Embed Size (px)

Citation preview

A MESSAGE FROM THE PRESIDENT . . . Kurt Subra

I hope you are encouraged that the days are getting warmer and l-o-n-g-e-r. Unfortunately, as we enter the negotiations and budget 'season' the discussions may get heated, and we will work even l-o-n-g-e-r days. Keep a positive attitude and send a note today to encourage one of your peers!

It is obvious that 2011 will be marked by leadership changes on many fronts. Here are a few that come to mind….

• My boss (West Des Moines CSD Superintendent) • Department of Education Director • Governor • Legislature (particularly in the House of Representatives) • IASB CEO and CFO, and last but certainly not least, the • IASBO Executive Director (our fearless leader)

The reality of change caused us to focus on IASBO’s future at our recent IASBO Leadership Conference in Des Moines. Your IASBO Board and leaders met for this purpose on February 1-2. Unfortunately, for the second straight year the snow and wind forced us to cancel our evening reception with legislators. In fact, in 2010 the entire IASBO Leadership Conference was cancelled because of adverse weather. Nearly two-thirds of the 2011 participants were unable to come, but Dr. Michael Jacoby, Executive Director of Illinois ASBO, arrived a day early to beat the blizzard.

Dr. Jacoby first described the lifecyle of organizations, and then he facilitated small and large group discussion regarding IASBO’s position on the lifecyle continuum. We also considered possible goals and priorities and assessed the “ease vs. impact” of implementing them. Finally, we considered what IASBO might do to keep it viable and even indispensible as an organization. A special thank you to Dr. Jacoby for making the extra effort to be with us.

ISU has advertised for the position that Dr. Jim Scharff has so capably filled for the past 9 years. He submitted his resignation to the University effective at the end of the current school year. Leslie Finger (Past President) and I will participate in screening candidates and your IASBO Board will play a vital role in any decisions. Honestly, we have concerns about the sustainability of the current ISU model, which requires that the person hold a doctorate to fulfill the teaching aspects of the position. We will keep you informed as we progress in the search process. Thank you to Lisa Oakley, Jackie Black and Jan Miller-Hook for the timely information they presented during the February 9 webinar and regional meeting. I was able to participate from Red Oak with about 20 of your peers. It is always good to connect face-to-face for a time of sharing and mutual encouragement.

Finally, I hope you plan to attend the spring conference in Ames on March 31-April 1. We have a strong line-up of professional development sessions for you. And as announced during the February 9 webinar, we have some high profile speakers for our general sessions. We also have a fun social activity planned for the evening of March 31. Bring your bowling shoes, your favorite pool cue, and your laser warfare clothing. If none of these activities interests you, come and enjoy the food, drink and camaraderie with your IASBO peers. Remember….Jim (with your Board’s consent) has authorized money for food and great prizes!

Kurt Subra IASBO President

Iowa ASBO 2010-2011 FISCAL YEAR OFFICERS

President Kurt G Subra. - West Des Moines CSD

President Elect Janice Miller-Hook - Johnston CSD Past President Leslie Finger - Iowa City CSD

Secretary Doug Nefzger - Cedar Falls CSD

Treasurer Karron Stineman - Louisa-Muscatine CSD

District Directors Angie K.Walter -West Branch CSD Kristy L.Hansen - Harlan CSD Academy and IASBO Secretary Chris Trower E-mail: [email protected]

Mentor Coordinator Shirley McAdon [email protected] Professional Development Coordinator Nancy Blow [email protected]

Executive Director Dr. James R. Scharff Iowa Association of School Business Officials Iowa State University N229E Lagomarcino Hall Ames, Iowa 50011-3195 Office Phone: 515-294-9468 E-mail: [email protected]

IASBO MISSION STATEMENT: The mission of the Iowa Association of School Business Officials is to provide programs

and services that provide the highest standards of school business management practices and professional growth.

February/March 2011

Annual Conference Scheman Continuing Education Center Ames, Iowa March 31 and April 1, 2011

Thursday, March 31, 2011 Registration - coffee and rolls President Kurt Subra

• Opening comments and introductions • Present certificates to those known to be retiring at the conclusion of the current year • Proposed Nominations for IASBO Board and Professional Growth Committee

Plenary Sessions Auditorium:

• Governor Terry Branstad will address IASBO members • John Musso, ASBO International Executive Director • Internal Controls – Closing the Gaps – Steve Graham, Cedar Rapids and Stacy Matus,

Springville will present changes in their districts to improve internal controls

Vendor displays will be open from 10:30 until 3:30. Lunch will be available from 11:30 – 1:00 Breakout Sessions 10:30-3:00 • Internal Controls Continued – Steve Graham, Cedar Rapids, will continue in this breakout session

with changes made in the Cedar Rapids school district to improve such things as cash

management procedures, segregation of duties, audit committee improvements and Board of

Education communication.

• PowerPoint Basics – Jeff Dieleman, Washington, will present tips on creating useful PowerPoint

presentations

• Bonds 101 – Beth Grob, Ahlers Law Firm, will lead two breakout sessions on bonding. Also

starring Paul Bobek as the Underwriter, Ron Peeler as Bond Counsel, Michelle Wearmouth

as Independent Financial Advisor, and Ramona Jeffrey as the Issuer/School District. Bonds 101

will be the basics including who are the players, what are their responsibilities and

documentation identification.

• Bonds 201 – Beth Grob, Ahlers Law Firm, Bonds 201 will be a more advanced session including

SEC and tax compliance and expectations as well as post-issuance SEC and tax compliance.

• RFP Consulting Services – Kristy Latta, Ahlers Law Firm, An overview of requests for proposals

(RFPs) - when they should be used, what they should contain, and recommend steps to guide

you through the RFP process.

• Leadership is Not a Spectator Sport – Larry Johnson, Author and Speaker, will address how you

can inspire others to contribute more, behave ethically, and change your school for the better.

• Crackerbarrel Sessions – This will be expanded from the past with size-alike Districts, Payroll,

Accounts Payable/Accounts Receivable and Financial Reporting

Plenary Sessions - Auditorium: 3:30 – 5:00 2011 Professional Leadership Awards Larry Johnson – “Absolute Honesty” – Larry will show how to establish a standard of communication that encourages creativity through candid discussions, frank expression of ideas, and healthy debate. A standard that tells the truth, doesn’t mince words and is guided by a clear sense of right and wrong.

Thursday, March 31, 2011 Evening Activities – Regional competitions in Bowling and Minute-to-Win-It held at the Perfect Game facility in Ames. Pool, laser tag and arcade also in this new Ames facility. See ad on the IASBO website in the file share section.

Friday, April 1, 2011 – Iowa School Business Management Academy Registration Iowa ASBO Business Meeting

• Elect and install officers for 2011-2012 (Pres-elect, Treasurer, Director District 1) Jason Glass, Iowa Department of Education, Director will present his vision for education Categorical Funding:

• Steve Crew, DE, Administrative Consultant, Special Education Finances

• Susan Walkup, DE, At-Risk/Dropout Prevention Funding

• Julie Jensen, Executive Director Students Services & Kevin McCauley, Student Assistance

Specialist Linn Mar CSD, will highlight their Student Assistance Drop Out Prevention Program

• Rosanne Malek, DE, Talented and Gifted, will be presenting on categorical funding for gifted

programming as outlined in Chapter 98.

• David King, Heartland AEA, AEA Funding, a brief history why AEA school foundation aid "flows

through" local school budgets and an explanation of the main component funding sources for

AEA's.

12:00 Adjourn

In trying to get our own way, we should remember that. . . kisses are sweeter than whine.

Remember your first couple of days at work? They were exciting. You had your orientation session, learned about the history of the district, became familiar with its organization, and discovered the benefits of working there. Or remember your first days as a new team leader, supervisor, manager, or even as a new “boss?” That was extra exciting. Then some old timer came along side you and said, "That all sounds good, but wait until you've been here a while. You'll see what it's REALLY like!" And your feelings switched from excitement to trepidation. You began to wonder what you got yourself into. Simple. You got yourself into the average workplace today ... where whining, complaining, griping, gossip, and excuse making may be common. As Roxanne Emmerich points out in her book, "Thank God It's Monday," one out of every three payroll dollars is LOST due to negative, disengaged employees. And more than 91% of people spend a huge chunk of their day frustrated by their coworkers' dysfunctional behaviors and think regularly about quitting their jobs. So what can YOU do if you're stuck in a work situation like that? You could quit and go elsewhere. But that may not be practical in today's economy. Besides that, another work site may have just as many complainers. A better option is to learn how to deal with complainers ... in your organization, or even at home. 1. Control your attitude. In the beginning, you may have decided to simply ignore the complainers. It was no big deal. But they didn't stop. And their constant complaining began to irritate you ... even anger or depress you. You can't let that happen to you. You can't let the complainers determine your emotional, financial, relational, or occupational destiny. You've got to do something to change yourself and the complainers when you find yourself in that situation. You've got to start with your own attitude. Remind yourself that you've got a job to do. You're paid to do it. You're a professional. And you refuse to be brought down to the complainer's level. But you've also got to take control of your attitude towards the complainers. If you think of them as a pain in the neck, if you approach them as the enemy, they'll become even more difficult to handle. Instead, think of them as people with problems that need to be solved. With that kind of an attitude, you have a better chance of getting through to them and turning off their complaints. 2. Bring a specific complaint to the surface. More often than not, complainers complain about a variety of issues a lot of the time. They act like a hose, spraying their garbage over anything or anyone in sight. And it's no wonder. In 2010, The Conference Board research group reported job satisfaction has fallen to a record low of 45 percent, the lowest level ever recorded in 22 years of surveys! Extrapolating from that number, more than half (55 percent) of US workers say that they are "dissatisfied" with their jobs. And the most dissatisfied workers are under the age of 25 ... where 64 percent of them say they are unhappy in their jobs. Now you could sit down with your complainers and ask them to explain all their complaints in detail. But don't do that. You don't have that much time. As it stands, Emmerich reports that managers already spend 37% or more of their day dealing with dysfunctional behavior. A better approach would be to get specific. Tell the complainer that you've noticed his apparent job dissatisfaction, and you would like to start the process of understanding his feelings. Of course, the complainer may have several issues that are upsetting him, but it's almost impossible to deal with more than one issue at a time. Things simply get too emotional. So as a rule of

thumb, I often advise leaders, managers, team members, and even families to stick with one issue at a time, one week at a time. And once you've brought a complaint to the surface... 3. Honor the other person's perspective. Show some respect for the other person's point of view ... even if it is way off base ... because to him or her, it is the truth. The important thing at this stage of the conversation is honor ... not who's right and who's wrong. So show the other person your genuine concern for her feelings and your honest respect for her perspective. When you honor the other person's perspective, you reduce the intensity of her complaint. Unfortunately, that's not happening in some workplaces. When someone complains about all the layoffs and the unreasonable work load, she may be told to shut up, because "You should be thankful you've even got a job." While that may be true, it's not helpful. When a worker gets that kind of response to her complaint, she may STUFF her feelings. With twice the work and half the friends, she may be so filled with fear and stress that she doesn't say anything, lest she end up in the unemployment line as well. But let me remind you that a shut-up, non-complaining workforce is not necessarily a happy and productive workforce. As The Herman Group warns ... "just because employees are not leaving does not mean they are engaged ... in fact, over 45% of today's workers are disengaged, costing their employers millions. "That being the case, you're always better off HONORING the other person's perspective than ignoring it ... even if you don't agree with it. As the old "Farmer's Almanac" puts it, "Meanness don't jes' happen overnight." There's some history behind the other person's complaint, and that history needs to be understood. 4. Practice empathic listening. Complaints and complaining people can be tricky. As American humorist Will Rogers acknowledged, "Lettin' the cat outta the bag is a whole lot easier 'n puttin' it back." So you need to have some excellent communication skills working for you. Let the other person talk. Give him time to explain his complaint, share his feelings, and get it out of his system. Give him time to vent. As that's happening, let your nonverbals show that you're listening. Nod your head, maintain eye contact, and say "uh-huh." When the complainer begins to repeat himself, you know the venting is almost over. Then move to clarification. Try to repeat exactly what he said. Don't put in too many of your own words because he might find something else to get upset about. You want the complainer to feel understood. You can even ask questions to get more information and more clarification 5. Avoid defensiveness. Most people want to defend themselves when someone complains. They want to justify their actions, stand up for the company, or point the finger of blame somewhere else. You've got to resist this at all costs. Don't make excuses or argue. At this point, it's your job to demonstrate the fact you're there for him with a statement such as "Tell me more. "Somewhere along the way, you might also say, with true sincerity, "I'm sorry." The statement has nothing to do with admitting fault, but it has everything to do with saying you're sorry he's upset. You're sorry he's frustrated. You're sorry he is not happy with something you or someone in your company did. Saying you're sorry expresses your empathy, avoids defensiveness, and diffuses negative emotions. Let the complainer know that he or she is not alone. You're in this situation together, and together you can find some kind of solution. It's kind of like Joe and Lars who came to America from the old country. As they traveled on an old, beat-up freighter crossing the North Sea, a huge storm arose. Joe said, "Lars, Lars, da ship is going down." Lars replied, "What do we care? It's not our ship. "The point is ... when there's a complaint in your organization; you can't ignore it ... because you're all in the same ship. And what affects one person probably affects a lot of other people as well.

6. Work towards a mutually acceptable agreement. You want to resolve the issue as quickly as possible. The quicker the resolution, the less it will affect your overall relationship. So thank the other person for bringing the issue to your attention ... because you want your communication to be as candid as possible. Then ask him how he would like his complaint to be handled. And if you can do what he asks, just go ahead and do it. That's easy. That's the fun part in conflict resolution. However, if you can't give the other person exactly what he wants ... which is often the case ... tell him what you CAN do to make things better. If you spend too much time telling him what you CAN'T do, he'll just get more upset. Stick with what you CAN do, and somewhere, in the give and take between the two of you, you will find an understanding or a solution that is better than the complaint you started with. Action: Instead of getting upset with your complainers, use these tips to turn them around. "©2010 Dr. Alan R. Zimmerman. Reprinted with permission from Dr. Alan Zimmerman's Internet newsletter, the 'Tuesday Tip.' For your own personal, free subscription to the 'Tuesday Tip' as well as information on Dr. Zimmerman's keynotes and seminars, go to http://www.drzimmerman.com/ or call 800-621-7881.

Iowa Medicaid Policy Updates Since 2001, Iowa Medicaid has allowed local school districts to submit claims for financial reimbursement of covered Special Education services. In order to access this revenue source, districts enroll with Iowa Medicaid as a LEA provider. LEA stands for Local Education Agency and any of the 360+ districts in the state qualify to be this provider. As an Iowa Medicaid provider, districts must comply with all the regulations and policies of Iowa Medicaid. There have been a few significant changes in Iowa Medicaid policy since the start of the school year. The first change is financially oriented. Medicaid is a mix of state and federal funds, with the ratio changing each October. This is when the new federal fiscal year begins. For Iowa, Medicaid payments starting October 1, 2010 are reimbursed by the federal government at a lower rate than the previous year. This impacts local school districts, as all districts and AEAs return the state portion of the Medicaid reimbursement to the Iowa Department of Human Services (the Medicaid agency in Iowa). This does allow districts to access federal Medicaid funds to support the Special Education services for the students in the district. With the passage of the Stimulus Bill in 2009, Medicaid received an increase in the federal portion of the Medicaid reimbursement. This meant that less state funds were required for the same services. This also meant the school districts were able to retain more of the Medicaid reimbursement. This enhancement to the federal rate was only temporary and was originally scheduled to expire on December 31, 2010. There has been one modification to the plan and a six month transition period has been approved by Congress. This allows for a two quarter phase out of the enhanced federal Medicaid rate. The other significant change is related to the submission of the Medicaid claims for reimbursement. In order to comply with the Health Care Reform bill, passed last summer, Iowa Medicaid has changed the way claims are submitted. As of December 1, 2010 all providers are required to submit their claims in date frequency. Prior to this date, providers were able to enter services in a month range. This results in much more time to process the paperwork and submit the claims for reimbursement by Medicaid. At the state level, the Iowa Department of Education and the Iowa Medicaid Enterprise calculate the cost rates for each district. The cost rates are set for the state fiscal year, from July 1st to June 30th. The statewide average cost rates for the current fiscal year took a drop of about 9-10%, which means less funds for the same services to most districts. These are just a few of the policy changes this school year. There will undoubtedly be other changes and more every year. For more information about this article, please feel free to contact Dann Stevens, CEO of Timberline Billing Service LLC at [email protected] or at (515) 222-0827.

UPDATE ON 1099 REPORTING AFTER DECEMBER 2011 Information applicable as of February 2011

Kev Group has been asked to share more information on the new Bill passed in 2010 which establishes a $600 threshold for producing 1099 IRS tax forms and, in addition, expands the scope of reporting to include corporations. The changes to the reporting requirements set forth in the Bill apply to payments made after December 31, 2011. The exact text of the amendment is detailed below from section 9006: “SEC. 9006. EXPANSION OF INFORMATION REPORTING REQUIREMENTS. (a) IN GENERAL.—Section 6041 of the Internal Revenue Code of 1986 is amended by adding at the end the following new subsections: ‘‘(h) APPLICATION TO CORPORATIONS.—Notwithstanding any regulation prescribed by the Secretary before the date of the enactment of this subsection, for purposes of this section the term ‘person’ includes any corporation that is not an organization exempt from tax under section 501(a). ‘‘(i) REGULATIONS.—The Secretary may prescribe such regulations and other guidance as may be appropriate or necessary to carry out the purposes of this section, including rules to prevent duplicative reporting of transactions.’’.

(b) PAYMENTS FOR PROPERTY AND OTHER GROSS PROCEEDS.—Subsection (a) of section 6041 of the Internal Revenue Code of 1986 is amended— (1) by inserting ‘‘amounts in consideration for property,’’ after ‘‘wages,’’, (2) by inserting ‘‘gross proceeds,’’ after ‘‘emoluments, or other’’, and (3) by inserting ‘‘gross proceeds,’’ after ‘‘setting forth the amount of such’’. (c) EFFECTIVE DATE.—The amendments made by this section shall apply to payments made after December 31, 2011.” Full access to the Reform Bill can be accessed here: http://democrats.senate.gov/reform/patient-protection-affordable-care-act-as-passed.pdf The new vendor 1099 reporting requirements will pose a significant challenge for some Districts within the school activity funds arena that have thousands of vendors across a large number of schools. KEV has assembled three recommendations to help ease the pain of 1099 reporting:

1. Maintain a single district vendor list for your school generated funds to ensure lost or missing vendor information is minimized. Many databases can uniquely identify vendors by tax ID which will help greatly.

2. Establish a district policy for all schools to capture vendor tax-id information at the time an invoice is paid. It is much easier to gather this information up front rather than at the end of the year when tight deadlines are in place.

3. Track all disbursement transactions in a web-based accounting system. Having all data centralized in a single system reduces the need to collect data from multiple sources and combine information at year end.

Yours in Planning, Kim Vivian-Downs Co-Founder School Cash Simplified Email: [email protected] Web: www.kevgroup.com

Audit Summary The following was developed as a tool to help walk your Board of Education / Finance Committee / etc. through the audit report. It is meant to be a flowchart to systematically review the audit. It may not answer all questions your Board may ask but will provide an initial procedure for you to use. Feel free to use, adapt, edit, etc. as best fit your circumstances. Thanks are due to Jan Miller-Hook at Johnston for preparing this tool. A version in Word (to facilitate editing and including the page #s etc.) can be located in the file share of the IASBO website.

1. Chapter 11 of the Code of Iowa requires an annual audit, and federal funding is subject to A-133 audits and since districts receive federal funding, our audits fall under those requirements.

2. The Letter of Transmittal on pages _____ is a required document written by the district

that gives a footprint of the entire audit. This document gives a good deal of information regarding the audit and where to find particular information. On the first page, you see a breakdown of the four sections, and I will further break those down below:

A. Introductory Section-Includes transmittal letter noted above written by the district,

organizational chart, list of District officials, and the recognition certificates received by the district (pages_____).

B. Financial Section-Includes Independent Auditor’s Report on pg _____ which is directed to the board and spells out the work of the auditors, and their opinions on the financial statements as well as internal controls. Starting on page ____ is the MD&A (Management’s Discussion and Analysis) written by the district which really tells the story for the year. It takes the audited financial statements and puts the information in a narrative form. You should read this, as it will help answer questions as you review the financial statements.

OK, starting on page ___ are the basic financial statements. Pages ______are government wide statements. One big difference in government wide and fund financial statements is the inclusion of capital assets. For fund financials and the way we keep our books throughout the year, capital assets are expensed. However, on government wide statements, the cumulative expenses for capitalized items and their related cumulative depreciation are shown as assets. Starting on page ____ are the fund financial statements which do not include the capital assets and depreciation. These statements are the familiar statements including the general fund, debt service, capital projects (capital and sales tax funds), and then a column for special revenue. The special revenue column includes the student activity fund, management fund, and PPEL fund. Starting on page ____ and through page ___ are financial statements for the enterprise or proprietary funds which include the nutrition fund, preschool, daycare, and community education funds. The column labeled internal service fund represents our self funded insurance accounts and flexible spending account. Starting on page ___ through page ___are the notes to the financial statements which are really worth reading as they include a summary of accounting policies, definitions throughout the notes, details of investments, capital assets, long-term liabilities, as well as others. Pages ______ represent supplementary information required, and there you can find the breakdown of funds. For example, on page _________, you find the funds broken down by management, student activity, PPEL where on the government wide statements they are shown as total under Non-major Special Revenue. If you compare the total on page ____ with the breakdown, you will see the same total of $___________ on page ____ of the government fund financials. Then, on pages _________, you see the breakdowns of the enterprise funds and the governmental activities. For example, you can take the same totals from the fund breakdowns on page ___ and tie to the cumulative on page ____ for the Statement of Net Assets. Pages _____ are capital asset details which represent the original costs of all items capitalized on our fixed asset listing. It breaks those expenses down by functions. Page ______ details all the fund balances within the student activity fund by site. Page ____ is a statement of revenues by source and expenditures by function.

C. Compliance Section-Pages _____ lists all federal funds received and the respective amounts. Page _______ is the Auditor’s report on internal controls and compliance in accordance with government auditing standards, and on page ______ is the Auditor’s

report on internal controls and compliance in accordance with OMB Circular A-133. Pages _________ are findings and responses.

D. Statistical Section for those applying for the Certification of Excellence in fund reporting -

This entire section (pages _________) represents historical information required in order to apply for the ASBO and GFOA certificates of excellence in financial reporting. This information comes from various sources-most of it from district information. However, some information comes from the city, county, state, etc, and the sources are shown on the bottom of the exhibits.

This long article, taken from the USA Today, may seem out of place in an IASBO newsletter. Before casting it away or writing a snarly email to your executive director first consider that 80% of IASBO members are women and your work responsibilities are often extremely stressful. Many of you go home to the ongoing family demands of preparing meals, cleaning, etc. etc.

This may be meant for you……….

Campaign focuses on women, heart attacks

A decade-long effort seeks to raise awareness By Anita Manning Special for USA TODAY In an emergency, women don't hesitate to call 911 for help - for someone else. But when they're the ones having a heart attack, only about half will make the call that could save their own lives. A major public health campaign launching today aims to change that. Make the Call, Don't Miss a Beat is "the first national campaign targeted to women to learn about the symp¬toms of heart attack and to call 911," says campaign director Suzanne Haynes of the Office of Women's Health at the US. Department of Health and Human Services. The campaign will spread the word through public service ads on television and radio, in print, on billboards and public transit, and through speakers with WomenHeart, a national coalition of women with heart disease. A decade-long effort to raise awareness of women's heart disease risks has been successful, Haynes says, but the results of a survey by the American Heart Association last year caught health officials by surprise. It showed "a huge decline in the percentage of women who would call 911, down from 79% in 2006 to 50% in 2009," Haynes says. "This was very alarming, and there was no explanation for it." The survey showed that "women don't know if they're having a heart attack," says Lori Mosca, director of Preventive Cardiology at New York Presbyterian Hospital and a member of the expert panel working with HHS to develop Make the Call, Don't Miss a Beat. 1100 MMyytthhss AAbboouutt HHeeaarrtt DDiisseeaassee 1 It will go away: The survey also found that 78% of women would call 911 to save someone else, but if they're the ones having symptoms, "less than half said they'd call 911." Instead, they'd take an aspirin, call the doctor or "wait it out," Mosca says. Why? "They're waiting for it to go away," she says. "They're hoping they'll be wrong." Often, women say they're afraid their symptoms will be dismissed, or they don't want to cause a fuss by calling an ambulance. "We've gotten some realty wild reasons - 'I don't want the EMTs (emergency medical technicians) to see my messy house,' or 'I want to put my makeup on,'" Mosca says.

Eileen Williams, 58, of Manassas, Va., was a paramedic herself when, at age 43, she had a heart attack. At the end of a 24-hour shift at a local fire-house, she "felt an explosion at the side of my neck" that became a persistent, dull pain. Yet, she says, she waited 12 hours before calling her own 911 team. "Everyone denies they're having a problem," she says. Now she speaks to women's groups about knowing their symptoms of heart attack and dialing 911. "Call us," she says. "You're not inconveniencing us. "That's why we're here. We can save your life - if you call us soon enough." Years ago, we'd see men in their 50s, 60s and 70s with heart attacks, women a decade later," Milani says. "Today we're seeing men and women in their 30s and 40s with heart attacks." 2 It doesn't affect children. Heart disease affects people at any age, doctors say. Congenital heart diseases, infections that damage the heart, and the same problems of overeating and under-exercising that afflict their parents also strain the hearts of children. "With the growing prevalence of obesity in children, we're seeing heart disease in even younger adults due to under-controlled risk factors," such as high blood pressure and cholesterol, Sacco says. Cardiac arrest strikes an estimated 5,920 children each year, the heart association says. Most unexpected deaths in young athletes are the result of heart disease; they account for up to one death per 100,000 high school athletes. 3 It doesn't affect those who are fit and strong. Staying fit and active improves heart health, but doctors can cite many cases in which even the healthiest habits are not enough. "Exercise does afford you benefits," Milani says. "Fitness reduces the potency of risk factors, but it doesn't eliminate them." You may run marathons, but "you still have to have your cholesterol checked," he says. "You still can't smoke." 4 I'd feel sick if I had high cholesterol or high blood pressure That's a mistake, Sacco says. Neither condition produces early warning signs, and both can lead to heart attack or stroke. High cholesterol, a fatlike substance, can clog arteries and block blood flow to the heart or brain. "Anybody can have it. It can run in families," Sacco says. "You can be thin and have high cholesterol. It needs to be checked, regardless of your weight." Blood pressure is a measurement of the force of blood hitting the walls of arteries as blood circulates. It should be checked regularly, too, he says, because "you don't feel anything when your blood pressure is high." One in three adults has high blood pressure, and a third of them don't know it. Ideally, the level of total cholesterol in blood should be 200 or less, and normal blood pressure is 120/80. Both conditions can be improved with diet, exercise and medications. 5 Heart attack symptoms are the same in men and women. Men and women I alike can experience the Hollywood-Style heart attack - severe chest pain, cold sweat - but women, more often than men, may have subtler, less recognizable symptoms, such as abdominal pain, achiness in the jaw or back, nausea and shortness of breath. "Half of women have no chest pain at all," says heart surgeon Kathy Magliato of St. John's Health Center in Santa Monica, Calif., and author of Heart Matters: A Memoir of a Female Heart Surgeon. A common symptom: unusual tiredness, "this uncanny fatigue that a woman can't put her finger on." Too often, women "blow off" their symptoms, she says, mistaking them for indigestion or a sign of being out of shape. That can be deadly. "The No. 1 way women present with heart disease is dead," she says. "They don't come in with chest pain or fatigue. It's sudden cardiac death." Balancing the competing demands of home, work, kids and life, women "walk through the days and weeks and months overtaxed, and it hits By Kevin Foiey somewhere in the body, whether the neck or back, or in the form of depression or nausea," says Pamela Serure, executive director of Events of the Heart, a non-profit group that uses creative arts to promote women's heart health. "So, I say, 'Oh, he's a pain in the neck,' and I have neck pain for a week. I get tired and say, 'I need to go to the spa.' I get nauseous and think I shouldn't have had that extra pizza It's never heart disease."

That has to change, she says. Women need to become advocates for their own health. "The new math is, these symptoms equal heart disease," she says. "And the new math inside is, I’m No.l.'" 6 Heart disease is genetic. If your parents didn't have it, you won't, either. There are risk factors you can control, such as diet, smoking and exercise, and there are those you can't, including your age and family history. If your father had a stroke or heart attack before age 55 or your mother had one before 65, you're at higher risk, says Magliato. We can't change our genes, she says, so we'd better control what we can. "If you have a family history of heart disease, you'd better not be smoking, and you'd better keep your cholesterol under control and be getting regular heart checkups," she says. 7 Extra weight is just more to love. Obesity can lead to high blood pressure and diabetes, and weight loss can mitigate those risks. "If a woman just loses weight, her blood pressure comes down," Magliato says. "She can be on four blood pressure medications, lose 100 pounds and be off all meds." Leway Chen, director of the University of Rochester Heart Failure and Transplantation Pro¬gram, says "in general, obesity itself seems to have an association with cardiomyopathy," or disease of the heart muscle, and high blood pressure. 8 Women are more likely to die of breast cancer than heart disease. "The leading cause of death in women is heart disease, by a long shot," Ochsner's Milani says. "It beats the living daylights out of all forms of cancer. "This is not pushing down the importance of cancer research, but it's critically important that women get this." If they don't, they could ignore symptoms. Heart disease deaths are more common than breast cancer in all age groups, Magliato says, even those of childbearing age. For younger women, the combination of birth control pills and smoking boosts heart risks by 20%, Magliato says. "The message to young women is you have to start taking care of your heart now." 9 Diabetes is not a heart threat, as long as my blood sugar level is under control. People with diabetes are healthiest when their blood sugar levels are within a normal range, Chen says, but diabetes itself causes inflammation that can damage blood vessels, raising the risk of heart disease and other health problems. "You shouldn't rest on your laurels if you have diabetes and your sugar is controlled," he says. "Your weight and blood pressure and cholesterol all need to be treated at the same time." 10 If I were at risk for heart disease, my doctor would order tests. Don't assume that will happen, says cardiologist Merdod Ghafouri of Inova Fairfax (Va.) Hospital. Screening tests for cancer are routinely recommended, he says, but simple heart tests, such as a CT scan, are not -and he thinks they should be. Mammograms and colonoscopies are important, but "most people are going to die of heart disease." A cardiac scan can detect plaque buildup in arteries at an early, easily treatable stage and should be recommended for people with a family history of heart disease, he advises. With diet, exercise and greater awareness of risks, most heart disease is preventable, Sacco says. But too often, "people treat their cars better than their bodies," he says, "bringing them in for checkups, oil changes and other preventive maintenance." Hearts deserve at least that much care. How to be hearthealthy The American Heart Association recommends "Life's Simple 7" steps for better health: 1 ‐ Get active. At least 150 minutes a week of moderate activity.

2 ‐ Control cholesterol. Aim for under 200 mg/dl. 3 ‐ Eat better. More fruits, vegetables, less salt (under 1,500 mg sodium per day). 4 ‐ Control blood pressure. Normal is below 120/80 mg/Hg. 5 ‐ Lose weight. Normal body mass index is 25 kg/m2. 6 ‐ Reduce blood sugar. Diabetes more than doubles the risk for heart disease and stroke. 7 ‐ Stop smoking. Smoking raises the risk of heart disease and many chronic disorders.

Iowa ASBO Member

Recognition: In addition to the members serving on your Iowa ASBO Board of Directors, as Regional Directors, and on the ISBMA advisory committee there are several others serving in other capacities.

Marsha Tangen – Chief Financial Officer, Davenport CSD She was appointed to the original ASBO Intl Certification Commission and her term has just been renewed for an additional 3 years. Marsha was also on the Iowa School Business Official Authorization Advisory Committee. Jan Miller-Hook – Director of Business and Finance, Johnston CSD Jan has served on the CAR/SES Department of Education advisory group-since the group was formed

Doug Nefzger - Director of Business Affairs, Cedar Falls CSD Doug serves as the business official representative on the ISEBA board of directors Greg Reynolds – Board Secretary / Business Manager, Keokuk CSD Greg serves as the business official representative on the ISJIT Board of Trustees Karen Shimp – CFO / Board Secretary, Ames CSD Karen serves as the business official representative on the ISCAP Board

Department of Education Finance Roundtable. This gathering of business officials, superintendents, AEA, Department of Management, State Auditor, IASBO, SAI, IASB, and ISEA meets with D.E. finance staff four times a year to discuss the impact of pending or enacted legislative and rules in regard to public school funding. IASBO members currently serving here include: Kate Baldwin – Business Manager, Norwalk CSD Paul Bobek – Executive Director of Administrative Services, Iowa City CSD Jack Christensen – Board Secretary / Director of Financial Services, Ft. Dodge CSD Jean Garner – Director of Finance and Budget, Muscatine CSD Craig Hansel – Chief Financial Officer and Board Secretary, Ankeny CSD Jim Scharff - Executive Director, Iowa ASBO Dennis Scudder – Director of Finance, AEA 267 Angie Walter – Business Manager, West Branch CSD The above individuals are going above and beyond the siren call of the desk in the business office to enhance and support school finance issues and the profession. They are all to be highly commended and thanked for this additional service to the profession. It is most certain there are others serving in additional capacities and are omitted only because their humility prevented them from submitting the information when asked some weeks ago.

A big CONGRATULATIONS is also due to the following pioneers The following Iowa ASBO members have successfully passed Part I of the SFO test on accounting systems and accounting functions. Part II of the process will include a test on management and operations with several criteria needed before this step can be accomplished (details are on the ASBO Intl website). Kevin Kelleher - Assistant Director of Business Services/Finance Manager, Dubuque Joan Loew + Board Secretary/Business Manager, Oelwein Craig Mobley – Business Manager,Knoxville Karen Shimp - CFO/Bd. Secretary,Ames Claudia Wood - Associate Director of Finance, Davenport

Certified Administrator of School Finance and Operations (SFO)

Looking for a way to set yourself apart from other school business officials?

The SFO designation demonstrates a mastery of what it takes to manage school finances and operations.

This is a nation-wide certification for school business officials -- because not just anyone can walk off the street and do what you do.

Official Notice:

This will provide official notice of nominees for election at the April 1 business meeting of the Iowa Association of School Business Officials. President Elect (advances to President in 2012-13) – Karron Stineman Karron is the business manager at Louisa Muscatine schools and has served Iowa ASBO as a regional director, district director representative on the IASBO board, and treasurer of Iowa ASBO.

Treasurer (2 year term) – Trudy Pedersen Trudy is the Business Manager at Storm Lake schools and has served Iowa ASBO as a regional director and as a district director representative on the IASBO board. IASBO Board Director (2 year term) – District One – Angie Walter Angie is the Business Manager at West Branch schools and has served Iowa ASBO as a regional director and one term as a district director representative on the IASBO board. Iowa ASBO members on the Iowa School Business Management Professional Growth Committee - (4 year term) Jeff Dieleman, Washington CSD Melissa Fettkether, Valley CSD There are no constitution or bylaws items submitted for vote this year.

Professional Certification Program For New and Continuing School Administrators and School Business Officials:

Iowa School

Business Management

Academy

Introductory Level I Course Intermediate Level II Course Advanced Level III Course

Final Level IV Course Graduate Level Course

Levels I, II, III and IV: May 18-20, 2011 ♦ Graduate Course: May 19-20, 2011

Scheman Building

Iowa State University Campus - Ames, Iowa

Sponsored By: Iowa State University - Department of Educational Leadership & Policy Studies

Iowa Association of School Business Officials Iowa Association of School Boards

School Administrators of Iowa Iowa Department of Education

Register before April 15 and save!

Program Information

Registration and Fees IASBO MEMBERS CAN REGISTER ON-LINE AT

THE IASBO WEBSITE Advance registration is required for all levels. Registration fees (includes materials, continental breakfasts, refreshments and buffet luncheons) are as follows. IASBO members who register by April 15: $375 for Level I, II, III and IV; $225 for graduate level. (No registrations will be accepted after Monday, May 2.) Non-members who register by April 15: $450 for Levels I, II, III and IV; $325 for graduate level. (No registrations will be accepted after Monday, May 2.) Any registration received after April 15: $500 for Level I, II, III and IV; $375 for graduate level. (No registrations will be accepted after Monday, May 2.) Fees are to be paid prior to the start of the academy. Make checks payable to Iowa State University. Do not combine with IASBO payments

Iowa School Business Management AcademyN229 Lagomarcino Hall Iowa State University Ames, IA 50011-3190

If you have any questions, please call Chris Trower at (515) 294-4375, write to the above address, or send e-mail to: [email protected]. Lodging You are responsible for making your own room reservations The Hotel at Gateway Center (515‐292‐8600) Best Western University (515‐296‐2500) Country Inn & Suites (515) 233‐3935 Comfort Inn ‐ (515‐ 232‐0689) Grandstay Residential Suites (515‐232‐8363) Holiday Inn (515‐268‐8808) Meals Continental breakfasts (W-Th-F) and buffet luncheons (W-Th) are provided daily in the Scheman Center as part of your registration fee. There is no lunch offered on Friday.

Academy Staff Faculty for the Iowa School Business Management Academy is carefully selected from among the best professional talent in a given area of study. Whether the topic is law, finance, accounting, materiel management, or how to work with people, you will find that the Academy faculty is outstanding. Most faculty are actual field practitioners and experts in their field, and you will have an opportunity to evaluate each instructor so we can maintain the highest caliber instructional staff possible. Courses are scheduled in two-hour blocks, and are held in the Scheman Continuing Education Center. Course Schedule for Levels I, II III, and IV: Pick up your nametag, class schedule and course binder beginning at 9:15 a.m. on Wednesday, May 18, at the second floor registration desk. Level I, II, III and IV classes start at 10:00 a.m. Wednesday morning. You should plan to be in class promptly to begin each session, as time is at a premium. Class schedules for the rest of the week are as follows:

First session, 8:00 a.m. -- 9:50 a.m. Second session, 10:00 -- 11:50 a.m. Lunch, 12:00 noon -- 12:50 p.m. Third session, 1:00 -- 2:50 p.m. Fourth session, 3:00 -- 4:50 p.m. (All classes end at noon on Friday, May 20.)

Graduate level attendees may pick up their registration materials beginning at 7 a.m. on Thursday, May 19. Class schedules are the same as above.

Course Sections Graduate Level course sections are scheduled to provide class sizes of approximately 50 people per section. You will be assigned to a section, and you should plan to stay with that section throughout the three day Academy program. Course Materials All printed course materials are included with your registration fee. Books, notebooks, and other materials issued to you become your property, and you may wish to place your name and school district in all materials in case they become misplaced.

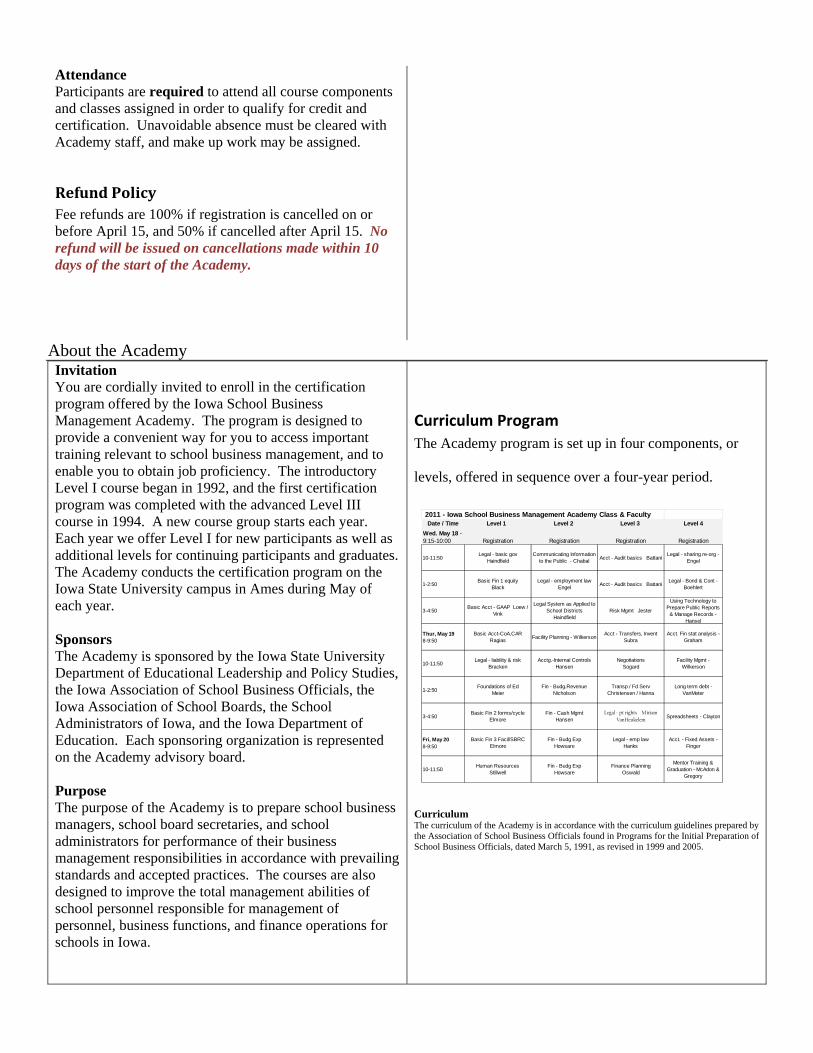

Attendance Participants are required to attend all course components and classes assigned in order to qualify for credit and certification. Unavoidable absence must be cleared with Academy staff, and make up work may be assigned.

Refund Policy Fee refunds are 100% if registration is cancelled on or before April 15, and 50% if cancelled after April 15. No refund will be issued on cancellations made within 10 days of the start of the Academy.

About the Academy Invitation You are cordially invited to enroll in the certification program offered by the Iowa School Business Management Academy. The program is designed to provide a convenient way for you to access important training relevant to school business management, and to enable you to obtain job proficiency. The introductory Level I course began in 1992, and the first certification program was completed with the advanced Level III course in 1994. A new course group starts each year. Each year we offer Level I for new participants as well as additional levels for continuing participants and graduates. The Academy conducts the certification program on the Iowa State University campus in Ames during May of each year. Sponsors The Academy is sponsored by the Iowa State University Department of Educational Leadership and Policy Studies, the Iowa Association of School Business Officials, the Iowa Association of School Boards, the School Administrators of Iowa, and the Iowa Department of Education. Each sponsoring organization is represented on the Academy advisory board. Purpose The purpose of the Academy is to prepare school business managers, school board secretaries, and school administrators for performance of their business management responsibilities in accordance with prevailing standards and accepted practices. The courses are also designed to improve the total management abilities of school personnel responsible for management of personnel, business functions, and finance operations for schools in Iowa.

Curriculum Program The Academy program is set up in four components, or

levels, offered in sequence over a four-year period.

2011 - Iowa School Business Management Academy Class & FacultyDate / Time Level 1 Level 2 Level 3 Level 4

Wed. May 18 - 9:15-10:00 Registration Registration Registration Registration

10-11:50Legal - basic gov

HaindfieldCommunicating Information

to the Public - Chabal Acct - Audit basics BattaniLegal - sharing re-org -

Engel

1-2:50 Basic Fin 1 equity Black

Legal - employment law Engel Acct - Audit basics Battani Legal - Bond & Cont -

Boehlert

3-4:50 Basic Acct - GAAP Loew / Vink

Legal System as Applied to School Districts

HaindfieldRisk Mgmt Jester

Using Technology to Prepare Public Reports

& Manage Records - Hansel

Thur, May 19 8-9:50

Basic Acct-CoA,CAR Ragias Facility Planning - Wilkerson Acct - Transfers, Invent

SubraAcct. Fin stat analysis -

Graham

10-11:50 Legal - liability & risk Bracken

Acctg.-Internal Controls Hansen

Negotiations Sogard

Facility Mgmt - Wilkerson

1-2:50Foundations of Ed

MeierFin - Budg.Revenue

NicholsonTransp / Fd Serv

Christensen / HannaLong term debt -

VanMeter

3-4:50 Basic Fin 2 forms/cycle Elmore

Fin - Cash Mgmt Hansen

Legal - pt rights Miriam VanHeukelem

Spreadsheets - Clayton

Fri, May 20 8-9:50

Basic Fin 3 Facil/SBRC Elmore

Fin - Budg Exp Howsare

Legal - emp law Hanks

Acct. - Fixed Assets - Finger

10-11:50 Human Resources Stillwell

Fin - Budg Exp Howsare

Finance Planning Oswald

Mentor Training & Graduation - McAdon &

Gregory

Curriculum The curriculum of the Academy is in accordance with the curriculum guidelines prepared by the Association of School Business Officials found in Programs for the Initial Preparation of School Business Officials, dated March 5, 1991, as revised in 1999 and 2005.

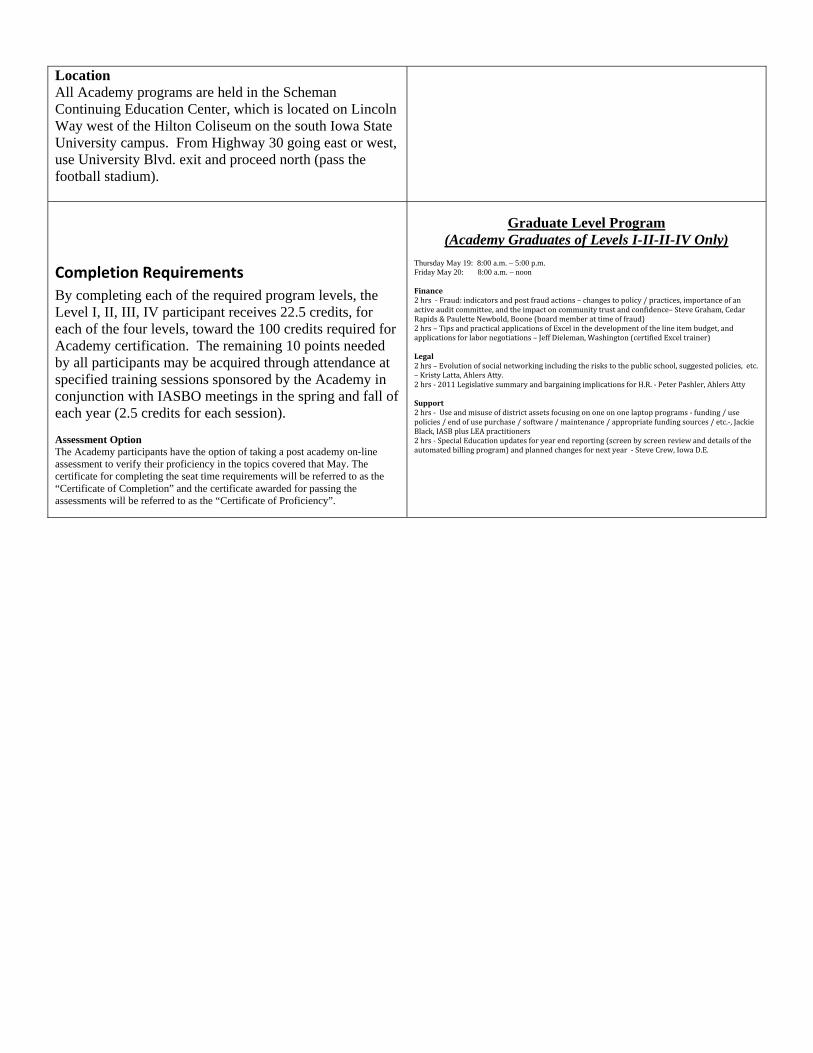

Location All Academy programs are held in the Scheman Continuing Education Center, which is located on Lincoln Way west of the Hilton Coliseum on the south Iowa State University campus. From Highway 30 going east or west, use University Blvd. exit and proceed north (pass the football stadium).

Completion Requirements By completing each of the required program levels, the Level I, II, III, IV participant receives 22.5 credits, for each of the four levels, toward the 100 credits required for Academy certification. The remaining 10 points needed by all participants may be acquired through attendance at specified training sessions sponsored by the Academy in conjunction with IASBO meetings in the spring and fall of each year (2.5 credits for each session). Assessment Option The Academy participants have the option of taking a post academy on-line assessment to verify their proficiency in the topics covered that May. The certificate for completing the seat time requirements will be referred to as the “Certificate of Completion” and the certificate awarded for passing the assessments will be referred to as the “Certificate of Proficiency”.

Graduate Level Program

(Academy Graduates of Levels I-II-II-IV Only) Thursday May 19: 8:00 a.m. – 5:00 p.m. Friday May 20: 8:00 a.m. – noon Finance 2 hrs ‐ Fraud: indicators and post fraud actions – changes to policy / practices, importance of an active audit committee, and the impact on community trust and confidence– Steve Graham, Cedar Rapids & Paulette Newbold, Boone (board member at time of fraud) 2 hrs – Tips and practical applications of Excel in the development of the line item budget, and applications for labor negotiations – Jeff Dieleman, Washington (certified Excel trainer) Legal 2 hrs – Evolution of social networking including the risks to the public school, suggested policies, etc. – Kristy Latta, Ahlers Atty. 2 hrs ‐ 2011 Legislative summary and bargaining implications for H.R. ‐ Peter Pashler, Ahlers Atty Support 2 hrs ‐ Use and misuse of district assets focusing on one on one laptop programs ‐ funding / use policies / end of use purchase / software / maintenance / appropriate funding sources / etc.‐, Jackie Black, IASB plus LEA practitioners 2 hrs ‐ Special Education updates for year end reporting (screen by screen review and details of the automated billing program) and planned changes for next year ‐ Steve Crew, Iowa D.E.

Registration Form (Only one registration per form. Please duplicate for additional registrations)

The Iowa School Business Management Academy May 18‐20, 2010

Note deadlines and fees! Register before April 15 and save! IASBO MEMBERS CAN REGISTER ON-LINE AT THE IASBO WEBSITE

Name: Title: School District: Daytime phone: ( ) Address: Evening phone: ( ) City: State: Zip: Note: Iowa State University requests this information for the purpose of registering you in a conference. No one outside the university, with the exception of participants in this conference, is routinely provided this information. If you fail to provide the required information, we cannot promise accurate registration. (Reference: Iowa Code, Chapter 22:11; Iowa Fair Information Practices Act).

REGISTRATION IS FOR: _____Level I (New Enrollee) _____Level II (Continuing Enrollee) _____Level III (Continuing Enrollee) _____ Level VI (Continuing Enrollee) Graduate Level (Must have already completed Levels I, II, III and IV.) PLEASE CHECK ONLY ONE BOX BELOW:

Level I, II, III and IV fee - IASBO member - $375 is enclosed (if registered by April 15.) Level I, II, III and IV fee - Non-member - $450 is enclosed (if registered by April 15.) All Level I, II, III and IV late fees - $500 is enclosed (IASBO member or non-member registered after April 15.)

Graduate fee – IASBO member - $225 is enclosed (if registered by April 15.) Graduate fee – Non-member - $325 is enclosed (Non-member, registered by April 15.) Graduate late fee - $375 is enclosed (IASBO member or non-member, registered after April 15.)

Please make checks payable to Iowa State University, not IASBO. Registrations will be closed after Monday, May 2. Check/PO must be enclosed to ensure your place.

To FAX registration, transmit a completed copy of this form with a copy of your purchase order to (515) 294-4942, attention: Chris.

The Iowa School Business Management Academy and Iowa State University programs and policies are consistent with pertinent federal and state laws and regulations on non-discrimination regarding race, color, national origin, religion, sex, age, and handicap.

Iowa School Business Management Academy Ms. Chris Trower, Executive Assistant Iowa State University Department of Educational Leadership and Policy Studies N229 Lagomarcino Hall Ames, Iowa 50011-3190

I O W A S T A T E U N I V E R S I T Y O F S C I E N C E A N D T E C H N O L O G Y

Please welcome these IASBO Associate members for 2010-11 When your district is in need of services or products these vendors provide be sure to contact

them for pricing and service.

SILVER LEVEL PARTNERS Perspective Consulting Stacy Wanderscheid 2670 ‐ 106th Street, Suite 240 Urbandale, IA 50322 Email: [email protected] Phone: 515-875-4838 Timberline Billing Service LLC 1315 50th Street West Des Moines, IA 50266 Phone: 515-222-0827 Email:[email protected] www.timberlinebilling.com [email protected] Timothy J.Oswald – Deb Harmsen Piper Jaffray Inc. 3900 Ingersoll Ave. Suite 110 Des Moines, IA 50312 515-247-2358 [email protected] ClaimAid 8141 Zionsville Rd. Indianapolis, Indiana 46268 Contact: Chas LaPierre [email protected] 317-777-7539 www.claimaid.com

BRONZE LEVEL PARTNERS

Debbie Ogrizovich - MJCare 2448 S. 102nd St. Suite 340 Milwaukee, WI 53227 414-329-2420 Dan Gould – School Dude 11000 Regency Parkway, Suite 200 Cary, NC 27518 877-868-3833

David Schmidt, Ph.D. – TIAA-CREF 200 North LaSalle, Suite 1600 Chicago, Illinois [email protected] John Seefeld - Jester Ins. Services 303 Watson Powell Jr. Way Des Moines, IA 50309 [email protected] Steve Hewitt - ING 909 Locust St. MS 155 Des Moines, IA 50309 [email protected]

24

COUNSEL’S CORNER

The Top 5 Public Fund Investment Questions

By: Beth Grob Ahlers & Cooney, P.C.

Public entities are often approached about investing public funds in various financial products that seem to earn a larger rate of return than what the market rate is at the time. Whether certain types of financial products are qualified investments under Iowa Code Chapter 12B may be an issue. In general, in which type of investment products may public entities invest? Iowa Code sections 12B.10(5)(a) and 12B.10(7) provide a very specific list of investment for public entities: (1) Obligations of the United States government, its agencies, and instrumentalities. (2) Certificates of deposit and other evidences of deposit at federally insured depository institutions approved pursuant to chapter 12C. (3) Prime bankers' acceptances that mature within two hundred seventy days and that are eligible for purchase by a federal reserve bank, provided that at the time of purchase no more than ten percent of the investment portfolio shall be in investments authorized by this subparagraph and that at the time of purchase no more than five percent of the investment portfolio shall be invested in the securities of a single issuer. (4) Commercial paper or other short-term corporate debt that matures within two hundred seventy days and that is rated within the two highest classifications, as established by at least one of the standard rating services approved by the superintendent of banking by rule adopted pursuant to chapter 17A, provided that at the time of purchase no more than five percent of all amounts invested in commercial paper and other short-term corporate debt shall be invested in paper and debt rated in the second highest classification, and provided further that at the time of purchase no more than ten percent of the investment portfolio shall be in investments authorized by this subparagraph and that at the time of purchase no more than five percent of the investment portfolio shall be invested in the securities of a single issuer. (5) Repurchase agreements whose underlying collateral consists of the investments set out in subparagraph (1) if the political subdivision takes delivery of the collateral either directly or through an authorized custodian. Repurchase agreements do not include reverse repurchase agreements. (6) An open-end management investment company registered with the federal securities and exchange commission under the federal Investment Company Act of 1940, 15 U.S.C. § 80(a), and operated in accordance with 17 C.F.R. § 270.2a-7. (7) A joint investment trust organized pursuant to chapter 28E prior to and existing in good standing on the effective date of this Act or a joint investment trust organized pursuant to chapter 28E after April 28, 1992, provided that the joint investment trust shall either be rated within the two highest classifications by at least one of the standard rating services approved by the superintendent of banking by rule adopted pursuant to chapter 17A and operated in accordance with 17 C.F.R. § 270.2a-7, or be registered with the federal securities and exchange commission under the federal Investment Company Act of 1940, 15 U.S.C. § 80(a), and operated in accordance with 17 C.F.R. § 270.2a-7. The manager or investment advisor of the joint investment trust shall be registered with the federal securities and exchange commission under the Investment Advisor Act of 1940, 15 U.S.C. § 80(b). (8) Notwithstanding sections 12C.2, 12C.4, 12C.6, 12C.6A, and any other provision of law relating to the deposits of public funds, if public funds are deposited in a depository, as defined in section 12C.1, any uninsured portion of the public funds invested through the depository may be invested in certificates of deposit arranged by the depository that are issued by one or more federally insured banks or savings associations regardless of location for the account of the public funds depositor if all of the following requirements are satisfied:

25

a. The full amount of the principal and any accrued interest of each certificate of deposit issued shall be covered by federal deposit insurance. b. The depository, either directly or through an agent or subcustodian, shall act as custodian of the certificates of deposit. c. The day the certificates of deposit are issued, the depository shall have received deposits in an amount eligible for federal deposit insurance from, and issued certificates of deposit to, customers of other financial institutions wherever located that are equal to or greater than the amount of public funds invested under this subsection by the public funds depositor through the depository. Public entities may NOT invest in (1) reverse repurchase agreements; or (2) future and options contracts. Can public entities invest in money market funds? Yes, under certain circumstances. See number 6 above. If so, what types of money market funds? A public entity may only invest in a money market fund that is registered with the federal securities and exchange commission under the federal Investment Company Act of 1940, 15 U.S.C. § 80(a), and operated in accordance with 17 C.F.R. § 270.2a-7 (see number 6 above). How do you determine if a money market fund is registered with the S.E.C. and operated in accordance with S.E.C. rule 2a-7? (1) Any money market fund registered with the S.E.C. will have a prospectus or information statement, a copy of which the municipality must receive. The prospectus/information statement should plainly state in the body of the document that it is registered with the S.E.C. and operated in accordance with S.E.C. rule 2a-7. (2) If a money market fund is registered with the S.E.C. that money market fund is required to make certain quarterly and annual filings with the S.E.C. and which are available on the S.E.C.’s website at http://www.sec.gov/edgar/searchedgar/webusers.htm. Is a verbal confirmation that the money market fund is an authorized investment sufficient? No. It is incumbent on public entities to perform due diligence in determining on their own if an investment fits within the law. A verbal representation that an investment qualifies is not sufficient. A copy of the documents identified in the previous question MUST be requested and retained by the municipality. In this record-low interest rate environment and the ever-increasing number of financial products available for investment, it may be wise for public entities to review its investment policies and practices and to consult with legal counsel. The purpose of this article is to identify issues. It does not purport to be exhaustive or to render legal advice. You should consult with qualified counsel or other professionals in developing responses to specific situations. # 683522.1

26

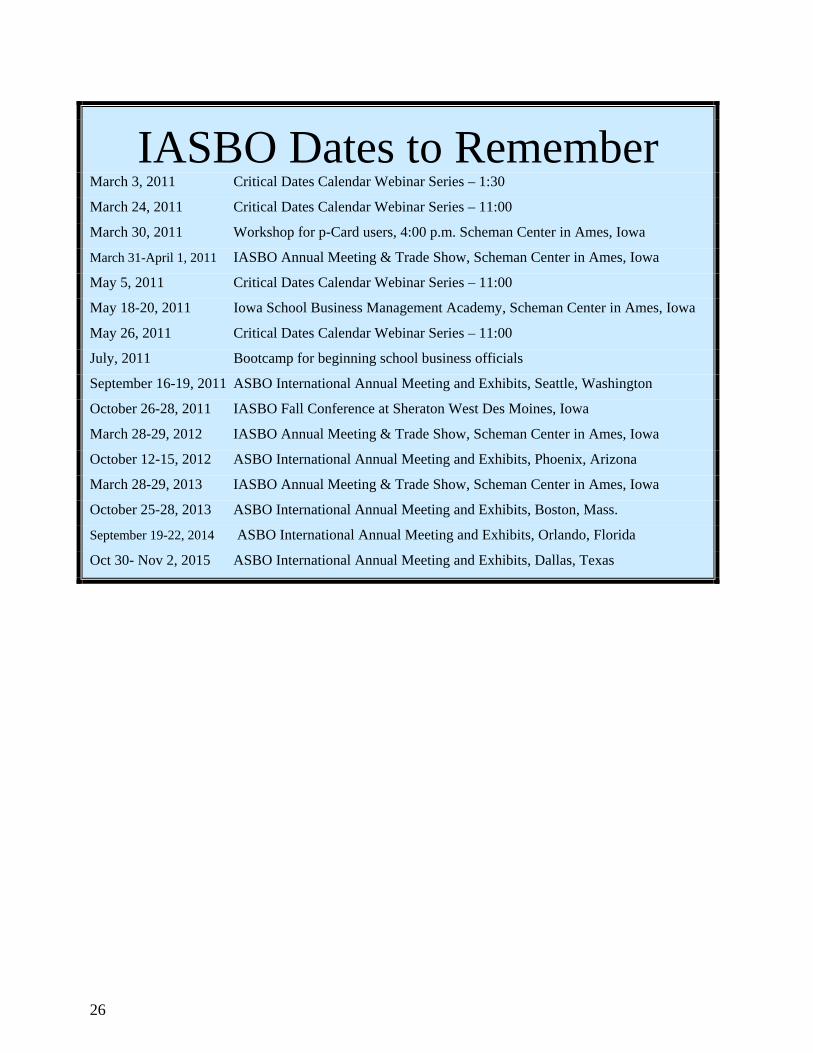

IASBO Dates to Remember March 3, 2011 Critical Dates Calendar Webinar Series – 1:30

March 24, 2011 Critical Dates Calendar Webinar Series – 11:00

March 30, 2011 Workshop for p-Card users, 4:00 p.m. Scheman Center in Ames, Iowa

March 31-April 1, 2011 IASBO Annual Meeting & Trade Show, Scheman Center in Ames, Iowa

May 5, 2011 Critical Dates Calendar Webinar Series – 11:00

May 18-20, 2011 Iowa School Business Management Academy, Scheman Center in Ames, Iowa

May 26, 2011 Critical Dates Calendar Webinar Series – 11:00

July, 2011 Bootcamp for beginning school business officials

September 16-19, 2011 ASBO International Annual Meeting and Exhibits, Seattle, Washington

October 26-28, 2011 IASBO Fall Conference at Sheraton West Des Moines, Iowa

March 28-29, 2012 IASBO Annual Meeting & Trade Show, Scheman Center in Ames, Iowa

October 12-15, 2012 ASBO International Annual Meeting and Exhibits, Phoenix, Arizona

March 28-29, 2013 IASBO Annual Meeting & Trade Show, Scheman Center in Ames, Iowa

October 25-28, 2013 ASBO International Annual Meeting and Exhibits, Boston, Mass.

September 19-22, 2014 ASBO International Annual Meeting and Exhibits, Orlando, Florida

Oct 30- Nov 2, 2015 ASBO International Annual Meeting and Exhibits, Dallas, Texas