Embed Size (px)

Citation preview

FFI Holdings PLC(AIM: FFI)

FY 2017 RESULTS AND TRADING UPDATE

Summary

2

FFI

• Ticker: AIM: FFI

• Incorporation: UK incorporated. Founded in London in 1950. Headquartered in LA,

11 offices worldwide.

• AIM Admission: 30th June 2017

• Shares Outstanding: 157,041,248

• Market Cap: £250 million (approx.)

• Broker: Liberum

Investment

Thesis

• World leader in provision of completion contracts to the entertainment industry for films, TV,

mini-series and streaming product.

• We guarantee on-time and on-budget production - offloading risk for financiers, as well as

FFI, through long standing insurance relationships

• Increased demand for content globally enables us to leverage our core business to growth

opportunities in the cross-selling of non-creative ancillary services:

• M&A - Editing solutions business recently acquired; Multiple other opportunities

• China - Completion contracts and entertainment insurance

• Content – Strategic, low risk investment

Film Finances, Inc.Financial Highlights for the year ended 31 March 2017

• Group revenue up 9.1% to $38.8m (2016: $35.6m*)

• Underlying EBIT of $12.7m, with Reported EBIT of $10.5m (2016: $3.0m)

• Adjusted net income of $5.5m (2016: $1.9m)

• First-time revenue contributions from editing and equipment rental following the acquisition of

Pivotal Post late in the financial year (February 2017)

• Successful IPO on AIM market raised net proceeds of approximately £26.5m on 30 June 2017

3

Continuing operations (USD) 31 March 2017 YoY change (%) Margin (%)

Revenue 38,812,125 9.1

Gross profit 30,321,575 15.6 78.1

Underlying EBIT * 12,744,599 119.7 32.8

Reported EBIT ** 10,455,834 244.5 26.9

Pre-tax profit 10,295,939 232.4 26.5

After tax profit from

continuing operations ***

5,777,498 204.1 14.9

Adjusted Net income** 5,450,365 183.1 14.0

* Reported EBIT adjusted for certain exceptional and lifestyle expenses

** Presented as "Operating profit" in the income statement

*** Adjusted to exclude one-time profit from discontinued operations of $2.8m

FFI Holdings PLC Trading Update for six months to end-Sept. 2017

Completion Contract

• Core business trading well, with continued growth in the first half of FY 2018

Pivotal Post

• Delivering significant growth through successful cross-selling from FFI’s core business

M&A

• Binding LOI signed with a company engaged in duplication, authoring and production consulting for film and TV

productions, with completion expected before calendar year end

• Other opportunities in advanced stages of negotiation, several completions anticipated before calendar year end

Captive Insurer

• Successful creation of FFI Insurance, a Captive Insurer, enabling significant cost savings going forward

• New agreement with Amlin, a long-term insurance partner and shareholder of FFI, which is working with FFI

Insurance on operational implementation

China

• First Chinese completion contract quarterly payment of $1.25m received in June

• PICC agreement signed in June. Working with Chinese counterparts towards writing insurance business in China

Content

• Photography of IMAX panda movie complete and now in editing, anticipated release on schedule

4

About FFI

5

Positioned at the Core of the Film Making Industry

6

Development Phase Production Phase

• Financiers ordinarily require a guarantee that films will be delivered on time and on budget

• Producers ordinarily need completion guarantee in order to get their financing

• FFI provides completion contracts to fulfil this need:

– Staff of industry experts

– Extensive assessment of budgeted production plans

– Monitoring of production to delivery

No Completion Contract = No Financing = No Production

• As gatekeeper, FFI sees film projects first

– First sight immediately after the producer raises the money needed to produce a film

• From this position, FFI is uniquely positioned to provide various ancillary services and products to film makers

Distribution &

Marketing

Pre Production Production Post ProductionCreative Phase Financial PhaseCollection

Accounts

Completion

Contracts

FFI Core Business World Leader in Completion Contracts

• Approximately 200 productions bonded per annum (more than all movies by major studios combined)

– Leading global market share

– Skewed towards independent film producers

– High level of repeat clients

• Limited exposure taken by FFIs completion contract business

– Only cover on-time, on-budget completion (not commercial success, health, accidents etc.)

– The Company simultaneously mitigates its risk (less an excess) through a syndicate of insurance companies

• FFI earns the spread between fees charged to the production company for the completion contract (c.150-200bps) of the productionbudget and the net cost of insurance to FFI to have the contract underwritten (c. 30-50bps)

• FFI’s track record is evidenced by a negligible loss ratio

– Since 2008, FFI has provided completion contracts for approximately 1,700 productions with a total budget of over $17bn and onlyincurred $17.6m in claims (approximately $275m in fee or 6.4% of fee revenue)

– Virtually all of these claims have fallen within FFI’s excess and management is currently negotiating a reduction in insurance costs to improve gross margins post IPO

– We take no commercial risk- production can succeed or fail!

• Insurance partnership with MS Amlin, wholly owned by MS&AD Insurance Group, the 8th largest non-life insurer globally, and a 9% shareholder in FFI

– Largest capacity provider at Lloyds of London

7

FFI Core Business Key Characteristics

• High barriers to entry

– Extensive network of relationships with studios, streaming companies, producers, and financiers

– Claims performance keeps underwriting costs low

– Management depth and longevity; proprietary database

• Low ticket item

– Substitution risk for clients is high so appetite to change a trusted supplier is very low

• Stable revenue business

– FFI consistently deliver c.200 projects per annum at an average budget of $14.1m per project in FY 2017

• High margin, low risk model

– Profitable core business with a minimum expected gross margin on each project of 60%

• Cash generative

– Fees paid upfront

8

$4.4m $4.9m

$7.9m

$14.1m

$0m

$4m

$8m

$12m

$16m

FY 2000 FY 2005 FY 2010 FY 2017

Average Budget of FFI Bonded Projects

Source: Company

Total Budget of FFI Bonded Projects

$0.8bn $0.9bn

$1.8bn

$2.4bn

$0bn

$1bn

$2bn

$3bn

FY 2000 FY 2005 FY 2010 FY 2017

Source: Company

• Market commentators suggest that China could become the largest box office market in the world by the end of

2017

• FFI is negotiating a licensing agreement with an investor who pays $5m to FFI for a share of FFI’s Chinese

Completion Contracts for 2018

9

$0

$1

$2

$3

$4

$5

$6

$7

2010 2011 2012 2013 2014 2015 2016

$ Amount in Billions

Source: ENTGROUP

FFI Core Business China

China’s box office revenue 2010-2016

Market Backdrop Growing Demand for Content

• Global In-home and Cinema demand is projected to continue growing

• The projected growth in content demand, partly driven by the increased use of streaming technology, is expected

to keep FFI’s products and services in demand

10

Source: McKinsey & Company Global Media Report 2015

$100

$150

$200

$250

$300

$350

$400

$15

$20

$25

$30

$35

$40

$45

$50

Total Global Cinema Spending ($bn)Total Global In-Home Viewing Spending ($bn)

• Proliferation of viewing platforms – cinema, TV and on-demand, online streaming via tablet and smart phone

– Driving rapid take up of second screen viewings

– Total home viewing revenues in U.S. now exceed Box Office

• The likes of Netflix and Amazon Films are acquiring multi-territory rights for feature films and want to distribute

content online

– Shrinking theatrical window is also a catalyst for additional content

• Google, Hulu and AT&T are looking to enter the market with original content to drive their subscription model

– Opportunity to use FFI’s expertise as they have no production infrastructure

11

FFI Streaming Content - Number of Titles Per Year

Market BackdropDigital Streaming Driving Growth

Source: Company

1

8

17

FY 2013 FY 2015 FY 2017

Growth StrategyNon-creative ancillary services

12

Revenue CollectionAccounting Editing solutions

Accounting

Localisation

Entertainment

InsuranceBonding (FFI)

• FFI continues to build a trusted ecosystem to service the entire production cycle, cross selling and packaging services into our

client base

• This is leveraging FFI’s leading market position to drive growth in our ancillary services platform, which a production will require

as it moves from concept, to production, to screen

– FFI has unparalleled visibility, seeing projects and detailed budgets at embryonic stage

– This market intelligence enables us to introduce existing production clients to FFI’s ancillary service providers

• Producers know time is key for completion contract schedule so take comfort from our recommendations

– Producers agnostic where they go for non creative/commodity services

• Low risk, low multiple acquisitions to monetise our existing relationships

– Acquired editing solutions business in February 2017

– Plan to acquire other small companies with great management (minimal integration risk)

Development Phase Production PhaseDistribution &

Marketing

Pre Production Production Post ProductionCreative Phase Financial PhaseCollection

Accounts

Completion

Contracts

Sound design

VFX

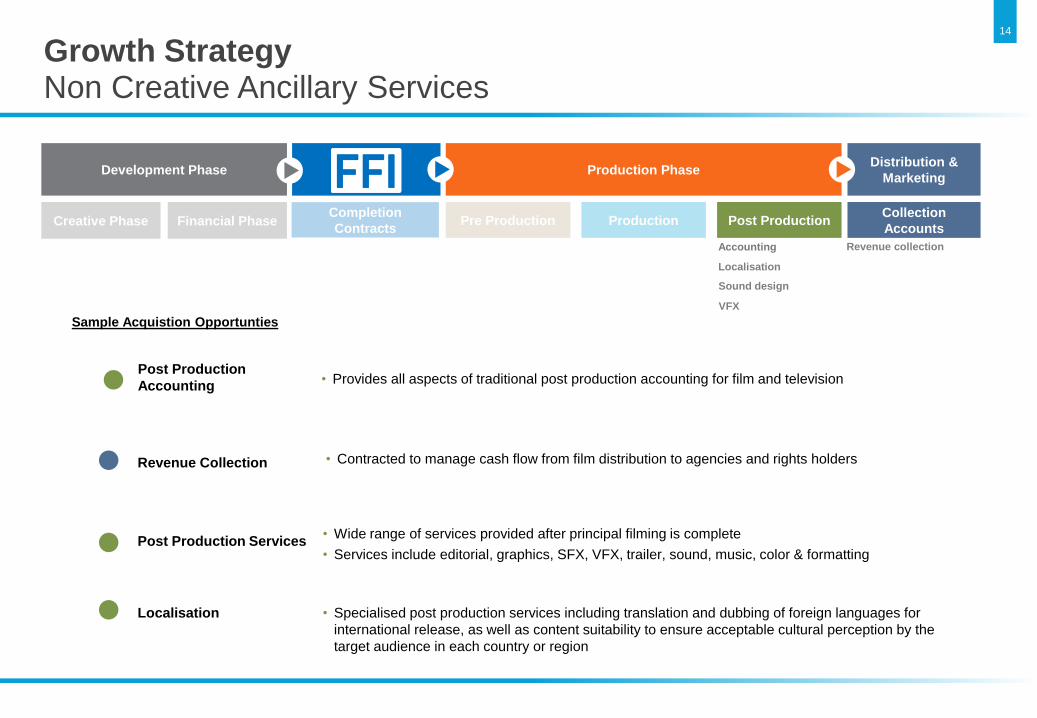

Growth StrategyPost Production

13

Development Phase Production PhaseDistribution &

Marketing

Pre Production Production Post ProductionCreative Phase Financial PhaseCollection

Accounts

Completion

Contracts

• FFI has already acquired a post production editing company

– Acquired Pivotal Post in February 2017

– $10.6m revenue, $2.5m EBITDA in 2016

– Over 16 projects already introduced from FFI platform – our market intelligence is key

• In post production alone, the addressable market within FFI’s existing customer base is significant

– The total budget of FFI’s bonded projects in FY2017 was c. $2.4bn

– On average, post production represents c. 15% of a production budget

– We believe a c.15% profit margin on post production services is achievable - this is currently being earnt

by a fragmented base of post production service providers

Editing solutions

Growth StrategyNon Creative Ancillary Services

14

Post Production

Accounting• Provides all aspects of traditional post production accounting for film and television

Revenue Collection • Contracted to manage cash flow from film distribution to agencies and rights holders

Sample Acquistion Opportunties

Post Production Services

Localisation

• Wide range of services provided after principal filming is complete

• Services include editorial, graphics, SFX, VFX, trailer, sound, music, color & formatting

• Specialised post production services including translation and dubbing of foreign languages for

international release, as well as content suitability to ensure acceptable cultural perception by the

target audience in each country or region

Development Phase Production PhaseDistribution &

Marketing

Pre Production Production Post ProductionCreative Phase Financial PhaseCollection

Accounts

Completion

Contracts

Revenue collection Accounting

Localisation

Sound design

VFX

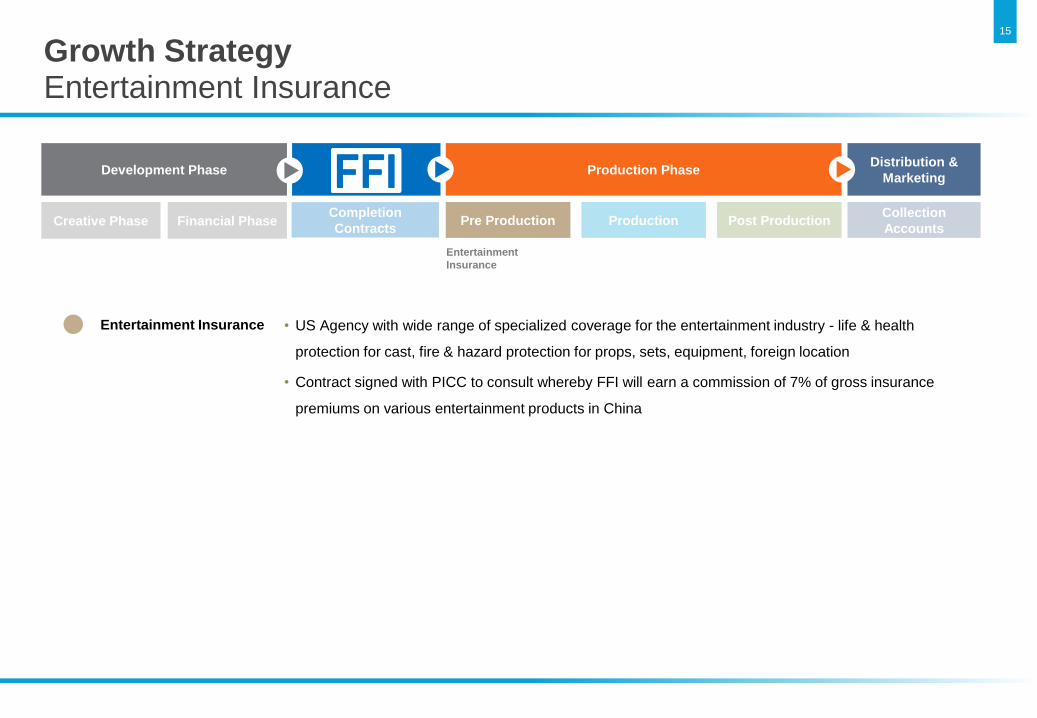

Growth StrategyEntertainment Insurance

15

Entertainment Insurance • US Agency with wide range of specialized coverage for the entertainment industry - life & health

protection for cast, fire & hazard protection for props, sets, equipment, foreign location

• Contract signed with PICC to consult whereby FFI will earn a commission of 7% of gross insurance

premiums on various entertainment products in China

Development Phase Production PhaseDistribution &

Marketing

Pre Production Production Post ProductionCreative Phase Financial PhaseCollection

Accounts

Completion

Contracts

Entertainment

Insurance

Growth StrategyStrategic, Low Risk, Content Acquisition

Pre-sold opportunities

• Of approximately 200 new projects per annum, FFI expects 5-6 opportunities where producers don’t have our high level

relationships

– Expect to deploy c. $5-6m per annum in acquiring such rights to distribute content

– FFI can purchase rights to distribute content with predetermined exits (but only where such rights to distribute content

will be sold at a profit)

• First project was Snowden that cost FFI $1m to buy certain territorial rights to distribute content

– The exploitation by a major studio of these rights is expected to deliver a return of approximately $2.0m over 15

months, commencing September 2017

IMAX Documentary

• In advanced discussions for a 5 film documentary deal to produce and exploit original content in conjunction with IMAX

– 1,215 IMAX theatres, 166 new theatres built in 2016, 150 in 2017

• Low risk distribution model can deliver relatively predictable, long term income streams

– IMAX theatre experience is primary driver for audience, where content typically has a far longer shelf-life than

traditional film

• FFI is backing the Pandas 3D documentary with IMAX

– Warner Brothers is co-financier and is handling the non-theatrical distribution rights

– Budget of $8.0m - the intention is that FFI will be entitled to approximately 21% of the net revenues of this film after

repayment of the production costs, and deduction of distribution fees and expenses

– Photography of movie complete and now in editing, anticipated release on schedule

16

• Core business of Completion Contracts

– Targeting a more diverse revenue mix by FY2018

• The core business provides foundation to leverage existing platform, management, operational expertise and client base

– Editing Solutions

– Post Production Accounting

– Revenue Collection

– Documentary partnerships

– Completion Contracts and ancillary services in China

• Insurance services and products

17

Growth Strategy Target Revenue Mix

Target Revenue Mix

FY17 FY18 FY19

Completion Contracts Equipment Rental

Content China & PICC

Collection & Accounting Other revenue

Source: Company Estimates

Summary & Conclusion

• Worldwide leader in Completion Contracts – leading market share

• Iconic status and unique privileged position in industry enables FFI to direct customers to

subsidiaries providing ancillary services

• High barriers to entry

• Scalable platform

• Significant growth opportunity in China

• Low risk / high growth business model

18

Disclaimers

This presentation has been prepared by FFI Holdings PLC (the “Company”). By receiving this presentation and/or attending the meeting where this presentation is made, or by reading the presentation slides, you agree to be bound by the following limitations.

In the United Kingdom, this presentation is directed only at (i) persons having professional experience in matters relating to investments who fall within the definition of "investment professionals" in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended from time to time) (the “Order”); (ii) high net worth bodies corporate, unincorporated associations, partnerships and trustees of high value trusts as described in Article 49(2)(a)-(d) of the Order; or (iii) persons to whom it would otherwise be lawful to distribute it (all such persons being “Relevant Persons”). Persons within the United Kingdom who receive this communication (other than Relevant Persons) should not rely on or act upon the contents of this presentation. Any investment or investment activity, or controlled investment or controlled activity to which this communication relates is available only to Relevant Persons and will be engaged in only with Relevant Persons. This presentation is not intended to be distributed or passed on to any other class of persons in the United Kingdom.

This presentation does not constitute or form part of any offer to sell or issue, or invitation to purchase or subscribe for, or any solicitation of any offer to purchase or subscribe for, any securities of the Company or any of its subsidiaries (together the “Group”) in any other entity, nor shall this document or any part of it, or the fact of its presentation, form the basis of, or be relied on in connection with, any contract or investment decision, nor does it constitute a recommendation regarding the securities of the Group. Past performance, including the price at which the Company’s securities have been bought or sold in the past and the past yield on the Group’s securities, cannot be relied on as a guide to future performance. Nothing herein should be construed as financial, legal, tax, accounting, actuarial or other specialist advice and persons needing advice should consult an independent financial adviser or independent legal counsel.

Any securities described herein have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”), or under the securities laws of any state or other jurisdiction of the United States and may not be offered or sold in or into the to the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. The Company does not intend to make any public offering of securities in the United States. The securities of the Company have not been approved by the US Securities and Exchange Commission, any state securities commission in the United States or any regulatory authority in the United States, nor have any of the foregoing authorities passed upon or endorsed the merits of any proposed offering of securities of the Company or the adequacy or accuracy of this presentation. Any representation to the contrary is a criminal offence in the United States.

Neither this presentation nor any information contained in this presentation should be transmitted into, distributed in or otherwise made available in whole or in part by the recipients of the presentation to any other person in the United States, Canada, Australia, Japan or any other jurisdiction which prohibits or restricts the same except in compliance with applicable securities laws. Recipients of this presentation are required to inform themselves of and comply with all restrictions or prohibitions in such jurisdictions.

No responsibility is accepted, and to the fullest extent permitted by law or regulation, no representation, undertaking, warranty or other assurance is made or given, in either case, expressly or impliedly, by the Group or any of their respective directors, officers, partners, employees, agents, affiliates, representatives or advisors (“Affiliates”) or any other person, as to the accuracy, fairness, reliability or completeness of the information contained herein or discussed verbally or as to the reasonableness of any assumptions on which any of the same is based or the use of any of the same. Accordingly, no such person will be liable for any direct, indirect or consequential loss or damage suffered by any person resulting from the use of the information contained herein, or for any opinions expressed by any such person, or any errors, omissions or misstatements made by any of them. No duty of care is owed or will be deemed to be owed to any person in relation to the presentation.

The information contained in this presentation has not been independently verified. This presentation does not purport to be all-inclusive or to contain all the information that a prospective investor in securities of the Group may desire or require in deciding whether or not to offer to purchase such securities.

The information in this presentation includes forward-looking statements, made in good faith, which are based on the Group’s or, as appropriate, the Group’s directors' current expectations and projections about future events. These forward-looking statements may be identified by the use of forward-looking terminology including, but not limited to, the terms "believes", "estimates", "plans", "projects", "anticipates", "expects", "intends", "may", "will" or "should" or, in each case, their negative or other variations or comparable terminology, or by discussion of the Group’s strategy, plans, operations, financial performance and condition, objectives, goals, future events or intentions. These forward-looking statements, as well as those included in any other material discussed at any analyst presentation, are subject to risks, uncertainties and assumptions about the Group and investments many of which are outside of the Group’s control, including, among other things, the development of its business, the trends in its operating industry, changing economic, financial, or other market conditions and future capital expenditures. In light of these risks, uncertainties and assumptions, the events or circumstances referred to in the forward-looking statements may differ materially from those indicated in these statements. Forward-looking statements may, and often do, materially differ from actual results. Thus, these forward-looking statements should be treated with caution and the recipients of the presentation should not place undue reliance on any forward-looking statements. None of the future projections, expectations, estimates or prospects or any other statements contained in this presentation should be taken as forecasts or promises nor should they be taken as implying any indication, assurance or guarantee that the assumptions on which such future projections, expectations, estimates or prospects have been prepared are correct or exhaustive or, in the case of the assumptions, fully stated in the presentation.

19

Disclaimers (continued)

The information and opinions contained in this presentation and any other material discussed verbally are provided as at the date of this presentation and are subject to verification, completion and

change without notice. The delivery of this presentation shall not give rise to any implication that there have been no changes to the information and opinions contained in this presentation since the time

specified. Subject to obligations under the AIM Rules for Companies published by the London Stock Exchange plc and the Market Abuse Regulation (Regulation 596/2014) (each as amended from time

to time), neither the Group nor any of its Affiliates, undertakes to publicly update or revise any such information or opinions, including without limitation, any forward-looking statement or any other

statements contained in this presentation, whether as a result of new information, future events or otherwise. In giving this presentation neither the Group nor any of its Affiliates, undertakes any obligation

to provide the recipient with access to any additional information or to update any additional information or to correct any inaccuracies in any such information which may become apparent.

Certain industry and market data contained in this presentation has been obtained from third party sources. Third party industry publications, studies and surveys generally state that the data contained

therein have been obtained from sources believed to be reliable, but that there is no guarantee of the accuracy or completeness of such data. While the Company believes that each of these publications,

studies or surveys has been prepared by a reputable source, the Company has not independently verified the data contained therein. In addition, certain of the industry, scientific and market data

contained in this presentation comes from the Company’s own internal case studies, research and estimates based on the knowledge and experience of the Company’s management in the market in

which it operates. While the Company believes that such research, estimates and results from its case studies are reasonable and reliable, they, and their underlying methodology and assumptions, have

not been verified by any independent source for accuracy or completeness unless otherwise stated and are subject to change without notice.

20