Embed Size (px)

Citation preview

FASB Taxonomy Advisory Group Meeting

With Highlights

Date: February 14, 2013 Location: Web Conference

FINANCIAL ACCOUNTING STANDARDS BOARD

2

Table of Contents I. Agenda ................................................................................................................................................................. 3

II. Sessions and Highlights ....................................................................................................................................... 4

Session 1 - DRAFT 2013 XBRL Plan ........................................................................................................................... 4

A. DRAFT 2013 XBRL Plan ................................................................................................................................ 4

B. Meeting Highlights ...................................................................................................................................... 4

Session 2 - Workflow Criteria .................................................................................................................................. 5

A. Issue ............................................................................................................................................................. 5

B. Workflow Chart Decision Tree .................................................................................................................... 5

C. Meeting Highlights ...................................................................................................................................... 6

Session 3 - Legal Entity/Consolidation Axis ............................................................................................................. 7

A. Issue ............................................................................................................................................................. 7

B. Meeting Highlights ...................................................................................................................................... 7

Session 4 - Implementation Guides ......................................................................................................................... 8

A. Segments ..................................................................................................................................................... 8

B. Other Implementation Guides in Draft Form ............................................................................................. 8

C. Meeting Highlights ...................................................................................................................................... 9

Session 5 - ASU Status ............................................................................................................................................ 10

A. Summary of ASUs and EITFs ..................................................................................................................... 10

B. Meeting Highlights .................................................................................................................................... 11

Session 6 - Calendar ............................................................................................................................................... 12

A. Issue ........................................................................................................................................................... 12

B. TAG 2013 Meeting Calendar ..................................................................................................................... 12

C. Meeting Highlights .................................................................................................................................... 12

Session 7 - Review of November 15, 2012 meeting .............................................................................................. 13

A. Issue ........................................................................................................................................................... 13

B. Meeting Highlights .................................................................................................................................... 13

III. Appendix I – Attendance................................................................................................................................... 14

FINANCIAL ACCOUNTING STANDARDS BOARD

3

I. Agenda

Session Presenter

1. 2013 Plan Louis

2. Workflow criteria David

3. Legal Entity/Consolidation Axis – preliminary discussion Campbell

4. Implementation Guides

a. Segments Meredith

b. Insurance Donna

c. OCI Meredith

d. Oil & Gas/Fair Value Vickie

5. ASU Status Donna

a. Repurchase Agreements David

6. Calendar Donna

7. Review of item resolution from November 15, 2012 meeting Donna

FINANCIAL ACCOUNTING STANDARDS BOARD

4

II. Sessions and Highlights

TAG discussed DRAFT 2013 plan for the XBRL team and reviewed ASU integration, data quality improvements,

goal of stability, outreach efforts and change management requirements. Further actions are to set priorities,

assign responsibilities and timing.

Session 1 - DRAFT 2013 XBRL Plan

A. DRAFT 2013 XBRL Plan

B. Meeting Highlights

DRAFT XBRL plan for 2013 was reviewed along with a process to evaluate workflows. The status of the

Implementation Guides and Accounting Standards Updates were also reviewed and further discussion on certain

issues within the Segment guide will be required. An issue regarding category of legal entity was discussed.

FINANCIAL ACCOUNTING STANDARDS BOARD

5

Session 2 - Workflow Criteria

A. Issue

In the interests of promoting stability in the taxonomy, a process for evaluating workflows was proposed for

comment. The criteria for change include materiality and cost/benefit considerations.

B. Workflow Chart Decision Tree

FINANCIAL ACCOUNTING STANDARDS BOARD

6

C. Meeting Highlights

TAG members were shown a draft of the workflow decision tree with a brief walkthrough of the steps involved.

The document is still in draft and certain terms and phrases are still being worked out. Further action to refine

the criteria for decision points regarding materiality, cost/benefit analysis, and list of known areas were not

addressed. An update will be provided at a future TAG meeting.

FINANCIAL ACCOUNTING STANDARDS BOARD

7

Session 3 - Legal Entity/Consolidation Axis

A. Issue

The legal entity axis is used for the name of the entity and for the type of entity such as consolidated, joint

venture, and partnership interest. What is the impact to users of the data? Is it helpful to know whether an entity

is included in the consolidation or not?

B. Meeting Highlights

Discussions indicate that the information to separate these concepts is valuable. The Legal Entity [Axis] is part of

the dei group and cannot be altered by the FASB XBRL team. Further research will be needed to determine if this

is a significant issue and the best course of action.

FINANCIAL ACCOUNTING STANDARDS BOARD

8

Session 4 - Implementation Guides

A. Segments

1. “SegmentImplementationGuide_02082013” version has been updated based on the feedback and suggestion

received from TAG during the TAG comment period (ends January 25th).

2. The XBRL team would like to solicit the TAG’s input regarding the two issues below that were raised by TAG

members:

a. “Example 5—Reconciliation of Segment Revenue by Geographic Area” provides preparers a more

complicated segment modeling structure of “Geographical [Axis]” – the geographic information further

broken down by segments. The goal is that when filers model a simplified disclosure, they can interpret

the appropriate modeling structure based on this example. Comments have been submitted by TAG

members that additional examples may be helpful in terms of clarifying the preferred usage of

“Geographical [Axis]” and/or “Segments [Axis]” and their members. Suggested disclosures have been

proposed such as 1) consolidated company information by geography or 2) a company’s segments are the

same as its geographies (e.g. segment A is Asia Pacific, segment B is EMEA).

Do you think additional modeling examples of segment geographic disclosures will be helpful? If yes,

what disclosure you would like to be included in the Segment Implementation Guide?

b. “Example 3—Reconciliation of Segment Profit (Loss)” illustrates the modeling of reconciliation of segment

profit (loss) to the entity's consolidated income. Questions have been raised by TAG members that if

there were no segment reconciling items in the table and it was just the fact values of Segment A. B and C

and then a total that matches the Income statement, should companies still use the “Operating Segments

Member” under the “Consolidation Items Axis” in addition to the extended segment members for the

Segment A, B and C? For above identified disclosure, only extended segment members together with

“Segment [Axis]” would be required – no “Consolidation Items [Axis]” needed since there were no

components or eliminations used in consolidating a parent entity and its subsidiaries or its operating

segments. Same modeling ideas apply to “Example 7—Revenue Disclosure Broken Down by Operating

Segment and Subsegment”.

Do you agree with this modeling clarification? If not, why?

c. Is there any other comment or question regarding this Segment Implementation Guide you want to

discuss or need clarification?

3. Next step: Segment Implementation Guide is currently under SEC review. We will post the latest version on

the FASB website once the review process is complete and initiate the public comment period.

B. Other Implementation Guides in Draft Form

The TAG also had the opportunity to review the Other Comprehensive Income, and Insurance guides.

FINANCIAL ACCOUNTING STANDARDS BOARD

9

C. Meeting Highlights

These documents will be available on the FASB website after the TAG’s comments have been processed. See http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1176160665046.

TAG members expressed support for inclusion of additional examples of segment geographic disclosure into the

implementation guide in order to provide guidance in terms of the preferred usage of “Geographical [Axis]”

and/or “Segments [Axis].” For example, suggested disclosure could include a scenario where a company’s

operating segment is identified by geographic area, i.e., Asia or North America. In addition, similar examples

using the “Products and Services [Axis]” and/or “Segments [Axis]” that include sub-segments were proposed by

TAG members as well. Segment Implementation Guide will be updated based on above feedback/suggestion

before posting on FASB website for public comment.

The XBRL team provided TAG a status update and overview of the drafts for Other Comprehensive Income, and

two Insurance Implementation Guides. The TAG was reminded that their comments on the guides are due

March 6th and March 8th, respectively.

The XBRL team also solicited input regarding any specific issues related to Oil and Gas and or Fair Value to be

included in the subject Implementation Guides. The TAG had no specific issues that they wanted addressed.

FINANCIAL ACCOUNTING STANDARDS BOARD

10

Session 5 - ASU Status

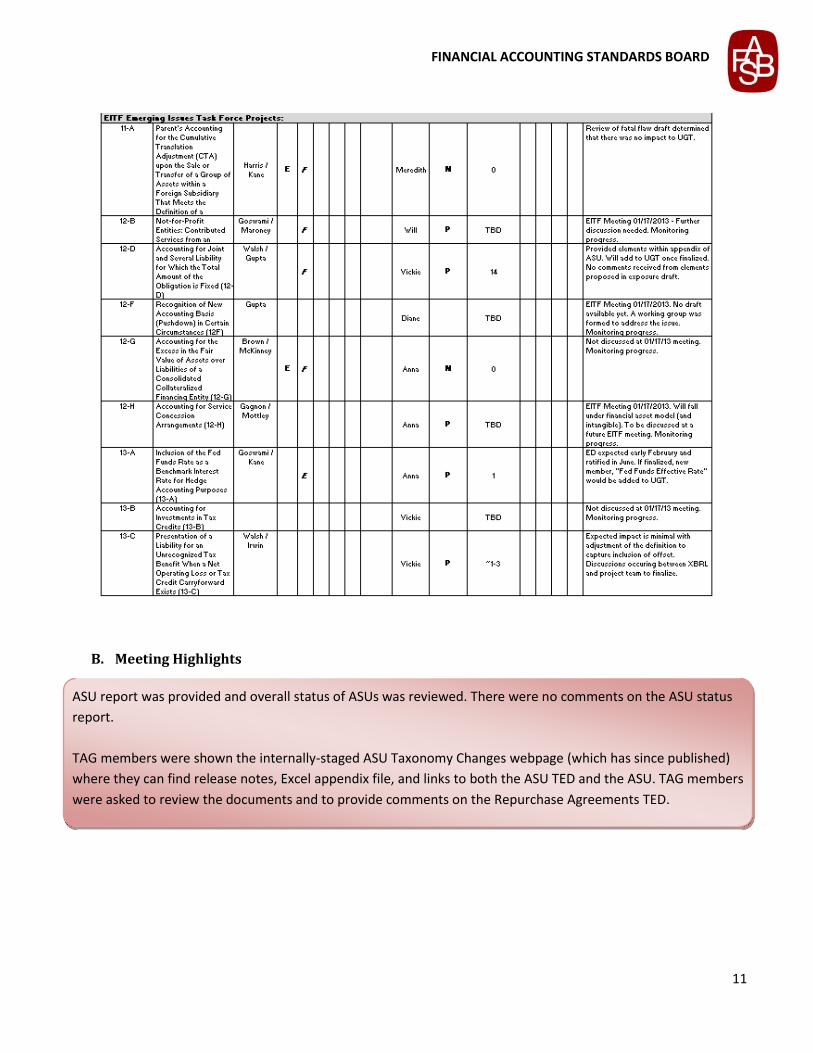

A. Summary of ASUs and EITFs

Below are the upcoming ASUs and EITFs that may impact the UGT when they become effective. The TAG was

asked to provide comments on the exposed Repurchase Agreement Taxonomy Exposure Document (TED).

FINANCIAL ACCOUNTING STANDARDS BOARD

11

B. Meeting Highlights

ASU report was provided and overall status of ASUs was reviewed. There were no comments on the ASU status

report.

TAG members were shown the internally-staged ASU Taxonomy Changes webpage (which has since published)

where they can find release notes, Excel appendix file, and links to both the ASU TED and the ASU. TAG members

were asked to review the documents and to provide comments on the Repurchase Agreements TED.

FINANCIAL ACCOUNTING STANDARDS BOARD

12

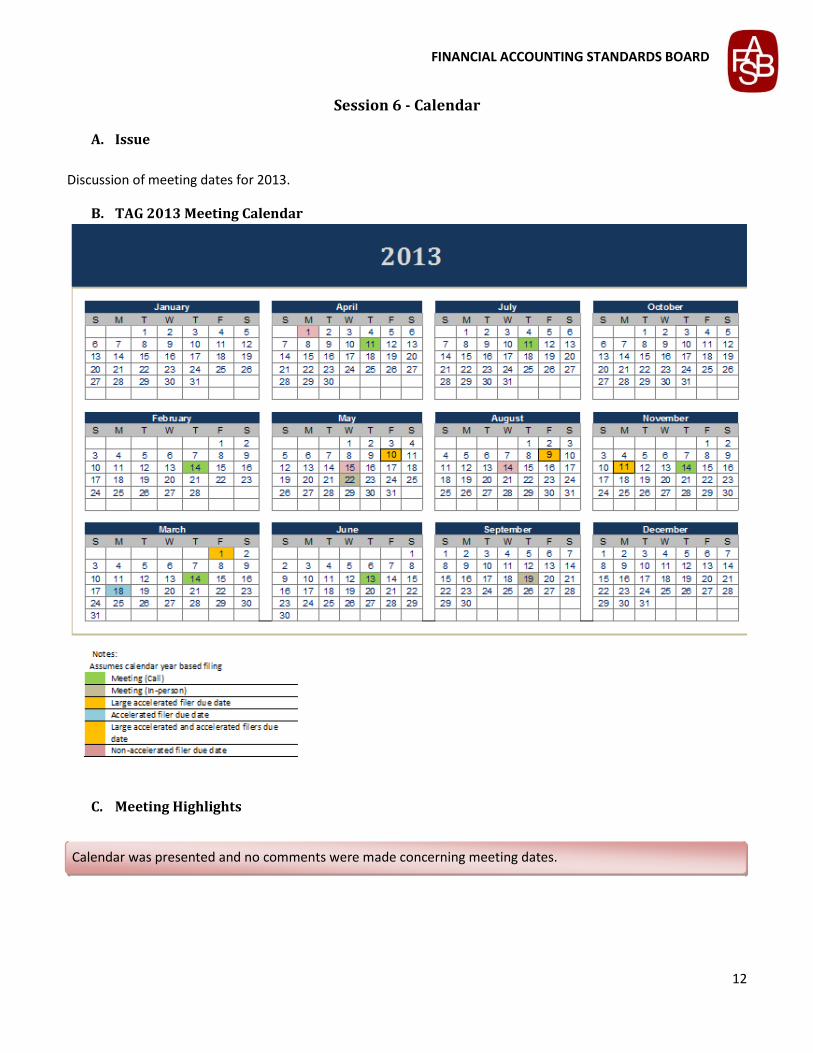

Session 6 - Calendar

A. Issue

Discussion of meeting dates for 2013.

B. TAG 2013 Meeting Calendar

C. Meeting Highlights

Calendar was presented and no comments were made concerning meeting dates.

FINANCIAL ACCOUNTING STANDARDS BOARD

13

Session 7 - Review of November 15, 2012 meeting

A. Issue

Review of items from November 15, 2012 meeting.

B. Meeting Highlights

TAG members had no issues or comments on the highlights from the November 15, 2012 meeting.

FINANCIAL ACCOUNTING STANDARDS BOARD

14

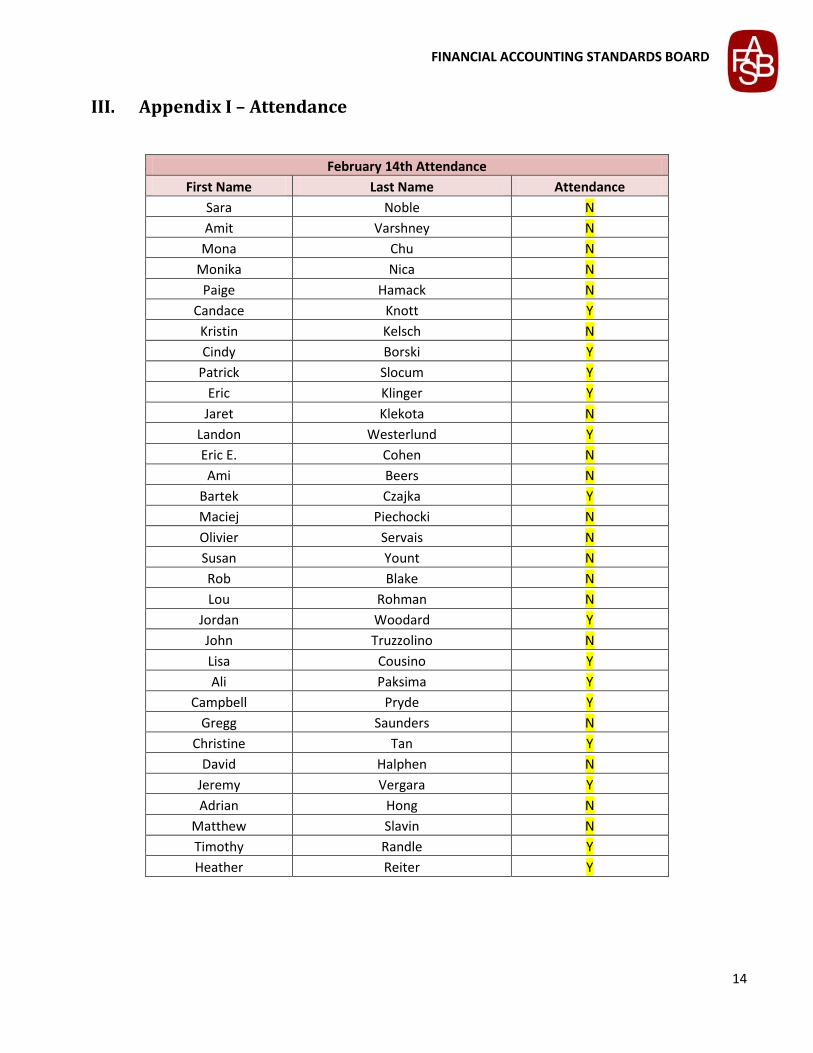

III. Appendix I – Attendance

February 14th Attendance

First Name Last Name Attendance

Sara Noble N

Amit Varshney N

Mona Chu N

Monika Nica N

Paige Hamack N

Candace Knott Y

Kristin Kelsch N

Cindy Borski Y

Patrick Slocum Y

Eric Klinger Y

Jaret Klekota N

Landon Westerlund Y

Eric E. Cohen N

Ami Beers N

Bartek Czajka Y

Maciej Piechocki N

Olivier Servais N

Susan Yount N

Rob Blake N

Lou Rohman N

Jordan Woodard Y

John Truzzolino N

Lisa Cousino Y

Ali Paksima Y

Campbell Pryde Y

Gregg Saunders N

Christine Tan Y

David Halphen N

Jeremy Vergara Y

Adrian Hong N

Matthew Slavin N

Timothy Randle Y

Heather Reiter Y