Embed Size (px)

Citation preview

FFS REFINERS (PTY) LTD (“FFS”)

TARIFF APPLICATION

FOR THE YEAR MARCH 2012 TO FEBRUARY 2013

CAPE TOWN HARBOUR TANK FARM

LICENCE PPL.sf.F3/80/10/2008

FOR NERSA REVIEW ONLY

PLEASE REVERT TO SENSITISED VERSION FOR PUBLIC COMMENT

2

Table of Contents

1 Executive Summary ........................................................................................ 4

2 Background .................................................................................................. 7

3 Approach and base of assumptions used ............................................................... 7

3.1 Property, Plant Vehicles & Equipment (V) ..................................................... 8

3.1.1 Indexation ............................................................................... 9

3.1.2 Useful Lives .............................................................................. 9

3.1.3 Decommissioning provision ........................................................ 9

3.1.4 Summary of RAB asset values ..................................................... 9

3.2 Borrowing costs .................................................................................. 10

3.3 Net working capital (w) ......................................................................... 11

3.4 Deferred Tax (dtax) ............................................................................. 12

4 Weighted Average Cost of Capital (WACC) ........................................................... 12

4.1 Cost of Equity .................................................................................... 13

4.1.1 Risk free rate ............................................................................ 13

4.1.2 Market risk premium (“MRP”) ........................................................ 13

4.1.3 BETA ...................................................................................... 13

4.1.4 Real cost of equity calculation .................................................. 18

4.1.5 Comparable IRRs for related industries ...................................... 19

4.2 Cost of Debt .................................................................................... 21

4.3 WACC ............................................................................................. 22

5 Expenses ................................................................................................... 23

6 Income Taxation .......................................................................................... 24

7 Depreciation ............................................................................................... 24

8 Clawback ................................................................................................... 24

9 Allowable Revenue Calculation ......................................................................... 25

10 Volumes .................................................................................................... 25

11 Conclusion ................................................................................................. 26

3

List of Tables Table 1: RAB Asset Values (ZAR) ...................................................................... 9

Table 2: Replacement Cost Estimate (ZAR) ....................................................... 10

Table 3: Working Capital Summary (ZAR) ......................................................... 12

Table 4: Reviewed BETA Summary ................................................................... 18

Table 5: Real Cost of Equity............................................................................. 18

Table 6: Comparable IRRs ............................................................................... 19

Table 7: Comparable IRRs Summary ................................................................ 20

Table 8: Real Cost of Debt ............................................................................... 21

Table 9: Post Tax Real WACC ........................................................................... 22

Table 10:Site Expense Summary (ZAR mil) ....................................................... 23

Table 11:Allowable Revenue (ZAR mil) .............................................................. 25

4

1 Executive Summary

FFS submits its 2012/13 petroleum Loading and Storage facilities tariff application in terms of

section [4(f)] of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003) (“PPA”). This tariff

application has been guided by the National Energy Regulator of South Africa’s (“NERSA”) “Tariff

Methodology for Petroleum Loading Facilities and Petroleum Storage facilities” as approved on

March 31st, 2011 (“the methodology”). Furthermore, FFS has endeavoured to meet NERSA’s

draft Minimum Information Required for Tariff Applications (“draft MIRTA”), subject to limitations

on accounting information as FFS does not specifically account for Petroleum licensed storage

business. Refer to Annexure B for the checklist of information submitted

FFS is requesting a one year tariff for the period – ending February 2013. It is expected that in

the 2nd tariff period a 3 year tariff will be requested once FFS fully understands the impact of the

methodology and that Petroleum licensed storage business related information is available.

FFS has complied with the NERSA methodology with the exception of the following:

1. Used a differing approach to calculate BETA specific for FFS (in line with other

applications and based on currently available economic best practice)

A point to note:

The impact should Ankelig not have diesel fuel available to provide peak power would result in a

substantially larger impact on the South African economy than the current tariffs agreed with

FFS. The impact of this cannot be accurately measured but could be over R200million per annum

– loss of production / downtime and other negative impacts.

FFS specific business considerations:

FFS specific issues compared to Loading Facilities and Petroleum Storage facilities owned by

other bulk liquid storage operators:

• FFS designs, builds and operates its own storage facilities. The Tank Farm in the Cape

Town Harbour is a case in point. This was built to enable FFS to take advantage of marine

de-bunkers (the purchase of out of specification bunker fuel and the purchase of bunker

fuel from vessels, over-loaded or in distress, such as the Maersk Sealander, that went

5

ashore of Milnerton Beach) and also to prevent Chevron, who is the only supplier of

heavy fuel oil in the Western Cape, from charging excessively high prices above import

parity (as the Tank farm gave FFS the opportunity to import fuel oil for its production

facility at Vissershok).

• The use of the Tank Farm changed when Eskom and PetroSA needed storage facilities in

the Western Cape for the storage of diesel fuel for Eskom’s emergency power generators

at Ankelig. There were no other bulk fuel storage facilities available in the Western Cape,

and FFS reluctantly agreed to provide this facility to Eskom and PetroSA to improve

electrical supply security to the Western Cape.

• As FFS is primarily a manufacturer and supplier of “cost effective, fit for purpose industrial

heating fuels” and does not account separately for its storage facility, the current FFS

information is based on best available information obtained through manual interventions

in the FFS accounting system. It is expected that over time the quality of this information

will improve.

• FFS is planning to interact with NERSA on the RRMs after the tariff approval

6

Basis of the Application

This application has been prepared for the currently licensed loading facilities and Petroleum

Storage facilities in the FFS Cape Town Harbour Tank Farm.

In arriving at the 2012/13 Allowable Revenue (“AR”), FFS has adhered to the PPA, the

Regulations made thereunder and the methodology, save for some deviations from the

methodology in the calculation of the cost of equity (Ke) – specifically in relation to the

calculation of the relevant Beta for FFS.

FFS’s approach is supported by literature, international best practice and sound rationale. Refer

to Annexure F for the supporting calculations for the BETA calculations.

Annexure D provides an excel spread sheet supporting the many calculations involved with this

application based on the original NERSA calculations sheets and updated for FFS specific

requirements.

RAB Considerations:

In arriving at the Regulatory Asset Based (“RAB”) for the application, historical information is

unfortunately not available with the first tank built in July 1995. As with other companies

historical information is scarce, unreliable and generally irrelevant. FFS has obtained a detailed

cost estimate from a reputable construction company (dated 9th February 2012) for the building

of such a facility which indicates that a replacement cost for this facility would be R121 - R449

million. Refer to Annexure C for the cost estimate from --- ----, a reputable South African

contractor with experience of storage facility construction.

This is in line with the tariff applications submitted by Transnet and Vopak, in which they also

revalued the storage assets based on independent valuations at replacement value at the start of

the tariff period and then applied the TOC methodology for the following period.

Unlike other independent tank storage operators, bulk liquid storage is not the core business of

FFS. The structural, safety and environmental control over the FFS storage assets is, however,

key and even though some of the FFS assets may be close to the end of the accounting specific

7

useful lives, the strict maintenance requirements that FFS complies with and ensures require FFS

to continue to invest in the assets through on-going capital expenditure and maintenance.

2 Background

FFS designed, built and commissioned the Cape Harbour Tank Farm for its own use, to take

advantage of marine and refinery distress cargo and to enable FFS to import industrial fuel oil to

supply its markets in times when the availability of supply in the Western Cape was interrupted.

It was used on a number of occasions, most notably for the receipt and storage of the Bunker

fuel removed from the Maersk Sealander, the vessel that went aground off Milnerton beach. The

recovery of this vessel would not have been possible without the FFS Cape Harbour Tank Farm

being available to take the bunker fuel removed from the vessel.

As mentioned earlier, FFS eventually agreed, in the interests of the national economy, to enter

into an agreement with Eskom and PetroSA for the full capacity of the Tank Farm for the storage

of diesel for the operation of Eskom’s emergency power generators at Ankerlig.

There is no other storage facility in the Western Cape available for this purpose.

3 Approach and base of assumptions used

FFS has complied with the NERSA methodology relating to the calculation of Allowable Revenue

with the exception of the methodology used to calculate BETA (based on the use of the CAPM

model) and the impact on Ke (within the WACC calculation – refer to Annexure D for additional

information).

The building blocks of the methodology are reflected in the following formula:

Allowable Revenue = (RAB x WACC) +E +T + D ± C

Where:

RAB = Regulatory Asset Base

WACC = Weighted average cost of capital

E = Expenses: operating and maintenance expenses for the tariff period under review

8

T = Tax: estimated tax expense for the tariff period under review

D = Depreciation: the charge for the tariff period under review

C = Clawback adjustment (to correct for differences between actuals and forecasts in

formula elements as well as efficiency gains and volume differences) from a preceding

tariff period in relation to the latest estimates for that tariff period

The formula allows for the calculation of an AR for the petroleum storage assets. A detailed

spread sheet (as per the NERSA format) is included in this application – refer to Annexure D

Base worksheet for full calculation.

In terms of the methodology, the value of the RAB is the inflation-adjusted historical cost or

“trended original cost” (“TOC”) of property, plant, vehicles and equipment less the accumulated

depreciation for the period under consideration, plus net working capital and adjusted for

deferred tax.

The formula for the RAB is as follows:

RAB = (V – d) + w ± dtax1

Where:

V = Value of property, plant, vehicles and equipment

D = accumulated depreciation up to the commencement of the tariff period under review

w = net working capital

dtax = deferred tax

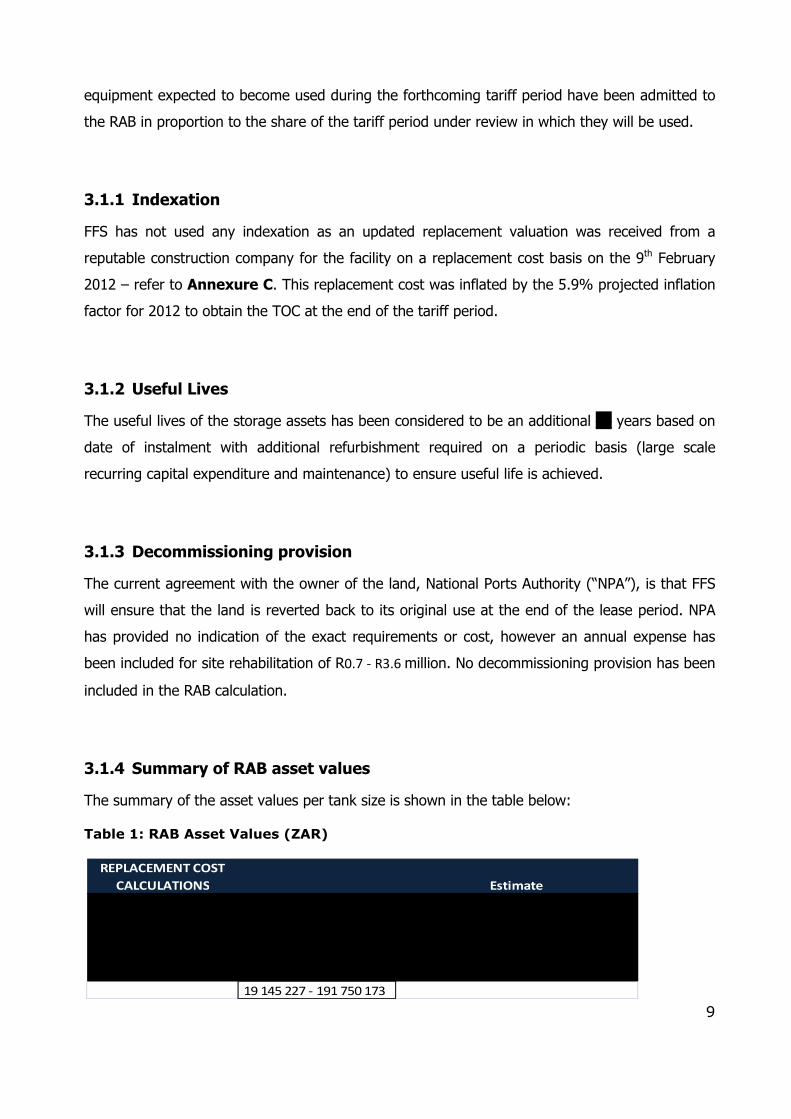

3.1 Property, Plant Vehicles & Equipment (V)

Property, plant, vehicles and equipment are valued on the Trended Original Cost (“TOC”) basis

using the consumer price index (“CPI”) as the inflation measure. Property, plant, vehicles and

9

equipment expected to become used during the forthcoming tariff period have been admitted to

the RAB in proportion to the share of the tariff period under review in which they will be used.

3.1.1 Indexation

FFS has not used any indexation as an updated replacement valuation was received from a

reputable construction company for the facility on a replacement cost basis on the 9th February

2012 – refer to Annexure C. This replacement cost was inflated by the 5.9% projected inflation

factor for 2012 to obtain the TOC at the end of the tariff period.

3.1.2 Useful Lives

The useful lives of the storage assets has been considered to be an additional __ years based on

date of instalment with additional refurbishment required on a periodic basis (large scale

recurring capital expenditure and maintenance) to ensure useful life is achieved.

3.1.3 Decommissioning provision

The current agreement with the owner of the land, National Ports Authority (“NPA”), is that FFS

will ensure that the land is reverted back to its original use at the end of the lease period. NPA

has provided no indication of the exact requirements or cost, however an annual expense has

been included for site rehabilitation of R0.7 - R3.6 million. No decommissioning provision has been

included in the RAB calculation.

3.1.4 Summary of RAB asset values

The summary of the asset values per tank size is shown in the table below:

Table 1: RAB Asset Values (ZAR)

REPLACEMENT COST

CALCULATIONS Estimate

19 145 227 - 191 750 173

10

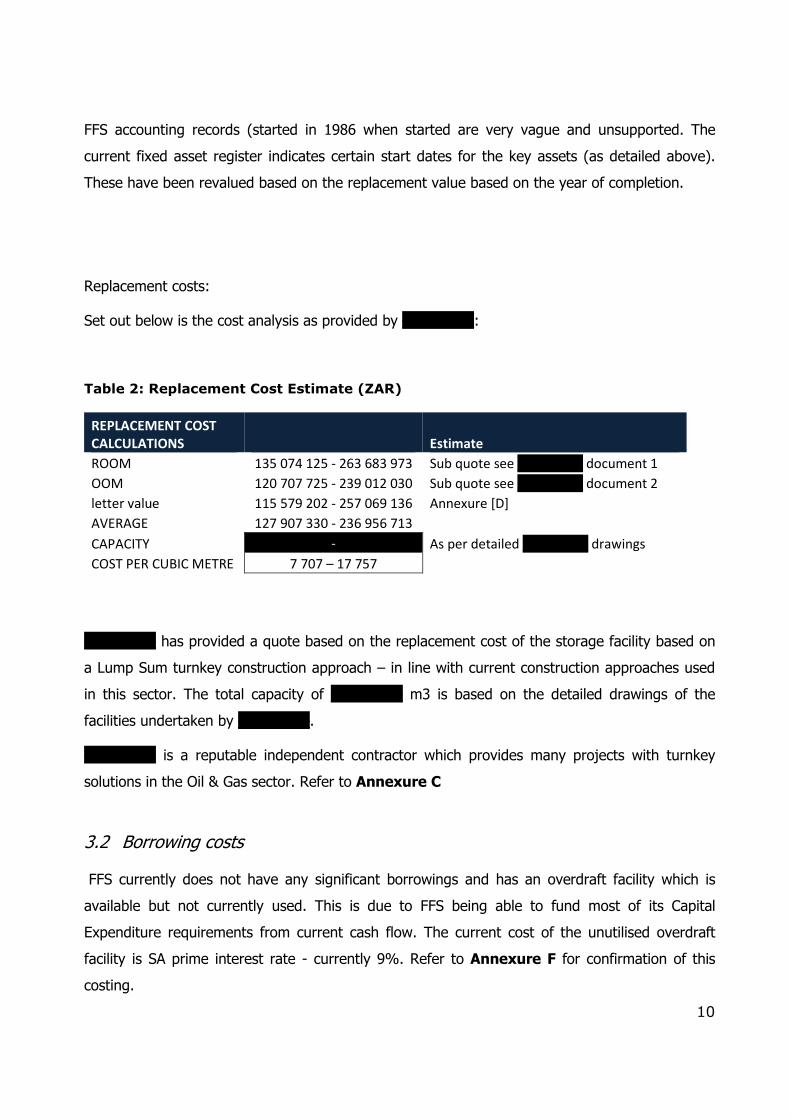

FFS accounting records (started in 1986 when started are very vague and unsupported. The

current fixed asset register indicates certain start dates for the key assets (as detailed above).

These have been revalued based on the replacement value based on the year of completion.

Replacement costs:

Set out below is the cost analysis as provided by _________:

Table 2: Replacement Cost Estimate (ZAR)

REPLACEMENT COST

CALCULATIONS Estimate

ROOM 135 074 125 - 263 683 973 Sub quote see _________ document 1

OOM 120 707 725 - 239 012 030 Sub quote see _________ document 2

letter value 115 579 202 - 257 069 136 Annexure [D]

AVERAGE 127 907 330 - 236 956 713

CAPACITY As per detailed _________ drawings

COST PER CUBIC METRE 7 707 – 17 757

_________ has provided a quote based on the replacement cost of the storage facility based on

a Lump Sum turnkey construction approach – in line with current construction approaches used

in this sector. The total capacity of _________ m3 is based on the detailed drawings of the

facilities undertaken by _________.

_________ is a reputable independent contractor which provides many projects with turnkey

solutions in the Oil & Gas sector. Refer to Annexure C

3.2 Borrowing costs

FFS currently does not have any significant borrowings and has an overdraft facility which is

available but not currently used. This is due to FFS being able to fund most of its Capital

Expenditure requirements from current cash flow. The current cost of the unutilised overdraft

facility is SA prime interest rate - currently 9%. Refer to Annexure F for confirmation of this

costing.

11

FFS understands that NERSA require a minimum Debt / Equity ratio of 30%. Although FFS

reading of the relevant wording indicates that this will only be included when the actual market

cost of debt is vague or the Project is highly structured. FFS, based on its comparable company

study, has applied the average Debt / Equity ratio applicable to its sector. This has been used in

the tariff application and the subsequent leveraging of the relevant BETA.

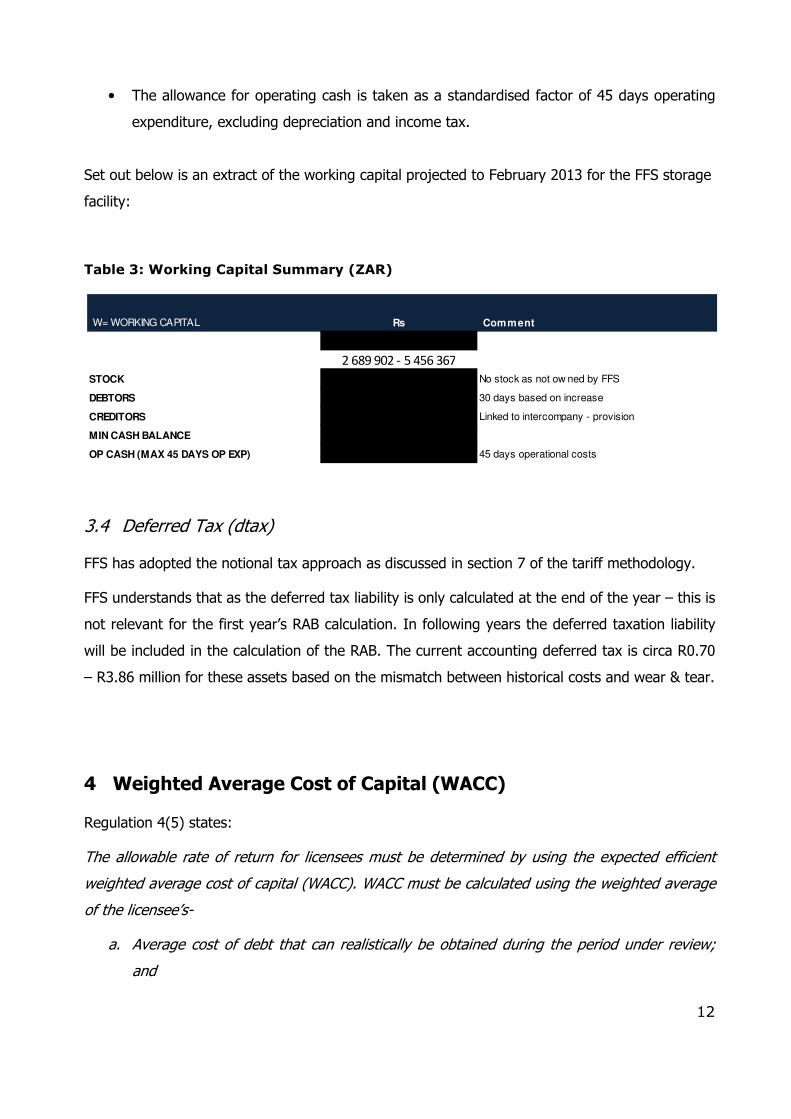

3.3 Net working capital (w)

Net working capital refers to various regulated business operations, funding requirements other

than utility plant in service. These funding requirements include inventories, prepayments,

minimum bank balances, cash working capital and other non-plant operating requirements.

Working capital funding requirements funded by investors are legitimate Regulatory Asset Base

allowances on which a return may be granted.

Net working capital is included in the RAB and is calculated according to the formula provided in

the methodology which is as follows:

Net working capital = inventory + receivables + operating cash + minimum cash

balance – trade payables2

The components are recognised as follows:

• No inventory is considered – spares procured based on required demand

• Trade receivables are based on 30 days of turnover based on the current customer

contract. Allowances for irrecoverable amounts are recognised in the income statement

when there is objective evidence that the asset is impaired. Other receivables include

prepayments;

• Direct labour and direct operating expenses are, where possible, charged to the Tank

Farm. The expenses of the FFS Western Cape Region are allocated on a percentage basis

to the Tank Farm.

• External Trade payables are settled within 45 days with majority based on intercompany

with no credit terms; and

2 Refer to section 4.3.2 of tariff methodology

12

• The allowance for operating cash is taken as a standardised factor of 45 days operating

expenditure, excluding depreciation and income tax.

Set out below is an extract of the working capital projected to February 2013 for the FFS storage

facility:

Table 3: Working Capital Summary (ZAR)

3.4 Deferred Tax (dtax)

FFS has adopted the notional tax approach as discussed in section 7 of the tariff methodology.

FFS understands that as the deferred tax liability is only calculated at the end of the year – this is

not relevant for the first year’s RAB calculation. In following years the deferred taxation liability

will be included in the calculation of the RAB. The current accounting deferred tax is circa R0.70

– R3.86 million for these assets based on the mismatch between historical costs and wear & tear.

4 Weighted Average Cost of Capital (WACC)

Regulation 4(5) states:

The allowable rate of return for licensees must be determined by using the expected efficient

weighted average cost of capital (WACC). WACC must be calculated using the weighted average

of the licensee’s-

a. Average cost of debt that can realistically be obtained during the period under review;

and

W= WORKING CAPITAL Comment

STOCK

DEBTORS

CREDITORS

MIN CASH BALANCE

OP CASH (MAX 45 DAYS OP EXP)

Rs

-

45 days operational costs

Linked to intercompany - provision

30 days based on increase

No stock as not ow ned by FFS

-

2 689 902 - 5 456 367

13

b. Cost of equity capital calculated by means of the capital asset pricing model or any other

appropriate model

The approach taken by FFS in this application is fully compliant with Regulation 4(5). Also, in

line with NERSA, FFS has applied the capital asset pricing model (“CAPM”) to estimate the cost of

equity, with an exception being the calculation of BETA, which adjusts the final BETA calculation

4.1 Cost of Equity

Section 5.6.2 of the methodology sets out the formula for calculating the real cost of equity. In

this section of the application, we deal in turn with the individual components of the cost of

equity calculation embodied in the Capital Asset Pricing Model (“CAPM”), namely the risk free

rate, the market risk premium and beta.

4.1.1 Risk free rate

FFS has derived the risk free rate element for the cost of equity based on the MRP information

available on NERSAs website for applications of 4.40%

4.1.2 Market risk premium (“MRP”)

In common with the methodology, FFS has derived the MRP element of the cost of equity from

monthly observations, as published by NERSA in line with section 5.6.3 of the methodology. As

the methodology does not specify how to calculate the average, FFS has used the real MRP as

published by NERSA, which indicates a Market risk premium of 7.32% for the 25 year period

starting May, 1987 to mid last year 2011 based on current available information.

4.1.3 BETA

The methodology requires the licensee to propose a beta along with details of proxies used to

derive the beta suggested.

FFS Beta limitations:

In estimating the beta, FFS notes several key elements:

a. FFS is not a listed or stock exchange traded company

14

b. Its primary business is industrial heating fuels from waste products and Refinery by-

products and not tank farm rentals.

c. Information on local companies operating in the industry is not publicly available,

therefore FFS has had to use off shore comparable companies, and primarily those

companies traded on the NYSE.

d. No public companies on the NYSE are businesses which operate solely in petroleum

storage. In the cases observed, petroleum storage is a segment within the broader

business.

Beta

e. This situation described above has several major implications for deriving the beta that is

applicable:

I. Beta (as defined) is a measure of systematic risk; a measure of risk present in the

company across its business segments and measures the stock performance in

relation to the index.

II. The standard procedure for estimating betas, is to regress the specific stock

returns ���� against the market returns ����:���� = � + ����, where b is the

slope of the regression (referred to as �), and a is the intercept. It can be shown

mathematically, that the relationship described above can be expressed as

= ���/��� × � , where � is the variance of the stock/market and � is the

correlation between the two. This equation implies that the measure of market

risk is the portion of the relative standard deviation (i.e. the stock performance

compared to the market performance) that comes from the stock correlation with

the market.

III. R�, which by definition is R� = ρ� , is percentage in variance of the independent

variable that can be explained by the dependent variable. In our discussion, R� is

the percentage in variance of the stock, �R��, that can be explained by market

performance �R��. Assuming R� of 30%, would suggest that 30% of the risk in

the stock comes from market sources, and that 70% of the risk, comes from

company specific risk, which can arise from lack of diversification in business

15

segments, lack of geographic diversification etc. The R� statistic is reported by

financial information providers, along with other information relating to beta.

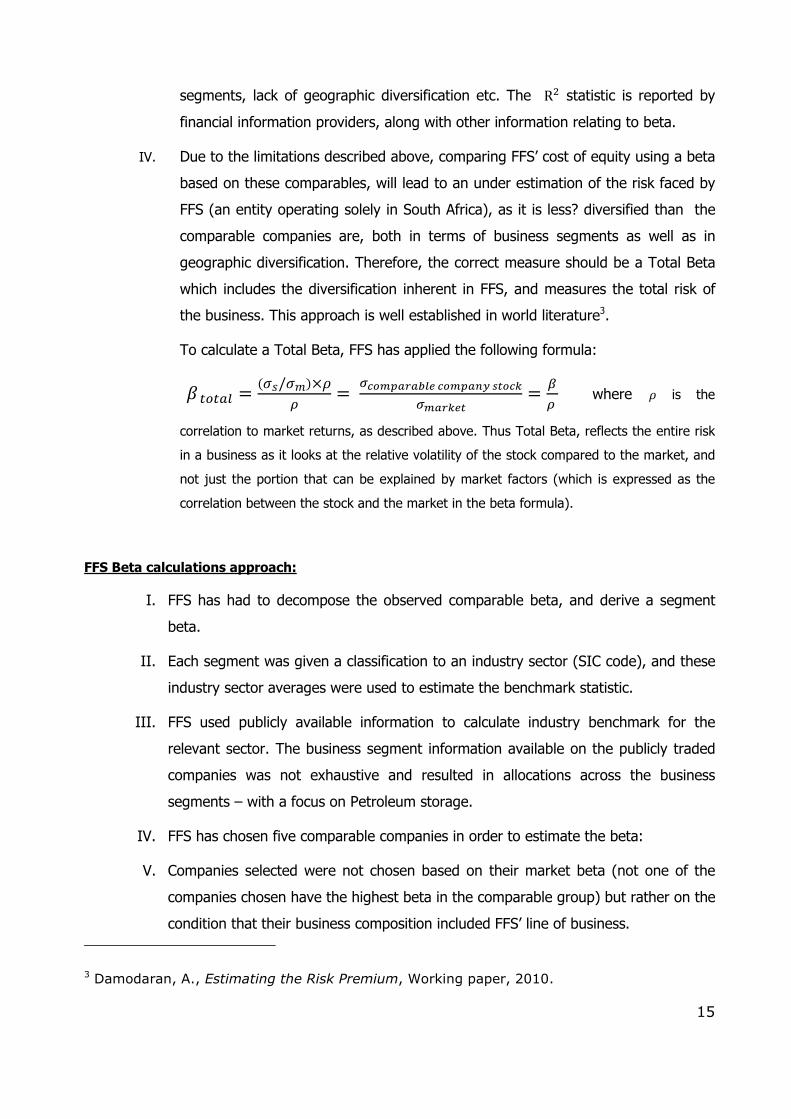

IV. Due to the limitations described above, comparing FFS’ cost of equity using a beta

based on these comparables, will lead to an under estimation of the risk faced by

FFS (an entity operating solely in South Africa), as it is less? diversified than the

comparable companies are, both in terms of business segments as well as in

geographic diversification. Therefore, the correct measure should be a Total Beta

which includes the diversification inherent in FFS, and measures the total risk of

the business. This approach is well established in world literature3.

To calculate a Total Beta, FFS has applied the following formula:

� ����� = ���/����� = ���� !"!#$% ��� !&' ()��*

��!"*%) = +

� where � is the

correlation to market returns, as described above. Thus Total Beta, reflects the entire risk

in a business as it looks at the relative volatility of the stock compared to the market, and

not just the portion that can be explained by market factors (which is expressed as the

correlation between the stock and the market in the beta formula).

FFS Beta calculations approach:

I. FFS has had to decompose the observed comparable beta, and derive a segment

beta.

II. Each segment was given a classification to an industry sector (SIC code), and these

industry sector averages were used to estimate the benchmark statistic.

III. FFS used publicly available information to calculate industry benchmark for the

relevant sector. The business segment information available on the publicly traded

companies was not exhaustive and resulted in allocations across the business

segments – with a focus on Petroleum storage.

IV. FFS has chosen five comparable companies in order to estimate the beta:

V. Companies selected were not chosen based on their market beta (not one of the

companies chosen have the highest beta in the comparable group) but rather on the

condition that their business composition included FFS’ line of business.

3 Damodaran, A., Estimating the Risk Premium, Working paper, 2010.

16

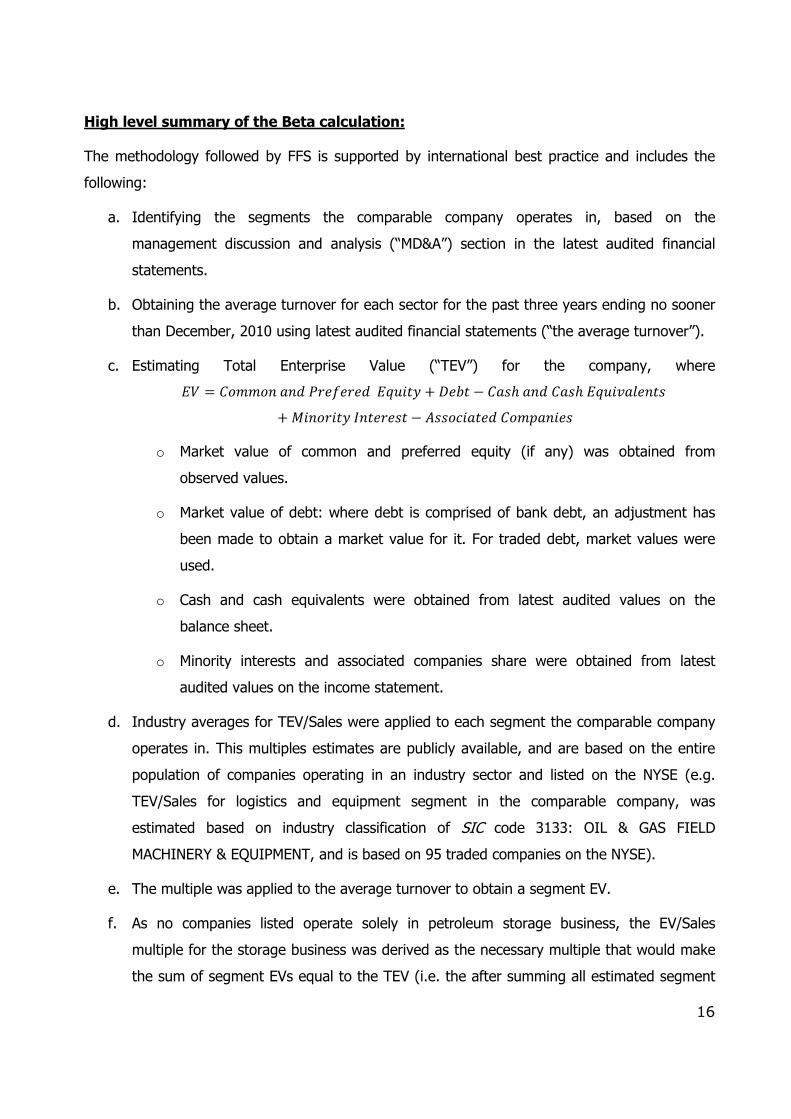

High level summary of the Beta calculation:

The methodology followed by FFS is supported by international best practice and includes the

following:

a. Identifying the segments the comparable company operates in, based on the

management discussion and analysis (“MD&A”) section in the latest audited financial

statements.

b. Obtaining the average turnover for each sector for the past three years ending no sooner

than December, 2010 using latest audited financial statements (“the average turnover”).

c. Estimating Total Enterprise Value (“TEV”) for the company, where

,- = ./��/0 �01 23454341 ,6789: + ;49 − .��ℎ �01 .��ℎ ,678>�?409�+ @80/389: A09434�9 − B��/C8�941 ./�D�084�

o Market value of common and preferred equity (if any) was obtained from

observed values.

o Market value of debt: where debt is comprised of bank debt, an adjustment has

been made to obtain a market value for it. For traded debt, market values were

used.

o Cash and cash equivalents were obtained from latest audited values on the

balance sheet.

o Minority interests and associated companies share were obtained from latest

audited values on the income statement.

d. Industry averages for TEV/Sales were applied to each segment the comparable company

operates in. This multiples estimates are publicly available, and are based on the entire

population of companies operating in an industry sector and listed on the NYSE (e.g.

TEV/Sales for logistics and equipment segment in the comparable company, was

estimated based on industry classification of SIC code 3133: OIL & GAS FIELD

MACHINERY & EQUIPMENT, and is based on 95 traded companies on the NYSE).

e. The multiple was applied to the average turnover to obtain a segment EV.

f. As no companies listed operate solely in petroleum storage business, the EV/Sales

multiple for the storage business was derived as the necessary multiple that would make

the sum of segment EVs equal to the TEV (i.e. the after summing all estimated segment

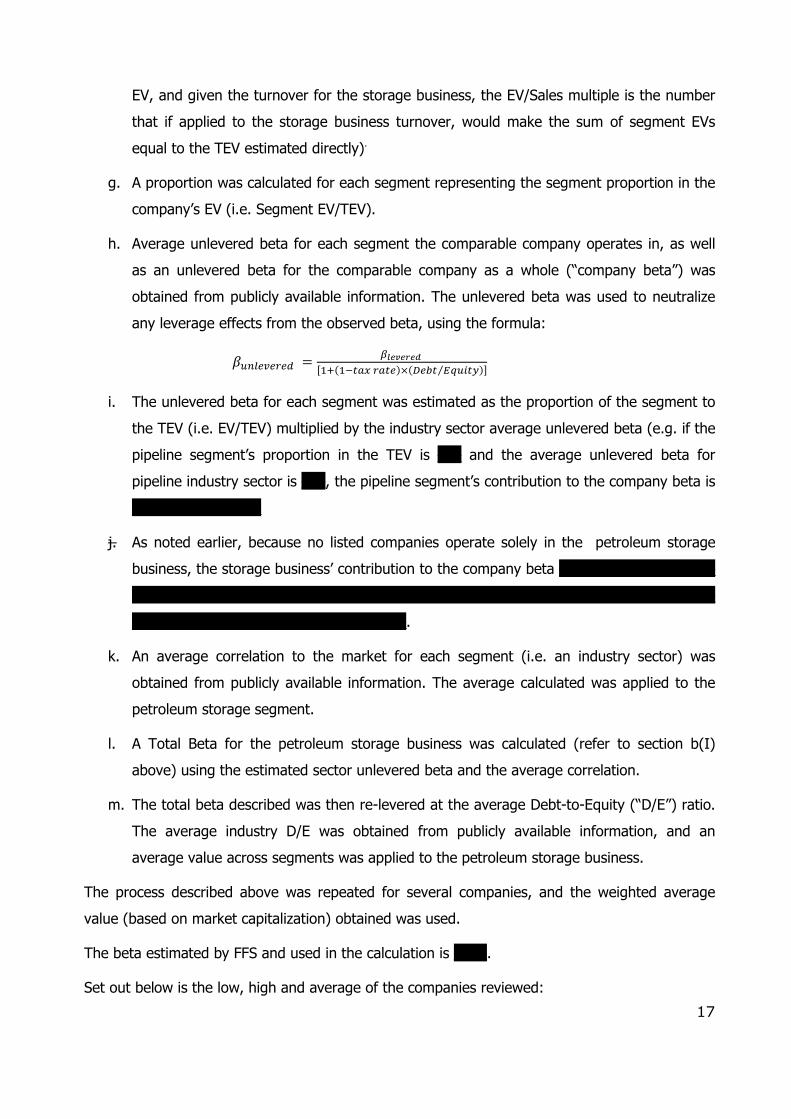

17

EV, and given the turnover for the storage business, the EV/Sales multiple is the number

that if applied to the storage business turnover, would make the sum of segment EVs

equal to the TEV estimated directly).

g. A proportion was calculated for each segment representing the segment proportion in the

company’s EV (i.e. Segment EV/TEV).

h. Average unlevered beta for each segment the comparable company operates in, as well

as an unlevered beta for the comparable company as a whole (“company beta”) was

obtained from publicly available information. The unlevered beta was used to neutralize

any leverage effects from the observed beta, using the formula:

�EF�GHGIGJ = +$%K%"%L MNO�NP��Q I��G�×�RGS� T⁄ VEW�X�Y

i. The unlevered beta for each segment was estimated as the proportion of the segment to

the TEV (i.e. EV/TEV) multiplied by the industry sector average unlevered beta (e.g. if the

pipeline segment’s proportion in the TEV is ___ and the average unlevered beta for

pipeline industry sector is ___, the pipeline segment’s contribution to the company beta is

_ __

j. As noted earlier, because no listed companies operate solely in the petroleum storage

business, the storage business’ contribution to the company beta _ ___ _

___ ___ ___ ___ ___

___ ___ __.

k. An average correlation to the market for each segment (i.e. an industry sector) was

obtained from publicly available information. The average calculated was applied to the

petroleum storage segment.

l. A Total Beta for the petroleum storage business was calculated (refer to section b(I)

above) using the estimated sector unlevered beta and the average correlation.

m. The total beta described was then re-levered at the average Debt-to-Equity (“D/E”) ratio.

The average industry D/E was obtained from publicly available information, and an

average value across segments was applied to the petroleum storage business.

The process described above was repeated for several companies, and the weighted average

value (based on market capitalization) obtained was used.

The beta estimated by FFS and used in the calculation is _ __.

Set out below is the low, high and average of the companies reviewed:

18

Table 4: Reviewed BETA Summary

Value High _ __ Low Weighted Average

_ __ _ __

Beta Used __ _

The weighted average Beta for the 5 companies compared was used

Point to note:

FFS understands that the current NERSA Beta’s calculation only considers the

levered beta for integrated pipeline companies and that no similar analysis to

understand the specific Beta for private companies solely linked to the independent

storage sector - has been undertaken. It is hoped that FFS approach will be

considered for reasonableness by NERSA and considered in the final decision.

___________________________________________________________________

_________________________________________________

FFS will share these detailed calculations with NERSA as required.

4.1.4 Real cost of equity calculation

Using the results of the calculation of the annualized real risk free rate, the market risk premium

and beta, the real cost of equity can be calculated.

Table 5: Real Cost of Equity

Tariff Application

Annualized real risk free 4.4 % Market risk premium (“MRP”) 7.32% Beta _____ Real cost of equity __ __

19

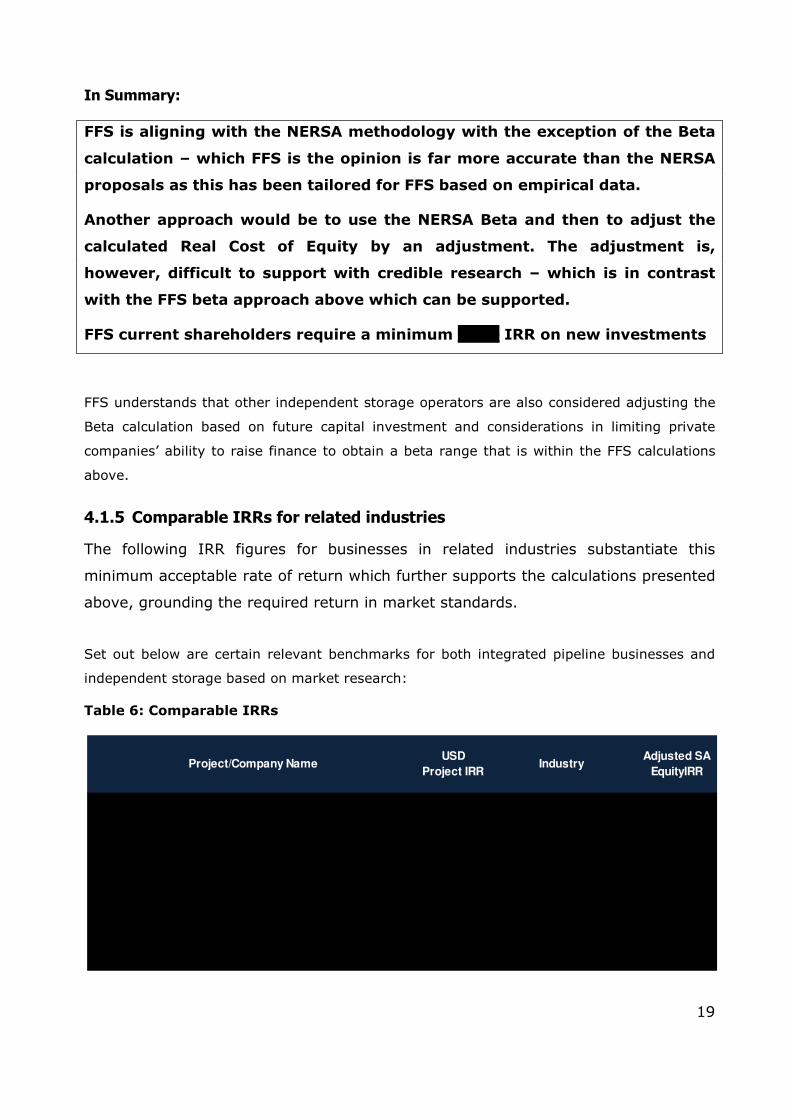

In Summary:

FFS is aligning with the NERSA methodology with the exception of the Beta

calculation – which FFS is the opinion is far more accurate than the NERSA

proposals as this has been tailored for FFS based on empirical data.

Another approach would be to use the NERSA Beta and then to adjust the

calculated Real Cost of Equity by an adjustment. The adjustment is,

however, difficult to support with credible research – which is in contrast

with the FFS beta approach above which can be supported.

FFS current shareholders require a minimum ____ IRR on new investments

FFS understands that other independent storage operators are also considered adjusting the

Beta calculation based on future capital investment and considerations in limiting private

companies’ ability to raise finance to obtain a beta range that is within the FFS calculations

above.

4.1.5 Comparable IRRs for related industries

The following IRR figures for businesses in related industries substantiate this

minimum acceptable rate of return which further supports the calculations presented

above, grounding the required return in market standards.

Set out below are certain relevant benchmarks for both integrated pipeline businesses and

independent storage based on market research:

Table 6: Comparable IRRs

Project/Company NameUSD

Project IRRIndustry

Adjusted SA

EquityIRR

20

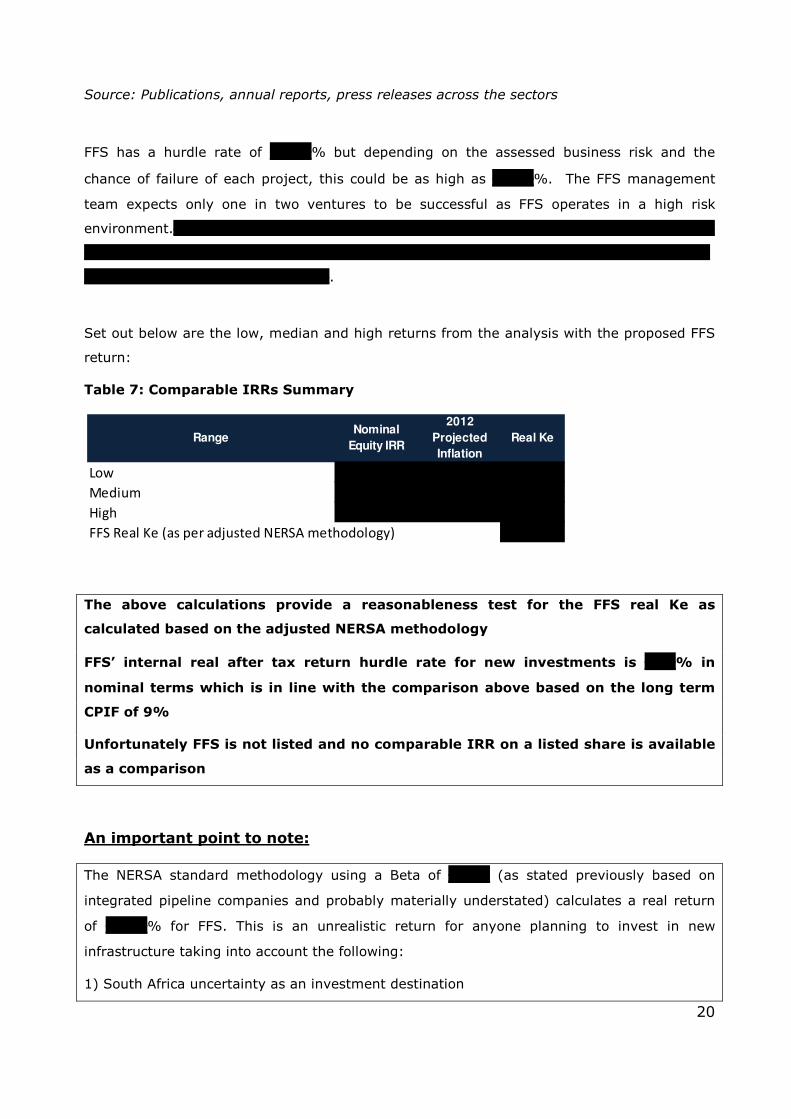

Source: Publications, annual reports, press releases across the sectors

FFS has a hurdle rate of ____% but depending on the assessed business risk and the

chance of failure of each project, this could be as high as ____%. The FFS management

team expects only one in two ventures to be successful as FFS operates in a high risk

environment.________________________________________________________________

__________________________________________________________________________

_____________________________.

Set out below are the low, median and high returns from the analysis with the proposed FFS

return:

Table 7: Comparable IRRs Summary

The above calculations provide a reasonableness test for the FFS real Ke as

calculated based on the adjusted NERSA methodology

FFS’ internal real after tax return hurdle rate for new investments is ___% in

nominal terms which is in line with the comparison above based on the long term

CPIF of 9%

Unfortunately FFS is not listed and no comparable IRR on a listed share is available

as a comparison

An important point to note:

The NERSA standard methodology using a Beta of ____ (as stated previously based on

integrated pipeline companies and probably materially understated) calculates a real return

of ____% for FFS. This is an unrealistic return for anyone planning to invest in new

infrastructure taking into account the following:

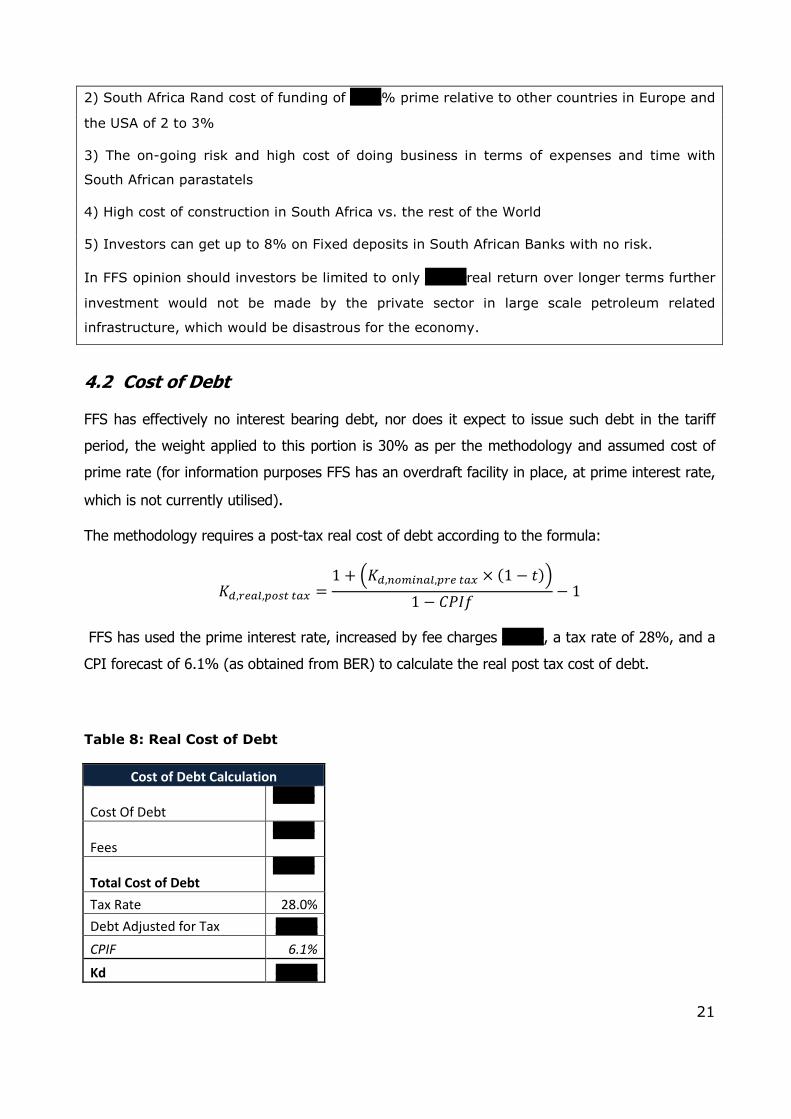

1) South Africa uncertainty as an investment destination

RangeNominal

Equity IRR

2012

Projected

Inflation

Real Ke

Low

Medium

High

FFS Real Ke (as per adjusted NERSA methodology)

21

2) South Africa Rand cost of funding of ___% prime relative to other countries in Europe and

the USA of 2 to 3%

3) The on-going risk and high cost of doing business in terms of expenses and time with

South African parastatels

4) High cost of construction in South Africa vs. the rest of the World

5) Investors can get up to 8% on Fixed deposits in South African Banks with no risk.

In FFS opinion should investors be limited to only ____real return over longer terms further

investment would not be made by the private sector in large scale petroleum related

infrastructure, which would be disastrous for the economy.

4.2 Cost of Debt

FFS has effectively no interest bearing debt, nor does it expect to issue such debt in the tariff

period, the weight applied to this portion is 30% as per the methodology and assumed cost of

prime rate (for information purposes FFS has an overdraft facility in place, at prime interest rate,

which is not currently utilised).

The methodology requires a post-tax real cost of debt according to the formula:

ZJ,IG��,\��� ��Q = 1 + ^ZJ,F��WF��,\IG ��Q × �1 − 9�_1 − .2A5 − 1

FFS has used the prime interest rate, increased by fee charges ____, a tax rate of 28%, and a

CPI forecast of 6.1% (as obtained from BER) to calculate the real post tax cost of debt.

Table 8: Real Cost of Debt

Cost of Debt Calculation

Cost Of Debt ____

Fees

____

Total Cost of Debt ____

Tax Rate 28.0%

Debt Adjusted for Tax ____

CPIF 6.1%

Kd ____

22

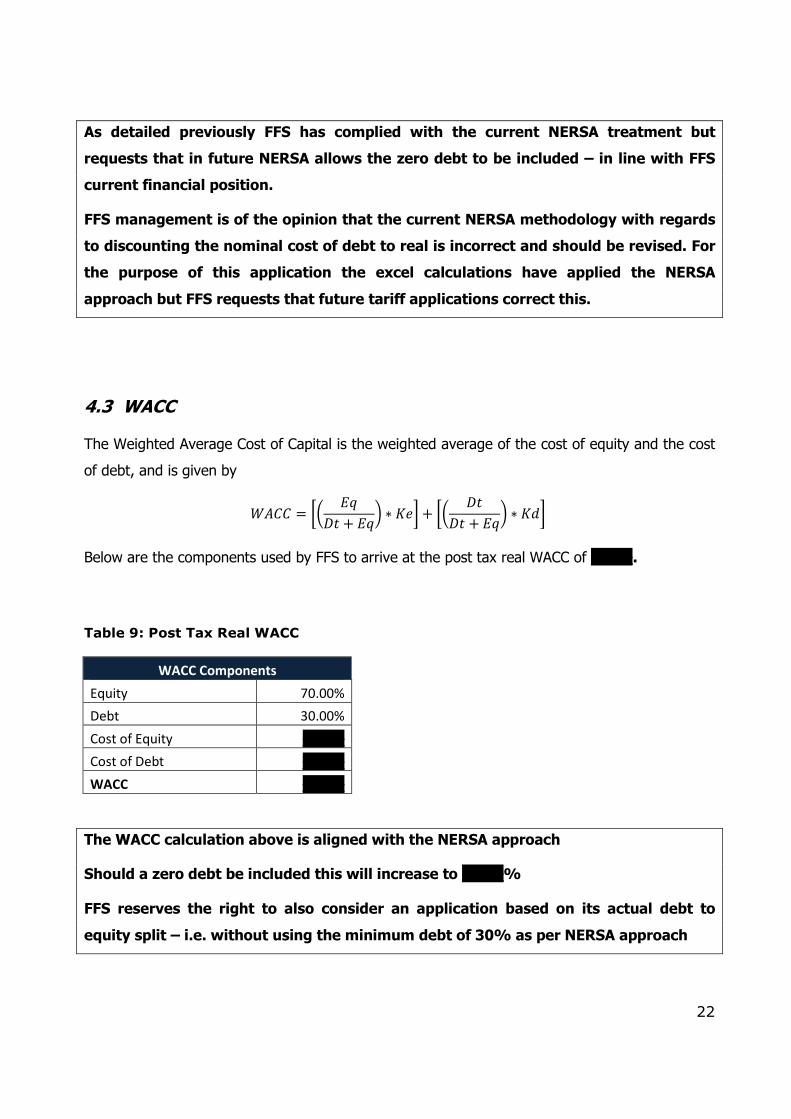

As detailed previously FFS has complied with the current NERSA treatment but

requests that in future NERSA allows the zero debt to be included – in line with FFS

current financial position.

FFS management is of the opinion that the current NERSA methodology with regards

to discounting the nominal cost of debt to real is incorrect and should be revised. For

the purpose of this application the excel calculations have applied the NERSA

approach but FFS requests that future tariff applications correct this.

4.3 WACC

The Weighted Average Cost of Capital is the weighted average of the cost of equity and the cost

of debt, and is given by

`B.. = ab ,6;9 + ,6c ∗ Z4e + ab ;9

;9 + ,6c ∗ Z1e

Below are the components used by FFS to arrive at the post tax real WACC of ____.

Table 9: Post Tax Real WACC

WACC Components

Equity 70.00%

Debt 30.00%

Cost of Equity ____

Cost of Debt ____

WACC ____

The WACC calculation above is aligned with the NERSA approach

Should a zero debt be included this will increase to ____%

FFS reserves the right to also consider an application based on its actual debt to

equity split – i.e. without using the minimum debt of 30% as per NERSA approach

23

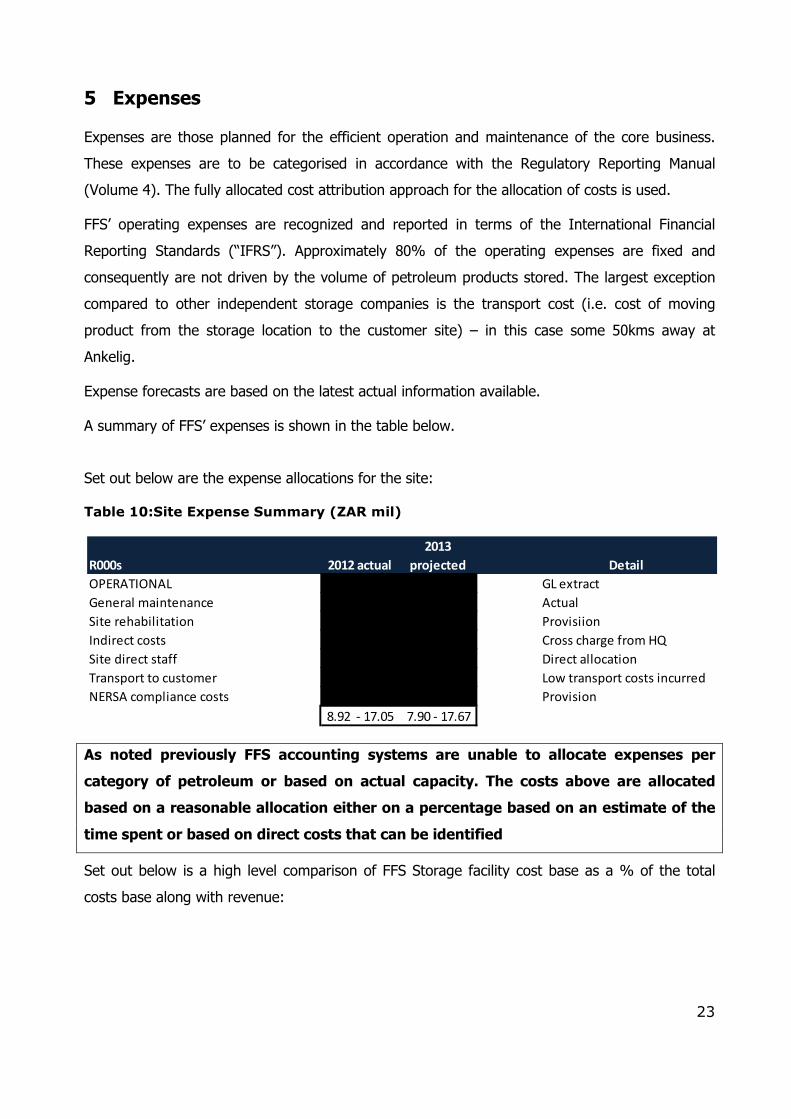

5 Expenses

Expenses are those planned for the efficient operation and maintenance of the core business.

These expenses are to be categorised in accordance with the Regulatory Reporting Manual

(Volume 4). The fully allocated cost attribution approach for the allocation of costs is used.

FFS’ operating expenses are recognized and reported in terms of the International Financial

Reporting Standards (“IFRS”). Approximately 80% of the operating expenses are fixed and

consequently are not driven by the volume of petroleum products stored. The largest exception

compared to other independent storage companies is the transport cost (i.e. cost of moving

product from the storage location to the customer site) – in this case some 50kms away at

Ankelig.

Expense forecasts are based on the latest actual information available.

A summary of FFS’ expenses is shown in the table below.

Set out below are the expense allocations for the site:

Table 10:Site Expense Summary (ZAR mil)

As noted previously FFS accounting systems are unable to allocate expenses per

category of petroleum or based on actual capacity. The costs above are allocated

based on a reasonable allocation either on a percentage based on an estimate of the

time spent or based on direct costs that can be identified

Set out below is a high level comparison of FFS Storage facility cost base as a % of the total

costs base along with revenue:

R000s 2012 actual

2013

projected Detail

OPERATIONAL GL extract

General maintenance Actual

Site rehabilitation Provisiion

Indirect costs Cross charge from HQ

Site direct staff Direct allocation

Transport to customer Low transport costs incurred

NERSA compliance costs Provision

8.92 - 17.05 7.90 - 17.67

24

The FFS licensed storage facility accounts for __ of the total Group’s revenue but only has __ of

the Total Group’s expenses allocated towards application this based on the current costing

approach.

6 Income Taxation

An election between the use of either (a) flow through (actual tax) payment or (b) notional tax

payment needs to be made. Once the election has been made; the selected option will be used

in future for all the licensee’s assets.

FFS elects to use the normalised (notional) tax approach in its tariff application. Normalised tax

refers to an estimated normalised tax expense with respect to the regulated activity for the tariff

period under review. In accordance with the methodology it is calculated based on the following

formula:

Tax = (NPBT (excluding tax allowance) / (1-tr)) x tr

Where:

NPBT (excl tax allowance) = {(RAB x WACC) +E + D (of total TOC asset base) ± C} – {E +

D (historic)}

tr = prevailing corporate tax rate

7 Depreciation

Depreciation is calculated on a straight line basis over the useful lives of the assets as per the

methodology over __ year. This is a conservative assumption and could be reduced which would

increase the AR.

The estimated depreciation charge for 2012/13 is R0.70 –R2.84million.

8 Clawback

No Clawback adjustment has been noted in the application as it is the first

application. The impact of this will be considered in the next application.

25

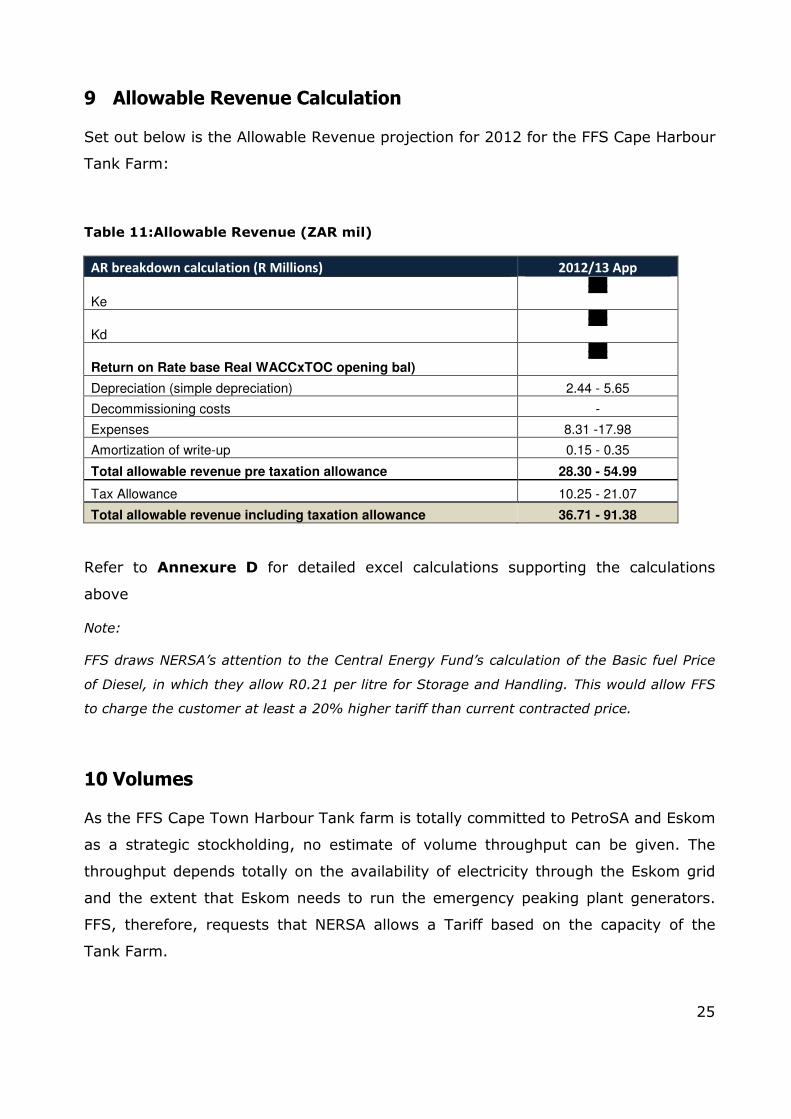

9 Allowable Revenue Calculation

Set out below is the Allowable Revenue projection for 2012 for the FFS Cape Harbour

Tank Farm:

Table 11:Allowable Revenue (ZAR mil)

AR breakdown calculation (R Millions) 2012/13 App

Ke

__

Kd

__

Return on Rate base Real WACCxTOC opening bal) __

Depreciation (simple depreciation) 2.44 - 5.65

Decommissioning costs -

Expenses 8.31 -17.98

Amortization of write-up 0.15 - 0.35

Total allowable revenue pre taxation allowance 28.30 - 54.99

Tax Allowance 10.25 - 21.07

Total allowable revenue including taxation allowance 36.71 - 91.38

Refer to Annexure D for detailed excel calculations supporting the calculations

above

Note:

FFS draws NERSA’s attention to the Central Energy Fund’s calculation of the Basic fuel Price

of Diesel, in which they allow R0.21 per litre for Storage and Handling. This would allow FFS

to charge the customer at least a 20% higher tariff than current contracted price.

10 Volumes

As the FFS Cape Town Harbour Tank farm is totally committed to PetroSA and Eskom

as a strategic stockholding, no estimate of volume throughput can be given. The

throughput depends totally on the availability of electricity through the Eskom grid

and the extent that Eskom needs to run the emergency peaking plant generators.

FFS, therefore, requests that NERSA allows a Tariff based on the capacity of the

Tank Farm.

26

The customer currently uses a strategic reserve as lack of own storage capacity on-

site. This approach can change based on the customer’s requirements – which is

impacted by South Africa’s electricity shortage position.

11 Conclusion

FFS has endeavoured to meet the draft MIRTA requirements in this application. In arriving at its

AR requirement, FFS has applied the methodology in all respects with the exception of the

calculation of cost of equity relating to the BETA calculation as discussed earlier.

FFS is cognisant that this is a maximum tariff and that FFS takes on the risk if a lower monthly

tariff is charged, along with the lower revenue. The requested tariff for the 2012/13 period is

R3,346 per m3 – as detailed by the methodology.