Embed Size (px)

Citation preview

FATCA– What is the impact to you?

Citi Global Banks Forum | April 18, 2012

www.pwc.com

PwC

Agenda

• Background

• What does it mean?

• How does it work?

• So what are people doing now?

• What else is going on?

This document was not intended or written to be used, and it cannot be used, for the purpose of avoiding US Federal, state or local tax penalties.

April 2012 1

FATCA–What is the impact to you?

PwC

Background

April 2012

2

FATCA–What is the impact to you?

PwC

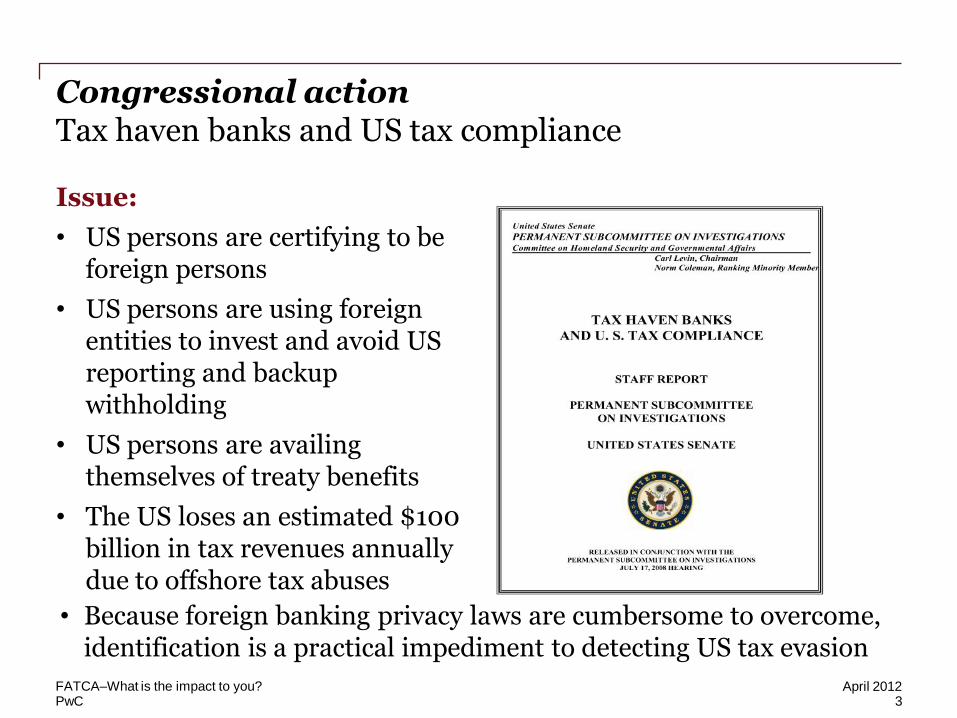

Congressional action Tax haven banks and US tax compliance

Issue:

• US persons are certifying to be foreign persons

• US persons are using foreign entities to invest and avoid US reporting and backup withholding

• US persons are availing themselves of treaty benefits

• The US loses an estimated $100 billion in tax revenues annually due to offshore tax abuses

3 April 2012 FATCA–What is the impact to you?

• Because foreign banking privacy laws are cumbersome to overcome, identification is a practical impediment to detecting US tax evasion

PwC

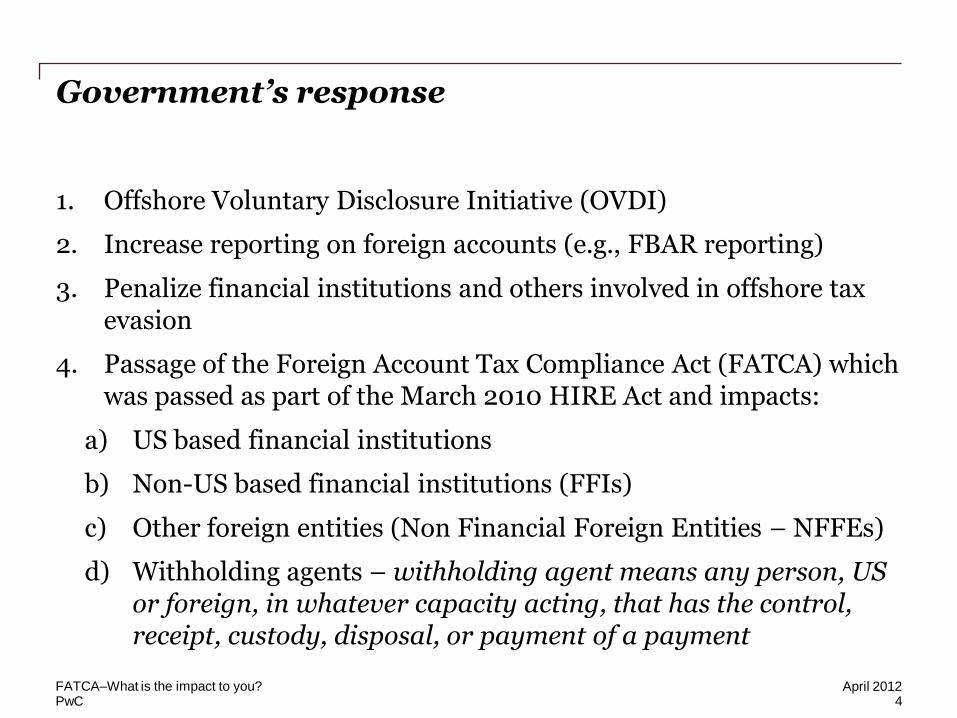

Government’s response 1. Offshore Voluntary Disclosure Initiative (OVDI)

2. Increase reporting on foreign accounts (e.g., FBAR reporting)

3. Penalize financial institutions and others involved in offshore tax evasion

4. Passage of the Foreign Account Tax Compliance Act (FATCA) which was passed as part of the March 2010 HIRE Act and impacts:

a) US based financial institutions

b) Non-US based financial institutions (FFIs)

c) Other foreign entities (Non Financial Foreign Entities – NFFEs)

d) Withholding agents – withholding agent means any person, US or foreign, in whatever capacity acting, that has the control, receipt, custody, disposal, or payment of a payment

April 2012 4

FATCA–What is the impact to you?

PwC

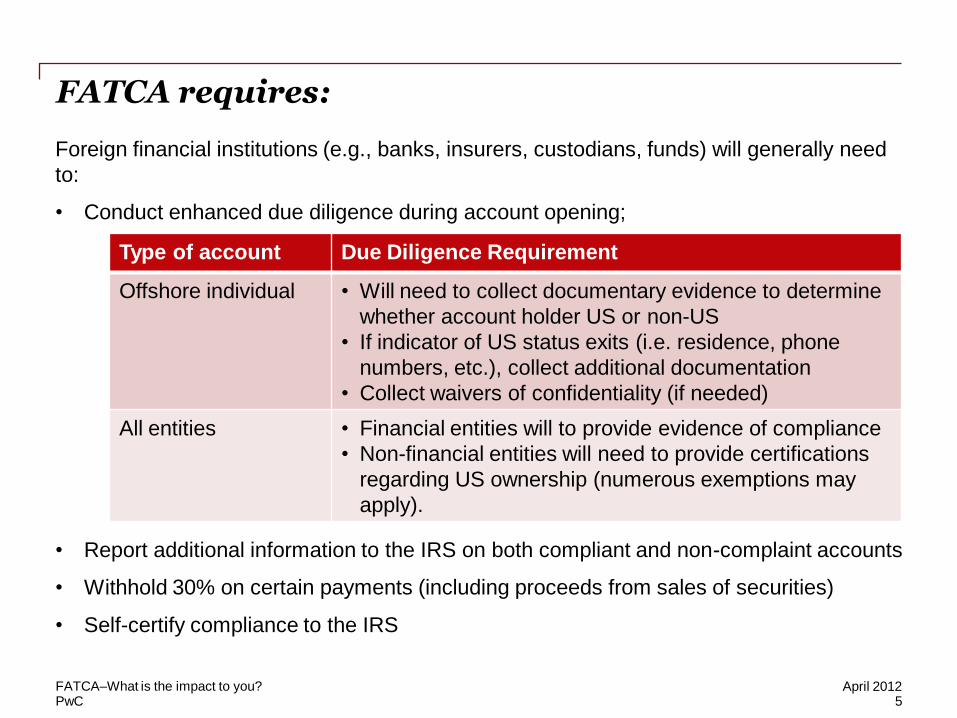

Foreign financial institutions (e.g., banks, insurers, custodians, funds) will generally need

to:

• Conduct enhanced due diligence during account opening;

• Report additional information to the IRS on both compliant and non-complaint accounts

• Withhold 30% on certain payments (including proceeds from sales of securities)

• Self-certify compliance to the IRS

FATCA requires:

April 2012 5

FATCA–What is the impact to you?

Type of account Due Diligence Requirement

Offshore individual • Will need to collect documentary evidence to determine

whether account holder US or non-US

• If indicator of US status exits (i.e. residence, phone

numbers, etc.), collect additional documentation

• Collect waivers of confidentiality (if needed)

All entities • Financial entities will to provide evidence of compliance

• Non-financial entities will need to provide certifications

regarding US ownership (numerous exemptions may

apply).

PwC

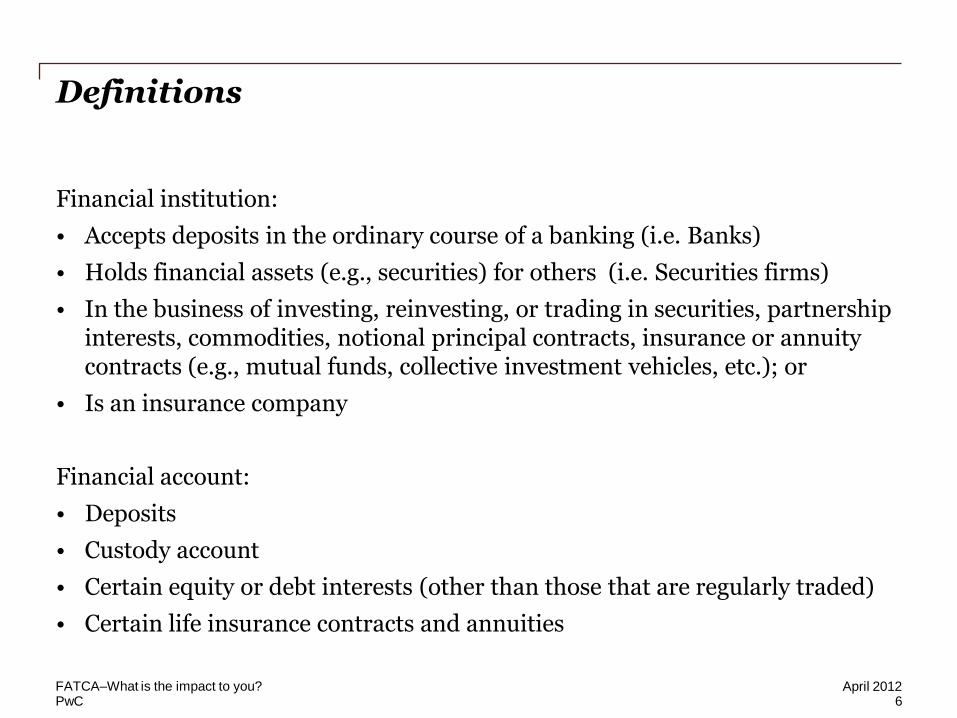

Definitions

Financial institution:

• Accepts deposits in the ordinary course of a banking (i.e. Banks)

• Holds financial assets (e.g., securities) for others (i.e. Securities firms)

• In the business of investing, reinvesting, or trading in securities, partnership interests, commodities, notional principal contracts, insurance or annuity contracts (e.g., mutual funds, collective investment vehicles, etc.); or

• Is an insurance company

Financial account:

• Deposits

• Custody account

• Certain equity or debt interests (other than those that are regularly traded)

• Certain life insurance contracts and annuities

6 April 2012 FATCA–What is the impact to you?

PwC

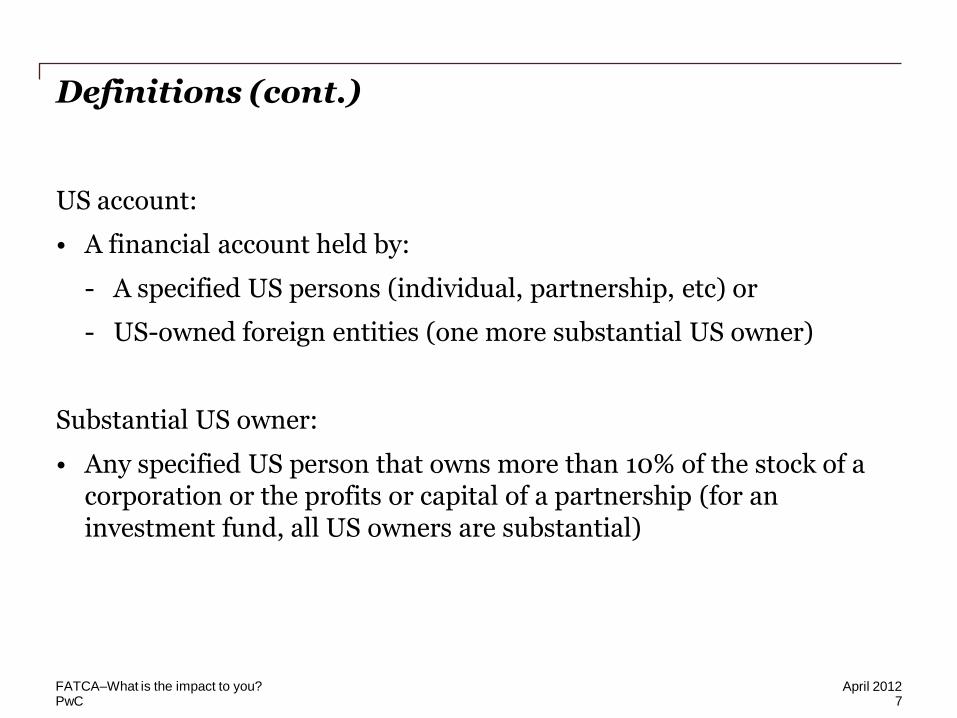

Definitions (cont.)

US account:

• A financial account held by:

- A specified US persons (individual, partnership, etc) or

- US-owned foreign entities (one more substantial US owner)

Substantial US owner:

• Any specified US person that owns more than 10% of the stock of a corporation or the profits or capital of a partnership (for an investment fund, all US owners are substantial)

7 April 2012 FATCA–What is the impact to you?

PwC

What does it mean?

April 2012 FATCA–What is the impact to you?

8

PwC

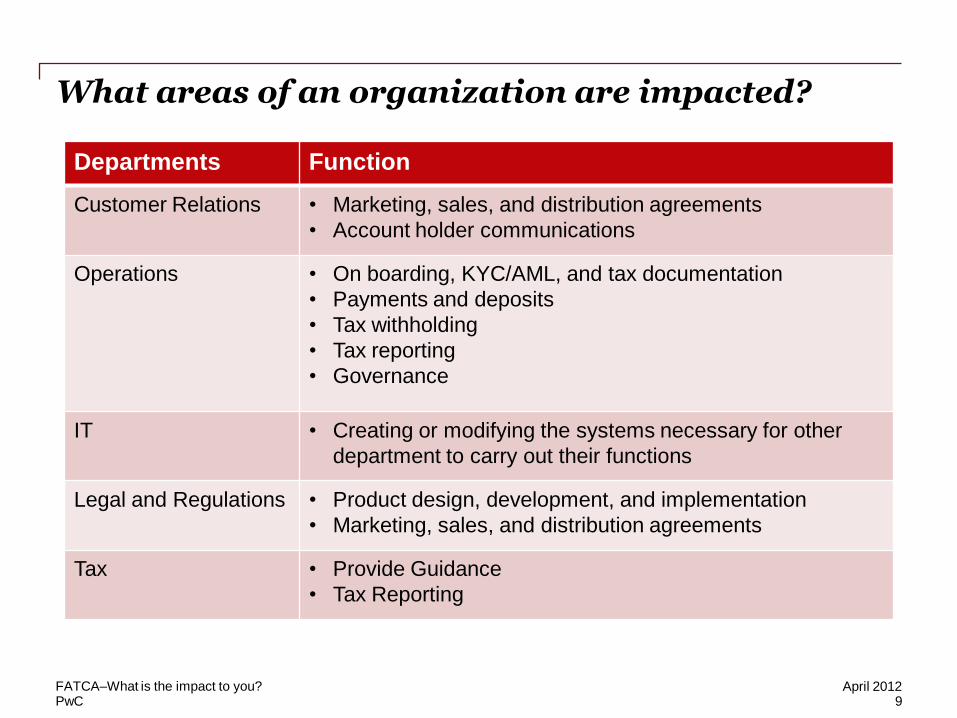

What areas of an organization are impacted?

9 April 2012 FATCA–What is the impact to you?

Departments Function

Customer Relations • Marketing, sales, and distribution agreements

• Account holder communications

Operations • On boarding, KYC/AML, and tax documentation

• Payments and deposits

• Tax withholding

• Tax reporting

• Governance

IT • Creating or modifying the systems necessary for other

department to carry out their functions

Legal and Regulations • Product design, development, and implementation

• Marketing, sales, and distribution agreements

Tax • Provide Guidance

• Tax Reporting

PwC

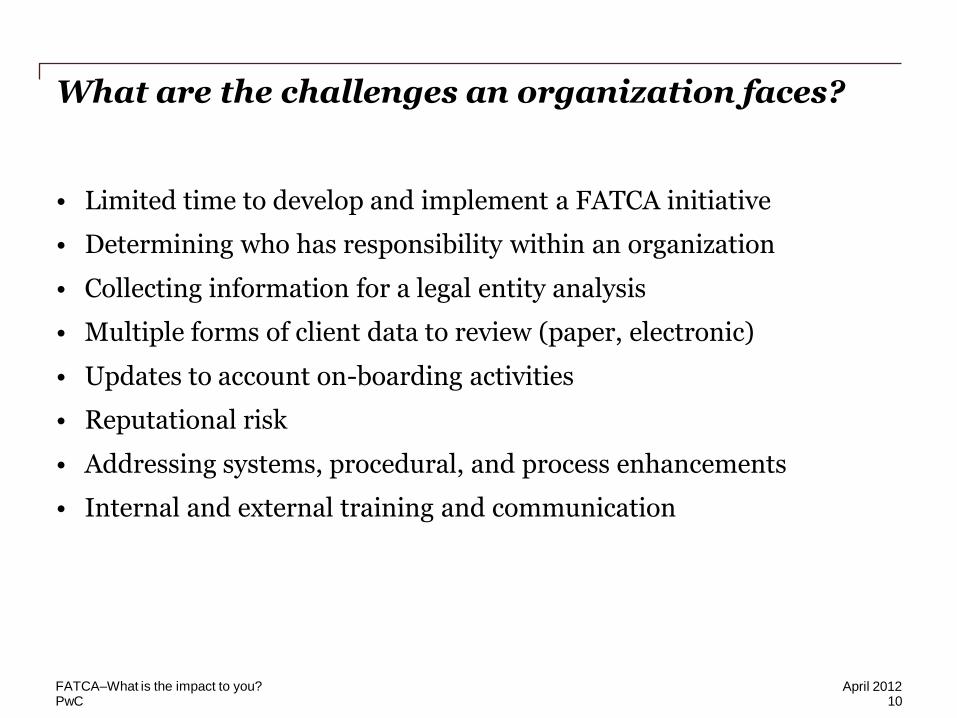

What are the challenges an organization faces?

• Limited time to develop and implement a FATCA initiative

• Determining who has responsibility within an organization

• Collecting information for a legal entity analysis

• Multiple forms of client data to review (paper, electronic)

• Updates to account on-boarding activities

• Reputational risk

• Addressing systems, procedural, and process enhancements

• Internal and external training and communication

April 2012 10

FATCA–What is the impact to you?

PwC

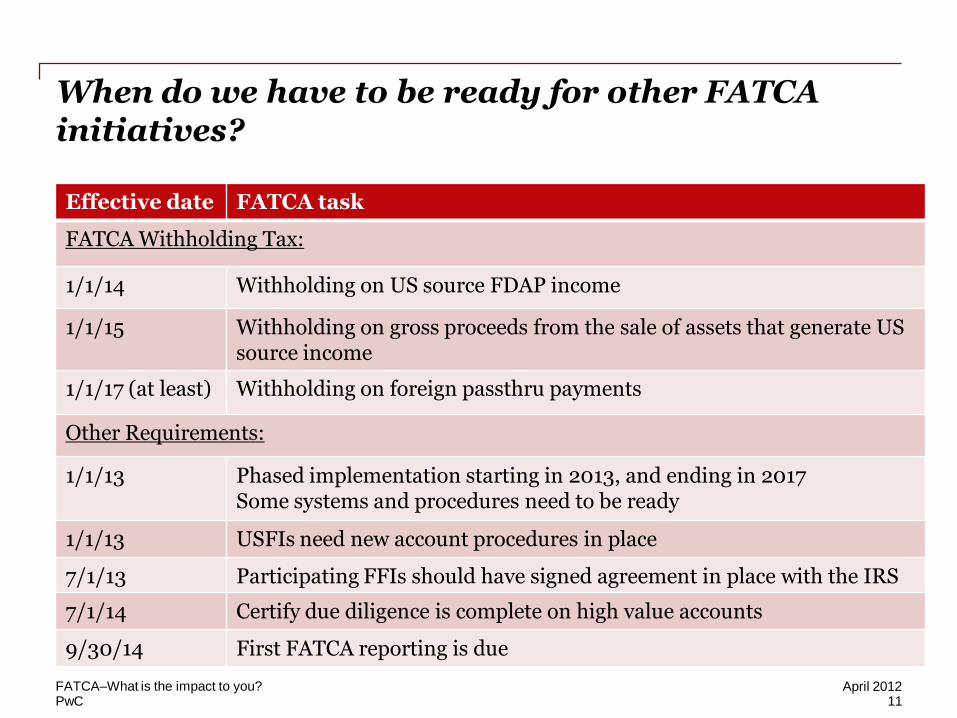

When do we have to be ready for other FATCA initiatives?

Effective date FATCA task

FATCA Withholding Tax:

1/1/14 Withholding on US source FDAP income

1/1/15 Withholding on gross proceeds from the sale of assets that generate US source income

1/1/17 (at least) Withholding on foreign passthru payments

Other Requirements:

1/1/13 Phased implementation starting in 2013, and ending in 2017 Some systems and procedures need to be ready

1/1/13 USFIs need new account procedures in place

7/1/13 Participating FFIs should have signed agreement in place with the IRS

7/1/14 Certify due diligence is complete on high value accounts

9/30/14 First FATCA reporting is due

11 April 2012 FATCA–What is the impact to you?

PwC

How does it work?

April 2012 FATCA–What is the impact to you?

12

PwC

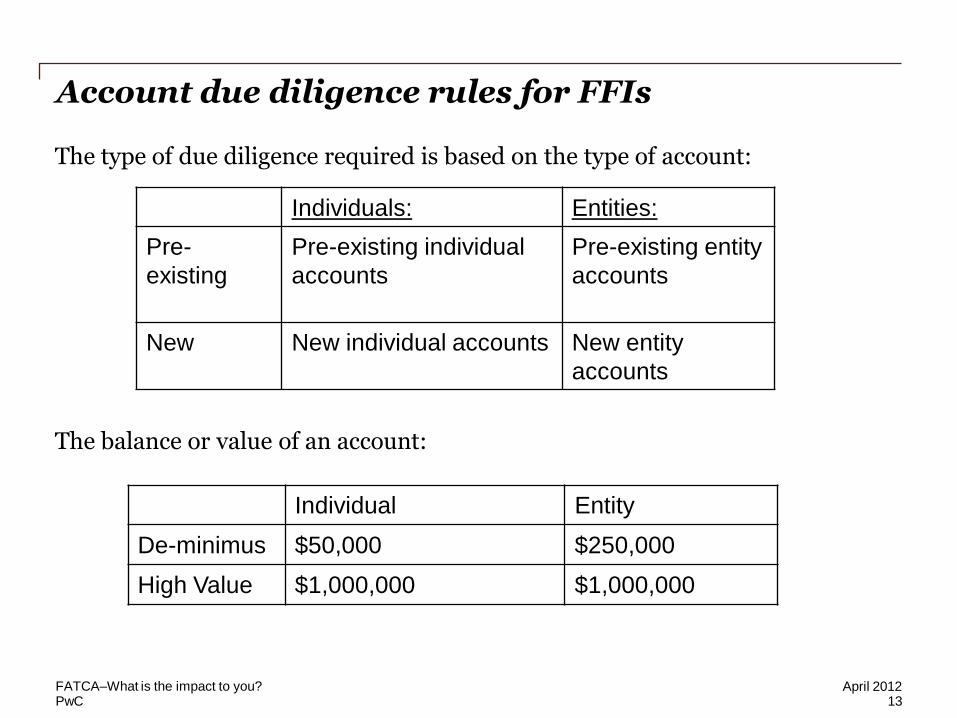

Account due diligence rules for FFIs The type of due diligence required is based on the type of account:

The balance or value of an account:

13 April 2012 FATCA–What is the impact to you?

Individuals: Entities:

Pre-

existing

Pre-existing individual

accounts

Pre-existing entity

accounts

New New individual accounts New entity

accounts

Individual Entity

De-minimus $50,000 $250,000

High Value $1,000,000 $1,000,000

PwC

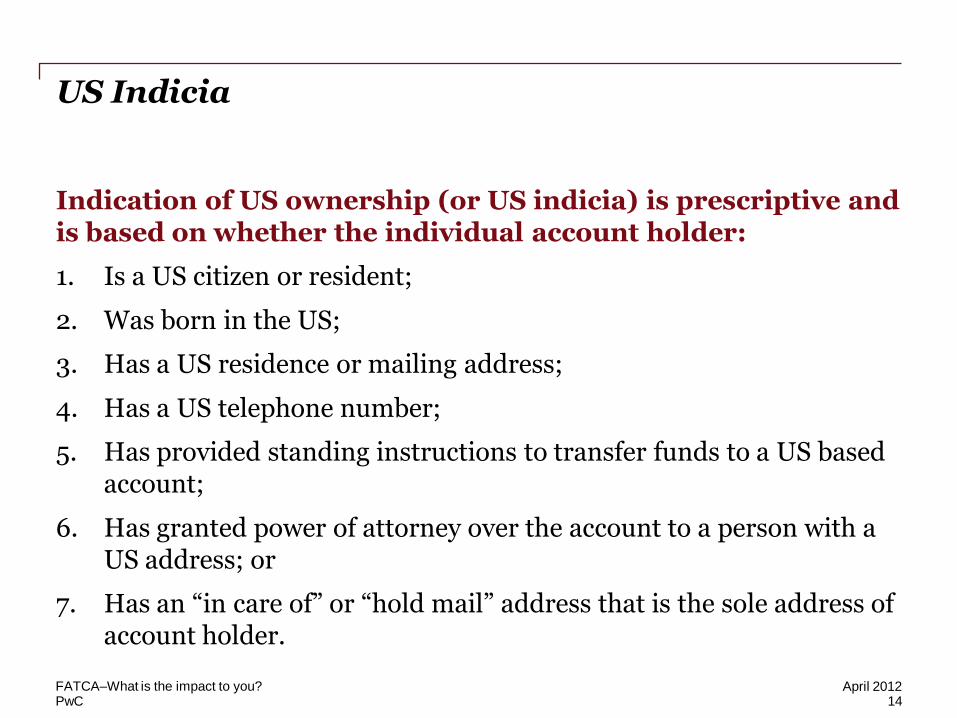

US Indicia

Indication of US ownership (or US indicia) is prescriptive and is based on whether the individual account holder:

1. Is a US citizen or resident;

2. Was born in the US;

3. Has a US residence or mailing address;

4. Has a US telephone number;

5. Has provided standing instructions to transfer funds to a US based account;

6. Has granted power of attorney over the account to a person with a US address; or

7. Has an “in care of” or “hold mail” address that is the sole address of account holder.

14 April 2012 FATCA–What is the impact to you?

PwC

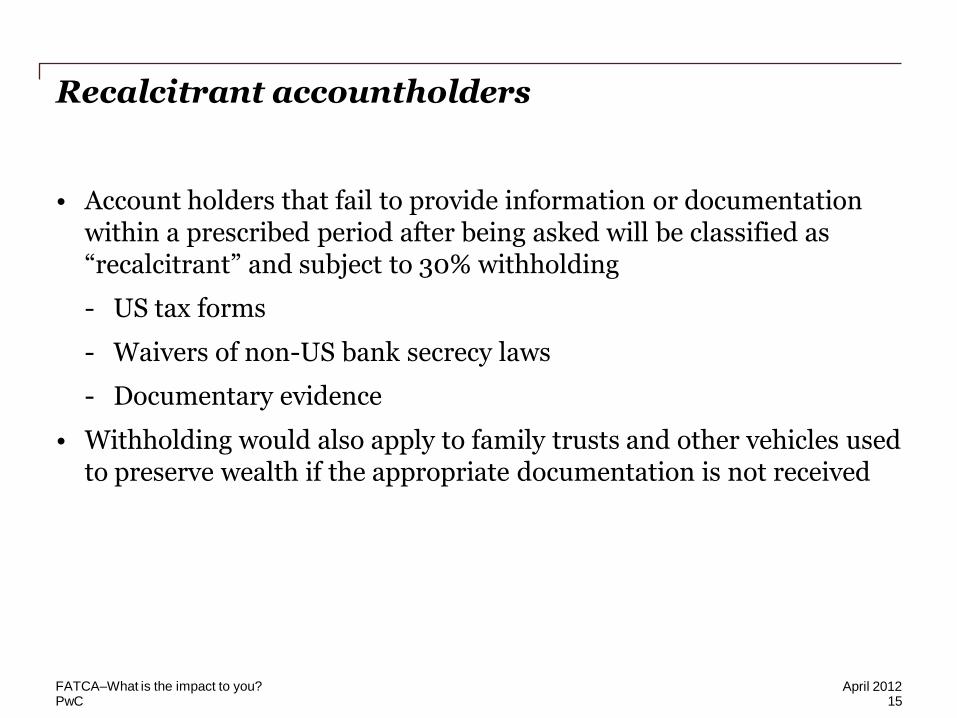

Recalcitrant accountholders

• Account holders that fail to provide information or documentation within a prescribed period after being asked will be classified as “recalcitrant” and subject to 30% withholding

- US tax forms

- Waivers of non-US bank secrecy laws

- Documentary evidence

• Withholding would also apply to family trusts and other vehicles used to preserve wealth if the appropriate documentation is not received

April 2012 15

FATCA–What is the impact to you?

PwC

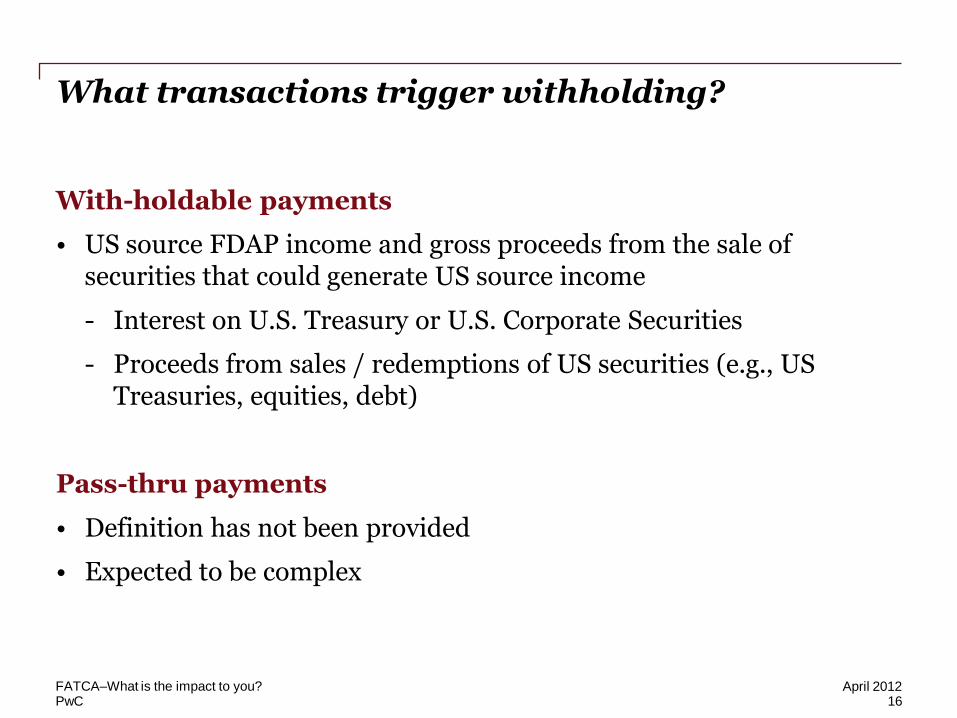

What transactions trigger withholding?

With-holdable payments

• US source FDAP income and gross proceeds from the sale of securities that could generate US source income

- Interest on U.S. Treasury or U.S. Corporate Securities

- Proceeds from sales / redemptions of US securities (e.g., US Treasuries, equities, debt)

Pass-thru payments

• Definition has not been provided

• Expected to be complex

April 2012 16

FATCA–What is the impact to you?

PwC

Verification of compliance

• Standards and procedures to be developed by IRS in draft FFI Agreement (pending publication)

• A self-certification model with phased dates

- One-time certification asserting no practices exist to assist clients in avoiding identification

- One-time certification regarding the review of pre-existing high-value accounts

- One-time certification regarding the review of all other pre-existing accounts

- Ongoing certifications of compliance with terms of FFI agreement, and to provide information to IRS upon request

17 April 2012 FATCA–What is the impact to you?

PwC

Potentially less impacted entities

Certified deemed compliant FFIs

Certified deemed compliant FFIs include local banks, certain retirement funds, certain non-profits and FFIs with only low-value accounts. Certification needs to be made to withholding agents only.

Registered deemed compliant FFIs

Registered deemed compliant FFIs include non-reporting members of FFI groups, qualified collective investment vehicles and restricted funds. Initial registration required with IRS, and re-certification with IRS required every three years.

Owner documented FFIs

Family owned trusts, personal investment companies

April 2012 18

FATCA–What is the impact to you?

PwC

So what are people doing now?

April 2012 FATCA–What is the impact to you?

19

PwC

What should we expect?

• FATCA will require more documents to be collected from clients

• Relationship managers will have more responsibility for compliance

• Doing it wrong can cause reputational risk

• Withholding should not apply except in situations where customers do not adequately respond to requests for information or documentation, or where a customer is a non-participating FFI

• Increased US tax reporting of US persons’ income and assets

April 2012 20

FATCA–What is the impact to you?

IRS expects to collect little revenue from FATCA withholding tax – intent is to

generate revenue through enhanced disclosure of US persons

PwC

US tax consequences for customers

• Account holders who have been properly reporting income and paying US taxes should not owe any additional or back taxes as a result of FATCA

• If an account holder has underreported income in an account or from assets now reported under FATCA, it may face increased audit scrutiny and additional US tax (and possibly interest and penalties) could be assessed

• Prospectively, the income will be reported to the US

April 2012 21

FATCA–What is the impact to you?

PwC

What else is going on?

April 2012 FATCA–What is the impact to you?

22

PwC

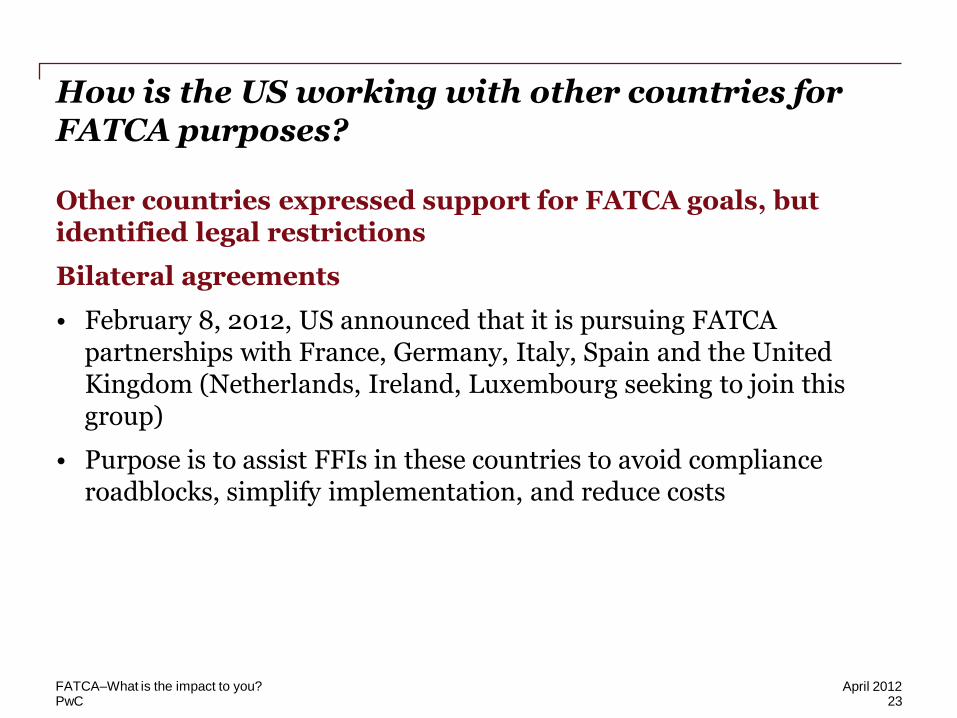

How is the US working with other countries for FATCA purposes?

Other countries expressed support for FATCA goals, but identified legal restrictions

Bilateral agreements

• February 8, 2012, US announced that it is pursuing FATCA partnerships with France, Germany, Italy, Spain and the United Kingdom (Netherlands, Ireland, Luxembourg seeking to join this group)

• Purpose is to assist FFIs in these countries to avoid compliance roadblocks, simplify implementation, and reduce costs

23 April 2012 FATCA–What is the impact to you?

PwC

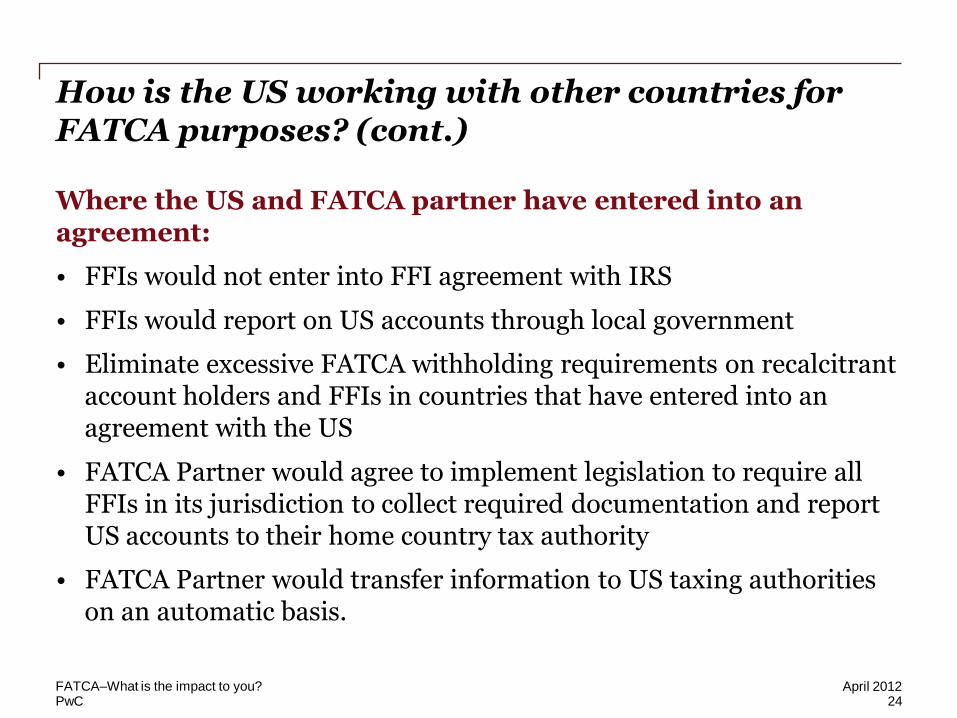

How is the US working with other countries for FATCA purposes? (cont.)

Where the US and FATCA partner have entered into an agreement:

• FFIs would not enter into FFI agreement with IRS

• FFIs would report on US accounts through local government

• Eliminate excessive FATCA withholding requirements on recalcitrant account holders and FFIs in countries that have entered into an agreement with the US

• FATCA Partner would agree to implement legislation to require all FFIs in its jurisdiction to collect required documentation and report US accounts to their home country tax authority

• FATCA Partner would transfer information to US taxing authorities on an automatic basis.

24 April 2012 FATCA–What is the impact to you?

PwC

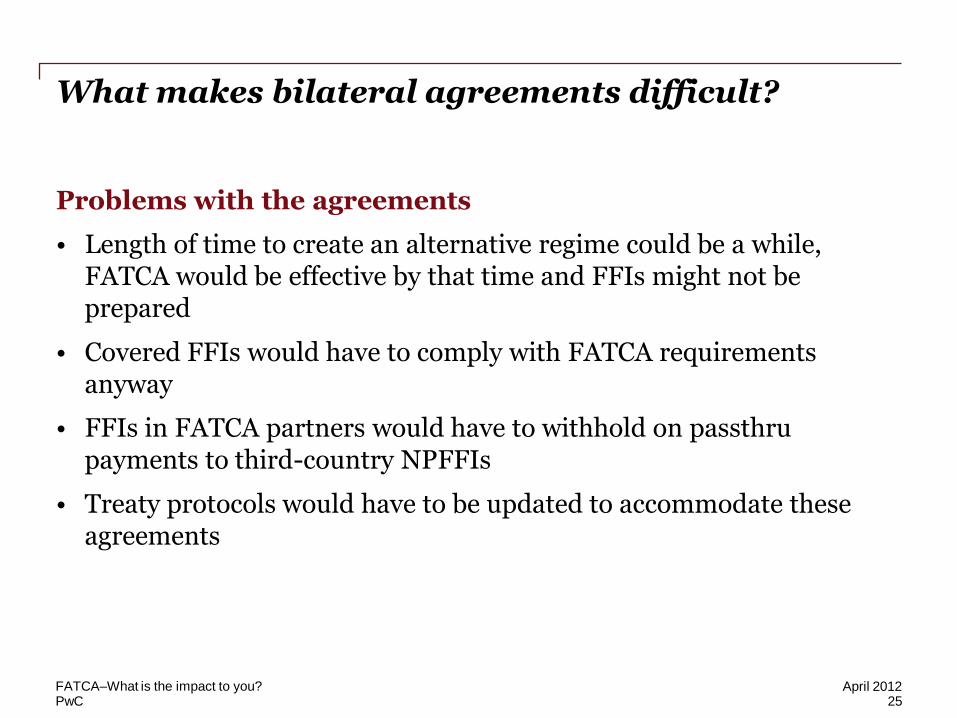

What makes bilateral agreements difficult?

Problems with the agreements

• Length of time to create an alternative regime could be a while, FATCA would be effective by that time and FFIs might not be prepared

• Covered FFIs would have to comply with FATCA requirements anyway

• FFIs in FATCA partners would have to withhold on passthru payments to third-country NPFFIs

• Treaty protocols would have to be updated to accommodate these agreements

25 April 2012 FATCA–What is the impact to you?

PwC

What makes bilateral agreements difficult? (cont.)

What are other countries expecting from US financial institutions

• US open to adopting intergovernmental approach to FATCA

• Common approach reached between countries

• FFIs would report FATCA information to their own country

- FATCA partner would report FATCA information to the US

- US commits to reciprocity in collecting information and reporting to FATCA partner

• Alternative regime based on automatic exchange authorized in existing bilateral tax treaties

26 April 2012 FATCA–What is the impact to you?

This presentation has been prepared for general guidance on matters of interest only, and

does not constitute professional advice. You should not act upon the information contained in

this publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights

reserved. PwC refers to the US member firm, and may sometimes refer to the PwC network.

Each member firm is a separate legal entity. Please see www.pwc.com/structure for further

details. This content is for general information purposes only, and should not be used as a

substitute for consultation with professional advisors.

Solicitation