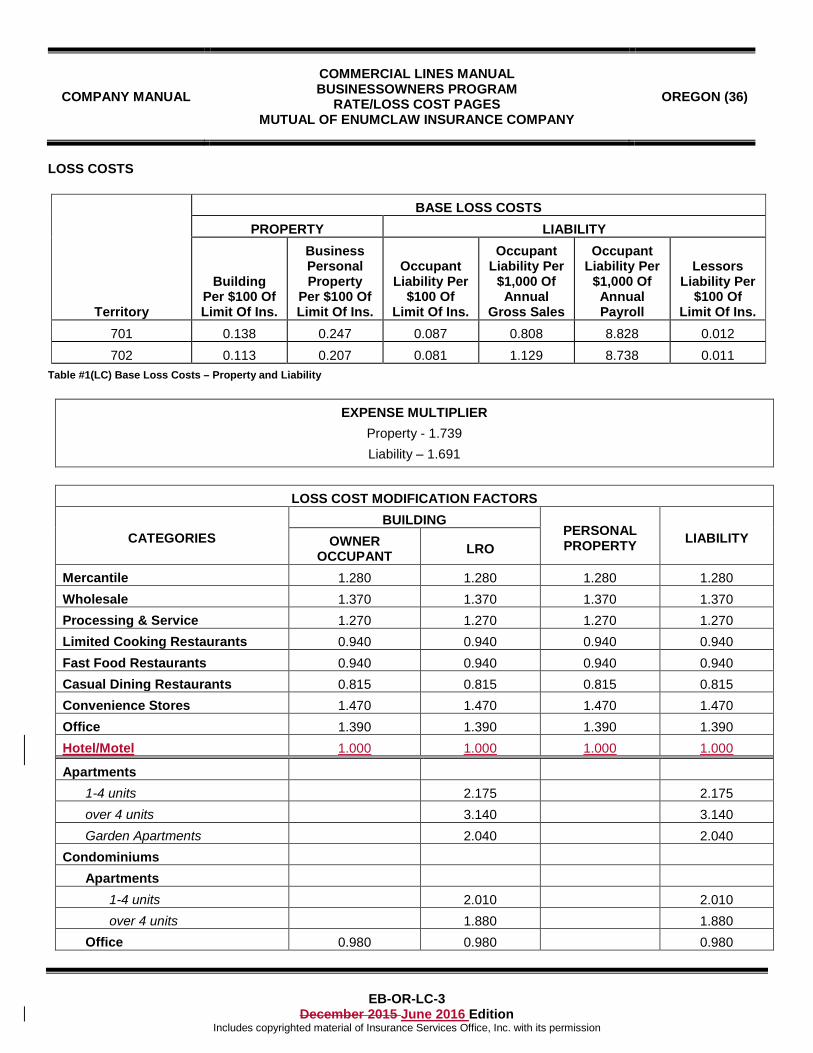

LOSS COSTS

BASE LOSS COSTS PROPERTY LIABILITY

Territory

Building Per $100 Of Limit Of Ins.

Business Personal Property

Per $100 Of Limit Of Ins.

Occupant

Liability Per $100 Of

Limit Of Ins.

Occupant Liability Per

$1,000 Of Annual

Gross Sales

Occupant Liability Per

$1,000 Of Annual Payroll

Lessors

Liability Per $100 Of

Limit Of Ins. 701 0.138 0.247 0.087 0.808 8.828 0.012 702 0.113 0.207 0.081 1.129 8.738 0.011

Table #1(LC) Base Loss Costs – Property and Liability

EXPENSE MULTIPLIER Property - 1.739 Liability – 1.691

LOSS COST MODIFICATION FACTORS

CATEGORIES BUILDING

PERSONAL PROPERTY LIABILITY OWNER

OCCUPANT LRO

Mercantile 1.280 1.280 1.280 1.280 Wholesale 1.370 1.370 1.370 1.370 Processing & Service 1.270 1.270 1.270 1.270 Limited Cooking Restaurants 0.940 0.940 0.940 0.940 Fast Food Restaurants 0.940 0.940 0.940 0.940 Casual Dining Restaurants 0.815 0.815 0.815 0.815 Convenience Stores 1.470 1.470 1.470 1.470 Office 1.390 1.390 1.390 1.390 Hotel/Motel 1.000 1.000 1.000 1.000

Apartments 1-4 units 2.175 2.175 over 4 units 3.140 3.140 Garden Apartments 2.040 2.040

Condominiums Apartments

1-4 units 2.010 2.010 over 4 units 1.880 1.880

Office 0.980 0.980 0.980

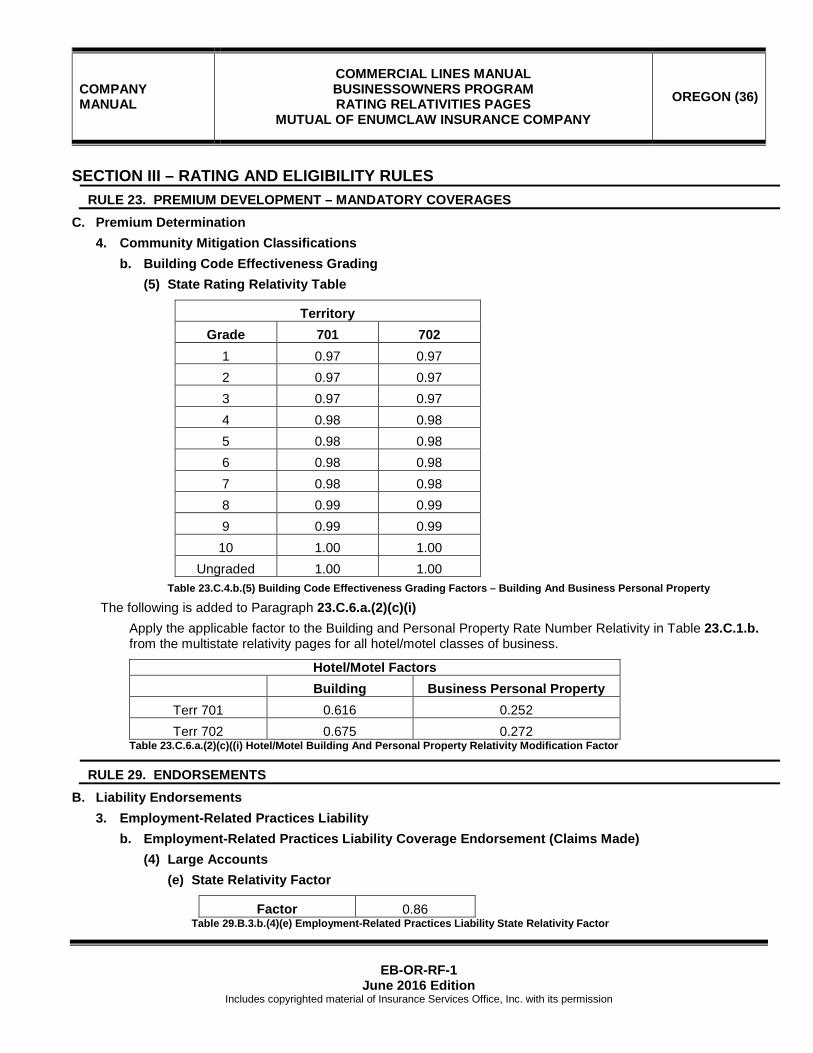

COMPANY MANUAL

COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM RATING RELATIVITIES PAGES

MUTUAL OF ENUMCLAW INSURANCE COMPANY

OREGON (36)

EB-OR-RF-1

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

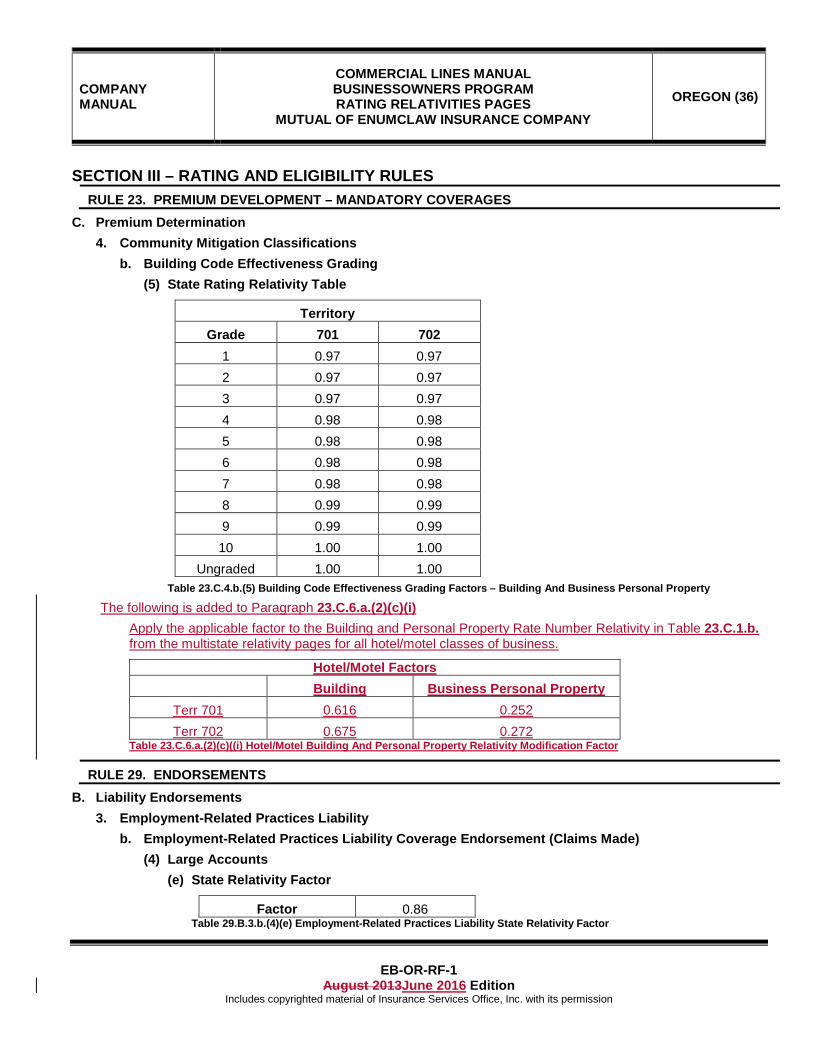

SECTION III – RATING AND ELIGIBILITY RULES

RULE 23. PREMIUM DEVELOPMENT – MANDATORY COVERAGES C. Premium Determination

4. Community Mitigation Classifications b. Building Code Effectiveness Grading

(5) State Rating Relativity Table

Territory Grade 701 702

1 0.97 0.97 2 0.97 0.97 3 0.97 0.97 4 0.98 0.98 5 0.98 0.98 6 0.98 0.98 7 0.98 0.98 8 0.99 0.99 9 0.99 0.99 10 1.00 1.00

Ungraded 1.00 1.00 Table 23.C.4.b.(5) Building Code Effectiveness Grading Factors – Building And Business Personal Property

The following is added to Paragraph 23.C.6.a.(2)(c)(i) Apply the applicable factor to the Building and Personal Property Rate Number Relativity in Table 23.C.1.b. from the multistate relativity pages for all hotel/motel classes of business.

Hotel/Motel Factors Building Business Personal Property

Terr 701 0.616 0.252 Terr 702 0.675 0.272

Table 23.C.6.a.(2)(c)((i) Hotel/Motel Building And Personal Property Relativity Modification Factor

RULE 29. ENDORSEMENTS B. Liability Endorsements

3. Employment-Related Practices Liability b. Employment-Related Practices Liability Coverage Endorsement (Claims Made)

(4) Large Accounts (e) State Relativity Factor

Factor 0.86 Table 29.B.3.b.(4)(e) Employment-Related Practices Liability State Relativity Factor

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 12

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

c. Casual Dining Restaurants (1) Definition

Casual dining restaurants serve moderately priced food in a casual atmosphere to patrons who generally order and are served while seated and pay after eating. Take-out service and the use of a buffet may also be available. These restaurants may serve no alcoholic beverages; serve beer and wine only; or serve beer, wine and liquor.

(2) Additional Eligibility Requirement Casual dining restaurants are subject to the following additional eligibility requirements: (a) Sales of alcohol no greater than 35% of total sales; (b) Gross annual sales may be no more than $7,500,000 per location; (c) Seasonal operations (risks that are closed for more than 30 consecutive days) must be referred to

company for approval; (d) Installation and maintenance of an automatic extinguishing system for cooking equipment

equivalent to that which is recommended by NFPA Standard #96, as described in Paragraph b.(3); (e) No dancing permitted; (f) No bar operations during hours when full table service is not also available. Bar operations for the

sole purpose of consuming alcoholic beverages are not permitted. 8. Wholesale Risks

Building and business personal property for wholesale businesses listed in the Businessowners Classification Table Section of the manual are the only types of wholesale risks eligible for the Businessowners Program, subject to the following requirements: a. No more than 50,000 square feet of total floor area any one building; b. Gross annual sales may be no more than $10,000,000 per location; c. No more than 15% of gross annual sales or total floor area may be derived from retail operations; The Wholesale classifications do not include the operations of manufacturers’ representatives or contractors.

9. Hotel/Motels Building and business personal property for hotel/motel risks are eligibile for coverage under the Businessowners Program. Hotel/Motels are subject to the following additional eligibility requirements: a. Buildings not to exceed six(6) stories in height. Buildings with four(4) stories or more must be sprinklered.

No limitation applies to floor area; b. Seasonal operations (risks that are closed for more than 30 consecutive days) must be referred to company

for approval; c. Pools allowed – no diving board or slide – fenced and available to guests only; and d. Gross annual sales may be no more than $7,000,000 per location.

B. Ineligibility Risks specifically listed below are not eligible for the Businessowners Policy: 1. Automobile repair or service stations; automobile, motor home, mobile home or motorcycle dealers, unless

described as eligible in the Businessowners Classification Table; 2. Parking lots or garages, unless incidental to another otherwise eligible class; 3. Bars, grills and restaurants; unless described as eligible in Paragraph 7. above; 4. Contractors; 5. Buildings occupied in whole or in part for manufacturing or processing, unless all such occupancies are eligible

risks as shown in the Businessowners Classification Table;

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 13

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

6. Insureds whose business operation involves one or more locations which are used for manufacturing, processing or servicing; unless described as eligible in the Businessowners Classification Table;

7. Household personal property; 8. One or two family dwellings unless of garden apartment variety where multiple units are grouped within a single

area and are under common ownership, management and control; 9. Places of amusement; 10. Banks, building and loan associations, savings and loan associations, credit unions, stockbrokers and similar

financial institutions; (Lessors risks with these occupancies are eligible); 11. Rental equipment stores; 12. Buildings constructed more than 30 years ago unless the common hazards (heating, cooling, electrical, wiring,

plumbing and roof) have been completely renovated or replaced within the last 20 years, unless approved by the company. The common hazards must meet applicable local and state codes;

13. Consignment goods in excess of 25% of total inventory; 14. Espresso Stands or Carts which are transported between multiple locations; 15. Second hand, used goods and antique stores or dealers; 16. "Direct import" of goods or merchandise for resale (wholesale or retail) or "direct import" of stock used in

manufacturing, service or repair operations. "Direct import" is defined as products imported directly from sources outside the United States of America;

17. Manufacturers representatives; 18. Businesses specializing in liquidated or distressed goods; For exceptions, refer to company.

C. Computation of Floor Area Do not use basement areas not open to the public in computing floor areas.

D. Aggregate Building and Personal Property Limit Businesses having building and personal property aggregate values of $15,000,000 or less per location are eligible.

E. Building and Personal Property Ownership 1. When under one ownership, eligible building and personal property must be included in the same policy. 2. When writing a home business policy, the applicable homeowners coverage policy must also be written with

Mutual of Enumclaw Insurance Company.

RULE 23. PREMIUM DEVELOPMENT – MANDATORY COVERAGES A. General Rules

1. Annual Period All rates and premiums referred to in this manual are for an annual period.

2. Applicable to All Types of Eligible Risks a. Compute premium separately for mandatory property and liability coverages. b. For mandatory property coverage, the rates apply per $100 of the limit of insurance. The limit of insurance

must be the replacement cost value of the property to be insured unless the Actual Cash Value – Buildings Option applies. Refer to Rule 28.A.2.

c. Compute premium for Tenants Improvements and Betterments using the rates for Building in lieu of Business Personal Property.

d. For mandatory liability coverage, rates apply per $100 of the limit of insurance (as defined in Paragraph b.) or per $1,000 of annual gross sales. Refer to Paragraphs 3. and 4.

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 14

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

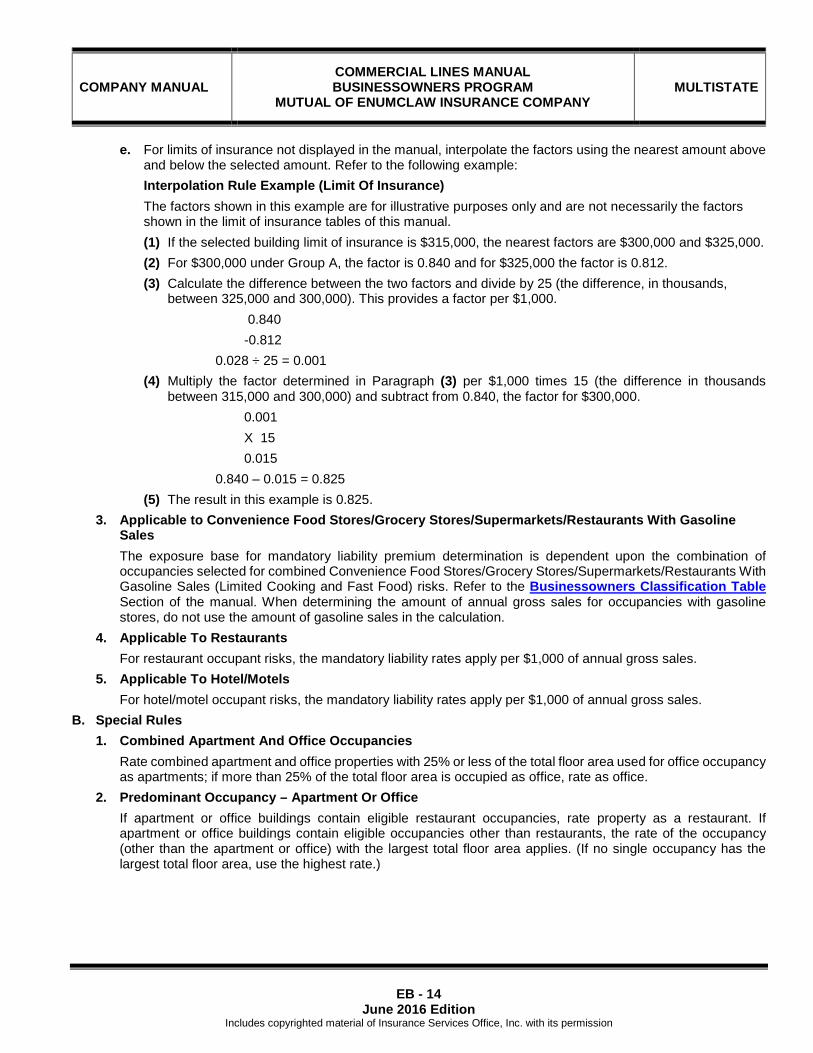

e. For limits of insurance not displayed in the manual, interpolate the factors using the nearest amount above and below the selected amount. Refer to the following example: Interpolation Rule Example (Limit Of Insurance) The factors shown in this example are for illustrative purposes only and are not necessarily the factors shown in the limit of insurance tables of this manual. (1) If the selected building limit of insurance is $315,000, the nearest factors are $300,000 and $325,000. (2) For $300,000 under Group A, the factor is 0.840 and for $325,000 the factor is 0.812. (3) Calculate the difference between the two factors and divide by 25 (the difference, in thousands,

between 325,000 and 300,000). This provides a factor per $1,000. 0.840 -0.812

0.028 ÷ 25 = 0.001 (4) Multiply the factor determined in Paragraph (3) per $1,000 times 15 (the difference in thousands

between 315,000 and 300,000) and subtract from 0.840, the factor for $300,000. 0.001 X 15 0.015

0.840 – 0.015 = 0.825 (5) The result in this example is 0.825.

3. Applicable to Convenience Food Stores/Grocery Stores/Supermarkets/Restaurants With Gasoline Sales The exposure base for mandatory liability premium determination is dependent upon the combination of occupancies selected for combined Convenience Food Stores/Grocery Stores/Supermarkets/Restaurants With Gasoline Sales (Limited Cooking and Fast Food) risks. Refer to the Businessowners Classification Table Section of the manual. When determining the amount of annual gross sales for occupancies with gasoline stores, do not use the amount of gasoline sales in the calculation.

4. Applicable To Restaurants For restaurant occupant risks, the mandatory liability rates apply per $1,000 of annual gross sales.

5. Applicable To Hotel/Motels For hotel/motel occupant risks, the mandatory liability rates apply per $1,000 of annual gross sales.

B. Special Rules 1. Combined Apartment And Office Occupancies

Rate combined apartment and office properties with 25% or less of the total floor area used for office occupancy as apartments; if more than 25% of the total floor area is occupied as office, rate as office.

2. Predominant Occupancy – Apartment Or Office If apartment or office buildings contain eligible restaurant occupancies, rate property as a restaurant. If apartment or office buildings contain eligible occupancies other than restaurants, the rate of the occupancy (other than the apartment or office) with the largest total floor area applies. (If no single occupancy has the largest total floor area, use the highest rate.)

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 36

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

c. Premium Determination (1) Deductibles

Apply the mandatory percentage deductibles as specified in the Earthquake company rates/ISO loss costs of CLM Division Five - Fire and Allied Lines.

(2) Rating Multiply the 80% coinsurance earthquake company loss cost determined in CLM Division Five - Fire and Allied Lines by a factor of 1.621. Multiply the rate determined in Paragraph (1) above by a factor of 1.20 (in recognition of coverage granted for loss of income) to obtain the Businessowners Earthquake company rate. Multiply the result by the limit of insurance (per $100).

NOTE: This coverage is not available for new business and cannot be added to an existing policy. 10. Restaurant Enhancement Endorsement

a. Description Of Coverage The following optional enhancement endorsement is available to any risk that includes a restaurant exposure.

b. Endorsement Use Restaurant Enhancement Endorsement EB 99 07.

c. Premium Determination The premium charge for this optional enhancement is a flat charge and no modifications will apply: (1) First location; $200; (2) Each additional location; $50.

11. Hotel/Motel Enhancement Endorsement a. Description of Coverage

The following optional enhancement endorsement is available to any risk that includes a hotel/motel exposure.

b. Form Use Hotel/Motel Enhancement Endorsement EB 99 09.

c. Premium Determination The premium charge for this optional enhancement is a flat charge and no modifications will apply: (1) First location; $175; (2) Each additional location; $50.

B. Liability Endorsements 1. Comprehensive Business Liability Exclusion (All Hazards in Connection With Designated Premises,

Operations Or Products a. Description Of Coverage

This endorsement excludes specific projects, location hazards, operations or equipment, if clearly separable and definable.

b. Endorsement Use Comprehensive Business Liability Exclusion Endorsement BP 04 01.

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 54

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

(2) Contractors on policies covering subcontractors; but only for liability for ongoing operations performed for such owners, lessees or contractors by the insured contractor or subcontractor.

b. Endorsement Use Additional Insured - Owners, Lessees Or Contractors Endorsement BP 04 50.

17. Primary And Noncontributory – Other Insurance Condition – Refer To Company a. Description

This endorsement provides that the coverage made available to an additional insured will be provided on a primary and noncontributory basis.

b. Endorsement Use Primary And Noncontributory – Other Insurance Condition Endorsement BP 14 88.

c. Premium Development (1) The premium for the attachment of this endorsement is Refer To Company; or (2) $25 unless otherwise adjusted.

D. Endorsements Applicable to Specific Classes 1. Professional Liability Endorsements

a. Barber Shops and Hair Salons Professional Liability (1) Description Of Coverage

This endorsement is used to provide professional liability coverage for bodily injury, property damage, personal injury and advertising injury or other injury that results from the rendering of or failure to render professional services in the operation of a barbershop or hair salon. The Barber Shops and Hair Salons Professional Liability Limit is not a separate limit of insurance. The limit provided is included within the Businessowners Liability Limit of insurance. The occurrence and aggregate limits for Barber Shops and Hair Salons Professional must be equal to the Liability and Medical Expenses Limit. This limit represents the aggregate limit for all occurrences during each annual policy period.

(2) Endorsement Use Barber Shops And Hair Salons Professional Liability Endorsement BP 08 01.

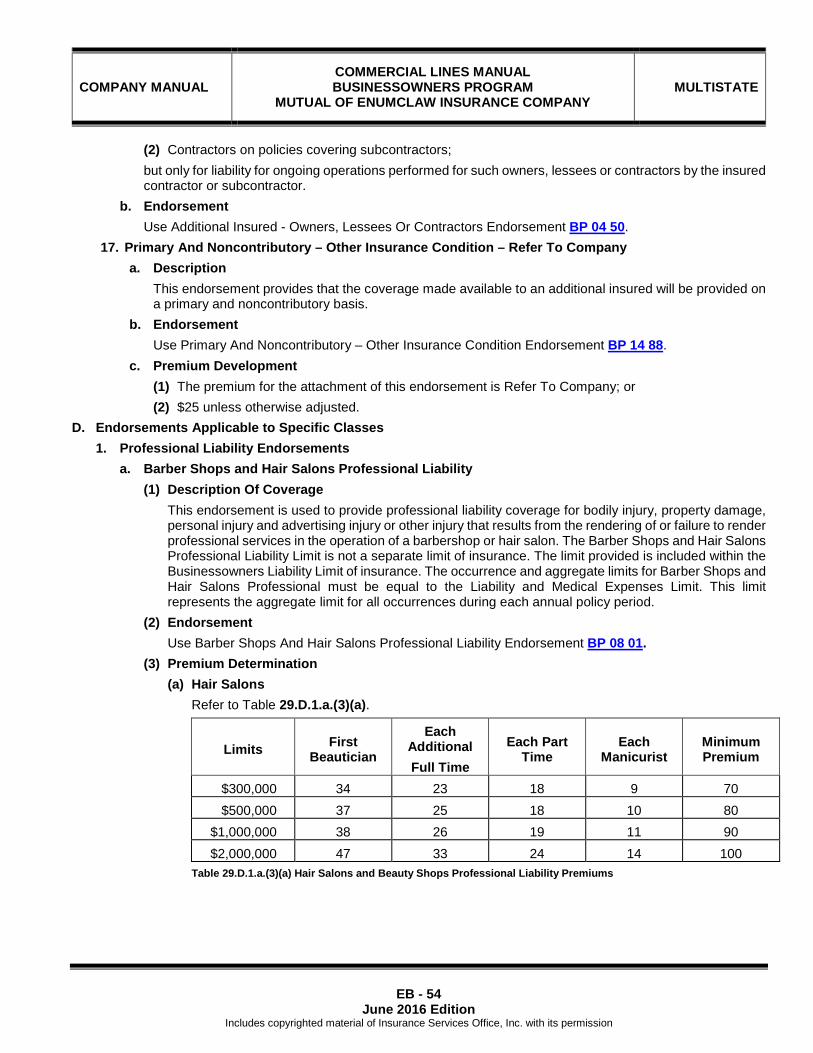

(3) Premium Determination (a) Hair Salons

Refer to Table 29.D.1.a.(3)(a).

Limits First Beautician

Each Additional Full Time

Each Part Time

Each Manicurist

Minimum Premium

$300,000 34 23 18 9 70 $500,000 37 25 18 10 80

$1,000,000 38 26 19 11 90 $2,000,000 47 33 24 14 100

Table 29.D.1.a.(3)(a) Hair Salons and Beauty Shops Professional Liability Premiums

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 55

June 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

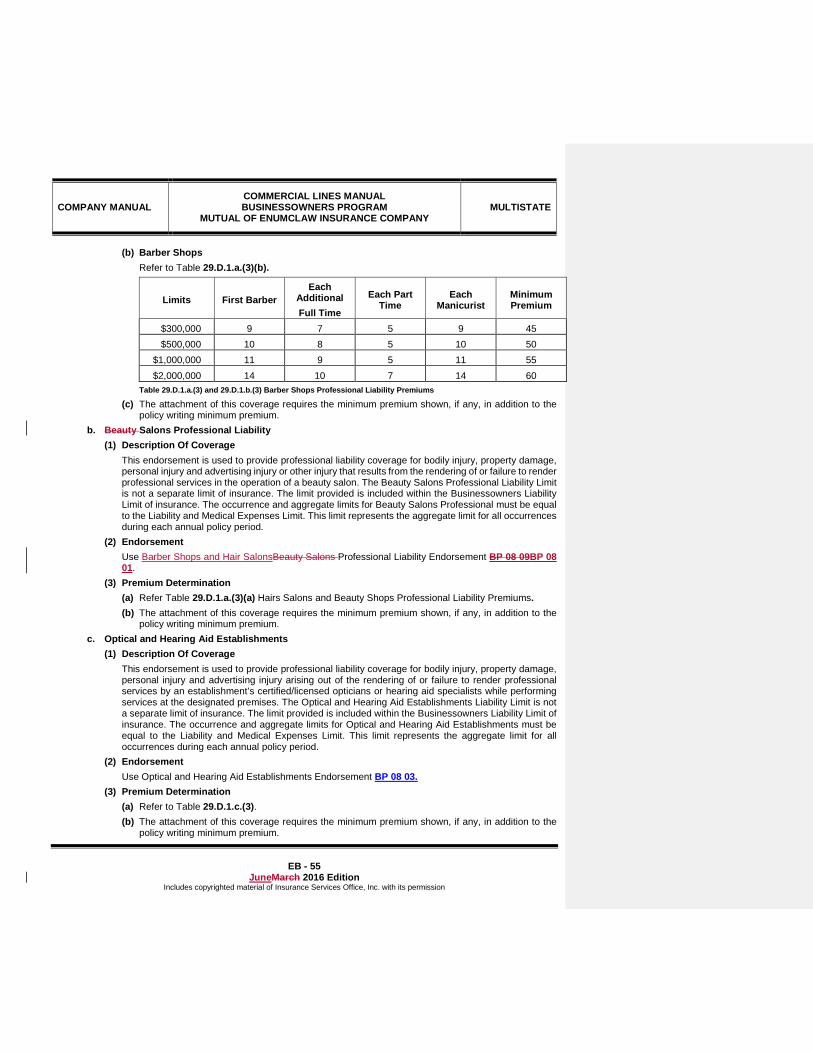

(b) Barber Shops Refer to Table 29.D.1.a.(3)(b).

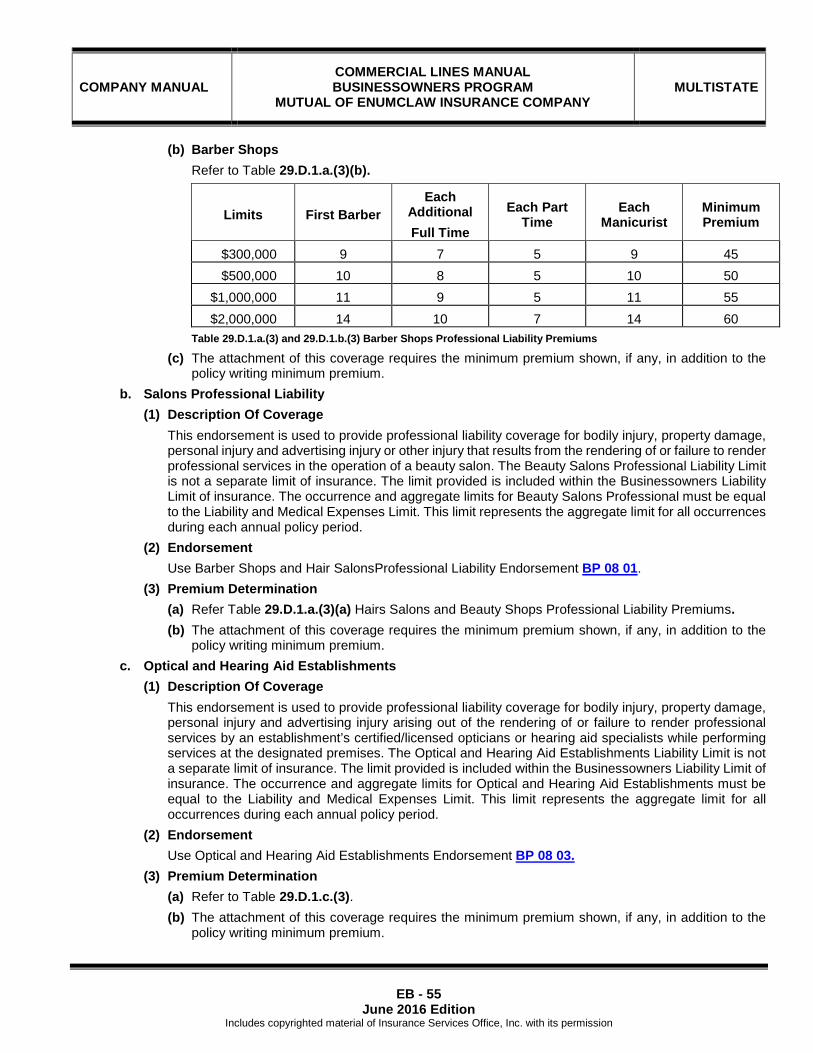

Limits First Barber Each

Additional Full Time

Each Part Time

Each Manicurist

Minimum Premium

$300,000 9 7 5 9 45 $500,000 10 8 5 10 50

$1,000,000 11 9 5 11 55 $2,000,000 14 10 7 14 60

Table 29.D.1.a.(3) and 29.D.1.b.(3) Barber Shops Professional Liability Premiums

(c) The attachment of this coverage requires the minimum premium shown, if any, in addition to the policy writing minimum premium.

b. Salons Professional Liability (1) Description Of Coverage

This endorsement is used to provide professional liability coverage for bodily injury, property damage, personal injury and advertising injury or other injury that results from the rendering of or failure to render professional services in the operation of a beauty salon. The Beauty Salons Professional Liability Limit is not a separate limit of insurance. The limit provided is included within the Businessowners Liability Limit of insurance. The occurrence and aggregate limits for Beauty Salons Professional must be equal to the Liability and Medical Expenses Limit. This limit represents the aggregate limit for all occurrences during each annual policy period.

(2) Endorsement Use Barber Shops and Hair SalonsProfessional Liability Endorsement BP 08 01.

(3) Premium Determination (a) Refer Table 29.D.1.a.(3)(a) Hairs Salons and Beauty Shops Professional Liability Premiums. (b) The attachment of this coverage requires the minimum premium shown, if any, in addition to the

policy writing minimum premium. c. Optical and Hearing Aid Establishments

(1) Description Of Coverage This endorsement is used to provide professional liability coverage for bodily injury, property damage, personal injury and advertising injury arising out of the rendering of or failure to render professional services by an establishment’s certified/licensed opticians or hearing aid specialists while performing services at the designated premises. The Optical and Hearing Aid Establishments Liability Limit is not a separate limit of insurance. The limit provided is included within the Businessowners Liability Limit of insurance. The occurrence and aggregate limits for Optical and Hearing Aid Establishments must be equal to the Liability and Medical Expenses Limit. This limit represents the aggregate limit for all occurrences during each annual policy period.

(2) Endorsement Use Optical and Hearing Aid Establishments Endorsement BP 08 03.

(3) Premium Determination (a) Refer to Table 29.D.1.c.(3). (b) The attachment of this coverage requires the minimum premium shown, if any, in addition to the

policy writing minimum premium.

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 12

JuneMarch 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

c. Casual Dining Restaurants (1) Definition

Casual dining restaurants serve moderately priced food in a casual atmosphere to patrons who generally order and are served while seated and pay after eating. Take-out service and the use of a buffet may also be available. These restaurants may serve no alcoholic beverages; serve beer and wine only; or serve beer, wine and liquor.

(2) Additional Eligibility Requirement Casual dining restaurants are subject to the following additional eligibility requirements: (a) Sales of alcohol no greater than 35% of total sales; (b) Gross annual sales may be no more than $7,500,000 per location; (c) Seasonal operations (risks that are closed for more than 30 consecutive days) must be referred to

company for approval; (d) Installation and maintenance of an automatic extinguishing system for cooking equipment

equivalent to that which is recommended by NFPA Standard #96, as described in Paragraph b.(3); (e) No dancing permitted; (f) No bar operations during hours when full table service is not also available. Bar operations for the

sole purpose of consuming alcoholic beverages are not permitted. 8. Wholesale Risks

Building and business personal property for wholesale businesses listed in the Businessowners Classification Table Section of the manual are the only types of wholesale risks eligible for the Businessowners Program, subject to the following requirements: a. No more than 50,000 square feet of total floor area any one building; b. Gross annual sales may be no more than $10,000,000 per location; c. No more than 15% of gross annual sales or total floor area may be derived from retail operations; The Wholesale classifications do not include the operations of manufacturers’ representatives or contractors.

9. Hotel/Motels Building and business personal property for hotel/motel risks are eligible for coverage under the Businessowners Program. Hotel/Motels are subject to the following additional eligibility requirements: a. Buildings not to exceed six(6) stories in height. Buildings with four(4) stories or more must be sprinklered.

No limitation applies to floor area; b. Seasonal operations (risks that are closed for more than 30 consecutive days) must be referred to company

for approval; c. Pools allowed – no diving board or slide – fenced and available to guests only; and a.d. Gross annual sales may be no more than $7,000,000 per location.

B. Ineligibility Risks specifically listed below are not eligible for the Businessowners Policy: 1. Automobile repair or service stations; automobile, motor home, mobile home or motorcycle dealers, unless

described as eligible in the Businessowners Classification Table; 2. Parking lots or garages, unless incidental to another otherwise eligible class; 3. Bars, grills and restaurants; unless described as eligible in Paragraph 7. above; 4. Contractors; 5. Buildings occupied in whole or in part for manufacturing or processing, unless all such occupancies are eligible

risks as shown in the Businessowners Classification Table;

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 13

JuneMarch 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

6. Insureds whose business operation involves one or more locations which are used for manufacturing, processing or servicing; unless described as eligible in the Businessowners Classification Table;

7. Household personal property; 8. One or two family dwellings unless of garden apartment variety where multiple units are grouped within a single

area and are under common ownership, management and control; 9. Places of amusement; 10. Banks, building and loan associations, savings and loan associations, credit unions, stockbrokers and similar

financial institutions; (Lessors risks with these occupancies are eligible); 11. Rental equipment stores; 12. Buildings constructed more than 30 years ago unless the common hazards (heating, cooling, electrical, wiring,

plumbing and roof) have been completely renovated or replaced within the last 20 years, unless approved by the company. The common hazards must meet applicable local and state codes;

13. Consignment goods in excess of 25% of total inventory; 14. Espresso Stands or Carts which are transported between multiple locations; 15. Second hand, used goods and antique stores or dealers; 16. "Direct import" of goods or merchandise for resale (wholesale or retail) or "direct import" of stock used in

manufacturing, service or repair operations. "Direct import" is defined as products imported directly from sources outside the United States of America;

17. Manufacturers representatives; 18. Businesses specializing in liquidated or distressed goods; For exceptions, refer to company.

C. Computation of Floor Area Do not use basement areas not open to the public in computing floor areas.

D. Aggregate Building and Personal Property Limit 1. Businesses having building and personal property aggregate values of $15,000,000 or less per location are

eligible. 2. Locations will be considered as separate locations if they are a minimum of 100 feet apart.

E. Building and Personal Property Ownership 1. When under one ownership, eligible building and personal property must be included in the same policy. 2. When writing a home business policy, the applicable homeowners coverage policy must also be written with

Mutual of Enumclaw Insurance Company.

RULE 23. PREMIUM DEVELOPMENT – MANDATORY COVERAGES A. General Rules

1. Annual Period All rates and premiums referred to in this manual are for an annual period.

2. Applicable to All Types of Eligible Risks a. Compute premium separately for mandatory property and liability coverages. b. For mandatory property coverage, the rates apply per $100 of the limit of insurance. The limit of insurance

must be the replacement cost value of the property to be insured unless the Actual Cash Value – Buildings Option applies. Refer to Rule 28.A.2.

c. Compute premium for Tenants Improvements and Betterments using the rates for Building in lieu of Business Personal Property.

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 14

JuneMarch 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

d. For mandatory liability coverage, rates apply per $100 of the limit of insurance (as defined in Paragraph b.) or per $1,000 of annual gross sales. Refer to Paragraphs 3. and 4.

e. For limits of insurance not displayed in the manual, interpolate the factors using the nearest amount above and below the selected amount. Refer to the following example: Interpolation Rule Example (Limit Of Insurance) The factors shown in this example are for illustrative purposes only and are not necessarily the factors shown in the limit of insurance tables of this manual. (1) If the selected building limit of insurance is $315,000, the nearest factors are $300,000 and $325,000. (2) For $300,000 under Group A, the factor is 0.840 and for $325,000 the factor is 0.812. (3) Calculate the difference between the two factors and divide by 25 (the difference, in thousands,

between 325,000 and 300,000). This provides a factor per $1,000. 0.840 -0.812

0.028 ÷ 25 = 0.001 (4) Multiply the factor determined in Paragraph (3) per $1,000 times 15 (the difference in thousands

between 315,000 and 300,000) and subtract from 0.840, the factor for $300,000. 0.001 X 15 0.015

0.840 – 0.015 = 0.825 (5) The result in this example is 0.825.

3. Applicable to Convenience Food Stores/Grocery Stores/Supermarkets/Restaurants With Gasoline Sales The exposure base for mandatory liability premium determination is dependent upon the combination of occupancies selected for combined Convenience Food Stores/Grocery Stores/Supermarkets/Restaurants With Gasoline Sales (Limited Cooking and Fast Food) risks. Refer to the Businessowners Classification Table Section of the manual. When determining the amount of annual gross sales for occupancies with gasoline stores, do not use the amount of gasoline sales in the calculation.

4. Applicable To Restaurants For restaurant occupant risks, the mandatory liability rates apply per $1,000 of annual gross sales.

5. Applicable To Hotel/Motels For hotel/motel occupant risks, the mandatory liability rates apply per $1,000 of annual gross sales.

B. Special Rules 1. Combined Apartment And Office Occupancies

Rate combined apartment and office properties with 25% or less of the total floor area used for office occupancy as apartments; if more than 25% of the total floor area is occupied as office, rate as office.

2. Predominant Occupancy – Apartment Or Office If apartment or office buildings contain eligible restaurant occupancies, rate property as a restaurant. If apartment or office buildings contain eligible occupancies other than restaurants, the rate of the occupancy (other than the apartment or office) with the largest total floor area applies. (If no single occupancy has the largest total floor area, use the highest rate.)

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 36

JuneMarch 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

c. Premium Determination (1) Deductibles

Apply the mandatory percentage deductibles as specified in the Earthquake company rates/ISO loss costs of CLM Division Five - Fire and Allied Lines.

(2) Rating Multiply the 80% coinsurance earthquake company loss cost determined in CLM Division Five - Fire and Allied Lines by a factor of 1.621. Multiply the rate determined in Paragraph (1) above by a factor of 1.20 (in recognition of coverage granted for loss of income) to obtain the Businessowners Earthquake company rate. Multiply the result by the limit of insurance (per $100).

NOTE: This coverage is not available for new business and cannot be added to an existing policy. 10. Restaurant Enhancement Endorsement

a. Description Of Coverage The following optional enhancement endorsement is available to any risk that includes a restaurant exposure.

b. Endorsement Use Restaurant Enhancement Endorsement EB 99 07.

c. Premium Determination The premium charge for this optional enhancement is a flat charge and no modifications will apply: (1) First location; $200; (2) Each additional location; $50.

11. Hotel/Motel Enhancement Endorsement a. Description of Coverage

The following optional enhancement endorsement is available to any risk that includes a hotel/motel exposure.

b. Form Use Hotel/Motel Enhancement Endorsement EB 99 09.

c. Premium Determination The premium charge for this optional enhancement is a flat charge and no modifications will apply: (1) First location; $175; (2) Each additional location; $50.

B. Liability Endorsements 1. Comprehensive Business Liability Exclusion (All Hazards in Connection With Designated Premises,

Operations Or Products a. Description Of Coverage

This endorsement excludes specific projects, location hazards, operations or equipment, if clearly separable and definable.

b. Endorsement Use Comprehensive Business Liability Exclusion Endorsement BP 04 01.

COMPANY MANUAL COMMERCIAL LINES MANUAL BUSINESSOWNERS PROGRAM

MUTUAL OF ENUMCLAW INSURANCE COMPANY MULTISTATE

EB - 54

JuneMarch 2016 Edition Includes copyrighted material of Insurance Services Office, Inc. with its permission

(2) Contractors on policies covering subcontractors; but only for liability for ongoing operations performed for such owners, lessees or contractors by the insured contractor or subcontractor.

b. Endorsement Use Additional Insured - Owners, Lessees Or Contractors Endorsement BP 04 50.

17. Primary And Noncontributory – Other Insurance Condition – Refer To Company a. Description

This endorsement provides that the coverage made available to an additional insured will be provided on a primary and noncontributory basis.

b. Endorsement Use Primary And Noncontributory – Other Insurance Condition Endorsement BP 14 88.

c. Premium Development (1) The premium for the attachment of this endorsement is Refer To Company; or (2) $25 unless otherwise adjusted.

D. Endorsements Applicable to Specific Classes 1. Professional Liability Endorsements

a. Barber Shops and Hair Salons Professional Liability (1) Description Of Coverage