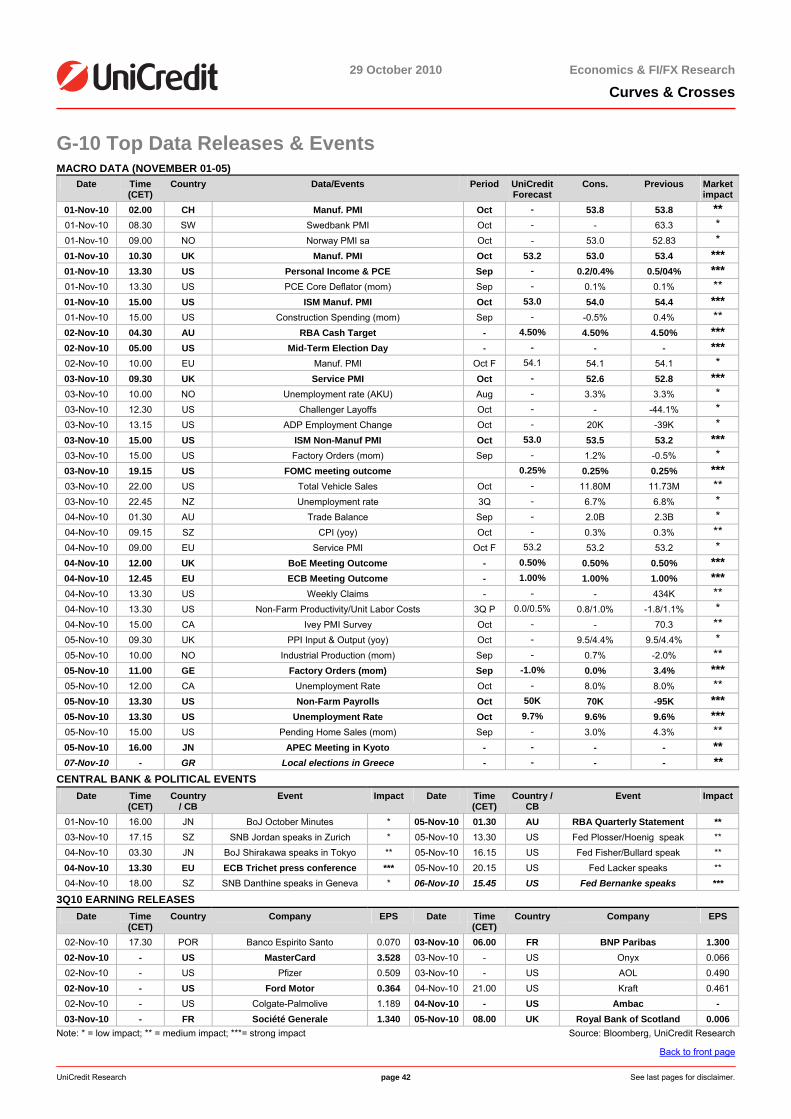

Embed Size (px)

Citation preview

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 1 See last pages for disclaimer.

Fed unlikely to go ALL-IN Fixed Income

■ FI Strategizer: Next week’s calendar is packed with data and events, but we think the only one really driving bonds will be the long awaited FOMC meeting. Expectations on the size of the QE program have been scaled down in the past week, and only a bold move coupled with a dovish FOMC statement would trigger a significant rally in 10Y USTs. Real yields, although already very low, should benefit more from Fed buying.

■ EU Portfolio Strategy: After reverting to benchmark weightings on all peripheral countries except Italy, we leave our allocation unchanged ahead of the FOMC and we also stay duration neutral.

■ ECB: The ECB November meeting should not be a relevant market mover. The recent rise in MM rates and the 3M LTRO outcome suggest the exit strategy is well on track. The recent discussion on economic governance in the eurozone may attract questions in the Q&A session.

■ MM: Demand at the 3M LTRO surprised on the upside. This is due to the increase in MM rates rather than to renewed tensions on the MM. In the coming months, the full allotment should keep the 3M Euribor stable.

■ Inflation: The October flash estimate came in at 1.9% yoy, a touch higher than we had expected. The HICP ex-tobacco should print at 1.8%. We think that this will be the peak for several months.

■ Supply Corner: Next week, there will be no redemptions in the EMU. Gross supply should be EUR 18.5/20.5bn, mainly from core. Within periphery, Spain is the only country issuing (new 5Y Apr16). Portugal will hold a T-bill auction on 3 November, the day of the budget vote.

Forex

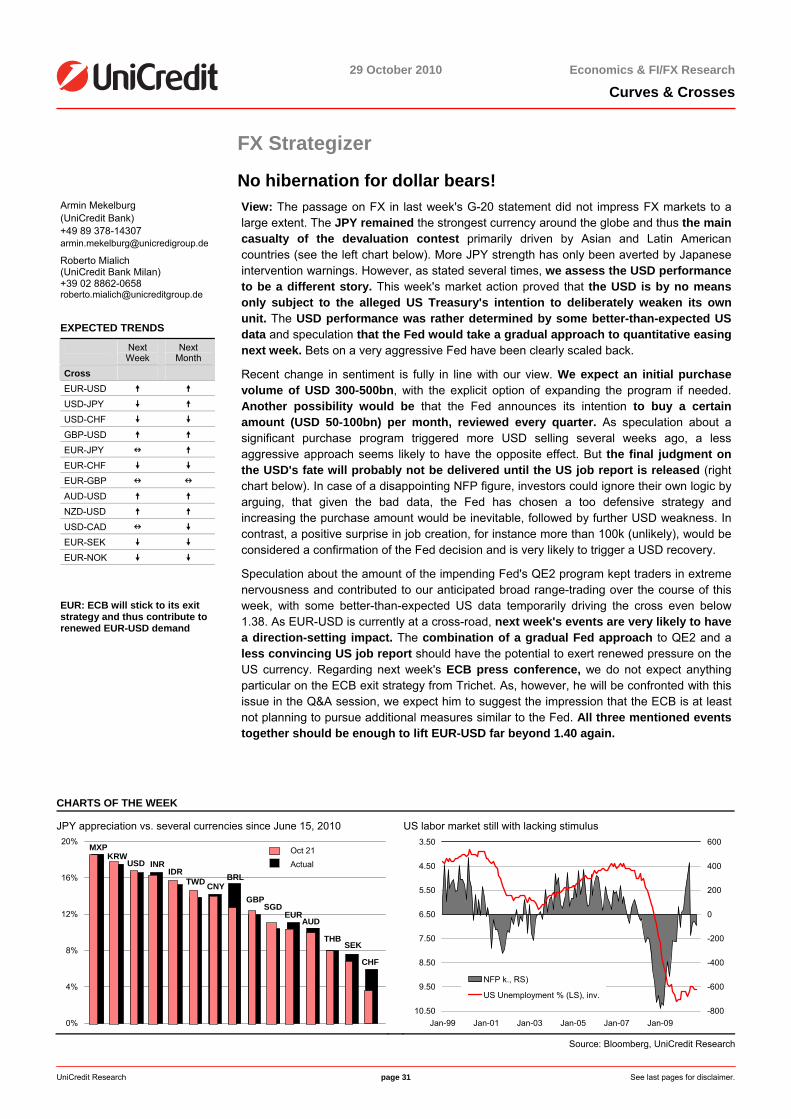

■ FX Strategizer: The Fed’s decision, NFP and US mid-term elections will be the main drivers for FX majors in the coming days. On balance, we expect the greenback to remain on the offer side across the board.

■ EUR: A gradual Fed approach to QE2, ECB welcoming the normalization in the EU money market and a less convincing US job report should all lift EUR-USD further. We expect it to rally far beyond 1.40.

■ JPY: As the USD stays weak, Japanese MoF & the BoJ will face a hard time to avoid a USD-JPY fall to the record low of 79.75. Caught between USD-JPY & EUR-USD, EUR-JPY will move in the 111.50-114.80 band.

■ CHF: The continuation of the CHF downward correction will depend on the USD reaction to the Fed’s QE2 decisions: any poor USD response should trim recent USD-CHF gains and prevent a further EUR-CHF rise.

■ GBP: Even in case the USD weakens, cable is unlikely to rally above this month’s highs at 1.6110. EUR-GBP should remain in the 0.86-0.88 band, despite creeping EMU woes, as the BoE meeting will be a non-event.

■ The three dollars: A new USD slide should recommend reopening AUD-USD & NZD-USD long positions, but only in the aftermath of the US job report. The RBA is expected to remain on hold at 4.50% on Tuesday.

■ Nordics: A less aggressive stance on rates by both the Riksbank and the Norges Bank should weigh on both the SEK and the NOK, at least in the near term. We also lowered our Norwegian key rate trajectory

More insight in our monitors: Swap Curve – Trade Idea – EGB spreads – Money Market – Real Money – Inflation - FX Monitor – IMM Monitor – FX PPP – Beta analysis – FX Correlation – FX Hit Parade – Data Calendar - Periphery Calendar – Forecasts.

MARKET PRICES & FORECASTS

Actual Dec10 Mar11 Jun11 Sep11

US FedFunds 0.25 0.25 0.25 0.25 0.25 2Y UST 0.36 0.45 0.50 0.80 0.90 10Y UST 2.65 2.50 2.40 2.70 2.85 EUROZONE Refi 1.00 1.00 1.00 1.00 1.00 2Y Bund 0.99 0.80 0.80 1.10 1.40 10Y Bund 2.54 2.25 2.25 2.50 2.75 UK Base rate 0.50 0.50 0.50 0.50 0.50 2Y Gilt 0.69 0.70 0.70 1.00 1.25 10Y Gilt 3.11 2.80 2.70 2.90 3.10 (10Y, bp) US - EU 10 25 15 20 10 US - UK -46 -30 -30 -20 -25 UK - EU 57 55 45 40 35 Swap Spread (10Y, bp) US 8 5 5 10 10 EUROZONE 29 30 30 25 20 UK 11 10 10 20 20

Currencies EUR-USD 1.38 1.43 1.39 1.42 1.44 USD-JPY 81 83 85 88 90 GBP-USD 1.59 1.61 1.58 1.63 1.67 EUR-CHF 1.37 1.33 1.30 1.33 1.36

BUY THE RUMOR, SELL THE FACT?

Fed announces LSAP

Bernanke says Fed could buy USTs

Fed to buy up to USD 300bn of USTs

FOMC to "keep constant holdings of securities"

FED prepared to provide additional accommodation

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

Jun-08 Nov-08 May-09 Nov-09 May-10 Nov-10

Fed Funds 10Y TIPS

Source: Bloomberg, UniCredit Research

Chief Economist – UniCredit Group Global Head of Economics & FI/FX Research Marco Annunziata +44 20 7826-1770 [email protected] Head of Global FI & FX Research Michael Rottmann +49 89 378-15121 [email protected]

Editor Luca Cazzulani +39 02 8862-0640 [email protected]

Editorial deadline Friday, October 29, 2010 15:30 Prices as of Friday, October 29, 2010, 15:00 Bloomberg: UCGR Internet: www.research.unicreditgroup.eu

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 2 See last pages for disclaimer.

The story so far… Yield 1w ch 1m ch DE IT US UK DE IT US UK DE IT US UK2Y 1.01 1.50 0.36 0.73 3 4 0 6 21 -9 -7 45Y 1.61 2.53 1.02 1.85 7 9 5 21 23 0 -6 1110Y 2.55 3.89 2.56 3.15 9 8 10 20 28 6 11 1830Y 3.06 4.80 4.03 4.22 6 8 11 14 18 2 32 302/5 61 104 65 112 4 5 5 15 2 9 1 75/10 94 136 155 130 2 -2 6 -1 5 6 17 72/10 155 239 220 242 6 4 10 14 7 15 18 1410/30 51 91 147 107 -3 1 1 -6 -10 -4 21 122/5/10 -17 -16 -45 -9 1 3 0 8 -1 1 -8 010Y BE 168 168 215 284 0 0 3 4 0 9 33 14

ASW 1w ch 1m ch DE IT US UK DE IT US UK DE IT US UK2Y -54 11 -16 -50 -1 2 2 -1 6 -18 4 35Y -46 59 -20 -28 -1 1 0 4 3 -20 5 510Y -28 101 -2 3 -1 -3 0 5 2 -20 1 -130Y 3 175 40 28 -1 -2 -1 1 1 -17 0 02/5 7 48 -4 23 0 -1 -2 5 -4 -2 1 25/10 19 42 18 31 1 -3 0 1 -1 0 -5 -610/30 31 73 42 25 -1 1 -1 -3 -1 3 0 1

Swap curves EMU 10Y benchmarks EU US BP SZ JP Yield ASW Spread

vs. DE 1w ch 1m ch

EONIA 0.79 0.23 0.55 0.06 0.10 GE10Y 2.55 -28 - - -1M 0.85 0.25 0.57 0.13 0.13 NL10Y 2.76 -7 21 -2 -23M 1.05 0.29 0.74 0.17 0.20 FI10Y 2.77 -3 22 -1 -46M 1.27 0.45 1.03 0.24 0.40 FR10Y 2.86 5 31 -3 -712M 1.54 0.76 1.48 0.52 0.64 AT10Y 2.94 12 39 -2 -142Y 1.61 0.53 1.32 0.52 0.38 BE10Y 3.36 53 81 -7 -25Y 2.20 1.48 2.17 1.21 0.48 IT10Y 3.89 101 134 -1 -2210Y 2.85 2.74 3.26 1.87 1.01 SP10Y 4.11 124 156 -3 -1930Y 3.00 3.68 3.93 1.90 1.90 PT10Y 5.92 279 337 -1 -472/5 58 95 86 68 9 IE10Y 6.81 348 426 20 95/10 65 126 109 66 53 GR10Y 10.39 619 784 95 -210/30 16 94 68 3 90

Forex EUR USD Last 1w ch 1m ch 3m ch 6m ch Last 1w ch 1m ch 3m ch 6m chEUR-USD 1.3857 -0.7% 1.7% 5.9% 4.7% EUR-USD 1.3857 -0.7% 1.7% 5.9% 4.7%EUR-JPY 111.89 -0.8% -3.5% -7.0% -14.1% USD-JPY 80.75 -0.8% -3.5% -7.0% -14.1%EUR-GBP 0.8685 1.2% 1.2% -5.0% -8.7% GBP-USD 1.5956 1.2% 1.2% -5.0% -8.7%EUR-SEK 9.3589 1.7% 1.1% 2.2% 4.2% USD-SEK 6.7540 1.7% 1.1% 2.2% 4.2%EUR-NOK 8.1929 -0.8% 0.5% 8.3% 5.1% USD-NOK 5.9126 -0.8% 0.5% 8.3% 5.1%EUR-CHF 1.3707 1.5% 2.7% 4.8% 4.8% USD-CHF 0.9892 1.5% 2.7% 4.8% 4.8%EUR-AUD 1.4215 -0.5% -1.1% -1.6% 1.6% AUD-USD 0.9748 -0.5% -1.1% -1.6% 1.6%EUR-NZD 1.8277 -1.4% -1.9% -1.4% -10.1% NZD-USD 0.7582 -1.4% -1.9% -1.4% -10.1%EUR-CAD 1.4145 0.6% 3.0% 0.7% -4.4% USD-CAD 1.0208 0.6% 3.0% 0.7% -4.4%

Equity Commodities Last 1w ch 1m ch 3m ch 6m ch Last 1w ch 1m ch 3m ch 6m chS&P 1183.8 0.3% 3.4% 7.5% -1.9% OIL 81.83 0% 5% 4% -4%Eurostoxx 2835.4 -1.3% 3.0% 3.0% 0.3% Gold 1351.35 2% 3% 16% 16%DAX 6584.3 -0.3% 5.4% 7.3% 7.2% CRB 492.34 1% 2% 14% 10%FTSE 5659.7 -1.4% 1.6% 6.5% 0.7% iTraxx 458.34 0 -53 -20 28Nikkei 9202.5 -2.4% -3.7% -5.1% -15.8% Shanghai 2978.8 0.1% 14.1% 12.5% 3.8%

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 3 See last pages for disclaimer.

Favorite Trends & Medium-Term Strategies

Fixed Income EU US UK Change Actual Expected trend Change Actual Expected trend Change Actual Expected trend -3M -1M 1M 3M -3M -1M 1M 3M -3M -1M 1M 3M Key policy

rates 1.00 1.00 1.00 0.25 0.25 0.25 0.50 0.50 0.50

Libor rates 0.90 0.88 1.05 0.47 0.29 0.29 0.74 0.73 0.74

10Y 2.72 2.25 2.55 2.98 2.47 2.64 3.41 2.93 3.11

2/10Y 188 151 156 240 203 227 291 220 241

2/5/10Y -6 -8 -4 -12 -22 -29 2 -18 -24

10Y SwSp 26 32 29 -2 3 10 5 8 10

Portfolio allocation After reverting to benchmark on all periphery except Italy, we leave our allocation unchanged ahead of the FOMC meeting. We stay duration neutral ahead of next week FOMC, given the may uncertainties surrounding the Fed announcement.

Supply

Liquidity in November will be pretty low. Redemptions will amount to EUR 21bn, while coupons will be EUR 4.8bn. We expect gross supply in November to be EUR 64/71bn, slightly lower than in October and still much lower than the average monthly volume registered so far (EUR 87bn). Net supply however, should be much higher than in October, in the EUR 42/50bn area (vs. EUR 33bn), as redemptions will be lower. 60% of the supply should come from core/mid countries, while 40% should come from periphery, with Italy and Spain the main contributors. Ireland and Belgium should not hold any auction in November.

FX Change Actual Expected

trend Change Actual Expected

trend Change Actual Expected

trend -3M -1M 1W 1M -3M -1M 1W 1M -3M -1M 1W 1M EUR-USD 6% 1% 1.38 EUR-JPY -2% -2% 112 EUR-NOK 3% 3% 8.21 USD-JPY -7% -3% 81 EUR-CHF 0% 3% 1.37 AUD-USD 8% 0% 0.97 USD-CHF -5% 1% 0.99 EUR-GBP 4% 1% 0.87 NZD-USD 4% 2% 0.75 GBP-USD 2% 1% 1.59 EUR-SEK -1% 2% 9.37 USD-CAD -1% -1% 1.02

EUR-USD Divergences between the Fed and the ECB monetary policy, with the Fed expected to run an ultra-loose monetary policy through a new round of QE, while the ECB may start an exit strategy as early as in 2H11, should keep EUR-USD firm going forward, in the 1.43-1.46 band. A minor correction below 1.40 is possible in 1Q11, if EMU tensions escalate again.

JPY

The BoJ intervention failed to pose a floor to the USD-JPY depreciation and a test of 80 is still possible, if the USD slide persists. Looking ahead, with global risk aversion gradually easing, the JPY should lose its grip, but USD-JPY is unlikely to break through the 90-93 area in 1Y time, while EUR-JPY should rally further above 1.30, as long as EUR-USD stays firm.

CHF

The renewed EUR-USD strength should spill over to EUR-CHF too, but as long as global uncertainty persists, risks of a EUR-CHF retreat back towards 1.30 are still concrete, considering a possible SNB rate hike in 1Q11. EUR-CHF recovery on a better global risk picture in about 1Y time should not exceed 1.40.

GBP

Cable should remain mostly dominated by the renewed broad-based USD weakness, increasing the room for a test towards 1.62-1.63. As the USD should stay weak and the BoE is expected to hike rates next year, cable should rally back above 1.70 in late 2011. EUR-GBP should show smoother fluctuations, but the start of the BoE’s tightening process should bring it back below 0.85 at the end of 2011.

Pacific Rim & the CAD

The Aussie, the Kiwi and the loonie dollar should remain firm against the USD for now and the AUD still seems to be in the best shape, as chances of a break through parity increased. Both the NZD and the CAD are most exposed to some correction due to a less aggressive monetary policy at home. In any case, all three dollars are now overstretched and some retreat is required before buying them again.

Nordic Block A more dovish stance on rates by both the Riksbank and the Norges Bank should weigh on the SEK and the NOK in the near term, spurring more consolidation for both EUR-SEK and EUR-NOK. Indeed, as the rate hike cycle in both countries is not over, we still target EUR-SEK and EUR-NOK at 9.05 and 7.75 by 4Q11.

Source: UniCredit Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 4 See last pages for disclaimer.

Favorite Trades

Favorite FI trades Type Trade Rationale Entry date Entry

level Act. Stop Target P&L (bp)

Curve trades

Buy SPGB Jul25, sell SPGB Oct20 & Jul41

On the Spanish curve the 15Y has reached interesting levels vs. the 10Y and the 30Y. We expect the recent trend to reverse.

24-Sep-10 16 21 35 0 -4.6

Buy Obl Oct15 sell Obl Apr15

The new OBL Oct15 offers an historical high premium vs. its forerunner OBL Apr15. We expect the market to arbitrage away this large roll spread.

24-Sep-10 13 11 25 0 1.6

EMU cross country

Sell BTP Apr15 buy SPGB Apr15

At the 5Y tenor SPGBs have cheapened more than BTPs opening a switch opportunity. We expect the spread between BTP Apr15 and SPGB Apr15 to tighten.

10-Sep-10 45 33 40 10 11.1

Buy BTP Jun13 vs. SPGB Apr13

TAKE PROFIT 30-Jul-10 10 20 20 60 9.8

Buy RFGB Jul15 vs. DSL Jul15

Finland trades at roughly the same level of the Netherlands in ASW, however, it enjoys a more favorable public finance outlook, a lower refinancing risk and a lower private debt. We thus expect it to richen vs. the Netherlands.

11-Jun-10 2 0 -9 12 -1.5

Buy FRTR Apr41 Sell DBR Jul40

At the 30Y, France has cheapened significantly vs. Germany; the current level appears too wide. We expect the yield spread to tighten.

2-Sep-10 31 36 45 20 -4.6

Swap spreads

Buy 10Y Gilts vs. Swap

10Y Gilts appear attractive given the reduced case for rating downgrade and the recent UK budget

9-Jul-10 -4 -10 -5 -50 6.4

Buy 10Y bund vs swap, sell 2Y

Germany has richened up vs. Swap at the short end due to safe haven demand. We expect a normalization.

7-Jul-10 47 32 35 10 15.3

Inflation Buy US 10Y BE, Sell UK 10Y BE

The US BE at the 10Y maturity has started moving up, with the Fed aiming at higher inflation expectations this trend will not likely reverse in the near future. In the UK, inflation expectations should, on the contrary, slow down. Hence, we suggest buying US 10Y BE and selling UK 10Y BE.

15-Oct-10 65 69 100 20 -3.8

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 5 See last pages for disclaimer.

FX Trades SHORT-TERM SPOT TRADES

Cross Position Start Entry Level

Target Current Spot

Stop 3M Carry % Return P/L net EUR

Rationale / Status

EUR-SEK short 22-Oct-10 9.29 9.15 9.34 9.34 0.017 -0.54% -5.456 S/L reached on Oct, 26 P/L Open Trades 0.000 P/L Closed Trades 171.865

Update 29-Oct-10 12:15h CET

P/L Total Trades 171.865

Note: P/L Net EUR also includes carry cost calculations and refers to a notional amount (1mn EUR or USD). Source: Bloomberg, UniCredit Research

MEDIUM-TERM OPTION STRATEGIES

Strategy Direction Start Maturity Strike Current Spot

Entry Level

Actual

% Return P/L net EUR

Rationale / Status

EUR-GBP strangle

short 27-Aug-10 1-Sep-11 0.86-0.76 0.8682 4.35% 5.20% -0.85% -8.500 We close at current levels, as we cannot rule out a resumption of the BoE QE expanding topic

EUR-NOK put spread

long 10-Sep-10 14-Jun-11 7.85-7.70 8.24 0.83% 0.23% -0.60% -6.000 NOK to benefit from gradual rising Norges Bank key rates and a brighter global risk picture next year

EUR-SEK put spread

long 17-Sep-10 21-Jun-11 9.20-9.10 9.40 0.60% 0.30% -0.30% -3.000 SEK to benefit further from rate hikes by the Riksbank and a brighter global risk scenario next year

USD-CAD strangle

short 01-Oct-10 4-Oct-11 1.10-0.98 1.0240 5.32% 5.55% -0.23% -1.653 USD weakness and Canada's wish to protect its export competitiveness to offset each other

Cable call spread

long 15-Oct-10 19-Apr-11 1.63-1.70 1.594 1.37% 1.20% -0.17% -1.950 More dollar weakness to come and close correlation between Cable and EUR-USD likely to persist

P/L Open Trades -1.30% -12.603

P/L Closed Trades -3.03% -28.054

Update 29-Oct-10 12:15h CET

P/L Total Trades -4.33% -40.657

Note: entry/actual levels are calculated as cost/income as a percentage of the notional amount (EUR 1mn or USD). Source: Bloomberg, UniCredit Research

SUMMARY TABLE

FX Open Trades -12.603

FX Closed Trades 143.811 FX Total Trades 131.208

Update 29-Oct-10

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 6 See last pages for disclaimer.

Macroeconomic focus

ECB: Rendez-vous in December Marco Annunziata (UniCredit Bank) +44 20 7826-1770 [email protected]

Marco Valli (UniCredit Bank Milan) +39 02 8862-8688 [email protected]

The 4 November ECB meeting is unlikely to bring major news – for market-sensitive announcements, the "rendez-vous" is in December, with the publication of updated macroeconomic forecasts (including for the first time the estimates for 2012) and new details on the liquidity strategy. Next week, Trichet should confirm that the central bank remains cautiously optimistic on the area’s growth prospects, with higher interbank rates seen reflecting the ongoing process of normalization in the financial sector.

The ECB’s disappointment about recent proposals to reform economic governance in the euro area will probably be a topic of discussion during the Q&A session.

Economic and monetary analysis On balance, the October round of business surveys provided reassuring evidence on the

health of the eurozone economy, validating the ECB’s assessment that the recovery remains on track. If anything, the most recent growth data indicate some upside risks to the central bank’s GDP projections for the final part of 2010.

The renewed acceleration in the German Ifo to the highest level since mid-2007, with a surprising rebound also in the expectations index, points to an increasingly sustainable upswing in the largest economy of the area. This helps further reduce the (already low) probability that the eurozone will face nasty GDP surprises down the road. Even the growth implications of the recent euro appreciation should not be overestimated, in our view. This is because prospects of further expansionary measures by the Fed – the key driver of USD weakness since the end of August – led to a generalized increase in equity prices and a drop in volatility and corporate bond spreads, which will probably suffice to neutralize some of the damaging growth impact of a stronger euro.

Coming to the monetary analysis, the main novelty is the second consecutive increase in the monthly flow of lending to Non-financial corporations (NFCs) in September, which will probably make the ECB more confident that the credit cycle is about to turn

Although overall lending to the private sector remained very weak at 1.2% yoy and M3 growth fell back to only 1% yoy, the ECB could be temped to start sounding slightly more upbeat on the monetary pillar. The October Bank Lending Survey released yesterday showed mixed results, but on balance confirmed a picture of moderate improvement

Money market normalization On 19 October, the 3M Euribor rate rose above the refi rate for the first time since July 2009.

This adjustment, which is endogenously determined by the decline in excess liquidity and therefore contains no monetary policy signal, certifies that the financial sector continues to recover, as also shown by the fact that Spain, Greece and Portugal in September reported a decline in central bank funding.

We also point out that the upward trend in the 3M Euribor rate has tracked very closely the “fair” refi rate prescribed by our Taylor rule in response to some narrowing of the output gap and a moderate recovery in lending to the private sector. In other words, money market normalization is now fully justified by the improvement recorded both in the financial sector and the real economy. What’s more, the last leg up of interbank rates has been relatively fast, a signal that the ECB doesn’t need to be overly cautious in its exit.

Note that higher demand at the last 3M LTRO (EUR 42bn bid vs. EUR 23bn expiring) is unlikely to have reflected increased money market tensions. Rather, it was probably due to the fact that the Euribor rate is now slightly above the refi rate, with risks skewed towards a further increase in the coming weeks. If anything, this suggests that the full-allotment is creating some distortions in demand for liquidity and offers arguments for removing it as soon as possible.

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 7 See last pages for disclaimer.

Although there remain considerable pockets of weakness in the banking sector of peripheral countries, our view that the ECB will drop the full-allotment on 3M LTROs at the December meeting seems fully on track.

Economic governance The ECB has done nothing to hide its disappointment on the agreement reached by euro

area finance ministers on the reform of economic governance. By de-facto leaving the decision to impose sanctions in political hands, the final accord is weak on all the main points that the central bank deemed as important to solve the problem of moral hazard, namely automatism and timeliness in the application of sanctions. This low-profile compromise puts the ECB in a difficult position: the central bank has the right to forcefully argue its point of view on economic governance issues, because it is ultimately the ECB that is left “holding the bag”, i.e., acting to ensure financial stability: this is the case both for its enhanced liquidity support measures to help the residual pockets of weakness in the banking sector, and for the government bond purchase program. Remember that the government bond purchase program has been particularly controversial, and Governing Council member Weber has recently again called for it to be discontinued soon. Lack of significant and credible progress on strengthening the Stability and Growth Pact, instead, flags the risk that the program might need to remain in place for quite a while longer.

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 8 See last pages for disclaimer.

FI Strategizer

Final countdown before the Fed meeting Luca Cazzulani (UniCredi Bank Milan) +39 02 8862 0640 [email protected] Chiara Cremonesi (UniCredit Bank London) +44 207 826 1771 [email protected]

In line with expectations, yield curves have remained stable during the week, as investors have preferred to stay on the sidelines ahead of the FOMC meeting. If anything, during the week, investors have focused more on the level of disagreement within the FOMC, which has somewhat cooled expectations for an impressive announcement at next week's meeting. 10Y USTs have moved up, leading to an only modest increase in 10Y BE. The USD has also remained fairly stable vs. the euro, with renewed concerns on some periphery countries unable to significantly alter investors' 'mood.

Periphery again under pressure Periphery were under strong pressure for most of the week: Greek spreads widened a whopping 100bp; Ireland widened 20bp and Portugal was volatile but, at the end of the week, unchanged. Market rumors suggested that the ECB intervened in the market, supporting Irish bonds. This is certainly possible, although at odds with the recent weeks’ trend when the ECB did not buy anything in the market. A confirmation will only arrive with the Monday release of ECB data.

Demand for the 3M LTRO surprised on the upside

Demand at the 3M LTRO surprised on the upside. As a result, liquidity in the eurosystem increased around EUR 20bn, pushing down short maturity rates. The EONIA and the 1M OIS fell back to 0.60%. The full allotment will likely keep liquidity abundant enough so that rates shorter than 3M will remain below 1%. See MM rates for a more detailed discussion.

Equities correcting their recent gains

Equities corrected some of their recent gains, with a more pronounced correction in the EMU than in the US. Overall, S&P was almost unchanged vs. last week, Dow Jones declined by 0.16% , while the Dax declined by 0.25%.

Next week: a very crowded calendar, but with only one event really important

Next week’s calendar will be extremely crowded: US personal income, ISM manufacturing, US NFP, UK manufacturing PMIs and three central bank meetings. However, the only one event that will be central for market action is the FOMC.

Ahead of the FOMC meeting: US real yields at all-time lows. BE has risen in the last few weeks

At the time of writing, real yields in the US have plunged to historical lows. This week, the UST sold a 5Y TIPS at a negative real yield for the first time ever. US 10Y TIPS trade at an all-time low of 0.50%. The breakeven, although lower than the historical average as we pointed out in last week's inflation monitor, has increased over the last few weeks as investors have attached great credibility to the Fed’s QE strategy.

Analyzing previous QE episodes, it possible to draw three main conclusions. The first is that most of the movement in yields (especially the nominal curve) happened before the program is actually launched. The second is that on the announcement date markets tend to display a high volatility. The third is that the medium-term reaction of markets can be significantly different from the near term one.

Fed QE1 suggests: buy the rumor, sell the fact Greece widens further

Fed announces LSAP

Bernanke says Fed could buy USTs

Fed cut rates from 1% to 0.25%

Fed to buy up to USD 300bn of USTs

FOMC to "keep constant holdings of securities"

FOMC "is prepared to provide additional accommodation"

0.000.250.500.751.001.251.501.752.002.252.502.753.003.25

Jun-08 Nov-08 May-09 Nov-09 May-10 Nov-10

Fed Funds 10Y TIPS

0

200

400

600

800

1000

1200

1400

1600

1800

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

10Y 2Y

Source: Bloomberg, UniCredit Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 9 See last pages for disclaimer.

Focus on the Fed meeting

The key variables to watch at the Fed meeting: 1) The size of the announced asset purchases 2) The timing and mode of QE2 3) The wording of the statement

It is needless to say that the main even next week will be the Fed meeting. As we argued last week, three aspects will be key to watch at the meeting:

1) The size of the announced asset purchases. At present, one of the most popular view in the market sees the Fed buying around USD 500bn of Treasuries in six months. We think that any size below this would be taken as disappointing by the market. A size higher than USD 1tn would represent positive news for the market.

2) The timing and mode of QE2. Our economists expect an initial purchase volume of Treasuries of USD 300-500bn, with the explicit option of expanding the program further if needed. Another possibility would be that the Fed announces its intention to buy a certain amount (USD 50-100bn) per month, reviewed every quarter. This more gradual approach, however, might disappoint markets.

3) The wording of the statement. The Fed could attempt to push yields even lower by modifying the wording of its statement. That would probably mean that the mantra so far – that the Fed would hold interest rates at this extremely low level "for an extended period" – will be modified.

Starting from an analysis of QE in the UK

Before analyzing the impact of the Fed announcement on the markets, we briefly review what happened in the UK when, at the beginning of 2009, the BoE decided to embark on QE. It is interesting to analyze QE in the UK because the BoE bought mainly Gilts from the secondary market through the APF, and this represents an important analogy with what we expect will be the Fed’s QE2. The possible disadvantage of this comparison is that, after all, we are comparing two different markets.

Official announcement of QE at the 5 March meeting: GBP 75bn of Gilt buying

On 5 March in 2009, the BoE cut the repo rate to 0.5% and announced QE, stating it could use the APF up to GBP 150bn to buy Gilts. Also, on March 5, the BoE announced that it would buy GBP 75bn in the following three months (12% of the Gilts stock).

…increased to GBP 125bn at the May meeting…

At the May meeting, the BoE announced that it would buy an additional GBP 50bn, but this did not come as a surprise, as with the first announcement they already suggested that they could use the APF up to GBP 150bn.

…and again to GBP 175bn at the August meeting…

At the August meeting, they surprised the market by announcing that they would buy a further GBP 50bn of Gilts, also expanding the APF from GBP 125bn to GBP 175bn.

…and finally upgraded to GBP 200bn at the November meeting

At the November 2009 meeting, the BoE announced the last GBP 25bn increase to GBP 200bn. While there were a few revisions during the life of the QE, the bulk of the amount was announced right at the beginning. Hence, the first announcement is the one that should have had the strongest market impact.

Analyzing the market impact of QE in the UK before and after the official announcement (5 March)

Analyzing the market impact of the BoE QE could be helpful in giving us a guideline of the impact which QE2 could have in the US. The table below shows the changes in nominal and real yields in three different periods:

1) From the start of February to 5 March 2009: when the market started to price in QE.

2) From 5 March 2009 to 12 March 2009: since the BoE officially announced the beginning of QE and the timing of the purchases for the first purchase. This can give an interesting indication about the short-term reaction of investors to the announcement of QE.

3) From 12 March 2009 to 30 November 2009: from the date of the first Gilt purchase by the BoE to November 2009, when for the last time the BoE increased the APF size by GBP 25bn from GBP 175bn to GBP 200bn.

Most of the plunge in nominal yields happened before the actual start of the BoE’s Gilts buying…

Results show that most of the reaction in Gilts nominal yields happened before the official announcement of QE (March 5) and in the first week after the announcement itself. After the start of the Gilt purchases by the BoE, nominal yields started to rise, correcting much of the plunge ahead of the QE beginning.

…while real yields continued to plunge during the actual start of the BoE’s Gilts buying

Like nominal yields, real yields fell between February 2009 and the official QE announcement, as the market priced in the QE effect, but then retraced slightly during the first week after the official QE announcement. Then, real yields experienced a large fall during the actual Gilt purchase program by the BoE.

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 10 See last pages for disclaimer.

In other words, while most of the impact on nominal yields happened BEFORE the program started, real yields plunged sizably DURING the program. In the US, the dynamics of nominal yields during QE1 were similar to the UK, while real yields did not really fall.

So, looking at the BoE QE program, the main conclusion is that nominal yields tended to rise after the beginning of the program (this was also due to factors such as increasing credit risk premia) and real yields fell after the beginning of the program. Reaction one week after the beginning of the program was quite different from the medium term impact of the program.

MARKET IMPACT OF QE IN UK

Nominal yield Real yield 2Y 5Y 10Y 15Y 30Y 2Y 5Y 10Y 30Y

4-Feb-09 1.7 2.9 3.8 4.5 4.4 0.1 1.5 1.7 1.0 5-Mar-09 1.2 2.3 3.4 4.1 4.3 0.7 1.2 1.3 1.3 12-Mar-09 1.4 2.1 3.0 3.6 3.9 0.9 1.4 1.4 1.1 30-Nov-09 1.2 2.6 3.5 4.0 4.1 -1.1 0.0 0.4 0.4 Change before QE -48.1 -60.5 -41.4 -34.7 -15.9 67.6 -30.5 -42.3 25.5 Change after official QE announcement first week 16.3 -17.9 -40.7 -56.4 -34.4 19.1 18.6 14.0 -16.6 Change during QE -19.3 47.7 57.2 48.0 18.3 -208.4 -133.2 -98.2 -69.4

Source: Bloomberg, UniCredit Research

As we have argued in the introduction, there are three aspects that need to be taken into consideration to analyze the market impact of QE2: the size, the timing and the wording of the statement. Right now, the market expects the Fed to announce USD 500bn in six months. To make things simple, we first analyze the short-term impact of next week's announcement and in a second step we try to analyze the market implications in the medium term.

Three different scenario for the size of the Fed’s QE2… …in all the three scenario, the Fed should buy a percentage of Treasuries outstanding lower compared to the one the BoE bought

First of all, we distinguish between three different scenarios:

■ The negative scenario: the Fed announces it will buy less than USD 500bn

■ The neutral scenario: the Fed announces it will buy between USD 500bn and USD 1tn.

■ The positive scenario: the Fed announces it will buy between USD 1tn and USD 2tn.

Note that in all the three scenarios, the Fed will buy a percentage of the Treasuries outstanding lower than the one bought by the BoE. At the time of writing, the total outstanding of US Treasuries (excluding Bills) amounts to USD 6.7tn. Hence, USD 300/500bn would represent 4.5% / 7.5% of the current outstanding. USD 1tn would represent almost 15% of UST outstanding. To buy an amount similar to the UK (28%), the Fed would have to buy USD 1.8tn.

….also in terms of timing, the purchases by the Fed should be slower

In terms of timing of the buying, one of the most popular view in the market sees the Fed buying around USD 500bn of Treasuries in six months, which would correspond to USD 83bn each month, or 1.2% of the overall Treasuries outstanding each month. In its program, the BoE bought an average of GBP 18bn each month, or 2.5% of the total Gilt outstanding each month; the speed of the buying was even higher in the first months of the program. So far, it seems that the Fed QE2 should overall have a milder impact on yields, as we are likely talking about a less massive purchase program both in size and in terms of speed of buying.

In the US, the actual level of both nominal and real yield is more stretched than in the UK ahead of the QE start

Finally, we have to take into consideration that in the US the level of both nominal and real yields is more stretched than the level of yields in UK ahead of the QE start, meaning that yields in the US have much less room to rally.

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 11 See last pages for disclaimer.

Short-term market impact in the negative, neutral and positive scenarios

The table below shows the market impact we expect on nominal yields, real yields and BE in the short term in the three different scenarios outlined above.

Let’s start with the short-term.

■ Negative scenario: Market would be disappointed with both real and nominal yields climbing significantly. Inflation expectations would decline at least a bit.

■ Neutral scenario: Both real and nominal yields should trade sideways around current levels. Inflation expectations remain unchanged.

■ Positive scenario: both real yields and nominal yields would plunge, however nominal yields are unlikely to re-test 2008 lows. Inflation expectations should rise further from the current levels.

Better than expected As expected Worse than expected

RY NY BE RY NY BE RY NY BE

Impact (1st week)

-30/-40b -10/-20bp +15/25bp 0.55% 2.70% 215bp +20/30bp +10/20bp -5/-15bp

Judging the reaction in the medium-term is a bit more complicated, because a view on how

effective the QE would be is required, and not even the FOMC members agree on this point. In this paragraph, we base the reasoning on the assumption that a USD 500/1000bn program would have some positive impact on the US inflation and growth. Hence:

■ Negative scenario: Less buying than USD 500/1000bn would not be enough to support inflation and inflation expectations. After an initial rise, real yields would probably decline a bit to revert, probably, to current levels.

■ Neutral scenario: Under this outcome, real and nominal yields would rise moderately, and so would BE. After all, the Fed would be pouring some money into the economy.

■ Positive scenario: In the medium term real yields would probably rise as a result of improved expectations on the economic cycle. Inflation expectations would pick up relative to current levels, leading to a rise in nominal yields.

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 12 See last pages for disclaimer.

Periphery Calendar Where When What Greece November IMF/EU officials visit Athens to decide on the third tranche of the loan (EUR 9bn) Event

November Eurostat publishes the revised public finance figures for 2009 Event 9-Nov-10 26W, 52W T-bill auction Auction 9-Nov-10 CPI (Oct)/ IP (Sep) Macroeconomic data 11-Nov-10 Unemployment rate (Aug) Macroeconomic data 12-Nov-10 GDP (3Q P) Macroeconomic data 16-Nov-10 13W T-bill auction Auction 19-Nov-10 Current account (Sep) Macroeconomic data 30-Nov-10 Retail sales (Sep) Macroeconomic data 8-Dec-10 CPI (Nov) Macroeconomic data 9-Dec-10 GDP (3Q F)/ Unemployment rate (Sep) Macroeconomic data 10-Dec-10 IP (Oct) Macroeconomic data 14-Dec-10 26W, 52W T-bill auction Auction 21-Dec-10 Current Account (Oct) Macroeconomic data 21-Dec-10 13W T-bill auction Auction 30-Dec-10 Retail sales (Oct) Macroeconomic data

Ireland 1-Nov-10 Manufacturing PMI Macroeconomic data 3-Nov-10 Service PMI/ Unemployment rate (Oct) Macroeconomic data Early November Finance Ministry to publish detailed 4Y plan Event 8/12 Nov-10 IP (Sep)/ Retail sales (Sep) Macroeconomic data 8/15 Nov-10 CPI (Oct) Macroeconomic data 22/26 Nov-10 Trade balance (Sep) Macroeconomic data 1-Dec-10 Manufacturing PMI/ Unemployment rate (Nov) Macroeconomic data 3-Dec Service PMI Macroeconomic data 7-Dec-10 Presentation of Budget for 2011 Event 7/13 Dec10 CPI (Nov)/ IP (Oct) Macroeconomic data 20/27 Dec10 Trade Balance (Oct) Macroeconomic data 28/31 Dec10 Current Account Balance (3Q)/ GDP (3Q) Macroeconomic data

Portugal 3-Nov-10 Debate and vote on general guidelines of draft 2011 budget bill in Parliament Event 3-Nov-10 4M T-bills (EUR 0.5/0.75bn), 12M T-bills (EUR 00.5/0.75bn) Auction 9-Nov-10 Trade Balance (Sep) Macroeconomic data 11-Nov-10 CPI (Oct) Macroeconomic data 12-Nov-10 GDP (4Q P) Macroeconomic data 17-Nov-10 Unemployment rate (3Q) Macroeconomic data 17-Nov-10 12M T-bill auction (EUR 750/1.25bn) Auction 24-Nov-10 Portugal largest union, the CGTP, to hold general strike Event 29-Nov-10 Retail sales (Oct) Macroeconomic data 30-Nov-10 IP (Oct) Macroeconomic data 9-Dec-10 GDP (3Q F) Macroeconomic data 14-Dec-10 CPI (Nov) Macroeconomic data 30-Dec-10 IP(Nov)/ Retails Sales (Nov) Macroeconomic data (-) IGCP will hold one bond auctions offering a total of EUR 1.5 Auction

Source: Reuters, UniCredit Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 13 See last pages for disclaimer.

Real Money Section: Euroland Portfolio Strategy Rocky Horror Picture Show hurts domestic bond market

Michael Rottmann (UniCredit Bank) +49 89 378-15121 [email protected] A wide range of factors put further pressure on EGBs …

"It's just a jump to the left and then a step to the right. With your hands on your hips, you bringyour knees in tight…" This may describes the battle over the idea of a stability pact with teeth.The abandonment of positions and a continuous search for compromise with the risk of losing the hoped-for "teeth" ultimately impacted sentiment towards Europeangovernment bonds across the board. Furthermore, the bickering over austerity packagesin Portugal and the discussion of early elections in Greece are of course poisonous. ECB rhetoric that increasingly sounds like the central bank is determined to forge ahead with the exit strategy as quickly as possible is also taking its toll, driving the total return down to4.33% YTD with our excess return unchanged at 25 bp.

EGB RETURNS, VOLATILITY AND CROSS ASSET CORRELATIONS

5-day return

20-day return

YTD return

20-day return

volatility

YTD return

volatility

60-day return/20-day return correlation

EGBs> 1Y

EGBHICP-ILB

1-10Y

iBoxx EUR Corp. BBB

Euro- Stoxx

DJ AIG Commodity

Oilprice

3M Euribor 0.01 0.05 0.54 0.04 0.03 EGBs >1 1 0.61 0.77 -0.47 -0.04 -0.12EGBs >1Y -0.42 -0.51 4.33 3.41 3.55 EGB HICP-ILB 1-10Y 0.70 1 0.45 -0.21 0.16 0.01EGBs 1-3Y -0.13 -0.01 1.30 1.07 1.77 iBoxx EUR Corp. BBB 0.73 0.57 1 -0.41 -0.05 -0.25EGBs 3-5Y -0.33 -0.25 3.11 2.25 3.00 EuroStoxx -0.12 -0.06 0.03 1 0.43 0.44EGBs 5-7Y -0.45 -0.46 3.99 3.24 3.75 DJ AIG Commodity 0.40 0.40 0.26 0.29 1 0.61EGBs 7-10Y -0.64 -0.65 4.15 4.56 4.72 Oil price 0.41 0.29 0.00 0.20 0.65 1EGBs >10Y -0.58 -1.11 8.75 6.31 6.20 EGB HICP-ILB 1-10Y -0.38 -0.45 2.52 2.79 3.40

Source: Bloomberg, UniCredit Research

… and given the almost unpredictable response to the outcome of the FOMC-meeting … … we keep a neutral duration stance

From a domestic standpoint, the ECB press conference next week is consequently of paramount importance. Details on the future timing of the exit strategy will most likely held back until the December meeting, but we see few chances for "dovish" overtones. There is, therefore, the fear that the money market forwards will shift slightly higher again and pull the long end up with them, even though developments here will depend to a very large extent on US influences. In the US, by far the most interesting FOMC meeting in several months is on the agenda, and the usual data heavyweights. There has been no end to the metaphors. Rogoff compared the US strategy to a bunker shot in golf. What is needed here in his view is an explosion shot – the stronger the better. Whether you overshoot the green is irrelevant, the main thing is that you are out of the bunker. Using a turkey Thanksgiving analogy in an article entitled "Run Turkey Run", Bill Gross espoused the view that - one way or another - the FOMC announcement on Wednesday will mark the final turning point at the long end. But what is more important than a volume of USD 400 or 600bn is the message between the lines. If investors conclude that the US central bank will continue this program doggedly until, for example, an annual rate of change in the core deflator of 2% or higher is reached, the reaction is likely to be positive. There is reason todoubt whether there will already be such a commitment in the current situation where FOMC members are in some cases espousing diametrically opposing views. Overall, there is the fear that the current rise in yields at the long end in the euro zone is not over yet and we stick to the neutral duration position.

EGBS: EXPECTED RETURNS AND PORTFOLIO RECOMMENDATION

Modified Duration in Years Effas Benchmark weighting Recommended UniCredit weighting3M Euribor 0.25 0EGBs 1-3Y 1.80 24.20 24EGBs 3-5Y 3.60 19.70 20EGBs 5-7Y 5.21 11.71 11EGBs 7-10Y 7.05 18.69 19EGBs >10Y 12.43 25.70 26EGB HICP-ILB 1-10Y 5.28 0Average Duration 6.27 6.30

Source: Bloomberg, UniCredit Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 14 See last pages for disclaimer.

Real Money Section: Euroland Country Strategy

No changes ahead of FOMC meeting Elia Lattuga (UniCredit Bank Milan) +39 02 88622027 [email protected]

EMU bonds delivered a negative performance last week, especially Greece and Ireland. FI markets have been on a wait-and-see mood during the last weeks, with investors adjusting their positions ahead of the next FOMC meeting. Renewed concerns on the fiscal outlook ofGreece, Ireland and Portugal weighted on the performance of periphery. Greece has been particularly hit with the 10Y yield rising again to above10%. Thin market volumes favoredlarge yield swings.

The EFFAs index lost 0.48%, after last week rebalancing on peripheral countries, our portfolioperformed slightly better than the market. The main benefit came from Belgium, which wasthe best performer of the week.

Next week, we expect gross supply to be ca EUR 20bn, mainly coming from core countries(France, Germany and Finland). Among periphery, Spain will sell a new 5Y Bono while Portugal will sell T-bills. Supply will not be too friendly.

We decide not to make major changes ahead of next week’s FOMC meeting. We remain overweigh Belgium among core-mid countries and Italy among periphery.

EFFAS redemption yield EFFAS weekly returns

2

3

4

5

6

7

8

9

10

11

GR IE PT ES IT BE AT FR NL DE FI

Core Mid Periphery

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

BE PT AT FR FI ES NL DE IT IE GR

weekly performance

Source: Bloomberg, UniCredit Research EGB COUNTRY RECOMMENDATION >1Y YTM Duration YTD return Last week return EFFAS weighting Our weighting Ch. since last week Over / Under w.Austria 2.81 6.61 8.60% -0.29% 4.0% 4.5% 0.5%Belgium 3.08 6.04 5.26% -0.01% 6.0% 7.5% 1.5%Germany 2.49 6.20 7.57% -0.39% 21.6% 19.5% -2.1%Spain 4.10 5.86 1.74% -0.34% 9.9% 10.5% 0.6%Finland 2.37 5.39 6.83% -0.30% 1.3% 0.0% -1.3%France 2.78 6.75 7.48% -0.29% 21.0% 19.5% -1.5%Greece 10.14 4.56 -14.96% -3.68% 3.6% 3.5% -0.1%Ireland 6.31 5.17 -5.73% -1.30% 2.0% 1.5% -0.5%Italy 3.96 6.52 3.44% -0.44% 23.0% 26.0% 3.0%Netherlands 2.58 6.34 7.55% -0.35% 5.5% 5.5% 0.0%Portugal 5.45 5.59 -5.15% -0.22% 2.1% 2.0% -0.1%Eurozone 3.45 6.27 4.19% -0.48%

SUMMARY

Yield 3.51 3.54

Duration 6.27 6.28

YTD return 4.32% 4.15%

Tot. Ret. Last week -0.48% -0.47%

Source: Bloomberg, UniCredit Research (all tables and charts on this page)

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 15 See last pages for disclaimer.

Total Return Monitor

TOTAL RETURN YTD OF FIXED INCOME ASSETS

1.3

13.4

2.6

10.3

2.7

5.2

0.2

13.4

2.6

10.1

2.5

5.5

0.5

18.2

7.0

5.9

19.7

4.0

13.7

25.7

0

5

10

15

20

25

30

35

Euro 7-10 Euro 1-3 US 7-10 US 1-3 UK 7-10 UK 1-3 JP 7-10 JP 1-3

Tota

l ret

urn

(%)

Asset return Hedged EUR Eur return

TOTAL RETURN YTD OF CURRENCIES AND EQUITIES

4.3

3.1

19.4

8.7

4.5

8.7

-13.

6

2.7

19.3

14.6

8.9

8.7

3.1 5.

9

24.4

19.5

-20-16-12-8-4048

121620242832

USD GBP JPY CHF S&P DAX Nikkei FTSE Gold CRB

Tota

l ret

urn

(%)

Asset return Eur return

TOTAL RETURN BY COUNTRY AND MATURITY BUCKET

Euro 7-10

Euro 1-3

US 7-10

US 1-3 UK 7-10

UK 1-3

JP 7-10

JP 1-3

1W -0.68 -0.13 -0.69 0.01 -1.39 -0.16 -0.08 0.01 1M -0.88 -0.07 -0.57 0.16 -0.96 -0.02 0.37 0.01

TOTAL RETURN BY ASSET CLASS EUROZONE (2010 YTD)

5.3

9.6

5.7

-0.9

1.6

4.5

4.0

3.4

3.3

1.8

3.8

6.7

4.1

1.3

2.5

2.2

1.9

3.6 4.

1

1.0

4.3

-0.1

7.6

9.5

3.5

-0.1

3.5 3.9

6.9

2.4

9.8

2.0

-4

-2

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010

YTD

tota

l ret

urn

(%).

Euro 7-10 Euro 1-3 CCT ILB

TOTAL RETURN BY COUNTRY AND MATURITY BUCKET

USD GBP JPY CHF S&P DAX Nikkei

FTSE

Gold CRB

1W 0.93 2.33 1.70 -0.18 0.06 -0.43 -2.38 -1.61 0.66 0.91 1M -0.2 0.3 2.8 -1.7 3.3 5.9 -2.1 1.0 1.4 1.7

TOTAL RETURN BY ASSET CLASS US (2010 YTD)

3.3 4.

9

2.8

2.5

10.1

-5.2

13.4

2.4

1.0

3.8

7.3

6.4

0.9 2.

6

7.9

7.5

2.3

1.4

11.3

-2.6

6.5

17.2

1.8

12.0

-10

-5

0

5

10

15

20

2003 2004 2005 2006 2007 2008 2009 2010

YTD

tota

l ret

urn

(%).

US 7-10 US 1-3 ILB

TOTAL RETURN YTD BY COUNTRY AND MATURITY BUCKET

Maturity bucket DE FR AT FI NL BE ES PT IT GR IE EU 1 -3 1.53% 1.69% 2.13% 2.04% 1.73% 1.64% 0.96% 0.96% 1.42% -3.31% -0.41% 1.22% 3 -5 4.84% 4.71% 5.18% 4.83% 4.95% 3.50% 2.52% -1.59% 2.85% -11.21% - 3.02% 5 - 7 6.84% 6.60% 7.29% 4.39% 6.85% 4.43% 2.64% -3.39% 3.77% -18.14% -5.12% 3.90% 7 - 10 8.87% 8.55% 8.98% 9.02% 9.00% 5.95% 2.33% -6.59% 4.47% -22.02% -7.93% 4.05% >1 7.59% 7.50% 8.66% 6.85% 7.57% 5.31% 1.74% -5.11% 3.46% -14.88% -5.72% 4.21% SPREAD TO DE 1 -3 - 0.16% 0.60% 0.51% 0.20% 0.11% -0.57% -0.57% -0.11% -4.84% -1.94% -0.31% 3 -5 - -0.13% 0.34% -0.01% 0.11% -1.34% -2.32% -6.43% -1.99% -16.05% - - 5 - 7 - -0.25% 0.45% -2.46% 0.01% -2.41% -4.21% -10.23% -3.08% -24.98% -11.96% -2.94% 7 - 10 - -0.32% 0.10% 0.15% 0.13% -2.92% -6.54% -15.46% -4.40% -30.89% -16.80% -4.82% >1 - -0.09% 1.07% -0.74% -0.02% -2.28% -5.85% -12.70% -4.13% -22.47% -13.31% -3.38%

Total return for the following combinations of bucket & countries are calculated using EFFAS indices of total return: EUR 7-10, EUR 1-3, US 7-10, US 1-3, UK 7-10, UK 1-3, JP 7-10, JP 1-3. CCTs total return is calculated using MTS index

Source: Bloomberg, EFFAS, UniCredit Research (all tables and charts in this page)

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 16 See last pages for disclaimer.

Money Market Monitor

High demand at 3M LRO does not reflect higher MM tension Luca Cazzulani (HVB) +39 02 8862 0640 [email protected]

Demand at the 1W MRO was in line with the past week (EUR 183bn), but the number ofbanks participating in the auction increased sizably. This has led to a fall in the averageallotted size.

Demand at the 3M LTRO increased EUR 20bn …

The 3M LTRO was somewhat of a surprise: demand was EUR 42bn, well above the EUR23bn expiring. The number of banks participating in the auction was 132, higher than the 70 banks that participated in the end of July auction of the 3M LTRO that expired on Wednesday. The average bid size was EUR 300mn/bidder, in line with the expiring auction.

… we think this is mostly related to the recent rise in MM rates …

The increase in demand is most likely due to the recent rise in Euribor that has brought the rate above the 1% level. Even if the two rates are not directly comparable, the rise in the3M Euribor is a good thermometer of market expectations, and its recent rise suggestsseveral banks preferred to bid at the ECB and secure funds for three months at 1%. The increase in demand, hence, does not reflect an increase in tensions on the moneymarket, but rather the banks' response to the current level of rates.

… the year-end effect has probably supported demand

The approach of the end of the year has probably been also a factor supportive fordemand: the recent 3M LTRO will expire in January.

The increase in demand does not change our expectations for the exit strategy

From a monetary policy perspective, the outcome of the 3M LTRO does not change our expected path for the exit strategy (the full allotment at the 3M LTRO will not be extended into 2011, while it will remain at the 1W MRO, at least in 1Q). If anything, this week outcome shows that the full allotment is creating some distortions in demand for liquidity and offersarguments for removing it as soon as possible.

We expect the 3M Euribor to stabilize at current levels or even fall back to 1%. Actually, the recent fixings point already in this direction. Shorter maturities (the EONIA, the 1W, the 1M) have dropped consistently. At the end of November, there will be another 3M LTRO(EUR 19bn will expire, 49 banks participated to the auction in August). If the 3M Euribor willstill be above the 1% level, we expect an outcome similar to the one we had this week.

Demand at 3M LTRO in the next months:

Demand at the 3M LTRO in the next few months will come from: - Banks with still difficult access to liquidity - Banks with easy access to liquidity but which will bid at the ECB as long as it’s cheaper than the market. Hence, as long as the full allotment framework remains in place, bank demand at ECB refinancing operations will keep excess liquidity at a level that stabilizes MM rates (up to the 3M tenor) at 1% (or less).

KEY CHARTS

Excess liquidity in the EMU Normalization, at last

-100

-50

0

50

100

150

200

250

300

350

400

May-07 Nov-07 May-08 Nov-08 May-09 Nov-09 May-10 Nov-10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

Refi 1M OIS EONIA Depo

Source: Bloomberg, UniCredit Global Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 17 See last pages for disclaimer.

Short maturities have been more affected by the 3M LTRO

The result of the recent 3M LTRO has had an important impact on short maturities. The EONIA has fallen some 20bp in the last few days and the 1W OIS has experienced a similardecline.

Compared to a month ago, the OIS curve has moved up with a parallel movement. The 1MOIS is now projected to reach 1% by the end of the year and to trade at 1.25% at the end of 2011. We regard the first target as possibly a bit too high, while the second one is in line withour expectations.

Next week should be a rather quiet week on the MM side, at least in the eurozone. There are several central bank meetings but only the Fed meeting will be a real market mover, while the ECB and BOE meetings should have a very moderate market impact.

KEY MONEY MARKET CHARTS

1M OIS forward Euribor futures before and after the 12M LTRO expiry

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

Jan-09 Jul-09 Dec-09 Jul-10 Dec-10 Jun-11 Dec-11

Refi 1M OIS 1-Oct-10 29-Oct-10

0.50

0.75

1.00

1.25

1.50

1.75

2.00

Jan-09 Jul-09 Feb-10 Aug-10 Mar-11 Sep-11 Apr-12

3M EU Strip nowStrip @ 01-Oct-10 3M (e)key rate

Source: Bloomberg, UniCredit Global Research

EUROSYSTEM: LIQUIDITY CONDITIONS AT A GLANCE (EUR BN) Liquidity demand Liquidity supply Excess liquidity Use of excess Res. requirement Autonomous fact. Total ECB overnight Exc. Reserves1W ch. 0.0 11.1 11.1 19 8 16 -81M ch. 2.1 -10.5 -8.4 -60 -51 -36 -1528-Oct-10 214 269 483 531 48 37 1121-Oct-10 214 258 472 513 41 22 1922-Sep-10 212 280 491 591 99 73 26

ECB LIQUIDITY CALENDAR

Expiry schedule Upcoming auction calendar 1w 1m 3m 6m 12m total 1W 1M 3M Other03-Nov-10 183 52 235.6 2-Nov-10 9-Nov-10 24-Nov-10 11-Nov-10 (6D)11-Nov-10 36 35.7 9-Nov-10 7-Dec-10 22-Dec-10 23-Dec-10 (13D)25-Nov-10 19 19.1 16-Nov-10 23-Dec-10 104 97 200.9 23-Nov-10 27-Jan-11 43 42.5 30-Nov-10 7-Dec-10 14-Dec-10 21-Dec-10

Auction calendar report the auction dates (settlement is t+1). Figures in EUR bn - Source: ECB, UniCredit research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 18 See last pages for disclaimer.

Euribor rates: historical movements and expectations 3M EURIBOR STRIP (RATES, %)***

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

Current 1st (Dec10 ) 2nd (Mar11 ) 3rd (Jun11 ) 4th (Sep11 )

Strip now Strip @ 29-Sep-10 3M (e) keyrate (e)

3M USD LIBOR STRIP (RATES, %)***

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Current 1st (Dec10 ) 2nd (Mar11 ) 3rd (Jun11 ) 4th (Sep11 )

Strip now Strip @ 29-Sep-10 3M (e) keyrate (e)

3M GBP LIBOR STRIP (RATES, %)***

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Current 1st (Dec10 ) 2nd (Mar11 ) 3rd (Jun11 ) 4th (Sep11 )

Strip now Strip @ 29-Sep-10 3M (e) keyrate (e)

3M 6M BASIS SWAP

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Jun-02 Dec-03 Jun-05 Dec-06 Jun-08 Dec-09

3M 6M EUR

***. Triangles are the difference between the Euribor future with maturity are the indicated date and the 3M forward on the OIS curve, starting from the expiration date of the future. For example, the Mar09 triangles is the difference between the Euribor future expiring in Mar09 and the 3M forward on the OIS curve starting on the expiration date.

MONEY MARKET RATES RECENT CHANGES

Refi EONIA Euribor OIS Euribor / OIS 1M 3M 6M 12M 1M 3M 6M 12M 1M 3M 6M 12MLast M 1.00 0.70 0.79 1.00 1.23 1.50 0.74 0.76 0.81 0.89 5 24 42 61Last 3M 1.00 0.52 0.67 0.92 1.16 1.44 0.55 0.60 0.65 0.74 12 32 51 70Last week 1.00 0.83 0.84 1.04 1.26 1.53 0.78 0.82 0.88 0.98 6 23 38 55 1W ch. 0.0 -6.4 2.5 1.6 1.7 1.9 3.8 5.0 3.9 2.8 -1.3 -3.4 -2.2 -0.91M ch. 0.0 11.5 12.1 9.2 7.6 7.0 11.2 13.6 15.5 16.4 0.9 -4.4 -7.9 -9.43M ch. 0.0 23.0 23.6 17.5 14.5 14.8 19.0 20.4 20.4 20.8 4.6 -2.9 -5.9 -6.01Y ch. 0.0 46.1 42.1 32.5 26.6 30.2 37.0 38.0 37.4 23.3 5.1 -5.5 -10.8 6.9

The first three rows of the above table show average values computed on monthly, quarterly and weekly horizons. Row five to eight display the bp rate changes vs. the values recorded 1 week, month, quarter and year ago.

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 19 See last pages for disclaimer.

Swap Monitor SWAP CURVE: PAST, SPOT, 6M FRA

1.6

1.9

2.7

5.7

5.84.8

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0 5 10 15 20 25 30Maturity (years)

29-Oct-10 3 months ago Forward 6M

Numbers denote the 1w bp change in yields

ROLLDOWN &CARRY (6M HORIZON)

0

2

4

6

8

10

12

14

16

18

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30

maturity (years)

bp

Today 1 week ago

2 & 5 YEAR SWAP RATE: WHAT FORWARDS TELL US

Cur

rent

: 59

3m: 5

7

6m: 5

8

9m: 5

7

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

2Y swap rate (%) 5Y swap rate (%) Forward rates

Numbers denote the spread in bp

10 & 30 YEAR SWAP RATE: WHAT FORWARDS TELL US

9m: 2

6m: 7

3m: 1

1

Cur

rent

: 17

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

10Y swap rate (%) 30Y swap rate (%) Forward rates

Numbers denote the spread in bp

10&30 AND 2&30 SPREADS: HISTORY AND FORWARD

140

3m 6m 9m

-100

-50

0

50

100

150

200

250

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11

10/30Y spread (bp)

2/30Y spread (bp)

2/10Y spread (bp)

Forward spread

SWAP RATES AT A GLANCE

Average Cheap / rich Last Short term

(last 6M) Long term

(Jan99)Short term

(last 6M) Long term

(Jan99)2Y 1.60 1.37 3.38 CCCC EEEE5Y 2.18 2.04 3.89 CCC EEEE10Y 2.83 2.80 4.40 E EEEE15Y 3.13 3.15 4.65 E EEEE30Y 2.99 3.11 4.77 E EEEE

Cheap and rich indicators are base on distribution percentiles. EEEE=Very expensive, E= Expensive, CCCC=Very cheap, C=cheap. Valuations are from the investor’s perspective.

5Y SWAP-OPTION VOLA AT 5Y TENOR

22.59

13.6

16.0

8

10

12

14

16

18

20

22

24

26

28

Jan-99 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

Swaption vola (5Y) average since 1999 average since Aug07

SWAP CURVE AT A GLANCE

Average Cheap / rich Last Short term

(last 6M)Long term

(Jan99) Short term

(last 6M)Long term

(Jan99)2/5 58 67 49 EE -5/10 65 76 49 EEE C10/15 30 35 25 EEEE C15/30 -13 -4 11 EEEE EEEE2/5/10 -3 -5 0 CC E10/15/30 22 19 7 CCC CCCC

Source: Bloomberg, UniCredit Research

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 20 See last pages for disclaimer.

Relative Value Monitor Greek spreads widen significantly

Elia Lattuga (UniCredit Bank Milan) +39 02 8862 2027 [email protected]

This week was characterized by choppy trading as investors' focus was on the upcoming FOMC meeting. Overall, Bund and UST yields moved up a bit. Peripheral countries delivereda very volatile performance (especially Ireland and Portugal). Most of EMU issuers moved inline with the swap curve, at the 30Y maturity most countries widened several bp. The dramatic sell-off hitting Greek bonds triggered a widening of GGBs vs. swap and vs.Germany, particularly at the belly and at the 10Y maturity. The GGBs ASW spread vs.Germany approached 790bp at the 5Y and 650bp at the 10Y.

1-WEEK ASW CHANGE (BP) 5Y MATURITY ASW SPREAD VS. GERMANY (BP)

-10

0

10

20

30

40

50

60

70

80

BE FR NL AT GE PT IT SP GR

13 18 3266

107144

263

789

0

100

200

300

400

500

600

700

800

900

NL FR AT BE IT SP PT GR

10Y MATURITY

-10

0

10

20

30

40

50

60

BE FR NL AT GE PT IT SP GR

21 33 4178

129154

305

647

0

100

200

300

400

500

600

700

NL FR AT BE IT SP PT GR

30Y MATURITY

-2

0

2

4

6

8

10

12

14

PT BE AT GE NL FR IT SP GR

1136 41

81

174188

237

369

0

50

100

150

200

250

300

350

400

NL AT FR BE IT SP PT GR

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 21 See last pages for disclaimer.

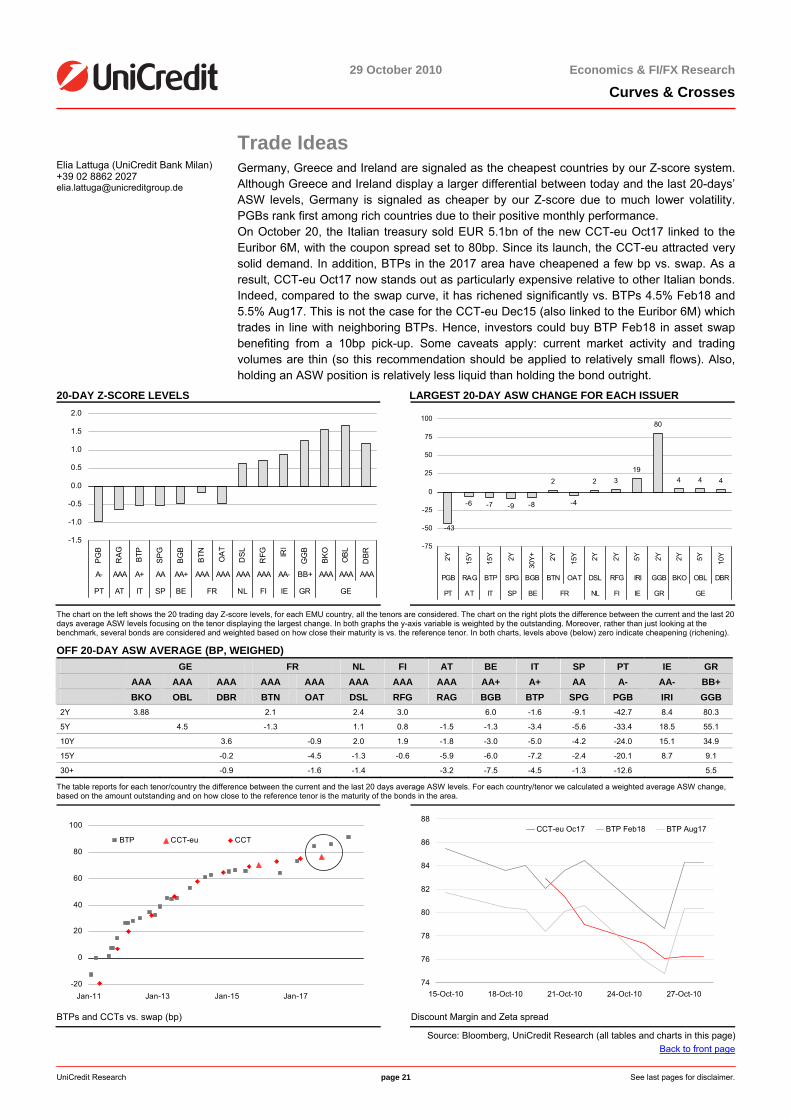

Trade Ideas Elia Lattuga (UniCredit Bank Milan) +39 02 8862 2027 [email protected]

Germany, Greece and Ireland are signaled as the cheapest countries by our Z-score system. Although Greece and Ireland display a larger differential between today and the last 20-days’ ASW levels, Germany is signaled as cheaper by our Z-score due to much lower volatility. PGBs rank first among rich countries due to their positive monthly performance. On October 20, the Italian treasury sold EUR 5.1bn of the new CCT-eu Oct17 linked to the Euribor 6M, with the coupon spread set to 80bp. Since its launch, the CCT-eu attracted very solid demand. In addition, BTPs in the 2017 area have cheapened a few bp vs. swap. As aresult, CCT-eu Oct17 now stands out as particularly expensive relative to other Italian bonds.Indeed, compared to the swap curve, it has richened significantly vs. BTPs 4.5% Feb18 and5.5% Aug17. This is not the case for the CCT-eu Dec15 (also linked to the Euribor 6M) which trades in line with neighboring BTPs. Hence, investors could buy BTP Feb18 in asset swapbenefiting from a 10bp pick-up. Some caveats apply: current market activity and trading volumes are thin (so this recommendation should be applied to relatively small flows). Also, holding an ASW position is relatively less liquid than holding the bond outright.

20-DAY Z-SCORE LEVELS LARGEST 20-DAY ASW CHANGE FOR EACH ISSUER

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

PG

B

RA

G

BTP

SP

G

BG

B

BTN OA

T

DS

L

RFG IR

I

GG

B

BK

O

OB

L

DB

R

A- AAA A+ AA AA+ AAA AAA AAA AAA AA- BB+ AAA AAA AAA

PT AT IT SP BE FR NL FI IE GR GE

-6 -7 -9 -8

2

-4

2 319

80

4 4 4

-43

-75

-50

-25

0

25

50

75

100

2Y 15Y

15Y 2Y

30Y+ 2Y 15Y 2Y 2Y 5Y 2Y 2Y 5Y 10Y

PGB RAG BTP SPG BGB BTN OAT DSL RFG IRI GGB BKO OBL DBR

PT AT IT SP BE FR NL FI IE GR GE

The chart on the left shows the 20 trading day Z-score levels, for each EMU country, all the tenors are considered. The chart on the right plots the difference between the current and the last 20 days average ASW levels focusing on the tenor displaying the largest change. In both graphs the y-axis variable is weighted by the outstanding. Moreover, rather than just looking at the benchmark, several bonds are considered and weighted based on how close their maturity is vs. the reference tenor. In both charts, levels above (below) zero indicate cheapening (richening).

OFF 20-DAY ASW AVERAGE (BP, WEIGHED) GE FR NL FI AT BE IT SP PT IE GR AAA AAA AAA AAA AAA AAA AAA AAA AA+ A+ AA A- AA- BB+ BKO OBL DBR BTN OAT DSL RFG RAG BGB BTP SPG PGB IRI GGB 2Y 3.88 2.1 2.4 3.0 6.0 -1.6 -9.1 -42.7 8.4 80.3

5Y 4.5 -1.3 1.1 0.8 -1.5 -1.3 -3.4 -5.6 -33.4 18.5 55.1

10Y 3.6 -0.9 2.0 1.9 -1.8 -3.0 -5.0 -4.2 -24.0 15.1 34.9

15Y -0.2 -4.5 -1.3 -0.6 -5.9 -6.0 -7.2 -2.4 -20.1 8.7 9.1

30+ -0.9 -1.6 -1.4 -3.2 -7.5 -4.5 -1.3 -12.6 5.5

The table reports for each tenor/country the difference between the current and the last 20 days average ASW levels. For each country/tenor we calculated a weighted average ASW change, based on the amount outstanding and on how close to the reference tenor is the maturity of the bonds in the area.

-20

0

20

40

60

80

100

Jan-11 Jan-13 Jan-15 Jan-17

BTP CCT-eu CCT

BTPs and CCTs vs. swap (bp)

74

76

78

80

82

84

86

88

15-Oct-10 18-Oct-10 21-Oct-10 24-Oct-10 27-Oct-10

CCT-eu Oc17 BTP Feb18 BTP Aug17

Discount Margin and Zeta spread

Source: Bloomberg, UniCredit Research (all tables and charts in this page) Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 22 See last pages for disclaimer.

EGB spread monitor: yield spreads vs. Germany (bp) Country Bond 10Y yield Spread vs. DE 1W ch. (bp) 1M ch. (bp) All-time high All-time low DE DBR 2.25 Sep-20 2.54 - NL NETHER 3.5 Jul-20 2.75 21 -1 -1 87 17-Feb-09 -9.4 20-May-05 FI RFGB 3.375 Apr-20 2.76 22 0 -3 89 21-Jan-09 -9.2 25-Nov-05 FR FRTR 2.5 Oct-20 2.93 39 -1 2 63 9-Mar-09 -1.4 11-Jul-03 AT RAGB 3.9 Jul-20 2.93 39 -1 -12 137 18-Feb-09 -7 21-Apr-06 BE BGB 3.75 Sep-20 3.36 82 -5 1 138 22-Jan-09 -3.5 27-Jan-05 IT BTPS 3.75 Mar-21 3.94 140 3 -17 178 8-Jun-10 3.5 2-Jul-03 ES SPGB 4.85 Oct-20 4.20 166 0 -15 221 16-Jun-10 -5.9 25-Nov-04 PT PGB 4.8 Jun-20 6.04 350 11 -34 427 28-Sep-10 -3.2 7-Mar-05 IE IRISH 5 Oct-20 6.94 440 35 37 449 28-Sep-10 -6.9 14-Jan-04 GR GGB 6.25 Jun-20 10.71 817 129 31 965 7-May-10 8.1 18-Feb-05

AAA GROUP NOT AAA GROUP 5Y MATURITY

-20

0

20

40

60

80

100

120

140

160

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

5Y FR-DE 5Y AT-DE 5Y NL-DE

5Y MATURITY

0

200

400

600

800

1000

1200

1400

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

5Y IT-DE 5Y GR-DE 5Y PT-DE

5Y BE-DE 5Y ES-DE

10Y MATURITY

0

20

40

60

80

100

120

140

160

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

10Y FR-DE 10Y AT-DE 10Y NL-DE

10Y MATURITY

0

100

200

300

400

500

600

700

800

900

1000

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

10Y IT-DE 10Y GR-DE 10Y PT-DE

10Y BE-DE 10Y ES-DE

30Y MATURITY

0

20

40

60

80

100

120

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

30Y FR-DE 30Y AT-DE 30Y NL-DE

30Y MATURITY

0

100

200

300

400

500

600

700

Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

30Y IT-DE 30Y GR-DE 30Y PT-DE30Y BE-DE 30Y ES-DE

Note: We use Bloomberg generics for all issuers across maturities Source Bloomberg, UniCredit Research (for all charts in this page) Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 23 See last pages for disclaimer.

Inflation Monitor

Eurozone October inflation: a tad higher than expected Marco Valli (UniCredit Bank Milan) +39 02 8862 8688 [email protected]

• The flash estimate showed that eurozone inflation in October was a tad higher than we had expected, showing an acceleration to 1.9% yoy vs. the previous 1.8%. We and consensushad penciled in a stable outcome. On a monthly basis, prices probably rose 0.3%. Theflash estimate is consistent with HICP ex tobacco printing at 1.8% yoy.

• Judging from the limited information available at the country level, we think that the upsidesurprise with respect to our forecast was mostly driven by core items, while food andenergy inflation seems to have moved broadly in line with our forecast. For the final release, we see risks skewed towards a downward revision of the preliminary estimate.

• In Italy, October CPI was reported at +0.2% mom, +1.7% yoy. The monthly reading was0.1pp higher than we had expected, while the yearly rate was on track. The data breakdown shows unusually solid gains in leisure/culture and hotels/restaurants prices,which we suspect hide some changes in the usual seasonal pattern. If this reading iscorrect, today’s upside surprise on these price categories should be reversed inNovember.

• We don’t expect eurozone inflation to rise further from the current level for several months.

• Our year-end inflation target in the eurozone remains 1.8% yoy.

US INFLATION-LINKED MARKET

0.0

0.5

1.0

1.5

2.0

2.5

3.0

BE 30Y BE 10Y BE 5Y 5Y5Y FFWD Inflation

L-T 1Y 6M Last

EU INFLATION-LINKED MARKET

0.0

0.5

1.0

1.5

2.0

2.5

3.0

BE 30Y BE 10Y BE 5Y 5Y5Y FFWD Inflation

L-T 1Y 6M Last

Source: Bloomberg, UniCredit Research

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 24 See last pages for disclaimer.

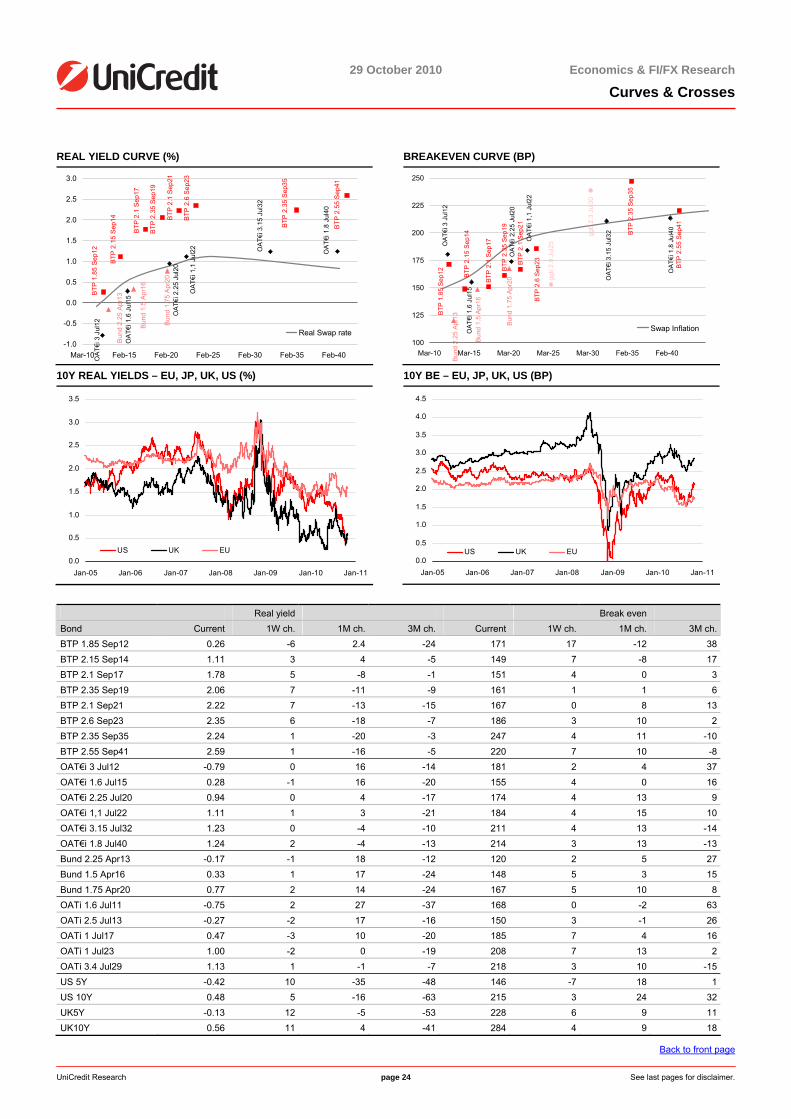

REAL YIELD CURVE (%)

BTP

2.6

Sep

23

BTP

2.1

Sep

21

BTP

2.3

5 S

ep19

BTP

2.1

Sep

17

BTP

2.1

5 S

ep14

BTP

1.8

5 S

ep12

BTP

2.3

5 S

ep35

BTP

2.5

5 S

ep41

OAT

€i 3

Jul

12

OAT

€i 1

.6 J

ul15

OA

T€i 2

.25

Jul2

0

OA

T€i 1

,1 J

ul22 O

AT€

i 3.1

5 Ju

l32

OA

T€i 1

.8 J

ul40

Bun

d 2.

25 A

pr13

Bun

d 1.

5 A

pr16

Bun

d 1.

75 A

pr20

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mar-10 Feb-15 Feb-20 Feb-25 Feb-30 Feb-35 Feb-40

Real Swap rate

BREAKEVEN CURVE (BP)

BTP

2.55

Sep

41

BTP

2.35

Sep

35

BTP

1.85

Sep

12 BTP

2.15

Sep

14

BTP

2.1

Sep1

7

BTP

2.35

Sep

19

BTP

2.1

Sep2

1

BTP

2.6

Sep2

3

OAT

€i 1

.8 J

ul40

OA

T€i 3

.15

Jul3

2

OAT

€i 1

,1 J

ul22

OAT

€i 2

.25

Jul2

0

OAT

€i 1

.6 J

ul15

OAT

€i 3

Jul

12

Bund

1.7

5 Ap

r20

Bund

1.5

Apr

16

Bund

2.2

5 Ap

r13

ggb

2.3

Jul3

0

ggb

2.9

Jul2

5

100

125

150

175

200

225

250

Mar-10 Mar-15 Mar-20 Mar-25 Mar-30 Feb-35 Feb-40

Swap Inflation

10Y REAL YIELDS – EU, JP, UK, US (%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

US UK EU

10Y BE – EU, JP, UK, US (BP)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

US UK EU

Real yield Break even Bond Current 1W ch. 1M ch. 3M ch. Current 1W ch. 1M ch. 3M ch.BTP 1.85 Sep12 0.26 -6 2.4 -24 171 17 -12 38BTP 2.15 Sep14 1.11 3 4 -5 149 7 -8 17BTP 2.1 Sep17 1.78 5 -8 -1 151 4 0 3BTP 2.35 Sep19 2.06 7 -11 -9 161 1 1 6BTP 2.1 Sep21 2.22 7 -13 -15 167 0 8 13BTP 2.6 Sep23 2.35 6 -18 -7 186 3 10 2BTP 2.35 Sep35 2.24 1 -20 -3 247 4 11 -10BTP 2.55 Sep41 2.59 1 -16 -5 220 7 10 -8OAT€i 3 Jul12 -0.79 0 16 -14 181 2 4 37OAT€i 1.6 Jul15 0.28 -1 16 -20 155 4 0 16OAT€i 2.25 Jul20 0.94 0 4 -17 174 4 13 9OAT€i 1,1 Jul22 1.11 1 3 -21 184 4 15 10OAT€i 3.15 Jul32 1.23 0 -4 -10 211 4 13 -14OAT€i 1.8 Jul40 1.24 2 -4 -13 214 3 13 -13Bund 2.25 Apr13 -0.17 -1 18 -12 120 2 5 27Bund 1.5 Apr16 0.33 1 17 -24 148 5 3 15Bund 1.75 Apr20 0.77 2 14 -24 167 5 10 8OATi 1.6 Jul11 -0.75 2 27 -37 168 0 -2 63OATi 2.5 Jul13 -0.27 -2 17 -16 150 3 -1 26OATi 1 Jul17 0.47 -3 10 -20 185 7 4 16OATi 1 Jul23 1.00 -2 0 -19 208 7 13 2OATi 3.4 Jul29 1.13 1 -1 -7 218 3 10 -15US 5Y -0.42 10 -35 -48 146 -7 18 1US 10Y 0.48 5 -16 -63 215 3 24 32UK5Y -0.13 12 -5 -53 228 6 9 11UK10Y 0.56 11 4 -41 284 4 9 18

Back to front page

29 October 2010 Economics & FI/FX Research

Curves & Crosses

UniCredit Research page 25 See last pages for disclaimer.

Supply Corner: The week ahead

Focus on the new 5Y benchmark from Spain Weekly recap

Chiara Cremonesi (UniCredit Bank London) +44 207 826 1771 [email protected]

The leading theme of the week was a progressive deterioration in the sentiment on periphery, especially on Ireland, Portugal and Greece. Results at the Spanish T-bill and Portuguese bond auctions were not up to the standards of the previous auctions; nevertheless, demand held up rather well considering the difficult environment. As expected, demand at the Italian auctions was healthy.

Italian and Spanish T-bill auctions The Italian 6M BOT auction on Tuesday was well received, while Spain did not collect themaximum of the range announced with the 3M & 6M T-bills sale.

Portugal On Wednesday, Portugal sold EUR 0.611bn of OT Oct 2014 and EUR 0.614bn of OTJun2018, overall EUR 1.225bn, towards the upper end of the announced range (EUR0.75/1.25). Demand was less strong than at previous auctions, with OT Jun18 registering a 1.7x bid to cover and OT Oct14 registering a 2.8x bid-to-cover. Portugal managed to sell both bonds at an average yield below market level ahead of the auction. However, one has to takeinto consideration that both bonds were under pressure yesterday. While the auction results compare unfavorably with the previous Portuguese auctions, they were still rather decent taking into account that negotiations on the 2011 budget between thegovernment and the opposition are still ongoing and there is a lot of uncertainty on this issue (note that the opposition interrupted the talks right after the auction). With this auction, YTD Portugal has issued EUR 19.725bn, completing 94% of theissuance target for this year. We expect Portugal to hold another auction until year end to complete its yearly funding.

The new 3Y benchmark from Italy Yesterday, the Italian Treasury sold EUR 4bn of the new 3Y benchmark, BTP Nov11 andEUR 3.25bn of BTP Mar2. The auction went well. Overall, Italy sold EUR 7.25bn, the maximum of the range announced. BTP Mar21 was sold at 3.89%, roughly corresponding to the level where the 10Y benchmark was sold one monthago (3.90%). The new 3Y benchmark was sold at 2.32%, 11bp higher than the level of the 3Yat the end of September auction (the Treasury sold BTP Jun13 back then). The higher yield, however, is entirely due to the longer maturity of the new benchmark. Bid-to-cover ratios were 1.41x for the 10Y and 1.34x for the new 3Y, only slightly lower thanat the previous auctions (1.48x for the 10Y re-opening at the end of September and 1.52x, back at the end of May auction, when Italy issued the previous 3Y benchmark, BTP Jun13). Overall, the results were good and confirmed that appetite for Italian paper remains sound. AsEUR 21bn of BTPs will expire on Monday, one could argue that demand could have beeneven stronger. However, some investors could have been unwilling to open fresh positionsahead of the crucial Fed meeting next week. Moreover, the environment for periphery has sharply deteriorated over the last few days, as also confirmed by the not stellar results at the Spanish T-bill and Portuguese bond auctions. With this auction, YTD Italy has issued EUR 243bn of bonds (including CCTs andCTZs). We expect Italy to hold one CTZ re-opening, a 5Y/long-term BTP auction in mid-November, and a 3/10Y BTP, CCT auction at the end of November for an overall amount ofca. EUR 16/17bn, which would lead to a yearly target of gross issuance in the EUR 260bnarea. We expect the November ILB auction and the mid-December BTP auctions to becancelled.

Next week's preview Next week, there will be no redemptions and we expect gross supply to be in the EUR 18.5/20.5bn