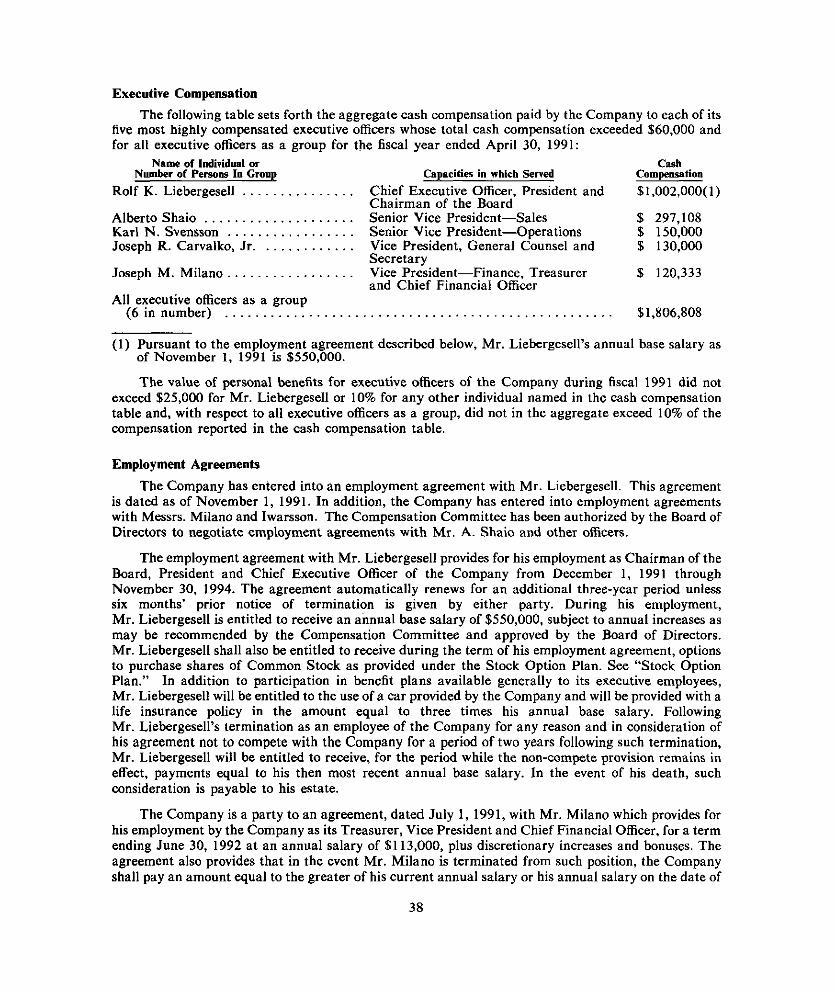

Embed Size (px)

Citation preview

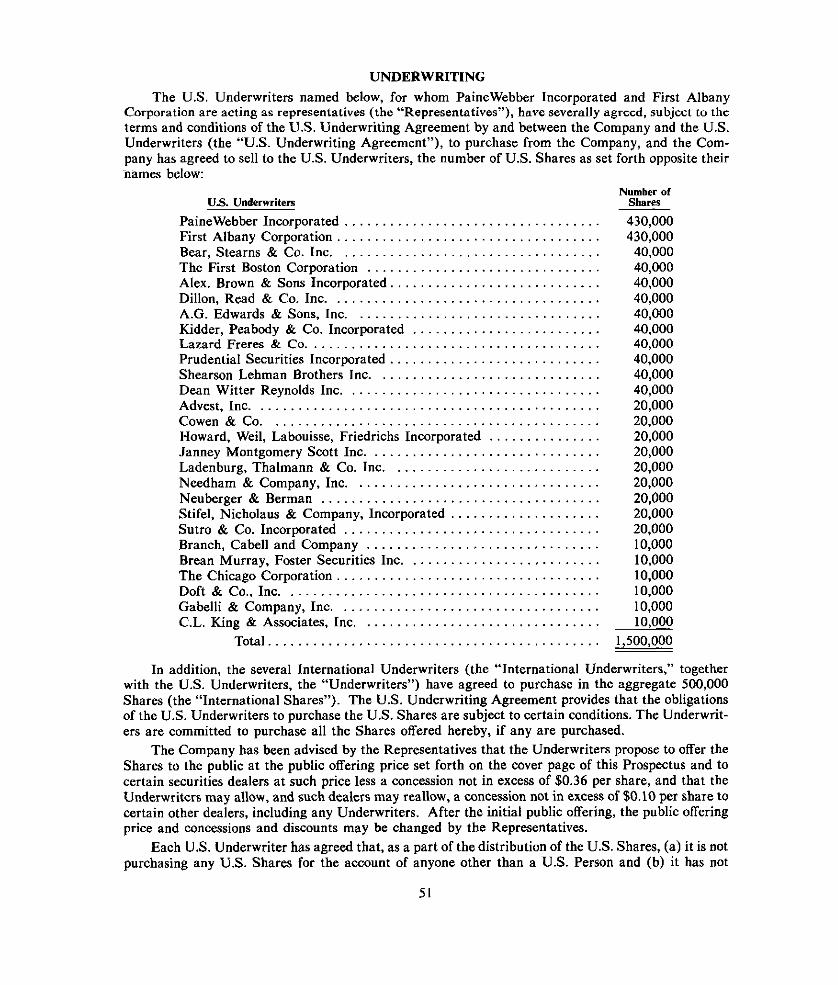

2,000,000 Shares

@ J

Farrel Corporation Common Stock

All of the shares of Common Stock are being offrrrd hereby by Farral Corporation (the "Company"). Of thc 2,000,000 sharrs uf Common Srock offered, 1,500,000 sharrs are being offered hereby in the United States (the "U.S. Shares") and 500,000 shares are bring offered in a concurrent international offering outside the United States. Thc price to the public and aggregate underwriting discounts and commissions per share is identical for both offerings. See "Undcnvriting."

Prior to this offering, there has been no public market for the Common Stock. See "Underwriting" for a discussion of thr factors considered in determining the initial public offering price.

The Common Stuck has been approved for quotation on thr NASDAQ National Market System under the symbol "FARL."

Of the procurds of this offering, $3.8 million will be uscd to repay indebtedness relating to the repurchase of shares of Common Stock from certain principal stockholders of the Company. The Company has agreed to purchase 157,894 shares of Common Stock from its chief exrcutive officer; payment of the $1.5 million purchase pricc therefor will be madc by cancellation of existing indebtedness of such officer KO the Company. Srr "Certain Transactions."

See "Risk Factors" fo r a discussion o f certain factors tha t should b e considered by prospective investors.

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND EXCHANGE COMMISSION OR ANY STATE SECURITIES

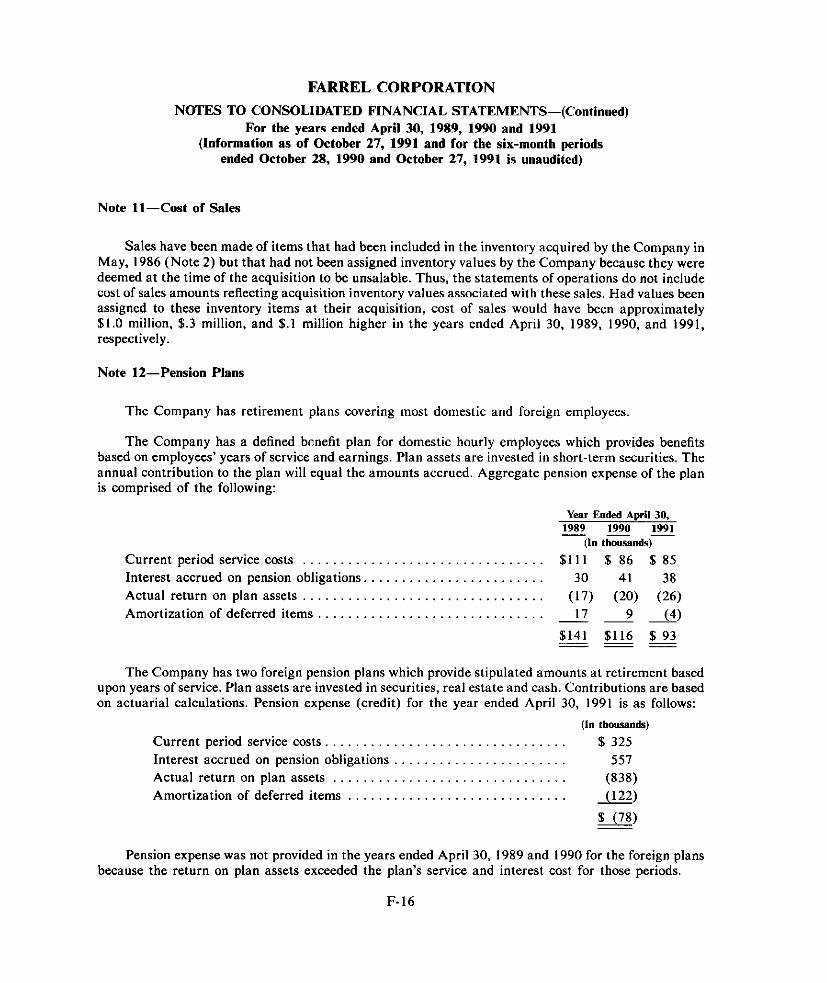

COMMISSION NOR HAS THE SECURITIES AND EXCHANGE COMMISSION OR ANY STATE SECURITIES COMMISSION PASSED UPON THE ACCURACY

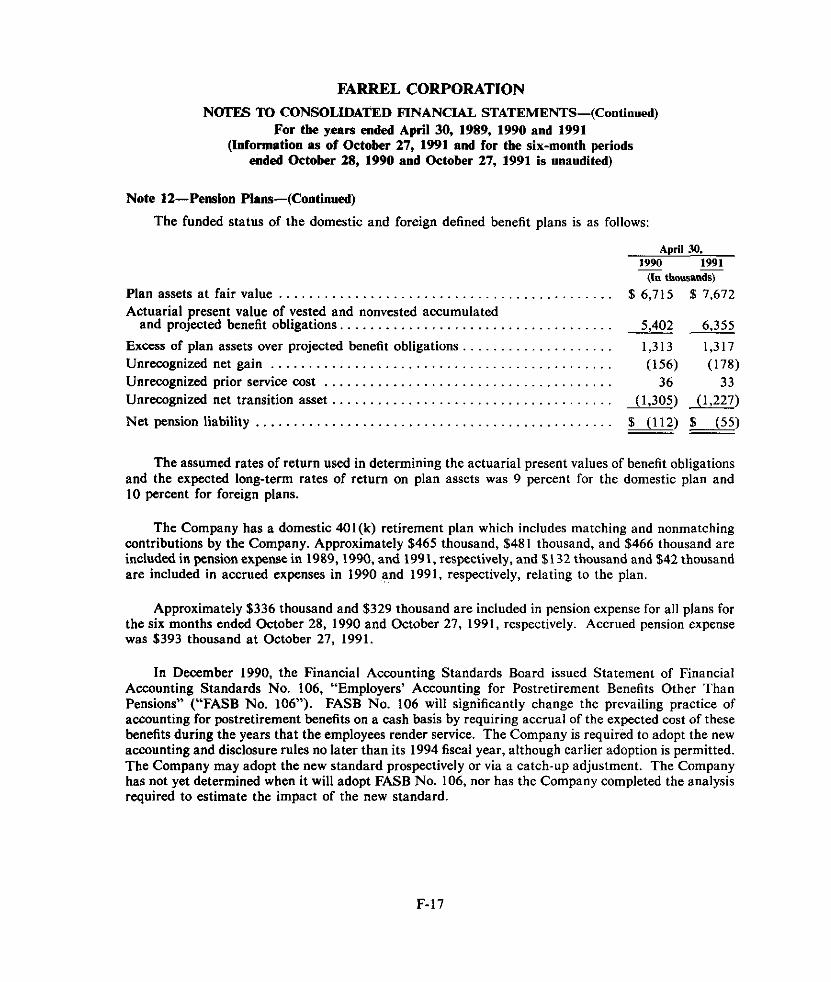

OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

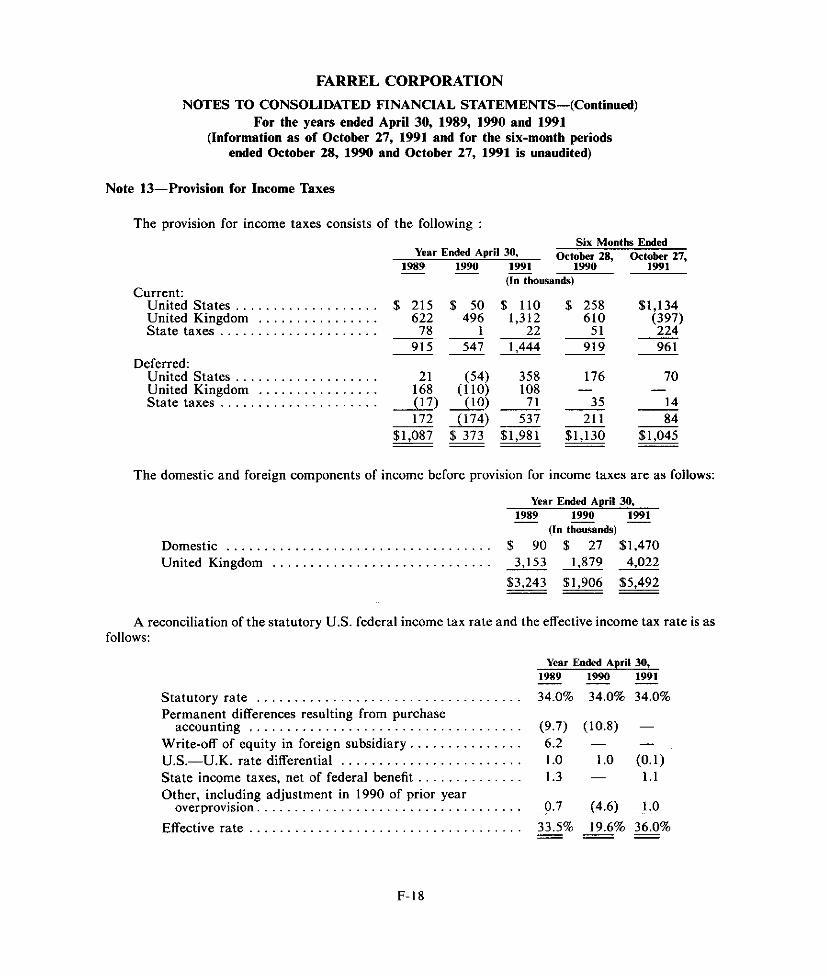

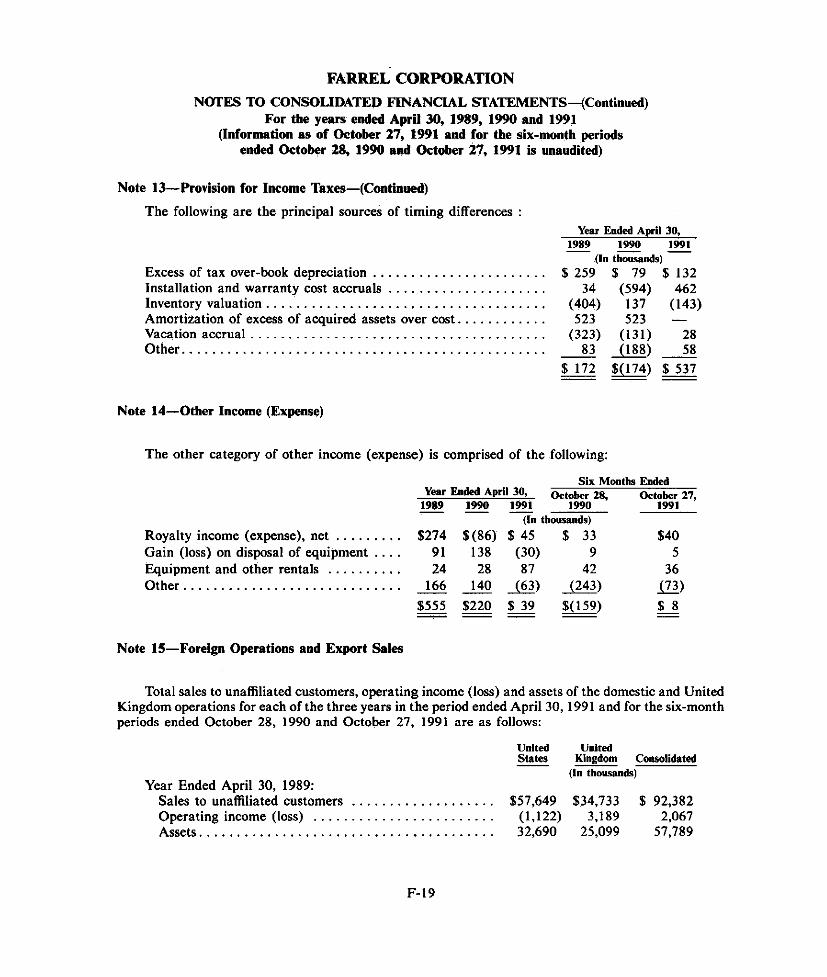

p~

PaineWebber Incorporated First Albany Corporation

Total Assuming Full Exercise of Over- Allotment Option(3). . . . . . . . . . . . .

The date of this Prospecrus is January 17, 1992

Prorrrdr ro compnnri21

58.835

$17,670,000

Underwriting Diirounrr nnd

c ~ m m i ~ r i ~ n ~ i 1 l

$0.665

$1,330,000

Per Sharr . . . . . . . . . . . . . . . . . ... . . . Total . . . . . . . . . . . . . . . . . . . . . . . . . .

(1) See "Underwriting." (2) Before deducting expenses estimated at $1,460,000, which are payable by the Company. (3) Assuming cxercise in full of the 30-day option granted by the Company to the Underwriters to purchasr

up to 300.000 additional shares, on the same terms, solely to cover over-allotments. See "Underwriting."

The US. Shares are offered by the U.S. Undcnvriters, subject to prior sale, when, as and if delivered tu and accepted by the U.S. Underwriters, and subject to their right to reject orders in whole or in part. It is expected chat delivery of thr Common Stock will be made in New York City on or about January 27, 1992.

$21,850,000

Prim to ~ u b i i i

$9.50

$19,000,000

$1,529,500 520,320,>00

THE U.S. SHARES MAY NOT BE OFFERED OR SOLD, DIRECTLY OR INDIRECTLY, OUTSIDE THE UNITED STATES OR TO ANY PERSON WHO IS NOT A UNITED STATES PERSON, AS PART OF THE DISTRIBUTION OF THE U.S. SHARES. FOR A DESCRIPTION OF THIS AND OTHER RESTRICTIONS ON THE OFFERING AND SALE OF THE SHARES, SEE "UNDERWRITING."

I S COUNECTION WI I'H 'I'HIS OFFERING. I'HE I!SDERM'RITERS MAY OVER-ALWT OR EFFECT TRANSACTIONS H HlCH ST.4BILIZE OR MAIYI'AIN THE MAHKEI' PRICE OF THE COMMON STOCK OF THE COMPANY AT A LEVEL ABOVE THAT WHICH MIGHT OTHER- WISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

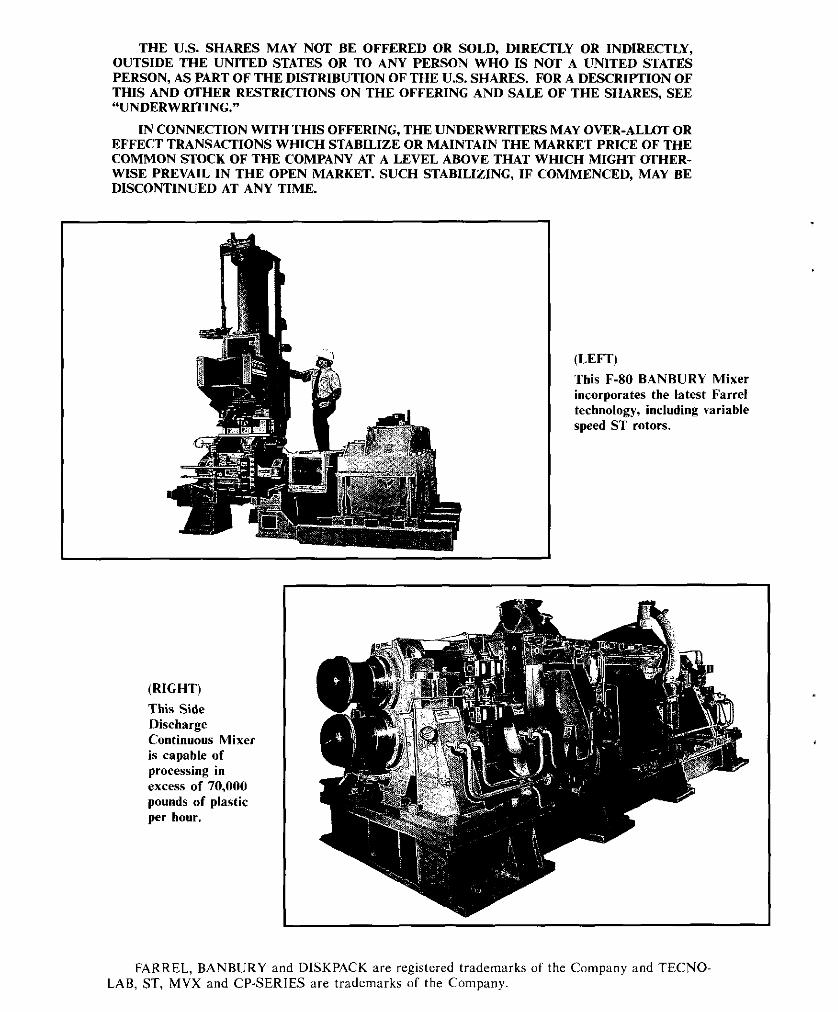

( L E m This F-80 BANBURY Mixer incorporates the latest Farrel technology, including variable speed ST rotors.

(RIGHT)

This Side Discharge Continuous Mixer is capable of processing in excess of 70,000 pounds of plastic per hour.

FARREL, BANBURY and DISKPACK are registered trademarks of the Company and TECNO- LAB, ST, MVX and CP-SERIES are trademarks of the Company.

PROSPECWS SUMMARY The following summary is qualified in its entirety by the more detailed information andJinancia1

statements appearing elsewhere in this Prospectus. This Prospectus relates to the ofer of 2,000,000 shares (the "Shares"') of common stock, S.01 par value (the 'Common Stock'J, of Farrel Corporation. a Delaware corporation ("Farrel" or the "Company '7. Unless otherwise indicated, all share and per share data set forth in this Prospectus have been adjusted to give eflect to a stock split eficted October 24.1991, to the purchase by the Company of 1.483.870 shares of its Common Stock pursuant to an option and to the purchase by the Company of 157,894 shares of Common Stock from an oficer of the Company. See "Certain Transactions." Unless otherwise indicated, the information in this Prospectus assumes the Underwriters' over-allotment option will not be exercised. See "Underwrit- ing." Investors should carefully consider the information set forth under 'Risk Factors."

The Company The Company designs, manufactures, sells and services capital equipment used to process rubber

and plastics materials. The Company's principal products are BANBURY Mixers, continuous mixers, extruders, compact processors, pelletizers, gear pumps, calenders and mills. In conjunction with sales of capital equipment, the Company provides process engineering, process design and related services for rubber and plastics processing systems. The Company's aftermarket business consists primarily of repair, refurbishment and equipment upgrade services, spare parts sales and field services. The Company also provides laboratory services and facilities for product demonstrations and for the development and testing of rubber and plastics equipment and processes.

The Company's customers include tire manufacturing and petrochemical firms. In fiscal 1991, approximately 65% of the Company's sales of new capital equipment and process engineering services was to customers in the rubber industry and 35% was to customers in the plastics industry. Sales outside of the United States accounted for approximately 62% of the Company's net sales during fiscal 1991.

Management believes that the Company's financial performance since 1986 is attributable to, among other factors, a strategic focus on the rubber and plastics processing industries where the Company's market position had historically been strong, the divestiture of unrelated machinery product lines, production efficiencies resulting from increased outsourcing of selected machine components and more efficient purchasing practices, an increase in the portion of the Company's revenues derived from aftermarket products and services which generally carry higher margins than new equipment salcs, and in years prior to fiscal 1991, the amortization of the excess of acquired assets over cost.

The Company was formed by its current stockholders in 1986 to acquire certain assets and to assume certain liabilities of the former Farrel Company, an unprofitable division of USM Corporation ("USM"), a subsidiary of Emhart Corporation ("Emhart"), in a leveraged buyout.

The total purchase price paid in the acquisition was $18.8 million, which included the payment of $1.8 million in cash and the assumption of $17.0 million in balance sheet liabilities of the business acquired. The Company incurred $3.1 million of indebtedness at the time of the acquisition to fund the balance of the cash portion of the purchase price, to pay expenses relating to the acquisition and for working capital, all of which bas since been repaid. See "Legal Proceedings" for a description of certain material provisions of the agreements among the parties to the acquisition, as well as certain actions pending among the parties.

The Farrel name was initially used by the Company's predecessor, Almon Farrel & Company, in 1848.

The Mering

Common Stock offered by the Com any . . . . . 2,000,000 shares P Common Stock to be outstanding a ter the offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,842,106 shares

Use of proceeds . . . . . . . . . . . . . . . . . . . . . . . . . Upgrade and expand Company facilities, acquire new machinery and add~tional facilities, establish research and development facilities, repay indebtedness relating to the acquisition of 1,483,870 shares of Common Stock, working capital and other general corporate purposes

NASDAQ Symbol.. . . . . . . . . . . . . . . . . . . . . . FARL

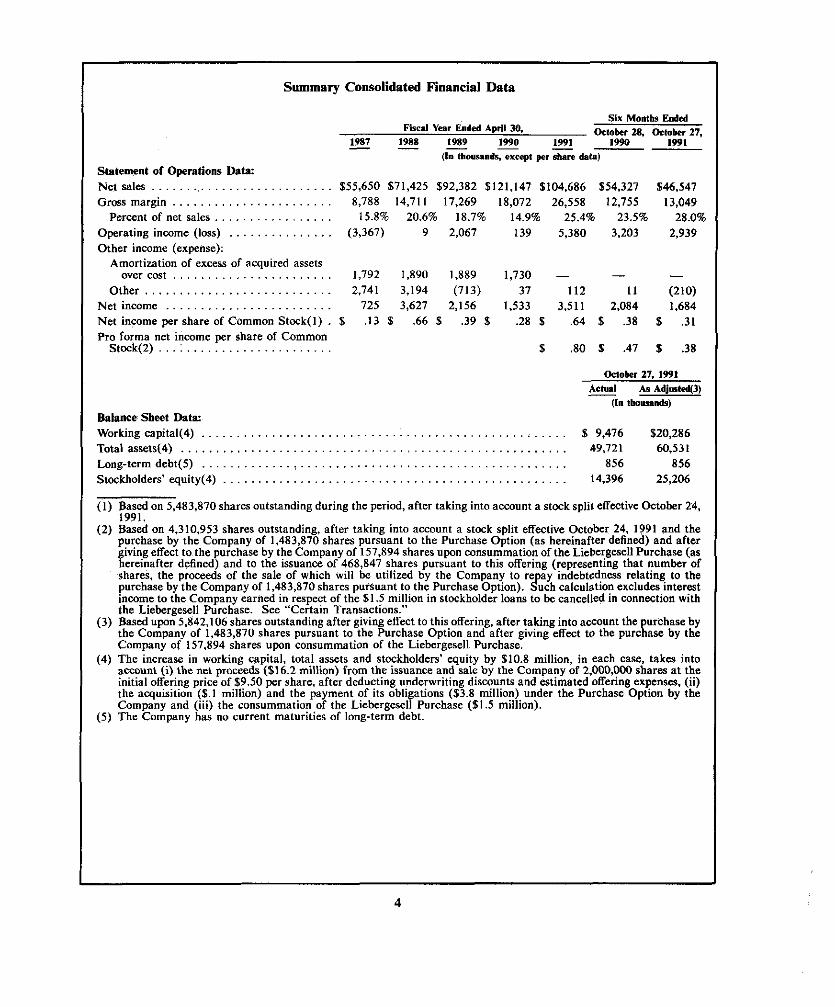

Summary Consolidated Financial Data

Six Months Eodcd Fiscal Year Ended April 30, Oelokr 28. Oetober 27,

1987 1988 1989 1990 - - - - - 1991 1990 1991 (In thousands, except p r share dab)

Siatement of Operations Datr: Net sales . . . . . . . . . . . . . . . . . . . . . . . . . . $55,650 $71,425 $92.382 $121,147 $104,686 $54,327 $46.547 Gross margin . . . . . . . . . . . . . . . . . . . . . . . 8,788 14,711 17,269 18,072 26,558 12,755 13,049

Percent of net sales . . . . . . . . . . . . . . . . . 15.8% 20.6% 18.7% 14.9% 25.4% 23.5% 28.0% Operating income (loss) . . . . . . . . . . . . . . . (3,367) 9 2,067 139 5,380 3,203 2,939 Other income (expense):

Amortization of excess of acquired assets overcost . . . . . . . . . . . . . . . . . . . . . . . 1,792 1,890 1,889 1,730 - - -

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.741 3,194 (713) 37 112 I1 (210) Netincome . . . . . . . . . . . . . . . . . . . . . . . . 725 3,627 2,156 1,533 3,511 2,084 1,684 Net income per share of Common Stock(1) . $ 3 $ .66 $ .39 $ .28 $ .64 $ .38 $ .31 Pro forma net inwme per share of Common

Stock(2) . . . . . . . . . . . . . . . . . . . . . . . . . S .80 1 .47 S .38

Oelokr 27, 1991 Actual As AdjtalCd(3) -

(I" thouundr)

Balance Sheet Data: Working capital(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9,476 $20.286 Total assets(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49,721 60,531 Long-term deht(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 856 856 Stockholders' equity(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14,396 25,206

(1) Based on 5,483,870 shares outstanding during the period, after taking into account a stock split effective October 24, 1991.

(2) Based on 4,310.953 shares outstanding, after taking into account a stock split effective October 24, 1991 and the pumhase by the Company of 1,483,870 shares pursuant to the Purchase Option (as hereinafter defined) and after glvlng effect to the purchase by the Company of 157,894 shares upon consummation of the Liebergesell Purchase (as hereinafter defined) and to the issuance of 468,847 shares pursuant to this offering (representing that number of shares, the proceeds of the sale of which will be utilized by the Company to repay indebtedness relating to the purchase by the Company of 1,483,870 shares pursuant to the Purchase Option). Such calculation excludes interest income to the Company earned in respect of the $1.5 million in stockholder loans to be cancelled in wnnection with the Liebergesell Purchase. See "Certain Transactions."

(3) Based upon 5,842,106 shares outstanding after giving effect to this offering, after taking into account the urchase by the Company of 1,483,870 shares pursuant to the Purchase Option and after giving effect to the purclase by the Company of 157,894 shares upon consummation of the Liebergesell Purchase.

(4) The increase in working capital, total assets and stockholders' equity by $10.8 million, in each case, takes into account (i) the net proceeds ($16.2 million) from the issuance and sale by the Company of 2,000,000 shares at the initial offering price of $9.50 per share, after deducting underwriting discounts and estimated offering expenses, (ii) the acquisition ($.I million) and the payment of its obligations ($3.8 million) under the Purchase Option by the Company and (iii) the consummation of the Liebergesell Purchase ($1.5 million).

(5) The Company has no current maturities of long-term debt.

-

THE COMPANY

The Company designs, manufactures, sells and services capital equipment used to process rubber and plastics materials. The Company's principal products are BANBURY Mixers, continuous mixers, extruders, compact processors, pelletizers, gear pumps, calenders and mills. In conjunction with sales of capital equipment, the Company provides process engineering, process design and related services for rubber and plastics processing systems. The Company's aftermarket business consists primarily of repair, refurbishment and equipment upgrade services, spare parts sales and field services. The Company also provides laboratory services and facilities for product demonstrations and for the development and testing of rubber and plastics equipment and processes. Unless the context otherwise requires, all references to the "Company" in this Prospectus are to the Company and its subsidiary, Farrel Limited, collectively. See "Business of the Company-Products and Services."

The Company's customers include tire manufacturing and petrochemical firms. The Company's rubber processing equipment is primarily sold to tire manufacturers and manufacturers of rubber goods, such as sheet products, molded products, footwear a@ wire and cable. In the plastics processing industry, the Company's equipment is primarily sold to &mmodity plastics producers and value-added

o o the Company's sales of new capital equipment mixers of plastics. In fiscal 1991, approximately 65Y '1. and process engineering services was to customers in the rubber industry and 35% was to customers in the plastics industry. Sales outside of the United States accounted for approximately 62% of the Company's net sales during fiscal 1991.

Sales of new capital equipment and process engineering services accounted for approximately 63%. and sales of aftermarket products and services accounted for approximately 37%, of the Company's net sales in fiscal 1991. See "Business of the Company- Customers."

The Company's primary manufacturing facilities are located in Derby, Connecticut and Rochdale, England. The Company also operates repair facilities in Ansonia, Connecticut, Deer Park, Texas and Rochdale, England. The Company markets its products through an international sales and service organization that includes four offices in the United States, one in Canada, six in other countries, and independent sales representatives covering 28 countries. See "Business of the Company-Sales and Marketing."

Demand for the Company's products and services is principally influenced by the expansion, modernization and maintenance of the manufacturing infrastructure in the segments of the rubber and plastics processing industries served by the Company. Equipment purchases in each of these segments are especially influenced by capital expenditures resulting from manufacturing requirements, capacity utilization, the age of the installed equipment and related replacement rates. Purchases of spare parts and repair, refurbishment and equipment upgrade services are also influenced by the age of the installed equipment and equipment replacement rates, with equipment generally requiring greater levels of repair and maintenance the longer it is left in service.

The Company was formed by its current stockholders in 1986 to acquire certain assets and to assume certain liabilities of the former Farrel Company, an unprofitable division of USM, a subsidiary of Emhart, in a leveraged buyout. The total purchase price paid in the acquisition was $18.8 million, which included the payment of $1.8 million in cash and the assumption of $17.0 million in balance sheet liabilities of the business acquired. The Company's current stockholders contributed $1.0 million to the capital of the Company. The Company incurred $3.1 million of indebtedness at the time of the acquisition to fund the balance of the cash portion of the purchase price, to pay expenses relating to the acquisition and for working capital, all of which has since been repaid. See "Legal Proceedings" for a description of certain material provisions of the agreements among the parties to the acquisition, as well as certain actions pending among the parties. Based on the initial public offering price of $9.50 per share, the value of the Common Stock of the Company owned by its current stockholders, excluding the shares related to the Purchase Option and the shares to be acquired pursuant to the Liebergesell

Purchase, is equal to approximately $36,500,000. Based on the initial public offering price of $9.50 per share, the value of the Common Stock of the Company owned by its current stockholders, including the shares related to the Purchase Option and the Liebergesell Purchase, is equal to approximately $52,097,000.

Management believes that the Company's financial performance since 1986 is attributable to, among other factors, a strategic focus on the rubber and plastics processing industries where the Company's market position had historically been strong, the divestiture of unrelated machinery product lines, production efficiencies resulting from outsourcing of selected machine components and more efficient purchasing practices, an increase in the portion of the Company's revenues derived from aftermarket products and services which generally carry higher margins than new equipment sales, and in years prior to fiscal 1991, the amortization of the excess of acquired assets over cost.

The Company's business strategy focuses on continuing the technological development of its products, improving its global market position, reducing the manufacturing cost of its products and pursuing new market opportunities as they develop. Currently, the Company is working with certain customers to develop equipment that can reduce the level of volatile gases found in plastics and is exploring applications for the Company's equipment in the plastics recycling industry.

The Company's principal executive offices are located a t 25 Main Street, Ansonia, Connecticut 06401. Its telephone number is (203) 736-5500.

RISK FACTORS

In addition to the information set forth elsewhere in this Prospectus, prospective investors should carefully evaluate the following risk factors before purchasing the Shares offered hereby.

Cyclical Business. The Company primarily sells its products to participants in the rubber and plastics processing industries, which are cyclical in nature. Orders for the Company's products have fluctuated based upon its customers' capital expenditure budgets, demand for such customers' end products, the need for upgraded or retooled equipment, competition within the Company's and customers' respective industries, general economic conditions and other factors. There can be no assurance that orders from any one or more of the Company's customers will not decline in the future. Principally as a result of the continuing economic slowdown and consolidation in the primary industries served by the Company, conditions of overcapacity exist in the Company's primary markets, and the Company has experienced a decline in the level of new orders compared to levels experienced in previous years. The Company's ability to maintain and increase sales levels will depend upon a recovery in these markets and a corresponding increase in order activity. There can be no assurance that such a recovery will occur, or that such a recovery will lead to increased orders for the Company's products. See "Management's Discussion and Analysis of Financial Condition and Results of Operations--Orders and Backlog."

Dependence on Tire and Plastics Industries. During the fiscal year ended April 30, 1991 approxi- mately 40% of the Company's net sales of new capital equipment and project engineering services was to tire manufacturers, and 35% was to customers in the plastics industry. Many tire manufacturers are highly leveraged as a result of industry consolidation, and the industry is currently operating at less than full capacity largely as a result of recessionary forces. In the plastics industry, which is also currently operating at less than full capacity, many manufacturers have been impacted by recessionary forces and relatively depressed prices for their products. New capital expenditures by customers in both industries will depend, in large part, on the ability of manufacturers to increase capacity utilization above current levels and on the need for more efficient machinery. There can be no assurance that such new capital expenditures will occur or result in increased orders for the Company's products. Substantially all of the Company's customers are in the rubber and plastics processing industries, which effectively limits the number of potential customers for the Company's products. While there are customers for the

Company's products outside of the rubber and plastics processing industries, the number of such customers is also limited.

Fluctuations in Operating Results. The Company's customers often purchase equipment in significant quantities for new plants, plant expansion or plant modernization. The dollar value of purchases by any single customer from year to year may vary significantly according to that customer's capital equipment needs. The composition of the Company's largest customers will vary from year to year, and the timing of purchase orders and product shipments can cause backlog and operating results to fluctuate significantly from fiscal period to fiscal period. Some of the Company's products have higher profit margins than others, and a change in the Company's product mix could contribute to fluctuating operating results.

Decline in Orders and Backlog. During each of the past three fiscal years, the Company has experienced a decline in orders received. The Company's fiscal year end backlog of unfilled orders has also declined in each of the past three fiscal years. The Company believes that the decline in orders and backlog is a reflection of the cyclical nature of the markets it serves, the general economic slowdown in the United States and Western Europe, political and economic unrest in Eastern Europe, the Middle East and China and consolidation in the primary industries sewed by the Company, leading to conditions of overcapacity in the Company's primary markets. In addition, in fiscal 1991, the decline was due in part to the Company's strategic decision to emphasize product line profitability over aggregate sales levels, thereby reducing sales efforts associated with lower margin products. The Company's ability to increase sales levels will depend upon a recovery in the Company's primary markets and a corresponding increase in order activity. During the first six months of fiscal 1992, orders increased to $45.7 million from $39.3 million during the comparable period in fiscal 1991. However, as of October 27, 1991, the backlog of orders considered to be firm decreased to $52.9 million from $57.3 million at October 28, 1990. There can be no assurance that this increase in order activity is indicative of a recovery in the Company's primary markets, or that orders and backlog will increase in the future or that they will not continue to decline.

Foreign Operations. The Company's sales outside the United States, which accounted for approxi- mately 62% of net sales for fiscal 1991, may be subject to special risks inherent in doing business outside the United States, including risks of war, civil disturbance and government activities, which may limit or disrupt the Company's operations. Some of the Company's major foreign equipment sales are conducted on the basis of documentary letters of credit assuring payment in U.S. dollars or British pounds sterling at the time of export. Where appropriate and available, foreign credit insurance is secured by the Company and the Company's practice has been to hedge against foreign currency fluctuations when it has deemed such hedging appropriate. No assurance can be given as to the adequacy or availability of such insurance or as to the success of any such hedging activities.

Competition. The Company competes on a global basis with other companies, many of whom are divisions or subsidiaries of larger companies with greater financial and other resources than those of the Company. The Company's ability to compete also can be affected by the relative strength of different currencies.

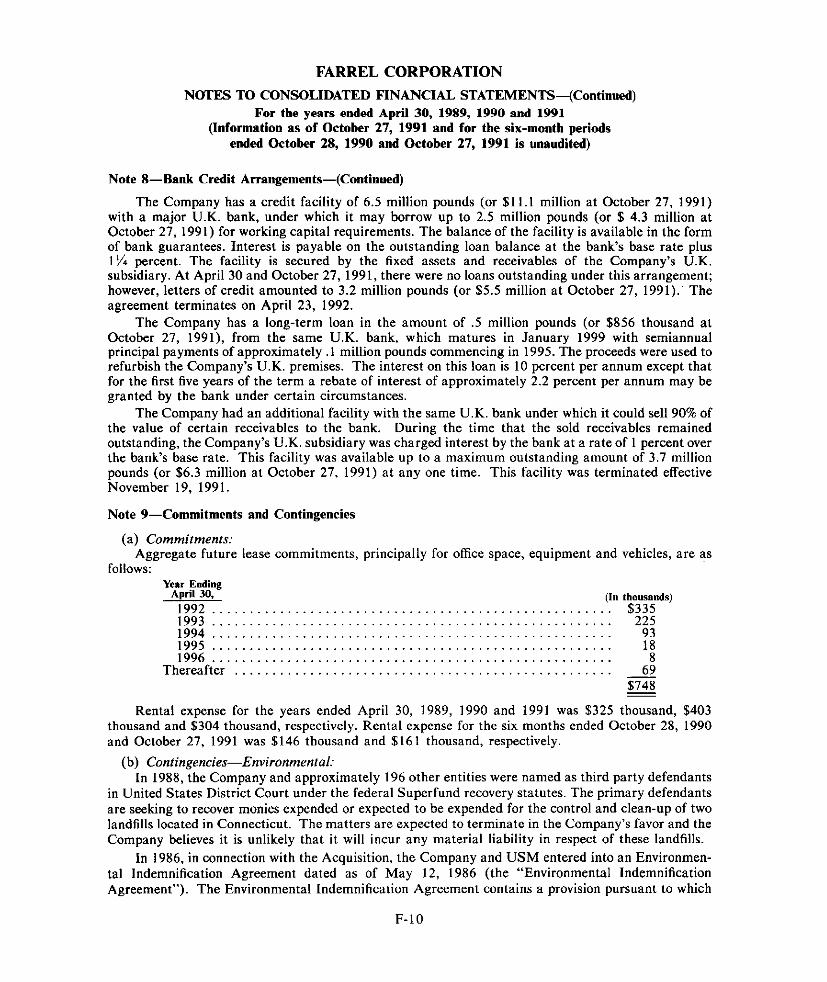

Environmental Matters. The Company's United States operations are subject to extensive federal, state and local laws and regulations relating to the generation, storage, handling and transportation of certain materials and the discharge of these materials into the environment. The Company's operations outside the United States are also subject to extensive requirements governing environmental protec- tion. Environmental requirements are constantly changing and it is difficult to predict the effect of future requirements on the Company. Future developments, including the discovery of existing condi- tions not currently known by the Company or changes in existing regulations, could require the significant expenditure of funds for capital improvements or require the clean-up of sites not currently subject to such requirements. For a description of potential environmental liabilities of the Company relating to conditions presently known to the Company, see "Business of the Company-Legal

Proceedings- Environmental." While under certain circumstances the Company could be required to incur significant costs in complying with environmental laws and regulations relating to conditions presently known to the Company, the Company does not currently believe that such costs will have a material adverse effect on its financial condition. The Company's belief is based upon, among other things, (i) the advice of the Company's special environmental counsel, Murtha, Cullina, Richter and Pinney, concerning the status of and the legal bases for environmental litigation with USM and Emhart; (ii) the Company's understanding of the underlying facts which give rise to its claims against USM; and (iii) technical advice received from outside consultants relating to the presence and/or nature and scope of subsurface contamination a t the Ansonia and Derby properties and possible remediation options which could be required by the Connecticut Department of Environmental Protection and the United States Environmental Protection Agency with respect thereto. There is no assurance, however, that the Company will prevail in its suit against USM for indemnification under the Environmental Indemnifi- cation Agreement or for strict liability under the Connecticut Transfer Act, or that, if it should prevail, USM will be able to meet its obligations thereunder or that any such recovery from USM would cover all such costs.

No Prior Public Market. Prior to this offering, there has been no public market for the Common Stock, and there is no assurance that following this offering a significant public market for the Common Stock will develop or be sustained. The initial p1;blic offering price has been determined by negotiation between the Company and the Underwriters. See "Underwriting."

Dilution. The purchase price per share paid by investors in this offering will be substantially in excess of the net tangible book value per share of Common Stock outstanding immediately after the offering. Accordingly, the purchasers of Common Stock will experience immediate and substantial dilution. See "Dilution."

Products Liability. The Company faces an inherent business risk of exposure to products liability claims. There can be no assurance that the Company's insurance coverage will be adquate in all events, that such insurance will he available in all future periods a t an acceptable cost or that a future products liability claim will not materially adversely affect the business or financial condition of the Company. Management believes that the outcome of existing products liability claims will not have a material adverse effect on the financial condition of the Company based upon (i) the current status of the proceedings, (ii) liability insurance carried by the Company, (iii) the fact that the Company specifically did not assume or agree to be responsible for product liability claims arising out of products shipped prior to the closing date of the 1986 asset acquisition and (iv) review of attorneys' letters with respect to such proceedings. See "Business of the Company."

Shares Eligible for Future Sale. Upon completion of this offering, 3,842,106 shares of Common Stock owned by existing stockholders will be eligible for sale in the public market, subject to the restrictions of Rule 144 promulgated under the Securities Act of 1933 The prevailing market price of the Common Stock after the offering could be adversely affected by future sales of Common Stock by existing stockholders. See "Shares Eligible for Future Sale."

Control of the Company. Upon completion of this offering, after taking into account the purchase by the Company of 1,483,870 shares of Common Stock pursuant to an option (the "Purchase Option") and assuming the purchase by the Company of 157,894 shares from Rolf K. Liebergesell (the "Liehergesell Purchase"), the current stockholders of the Company will beneficially own approximately 66% of the outstanding Common Stock (approximately 63% if the Underw:iters' over-allotment option is exercised in full) and will be able to control the affairs of the Company and the vote on any action requiring stockholder approval, including the election of directors, other than an amendment to the provisions of the Company's Certificate of Incorporation relating to its classified board. See "Certain Transactions" and "Principal Stockholders."

Certain Transactions. The Company intends to use $3.8 million of the net proceeds to be received in this offering to repay indebtedness relating to the purchase by the Company of 1,483,870 shares of

Common Stock from existing stockholders pursuant to the Purchase Option. The Company has also agreed to purchase shares of Common Stock from Mr. Liebergesell pursuant to the Liebergesell Purchase. The Company will purchase from Mr. Liebergesell that number of shares equal to $1.5 million divided by the initial public offering price set forth on the cover page of this Prospectus. The Company will pay the purchase price by cancellation of Mr. Liebergesell's indebtedness to the Company in the amount of $1.5 million. Based on the initial public offering price of $9.50, the Company would purchase 157,894 shares from Mr. Liebergesell. See "Use of Proceeds," "Certain Transactions" and "Indebtedness of Management; Liebergesell Purchase." The Company has entered into an agreement with a related corporation providing for certain financial advisory services to the Company that requires payment of an annual retainer of $450,000, plus certain other fees. See "Certain Transactions." Other than the transactions referred to under "Certain Transactions," the Company has no current intention of entering into any material transaction with any of its affiliates.

Anti-takeover Eflects of the Certificate of Incorporation and Delaware Law. The Company's Certificate of Incorporation and the Delaware General Corporation Law contain provisions that may have the effect of making more difficult or delaying attempts by others to obtain control of the Company. These provisions (i) classify the Company's Board of Directors into two classes, each of which serves for a staggered two-year term, (ii) require a 2/3 vote of stockholders for certain changes to directors and/or directorships and (iii) authorize only the Board of Directors to fill vacant directorships. The Company's Certificate of Incorporation also authorizes the Board of Directors to issue one or more series of preferred stock without stockholder approval, which stock could have voting and conversion rights that adversely affect the voting power of the holders of Common Stock. The Delaware General Corporation Law also imposes conditions on certain business combination transactions with "interested stockholders" (as defined therein). See "Description of Capital Stock."

Limitation on Dividends. The Company has not paid any dividends on its Common Stock since its incorporation. The Company intends to pay a quarterly cash dividend subject to the discretion of the Board of Directors. The Company's ability to pay dividends will be limited by a credit agreement to 50% of cumulative consolidated net income during specified periods. See "Dividend Policy."

USEOFPROCEEDS

The net proceeds to be received by the Company from the sale of the 2,000,000 Shares offered by the Company will be $16.2 million ($18.9 million if the Underwriters' over-allotment option is exercised in full), after payment of the underwriting discount and estimated offering expenses.

The Company intends to use the net proceeds of the offering to upgrade and expand the Company's U.S. and foreign facilities and to acquire new machinery and additional facilities (approximately $10.1 million in the aggregate), to establish research and development facilities for new or improved products (approximately $2.1 million) and to repay indebtedness relating to the purchase by the Company of 1,483,870 shares pursuant to the Purchase Option ($3.8 million), with the balance for working capital and other general corporate purposes. See "Certain Transactions" for a description of the Purchase Option. The acquisition of additional facilities may be in the form of an acquisition of an existing business with such facilities. However, no negotiations are currently being undertaken by the Company in respect of any such acquisition.

Until the net proceeds of the offering are fully used, the Company intends to invest such proceeds in investment grade, short-term, interest-hearing obligations or U.S. government obligations.

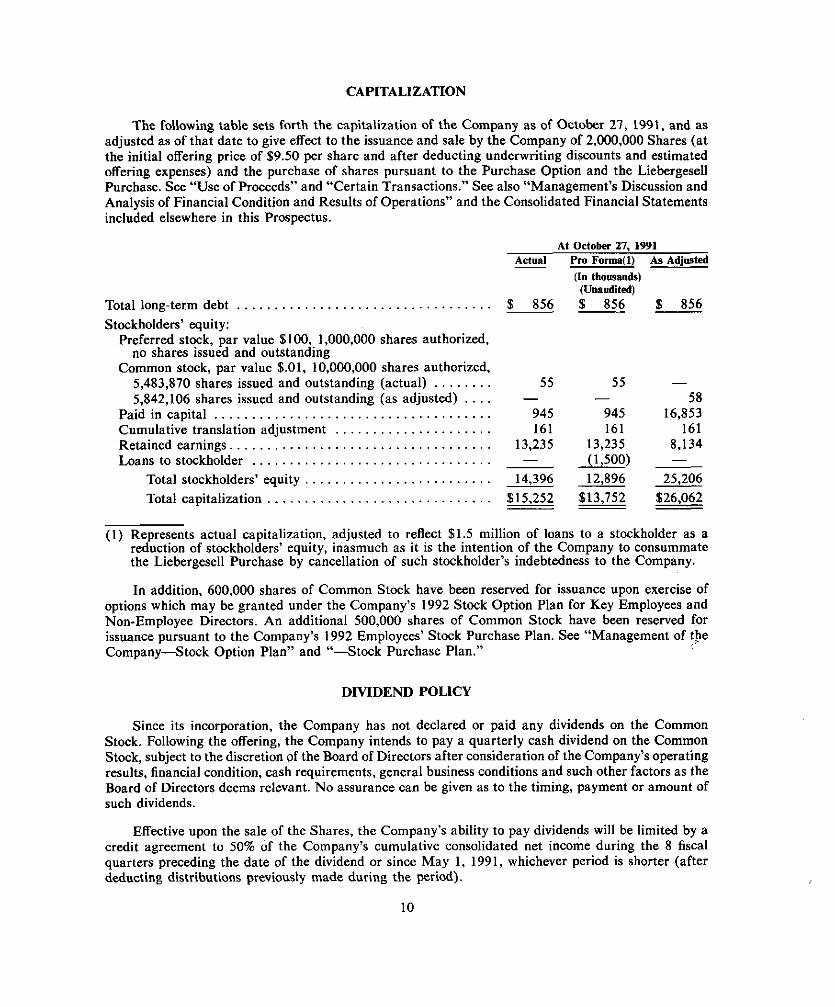

CAPITALIZATION

The following table sets forth the capitalization of the Company as of October 27, 1991, and as adjusted as of that date to give effect to the issuance and sale by the Company of 2,000,000 Shares (at the initial offering price of $9.50 per share and after deducting underwriting discounts and estimated offering expenses) and the purchase of shares pursuant to the Purchase Option and the Liebergesell Purchase. See "Use of Proceeds" and "Certain Transactions." See also "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the Consolidated Financial Statements included elsewhere in this Prospectus.

At October 27, 1991 Actual Pm Forma(1) As Adjmted

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Total long-term debt Stockholders' equity:

Preferred stock, par value $100, 1,000,000 shares authorized, no shares issued and outstanding

Common stock, par value $.01, 10,000,000 shares authorized, 5,483,870 shares issued and outstanding (actual) . . . . . . . . 5,842,106 shares issued and outstanding (as adjusted) . . . .

Paid incapital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Cumulative translation adjustment . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Retained earnings. Loans to stockholder . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Total stockholders' equity . . . . . . . . . . . . . . . . . . . . . . . . . Total capitalization . . . . . . . . . . . . . . . . . . . . . . .

(In thousands) (Unaudited)

% 856 $ 856 $ 856 - --

(1) Represents actual capitalization, adjusted to reflect $1.5 million of loans to a stockholder as a reduction of stockholders' equity, inasmuch as it is the intention of the Company to consummate the Liebergesell Purchase by cancellation of such stockholder's indebtedness to the Company.

In addition, 600,000 shares of Common Stock have been reserved for issuance upon exercise of options which may be granted under the Company's 1992 Stock Option Plan for Key Employees and Non-Employee Directors. An additional 500,000 shares of Common Stock have been reserved for issuance pursuant to the Company's 1992 Employees' Stock Purchase Plan. See "Management of the Company-Stock Option Plan" and "-Stock Purchase Plan."

DIVIDEND POLICY

Since its incorporation, the Company has not declared or paid any dividends on the Common Stock. Following the offering, the Company intends to pay a quarterly cash dividend on the Common Stock, subject to the discretion of the Board of Directors after consideration of the Company's operating results, financial condition, cash requirements, general business conditions and such other factors as the Board of Directors deems relevant. No assurance can be given as to the timing, payment or amount of such dividends.

Effective upon the sale of the Shares, the Company's ability to pay dividends will be limited by a credit agreement to 50% of the Company's cumulative consolidated net income during the 8 fiscal quarters preceding the date of the dividend or since May 1, 1991, whichever period is shorter (after deducting distributions previously made during the period).

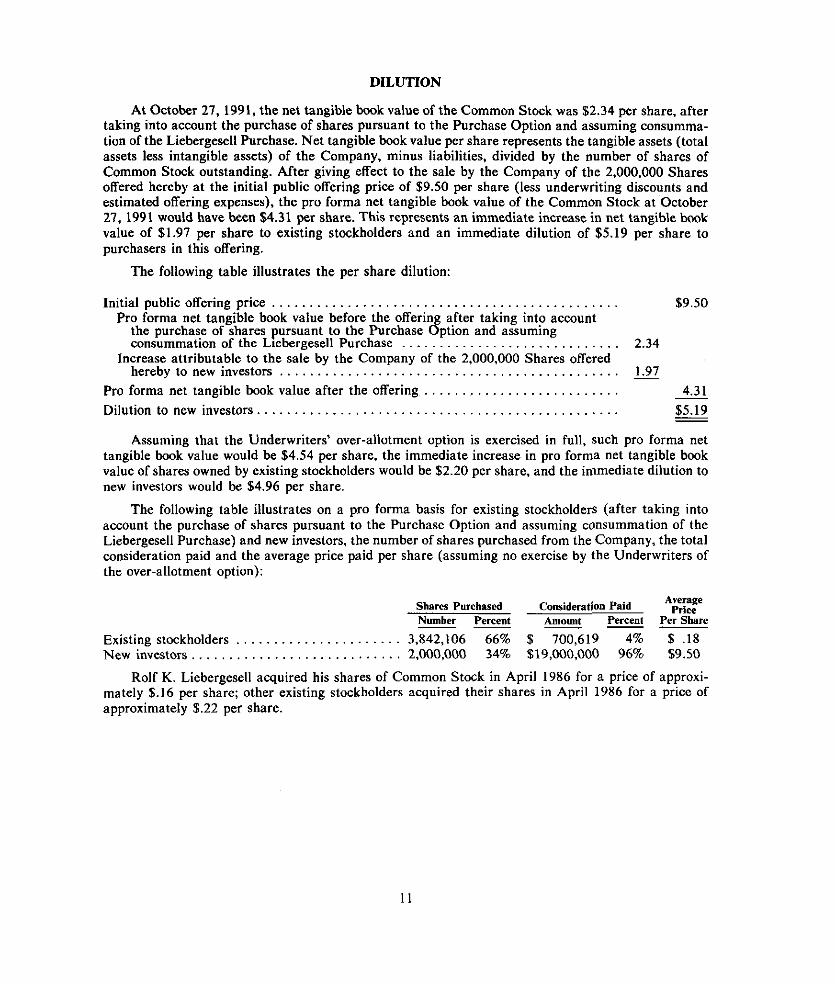

DILUTION

At October 27, 1991, the net tangible book value of the Common Stock was $2.34 per share, after taking into account the purchase of shares pursuant to the Purchase Option and assuming consumma- tion of the Liebergesell Purchase. Net tangible book value per share represents the tangible assets (total assets less intangible assets) of the Company, minus liabilities, divided by the number of shares of Common Stock outstanding. After giving effect to the sale by the Company of the 2,000,000 Shares offered hereby at the initial public offering price of $9.50 per share (less underwriting discounts and estimated offering expenses), the pro forma net tangible book value of the Common Stock at October 27, 1991 would have been $4.31 per share. This represents an immediate increase in net tangible book value of $1.97 per share to existing stockholders and an immediate dilution of $5.19 per share to purchasers in this offering.

The following table illustrates the per share dilution:

Initial public offering price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $9.50 Pro forma net tangible book value before the offering after taking into account

the purchase of shares pursuant to the Purchase Option and assuming consummation of the L~ebergesell Purchase . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.34

Increase attributable to the sale by the Company of the 2,000,000 Shares offered hereby to new investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.97 -

.. . . . . . . . . . . . . . . . . . . . . . . . . Pro forma net tangible book value after the offering 4.31 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Dilution to new investors.. $5.19 -

Assuming that the Underwriters' over-allotment option is exercised in full, such pro forma net tangible book value would be $4.54 per share, the immediate increase in pro forma net tangible book value of shares owned by existing stockholders would be $2.20 per share, and the immediate dilution to new investors would be $4.96 per share.

The following table illustrates on a pro forma basis for existing stockholders (after taking into account the purchase of shares pursuant to the Purchase Option and assuming consummation of the Liebergesell Purchase) and new investors. the number of shares purchased from the Company, the total consideration paid and the average price paid per share (assuming no exercise by the Underwriters of the over-allotment option):

Shares Purchased Average Consideration Paid Price

-- Amount Percent Per Share Number Percent

Existing stockholders . . . . . . . . . . . . . . . . . . . . . . 3,842,106 66% $ 700,619 4% $ .18 New investors.. . . . . . . . . . . . . . . . . . . . . . . . . . . 2,000,000 34% $19,000,000 96% $9.50

Rolf K. Liebergesell acquired his shares of Common Stock in April 1986 for a price of approxi- mately 6.16 per share; other existing stockholders acquired their shares in April 1986 for a price of approximately $.22 per share.

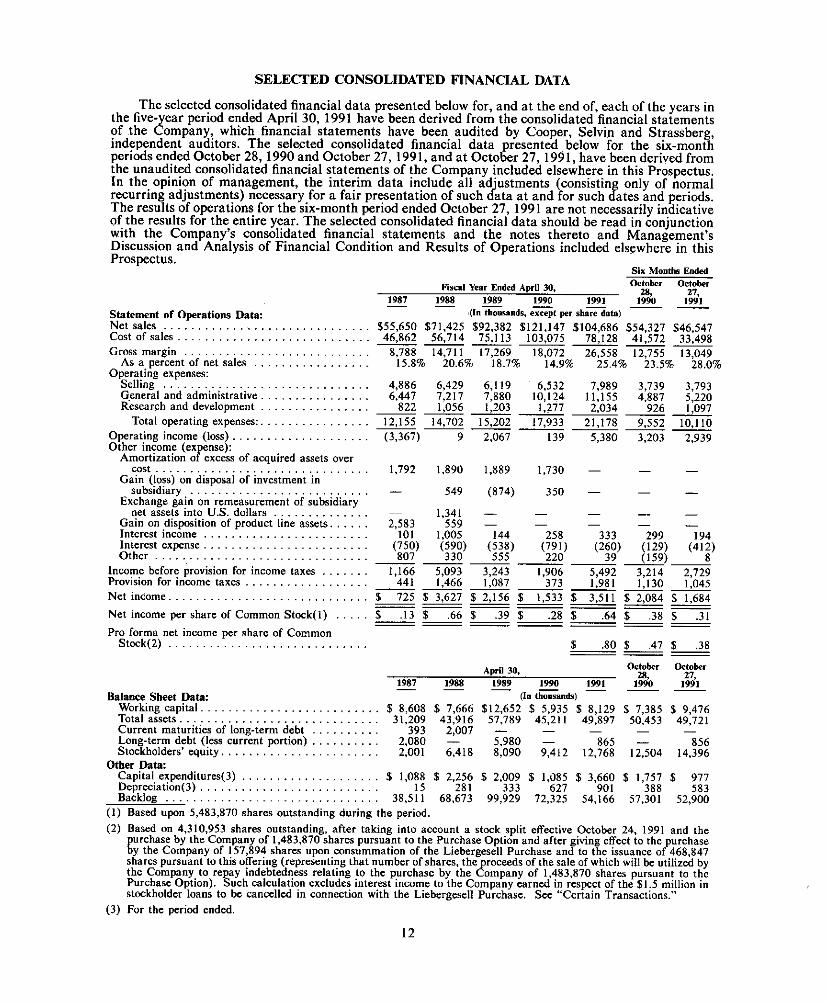

SELECTED CONSOLIDATED FINANCIAL DATA

The selected consolidated financial data presented below for, and a t the end of, each of the years in the five- ear period ended April 30, 1991 have been derived from the consolidated financial statements of the C! ompany, which financial statements have been audited by Cooper, Selvin and Strassberg, independent auditors. The selected consolidated financial data presented below for the six-month periods ended October 28,1990 and October 27,1991, and at October 27,1991, have been derived from the unaudited consolidated financial statements of the Company included elsewhere in this Prospectus. In the opinion of management, the interim data include all ad'ustments (consistin only of normal recurring adjustments) necessary for a fair presentation of such d ata at and for such ates and periods. The results of operations for the six-month period ended October 27, 1991 are not necessarily indicative of the results for the entire year. The selected consolidated financial data should be read in conjunction with the Company's consolidated financial statements and the notes thereto and Management's Discussion and Analysis of Financial Condition and Results of Operations included elsewhere in this Prospectus.

Six Mootha Ended

Fi-l Year Ended April 30, October October

1987 1988 1990 1991 283 27,

1990 1991 - Statement of Oprations Data: (h thousands, e-t per shiat.) - - Net sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $55,650 $71.425 $92,382 $121,147 $104,686 $54,327 $46,547 Cost of sa les . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46,862 56,714 75,113 . 103,075 78,128 41,572 33.498 - - - - - - - Gross margin . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,788 14,711 17,269 18,072 26,558 12,755 13,049

As a percent of net sales . . . . . . . . . . . . . . . . . 15.8% 20.6% 18.7% 14.9% 25.4% 23.5% 28.0% Operating expenses:

Selling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,886 6,429 6,119 6.532 7,989 3,739 3,793 General and administrative. . . . . . . . . . . . . . . . 6,447 7,217 7,880 10,124 11,155 4.887 5,220 Research and development . . . . . . . . . . . . . . . . 822 1,056 1,203 1,277 2,034 926 1,097 - - - - - - -

Total operating expenses:. . . . . . . . . . . . . . . . 12,155 14,702 15,202 17,933 21,178 9,552 10,110 Operating income (loss) . . . . . . . . . . . . . . . . . . . . (3,367) 9 2,067 I39 5,380 3.203 2,939 Other income (ex ense):

Amortization a! excess of acquired assets over cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,792 1.890 1,889 1,730 - - -

Gain (loss) on disposal of investment in subsidiary . . . . . . . . . . . . . . . . . . . . . . . . . . - - - 549 (874) 350 -

Exchange gain on remeasurement of subsidiary . . . . . . . . . . . . . . net assets into U.S. dollars - 1,341 - - - - -

Gain an disposition of product line assets. . . . . . 2,583 559 - - - - - Interest income . . . . . . . . . . . . . . . . . . . . . . . . 101 1.005 144 258 333 299 194

. . . . . . . . . . . . . . . . . . . . . . . . Interestexpense (750) (590) (538) (791) (260) (129) (412) Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 807 330 555 220 39 (159)- ------ 8

Income before provision for income taxes . . . . . . . 1,166 5,093 3,243 1,906 5,492 3,214 2,729 Provision for income taxes . . . . . . . . . . . . . . . . . . 441 1,466 1087 373 1,981 1,130 1,045 --L---- Net income.. . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 725 $ 3,627 $ 2,156 $ 1,533 $ 3.511 $ 2,084 $ 1,684 - - - - - - - - - - - - - - Net income per share of Common Stock(l) . . . . . $ . I3 $ .66 $ .39 $ .28 $ .64 $ $ ,31 - - - - - - - - - Pro forma net income per share of Common

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . Stock(2) $ .80 $ .47 $ .38 --- April 30. October Oclober

28. 27, 1987 1988 1989 1990 1991 19% 1991 - - - - - -

Balance Sheet Data: (I" t=nds) Working capital. . . . . . . . . . . . . . . . . . . . . . . . . . $ 8,608 $ 7,666 $12,652 $ 5,935 $ 8,129 $ 7,385 $ 9,476 Totalassets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31,209 43,916 57,789 45,211 49,897 50,453 49,721 Current maturities of long-term debt . . . . . . . . . . 393 2,007 - - - - - Long-term debt (less current portion) . . . . . . . . . . 2,080 - 5,980 - 865 - 856 Stockholders' equity. . . . . . . . . . . . . . . . . . . . . . . 2.001 6,418 8,090 9,412 12,768 12,504 14.396

Other Data: Capital expenditures(3) . . . . . . . . . . . . . . . . . . . . $ 1.088 $ 2,256 $ 2,009 $ 1,085 $ 3,660 $ 1,757 $ 977 Depreciation(3) . . . . . . . . . . . . . . . . . . . . . . . . . . 15 281 333 627 901 388 583 Backlog . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38,511 68,673 99,929 72,325 54,166 57,301 52,900

( I ) Based upon 5,483,870 shares outstanding during the period. (2) Based on 4,310,953 shares outstanding, after taking into account a stock split effective October 24, 1991 and the

urchase by the Company of 1,483,870 shares pursuant to the Purchase Option and after giving effect to the purchase !y the Company of 157,894 shares upon consummation of the Liebergesell Purchase and to the issuance of 468,847 shares pursuant to this offering (representing that number of shares, the roceeds of the sale of which will be utilized by the Company to re ay indebtedness relating to the purchase by the Eompany of 1.483.870 shares pursuant to the Purchase Option). Euch calculation excludes interest income to the Company earned in respect of the $1.5 million in stwkholder loans to be cancelled in connection with the Liebergesell Purchase. See "Certain Transactions."

(3) For the period ended.

12

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the Selected Consolidated Financial Data and the Consolidated Financial Statements of the Company and related notes thereto appearing elsewhere in this Prospectus.

Overview

The Company was formed by its current stockholders in 1986 to acquire certain assets and to assume certain liabilities of the former Farrel Company, an unprofitable division of USM, a subsidiary of Emhart. Management believes that the Company's performance since 1986 is attributable to a number of factors including:

Strategic Focus. The Company's predecessor manufactured a number of product lines for the metal working industry. These product lines were divested to facilitate the Company's strategic focus on the rubber and plastics processing industries where management felt that the Company's prospects for a successful turnaround were high due to the Company's strong historical market position in these industries.

Production Eficiencies. Where possible, the Company has subcontracted the manufacture of certain components to lower cost vendors without diminishing the quality of the components. Increased outsourcing and more efficient purchasing practices have been factors in the improvement in the Company's performance.

More Profitable Product Mix. The Company has emphasized product line profitability over aggregate sales levels, putting greater effort behind those products expected to deliver higher margins. The Company has also increased the portion of its revenues derived from its aftermarket business, which generally carries higher margins..

General

The assets acquired in 1986 from USM were recorded on the books of the Company at their estimated fair market values. The value of the net assets acquired by the Company in 1986 exceeded the wst of the acquisition by approximately $20.0 million. A portion of this excess was accounted for as a reduction of the acquired non-current asset values to zero. The remainder, approximately $7.3 million, was accounted for as a credit on the balance sheet of the Company. This credit was deemed to represent primarily discounts from the inventory values acquired, and was amortized to income over the four-year period ended April 30, 1990.

As a result of the aforementioned reduction of the acquired non-current asset values to zero, the non-current assets, including property, plant and equipment acquired from USM in 1986, are carried on the Company's consolidated balance sheet at zero value. Property, plant and equipment values carried on the Company's April 30, 1991 consolidated balance sheet represent the values, net of depreciation, of property, plant and equipment acquired after May 1986. As a consequence, the Company's level of depreciation has been less than if such depreciation had been based on historic carrying values or on fair market values.

The Company recognizes revenue and associated costs of manufacturing at the time it ships its products. In order to manage working capital more efficiently, the Company generally receives down payments and progress payments in order to finance the cost of product completion. Due to the large dollar value and long lead times (up to twelve months or more) associated with revenues derived from major equipment orders, the Company's financial results may fluctuate widely depending upon the timing of the actual shipment of such orders.

See Note 15 to the Company's Consolidated Financial Statements included elsewhere in this Prospectus for financial information relating to the Company's foreign operations and export sales. Due to the global nature of the business of many of the Company's customers, the Company operates under a global management structure with interdependent domestic and foreign operations. The Company's domestic and foreign sales, engineering and research and development groups are each supervised by a single group executive, and Mr. Liebergesell serves as chief executive officer of both domestic and foreign operations. In appropriate circumstances, the Company's domestic operations subcontracts with the Company's U.K. subsidiary to manufacture component parts of equipment ordered by a U.S. customer, or vice versa. Based upon plant utilization, interest rates, production capacity, currency fluctuations and exchange rates, shipping costs, tax considerations, the availability of credit insurance and other factors, management has discretion with respect to the place of manufacture irrespective of the location from which an order originates or to which the equipment is to he delivered.

Results of Operations

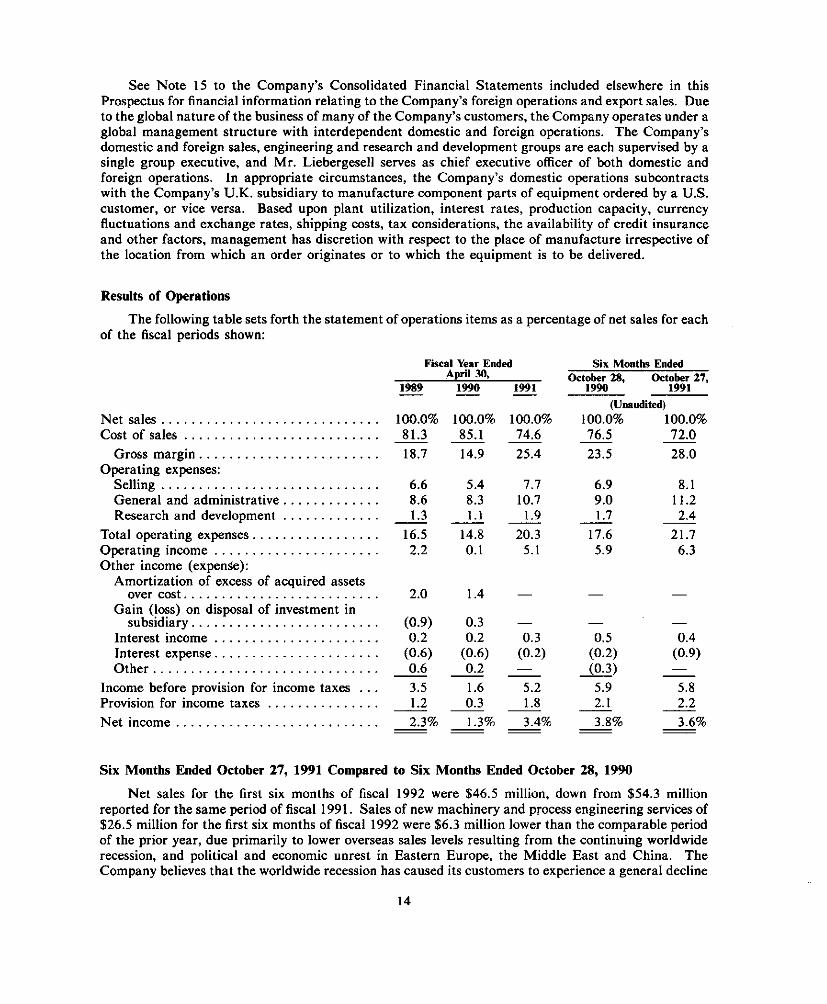

The following table sets forth the statement of operations items as a percentage of net sales for each of the fiscal periods shown:

Fiscal Year Ended Six Months Ended April 30, October 28, October 27,

1989 - 1990 - 1991 - 1990 1991

Net sales.. . . . . . . . . . . . . . . . . . . . . . . . . . . . 100.0% 100.0% 100.0% Cost of sales . . . . . . . . . . . . . . . . . . . . . . . . . . 81.3 85.1 74.6

Gross margin . . . . . . . . . . . . . . . . . . . . . . . . 18.7 14.9 25.4 Operating expenses:

Selling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.6 5.4 7.7 General and administrative . . . . . . . . . . . . . 8.6 8.3 10.7 Research and development . . . . . . . . . . . . . 1.3 - 1.1 - 1.9

Total operating expenses. . . . . . . . . . . . . . . . . 16.5 14.8 20.3 Operating income . . . . . . . . . . . . . . . . . . . . . . 2.2 0.1 5.1 Other income (expense):

Amortization of excess of acquired assets over cost. . . . . . . . . . . . . . . . . . . . . . . . . . 2.0 1.4 -

Gain (loss) . . on disposal of investment in subs~d~ary . . . . . . . . . . . . . . . . . . . . . . . . . (0.9) 0.3 -

Interest income . . . . . . . . . . . . . . . . . . . . . . 0.2 0.2 0.3 Interest expense.. . . . . . . . . . . . . . . . . . . . . (0.6) (0.6) (0.2) Other. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.6 0.2 - - - -

Income before provision for income taxes . . . 3.5 1.6 5.2 Provision for income taxes . . . . . . . . . . . . . . . 1.2 0.3 - 1.8 Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.3% 1.3% 3.4% - - - - - -

(Unaudited)

Six Months Ended October 27, 1991 Compared to Six Months Ended October 28, 1990

Net sales for the first six months of fiscal 1992 were $46.5 million, down from $54.3 million reported for the same period of fiscal 1991. Sales of new machinery and process engineering services of $26.5 million for the first six months of fiscal 1992 were $6.3 million lower than the comparable period of the prior year, due primarily to lower overseas sales levels resulting from the continuing worldwide recession, and political and economic unrest in Eastern Europe, the Middle East and China. The Company believes that the worldwide recession has caused its customers to experience a general decline

in the demand for their products, and has resulted in postponement of expenditures by such customers for new equipment and a corresponding decline in sales of the Company's products. The Company has closely monitored operating costs and hiring levels to bring them in line with such lower sales levels. Aftermarket sales were $18.0 million for the first six months of fiscal 1992, or $1.5 million lower than the comparable period of the prior year. Aftermarket sales were less significantly affected by the worldwide recession as customers continued to have needs for the repair and service of presently owned equipment. Orders received by the Company during the first six months of fiscal 1992 were $45.7 million, a 16.3% increase over the first six months of fiscal 1991. Backlog at the end of the six-month period ended October 27, 1991 was $52.9 million, compared to $57.3 million at October 28, 1990. Of the backlog of orders considered to be firm as of October 27, 1991, the Company expects to fill approximately $40.7 million during the current fiscal year.

Gross margin increased to $13.0 million in the first six months of fiscal 1992 from $12.8 million in the first six months of fiscal 1991 and gross margin as a percentage of net sales increased to 28.0% from 23.5%. During the last six months of fiscal 1991, the Cornpafly's gross margin as a percentage of sales was 27.4%. The increase in gross margin was due to several factors, including higher margins on new equipment sales, more efficient purchasing practices and a more profitable product mix, as aftermarket sales represented a higher percentage of total sales in fiscal 1992. These gains were offset in part by higher warranty and installation expenses.

Selling expenses increased $54,000 primarily due to participation in trade shows. Selling expenses increased to 8.1% of net sales compared to 6.9% in the comparable prior year period due principally to the fixed nature of many of the Company's selling expenses and lower sales levels. General and administrative expenses increased $333,000 in the first six months of fiscal 1992 compared to the first six months of fiscal 1991. Higher salaries and related fringe benefit expenses accounted in large part for the increase. Due to the fixed nature of these expenses and lower sales levels, general and administrative expenses as a percentage of net sales increased from 9.0% in the first six months of fiscal 1991 to 11.2% in the first six months of fiscal 1992. Research and development expense increased $171,000 reflecting the Company's ongoing development efforts.

Other income, exclusive of interest income and interest expense, increased by $167,000 in the first six months of fiscal 1992 compared to the comparable prior year period due to reductions in foreign exchange losses and miscellanwus other expenses.

Interest income decreased by $105,000 to $194,000. Interest expense increased by $283,000 to $412,000 in the first six months of fiscal 1992 compared to the first six months of fiscal 1991. The increase was due to interest charges associated with the sale of certain receivables under the terms of a credit facility with a major U.K. bank. See "Liquidity and Capital Resources; Capital Expenditures."

Income tax expense as a percentage of pre-tax income increased to 38.3% in the first six months of fiscal 1992 from 35.2% in the first six months of fiscal 1991.

Fiscal 1991 Compared to Fiscal 1990

Net sales for fiscal 1991 were $104.7 million, which was 13.6% lower than the $121.1 million reported for fiscal 1990. In fiscal 1990, the Company experienced a very significant increase in sales ($28.8 million) over the prior year, in part due to significant capacity additions by plastics manufactur- ers, which additions did not recur in fiscal 1991. The $16.5 million decrease in net sales from fiscal 1990 to 1991 was attributable to a $17.7 million decline in sales of new machines and process engineering services, offset, in part, by a $1.2 million increase in aftermarket sales from $37.2 million to $38.4 million. The decline in sales of new equipment and process engineering services was primarily due to lower sales to plastics manufacturers that were absorbing significant capacity additions made in prior years, and to the general economic slowdown, which caused a reduction in the manufacturing activity of

the Company's customers, and a corresponding postponement of capital expenditures for new equip ment. The decline also resulted from an emphasis by the Company on higher margin business, which led the Company to reduce sales efforts associated with lower margin products. During fiscal 1991, net sales were favorably affected by $7.9 million due to the devaluation of the U.S. dollar relative to the pound sterling. Revenues and expenses of the Company's U.K. subsidiary are denominated in pounds sterling, and significant movements in the value of the pound sterling relative to the U.S. dollar can affect the operating results of the Company. Orders received by the Company during fiscal 1991 were $86.5 million, 7.5% less than orders received of $93.5 million during fiscal 1990. Backlog at the end of fiscal 1991 was $54.2 million, compared to $72.3 million at the end of fiscal 1990.

Gross margin increased from $18.1 million in fiscal 1990 to $26.6 million in 1991. Gross margin as a percentage of net sales increased from 14.9% in fiscal 1990 to 25.4% in fiscal 1991. The significant increase in the gross margin percentage was attributable to a number of factors. First, the Company's 14.9% gross margin percentage in fiscal 1990, which was significantly lower than the 18.7% gross margin percentage achieved in fiscal 1989, was negatively affected by several low margin orders accepted by the Company as a means of gaining market acceptance for a newly developed continuous mixer targeted for the plastics industry. This discounting allowed the Company to establish several installations of the new machine in the field, and such installations are expected to facilitate future sales. In fiscal 1991, the Company did not pursue a discounting strategy for this product. Second, in fiscal 1991 the percentage of the Company's net sales derived from aftermarket sales, which generally carry higher margins than new equipment sales, increased to 37%. from 31% in fiscal 1990. Third, gross margin was favorably affected in fiscal 1991 by effective cost controls resulting in more efficient purchasing practices, greater adherence to manufacturing delivery schedules and lower warranty and installation expenses. Fourth, gross margin was favorably affected by the aforementioned favorable impact of the devaluation of the U.S. dollar relative to the pound sterling.

Selling expenses increased $1.5 million to 7.7% of net sales in fiscal 1991 compared to 5.4% in fiscal 1990, primarily due to increased staffing levels, including the opening of a new sales ofice in Charlotte, North Carolina, in anticipation of future growth. In addition, expenses associated with an industry trade show accounted for a portion of the difference. General and administrative expenses increased $1.0 million to 10.7% of net sales in fiscal 1991 compared to 8.3% in fiscal 1990. The increase in general and administrative expenses was primarily due to increased legal fees relating to commercial disputes in fiscal 1991 and increased staffing levels, offset by a bonus paid in fiscal year 1990 to an officer of the Company in recognition of past services. Research and development expense increased $757,000 to 1.9% of net sales in fiscal 1991 from 1.1% of net sales in fiscal 1990 in part due to costs associated with the Company's emphasis on development of improved and new products and the appointment of a vice president of technology.

Other income, exclusive of interest income and interest expense, decreased by $2.3 million to $39,000. The principal reason for this decrease was the absence in fiscal 1991 of income from the amortization of the excess of acquired assets over cost relating to the 1986 acquisition. This excess of acquired assets over cost became fully amortized in fiscal 1990, and in that fiscal year, the Company recognized income from such amortization of $1.7 million. Also contributing to the decrease in other income was the recognition in fiscal 1990 of a gain on the disposal of a subsidiary in the amount of $350,000.

Interest income increased from $258,000 in fiscal 1990 to $333,000 in fiscal 1991 due in large part to a higher average balance of cash available for investment. Interest expense decreased from $791,000 in fiscal 1990 to $260,000 in fiscal 1991 due principally to lower average borrowings.

Income tax expense as a percentage of pre-tax income increased from 19.6% in fiscal 1990 to 36.0% in fiscal 1991. The percentage was lower in fiscal 1990 primarily because a tax provision was not

16

required to be made on the amortization of the excess of acquired assets over cost relating to United Kingdom net assets.

Fiscal 1990 Compared to Fiscal 1989

Net sales were $121.1 million for fiscal 1990 or $28.8 million higher than fiscal 1989, a 31.1% increase. New machines and process engineering sales for fiscal 1990 were $83.9 million or $23.0 million higher than the prior year. Aftermarket sales for fiscal 1991 were $37.2 million or $5.8 million higher than the prior year. Deliveries relating to several large orders accepted as a strategic means of entering new markets accounted for a significant portion of the increase in new machine sales. Orders received by the Company during fiscal 1990 were $93.5 million, a 24.3% decrease from fiscal 1989. Backlog at the end of fiscal 1990 was $72.3 million, compared to $99.9 million at the end of fiscal 1989.

Gross margin increased from $17.3 million in fiscal 1989 to $18.1 million in fiscal 1990. Gross margin as a percentage of net sales decreased from 18.7% in fiscal 1989 to 14.9% in fiscal 1990 due in part to lower than expected margins on several large orders that were accepted at relatively low margins as a strategic means of entering new markets. In addition, higher than anticipated warranty and installation expenses contributed to the decline in gross margin.

Selling expenses increased $413,000 to $6.5 million in fiscal 1990 hut declined as a percentage of net sales from 6.6% in fiscal 1989 to 5.4% in fiscal 1990. Such increase was generally due to normal growth in anticipation of future increases in sales. General and administrative expenses increased $2.2 million in fiscal 1990 to $10.1 million due, in large part, to a bonus paid to an officer of the Company in recognition of past services and to increased recruiting and legal expenses. However, general and administrative expenses decreased as a percentage of net sales to 8.3% compared to 8.6% in fiscal 1989 due to the greater percentage increase in net sales. Research and development expenses increased $74,000 to $1.3 million and declined as a percentage of net sales to 1.1% in fiscal 1990 from 1.3% in fiscal 1989.

Other income, exclusive of interest income and interest expense, increased by $730,000 in fiscal 1990, principally due to a gain of $350,000 on the disposal of a subsidiary. The investment in this subsidiary had been written off in fiscal 1989 at a cost of $874,000 and thereby generated a year-to-year galn. The write-off in fiscal 1989 and the gain on disposal in fiscal 1990 related to the closure and subsequent sale of the Company's Brazilian subsidiary. The Company decided to divest this subsidiary due to adverse economic conditions in Brazil. The Company continues to service that market through its U.S. operations. Partially offsetting the increase in other income in fiscal 1990 was a $335,000 decrease due principally to a reduction in royalty income.

Interest income increased from $144,000 in fiscal 1989 to $258,000 in fiscal 1990, primarily due to interest earned on stockholder loans. Interest expense increased from $538,000 to $791,000 due to higher average borrowings.

Income tax expense as a percentage of pre-tax income decreased from 33.5% in fiscal 1989 to 19.6% in fiscal 1990. The percentage was higher in fiscal 1989 primarily because a tax benefit was not recorded in that fiscal year on a portion of the write-off of the investment in the Brazilian subsidiary which was made in that fiscal year. The portion of the write-off on which a tax benefit was not recorded was that portion which represented previously recognized, but undistributed, income for which a U.S. tax expense had not been previously provided.

Orders and Backlog

During each of the past three fiscal years, the Company has experienced a decline in orders received. In fiscal 1989, the Company received several large orders from plastics manufacturers planning significant capacity additions, and orders totalled $123.5 million. In fiscal 1990, orders

decreased from the fiscal 1989 level to $93.5 million in part due to the general economic slowdown in the United States and Western Europe, which caused certain of the Company's customers to reduce or postpone planned capacity additions. Orders received in fiscal 1991 were $86.5 million. The further decline in orders resulted from continuing recessionary conditions in the Company's markets in the United States and Western Europe. Moreover, political and economic unrest in Eastern Europe, the Middle East and China caused certain of the Company's customers in those regions to postpone capital spending programs. In addition, the decline in orders since fiscal 1989 is due in part to reduced capital spending by plastics manufacturers that have been absorbing significant capacity additions made in prior periods.

A decline in orders in any fiscal period may result in a decline in sales in the same or a subsequent fiscal period. The Company recognizes revenue at the time it ships its products and in the case of major equipment orders often up to 12 months or more is required to complete the manufacturing process. Accordingly, the revenue from an order may be recognized in a later accounting period than the one in which the order was received.

The Company has experienced a decline in net sales in its 1991 fiscal year. Net sales in fiscal 1991 were $104.7 million, as compared to $121.1 million in fiscal 1990. Similarly, net sales during the first six months of fiscal 1992 declined to $46.5 million from $54.3 million in the first six months of fiscal 1991. The decline in net sales is due in part to the decline in orders over the past three fiscal years. The decline is also due in part, however, to the Company's strategic decision to emphasize product line profitability over aggregate sales levels. The emphasis on higher margin business has led the Company to reduce sales efforts associated with lower margin products.

The Company's ability to increase net sales levels will depend upon a recovery in the Company's primary markets and a corresponding increase in order activity. During the first six months of fiscal 1992, orders increased to $45.7 million from $39.3 million during the comparable period in fiscal 1991. This increase was primarily attributable to an increase in orders from the Company's customers in the plastics industry, particularly in the value-added mixing segment of the market. There can be no assurance that this increase in order activity is indicative of a recovery in the Company's primary markets or that orders and backlog will increase in the future or that they will not again decline.

The Company's backlog has declined as of the end of each of the past three fiscal years. Backlog at the end of fiscal years 1989, 1990 and 1991 was $99.9 million, $72.3 million and $54.2 million, respectively. Backlog has declined, in part, due to the decline in orders received. Of the backlog of orders considered to be firm as of April 30, 1991, the Company expects to fill approximately $52.6 million during the current fiscal year.

Over the past three years, the Company has shortened the lead time required to deliver certain new equipment from over one year to approximately six months, resulting in individual equipment orders generally spending less time in backlog. The Company has also increased the portion of its revenues derived from aftermarket sales, which have significantly faster turnaround times than new equipment sales. The effect of these two trends, assuming a level volume of net sales, is to reduce average backlog. Assuming no significant worsening of political and economic conditions, the Company believes that the decline in backlog from the 1989 level to the current level will not have a material adverse effect on the Company.

Environmental

The Company's United States operations are subject to extensive federal, state and local laws and regulations relating to the generation, storage, handling and transportation of certain materials and the discharge of these materials into the environment. The Company's operations outside the United States

18

are also subject to extensive requirements governing environmental protection. Environmental require- ments are constantly changing and it is difficult to predict the effect of future requirements on the Company. Future developments, including the discovery of existing conditions not currently known by the Company or changes in existing regulations, could require the significant expenditure of funds for capital improvements or require the clean-up of sites not currently subject to such requirements. While under certain circumstances the Company could be required to incur significant costs in complying with environmental laws and regulations relating to conditions presently known to the Company, the Company does not currently believe that such costs will have a material adverse effect on its financial condition. For a description of potential environmental liabilities of the Company relating to conditions presently known to the Company, including preliminary estimates as to the costs of remediation, see "Business of the Company-Legal Proceedings-Environmental."

Liquidity and Capital Resources; Capital Expenditures

Working capital at October 27, 1991 was $9.5 million, or $2.1 million higher than at October 28, 1990. The ratio of current assets to current liabilities was 1.3 to 1.0 at Octoher 27, 1991 and 1.2 to 1.0 at October 28, 1990. Due to the nature of the Company's business, many sales are of a large dollar amount. Consequently, accounts receivable and/or inventory may be temporarily at high levels which may result in a temporary decline in cash provided from operating activities. Historically, the Company has not experienced significant problems regarding the collection of accounts receivable. The Company has historically financed its operations with cash generated by operations and with borrowings under its bank credit facilities. The Company currently has individual credit facilities in the U.S. and the U.K. The principal reason the Company incurs indebtedness under these facilities is to fund working capital requirements. The Company's credit agreement in the U.S. is with a major U.S. hank under which it is authorized to borrow up to the lesser of $10 million or an amount equal to the sum of stipulated percentages of eligible real property, receivables and inventory. This credit facility may also be utilized for letters of credit and acceptances. At October 27, 1991, letters of credit outstanding under this agreement amounted to approximately $1.7 million. Interest is payable monthly and accrues on the outstanding loan balance at the bank's prime rate plus one percent. At October 27, 1991, there were no loans outstanding under this agreement.

The credit agreement has been amended, as of November 27, 1991, to increase the amount available thereunder by an additional $5 million for the sole purpose of making available to the Company a sufficient amount of funds to purchase the 1,483,870 shares of Common Stock under the Purchase Option. The amendment requires a nonrefundable commitment fee of $15,000 and a fee of $35,000 in connection with borrowings ($3.8 million) to purchase shares pursuant to the Purchase Option. The interest provisions were not amended. The increased commitment expires on February 28, 1992. The Company intends to repay any borrowings thereunder out of the proceeds of this offering.

Outstanding amounts are secured by a pledge of substantially all of the U.S. assets of the Company, including mortgages on real property. The agreement contains certain restrictions on the making of investments, loans and capital expenditures, on borrowings, on the sales of assets and on the payment of dividends. The agreement requires the maintenance of minimum levels of net worth, as defined, and maximum ratios of total liabilities, as defined, to net worth, as well as the maintenance of stipulated levels of operating profit and backlog. The agreement terminates on December 31, 1992.

The Company's credit facility in the U.K. is with a major U.K. hank and is for a total of 6.5 million pounds sterling (or $11.1 million at Octoher 27, 1991) under which it may borrow up to 2.5 million pounds sterling (or $4.3 million a t October 27, 1991) for working capital requirements. The balance of the facility is available in the form of bank guarantees. Interest is charged a t the bank's base rate plus 1% percent. The facility is secured by the fixed assets and receivables of the Company's U.K. subsidiary. At October 27, 1991, there were no loans outstanding under this arrangement. Letters of

credit amounted to 3.2 million pounds sterling (or $5.5 million at October 27, 1991). The agreement terminates on April 23, 1992.

The Company has a long-term loan in the amount of 500,000 pounds sterling (or $856,000 at October 27, 1991). from the same U.K. bank, which matures in January 1999 with semiannual principal payments commencing in 1995. The proceeds were used to refurbish the Company's U.K. facilities. The interest on this loan is 10% per annum except that, for the first five years of the term, certain rebates of interest may be granted by the bank under certain circumstances.

The Company anticipates that its operating cash flows, available lines of credit and the net proceeds of this offering will be adequate to fund its anticipated capital commitments and working capital requirements for at least the next twelve months.

During fiscal years 1990 and 1991, the Company had capital expenditures of $1.1 million and $3.7 million, respectively. Through the six months ended October 27, 1991 the Company had capital expenditures of $977,000.

FASB No. 106

In December 1990, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 106, "Employers' Accounting for Postretirement Benefits Other Than Pensions" ("FASB No. 106"). FASB No. 106 will significantly change the prevailing practice of accounting for postretirement benefits on a cash basis by requiring accrual of the expected cost of these benefits during the years that the employees render services. The Company is required to adopt the new accounting and disclosure rules no Later than its 1994 fiscal year, although earlier adoption is permitted. The Company may adopt the new standard prospectively or via a catch-up adjustment. The Company has not yet determined when it will adopt FASB No. 106, nor has the Company completed the analysis required to estimate the impact of the new standard.

BUSINESS OF THE COMPANY General

The Company designs, manufactures, sells and services capital equipment used to process rubber and plastics materials. The Company's principal products are BANBURY Mixers, continuous mixers, extruders, compact processors, pelletizers, gear pumps, calenders and mills. In conjunction with sales of capital equipment, the Company provides process engineering, process design and related services for rubber and plastics processing systems. The Company's aftermarket business consists primarily of repair, refurbishment and equipment upgrade services, spare parts sales and field services. The Company also provides laboratory services and facilities for product demonstrations and for the development and testing of rubber and plastics equipment and processes.

Sales of new capital equipment and process engineering services accounted for approximately 63% of the Company's net sales in fiscal 1991. Sales of aftermarket products and services accounted for approximately 37% of net sales in fiscal 1991. In fiscal 1991, approximately 65% of the Company's sales of new capital equipment and process engineering services was to customers in the rubber industry and 35% was to customers in the plastics industry.

The Company's customers include tire manufacturing and petrochemical firms. The Company's rubber processing equipment is primarily sold to tire manufacturers and manufacturers of rubber goods, such as sheet products, molded products, footwear and wire and cable. In the plastics processing industry, the Company's equipment is primarily sold to commodity plastics producers and value-added mixers of plastics materials. The Company markets its products through an international sales and service organization which includes four offices in the United States, one in Canada, six in other countries, and independent sales representatives covering 28 countries.