Embed Size (px)

Citation preview

US Companies Doing Business in Canada

Time for a Reality Check

Bottomed out for now?

Technical analysis along with fundamentals– part 2

this issue

US Companies P.4 Reality Check P.7

Bottomed Out P.12 Technical analysis P.18

Canadians Resident Abroad

ISSUE 4: July/Aug 2012

Featured Articles

US Companies in Canada

Canada is a critical market for US com-

panies with the US selling three times

more goods to Canada than to China.

Because of the proximity and size of

the market, many US companies look

to Canada when expanding interna-

tionally.

Read more: page 4

Reality Check

Ever since we had the financial and

housing meltdown in the US in

2007/2008, we have lived on pins and

needles wondering whether we are on

a precipice teetering on the edge of

financial oblivion. One thing that the

previous whitewash taught us is that

there are very few asset classes, re-

gions or sectors,

Read more: page 7

2

Canadians Resident Abroad July/Aug 2012

Contents

Join our Facebook

group

Publisher: Dax Sukhraj Editor: Dax Sukhraj

Editorial Board: Pervez Patel Arun Nagratha

Dax Sukhraj

CRA Magazine is Canada’s first e-magazine designed specifically for Canadians who are presently

living abroad, who have done so in the past or who are contemplating an out-of-country sojourn in

the future.

Our magazine is distributed electronically free of charge to subscribers in 142 countries around the

world. In addition to sound and timely advice in the investment and tax arenas, CRA e-magazine

covers everything from offshore employment, vacation/travel and international real estate informa-

tion to country profiles, medical/insurance and education options for your children.

3

Canadians Resident Abroad July/Aug 2012

First Word

Welcome to the July/Aug 2012 edition of CRA Magazine.

In this issue, our residency experts, Arun Nagratha and Todd Trowbridge, write about US companies doing business in

Canada. With Canada being a critical market for US companies, the writers provide an overview of key corporate and

individual tax considerations for US companies doing business in Canada. This article will help thousands of Canadians

working for US companies in various tax matters.

In Pervez H. Patel’s article this month, our international financial consultant discusses why it is illogical to hold conven-

tional asset allocation positions that are out of sync with what is happening in the real world. The Western world has been

living for far too long on borrowed money to finance a lifestyle/entitlement system that is simply unaffordable. Are we

on the edge of a financial precipice all over again? Please read on to find the answer to this intriguing question.

In this edition, we are publishing an article from one of the leading Canadian portfolio managers which includes an in-

depth analysis about the current market conditions including the corrections we have seen since April 2012.

Abu Nizam continues his technical analysis article and shows some commonly used chart patterns for investment consid-

erations. As always, charts should always be used along with fundamentals.

We sincerely hope that you enjoy this issue. Should you wish to contact us please send an e-mail to

[email protected]. As always, your questions and comments are welcome.

Dax Sukhraj

Publisher Cover page photo credit: Afroza Sarwar

4

US Companies Doing Business in

Canada

Todd C. Trowbridge, CA

Arun (Ernie) Nagratha, CA, CPA

By: Todd C. Trowbridge & Arun Nagratha. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 4

Canada is a critical market for US companies with

the US selling three times more goods to Canada

than to China. Because of the proximity and size of

the market, many US companies look to Canada

when expanding internationally.

However, companies doing business in Canada have

both corporate tax and employee personal tax withhold-

ing and reporting considerations. This article provides

an overview of key corporate and individual tax consid-

erations for US companies doing business in Canada.

Corporate Tax Withholding and Reporting Obligations

If a US company has employees performing services in

Canada, it may be seen to be carrying on business in

Canada. This result does not require a physical plant or

office location, but can occur simply by soliciting orders

or offering services for sale through an agent or em-

ployee. If a Company is deemed to be carrying on busi-

ness in Canada, there will be corporate tax reporting re-

quirements and potentially Canadian taxation. Where

filing requirements are not met, significant penalties may

result even where no tax is owed to Canada. Registra-

tion, collection and reporting requirements may also be

necessary in many circumstances for Canadian Goods

and Services Tax (GST) and Harmonized Sales Tax

(HST).

A US company rendering services in Canada is subject

to a 15% tax withholding on their invoices under Regula-

tion 105 of The Income Tax Act (and an additional 9%

under Quebec tax law if services are rendered in Que-

bec). The Canadian customer is required to withhold

and remit the tax to the Canada Revenue Agency (CRA)

as well as file Form T4A-NR to report this tax withhold-

ing. The withholding is not a final tax but rather a tax

instalment against a potential tax liability in Canada.

Under the Canada-US Tax Treaty, a US corporation car-

rying on business in Canada is only subject to taxation

on income earned in Canada through a fixed place of

business or permanent establishment (PE in Canada).

Even if a US Company providing services in Canada

doest not have a factual PE, the Fifth Protocol of the

Canada-US tax treaty expands the definition of PE to

provide the possibility of a “deemed” permanent estab-

lishment in Canada. A deemed PE would occur in a

case where services are provided in Canada for an ag-

gregate of 183 days or more in any twelve-month period

beginning or ending in the year with respect to the same

or connected project for customers who are either resi-

dents of Canada or who maintain a permanent establish-

ment in Canada and the services are provided in respect

of that permanent establishment.

5

US Companies Doing Business in

Canada

By: Todd C. Trowbridge & Arun Nagratha. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 5

If it is determined that the US company does not have a

factual or deemed PE in Canada, it can file a treaty

based exemption with its Canadian corporate tax return

in order to obtain a refund of the tax withheld on its in-

voices. Further, where a US company will not have a

PE in Canada in respect of their services, it may be pos-

sible to obtain a Regulation 105 waiver (in respect of the

15% tax withholding) in advance of providing their ser-

vices in Canada in order to eliminate the cash flow im-

pact of this tax withholding.

Individual Tax Withholding and Reporting Obligations

A US company will have payroll withholding and report-

ing obligations for both Canadian resident and non-

resident employees, in relation to employment exercised

in Canada, even if it does not have a deemed or actual

PE in Canada. There is potential for significant penalties

and interest charges if the company is not compliant with

the tax withholding requirements.

However, if applied and approved by the Canada Reve-

nue Agency in advance, a Regulation 102 waiver may

be obtained for employees resident in the US that will

ultimately be exempt from Canadian tax under the Can-

ada-US tax treaty. This waiver would eliminate the need

to withhold and remit payroll taxes in respect of their em-

ployment in Canada.

A Regulation 102 waiver can only be obtained if the Ca-

nadian source remuneration is less than $10,000 or the

employee is present in Canada in any 12 month period

beginning or ending in the fiscal year for less than 183

days and the remuneration is not paid by or on behalf of

a person who is a resident of Canada and is not borne

by a PE in Canada. In order to qualify for a Regulation

102 waiver, the non-resident Corporation must first ob-

tain a Regulation 105 waiver to prove it does not have a

PE in Canada.

Where a waiver is not obtainable because the compen-

sation is borne by a PE in Canada or the employee does

not otherwise meet the criteria for a waiver, the US com-

pany will be required to meet the payroll tax withholding

requirements. Also, the employee will have a tax liabil-

ity in Canada and will have a Canadian personal tax re-

turn filing requirement where tax is owing, a return is re-

quested by CRA, or if they wish to claim a refund of

overpaid taxes.

6

US Companies Doing Business in

Canada

By: Todd C. Trowbridge & Arun Nagratha. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 6

Where a waiver is obtainable although not requested,

but the company does not have a PE in Canada, and the

employee otherwise meets the criteria for a waiver, the

company will still be required to meet the payroll tax

withholding requirements. In order to re-claim the taxes

that have been withheld, the employee must file a Cana-

dian tax return. This brings about other complexities in

terms of who will fund the Canadian tax withholdings and

the mechanics of reclaiming this refund if it is determined

that the employee will not have an actual tax liability in

Canada, especially where they have been subject to full

payroll withholding in the US.

The company is required to report Canadian source

earnings and tax withholdings, if applicable, on Form T4

on an annual basis. Even if a Regulation 102 waiver is

granted and no taxes have been withheld, T4 reporting

is still required. Employees would need to apply for ei-

ther an Individual Tax Number or a Social Insurance

Number. There are potential penalties and interest for

failure to file the annual T4 summary and distribute Form

T4.

Canadian social security requirements (Canada Pension

Plan and Employment Insurance) would need to be re-

viewed. If the criteria are met for exemption from Can-

ada Pension Plan contributions for an employee, a Cer-

tificate of Coverage would need to be applied for with the

IRS. The Employment Insurance rules would need to be

reviewed to determine if the employee and Company are

exempt from contributions.

Canada does have a Voluntary Disclosure Program

(VDP) that allows for the relief from penalties and inter-

est for both corporations and individuals that have been

non-compliant in the past. If the voluntary disclosure is

accepted, the taxpayer is still required to pay the taxes

owing plus interest. However, penalties would be

waived if the VDP criteria are met and the Canada

Revenue Agency accepts the VDP.

This article is meant to provide a brief summary of the

withholding and reporting requirements in Canada for

US companies doing business in Canada. A thorough

analysis should be done by companies either contem-

plating doing business in Canada or already doing busi-

ness in Canada.

Arun (Ernie) Nagratha is a partner of Trowbridge Professional Corpo-

ration, Chartered Accountants | Tax Advisors, and specializes in tax

for Canadian expatriates that live abroad. The firm focuses on inter-

national tax services for Canadians and Americans around the world

as well as domestic personal and corporate taxation. For further infor-

mation on their firm and the services they provide, you can contact

him at the details below.

7

Time for a Reality Check of the Global

Conundrum

Pervez H. Patel, ACA, AICWA, CIM, FCSI

By: Pervez Patel. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 7

Ever since we had the financial and housing melt-

down in the US in 2007/2008, we have lived on pins

and needles wondering whether we are on a preci-

pice teetering on the edge of financial oblivion.

One thing that the previous whitewash taught us is that

there are very few asset classes, regions or sectors, out

there that were immune – virtually all equity markets

around the world reverberated to what was happening

on American soil, and theories of the emerging markets

being delinked from the Western world were consigned

to the dustbin of history. Quite literally there was one

market that stood firm in 2008 – Venezuela – and with all

candour, I would suggest that you would not want to in-

vest with the likes of Chavez and Co. Even corporate

bonds and other variations of fixed income / yield were

not immune from the scourge. Of course, one can only

empathize for the bond holders of Lehmann Brothers, at

the time the fourth largest investment bank in the US

who were left with 18 cents on the dollar. Thankfully fi-

nancial institutions North of the 49th parallel were not

quite as narcissistic in their behaviour and held their

ground reasonably well, all things considered.

What has really changed in the last three and a half

years that has us celebrating and making pronounce-

ments that what happened not too long ago was a mere

aberration. Financial advisors and money managers

have suggested a reversion to the mean was inevitable

and have gone back to conventional asset allocations –

in particular the index groupies have once again sug-

gested that passive investing through exchange traded

funds at miniscule fees was the universal panacea for all

the world’s investing woes. It is interesting that every

time in this new millennium we have had bouts of market

euphoria, little heed is paid to the fact that several times

in history markets have decimated portfolios and retire-

ment plans in a way that no one could have foreseen.

With the fixed income world also becoming a desert of

value – how else would you describe getting near zero

yields on two year sovereign debt deposits in US / UK /

Germany and Japan – “safe” fixed income alternatives

offer little recourse. So even if we figure out what ails the

world today, figuring out what could keep principal intact

and yield predictable if nominal outcomes, is entirely an-

other matter.

8

Time for a Reality Check of the Global

Conundrum

By: Pervez Patel. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 8

I had the opportunity of interacting with Krish (Nandu)

Narayanan (the manager of the Trident Global Opportu-

nities fund) in the month of May, and what he observed

had some interesting similarities to what I had gleaned at

a PIMCO conference in mid April. For those of you who

did not read my last published report, PIMCO is the larg-

est fixed income house in the world with approximately

US$ 1.7 trillion under management. A large part of my

current diatribe alludes to market intelligence that I

picked up at these two excellent conferences that I had

the pleasure and distinction of attending. As an advisor

who likes to stay abreast of latest developments, when I

hear two corroborating views from houses which I trust,

it kind of reinforces their thesis on what is likely to hap-

pen. To be fair, we live in quite interesting times, and it

would be churlish for anyone to suggest that we can

state anything about the world economy with exactitude.

Source: Bloomberg, International Monetary Fund (IMF) and Organization for

Economic Cooperation and Development (OECD) websites

What is fairly clear is that we have muddled on in the last

few years post 2008 and seen fairly anemic growth in

most parts of the world - even this very weak-kneed

growth has been due to the financial steroids that gov-

ernments and central banks have forced to inject into the

system. Take away the steroids and we could be staring

into an abyss very soon. Think about this for a moment,

we have fully extended ourselves on monetary policy

with interest rates near zero, and the job growth recov-

ery in the US is still the weakest in post war history and

the fiscal deficit still runs at about the 8% of GDP. A host

of economic figures published in the first week of July

are just wretched.

In most developed nations, we are also quite extended

in terms of debt levels, and so from a fiscal standpoint

we are reaching quite literally a breaking point in terms

of how much more money can be printed to sustain flag-

ging economies.

9

Time for a Reality Check of the Global

Conundrum

By: Pervez Patel. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 9

Please recognize that the table above relates to public

debt. If we were to add private and public debt, the fig-

ures get even scarier: witness the UK where the total of

public and private debt is 950% of GDP – which makes it

quite literally worse than Greece!!!

We are in fact rapidly coming to the point where the abil-

ity of some nations to repay debt is questionable – the

lack of measures to usher in austerity in these nations is

emblematic of their unwillingness to repay debt. While

the Keynesians are suggesting a continuation in printing

more and more money at cheaper and cheaper rates – if

history is any indicator, we are only creating more asset

bubbles, and may I add with all due humility the flow of

capital is clearly sub-optimal as the government (aka the

taxpayer) keeps rewarding the inefficient with more and

more dollops of money. This is the very anti-thesis of

capitalism as we know it as it means society at large

pays the price for those who are incompetent, inefficient

and potentially corrupt.

Most central banks have reacted to this new normal by

ushering in an era of what Bill Gross of PIMCO refers to

as an era of financial repression. This is evidenced by

interest rates close to zero that has absolutely deci-

mated risk-free yields for the retirement community, and

has effectively thrown a monkey wrench into the working

of the insurance and pension industry. Equally there has

been a wholesale fudging of economic data – whether it

be inflation (through hegemonic adjustments), unem-

ployment data (through not counting of people who have

dropped off the rolls in looking for jobs or by counting the

partially employed as full employed) or growth rate as-

sumptions that are dressed up to make incumbent office

holders look good. To be cynical, Western governments

have placed retirees on a sacrificial altar to secure fi-

nancing at artificially low rates of interest to fund their

excesses and those of their major financial houses.

In the last few days and weeks, we have had more evi-

dence of bankers behaving badly all over again. US

banks were once again the subject of focus when they

were obliged to provide their so-called living wills that the

government would use to efficiently wind down these

huge entities. Studies at the MIT Sloan School of Man-

agement by Simon Johnson / John Parsons, recently

brought out this nugget of information about one of the

largest banks in the US. JP Morgan Chase revealed that

$ 50 billion could hypothetically bring down the bank.

Recently this bank indicated that it had lost a figure lar-

ger than $ 3 billion during a period of relative economic

calm through incompetence and negligence on part of its

London trading office. JP Morgan’s total balance sheet is

valued under US accounting standards at about US$ 2.3

trillion. However US rules allow a more generous netting

of derivatives (offsetting netting effect of derivatives that

caused the relatively “minor trading loss”) than European

banks are allowed. JP Morgan’s balance sheet using the

European method expands to $ 4 trillion, making it the

largest bank in the world. Is there a realistic chance of

JP Morgan losing more than $ 50 billion on assets of $ 4

trillion – most of which is in complex derivatives – in the

event of another black swan event like a Euro area

breakup. This would create the biggest financial crisis in

world history – and would make what took place in 2008

look like a picnic.

10

Time for a Reality Check of the Global

Conundrum

By: Pervez Patel. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 10

Of course, just in the last week we had another reminder

courtesy of Barclays that the London Interbank Offered

Rate or LIBOR had been systematically manipulated by

colluding banks in one of the most massive frauds on the

investment community at large. The U.K. Serious Fraud

Office opened a criminal probe into the attempted rigging

of interest rates that led to a record fine against Barclays

Plc (BARC), adding to pressure on banks already under

investigation by regulators around the globe.

Recently the world famous economist Nouriel Roubini

remarked on this last banking debacle that it was unreal-

istic to expect anything better as long as banks had in-

centives to cheat or do things that were illegal or im-

moral. In his mind, the only way to improve the situation

was to break up these financial supermarkets where at

present there were no Chinese walls separating invest-

ment banking / commercial banking / asset manage-

ment / brokerages – to avoid conflicts of interest where

you currently have banks acting on both sides of deals.

Evidence Goldman Sachs holding out as defence that it

could take profits as a principal in the same deal in

which a party for whom it was acting as an agent ended

up losing capital. If in 2008, we believed that banks were

too big to fail, they are now even bigger with JP Morgan

taking over Washington Mutual and the carcass of Bear

Stearns, and with Bank of America taking over Merrill

Lynch and Countrywide Credit.

Nandu sums it up nicely by stating that the West has a

crippled financial system that has significant issues of

capital adequacy stemming from the following:

1. Subprime debt losses from 2007/2008 that are not

recognized

2. Falling home prices signifying future mortgage impair-

ment

3. Huge real estate inventories on bank balance sheets

that are still not marked to market valuations

4. Potential sovereign debt losses in Europe and else-

where

We may not be far wrong in concluding that we have all

the ingredients in place for a perfect economic ty-

phoon. Indeed we may have a confluence of simultane-

ous global train-wrecks in Europe (with the potential of a

Greek exit from the Eurozone),

11

Time for a Reality Check of the Global

Conundrum

By: Pervez Patel. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 11

in the US (with a stall speed recovery that limps into a

double dip given with each new round of quantitative

easing – QE - resulting in diminishing returns), in China

(where the stakes are more in favour of a hard landing

than ever before), in most of the other BRIC nations (hit

by the Eurozone recessions as well as a breakdown of

reforms needed to get these nations moving on domestic

consumption) and finally the potential for conflict in the

Middle East, as an increasingly belligerent Iran thumbs it

nose at US and Israel. The last would inevitably cause

oil prices to spiral out of control that would hasten reces-

sion in most of the Western world.

What is quite worrisome is that we may have run out of

both fiscal and monetary elixirs to resolve this impending

crisis. In 2008, we had interest rates that could move

down from 5 to 6% to near zero – how could interest

rates now go any lower; we had the potential of fiscal

stimuli by way of quantitative easing that is now becom-

ing less and less effective; we had the ability to rescue

and backstop banks – with governments now grappling

with their own insolvencies, the scope for running on fi-

nancial steroids is now effectively diminished. Equally

there is no political appetite for financial austerity as any

move to cut entitlement programs is greeted with indig-

nation.

I will sign off on this rather dour note – my honest effort

has been to represent the state of the global conundrum

with realism without trying to obfuscate the truth. In my

next missive, I will investigate investment alternatives

that I believe will lend themselves well to this new world.

Good tidings and have a wonderful summer with your

loved ones wherever in the world you may be.

The author is an International Financial Planner with Canadian Invest-

ment Consultants. He helps Canadians around the world with financial,

retirement and estate planning and with investments and insurance.

Canadian Investment Consultants is a division of Keybase Financial

Group, with offices across Canada.

12

Bottomed out for now?

Jurrien Timmer

Courtesy: Fidelity Investments

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 12

The stage may be set for government help and a

short-term rally, but problems persist.

It has been quite a few months for stocks. The S&P

500 Index topped out on April 2 at an intra-day high

of 1,422. Then, on June 4, it fell to 1,267 on an intra

-day basis. That’s a correction of 10.9% in the span

of only two months.

In the grand scheme of things, 11% is not a huge de-

cline. We have had many corrections of this magnitude

throughout the decades, and most (but not all) of them

turned out OK. But this one somehow feels worse. Per-

haps it was the speed and persistence of the decline. As

of last Friday (June 1), the Dow had fallen 17 of the past

23 days. Crude oil was even more dramatic, falling 20 of

the past 23 days.

Or perhaps it is the fact that while the S&P 500 fell a

“mere” 11%, many other markets have fared much

worse: the MSCI All Country World Index (ACWI) has

fallen 14% since March, as has the MSCI Europe Index,

and the MSCI Emerging Markets Index has fallen 19%.

Copper has declined 19% since March, and crude oil

has declined 26%, from a high of $111 in March to $82

today. The U.S. has definitely been the best house in a

bad neighbourhood.

We all know the reasons, of course, and they are plenti-

ful: Greece, Spain, China and now even the U.S.

Unresolved issues in Greece and Spain

First of all, there is the ever-spreading eurozone crisis. It

wasn’t bad enough that Greek voters voiced their anti-

austerity anger by electing a variety of so many fringe

parties that it has necessitated a second election (to be

held on June 17), but now the crisis has squarely spread

to Spain. Unlike Greece, which has a solvency problem

at the sovereign level, Spain has a banking crisis. Like

the U.S., Spain went through a property bubble, which is

only now unravelling, leaving its banks exposed, with too

many bad loans and too little capital. The problem is that

the Spanish government doesn’t have the money to re-

capitalize its banks, which means that it has to borrow.

However, there is little appetite for Spanish debt these

days, as evidenced by the fact that Spain’s 10-year yield

has risen to 6.37%, and its spread against German

bonds (bunds) has widened to over 500 basis points.

13

Bottomed out for now?

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 13

Spain is stuck between a rock and a hard place. Prime

Minister Mariano Rajoy wants the “troika” (the EU, IMF

and ECB) to bail out Spain’s banks directly, as opposed

to doing so indirectly through a bailout of the Spanish

sovereign (with the funds then being disbursed to the

banks). Why is this important? The thinking goes that if

Spain accepts bailout money at the sovereign level, it

would have to agree to the same kinds of austerity con-

ditions that caused Greek politicians to get voted out of

office. So if the Rajoy administration can get the troika to

bail out the banks directly, it can presumably avoid a

similar fate. The problem is that the troika’s bailout fund

(the European Financial Stability Fund, or EFSF) is not

allowed to bail out banks directly, only governments (as

it did with Greece). Plus, Germany wants to make sure

that there is a stick to go along with the carrot.

It looks to me as though Spain is playing a game of

chicken with Germany to see if it can let the markets get

close enough to the abyss to force Angela Merkel to

blink first and approve a direct bank recapitalization by

the EFSF, or by the soon-to-be-established European

Stability Mechanism (ESM). We’ll see how this all plays

out, but for now the markets remain on edge, waiting for

some sort of policy response from Germany or the Euro-

pean Central Bank.

14

Bottomed out for now?

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 14

What would a Merkel blink look like? Perhaps Germany

will agree to have the upcoming ESM (expected to

launch on July 9) lend directly to the banks, or for the

ESM to borrow from the ECB so that it can “lever up”

and gain more firepower. Or perhaps Germany could

agree to provide funding for Spain, but with fewer strings

(e.g., austerity conditions) attached. Or perhaps Ger-

many is willing to back-stop a eurozone-wide bank de-

posit guarantee, which is what the U.S. has with the

FDIC.

Any or all of these developments could certainly have a

positive impact, which would be magnified if the ECB

stepped back into the fray with bold action, such as cut-

ting its policy rate (currently at 1%), conducting another

long-term refinancing operation (LTRO) or even buying

sovereign debt outright, like the Fed’s quantitative eas-

ing (QE).

But so far, none of this is happening, and it is hard to

see the troika or even the ECB taking bold action before

the June 17 Greek elections and the French Parliamen-

tary election, or the June 28 and 29 Euro Summit. They

may want to keep their powder dry should the worst-

case scenario of a Greek exit come to pass. The good

news is that there is now a dialogue taking place be-

tween Germany and Spain about a potential bailout, and

we are starting to hear more talk about a banking union

(including deposit guarantees). So that is a step in the

right direction.

Serious slowdown in China

The problems are not just in Europe, of course. We now

have a serious slowdown going on in China that has had

a real impact on Asian stock markets and currencies, as

well as on most commodities.

The question is, what can and will the Chinese govern-

ment do about this? Many investors are assuming that

the central government will simply pull some levers and

stimulate the economy, as it did in 2009, when China

underwent a massive infrastructure spending boom that

benefited the global economy. A repeat of such a boom

is unlikely, in my opinion, because the last one produced

not only a lot of inflation but also a property bubble, as

well as an increase in non-performing loans in the bank-

ing sector.

That doesn’t mean, of course, that China will just sit idly

by. There are still some levers that it can pull. One of

them is to get more aggressive in cutting the reserve re-

quirement ratio (RRR) for banks. This is the amount of

funds that banks have to set aside when they make

loans. The higher the ratio, the less there is available to

lend, and vice versa. So far, the People’s Bank of China

has lowered the RRR only a few times, and the rate is

still very high, at 20%. So there is a lot more that can be

done. In fact, China just lowered rates this week, by 25

basis points.

15

Bottomed out for now?

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 15

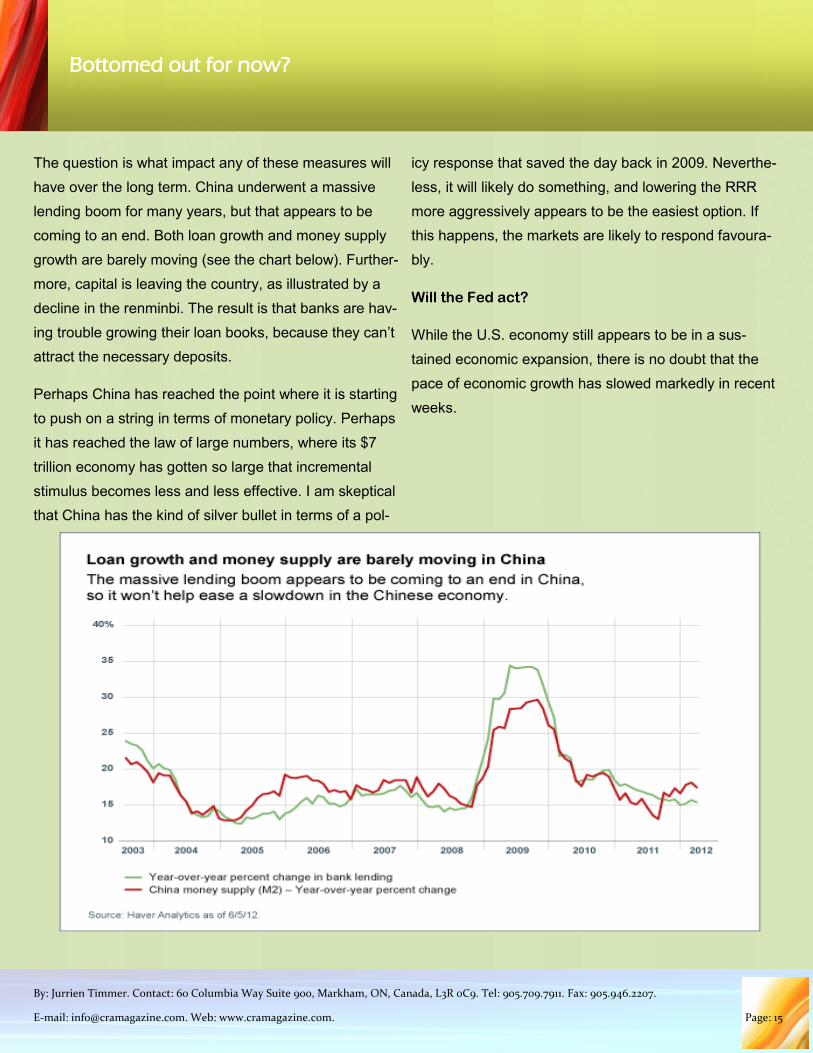

The question is what impact any of these measures will

have over the long term. China underwent a massive

lending boom for many years, but that appears to be

coming to an end. Both loan growth and money supply

growth are barely moving (see the chart below). Further-

more, capital is leaving the country, as illustrated by a

decline in the renminbi. The result is that banks are hav-

ing trouble growing their loan books, because they can’t

attract the necessary deposits.

Perhaps China has reached the point where it is starting

to push on a string in terms of monetary policy. Perhaps

it has reached the law of large numbers, where its $7

trillion economy has gotten so large that incremental

stimulus becomes less and less effective. I am skeptical

that China has the kind of silver bullet in terms of a pol-

icy response that saved the day back in 2009. Neverthe-

less, it will likely do something, and lowering the RRR

more aggressively appears to be the easiest option. If

this happens, the markets are likely to respond favoura-

bly.

Will the Fed act?

While the U.S. economy still appears to be in a sus-

tained economic expansion, there is no doubt that the

pace of economic growth has slowed markedly in recent

weeks.

16

Bottomed out for now?

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 16

We are now in a global slowdown, coupled with a debt

crisis in Europe and a potential hard landing in China.

And I haven’t even mentioned the fiscal cliff, which, ac-

cording to the Congressional Budget Office, would cause

a recession in the U.S. if it came to pass. When it rains,

it certainly pours.

This has the potential to bring the Federal Reserve (the

Fed), which meets on June 20, back into the game with

another policy response. Fed chair Ben Bernanke can’t

be too pleased to see the dollar rally as sharply as it has,

to see the payroll numbers come in as soft as they have

and to see the stock market correct so sharply in the

span of just a few weeks.

So perhaps the Fed is ready to act. But what can it do?

Certainly the markets would be thrilled if the Fed were to

embark on another traditional large-scale asset program,

more commonly known as QE. Certainly the gold bugs

would. Or perhaps it will announce an extension of Op-

eration Twist (which would entail selling more short-

dated securities in exchange for long-dated Treasury

bonds and mortgages).

My guess is that the Fed is not there yet. I think the bar

is pretty high for it to take such dramatic action, espe-

cially in an election year. Besides, what will either action

accomplish over the long term? It is questionable

whether the Fed's previous large-scale asset purchases

provided much more than a temporary sugar high, and

after all, Treasury yields are already at historic lows, with

the 10-year yield dropping to 1.43% on May 30.

Besides, there’s a reason rates are so low, and that is

that collateral is becoming scarcer and investors are run-

ning out of so-called risk-free assets. This is why inves-

tors have been hoarding Treasuries, German bunds and

Japanese government bonds in recent months (and, as

of last week, even gold).

The whole purpose of QE1 and QE2 was linked to the so

-called Portfolio Channel Theory, which holds that when

the Fed steps in as an artificial buyer of risk-free assets

(i.e., Treasuries), investors will then sell these safe as-

sets to the Fed and be forced to go out along the risk

curve to buy risky assets like corporate bonds and equi-

ties. But in the current climate, one really has to wonder

if the Fed can make this Portfolio Channel Theory work.

After all, if Treasuries are the ultimate safe haven, will

investors easily part with them, even at inflated prices?

Recent market behaviour suggests they won’t.

What’s next?

So what will actually happen? I can only guess, of

course. My sense is that things are getting bad enough

to once again force the hand of policy makers in Europe,

China and even the U.S. But what can central bankers

and policy makers do quickly in order to satisfy impatient

investors looking for instant gratification? Most of the

measures in Europe, for instance, will take time to be

agreed upon, let alone implemented.

17

Bottomed out for now?

By: Jurrien Timmer. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 17

There is still one piece of low-hanging fruit out there on

the monetary policy front: a central bank liquidity swap,

highlighted in a recent report by Aitken Advisors. This is

a facility that the world’s largest central banks use to bor-

row and lend funds to each other. Currently, the rate at

which other central banks can borrow dollars from the

Fed is 50 basis points (bps) – half of one percent – for

up to three months. You may remember that the Fed, in

conjunction with five other central banks, lowered the

dollar swap rate from 100 bps to 50 bps last fall in order

to mitigate last summer’s liquidity squeeze (this liquidity

injection was shortly thereafter reinforced by the ECB’s

two LTROs).

With the dollar soaring and liquidity once again drying

up, it is quite plausible that the Fed and its fellow central

banks will resort to another coordinated move to lower

the dollar swap rate (maybe to zero this time) and per-

haps even extend the term (perhaps to 12 months). The

advantage of a coordinated cut in the swap line

(combined with a maturity extension) is that it can be

done quickly, and it would be relatively uncontroversial.

In other words, for the Fed, this course of action might

relieve the liquidity squeeze, please the markets and do

so without bringing with it the kind of political baggage

that a QE3 would. As I said, it is low-hanging fruit, and it

could have an immediate impact on market sentiment,

even if it does little to structurally improve the health of

the world’s financial system.

Short-term market response

The global equity markets have been in a sharp decline

since March, but things have now gotten bad enough

that some sort of policy response seems likely. In fact, it

is happening already, with several dovish speeches by

Fed governors, a rate cut in China and more positive

statements coming from Merkel about a unified Europe.

Combined with oversold technicals, this seems to set the

stage for a short-term counter-trend rally in risk assets,

including stocks, currencies, commodities and credit, but

our longer-term view hasn’t changed. The structural

problems facing Europe and the global economy are

likely to persist for some time (and perhaps even get

worse). My sense is that the market has bottomed for

now and that we are due for a temporary reprieve. I re-

main considerably cautious over the longer term.

Jurrien Timmer, Director of Global Macro and Portfolio Co-Manager of Fidelity

Tactical Strategies Fund– June 8, 2012

Before investing, consider the funds’ investment objectives, risks, charges, and

expenses. Contact Fidelity for a prospectus or, if available, a summary prospectus

containing this information. Read it carefully.

The information presented above reflects the opinions of Jurrien Timmer, Director

of Global Macro and Portfolio Co-Manager of Fidelity Tactical Fund, as of June 8,

2012. These opinions do not necessarily represent the views of Fidelity or any other

person in the Fidelity organization, and are subject to change at any time based on

market or other conditions. Fidelity disclaims any responsibility to update such

views. These views may not be relied on as investment advice and, because invest-

ment decisions for a Fidelity fund are based on numerous factors, may not be relied

on as an indication of trading intent on behalf of any Fidelity fund.

Views expressed regarding a particular company, security, industry or market sec-

tor are the views of that individual at the time expressed and do not necessarily

represent the views of Fidelity or any other person in the Fidelity organization.

These views may not be relied upon as investment advice, nor are they an indica-

tion of trading intent for any Fidelity Fund. These views are subject to change at

any time based upon markets and other conditions, and Fidelity disclaims any re-

sponsibility to update such views.

18

Using Technical Analysis along with

Fundamentals– part 2

Abu Nizam, CIM

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 18

In my May/June 2012 article I talked about some com-

monly used technical analysis and how we should con-

sider some of them along with fundamentals in our in-

vestment decisions.

A few years earlier Kevin Matras from Zacks Investment

Research, a US based equity research company, pro-

duced a guide book about common chart patterns. The

guide book can be found in this link. Today’s article is

almost entirely based from this guide book and I will

briefly touch a few of the patterns most commonly seen

and easy to understand.

As always, I do more fundamental analysis than techni-

cal analysis, but it’s better to understand some of the

chart patterns so you can more precisely choose a point

of entry and exit.

“Fundamentals of course are ultimately the

key in determining the price or value of a

stock. And statistics have shown that compa-

nies receiving upward earnings estimate revi-

sions outperform the market while companies

receiving downward earnings estimate revi-

sions underperform the market. But technical

analysis (and specifically chart pattern analy-

sis) can give you insight as to when the market

is ready to react to those fundamentals.”-

Kevin Matras

19

Using Technical Analysis along with

Fundamentals– part 2

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 19

Symmetrical Triangle in an Uptrend (Bullish):

When most of the known information is already factored

in and there is a prevailing bullish outlook, market partici-

pants will be looking for new information. While they are

searching for new information the markets can go

through a pause. In an uptrend, a pause like this can

create symmetrical triangles. This signals it’s likely that

the markets will continue to move upward once new in-

formation is available (example on your right and below).

Symmetrical Triangle in a downtrend (Bearish):

Symmetrical Triangles in downtrends will typically break-

out to the downside (example on your right).

20

Using Technical Analysis along with

Fundamentals– part 2

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 20

Bull and Bear Flags:

This is a very similar concept but the chart looks more

like a flag than triangle. The following is what Kevin said

about flags:

“The consolidation part of the pattern usually

represents only a brief pause in an otherwise

powerful market. They are typically seen right

after a big, quick move – either up or down.

The market then usually takes off again in the

same direction. Research has shown that Flags

and Pennants are some of the most reliable

chart patterns to trade. And they can be found

in some of the most explosive price moves.”

21

Using Technical Analysis along with

Fundamentals– part 2

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 21

Head and Shoulders:

The Head and Shoulders pattern is one of the most com-

mon patterns and shows a reliable signal in an uptrend.

This pattern usually forms at the top of an uptrend and

signals a reversal of the trend. The reason it is called

head and shoulders is because if you look carefully you

will vaguely find a silhouette of a person’s head and

shoulders.

(example on next page)

22

Using Technical Analysis along with

Fundamentals– part 2

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 22

23

Using Technical Analysis along with

Fundamentals– part 2

By: Abu Nizam. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 23

Conclusion: Because of space constraints I have to stop

here. Unfortunately, there is lots of homework to do be-

fore starting to use these patterns. Kevin has demon-

strated how to identify different points and how to con-

nect them so that investors can properly construct a pat-

tern and develop a better signal. Each pattern can give

misleading or confusing signals and in some cases can

work in a completely different way than expected. For

this reason, readers should also learn how to spot failed

breaks and stop-out points to manage misleading pat-

terns.

All the charts are taken from stockcharts.com.

24

E-mail: [email protected] Website: www.cramagazine.com

60 Columbia Way, Suite 900, Markham, ON, Canada, Tel: 905.709.7911 Fax: 905.946.2207

Canadians Resident Abroad Inc. is part of the Keybase Financial Group Inc.

CRA magazine is published bi-monthly by Canadians Resident Abroad Inc. All rights reserved. No

part of this publication or any part of it may be reproduced, stored in a retrieval system, or

transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or

otherwise for commercial purposes, without the permission of Canadians Residents Abroad Inc.

Every effort has been made to ensure the accuracy of the contents of the magazine. All articles

represent the opinions of the authors. Canadians Resident Abroad Inc. makes no warranty, ex-

press or implied, concerning the content of this publication.

Creative Director: Abu Nizam Creative Assistant: Mike Beaudoin

Circulation: Jerome Pare & Lindsay Penner Web Site Manager: Keith Sutherland