Embed Size (px)

Citation preview

8/9/2019 FEL Newsletter Sept 2009

http://slidepdf.com/reader/full/fel-newsletter-sept-2009 1/4

Equities anticipating recovery

UK Equity Market : FTSE All-Share Index since start of 2009

Source: Bloomberg

Issue 73 | September 2009

The Newsletter is now available via email.

If you wish to receive it in this format please contact

us at: [email protected]

8/9/2019 FEL Newsletter Sept 2009

http://slidepdf.com/reader/full/fel-newsletter-sept-2009 2/4

The UK market: a remarkable rise through the summer

Having started July in a positive mood, stock markets soon turned sharply lower as poor US employment numbers led

nervous investors to question hopes of an early robust recovery in the global economy. However, from thereon the

FTSE100 index has maintained a strong upward trend through July and August. The change in sentiment came as

investors chose to concentrate on strong corporate earnings from a number of major US companies, comment from

the Federal Reserve meeting that the economy had passed the trough of the recession and the outlook for the second

half of 2009 was improving, and China reported resurgent economic growth. A record eleven straight positive days

towards the end July left the FTSE100 index just below its early January high point of the year. Again the new month

started strongly as good corporate results, and positive manufacturing data from the US, eurozone and UK fuelled

optimism that the global economy really was poised for recovery. The UK stock market then entered a phase where it

struggled to make progress as the Bank of England left interest rates unchanged, but surprised investors by increasing

the quantitative easing programme – a reminder that the economic outlook remained uncertain. However world stock

markets surged again late in August as the Federal Reserve commented that prospects for a return to growth in the US

and elsewhere in the near term appear good, and while the FTSE100 index finshed the month just below its best level

for ten months (at over the 4900-level) the feeling in the market was that the combination of market fatigue, and profit

taking, could make significant progress from here difficult.

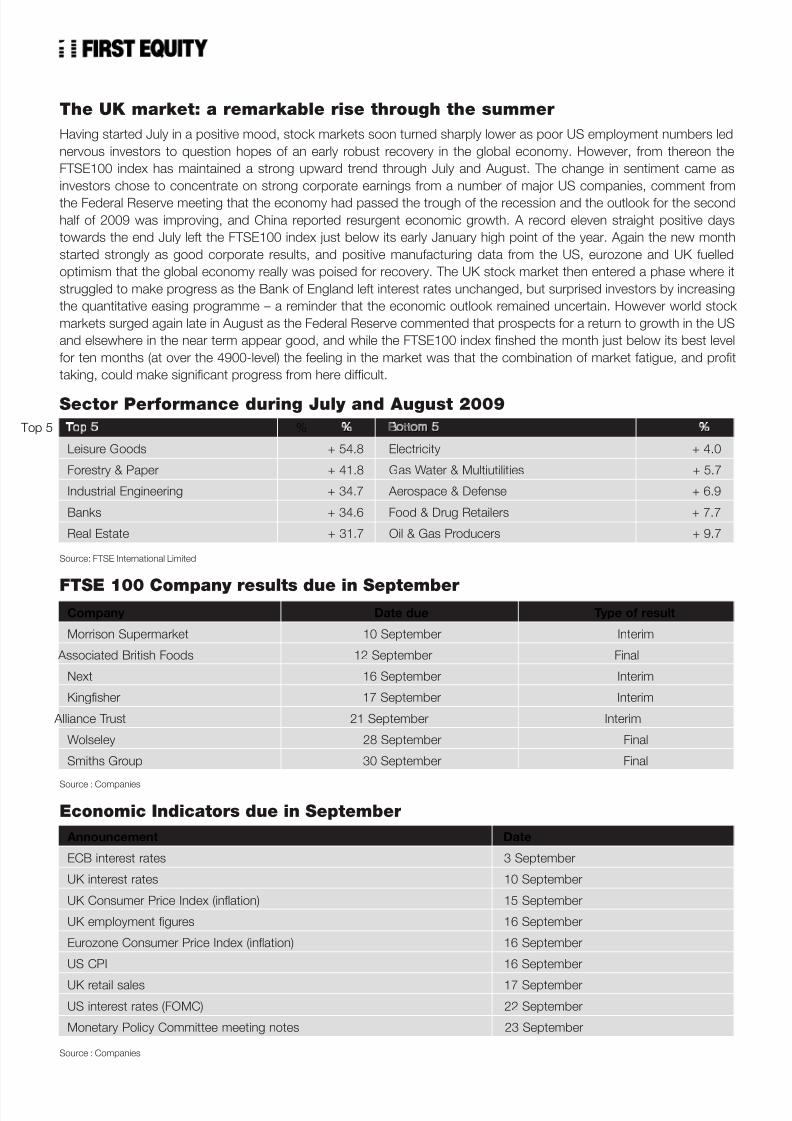

Sector Performance during July and August 2009

Source: FTSE International Limited

Top 5 % B ottom 5 %

Leisure Goods + 54.8 Electricity + 4.0

Forestry & Paper + 41.8 Gas Water & Multiutilities + 5.7

Industrial Engineering + 34.7 Aerospace & Defense + 6.9

Banks + 34.6 Food & Drug Retailers + 7.7

Real Estate + 31.7 Oil & Gas Producers + 9.7

Source : Companies

Economic Indicators due in September

Company Date due Type of result

Morrison Supermarket 10 September Interim

Associated British Foods 12 September Final

Next 16 September Interim

Kingfisher 17 September Interim

Alliance Trust 21 September Interim

Wolseley 28 September Final

Smiths Group 30 September Final

FTSE 100 Company results due in September

Source : Companies

Announcement Date

ECB interest rates 3 September

UK interest rates 10 September

UK Consumer Price Index (inflation) 15 September

UK employment figures 16 September

Eurozone Consumer Price Index (inflation) 16 September

US CPI 16 September

UK retail sales 17 September

US interest rates (FOMC) 22 September

Monetary Policy Committee meeting notes 23 September

8/9/2019 FEL Newsletter Sept 2009

http://slidepdf.com/reader/full/fel-newsletter-sept-2009 3/4

Improving economic outlook

While the tone of the Bank of England’s latest quarterly Inflation Report, published in early August, remained downbeat,

continuing that of the previous report released in May, as much of the world economy stayed in a deep recession and

its financial systems in a fragile condition, there are now more encouraging signs looking ahead. In the Bank’s view

financial market strains eased and bank funding conditions improved a little, due to the extensive global policy stimuli

packages. The Bank, therefore, remains cautious on the nascent recovery, as banks, in its view, continue to beundercapitalised, impairing their potential to lend, while companies and households may tend to save or cut debt rather

than spend, affecting recovery prospects. The Governor also said that the financial crisis might well be the worst ever,

rather than just the worst since the 1920s, with nominal spending contracting at a pace seen only twice since 1900.

Given this grim background the Bank was nervous of appearing to exaggerate any potential recovery. However, the

Bank did put forward a more robust forecast than in its May Report for UK economic growth over the remainder of this

year and into 2010, even though it warned that recovery was likely to be slow and protracted.

The recently announced revised estimate for UK GDP in the second quarter, a contraction of 0.7% (from an initial

estimate of 0.8%), due to a slightly smaller decline in manufacturing output, was nonetheless unexpectedly poor given

the raft of encouraging economic news in recent weeks. City economists had been forecasting a decline of around

0.3%. Other data confirmed the continued fall in consumer spending (-0.7% in the second quarter compared to –1.3%

in the first quarter) despite rising retail sales, and a significant fall in investment spending by businesses amid a shortageof credit. There was particular surprise over the 0.6% contraction of output in the UK’s service industry, which appeared

to contradict a recent CIPS/Markit purchasing managers index survey, regarded by economists and the Bank of England

as among the more reliable of leading indicators, that the sector had started to recover in May. The Office for National

Statistics makes the point that initial estimates of output are often less reliable, particularly when the economy is on the

turn. Following the disappointing growth figure, the announcement by the Monetary Policy Committee in early August

that it had voted to extend its so-called quantitative easing programme – buying government and corporate bonds in a

bid to increase the volume of cash in the economy – from £125bn to £175bn, surprised the markets and raised fresh

doubts about the strength of the economic recovery. The minutes of the meeting later revealed that the Governor had

actually wanted to increase the amount to £200bn, but was outvoted. (In contrast the Federal Reserve opted to slow

down its $300bn (£181bn) programme of government bond purchases, while commenting that economic activity is

levelling out). Behind the decision to increase quantitative easing was the recent poor GDP numbers, which hadthreatened to push inflation further below target. There was also the view among commentators that despite generally

encouraging economic news, it may have been done deliberately to keep Sterling low and thus help cement any

economic recovery. The Governor of the Bank of England also commented that although there are signs that credit

conditions may have started to ease, lending to business has fallen and spreads on bank loans remain elevated, as

banks tried to repair their balance sheets. This raises concerns over longer-term growth prospects at a time when the

outlook for the UK economy was unusually unclear.

The disappointing UK GDP figures came at the same time as the European Central Bank turned more optimistic oneconomic prospects in the eurozone and beyond, with the eurozone area seeing a second quarter GDP contraction of

just 0.1%, while both France and Germany reported that their economies had broken out of recession with growth of

0.3% - after four quarters of contraction. The figures were significantly better than expectations and followed

contractions in both countries of 1.3% and 3.5%, respectively, in the first quarter. With the French and German

Source: Bank of England

GDP projection based on market interest rateexpectations and £175 billion asset purchases

European GDP growth% change on previous quarter

Source: Thomson Reuters Datastream

Percentage increases in output on a year earlier

8/9/2019 FEL Newsletter Sept 2009

http://slidepdf.com/reader/full/fel-newsletter-sept-2009 4/4

economies accounting for around 48% of eurozone GDP, economists now expect the eurozone to return to growth in

the third quarter of 2009. The view is that this turnaround came from re-emerging export-led growth despite continued

destocking, while future GDP growth should benefit from restocking it could be held back by rising unemployment,

restrained bank lending and the withdrawal of fiscal stimulus packages.

While the US economy continued to shrink in the second quarter the pace of contraction slowed. GDP fell by 0.3%

quarter-on-quarter, and by 1% on an annualised rate. This compares to an annualised contraction of 6.4% in the first

quarter. The government estimates that the federal spending stimulus had probably added between 2% and 3% to GDP

growth over the period, while consumer spending (around two thirds of GDP) fell by a worst than expected 1.2%. This

reflects continued cutbacks in the face of rising unemployment (9.4% in July) and the still falling value of homes and

investments. Experts believe the US economy is levelling off and that it will return to growth by the end of 2009, although

the recovery is likely to be sluggish and protracted. The IMF is forecasting US GDP growth of 0.8% in 2010. The

Japanese economy also returned to growth (plus 0.9%) in the second quarter, after four quarters of steep declines,

substantially as a result of government stimulus packages, a sharp fall in imports and export growth. Nevertheless, most

experts remain highly cautious on the country’s economic outlook

The contraction in the UK economy over the last quarter of 2008, and particularly the first quarter in 2009 (a fall of 5.6%

over the previous twelve months, and 6% below the economy’s peak), was much steeper and deeper than the Bank had expected, with approaching half of that decline estimated to have been due to de-stocking. However, with the

significantly improved second quarter GDP figure the view, backed by a number of surveys, is that the trough in output

is near, or has indeed past. The outlook for the UK economy is much improved as it continues to respond to the

considerable stimulus from easing in monetary and fiscal policies, low interest rates, the past depreciation in Sterling,

an improving global economic environment and the Bank’s quantitative easing programme. A temporary boost to output

will also be felt as inventory adjustments run their course. Very considerable uncertainties remain, however, as to the

strength and timing of the recovery in economic activity. This is partly due to the continuing reluctance of banks to lend,

past falls in asset prices and high levels of public and private debt, all of which will restrain consumer and business

activity, while the durability of the recovery in global economic activity remains unclear.

The deeper than expected contraction in the first and second quarters of 2009 has resulted in the Bank revising its

central forecast for a fall in GDP for the current year to 4.4%, down from a decline of 3.9% - estimated in May’s InflationReport. Nevertheless, the improving outlook, boosted by the increased quantitative easing programme, has led the

Bank to revise up its central forecasts for UK GDP in 2010 to 1.8%, from 1.1% in May’s Report. Following the publication

of detailed data post the Inflation Report, growth figures have been extrapolated from the data by economists and show

that the Bank expects GDP growth of 0.2% and 0.4% in the third and fourth quarters of 2009, respectively, which would

seem to imply a smaller contraction over 2009 than that mentioned above. Furthermore, the Bank’s central forecast is

for strong growth of 2.2% (again higher) in 2010, although this is reduced to 1.3% taking into account downside risks

to growth. These figures compare to forecast growth of 1.75% from the Treasury and a consensus of City forecasts of

0.8%. Overall the Bank seems much more confident on forecasts for short-term growth despite continued uncertainty

not only over the UK economy’s recovery path, but also the strength of the global picture. Longer term the big picture

hasn’t changed as banks continue to restructure their balance sheets, consumers and companies face high levels of

debt, and job insecurity curtails spending, leading to doubts over the ability of the global economy to sustain the likely

short-term recovery in GDP growth.

First Equity Limited

Salisbury House, London Wall, London EC2M 5QQ

Tel: 020 7374 2212 Fax: 020 7374 2336

Website: www.firstequity.ltd.uk

Paul Henry

email: [email protected]

The information in the newsletter is taken from publicly available sources and the newsletter is distributed for information purposesonly. Whilst reasonable steps have been taken to ensure the fairness of any views expressed, First Equity Limited does not offer anyguarantee as to the accuracy or completeness of the information. The newsletter is not intended as a solicitation to buy or sell anysecurities or investments which may be mentioned. First Equity Limited is regulated and authorised by the Financial Services Authorityand is a member of the London Stock Exchange and the PLUS Market.