Embed Size (px)

Citation preview

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 1/57

Fi8000Fi8000Basics of Basics of

Options: Calls, PutsOptions: Calls, Puts

Milind ShrikhandeMilind Shrikhande

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 2/57

Derivatives - OverviewDerivatives - Overview

Derivative securitiesDerivative securities are financial contractsare financial contracts

that derive their value from other securities.that derive their value from other securities.

They are also calledThey are also called contingent claimscontingent claims because their payoffs are contingent of thebecause their payoffs are contingent of the

prices of other securities.prices of other securities.

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 3/57

Derivatives - OverviewDerivatives - Overview

☺Examples of underlying assets:Examples of underlying assets:☺Common stock and stock indexesCommon stock and stock indexes☺Foreign exchange rate and interest rateForeign exchange rate and interest rate☺

Futures contractsFutures contracts☺ Agricultural commodities and precious metals Agricultural commodities and precious metals

☺Examples of derivative securities:Examples of derivative securities:☺ Options (Call, Put)Options (Call, Put)☺ Forward and Futures contractsForward and Futures contracts☺ Fixed income and foreign exchange instruments suchFixed income and foreign exchange instruments such

as swapsas swaps

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 4/57

Derivatives - OverviewDerivatives - Overview

☺Trading venues:Trading venues:☺ Exchanges – standardized contractsExchanges – standardized contracts☺ Over the Counter (OTC) – custom-tailored contractsOver the Counter (OTC) – custom-tailored contracts

☺They serve as investment vehicles for They serve as investment vehicles for

both:both:☺

Hedgers (decrease the risk level of the portfolio)Hedgers (decrease the risk level of the portfolio)☺ Speculators (increase the risk)Speculators (increase the risk)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 5/57

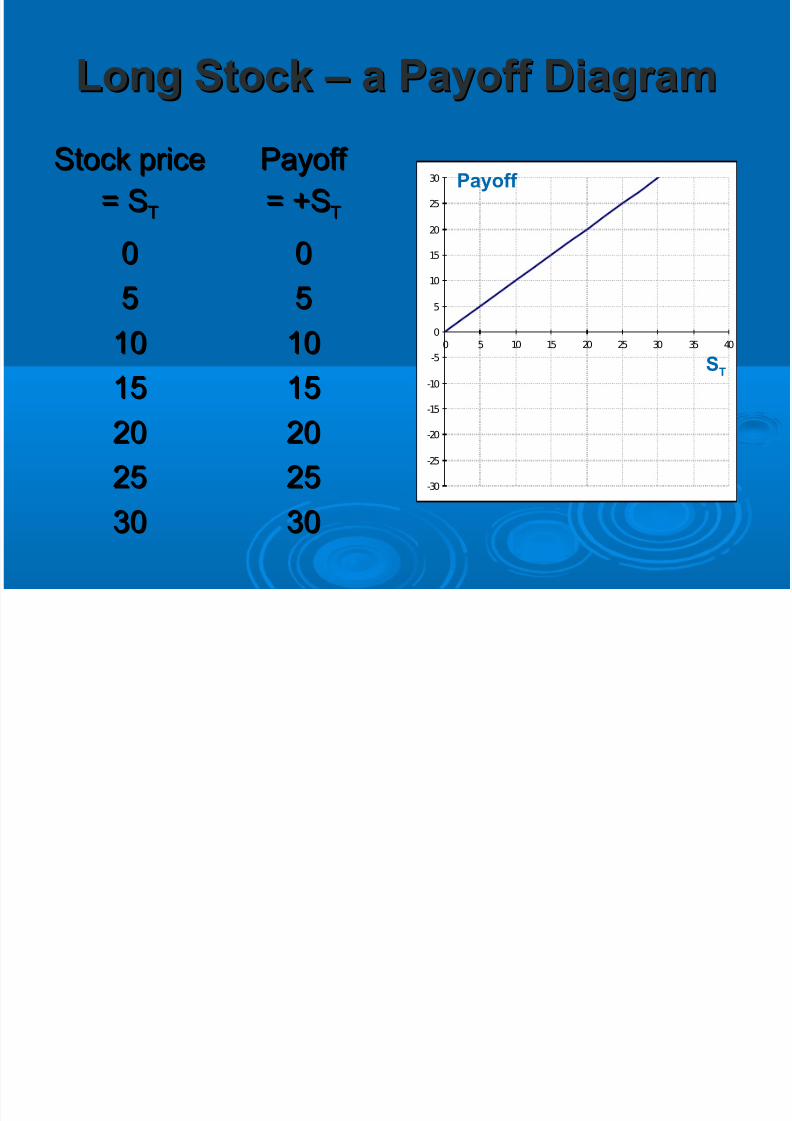

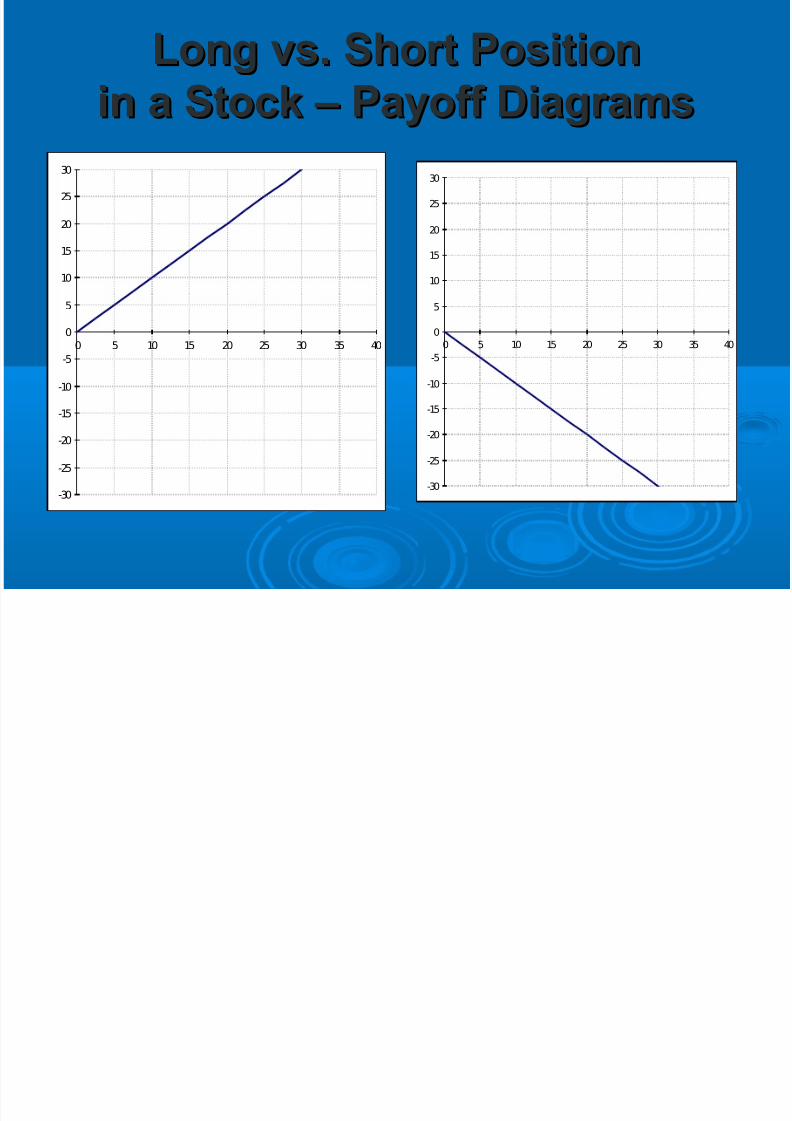

Long Position in a StockLong Position in a Stock

☺The payoff increases as the value (price)The payoff increases as the value (price)

of the stock increasesof the stock increases

☺The increase is one-for-one: for eachThe increase is one-for-one: for each

dollar increase in the price of the stock,dollar increase in the price of the stock,

the value of our position increases by onethe value of our position increases by one

dollar dollar

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 6/57

Long Stock – a Payoff DiagramLong Stock – a Payoff Diagram

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

Stock priceStock price

= S= STT

Payoff Payoff

= +S= +STT

00 00

55 55

1010 1010

1515 1515

2020 2020

2525 2525

3030 3030

ST

Payoff

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 7/57

Short Position in a StockShort Position in a Stock

☺The payoff decreases as the value (price)The payoff decreases as the value (price)of the stock increasesof the stock increases

☺The decrease is one-for-one: for eachThe decrease is one-for-one: for eachdollar increase in the price of the stock,dollar increase in the price of the stock,the value of our position increases by onethe value of our position increases by onedollar dollar

☺Note that the short position is a liabilityNote that the short position is a liabilitywith a value equal to the price of the stockwith a value equal to the price of the stock(mirror image of the long position)(mirror image of the long position)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 8/57

Short Stock – a Payoff DiagramShort Stock – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff Payoff

= -S= -STT

00 00

55 -5-5

1010 -10-10

1515 -15-15

2020 -20-20

2525 -25-25

3030 -30-30

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 9/57

Long vs. Short PositionLong vs. Short Position

in a Stock – Payoff Diagramsin a Stock – Payoff Diagrams

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 10/57

Long and Short Positions in theLong and Short Positions in the

Risk-free Asset (Bond)Risk-free Asset (Bond)

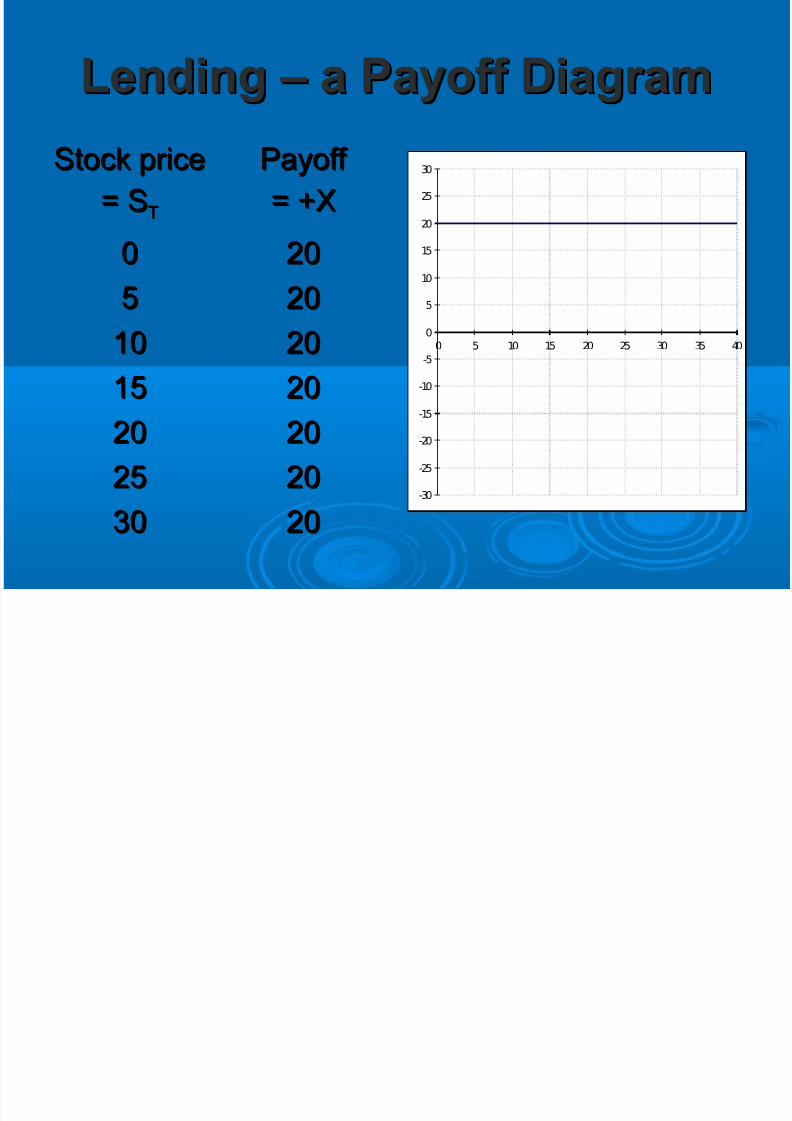

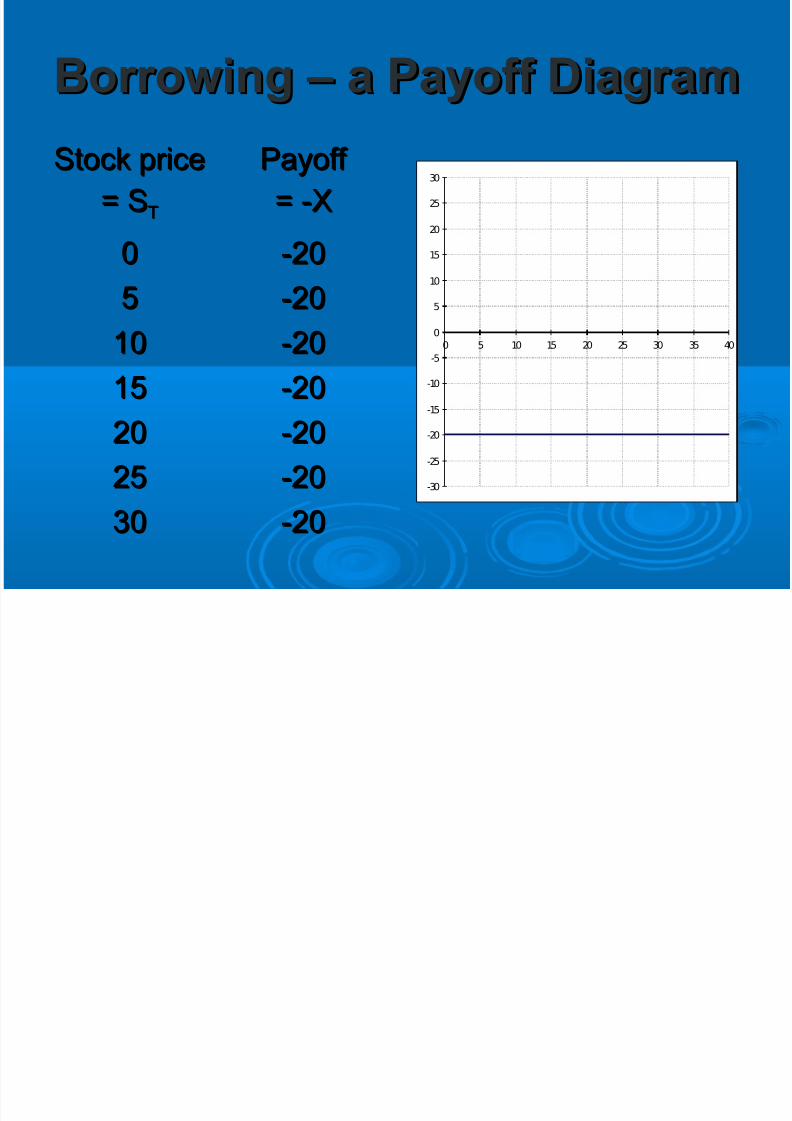

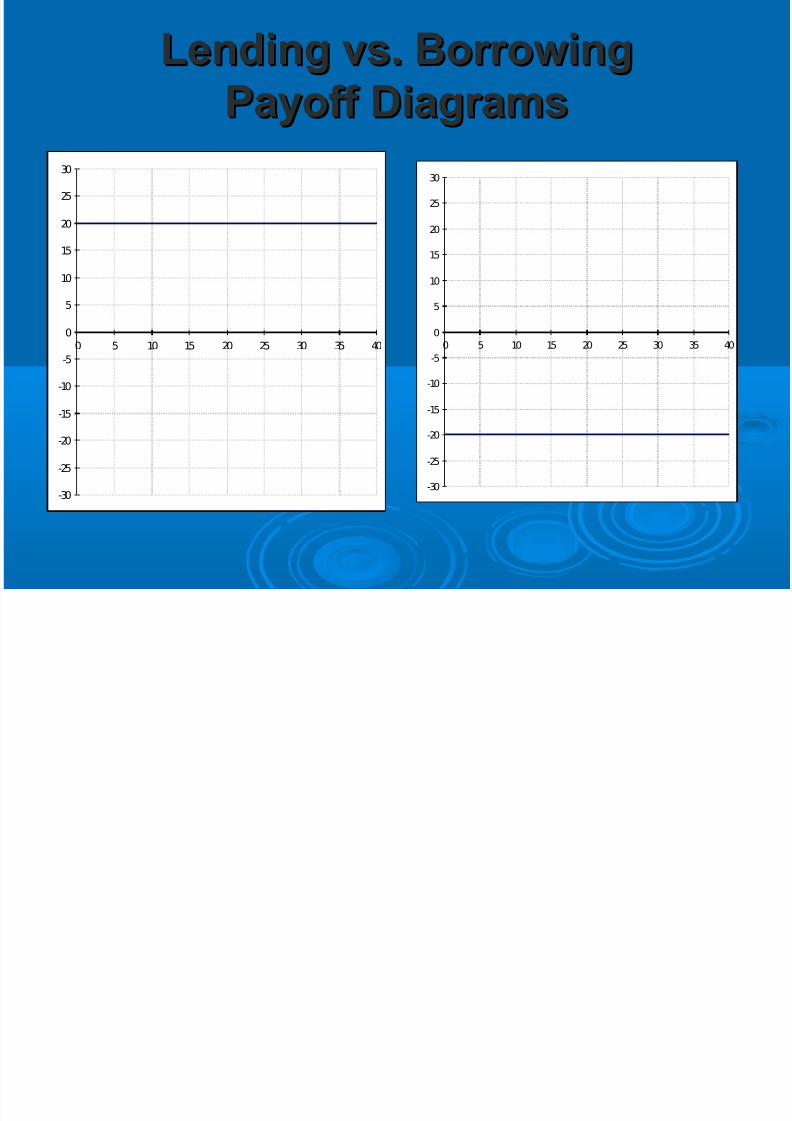

☺The payoff is constant regardless of theThe payoff is constant regardless of the

changes in the stock pricechanges in the stock price

☺The payoff is positive for a lender (longThe payoff is positive for a lender (long

bond) and negative for the borrower (shortbond) and negative for the borrower (shortbond)bond)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 11/57

Lending – a Payoff DiagramLending – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff Payoff

= +X= +X

00 2020

55 2020

1010 2020

1515 2020

2020 2020

2525 2020

3030 2020-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 12/57

Borrowing – a Payoff DiagramBorrowing – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff Payoff

= -X= -X

00 -20-20

55 -20-20

1010 -20-20

1515 -20-20

2020 -20-20

2525 -20-20

3030 -20-20

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 13/57

Lending vs. BorrowingLending vs. Borrowing

Payoff DiagramsPayoff Diagrams

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 14/57

A Call OptionA Call Option

A European* call option gives the buyer A European* call option gives the buyer of the optionof the option a right to purchasea right to purchase thetheunderlying asset, at the contractedunderlying asset, at the contractedprice (theprice (the exerciseexercise or or strike pricestrike price) on) ona contracted future date (thea contracted future date (theexpiration dateexpiration date))

** An An American American call option gives the buyer of the option (long call) acall option gives the buyer of the option (long call) aright to buy the underlying asset, at the exercise price,right to buy the underlying asset, at the exercise price, on or beforeon or before the expiration datethe expiration date

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 15/57

Call OptionCall Option - an Examplean Example

A March (European) call option on Microsoft A March (European) call option on Microsoftstock with a strike price $20, entitles thestock with a strike price $20, entitles theowner with a right to purchase the Microsoftowner with a right to purchase the Microsoft

stock for $20 on the expiration date*.stock for $20 on the expiration date*.

What is the owner’s payoff on the expirationWhat is the owner’s payoff on the expirationdate? Under what circumstances does hedate? Under what circumstances does he

benefit from the position?benefit from the position?* Note that exchange traded options expire on the third Friday of the* Note that exchange traded options expire on the third Friday of theexpiration month.expiration month.

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 16/57

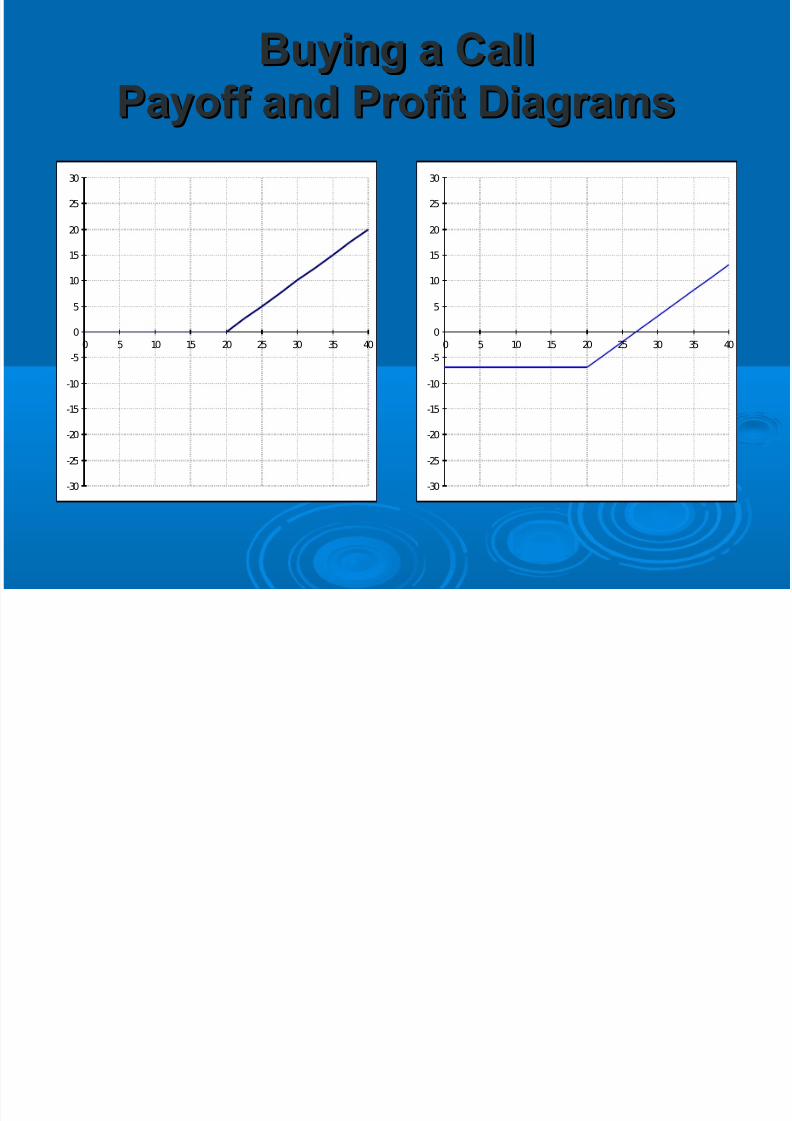

The Payoff of a Call OptionThe Payoff of a Call Option

☺ On the expiration date of the option:On the expiration date of the option:☺ If Microsoft stock had fallen below $20, the call wouldIf Microsoft stock had fallen below $20, the call would

have been left to expire worthless.have been left to expire worthless.☺ If Microsoft was selling above $20, the call holder If Microsoft was selling above $20, the call holder

would have found it optimal to exercise.would have found it optimal to exercise.☺ Exercise of the call is optimal at maturity if theExercise of the call is optimal at maturity if the

stock price exceeds the exercise price:stock price exceeds the exercise price:☺ Value at expiration (payoff) is the maximum of two:Value at expiration (payoff) is the maximum of two:

Max {Stock price – Exercise price, 0} = Max {S Max {Stock price – Exercise price, 0} = Max {S T T – X, 0} – X, 0}

☺ Profit at expiration = Payoff at expiration - PremiumProfit at expiration = Payoff at expiration - Premium

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 17/57

NotationNotation

S = the price of the underlying asset (stock)S = the price of the underlying asset (stock)

(we will refer to S(we will refer to S00=S, S=S, S

tt or Sor STT))

C = the price of a call option (premium)C = the price of a call option (premium)(we will refer to C(we will refer to C

00=C, C=C, Ctt or Cor C

TT))

X or K = the exercise or strike priceX or K = the exercise or strike price

T = the expiration dateT = the expiration date

t = a time indext = a time index

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 18/57

Buying a Call – a Payoff DiagramBuying a Call – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff =Payoff =

Max{SMax{STT-X, 0}-X, 0}

00 00

55 00

1010 00

1515 00

2020 00

2525 55

3030 1010-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 19/57

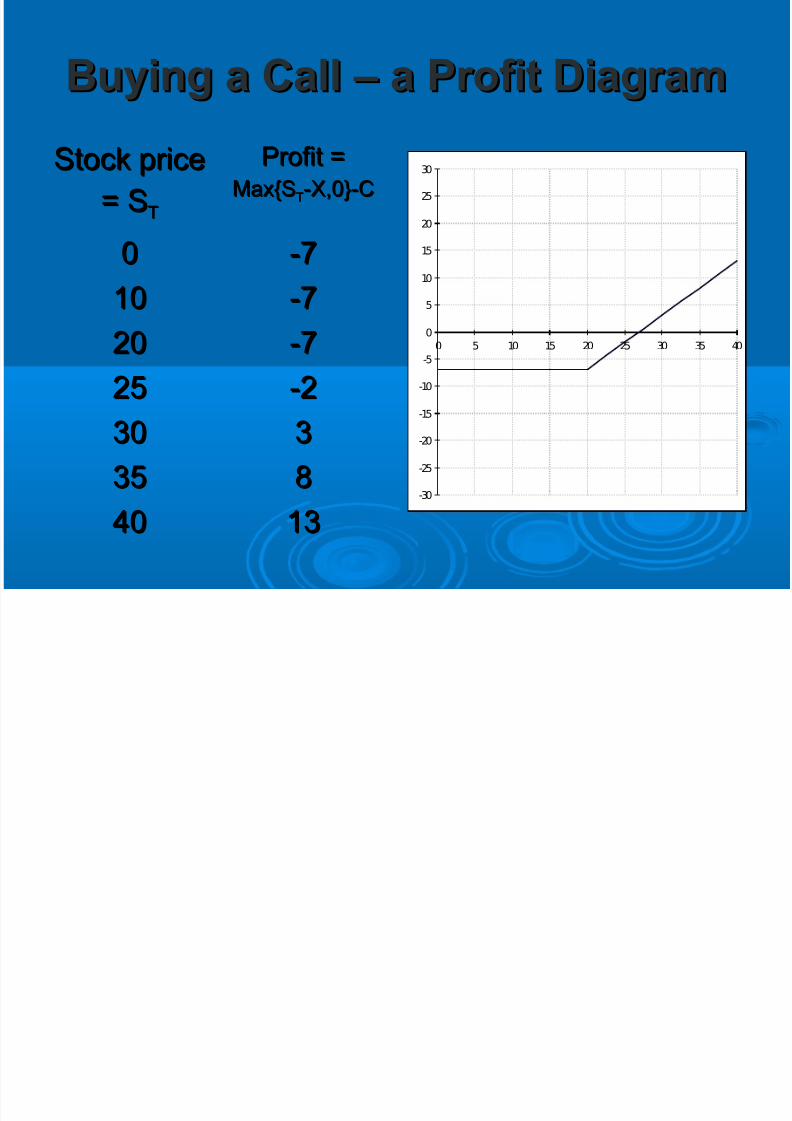

Buying a Call – a Profit DiagramBuying a Call – a Profit Diagram

Stock priceStock price

= S= STT

Profit =Profit =Max{SMax{STT-X,0}-C-X,0}-C

00 -7-7

1010 -7-7

2020 -7-7

2525 -2-2

3030 33

3535 88

4040 1313-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 20/57

Buying a CallBuying a Call

Payoff and Profit DiagramsPayoff and Profit Diagrams

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 21/57

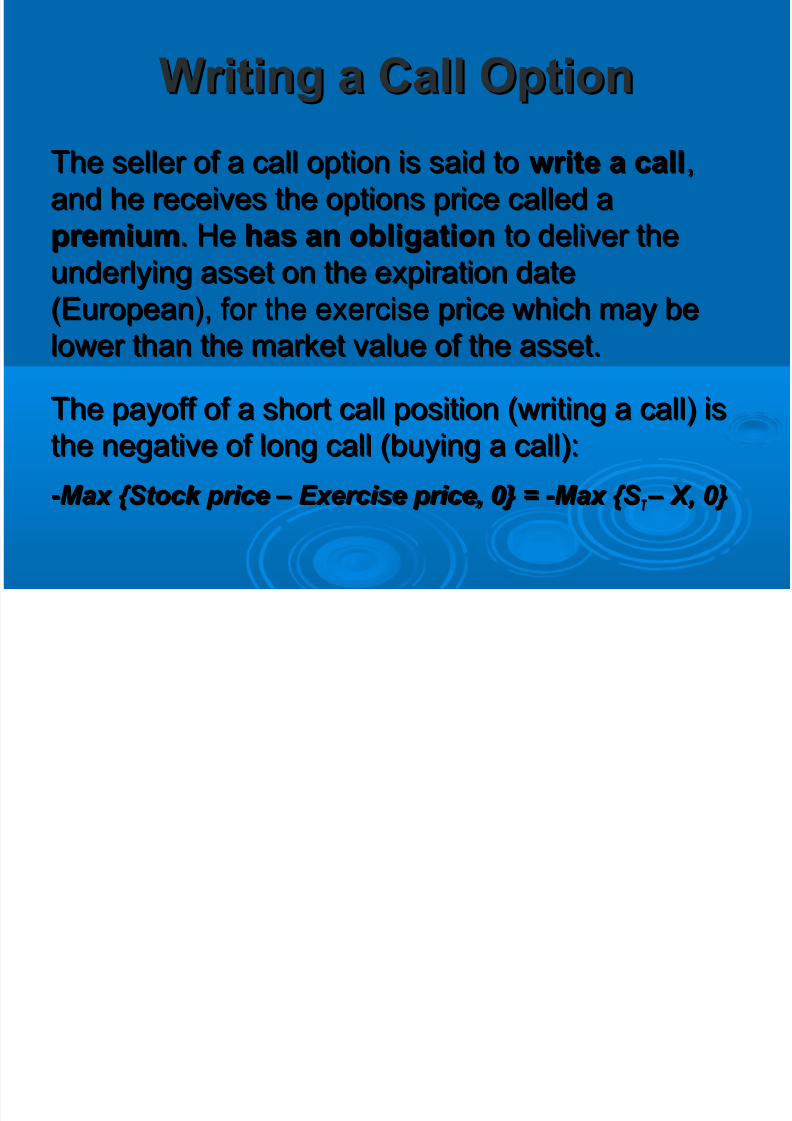

Writing a Call OptionWriting a Call Option

The seller of a call option is said toThe seller of a call option is said to write a callwrite a call,,

and he receives the options price called aand he receives the options price called apremiumpremium. He. He has an obligationhas an obligation to deliver theto deliver the

underlying asset on the expiration dateunderlying asset on the expiration date(European), for the exercise price which may be(European), for the exercise price which may belower than the market value of the asset.lower than the market value of the asset.

The payoff of a short call position (writing a call) isThe payoff of a short call position (writing a call) isthe negative of long call (buying a call):the negative of long call (buying a call):

--Max {Stock price – Exercise price, 0} = -Max {S Max {Stock price – Exercise price, 0} = -Max {S T T – X, 0} – X, 0}

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 22/57

Writing a Call – a Payoff DiagramWriting a Call – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff =Payoff =

--Max{SMax{STT-X,0}-X,0}

00 00

1010 00

1515 00

2020 00

2525 -5-5

3030 -10-10

4040 -20-20

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 23/57

Buying a Call vs. Writing a CallBuying a Call vs. Writing a Call

Payoff DiagramsPayoff Diagrams

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 24/57

MoneynessMoneyness

☺We say that an option isWe say that an option is in-the-money in-the-money when the payoff from exercising is positivewhen the payoff from exercising is positive☺ A call options is in-to-money when (S A call options is in-to-money when (S

tt –X) > 0 –X) > 0

(i.e. when stock price > strike price)(i.e. when stock price > strike price)

☺We say that an option isWe say that an option is out-of-the-money out-of-the-money when the payoff from exercising is zerowhen the payoff from exercising is zero☺ A call options is out-of-the-money when A call options is out-of-the-money when

(S(Stt –X) < 0 –X) < 0

(i.e. when the stock price < the strike price)(i.e. when the stock price < the strike price)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 25/57

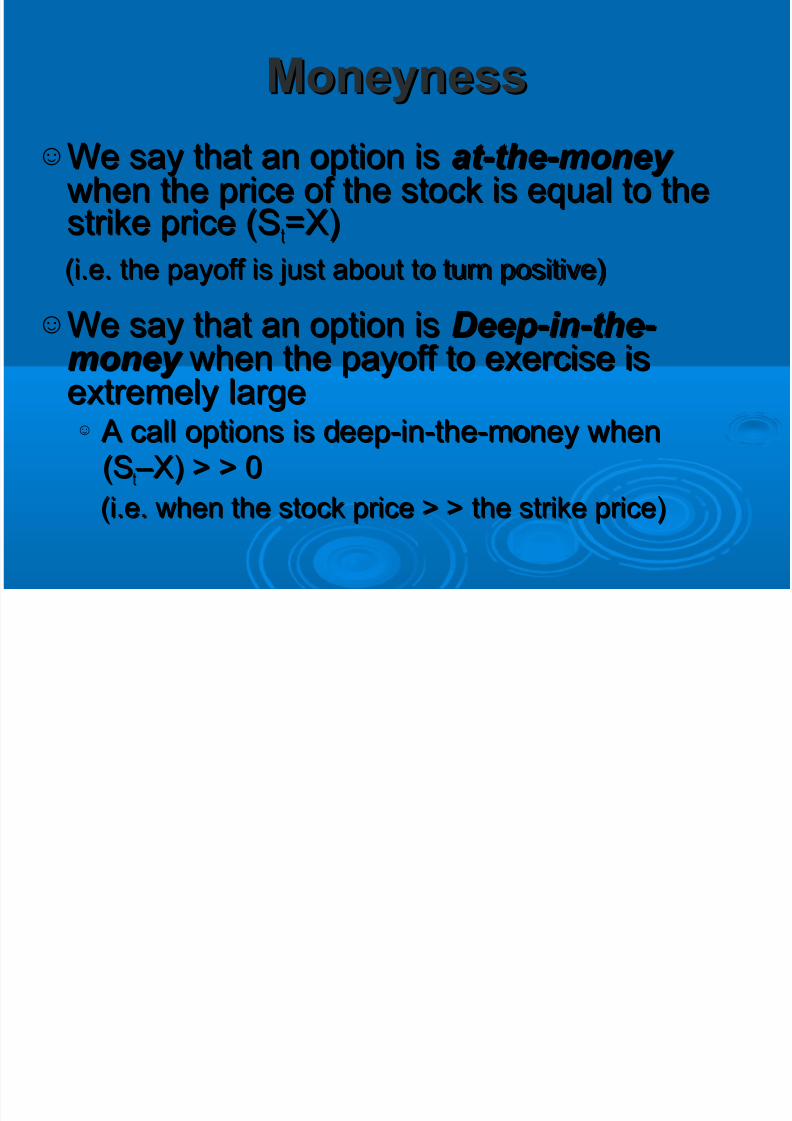

MoneynessMoneyness

☺We say that an option isWe say that an option is at-the-money at-the-money when the price of the stock is equal to thewhen the price of the stock is equal to thestrike price (Sstrike price (S

tt=X)=X)

(i.e. the payoff is just about to turn positive)(i.e. the payoff is just about to turn positive)☺We say that an option isWe say that an option is Deep-in-the- Deep-in-the-

money money when the payoff to exercise iswhen the payoff to exercise isextremely largeextremely large☺ A call options is deep-in-the-money when A call options is deep-in-the-money when

(S(Stt –X) > > 0 –X) > > 0

(i.e. when the stock price > > the strike price)(i.e. when the stock price > > the strike price)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 26/57

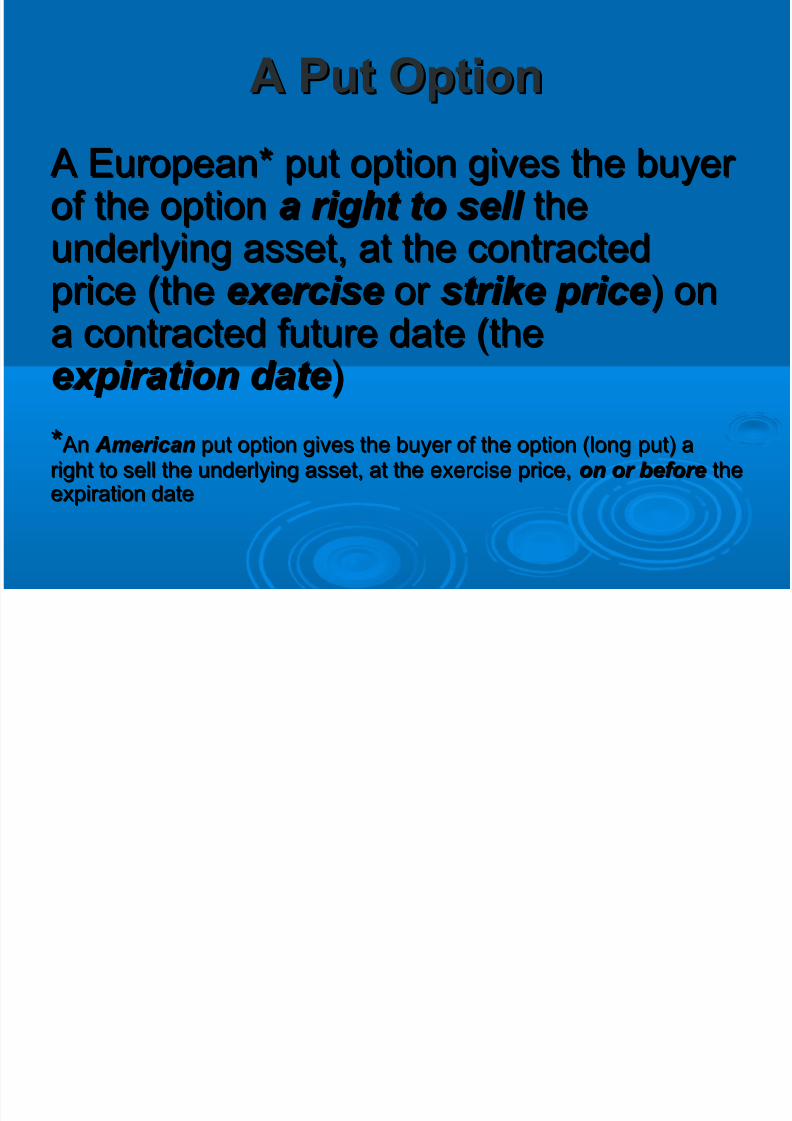

A Put OptionA Put Option

A European* put option gives the buyer A European* put option gives the buyer of the optionof the option a right to sell a right to sell thetheunderlying asset, at the contractedunderlying asset, at the contracted

price (theprice (the exerciseexercise or or strike pricestrike price) on) ona contracted future date (thea contracted future date (theexpiration dateexpiration date))

** An An American American put option gives the buyer of the option (long put) aput option gives the buyer of the option (long put) aright to sell the underlying asset, at the exercise price,right to sell the underlying asset, at the exercise price, on or beforeon or before thetheexpiration dateexpiration date

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 27/57

Put Option - an ExamplePut Option - an Example

A March (European) put option on Microsoft A March (European) put option on Microsoft

stock with a strike price $20, entitles thestock with a strike price $20, entitles the

owner with a right to sell the Microsoft stockowner with a right to sell the Microsoft stock

for $20 on the expiration date.for $20 on the expiration date.

What is the owner’s payoff on the expirationWhat is the owner’s payoff on the expiration

date? Under what circumstances does hedate? Under what circumstances does hebenefit from the position?benefit from the position?

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 28/57

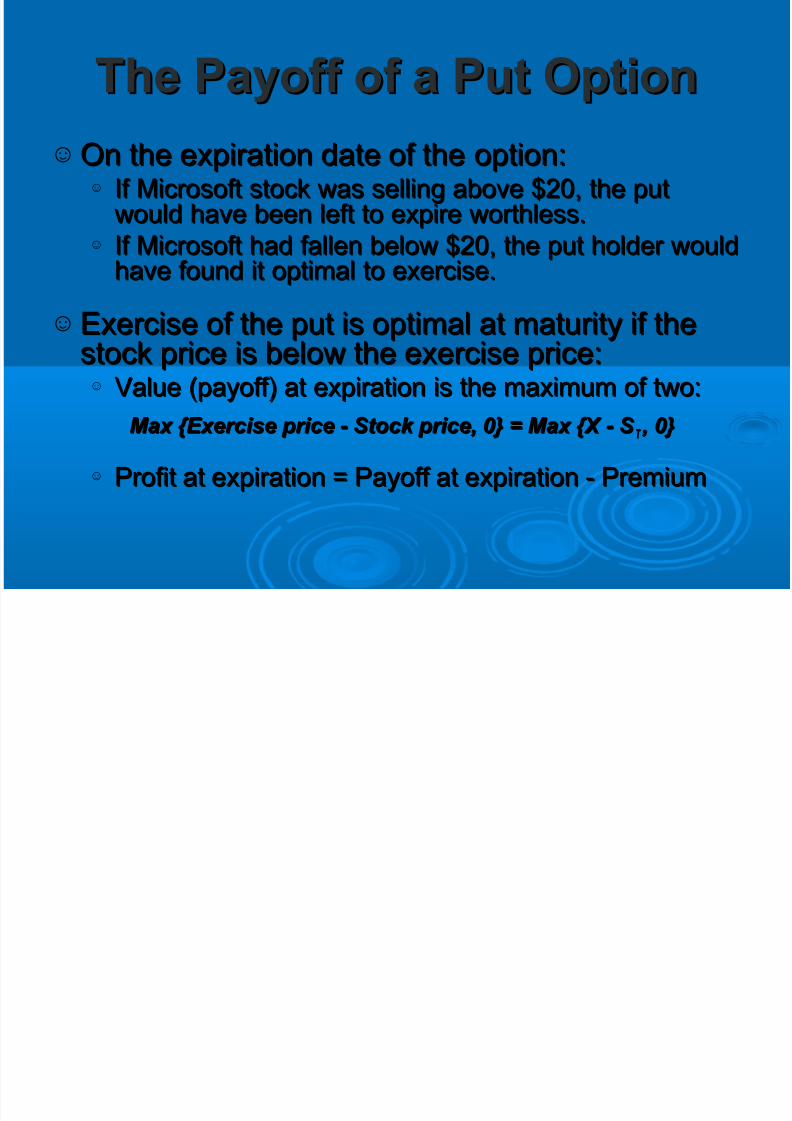

The Payoff of a Put OptionThe Payoff of a Put Option

☺ On the expiration date of the option:On the expiration date of the option:☺ If Microsoft stock was selling above $20, the putIf Microsoft stock was selling above $20, the put

would have been left to expire worthless.would have been left to expire worthless.☺ If Microsoft had fallen below $20, the put holder wouldIf Microsoft had fallen below $20, the put holder would

have found it optimal to exercise.have found it optimal to exercise.☺ Exercise of the put is optimal at maturity if theExercise of the put is optimal at maturity if the

stock price is below the exercise price:stock price is below the exercise price:☺ Value (payoff) at expiration is the maximum of two:Value (payoff) at expiration is the maximum of two:

Max {Exercise price - Stock price, 0} = Max {X - S Max {Exercise price - Stock price, 0} = Max {X - S T T , 0}, 0}

☺ Profit at expiration = Payoff at expiration - PremiumProfit at expiration = Payoff at expiration - Premium

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 29/57

Buying a Put – a Payoff DiagramBuying a Put – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff =Payoff =

Max{X-SMax{X-STT, 0}, 0}

00 2020

55 1515

1010 1010

1515 55

2020 00

2525 00

3030 00

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 30/57

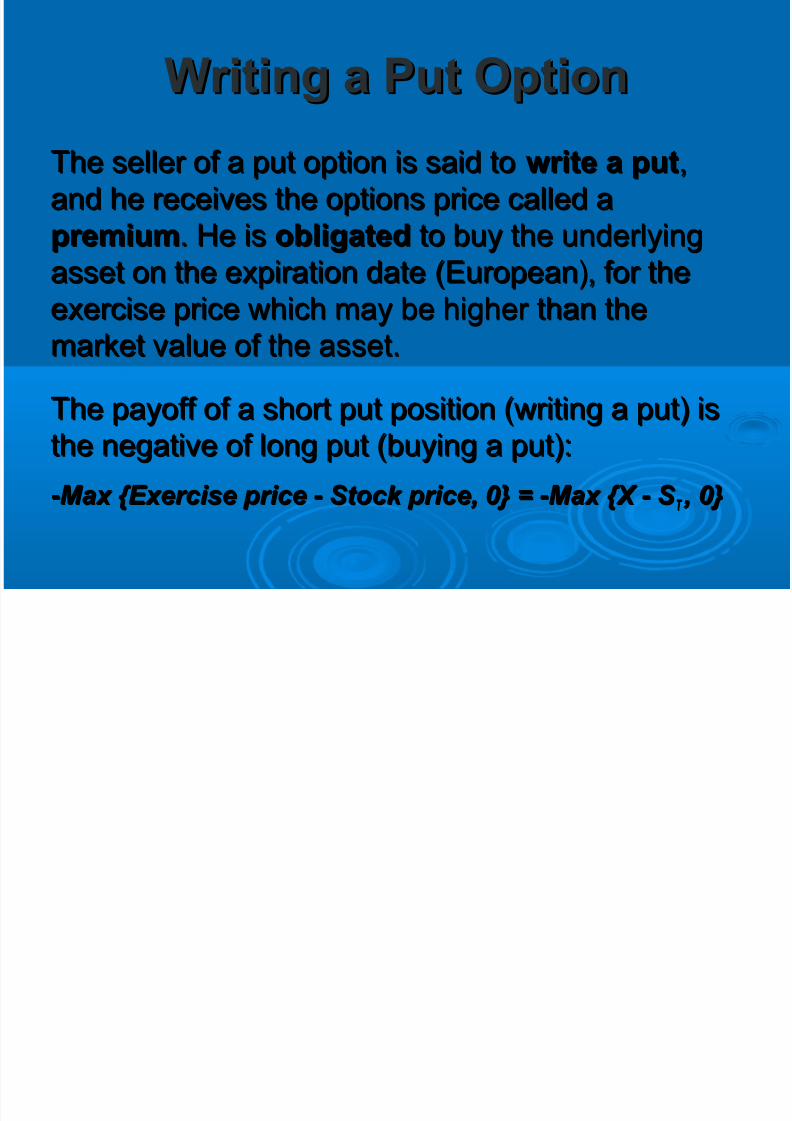

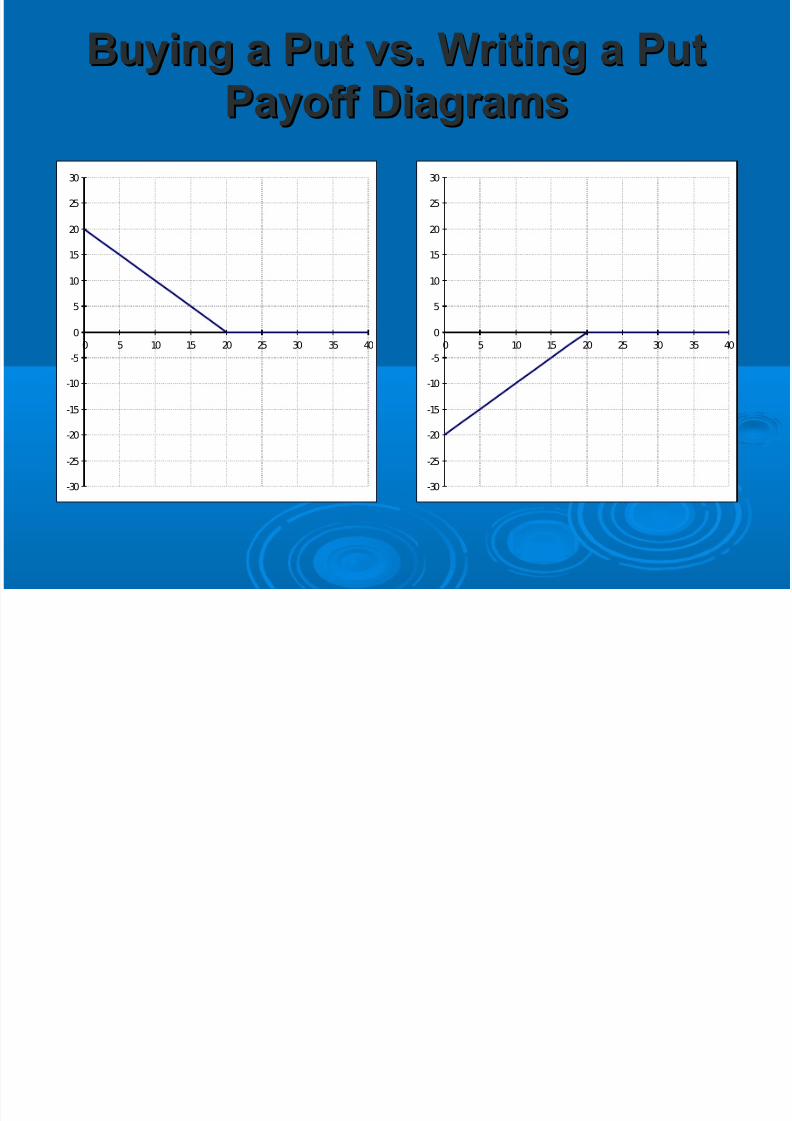

Writing a Put OptionWriting a Put Option

The seller of a put option is said toThe seller of a put option is said to write a putwrite a put,,

and he receives the options price called aand he receives the options price called apremiumpremium. He is. He is obligatedobligated to buy the underlyingto buy the underlying

asset on the expiration date (European), for theasset on the expiration date (European), for theexercise price which may be higher than theexercise price which may be higher than themarket value of the asset.market value of the asset.

The payoff of a short put position (writing a put) isThe payoff of a short put position (writing a put) isthe negative of long put (buying a put):the negative of long put (buying a put):

--Max {Exercise price - Stock price, 0} = -Max {X - S Max {Exercise price - Stock price, 0} = -Max {X - S T T , 0}, 0}

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 31/57

Writing a Put – a Payoff DiagramWriting a Put – a Payoff Diagram

Stock priceStock price

= S= STT

Payoff =Payoff =

-Max{X-S-Max{X-STT,0},0}

00 -20-20

55 -15-15

1010 -10-10

1515 -5-5

2020 00

2525 00

3030 00

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 32/57

Buying a Put vs. Writing a PutBuying a Put vs. Writing a Put

Payoff DiagramsPayoff Diagrams

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 33/57

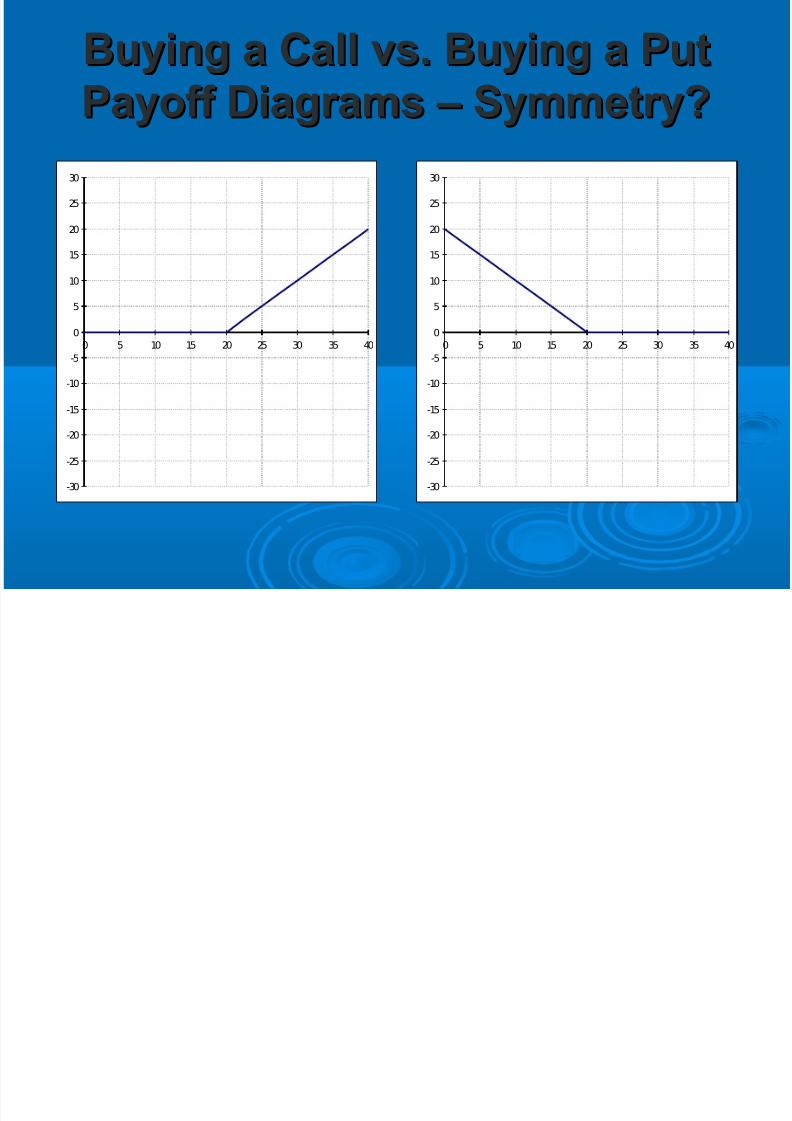

Buying a Call vs. Buying a PutBuying a Call vs. Buying a Put

Payoff Diagrams – Symmetry?Payoff Diagrams – Symmetry?

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 34/57

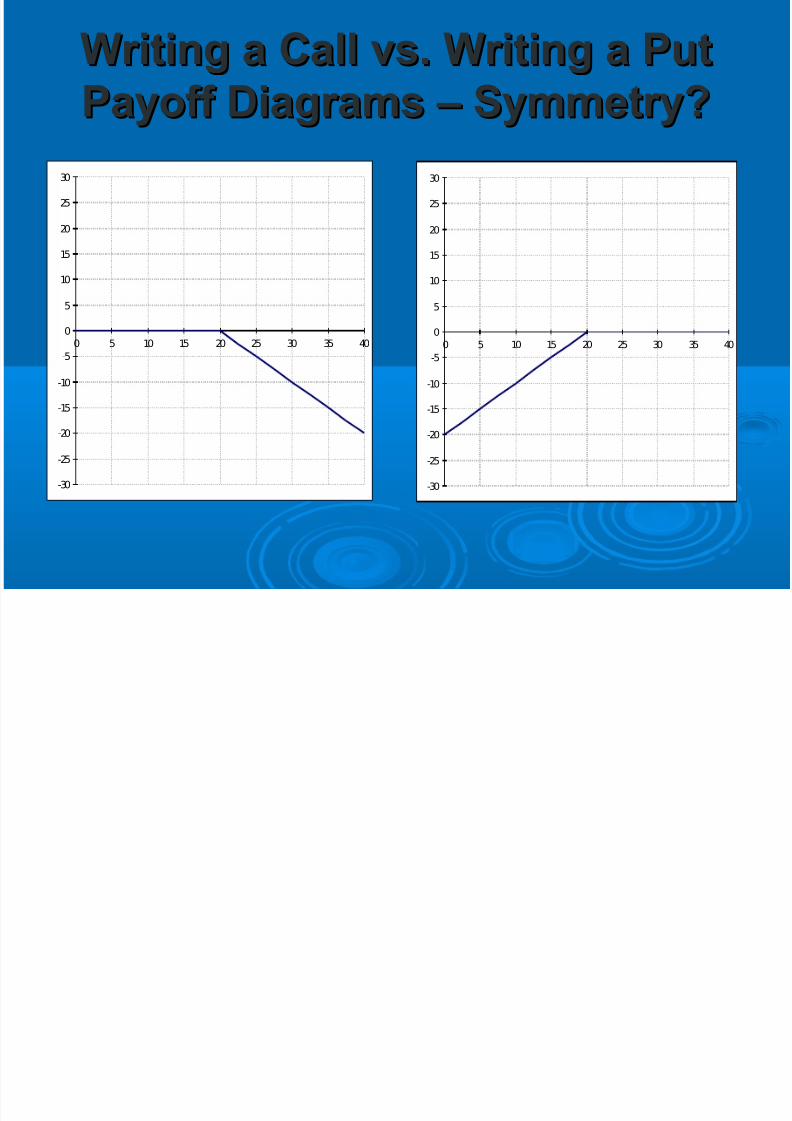

Writing a Call vs. Writing a PutWriting a Call vs. Writing a Put

Payoff Diagrams – Symmetry?Payoff Diagrams – Symmetry?

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 35/57

Investment StrategiesInvestment Strategies

A Portfolio of Investment VehiclesA Portfolio of Investment Vehicles

☺ We can use more than one investmentWe can use more than one investment

vehicle to from a portfolio with the desiredvehicle to from a portfolio with the desired

payoff.payoff.

☺ We may use any of the instrument (stock,We may use any of the instrument (stock,

bond, put or call) at any quantity or positionbond, put or call) at any quantity or position

(long or short) as our investment strategy.(long or short) as our investment strategy.

☺ The payoff of the portfolio will be the sum of The payoff of the portfolio will be the sum of

the payoffs of the it’s instrumentsthe payoffs of the it’s instruments

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 36/57

Investment StrategiesInvestment Strategies

Protective PutProtective Put

☺ Long one stock. The payoff at time T is: SLong one stock. The payoff at time T is: STT

☺ Buy one (European) put option on the sameBuy one (European) put option on the same

stock, with a strike price of X = $20 andstock, with a strike price of X = $20 andexpiration at T. The payoff at time T is:expiration at T. The payoff at time T is:

Max { X-SMax { X-STT , 0 } = Max { $20-S, 0 } = Max { $20-S

TT , 0 }, 0 }

☺ The payoff of the portfolio at time T will beThe payoff of the portfolio at time T will bethe sum of the payoffs of the two instrumentsthe sum of the payoffs of the two instruments

☺ Intuition: possible loses of the long stockIntuition: possible loses of the long stock

position are bounded by the long put positionposition are bounded by the long put position

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 37/57

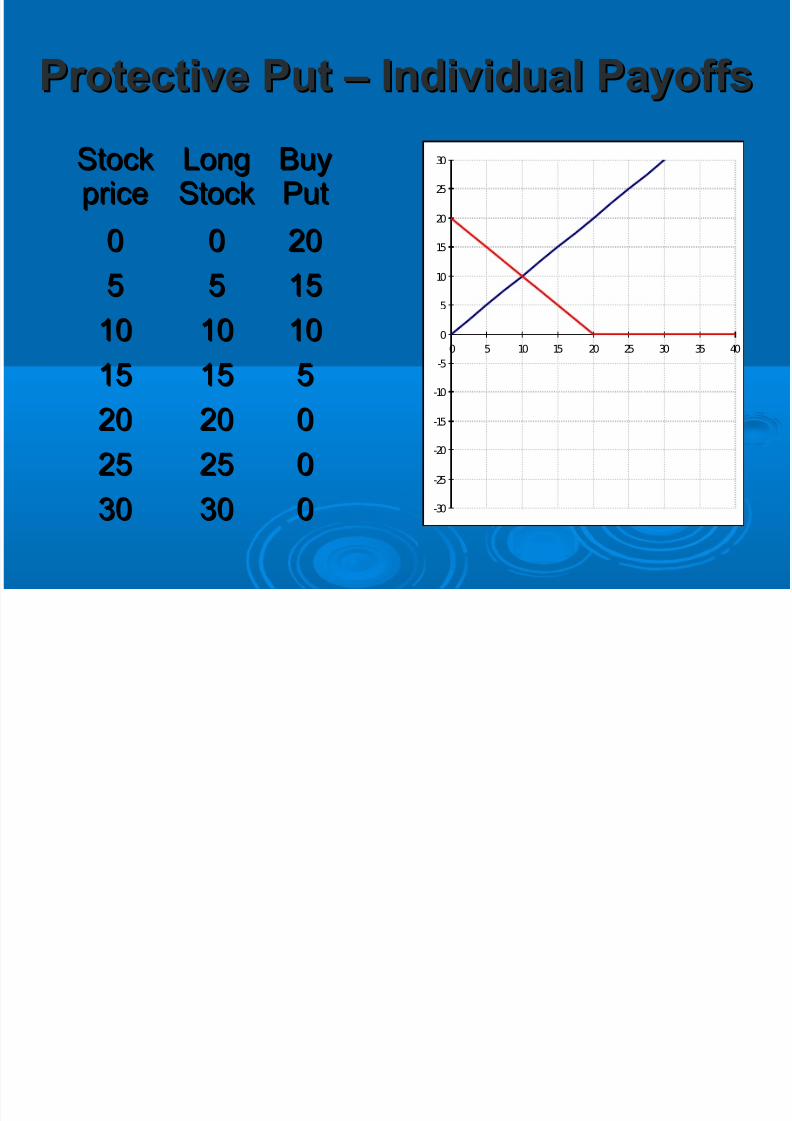

Protective Put – Individual PayoffsProtective Put – Individual Payoffs

StockStockpriceprice

LongLongStockStock

BuyBuyPutPut

00 00 2020

55 55 15151010 1010 1010

1515 1515 55

2020 2020 002525 2525 00

3030 3030 00 -30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 38/57

Protective Put – Portfolio Payoff Protective Put – Portfolio Payoff

StockStockpriceprice

LongLongStockStock

BuyBuyPutPut

All All(Portfolio)(Portfolio)

00 00 2020 2020

55 55 1515 20201010 1010 1010 2020

1515 1515 55 2020

2020 2020 00 20202525 2525 00 2525

3030 3030 00 3030 -30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 39/57

Investment StrategiesInvestment Strategies

Covered CallCovered Call

☺ Long one stock. The payoff at time T is: SLong one stock. The payoff at time T is: STT

☺ Write one (European) call option on the sameWrite one (European) call option on the same

stock, with a strike price of X = $20 andstock, with a strike price of X = $20 andexpiration at T. The payoff at time T is:expiration at T. The payoff at time T is:

-Max { S-Max { STT - X- X

, 0 } = -Max { S, 0 } = -Max { STT - $20- $20

, 0 }, 0 }

☺ The payoff of the portfolio at time T will beThe payoff of the portfolio at time T will bethe sum of the payoffs of the two instrumentsthe sum of the payoffs of the two instruments

☺ Intuition: the call is “covered” since, in case of Intuition: the call is “covered” since, in case of

delivery, the investor already owns the stock.delivery, the investor already owns the stock.

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 40/57

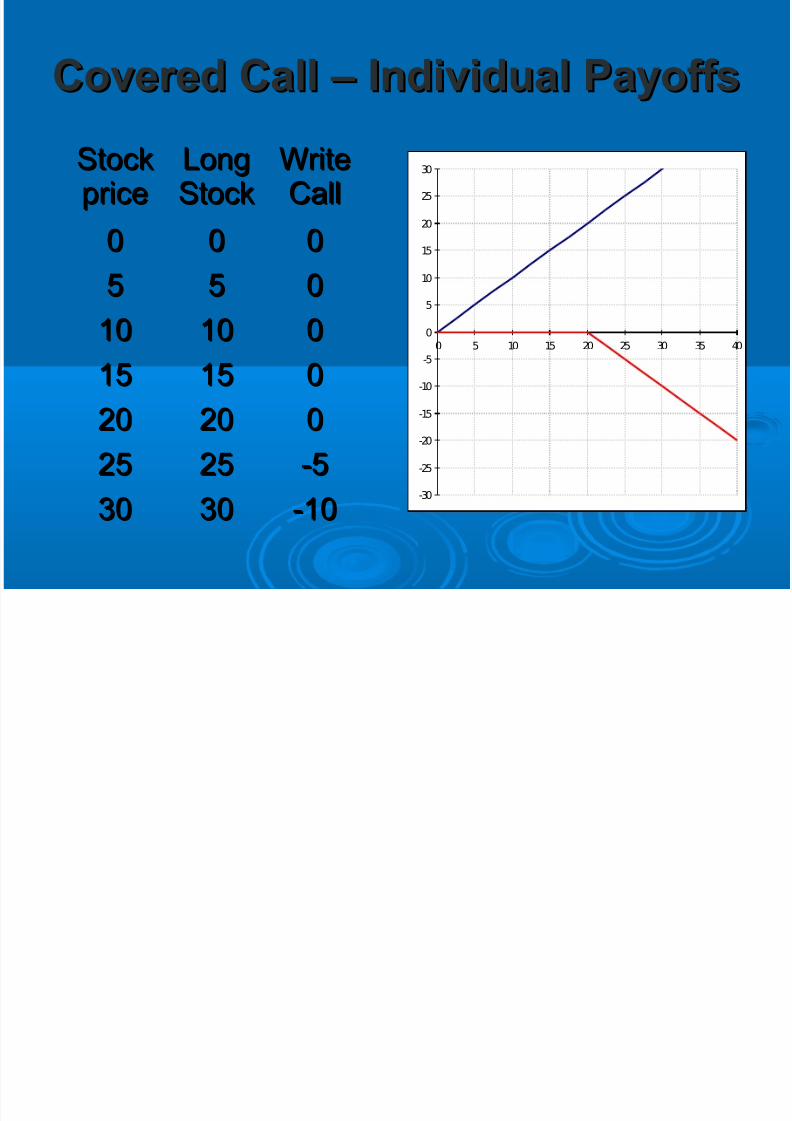

Covered Call – Individual PayoffsCovered Call – Individual Payoffs

StockStockpriceprice

LongLongStockStock

WriteWriteCallCall

00 00 00

55 55 001010 1010 00

1515 1515 00

2020 2020 002525 2525 -5-5

3030 3030 -10-10-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 41/57

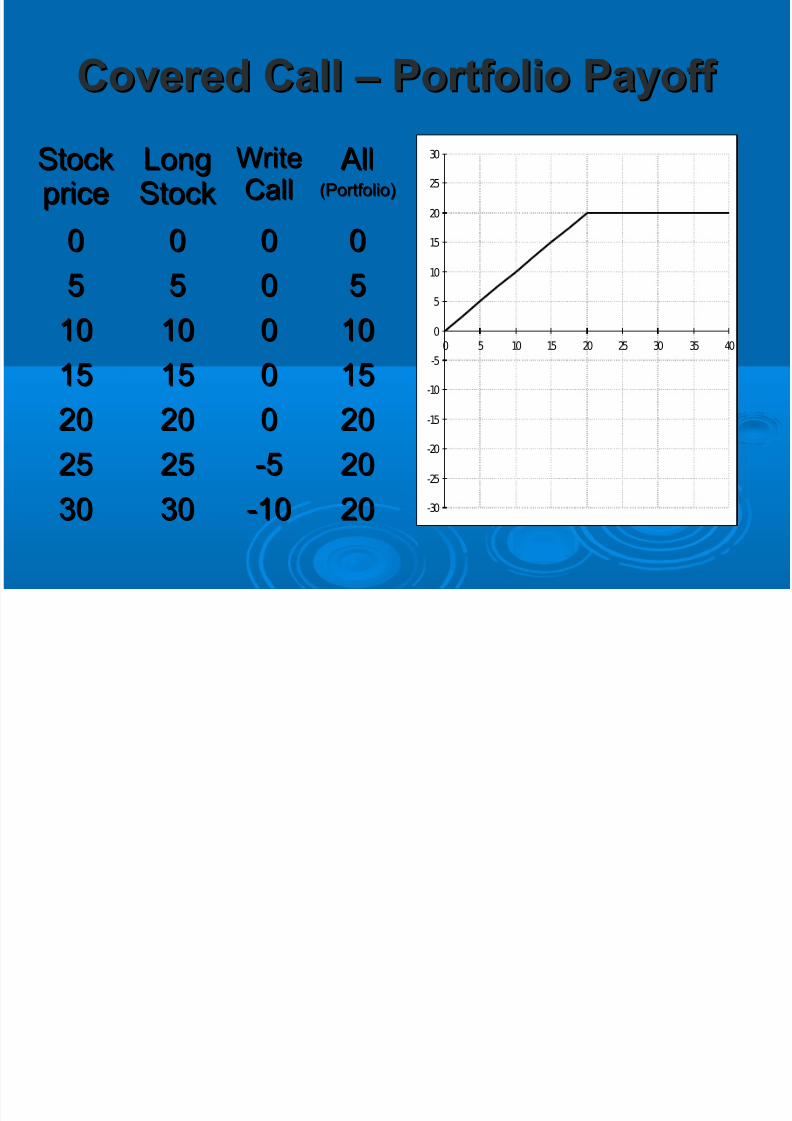

Covered Call – Portfolio Payoff Covered Call – Portfolio Payoff

StockStockpriceprice

LongLongStockStock

WriteWriteCallCall

All All(Portfolio)(Portfolio)

00 00 00 00

55 55 00 551010 1010 00 1010

1515 1515 00 1515

2020 2020 00 20202525 2525 -5-5 2020

3030 3030 -10-10 2020 -30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 42/57

Other Investment StrategiesOther Investment Strategies

☺ Long straddleLong straddle☺ Buy a call option (strike= X, expiration= T)Buy a call option (strike= X, expiration= T)☺ Buy a put option (strike= X, expiration= T)Buy a put option (strike= X, expiration= T)

☺ Write a straddle (short straddle)Write a straddle (short straddle)☺ Write a call option (strike= X, expiration= T)Write a call option (strike= X, expiration= T)☺ Write a put option (strike= X, expiration= T)Write a put option (strike= X, expiration= T)

☺ Bullish spreadBullish spread☺ Buy a call option (strike= XBuy a call option (strike= X

11, expiration= T), expiration= T)

☺ Write a Call option (strike= XWrite a Call option (strike= X22>X>X

11, expiration= T), expiration= T)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 43/57

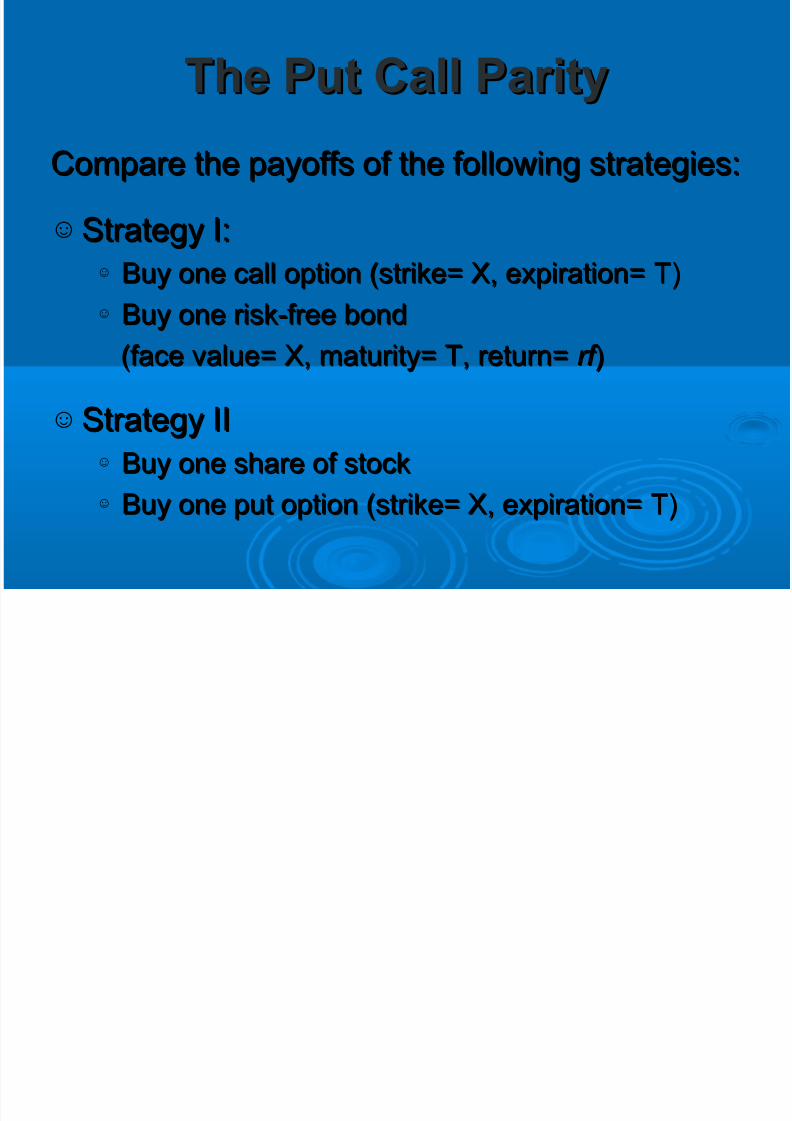

The Put Call ParityThe Put Call Parity

Compare the payoffs of the following strategies:Compare the payoffs of the following strategies:

☺ Strategy I:Strategy I:☺

Buy one call option (strike= X, expiration= T)Buy one call option (strike= X, expiration= T)☺ Buy one risk-free bondBuy one risk-free bond

(face value= X, maturity= T, return=(face value= X, maturity= T, return= rf rf ))

☺ Strategy IIStrategy II☺ Buy one share of stockBuy one share of stock☺ Buy one put option (strike= X, expiration= T)Buy one put option (strike= X, expiration= T)

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 44/57

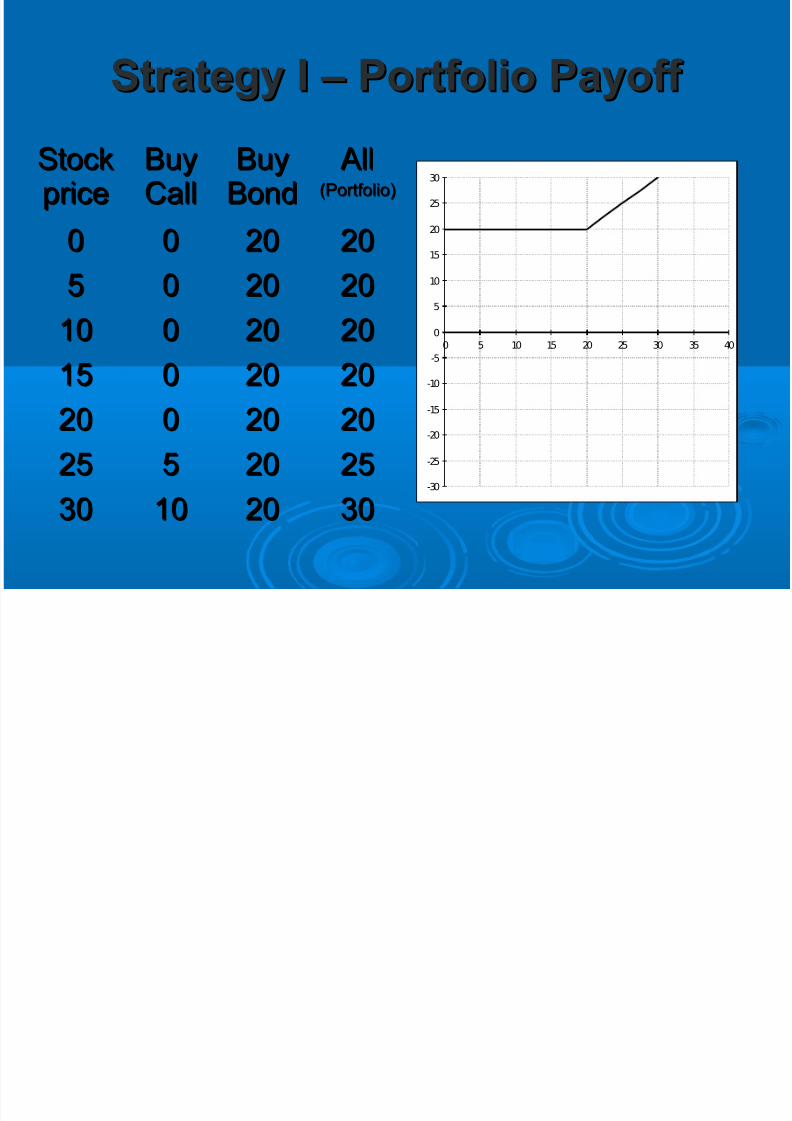

Strategy I – Portfolio Payoff Strategy I – Portfolio Payoff

StockStockpriceprice

BuyBuyCallCall

BuyBuyBondBond

All All(Portfolio)(Portfolio)

00 00 2020 2020

55 00 2020 20201010 00 2020 2020

1515 00 2020 2020

2020 00 2020 20202525 55 2020 2525

3030 1010 2020 3030-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 45/57

Strategy II – Portfolio Payoff Strategy II – Portfolio Payoff

StockStockpriceprice

BuyBuyStockStock

BuyBuyPutPut

All All(Portfolio)(Portfolio)

00 00 2020 2020

55 55 1515 20201010 1010 1010 2020

1515 1515 55 2020

2020 2020 00 20202525 2525 00 2525

3030 3030 00 3030-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35 40

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 46/57

The Put Call ParityThe Put Call Parity

If two portfolios have the same payoffs inIf two portfolios have the same payoffs inevery possible state and time in the future,every possible state and time in the future,

their prices must be equal:their prices must be equal:

(1 )T

X

C S P rf + = +

+

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 47/57

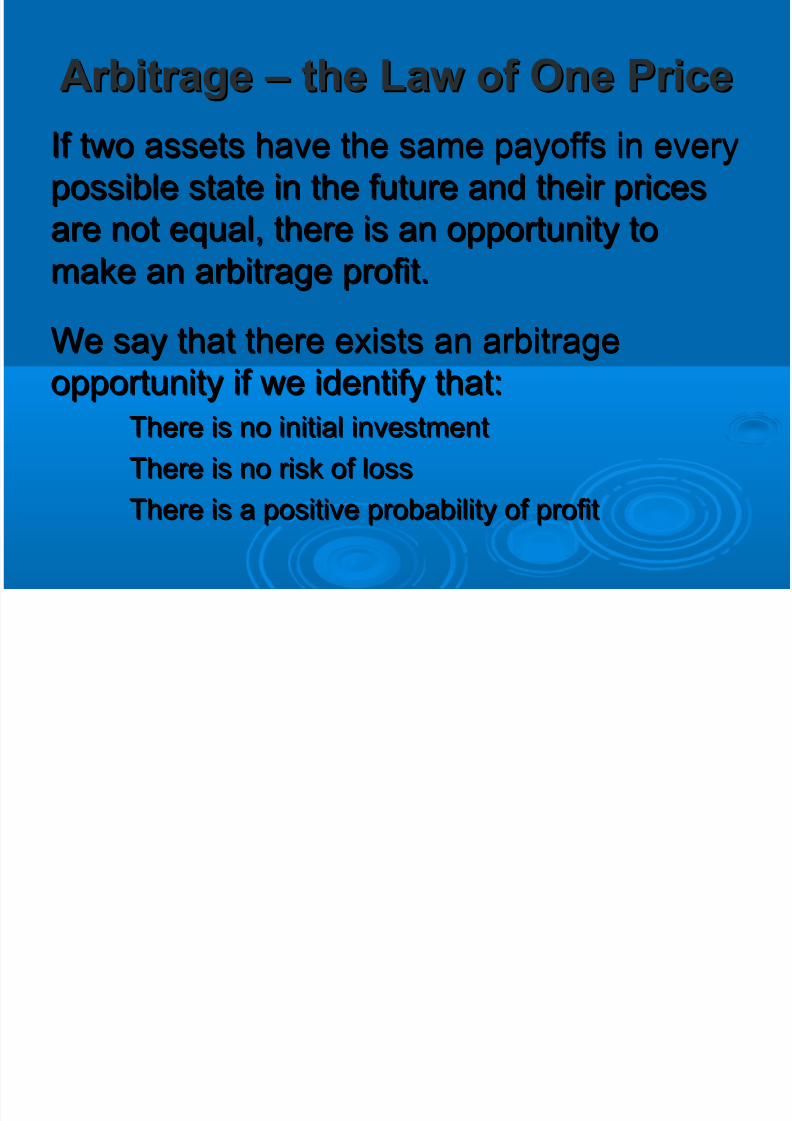

Arbitrage – the Law of One PriceArbitrage – the Law of One Price

If two assets have the same payoffs in everyIf two assets have the same payoffs in everypossible state in the future and their pricespossible state in the future and their prices

are not equal, there is an opportunity toare not equal, there is an opportunity to

make an arbitrage profit.make an arbitrage profit.We say that there exists an arbitrageWe say that there exists an arbitrage

opportunity if we identify that:opportunity if we identify that:

There is no initial investmentThere is no initial investmentThere is no risk of lossThere is no risk of loss

There is a positive probability of profitThere is a positive probability of profit

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 48/57

Arbitrage – a Technical DefinitionArbitrage – a Technical Definition

Let CFLet CFtjtj be the cash flow of an investmentbe the cash flow of an investmentstrategy at time t and state j. If the followingstrategy at time t and state j. If the following

conditions are met this strategy generatesconditions are met this strategy generates

an arbitrage profit.an arbitrage profit.(i)(i) all the possible cash flows in everyall the possible cash flows in every

possible state and time are positive or zero -possible state and time are positive or zero -

CFCFtjtj ≥ 0 for every t and j.≥ 0 for every t and j.

(ii)(ii) at least one cash flow is strictly positive -at least one cash flow is strictly positive -

there exists a pair ( t , j ) for which CFthere exists a pair ( t , j ) for which CFtjtj > 0.> 0.

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 49/57

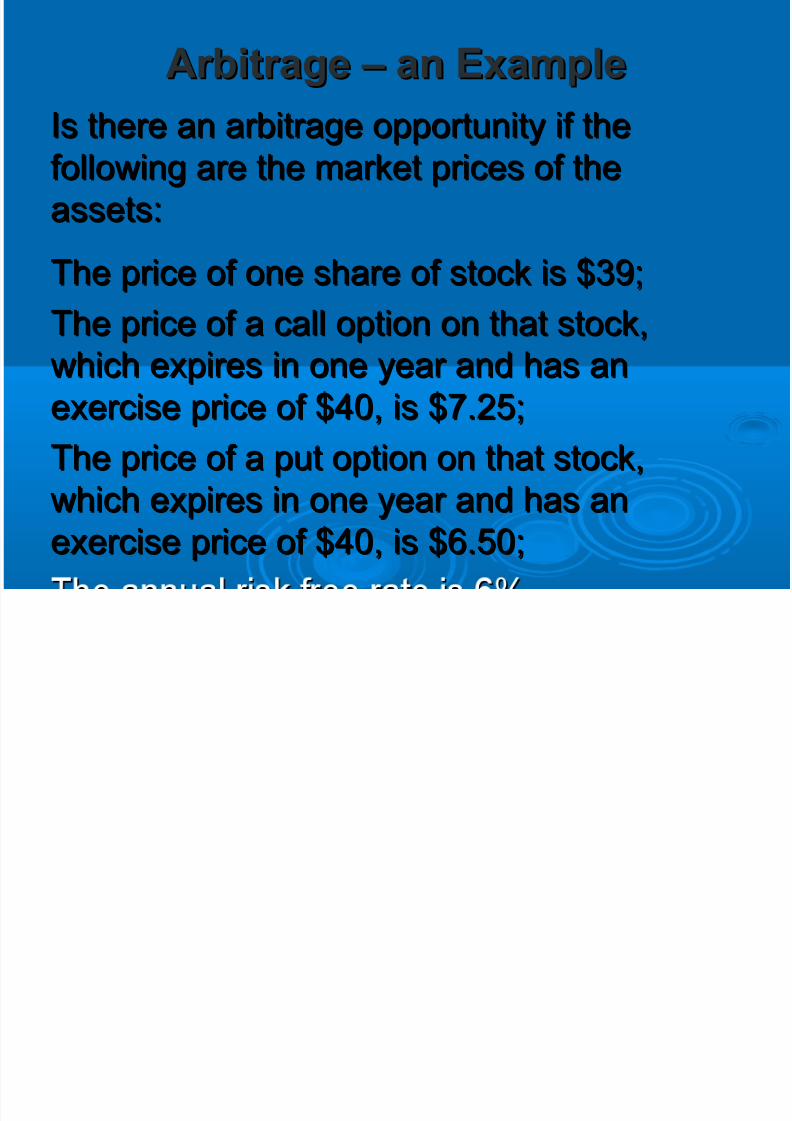

Arbitrage – an ExampleArbitrage – an Example

Is there an arbitrage opportunity if theIs there an arbitrage opportunity if the

following are the market prices of thefollowing are the market prices of the

assets:assets:

The price of one share of stock is $39;The price of one share of stock is $39;The price of a call option on that stock,The price of a call option on that stock,which expires in one year and has anwhich expires in one year and has an

exercise price of $40, is $7.25;exercise price of $40, is $7.25;The price of a put option on that stock,The price of a put option on that stock,

which expires in one year and has anwhich expires in one year and has an

exercise price of $40, is $6.50;exercise price of $40, is $6.50;

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 50/57

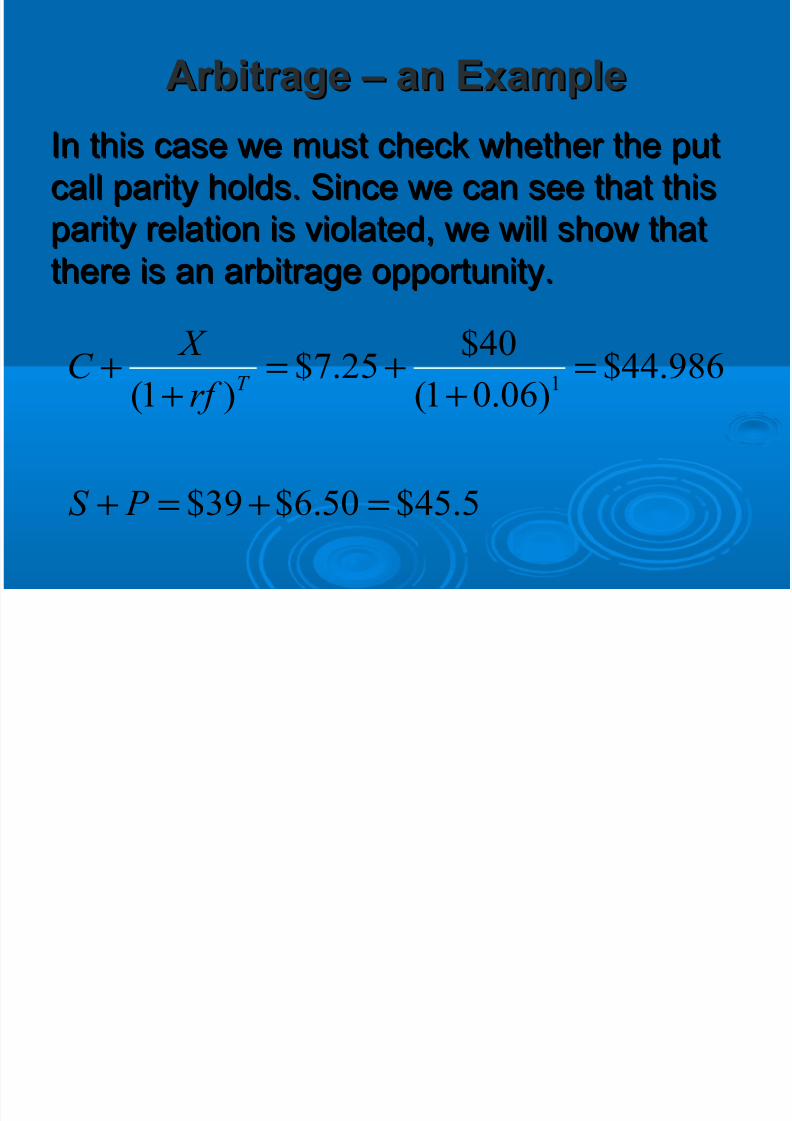

Arbitrage – an ExampleArbitrage – an Example

In this case we must check whether the putIn this case we must check whether the putcall parity holds. Since we can see that thiscall parity holds. Since we can see that this

parity relation is violated, we will show thatparity relation is violated, we will show that

there is an arbitrage opportunity.there is an arbitrage opportunity.

1

$40$7.25 $44.986

(1 ) (1 0.06)

$39 $6.50 $45.5

T

X C

rf

S P

+ = + =

+ +

+ = + =

Th C t ti f

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 51/57

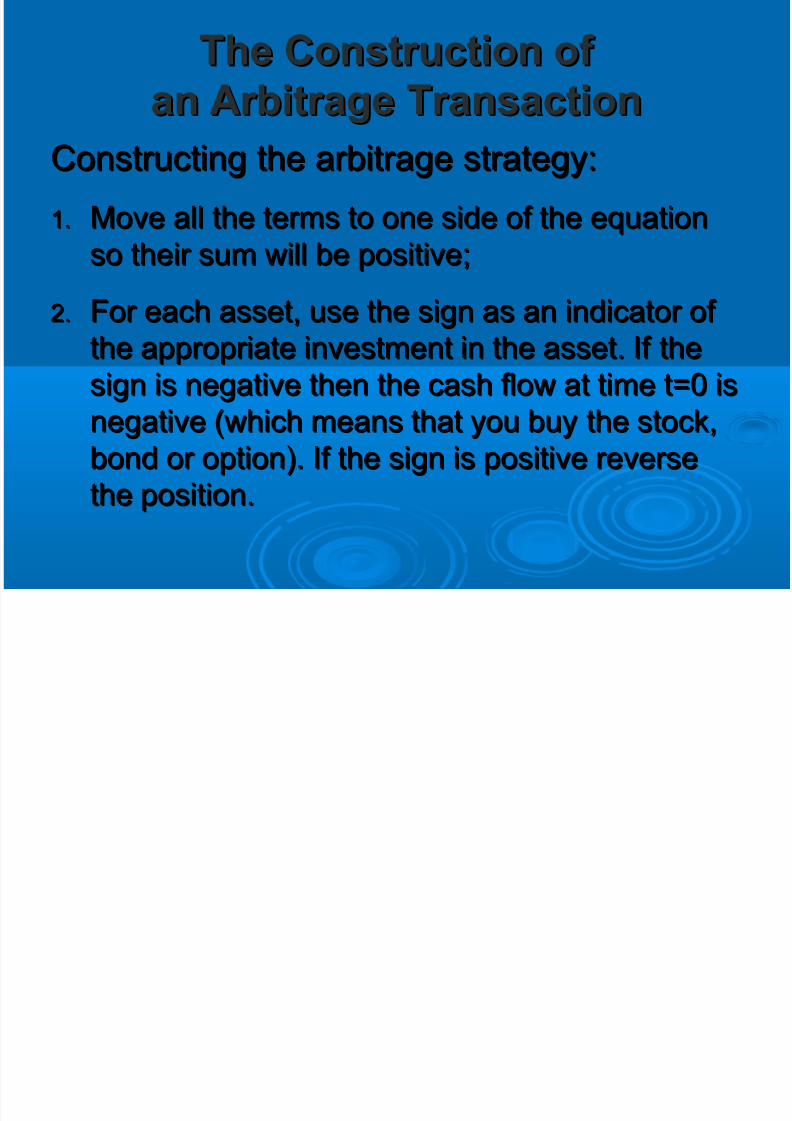

The Construction of The Construction of

an Arbitrage Transactionan Arbitrage Transaction

Constructing the arbitrage strategy:Constructing the arbitrage strategy:

1.1. Move all the terms to one side of the equationMove all the terms to one side of the equation

so their sum will be positive;so their sum will be positive;

2.2. For each asset, use the sign as an indicator of For each asset, use the sign as an indicator of the appropriate investment in the asset. If thethe appropriate investment in the asset. If the

sign is negative then the cash flow at time t=0 issign is negative then the cash flow at time t=0 is

negative (which means that you buy the stock,negative (which means that you buy the stock,bond or option). If the sign is positive reversebond or option). If the sign is positive reversethe position.the position.

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 52/57

Arbitrage – an ExampleArbitrage – an Example

In this case we move all terms to the LHS:In this case we move all terms to the LHS:

( ) $45.5 $44.986 $0.514 0(1 )

. .

0(1 )

T

T

X S P C

rf

i e

X S P C rf

+ − + = − = >

÷+

+ − − >+

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 53/57

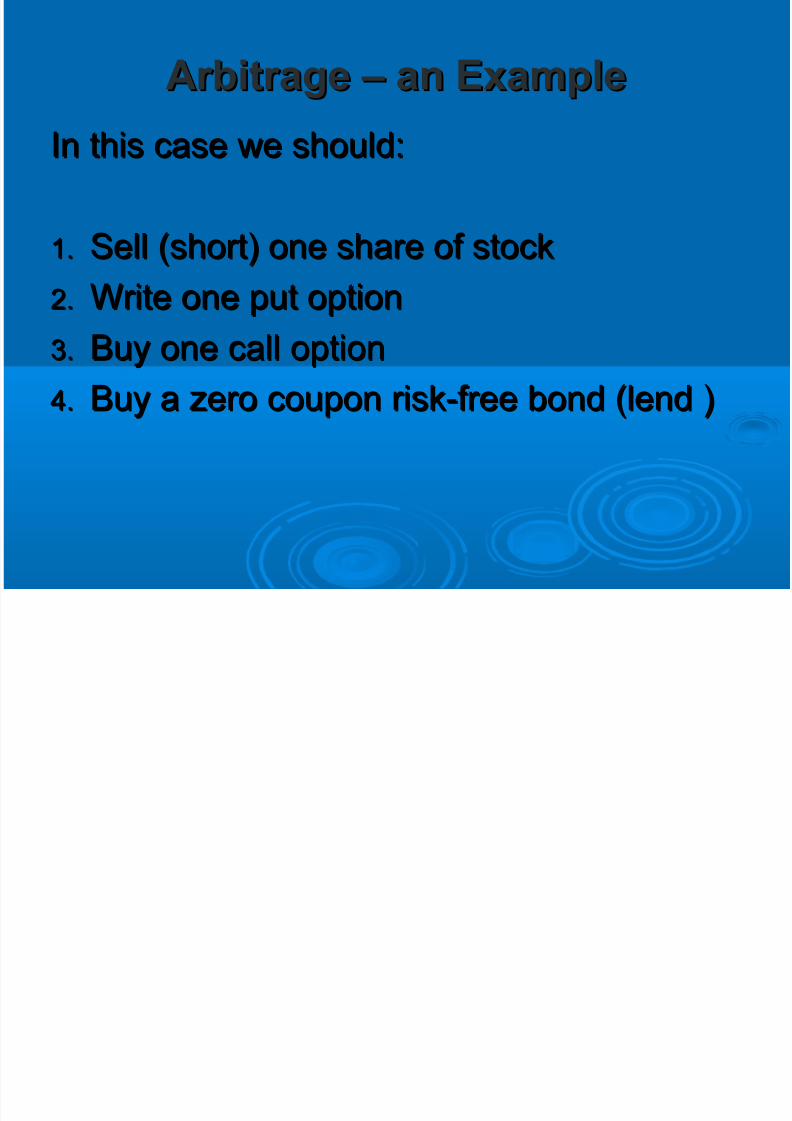

Arbitrage – an ExampleArbitrage – an Example

In this case we should:In this case we should:

1.1. Sell (short) one share of stockSell (short) one share of stock

2.2. Write one put optionWrite one put option

3.3. Buy one call optionBuy one call option

4.4. Buy a zero coupon risk-free bond (lend )Buy a zero coupon risk-free bond (lend )

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 54/57

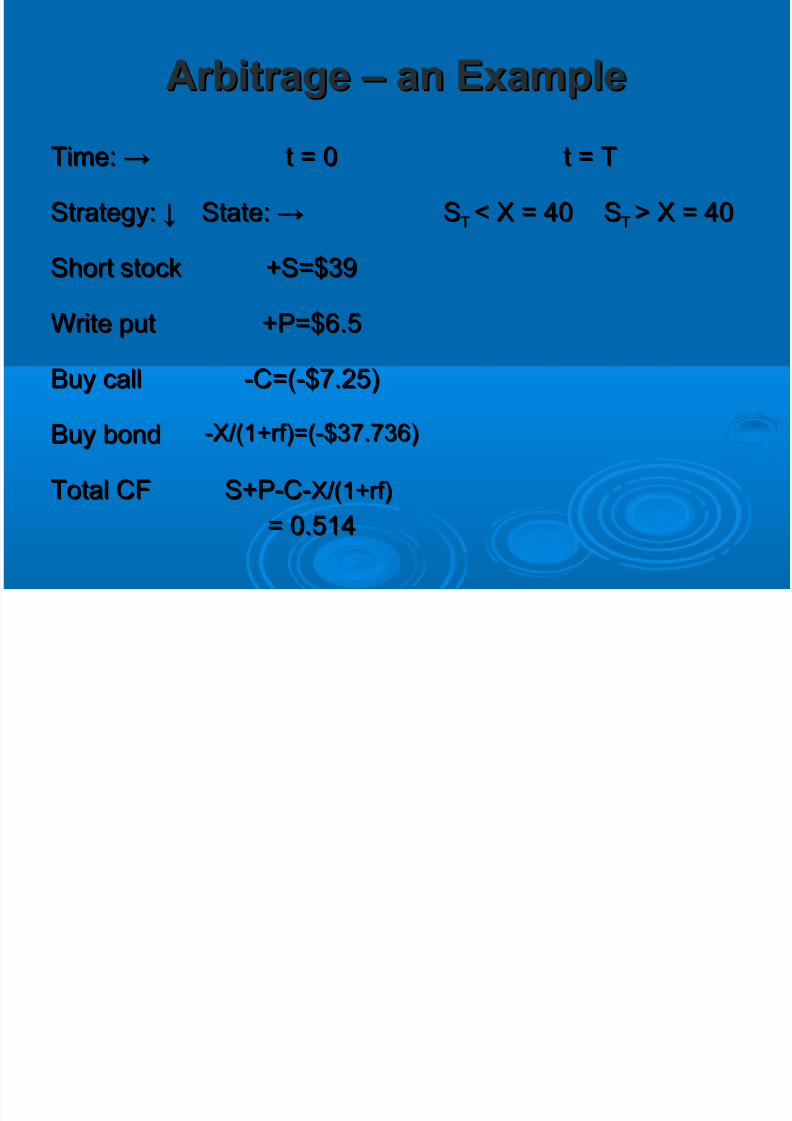

Arbitrage – an ExampleArbitrage – an Example

Time: →Time: → t = 0t = 0 t = Tt = T

Strategy: ↓Strategy: ↓ State: →State: → SSTT < X = 40< X = 40 SSTT > X = 40> X = 40

Short stockShort stock

Write putWrite put

Buy callBuy call

Buy bondBuy bond

Total CFTotal CF CFCF00 CFCFT1T1 CFCFT2T2

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 55/57

Arbitrage – an ExampleArbitrage – an Example

Time: →Time: → t = 0t = 0 t = Tt = T

Strategy: ↓Strategy: ↓ State: →State: → SSTT < X = 40< X = 40 SSTT > X = 40> X = 40

Short stockShort stock +S=$39+S=$39

Write putWrite put +P=$6.5+P=$6.5

Buy callBuy call -C=(-$7.25)-C=(-$7.25)

Buy bondBuy bond -X/(1+rf)=(-$37.736)-X/(1+rf)=(-$37.736)

Total CFTotal CF S+P-C-S+P-C-X/(1+rf)X/(1+rf)

= 0.514= 0.514

7/30/2019 Fi8000 Basics of Options

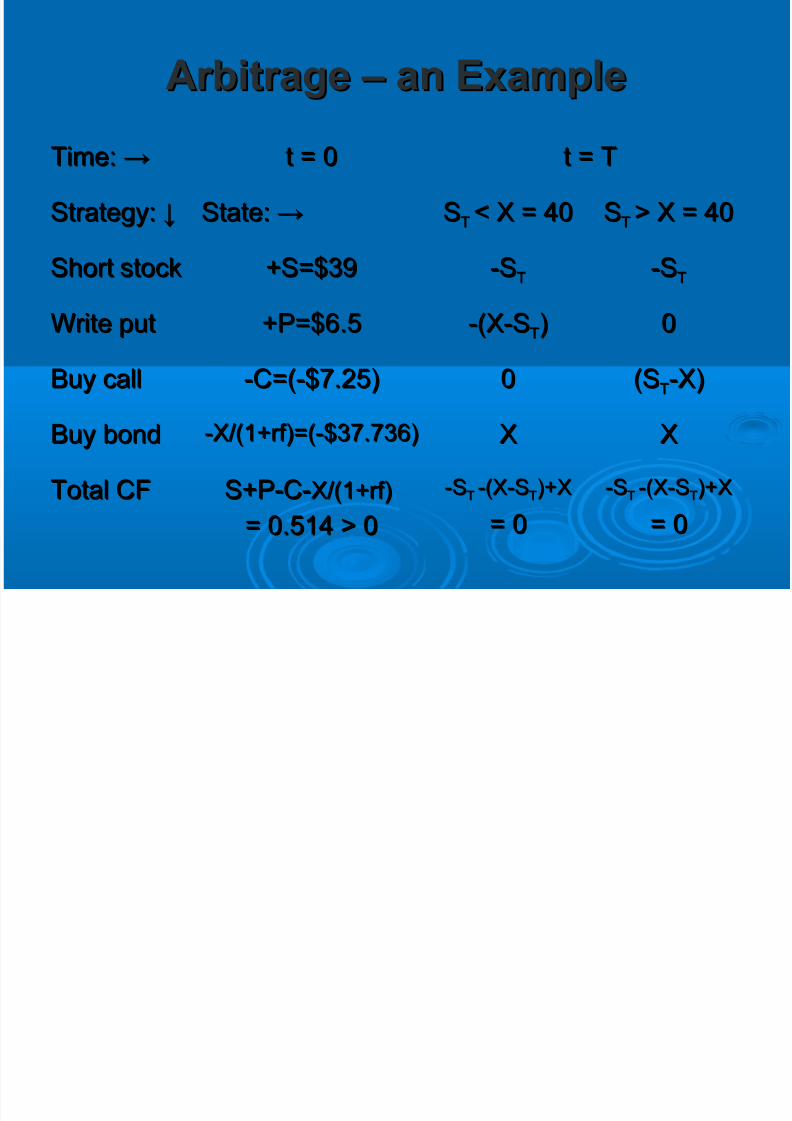

http://slidepdf.com/reader/full/fi8000-basics-of-options 56/57

Arbitrage – an ExampleArbitrage – an Example

Time: →Time: → t = 0t = 0 t = Tt = T

Strategy: ↓Strategy: ↓ State: →State: → SSTT < X = 40< X = 40 SSTT > X = 40> X = 40

Short stockShort stock +S=$39+S=$39 -S-STT

-S-STT

Write putWrite put +P=$6.5+P=$6.5 -(X-S-(X-STT)) 00

Buy callBuy call -C=(-$7.25)-C=(-$7.25) 00 (S(STT-X)-X)

Buy bondBuy bond -X/(1+rf)=(-$37.736)-X/(1+rf)=(-$37.736) XX XX

Total CFTotal CF S+P-C-S+P-C-X/(1+rf)X/(1+rf)

= 0.514 > 0= 0.514 > 0

-S-STT -(X-S-(X-STT)+X)+X

= 0= 0

-S-STT -(X-S-(X-STT)+X)+X

= 0= 0

7/30/2019 Fi8000 Basics of Options

http://slidepdf.com/reader/full/fi8000-basics-of-options 57/57

Practice ProblemsPractice Problems

BKM Ch. 20: 1-12, 14-23BKM Ch. 20: 1-12, 14-23

Practice Set: 1-16Practice Set: 1-16

![The Basics of MACRA and 2017 Reporting Options [SLIDESHOW]](https://img.pdfslide.us/doc/110x75/5879ad4e1a28ab6b2c8b49af/the-basics-of-macra-and-2017-reporting-options-slideshow.jpg)