Embed Size (px)

Citation preview

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 1/41

Customer Service Strategy in High Street Banking System within

the UK (A Case Study on the METRO BANK, Holborn Branch,

UK)

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 2/41

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 3/41

Acknowledgement

This is Harun or Rashid. As a student London Churchill College, I done the research work in

order to complete my Bsc (Hons) degree awarded by Manchester Metropolitan University. In

this stage I would like to share my feelings and liked to thank my respective supervisor

S. SCOFFIELD, who always has been very helpful and generous to me and all other

classmates. I always motivated and encouraged by the high knowledge and enthusiasm of my

supervisor. In addition, I would also like to thank me college management team who chose an

excellent supervisor. It wouldn’t be possible without the co-operation of my respective

teachers and all other academics. I like to say a big thanks to you all for a huge contribution

on my academic life.

My research work is dedicated to my parents and other friends and family members, who

always helped me, encourage me and inspire me.

Thanks and Regards

Harun or Rashid

15th

January 2012

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 4/41

Abstract

This paper aims to focus on the strategic choices that have been made to serve customer by

bearing in mind the current competition in the industry and other environmental challenges.

This paper also looks for the core strategic issues that differentiate customer service of Metro

Bank from others retail banking in UK. This paper lead to focus on the organization’s

identical and differentiated strategy related to the Branch Service, Contract Centre Service

and Web Service. This study has been followed by the qualitative method and data collected

by semi structured interview from the responsible individuals of the bank who are responsible

for the desired service strategy and process. This paper shows that there are ten strategic

choices followed for the combination of the three broadly service sectors category (Branch

Service, Contract Centre Service and Web Service). The analysis of data leads to the

understanding of the maturity of the customer service strategy and concludes that the

strategies are quite equipped with the business aim and objectives. Despite of the fact, the

substantial recommendation was to follow the Live Chat technology, ‘Open Dialogue Call

Steering’ as an alternative to the tradition IVR system and an intensive emphasize on the

contact centre besides in branch customer services.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 5/41

Chapter One

Introduction

1.0 IntroductionThis study is designed to examine the different issues that are challenging to provide effective

customer service in retail banking system that means the high street bank in the UK. This

study also tries to examine the concepts those are central to minimize the challenges like

service quality, customer satisfaction and so on. The certain focus has been initiated certainly

on the changing patter of the business environment and global market that demands the

updated and more customer centric service matching the changed situation. In doing so, the

focus has been taken in the retail banking industry of Metro Bank in the UK. More

specifically, the focus was on the Holborn Branch of Metro Bank to conduct primary

research.

The current competitive market demands for an in-depth strategy to deal with customers and

provide best service over competitors to boast the company. Customer satisfaction, quality in

service, global issue and different alternative of choice to get desired service, customer taste

and trustworthy towards company all affect the retail banking (Appiah-Adu, 1999; Bull,

2003). One of the most important facts to note that European market has been struck by the

economic recession, that also demands for new strategy to grabs customers and provide

newer tools to marketing that demand for a well adopted customer service strategy that is

suited to Metro Bank for retail banking.

Metro Bank, currently with only ten branches, is the high street bank in England over

hundred years. The strategy of bank is unique as it has customer focused retail business. This

bank reinvented the system of retail banking. It makes each and every attempt to get rid of all

dim bank rules from day to day services to provide easier and further suitable banking to

customer as it is providing traditional or typical face to face service (Jervis, 2010). This bank

address the dialogue ‘‘no stupid bank rules’’. This exemplifies the strategy to provide

customer service with an alternative way. It means the bank avoid one rule to all where

computer says no approach. The branch manager has the self-reliance to make decision over

the computer system. This system differentiates customer service strategy from other service

provider in retail banking (Jervis, 2010). In this circumstance, the focus on the challenges and

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 6/41

strategy to customer service is very central to this study. Most of the organizations are

fascinated in examining, assessing and implementing tools and techniques that aim at getting

better result in customer maintenance and maximizing share of customers rather than

focusing on the challenging issues that hinder to provide better customer service. There may

have an excellent arsenal of customer service provider are available in the organization but

the poor strategic choice may limit the access to provide better service. Hence, the focus on

the improvement of the strategic issue of the customer service is really necessity to be

searched.

1.1 Background of the Study

As the strategy is very central to serve customers properly in the retail banking system, it is

significant to focus on strategy related to customer service. Many studies have been

formulated to identify the different issues and concept that are initiated to foster the customer

service, to make the relationship better in the retail banking but the focus on the strategies

that is central is required to focus especially in the period of economic recession.

This bank has a little sales message overall. This bank has three promotional strategies to

serve their customer are like “Metro Bank Promise”, “Reasons To Switch”, “New Account

Gifts” are the most display leaflets of the bank. The apparent dependence on employees to

deliver messages and offer the explanation for the relationship is refreshing. Those are

generally core to any bank’s strategy. While the other bank has a dependency to make

decision to system software and the lack of autonomy of the managers to make decision,

Metro Bank has the opposite issue to operate their retail banking. There is a big question to

rise that is their refocus on traditional ways and humanising of the banking relationship

sufficient to maintain a revolution for high street banking? This point view provides a clear

scope to study the challenges of customer service strategy and look for further issues that will

strengthen the strategy to refocus on the customer service. The way of de-centralisation of

authority along with rigidity to the rules at a time perhaps stimulates revolution. Jervis (2010)

argued that the overall process that is claimed in poster may be hampered as a lack of

enthusiastic energy of them. He also pointed out that the products are offered very simply in

their website but have a very strong functional language though formal by saying “No stupid

bank rules”. Now it is really necessary to investigate how the strategy for product and service

to customer are more consumer-centric and how it likely benefits the customer going beyond

the usual banking constraint.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 7/41

But, the usual way of switching to this bank may work if the strategies to serve the customer

and grabs the customer through strategic way that is ‘viable alternative’. Hence, the focus on

the strategic issue to customer service than the procedure to accomplish the task is very

important. It is significant what will the bank do to attract their customer and serve alternativeway form others is issue to study for further development.

It is tough to develop retail banking organically as a result of slow industry growth and

competition. Most of the banks have trouble to meet the expected performance as a result of

distressing antagonism from both conventional brick and mortar operations and rising

Internet banking. There is a sort of difficulty to differentiate business and to reach to the

customers with new sales opportunity. Those retail banks will meet the challenges

successfully to compete will flourish in future. So, in this circumstance, this study scrutinizes

the strategic issues of the customer service process in retail banking. This paper also makes a

scope to understand the procedure of delivering service which will increase revenue and will

be cost effective to lead profitability by maintaining shareholder value. Some have argued

(Dall, & Bailine, A. 2004; Solomon, 2010) that the excellence and intensity of customer

service has diminished in recent years as a result of not focusing on the strategic issues to

deliver customer service. A verity of methods has been employed to overcome this situation

rather than focusing on the strategy. This paper is critically focuses on the strategic issues to

customer service.

Retail banks countenance a cut-throat setting and put a main concern on customer

responsiveness and maintenance. Unsuccessful and effective less communication is the cause

of customer disappointment and customer slow destruction. Retail banks’ main goals are

developing customer satisfaction, increasing profitability and maintaining expenses,

increasing service efficiency and so on. Among all these obstacles one of the obstacle is

related to customer service strategy and procedure. To deliver effective service the setting of

the strategy and the decision of utilizing certain channel to provide service and how the

channel will be utilized that means service will be provided is very central to the strategy

process of customer service. Hence, it is significant to make a detail study on the customer

service strategy in retail banking. It is also most significant for the Metro Bank as it is

focusing on to provide decision making service in the bank branch.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 8/41

1.2 Research Question

This study has been concerned to investigate the certain question that is as follows:

What are the current challenges are faceding by organization like Metro Bank in relation to

customer service strategy for the retail banking?

What are the strategic changes related to customer service should be accounted to be more

effective in the field of retail banking by Metro Bank? This does not make sense

1.3 Aim and Objectives

The aim of this study is to critically discuss the current customer service strategies to

recommend for the further customer service strategies depending on the nature of the current

challenging issues of customer service for the betterment of retail banking of Metro Bank.

Objectives: The following objectives have been formulated to fulfil the desired aim of the

study.

To analyse the current literature on the different issues like customer service, quality,

satisfaction, local and global issues, changes in technology etc. that are challenges and have

been accounted in formulating strategy in relation to retail banking customer service.

To examine the current customer service strategy that has been adopted by Metro Bank in its

retail banking.

To scrutinize the different issues to recommend for Metro Bank in developing the current

strategy to be more customer and profit oriented in retail banking.

1.4 Chapter Review

The study has been formulated by following five chapters. Chapter One is the introduction

of the topic that is going to be searched and central to the study notions like introducing the

background of the research, significance, purpose and scope, research question, aim and

objectives of the research.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 9/41

Chapter Two has been focused on the current literature contend that is the theories, model,

ideas, notions and issues that are challenging to the customer service issue and strategy in

special to retail banking.

Chapter Three is the critical analysis of the way of conducting the study. The study has been

conducted through in-depth interview which is the main strength to collect the focused

primary data. There is also focus on the secondary data from the bank annual report, press

release on the certain issue in the recent past that lead to t he substantial analysis of the data.

Chapter Four is the central part of the study as it is the analysis of the obtained data. This

chapter illuminated the different challenges and the focused issue that are central to concern

to formulate strategy to serve the customer in the changed situation of the current economic

situation. This chapter mainly concentrate on the findings of the study that is the core to make

a valuable recommendation. This paper introduces 10 critical strategies to focus on the

customer service for the Metro Bank. Those are highlighted as facilitating incorporated and

unfaltering exchanges across all channels, serving by decreasing the volume of call,

integrating self-service with agent assistance, handling calls brilliantly, initiating proactive

contact, using customer data and segmentation effectively, serving through inbound

marketing strategy, establishing customer intimacy through controlled demographic profile,

creating an appealing team effort with contact centre and blending interaction to increase

productivity of agents.

Chapter Five is the recommendation and conclusion of the study. This chapter recommend

for the further study. This study has been recommended to follow the certain strategy to be

more customers oriented and profitable. The study recommends using the live chat

technology in real banking and using open dialogue call steering to save costs and serve

better.

Conclusion

The further chapters are going to carry out the respective parts of the research that has been

stated in the sub-point of ‘Chapter Review’ earlier by focusing the aim and objective of this

study.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 10/41

Chapter Two

Literature Review

2.0 Introduction

In this chapter, the current concept, ideas, notion, model and theories related to the challenges

to customer service and theoretical strategy to customer service, particularly in relation to

retail banking has been analysed. This chapter commence to critically describe the issues like

retail banking and its product, customer service and the challenges that make us to focus on

strategic issues to formulate the way of dealing with customer in the current economic state.

2.1 Retail Banking and Its Product

Retail banks are known as the serving product to the general public (Croxford, et al., 2005)

rather than to the corporate and other banks (Pond, 2007). The different retail banks

systematize their functioning units in various ways. Retail bank in the UK is recognized as

the ‘‘high street’’ bank with a physical emergence in city and metropolitan area in the UK.

The utilization of phone banking and internet banking provides a scope to develop or extent

the retail banking definition by adding these two features to the retail banking to serve

customers (Caruana, 2002). Small retail banks also have a focus on the cost cutting approach

by not following the phone baking. This provides a savings as the cost of outsourcing activity

like maintaining database, call centres and other activity (Caruana, 2002; Kaplan and Norton,

2001). The retail banking services are current account, deposit account, individual savings

account (ISA), term savings that are termed as savings product. On the other hand, loan

products are mortgage loan, personal loan, credit card/ revolving credit and overdraft

(Charles, & Gareh, 2009). Key protection products in retail banking are life insurance,

health insurance, and general insurance. The major investment products are endowment

assurance, stocks and shares, unit and investment trust, pension etc. The other products are

foreign exchange, money transmission, safe custody and wills and trustee services (Charles,

& Gareh, 2009).

2.2 Customer Service and Its Focus

Customer service, of course, is very vital and core to the organizational activity and it is very

much true for the service sector like retail banking. So, before providing service, the main

issue is to formulate the strategy what will be done to focus on the customer and how the

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 11/41

service will be provided. Customer service is the specification of service to customers

previous to, throughout and after a purchase (Charles, & Gareh, 2009; Jones, and Suh, 2000).

Turban et al. (2002) describes customer service is a succession of performance intended to

improve the intensity of customer satisfaction – that is, the sentiment that an item for

consumption or service has congregate the customer anticipation. It can be used as a

framework to look various aspects of business, including retail banking, like portrait andappearance of the business, advertising of services, solving customer inconvenience,

managing better relationship with customer etc (Jones, and Suh, 2000). Customer service,

from that perspective, service has to be incorporated as element of a holistic approach to

methodical and systematic development.

2.3 The Key Challenges Facing Retail Banking

There are various factors that have been identified in the study as challenging issue that put

pressure for searching various strategies to attract customer. The challenges that remain in thearea of strategic issues in the customer service arena are as follows:

2.3.1 Increased Competition Lowers Profit Margin

It is becoming difficult to achieve growth in retail banking. Mortgage and deposit returns are

diminishing industry-wide and credit card development is lethargic (Hart and Sacasa, 2009,

Hormozi and Giles 2004, Jones and Farquhar 2003, Jones and Suh 2000). The increasingly

withdrawal of share of the marketplace is splitting more than ever. This provides a scope of

competition. This competition makes every organization, including retailing banking, to think

about new and comprehensive strategy for the customer service.

Non banking organizations like Wal-Mart, Tesco and Sainsbury’s are offering different

traditional banking service through creating banking centre in their stores that brings up and

open the competition in price and strategy (Jones and Farquhar 2003, Jones and Suh 2000).

This process of serving a segment of customer who was depending on the bank has been

transformed. On the other hand, customers are looking for cost effectiveness and various

facilities. This situation is very much challenging for the retail banking and demands for new

customer service strategy.

There is also the presence of other non traditional competitors like internet banks in the

industry which is threat and alternative way against in some sort of retail banking. This

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 12/41

system has leveraged low, cost effective and offered fee structure is very attractive and

advantageous to customers (Hart and Sacasa, 2009). The offer of wider range of lending

product with lower price makes a problematic issue for the retail banks. This, therefore,

makes a competition for retail banks to look for strategy in the process of retaining and

attracting customer and provide the excellence service.

2.3.2 Customer Service Drives Customer Loyalty in Banking

Most of the banking products are undifferentiated commodities. It has been observed that

retail banks are frequently following techniques to place themselves separately from the

competition to assist them succeed and grasp customers and to get better the establishment

(McDonald and Keasey 2002; Potgieter and Roodt 2004). All banks are generally identical

to consumers and they select product based on the best cost effective price evidence?. Retail

banks can distinguish themselves from others by optimizing their customer service. A study

by Genesys (2011) of 19 retail banks has revealed that the customer service is the main

determined factor of customer loyalty. Customer service is the most important factor to

decide to continue with a company. In this circumstance, retail banks are following a

strategy to execute and optimize an augmented customer contact centre which will help to

develop a distinguishing approach to take advantage over competitor.

2.3.3. Challenges in Utilizing Various Distribution Channels for Selling

One of the challenges has been identified as the instability of the customer to continue with

their current banking as a poor result of customer service. This is not about the problem of

employee that means the certain employee has not provided any facilities; it is about the

problems that come from strategic issues (Lewis and Soureli 2006; Lindlof and Taylor 2002;

Liu and Wu 2007). It is about poor strategic configuration of customer service and

insufficiency to grasp new technique to provide service. This is also associated with the issue

of cross- selling and up-selling efforts.

A. T. Kearney (2005) provides a special financial report about the attitude of the customers to

use their financial institution. It has been identified that most of the customers are using one

or two accounts with their most important monetary organization. About 50% customers are

like to enhance value to their existing equity account. This is a direct result of using such

channels that is alternative to the day-to-day banking and walk-in centre services.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 13/41

Another study of forty one retail banks on the utility of different channels while choosing

customer service worldwide has been revealed by Capgemini (2008). In this issue, it has been

identified that 58% of banking transaction was carried out by remote channels like ATMs,

Websites and Call centres. It also identified that the service of remote channels has been

diminishing and banks are relatively disappointed with the current performance. This study

also reveals that 14% sales were closed through those channels in 2008.

Another report by Genesys (2011) on the media of distribution of services and sales through

those media has been outlined. This study has been provided a contrast of five years gap from

2000 to 2005 and 2010. It has been identified, in 2000, that 70% service has been provided

through branch and sales was distributed through that channel in that year is 94%. On the

other hand, services in branch has been provided in 2010 on the branch is 30% and sales

through this channel is 67%. So, the retail banking sector has emphasized the other sources

than the dependency to the branches as the technological up gradation and availability of

other sources to serve customer are the current pattern of providing service channels in the

globalized era. Utilization of web to provide service has been increased 4% in 2000 to 28% in

2010 while in 2005 it was 18%. So, there is a substantial shift to the utilization of that

channel. In relation to utilization of this channel the sales has been conducted 2% in 2000 to

17% in 2010 while the sale in 2005 was only 5%. The similar conclusion can be drawn for

the channel of call centre or phone. In 2000 the utilization of phone to provide service was

only 5% where it emerged and raised 12% in 2010 and was 9% in 2005. Sales through this

channel were completed only 4%, 8% and 13% respectively for the year 2000, 2005 and

2010.

One of the limitations of the Genesys (2011) study may be focusing on the utilization of

remote channels as the media of customer service providing rather than the service in the

branch centre. This organization is a telecommunication organization so its focus on up

grading remote channels is very much emphasized. However, their study is very much

significant in the sense that the change in the service system has been occurred in the recent

past and emphasize on the remote channels are very much influential to the business. Now, it

is a challenge for retail banking to utilization of different channels to provide service and how

those channels will provide service is a strategic issue to set to customer service pattern for

retail banking.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 14/41

The way of utilizing remote channels to provide service is questionable strategy as a Forrester

Consulting (2007) study revealed that it minimize the visit of branches and being convinced

through direct interaction has gone lower by profitable client segments. This limits cross- sell

and up-sell opportunity with these customers. This study also disclose that the though the

closing stage of selling procedure happen in branch, customers like to find initial information

and like to do comparison via remote channels mostly by Web. Forrester Study found that

mortgage customers like to use a mix of sales channels. Customers like to research and

compare rate and fee in online before applying. This hampers as the bank has no opportunity

to make available further relevant information or advisory assistance. There is no face to face

interaction to convince the customer in their decision making process.

Several study (Lewis and Soureli 2006; McDonald and Keasey 2002; Habryn, Blau, Satzger

and Kölmel 2010; Creswell & Miller, 2000) discloses the challenges regarding formulation of

strategy is related to the problems of setting insufficient service regardless whatever the

channel- branch, ATM, Web or phone, is chosen by the customers.

There is also lacking of available individual who will handle complex issues related to

customer service and others. Banks always have insufficiency in expert employee in each

branch when there is a necessity to provide complex service (Creswell & Miller, 2000). This

is not a problem that is insufficiency in the service providing issue; it is about the

insufficiency in the strategy to handle this issue critically (Lewis and Soureli 2006). This

facts lead to the dissatisfaction among the customers.

The strategic gap also related in the issue of supporting banking activity during peak banking

hour. Drops in Service level over telephone and on Web is also one issue to focus on for

better service. Strategy is required to develop such issues.

2.3.4 Difficulty in the Agent Efficiency

Several studies (Lindlof and Taylor 2002; Liu and Wu 2007; Grigoroudis, Politis, Siskos,

2002; Charles & Gareh 2009; Cooper, 2008) has been identified that the focus on the

strategic issues in various sector as the most of the success of the retail banking depends on

the branch staff during the finalization of service and on the call centre and other channels

like Web. Study by Genesys (2011) has outlined that the common staff attrition rate in the

retail banking industry are 26% for branch employee and 33% for call centre employee. The

situation may be worsened by the entry-level employee in the call centre who may have the

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 15/41

cause for over 70%. Outbound selling staff may enlarge the situation more problematic. It has

been outlined that the retail banking products are generally more complex in nature and

required to be handled by highly-skilled, expensive agents so focus on the effectual sales

presentation and service. To make branch agent more effective many branches have been

focused on reallocation of routine of branch calls.

2.3.5 Upgrading Agent Performance by Strategic Combination

Several study (Habryn, Blau, Satzger and Kölmel 2010; Potgieter and Roodt 2004; Cooper,

2008) focus on the Strategic role of the contact centre in retail banking to be more effective in

the formulation of customer service strategy. It has been argued that the usefulness of

interaction channels are not broadly focused and the fallacy in the integration of different

channels. Strategic problems are prevalent in executing the company as whole such as

creating and focusing a great customer experience, growing performance and contentment of

agents and more up selling and cross selling products and service.

2.3.6 Theoretical Initiative Offered to Upgrade the Customer Service Strategy in Retail

Banking

Many scholars (Habryn, Blau, Satzger and Kölmel 2010; Grigoroudis, Politis, Siskos, 2002)

and organization like (Essvale Corporation Limited 2007; Forrester Consulting 2007) offer a

mix of different strategy for the retail banking customer service depending the challenged

that the organization faced.

Most of the study focuses on the global survey as a method to conclude their study. Their

study is one kind of generalization may not fit for others. Despite of this, their valuable

notification help us to understand various mix of the assortment in the theoretical assumption.

It has been argued that generating further Web site sale with online alliance with specialist is

one of the main issues to be considered for the retail banking (Jones, and Suh, 2000). Many

are in favour of the strategic importance to ensure customer satisfaction by reducing delays in

customer response time (Charles, & Gareh, 2009; Jones, and Suh, 2000; Turban et al. 2002).

It also focused to the improvement of collaboration with different partners to do the work

accomplished with in the specific period of time (Hart and Sacasa, 2009, Hormozi and Giles

2004). Some also argued to develop strategy to serve customer that not only improve the

customer service strategy but also focus on the brand image development such as offering

digital merchandising at branches (Jones and Farquhar 2003, Jones and Suh 2000). It also

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 16/41

favoured to increase immediate expert support to the customers to increase sales. More

effective branch communication is one strategic issue that must be considered in the retail

banking. It is one of the core ideas to deliver the final service that will influence the customer

to get the desired product. Strategic issues to reduce cost of training by Web/video

conferencing. This also will be helpful to get the certain decision that is urgent and need to

talk with higher authority. E- Learning training is also necessity to focus while developing

strategy to serve better. Staff sharing with call centre team also effective to serve better as

this sharing provides a way to mutualisation in workplace.

2.4 Conclusion

It has been identified that the various factors affecting the strategic choice for providing

customer service. Technological issue, globalization, and competitiveness in the market

hence quality, management, maintaining service channels etc. comes as a point to focus to

make a better and competitive strategy regarding to customer service. The following chapters

are going to focus on what are the strategic choices has been made to cover all these threats

by metro bank has been analysed. To what extent have the research questions been answered?

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 17/41

Chapter Three

Methodology

3.0 Introduction

This chapter has discussed about the way of carrying out the research process to get the

substantial aim and objective of the research. Methodology for this research has been

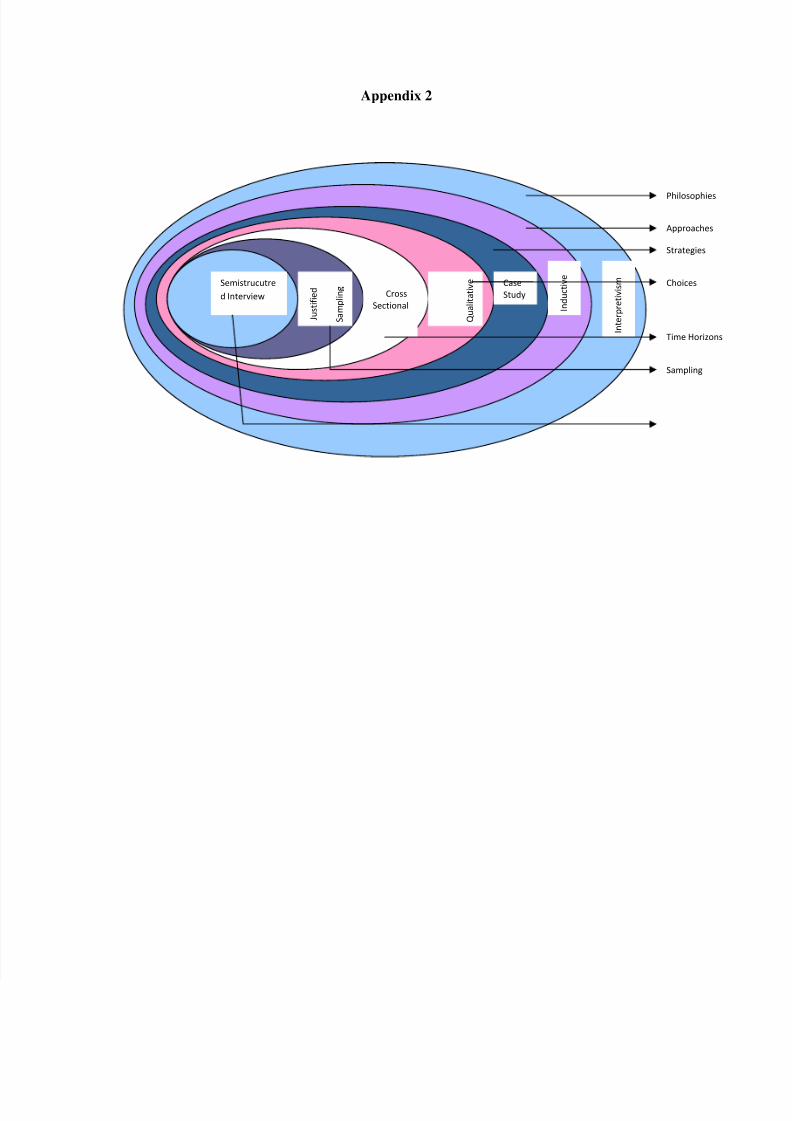

followed by the most quoted research Onion Model (Appendix 2) of Saunders, et al. (2009).

This chapter stands for discussion on the philosophical stance of the researcher to the way of

collecting data, research approach, research strategy, research methods, tools and techniques

and so on. This chapter also summarize the research validity and generalisability.

3.1 Research Philosophy

It is widely known that each of the philosophical stances has its own point of view to search

any topic and the main succession of any research lies on the right choice of philosophical

view which will cover the study and match with the issue. Research philosophy is the world

view of the researcher about what constitute the belief system of the researcher (Saunders, et

al. 2009). This view guides the way of investigation. Varied research philosophy view has

difference stance on ontology, epistemology, axiology and data collection techniques issues

apart from one philosophy to another. Strategic issue especially on the customer service

provides a critical scope to understand the outer environment, customers’ behaviour or

psychology and others inter related issues. In this circumstance, a subjective understanding

and regulatory perspective (Saunders, et al. 2009) makes a scope to understand the

researched topic form the interpretive perspective. This approach is widely used in various

research traditions (Gephart, 2004) because this view tries to focus on ‘authentic production’

of the meaning and positive to reach to the actual context. This approach is fundamentalism

on the complication of individual sense making as the appeared circumstances apart from

predefining variables (Denzin & Lincoln, 2003). Strategy must be operated for the betterment

of customer service so the meaning of different strategic issue of customer service must be

accepted by the customers. Customer view about the service depends on their interpretation,

and the difficulty they face to get the service. Hence, customers view and choice are varied

and their view must be granted in strategic issues. The management should have the vision of

transcribing customers view and tries to formulate strategy. This activity depends on the

getting closer to the meaning of the different strategy and how it will work from different

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 18/41

perspective cross and diagonally tested. Thus, the philosophical stance is very much

interpretive for this research.

3.2 Research Approach

The research approach is the clue whether a theory is functional clearly in study plan

(Saunders, et al. 2009). Check syntax Kalof (2008) outlined that what theory is going to

follow in the study as research approach. This approach has two views, inductive and the

other one is deductive.

If any study is going to generating new theory based on collected data will be inductive

approach and if the research is going to be completed by following any particular theory is

called as deductive approach. refs Sometimes, it has been identified that various study have

been conducted by the combination both approaches. The current study wasn’t formulated

based on or following any theory as a starting point. This research tried to generate the view

of management on strategic issues and later on conclude by gathering primary data. Hence,

the nature of this study is mainly inductive. This study also wasn’t concern with

generalization that is inductive in nature. The study conducted by following in-depth

interview of the researcher to gain primary data and lead the study. A close understanding of

the research context was the central issue which is inductive approach.

3.3 Research Strategy: Case Study

Case study method is very suitable for where the multiple sources of evidence are out here

and factual circumstances are available in the contemporary phenomenon (Robson, 2002; Yin,

2003). To gain an in-depth understating of any researched topic, the case study is preferable

as the certain case provides certain background for the certain topic which may not be

matched in other case (Saunders et al, 2009). This method endows with the answer of the questions

like ‘what’, ‘why’ and ‘how’ of the studied issue and it mostly tries to cover descriptive, exploratory

and explanatory and predictive study (Saunders et al, 2009). This study has been formulated based on

single case study of Metro Bank, Holborn Branch to investigate the customer service strategies for

retail banking. The substantial answer for what are the challenges are kept in mind while formulating

strategy is considered to answer by case study, what strategy taken and why taken certain strategy

over other is a issue of investigated through case study strategy. To minimize the case study strategy

limitations, biasness a careful review of drafts has been done by academic research supervisor.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 19/41

3.4 Choice of Methods

Study has been conducted generally by the way of collection techniques and analysis

procedure. This research followed qualitative study by following the assortment of in-depth

face to face semi-structured interview. Interview of the branch manager, HR manager,

senior employee of customer service provider, senior technician have been taken about the

strategic option that has been following currently to serve customer and further the strategy

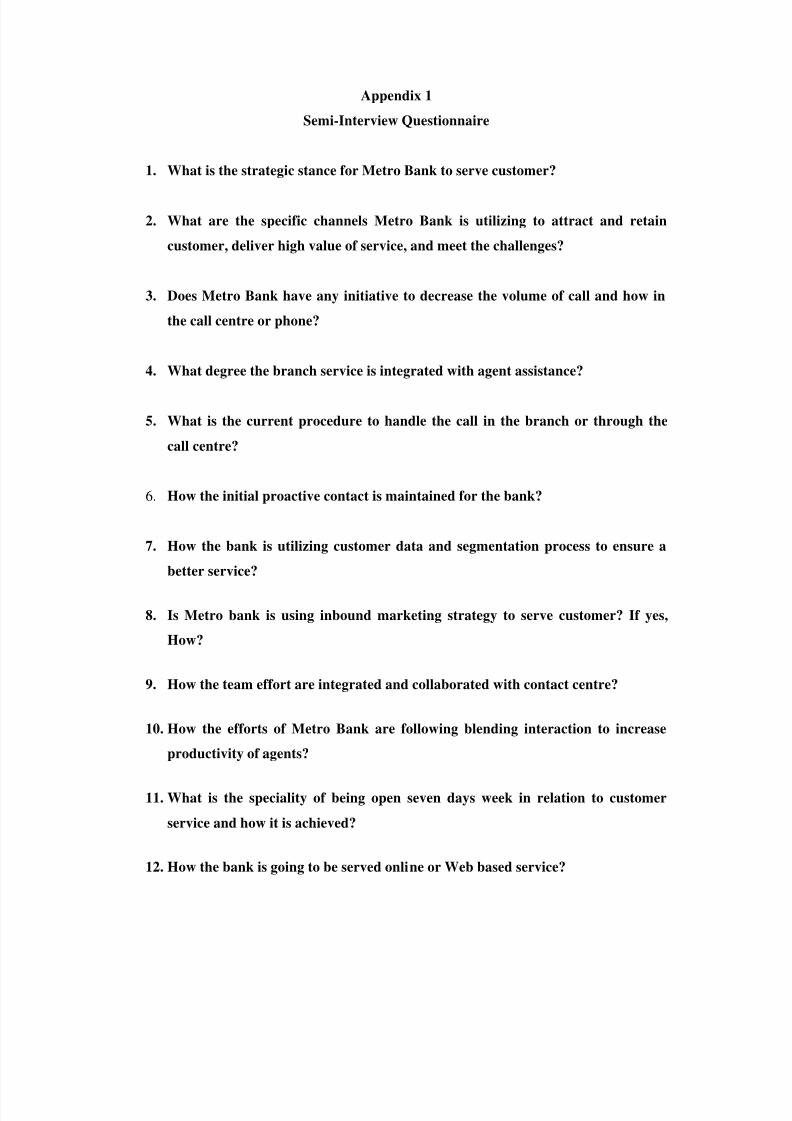

that is under process to follow near future. A set of semi interview questionnaire developed to

interview the selected individual for the study were considered to gather data. An

epidemiological critical analysis has been followed to reveal the strategy related to customer

service and the questionnaire distributed to those people are related to the implementation of

certain strategic issue related to the customer service. Moreover, different documents, annual

reports, press release about the strategic issues of customer service and about the service of

Metro Bank and other related materials i.e. books, academic journals and article sources have

been analysed to make a conclusion of the study.

3.4.1 Semi Structured Interview

A semi-structured interview is a research method generally used to collect data through a

formalized, limited set questions, which is flexible and allow new questions to be brought up

during the interview by following what the interviewee says (Lindlof and Taylor, 2002).

Semi-structured interview was conducted among the employee who are engaged in different

sector of customer service like in call centre, branch centre staff and Web design related staff

and manager of the branch and HR manager of the branch. The staff of these sector are

mostly related to the customer service and hence the valuable and authentic to make them a

part of this research. Interview questionnaire was set by analysing the content of the

literature. It was bear in mind to develop the questionnaire. The strategic issue, like training

and development, customer dealings, answering time of the phone, the important issue of the

Web design and others was entitled in the interview questionnaire. The in-depth interview is

very suitable to investigate and comprehend opinion, behaviour and attribute (Saunders et al.,

2009). To build and endow with sufficient reporting of the analytical questions a cautious

account was taken through the literature review (Copper and Schindler, 2008). Moreover,

supervisor scrutinized the content of semi structured interview to evaluate of the essentiality,

usefulness and appropriateness of the content. As this study is predictive in nature for further

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 20/41

recommendation, the predictive validity of the content of the semi structured interview also

included. What are the future strategy are going to taken by this bank and call centre, web

design and what issues will be the further threat for the valued customer service are led

through the predictive validity. Moreover, semi structured interview questionnaire followed

the robustness to construct reliable findings at diverse period beneath diverse circumstances

(Saunders et al., 2009). Interview validity was assessed by comparing different answers of

the staff and employees on certain issue. An audio record of the data was taken as the

researcher’s first language is not English. Later on, it was transcribed and during transcribed

it was focused to maintain the meaning of the different word that must meet lexical, idiomatic

and experiential meaning and grammar and syntax. refs

3.5 Time Horizon

Time horizon says about the optimal time for the conducting of the research. Each study has

to main time constrained and can’t be repeated. Study can be carried out for short period of

time which is called cross-sectional and it can be longitudinal which also stated as ‘diary

perspective’ (Saunders et al, 2009). This study is academic purpose and time bound that’s

why the nature of this research is persuaded by cross-sectional approach. Since this study is

conducted by focus on a particular phenomenon at a particular time in lieu of focusing on the

change and development for a long period of time, this study is cross sectional.

3.6 Sampling – need theory and refs

Four individual of four different areas of customer service were included in the study to

conduct semi-structure interview. Sampling was used to gather primary data from the huge

number of study population. Metro Bank has substantial number of employee. By using

judgemental sampling the branch manager and the HR manager who are must responsible for

customer service issues of the branch were included in the study. There were several

employees who are related to receiving phone and maintaining to receive customer calls.

Senior of staff related to this service was taken for the interview. Moreover, the senior

technician who is responsible to maintain IT sector and maintaining Web service was

included in the interview process. So, using judgemental sampling the four responsible

individuals have been selected for the semi structure interview and data were collected.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 21/41

Table 1: A list of Sampling

Interview Individual Population Sampling

Branch Manager 1 1

HR Manager 1 1

Most Senior Customer Service Employee 1 1

Head technician for Web maintaining 1 1

Total 4 4

3.7 Credibility of Research Findings

Credibility of research findings is usually related to reducing the probability of reaching

erroneous respond (Saunders et al., 2009). In this point, reliability and validity are the most

significant part of research issue and hence necessity to be examined. Generalisability that is

external validity and says on the interpretation of data and development of conclusion should

be in a very rational and noteworthy approach to lead to the superior credibility for any

research (Saunders et al., 2009). The analysis of the above issue has been described below.

3.7.1 Reliability

Reliability linked to the producing reliable, truthful and dependable findings on the basis of

data collection techniques and data analysis methods (Easterby-Smith et al., 2008). It

provides the way of cultivating the procedure that lead the study not to generate leaps and

false assumption (Robson, 2002). Robson (2002) also identified four types of threats for

validity those are participant error, subject or participant bias, observer error and observer

bias. So, it is clear that the reliability of the data depend on the trustworthiness in data obtain

process and data analysis process. Report build up is one of the concerns before collecting

data for the quality full research. Prior to starting point the pilot survey was conducted to

make sure that the backup from the bank branch is possible or not. The point is that before

starting my research, researcher went to talk the authority. As research hasn’t start, the

authority may respond negatively. After getting the assurance from the branch manager, the

research was started. As the organization has provided a full authentic and enthusiastic

support, the assurance of getting reliable data was maintained. An analysis of the study topic

prior to the research to the management has provided an intimacy to the study. Moreover,

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 22/41

prior to starting research the usual conversation about the background of the researcher,

country of origin and global and international issue lessen the gap between the researcher and

the interview personal. The main effective issue was that the employees have the high

academic background makes the issue very normal and favourable to researcher. The

education level of the interview person was a helpful point as they caught the research issue

depth and content. The analysis of the research aim, objective, and the purpose of the use of

data and the confidentiality of the research was very helpful to make a place to the interview

person.

3.7.2 Validity

It is depicted by a broad choice of conditional construct rather than general concept to

generate the procedure and intension of research methodology (Winter, 2000). This actuality

and bilinear notion mostly created by the researcher’s own insight of legitimacy and

paradigmatic attitude of the researcher (Creswell & Miller, 2000). Several authors

(Golafshani, 2003; Davies & Dodd, 2002; Stenbacka, 2001) pointed out quality, rigidity

(exploring subjectivity, reflexivity, and the social interaction of interviewing) and

trustworthiness as more suitable idiom to replicate interpretive conception of validity.

Validity of this research connected to consenting adequate data by recognizing research

population, collection and interpretation of data and substantial conclusion. As the research is

focusing on the strategic issues to the retail banking of Metro Bank and the history of setting

this bank in UK is new and the historic issue is not going to influence the historic issues. The

study result is not going to disadvantageous as the analysis and confidentiality is maintained

properly. Mortality is not threat to validity as there is no drop out of participants and

maturity of the study enough as the Metro Bank has passed much time in the operation in UM

to be mature to point out the organizational issue to study.

The starting point of this research is predetermined that limits the starting and ending point of

a research. Moreover, Case study is ‘bounded context’ which limits the study. In this stance,

the focus on how inclusive should the researched issue be? To be inclusive and reach to the

validity, several moderations ware necessary for this study. Data gather process was the

central issues were the attempting to identify new lead, broadening the information gathering,

recounting the current constituent and the quality of information.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 23/41

3.7.3 Generalisability

This study is a case based study and focused on the particular organization that has a different

strategy of providing customer service by going back to the typical banking system of making

humanising decision before providing service, so this study is not uniformly applicable to

such other organization. In addition, the research objective was to recommend fruit fully

instead of building theory that means to generalize. The attempt of this study is to explain the

particular situation, so robustness of this study can be tested further by more intensive

method or survey.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 24/41

Chapter Four

Data Analysis and Findings

4.0 Introduction

This chapter examines the current strategies to serve the customer and the aim, objective of

the strategy and how the overall process is going on to the betterment for the organization.

The identification of current trend and the lacking of focusing certain issues by this

organization are central to this chapter. It is also known that there is no specific way of

interpreting qualitative data and concluding to the research (Yin, 2003). Interpretation was

based on the scrutinized data collected from the four Semi-Structure Interview anddescribed below.

4.1 Facilitating Incorporated and Unfaltering Exchanges across all Channels

The bank has a focus on the incorporations and good mode of exchange of information and

support from all the channels. The combination of the all channels is very important for this

retail bank. Technological improvement has provided facilitation to the customers not to be

willing to make be related physically for all information on a broader basis. Decrease in the

number of customer to the visit of the bank branch does not necessarily mean that the bank

lose the connection to their customers. Though this issue challenge the organic growth, there

is ample facilitation to attain desired goal by developing concentrated connection through the

phone call and Web. So, the customer service issues are generally handled by three sources,

directly Branch Service, Phone Call Service (through branch and call centre) and Online or

Web Service.

The first and foremost strategic action relates to the offerings of an outstanding customer

service via multi channel communication among branches, phone, fax, SMS, e-mail, ATM

and Web chat so that customers are able to perform business activity accurately when and

how they like.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 25/41

There is a strategic choice has been initiated to provide as much as can be practiced faultless

run through across all channels so that communications are as reliable, fair ,consistent and

well-organized, efficient and competent. The aim of this strategic choice is to build a

solidarity relation with the customers. For example, the bank has a strategic choice to

focusing on the relationship selling. In this case, it has been emphasized by Metro Bank to the

interactions across all channels through a unified view. The focus has been given on the

promotional stage. The strategy has been taken not to touch the same and repeated activity to

serve the customer by different touch point. That means the ways of handling one issue by

the branch and by the call centre are different. It is emphasized to the agents to pick up the

reaction where the customer left off at one step in the sales progression, not considering of

which channel the customer was using. If a customer asks about a loan online, the call centre

is very aware about the all aspects to close the deal. The call centre employees are trained like

that way. In addition, it has been identified that the bank has not a strategic focus to use the

live chat option to deal with the current situation. It has been addressed that using the live

chat technology is not too expensive to maintain.

4.2 Serving by Decreasing the Volume of Call

The Interactive Voice Response (IVR) system is utilized to provide a first impression of the

bank when customers use this system. It also guides to the bank service. The different steps

are identified to decrease the volume of calls. In doing so, the preference has given to the

priority of the problems are faced by the organization. Metro bank has graded different

service on the basis of urgency and set those in a descending order. This helps to decrease the

volume of the call. The strategy to decrease the volume of the call is not a cause of boring for

the customers. The bank has not yet put ‘Open Dialogue Call Steering’ as an alternative to

the tradition IVR system. Metro bank is generally offering to come to the branch and the

dealing decision will be made through humanism way rather than depending on the automatic

machine to complete the deal. That’s why emphasize has not provided to the ‘Open Dialogue

Call Steering’.

4.3 Integrating Self-Service with Agent Assistance

This strategy consents customer to intermingle with the bank in a well-situated way though

still accepting the similar modified counselling service accessible in branch. As customers

connect in online search and dealings, it can be presented mediator support to construct

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 26/41

communication set off more effortlessly. For example, a customer logs into his/her online

account and tests his/her reserves in account, and after that click on a linkage for the

mortgage page. S/he starts understanding throughout information concerning loan

opportunity, choices and alternatives. As s/he comprehends, an online chat window pops up

appealing him/her to converse in the company of a loan expert or authority. S/he

acknowledges and is capable to instantaneously request the exceptional query s/he has after

re-examining the online resources.

4.4. Handling Calls Brilliantly

Call centre mechanization, on the basis of IVR input, identifies both customer and the reason

of calling why they are calling. With this information, intellectual direction-finding can be

placed to decide whether the call has to set out to a self-service list of options or to the

negotiator generally competent to bump the call. Intellectual managing comprises direction-

finding based on skilfulness, being certain that every caller is harmonized to the spokesperson

with the exact skill set. This strategy consents banks to equivalent service precedence with

customer value. For example, premium customers who produce the large returns for the bank

are frequently concerned of comprehensive service. This kind of direction-finding — named

business precedence routing — allow banks to prioritize calls on the basis of a broad choice

of consideration as well as customer value, such as existing channel resources, to grasp time

and other factor. The strategic importance has provided to deal with premier customer and an

ordinary customer during a period of pick demand very wisely. During that time the premium

customer’s call will be directed straight to a contact centre agent. During the same period,

ordinary customer or client handled with excellent service opportunity by providing self

service channel or agent or a call back afterwards as a last option if the agent is not available.

4.5 Initiating Proactive Contact

Metro Bank has proactive approach to service deliverance to attain excellent customer

service. For illustration, bank proactively informs their customers and patron on the basis of

prearranged priority choice (such as emailing, making phone call, sending SMS and others).

These announcements enhance banking service by getting customers act in response to

specific circumstances previous to occur. This is advantageous to customer as this option

helps to take full advantage of an opportunity or reduce a depressing force to their economic

well being.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 27/41

For instance, a low-income person may desire for receiving proactive caution throughout

immediate messaging (IM) concerning inspecting account balance that are lower than an

satisfactory and acceptable level, or a credit card balance that is close to credit limit. A high-

income investment customer may have a preference to get phone notice regarding change in

stock price in his/her collection which is also lower or over some range so that s/he can

formulate appropriate purchase choice. Proactive ring up managing is too a constructive type

of automatic telemarketing to array the contact centre for amplified cross-selling and up-

selling performance. Metro Bank further employs proactive contact to inform their clientele

of innovative or fresh products and services as well as exceptional promotions.

4. 6 Using Customer Data and Segmentation Effectively

It is outlined that several banking products are vulnerable as commodity to noteworthy price

opposition; a number of banks are discarding product-centric approach to business. As an

alternative, those banks are looking at cross-sell and up-sell strategies on the basis of the

purchaser affiliation. In this innovative paradigm, contact centres get to the buyer through

product configurations, product package and cost considered particularly to create a centre of

attention and congregate the wants of individual client. Front-office incorporation in the

contact centre assists banks to shift away from grubby analysis of customer data. Front-office

incorporation provides representatives or agents a 360-degree analysis of the customer to

construct relationship selling successful that is helpful to focus on life span customer

productivity. The strategic choice of Metro bank is to provide agents the access across to the

all touch point to get the right information about customer. This has been followed to

facilitate effectual communication with the customer. In this system, customers possibly will

obtain local office agent assistance and/or modified offer on the basis of their in progress

performance, current communications crossways all channels, breathing bank-wide product

collection, and comprehensive information of the customer’s demographic data and

susceptibility to purchase.

High-value clients might interact, while feasible and going one step further, with a life span

advisor who is confidentially well-known with the client’s account history and wants or

needs. For instance, a customer informs a local office mortgage expert that the bank’s loan

charges don’t look reasonable and sensible with other offers s/he has seen online. After

getting into the customer’s total folder and demographic information about his/her earnings

and credit position, the mortgage expert be able to inform him/her that s/he is qualified for a

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 28/41

premium customer particular as a result of his/her connection or bond with the bank and

his/her outstanding credit record. S/he is glad to know that s/he is able to obtain a reasonable

charge at his/her existing bank, and may consent to the offer.

4.7 Serving through Inbound Marketing Strategy

One of the strategies is to serve or go to the close to the customer utilizing inbound marketing

strategy. This helps to get the customer outside of the branch. It normally generates more

than 17% revenue for the Metro Bank. Since customers gradually carry out dealing outside

the branch, relative inbound marketing techniques on the basis of a 360-degree view of the

customer is utilized to construct modified maintenance and cross-sell offer while customers

visit a Web site, compose a call or entrance an ATM.

4.8 Establishing Customer Intimacy through Controlled Demographic Profile

Metro Bank is equipped with reserves of demographic particulars that are able to manipulate

cross-sell and up-sell opportunity. This bank has utilized its long used knowledge about

customers to put into practice undertaking marketing campaign. Nevertheless, to improve the

relationship with their customers bank do yet further with demographic resources.

Demographic harmonizing is a method to allocate the customer to an agent who possesses a

widespread demographic outline. This facilitates customers to work together with agents who

are further willingly related to the customer. It is the result of the sharing certain

commonalities, i.e. local tongue words, speech, age range, level of technological capability

and so on.

4.9 Creating an appealing Team Effort with Contact Centre

Several banks are shifting their attention in the direction of a virtual contact centre to permit

geologically diffused agents to function as a solitary and winning team. Not considering

locality, agents are called upon, as presented; to make certain suitable reply altitude and to

offer entree to required expertise. In the circumstance, an agent can receive a call that involve

in having additional help from skilled someone of the branch. Without making a frustrating

effort for the customer by given that shortened information, the agent will rapidly place

available branch experts and without a glitch exceed the call on to somebody who have total

particulars of the communication.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 29/41

In this technique, the customer hasn’t required repeating details of the preceding discussion,

and Metro Bank increase the advantage of a decrease in expenses through the function of

numerous locations as one centre. For instance, it can be illustrated by the following way.

One customer has called to the call centre to quarry about a home loan.

Nonetheless, the call centre agent rapidly understand that customer thorough questions about

a ‘Home Equity Line of Credit (HELOC) Loan’. This means the customer needs to required

information about mortgage loan and systems and the condition etc. Then, the call centre

agent will quickly look for assistance from the mortgage loan specialists and direct the call to

the available mortgage loan specialist. Rather than repeating the particulars of the discussion

that the customer immediately had with the call centre agent, the customer is capable to carry

on the conversation where she left off as the mortgage specialist has seamless right of entry to

the communication at the call centre.

4.10 Blending Interaction to Increase Productivity of Agents

Metro Bank gains by optimizing agents’ time so far likely achievable. Call combination

consents agents to hold both inbound and outbound sale calls as call number and skills allow,

whereas task blending permit agents to put forward their support at diverse communication

channels. For instance, this strategy facilities loan officers and specialist at the branch to grip

service calls at the call centre or engage in making sells call when branch activity is relatively

low. On the other hand, call centre agents are used to replying emails, or employed in text

chat with customer. This strategy does both maximize the agent productivity and increase the

blending interaction. It also helps not being impending monotony of the situation. This

strategy enhances the customer service efficiently.

4.11 Strategies to Serve and Maintain Quality through Online Service

To provide online service the web page design is important so that customers can easily

obtain necessary information regarding customer service and product. The web page, for

Metro Bank, contains many traditional or typical link to get through different service i.e.

FAQs questions, contact information, store, carrier, business, link to customer service centre,

social media such as twitter link to follow, securities, legal information, accessibility, open

seven days and others. It has been addressed inn all interview that the online or Web design

has been followed by regular daily update information when it takes necessary the Web page

updated through the current and very recent information.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 30/41

4.12 Strategies to Serve in the Branch

One of the important strategies taken to grasp customer and retain customer and maintain

quality is the decision of being open for seven days in a week. Metro Bank has the view of

being unique as it has customer focused retail business. This bank reinvented the system of

retail banking. It makes each and every attempt to get rid of all dim bank rules from day to

day services to provide easier and further suitable banking to customer as it is providing

traditional or typical face to face service (Jervis, 2010). This bank address the dialogue ‘‘no

stupid bank rules’’. This exemplifies the strategy to provide customer service with an

alternative way. It means the bank avoid one rule to all where computer says no approach.

The branch manager has the self-reliance to make decision over the computer system. This

system differentiates customer service strategy from other service provider in retail banking

(Jervis, 2010). In doing so, Metro Bank decides to be open for seven days week. It will

facilitate customers to walk in the centre when it is holiday as well. As the decision will be

made by following humanism rather than computing system, there is a scope of getting

customer visit in normal holiday’s not public holidays.

A case study needs refs please and would normally draw on multiple sources, corporate

documents etc

4.13 Conclusion

This chapter has been illuminated the current strategic choices made by Metro Bank to

support the overall business aim and objectives, which are very realistic and better to

compete in the market. The strategic choices generally look good but the implementation is

the main role to be practical. Though there are several strategic choices, there are some

limitations in the utilization process of technological tools like Live Chat for retail banking

and others. The following chapter is going to discuss how the study objectives has been met

and what the future strategic choices can be made by Metro Bank.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 31/41

Chapter Five

Conclusion and Recommendation

5.0 Introduction

This chapter has focused on the analysis of the objectives that met by this study. It, in

addition, endow with supplementary recommendation for the betterment of the strategic

choice to provide more reliable, authentic, time saving, exact and fully customer driven ways.

It also describes the limitation of this study and recommend for further study. The

recommended strategies consist of focusing in divergence issues that are threat to reach to

customer and look for more prominent ways to overcome the threat and follow the suitable

and well suited strategy for the further development of the customer service. There are

several additions, describes below, in the strategy to focus on better customer service by

Metro Bank.

5.1 Meeting First Objective

The first objective was ‘to analyse the current literature on the different issues like customer

service, quality, satisfaction, local and global issues, changes in technology etc. that are

challenges and have been accounted in formulating strategy in relation to retail banking

customer service’.

The challenges for the retail banking for the strategic issue in the customer service arena

remains in the field of three combined areas, and those are branch areas, phone and call

centres and Web configuration of information providing. The competative nature of the

industry also chellengeing for any organizationand hence strategy differs one organization

than others. The way of utilizing remote channels to provide service is very chellenging

issue in the formulation of the strategy for customer service. Metro bank has the objective tobe huminisim in the process of decission making rather than depending on the computer

system which allows customers to walk in the branch. This facilitates a burgaining point for

the customers. However, the chaellenging issuses are related to the use of technological

advancment equpment in the process of customer service. The complex nature of post

moderen life and technology have created an obvious emphasize on the technology to

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 32/41

formulate strategy for customer service. Though Metro Bank is focusing on the typical

huminisation of the banking service, the bank must have to use call centre and use Web or

online equpments to grab customers’ attention. If the technologicla adancement is not

followed by the bank, it will lack behid whatever the perfection in the service. Suppose,

Metro Bank is not utilizing Live Chat technology as a media of providing service. But, the

other media which are used providing service is excelent, but the bank is not going to use this

type of techological equipment which makes it to be lack behind. In addition , the utilization

of the ‘Open Dialogue Call Steering’ over the traditional IVR system will reduce the cost and

most importantly it will the time. This will make the customers comfortable to use less words

that IVR syste. May the service through the IVR is excelent but use of this tradtional system

will hinder the pace of the service and organization as a whole. So, the main challenging

issue in formulating customer service strategy is to maintaing techonological equipment for

attracting custmer and replacing old technology.

5.2 Meeting Second Objective

Second objective was ‘to examine the current customer service strategy that has been

adopted by Metro Bank in its retail banking.’

In this circumstance, the main findings related to the utilization of different issues that will be

useful have been utilized and introduce by Metro Bank. One of the main concerns is to

provide a huministic service on the decesion making process rather than depending on the

computarized system in the branch. Where as automated mechanisms in the computing

system may refuse the proposal of a customer, there is a huministic apprach to deal with the

customer in product buying. This is quite good to look in the traditional way and well

strategy to serve customer. The strategy is well however the degree of the service level in the

branch.

In the case of the call centre there are a lot of strategic issue related to the utilization of the

Call Centre. The organization is following ten strtegic issues for handleing and the betterment

of the customer service related to the call centre. Those strategic choices are quite good and

well suited for Metro Bank. Those are highlighted as facilitating incorporated and unfaltering

exchanges across all channels, serving by decreasing the volume of call, integrating self-

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 33/41

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 34/41

customers want. After specifying and by integrating with business rules and routing

strategies, the open dialogue can be used. To make this understandable how it will reduce the

service time and cost and will be effective an example has been initiated in the below:

• IVR: “Thank you for contacting Metro Bank. May I help you?”

• Customer: “I would like to enquire on the mortgage facilities by the bank?

The Open Dialogue Call Steering can then either locate an agent who handles mortgage

issues, or execute a self-service application for the requested issue.

5.3.3 Intensive Emphasize On the Contact Centre besides Branch Service

Contact Centre is intended to convert customer service by mechanically optimizing customer

traffic, business outcomes and internal resources. As contact centre is able to manually

regulate to change pattern, a sophisticated — or ‘dynamic’ — contact centre has the

knowledge and equipment to construct usual modification immediately. As contact centre

develop into ever more significant retail banking channels, Metro Bank can exchange to self-

motivated contact centre to mechanically optimize the customer experience, promote cross-

sell and up-sell prospect and amplify agent efficiency with contentment.

5.4 Recommendation for Further Study

A further precious and worthy expansion of this study of developing strategic choices to

provide more intensive customer service proving ways as well by using larger sample,

survey, comparative and qualitative methods.

The central focus was given to certain questions like is this study provide an insight into the

inner scenery of the study, have the analysis and findings reliable, appropriate, applicable for

the identical organizations like Metro Bank. In spite of the addressing of these issues, the

involvement might be suggestive of further research on the effort from a diverse viewpoint

that would permit a demanding, intensive and rigorous measurement. It is obvious from the

preceding justification that the Metro retail banking is the only high street banking in the UK

for the last hundred years. So, the focus of Metro bank in humanizing effort of decision

making needs to be more emphatic and strategic in the issues of customer service that can be

done by further qualitative study. This research can be an action research from an

interdisciplinary perspective to develop a well suited model for the organization.

8/3/2019 Feedback - Research Project

http://slidepdf.com/reader/full/feedback-research-project 35/41

5.5 Limitation of the Study

The Case Study research is one kind of ‘bounded context’ and hence limit the study. On the

other hand, qualitative study has a starting point with predesigned idea, what will encompass

and where is the ending to observe of the study which limits the study. To overcome these

problems the focus was on the process of inclusiveness in the study, moderations to conclude

the study. The study also tried to be accomplished by gathering as much as data possible

from the qualitative interview and the wide range of literature review. However, the study has

the following limitations as well as there are certain issues that are out of control for the

researcher.

The study has to be completed with a very short span of time which did not allow to focus on

the more intensive way to observation or to add the customers’ view who has received the

service from the Metro Bank. If the customers view on the limitation of varied service of

Metro Bank could be added, the study could be more inclusive to recommend for the strategic

choice. Discussion needs to relate back to the literature please

5.6 Conclusion

This study has been focused on the strategic issues to support the customer service

remembering the challenges that will invade the customer service and will be the reason for