Embed Size (px)

Citation preview

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 1/19

FII inflows and rising rupee

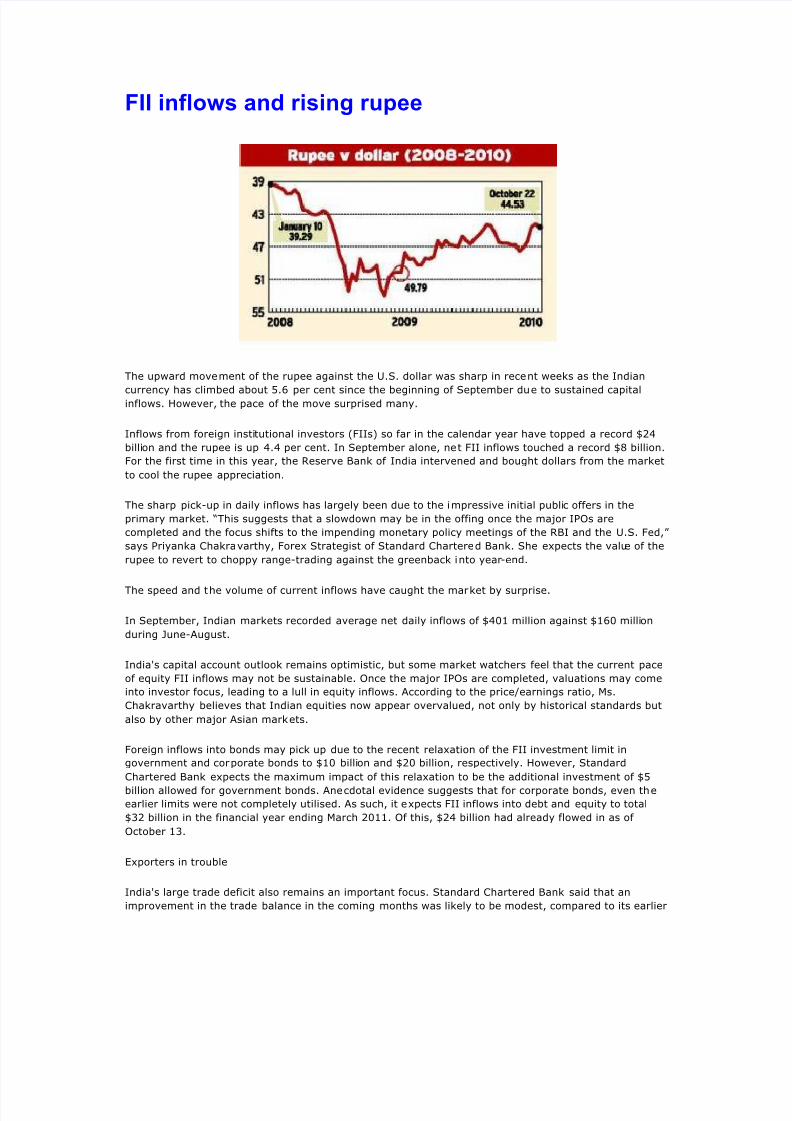

The upward movement of the rupee against the U.S. dollar was sharp in recent weeks as the Indian

currency has climbed about 5.6 per cent since the beginning of September due to sustained capitalinflows. However, the pace of the move surprised many.

Inflows from foreign institutional investors (FIIs) so far in the calendar year have topped a record $24

billion and the rupee is up 4.4 per cent. In September alone, net FII inflows touched a record $8 billion.

For the first time in this year, the Reserve Bank of India intervened and bought dollars from the market

to cool the rupee appreciation.

The sharp pick-up in daily inflows has largely been due to the impressive initial public offers in the

primary market. ³This suggests that a slowdown may be in the offing once the major IPOs are

completed and the focus shifts to the impending monetary policy meetings of the RBI and the U.S. Fed,´

says Priyanka Chakravarthy, Forex Strategist of Standard Chartered Bank. She expects the value of the

rupee to revert to choppy range-trading against the greenback into year-end.

The speed and the volume of current inflows have caught the market by surprise.

In September, Indian markets recorded average net daily inflows of $401 million against $160 million

during June-August.

India's capital account outlook remains optimistic, but some market watchers feel that the current pace

of equity FII inflows may not be sustainable. Once the major IPOs are completed, valuations may come

into investor focus, leading to a lull in equity inflows. According to the price/earnings ratio, Ms.

Chakravarthy believes that Indian equities now appear overvalued, not only by historical standards but

also by other major Asian markets.

Foreign inflows into bonds may pick up due to the recent relaxation of the FII investment limit in

government and corporate bonds to $10 billion and $20 billion, respectively. However, Standard

Chartered Bank expects the maximum impact of this relaxation to be the additional investment of $5

billion allowed for government bonds. Anecdotal evidence suggests that for corporate bonds, even the

earlier limits were not completely utilised. As such, it expects FII inflows into debt and equity to total

$32 billion in the financial year ending March 2011. Of this, $24 billion had already flowed in as of

October 13.

Exporters in trouble

India's large trade deficit also remains an important focus. Standard Chartered Bank said that an

improvement in the trade balance in the coming months was likely to be modest, compared to its earlier

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 2/19

expectations. ³We now expect the trade deficit to widen to $146 billion 2010-11 from $138 billion

previously. Thus, the monthly trade deficit is likely to stay in double digits.

In such a scenario, a slowdown in capital inflows may result in a renewed focus on deficit financing risks,

leading to another episode of dollar-rupee range-trading,'' the bank said.

The rupee appreciation in the last few weeks again put exporters into enormous trouble, says S.

Dhananjayan, Financial Advisor, Forex Derivatives Consumer Forum, Tirupur. According to him,exporters are finding it extremely difficult to cope with such wide and short-term fluctuations in the

dollar-rupee exchange rate due to heavy competition among other competing countries and the less

favourable status for Indian exports as compared to, say, Bangladesh due to its most favoured nation

status with the U.S. and the EU.

As seen in 2007-08, the rupee appreciation is caused mainly due to FII inflows into the capital market in

India. Mr. Dhananjayan warns that these inflows are purely speculative and hedge fund money which

are intended to jack up the indices and the FIIs would quit instantaneously as and when they decide to

book profits. ³This kind of uncontrolled capital flows that artificially creates volatility in the currency

market is unhealthy for the real economy.´ According to him, a similar scenario in 2007 was grossly

misused by banks which acted as cat's paw for their U.S. counterparts, thereby, selling illegal derivative

contracts to gullible exporters across the country. ³We've seen the rupee go from 52 to 39 and back and

forth,´ V. Balakrishnan, Infosys Chief Financial Officer told reporters early this month. ³It will kill the

whole export industry. The RBI has no choice but to intervene at some point in time, like every othercountry,´ he said. It was also reported that Infosys suffers a 40-basis point drop in operating margin for

every one per cent movement in the rupee.

The rupee has gained about 15 per cent since it slid to a record low of 52.185 in March 2009. It had

strengthened past 39 on January 15, 2008.

The International Monetary Fund (IMF) chief recently asserted the need for better control over capital

flows. While meeting central bankers, IMF Managing Director Dominique Strauss-Kahn said, ³Asia is

leading the global recovery and is moving swiftly back toward normal policy conditions. Capital flows are

flooding in. We do not want history to repeat itself in such a short time span.´ Mr. Kahn noted that while

the capital flooding into fast-growing China and other Asian countries could spur growth, it could also

fuel excessive lending, asset price bubbles and financial instability.

In some cases, controls on capital might be justified to stem such risks, he said.

But India and China are unlikely to heed this. After the rupee rose to a two-year high against the dollar,

Finance Minster Pranab Mukherjee told reporters in Washington early this month that there was no need

to curb foreign investment. ³I do not think that the situation has arisen in the Indian economy today,´

said Mr. Mukherjee. It is the responsibility of the central bank of every country to watch inflows that

may make it vulnerable to currency appreciation, and intervene as and when it is necessary, he said.

China is in no mood to appreciate the yuan. Yi Gang, Vice Governor of the People's Bank of China,

reportedly stated that the country was resolved to push ahead with cautious reforms of its own currency

regime. This statement, critics believe, is the strategy of keeping the Chinese yuan artificially

undervalued, making the country's exports cheaper in overseas markets and contributing to huge

imbalances in trade.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 3/19

FII INFLOWS IN INDIA

The FII inflows into the primary market in India comes mainly through the conversion of foreign

currency convertible bonds (FCCBs), private placement to qualified institutions placements (QIPs), initial

public offers (IPOs), follow-on overseas offers, conversion of warrants and preferential offers.

PREFERENTIAL ALLOTMENT OF SHARES

Meaning

Every firm needs capital for investment. They need capital to meet expenditure like expansion,

diversification, modernization, M&A, etc., from time to time.

When a listed company doesn't want to go for further public issue and the objective is to raise huge

capital by issuing bulk of shares to selected group of people, preferential allotment is a good option.

A private placement is an issue of shares or of convertible securities by a company to a select group of

persons under Section 81 of the Companies Act, 1956 which is neither a rights issue nor a public issue.

This is a faster way for a company to raise equity capital.

A private placement of shares or of convertible securities by a listed company is generally known by

name of preferential allotment. A listed company going for preferential allotment has to comply with the

requirements contained in Chapter XIII of SEBI (DIP) Guidelines, in addition to the requirements

specified in the Companies Act. In short, preferential issue means allotment of equity to some selected

people by a company which has its share already listed.

Advantages

One advantage of raising money via a preferential issue is that it helps save costs and time involved in apublic issue. More important, if the concerned company is not doing too well at that point in time but

requires capital, then retail investors may not want to participate in an issue.

At the same time, there could be some institutions which view the company's troubles as being

temporary and feel that some injection of capital could help it out of the trough.

In fact, promoters need such investors in times when the market sentiment is weak and a public issue

could fail. Moreover, if promoter is being allotted preferential issue and they acquire more shares in the

company, it is a good sign because it shows that the corporate ship is not sinking and they have abiding

interest in the company.

There is no requirement of filing any offer document / notice to SEBI in case of the preferential allotment

and even no eligibility norm for the company for the preferential allotment.

Apart from this, in the preferential allotment, the shares are issued in bulk and, hence, when huge fund

requirement is there without incurring much cost and without investing much time.

In current scenario, where there is lots of takeover in preferential issues, the shares are issued to

friendly investors like promoters to ward-off the risk of take over. If shares are issued to public, there is

a chance that later they can sell it to a firm which has an intension of take over.Demerits

The preferential allotment is often misused by the promoters as they could secure it because of majority

holding by them and they consolidate their hold on the company without paying a fair price for it. There

is also the chance of insider trading.

QUALIFIED INSTITUTIONS PLACEMENTS

Meaning

Primarily an issue can be classified as public issues, rights and private placements (also known as

preferential issues). QIPs are issued under the category of private placements.

A private placement is an issue of shares or of convertible securities by a company to a select group of

persons under Section 81 of the Companies Act, 1956 which is neither a rights issue nor a public issue.

This is a faster way for a company to raise equity capital. A private placement of shares or of convertible securities by a listed company is generally known by name of preferential

allotment.

A Qualified Institutions Placement is a private placement of equity shares or securities convertible into

equity shares by a listed company to Qualified Institutions Buyers only in terms of provisions of Chapter

XIIIA of SEBI (DIP) guidelines. The chapter contains provisions relating to pricing, disclosures, currency

of instruments etc. There are no eligibility norms for a listed company making a preferential issue.

However for Qualified Institutions' placement (QIP), only those companies whose shares are listed in

NSE or BSE and those who are having a minimum public float as required in terms of the Listing

agreement are eligible.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 4/19

Advantages

Investors subscribing to shares pursuant to a preferential allotment face a one year lock-in period. The

securities allotted pursuant to the QIP Scheme also cannot be sold by the allottees for a period of one

year from the date of allotment but they can still do the same on a recognized stock exchange (even

within one year). This provision allows the investors an exit mechanism on the stock exchange withouthaving to wait for a minimum period of one year. This advantage has also added to the preferential

treatment received by QIPs from investors.

Another reason for preferring QIPs is that not more than 50 per cent of the equity can go to one

investor. As such mutual funds that are increasingly becoming as large an investor base as FIIs, will now

be able to participate in these issuances, thereby, creating a more level playing field.

Guiding regulations

As per SEBI guidelines, placements can be made only to the qualified institutions buyers which includes

FIIs, SEBI-registered venture capital funds, mutual funds, insurance companies and other institutional

investors and issuers would have to allocate a minimum of 10 per cent of such placements to mutual

funds. Promoters or those related to the issuers are barred from participating in such issues. For each

QIPs, there have to be at least two allottees for an issue size of up to Rs 250 crore, and at least five

allottees for an issue size in excess of Rs 250 crore. No single allottees are allotted in excess of 50 per

cent of the issue size. As per SEBI regulations the securities issued through QIPs are equity shares or

any securities other than warrants that could be converted into (or exchangeable with) equity shares.The disclosures and procedural stipulations are relatively less compared to the public issue process. SEBI

said the aggregate funds that can be raised through QIPs in one fiscal year should not exceed five times

of the net worth of the issuer at the end of the previous year. The pricing of the specified securities are

similar to that for GDR/FCCB (global depository receipts/foreign currency convertible bonds) issues. It

also avail all benefits of corporate actions such as stock splits, rights issue, bonus issue and so on.

Only listed companies can opt for the QIP route. A company can phase out its QIP and can do two QIPs

at a six-month interval.

FCCB

Meaning

It is a type of convertible bond issued in a currency different than the issuer's domestic currency. Inother words, the money being raised by the issuing company is in the form of a foreign currency. A

convertible bond is a mix between a debt and equity instrument. It acts like a bond by making regular

coupon and principal payments but these bonds also give the bondholder the option to convert the bond

into stock.

These are the debt instrument issued in a currency different than the issuer¶s domestic currency with an

option to convert them in common shares of the issuer company. It¶s a quasi debt instrument that helps

companies raise foreign currency funds at attractive rates. FCCBs are similar to bonds as they make

regular coupon (interest) payments and also give the bondholder an option to convert the bond into

stock.

Advantages

These types of bonds are attractive to both investors and issuers. The investors receive the safety of

guaranteed payments on the bond and are also able to take advantage of any large price appreciation in

the company's stock. (Bondholders take advantage of this appreciation by means warrants attached tothe bonds, which are activated when the price of the stock reaches a certain point.)

INITIAL PUBLIC OFFERING

Meaning

Public issues can be classified into Initial Public offerings and further public offerings. In a public offering,

the issuer makes an offer for new investors to enter its shareholding family. The issuer company makes

detailed disclosures as per the DIP guidelines in its offer document and offers it for subscription. Initial

Public Offering (IPO) is when an unlisted company makes either a fresh issue of securities or an offer for

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 5/19

sale of its existing securities or both for the first time to the public. This paves way for listing and trading

of the issuer¶s securities.

IPO is new shares Offered to the public in the Primary Market .The first time the company is traded on

the stock exchange. A prospectus is issued to read about its risk before investing. IPO is A company's

first sale of stock to the public.

OVERSEAS LISTING Companies go for overseas listing to increase the FII flow. The government has amended the ADR/GDR

norms to allow them such issues for companies going for simultaneous listing of their shares or follow-

on offers in international capital market.

Relaxation in overseas listing norms: Under existing rules, a company needs to be listed on a domestic

exchange before being allowed to list overseas. But now they would be in a position to tap overseas

markets before having to divest stakes on domestic exchanges.

The government is likely to allow global depository receipts (GDRs) and American Depository Receipts

(ADRs) through the automatic route. This would mean that such issues could be floated without the

government¶s prior permission. Companies would simply have to inform RBI once the issue is concluded.

Up until now, only sponsored ADRs/ GDRs were allowed through the automatic route, on the condition

that RBI is informed once the proceeds of the issue were ploughed back into the company. The

relaxation means that Companies would not need FIPB approval for ADRs/ GDRs. Instead, they could go

ahead with such offers after informing RBI about their respective proposals.

Read more: http://www.articlesbase.com/regulatory-compliance-articles/fii-inflows-in-india-

1242465.html#ixzz14thCSV3v

Under Creative Commons License: Attribution

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 6/19

I i t A i i l i II i lBS R

¡

¢

£ t

£ / M

¤ mb

¥

i A¤

¦

¤

§

t 26, 2010, 0:48 IST

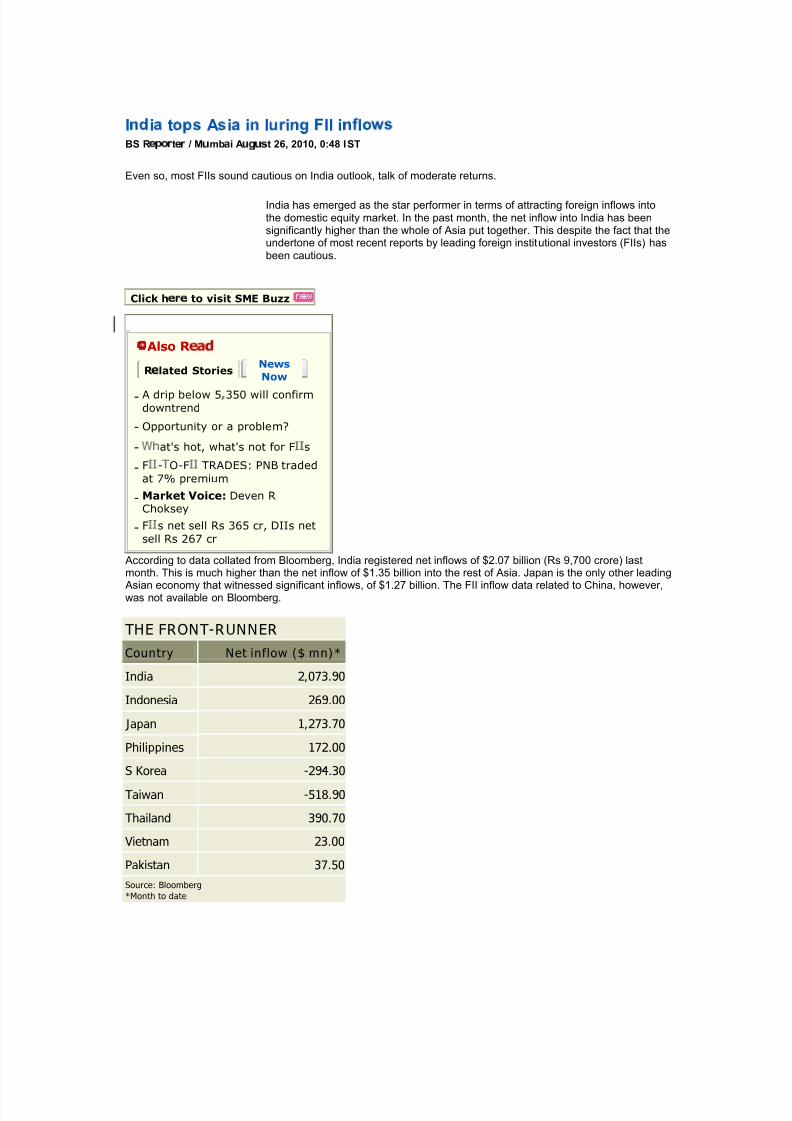

Even so, most FIIs sound cautious on India outlook, talk of moderate returns.

India has emerged as the star performer in terms of attracting foreign inflows intothe domestic equity market. In the past month, the net inflow into India has beensignificantly higher than the whole of Asia put together. This despite the fact that theundertone of most recent reports by leading foreign institutional investors (FIIs) hasbeen cautious.

Click h¨ © ̈

to visit SME Buzz

Also R

R ̈ lated Stories

News

Now

-

A drip below 5 350 will confirm downtrend

- Opportunity or a problem?

- at's hot, what's not for F s

- F -

O-F TRADES: PNB traded

at 7% premium

- Market Voice: Deven R

Choksey

- F s net sell Rs 365 cr, DIIs net

sell Rs 267 cr

According to data collated from Bloomberg, India registered net inflows of $2.07 billion (Rs 9,700 crore) lastmonth. This is much higher than the net inflow of $1.35 billion into the rest of Asia. Japan is the only other leading

Asian economy that witnessed significant inflows, of $1.27 billion. The FII inflow data related to China, however,was not available on Bloomberg.

THE FRONT-RUNNER

Country Net inflow ($ mn)*

India 2,073.90

Indonesia 269.00

Japan 1,273.70

Philippines 172.00

S Korea -294.30

Taiwan -518.90

Thailand 390.70

Vietnam 23.00

Pakistan 37.50

Source: Bloomberg

*Month to date

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 7/19

Some of t e ot er A

i!

" economies t

!

t repor ted net inflows in t e past mont

incl # de Indonesia $

%

&

6'

million),t

e P

ilippines

$

%

(

) &

million) and 0

ailand

$

%

1 ' 2

.)

million). Vietnam and Pakistan registered marginal inflows.Sout

Korea and 0

aiwan repor ted net outflows of %

& '

4million and %

3

(

'

million, respecti4

el5

. In India, t e past seven days alone saw

%

' 3

&

.3

million $ 6 s 4,43

2

crore) coming in. Incidentally, t e Indian 7 enchmark indices touched a new

1 2

-month high late last week.0

he inflows came in the 7 ackdrop of marketanalysts terming the recent surge as a ³li

8

uidity-dr iven rally´.

While 9 IIs have 7 een pour ing ample li

8

uidity into the Indian market, which 7 oasts one of the 7 est growth rates

across the globe, f oreign investors have also been talking about only modest earnings upgrade, going f orward,apar t f rom the low probability of high long-term returns.

In the latest India strategy repor t released on 0

uesday, Morgan Stanley has noted that valuation and return on equity $ 6 oE) need to be ³watched closely´.

³9 or now, we do not believe that long-term returns f rom Indian equities are likely to move significantly f rom the

recent trends $ the trailing

(

2

-year @

AG6

in returns is ( 4 per cent in rupee terms),´ it explains.

According toMorgan Stanley, there have been several examples in history when ³high growth has not translated into robust equity returns´. It, however , adds that India scores well on valuations and the ability of companies to translate macro growth into earnings. ³Valuations in India are off er ing equity investors an acceptable level of equity-r isk premium,´ it said.

Macquar ie attr ibutes the recent f oreign liquidity surge to the ³relative attractiveness of the economy´. It, however ,adds a word of caution: ³It is impor tant f or such flows to sustain, since there is always a r isk of shor t-term money flowing out in the event of r isk aversion coming back into the system. In the past, very high flows have indicated modest returns f or the market over the next (

&

months,´ says its latest India Strategy repor t.

According toMacquar ie, earning upgrades have become modest in India, after register ing a rapid surge in the past year . ³

0

here may be some downgrades in the near term as input cost pressures eat into the margins, but the under lying demand remains strong and bodes well f or corporate earnings,´ says the repor t.

While it is concerned on the valuation f ront, it f eels the Indian market still has upside potential. Macquar ie¶s one-year f orward Sensex target is (

'

,3 2 2

.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 8/19

FII inflows cross Rs. 1 Lakh Crore in 2010 !

At the start of the calendar year 2010, Sensex was perched at 17,500 levels. Since then, inflows from

FIIs has crossed the magical Rs.1 lakh crore mark ± an achievement by no means less than a gold

medal for the Indian stock markets and clearly a sign of confidence among the global funds in the India

Growth story. This gush of investment wind has taken the benchmark Sensex past 20,000 levels ± which

sums up to a decent 15 A rally since the start of the year.

Further, as more and more emerging markets ± such as Thailand, Brazil and South Korea ± impose

curbs on cheap overseas funds flow from developed nations; a substantial chunk of this flood of money

could find its way into the Indian markets. This sharp flow of money could render the Indian currency

more volatile in the light of increased inflows and outgo of capital at some point of time in future.

Investors must not lose sight of the crucial Law of Gravity which says ± whatever goes up, has to come

down! Moreover, the higher the markets move northward, steeper would be the fall on the downside.

Specifically, disappointing IIP data for the month of August that were released recently could well be a

cautionary sign for the investors to remain on their toes going forward.

After recording strong industrial output growth of 15.2 A in July, a fall in IIP numbers to just 5.9 A (the

lowest in past 15 months) has surprised the analysts ± questioning the sustainability of the current bout

of recovery.

Further, the sharp fluctuations in the IIP numbers over the last few months ± 15.2A

in April, 5.8A

in

June, 15.2A

in July and again 5.9A

in August ± has cast a doubt on the veracity and reliability of the

numbers. However, close observers of the key industrial data has pointed out that the volatility in

industrial growth rates has been driven by the capital goods segment, which grew by 72 A in July and

contracted by 2.6 A in August.

Additionally, equity analysts have expressed concerns about the heady levels of benchmark indices that

have witnessed a sharp run-up over the last couple of months ± powered by market euphoria and the

prevailing bout of liquidity wave (Read as Rs.1 lakh crore of hot FII money in 9-months). Concerns are

also being raised about the market¶s ability to absorb the mega-IPO offering from the state-owned Coal

India Ltd starting from October 18.

At current levels, markets have already factored in most of the positives including good monsoon and

better fiscal scenario of the domestic economy. However, the earnings season ± which is round thecorner ± might prove to be a good reality check to test the integrity and strength of the markets over

the next few weeks. Thus, for once, the fundamentals and earning prospects might try to over-whelm

the liquidity momentum and excess euphoria prevailing in the markets.

When the market sentiment is controlled by the liquidity ± it is not the right time for investments and

could well prove out to be more of a trading market.

Probably, this is not the time for stock market bravado !

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 9/19

µCurbs on FII inflows ruled out'

SPECIAL CORRESPONDENT

Union Finance Minister Pranab Mukherjee on Tuesday ruled out putting any curbs on FII(foreign institutional investor) inflows into the equity market but at the same time indicated that

the Reserve Bank of India might intervene to check the rupee appreciation if needed.

³At this time, I am not thinking of putting cap on FII inflows in the equity market,'' Mr.

Mukherjee said here. This year, the FII inflows have already reached $24.48 billion. Of this, FIIs

pumped in $6.11 billion, about 25 per cent of the total inflows so far in October alone.

The current levels of capital inflows, which exceeded the financing requirements of the current

account deficit, have put pressure on the rupee, resulting in its appreciation in the last few

months.

Mr. Mukherjee said the rising rupee had implications for exports. He hinted that the RBI was

keeping a close watch on the inflows and would take action if needed. ³We have faced similar

situation in the past and have overcome it without taking recourse to some of the more stringent

policy measures that are by now well known to discerning analysts,'' Mr. Mukherjee said.

The upward movement of the rupee against the U.S. dollar was sharp in recent weeks as the

Indian currency had climbed about 5.6 per cent since the beginning of September due to

sustained capital inflows.

Mr. Mukherjee said high FII inflows helped finance the current account deficit. ³I am confident

that with FII inflows and forex reserves, we will be able to contain the current account deficit at

around 3 per cent of GDP this fiscal,'' he said. It wa s around 3.6 per cent of GDP in the first

quarter of 2010-11.

The Finance Minister attributed this to higher non-petroleum imports which reflected in robust

customs duty collections. In the first six months of this fiscal, revenue collections from customs

jumped by 66.8 per cent to Rs.63,229 crore as compared to the same period in the previous year.

He said auction of 3G and broadband spectrum and disinvestment proceeds would help Indian

economy meet its expected growth. For the current fiscal, Mr. Mukherjee put the economic

growth at 8.25-8.75 per cent.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 10/19

FII inflows and their impact in

ajan Ghotgalkar is ountry Head - INDIA at Pr incipalInternational and Managing Director of Pr incipal Pnb AssetManagement ompany in association with Vi jaya Bank). he views expressed in this column are his own)

By B ajan Ghotgalkar C

he year D E E

8 has been one heck of a roller coaster r ide which left us with the kind of f eeling

when we are near ing the peak of the r ide and its time f or us to clench at the hand bars in anticipation of a r ide to base.

Everyone missed the huge stock market rally f ollowing the May D E E F

election results and whilstmost waited f or a correction, the market went on to scale new highs. Not many would disagree that, the market was ahead of its f undamentals but then it had nowhere to go but up when there was a flood of money chasing limited stock.

It was liquidity dr iving the pr ices up. Looking back everyone in the business came up with seemingly rational explanations f or this phenomenon. Someone once told me that, exper ts are people who can off er better explanations f or their f ailure ± here it was the f ailure to recognise the rally ear ly enough f or anyone to capitalise on it.

It is theref ore hardly surpr ising that, we are anxious about the coming year ± will it make us look

good or bad in the eyes of the investors when they look down f rom peak Sensex G H

I

E E

!Year

D E E

H saw FIIs br ing in about USD G H Bn. In the year D E E

8, USD G

D

Bn exited and that too in a real hurry; only to have USD

G 8 Bn come back in year

D E E F

.C

he details are interesting -about

I E

% of the inflows subscr ibed to QIPs and only aboutD

I

% went into the equity secondary market. In f act the DIIs, mostly insurance companies, put more money into the market than the FIIs i.e. after mutual f unds sold about

B s.6E E E

crores.

I should conf ess I am not too worr ied about the macro economic f uture.C

he India growth story is very much intact and kicking. We survived the global financial cr isis and the resulting contraction

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 11/19

in expor ts and exit of FIIs .I can saf ely say that, with all the green shoots being sighted around,India¶s BOP should hardly give cause f or concern.

Well one could wonder if India was at all impacted by the global cr isis or was it exper iencing a cyclical downturn in its economy ± but that¶s a discussion f or another day. However , we willcontinue to need every type of inf rastructure, houses f or the common man, roads f or the cars,electr icity, retail chains to replace our ineff ective PDS, financial products to finance all these

needs, consumer goods f or the rural masses, etc.I have no doubt that, FIImoney coming into the secondary equity market works like adrenalin and the moment it whittles down the market will gradually begin its dr ift downward.

P

he big question is what will tr igger this and if it does, when will it happen?

P

here are in my view three main sources of f oreign inflows: NQ

Imoney, FDI and FII flows into the secondary market.

India saw NQ

I remittances of about USDR

S

Bn in S T T

8 and was Q anked U

in migrantremittances even ahead of

V hina at about USD 4S

Bn, in year S T T

8. I can saf ely say that, there should be no cause f or concern on this f ront.

As f or the FDI, the India story is too attractive to ignore and if can successf ully f ree ourselves of the dreaded red tape, I would not be surpr ised if the FDI inflow was to double and even tr iple in 4

years.

P

heref ore, all things remaining equal, it is unlikely we will be threatened on this f ronteither .P

hat leaves the final but cr itical component, the FII inflow into the secondary equity market.P

he liquidity sloshing around in the global market is now being f eared as the possible cause f or an emerging market asset bubble which could devastate the financial markets after the tech and real estate busts.

P

his is the unpredictable var iable in our equation.P

he outcome will depend on reasons varying f rom the US interest rates, US Bond markets being impacted by the possible drop in V hinese expor ts, unexpected bank def aults in Eastern Europe and possible pressure on the many sovereigns around the globe suff er ing f rom ballooning deficits. I am also not cer tain about the extent to which the USD carry trade has impacted the rally in emerging markets.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 12/19

IPO performance dampens he inflows

µFII inflows likely to pick up by August'.

³Over the last one year irrespective of the quality of IPOs, expected subscription has not happened´ ±

Mr Sandip W

aichura, Business Head, PIN

X

Money

Suresh Par thasarathy

X

hennai,Y

une ̀

Mr Sandip W aichura, Business Head, PINX

Money, has taken up his position as Head of Wealth Management atthe firm after a

̀

a

-year stint in the financial industry. Star ting out as Economist with theMurugappa Group, he was involved in the initial setting up of MS

X

hola General Insurance. His previous assignment with them was as Head of broking at DBS

X

holamandalam Secur ities. Excerpts f rom the interview.

With the global economy yet to recover f ully f rom the recent cr isis, what is your outlook f or the FII inflows into the emerging markets like India?

In the shor t-term, FII inflows will definitely get impacted f or the simple reason that roughly half of the FIIs are hedge f unds and they use a lot of leverage. Over the next one year through the consensus is that FII inflows willtend to be positive. We should expect

b

̀-

a

billion in monthly inflows over the next one and half years. In India, we should not worry too much about what is happening in Europe, but about what is likely to happen in South East

Asia. Europe accounts f or below a c

per cent of our trade and that is pr imar ily low margin products. A large par t of our trade is especially in I

d

, capital goods space, impor t and expor t linkages in raw mater ials are now increasingly with SE Asia.

d

o that extent, if there are Korean conflicts or d

hailand enters into deeper political cr isis then we might have an issue. In my view, the European cr isis will be over in the next f ew months and to that extent inflows are likely to pick up by August.

Do you recommend that investors invest overseas?

No, we are currently not recommending that our customers invest overseas.d

here are f ew reasons to it. One is

that Indian regulations are changing quite f requently, a lot of investors who want to invest abroad are not only residents; but they may also beN W Is with Indian linkages.

d

he citizenship rules are changing so dramatically thattoday lot of customers don't know where the taxability ar ises and where it stops. For example, last month, there was a new rule asking N

W Is to surrender their Indian passpor ts. Indians use dual citizenships, if I am r ight now

they have given one month time to surrender the passpor t, on account of this, their investment in India may become taxable.

In that kind of complicated regime, investing overseas will not work.d

hat is one reason we are notrecommending it.

d

hen there is the f act that today f oreign money is coming to India and chasing growth, there is no growth to be chased outside. So if we were to recommend deposits today, any instruments linked to LIBO

W

would much inf er ior to a fixed deposit in India. Hardly any market gives you a ̀

c

per cent return globally. If you

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 13/19

go abroad and invest, you will be actually losing the money post inflation and especially if you use that money in India.

e

hree, we are seeing that the Indian currency is likely to be very volatile, it's currently fluctuating. If your requirement is rupee dependent, then why should you r isk investing aboard?

f eponses to recent IPOs have been tepid. Do you f oresee an improvement in near f uture?

I will give you two or three reasons f or this. One, the retail por tion is not being subscr ibed heavily; this is a new development. Over the last one year irrespective of the quality of IPOs, expected subscr iption has not happened in any IPO.

e

wo, the retail investors are actually out of the equity markets not just pr imary IPOs. If you look out at the per f ormance of the markets f rom September

g h h i

onwards, retail par ticipation is extremely low. As a percentage of the overall volume, it's actually declined. Within the retail par ticipation, in the last six months HNIs are chasing alternative assets. You have seen real estate make a come back, in f act well bef ore the equity market.

e

his is very rare phenomenon, normally you will see real estate revival only after the equity markets pick up.

e

hree, a lot of money has been flowing to deposits. At one point of time, Government papers were trading atp

.p

per cent and deposits were off er ing 6.

p

per cent even 8.p

per cent. So, a lot of customers bitten by equity markets turned to deposits. On top of all this, it's the IPO per f ormance itself.

f oughly half the IPOs are trading

below the issue pr ice. So, the retail investors are dormant over the last six-eight months across asset classes.

What are the asset classes you are recommending to your HNI clients?

e

he asset allocation depends on a f ew impor tant cr iter ia. One is that the r isk profile of the customer . When we evaluate the r isk we look at whether this person has the ability to take downside r isk to the por tf olio.

e

wo,whether this person requires f requent cash flows or he is looking at a growth por tf olio.

e

hree, the person's exper ience vis-a-vis ear lier investments. If we see investors with an aggressive profile in a two years plus time hor izon, we usually recommend a

q h

per cent allocation to equity as growth capital. Looking at the other side, if cash flow requirements are higher , or his investment exper ience is bad, the client will tend to do opposite of whatshould be done. For example, withdrawing SIPs, or not investing when the markets dip extremely.

e

hese are the contrar ian examples and f or this customer we will be recommending only

g p

per cent in equity and rest in fixed income. With in fixed income, fixed deposit is a miniscule por tion, we pr imar ily recommend long-dated FMPs or capital preservation papers which are available in mutual f unds. If there are customers who expect sharp appreciation f rom equities, then we recommend trading.

Have your clients made money in last one year?

It is very difficult to give any numbers I think it will be p

- r

h

percentage points more than the indices, if they are notvery aggressive. But if they are aggressive they would be still sitting on losses, especially if they traded very f requently. So I can't give any numbers.

With limited debt options available, what is your suggestion to the retail investors planning to build a debtpor tf olio?

e

he easiest choice is fixed deposits.e

oday, AAA-rated companies off er any where between 8-8.p

per cent.e

he second option is FMPs- there are plain FMPs and there are some FMP with linkages to capital markets which are also tend to off er similar returns to bank deposits, but with tax benefits.

e

here are bonds with residual matur ity with

g

-s

years at very attractive coupons with the under lying companies with AAA and AA rated off er ing i

per cent. For the customer who understands debt and wants to get better -than-inflation rates, there are products like

debentures too. Debentures will come in two var ieties, non conver tible debentures and conver tible and they off er i

.p

-r

h

. For instance, instruments like Shr iram e

ranspor t Nt

D were oversubscr ibed in a shor t span of time.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 14/19

Surging rupee increases expor ers' worryNayanima Basu / New Delhi Oc

u

ov

er w

,x y

y

,y

x

IS

No consensus on what, when and how much to do. ³It¶s very scary. I do not know what to do,´ says afique Ahmed, one of the largest Indian leather goods

expor ters, who has the likes of Walmar t on his buyers list.

Ahmed, based in

hennai, speaks here of the ever -r ising rupee. For him, por tf olio flows into India are now as impor tant as recovery in Europe. After all, f oreign institutional investors

FIIs) have pumped in close to

billion s

,

crore) this calendar year into the Indian equity markets and there are three more months to go bef ore the end of

.

ompounding the problem f or Ahmed and other expor ters is the absence of hedging.

hough everyone expected the rupee to r ise, it is the quantity of increase and the pace it is appreciating that has f oxed them. Besides, with not too many orders in the bag, hedging was not on the immediate hor izon f or several expor ters.

Already, they are dealing with a situation where there is no substantial increase in orders,month-on-month.³

hough there are plenty of orders f or the f estival season, it is not increasing and is nowhere near the pre-cr isis levels,´ says Sudhir Dhingra, chairman and managing director of Or ient

raft, one of the large textile expor ters.

lick f or table & graph)

µYou¶ll have o cope¶

hough the Federation of Indian Expor t Organisations, the expor ters¶ lobby group, has already called f or eserve

Bank of India BI) intervention, officials in the commerce depar tment are no longer talking in a tone that would remind you of yesteryears. ³Expor ters have to learn to live in a volatile currency scenar io.

hey have to hedge.

here is no other option,´ Union commerce secretary ahul Khullar said recently.

So f ar , BI ² which f ollows a policy of intervening in the markets to check extreme volatility in the rupee² has stayed away f rom buying dollars to stem the appreciation. As a result, last week, the Indian currency hit a five-month high against the greenback f ollowing a surge in FII inflows. It had appreciated by 4.

per cent last month.

ompared to last August, in real terms the rupee has appreciated by 4.

per cent against a basket of six currencies

see graph). Dur ing the past

months, the rupee, which closed at 44.6

against the dollar , has appreciated by almost six per cent against theUS currency.

A par t of the reason f or the absence of BI intervention is the f ear of adding to supply of the rupee in the system as a result of the purchase of dollars by the central bank. A higher supply would not augur well f or inflation,identified as the pr imary area of assault.

³In the shor t term, some appreciation in the rupee does not spell doom f or anyone in the economy. ather , it

reduces the cost of impor ted goods.

he rupee has seen two-way movement and there is no point in the keeping the value down, especially when everyone around the globe is doing the same thing. Shor t-term appreciation also improves the investment scenar io. Having said that, this should not continue f or long,´ says AshimaGoyal,prof essor at the Indira Gandhi Institute of Development esearch.

HDFC Bank¶s chief economist, Abheek Barua, says the r ising trend f or the rupee is unlikely to see a reversalsoon. ³

he last phase had been a f erocious appreciation, which is temporary.

he rupee would continue to appreciate f or some more time due to the

G telecom spectrum) auction and other broadband auctions which will be ultimately f unded by ECBs external commercial borrowings).

hat would act as a tr igger . However , postthat scenar io, a gradual depreciation cannot be ruled out. Perhaps it¶s time the

BI intervenes little bit in the

capital markets,´ he said.

³

he BImay have to resor t to ster ilisation of these f unds in case they do get out of hand, though the present

scenar io of liquidity being scarce could def er this process,´ rating agency C A E said in a recent repor t.

Will i help? But economists say even if the trend was reversed immediately, expor ts will not benefit significantly. ³If the recovery in the international markets is not good, then even a depreciating rupee would nothelp,´ says Goyal.

And, Barua added that expor ts f rom India and other developing countr ies are likely to slow down by the end of the financial year , mainly because of slow recovery in Amer ica and Europe.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 15/19

While expor ters might be complaining of losing competitiveness due to the currency, r ival Asian currencies are also f acing a similar problem, though the magnitude may vary

see graphic).

³India is not the only country where appreciation of the currency is happening.

he scenar io is the same f or allother developing Asian economies. Yes, the exchange rate does put pressure on the margins but this is not a single-directional aggressive movement of the rupee.

here had also been two-way movements,´ says SonalVarma, India economist at Nomura, the

apanese financial services firm.

³

his sudden r ise in the rupee, no doubt substantial, will not impact expor ts adversely. Never theless, cer tain sectors might f ace some difficulties, especially SMEs

small and medium enterpr ises). But we do expect a

j

k

per cent growth in expor ts compared to

l k k m

-l k

j

k

,´ says ING Vysya Bank¶s chief economist, Deepali Bhargava.

Dur ing the first five months of the current financial year , expor ts were estimated atn

8o

.l

billion, compared to n

66. l

bn a year ear lier , indicating an increase of l

8.6 per cent. Impor ts dur ing the same per iod grew by

.j per

cent to n

j 4

j .

m

bn f rom n

j

k

6.6 bn last year .

For the moment, however , expor ters are complaining. ³

he government talks about diversif ying the markets. Butit¶s not an easy task,´ says Or ient Craft¶s Dhingra.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 16/19

Q2 resul s, FII inflows o drive marke s in near ermy Story

y Comments

Read more on »q2 earnings|markets|investors|fii

he domestic stock markets remained strong last week f uelled by the continued inflows f rom f oreign

institutional investors

FIIs). After a shor t consolidation last week, the markets came back to a r ising graph and attempted to cross the all-time high levels again.

Analysts believe that strong FII inflows have the potential to take the markets to an all-time high and

at the moment the chances of a sharp correction are looking quite remote. However , investors should

exercise caution as the Coal India IPO is opening next week and is expected to draw out a large

amount of liquidity f rom the markets and may tr igger some consolidation or correction in the shor t

term.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 17/19

Also, the second quar ter results will star t coming out next week and investors should track them

closely. In the commodity market, gold surged to its record high of around USD ,

per ounce

boosted by worr ies over the dollar depreciation due to another round of stimulus announced by the

Federal

eserve. Silver also peaked to USD 24 an ounce.

T hese are some factors that have the potential to influence market direction in the short to medium

terms:

US sentiments up

eat

In the US, the markets remained upbeat on a good September quar ter earnings announcement by

some of the leading companies.z

he strong earnings by the ear lybird companies have raised

sentiments in the stock markets. On the other hand, the third quar ter numbers show that China's

f oreign exchange reserves soared f rom USD{ |

4 billion to USD 2.6}

tr illion.

z

his news f ur ther raised sentiments in the US markets as analysts believe that a higher surplus will

put f ur ther pressure on China to let its currency appreciate more. Appreciation in the Yuan will make

Chinese goods expensive in the f oreign markets and hence help the domestic companies compete

better with Chinese goods and repor t better sales/earnings.

Large IPO may draw out liquidity

Next week, the large initial public off er ~ IPO) of Coal India is opening.

z he IPO is expected to raise

s

{ } , crores. z he money raised by this IPO is not going to the company as the government is selling

{ percent in Coal India.

Analysts believe that markets which are trading close to an all-time high f uelled by high liquidity may

take a breather after the Coal India IPO.z he IPO is expected to draw out a good amount of liquidity in

the shor t term. Also, a consolidation is long due in the markets. A similar market behaviour was seen

dur ing the ear lier big ticket IPOs of NMDC, Nz PC etc and hence investors should exercise caution in

the markets.

FII inflows

z he por tf olio investments by f oreign institutional investors

~ FIIs) remained healthy last week and the

markets were pushed up.z he FIIs' net purchases this month itself crossed USD 2 billion. Analysts

believe that expectations of a f resh stimulus package f rom the Federal eserve resulted in more

money flowing into the emerging markets including India and China.

z he depreciation of the dollar is another reason f or the strong flows into emerging markets. Analysts

believe the strong FII inflows will continue in the shor t term and the markets are expected to remain

strong, making new highs.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 18/19

FII inflows in stock mts at Rs 71,000 cr

Posted: Sep 20, 2010 at 1036 hrs IST

New Delhi Betting big on the Indian equity markets, foreign fund houses have invested over Rs

71,000 crore (USD 15.6 billion) so far this year and analysts believe that soon it will breach the

record figure achieved in 2009.

In the last fortnight alone (September 1-17), the foreign institutional investors have a made net

investment of a whopping Rs 12,442 crore (USD 2.67 billion) in the Indian stock market, as per the

data available with market regulator Securities and Exchange Board of India.

As per the SEBI data, FIIs have made a net investment of Rs 71,824.50 crore in local stocks, while

their exposure in debt instrument stands at Rs 42,124.5 crore (USD 9.1 billion).

The low interest rate regime followed in many advanced economies to avert recession, coupled with

a better economic performance of emerging markets such as India and China, are key to attract a

chunk of foreign inflows, analysts said.

"FIIs continue to pour money into Indian financial assets amid bright prospects for economic growth

and corporate earnings," India Infoline Ltd Vice President (Research) Amar Ambani said.

Stock brokers are optimist about the Indian growth story and believe that soon the FII investment in

stock markets will cross the last year's record level.

Last year, Indian stock market attracted record inflows of Rs 83,400 crore, a period when the Sensex

recorded a gain of nearly 80 per cent.

"The market is sustaining the rally as inflows from FIIs is coming in relentlessly and in coming days

too, this rising spree is likely to continue," Geojit BNP Paribas Research Head Alex Mathews said.

On the back of huge inflows from FIIs, Sensex had been on a rising-spree in recent sessions. It

regained the 19,500-mark this month after a struggle of 32 months.

With such huge inflows from FIIs, marketmen believe the Sensex could reach its record high level of

21,200 easily in coming period. The Sensex had hit its lifetime high of 21,206 on January 10, 2008.

At present, the 30-share benchmark of the Bombay Stock Exchange is already trading at its highest

level since January 17, 2008.

In the week gone by, the index recorded a gain of 4.2 per cent and ended at 19,594.75-- its best

close since January 17, 2008. This weekly gain of 4.2 per cent was the best gain in a week so far in

2010.

"Foreign institutional investors are in a buying spree. If the trend remains the same then we can see

the index touching its record level very soon," a broker said.

FIIs play a significant role in domestic equity markets and their movement (inflow and outflow)

causes fluctuation in benchmark indices.

8/8/2019 FII Inflows

http://slidepdf.com/reader/full/fii-inflows 19/19

After pouring in Rs 83,000 crore in local markets, these investors began exiting in early 2010 and in

January they were net sellers of Rs 500 crore.

But from February, the scenario started changing and they were net buyers of Rs 1,216 crore. In

April, FIIs were net purchasers of shares worth Rs 9,361 crore, after pumping in Rs 19,928 crore in

March.

In June and July, FIIs made a total net investment of Rs 27,125 crore.

Maintaining their bullish stance for the third month in a row, global fund houses made a net

investment of Rs 11,685 crore (USD 2.5 billion) in Indian equities in August.