Embed Size (px)

Citation preview

1

February 20, 2014 A Coleman Webinar

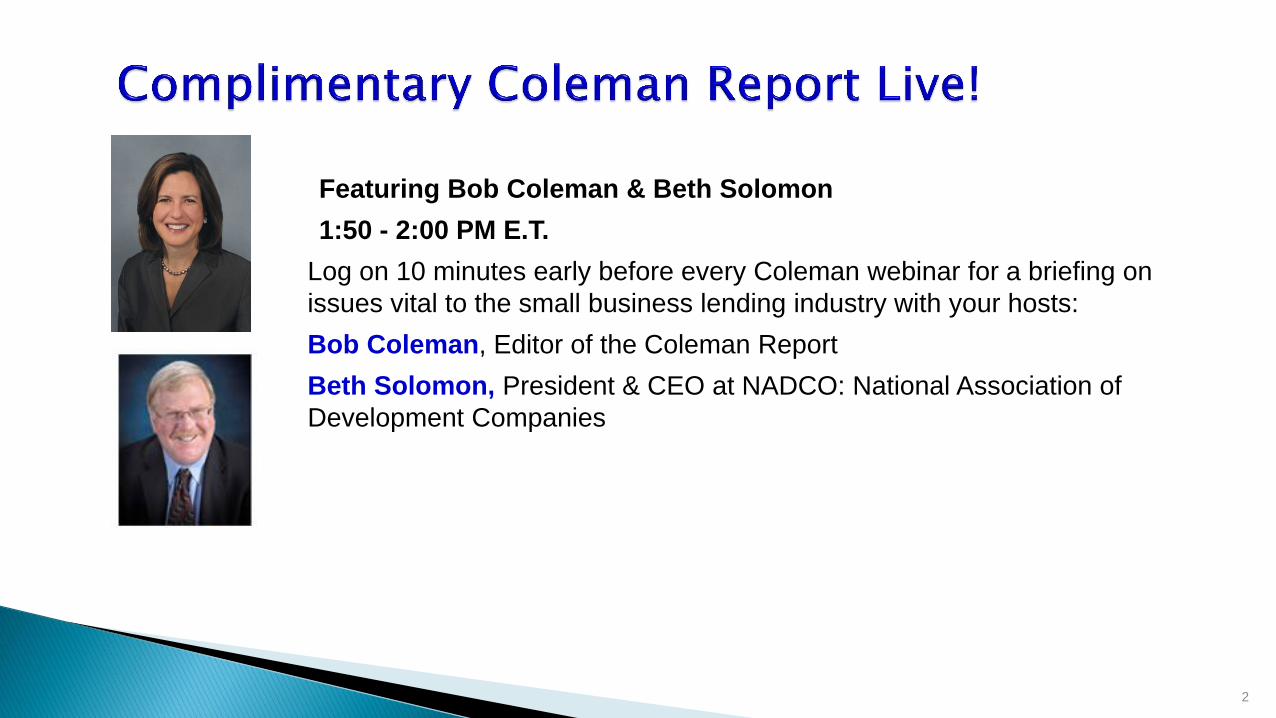

Featuring Bob Coleman & Beth Solomon

1:50 - 2:00 PM E.T.

Log on 10 minutes early before every Coleman webinar for a briefing on

issues vital to the small business lending industry with your hosts:

Bob Coleman, Editor of the Coleman Report

Beth Solomon, President & CEO at NADCO: National Association of

Development Companies

2

3

● Use Go‐to‐Meeting's chat function, you can choose to ask

a question in writing or verbally. If comfortable, give us

your first name, name of bank, and city.

● Send an email to [email protected]

4

● All Coleman Webinar attendees will receive a certificate of

participation. This documents your continuing education history

for your regulators. Also, this documents the answer for SBA’s

Review question of continuing staff education.

● We will automatically forward a certificate of participation for

those who are registered to attend the webinar via GoToWebinar.

● If you have purchased the unlimited site license and would like

certificates for all who attend simply forward their names and

email addresses to [email protected]. She will email the

certificates to all attendees.

When to transfer a loan into liquidation.

Steps to take prior to the Site Visit.

The Site Visit itself.

Writing a Liquidation Plan (or Work-out

Plan).

Offers in Compromise.

Copyright © 2014 Capital Growth Solutions, LLC.

The SBA Website is a wonderful resource tool! A great

deal of information referenced in this presentation is

taken directly from that site. It is WORTH YOUR

TIME to navigate that sight and explore all the resources

SBA has put together for your use. SBA is there to

HELP you through the process. They are there to make

sure your guaranty is honored!

READ the 50 57!!!!!!!!!!!!!!!!!!!!!

Copyright © 2014 Capital Growth Solutions, LLC.

Treat SBA loans just like you do any other commercial loan of

similar gross size at the Lender.

An annual Site Visit should be a requirement of ALL “prudent”

Lenders.

Review files annually before Site Visit to collect missing

financial information.

This opens up lines of communication between the Lender and

the Borrower to forestall any NEED for Liquidation Plans!!!

Copyright © 2014 Capital Growth Solutions, LLC.

Useful information including “Helpful Hints” and fillable file index pages can be found at http://www.sba.gov/HerndonNGPC . (General questions about the process can be made to [email protected].)

Resources specifically referenced in this presentation are: ◦SBA form 1179 ◦SOP 50 57 Chapter 15

Copyright © 2014 Capital Growth Solutions, LLC.

SBA is in the process of encouraging all

Lenders to submit their servicing requests via

E Tran. At this point in time, both methods

are acceptable. SBA is still some time away

from requiring repurchase packages be

submitted via E Tran.

Copyright © 2014 Capital Growth Solutions, LLC.

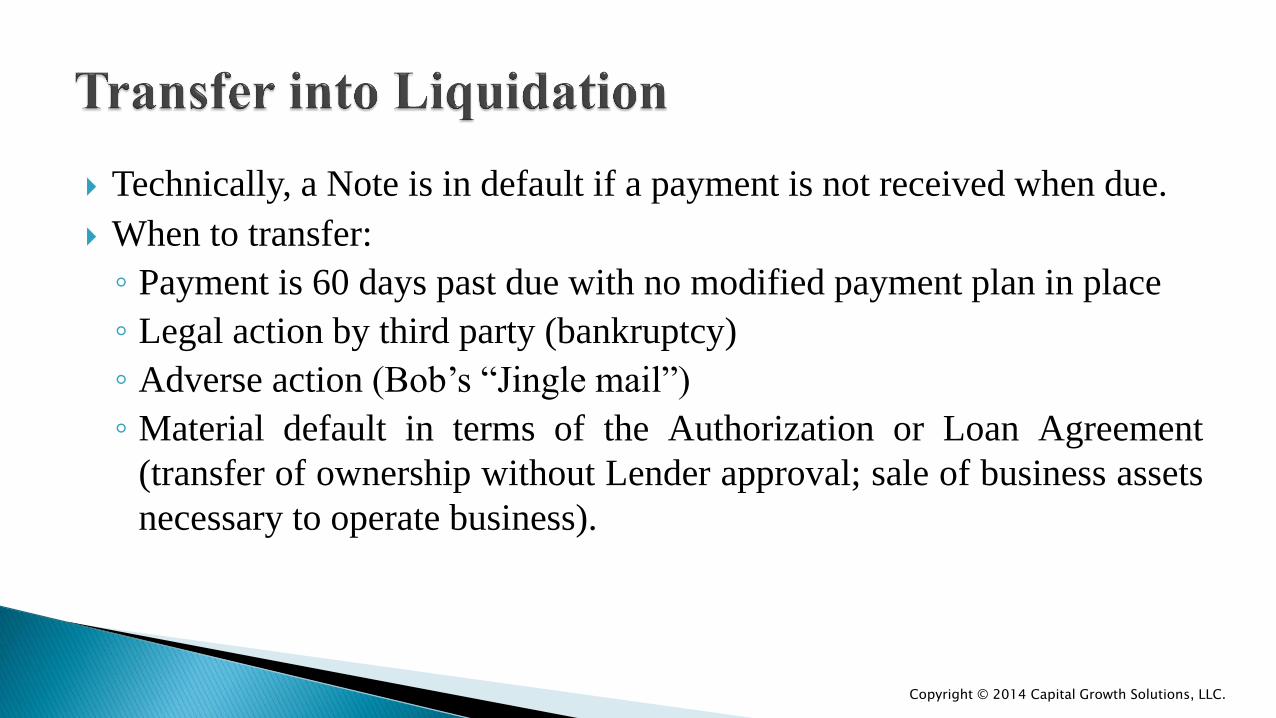

Technically, a Note is in default if a payment is not received when due.

When to transfer:

◦ Payment is 60 days past due with no modified payment plan in place

◦ Legal action by third party (bankruptcy)

◦ Adverse action (Bob’s “Jingle mail”)

◦ Material default in terms of the Authorization or Loan Agreement

(transfer of ownership without Lender approval; sale of business assets

necessary to operate business).

Copyright © 2014 Capital Growth Solutions, LLC.

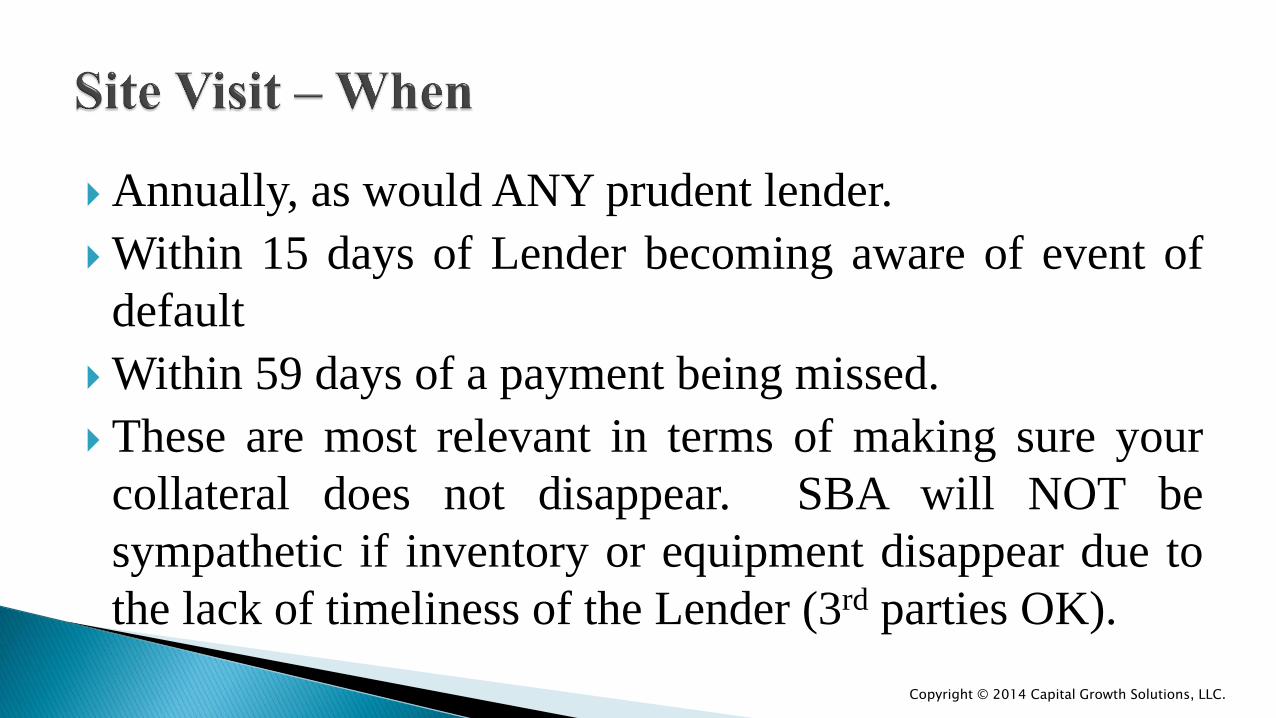

Annually, as would ANY prudent lender.

Within 15 days of Lender becoming aware of event of

default

Within 59 days of a payment being missed.

These are most relevant in terms of making sure your

collateral does not disappear. SBA will NOT be

sympathetic if inventory or equipment disappear due to

the lack of timeliness of the Lender (3rd parties OK).

Copyright © 2014 Capital Growth Solutions, LLC.

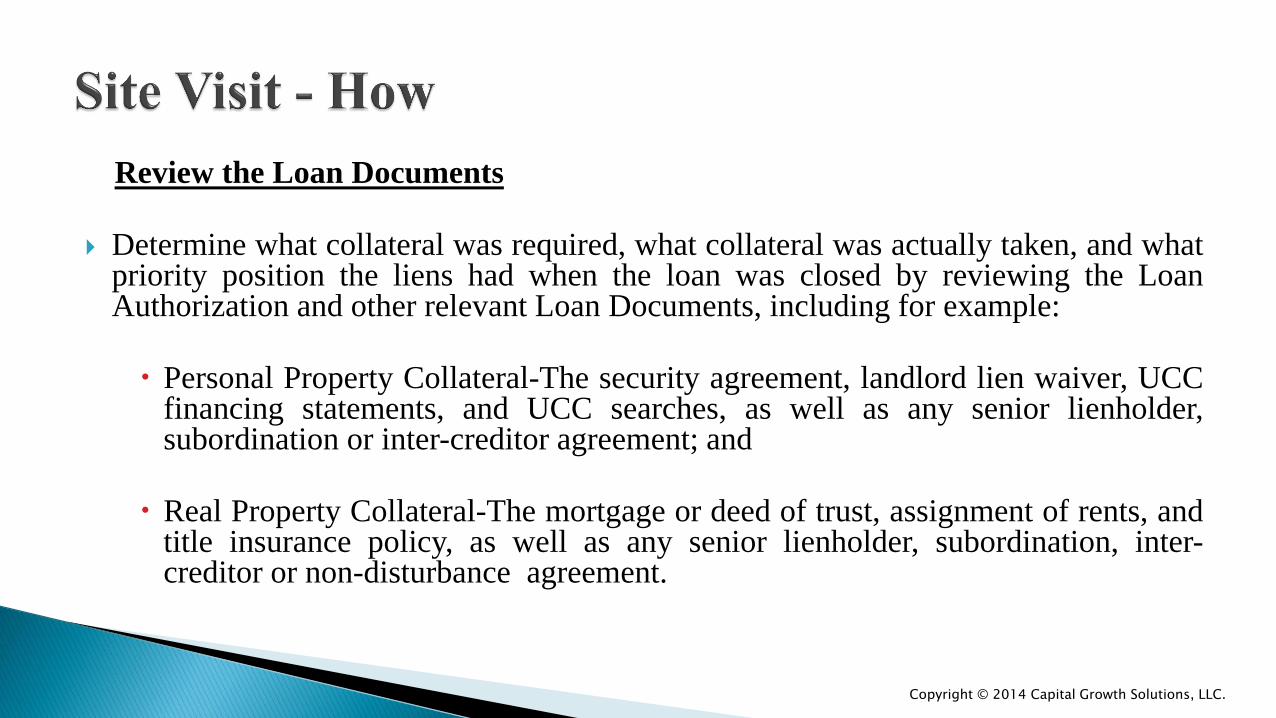

Review the Loan Documents Determine what collateral was required, what collateral was actually taken, and what

priority position the liens had when the loan was closed by reviewing the Loan Authorization and other relevant Loan Documents, including for example:

Personal Property Collateral-The security agreement, landlord lien waiver, UCC

financing statements, and UCC searches, as well as any senior lienholder, subordination or inter-creditor agreement; and

Real Property Collateral-The mortgage or deed of trust, assignment of rents, and

title insurance policy, as well as any senior lienholder, subordination, inter-creditor or non-disturbance agreement.

Copyright © 2014 Capital Growth Solutions, LLC.

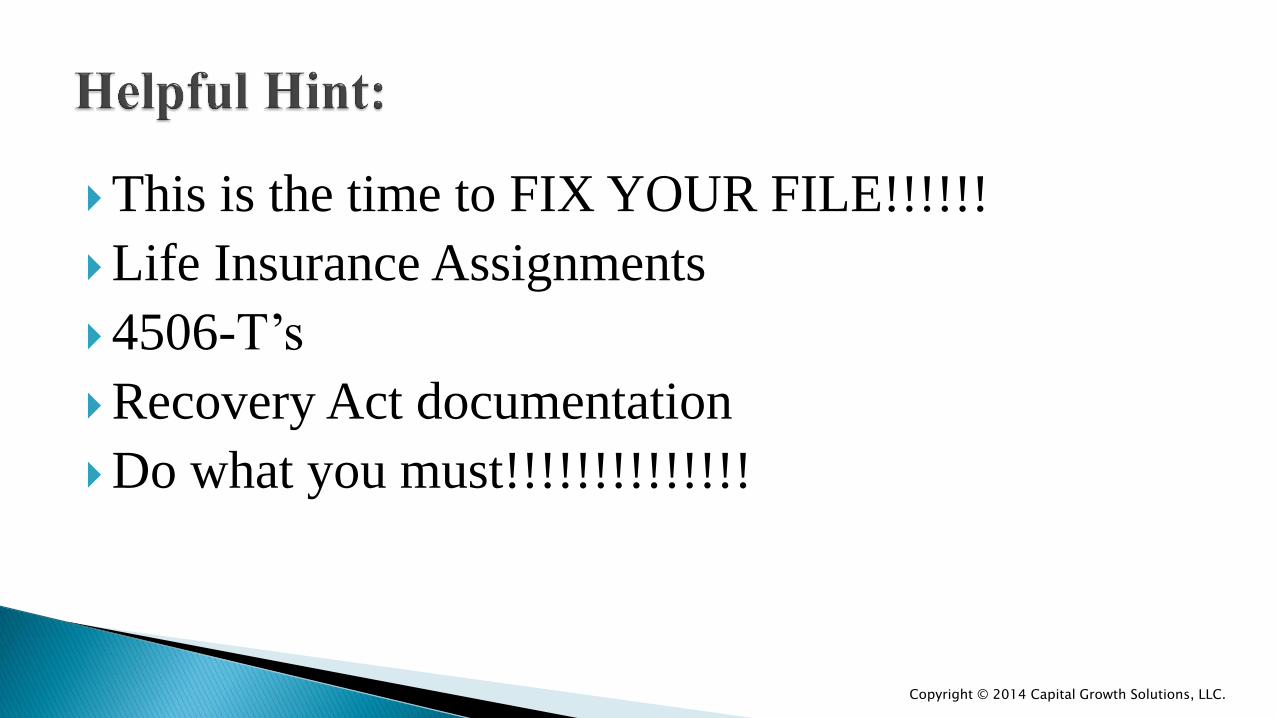

This is the time to FIX YOUR FILE!!!!!!

Life Insurance Assignments

4506-T’s

Recovery Act documentation

Do what you must!!!!!!!!!!!!!!

Copyright © 2014 Capital Growth Solutions, LLC.

Obtain a current title report or UCC search to verify the priority

of the lien(s) securing the SBA loan.

If the collateral is located on leased premises, contact the

landlord to determine whether the rent is past due.

Contact local taxing authorities to determine whether there are

delinquent real or personal property taxes that have, or will

soon have, priority over the lien securing the SBA loan.

Copyright © 2014 Capital Growth Solutions, LLC.

Personal Property

◦ If this is it (foreclosure time), bring an appraiser out with you,

along with a listing you provided SBA at the time of approval.

Take pictures and compare serial numbers, if appropriate. My

OPINION is to have an appraiser who can also auction and

store the collateral for you, if need be. I like to have the

Landlord present if at all possible, both to agree on what’s

who’s and to have a potential purchaser.

Copyright © 2014 Capital Growth Solutions, LLC.

Real Property

◦ State specific. I prefer a “liquidation value” appraisal. The major

benefits are that it can be done quickly, cheaply (relatively), and gives

the Lender a realistic value in a quick, forced sale situation.

◦ Fair value appraisals. These are required in some states which require

the Lender to bid at auction the lower of the “Fair Value” of the

property or the loan amount. Awful rule (running commentary!) This

essentially releases any guarantors from obligation with the assumption

that the property CAN be sold at that value.

Copyright © 2014 Capital Growth Solutions, LLC.

At a minimum, when you have completed the site visit you

have ascertained:

◦ Whether the business is viable

◦ Where your collateral is located

◦ Approximate value of the collateral

◦ Potential environmental hazards

◦ Roadblocks to orderly liquidation

◦ Workout options.

Copyright © 2014 Capital Growth Solutions, LLC.

SBA ALWAYS prefers a workout to a liquidation to preserve

the viability of the business, and to retain jobs and a tax base.

You have tremendous options at your disposal as a SBA lender

to give the small business borrower every chance of success.

The “Workout Plan” can be this vehicle and can be crafted with

the Borrower’s benefit in mind, and should be agreed to in

writing between the small business borrower and the lender.

These include deferments, suspension of payments, additional

funds (with SBA approval), and extending maturities.

Copyright © 2014 Capital Growth Solutions, LLC.

Justification for transfer to “liquidation” status:

(e.g., Non-Payment, Bankruptcy [attach 341

Notice - Meeting of Creditors], Property

Abandoned, 3rd Party Litigation/Foreclosure by

Prior Lienholder, Business Closed, other)

Copyright © 2014 Capital Growth Solutions, LLC.

Cause of business breakdown & workout attempts: Include comments

on management assistance offered and/or given, and attach copy of the

most recent field visit report or memo. SBA requires a site visit to the

borrower’s business premises and the site of any other worthwhile

collateral within 60 days of an unremedied default in payment, or as

soon as possible if there are assets of significant value that could be

removed or depleted. Whether or not a payment default exists, a site visit

must be conducted within 15 days of any event which causes a loan to be

placed into liquidation status.

Copyright © 2014 Capital Growth Solutions, LLC.

Describe any “non-SBA” loans lender has with

any borrower, guarantor or principal: if none, so

state. If yes, please attach copies of loan

documentation (e.g., Note, Security Agreement,

UCC filings, Deed of Trust, Mortgage, etc.) and a

proposal as to how you will allocate and share

expenses and funds recovered.

Copyright © 2014 Capital Growth Solutions, LLC.

List name, address, SSN and Tax ID# for all

obligors and guarantors: Include copies of

demand letters if sent, and whether life

insurance is still in force if it was required.

Copyright © 2014 Capital Growth Solutions, LLC.

Complete the Litigation Plan Tabs if court action is

necessary and any of the following are present: (1)

the litigation will be contested; (2) you have any-

non SBA loans to the borrower, guarantors or

principles; or (3) the litigation expenses are

expected to exceed $10,000.00.

Copyright © 2014 Capital Growth Solutions, LLC.

General Recovery Plan: Briefly describe the proposed liquidation process and the estimated time. Discuss actions to be taken to dispose of all collateral (e.g., voluntary sale, abandonment, judicial or non-judicial foreclosure, public auction, compromise settlement, deed in lieu, etc.). It is important to comment on any potential environmental/toxic concerns, whether hazard insurance is in effect or if purchase of insurance is recommended, and if there are any significant items of collateral missing. If it appears the liquidation value of all collateral is insufficient to fully repay the loan, include discussion of what other options are considered feasible compared with the estimated costs to pursue (e.g., litigation against guarantors). SBA procedures require that business assets be liquidated first and compromise alternatives be explored, if feasible, prior to foreclosure against a personal residence.

Copyright © 2014 Capital Growth Solutions, LLC.

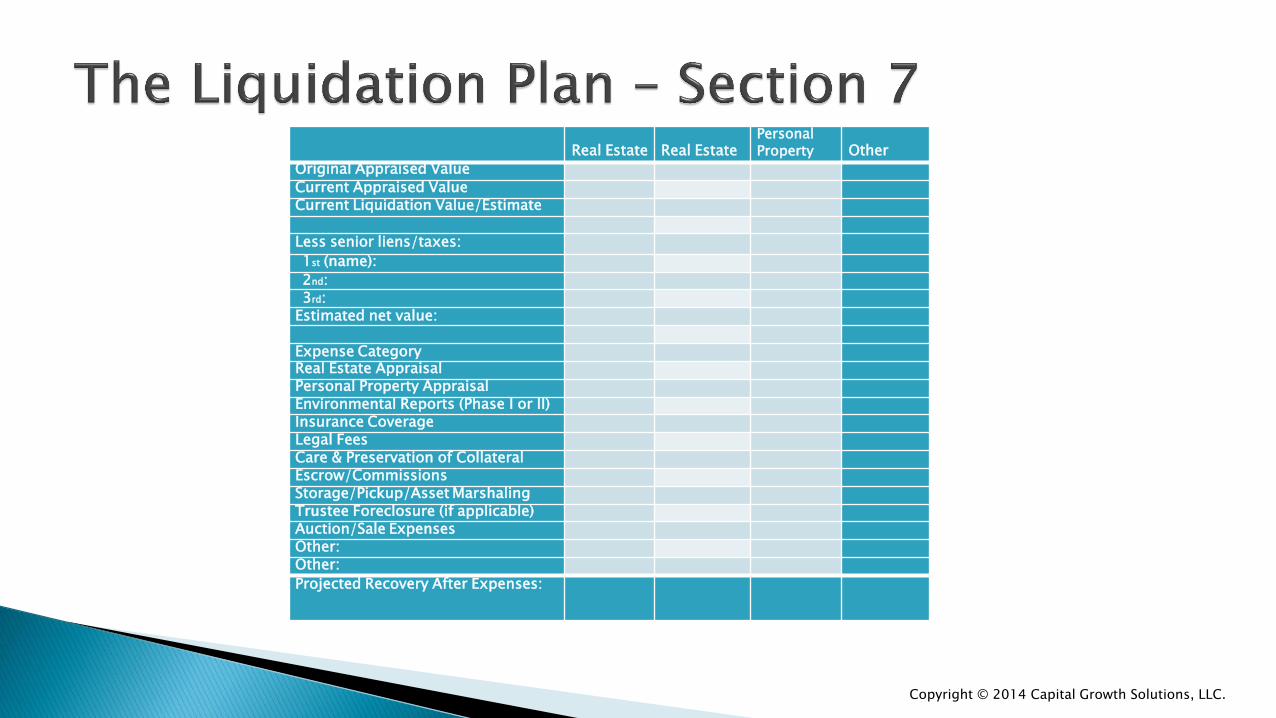

Real Estate

Real Estate

Personal Property

Other

Original Appraised Value Current Appraised Value Current Liquidation Value/Estimate

Less senior liens/taxes:

1st (name): 2nd: 3rd:

Estimated net value: Expense Category Real Estate Appraisal Personal Property Appraisal Environmental Reports (Phase I or II) Insurance Coverage Legal Fees Care & Preservation of Collateral Escrow/Commissions Storage/Pickup/Asset Marshaling Trustee Foreclosure (if applicable) Auction/Sale Expenses Other: Other: Projected Recovery After Expenses:

Copyright © 2014 Capital Growth Solutions, LLC.

Attach copies of prior/current real and personal property appraisal summaries, copies of the field visit report/memo, and the executive summary of any environmental reports. I have forwarded Coleman the following Liquidation Plan in Word format (YES please plagiarize!) which can be provided you upon request.

Copyright © 2014 Capital Growth Solutions, LLC.

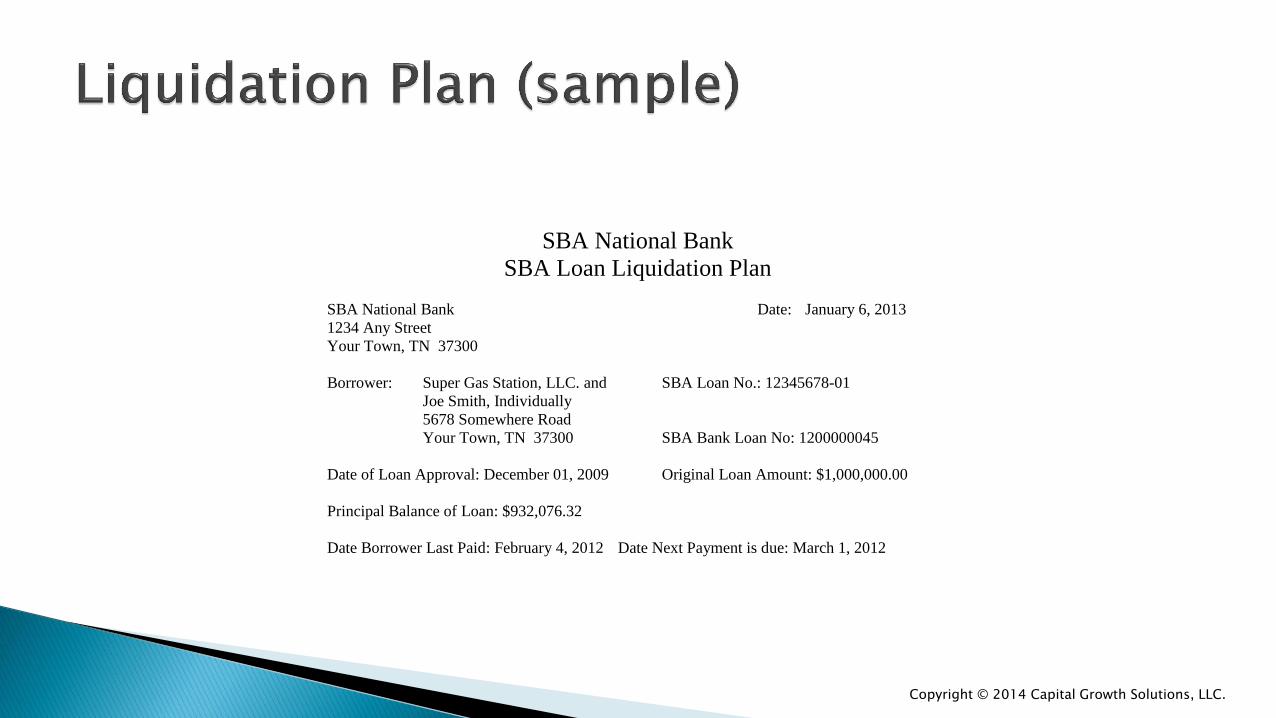

SBA National Bank

SBA Loan Liquidation Plan

SBA National Bank Date: January 6, 2013

1234 Any Street

Your Town, TN 37300

Borrower: Super Gas Station, LLC. and SBA Loan No.: 12345678-01

Joe Smith, Individually

5678 Somewhere Road

Your Town, TN 37300 SBA Bank Loan No: 1200000045

Date of Loan Approval: December 01, 2009 Original Loan Amount: $1,000,000.00

Principal Balance of Loan: $932,076.32

Date Borrower Last Paid: February 4, 2012 Date Next Payment is due: March 1, 2012

Copyright © 2014 Capital Growth Solutions, LLC.

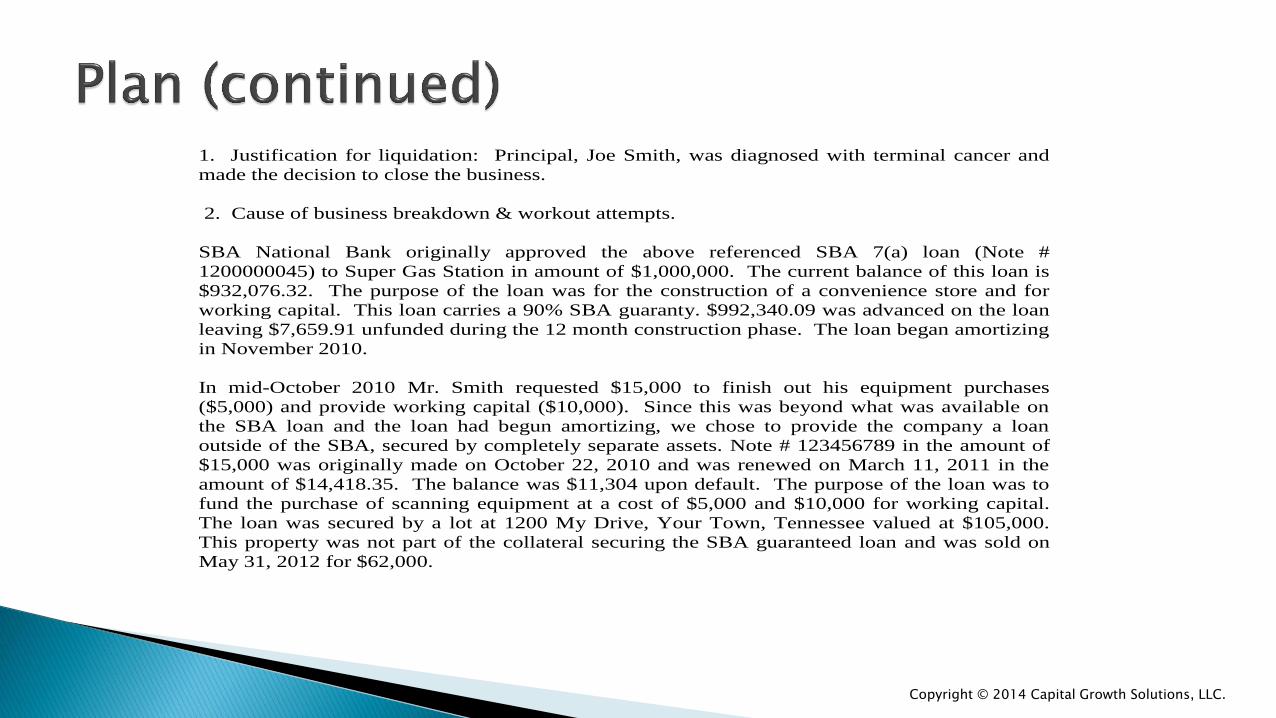

1. Justification for liquidation: Principal, Joe Smith, was diagnosed with terminal cancer and

made the decision to close the business.

2. Cause of business breakdown & workout attempts.

SBA National Bank originally approved the above referenced SBA 7(a) loan (Note #

1200000045) to Super Gas Station in amount of $1,000,000. The current balance of this loan is

$932,076.32. The purpose of the loan was for the construction of a convenience store and for

working capital. This loan carries a 90% SBA guaranty. $992,340.09 was advanced on the loan

leaving $7,659.91 unfunded during the 12 month construction phase. The loan began amortizing

in November 2010.

In mid-October 2010 Mr. Smith requested $15,000 to finish out his equipment purchases

($5,000) and provide working capital ($10,000). Since this was beyond what was available on

the SBA loan and the loan had begun amortizing, we chose to provide the company a loan

outside of the SBA, secured by completely separate assets. Note # 123456789 in the amount of

$15,000 was originally made on October 22, 2010 and was renewed on March 11, 2011 in the

amount of $14,418.35. The balance was $11,304 upon default. The purpose of the loan was to

fund the purchase of scanning equipment at a cost of $5,000 and $10,000 for working capital.

The loan was secured by a lot at 1200 My Drive, Your Town, Tennessee valued at $105,000.

This property was not part of the collateral securing the SBA guaranteed loan and was sold on

May 31, 2012 for $62,000.

Copyright © 2014 Capital Growth Solutions, LLC.

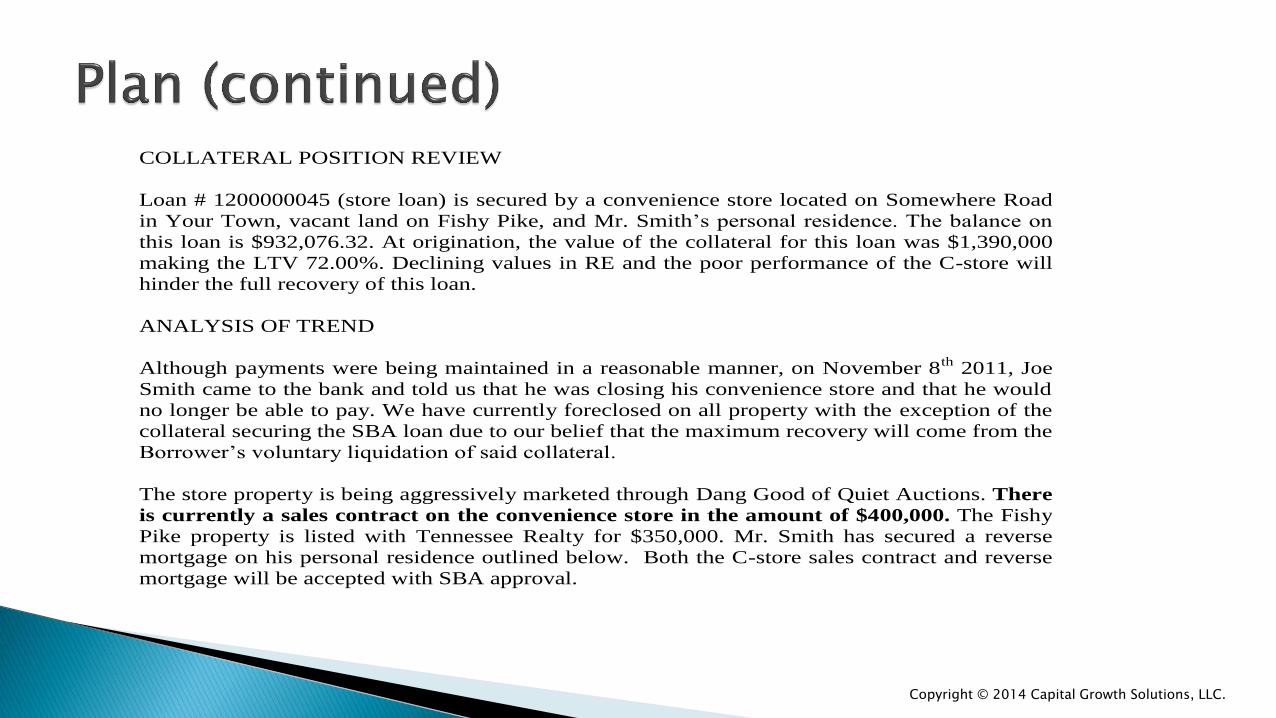

COLLATERAL POSITION REVIEW

Loan # 1200000045 (store loan) is secured by a convenience store located on Somewhere Road

in Your Town, vacant land on Fishy Pike, and Mr. Smith’s personal residence. The balance on

this loan is $932,076.32. At origination, the value of the collateral for this loan was $1,390,000

making the LTV 72.00%. Declining values in RE and the poor performance of the C-store will

hinder the full recovery of this loan.

ANALYSIS OF TREND

Although payments were being maintained in a reasonable manner, on November 8th

2011, Joe

Smith came to the bank and told us that he was closing his convenience store and that he would

no longer be able to pay. We have currently foreclosed on all property with the exception of the

collateral securing the SBA loan due to our belief that the maximum recovery will come from the

Borrower’s voluntary liquidation of said collateral.

The store property is being aggressively marketed through Dang Good of Quiet Auctions. There

is currently a sales contract on the convenience store in the amount of $400,000. The Fishy

Pike property is listed with Tennessee Realty for $350,000. Mr. Smith has secured a reverse

mortgage on his personal residence outlined below. Both the C-store sales contract and reverse

mortgage will be accepted with SBA approval.

Copyright © 2014 Capital Growth Solutions, LLC.

REPAYMENT SOURCES (INCLUDE DEBT SERVICE COVERAGE)

The repayment source for these loans will be the liquidation of collateral.

INDIVIDUAL (INCLUDE INDIVIDUAL’S LIQUID ASSETS)

Mr. Smith’s personal financial statement dated 03/11/2011 shows liquid assets of $23,440. This

was in a checking account at 1st Tennessee. His total assets are $1,719,940 which is made up

primarily of real estate. The total liabilities shown are $932,076. This is all store related debt. His

net worth is $787,864. It is believed that this is a highly inflated value based on his estimate of

RE values.

3. Does the Lender have any “non-SBA” loans with any borrower, guarantor, or principal?

SBA National Bank has funded three additional loans to Super Gas Station:

Note # 123456789

Note # 987654321

Note # 123567321

For further explanation see Page 1. Item 2: Cause of business breakdown and workout attempts.

In April of 2012 SBA Bank foreclosed on the collateral mention in the above referenced

loans. Copy of Notes and Deeds of Trust attached.

Copyright © 2014 Capital Growth Solutions, LLC.

. a. Obligors: Super Gas Station, LLC

5678 Somewhere Road

Your Town, TN 37300

EIN #27-123156

Joe G. Smith

1234 Rock Road

Your Town, TN 37300

SS#123-45-6789

b. Guarantor: N/A

c. Life Insurance: Original Life Insurance requirement of $1,000,000.00 was reduced to

$500,000 by stamp action January 19, 2010 (#573470) and later eliminated in its entirety by

stamp action dated February 10, 2010 (#578317).

d. Demand has not been made at this point in time. Borrower is voluntarily liquidating

collateral.

5. Will legal action be required? Not at this time.

Copyright © 2014 Capital Growth Solutions, LLC.

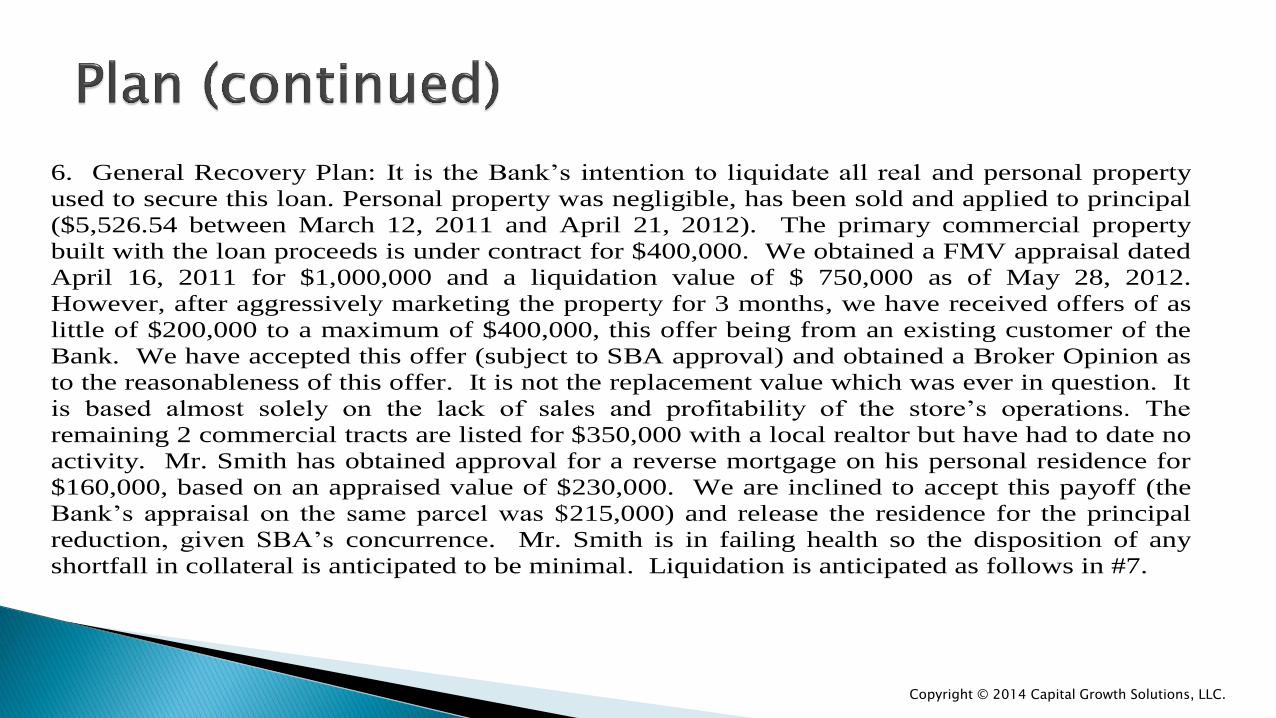

6. General Recovery Plan: It is the Bank’s intention to liquidate all real and personal property

used to secure this loan. Personal property was negligible, has been sold and applied to principal

($5,526.54 between March 12, 2011 and April 21, 2012). The primary commercial property

built with the loan proceeds is under contract for $400,000. We obtained a FMV appraisal dated

April 16, 2011 for $1,000,000 and a liquidation value of $ 750,000 as of May 28, 2012.

However, after aggressively marketing the property for 3 months, we have received offers of as

little of $200,000 to a maximum of $400,000, this offer being from an existing customer of the

Bank. We have accepted this offer (subject to SBA approval) and obtained a Broker Opinion as

to the reasonableness of this offer. It is not the replacement value which was ever in question. It

is based almost solely on the lack of sales and profitability of the store’s operations. The

remaining 2 commercial tracts are listed for $350,000 with a local realtor but have had to date no

activity. Mr. Smith has obtained approval for a reverse mortgage on his personal residence for

$160,000, based on an appraised value of $230,000. We are inclined to accept this payoff (the

Bank’s appraisal on the same parcel was $215,000) and release the residence for the principal

reduction, given SBA’s concurrence. Mr. Smith is in failing health so the disposition of any

shortfall in collateral is anticipated to be minimal. Liquidation is anticipated as follows in #7.

Copyright © 2014 Capital Growth Solutions, LLC.

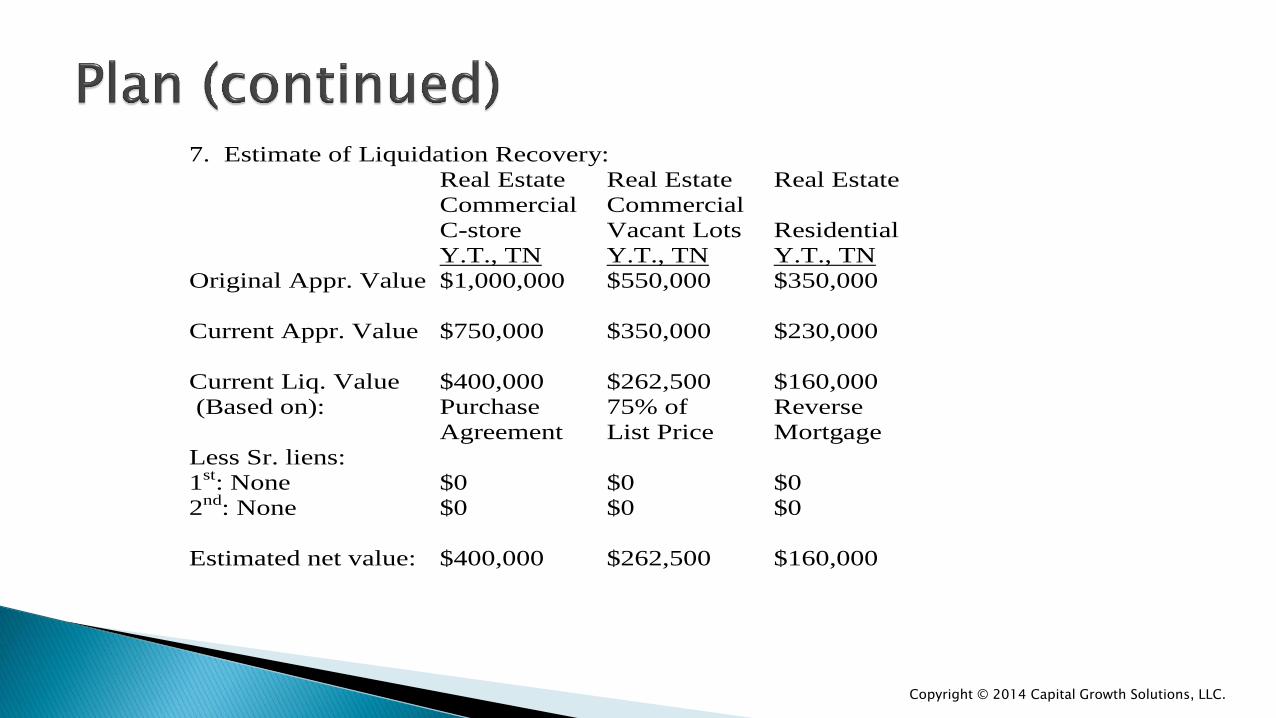

7. Estimate of Liquidation Recovery:

Real Estate Real Estate Real Estate

Commercial Commercial

C-store Vacant Lots Residential

Y.T., TN Y.T., TN Y.T., TN

Original Appr. Value $1,000,000 $550,000 $350,000

Current Appr. Value $750,000 $350,000 $230,000

Current Liq. Value $400,000 $262,500 $160,000

(Based on): Purchase 75% of Reverse

Agreement List Price Mortgage

Less Sr. liens:

1st: None $0 $0 $0

2nd

: None $0 $0 $0

Estimated net value: $400,000 $262,500 $160,000

Copyright © 2014 Capital Growth Solutions, LLC.

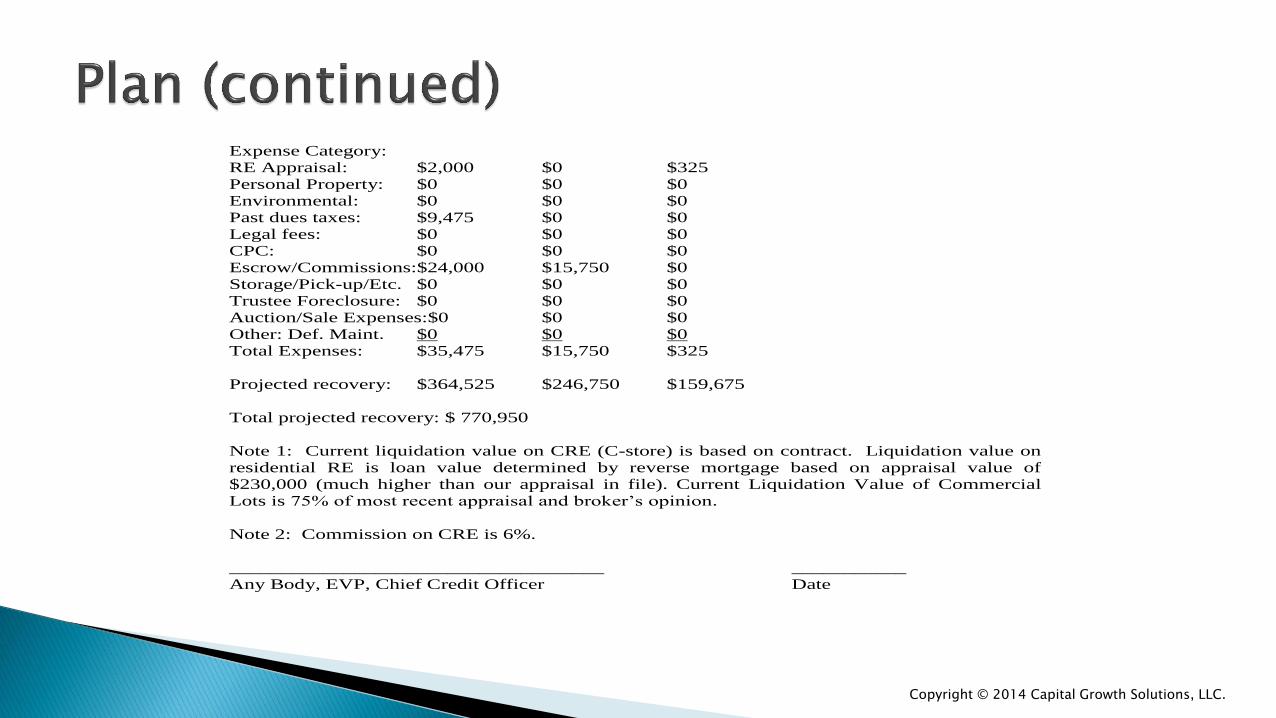

Expense Category:

RE Appraisal: $2,000 $0 $325

Personal Property: $0 $0 $0

Environmental: $0 $0 $0

Past dues taxes: $9,475 $0 $0

Legal fees: $0 $0 $0

CPC: $0 $0 $0

Escrow/Commissions:$24,000 $15,750 $0

Storage/Pick-up/Etc. $0 $0 $0

Trustee Foreclosure: $0 $0 $0

Auction/Sale Expenses:$0 $0 $0

Other: Def. Maint. $0 $0 $0

Total Expenses: $35,475 $15,750 $325

Projected recovery: $364,525 $246,750 $159,675

Total projected recovery: $ 770,950

Note 1: Current liquidation value on CRE (C-store) is based on contract. Liquidation value on

residential RE is loan value determined by reverse mortgage based on appraisal value of

$230,000 (much higher than our appraisal in file). Current Liquidation Value of Commercial

Lots is 75% of most recent appraisal and broker’s opinion.

Note 2: Commission on CRE is 6%.

____________________________________ ___________

Any Body, EVP, Chief Credit Officer Date

Copyright © 2014 Capital Growth Solutions, LLC.

Offer in Compromise. Typically at the culmination of the liquidation of all business and other worthwhile assets, an OIC is the process used to evaluate a monetary offer in exchange for the release of a personal guaranty on the loan. An Offer in Compromise is an action that requires SBA’s express written consent and may be submitted to SBA using the OIC Tabs.

Copyright © 2014 Capital Growth Solutions, LLC.

1) Needs to be substantial in relationship to Borrower/Guarantors’ ability to pay and the outstanding debt. The Bank MUST make a recommendation!

2) Extraordinary circumstances.

3) Last resort.

4) OIC Tabs; be COMPLETE!!!

Copyright © 2014 Capital Growth Solutions, LLC.

Gary E. Griffin

Capital Growth Solutions, LLC

6650 E. Brainerd Road, Suite 212

Chattanooga, TN 37421

423-475-5700 (office)

423-593-0976 (cell)

THANK YOU!!!

Copyright © 2014 Capital Growth Solutions, LLC.