Embed Size (px)

Citation preview

Prepared For

Mr. David Babatope, Member Mountain View Hospitality LLC

2183 Salem RoadConyers, Georgia 30013

&Peoples Bank

1793 Highway 138 SEConyers, Georgia 30013

Feasibility Study of

Proposed WoodSpring Suites

West Iris Dive in SWQ of I-20 Exit 84

Conyers, Georgia 30013

Prepared By

Shamrock Capital LLC

322 N Forest Boulevard

Lake Mary, Florida 32746

Date of Analysis

October 21, 2016

Date of Report

November 28, 2016

322 N Forest Blvd, Lake Mary, FL 32746 Tel. (407) 402-9042

SHAMROCK CAPITAL LLC

November 28, 2016

Mr. David Babatope, Member Mountain View Hospitality LLC2183 Salem Road&Peoples Bank1793 Highway 138 SEConyers, Georgia 30013

Reference: Feasibility Study

Proposed WoodSpring Suites

West Iris Dive in SWQ of I-20 Exit 84, Conyers, Georgia 30013

Dear Mr. Babatope & Mr. Khanna:

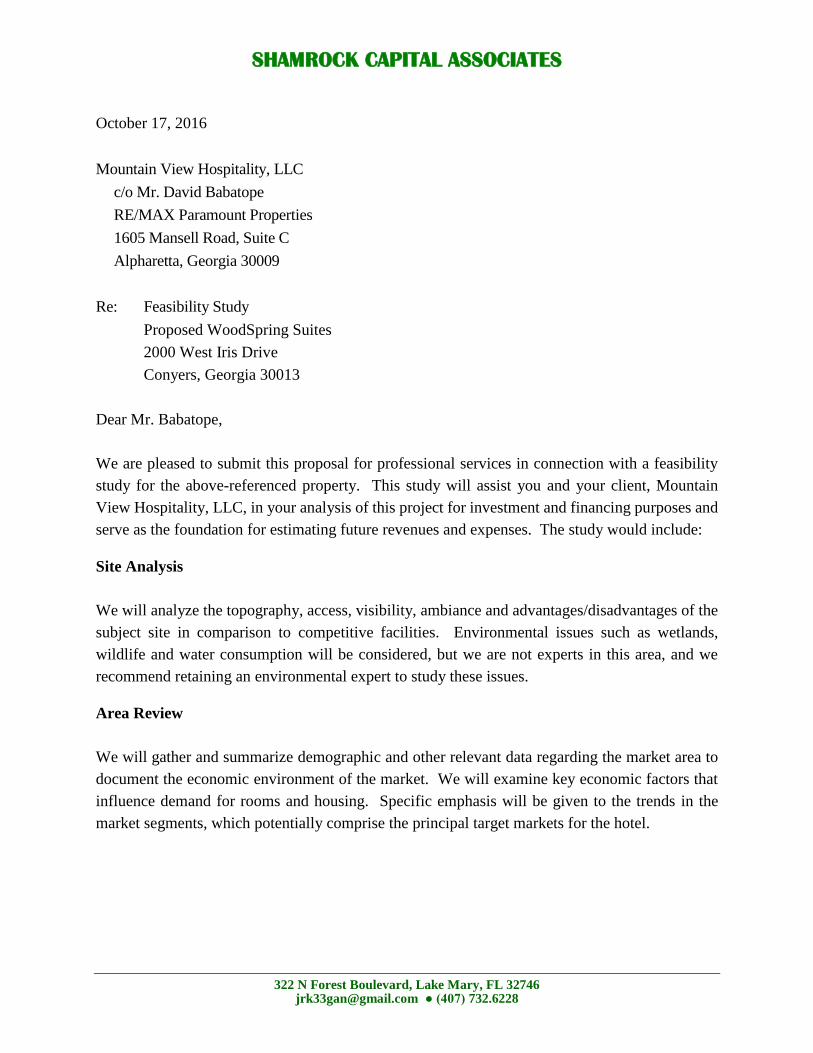

Per your request, on October 21, 2016 we analyzed the Conyers, Georgia lodging market as it

pertains to the proposed WoodSpring Suites. Based on the provided 124-room prototype design

and an all-in project cost of $7,700,000, the subject property should produce a free-and-clear

Internal Rate of Return (IRR) of 10.5%. This return is considered average based on accepted

market returns for similar hotel investments.

Please review the enclosed report and if you have any questions or need additional information,

please feel free to contact us.

Respectfully submitted,

Shamrock Capital LLC

Robert P Hill Christopher M. Keegan

Executive Summary

Proposed WoodSpring Suites Prototype

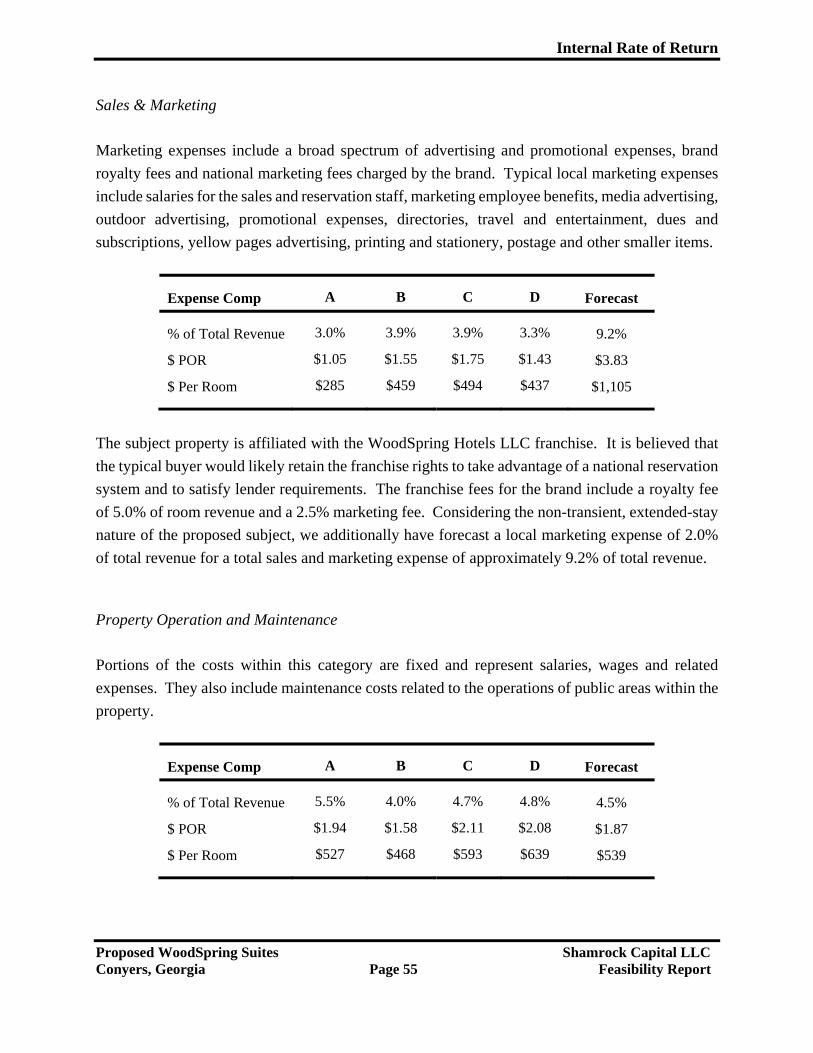

Project Summary A proposed 124-room prototype WoodSpring Suites extended-stay hotel is contemplated for the vacant parcel at West Iris Drive & Flat Shoals Road, Conyers, Georgia. The proposed WoodSpring will be positioned as an economy-priced extended-stay hotel. Our research indicates that the 124-room proposed design would be suitable for this market.

Client and Intended User The client and intended user of this feasibility study is

Mountain View Hospitality LLC. Mr. David Babatope,

Member, authorized the preparation of this feasibility study

by signing a letter of proposal dated October 17, 2016. Any

use of this report by third parties is unauthorized without the

written consent of the Client and Shamrock Capital LLC.

Client’s Intended Use Financial analysis and decision making as they pertain to the

development of the subject property and to provide

supporting documentation for financing.

Date of Report November 28, 2016

Executive Summary (cont’d)

Economy Conyers is experiencing a period of moderate economic

expansion whereby several film and television production

companies like Warner Brothers’ Bonanza Productions and

Twentieth Century Fox all located permanent production

facilities calling Rockdale County and the City of Conyers

home. These production companies alone lease more than

300,000 sf of office space and sound stages per month and

contract with over 75 local businesses for goods and

services. They employ over 300 people, with about 20

percent of their full-time employees coming from Rockdale

County. The metro area is supported by a number of

employers currently relocating their operations to the

city/county to take advantage of the significant tax

incentives and thus providing a solid foundation for the local

economy.

Immediately east and abutting the city's downtown core is

the Georgia International Horse Park. The park's 1,400 acres

can accommodate other entertainment and special event

venues such as concerts and outdoor festivals, providing

both employment and revenue to the City of Conyers.

Market Area Land uses in the proposed subject’s immediate market area

include light industrial, warehousing and distribution

facilities; Fieldstone Plaza Shopping Center; quick-service

food venues including Burger King, Dunkin’ Donuts,

Hardee’s, McDonald’s and Wendy’s; diners and casual

dining venues including Los Bravos, Sudo Bar & Grill,

Third Base Grill, Tokyo Hibachi Express, and Waffle

House; four gas station/convenience stores; a medical clinic

and animal hospital; two grocery stores; an auto dealership

and auto and truck accessory and service centers.

Executive Summary (cont’d)

Local Lodging Trends The projection of market demand by segment in

consideration of overall market supply indicates that market

occupancy is expected to end Fiscal 2017 up 3.0% followed

by a net decrease of -10.2% in Fiscal 2018 with the opening

of the subject WoodSpring Suites. In Fiscal 2019,

competitive occupancy is forecast to increase by 2.7% to a

stabilized level of 68.7%.

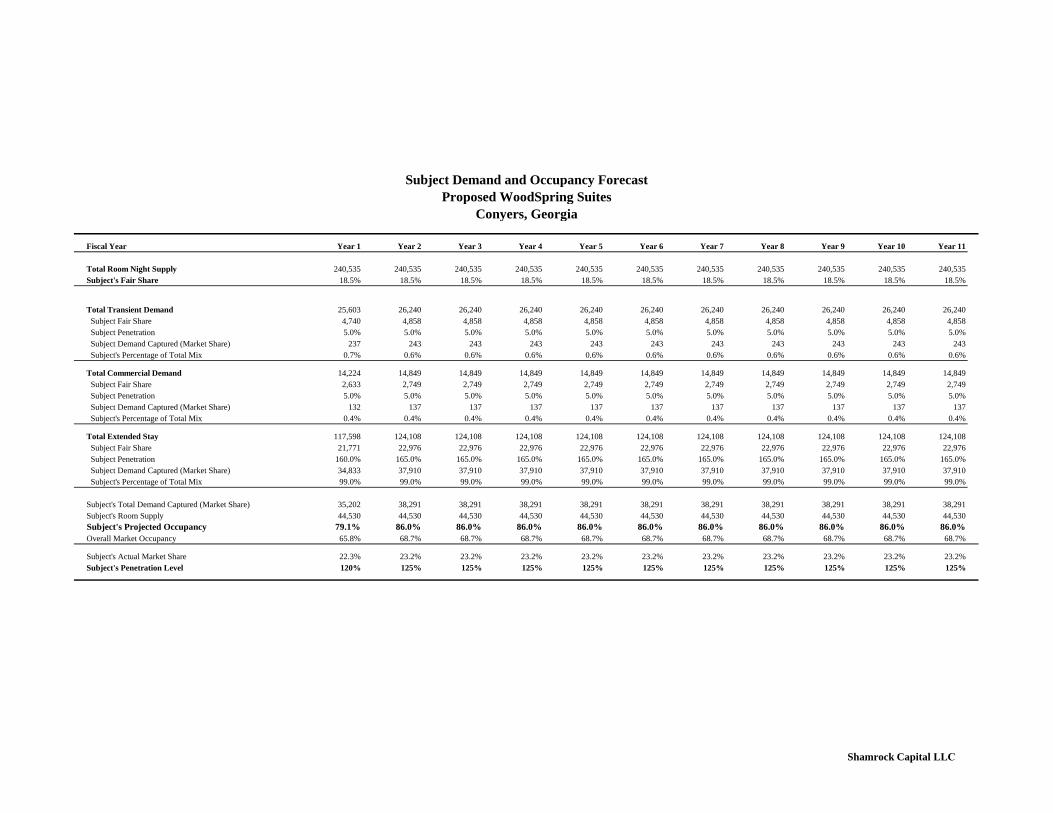

Occupancy Projection Using projections for the subject’s demand by segment and

considering overall market supply and demand forecasts, the

proposed subject’s Year 1 occupancy rate is projected to be

79.1% at a penetration rate of 120%. In Year 2, the proposed

subject’s occupancy and penetration rates are forecast to

increase to a stabilized level of 86.0% and 125%,

respectively.

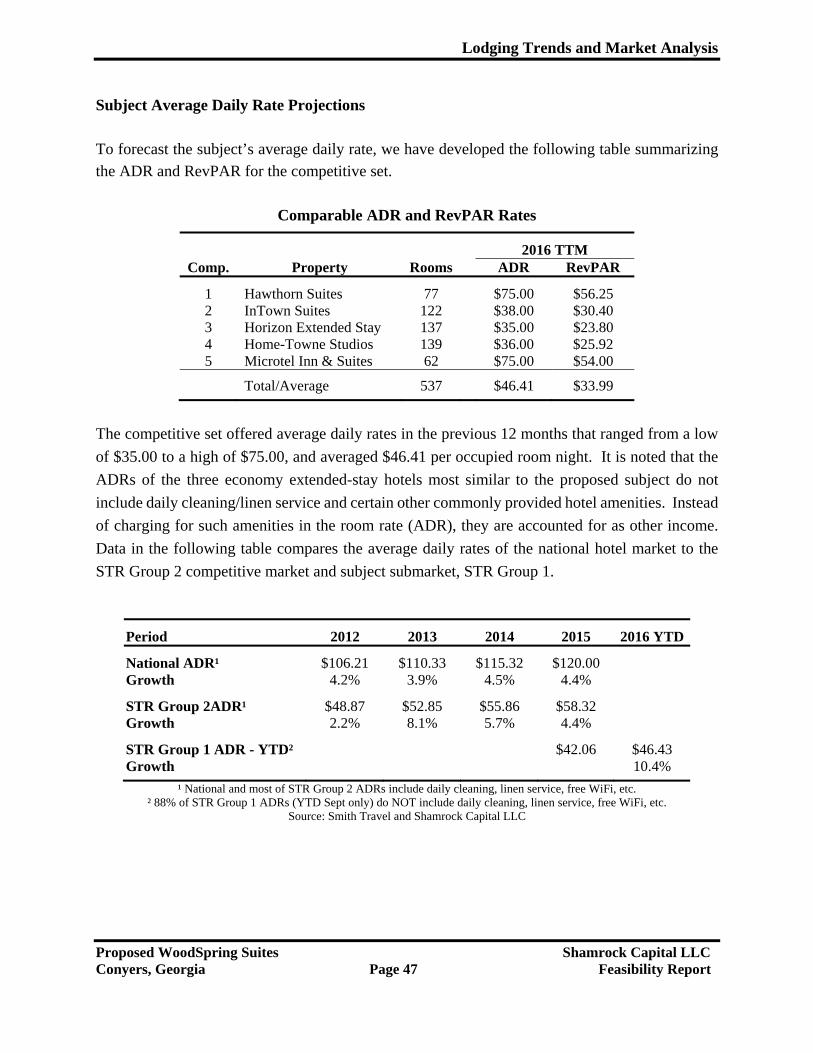

Revenue Projection The competitive set offered estimated average daily rates in

the previous 12 months that ranged from a low of $35.00 to

a high of $75.00, and averaged $46.41 per occupied room

night.

Considering the subject will be a new-construction, interior-

corridor, purpose-built, economy extended-stay hotel with a

fresh design and branding as a WoodSpring Suites, we

estimate, if the subject existed in today’s market, it would

command an ADR of $38.83, or an AWR of $271.84. Given

that the subject will not enter the market until early 2018,

and considering the historical ADR growth rates in the

market, we forecast a Year 1 ADR and AWR of $40.00 and

$280.00, respectively, with annual increases of 3.0% per

year throughout the projection period.

Executive Summary (cont’d)

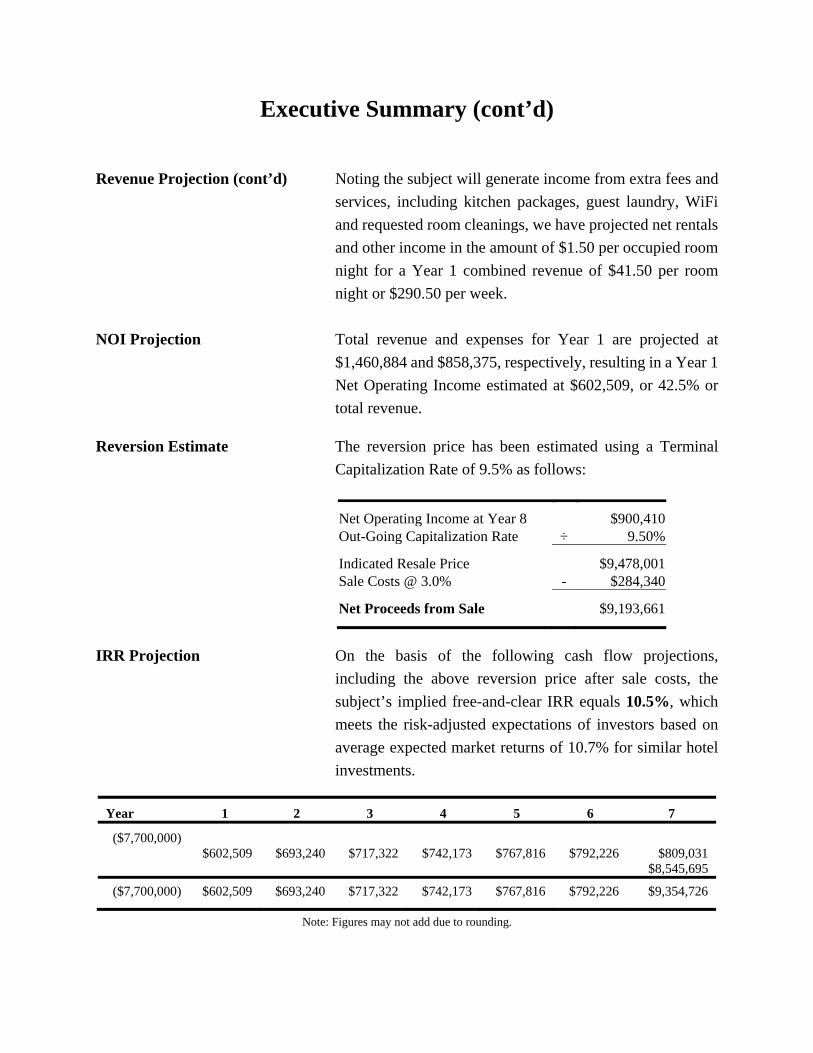

Revenue Projection (cont’d) Noting the subject will generate income from extra fees and

services, including kitchen packages, guest laundry, WiFi

and requested room cleanings, we have projected net rentals

and other income in the amount of $1.50 per occupied room

night for a Year 1 combined revenue of $41.50 per room

night or $290.50 per week.

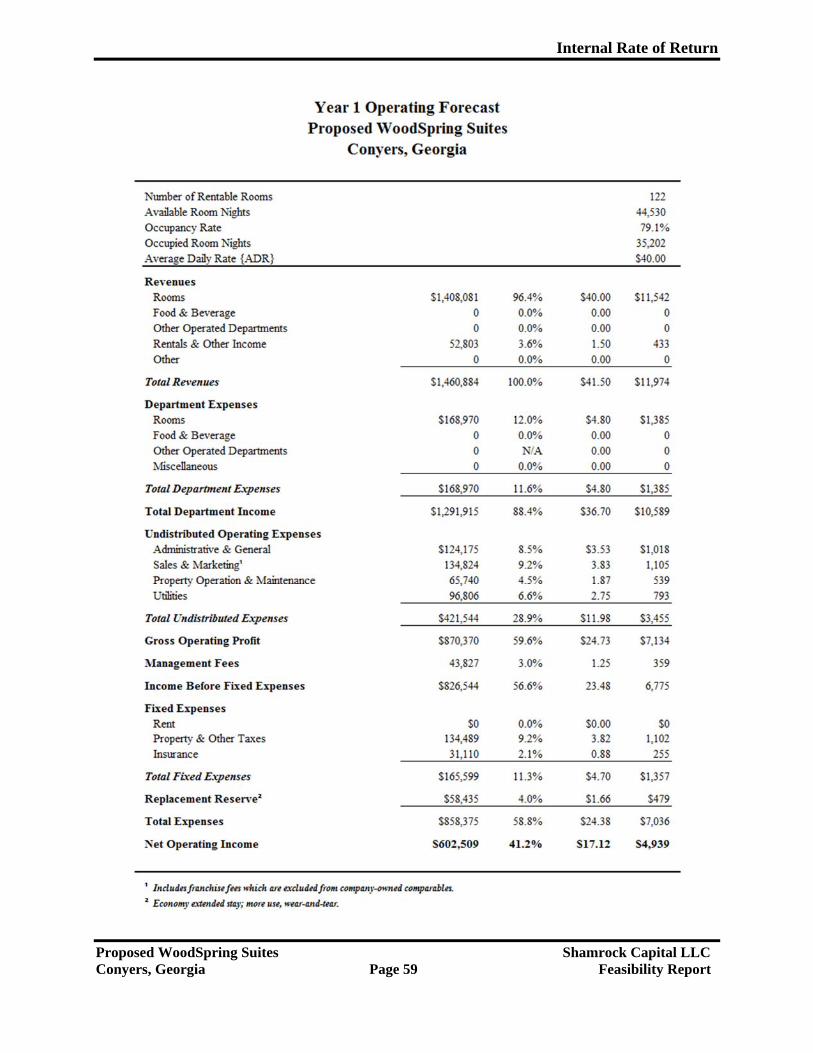

NOI Projection Total revenue and expenses for Year 1 are projected at

$1,460,884 and $858,375, respectively, resulting in a Year 1

Net Operating Income estimated at $602,509, or 42.5% or

total revenue.

Reversion Estimate The reversion price has been estimated using a Terminal

Capitalization Rate of 9.5% as follows:

Net Operating Income at Year 8 $900,410 Out-Going Capitalization Rate ÷ 9.50%

Indicated Resale Price $9,478,001 Sale Costs @ 3.0% - $284,340

Net Proceeds from Sale $9,193,661

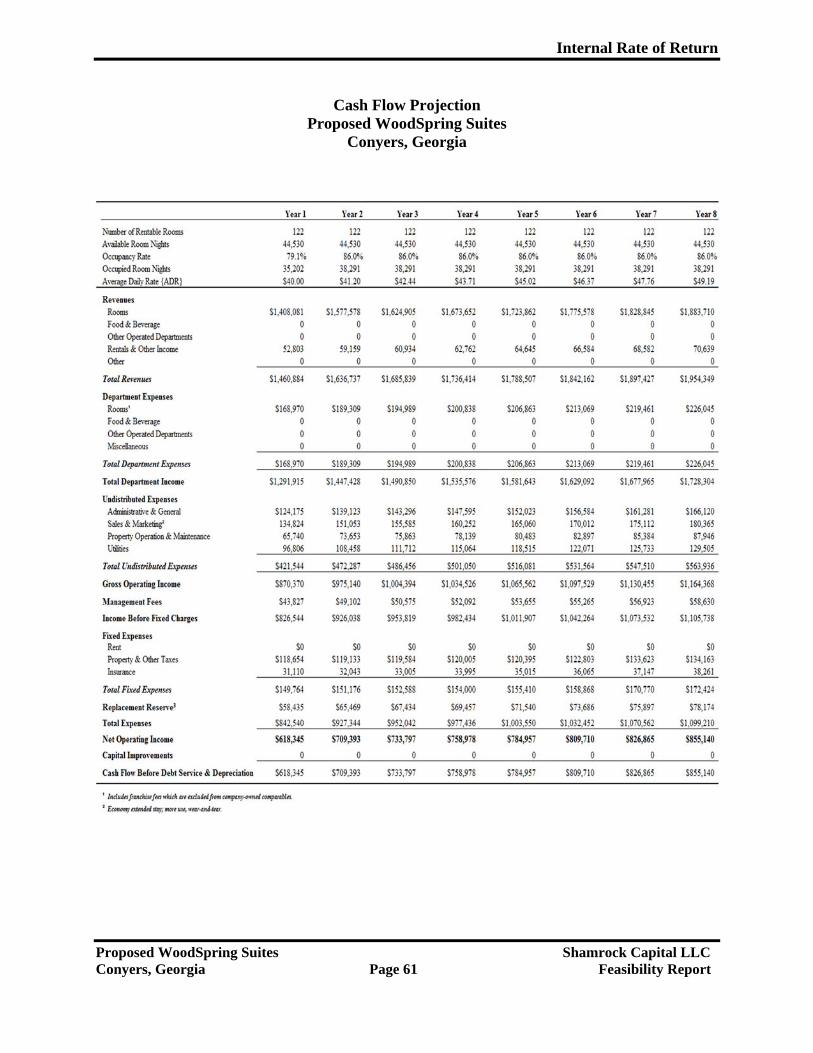

IRR Projection On the basis of the following cash flow projections,

including the above reversion price after sale costs, the

subject’s implied free-and-clear IRR equals 10.5%, which

meets the risk-adjusted expectations of investors based on

average expected market returns of 10.7% for similar hotel

investments.

Year 1 2 3 4 5 6 7

($7,700,000)$602,509 $693,240 $717,322 $742,173 $767,816 $792,226 $809,031

$8,545,695

($7,700,000) $602,509 $693,240 $717,322 $742,173 $767,816 $792,226 $9,354,726

Note: Figures may not add due to rounding.

Table of Contents

ASSUMPTIONS AND LIMITING CONDITIONS ....................................................................................................... 1

INTRODUCTION.................................................................................................................................................. 5

IDENTIFICATION OF THE PROPERTY .................................................................................................................................... 5 Site ....................................................................................................................................................................... 5 Improvements ...................................................................................................................................................... 7

CLIENT AND INTENDED USER DISCLOSURE ......................................................................................................................... 11 CLIENT’S INTENDED USE DISCLOSURE .............................................................................................................................. 11 DATE OF ANALYSIS ....................................................................................................................................................... 11 OWNERSHIP AND PROPERTY HISTORY .............................................................................................................................. 12 SCOPE OF THE FEASIBILITY STUDY .................................................................................................................................... 12

AREA OVERVIEW ............................................................................................................................................... 13

THE CITY OF CONYERS, ROCKDALE COUNTY, GA AND ATLANTA–SANDY SPRINGS–ROSWELL MSA .............................................. 13 Population/Demographics ................................................................................................................................. 15 Transportation ................................................................................................................................................... 15 Education ........................................................................................................................................................... 17 Health Services ................................................................................................................................................... 18 Economy ............................................................................................................................................................. 18

MARKET AREA ............................................................................................................................................................ 21

LODGING TRENDS AND MARKET ANALYSIS ........................................................................................................ 22

NATIONAL TRENDS ....................................................................................................................................................... 22 LOCAL LODGING TRENDS – LEVEL II MARKET ANALYSIS ....................................................................................................... 26

Competitive Supply Analysis .............................................................................................................................. 26 Historical Demand .............................................................................................................................................. 34 Demand Forecast ............................................................................................................................................... 38 Subject Occupancy Projections ........................................................................................................................... 41

SUBJECT AVERAGE DAILY RATE PROJECTIONS .................................................................................................................... 47

INTERNAL RATE OF RETURN METHODOLOGY .................................................................................................... 49

BASIS OF ASSUMPTIONS ................................................................................................................................................ 49 ANALYSIS OF REVENUES ................................................................................................................................................ 51

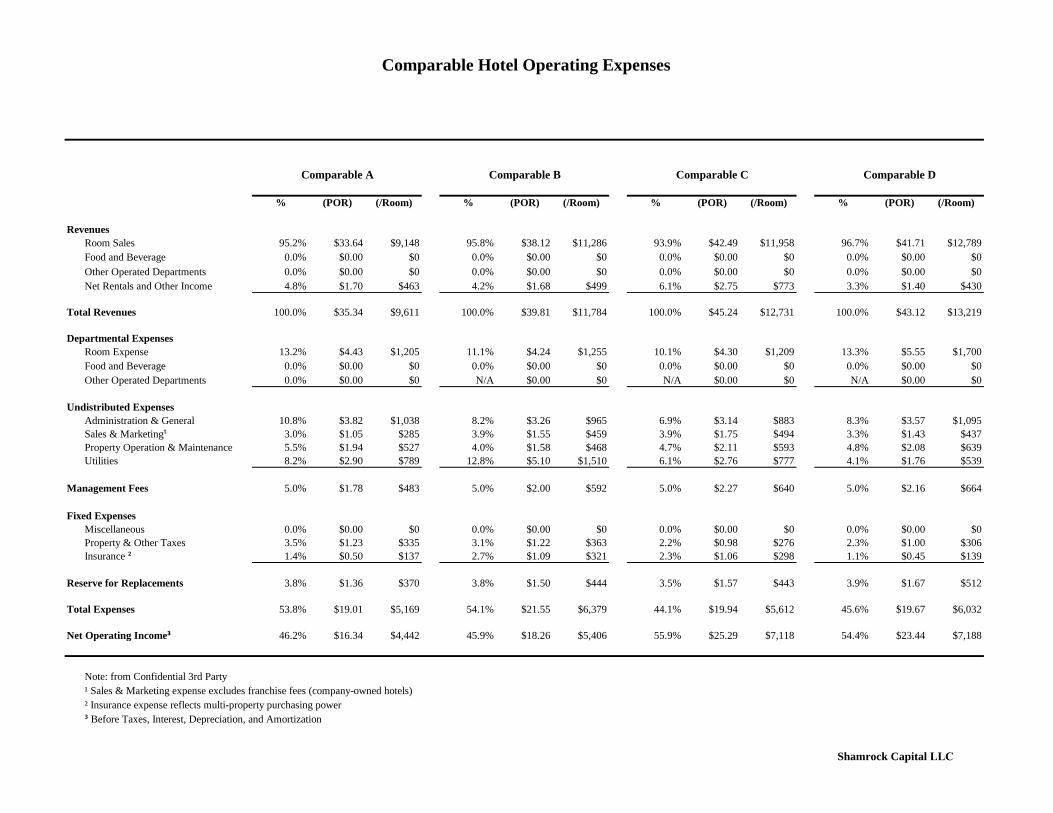

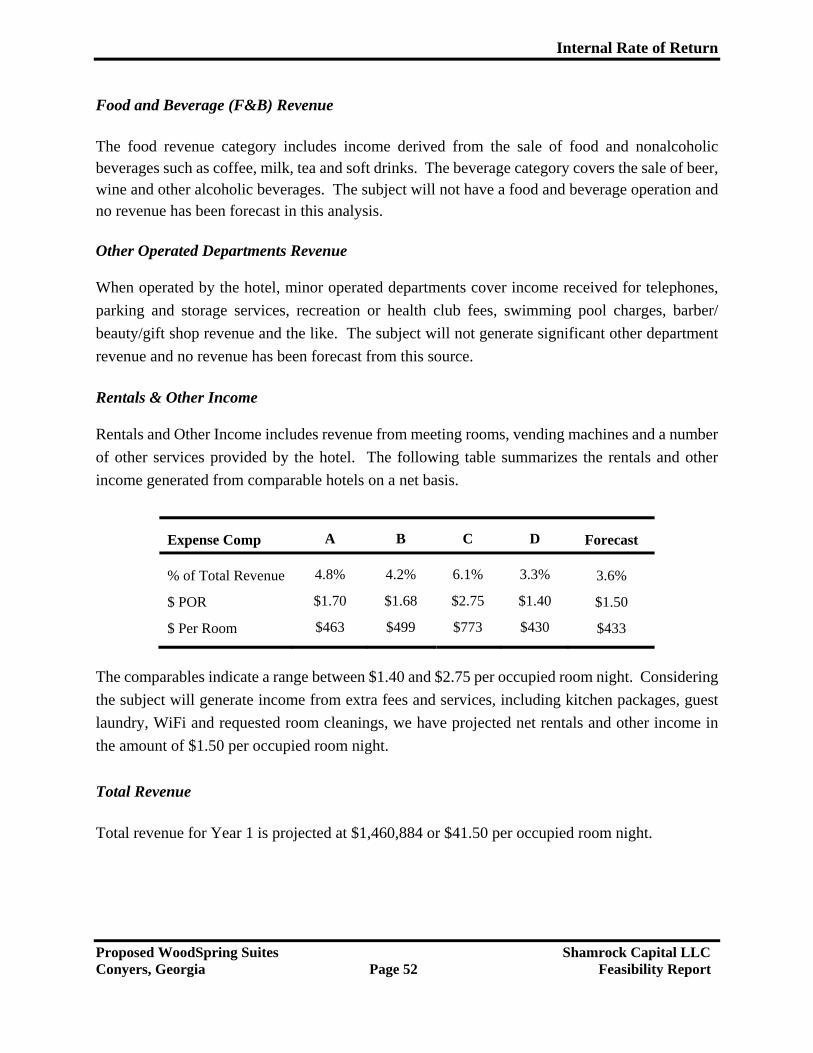

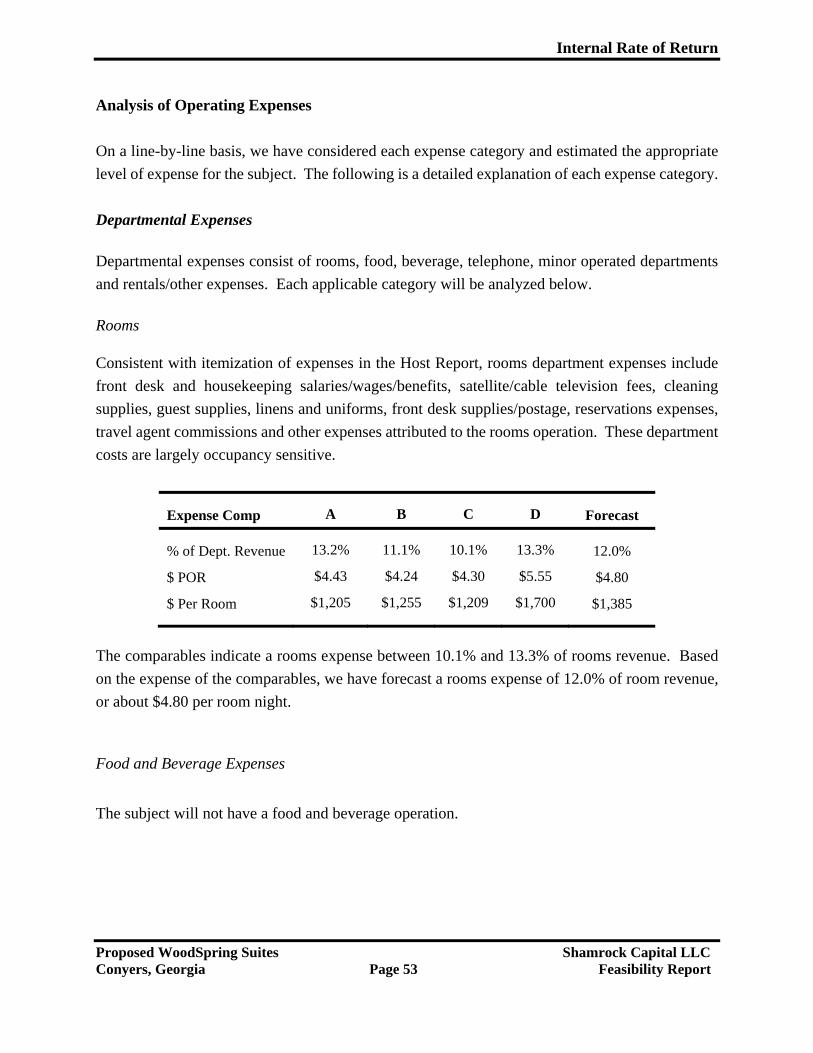

Rooms Revenue .................................................................................................................................................. 51 Food and Beverage (F&B) Revenue .................................................................................................................. 52 Other Operated Departments Revenue .............................................................................................................. 52 Rentals & Other Income..................................................................................................................................... 52 Total Revenue ..................................................................................................................................................... 52

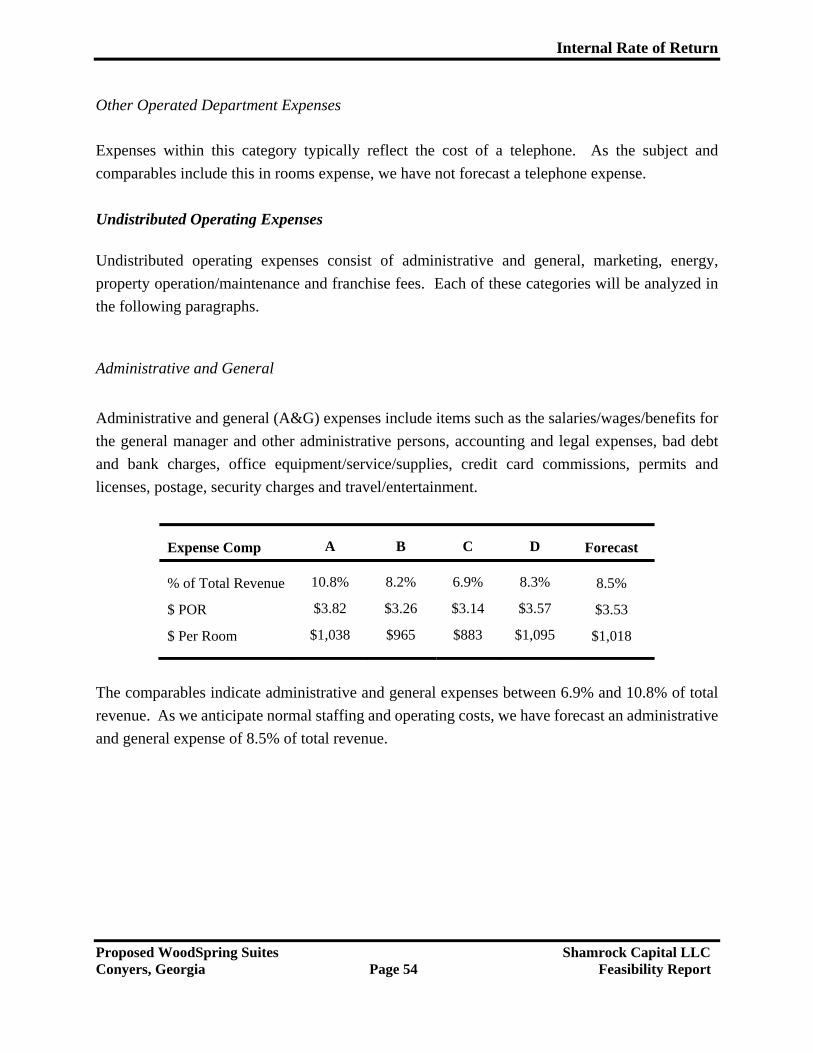

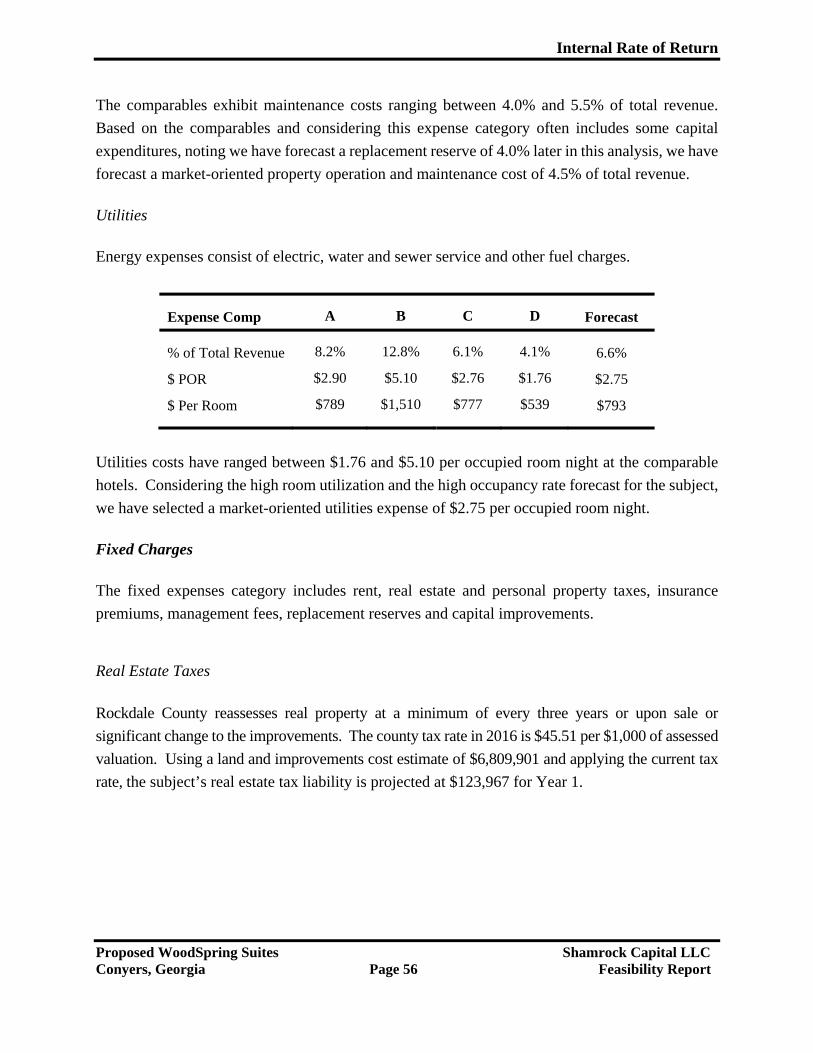

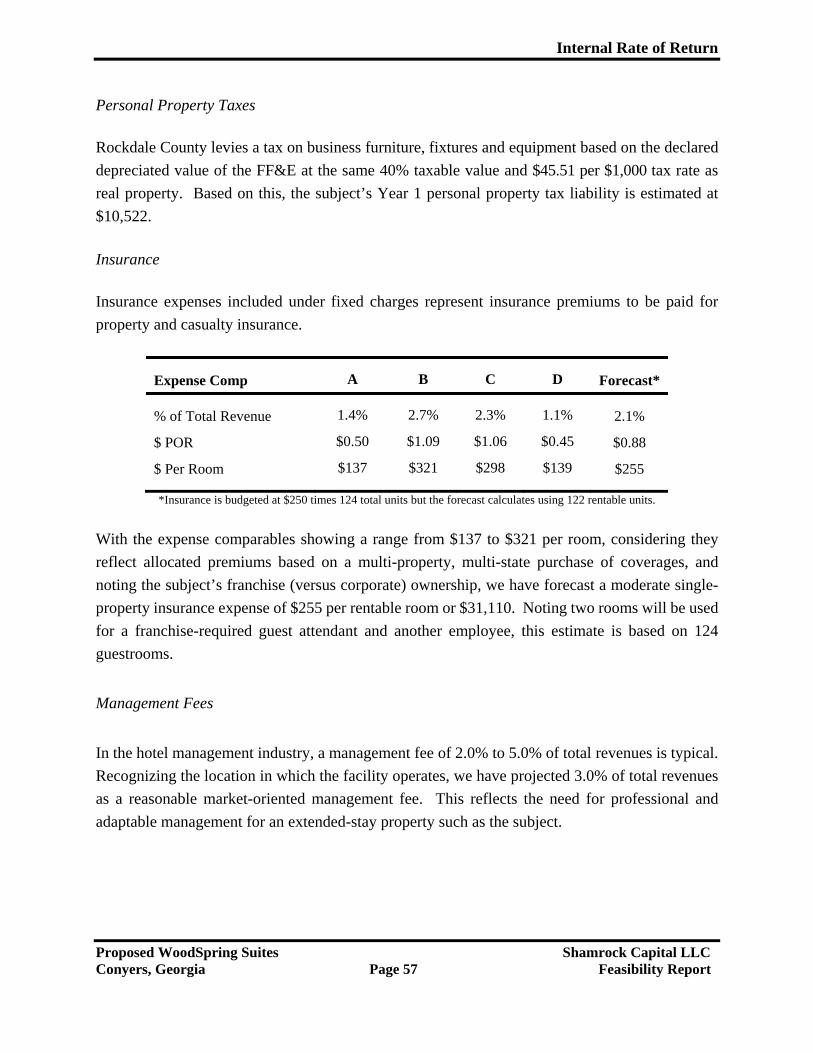

ANALYSIS OF OPERATING EXPENSES ................................................................................................................................. 53 Departmental Expenses ...................................................................................................................................... 53 Undistributed Operating Expenses .................................................................................................................... 54 Fixed Charges .................................................................................................................................................... 56 Total Expenses ................................................................................................................................................... 58

NET OPERATING INCOME .............................................................................................................................................. 58 INTERNAL RATE OF RETURN (IRR) ................................................................................................................................... 60

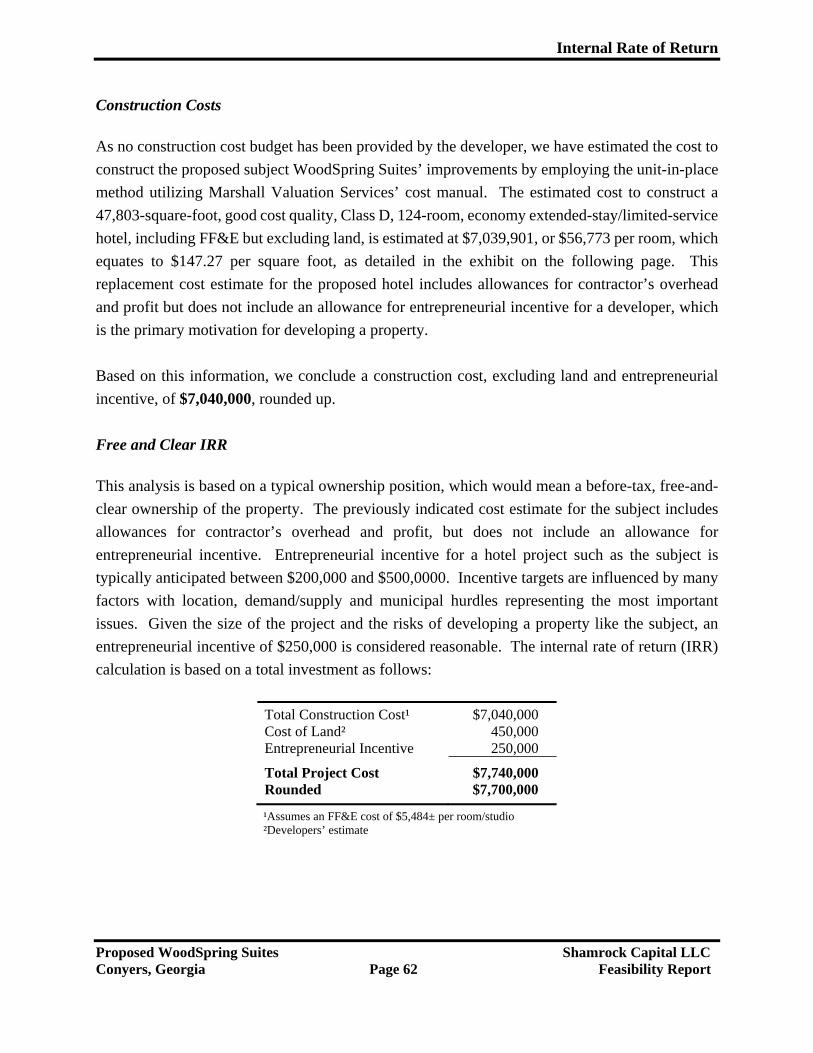

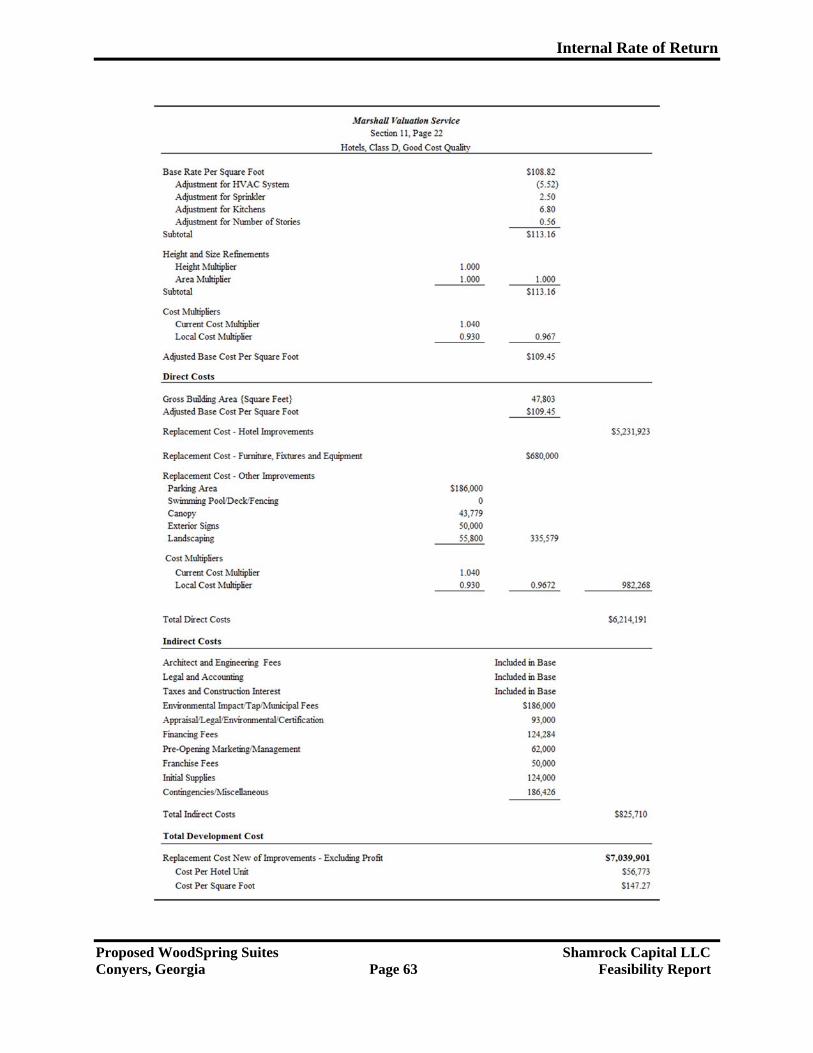

Construction Costs ............................................................................................................................................. 62 Free and Clear IRR ............................................................................................................................................ 62

CONCLUSION .................................................................................................................................................... 66

Free-and-Clear IRR ........................................................................................................................................... 66 Investment Caveats ............................................................................................................................................ 66 Investment Considerations ................................................................................................................................. 67

ANALYSTS’ CERTIFICATION ................................................................................................................................ 69

ADDENDA

ENGAGEMENT LETTER SURVEY SITE PLAN CUSTOM SMITH TRAVEL TREND REPORT PROPERTY PHOTOGRAPHS QUALIFICATIONS OF ANALYSTS

Assumptions and Limiting Conditions

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 1 Feasibility Report

Assumptions and Limiting Conditions

1. The analysts certify that, to the best of our knowledge and belief, the statements contained in this

report, subject to the limiting conditions set forth below are correct; also that this report has been

made in conformity with the accepted practices of the Appraisal Institute.

2. This property has been analyzed as though free of all liens and encumbrances, unless otherwise

stated herein. No responsibility is assumed for matters legal in nature, nor is any opinion of title

rendered herewith. Good title is assumed.

3. The analysts herein, by reason of this report, are not required to give testimony in court, with

reference to the property herein appraised, unless arrangements have been previously made.

4. Disclosure of the contents of this feasibility report is governed by the By-Laws and Regulations

of the Appraisal Institute.

5. Neither all nor any part of the contents of this report (especially any conclusions as to value, the

identity of the analysts or the firm with which they are connected, or any reference to the Appraisal

Institute or the MAI or SRA Designation) shall be disseminated to the public through advertising

media, public relations media, news media, sales media, or any other public means of

communication without the prior written consent and approval of the undersigned.

6. Certain information in this report was furnished from sources believed to be reliable; however, such information is

not guaranteed to be correct, although it has been checked insofar as possible and is believed to be correct.

7. We are not familiar with any engineering or geological studies made to determine the bearing capacity of the land or

that indicate any mineral contents of a significant nature. Because improvements in the area appear to be structurally

sound, we assume that soil and subsoil conditions are stable.

8. Plats, maps, and other exhibits in this report are used merely to help the reader visualize the

property and its surroundings, and no responsibility is assumed for their cartographic accuracy.

Assumptions and Limiting Conditions

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 2 Feasibility Report

9. The value estimates reported herein are under the purpose and land-use premise stated. They are

not valid for any other purpose or premise and must not be used in conjunction with any other

report, appraisal, or intended use.

10. Full compliance with all applicable federal, state, and local environmental regulations is assumed,

as well as all applicable zoning, use, and occupancy regulations and restrictions as stated and

considered in this report.

11. In this assignment, the existence of any hazardous or potentially hazardous material possibly

located on the site thereon, such as urea formaldehyde foam insulation, asbestos, or toxic waste,

etc., was not observed by the inspecting analysts and has not been considered. The analysts have

no knowledge of any such materials on or in the property but are not qualified to detect such

substances. The presence of such materials may have an effect on the value or use of the property.

It is assumed that there are no hazardous material spills, etc. resulting from underground storage

tanks or other causes associated with the subject property. Full compliance with all environmental

laws is assumed. The client is urged to retain an expert in this field if desired.

12. Any projections, forecasts, etc., regarding future patterns of income and/or expenses, prices/values, etc. represent the

analysts’ best estimates of investor anticipations with respect to these items, based on information available at the date

of appraisal or analysis. Such information includes forecasts/projections published by recognized sources such as

economists, financial publications, investor surveys, etc. Economic trends can affect future behavior of income,

expenses, values, etc. Changes in these items caused by future occurrences could result in values different from those

established in this report. We cannot accept responsibility for economic variables in the future that could not have

been known or anticipated at the date of analysis (inflation rates, economic upswings or downturns, fiscal policy

changes, etc.).

13. All mechanical equipment, existing or as proposed, in the building(s) is assumed to be in average to good working

order, unless otherwise stated and treated elsewhere in the report.

Assumptions and Limiting Conditions

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 3 Feasibility Report

14. The Americans with Disabilities Act (ADA) became effective January 26, 1992 setting strict and

specific standards for disabled access to and within most commercial and public buildings. We

have not made a specific compliance survey and analysis of the proposed property to determine

whether or not it will be in conformity with the various detailed requirements of the ADA. It is

possible that a compliance survey of the property together with a detailed analysis of the

requirements of the ADA could reveal that the proposed property will not be in compliance with

one or more of the requirements of the act. If so, this fact could have a negative effect upon the

value of the property. Since we have no direct evidence relating to this issue, we did not consider

possible noncompliance with the requirements of the ADA in estimating the value of the property.

15. The indicated values are subject to the completion of the property in accordance with the forecast

construction budget and other project information which has been provided by the developer. We assume the construction will be completed with quality materials in a workmanlike, timely and quality manner.

16. The estimated income and expense results are based upon competent, efficient management

and responsible ownership. Other than as set forth in this report, we assume no significant change in the competitive position of the competitive facilities (supply) in the area.

17. It should be noted that the estimated development costs are based on budgets provided by the

developer and on the premise that no atypical unforeseen delays or problems occur. In a construction project of this scope, there are numerous complications that may occur. For example, unexpected drainage problems resulting from soil conditions, springs, or unusual precipitation can complicate and prolong the construction. Similarly, unanticipated environmental issues can cause construction delays or expensive corrective measures. Unexpected weather conditions or other unpredictable factors may also influence the cost of the project. In addition, problems associated with the building or site improvements may occur. Changes in prices or availability of materials or labor can impact costs. Also, problems with timely work, inspections or approvals can slow construction and impact costs. Finally, other events outside of the control of the developer, such as bankruptcy of the general contractor or subcontractors, could cause delays and cost overruns. We have made an inspection of the subject commercial hotel site and have not noted any particular conditions that would indicate problems for the development process. We are not experts on soil conditions, subterranean rock, environmental issues or similar matters, but we simply have pointed out some important factors that can produce unexpected costs to construct a proposed project.

Assumptions and Limiting Conditions

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 4 Feasibility Report

18. If applicable to the subject’s market, a Trend Response Report from Smith Travel Research

(STR) has been utilized to verify and augment our primary market research. Sole reliance is

not made upon the STR data provided, specifically in instances when a period of non-reporting

has occurred in one or more of the properties in the sample set. Due to the methodology used

by Smith Travel, this situation may result in skewed data as the average of the reporting

properties is assumed for the entire sample, including any non-reporting property or properties.

19. Unless specifically stated otherwise, we assume the subject’s franchise agreement will extend

through the specified holding period and beyond such that it will not affect the marketability or

reversion price(s) forecast within this report. We have assumed that upon completion the hotel

will meet all the requirements of the franchise and no substantial capital improvements will be

required to maintain the agreement over the holding period and beyond.

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 5 Feasibility Report

Introduction

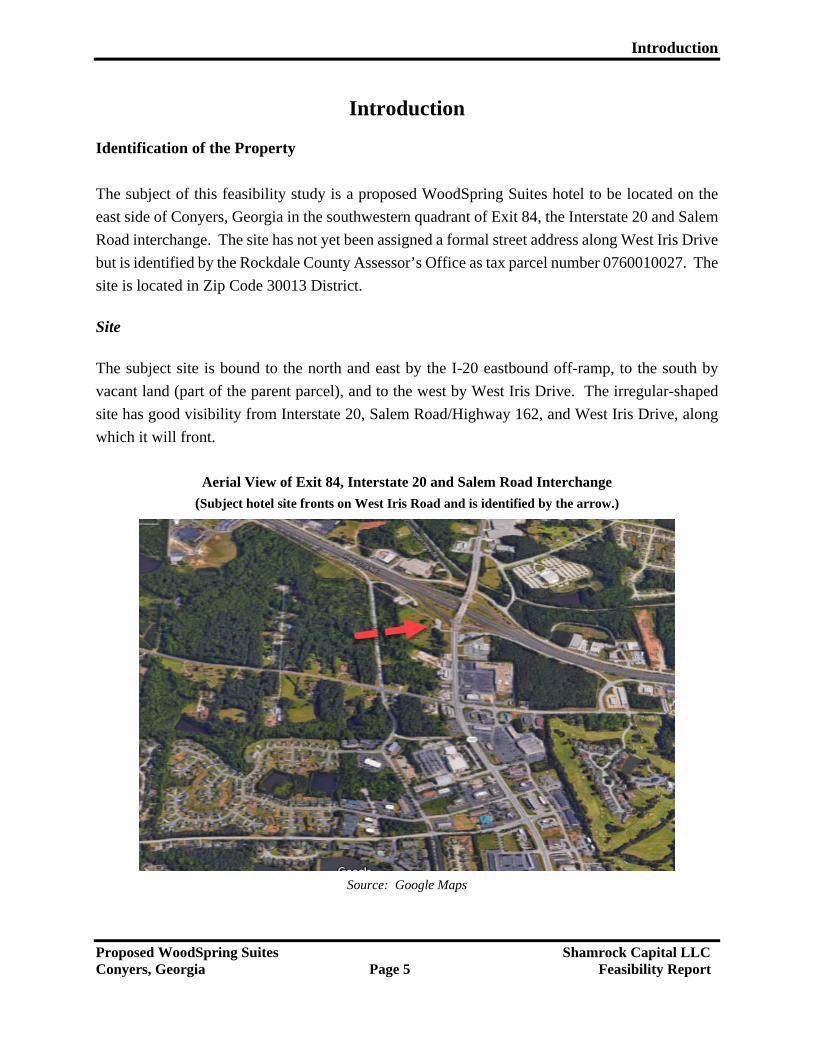

Identification of the Property

The subject of this feasibility study is a proposed WoodSpring Suites hotel to be located on the

east side of Conyers, Georgia in the southwestern quadrant of Exit 84, the Interstate 20 and Salem

Road interchange. The site has not yet been assigned a formal street address along West Iris Drive

but is identified by the Rockdale County Assessor’s Office as tax parcel number 0760010027. The

site is located in Zip Code 30013 District.

Site

The subject site is bound to the north and east by the I-20 eastbound off-ramp, to the south by

vacant land (part of the parent parcel), and to the west by West Iris Drive. The irregular-shaped

site has good visibility from Interstate 20, Salem Road/Highway 162, and West Iris Drive, along

which it will front.

Aerial View of Exit 84, Interstate 20 and Salem Road Interchange

(Subject hotel site fronts on West Iris Road and is identified by the arrow.)

Source: Google Maps

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 6 Feasibility Report

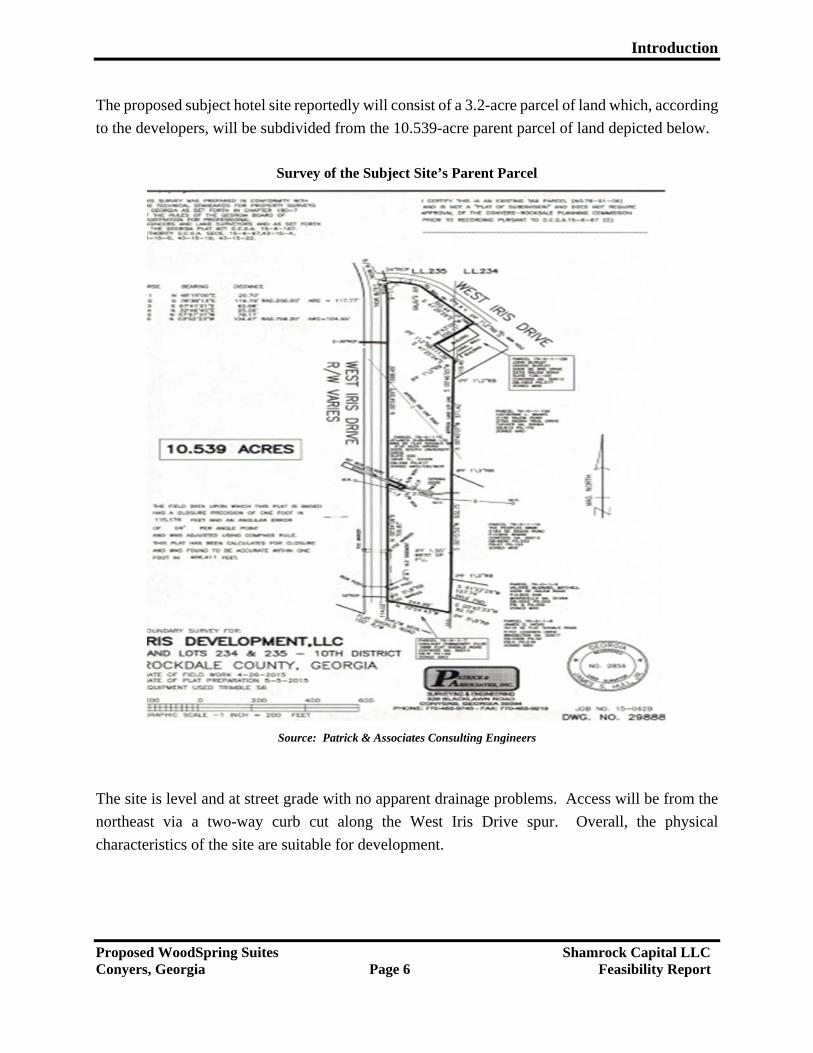

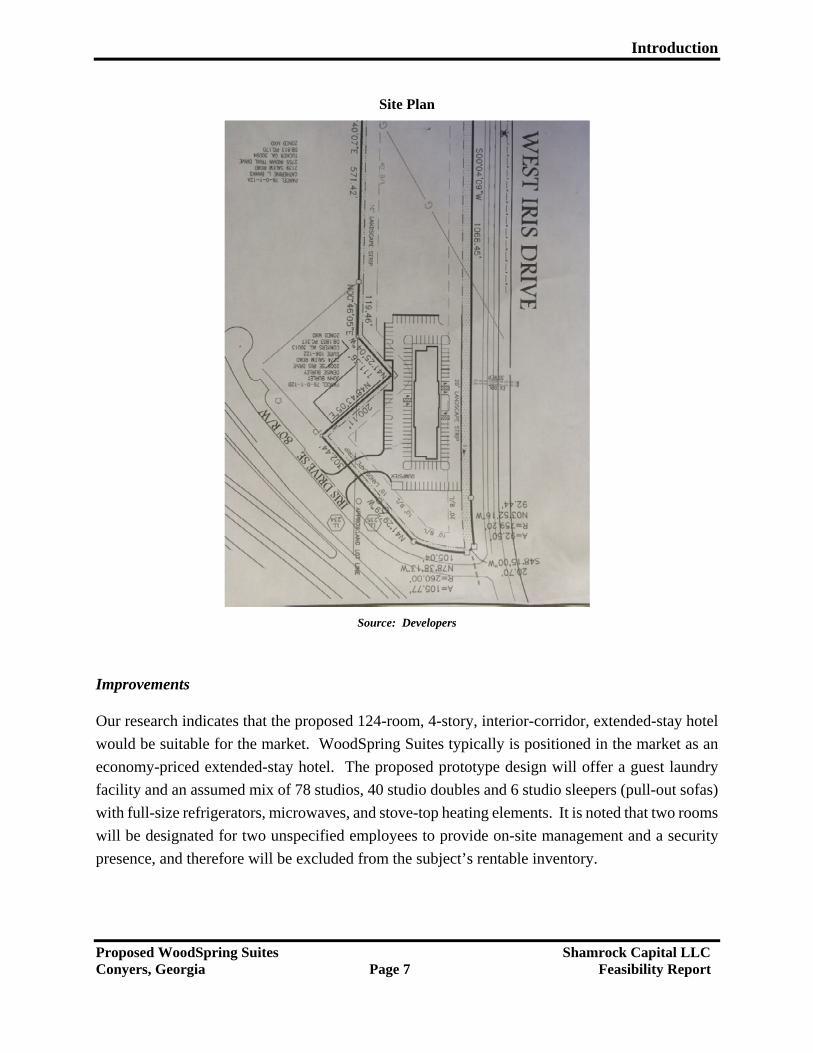

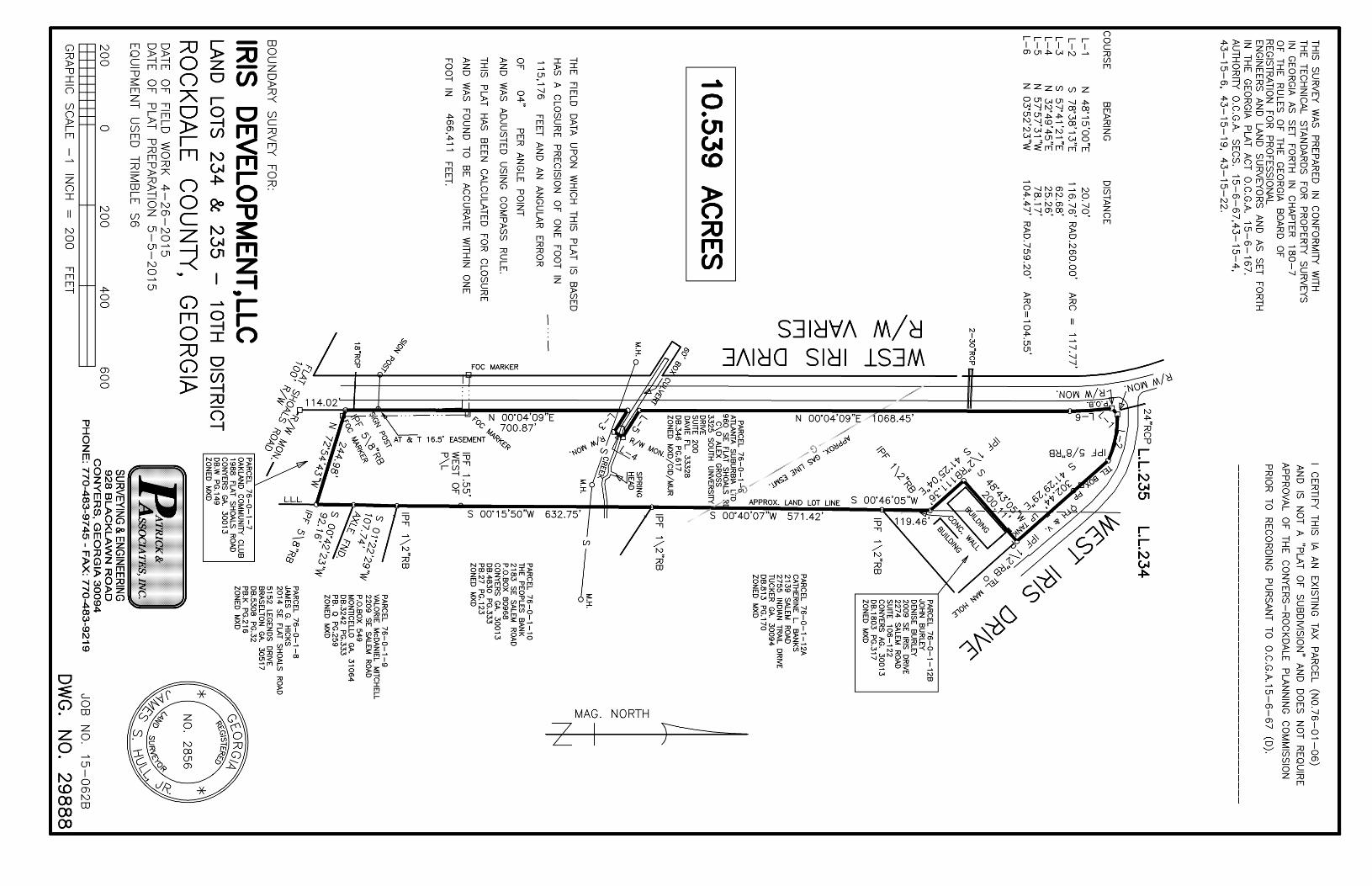

The proposed subject hotel site reportedly will consist of a 3.2-acre parcel of land which, according

to the developers, will be subdivided from the 10.539-acre parent parcel of land depicted below.

Survey of the Subject Site’s Parent Parcel

Source: Patrick & Associates Consulting Engineers

The site is level and at street grade with no apparent drainage problems. Access will be from the

northeast via a two-way curb cut along the West Iris Drive spur. Overall, the physical

characteristics of the site are suitable for development.

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 7 Feasibility Report

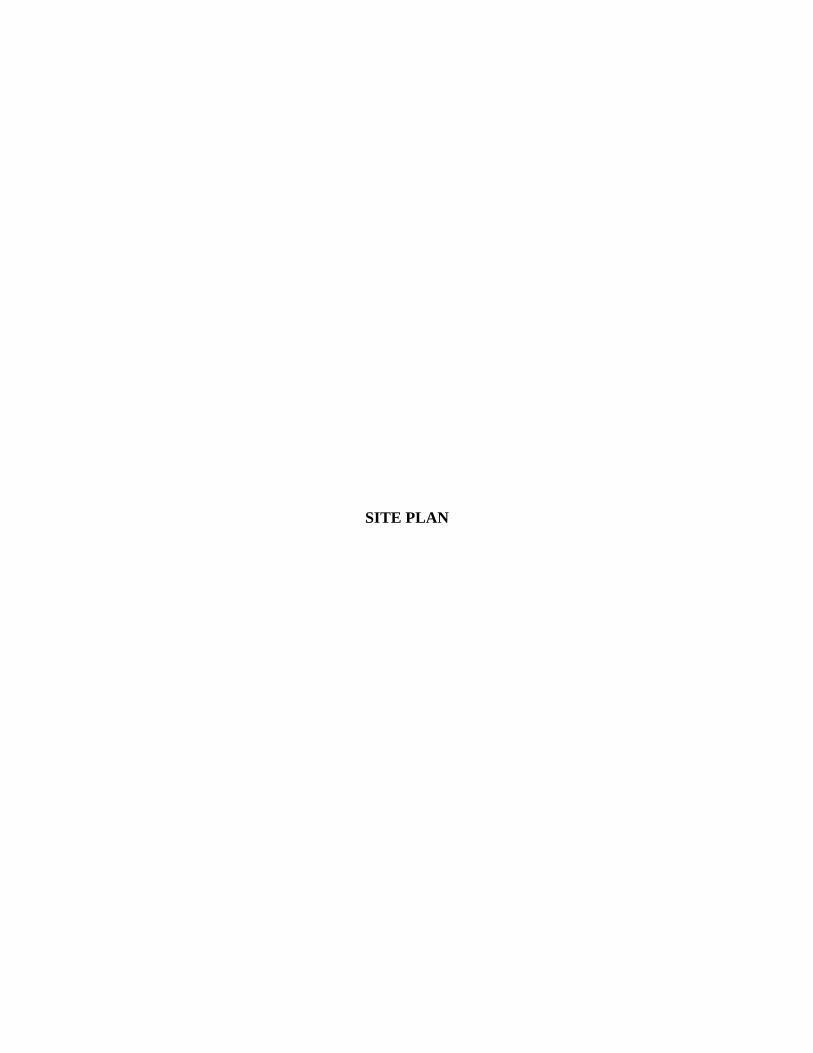

Site Plan

Source: Developers

Improvements

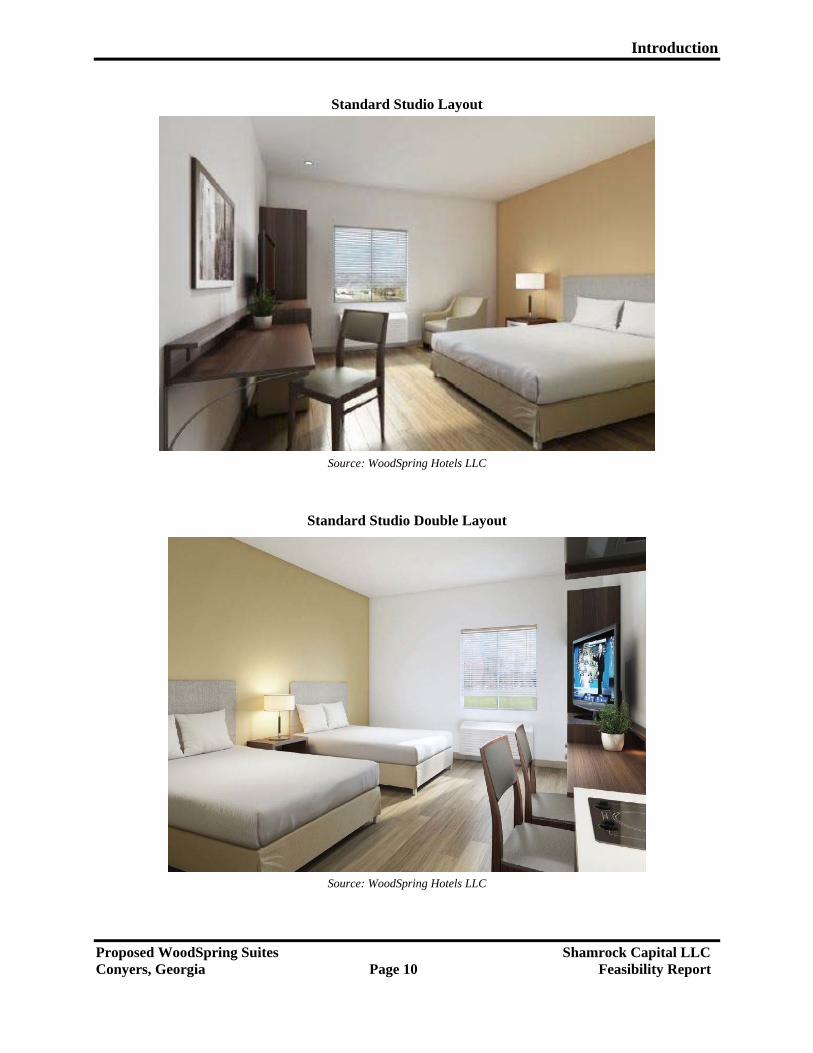

Our research indicates that the proposed 124-room, 4-story, interior-corridor, extended-stay hotel

would be suitable for the market. WoodSpring Suites typically is positioned in the market as an

economy-priced extended-stay hotel. The proposed prototype design will offer a guest laundry

facility and an assumed mix of 78 studios, 40 studio doubles and 6 studio sleepers (pull-out sofas)

with full-size refrigerators, microwaves, and stove-top heating elements. It is noted that two rooms

will be designated for two unspecified employees to provide on-site management and a security

presence, and therefore will be excluded from the subject’s rentable inventory.

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 8 Feasibility Report

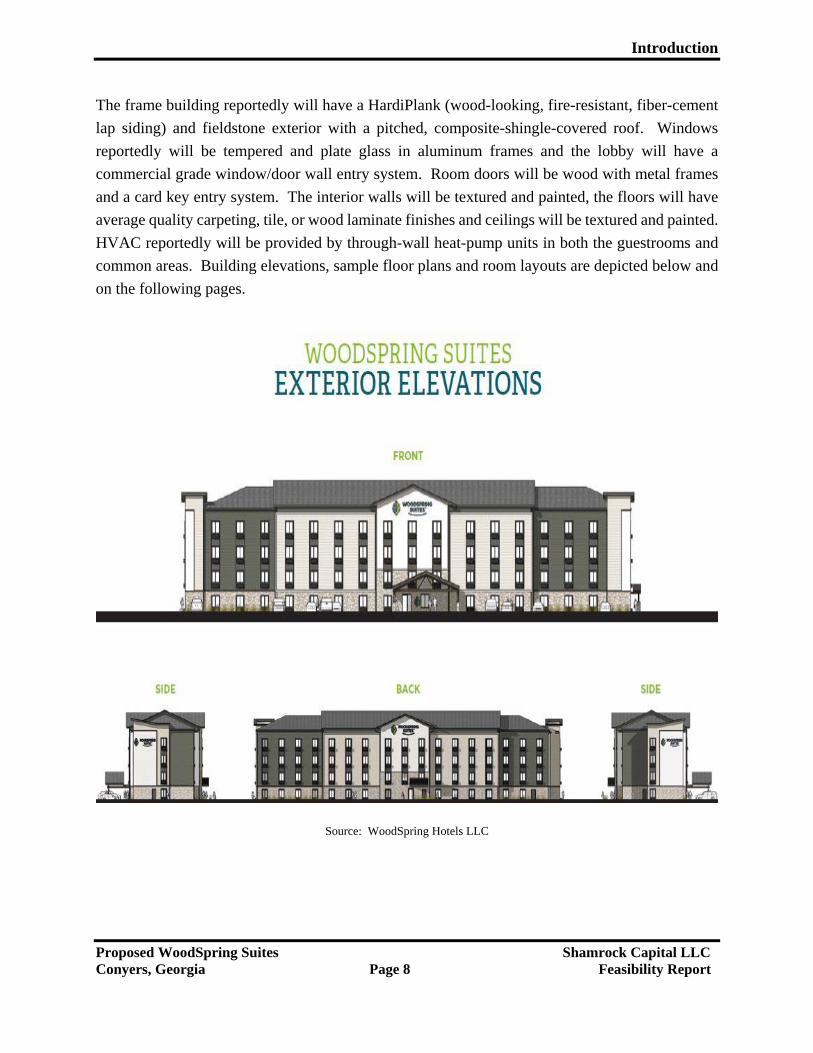

The frame building reportedly will have a HardiPlank (wood-looking, fire-resistant, fiber-cement

lap siding) and fieldstone exterior with a pitched, composite-shingle-covered roof. Windows

reportedly will be tempered and plate glass in aluminum frames and the lobby will have a

commercial grade window/door wall entry system. Room doors will be wood with metal frames

and a card key entry system. The interior walls will be textured and painted, the floors will have

average quality carpeting, tile, or wood laminate finishes and ceilings will be textured and painted.

HVAC reportedly will be provided by through-wall heat-pump units in both the guestrooms and

common areas. Building elevations, sample floor plans and room layouts are depicted below and

on the following pages.

Source: WoodSpring Hotels LLC

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 9 Feasibility Report

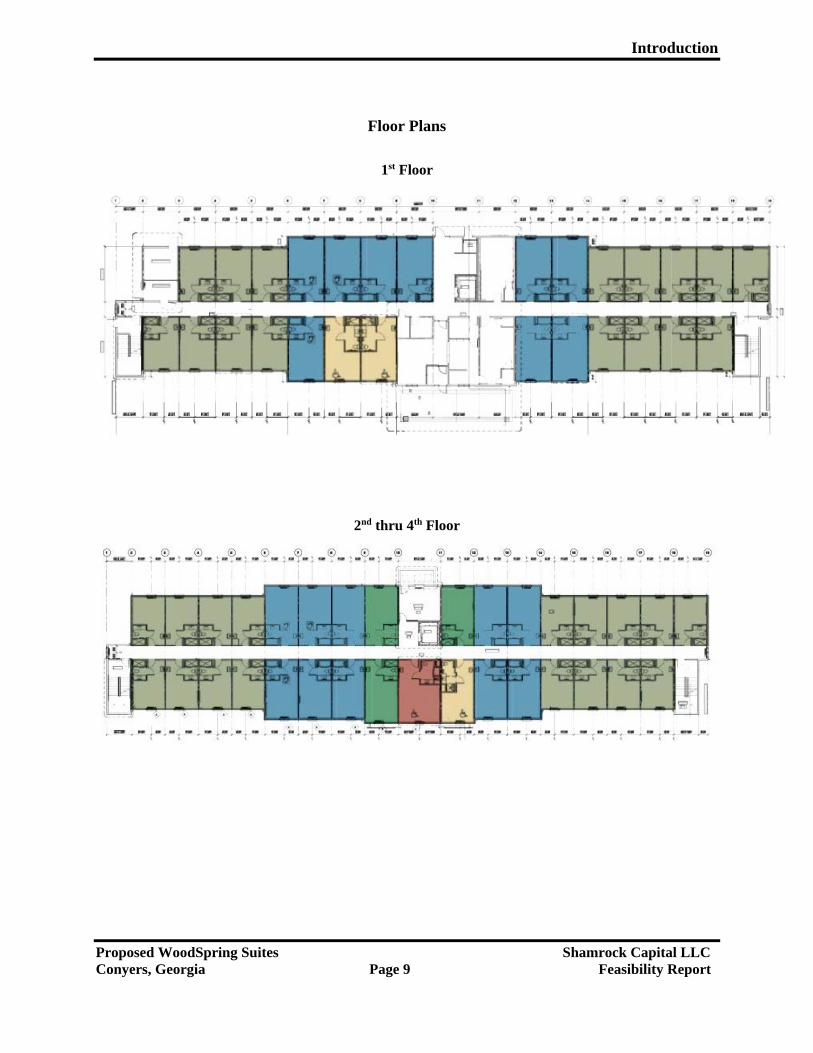

Floor Plans

1st Floor

2nd thru 4th Floor

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 10 Feasibility Report

Standard Studio Layout

Source: WoodSpring Hotels LLC

Standard Studio Double Layout

Source: WoodSpring Hotels LLC

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 11 Feasibility Report

Each guestroom and all public restroom areas are assumed to have adequate plumbing fixtures and

electrical supply to serve the needs of the proposed hotel’s clientele. Lighting will be provided by

LED energy-efficient fixtures in the ceilings and lamps throughout the hotel. Fire protection will

be provided by hard-wired smoke detectors and a sprinkler system. Sufficient parking will be

available onsite; hotel grounds will be adequately landscaped. The property will have exterior

wall-mounted signage consistent with brand standards and local zoning ordinances.

The subject is proposed and, according to the Marshall Valuation Service’s construction index,

will have an economic life of 45 years upon completion. For a well-maintained property, the

effective age may be considerably less than its actual age. As proposed, there do not appear to be

any reasons to make deductions in the depreciation category from a functional source. As will be

shown in the income analysis, the proposed improvements will contribute economically to the

property. Given the current market conditions, there is no evidence of economic/external

obsolescence that will negatively affect the property or diminish its value.

Client and Intended User Disclosure

The client and intended user of this feasibility study is Mountain View Hospitality LLC. Mr.

David Babatope, Member, authorized the preparation of this analysis by signing a letter of proposal

dated October 17, 2016. Any use of this report by third parties is unauthorized without the written

consent of the Client and Shamrock Capital LLC.

Client’s Intended Use Disclosure

The intent of this feasibility study is to determine the financial feasibility of the proposed extended-

stay hotel development utilizing market-derived income and expense estimates and developer-

provided construction costs for the Client’s use in internal financial analysis and decision making.

Date of Analysis

The subject market area and proposed site were most recently inspected on October 21, 2016 and

this date will serve as the effective date of our analysis. Based upon information provided by the

developer and our analysis of the market, the project is expected to be completed by January 1,

2018 and reach a stabilized level of occupancy not later than January 1, 2019.

Introduction

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 12 Feasibility Report

Ownership and Property History

Ownership of the parent parcel of the subject hotel site is vested in the name of Iris Development

LLC. The grantee acquired the parent property on June 22, 2015 from Atlanta Suburbia Ltd for a

disclosed amount of $280,675, as recorded in Deed Book 5719 at Page 16 in the Rockdale County

Board of Assessors’ Office.

Scope of the Feasibility Study

The scope of this feasibility study includes the investigations necessary to gather sufficient data from

which to derive an opinion of market conditions and trends, and encompasses the necessary research

and analysis to prepare a report in accordance with its intended use, the Standards of Professional

Practice of the Appraisal Institute and the Uniform Standards of Professional Appraisal Practice.

An inspection of the property and its neighborhood was conducted to determine the physical

features and condition of the subject site and the environment in which the proposed extended-

stay hotel will be located. When deemed appropriate, contacts were made with municipal

authorities (public works and utilities, zoning administration, planning, etc.) to determine

compliance or noncompliance with local, state, and federal regulations.

The subject property data is based upon information provided by the developer. Properties similar

in important key aspects to the subject were explored throughout the market area to determine

existing/proposed extended-stay and economy limited-service hotel inventory, supply-demand,

and marketability of properties within the subject’s classification. A thorough research effort was

conducted to extract market data to be used in the feasibility study. To the best of our ability, the

research, analysis and interpretation of the information in the marketplace were completed in

accordance with sound analytical principles and the opinions and conclusions are considered to be

reasonable and reliable.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 13 Feasibility Report

Area Overview

This analysis summarizes important demographic trends that influence real estate values in a

defined area. This analysis attempts to highlight important facets of the area economy and

illustrates past, current and future growth trends. The general area has first been studied to gain

an insight from a macro level, and then the market area has been studied with regards to

surrounding land uses and growth patterns.

The City of Conyers, Rockdale County, GA and Atlanta–Sandy Springs–Roswell MSA

Conyers, located 20 miles east of Atlanta on Interstate Highway 20, is the seat of Rockdale County

and part of the Atlanta Metropolitan Statistical Area, the ninth-largest in the U.S. By way of

contrast, Rockdale County comprises only 132 square miles and is ranked second-smallest among

Georgia’s 159 counties. The City of Conyers is transected east-west by Interstate Highway 20 and

lies between the cities of Covington 12± miles to the east in adjacent Newton County and Atlanta

25± miles to the west.

In the early 1840s, Covington banker W. D. Conyers acquired strategically important land from

its first-known settler and violently anti-railroad blacksmith named Holcombe, whereupon he

deeded the rights to Georgia Railroad, which needed the property to complete rail service between

Augusta and Marthasville (current day Atlanta). In 1845, the railroad named its newly completed

watering depot and post office “Conyers Station” which, nine years after the first train arrived, was

incorporated as the Town of Conyers with a population of 400. Sixteen years later, in 1870,

Rockdale became Georgia’s 133rd county.

Rockdale County borders Gwinnett and Walton Counties to the north, Newton County to the east

and south, and Henry and DeKalb Counties to the west. In addition to its past and present railroad,

distribution and manufacturing roots, Rockdale County also is known as a Camera Ready

Community, one which offers financial incentives, production resources and professional support

to the film industry for such companies as Warner Brothers’ Bonanza Productions and Twentieth

Century Fox, and one which has a rich history of having served as a filming location for such

movies as Flash, Sweet Home Alabama, Gods and Generals, Identity Thief, Endless Love, and

Selma, and for such TV shows as The Originals, The Following, Vampire Diaries, In the Heat of

the Night and Dukes of Hazard.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 14 Feasibility Report

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 15 Feasibility Report

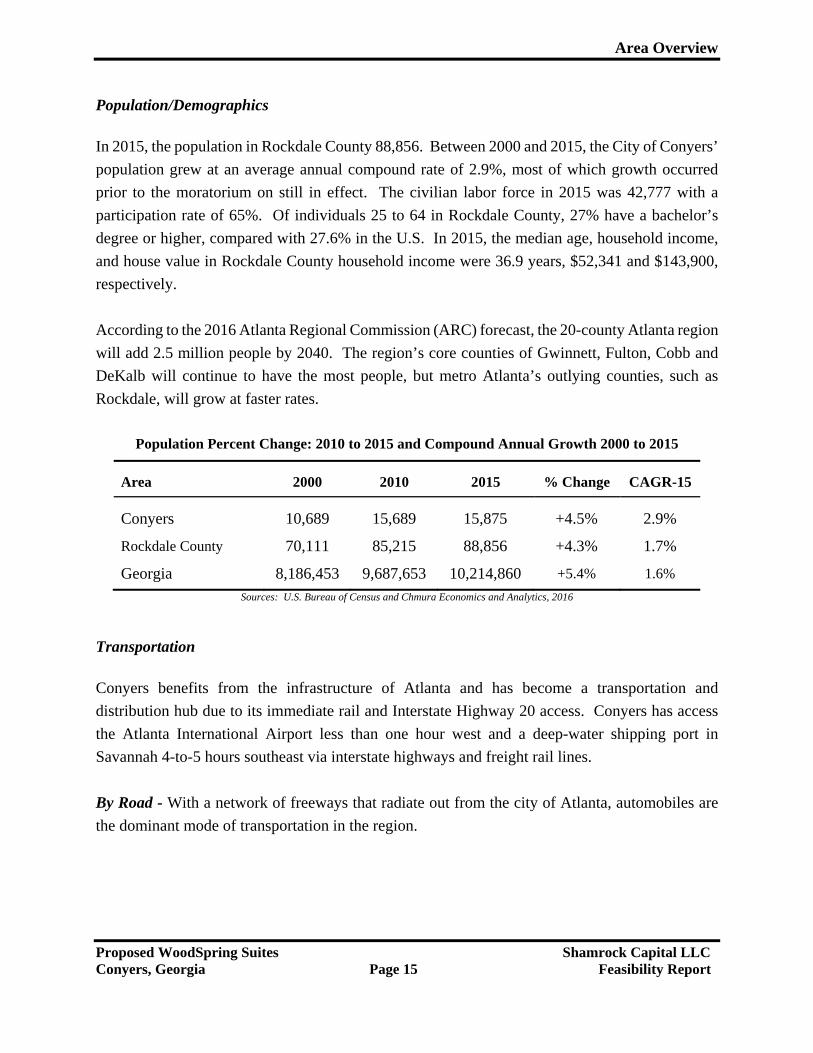

Population/Demographics

In 2015, the population in Rockdale County 88,856. Between 2000 and 2015, the City of Conyers’

population grew at an average annual compound rate of 2.9%, most of which growth occurred

prior to the moratorium on still in effect. The civilian labor force in 2015 was 42,777 with a

participation rate of 65%. Of individuals 25 to 64 in Rockdale County, 27% have a bachelor’s

degree or higher, compared with 27.6% in the U.S. In 2015, the median age, household income,

and house value in Rockdale County household income were 36.9 years, $52,341 and $143,900,

respectively.

According to the 2016 Atlanta Regional Commission (ARC) forecast, the 20-county Atlanta region

will add 2.5 million people by 2040. The region’s core counties of Gwinnett, Fulton, Cobb and

DeKalb will continue to have the most people, but metro Atlanta’s outlying counties, such as

Rockdale, will grow at faster rates.

Population Percent Change: 2010 to 2015 and Compound Annual Growth 2000 to 2015

Area 2000 2010 2015 % Change CAGR-15

Conyers 10,689 15,689 15,875 +4.5% 2.9%

Rockdale County 70,111 85,215 88,856 +4.3% 1.7%

Georgia 8,186,453 9,687,653 10,214,860 +5.4% 1.6%

Sources: U.S. Bureau of Census and Chmura Economics and Analytics, 2016

Transportation

Conyers benefits from the infrastructure of Atlanta and has become a transportation and

distribution hub due to its immediate rail and Interstate Highway 20 access. Conyers has access

the Atlanta International Airport less than one hour west and a deep-water shipping port in

Savannah 4-to-5 hours southeast via interstate highways and freight rail lines.

By Road - With a network of freeways that radiate out from the city of Atlanta, automobiles are

the dominant mode of transportation in the region.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 16 Feasibility Report

Three major interstate highways converge in Atlanta: I-20 (east-west), I-75 (northwest-southeast),

and I-85 (northeast-southwest). The latter two combine in the middle of the city to form the

Downtown Connector (I-75/85), which carries more than 340,000 vehicles per day and is one of

the most congested segments of interstate highway in the United States. Atlanta is mostly encircled

by Interstate 285, a beltway locally known as "the Perimeter," which has come to mark the

boundary between "Inside the Perimeter" (ITP), comprising the city and close-in suburbs, and

"Outside the Perimeter" (OTP), comprising the outer suburbs and exurbs. The three main arteries

from I-285 are:

Interstate 20

Interstate 75

Interstate 85

Being near these major thoroughfares provides good access to the major cities of the Southeast,

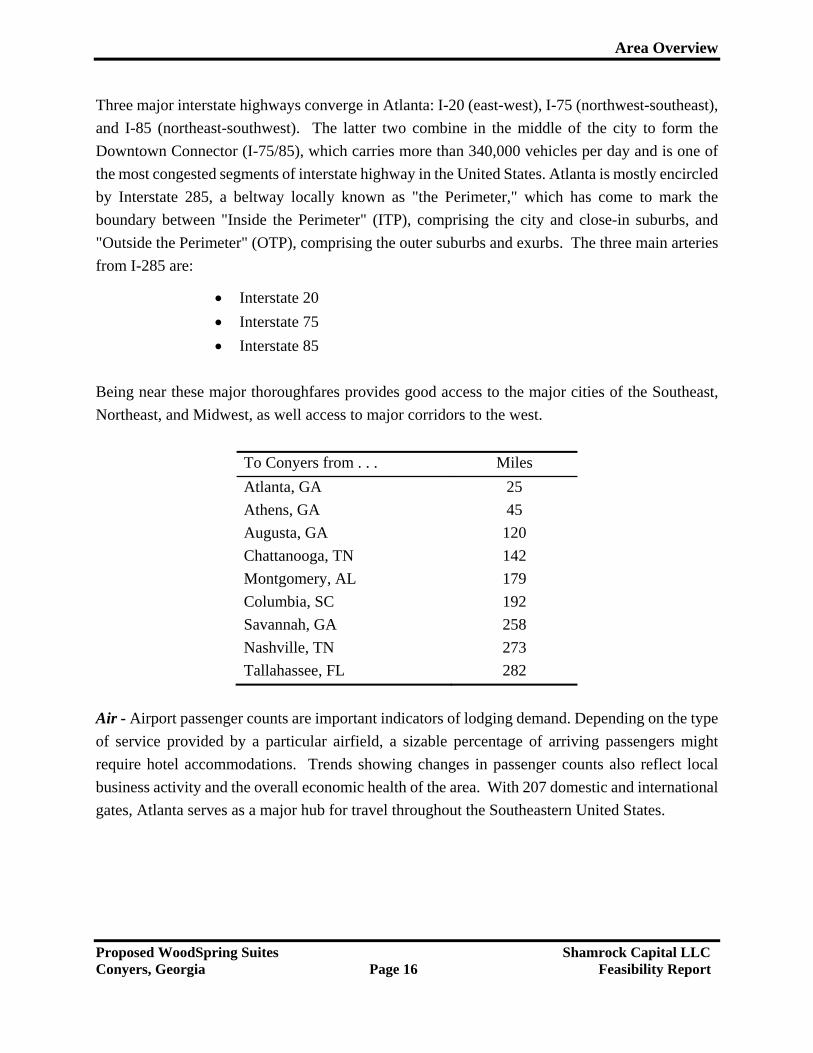

Northeast, and Midwest, as well access to major corridors to the west.

To Conyers from . . . Miles

Atlanta, GA 25

Athens, GA 45

Augusta, GA 120

Chattanooga, TN 142

Montgomery, AL 179

Columbia, SC 192

Savannah, GA 258

Nashville, TN 273

Tallahassee, FL 282

Air - Airport passenger counts are important indicators of lodging demand. Depending on the type

of service provided by a particular airfield, a sizable percentage of arriving passengers might

require hotel accommodations. Trends showing changes in passenger counts also reflect local

business activity and the overall economic health of the area. With 207 domestic and international

gates, Atlanta serves as a major hub for travel throughout the Southeastern United States.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 17 Feasibility Report

Hartsfield–Jackson Atlanta International Airport is an international airport located seven miles

south of the central business district of Atlanta. It has been the world's busiest airport by passenger

traffic since 1998, and by number of landings and take-offs from 2005 to 2013 and again in 2015.

Hartsfield–Jackson, often regarded as the world's busiest airport, accommodates 100+ million

passengers and 950,000± flights, most of which are domestic flights from within the United States.

It is noted that Covington Municipal Airport, 10 miles west of Conyers, serves private-sector

aircraft.

Freight - CSX offers rail service at Conyers and CSX and Norfolk Southern offer rail and

piggyback service from Atlanta. Metro Atlanta is serviced by 34 inter/intrastate carriers.

Overnight package delivery is provided by Federal Express, UPS, Airborne, and a number of other

couriers.

By Water - The nearest commercial river, Chattahoochee, maintains a nine-foot channel depth and

a public barge dock at Columbus, which is 116 miles away. The nearest seaport is 236 miles away

at Savannah, which has maintains a 42-foot channel depth.

Education

With more than 30 colleges and universities, Atlanta is considered a center for higher education.

Among the most prominent public universities in Atlanta is the Georgia Institute of Technology,

a research university located in Midtown that has been consistently ranked among the nation's top

ten public universities for its degree programs in engineering, computing, management, the

sciences, architecture, and liberal arts. Georgia State University, a public research university

located in Downtown Atlanta, is the largest of the 29 public colleges and universities in the

University System of Georgia and a major contributor to the revitalization of the city's central

business district. Atlanta also is home to nationally renowned private colleges and universities,

most notably Emory University, a leading liberal arts and research institution that ranks among the

top 20 schools in the United States and operates Emory Healthcare, the largest health care system

in Georgia.

Also located in the city is the Atlanta University Center, the largest contiguous consortium of

historically black colleges, comprising Spelman College, Clark Atlanta University, Morehouse

College, Morehouse School of Medicine, and Interdenominational Theological Center. Atlanta

also contains a campus of the Savannah College of Art and Design, a private university that has

proven to be a major factor in the recent growth of Atlanta's visual arts community.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 18 Feasibility Report

Health Services

Atlanta is the health service hub of the region for specialized care. The following local hospitals and facilities provide routine and emergency care.

Rockdale Healthcare Center

Multi-Care Holistic Health Center

Mercy Heart Clinic

Central Home Health Care an Amidases Company

Rockdale Medical Center

Economy

Rockdale County’s labor force is at a current level of 55,826. Initial claims for unemployment

insurance benefits in Rockdale County decreased from 491 to 412, a decrease of 16.1 percent

from August.

2015 Labor Force Statistics – Rockdale County

Labor Force Employed Unemployed Unemployment Rate

42,294 39,598 2,694 6.4% Source: Chmura Economics and Analytics, 2016

In 2016, the leading industries were: Modular Steel Fabrication, Thermoformed Plastic

Manufacturing, Home Interior Manufacturing, Mechanical Construction, Packing Companies, and

Distribution Centers.

Key Locally Headquartered Employers and Businesses

Madison Industries, Inc. of Georgia was established in 1962 to serve the major oil companies in

building their retail facilities. From a 10,000-square-foot building in 1962, the plant today has

over 295,000 square feet of production and office facilities. Madison has one of the largest beam-

and-channel fabricating drill lines in the Southeast, with cleaning, cutting and drilling capabilities

up to a 36” beam. Their sheet metal facility has a cut-to-length line, routing and hydraulic CNC

punching machines with roll-forming capabilities.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 19 Feasibility Report

At present, in addition to building retail facilities for the major oil companies, Madison also builds

modular medical clinics, hospitals, financial facilities and restaurants. Other product offerings

include architectural cladding, renovation of existing structures, structural steel packages, drive-

thru and tunnel carwashes, and building and canopy signage.

C+K Plastics, Inc. is a leading manufacturer of thermoformed plastic products and assemblies for

the aerospace, medical, agricultural equipment, refrigeration, petroleum, and other industries, has

officially opened its new manufacturing facility in Conyers, Georgia.

Bachelor & Kimball, Inc. (BKI) is a well-respected mechanical contractor with more than 30 years’

experience specializing in commercial HVAC mechanical and plumbing construction for mission

critical facilities including hospitals, laboratories, data centers, institutional, and manufacturing/

industrial high purity piping systems. They provide design-build expertise as well as turnkey

construction. BKI currently has approximately 200 employees and reports annual revenues of

more than $150,000,000. They plan to invest more than $5,000,000 into their new facility in

Rockdale County.

About 5,000 jobs in activities such as motor vehicle parts, communications and equipment

manufacturing are supported by the Advanced Manufacturing cluster.

There are 112 accommodations and food and beverage establishments in Conyers, including 15

hotels and motels, with an average annual payroll of $34,659 and an aggregate labor force of

3,000± persons.

Businesses locating or expanding in Rockdale County can take advantage of a variety of local and

state-wide business incentives designed to encourage economic investment and growth. Tax

credits give Georgia businesses the opportunity to minimize or even eliminate state corporate

income tax. They apply to all qualifying companies, whether already in Georgia or new to the

state. Typically, corporate income tax credits apply to 50 percent of a company’s state tax liability

in a given year, but in some cases they can offset up to 100 percent of corporate income tax as well

as payroll withholding liability. The tax credits referenced here are extended by the state of

Georgia. In addition, Georgia offers significant tax exemptions to support business growth.

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 20 Feasibility Report

The Atlanta metropolitan area is the 10th largest metro economy in the United States by real GDP

and the largest in the South, yet living and business costs compare favorably with metro areas of

smaller size. A diverse industrial structure, strong population growth, reasonable business costs,

and high educational attainment sustain Atlanta’s growth potential above the nation’s. Also, its

status as a major transportation and logistics hub makes the metro economy an important factor

throughout the South.

Key Economic Facts

Through October 2016, year-over-year housing market trends for Conyers indicate a 7% rise in

the median sales price of homes and a 0% rise in median rent per month, suggesting there exists

minimal-to-no frictional vacancy in the Conyers market as probable tenants have secured

accommodations elsewhere, at least until the waste water treatment moratorium on new apartment

construction can be lifted (est. 2020). It is noted the Conyers-Rockdale Economic Development

Council in May 2016 indicated that the sewer and water moratorium has impacted building

permits, with fewer than 100 issued year to date.

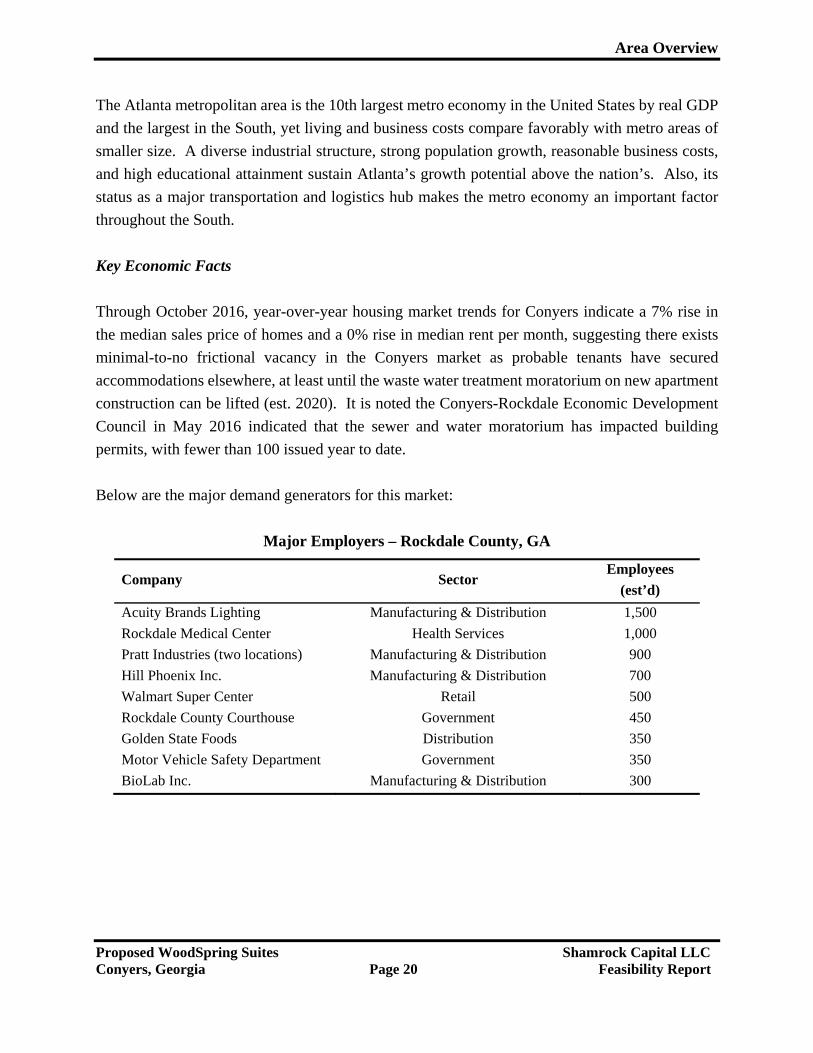

Below are the major demand generators for this market:

Major Employers – Rockdale County, GA

Company Sector Employees

(est’d)

Acuity Brands Lighting Manufacturing & Distribution 1,500

Rockdale Medical Center Health Services 1,000

Pratt Industries (two locations) Manufacturing & Distribution 900

Hill Phoenix Inc. Manufacturing & Distribution 700

Walmart Super Center Retail 500

Rockdale County Courthouse Government 450

Golden State Foods Distribution 350

Motor Vehicle Safety Department Government 350

BioLab Inc. Manufacturing & Distribution 300

Area Overview

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 21 Feasibility Report

Conclusion

Although Conyers is experiencing a period of moderate economic expansion due in significant

part the film industry and companies from other states relocating to the area, the sewer and water

moratorium continues to put downward pressure on growth. In addition to the film industry and

above-listed employers, the city, county and surrounding area are supported by a number of

employers and expansion projects that provide a solid foundation for the local economy, such as

the planned Baxter Pharma 1,000,000-square foot distribution center which will be completed by

2018. New development, coupled with thriving film and television production companies already

operating within the Conyers/Rockdale County market area, suggest the job and overall economic

outlook are trending positively.

Our analysis of this specific market also considers the broader context of the national economy.

The U.S. economy has experienced economic expansion during the last seven quarters, with the

most recent peak being the 3.7% growth realized in the second quarter of 2015. During the last

two quarters of 2015, growth waned, falling to a 1.0% growth rate during the fourth quarter. In

recent months, increases in personal consumption expenditures (PCE) and residential housing

were the primary factors in the net gain. PCE was up 1.3% and residential housing was up a robust

8.0%.

In the fourth quarter of 2015, both imports and exports declined slightly, and non- residential

investments also were down. U.S. economic growth is anticipated to support continued expansion

of lodging demand; however, as economic growth slows, demand growth may not be as robust in

FY 17 as in the last several years. Nevertheless, the stability in the U.S. economy is maintaining

strong interest in hotel investments by a diverse array of national and international market

participants.

Market Area

Land uses in the proposed subject’s immediate market area include light industrial, warehousing

and distribution facilities; Fieldstone Plaza Shopping Center; quick-service food venues including

Burger King, Dunkin’ Donuts, Hardee’s, McDonald’s and Wendy’s; diners and casual dining

venues including Los Bravos, Sudo Bar & Grill, Third Base Grill, Tokyo Hibachi Express, and

Waffle House; four gas station/convenience stores; a medical clinic and animal hospital; two

grocery stores; an auto dealership and auto and truck accessory and service centers.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 22 Feasibility Report

Lodging Trends and Market Analysis

The following analysis will examine hotel/motel supply and demand trends as well as factors that

influence the hotel investment market.

National Trends

The history of the lodging industry is characterized by periods of rapid expansion and

development, followed by periods of adjustment and recovery. The paragraphs that follow discuss

historical and current industry supply and demand, occupancy, average daily rate (ADR) and

revenue per available room (RevPAR). The principal sources for the following discussion on

national lodging industry trends and the U.S. economy include: Smith Travel Research, Hotel

News Now (STR), Pricewaterhouse Coopers, Forbes, and FocusEconomics.

Historical Industry Trends and Future Outlook

The U.S. economy expanded 2.4% in 2015, which matched 2014’s growth rate. However, Q4

GDP expansion slowed to a seasonally adjusted annualized rate of 1%, half of what it had been

the previous quarter. This slowdown is due to (1) a deceleration in domestic demand, as evidenced

by lower private consumption, higher savings, and weaker investment, and (2) a continuing drop-

off in demand for U.S.-manufactured goods attributable to a strong dollar and a slowdown in

global economic activity, a trend which is expected to continue as the Fed increases interest rates

and further strengthens the dollar. Accordingly, economists have revised their 2016 GDP forecast

downward by 0.3 percentage points to a sub-par growth rate of 2.1% year over year.

Following the recession of 2008 and 2009, hotel and resort operating fundamentals from 2010

through 2014 improved and the lodging industry experienced a notable turnaround, with the

breadth of the recovery encompassing the entire spectrum of chain-scale segments, particularly

the luxury, upper upscale and upscale segments, which include increasingly popular select-service

and lifestyle brands. During this period, rooms supply growth remained modest relative to overall

demand growth; however, in 2015 historical industry trends exhibited cautionary signs of change:

supply growth rates reached their highest level since 2011; demand growth remained healthy but

slowed significantly from 2014; occupancy and ADR growth rates decelerated; and Q2 through

Q4 2015 RevPAR growth rates slowed from record highs in 2014 and Q1 2015.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 23 Feasibility Report

Room Supply and Demand

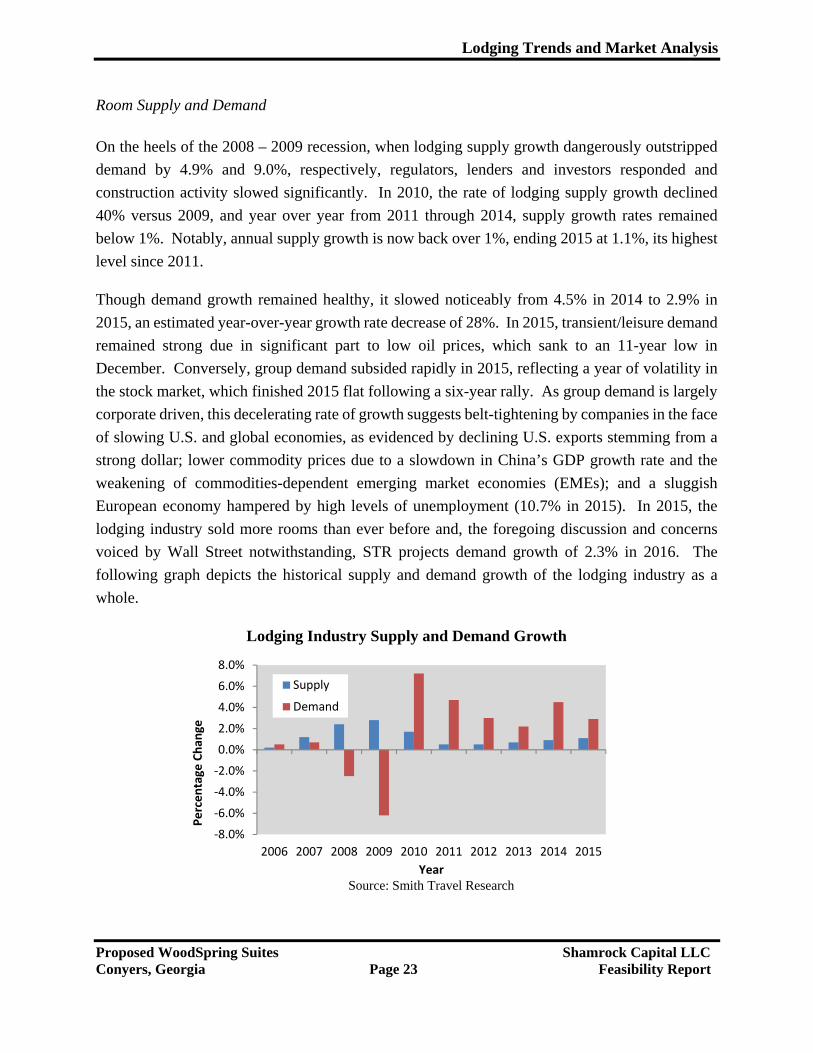

On the heels of the 2008 – 2009 recession, when lodging supply growth dangerously outstripped

demand by 4.9% and 9.0%, respectively, regulators, lenders and investors responded and

construction activity slowed significantly. In 2010, the rate of lodging supply growth declined

40% versus 2009, and year over year from 2011 through 2014, supply growth rates remained

below 1%. Notably, annual supply growth is now back over 1%, ending 2015 at 1.1%, its highest

level since 2011.

Though demand growth remained healthy, it slowed noticeably from 4.5% in 2014 to 2.9% in

2015, an estimated year-over-year growth rate decrease of 28%. In 2015, transient/leisure demand

remained strong due in significant part to low oil prices, which sank to an 11-year low in

December. Conversely, group demand subsided rapidly in 2015, reflecting a year of volatility in

the stock market, which finished 2015 flat following a six-year rally. As group demand is largely

corporate driven, this decelerating rate of growth suggests belt-tightening by companies in the face

of slowing U.S. and global economies, as evidenced by declining U.S. exports stemming from a

strong dollar; lower commodity prices due to a slowdown in China’s GDP growth rate and the

weakening of commodities-dependent emerging market economies (EMEs); and a sluggish

European economy hampered by high levels of unemployment (10.7% in 2015). In 2015, the

lodging industry sold more rooms than ever before and, the foregoing discussion and concerns

voiced by Wall Street notwithstanding, STR projects demand growth of 2.3% in 2016. The

following graph depicts the historical supply and demand growth of the lodging industry as a

whole.

Lodging Industry Supply and Demand Growth

‐8.0%

‐6.0%

‐4.0%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percentage

Chan

ge

YearSource: Smith Travel Research

Supply

Demand

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 24 Feasibility Report

As illustrated by the foregoing graph, rooms supply growth rates outstripped demand growth from

2007 through 2009. Then, from 2010 through 2015 demand growth exceeded supply growth,

posting year-over-year increases ranging from a high of 7.2% in 2010 to a low of 2.2% in 2013.

Notably, demand growth in 2015 slowed to 2.9% from 4.5% the year prior, and STR projects

modest demand growth of 2.3% in 2016.

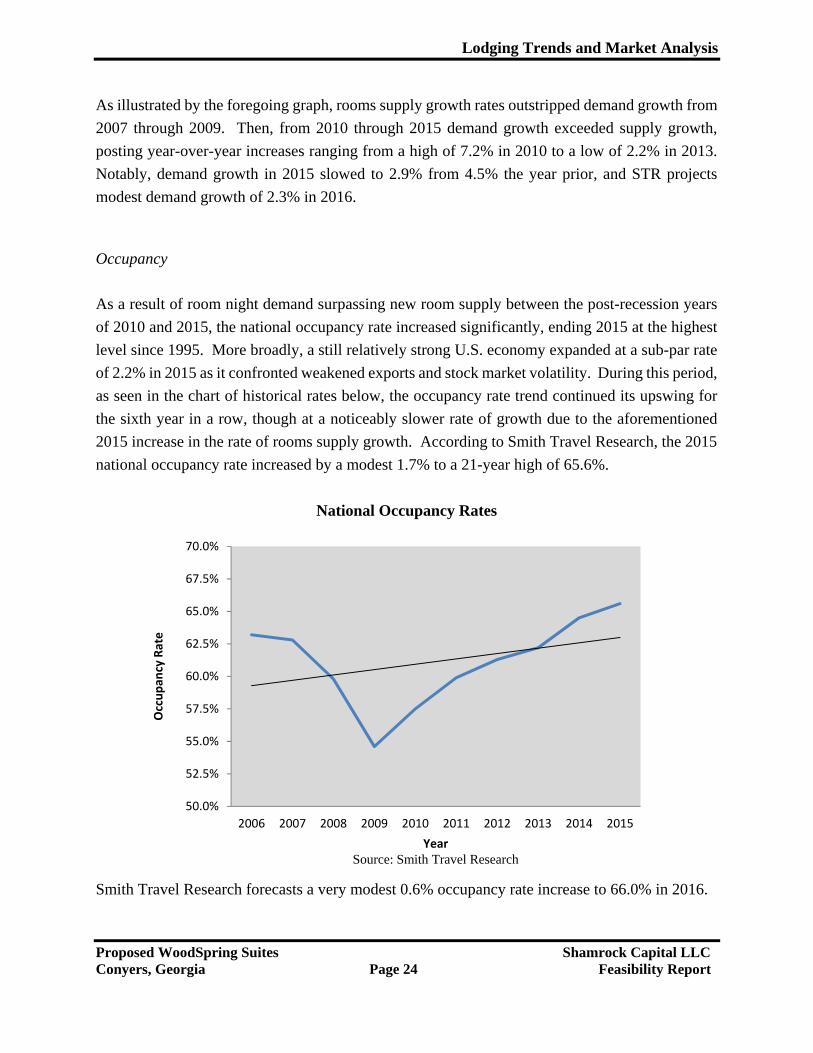

Occupancy

As a result of room night demand surpassing new room supply between the post-recession years

of 2010 and 2015, the national occupancy rate increased significantly, ending 2015 at the highest

level since 1995. More broadly, a still relatively strong U.S. economy expanded at a sub-par rate

of 2.2% in 2015 as it confronted weakened exports and stock market volatility. During this period,

as seen in the chart of historical rates below, the occupancy rate trend continued its upswing for

the sixth year in a row, though at a noticeably slower rate of growth due to the aforementioned

2015 increase in the rate of rooms supply growth. According to Smith Travel Research, the 2015

national occupancy rate increased by a modest 1.7% to a 21-year high of 65.6%.

National Occupancy Rates

Smith Travel Research forecasts a very modest 0.6% occupancy rate increase to 66.0% in 2016.

50.0%

52.5%

55.0%

57.5%

60.0%

62.5%

65.0%

67.5%

70.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Occupan

cy Rate

YearSource: Smith Travel Research

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 25 Feasibility Report

ADR and RevPAR

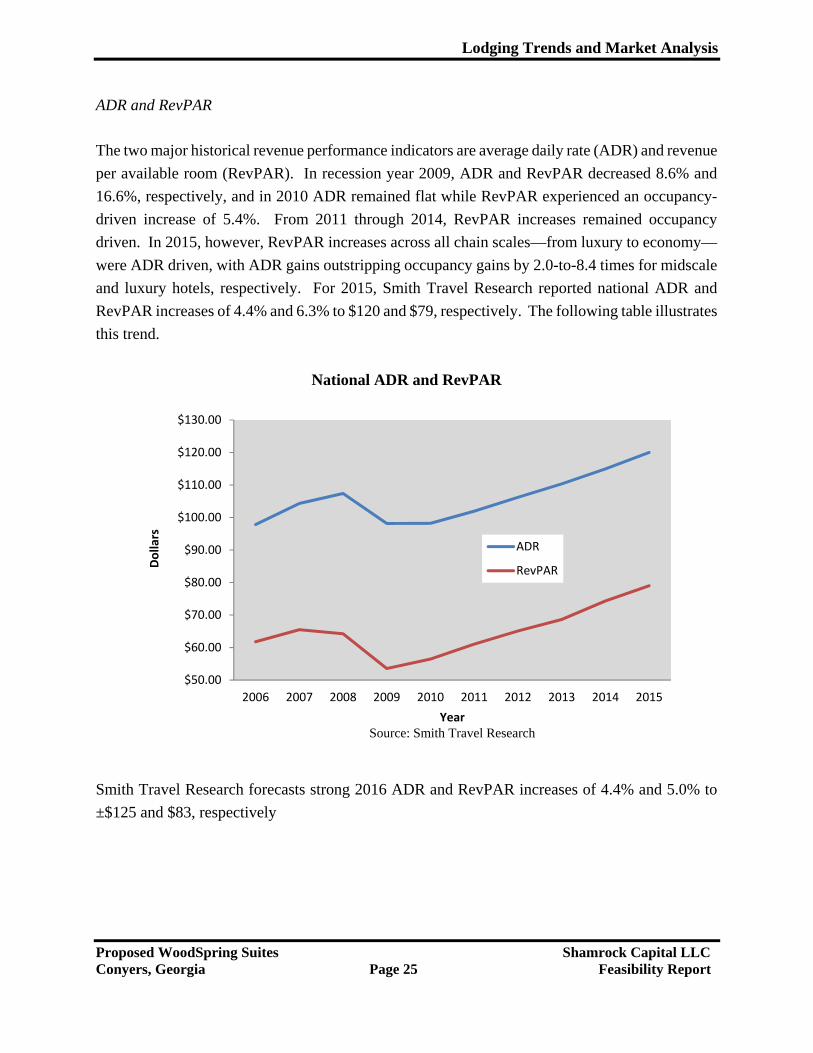

The two major historical revenue performance indicators are average daily rate (ADR) and revenue

per available room (RevPAR). In recession year 2009, ADR and RevPAR decreased 8.6% and

16.6%, respectively, and in 2010 ADR remained flat while RevPAR experienced an occupancy-

driven increase of 5.4%. From 2011 through 2014, RevPAR increases remained occupancy

driven. In 2015, however, RevPAR increases across all chain scales—from luxury to economy—

were ADR driven, with ADR gains outstripping occupancy gains by 2.0-to-8.4 times for midscale

and luxury hotels, respectively. For 2015, Smith Travel Research reported national ADR and

RevPAR increases of 4.4% and 6.3% to $120 and $79, respectively. The following table illustrates

this trend.

National ADR and RevPAR

Smith Travel Research forecasts strong 2016 ADR and RevPAR increases of 4.4% and 5.0% to

±$125 and $83, respectively

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

$110.00

$120.00

$130.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Dollars

YearSource: Smith Travel Research

ADR

RevPAR

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 26 Feasibility Report

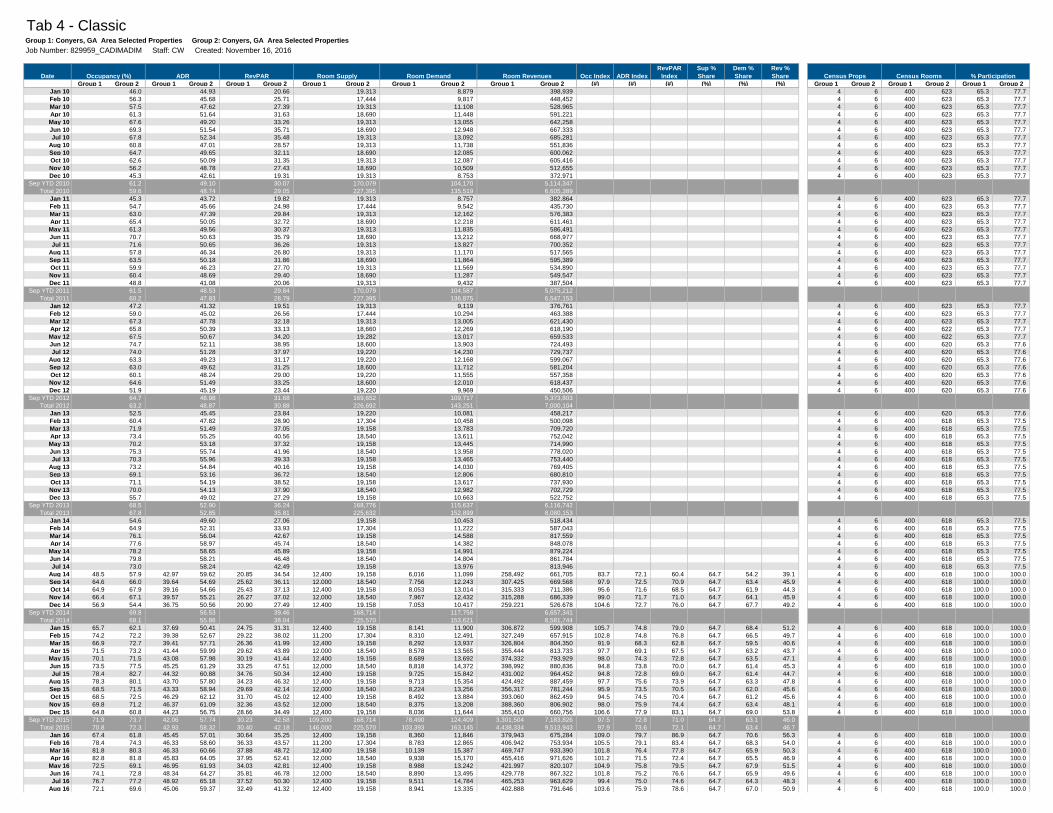

Local Lodging Trends – Level II Market Analysis

The purpose of this section of the report is to give an overview of the major factors influencing the

hospitality industry in the Sacramento market area and also serves to help test the viability of the

proposed economy-extended stay hotel in light of the current supply and demand factors in the

local lodging market.

Competitive Supply Analysis To properly evaluate the competitive lodging market, several supply factors have been considered.

Historic expansion of supply is outlined so as to identify larger submarket trends, most notably

in the general classifications (Resort, Suburban, Urban, Highway, Airport, etc.).

Existing lodging facilities are reviewed to determine those most competitive with the subject.

Proposed lodging facilities are identified and assessed in terms of potential competition with

the subject.

Historical Supply

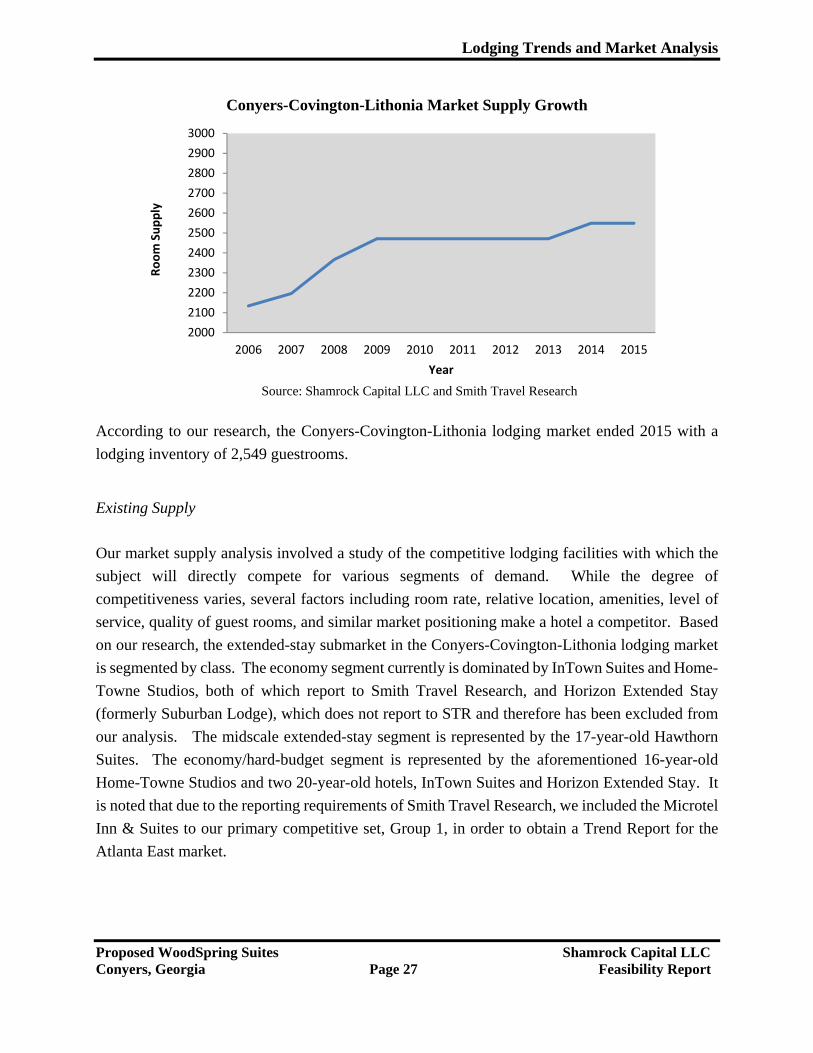

Similar to many markets, the Conyers-Covington-Lithonia market increased supply before and

into “The Great Recession,” with four hotels opening immediately prior to and three hotels opening

during and immediately after the downturn in the market. Supply increased at an annual compound

average growth rate of 3.2% during the decade ending 2015. No new hotels had been added to the

market between 2009 and 2014 when the 78-room Courtyard opened in Conyers. The graph below

summarizes this market’s historical room supply from 2006 through 2015.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 27 Feasibility Report

Conyers-Covington-Lithonia Market Supply Growth

Source: Shamrock Capital LLC and Smith Travel Research

According to our research, the Conyers-Covington-Lithonia lodging market ended 2015 with a

lodging inventory of 2,549 guestrooms.

Existing Supply

Our market supply analysis involved a study of the competitive lodging facilities with which the

subject will directly compete for various segments of demand. While the degree of

competitiveness varies, several factors including room rate, relative location, amenities, level of

service, quality of guest rooms, and similar market positioning make a hotel a competitor. Based

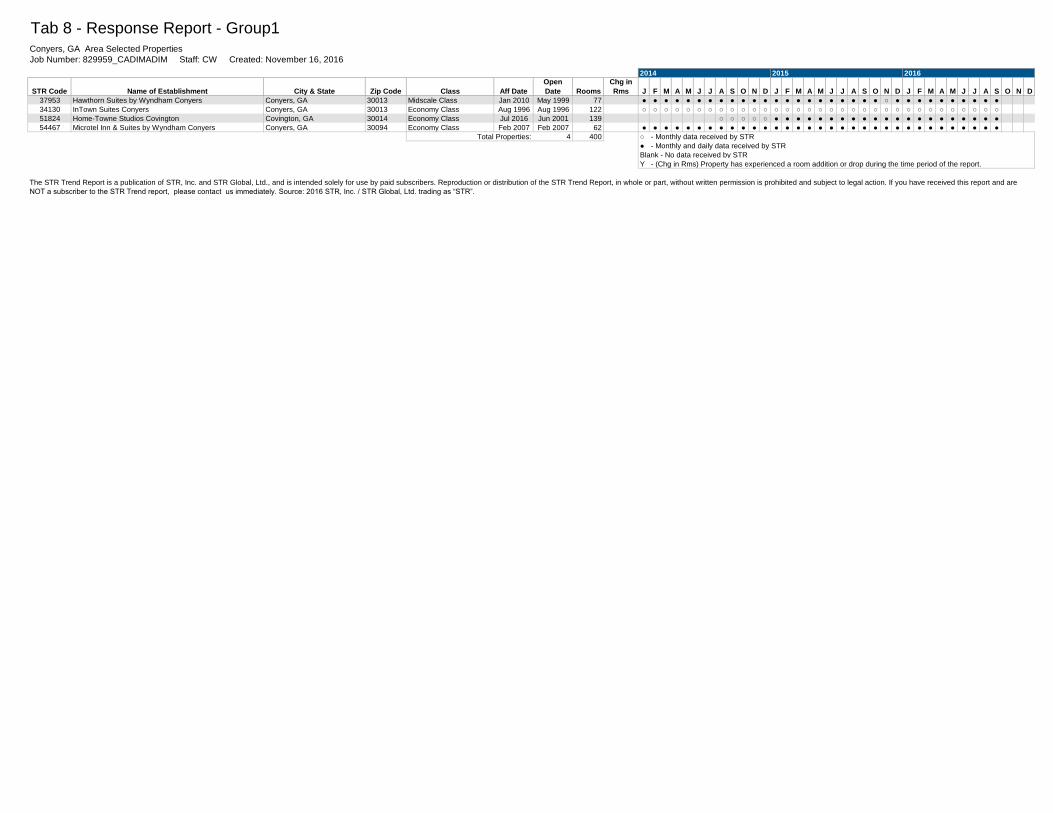

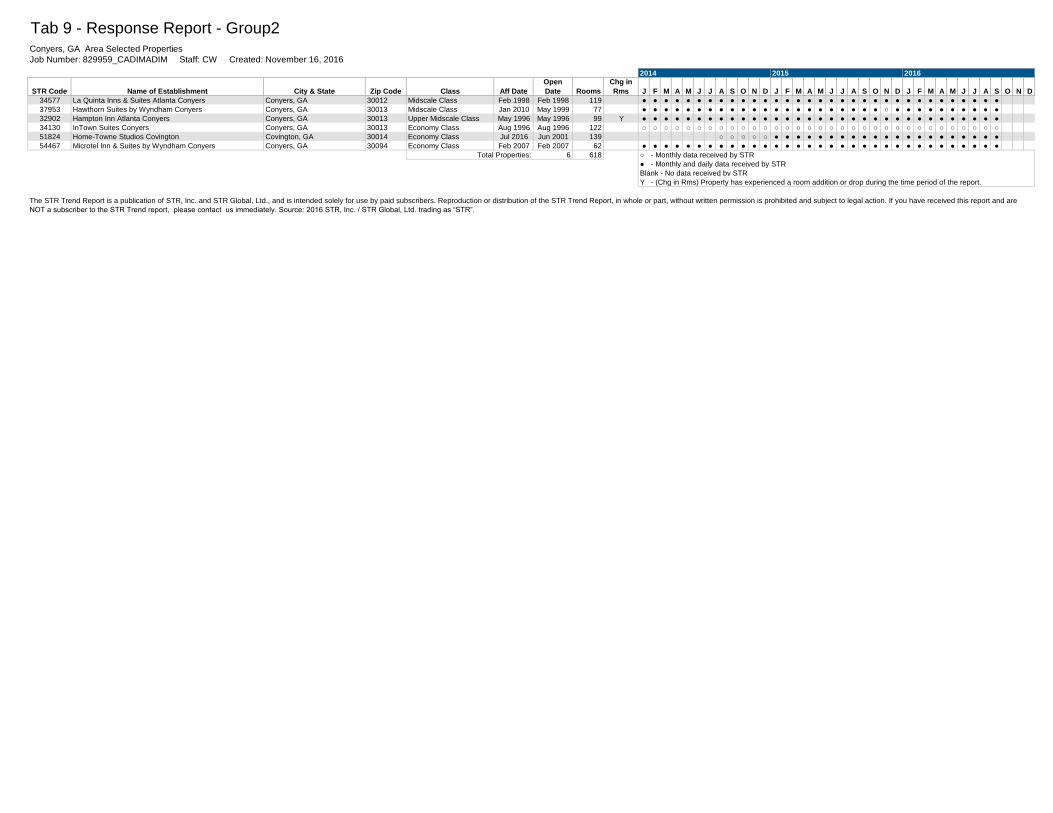

on our research, the extended-stay submarket in the Conyers-Covington-Lithonia lodging market

is segmented by class. The economy segment currently is dominated by InTown Suites and Home-

Towne Studios, both of which report to Smith Travel Research, and Horizon Extended Stay

(formerly Suburban Lodge), which does not report to STR and therefore has been excluded from

our analysis. The midscale extended-stay segment is represented by the 17-year-old Hawthorn

Suites. The economy/hard-budget segment is represented by the aforementioned 16-year-old

Home-Towne Studios and two 20-year-old hotels, InTown Suites and Horizon Extended Stay. It

is noted that due to the reporting requirements of Smith Travel Research, we included the Microtel

Inn & Suites to our primary competitive set, Group 1, in order to obtain a Trend Report for the

Atlanta East market.

2000

2100

2200

2300

2400

2500

2600

2700

2800

2900

3000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Room Supply

Year

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 28 Feasibility Report

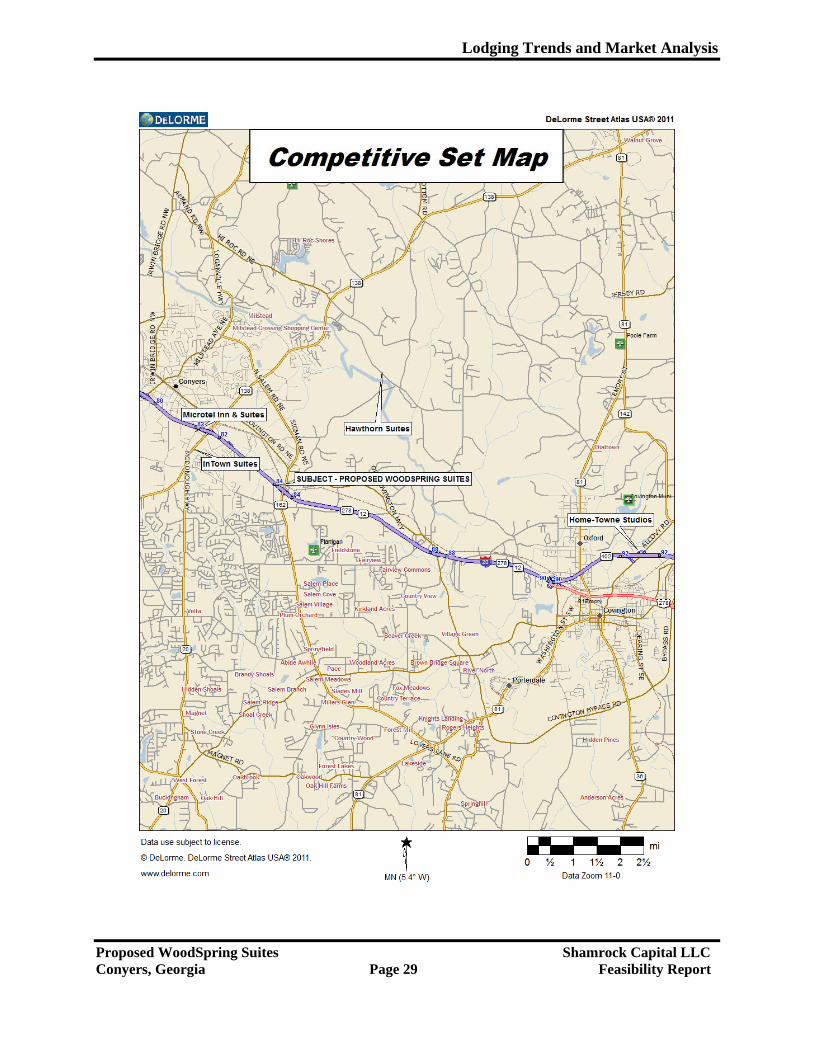

The map on the following page identifies each of the primary competitive properties in relation to

the subject’s location, followed by summary sheets with data based on our on-site interviews with

competitive property managers and other sources.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 29 Feasibility Report

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 30 Feasibility Report

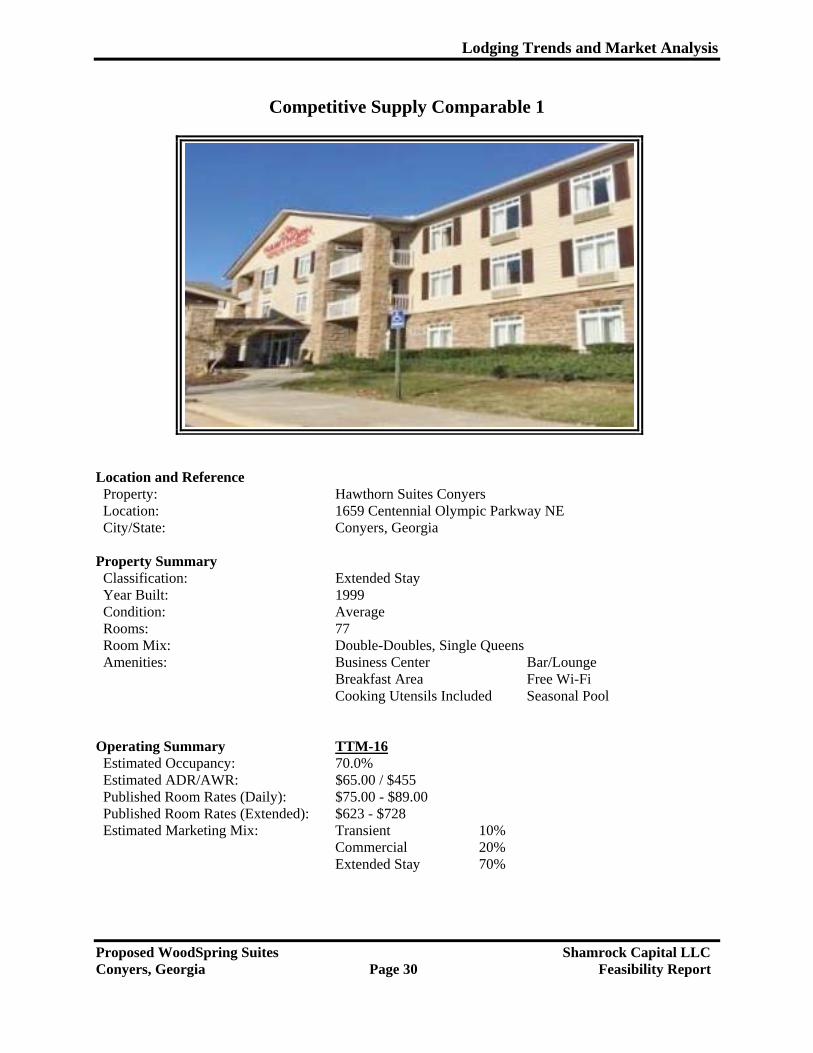

Competitive Supply Comparable 1

Location and Reference Property: Hawthorn Suites Conyers Location: 1659 Centennial Olympic Parkway NE City/State: Conyers, Georgia Property Summary Classification: Extended Stay Year Built: 1999 Condition: Average Rooms: 77 Room Mix: Double-Doubles, Single Queens Amenities: Business Center Bar/Lounge Breakfast Area Free Wi-Fi Cooking Utensils Included Seasonal Pool

Operating Summary TTM-16 Estimated Occupancy: 70.0% Estimated ADR/AWR: $65.00 / $455 Published Room Rates (Daily): $75.00 - $89.00 Published Room Rates (Extended): $623 - $728 Estimated Marketing Mix: Transient 10% Commercial 20% Extended Stay 70%

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 31 Feasibility Report

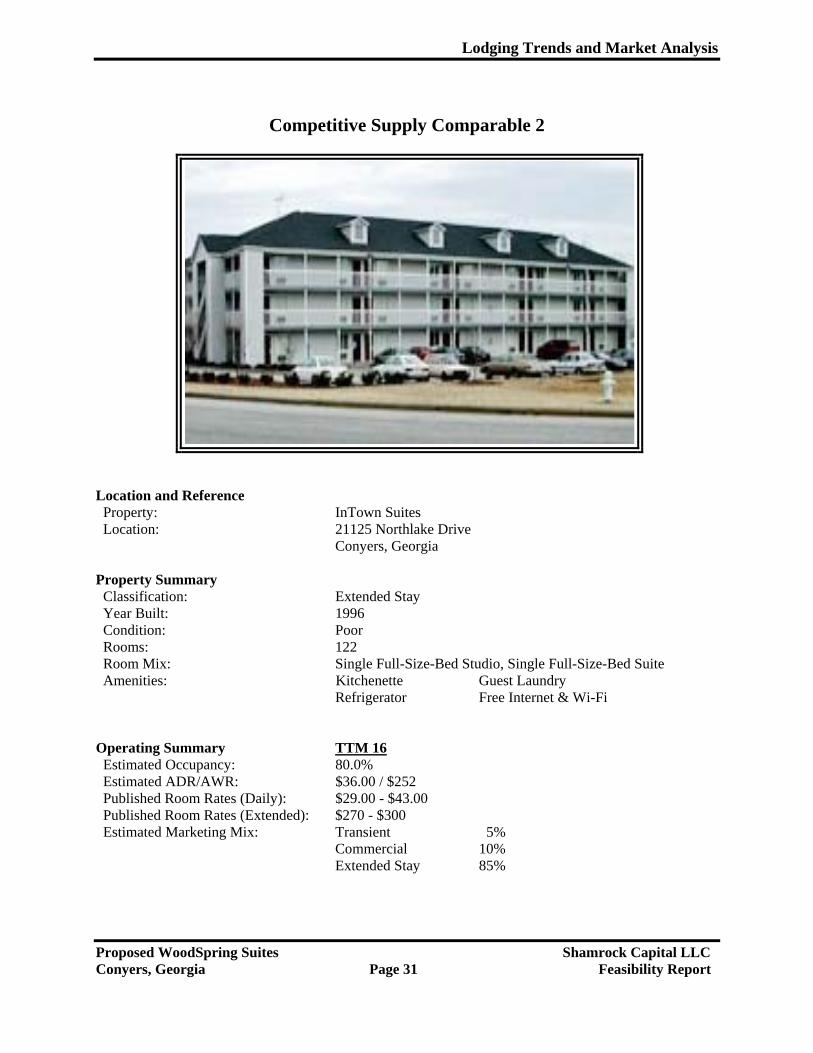

Competitive Supply Comparable 2

Location and Reference Property: InTown Suites Location: 21125 Northlake Drive

Conyers, Georgia

Property Summary Classification: Extended Stay Year Built: 1996 Condition: Poor Rooms: 122 Room Mix: Single Full-Size-Bed Studio, Single Full-Size-Bed Suite Amenities: Kitchenette Guest Laundry

Refrigerator Free Internet & Wi-Fi

Operating Summary TTM 16 Estimated Occupancy: 80.0% Estimated ADR/AWR: $36.00 / $252 Published Room Rates (Daily): $29.00 - $43.00 Published Room Rates (Extended): $270 - $300 Estimated Marketing Mix: Transient 5%

Commercial 10%Extended Stay 85%

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 32 Feasibility Report

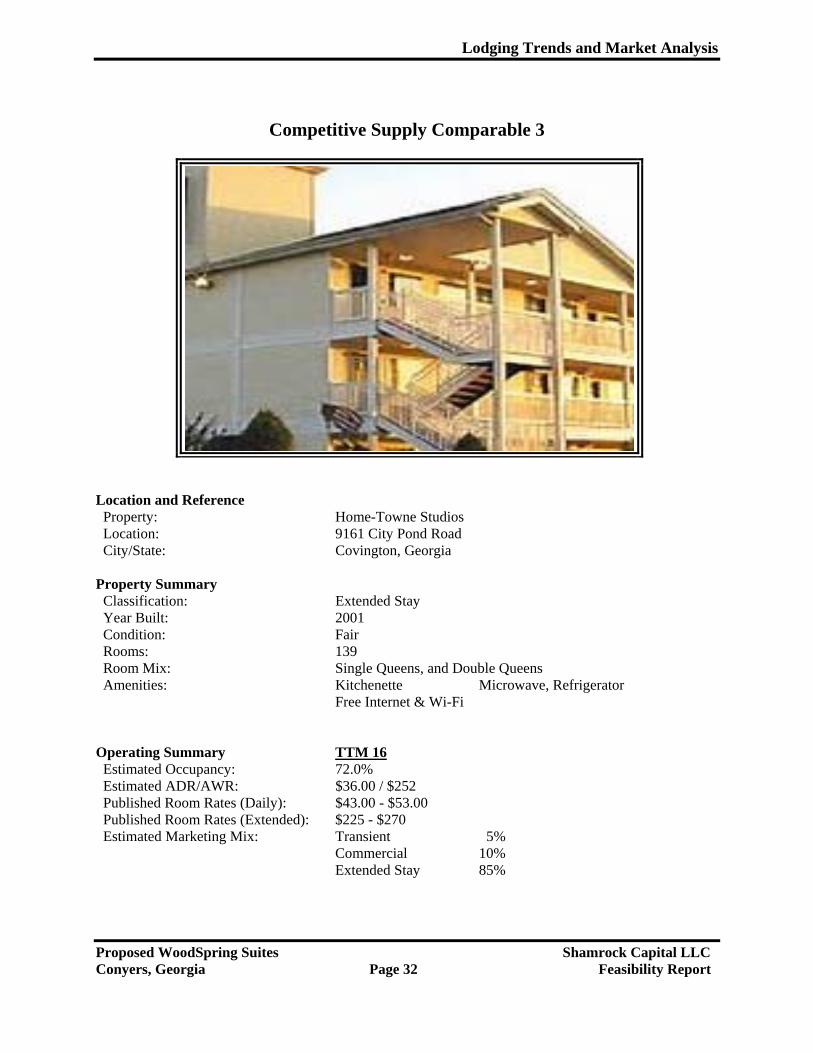

Competitive Supply Comparable 3

Location and Reference Property: Home-Towne Studios Location: 9161 City Pond Road City/State: Covington, Georgia

Property Summary Classification: Extended Stay Year Built: 2001 Condition: Fair Rooms: 139 Room Mix: Single Queens, and Double Queens Amenities: Kitchenette Microwave, Refrigerator

Free Internet & Wi-Fi

Operating Summary TTM 16 Estimated Occupancy: 72.0% Estimated ADR/AWR: $36.00 / $252 Published Room Rates (Daily): $43.00 - $53.00 Published Room Rates (Extended): $225 - $270 Estimated Marketing Mix: Transient 5%

Commercial 10%Extended Stay 85%

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 33 Feasibility Report

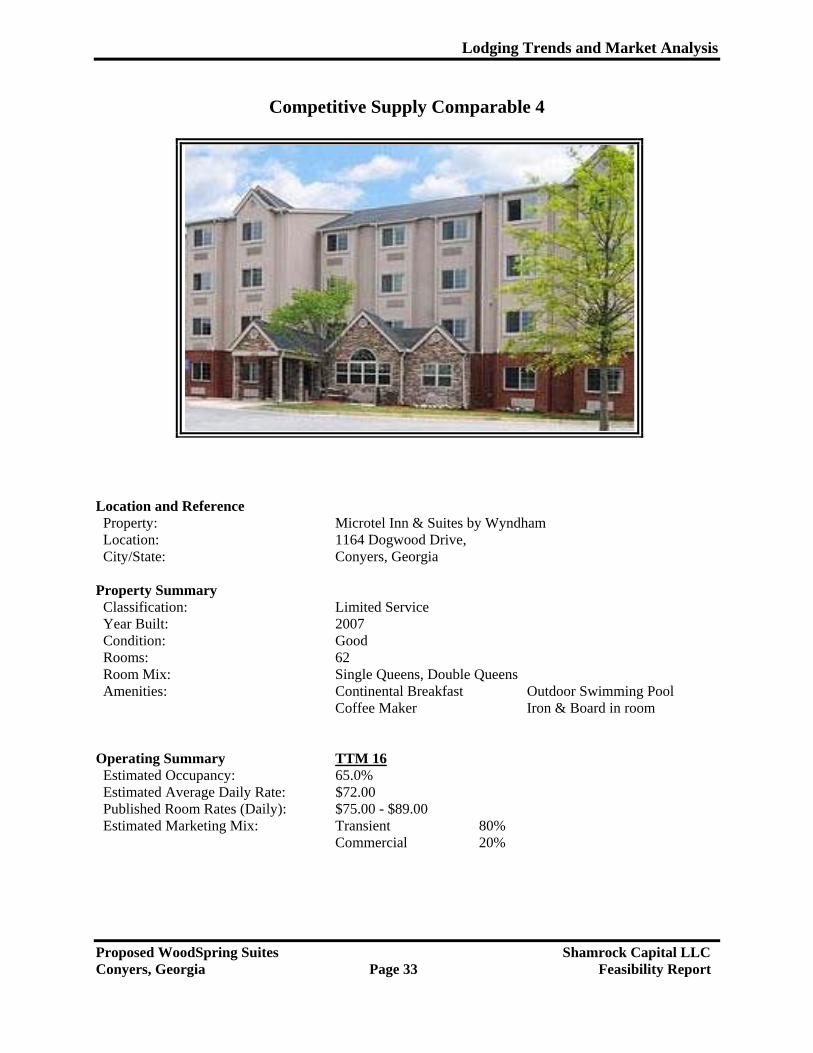

Competitive Supply Comparable 4

Location and Reference Property: Microtel Inn & Suites by Wyndham Location: 1164 Dogwood Drive, City/State: Conyers, Georgia Property Summary Classification: Limited Service Year Built: 2007 Condition: Good Rooms: 62 Room Mix: Single Queens, Double Queens Amenities: Continental Breakfast Outdoor Swimming Pool Coffee Maker Iron & Board in room

Operating Summary TTM 16 Estimated Occupancy: 65.0% Estimated Average Daily Rate: $72.00 Published Room Rates (Daily): $75.00 - $89.00 Estimated Marketing Mix: Transient 80% Commercial 20%

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 34 Feasibility Report

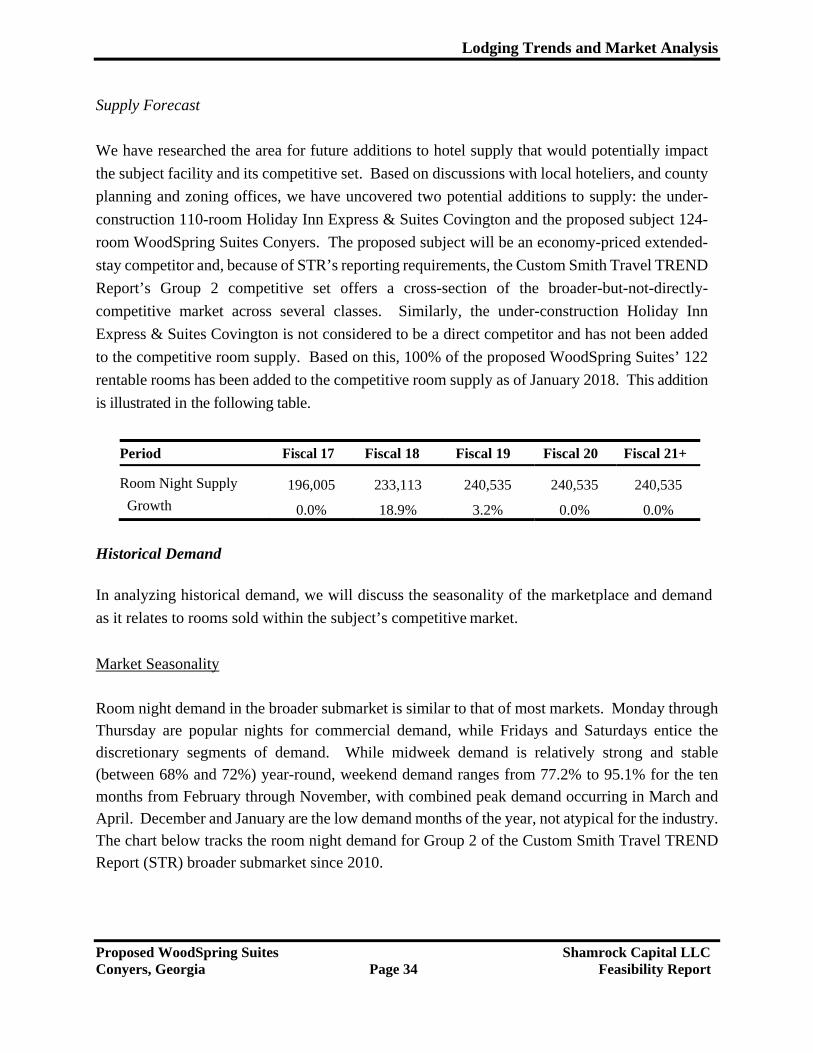

Supply Forecast

We have researched the area for future additions to hotel supply that would potentially impact

the subject facility and its competitive set. Based on discussions with local hoteliers, and county

planning and zoning offices, we have uncovered two potential additions to supply: the under-

construction 110-room Holiday Inn Express & Suites Covington and the proposed subject 124-

room WoodSpring Suites Conyers. The proposed subject will be an economy-priced extended-

stay competitor and, because of STR’s reporting requirements, the Custom Smith Travel TREND

Report’s Group 2 competitive set offers a cross-section of the broader-but-not-directly-

competitive market across several classes. Similarly, the under-construction Holiday Inn

Express & Suites Covington is not considered to be a direct competitor and has not been added

to the competitive room supply. Based on this, 100% of the proposed WoodSpring Suites’ 122

rentable rooms has been added to the competitive room supply as of January 2018. This addition

is illustrated in the following table.

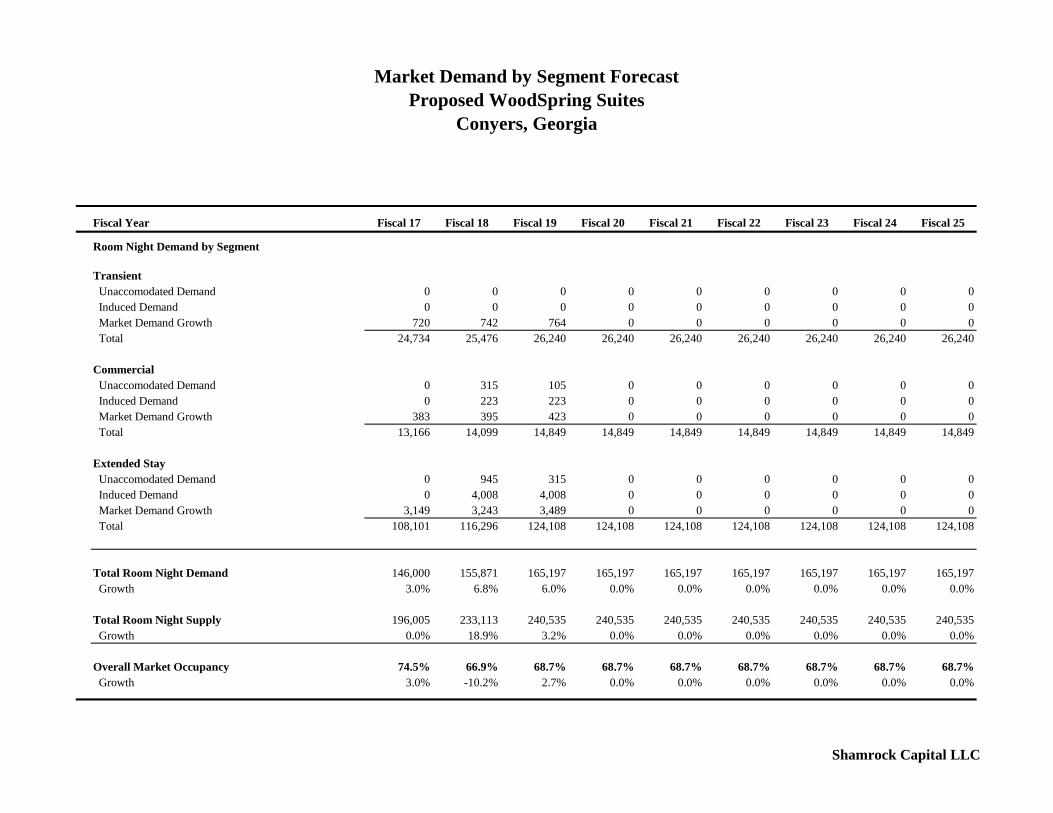

Period Fiscal 17 Fiscal 18 Fiscal 19 Fiscal 20 Fiscal 21+

Room Night Supply 196,005 233,113 240,535 240,535 240,535

Growth 0.0% 18.9% 3.2% 0.0% 0.0%

Historical Demand

In analyzing historical demand, we will discuss the seasonality of the marketplace and demand

as it relates to rooms sold within the subject’s competitive market.

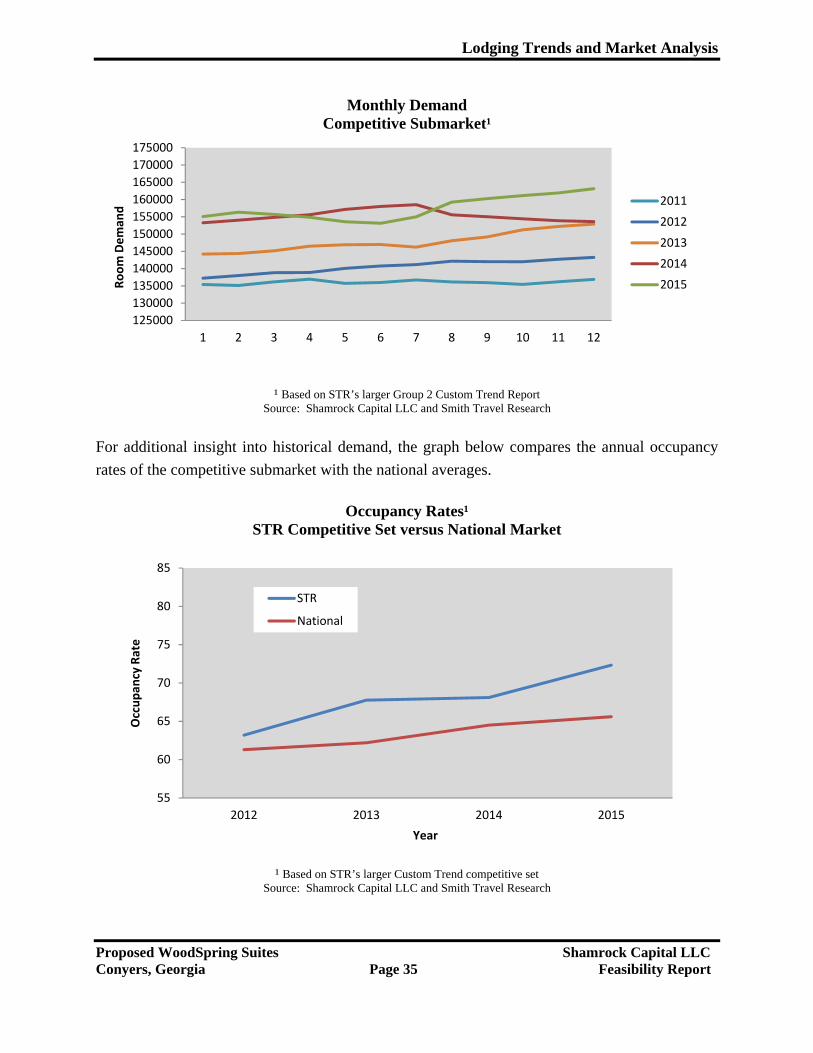

Market Seasonality

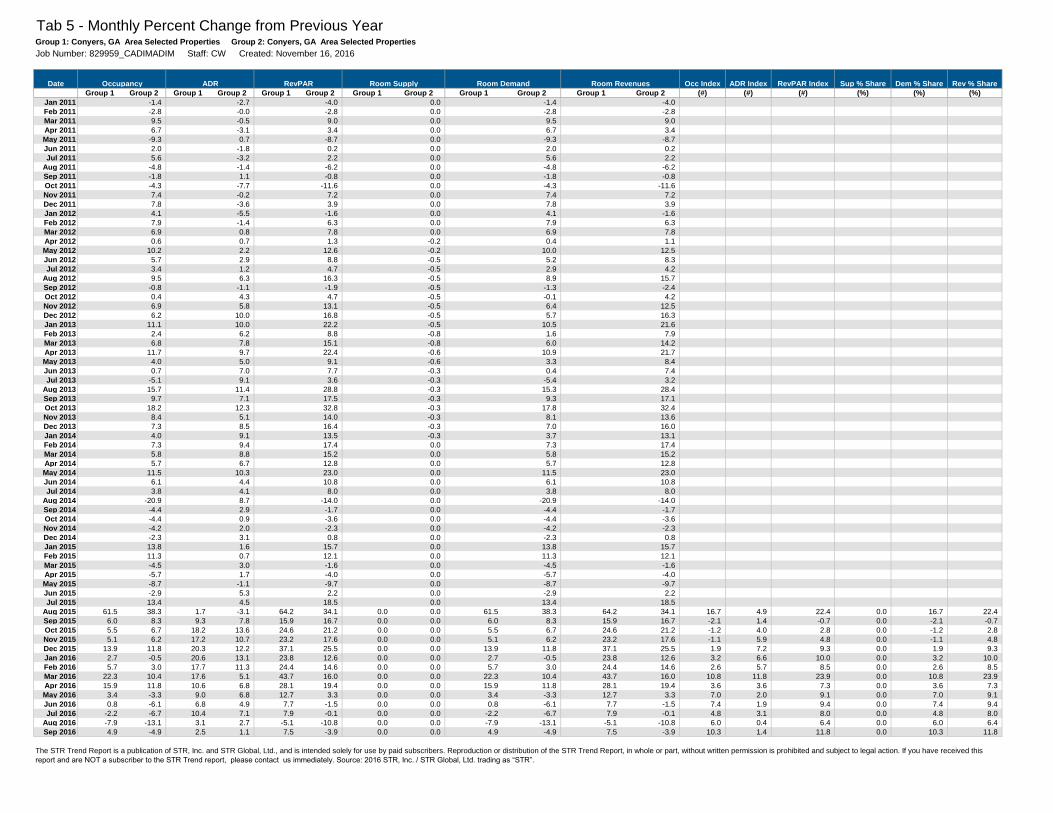

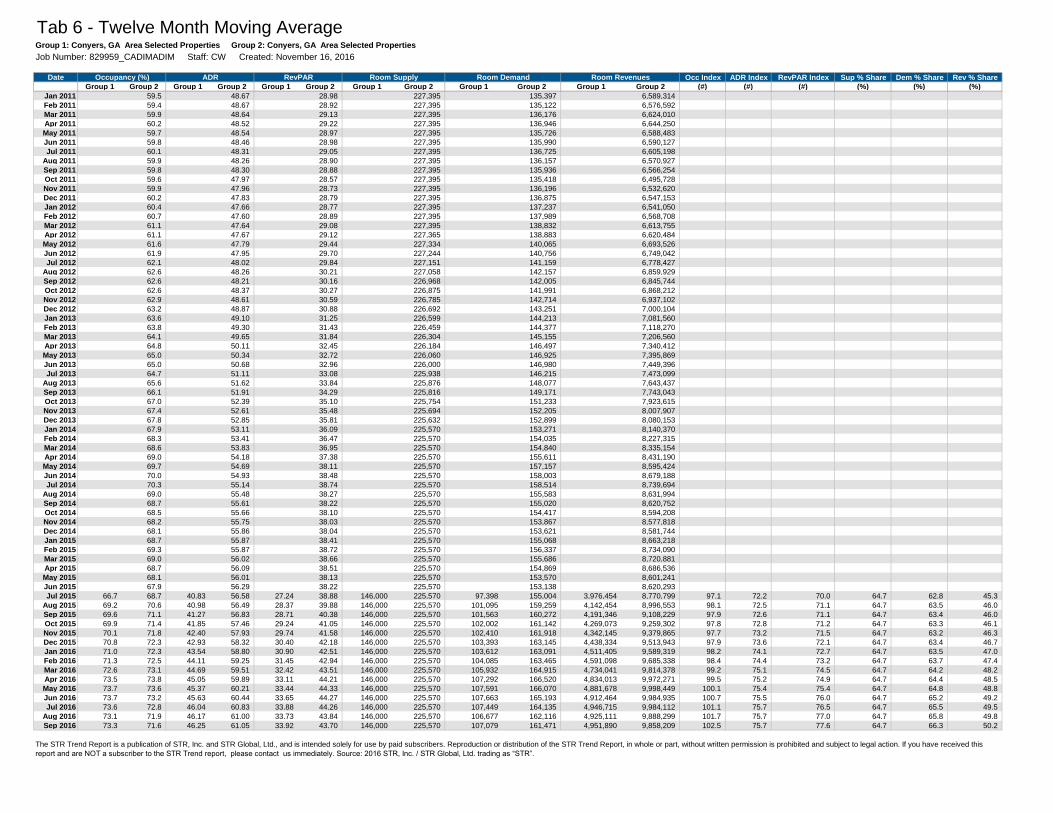

Room night demand in the broader submarket is similar to that of most markets. Monday through Thursday are popular nights for commercial demand, while Fridays and Saturdays entice the discretionary segments of demand. While midweek demand is relatively strong and stable (between 68% and 72%) year-round, weekend demand ranges from 77.2% to 95.1% for the ten months from February through November, with combined peak demand occurring in March and April. December and January are the low demand months of the year, not atypical for the industry. The chart below tracks the room night demand for Group 2 of the Custom Smith Travel TREND Report (STR) broader submarket since 2010.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 35 Feasibility Report

Monthly Demand Competitive Submarket¹

¹ Based on STR’s larger Group 2 Custom Trend Report

Source: Shamrock Capital LLC and Smith Travel Research

For additional insight into historical demand, the graph below compares the annual occupancy

rates of the competitive submarket with the national averages.

Occupancy Rates¹

STR Competitive Set versus National Market

¹ Based on STR’s larger Custom Trend competitive set

Source: Shamrock Capital LLC and Smith Travel Research

125000

130000

135000

140000

145000

150000

155000

160000

165000

170000

175000

1 2 3 4 5 6 7 8 9 10 11 12

Room Deman

d

2011

2012

2013

2014

2015

55

60

65

70

75

80

85

2012 2013 2014 2015

Occupan

cy Rate

Year

STR

National

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 36 Feasibility Report

Between 2012 and 2015 the broader Group 2 STR competitive submarket’s occupancy rate increased from 63.2% to 72.3%, a strong annual compound average growth rate increase of 4.6%. The occupancy trend for the national market has increased steadily over the same timeframe being studied and has exhibited a compound growth rate of 2.3%.

Existing Demand

The following section will analyze the market’s existing demand on the basis of the competitors’

ability to penetrate the market and their existing or accommodated demand mix.

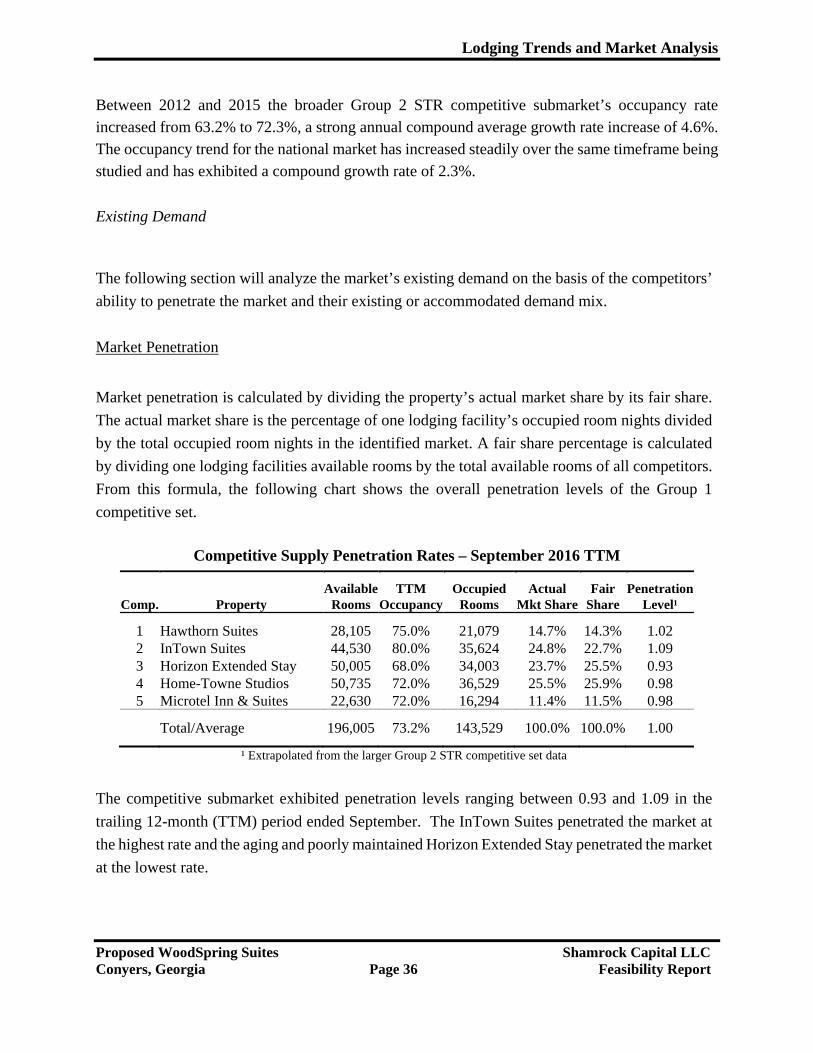

Market Penetration

Market penetration is calculated by dividing the property’s actual market share by its fair share.

The actual market share is the percentage of one lodging facility’s occupied room nights divided

by the total occupied room nights in the identified market. A fair share percentage is calculated

by dividing one lodging facilities available rooms by the total available rooms of all competitors.

From this formula, the following chart shows the overall penetration levels of the Group 1

competitive set.

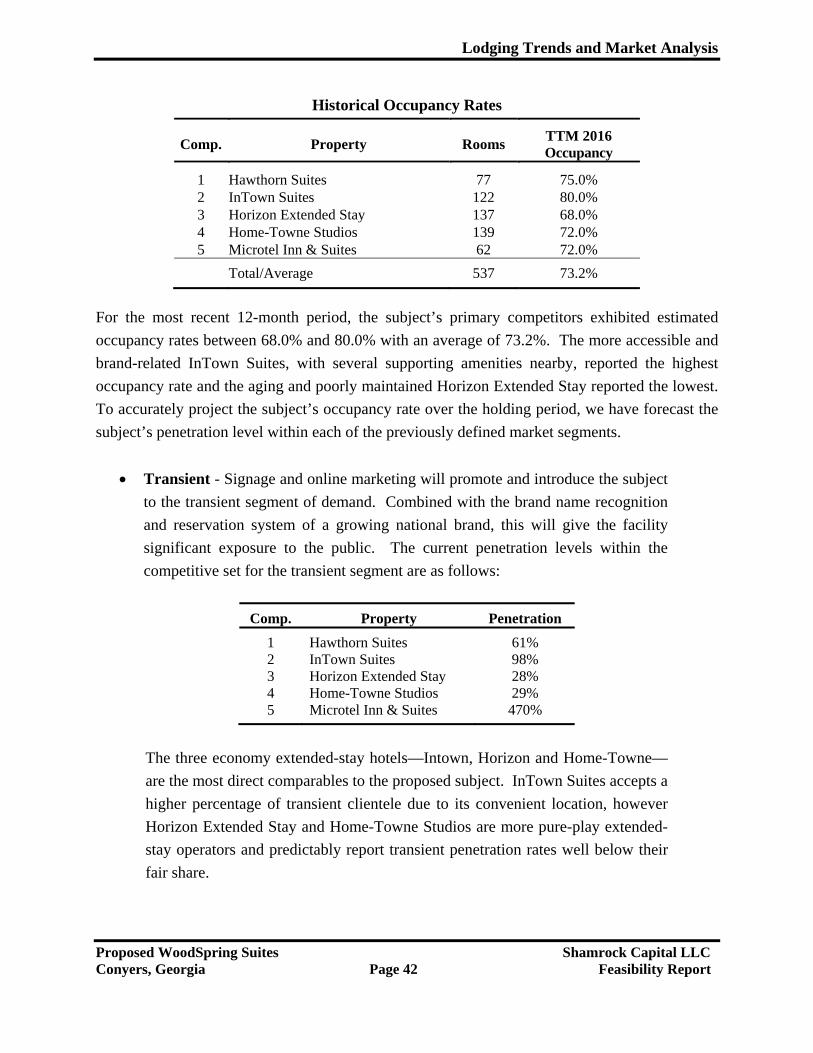

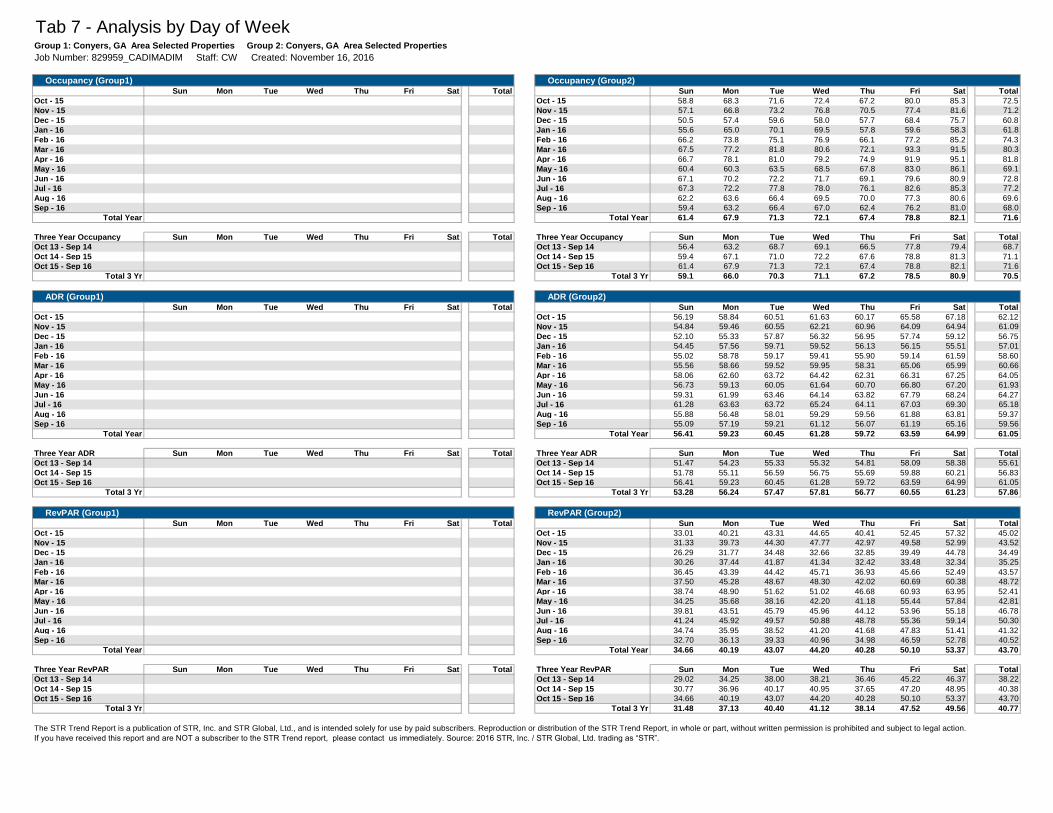

Competitive Supply Penetration Rates – September 2016 TTM

Available TTM Occupied Actual Fair PenetrationComp. Property Rooms Occupancy Rooms Mkt Share Share Level¹

1 Hawthorn Suites 28,105 75.0% 21,079 14.7% 14.3% 1.02 2 InTown Suites 44,530 80.0% 35,624 24.8% 22.7% 1.09 3 Horizon Extended Stay 50,005 68.0% 34,003 23.7% 25.5% 0.93 4 Home-Towne Studios 50,735 72.0% 36,529 25.5% 25.9% 0.98 5 Microtel Inn & Suites 22,630 72.0% 16,294 11.4% 11.5% 0.98

Total/Average 196,005 73.2% 143,529 100.0% 100.0% 1.00

¹ Extrapolated from the larger Group 2 STR competitive set data

The competitive submarket exhibited penetration levels ranging between 0.93 and 1.09 in the

trailing 12-month (TTM) period ended September. The InTown Suites penetrated the market at

the highest rate and the aging and poorly maintained Horizon Extended Stay penetrated the market

at the lowest rate.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 37 Feasibility Report

Accommodated Demand

The proposed subject’s accommodated demand may be analyzed by market segment (transient,

commercial, group, extended stay and transitional housing) by studying occupancies at

competitive properties as they relate to each segment. We have additionally conducted field and

telephone interviews with the hotel managers of the subject’s competitive set. In addition, data

taken from statistical reports and office files was also used in segmenting these properties. From

this information the market segments are then translated into estimated room nights and

occupancy percentages for each competitor as noted in the following chart.

Occupied Transient Commercial Extended StayProperty Nights Room Nights Room Nights Room Nights

Hawthorn Suites 21,079 2,108 4,216 14,755 InTown Suites 35,624 5,344 1,781 26,718 Horizon Extended Stay 34,003 1,700 1,700 30,603 Home-Towne Studios 36,529 1,826 1,826 32,876 Microtel Inn & Suites 16,294 13,035 3,259 0

Total/Average 143,529 24,013 12,782 104,952

The demand mix for the competitive submarket is approximately 16.7% transient, 8.9%

commercial, and 73.1% extended stay. It is noted that in the wake of the waste water treatment

plant moratorium, none of the competitors report significant transitional housing demand or group

demand and, as no near-term changes are expected that would generate significant demand in

these segments, they have not been considered further in this analysis.

Unaccommodated Demand

Unaccommodated demand refers to individuals who are unable to secure accommodations in the

market because all the local hotels are filled. These travelers must defer their trips, settle for less

desirable accommodations, or stay in properties located outside the market area. Because this

demand did not yield occupied room nights, it is not included in the estimate of historical

accommodated room night demand. If additional lodging facilities are expected to enter the

market, it is reasonable to assume that these guests will be able to secure hotel rooms in the future,

and it is therefore necessary to quantify this demand.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 38 Feasibility Report

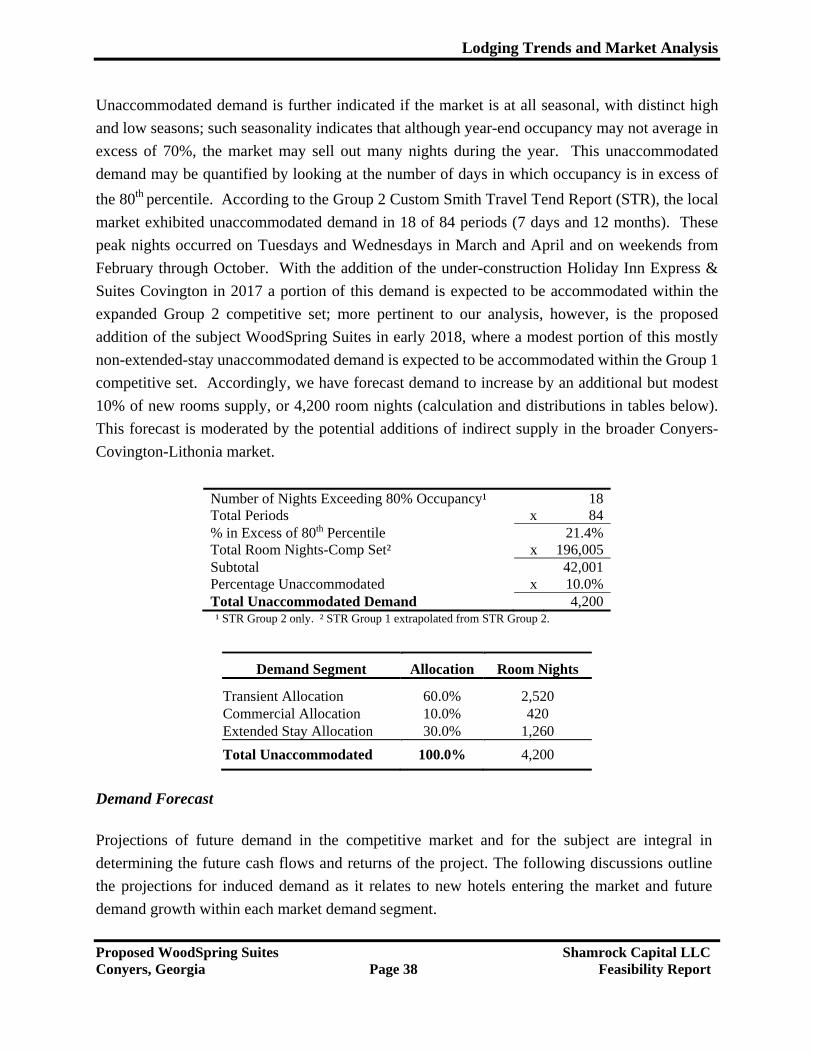

Unaccommodated demand is further indicated if the market is at all seasonal, with distinct high

and low seasons; such seasonality indicates that although year-end occupancy may not average in

excess of 70%, the market may sell out many nights during the year. This unaccommodated

demand may be quantified by looking at the number of days in which occupancy is in excess of

the 80th percentile. According to the Group 2 Custom Smith Travel Tend Report (STR), the local

market exhibited unaccommodated demand in 18 of 84 periods (7 days and 12 months). These

peak nights occurred on Tuesdays and Wednesdays in March and April and on weekends from

February through October. With the addition of the under-construction Holiday Inn Express &

Suites Covington in 2017 a portion of this demand is expected to be accommodated within the

expanded Group 2 competitive set; more pertinent to our analysis, however, is the proposed

addition of the subject WoodSpring Suites in early 2018, where a modest portion of this mostly

non-extended-stay unaccommodated demand is expected to be accommodated within the Group 1

competitive set. Accordingly, we have forecast demand to increase by an additional but modest

10% of new rooms supply, or 4,200 room nights (calculation and distributions in tables below).

This forecast is moderated by the potential additions of indirect supply in the broader Conyers-

Covington-Lithonia market.

Number of Nights Exceeding 80% Occupancy¹ 18 Total Periods x 84 % in Excess of 80th Percentile 21.4% Total Room Nights-Comp Set² x 196,005 Subtotal 42,001 Percentage Unaccommodated x 10.0% Total Unaccommodated Demand 4,200 ¹ STR Group 2 only. ² STR Group 1 extrapolated from STR Group 2.

Demand Segment Allocation Room Nights

Transient Allocation 60.0% 2,520 Commercial Allocation 10.0% 420 Extended Stay Allocation 30.0% 1,260

Total Unaccommodated 100.0% 4,200

Demand Forecast

Projections of future demand in the competitive market and for the subject are integral in

determining the future cash flows and returns of the project. The following discussions outline

the projections for induced demand as it relates to new hotels entering the market and future

demand growth within each market demand segment.

Lodging Trends and Market Analysis

Proposed WoodSpring Suites Shamrock Capital LLC Conyers, Georgia Page 39 Feasibility Report

Induced Demand

Similar to the concept of unaccommodated demand, it is apparent that the inducement of demand

occurs when a new product is added that attracts guests which previously stayed outside the

competitive set due to brand loyalty, or simply because the type of accommodations they prefer

were unavailable in the market area. The subject will be a new construction, purpose-built,

economy extended-stay hotel. Extended-stay and economy extended-stay are product types which

represent 17.9% and 15.0%, respectively, of the existing lodging inventory in the Conyers-

Covington-Lithonia market. The proposed WoodSpring Suites will offer a modern, fresh,

economy extended-stay option in a market whose direct competitors range in age from 15 to 20

years old.

Considering extended-stay hotels represent 88% of the competitive set, we have forecast the

subject to induce additional demand at a rate equal to 20% of its room supply. The allocation of

this incremental demand across all demand segments is displayed in the table below. It is noted

that transitional housing demand, which is generated from jobs growth and a shortage of housing

supply, has not been considered in this analysis due to the moratorium on new housing starts,

especially high-density apartment construction. Local officials are cautiously optimistic that